As filed with the Securities and Exchange Commission on February 7, 2012

No. 333-178835

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

TRONOX LIMITED

(ACN 153 348 111)

TRONOX INCORPORATED

(Exact name of registrant as specified in its charter)

| | | | |

Western Australia, Australia | | 2810 | | 98-1026700

|

(State or other jurisdiction of

incorporation or organization)

| | (Primary Standard Industrial Classification Code Number)

| | (I.R.S. Employer

Identification No.)

|

| | |

| Delaware | | 2810 | | 20-2868245

|

(State or other jurisdiction

of incorporation or organization) | | (Primary Standard Industrial Classification Code Number) | | (I.R.S. Employer

Identification No.) |

3301 N.W. 150th Street

Oklahoma City, Oklahoma 73134

(405) 775-5000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Michael Foster

General Counsel

3301 N.W. 150th Street

Oklahoma City, Oklahoma 73134

(405) 775-5000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

Daniel E. Wolf

Christian O. Nagler

Kirkland & Ellis LLP

601 Lexington Avenue

New York, New York 10022

(212) 446-4800

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effectiveness of this registration statement and the satisfaction or waiver of all other conditions to the closing of the Transaction described herein.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | | | |

| Large accelerated filer | | ¨ | | | | Accelerated filer | | ¨ |

| Non-accelerated filer | | x | | (Do not check if a smaller reporting company) | | Smaller reporting company | | ¨ |

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this Transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Takeover offer) ¨

Exchange Act Rule 14d-1(d) (Cross-Border Issuer Takeover offer) ¨

| | | | | | | | |

CALCULATION OF REGISTRATION FEE |

Title of Each Class of Securities

to be Registered | | Amount

to be Registered | | Proposed Maximum

Offering Price

Per Unit | | Proposed Maximum

Offering Price | | Amount of

Registration Fee(1) |

Class A ordinary shares issued by Tronox Limited (“Class A Shares”) | | 16,382,432 shares | | Not Applicable | | $1,945,413,800(3) | | $222,944.42 |

Exchangeable Shares, par value $0.01, issued by Tronox Incorporated (“Exchangeable Shares”) and exchangeable on a one for one basis into Class A Shares | | 2,457,365 shares | | Not Applicable | | Not Applicable(3) | | Not Applicable(3) |

Class A Shares issuable upon exchange of the Exchangeable Shares | | (2) | | (2) | | (2) | | (2) |

|

|

| (1) | The registration fee has been calculated pursuant to Rule 457(f) under the Securities Act of 1933, as amended. |

| (2) | The Class A Shares that are being registered include such indeterminate number of Class A Shares, if any, that may be issued upon exchange of the Exchangeable Shares registered hereunder, which Class A Shares are not subject to an additional fee pursuant to Rule 457(i) of the Securities Act. Pursuant to Rule 416 under the Securities Act, such number of Class A Shares registered hereby shall include an indeterminate number of Class A Shares that may be issued in connection with the anti-dilution provisions or stock splits, stock dividends, recapitalizations or similar events. |

| (3) | Pursuant to Rule 457(c) and Rule 457(f) under the Securities Act, and solely for the purpose of calculating the registration fee, the market value of the securities to be exchanged was calculated as the product of (i) 16,382,432 shares of Tronox Incorporated common stock (including all outstanding shares of Tronox Incorporated and shares for which warrants to purchase shares are outstanding), which reflects the maximum amount of shares of Tronox Incorporated to be exchanged for Class A Shares or Exchangeable Shares in Tronox Incorporated and (ii) the average of the high and low sales prices of shares of Tronox Incorporated common stock reported on the “Pink Sheets” on December 27, 2011. A separate fee has not been paid for the offering of the Exchangeable Shares as any Exchangeable Shares issued will reduce the amount of Class A Shares to be issued. |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Explanatory Note

This is a joint registration statement of Tronox Limited and Tronox Incorporated. Tronox Limited is offering Class A Shares. Tronox Incorporated is offering Exchangeable Shares.

This joint registration statement is being filed in connection with the transactions contemplated by the Transaction Agreement, dated as of September 25, 2011 by and among Tronox Incorporated, Tronox Limited, Exxaro Resources Limited and certain of their respective affiliates. The parties expect to amend the Transaction Agreement to reflect an additional internal merger and certain corporate restructurings, among other revisions. Accordingly, the descriptions of the Transaction Agreement and the transactions contemplated thereby contained in this Registration Statement, including all references to the Mergers, reflect these expected amendments.

Information contained in this proxy statement/prospectus is subject to completion or amendment. A registration statement relating to these securities has been filed with the Securities and Exchange Commission. These securities may not be sold nor may offers to buy be accepted prior to the time the registration statement becomes effective. This proxy statement/prospectus shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of these securities in any jurisdiction in which such offer, solicitation or sale is not permitted.

PRELIMINARY, SUBJECT TO COMPLETION, DATED FEBRUARY 7, 2012

TRANSACTION PROPOSED—YOUR VOTE IS VERY IMPORTANT

Dear Stockholders:

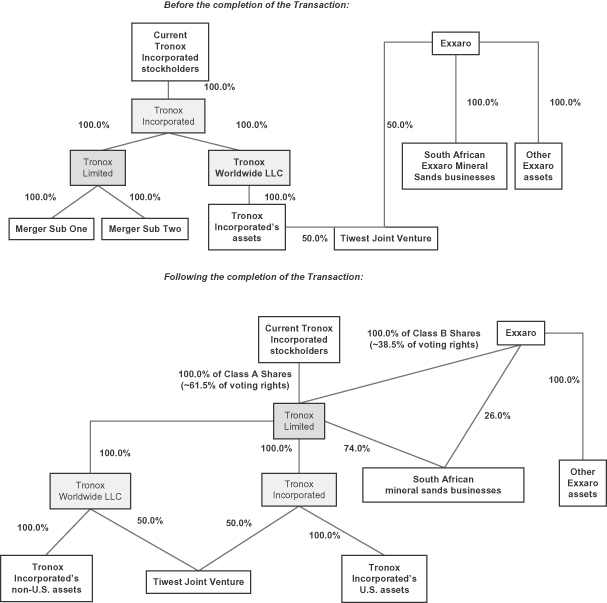

The board of directors of Tronox Incorporated and the board of directors of Exxaro Resources Limited, which we refer to as Exxaro, have agreed to combine Exxaro’s mineral sands business, which we refer to as Exxaro Mineral Sands, with the existing business of Tronox Incorporated under a new Australian holding company, Tronox Limited, pursuant to the terms of a Transaction Agreement dated September 25, 2011, which we refer to as the Transaction Agreement.

The Transaction Agreement provides that Tronox Incorporated will participate in two mergers, which we refer to as the Mergers, as a result of which it will become a subsidiary of Tronox Limited. In the Mergers, each share of Tronox Incorporated common stock will be converted into, at the holder’s election, either (i) one Class A ordinary share in Tronox Limited, which we refer to as a Class A Share, and an amount in cash equal to $12.50 without interest or (ii) one exchangeable share in Tronox Incorporated (subject to the proration procedures described in this proxy statement/prospectus), which we refer to as an Exchangeable Share, each of which is exchangeable for one Class A Share and an amount in cash equal to $12.50 without interest. As a result of the Mergers, any stockholder of Tronox Incorporated who does not elect to receive Exchangeable Shares will receive Class A Shares of Tronox Limited and cash, and therefore become subject to the Constitution of Tronox Limited and applicable provisions of Australian law. In consideration for Tronox Incorporated common stock, Tronox Incorporated stockholders will receive an aggregate of 15,235,360 Class A Shares, assuming no Tronox Incorporated stockholders elect to receive Exchangeable Shares.

Pursuant to the Transaction Agreement, in consideration for the sale of Exxaro Mineral Sands, Exxaro will receive 9,950,856 Class B ordinary shares of Tronox Limited, which we refer to as the Class B Shares. The consideration for Exxaro Mineral Sands will be subject to adjustments for net working capital, net debt and capital expenditures for certain specified projects, which adjustments will be made solely in cash and will not affect the number of Class B Shares to be issued to Exxaro.

