UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31 2006

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number

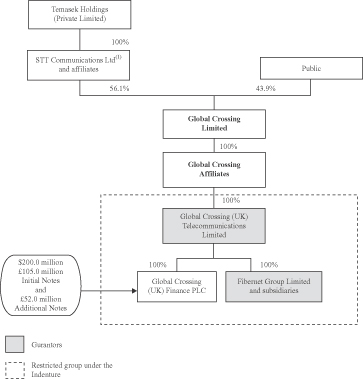

Global Crossing (UK) Telecommunications Limited

(Exact name of Registrant as specified in its charter)

Global Crossing (UK) Finance Plc

(Additional Registrant)

(Translation of Registrant’s name into English)

England and Wales

(Jurisdiction of incorporation or organization)

1 London Bridge, London, SE1 9BG, United Kingdom

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

None

| | |

Title of each class

| | Name of each exchange on which registered

|

| | | |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

(Title of Class)

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

10.75% pound sterling-denominated senior secured notes due 2014

11.75% US dollar-denominated senior secured notes due 2014

Guarantees relating to 10.75% senior secured notes due 2014 and 11.75% senior secured notes due 2014

(Title of Class)

Indicate the number of outstanding shares of each of the Issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

Ordinary shares, nominal value £1.00 per share: 101,000 shares.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in rule 405 of the Securities Act. Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer.

Large accelerated filer¨ Accelerated filer¨ Non-accelerated filerx

Indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ¨ Item 18 x

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ¨ No ¨

TABLE OF CONTENTS

1

PART I

PRESENTATION OF INFORMATION

Corporate Organization

All references in this annual report to:

| | • | | “we,” “us,” “our,” the “Company,” and “GCUK” are to Global Crossing (UK) Telecommunications Limited and its consolidated subsidiaries, including the Issuer, except where expressly stated otherwise or the context otherwise requires; |

| | • | | “Guarantors” are to GCUK and Fibernet and its direct and indirect subsidiaries; |

| | • | | “Guarantees” are to the guarantees by the Guarantors of the Notes on a senior basis; |

| | • | | “Fibernet Group” are to, collectively, Fibernet Group Limited (formerly Fibernet Group plc), a company incorporated in England and Wales, and its consolidated subsidiaries at such time; |

| | • | | “Fibernet” are to Fibernet Group excluding Fibernet Holdings Limited and Fibernet GmbH, which companies were transferred to Global Crossing International Ltd, one of our affiliates, prior to our acquisition of Fibernet Group Limited on December 28, 2006; |

| | • | | “GC Acquisitions” are to GC Acquisitions UK Limited, a wholly owned subsidiary of GCL formed for the purpose of acquiring Fibernet Group plc; |

| | • | | “GCI” are to Global Crossing International Ltd, a wholly owned subsidiary of GCL; |

| | • | | the “Issuer” and “GC Finance” are to Global Crossing (UK) Finance Plc, a company organized under the laws of England and Wales, and our direct, wholly owned finance subsidiary that is the Issuer of the Notes guaranteed by the Guarantors and which has had no trading activity, except where expressly stated otherwise or the context otherwise requires; |

| | • | | “GCL,” “Global Crossing,” “our parent” and “our parent company” are to Global Crossing Limited, a company organized under the laws of Bermuda and our indirect parent company by which we are indirectly wholly owned; |

| | • | | “old parent company” or “old parent” are to Global Crossing Ltd., a company formed under the laws of Bermuda and our parent company’s predecessor; |

| | • | | “Bidco,” “our immediate parent” and “our immediate parent company” are to Global Crossing (Bidco) Limited, a company organized under the laws of England and Wales and our direct parent company by whom we are directly wholly owned and which is indirectly wholly owned by GCL; |

| | • | | “group companies” are to the group of companies owned directly or indirectly by GCL, including us; |

| | • | | “Network Rail” are to Network Rail Infrastructure Limited, the successor to Railtrack plc, as the operator of the UK national railway infrastructure network; and |

| | • | | “Racal” are to the network services arm of Racal Telecommunications Limited, our predecessor. |

Financial and Other Information

All references in this annual report to:

| | • | | the “UK” are to the United Kingdom; |

| | • | | “pounds sterling,” “sterling,” “£” or “pence” are to the lawful currency of the United Kingdom; |

| | • | | the “United States” or the “US” are to the United States of America; |

| | • | | “US$,” “US Dollars,” “dollars” or “$” are to the lawful currency of the United States; |

| | • | | the “EU” are to the European Union; |

| | • | | “euro” or “€” are to the lawful currency of the European Union; |

| | • | | the “Initial Notes” are to the 10.75% dollar-denominated senior secured notes and the 11.75% pounds sterling-denominated senior secured notes issued by the Issuer on December 23, 2004 and to the exchange notes that the Issuer issued pursuant to a registered exchange offer in respect of such notes; |

2

| | • | | the “Additional Notes” are to the 11.75% pounds sterling-denominated senior secured notes issued by the Issuer on December 28 2006 and to the exchange notes the Issuer proposes to issue pursuant to a registered exchange offer; |

| | • | | the “Notes” and “Senior Secured Notes” are to, collectively, the Initial Notes and the Additional Notes; and |

| | • | | the “Indenture” are to the indenture, dated December 23, 2004, governing the Notes. |

The consolidated financial statements and the related notes in this annual report have been prepared in accordance with International Financial Reporting Standards,(“IFRS”), as adopted in the EU. References to “IFRS” hereafter should be construed as reference to IFRS as adopted by the EU. IFRS differs in certain material respects from accounting principles generally accepted in the US, or US GAAP. For a discussion of the differences between IFRS and US GAAP as they apply to us, see note 30 to the consolidated financial statements included elsewhere in this annual report. Unless otherwise indicated, financial information in this annual report has been prepared in accordance with IFRS.

Some financial information has been rounded and, as a result, the numerical figures shown as totals in this annual report may vary slightly from the exact arithmetic aggregation of figures that precede them.

CURRENCY PRESENTATION AND EXCHANGE RATE INFORMATION

The following table sets forth, for the periods indicated, certain information concerning the noon buying rate in the City of New York for cable transfers in pounds sterling as announced by the Federal Reserve Bank of New York for customs purposes, or the “noon buying rate,” for pounds sterling expressed in dollars per £1.00. As of April 16, 2007, the noon buying rate for pounds sterling expressed in dollars per £1.00 was 1.991.

| | | | | | | | | | | | |

| | | Dollars per £1.00 |

| | | 2002 | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 (through April 16) |

Exchange rate at end of period (Year ended December 31, except 2007) | | 1.609 | | 1.784 | | 1.916 | | 1.719 | | 1.959 | | 1.991 |

Average exchange rate during period* | | 1.508 | | 1.645 | | 1.836 | | 1.815 | | 1.858 | | 1.974 |

Highest exchange rate during period | | 1.610 | | 1.784 | | 1.948 | | 1.929 | | 1.979 | | 1.991 |

Lowest exchange rate during period | | 1.407 | | 1.550 | | 1.754 | | 1.714 | | 1.726 | | 1.924 |

| * | The average of the noon buying rates for cable transfer in pound sterling as certified for customs purposes by the Federal Reserve Bank of New York on the last business day of each month during the applicable period (through April 16 in the case of 2007). |

| | | | |

Month | | Highest exchange rate during the month | | Lowest exchange rate during the month |

October 2006 | | 1.903 | | 1.855 |

November 2006 | | 1.969 | | 1.888 |

December 2006 | | 1.979 | | 1.969 |

January 2007 | | 1.985 | | 1.931 |

February 2007 | | 1.970 | | 1.944 |

March 2007 | | 1.969 | | 1.924 |

April 2007 | | 1.991 | | 1.961 |

MARKET AND INDUSTRY DATA

In this annual report, we rely on and refer to information and statistics regarding our industry. We obtained these market data from independent industry publications or other publicly available information. Although we believe that these sources are reliable, we have not independently verified and do not guarantee the accuracy and completeness of this information.

