As filed with the Securities and Exchange Commission on September 27, 2005

Registration No. 333-127343

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

Form S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

DYNCORP INTERNATIONAL LLC

(Exact name of registrant as specified in Its Charter)

| | | | |

| Delaware | | 7389 | | 52-2287126 |

(State or other jurisdiction of incorporation or organization) | | (Primary Standard Industrial Classification Bankruptcy Code Number) | | (I.R.S. Employer Identification Number) |

| | |

Co-Registrants See Next Page c/o DynCorp International LLC 8445 Freeport Parkway Suite 400 Irving, Texas 75063 (817) 302-1460 | | Michael J. Thorne Chief Financial Officer 8445 Freeport Parkway Suite 400 Irving, Texas 75063 (972) 871-6723 |

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices) | | (Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service) |

Copies to:

Michael R. Littenberg, Esq.

Benjamin M. Polk, Esq.

Schulte Roth & Zabel LLP

919 Third Avenue

New York, NY 10022

Ph: (212) 756-2000

Fax: (212) 593-5955

Approximate Date of Commencement of Proposed Offer to the Public: As soon as practicable after this registration statement becomes effective.

If the securities being registered are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier registration statement for the same offering: ¨

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Co-Registrants

| | | | | | |

Exact Name of Co-Registrant as specified in Its Charter

| | State or Other

Jurisdiction of

Incorporation or

Organization

| | Primary Standard

Industrial

Classification Code

Number

| | I.R.S.

Employer

Identification

Number

|

| | | |

DIV Capital Corporation (Co-Issuer) | | Delaware | | 6719 | | 72-1591534 |

| | | |

DTS Aviation Services LLC (Guarantor) | | Nevada | | 4581 | | 43-2053132 |

| | | |

DynCorp Aerospace Operations LLC (Guarantor) | | Delaware | | 4581 | | 54-1696542 |

| | | |

DynCorp International Services LLC (Guarantor) | | Virginia | | 7389 | | 54-1108455 |

| | | |

Dyn Marine Services LLC (Guarantor) | | California | | 8744 | | 62-1221029 |

| | | |

DynCorp International of Nigeria LLC (Guarantor) | | Delaware | | 8741 | | 68-0606520 |

| | | |

Dyn Marine Services of Virginia LLC (Guarantor) | | Virginia | | 8744 | | 54-1741786 |

| | | |

Services International LLC (Guarantor) | | Delaware | | 7389 | | 41-2030325 |

| | | |

Worldwide Humanitarian Services LLC (Guarantor) | | Delaware | | 7389 | | 52-2314506 |

SUBJECT TO COMPLETION, DATED SEPTEMBER 27, 2005

PRELIMINARY PROSPECTUS

DYNCORP INTERNATIONAL LLC

DIV CAPITAL CORPORATION

$320,000,000

OFFER TO EXCHANGE

9.50% Senior Subordinated Notes due 2013, Series B

for any and all outstanding

9.50% Senior Subordinated Notes due 2013, Series A

of

DynCorp International LLC and DIV Capital Corporation

The exchange offer will expire at 12:00 midnight, New York City time,

on 2005, which is 20 business days after the commencement of the exchange offer, unless extended.