Upon completion of the transactions contemplated by the Transaction Agreement, assuming the exchange of all Exchangeable Shares, the former Tronox Incorporated stockholders will own all of the Class A Shares, representing approximately 61.5% of the voting securities of Tronox Limited, and Exxaro will own all of the Class B Shares, representing approximately 38.5% of the voting securities of Tronox Limited. Exxaro will retain a 26.0% ownership interest in the South African operations that are part of Exxaro Mineral Sands in order to comply with ownership requirements imposed by current Black Economic Empowerment legislation in South Africa. The ownership interest in the South African operations may be exchanged for Class B Shares under certain circumstances, which could result in Exxaro owning approximately 41.7% of the voting shares of Tronox Limited after such exchange (based on the total number of issued voting shares immediately after completion of the transactions contemplated by the Transaction Agreement and assuming the exchange of all Exchangeable Shares and no subsequent issuances of Tronox Limited shares).

Following completion of the Transaction, we expect to list the Class A Shares on .

Tronox Incorporated will hold a special meeting of stockholders to consider the Transaction Agreement and the Mergers contemplated thereby, which we refer to as the Transaction. We cannot complete the Transaction unless the stockholders of Tronox Incorporated approve the proposals related to the Mergers. Your vote is very important, regardless of the number of shares you own.Whether or not you expect to attend Tronox Incorporated’s special meeting in person, please vote your shares as promptly as possible by (1) accessing the Internet website specified on your proxy card, (2) calling the toll-free number specified on your proxy card or (3) signing all proxy cards that you receive and returning them in the postage-paid envelopes provided, so that your shares may be represented and voted at the special meeting, as applicable. You may revoke your proxy at any time before the vote at the special meeting by following the procedures outlined in the accompanying proxy statement/prospectus.

We look forward to the successful completion of the Transaction.

|

Sincerely, |

|

|

Thomas Casey Chairman of the Board of Directors Tronox Incorporated |

The obligations of Tronox Incorporated and Exxaro to complete the Transaction are subject to the satisfaction or waiver of several conditions set forth in the Transaction Agreement. More information about Tronox Limited, Tronox Incorporated, Exxaro Mineral Sands, the special meeting, the Transaction Agreement and the Transaction is contained in this proxy statement/prospectus.

Tronox Incorporated encourages you to read the entire proxy statement/prospectus carefully, including the section entitled “Risk Factors,” beginning on page 35.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the Transaction described in this proxy statement/prospectus, nor have they approved or disapproved of the issuance of the Class A Shares, the Class B Shares or the Exchangeable Shares in connection with the Transaction, or determined if this proxy statement/prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

This proxy statement/prospectus is dated , 2012, and is first being mailed to the stockholders of Tronox

Incorporated on or about , 2012.

REFERENCES TO ADDITIONAL INFORMATION

This proxy statement/prospectus forms a part of a registration statement filed with the Securities and Exchange Commission, or the SEC, and incorporates important business and financial information about Tronox Incorporated and Tronox Limited from other documents that we have not included in or delivered with this proxy statement/prospectus. This information is available for you to read and copy at the SEC Public Reference Room located at 100 F Street, N.E., Washington, DC 20549, and through the SEC’s website, www.sec.gov. You can also obtain those documents incorporated by reference into this proxy statement/prospectus free of charge by requesting them in writing or by telephone at the following addresses and telephone numbers:

Tronox Incorporated

3301 N.W. 150th Street

Oklahoma City, Oklahoma 73134

Call toll-free: or

call collect: (405) 775-5000

Email:

Investors may also consult Tronox Incorporated’s website for more information concerning the Transaction described in this proxy statement/prospectus. Tronox Incorporated’s website is www.tronox.com. Information included on Tronox Incorporated’s website is not incorporated by reference into this proxy statement/prospectus.

If you would like to request documents, please do so by , 2012 in order to receive them before the special meeting.

For more information, see “Where You Can Find More Information” beginning on page 323.

ii

TRONOX INCORPORATED

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON , 2012

To the Stockholders of Tronox Incorporated:

We will hold a special meeting of the stockholders of Tronox Incorporated on , 2012 at , Eastern time, in New York, New York:

(i) to adopt the Transaction Agreement for the purpose of approving the Mergers contemplated thereby (the “Merger Proposal”), as a result of which any stockholder of Tronox Incorporated who does not elect to receive Exchangeable Shares in the Mergers will receive Class A Shares of Tronox Limited, a new Australian holding company, and cash, and therefore become subject to the Constitution of Tronox Limited and applicable provisions of Australian law; and

(ii) to adjourn the Tronox Incorporated special meeting, if necessary, to solicit additional proxies if there are not sufficient votes to approve the Merger Proposal (the “Adjournment Proposal”).

We do not expect to transact any other business at the special meeting.

Only holders of record of shares of Tronox Incorporated common stock at the close of business on , 2012, the record date for the special meeting, are entitled to notice of, and to vote at, the special meeting and any adjournments or postponements of the special meeting. A list of these stockholders will be available for inspection by any Tronox Incorporated stockholder, for any purpose germane to the Tronox Incorporated special meeting, at such meeting.

We cannot complete the Transaction described in this proxy statement/prospectus unless we receive the affirmative vote of the holders of a majority of the shares of Tronox Incorporated common stock outstanding and entitled to vote at the Tronox Incorporated special meeting as of the record date, voting as a single class, either in person or by proxy.

The Tronox Incorporated board of directors unanimously recommends that the Tronox Incorporated stockholders vote “FOR” the Merger Proposal and the Adjournment Proposal. For a discussion of interests of Tronox Incorporated’s directors and executive officers in the Transaction that may be different from, or in addition to, the interests of Tronox Incorporated’s stockholders generally, see the disclosure included in this proxy statement/prospectus under the heading “The Transaction—Additional Interests of Tronox Incorporated Executive Officers and Directors in the Transaction.” Whether or not you expect to attend the special meeting in person, please authorize a proxy to vote your shares as promptly as possible by (1) accessing the Internet website specified on your proxy card, (2) calling the toll-free number specified on your proxy card or (3) signing all proxy cards that you receive and returning them in the postage-paid envelopes provided, so that your shares may be represented and voted at the special meeting.If your shares are held in the name of a bank, broker or other fiduciary, please follow the instructions on the voting instruction form furnished by the record holder.

By Order of the Board of Directors,

Michael J. Foster

Vice President, General

Counsel and Secretary

Oklahoma City, Oklahoma

, 2012

IMPORTANT

Whether or not you plan to attend the special meeting, we urge you to vote your shares over the Internet or via the toll-free telephone number, as we describe in this proxy statement/prospectus. As an alternative, if you received a paper copy of the proxy card by mail, you may sign, date and mail the proxy card in the envelope provided. No postage is necessary if mailed in the United States. Voting over the Internet, via the toll-free telephone number or mailing a proxy card will not limit your right to vote in person or to attend the special meeting.

ii

VOTING INSTRUCTIONS

Tronox Incorporated stockholders of record may attend the meeting in person and vote or may authorize a proxy to vote as follows:

Internet. You can authorize a proxy to vote over the Internet by accessing the website shown on your proxy card and following the instructions on the website. Internet voting is available 24 hours a day.

Telephone. You can authorize a proxy to vote by telephone by calling the toll-free number shown on your proxy card. Telephone voting is available 24 hours a day.

Mail. You can authorize a proxy to vote by mail by completing, signing, dating and mailing your proxy card(s) in the postage-paid envelope included with this proxy statement/prospectus.