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains certain “forward-looking statements,” as such term is defined in Section 21E of the US Securities Exchange Act of 1934. These statements set forth anticipated results based on our management’s plans and assumptions. From time to time, we also provide forward-looking statements in other materials we release to the public as well as oral forward-looking statements. Such statements give our current expectations or forecasts of future events; they do not relate strictly to historical or current facts. We have

3

tried, wherever possible, to identify these forward-looking statements by using words such as “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” “will”, “could” and similar expressions in connection with any discussion of future events or future operating or financial performance or strategies. Such forward-looking statements include, but are not limited to, statements regarding:

| | • | | our services, including the development and deployment of data products and services based on IP and other technologies and strategies to expand our targeted customer base and broaden our sales channels |

| | • | | the operation of our network, including with respect to the development of IP-based services; |

| | • | | our liquidity and financial resources, including anticipated capital expenditures, funding of capital expenditures, anticipated levels of indebtedness, and the ability to raise capital through financing activities; |

| | • | | trends related to and management’s expectations regarding results of operations, required capital expenditures, integration of acquired businesses, revenues from existing and new lines of business and sales channels, and cash flows, including but not limited to those statements set forth in Item 5 in “Operating and Financial Review and Prospects”; and |

| | • | | sales efforts, expenses, interest rates, foreign exchange rates, and the outcome of contingencies, such as legal proceedings. |

We cannot guarantee that any forward-looking statement will be realized. Our achievement of future results is subject to risks, uncertainties and potentially inaccurate assumptions. Should known or unknown risks or uncertainties materialize, or should underlying assumptions prove inaccurate, actual results could vary materially from past results and from those anticipated, estimated or projected. Investors should bear this in mind as they consider forward-looking statements.

We undertake no obligation to update forward-looking statements, whether as a result of new information, future events or otherwise. You are advised, however, to consult any further disclosures we make on related subjects in our quarterly and current reports on Form 6-K. Also note that we provide a discussion of risks and uncertainties related to our businesses. See Item 3.D. “Key Information—Risk Factors.” These are factors that we believe, individually or in the aggregate, could cause our actual results to differ materially from expected and historical results. You should understand that it is not possible to predict or identify all such factors. Consequently, you should not consider the “Risk Factors” section to be a complete discussion of all potential risks or uncertainties. As described in this annual report on Form 20-F, such risks, uncertainties and other important factors include, among others:

| | • | | our ability to successfully integrate the Fibernet business and realize the benefits we anticipate from our acquisition of Fibernet; |

| | • | | our dependence on a number of key personnel; |

| | • | | the level of competition in the marketplace; |

| | • | | technological advances and regulatory changes are eroding traditional barriers between formerly distinct telecommunications markets, which could increase the competition we face and put downward pressure on prices; |

| | • | | many of our competitors have superior resources, which could place us at a cost and price disadvantage; |

| | • | | our revenue is concentrated in a limited number of customers; |

| | • | | the absence of firm commitments to purchase minimum levels of revenue or services in some of our enterprise customer contracts; |

| | • | | our reliance on a limited number of third party suppliers; |

| | • | | periodic reviews of our financial condition by certain of our governmental customers; |

| | • | | a change of control could lead to the termination of many of our government contracts; |

| | • | | insolvency could lead to termination of certain of our contracts; |

| | • | | slower than anticipated adoption by customers of our next generation products; |

| | • | | the operation, administration, maintenance and repair of our systems are subject to risks that could lead to disruptions in our services and the failure of our systems to operate as intended for their full design lives; |

| | • | | our continued development of effective business support systems; |

4

| | • | | the influence of our parent, and actions our parent takes, or actions we are obliged to take as a result of our parent’s action, which may conflict with our interests together with potential conflicts of interest for certain of our directors due to ownership of, or options to purchase, our parent’s stock; |

| | • | | our directors may have conflicts of interest because of their ownership of, or options to purchase, our parent’s stock; |

| | • | | the sharing of corporate and operational services with our parent; |

| | • | | the return of assets to our parent if fraudulent conveyances to us by our parent occur; |

| | • | | terrorist attacks or other acts of violence or war may adversely affect the financial markets and our business and operations; and |

| | • | | our onerous lease provision is a material liability the calculation of which involves significant estimation. |

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISORS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| A. | Selected Financial Data |

You should read the following selected financial data together with the Item 5 “Operating and Financial Review and Prospects” and our financial statements and the accompanying notes thereto included elsewhere in this annual report.

The selected financial data at December 31, 2002 and 2003 and for the years then ended were derived from our financial statements which are not included in this annual report. The selected financial data at December 31, 2004, 2005 and 2006 and for each of the years then ended have been derived from our consolidated financial statements and related notes thereto included elsewhere in this annual report.

Unless otherwise indicated, the historical financial data have been prepared in accordance with IFRS. IFRS differs in certain significant respects from US GAAP. For a discussion of the differences between IFRS and US GAAP as they apply to us, see note 30 to our consolidated financial statements included elsewhere in this annual report.

As permitted by Instruction G of Form 20-F, we have presented selected financial data in accordance with IFRS for the years ended December 31, 2004, 2005 and 2006 and in accordance with US GAAP for the years ended December 31, 2002, 2003, 2004, 2005 and 2006.

In reading the selected historical financial data, please note the following:

| | • | | On December 28, 2006, we announced that our subsidiary, GC Finance, had completed its offering of the Additional Notes. The £52.0 million aggregate principal amount of the Additional Notes was priced at 109.25 percent of par value and the issue raised £56.8 million in gross proceeds. The Additional Notes were issued under the Indenture pursuant to which GC Finance issued the Initial Notes. |

| | • | | On December 28, 2006, proceeds from the offering were used to acquire Fibernet from GC Acquisitions, and to pay fees and expenses incurred in connection with the acquisition of Fibernet by GCUK and the offering of the Additional Notes. Upon completion of the acquisition by GCUK, Fibernet guaranteed the Additional Notes and all other obligations under the Indenture. Prior to the acquisition by GCUK, Fibernet Group transferred its German business operations to GCI, by way of a transfer of Fibernet Holdings Limited, and its wholly owned subsidiary Fibernet GmbH, to GCI, for consideration of £1 and the assumption, by GCI, of £3.6 million of debt outstanding to Fibernet. See note 4 to our consolidated financial statements included elsewhere in this annual report. |

| | • | | Fibernet results from December 28, 2006, only are included within the following income statement data. |

| | • | | Fibernets position as of December 31, 2006, only is included within the following balance sheet data. |

5

| | | | | | | | | | | | | | | | | | | | |

| | | Year ended December 31, | |

| | | 2002 | | | 2003 | | | 2004 | | | 2005 | | | 2006 | |

| | | (in thousands, except ratios) | |

IFRS Data | | | | | | | | | | | | | | | | | | | | |

Income Statement Data: | | | | | | | | | | | | | | | | | | | | |

Revenue | | | (1 | ) | | | (1 | ) | | £ | 271,096 | | | £ | 239,498 | | | £ | 240,612 | |