| | |

The Issuers: • DynCorp International LLC, or DynCorp International, and DIV Capital Corporation. DIV Capital Corporation is a wholly owned subsidiary of DynCorp International with nominal assets, which conducts no business or operations. DynCorp International and DIV Capital Corporation are collectively referred to in this prospectus as the “issuers.” The Offering: • Offered securities: the securities offered by this prospectus are senior subordinated notes, which are being issued in exchange for senior subordinated notes sold by us in our private placement that we consummated on February 11, 2005. The New Notes are substantially identical to the Original Notes and are governed by the same indenture governing the Original Notes. Original Notes tendered in the exchange offer must be in denominations of principal amount of $1,000 and any integral multiple thereof. • Expiration of offering: the exchange offer expires at 12:00 midnight, New York City time, on , 2005, which is 20 business days after the commencement of the exchange offer, unless extended. • Each broker-dealer that receives New Notes pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of the New Notes. If the broker-dealer acquired the Original Notes as a result of market making or other trading activities, such broker-dealer must use the prospectus for the exchange offer, as supplemented or amended, in connection with resales of the New Notes. • Broker-dealers who acquired the Original Notes directly from the issuers from registration must, in the absence of an exemption, comply with the registration and prospectus delivery requirements of the Securities Act of 1933, or the Securities Act, in connection with secondary resales and cannot rely on the position of the Securities and Exchange Commission or SEC staff enunciated in the Exxon Capital Holding Corp. no-action letter (available May 13, 1988). | | The New Notes: • Maturity: February 15, 2013. • Interest payment dates: semiannually on each February 15 and August 15, beginning on August 15, 2005. • Redemption: we can redeem the New Notes on or after February 15, 2009, except we may redeem up to 35% of the New Notes prior to February 15, 2008 with the net cash proceeds of one or more public equity offerings. We are required to redeem the New Notes under some circumstances involving a change of control and asset sales. • Ranking: the New Notes will be our general unsecured obligations, will be subordinated to our existing and future senior debt and will rank equally with our future senior subordinated debt. The guarantees of the New Notes will be general unsecured obligations of each guarantor and will be structurally subordinated to all of the existing and future senior debt of our guarantor subsidiaries and will rank equally with any of our senior subordinated debt. The New Notes will be structurally subordinated to all obligations of DynCorp International’s subsidiaries, which will not guarantee the New Notes. As of July 1, 2005, we had $664.1 million of indebtedness, including the New Notes and excluding interest accrued thereon, of which $344.1 million was secured. On the same date, we had approximately $69.9 million of availability under our senior secured credit facility (which gives effect to $5.1 million of outstanding letters of credit which reduced our availability by that amount). As of July 1, 2005, approximately $344.1 million of our indebtedness would have ranked senior to, or pari passu with, the New Notes, excluding $5.1 million of outstanding letters of credit. • Neither an exchange of an original note for a New Note nor the filing of a registration statement with respect to the resale of the New Notes should be a taxable event to you, and you should not recognize any taxable gain or loss or any interest income as a result of such exchange or such filing. |

See “Risk Factors,” beginning on page 14, for a discussion of some factors that should be considered by holders in connection with a decision to tender Original Notes in the exchange offer.

These securities have not been approved or disapproved by the Securities and Exchange Commission or any state securities commission nor has the Securities and Exchange Commission or any state securities commission passed on the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2005.

TABLE OF CONTENTS

INFORMATION ABOUT THE TRANSACTION

This prospectus incorporates important business and financial information about us that is not included in or delivered with this prospectus. Such information is available without charge to the holders of our Original Notes by contacting us at our address, which is 8445 Freeport Parkway, Suite 400, Irving, Texas, 75063 or by calling us at (817) 302-1460. To obtain timely delivery of this information, you must request this information no later than five business days before , 2005, which is 20 business days after the commencement of the exchange offer, unless extended.

MARKET SHARE, ESTIMATED CONTRACT VALUE, RANKING AND OTHER DATA

References to our “leading position” in this prospectus are based upon our revenues for the U.S. government’s fiscal year ended September 30, 2004. In this prospectus, we refer to information regarding market data obtained from internal sources, market research, publicly available information and industry publications. Although we believe the information is reliable, we cannot guarantee the accuracy or completeness of the information and have not independently verified it. Estimates are inherently uncertain and the estimates contained herein involve risks and uncertainties and are subject to change based on various factors, including those discussed under the caption “Risk Factors” in this prospectus. See “Risk Factors.”