If you are not the holder of record:

If you hold your common stock through a bank, broker, custodian or other record holder, please refer to your proxy card or voting instruction form or the information forwarded by your bank, broker, custodian or other record holder to see which options are available to you.

iii

TABLE OF CONTENTS

iv

v

vi

DEFINED TERMS

Unless otherwise specified or if the context so requires:

| | • | | “we,” “us,” and “our” refer to Tronox Limited and Tronox Incorporated, the registrants, together; |

| | • | | “$” refers to United States dollars; |

| | • | | “A$” refers to Australian dollars; |

| | • | | “Rand” and “R” refer to South African Rand; |

| | • | | “tonnes” refers to metric tons; |

| | • | | “Tronox Incorporated” refers to Tronox Incorporated, a Delaware corporation; |

| | • | | “Tronox Limited” refers to Tronox Limited, a public limited company registered under the laws of the State of Western Australia, Australia; |

| | • | | “Exxaro” refers to Exxaro Resources Limited, a public company organized under the laws of the Republic of South Africa; |

| | • | | “Exxaro Mineral Sands” refers to Exxaro’s mineral sands business that will be contributed to Tronox Limited as part of the Transaction; |

| | • | | “Acquired Companies” refers to all of the entities that comprise Exxaro Mineral Sands; |

| | • | | “New Tronox” refers to the combined businesses of Tronox Incorporated and Exxaro Mineral Sands after completion of the Transaction; |

| | • | | “Merger Sub One” refers to Concordia Acquisition Corporation, a Delaware corporation and an indirect, wholly-owned subsidiary of Tronox Incorporated; |

| | • | | “Merger Sub Two” refers to Concordia Merger Corporation, a Delaware corporation and an indirect, wholly-owned subsidiary of Tronox Incorporated; |

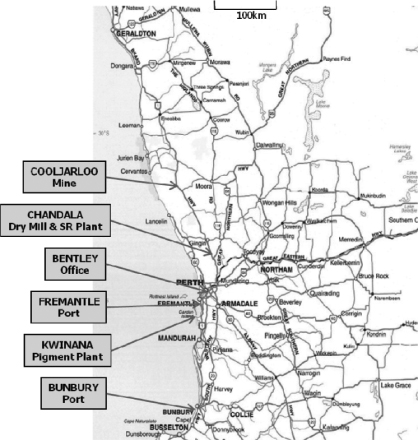

| | • | | The “Tiwest Joint Venture” is a joint venture between Tronox Incorporated and Exxaro in Western Australia, Australia which operates a chloride process TiO2 plant located in Kwinana, Western Australia, a mining venture in Cooljarloo, Western Australia, a mineral separation plant and a synthetic rutile processing facility, both in Chandala, Western Australia; |

| | • | | “Exxaro Holdings Sands” means Exxaro Holdings Sands Proprietary Limited, a company organized under the laws of the Republic of South Africa and a wholly-owned subsidiary of Exxaro; |

| | • | | “Exxaro Sands” refers to Exxaro Sands Proprietary Limited, a company organized under the laws of the Republic of South Africa; |

| | • | | “Exxaro TSA Sands” refers to Exxaro TSA Sands Proprietary Limited, a company organized under the laws of the Republic of South Africa; |

| | • | | “South African Acquired Companies” means Exxaro Sands and Exxaro TSA Sands; |

| | • | | “Class A Shares” refers to the Class A ordinary shares of Tronox Limited; |

| | • | | “Class B Shares” refers to the Class B ordinary shares of Tronox Limited; |

| | • | | “Exchangeable Shares” refers to Exchangeable Shares of Tronox Incorporated, each of which is exchangeable for one Class A Share and an amount in cash equal to $12.50 without interest; |

1

| | • | | “Transaction Agreement” refers to the Transaction Agreement dated as of September 25, 2011 by and among Tronox Incorporated, Tronox Limited, Merger Sub One, Merger Sub Two, Exxaro, Exxaro Holdings Sands Proprietary Limited, a company organized under the laws of the Republic of South Africa and wholly-owned subsidiary of Exxaro and Exxaro International BV, a company organized under the laws of the Netherlands and wholly-owned subsidiary of Exxaro, a copy of which is included in the registration statement of which this proxy statement/prospectus forms a part, and which is incorporated herein by reference (the parties expect to amend the Transaction Agreement to reflect an additional internal merger and certain corporate restructurings, among other revisions. The descriptions of the Transaction Agreement and the Transaction contained herein, including all references to the Mergers, reflect these expected amendments); |

| | • | | “Transaction” refers to the transactions contemplated by the Transaction Agreement, including the Mergers, as more fully described under the captions “The Transaction” and “Description of Transaction Documents”; |

| | • | | “First Merger” refers to the merger of Concordia Acquisition Corporation with and into Tronox Incorporated; |

| | • | | “Second Merger” refers to the merger of Concordia Merger Corporation with and into Tronox Incorporated; |

| | • | | “Mergers” refers to the First Merger and the Second Merger, together; and |

| | • | | “Unissued Share Merger Consideration” means Class A Shares required to be issued as consideration in the First Merger (excluding any Class A Shares required to be issued on conversion of Exchangeable Shares), but which have not been issued. |

Solely for the convenience of the reader, this proxy statement/prospectus contains translations of certain Australian dollar amounts into U.S. dollars at specified rates. Except as otherwise stated in this proxy statement/prospectus, all translations from Australian dollars to U.S. dollars are based on the noon buying rate of A$0.94 per $1.00 in the City of New York for cable transfers of Australian dollars, as certified for customs purposes by the Federal Reserve Bank of New York on January 15, 2012. In addition, this proxy statement/prospectus also contains U.S. dollar equivalent amounts of certain South African Rand amounts. Except as otherwise stated in this proxy statement/prospectus, all translations from South African Rand to U.S. dollars are based on (i) the closing rate as reported on the last business day of the period, (ii) acquisitions, disposals, share issuances and specific items within equity at the closing rate at the date the transaction was recognized, and (iii) income statement items at the average closing rate for the period. Estimated capital expenditures and estimated lost revenue and costs associated with furnace shutdowns have been translated at the closing rate used for balance sheet items as of June 30, 2011.

| | | | |

| Period ended | | Average(1) | | Period End(1) |

| June 30, 2011 | | 6.89 | | 6.76 |

| June 30, 2010 | | 7.53 | | 7.63 |

| December 31, 2010 | | 7.33 | | 6.62 |

| December 31, 2009 | | 8.42 | | 7.38 |

| December 31, 2008 | | 8.27 | | 9.35 |

(1) Factiva

No representation is made that the Australian dollar or South African Rand amounts referred to in this proxy statement/prospectus could have been or could be converted into U.S. dollars at such rates or any other rates. Any discrepancies in any table between totals and sums of the amounts listed are due to rounding.

2

INDUSTRY AND MARKET DATA

This proxy statement/prospectus includes market share, market position and industry data and forecasts. Industry publications, surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable. Tronox Incorporated and Exxaro Mineral Sands participate in various trade associations, such as the Titanium Dioxide Manufacturers Association (“TDMA”), and subscribe to various industry research publications, such as those produced by TZ Minerals International Pty Ltd (“TZMI”). While we have taken reasonable actions to ensure that the information is extracted accurately and in its proper context, we have not independently verified the accuracy of any of the data from third party sources or ascertained the underlying economic assumptions relied upon therein. Statements as to our market share and market position are based on the most currently available market data obtained from such sources.

3

QUESTIONS AND ANSWERS ABOUT THE TRANSACTION

Following are brief answers to certain questions that you may have regarding the proposals being considered at the special meeting of Tronox Incorporated stockholders, which we refer to as the special meeting. Tronox Incorporated urges you to read carefully this entire proxy statement/prospectus, including the exhibits to the registration statement of which this proxy statement/prospectus forms a part because this section does not provide all the information that might be important to you.

| Q: | When and where is the meeting of the stockholders? |

| A: | The special meeting of Tronox Incorporated’s stockholders will take place at , Eastern time, on , 2012, in New York, New York. We provide additional information relating to the special meeting in the section entitled “The Special Meeting of Tronox Incorporated Stockholders.” |

| Q: | Who can vote at the special meeting? |

| A: | If you are a Tronox Incorporated stockholder of record as of the close of business on , 2012, the record date for the special meeting, you are entitled to receive notice of and to vote at the special meeting. |

| A: | If you are a stockholder of record of Tronox Incorporated as of the record date for the special meeting, you may cast your vote in person at the special meeting. You may also authorize a proxy to vote by timely: |

| | • | | accessing the internet website specified on your proxy card; |

| | • | | calling the toll-free number specified on your proxy card; or |

| | • | | signing the enclosed proxy card and returning it in the postage-paid envelope provided. |

If you hold Tronox Incorporated common stock in “street name” through a bank, broker or other nominee, please follow the voting instructions provided by your bank, broker or other nominee to ensure that your shares are represented at the special meeting. If you hold shares through a bank, broker, custodian or other record holder and wish to vote at the special meeting, you will need to obtain a “legal proxy” from your bank, broker or other nominee.

| Q: | What will happen in the Transaction? |

| A: | In the Transaction, the existing businesses of Tronox Incorporated will be combined with the newly acquired Exxaro Mineral Sands business under a new Australian holding company, Tronox Limited. The Transaction will be effected in two primary steps: |

In the first step, Tronox Incorporated will participate in the Mergers, as a result of which it will become a subsidiary of Tronox Limited. In the Mergers, each share of Tronox Incorporated common stock will be converted into, at the holder’s election, either (i) one Class A Share and an amount in cash equal to $12.50 without interest or (ii) one Exchangeable Share (subject to the proration procedures described in this proxy statement/prospectus), which is exchangeable for one Class A Share and an amount in cash equal to $12.50 without interest. The Exchangeable Shares will not be transferable until after December 31, 2012 but the Class A Shares, including those deliverable upon the exchange of an Exchangeable Share, will be transferable. We refer to the consideration to be received by holders of Tronox Incorporated common stock in the Mergers as the “Transaction Consideration” in this proxy statement/prospectus. Unless you elect to receive Exchangeable Shares, you will receive Class A Shares of Tronox Limited and cash in the Mergers, and therefore become subject to the Constitution of Tronox Limited and applicable provisions of Australian law.