Cost of sales | | | (1 | ) | | | (1 | ) | | | (156,735 | ) | | | (136,317 | ) | | | (147,481 | ) |

| | | | | | | | | | | | | | | | | | | | |

Gross profit | | | (1 | ) | | | (1 | ) | | | 114,361 | | | | 103,181 | | | | 93,131 | |

| | | | | | | | | | | | | | | | | | | | |

Operating expenses: | | | | | | | | | | | | | | | | | | | | |

Distribution costs | | | (1 | ) | | | (1 | ) | | | (10,504 | ) | | | (10,009 | ) | | | (10,385 | ) |

Administrative expenses | | | (1 | ) | | | (1 | ) | | | (40,258 | ) | | | (47,738 | ) | | | (53,683 | ) |

Net gain arising from acquisition of Fibernet | | | (1 | ) | | | (1 | ) | | | — | | | | — | | | | 8,453 | |

| | | | | | | | | | | | | | | | | | | | |

| | | (1 | ) | | | (1 | ) | | | (50,762 | ) | | | (57,747 | ) | | | (55,615 | ) |

| | | | | | | | | | | | | | | | | | | | |

Operating profit | | | | | | | | | | | 63,599 | | | | 45,434 | | | | 37,516 | |

Finance costs, net | | | | | | | (1 | ) | | | (613 | ) | | | (39,919 | ) | | | (14,688 | ) |

Tax benefit/(charge) | | | (1 | ) | | | (1 | ) | | | 11,364 | | | | 2,477 | | | | (9,377 | ) |

| | | | | | | | | | | | | | | | | | | | |

Profit | | | (1 | ) | | | (1 | ) | | £ | 74,350 | | | £ | 7,992 | | | £ | 13,451 | |

| | | | | | | | | | | | | | | | | | | | |

Balance Sheet Data (at period end): | | | | | | | | | | | | | | | | | | | | |

Cash and cash equivalents | | | (1 | ) | | | (1 | ) | | £ | 21,193 | | | £ | 44,847 | | | £ | 40,309 | |

Trade and other receivables(2) | | | (1 | ) | | | (1 | ) | | | 64,633 | | | | 59,954 | | | | 59,182 | |

Working capital/(deficit)(3) | | | (1 | ) | | | (1 | ) | | | 6,897 | | | | (8,532 | ) | | | (18,798 | ) |

Intangible assets, net | | | (1 | ) | | | (1 | ) | | | 1,634 | | | | 1,296 | | | | 14,241 | |

Property, plant and equipment, net | | | (1 | ) | | | (1 | ) | | | 135,593 | | | | 129,005 | | | | 182,556 | |

Total assets | | | (1 | ) | | | (1 | ) | | | 241,092 | | | | 255,382 | | | | 336,877 | |

Total debt(4) | | | (1 | ) | | | (1 | ) | | | 234,950 | | | | 239,436 | | | | 282,054 | |

Total shareholders’ deficit | | | (1 | ) | | | (1 | ) | | | (219,105 | ) | | | (204,718 | ) | | | (195,574 | ) |

Other Data: | | | | | | | | | | | | | | | | | | | | |

Depreciation and amortization | | | (1 | ) | | | (1 | ) | | £ | 21,193 | | | £ | 20,104 | | | £ | 24,551 | |

Capital expenditures | | | (1 | ) | | | (1 | ) | | | 7,811 | | | | 9,452 | | | | 20,435 | |

| |

| | | Year ended December 31, | |

| | | 2002 | | | 2003 | | | 2004 | | | 2005 | | | 2006 | |

| | | (in thousands, except ratios) | |

US GAAP Data(5) | | | | | | | | | | | | | | | | | | | | |

Income Statement Data(6): | | | | | | | | | | | | | | | | | | | | |

Revenue | | £ | 265,663 | | | £ | 290,922 | | | £ | 263,776 | | | £ | 233,888 | | | £ | 234,964 | |

Operating (loss)/profit | | | (43,512 | ) | | | 23,633 | | | | 54,326 | | | | 39,048 | | | | 22,781 | |

(Loss)/income from continuing activities(7) | | | (17,271 | ) | | | 330,062 | | | | 40,546 | | | | (2,246 | ) | | | 5,805 | |

Net (loss)/income | | | (18,607 | ) | | | 330,062 | | | | 40,546 | | | | (2,246 | ) | | | 5,805 | |

Balance Sheet Data (at period end): | | | | | | | | | | | | | | | | | | | | |

Cash and cash equivalents | | £ | 41,565 | | | £ | 50,403 | | | £ | 21,193 | | | £ | 44,847 | | | £ | 40,309 | |

Fixed assets | | | 202,602 | | | | 112,404 | | | | 132,104 | | | | 125,543 | | | | 190,119 | |

Total assets | | | 385,134 | | | | 293,823 | | | | 244,241 | | | | 256,981 | | | | 340,184 | |

Total debt | | | 512,719 | | | | 371,867 | | | | 245,415 | | | | 248,626 | | | | 293,714 | |

Total shareholders’ deficit | | | (477,790 | ) | | | (307,289 | ) | | | (146,972 | ) | | | (134,303 | ) | | | (135,871 | ) |

Other Data: | | | | | | | | | | | | | | | | | | | | |

Depreciation and amortization | | £ | 46,336 | | | £ | 43,613 | | | £ | 22,186 | | | £ | 19,739 | | | £ | 24,226 | |

(1) | IFRS information is not required to be presented for these periods. |

(2) | Trade and other receivables include operating and non-operating receivables from other group companies. Excluding the receivables from other group companies, trade and other receivables are £55.4 million and £53.3 million at December 31, 2005 and 2006, respectively. |

(3) | Working capital/(deficit) consists of the current portion of trade and other receivables, less trade and other payables. Working capital/ (deficit) includes operating and non-operating receivables and payables from other group companies. Excluding all receivables and payables from other group companies, working capital deficit is £6.4 million and £18.0 million at December 31, 2005 and 2006, respectively. |

(4) | Total debt represents obligations under finance leases and hire purchase contracts, third-party indebtedness and loans owed to group companies. |

(5) | Upon its emergence from bankruptcy on December 9, 2003, our parent company implemented “fresh start” accounting and reporting in accordance with the AICPA SOP 90-7. Fresh start accounting required our parent company to allocate the reorganization value of its assets and liabilities based upon their estimated fair values. Although GCUK itself was not part of the bankruptcy proceedings, under US GAAP, fresh start accounting is pushed down to the entity level. |

6

(6) | Our results for the year ended December 31, 2002 include our cellular business, which was discontinued in 2001. This includes a net operating loss of £1.3 million for the year ended December 31, 2002. |

(7) | (Loss)/income from continuing activities represents profit adjusted to exclude discontinued operations. |

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

Our business, and an investment in us, are subject to a number of significant risks, including those described below. Additional risks and uncertainties not presently known to us, or that we currently believe are immaterial, could also impair our business, financial condition, results of operations and our ability to fulfill our obligations under the Notes. See Item 5.B. “Operating and Financial Review and Prospects—Liquidity and Capital Resources—Indebtedness—Senior Secured Notes.”