As used herein, except as otherwise indicated in this paragraph, estimated contract values are calculated as the greater of the bid price we submitted or expect to submit for the applicable contract and the sum of our actual revenues under the contract and our estimated revenues from future performance under options requested by the customer. For indefinite delivery, indefinite quantity contracts, the estimated value of such contracts is the sum of our actual revenues under the contract and our estimated revenues from future performance under task orders issued. Funded backlog is the actual amount appropriated by a customer for the payment of goods and services less actual revenue recorded as of the measurement date under that appropriation. Unfunded backlog is the actual dollar value of unexercised contract options. Anticipated revenues from indefinite delivery, indefinite quantity contracts are not included in unfunded backlog. Backlog is only a measure of funded contract values, and unfunded contract options, less any revenue that has been recognized to that point. Backlog does not take into account any expenses associated with contractual performance and converting backlog into revenue would not reflect net income associated with the contracts.

All references to fiscal years in “Business—Industry Trends” pertain to the fiscal year of the U.S. government, which ends on September 30th of each year.

i

FORWARD-LOOKING STATEMENTS

This prospectus contains “forward-looking statements.” All statements other than statements of historical fact are “forward-looking statements” for purposes of federal and state securities laws. Forward-looking statements may include the words “may,” “will,” “plans,” “estimates,” “anticipates,” “believes,” “expects,” “intends” and similar expressions. These forward-looking statements include, among others, the following:

| | • | | estimates of contract values; |

| | • | | anticipated revenues from indefinite delivery, indefinite quantity contracts; |

| | • | | expected percentages of future revenues represented by fixed-price contracts; and |

| | • | | statements covering our business strategy. |

See “Risk Factors” for examples of factors, risks and uncertainties that could cause actual outcomes and results to be materially different from those projected or assumed in our forward-looking statements.

We undertake no obligation to update or revise any forward-looking statements, either to reflect new developments, or for any other reason, except as required by law.

TRADEMARKS AND TRADE NAMES

We own or have the rights to various trademarks and trade names used in this prospectus. This prospectus also includes trade names and trademarks of other companies. We and our subsidiaries hold an exclusive, perpetual, irrevocable, worldwide, royalty-free and fully paid-up license to use the “Dyn International” and “DynCorp International” name in connection with aviation services, security services, technical services and marine services.

ii

PROSPECTUS SUMMARY

The following summary contains basic information about us and this exchange offer. It likely does not contain all the information that is important to you. You should read this entire prospectus carefully, including “Risk Factors” and the financial information included elsewhere. In this prospectus, unless the context requires otherwise, references to “we,” “our,” “the Company” or “us” refers, as applicable, to DynCorp International LLC, or DynCorp International, or its predecessors, and its consolidated subsidiaries. All references in this prospectus to the “issuers” are to DynCorp International and DIV Capital Corporation, or DIV Capital. All references in this prospectus to fiscal years made in connection with our financial statements or operating results refer to the fiscal year ended on the Friday closest to March 31st of such year. For example, “fiscal 2004” refers to our fiscal year ended April 2, 2004. Our narrative discussion of our fiscal 2005 and the twelve months ending July 1, 2005 results gives pro forma effect to our acquisition by Veritas Capital from Computer Sciences Corporation on February 11, 2005.

Our Company

We are a leading provider of a broad range of mission-critical outsourced technical services to civilian and military government agencies and commercial customers. Our specific global expertise is in law enforcement training and support, security services, base operations, logistics support and aviation services and operations. Although we began to operate independently as a stand-alone entity on December 27, 2000, since 1951 our predecessors have provided essential services to numerous U.S. government departments and agencies. Our current customers include the Department of State, the Army, Air Force, Navy and Marine Corps (collectively, the Department of Defense); the Department of Homeland Security and commercial customers and foreign governments. As of July 1, 2005, we had over 14,100 employees in 33 countries and 45 active contracts ranging in duration from three to ten years and over 75 task orders.