4

In the second step, Tronox Limited will acquire Exxaro Mineral Sands and, in consideration therefor, Tronox Limited will issue 9,950,856 Class B Shares to Exxaro and Exxaro International BV. Exxaro Mineral Sands is composed of Exxaro Sands and Exxaro TSA Sands in South Africa and Exxaro’s 50.0% interest in the Tiwest Joint Venture.

Upon completion of the Transaction, assuming the exchange of all Exchangeable Shares, the former Tronox Incorporated stockholders will own all of the Class A Shares, representing approximately 61.5% of the voting securities of Tronox Limited, and Exxaro will own all of the Class B Shares, representing approximately 38.5% of the voting securities of Tronox Limited. Exxaro will retain a 26.0% ownership interest in the South African operations that are part of Exxaro’s mineral sands business in order to comply with ownership requirements of Black Economic Empowerment (“BEE”) legislation in South Africa. The retained ownership interest in the South African operations may be exchanged for Class B Shares under certain circumstances, resulting in Exxaro owning approximately 41.7% of the voting securities of Tronox Limited after such exchange (based on the total number of issued voting shares immediately after completion of the transactions contemplated by the Transaction Agreement and assuming the exchange of all Exchangeable Shares and no subsequent issuances of new Tronox Limited shares).

We provide additional information on the Transaction under the headings “The Transaction” and “The Transaction Documents.”

| Q: | What will I receive for my shares? |

| A: | If you are a Tronox Incorporated stockholder, upon completion of the Mergers, each share of Tronox Incorporated common stock that you own immediately prior to the Transaction will convert into, at your election, either (i) one Class A Share and an amount in cash equal to $12.50 without interest or (ii) one Exchangeable Share (subject to the proration procedures described in this proxy statement/prospectus), each of which is exchangeable for one Class A Share and an amount in cash equal to $12.50 without interest. If you fail to make any election with respect to any of the shares of Tronox Incorporated common stock you own, each of your shares of Tronox Incorporated common stock will be converted into one Class A Share and an amount in cash equal to $12.50 without interest. Unless you elect to receive Exchangeable Shares, you will receive Class A Shares and cash in the Mergers, and therefore become subject to the Constitution of Tronox Limited and applicable provisions of Australian law. For a discussion of the material differences between the current rights of Tronox Incorporated stockholders and the rights they will have as holders of Class A Shares of Tronox Limited, see “Comparative Rights of Stockholders of Tronox Incorporated and Shareholders of Tronox Limited.” We provide additional information on the consideration to be received in the Transaction under the headings “The Transaction.” |

| Q: | How do I make an election to receive Class A Shares or Exchangeable Shares in the Transaction? |

| A: | Each Tronox Incorporated stockholder is being sent an election form and transmittal materials. You must properly complete and deliver to the exchange agent the election materials, together with your stock certificates if you hold stock certificates for your shares of Tronox Incorporated common stock (your election form will not be deemed properly completed if you fail to deliver such stock certificates to the exchange agent). A postage-paid return envelope will be enclosed for submitting the election form and certificates to the exchange agent. This is a different envelope from the envelope that you will use to return your completed proxy card.Please do not send your stock certificates or form of election in the envelope with your proxy card. |

If your shares are held in a brokerage or other custodial account, you should receive instructions from the entity which holds your shares advising you of the procedures for making your election and delivering your shares. If you do not receive these instructions, you should contact the entity which holds your shares.

In the event the Transaction Agreement is terminated, any Tronox Incorporated stock certificates that you previously sent to the exchange agent will be promptly returned to you without charge.

5

| Q: | Can I make one election for some of my shares and another election for the rest? |

| A: | Yes. Each election form permits the holder to specify the number of such holder’s shares of Tronox Incorporated common stock with respect to which such holder makes an election to receive Class A Shares or Exchangeable Shares in the Transaction. Such election will be honored, subject to the proration procedures with respect to the Exchangeable Shares described in this proxy statement/prospectus and provided that a minimum number of holders of Tronox Incorporated common stock make an Exchangeable Share Election as described in “The Exchangeable Share Election.” |

| Q: | What if I change my mind after I have made an election with respect to my shares? |

| A: | You can revoke or change your previous election by submitting a subsequently dated, properly completed election form to the exchange agent prior to the election deadline. |

| Q: | What if I do not make an election? |

| A: | Any share of Tronox Incorporated common stock for which an election is not made will, as a result of the Mergers, be converted into one Class A Share and an amount in cash equal to $12.50 without interest. An election shall be deemed not to have been made if the exchange agent has not received an effective, properly completed election form and, if you hold stock certificates for your shares of Tronox Incorporated common stock, such stock certificates, on or before 5:00 p.m., New York time, on the business day that is four business days prior to completion of the Transaction. Tronox Limited will publicly announce the closing date as soon as reasonably practicable, in any event not less than five business days prior to completion of the Transaction. |

Subject to the terms of the Transaction Agreement and the election form, the exchange agent, in consultation with Tronox Incorporated, will have reasonable discretion to determine whether any election, revocation or change has been properly or timely made and to disregard immaterial defects in the election forms. Any good faith decisions of the exchange agent regarding such matters shall be binding and conclusive. None of the parties to the Transaction Agreement or the exchange agent shall be under any obligation to notify any person of any defect in an election form.

| Q: | May I submit a form of election if I vote against the Merger Proposal? |

| A: | Yes. You may submit a form of election even if you vote against the Merger Proposal. However, if you have submitted a valid demand for appraisal for your shares, any election form submitted by you with respect to such shares will have no effect and if you subsequently withdraw your demand for appraisal such shares will be treated as if no election was made with respect to them. |

| Q: | When will I receive the Transaction Consideration? |

| A: | If you made a valid election with respect to your shares of Tronox Incorporated common stock prior to the election deadline, as promptly as practicable after completion of the Transaction, you will receive (i) a book-entry representing the number of whole shares of Class A Shares or Exchangeable Shares that you are entitled to receive after taking into account all the shares of Tronox Incorporated common stock (whether in book-entry form or represented by certificates) you have surrendered prior to completion of the Transaction and (ii) a check for the cash that you are entitled to receive, including, to the extent applicable, the cash portion of the Transaction Consideration, cash in lieu of any fractional shares as described in “The Exchangeable Share Election—No Fractional Shares” and other dividends or distributions, if any, as described in “The Exchangeable Share Election—Dividends or Distributions.” |

If you did not surrender your shares of Tronox Incorporated common stock prior to completion of the Transaction, as promptly as practicable following completion of the Transaction, Tronox Limited will cause the exchange agent to mail to you a letter of transmittal and instructions for use in surrendering the certificates (or affidavits of loss in lieu thereof) or book-entry shares of Tronox Incorporated common stock

6

in exchange for the Transaction Consideration. You will receive the Transaction Consideration upon surrender of your shares of Tronox Incorporated common stock to the exchange agent, together with the required letter of transmittal, duly completed and validly executed, and/or any other documents that the exchange agent may reasonably require.