In addition to the risk factors identified under the captions below, the operation and results of our business are subject to risks and uncertainties identified elsewhere in this annual report on Form 20-F as well as general risks and uncertainties such as those relating to general economic conditions and demand for telecommunications services.

Risks Related to Our Business and Industry

We may not be successful in integrating the Fibernet business into ours or may not be able to realize the benefits we anticipate from the Fibernet acquisition.

We are in the early stages of the process of integrating Fibernet with our business. The process of coordinating and integrating the two organizations, and making them operate as one company, has and will require managerial and financial resources. In addition, this process could cause the interruption to, or a loss of momentum in, the activities of any of our or Fibernet’s businesses, including its customer services, which could have a material adverse effect on our consolidated operations.

The management of the integration of the businesses, systems and culture of ourselves and Fibernet will require, among other things, the continued development of our financial and management controls, including the integration of information systems and structure, the integration of product offerings and customer base and the training of new personnel, all of which could disrupt the timeliness of financial information, place a strain on our management resources and require significant expenditure. Any significant diversion of management’s attention or any major difficulties encountered in the integration of the businesses could have a material adverse effect on our business, financial condition and results of operation. While we have budgeted anticipated integration costs, there can be no assurance that additional costs will not be incurred.

While we have identified certain potential revenue synergies and cost savings which we believe may be achievable as a result of the acquisition of Fibernet, and we believe the underlying assumptions upon which we have based our estimates are reasonable, the timing of and degree to which we are able to realize such synergies and savings, which remains subject to numerous significant risks and uncertainties, could nonetheless vary significantly. There can be no assurance that such potential revenue synergies, the cost saving plans, or other anticipated benefits will be realized in the near future, if at all.

We depend in large part on the efforts of our key personnel. Maintaining key personnel is vital for our business, and there is no guarantee we can keep such personnel.

Our business is managed by a number of key personnel, including our directors, the loss of any of whom could have a material adverse effect on our business. In addition to our senior management, we rely upon key personnel of GCL, our parent company. In addition, many of our key personnel spend time working for our parent or its affiliates and the amount of time they spend doing so is often out of our control. Our business and

7

operations depend upon qualified personnel successfully implementing our business plan, including the integration of Fibernet. We can offer no assurances that we will be able to attract and retain skilled and qualified personnel for senior management positions. The loss of key personnel employed by our parent or their need to spend additional time working for our parent or its affiliates or our failure to recruit and retain key personnel or qualified employees could have a material and adverse effect on our business, operations and financial condition.

We face significant competition in the marketplace.

In the enterprise data and voice markets, we compete chiefly with various divisions of BT, Cable & Wireless and Verizon (previously MCI). In the carrier data and voice markets, we compete primarily with BT, Cable & Wireless and Verizon which, on a combined basis, have a majority of the market share for these services. Concerning the government and rail sectors in particular, our principal competitors are Cable & Wireless and BT. Other competitors include COLT, Virgin Media (formerly NTL), Afiniti (previously Kingston), Vanco and Thus. Depending on the type of customer, we will compete on the basis of level of service, quality of technology and price. Our network reach, which includes not only the ability to connect with customers but also the ability to decrease the distance between enterprise entities and their point of interconnection with our network, is also a significant factor that determines our ability to compete for customers in the enterprise sector. The level of competition we face could lead to a reduction in our revenues and margins as well as other material adverse effects on our business, operations and financial condition.

Technological advances and regulatory changes are eroding traditional barriers between formerly distinct telecommunications markets, which could increase the competition we face and put downward pressure on prices.

The communications industry is subject to rapid and significant changes in technology. The introduction of new products or technologies, as well as the further development of existing products and technologies by our competitors, are blurring the distinctions between traditional and emerging telecommunications markets. This may reduce the cost or increase the supply of some services that are similar to the products we provide. Our most significant competitors in the future may be new entrants to the communications and information services industry. These new entrants may not be burdened by an installed base of existing equipment that may be required to be updated or replaced. Our future success depends, in part, on our ability to anticipate and adapt to technological changes in a timely manner. Technological changes, the resulting competition from existing competitors or new entrants and the capital expenditure required to adapt to these changes could have a material adverse effect on our business, operations and financial condition.

The Office of Communications (“Ofcom”) the UK regulatory authority, is encouraging new operators to build their own infrastructures to compete with BT. At the same time, BT is constructing a new, IP based network which it refers to as a 21st Century network. At present, it is not clear how operators will connect with this network. There are currently no proposals as to how and at what level BT will charge for access to the network. Regulation has historically provided for the expansion of competition in the marketplace and the subsequent lowering of tariffs charged across the industry. However, there is no way to know what regulatory actions Ofcom and other governmental and regulatory agencies may take in the future. Individually and collectively, these matters could have negative effects on our business, which could materially and adversely affect our business, operations and financial condition.

Many of our competitors have superior resources, which could place us at a cost and price disadvantage.

Many of our existing and potential competitors have significant competitive advantages, including greater market presence, name recognition and financial, technological and personnel resources, superior engineering and marketing capabilities, more ubiquitous network reach, and significantly larger installed customer bases. As a result, many of our competitors can raise capital at a lower cost than we can, and they may be able to adapt more swiftly to new or emerging technologies and changes in customer requirements, take advantage of acquisition and other opportunities (including regulatory changes) more readily, and devote greater resources to the development, marketing and sale of products and services than we can. Also, our competitors’ greater brand name recognition may require us to price our services at lower levels in order to win business. Our competitors’ financial advantages may give them the ability to reduce their prices for an extended period of time if they so choose. Many of these advantages are expected to increase with the recent trend toward consolidation by large industry participants. Any of these events, or a combination thereof, could materially and adversely affect our business, operations and financial condition.

8

Our revenue is concentrated in a limited number of customers.

A significant portion of our revenue comes from a limited number of customers. For example, 64.9% of our revenue for the year ended December 31, 2006 came from our ten top customers. The public sector generated 37.1% of our revenue and OGCbuying .solutions (Managed Telecom Services) generated 14.7% of our revenue for the year ended December 31, 2006.

If we lose one or more of our major customers, including failing to keep Fibernet’s existing major customers, or if one or more of our major customers significantly decreases use of our services, it may materially and adversely affect our business, operations and financial condition. Our future operating results will depend on the success of these customers and our other large customers, and our success in selling services to them. If we were to lose a significant portion of the revenue from any of our top customers, we would not be able to replace that revenue in the short term.

Our enterprise customer contracts do not provide for committed minimum levels of revenue or services purchased.

With few exceptions, our enterprise contracts do not provide for committed minimum revenues or service usage thresholds. Moreover, many of them contain benchmarking or similar provisions permitting or requiring the periodic renegotiation or adjustment of prices for our services based upon, among other things, changes in market prices within the industry. Accordingly, we cannot assure you that, even with respect to enterprise customer contracts of significant duration, we will be able to maintain per-unit pricing or overall revenue streams at current levels. If unit pricing declines and we are unable to sell additional services to such customers or services to new customers, or commensurately reduce costs, there could be a material adverse effect on our business, operations and financial condition.

We rely on a limited number of third parties for the timely supply of equipment and services and, if we experience problems with delivery from them, our business and operations could suffer.