We have increased our revenues and EBITDA from fiscal 2001 through fiscal 2005 at compound annual growth rates, or CAGR, of 34.7% and 49.2%, respectively. Our growth has primarily been driven by increasing demand for outsourced technical services and other non-combat-related functions, such as reconstruction, peace-keeping, logistics and other support activities. The term outsourcing is defined as the organizational practice of contracting for services from an external entity while retaining control over assets and oversight of the services being sources.In fiscal 2005, we generated revenues, EBITDA and net income of $1.9 billion, $114.6 million, and $58.8 million respectively, as compared with $1.2 billion, $60.0 million and $31.4 million in fiscal 2004. For the twelve months ending July 1, 2005 we had revenues, EBITDA and net income of $1.9 billion, $117.4 million and $13.8 million, respectively. As of July 1, 2005, we had a total backlog of approximately $2.6 billion and, historically, virtually our entire backlog has been converted into revenue at or above stated contract values. Backlog does not take into account any expenses associated with the contracts and converting backlog into revenue would not reflect net income associated with contracts. In addition to our backlog as of July 1, 2005, we had $19.8 billion of currently available ceiling under our existing indefinite delivery, indefinite quantity, contracts. From the beginning of fiscal 2001 through July 1, 2005, we have won a total of 83%, or $10.4 billion out of $12.5 billion, of the aggregate estimated value of new or renewed contracts on which we bid.

We operate through two core operating divisions, Field Technical Services and International Technical Services.

Our Field Technical Services operating division provides long-term aviation services and engineering and logistics support, ranging from daily fleet maintenance to extensive modification and overhauls on aircraft, weapons systems and support equipment. Field Technical Services generates revenue from a diverse mix of customers, services and platforms under long-term contracts that are typically three to ten years in duration. Accounting for 35.3% of our total revenue for fiscal 2005, revenues in our Field Technical Services division have

1

grown from $264.7 million in fiscal 2001 to $684.7 million for the twelve months ended July 1, 2005. Contract Field Teams is the most significant program of our Field Technical Services operating division based on revenues, and our predecessors have participated in this program for 54 consecutive years. We believe we are the largest provider of Contract Field Teams services to the Department of Defense. This program deploys highly mobile, quick-response field teams to customer locations worldwide to supplement our customers’ workforce, including generally providing mission support to aircraft and weapons systems in addition to depot-level repair. The Contract Field Teams contract, has an estimated value of $1.8 billion over a ten-year term, through October 2007. The Contract Field Teams contract contributed 18.0% and 19.3% of our revenues for fiscal 2005 and the three months ended July 1, 2005, respectively.

Our International Technical Services operating division primarily provides outsourced law enforcement training, drug eradication, global logistics, base operations and personal and physical security services to government and commercial customers in foreign jurisdictions. Since fiscal 2001, International Technical Services has grown revenues from $319.2 million to $1,254.7 million for the twelve months ended July 1, 2005, or 64.7% of our total revenues. The International Technical Services division has witnessed strong growth as a result of the U.S. government’s trend toward outsourcing critical related functions. In February 2004, as part of the Department of State’s outsourced law enforcement training in the Middle East, we were awarded a new Civilian Police contract, which expanded the existing Civilian Police program in place since 1994. As of July 1, 2005, we believe we performed in excess of 90% of the dollar value of awarded task orders for the Civilian Police program and have deployed civilian police officers from the United States to 12 countries to train and offer logistics support to the local police and assist them with infrastructure and reconstruction. We have been awarded multiple task orders under the Civilian Police program, including assignments in Iraq, Afghanistan and Haiti. The new Civilian Police contract has an estimated value of $1.75 billion over the five-year term of this program, through February 2009. The Civilian Police contract contributed 27.4% and 30.3% of our revenues for fiscal 2005 and the three months ended July 1, 2005, respectively.