We will issue Class A Shares or Exchangeable Shares, as applicable, to holders of Tronox Incorporated common stock in uncertificated book-entry form unless the holder requests a physical certificate for its Class A Shares or Exchangeable Shares.

| Q: | What are the material U.S. federal income tax consequences of the Transaction? |

| A: | In the opinion of our U.S. tax counsel, Kirkland & Ellis LLP, for U.S. federal income tax purposes, the exchange of a share of Tronox Incorporated common stock for a Class A Share and an amount in cash equal to $12.50 without interest will be a taxable exchange for a U.S. Holder (as defined in “The Transaction—Material U.S. Federal Income Tax Consequences of the Transaction”), while the exchange of a share of Tronox Incorporated common stock for an Exchangeable Share should not be a taxable exchange for a U.S. Holder unless and until such Exchangeable Share is converted into a Class A Share and an amount in cash equal to $12.50 without interest. In contrast, for U.S. federal income tax purposes, none of (i) the exchange of a share of Tronox Incorporated common stock for a Class A Share and an amount in cash equal to $12.50 without interest, (ii) the exchange of a share of Tronox Incorporated common stock for an Exchangeable Share, or (iii) the subsequent exchange of an Exchangeable Share into a Class A Share and an amount in cash equal to $12.50 without interest should generally be subject to tax for a Non-U.S. Holder (as defined in “The Transaction—Material U.S. Federal Income Tax Consequences of the Transaction”), in each case unless certain exceptions apply. Tax circumstances may be different in jurisdictions outside the United States. Each taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor. |

We provide a more complete description of the material U.S. federal income tax consequences of the Transaction under the heading “The Transaction—Material U.S. Federal Income Tax Consequences of the Transaction.”

| Q: | Why is Tronox Incorporated offering Exchangeable Shares to holders of Tronox Incorporated common stock in the Transaction? |

| A: | The Exchangeable Share structure will provide an opportunity for Tronox Incorporated stockholders to retain their interest in Tronox Incorporated following completion of the Transaction. The primary reason for offering the Exchangeable Shares is to permit U.S. Holders of Tronox Incorporated who elect to receive Exchangeable Shares to report their receipt of the Exchangeable Shares as a tax-free transaction and defer the recognition of gain or loss for U.S. federal income tax purposes until the Exchangeable Shares are subsequently exchanged for Class A Shares and cash. However, U.S. Holders who elect to receive Exchangeable Shares will be required to recognize gain or loss for U.S. federal income tax purposes when (i) they exchange their Exchangeable Shares for Class A Shares and cash, (ii) Tronox Incorporated exercises its right to redeem the Exchangeable Shares for Class A Shares and cash, or (iii) Tronox Limited exercises its right to require Tronox Incorporated to redeem the Exchangeable Shares for Class A Shares and cash. |

7

| Q: | What are the principal differences between electing to receive Class A Shares and cash and electing to receive Exchangeable Shares in connection with the Transaction? |

| A: | Before the Exchangeable Shares are exchanged for Class A Shares and cash, the principal differences between receiving Class A Shares and cash and Exchangeable Shares are the following: |

| | | | |

| | | Class A Shares and Cash | | Exchangeable Shares |

| Tax Consequences | | The receipt of Class A Shares and cash will be a taxable transaction for U.S. Holders. | | The receipt of Exchangeable Shares should be a tax-free transaction for U.S. Holders |

| Dividend and Voting Rights | | You will hold an equity interest in Tronox Limited and be entitled to all the rights of shareholders in Tronox Limited contemplated by the Constitution, including the receipt of dividends and other distributions by Tronox Limited and voting rights at shareholder meetings of Tronox Limited. | | You will continue to hold an equity interest in Tronox Incorporated, a majority-owned subsidiary of Tronox Limited, and be entitled to all the rights of shareholders in Tronox Incorporated contemplated by its charter and bylaws as in effect after the Mergers, including the receipt of dividends and other distributions by Tronox Incorporated and voting rights at shareholder meetings of Tronox Incorporated. Holders of Exchangeable Shares will not be entitled to receive any dividends or other distributions by Tronox Limited or to vote on any matters subject to a vote of the shareholders of Tronox Limited unless and until their Exchangeable Shares are exchanged or redeemed for Class A Shares and cash. |

| Transferability | | The Class A Shares are expected to be listed for trading on . | | The Exchangeable Shares will be non-transferable until December 31, 2012. |

| Q: | Why are Class B Shares being issued to Exxaro? |

| A: | In consideration for Exxaro Mineral Sands, Tronox Limited will issue 9,950,856 Class B Shares to Exxaro and Exxaro International BV. Assuming all the Exchangeable Shares are exchanged for Class A Shares, the Class B Shares will constitute approximately 38.5% of the outstanding voting securities of Tronox Limited immediately after completion of the Transaction. Class B Shares have different rights than Class A Shares. For example, the Transaction Agreement provides that, immediately following completion of the Transaction, the board of directors of Tronox Limited will consist of nine members, six of whom will be designated by Tronox Incorporated (of whom at least one will be ordinarily resident in Australia), and three of whom will be designated by Exxaro (of whom at least one will be ordinarily resident in Australia). Following the closing of the Transaction, Exxaro will continue to be able to appoint a certain number of representatives to the board of directors of Tronox Limited based on the number of Class B Shares it owns. Tronox Limited’s proposed constitution (the “Constitution”) provides that, for as long as the voting interest held by holders of Class B Shares (the “Class B Voting Interest”) is at least 10.0% of the total voting interest in Tronox Limited, there must be nine directors on the board of directors; and the holders of Class A Shares will be entitled to vote separately to elect a certain number of directors to the board (the “Class A Directors”), and the holders of Class B Shares will be entitled to vote separately to elect a certain number of directors to the board (the “Class B Directors”). If the Class B Voting Interest is: greater than or equal to |

8

| | 30.0%, the board of directors will consist of six Class A Directors and three Class B Directors; greater than or equal to 20.0% but less than 30.0%, the board of directors will consist of seven Class A Directors and two Class B Directors; and greater than or equal to 10.0% but less than 20.0%, the board of directors will consist of eight Class A Directors and one Class B Director. |

Also, the Constitution provides that, subject to certain limitations, for as long as the Class B Voting Interest is at least 20.0%, a separate vote by holders of Class A Shares and Class B Shares is required to approve certain types of mergers or similar transactions that result in a change in control or a sale of all or substantially all of the assets of Tronox Limited, or any reorganization or similar transaction that does not treat Class A Shares and Class B Shares equally.

For more information regarding ownership of Class B Shares by Exxaro and the rights associated with Class B Shares, see the sections of this proxy statement/prospectus entitled “Description of the Transaction Documents—Shareholder’s Deed” and “Governance of Tronox Limited.”

| Q | Why is Exxaro retaining an interest in Exxaro Mineral Sands’s South African operations? |

| A: | Exxaro will retain a 26.0% ownership interest in each of Exxaro Sands and Exxaro TSA Sands in order for these two entities to comply with the requirements of the Mineral and Petroleum Resources Development Act, 28 of 2002 (“MPRDA”) and the Broad-Based Socio-Economic Empowerment Charter for the South African Mining and Minerals Industry (the “South African Mining Charter”). Exxaro has agreed to hold such ownership interest until the earlier of the 10th anniversary of completion of the Transaction and the date when the South Africa Department of Mineral Resources (the “DMR”) determines that ownership is no longer required under Black Economic Empowerment legislation in South Africa. Exxaro’s 26.0% direct ownership interest in Exxaro Sands and Exxaro TSA Sands is subject to put/call arrangements with Tronox Limited, which allows the ownership interest to be exchanged for approximately 1.45 million additional Class B Shares in certain circumstances if the DMR determines that such ownership is no longer required. Exxaro may accelerate the put right in connection with a change of control of Tronox Limited. If Exxaro’s ownership interest in Exxaro Sands and Exxaro TSA Sands is exchanged for Class B Shares, Exxaro will own Class B Shares representing approximately 41.7% of the voting securities of Tronox Limited (calculated based on the number of issued shares of Tronox Limited immediately following completion of the Transaction and assuming the exchange of all Exchangeable Shares and no subsequent issuances of new Tronox Limited shares). |

For more information regarding Exxaro’s interest in Exxaro Mineral Sands’s South African operations, see “Description of the Transaction Documents—Shareholder’s Deed—Put/Call Option.”

| Q: | Why did Tronox Incorporated decide to pursue the Transaction? |

| A: | Based on 2010 numbers, the Transaction will join the world’s fifth largest producer and marketer of titanium dioxide (“TiO2”), Tronox Incorporated, with the world’s third largest producer of titanium feedstock and zircon, Exxaro Mineral Sands, which we believe will provide Tronox Limited with a strategic competitive advantage by assuring it of the supply of critical feedstock for its TiO2-producing operations and allowing it to participate in the financial performance of two levels of this industry. We believe that the combination of the existing business of Tronox Incorporated with Exxaro Mineral Sands will provide Tronox Incorporated stockholders and its customers and employees with substantial strategic and financial benefits, including expected cost savings and revenue opportunities. We expect these benefits to include: |

| | • | | Improving the flexibility and manageability of a key raw material. |

| | • | | Positioning of New Tronox as a highly efficient, vertically-integrated TiO2 producer; and |

| | • | | Ensuring a secure titanium feedstock supply in the near-term and long-term. |

We include additional information on the reasons for the Transaction and other factors considered by the Tronox Incorporated board of directors under the headings “The Transaction—Tronox Incorporated’s Reasons for the Transaction; Recommendation of the Tronox Incorporated Board of Directors.”