We depend on a limited number of suppliers and vendors for equipment and services relating to our network infrastructure. If these suppliers or vendors:

| | • | | experience financial or technical problems; |

| | • | | develop favorable relationships with our competitors; |

| | • | | experience interruptions or other problems in their own businesses; or |

| | • | | cannot or do not deliver these network components or services on a timely basis, |

our ability to obtain sufficient quantities of the products and services we require to operate our business successfully may be diminished, and our business and operating results could suffer significantly. In certain instances, we may rely on a single supplier that has proprietary technology that has become core to our infrastructure and business. As a result, we have come to rely upon a limited number of network equipment manufacturers and other suppliers, including BT, ECS United Kingdom, Ericsson and Siemens. If we needed to seek alternative suppliers, we may be unable to obtain satisfactory replacement suppliers on economically attractive terms, on a timely basis or at all, which could materially and adversely effect our business, operations and financial condition.

Certain of our governmental enterprise customers periodically review our financial condition.

We continue to provide to and review with the UK Foreign & Commonwealth Office (“FCO”) and OGCbuying.solutions periodic financial information about us and about our parent company. We regard these reviews as part of our ongoing cooperative relationship with some of our most important government customers. However, should the FCO or OGCbuying.solutions or other customers become concerned about our financial stability and therefore our ability to honor our contractual commitments, there may be a material and adverse effect on our business. While customers may not necessarily be able to terminate our contracts with them, they could simply choose not to use services and move to another telecommunications provider and may continue to have such plans. Although we believe there are costs associated with established long-term customers moving services from us to another provider, the FCO and OGCbuying.solutions had established contingency plans to transfer telecommunications services from us to another provider or take the management of the service in-house at the time of our parent company’s reorganization. They could rely upon such contingency plans to assist them in the orderly transition of services. The reduction in, or cessation of, the use of our services by any of our major customers would have a material adverse effect on our business, operations and financial condition.

9

Many of our most important government customers have the right to either terminate their contracts with us if a change of control occurs or to reduce the services they purchase from us.

Many of our government contracts contain broad change of control provisions that permit the customer to terminate the contract in the event that we undergo a change of control. A termination in many instances gives rise to other rights of the government customer, including, in some cases, the right to purchase certain of our assets used in servicing those contracts. Certain change of control provisions may be triggered when any lender (other than a bank lender in the normal course of business) or one or a group of holders of the Notes would have the right to control us or the majority of our assets upon any event, including upon bankruptcy. If the holders of the Notes have the right to control us or the majority of our assets upon such event, it could be deemed to be a change of control of us. In addition, if STT’s ownership interest in GCL falls below certain levels, it could be deemed to be an indirect change of control of us. See Item 7.B. “Major Shareholders and Related Party Transactions—Related Party Transactions—The Security Arrangement Agreement.” This could include a situation in which (assuming the sale or transfer of its equity interests or dilution thereof) STT sells or transfers all or a portion of the $250.0 million aggregate principal amount of mandatory convertible notes, due December 2008, issued by GCL concurrently with the completion of the offering of the Initial Notes. In addition, most of our government contracts do not include minimum usage guarantees. Thus the applicable customers could simply choose not to use our services and move to another telecommunications provider. If any of our significant government contracts are terminated as a result of a change of control or otherwise, or if the applicable customers were to significantly reduce the services they purchase under these contracts, we could experience a material and adverse effect on our business, operations and financial condition.

Insolvency could lead to termination of certain of our contracts.

The lease to us by Network Rail (which owns the United Kingdom’s railway infrastructure) of fiber optic cable and ancillary equipment and our capacity purchase agreement with them which enables our use of the copper cable and private automatic branch exchanges equipment (“PABXs”) which we use to deliver managed voice services to the train operating companies, comprise a key set of contractual documents in our relationship with Network Rail. The deed of grant is a related agreement that gives us wayleave rights until at least 2046 that permit us to maintain existing leased and owned fiber and network equipment and to lay new fiber and install new equipment, subject to specified payments to Network Rail. If we become insolvent, Network Rail becomes entitled, but not obligated, with certain exceptions, to terminate the lease, the capacity purchase agreement and the related deed of grant described above. Certain of our other enterprise contracts, including many of our government contracts, contain clauses entitling the counterparty to terminate should we become insolvent. Some of these contracts contain similar termination provisions that would apply if a direct or indirect parent company of us, including GCL, becomes insolvent. The loss of rights under the lease with Network Rail, the deed of grant, the capacity purchase agreement or any of the significant enterprise contracts containing similar termination provisions could have a material and adverse effect on our business, operations and financial conditions.

Slower than anticipated adoption by customers of our next generation IP-based products

While we are seeing an increasing rate of growth in demand for our next generation IP-based products, this demand has not to date occurred at a level that has allowed us to take full advantage of the investments we have made in this technology. Although we believe demand will continue to grow, it may take us longer than we originally anticipated to recover our initial investment. This could have a material and adverse effect on our business, operations and financial condition.

The operation, administration, maintenance and repair of our systems are subject to risks that could lead to disruptions in our services and the failure of our systems to operate as intended for their full design lives.

Our telecommunications systems, and those of our parent, are subject to the risks inherent in large-scale, complex fiber optic telecommunications systems. The operation, administration, maintenance and repair of these systems require the coordination and integration of sophisticated and highly specialized hardware and software technologies and equipment located throughout the world. These systems may not continue to function as expected in a cost-effective manner. The failure of the hardware or software to function as required could render a cable system unable to perform at design specifications.

Each of our terrestrial systems has a design life of at least 20 years, while each of our parent’s subsea systems generally have a design life of 25 years. The economic lives of these systems, however, may be shorter than their design lives, and we cannot provide any assurances as to the actual useful life of any of these systems.

10

A number of factors will ultimately affect the useful life of each of our systems, including, among other things, quality of construction, unexpected damage or deterioration and technological or economic obsolescence.

Interruptions in service or performance problems, for whatever reason, could undermine confidence in our services and cause us to lose customers or make it more difficult to attract new ones. In addition, because many of our services are critical to our customers’ businesses, a significant interruption in service could result in lost profits or other loss to customers. Although we attempt to disclaim liability for these losses in our service agreements, we are not always able to do so and, even where we are able to include such provisions, a court might not enforce a limitation on liability under certain conditions, which could expose us to financial loss. In addition, we often provide customers with guaranteed service level commitments. If we are unable to meet these guaranteed service level commitments for whatever reason, we may be obligated to provide our customers with credits, generally in the form of free service for a short period of time, with a resultant reduction in revenue, which could negatively affect our operating results.

Our business requires the continued development of effective business support systems to implement customer orders and to provide and bill for services and manage access costs.

Our business depends on our ability to continue to develop effective business support systems. This is a complicated undertaking requiring significant resources and expertise and support from third-party vendors. We need business support systems for:

| | • | | implementing customer orders for services; |

| | • | | provisioning, installing and delivering these services; |

| | • | | timely billing for these services; and |

| | • | | ensuring that we manage access costs efficiently. |

We need these business support systems to expand and adapt to our continued growth. We have generally been successful in moving customers to new services, and we therefore face a continuing challenge as business support systems become outdated and expensive to maintain, and the support available to them becomes limited. We have utilized and will continue to utilize the business support systems developed or maintained by our parent and its affiliates. Our parent and its affiliates are developing and upgrading the business support systems globally. We are closely involved in this effort and will benefit from certain of the enhancements in the global business support systems in our business in the UK. We can not assure you, however, that the development and upgrade of the global business support systems will be successful, will be timely completed, or will satisfy the specific needs of our business. This could have a material and adverse effect on our business, operations and financial condition.