Competitive Strengths

We believe our core strengths include the following:

| | • | | leading market position; |

| | • | | attractive industry fundamentals; |

| | • | | long-standing and strong customer relationships; |

| | • | | global business development capability; |

| | • | | strong and stable platform for growth; |

| | • | | attractive cash flow dynamics; and |

| | • | | experienced management team and distinguished board. |

Business Strategy

Our objective is to leverage our leading market position to further increase our revenues and earnings. We intend to achieve this objective through the following strategies:

| | • | | exploit current business opportunities and backlog; |

| | • | | capitalize on industry trends; |

| | • | | pursue commercial business and foreign government opportunities; |

2

| | • | | expand domestic service offerings; and |

| | • | | increase profitability and operating efficiency. |

We face certain risks in the implementation of our business strategy. Substantially all of our revenues are derived from contracts with the Department of Defense and the Department of State. Changes in the Department of Defense and the Department of State spending or termination of our contracts by the Department of Defense and the Department of State could have a material adverse effect on our business, results of operations and financial condition. In addition, we may never receive actual task orders to deliver services under our indefinite delivery, indefinite quantity contracts. Furthermore, political destabilization or insurgency in the regions in which we operate may keep us from continuing to provide services under our contracts or from expanding our service offerings in those regions. An accident or incident involving our employees or third parties could adversely impact our ability to implement our strategy.

Our substantial indebtedness also presents risks. As of July 1, 2005, we had aggregate indebtedness of $664.1 million (excluding $5.1 million in outstanding letters of credit) and our indebtedness under our indenture and senior secured credit facility impose significant operating and financial restrictions on us. We have limited experience operating as a stand-alone company. We believe that the most significant other risks that we face include:

| | • | | political and economic events affecting the United States and/or other countries or regions of the world; |

| | • | | our ability to attract and retain customers and to remain competitive in the markets we serve; |

| | • | | our dependence on key personnel; and |

| | • | | other the factors discussed below under the caption “Risk Factors.” |

The Transactions

On February 11, 2005, DynCorp International was acquired from Computer Sciences Corporation by DynCorp International Inc. (formerly known as DI Acquisition Corp.), a subsidiary of The Veritas Capital Fund II, L.P., a private equity investment fund organized and managed by Veritas Capital Management II, L.L.C., a leading private equity firm, and its co-investors. We refer to the foregoing transaction as the “2005 Acquisition” in this prospectus. As used in this prospectus, we refer to the “Transactions” collectively as (i) the consummation of the 2005 Acquisition, (ii) the borrowings under our senior secured credit facility entered into in connection with 2005 Acquisition and (iii) the issuance of the Original Notes and the application of the proceeds therefrom. We refer to The Veritas Capital Fund II, L.P. and its affiliates (other than DynCorp International Inc. and its subsidiaries) in this prospectus as “Veritas Capital” and we refer to DynCorp International Inc. in this prospectus as “our parent.”

The purchase price for the 2005 Acquisition was $857.3 million, $775.0 million of which was payable in cash. The remaining $75.0 million of the purchase price was paid to Computer Sciences Corporation in the form of preferred equity in our parent, with the amount of preferred stock issued to Computer Sciences Corporation subject to increase or decrease based upon an increase or decrease in the net working capital of DynCorp International at the closing of the 2005 Acquisition as compared to April 2, 2004. The purchase agreement established a procedure for determining the net working capital adjustment after the closing, with any dispute regarding such calculations to be resolved by an independent accounting firm. We are currently negotiating the amount of the working capital adjustment with Computer Sciences Corporation. An additional preferred equity investment of $50.0 million was made in our parent by The Northwestern Mutual Life Insurance Company on identical terms.

Dividends accrue on the preferred stock (during each annual period) at a rate per annum equal to 13% of the liquidation preference of the preferred stock. The preferred stock is subject to mandatory redemption 10 years from the date of issue.