9

| Q: | Why is the new holding company, Tronox Limited, organized under the laws of Australia? |

| A: | Tronox Incorporated’s headquarters are located in the United States, as are other operations of its business. Exxaro’s headquarters are located in South Africa. Both Tronox Incorporated and Exxaro have significant operations and assets in Australia through their interests in the Tiwest Joint Venture. Australia is therefore a convenient location for the new holding company under which the existing businesses of Tronox and Exxaro Mineral Sands will be combined. In addition, Australia is a commercially practical location because it has an established and stable legal and regulatory system which is familiar with the resources and manufacturing sectors. Australia also has a taxation system with attributes that encourage foreign investment. Reforms to the Australian taxation system introduced following the Federal Government’s Review of International Taxation Arrangements were designed to maintain and enhance Australia’s status as an attractive place for business and investment, including improving Australia’s attractiveness as a regional headquarters and base for multinational companies. In addition, Tronox Limited will be able to repatriate profits from non-Australian operations to its U.S. shareholders via unfranked dividends, without the imposition of additional Australian income or dividend withholding tax. This should increase Tronox Limited’s flexibility to pay dividends from these profits. If the combined business was based in another jurisdiction in which it conducts business, foreign earnings (relative to that jurisdiction) might have been subject to additional corporate taxation in that jurisdiction. |

| Q: | What happens to the equity awards held by directors and officers which have not yet vested upon completion of the Transaction? |

| A: | With some exceptions, all the equity awards held by directors and officers will vest upon completion of the Transaction. For a further discussion, see “Executive Compensation—Elements of Executive Compensation—Change in Control.” |

| Q: | Are there risks associated with the Transaction that I should consider in deciding how to vote? |

| A: | Yes. There are a number of risks related to the Transaction that are discussed in this proxy statement/prospectus. In evaluating the Merger Proposal, you should carefully read the detailed description of the risks associated with the Transaction described under the heading “Risk Factors” and other information included in this proxy statement/prospectus. |

| Q: | Who will serve on the board of directors and management of Tronox Limited following completion of the Transaction? |

| A: | The Transaction Agreement provides that, immediately following the closing, the board of directors of Tronox Limited will consist of nine members, six of whom will be designated by Tronox Incorporated (of whom at least one will be ordinarily resident in Australia) and three of whom will be designated by Exxaro (of whom at least one will be ordinarily resident in Australia). |

We expect the current management of Tronox Incorporated to serve in similar capacities in Tronox Limited following completion of the Transaction. We provide additional information on the board of directors of Tronox Limited following completion of the Transaction under the heading “The Transaction—The Governance of Tronox Limited Following Completion of the Transaction.”

| Q: | Where will Tronox Limited be headquartered following completion of the Transaction? |

| A: | The board of directors of Tronox Limited will consider the appropriate location for the operational headquarters but expects that it will be in the United States. |

10

| Q: | What vote is required to approve the Merger Proposal? |

| A: | The Merger Proposal must be approved by the affirmative vote by holders of a majority of the shares of Tronox Incorporated common stock outstanding on the record date for the special meeting. Abstentions and broker non-votes will have the same effect as votes against the Merger Proposal. |

As of , 2012, the record date for the special meeting of Tronox Incorporated stockholders, % of the outstanding shares of Tronox Incorporated common stock were owned by the directors and executive officers of Tronox Incorporated.

We provide additional information on the stockholder vote required to approve the Merger Proposal under the heading “The Special Meeting of Tronox Incorporated Stockholders.”

| Q: | What constitutes a quorum for the special meeting? |

| A: | The presence or representation of holders of a majority in voting power of shares of Tronox Incorporated common stock issued and outstanding as of the record date at the special meeting of Tronox Incorporated stockholders, whether present in person or represented by proxy, is required in order to conduct business at the special meeting. This requirement is called a quorum. Abstentions will be treated as present for the purposes of determining the presence or absence of a quorum; broker non-votes will not count towards quorum. |

| Q: | If I hold my shares in street name through my broker, will my broker vote my shares for me? |

| A: | If you hold your shares in a stock brokerage account or through a bank, broker or other nominee (that is, in street name), you must provide the record holder of your shares with instructions on how to vote your shares. Please follow the voting instructions provided by your bank, broker or other nominee. You may not vote shares held in street name by returning a proxy card directly to Tronox Incorporated or by voting in person at your special meeting unless you provide a “legal proxy,” which you must obtain from your broker or other nominee. Further, brokers who hold shares of Tronox Incorporated common stock on behalf of their customers may not give a proxy to Tronox Incorporated to vote those shares without specific instructions from their customers. |

If you are a Tronox Incorporated stockholder and you do not instruct your broker on how to vote your shares, your broker may not vote your shares to approve the Merger Proposal or to approve the Adjournment Proposal. We refer to this as a “broker non-vote.” A broker non-vote:

| | • | | will have the same effect as a “no” vote on the Merger Proposal; and |

| | • | | will have no effect on the Adjournment Proposal. |

| Q: | What effect does the Transaction have on any outstanding warrants to purchase shares of Tronox Incorporated common stock? |

| A: | Each outstanding warrant to purchase shares of Tronox Incorporated common stock will be adjusted at closing to provide that the obligations of Tronox Incorporated will be assumed by Tronox Limited without any action on the part of the holder of such warrant. Each outstanding warrant will become a warrant to acquire, under the same terms and conditions, upon payment of the exercise price, at the option of the warrantholder: (1) a share of common stock of Tronox Limited and $12.50 in cash, or (2) an Exchangeable Share (provided there are Exchangeable Shares outstanding immediately following the completion of the Transaction). Any fractional Class A Shares resulting from an aggregation of all such warrants granted to the holder under a particular award agreement with the same exercise price shall be rounded down. |

| Q: | What do I need to do now? |

| A: | After carefully reading and considering the information contained in or incorporated by reference into this proxy statement/prospectus, please vote your proxy by telephone or Internet, or by completing and signing |

11

| | your proxy card and returning it in the enclosed postage-paid envelope as soon as possible so that your shares may be represented at the special meeting. In order to ensure that your vote is recorded, please vote your proxy as instructed on your proxy card even if you currently plan to attend the special meeting in person. |

We provide additional information on voting procedures under the headings “The Special Meeting of Tronox Incorporated Stockholders—How to Vote.”

| Q: | How will my proxy be voted? |

| A: | If you vote by telephone, by Internet, or by completing, signing, dating and returning your signed proxy card, your proxy will be voted in accordance with your instructions. If you sign, date, and send your proxy card and do not indicate how you want to vote on any particular proposal, we will vote your shares in favor of that proposal. |

We provide additional information on voting procedures under the headings “The Special Meeting of Tronox Incorporated Stockholders—Voting of Proxies.”

| A: | Yes. If you are a stockholder of record of Tronox Incorporated common stock at the close of business on , 2012, you may attend the special meeting and vote your shares in person, in lieu of submitting your proxy by telephone, Internet or returning your signed proxy card. If you hold your shares through a bank, broker, custodian or other record holder, you must provide a “legal proxy” at the special meeting, which you must obtain from your broker or other nominee. |

| Q: | What must I bring to attend the special meeting of Tronox Incorporated stockholders? |

| A: | Only stockholders of record of Tronox Incorporated common stock at the close of business on , 2012 or their authorized representatives may attend the special meeting. If you wish to attend the special meeting, bring your proxy or your voter information form. You must also bring photo identification. If you hold your shares through a bank, broker, custodian or other record holder, you must also bring proof of ownership such as the voting instruction form from your broker or other nominee or an account statement. |

| Q: | What does it mean if I receive more than one set of materials? |

| A: | This means you own shares of Tronox Incorporated common stock that are registered under different names. For example, you may own some shares directly as a stockholder of record and other shares through a broker or you may own shares through more than one broker. In these situations, you will receive multiple sets of proxy materials. You must vote, sign and return all of the proxy cards or follow the instructions for any alternative voting procedure on each of the proxy cards you receive in order to vote all of the shares you own. Each proxy card you receive will come with its own postage-paid return envelope; if you vote by mail, make sure you return each proxy card in the return envelope that accompanied that proxy card. |

| Q: | What do I do if I want to change my vote? |

| A: | Send a later-dated, signed proxy card so that we receive it prior to the special meeting or attend the special meeting in person and vote. You may also revoke your proxy card by sending a notice of revocation that we receive prior to the special meeting to the Tronox Incorporated Corporate Secretary at the address under the heading “The Special Meeting of Tronox Incorporated Stockholders—Revocability of Proxies.” You may also change your vote by telephone or internet. You may change your vote by using any one of these methods regardless of the procedure used to cast your previous vote. |

We provide additional information on changing your vote under the headings “The Special Meeting of Tronox Incorporated Stockholders—Revocability of Proxies.”