Our parent company can influence us because it indirectly owns all of our common stock

Our parent company indirectly owns 100% of our share capital. Because our parent’s interests may differ from ours, actions our parent takes as a stockholder with respect to us may not be favorable to us or to holders of our Notes. Although we put into place upon the closing of the offering of the Initial Notes operational agreements to address the relationship between us and our parent, we remain somewhat dependent on our parent’s decisions regarding corporate strategies, its financial performance and other factors which may affect our parent as our sole stockholder. Also, the interests of our parent’s controlling stockholder, STT, may differ from ours. STT might impose certain strategic and other decisions on us through their control of our parent. We can offer no assurance that the interests of our parent or STT will not conflict with the interests of the holders of our Notes regarding these matters.

In addition to our operational agreements, our parent company can influence what we do with available cash flow. For example, during 2003 and 2004, we periodically upstreamed a portion of our cash on hand and operating cash flow to our parent company and its affiliates to repay loans. Although we did not upstream any cash in 2005, in 2006 we upstreamed $80.8 million via intercompany loans, $30.4 million of which were repaid in 2006. It is possible that our parent company may use us as a source of funding, subject to the terms of the Indenture and applicable restrictions under English law, and that we will continue to upstream available cash to fund our parent’s and its subsidiaries’ operations. The terms of the Indenture permit certain upstream payments including, subject to certain restrictions, upstreaming at least 50% of our designated cash flow, as defined in the Indenture.

11

Certain of our directors and officers may have conflicts of interest because of their ownership of, or options to purchase or other rights to receive, our parent’s stock

Some of our directors and officers own or have options to purchase or other rights to receive, our parent’s common stock and participate in our parent company’s incentive compensation programs. This could create, or appear to create, potential conflicts of interest when our directors and officers are faced with decisions that could have different implications for our parent than they do for us. Such directors and officers may not be liable to us or our stockholders for a breach of any fiduciary duty as one of our directors and officers by reason of the fact that our parent or any of its affiliates pursues or acquires a corporate opportunity for itself, directs a corporate opportunity to another person or such director or officer does not communicate information regarding such corporate opportunity to us, each of which could eventuality could have a material and adverse effect on our business, operations and financial condition.

Our business may be disrupted due to the sharing of corporate and operational services with our parent, and these and other arrangements with our parent may not be sustained on the same terms.

We are a wholly-owned, indirect subsidiary of our parent and have received, and will receive in the future, corporate and operational services from our parent and its affiliates. In connection with the offering of the Initial Notes, we entered into a series of agreements formalizing the agreements under which we receive these services. See Item 7.B. “Major Shareholders and Related Party Transactions—Related Party Transactions—Inter-company Agreements.” We rely, and will continue to rely, on our parent and its affiliates to maintain the integrity of these services. Under certain circumstances, the pricing formulas may change for these services and, in other instances, our parent may cease to provide these services, including by terminating the agreements on one year’s prior notice. In the event our parent discontinues providing these services, there can be no assurance that we could obtain them on the same terms. Moreover, deterioration in the financial situation of our parent may adversely affect our ability to operate due to our reliance on our parent and its affiliates in some of these areas. This could have a material and adverse affect on our business, operations and financial condition.

If any transfers of assets to us by our parent or its other subsidiaries are deemed to be fraudulent conveyances, we may be required to return such assets to our parent or its other subsidiaries.

If any transfers of assets to us by our parent or its other subsidiaries are found to be fraudulent conveyances, we may be required to return such assets to our parent or its other subsidiaries or may be held liable to our parent or its other subsidiaries or their creditors for damages alleged to have resulted from the conveyances. A court could hold a transfer to be a fraudulent conveyance if our parent or its other subsidiaries received less than reasonably equivalent value and our parent or its other subsidiaries were insolvent at the time of the transfer, were rendered insolvent by the transfer or were left with unreasonably small capital to engage in its business. A transfer may also be held to be a fraudulent conveyance if it was made to hinder, delay or defraud creditors. US courts have held that liabilities that are unknown, or that are known to exist but whose magnitude is not fully appreciated at the time of the transfer, may be taken into account in the context of a future determination of insolvency. This could make it very difficult to know whether a transferor is solvent at the time of transfer and would increase the risk that a transfer may be found to be a fraudulent conveyance in the future.

Terrorist attacks or other acts of violence or war may adversely affect the financial markets and our business.

Significant terrorist attacks against the UK, the United States or other countries in which we or group companies operate are possible. It is possible that our physical facilities or network control systems could be the target of such attacks, or that such attacks could impact other telecommunications companies or infrastructure or the internet in a manner that disrupts our operations. Terrorist attacks (or threats of attack) could also lead to volatility or illiquidity in world financial markets and could cause consumer confidence and spending to decrease or otherwise adversely affect the economy. These events could adversely affect our business and our ability to obtain financing on favorable terms. In addition, it is becoming increasingly difficult to obtain adequate insurance for losses incurred as a result of terrorist attacks at reasonable rates; in some cases, such insurance may not be available. Uninsured losses as a result of terrorist attacks could have a material adverse effect on our business, results of operations and financial condition.

Our onerous lease provision represents a material liability the calculation of which involves significant estimation.

We have engaged in restructuring activities, which require us to make significant judgments and estimates in determining restructuring charges, including, but not limited to, sublease income or disposal costs, length of

12

time on market for abandoned rented facilities, and contractual termination costs. Such estimates are inherently judgmental and changes in such estimates, especially as they relate to contractual lease commitments and related anticipated third-party sublease payments, could have a material effect on the onerous lease liabilities and consolidated income statement. We continue to review our anticipated costs and third party sublease payments on a quarterly basis and record adjustments for changes in these estimates in the period such changes become known.

The calculation of our onerous lease provision involves the estimation of receipts from subleases to third parties, including projections of material receipts from subleases to be entered into in the future. Although we believe these estimates to be reasonable, actual sublease receipts could turn out to be materially different than we have estimated.

Risk Related to the Notes and the Structure

Our ability to generate cash depends on many factors beyond our control.

The ability to make payments on our indebtedness, including the Notes, and to fund planned operating and capital expenditures will depend on our ability to generate cash in the future. This, to a certain extent, is subject to general economic, financial, competitive, legislative, regulatory and other factors, including other factors discussed above under “—Risks Related to Our Business and Industry”, that are beyond our control. Similarly, many telecommunications companies, including our old parent company, have defaulted on debt securities and bank loans in recent years and had their equity positions eliminated in bankruptcy reorganizations. This history has led to limited access to the capital markets by companies in our industry. Our access to the capital markets may also be limited in the future if our parent were to become financially distressed.

If our future cash flow from operations and other capital expenditures are insufficient to pay our debt obligations or to fund other liquidity needs, we may be forced to sell assets or attempt to restructure or refinance our existing indebtedness. We may also be required to raise additional debt or equity financing in amounts that could be substantial. We cannot assure our holders of the Notes that our business will generate sufficient cash flow from operations or that future borrowings will be available to us in an amount sufficient to enable us to pay our indebtedness, including principal, interest and other amounts due in respect of the Notes. Nor can we assure holders of our Notes that we will generate sufficient cash flow to fund our other liquidity needs. We may need to refinance all or a portion of its debt, including the Notes, on or before maturity. We cannot assure holders of the Notes that we will be able to refinance any of our debt, including the Notes, on commercially reasonable terms if at all.

The holders of the Notes should not rely upon funds from our parent company or its affiliates to service obligations under the Notes.

We have historically served, and in the future may serve, as a source of funding for our parent company and its affiliates. Prior to 2003, we incurred substantial amounts of intercompany indebtedness owed to our parent company and its affiliates. Since the second quarter of 2003, we have periodically made repayments on this indebtedness from our positive cash flow. Moreover, we upstreamed substantially all of the net proceeds of the offering of the Initial Notes on December 20, 2004, through repayment of debt or otherwise, to our parent company and its subsidiaries with the result that as at December 31, 2004 we had a zero intercompany debt balance. The intercompany debt balance remained zero as of December 31, 2005. As of December 31, 2006, there were loans due from affiliates of our parent in the amount of $50.4 million. See “Note 27. Related Parties” to the consolidated financial statements included in this annual report on Form 20-F.

We expect that our parent company may continue to use us as a source of funding, subject to the terms of the Indenture and applicable English law, and that we may, accordingly, continue to upstream available cash to fund our parent’s operations. This may happen in the form of loans or dividends or other distributions. However, it will not be possible for us to pay dividends to our shareholder, an indirect subsidiary of our parent, until such time as our accumulated realized profits exceed our accumulated realized losses. It is anticipated, therefore, that we will not be in a position to pay dividends for some time, and any funds to be upstreamed to our parent would be made by us by way of an intercompany loan. To the extent that these amounts take the form of loans, we are subject to the risk that our parent company and its affiliates will be unable to repay these amounts. The ability of our parent to repay these amounts is predicated upon, among other things, its financial condition and solvency. In addition, under the terms of the indenture governing our parent’s mandatory convertible notes, loans that we make to our parent or its subsidiaries are required to be subordinated to the payment of their obligations to the

13

holders of the mandatory convertible notes in the event of a default. Such subordination would restrict our ability to recover amounts under such intercompany loans during periods in which our parent would be experiencing financial difficulties. To the extent that these amounts take the form of dividends or other corporate distributions, there will be no obligation at all on the part of our parent company or its affiliates to repay these amounts. Although the terms of the Indenture restrict our ability to upstream amounts to our parent company and its affiliates in the future, these restrictions are subject to a number of important qualifications and exceptions that are described in the Indenture. The terms of the Indenture permit certain upstream payments including, subject to certain restrictions, upstreaming at least 50% of our designated cash flow, as defined in the Indenture.

Accordingly, we cannot assure holders of our Notes that we will have any access to funds from our parent company or its affiliates and the holders of the Notes, therefore, should not rely upon funds from them to service obligations under the Notes.

The restrictive covenants in the Indenture or future debt instruments may limit our operating flexibility. Our failure to comply with these covenants could result in defaults under the Indenture and any future debt instruments even though we may be able to meet our debt service obligations.

The Indenture imposes significant operating and financial restrictions on us. These restrictions significantly limit, among other things, our ability to:

| | • | | incur or guarantee additional indebtedness and issue certain preferred stock; |

| | • | | engage in layering of debt; |

| | • | | make certain payments, including dividends or other distributions, with respect to our shares or our restricted subsidiaries’ shares (save for dividends or other distributions by a restricted subsidiary to us or another restricted subsidiary); |

| | • | | prepay or redeem subordinated debt or equity; |

| | • | | make certain investments; |

| | • | | create encumbrances or restrictions on the payment of dividends or other distributions, loans or advances to us by our restricted subsidiaries or on the transfer of assets to us by any of our restricted subsidiaries; |

| | • | | sell, lease or transfer certain assets, including stock of restricted subsidiaries; |

| | • | | engage in certain transactions with affiliates; |

| | • | | enter into unrelated businesses; and |

| | • | | consolidate or merge with other entities. |

All these limitations are subject to significant exceptions and qualifications. See “Operating and Financial Review and Prospects—Liquidity and Capital Resources—Indebtedness”. These covenants could limit our ability to finance our future operations and capital needs and our ability to pursue business opportunities and activities that may in our interest.

Any future debt instruments may also contain similar or more restrictive provisions that may affect our ability to engage in certain transactions in the future. Although the indenture governing the mandatory convertible notes of our parent does not restrict us from engaging in transactions that are not restricted by the Indenture governing the Notes, the indenture for the mandatory convertible notes may be amended without the consent of the holders of our Notes. It is possible that amendments to the indenture governing the mandatory convertible notes could restrict our operating flexibility or conflict with the provisions or covenants in the Indenture governing the Notes, which in each case could be in ways that are adverse to the holders of the Notes.

The restrictions in the Indenture governing the Notes and such other restrictions could limit our ability to obtain future financing, incur capital expenditures, withstand a future downturn in our business or the economy in general or otherwise take advantage of business opportunities that may arise. If we fail to comply with these restrictions, the holders of our Notes, or lenders under any future debt instrument, could declare a default under the terms of the relevant debt, even though we are able to meet debt service obligations and this could cause certain of our debt to become immediately due and payable. If our parent company or the guarantors of the mandatory convertible notes fail to comply with the terms of those notes, then the holders of those notes could declare a default. A declaration of default under the mandatory convertible notes would have a material adverse effect on our parent, and consequently, would be likely to have a material adverse effect on us.

14

If a creditor accelerated any debt, we cannot assure holders of our Notes that we would have sufficient funds available, or that we would have access to sufficient capital from other sources, to repay the debt. Even if we could obtain additional financing, we cannot assure holders of our Notes that the terms would be favorable to us. If we default on any secured debt, the secured creditors could foreclose on their liens. As a result, any event of default could have a material adverse effect on our business and financial condition and could prevent us from paying amounts due under the Notes.

Holders of the mandatory convertible notes have certain rights relating to and affecting the Notes.

A security arrangement agreement governs certain rights and obligations between holders of the mandatory convertible notes and the holders of the Notes. See Item 7.B. “Major Shareholders and Related Party Transactions—Related Party Transactions—The Security Arrangement Agreement.” An affiliate of STT is the current holder of all of the mandatory convertible notes. In particular, this agreement provides that the security documents for the Notes are subject to a restriction on the exercise of remedies. Specifically, no holder of the Notes or anyone acting on a holder of the Notes behalf can dispose of the Issuer’s or our assets pursuant to an enforcement action unless:

| | • | | all of our assets or all of the Issuer’s assets, as the case may be, are sold; |

| | • | | the sale is for cash consideration payable at the closing of the transaction; |

| | • | | all claims of all holders of the Notes are unconditionally released and discharged concurrently with that sale and all liens for the benefit of the holders are unconditionally released and discharged; and |

| | • | | the sale is made pursuant to a public auction or for fair market value (taking into account the circumstances giving rise to such sale) as certified by an independent, internationally recognized investment bank selected by the holders of the mandatory convertible notes. |

These provisions may significantly limit the ability of a holder of our Notes to realize value from a sale of the collateral.

The Indenture governing the Notes provides that if there is a payment default on or an acceleration of the Notes, or in the case of certain enforcement events, then on giving not less than 10 business days’ notice, STT (or one of its affiliates) for so long as it, together with its affiliates, holds not less than 50% of the then outstanding aggregate amount of the mandatory convertible notes may, but is not required to, purchase the Notes from the holders of the Notes at a price equal to 100% of principal amount of the Notes plus accrued and unpaid interest.

The Issuer is a subsidiary that was initially formed for the purpose of facilitating the issuance of the Initial Notes and has limited assets and revenue generating operations. The Issuer will be dependent upon GCUK to provide it with funds sufficient to meet its obligations under the Notes.