12

| Q: | Should I send in my share certificates now? |

| A: | You should receive, along with this proxy statement/prospectus, an election form and other transmittal materials with instructions for making an election and surrendering your shares of Tronox Incorporated common stock (whether in book entry form or represented by certificates). |

If you fail to complete the election form or submit your share certificates with your election form prior to the election deadline, as soon as practicable after completion of the Transaction, we will send written instructions for exchanging your shares of Tronox Incorporated common stock for the Transaction Consideration. However, you will no longer be able to make an election at such time and your shares of Tronox Incorporated common stock will be exchanged for Class A Shares and cash.

| Q: | When do you expect to complete the Transaction? |

| A: | The companies are targeting a closing during the first half of 2012, although we cannot assure completion by any particular date. Completion of the Transaction is conditioned upon the approval of the Merger Proposal by the Tronox Incorporated stockholders, as well as other customary closing conditions, including the receipt of various required regulatory approvals and third party consents described under the headings “The Transaction—Regulatory Matters” and the “The Transaction—Exxaro Third Party Consents.” |

| Q: | Do I have dissenters’ or appraisal rights as a holder of Tronox Incorporated common stock? |

| A: | Pursuant to Section 262 of the General Corporation Law of the State of Delaware (“Section 262”), Tronox Incorporated stockholders who do not vote in favor of the Merger Proposal and who comply with the applicable requirements of Section 262 have the right to seek appraisal of the fair value of such shares, as determined by the Delaware Court of Chancery, if the Mergers are completed. It is possible that the fair value as determined by the Delaware Court of Chancery may differ from the consideration to be received in the Mergers. |

Stockholders who wish to preserve any appraisal rights they may have must so advise Tronox Incorporated by submitting a demand for appraisal in the form described in this proxy statement/prospectus prior to the vote on the Merger Proposal. In addition to submitting a demand for appraisal, in order to preserve any appraisal rights you may have, you must not vote in favor of the Merger Proposal, must not surrender your shares for payment of the consideration, and must otherwise follow the procedures prescribed by Section 262.In view of the complexity of Section 262, Tronox Incorporated stockholders who may wish to dissent from the Merger Proposal and pursue appraisal rights should consult their legal advisors.For additional information, please see the sections titled “The Transaction—Appraisal Rights” and “Appraisal Rights.”

| Q: | How can I find more information about Tronox Limited, Tronox Incorporated and Exxaro Mineral Sands? |

| A: | For more information about Tronox Limited, Tronox Incorporated and Exxaro Mineral Sands, we suggest you read this proxy statement/prospectus in its entirety. In addition, see the section of this proxy statement/prospectus entitled “Where You Can Find More Information.” |

| Q: | Who can answer any questions I may have about the special meeting or the Transaction? |

| A: | Tronox Incorporated stockholders who have questions about the Transaction or the other matters to be voted on at the special meeting or desire additional copies of this proxy statement/prospectus or additional proxy cards should contact: |

Call toll-free: or

Call collect:

Email:

13

SUMMARY

This summary highlights selected information contained in this proxy statement/prospectus and does not contain all the information that may be important to you. Tronox Incorporated and Tronox Limited urge you to read carefully this proxy statement/prospectus in its entirety, as well as the exhibits to the registration statement of which this proxy statement/prospectus forms a part. Additional, important information is also contained in the documents incorporated by reference into this proxy statement/prospectus; see the section entitled “Where You Can Find More Information.”

Tronox Limited’s unaudited pro forma condensed combined statements of operations for the nine months ended September 30, 2011, and the year ended December 31, 2010, are presented as if the Transaction had been completed on January 1, 2010. The unaudited pro forma condensed combined balance sheet as of September 30, 2011, is presented as if the Transaction had been completed on September 30, 2011. For the purposes of this discussion, references to “we,” “us,” and “our” refer to New Tronox when discussing the business following completion of the Transaction and to Tronox Incorporated or Exxaro Mineral Sands, as the context requires, when discussing the business prior to completion of the Transaction.

Our Company

Overview

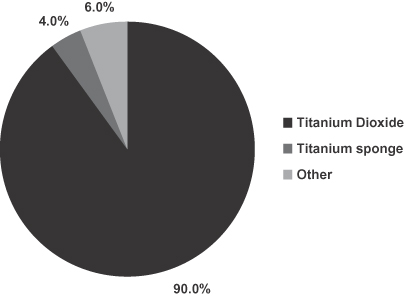

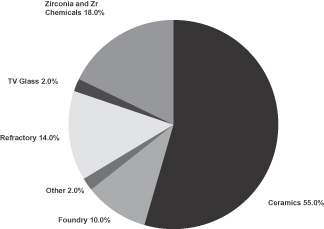

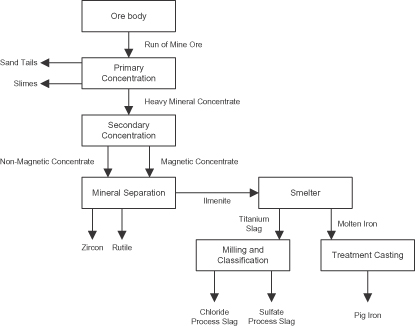

Based on 2010 numbers reported by TZMI, the Transaction will join the world’s fifth-largest producer and marketer of TiO2, Tronox Incorporated, with the world’s third-largest producer of titanium feedstock and second-largest producer of zircon, Exxaro Mineral Sands. New Tronox will be one of the leading integrated global producers and marketers of TiO2 and mineral sands. Our world-class, high-performance TiO2 products are critical components of everyday consumer applications such as coatings, plastics, paper and other applications. Our mineral sands business will consist primarily of two product streams – titanium feedstock and zircon. Titanium feedstock is used primarily to manufacture TiO2. Zircon, a hard, glossy mineral, is used for the manufacture of ceramics, refractories, TV glass and a range of other industrial and chemical products. In addition, we produce electrolytic manganese dioxide (“EMD”), sodium chlorate, boron-based and other specialty chemicals.

For the first nine months of 2011, we had pro forma net sales of $1.7 billion, pro forma adjusted EBITDA of $620.4 million, and pro forma income from continuing operations attributable to Tronox Limited of $865.2 million. In 2010, we had pro forma net sales of $1.7 billion, pro forma adjusted EBITDA of $335.7 million, and pro forma loss from continuing operations attributable to Tronox Limited of $44.6 million.

TiO2 Operations

We will be the world’s third-largest producer and marketer of TiO2 manufactured via chloride technology. We will have global operations in the Americas, Europe and the Asia-Pacific region. Our assured feedstock supply and global presence, combined with a focus on providing customers with world-class products, end-use market expertise and strong technical support, will allow us to continue to sell products to a diverse portfolio of customers in various regions of the world, with most of whom we have well-established relationships.

14

We will continue to supply and market TiO2 under the brand name TRONOX® to more than 1,000 customers in approximately 90 countries, including market leaders in each of the key end-use markets for TiO2 and have supplied each of our top ten customers with TiO2 for more than 10 years. These top ten customers represented approximately 44% of our total TiO2 sales volume in 2010. The tables below summarize our 2010 TiO2 sales volume by geography and end-use market:

| | | | | | | | | | |

2010 Sales Volume by Geography | | | | 2010 Sales Volume by End-Use Market | |

North America | | 40.0% | | | Paints and Coatings | | | 78.0 | % |

Latin America | | 8.0% | | | Plastics | | | 19.0 | % |

Europe | | 22.0% | | | Paper and Specialty | | | 3.0 | % |

Asia-Pacific | | 30.0% | | | | | | | | |

We will continue to operate three TiO2 facilities at Hamilton, Mississippi, Botlek, The Netherlands and Kwinana, Australia representing 465,000 tonnes of annual TiO2 production capacity. We are one of a limited number of TiO2 producers in the world with chloride production technology, which we believe is preferred for many of the largest end-use applications compared to TiO2 manufactured by other TiO2 production technologies. We hold more than 200 patents worldwide and have a highly skilled work force.