The Issuer was formed as a wholly owned subsidiary of GCUK for the purpose of facilitating the issuance of the Initial Notes. The Issuer has no operations and does not serve as a holding company for any operating subsidiaries. The intercompany loans funded with the proceeds from the Initial Notes and with the proceeds of the Additional Notes are the Issuer’s only significant assets. As such, the Issuer will be wholly dependent upon us to make payments on the inter-company loan or to make other funding arrangements in order for it to pay amounts due on the Notes.

A significant portion of our assets will not be pledged for the benefit of the holders of the Notes. The collateral securing the Notes, and the Guarantees may be diluted under certain circumstances. The value of the collateral securing the Notes and the Guarantees may not be sufficient to satisfy our obligations with regards to the holders of our Notes.

The Notes will be secured by certain of our assets and the assets of the Issuer, including the capital stock of GCUK’s subsidiaries, the Issuer and Fibernet. However, a significant portion of our assets will not serve as collateral for the Notes. In particular, we will not pledge:

| | • | | certain parts of the network leased by us, including any telecommunications cables and other equipment under a finance lease with Network Rail under which we lease approximately 24% of our lit fiber (calculated by fiber kilometers); |

| | • | | any rights, title, interest or obligations under certain specified excluded contracts, including (i) any contract in which our counterparty is a UK governmental entity and (ii) any contract in which our |

15

| | counterparty is a contractor or subcontractor to a UK governmental entity (these excluded contracts include those with the FCO, OGCbuying.solutions and other important customers); |

| | • | | any equipment or assets owned by us located on the premises of the parties to excluded contracts and any equipment or assets used exclusively by us in connection with the provision of services and the performance of obligations under such contracts; |

| | • | | property that we have pledged to Camelot in connection to our relationship with them; or |

| | • | | any contract or agreement (or rights or interests thereunder) which, if charged, would constitute a breach or default or result in the invalidation or unenforceability of any rights, title or interest of the chargor under such contract or agreement. |

Because these exceptions to the pledge mean that security will not be given over all or substantially all of our assets, the collateral agent will not be able to appoint either an administrative receiver or an administrator via an out of court procedure as a holder of a qualifying floating charge. The option to appoint an administrator by this route would likely otherwise have been available under applicable English insolvency law. The option to appoint an administrative receiver would also likely otherwise have been available under applicable English insolvency law for “Capital Market Arrangement” transactions as defined in the Insolvency Act 1986.

Moreover, the collateral that secures the Notes and the Guarantees may also secure additional debt to the extent permitted by the terms of the Indenture governing the Notes, including any further additional notes governed by the Indenture. The rights of the holders of the Notes to the collateral would be diluted by any increase in the debt secured by the collateral, including debt represented by additional notes issued under the Indenture.

Concurrent with the issue of the Initial Notes we entered into a five-year cross-currency interest rate swap transaction with an affiliate of Goldman, Sachs & Co. to minimize exposure to any dollar/sterling currency fluctuations related to interest payments on the dollar-denominated ($200 million) Initial Notes. The swap transaction converts the US dollar currency rate on interest payments to a specified pound sterling rate. At December 31, 2006 there was a liability of £2.7 million and an unrealized loss of £2.6 million on the swap. In connection with the swap transaction, the affiliate of Goldman, Sachs & Co. was granted a security interest in the collateral securing the Notes ranking equally with the security interest of the holders of the Notes. The security interest secures all obligations owed to the affiliate of Goldman, Sachs & Co. if a default occurs on the swap transaction or if the swap transaction is terminated. Depending on prevailing currency exchange rates, these obligations may be substantial. Any proceeds resulting from the exercise of security interests in the collateral will be shared pro rata among it and the holders of the Notes.

The value of the collateral and the amount to be received upon a sale of such collateral will depend upon many factors including, among others:

| | • | | the condition of the collateral; |

| | • | | the ability to sell the collateral in an orderly sale; |

| | • | | factors then affecting the telecommunications industry; |

| | • | | the condition of the economy; |

| | • | | the availability of buyers; |

| | • | | the time at which the collateral is sold; and |

| | • | | the market price for assets that are similar to the collateral. |

By their nature, portions of the collateral, including pledged capital stock of GCUK’s subsidiaries and real property and real property rights, may be illiquid and may have no readily ascertainable market value. In addition, a significant portion of the collateral consists of assets that may only be usable, and thus retain value, as part of our existing operating business. For example, although the collateral includes the portion of our fiber optic cable network that we own and that we are not prohibited by contract to pledge, it does not include the portion of our fiber optic cable network that is subject to the lease from Network Rail. Furthermore, although the collateral includes certain of our premises and other equipment that we are not prohibited by contract to pledge, it does not include such equipment that is subject to a right to purchase by certain of our government agency end-users. Accordingly, any such sale of the collateral separate from the sale of certain operating businesses may not be feasible or of significant value. To the extent that holders of other secured debt or third parties enjoy liens

16

(including statutory liens), whether or not permitted by the Indenture, such holders or third parties may have rights and remedies with respect to the collateral securing the Notes and the Guarantees that, if exercised, could reduce proceeds available to satisfy the obligations under the Notes and the Guarantees.

The ability of the collateral agent to foreclose on the secured property may be limited.

Bankruptcy law could prevent the collateral agent on behalf of the holders of the Notes from repossessing and disposing of the collateral upon the occurrence of an event of default; if the Issuer, the Guarantors or their respective creditors commence a bankruptcy proceeding before the collateral agent repossesses and disposes of the collateral. Under bankruptcy laws in certain jurisdictions, including the United States, secured creditors such as the holders of the Notes are prohibited from repossessing their security from a debtor in a bankruptcy case, or from disposing of security repossessed from such debtor, without bankruptcy court approval. It is impossible to predict how long payments under the Notes could be delayed following commencement of a bankruptcy case, and to what extent such payments would be made, and whether or when the collateral agent could repossess or dispose of the collateral or whether or to what extent a holder of the Notes would be compensated for any delay in payment or loss of value of the collateral.

We may not have the ability to raise the funds necessary to finance a change of control offer upon the occurrence of certain events constituting a change of control as required by the Indenture.

Upon the occurrence of a “change of control”, as defined in the Indenture, the Issuer will be required to make an offer to purchase all outstanding Notes at a price in cash equal to 101% of the principal amount thereof, plus any accrued and unpaid interest to the date of repurchase. Events involving a change of control may result in an event of default under any other debt that may be incurred in the future. This could result in an acceleration of the payment of that debt as well. We cannot assure holders of our Notes that the Issuer would have sufficient resources to repurchase the Notes or pay its obligations under the Notes or that we would have sufficient resources to do so if the debt under any other future debt were accelerated upon the occurrence of a change of control. If a change of control occurs at a time when we or the Issuer are prohibited from purchasing the Notes under any other debt agreements, we or the Issuer could seek the consent of any lenders to purchase the Notes or could attempt to refinance the borrowings that prohibit our repurchase of the Notes. If we or the Issuer do not obtain that consent or repay the borrowings, the prohibition from purchasing the Notes would remain. In addition, we expect that we would require third-party financing to make an offer to repurchase the Notes upon a change of control. We cannot assure you that we would be able to obtain such financing. Any failure by the Issuer to repurchase any of the tendered Notes would constitute an event of default under the Indenture, which would likely cause a default under any other indebtedness.