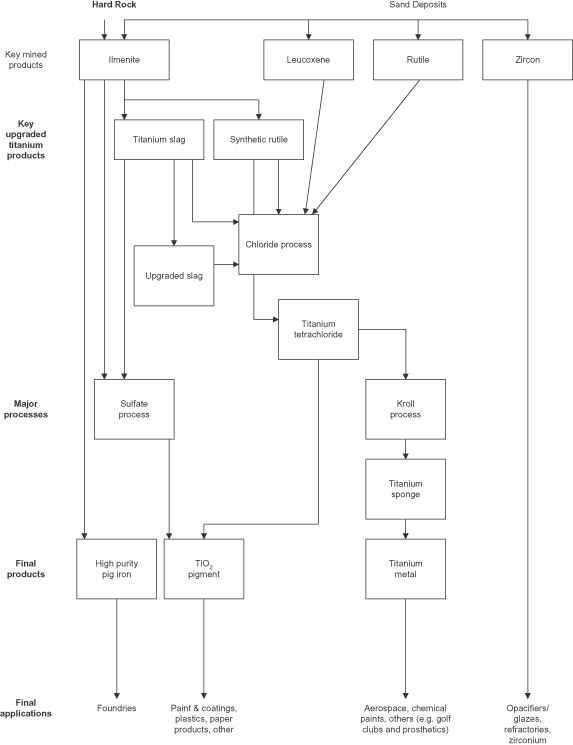

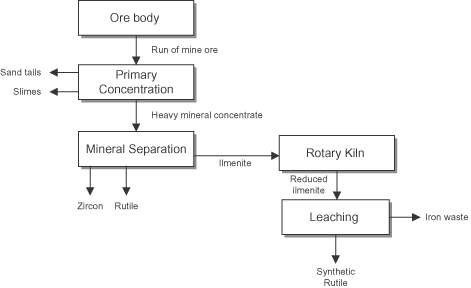

Mineral Sands Operations

Our mineral sands operations will consist of two product streams – titanium feedstock, which includes ilmenite, natural rutile, titanium slag and synthetic rutile, and zircon, which is contained in the mineral sands we extract to capture our natural titanium feedstock. Based on Exxaro’s internal estimates and data reported by TZMI, in 2010 Exxaro Mineral Sands was the third-largest titanium feedstock producer with approximately 10% of global titanium feedstock production and the second-largest zircon producer with approximately 20% of global zircon production. We will operate three separate mining operations: KZN Sands and Namakwa Sands located in South Africa and Tiwest located in Australia, which have a combined production capacity of 723,000 tonnes of titanium feedstock and 265,000 tonnes of zircon.

Titanium feedstock is the most significant raw material used in the manufacture of TiO2. We believe annual production of titanium feedstock from our mineral sands operations will continue to exceed the raw material supply requirement for our TiO2 operations. Zircon is primarily used as an additive in ceramic glazes, a market which has grown substantially during the previous decade and is favorably exposed to long-term development trends in the emerging markets, principally China.

The table set forth under “The Businesses—Description of Exxaro Mineral Sands—Properties and Reserves—Mineral Resources and Reserves” summarizes Exxaro Mineral Sands’s proven and probable ore reserves and estimated mineral resources as of December 31, 2010.

The mineral sands operations also produce high purity pig iron as a co-product. It is typically low in manganese, phosphorus and sulfur and is sold to foundries as a dilutant for trace elements and to steel producers for iron units.

Electrolytic and Other Chemical Products Operations

Our electrolytic and other chemical products operations are primarily focused on advanced battery materials, sodium chlorate and specialty boron products. Battery material end-use applications include alkaline batteries for flashlights, electronic games, medical and industrial devices as well as lithium batteries for power tools, hybrid electric vehicles, laptops and power supplies. Sodium chlorate is used in the pulp and paper industry in pulp bleaching applications. Specialty boron product end-use applications include semiconductors, pharmaceuticals, high-performance fibers, specialty ceramics and epoxies as well as igniter formulations.

15

We operate two electrolytic and other chemical facilities in the United States: one in Hamilton, Mississippi producing sodium chlorate and one in Henderson, Nevada producing EMD and boron products.

Industry Background and Outlook

TiO2 Industry Background and Outlook

TiO2 is used in a wide range of products due to its ability to impart whiteness, brightness and opacity. TiO2 is used extensively in the manufacture of coatings, plastics and paper and in a wider range of other applications, including inks, fibers, rubber, food, cosmetics and pharmaceuticals. TiO2 is a critical component of everyday consumer applications due to its superior ability to cover or mask other materials effectively and efficiently relative to alternative white pigments and extenders. We believe that, at present, TiO2 has no effective substitute because no other white pigment has the physical properties for achieving comparable opacity and brightness or can be incorporated in as cost-effective a manner. In addition to us, there are only four other major global producers of TiO2: E.I. du Pont de Nemours & Co., or Dupont; Millennium Inorganic Chemicals, Inc. (a subsidiary of National Titanium Dioxide Company Ltd.), or Cristal; Huntsman Corporation; and Kronos Worldwide Inc. Collectively, these five producers accounted for more than 60% of the global market in 2010, according to TZMI.

Based on publicly reported industry sales by the leading TiO2 producers, we estimate that global sales of TiO2 in 2010 exceeded 5.3 million tonnes, generating approximately $12 billion in industry-wide revenues. As a result of strong underlying demand and high TiO2 capacity utilization, TiO2 selling prices increased significantly in 2010 and have continued to increase in 2011. We believe average prices will continue to increase through the medium term due to the supply/demand dynamics and favorable outlook in the TiO2 industry. We believe demand for TiO2 from coatings, plastics and paper and specialty products manufacturers will continue to increase due to increasing per capita consumption in Asia and other emerging markets whereas we believe supply of TiO2 is constrained due to already high capacity utilization, and lack of publically announced new construction of additional greenfield production facilities, and limited incremental titanium feedstock supply available even if new production plants were to be constructed. At present, publicly reported TiO2 industry capacity expansions are almost exclusively through debottlenecking initiatives resulting in relatively modest industry-wide capacity additions.

TiO2 is produced using one of two commercial production processes: the chloride process and the sulfate process. The chloride process is a newer technology, and we believe it has several advantages over the sulfate process: it generates less waste, uses less energy, is less labor intensive and permits the direct recycle of a major process chemical, chlorine, back into the production process. Commercial production of TiO2 results in one of two different crystal forms, either rutile or anatase. Rutile TiO2 is preferred over anatase TiO2 for many of the largest end-use applications, such as coatings and plastics, because its higher refractive index imparts better hiding power at lower quantities than the anatase crystal form and it is more suitable for outdoor use because it is more durable. Although rutile TiO2 can be produced using either the chloride process or the sulfate process, customers often prefer rutile produced using the chloride process. All of our global production capacity utilizes the chloride process to produce rutile TiO2.

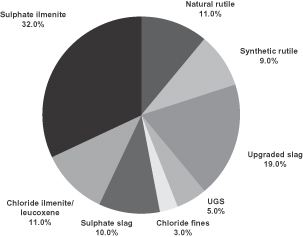

The primary raw materials that are used to produce TiO2 are various types of titanium feedstock, which include ilmenite, rutile, leucoxene, titanium slag (chloride slag and sulfate slag), upgraded slag and synthetic rutile. Based on TZMI titanium feedstock price forecasts and our own internal calculations, we estimate that global sales of titanium feedstock in 2010 exceeded 9.1 million tonnes, generating approximately $2.3 billion in industry-wide revenues. Titanium feedstock supply is currently experiencing supply constraints due to the depletion of legacy ore bodies, lack of investment in mining new deposits, and high risk and long lead time (typically up to 5 years) in starting new projects. At present, titanium feedstock industry capacity expansions are extremely limited and are expected to remain so over the medium term. Titanium feedstock prices, which are

16