3

Following the 2005 Acquisition, support for the business applications and communications technology of our business was provided by a combination of DynCorp’s and our dedicated resources and centralized Computer Sciences Corporation administrative and information technology resources. We entered into a transition services agreement with Computer Sciences Corporation upon the closing of the 2005 Acquisition, which covers support services for certain operating areas, including information technology, business systems, financial operations, payroll/HR and employee benefits. Pursuant to the agreement, Computer Sciences Corporation will continue to perform a portion of our internal finance and personnel accounting application support services and communications services until February 11, 2006 or, if earlier, until we convert these services to substitute systems installed on our own equipment. In addition, Computer Sciences Corporation performs certain employee benefits advising and consulting services on an hourly basis as we require them. We now provide all other services not extended under this agreement without any support from Computer Sciences Corporation. The total cost of transition services during fiscal 2005 and the three months ended July 1, 2005, were $355,000 and $988,000 respectively.

We pay Veritas an annual management fee of $300,000 to provide us with general business management, financial, strategic and consulting services. We also paid to Veritas a one-time transaction fee of $12.0 million at the closing of the 2005 Acquisition, as consideration for planning, structuring and consummating the 2005 Acquisition.

In addition to the issuance of the Original Notes on February 11, 2005, concurrently with the consummation or the offering of the Original Notes, we entered into a senior secured credit facility. This facility provides us with $345.0 million term loan, maturing in 2011, and up to $75.0 million in available revolving loan borrowings, maturing in 2010, our revolving credit facility was undrawn at the closing at the offering and as of July 1, 2005.

As of July 1, 2005, we had $664.1 million of indebtedness, including the New Notes and excluding interest accrued thereon, of which $344.1 million was secured. On the same date, we had approximately $69.9 million of availability under our senior secured credit facility (which gives effect to $5.1 million of outstanding letters of credit). As of July 1, 2005, approximately $344.1 million of our indebtedness would have ranked senior to, or pari passu with, the New Notes excluding, $5.1 million of outstanding letters of credit.

4

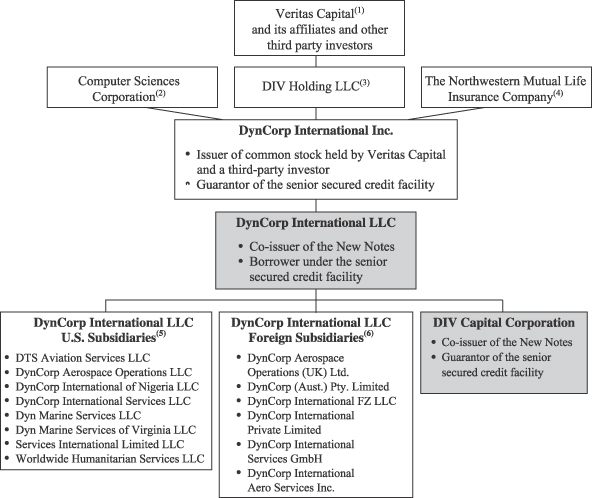

The following chart shows our organizational structure. DIV Capital, an issuer of the New Notes, is our wholly owned subsidiary with nominal assets and no active business or operations.

| (1) | The membership interests in DIV Holding LLC are held by affiliates of Veritas Capital and Carlisle Ventures, Inc. (an affiliate of The Northwestern Mutual Life Insurance Company) |

| (2) | Owns 100% of the Series A-2 preferred stock of our parent. |

| (3) | Owns 100% of the common stock of our parent. |

| (4) | Owns 100% of the Series A-1 preferred stock of our parent. |

| (5) | All U.S. subsidiaries of DynCorp International will also guarantee payment under the New Notes on a senior subordinated basis. They are also guarantors of the senior secured credit facility. |

| (6) | None of the foreign subsidiaries of DynCorp International will guarantee payment under the New Notes. |

Our principal executive offices are located at 8445 Freeport Parkway, Suite 400, Irving, Texas, 75063 and our telephone number is (817) 302-1460. Our website address is (http://www.dyncorpinternational.com). We do not incorporate the information on our website into this prospectus and you should not consider it part of this prospectus.

5

THE EXCHANGE OFFER

Expiration Date | 12:00 midnight, New York City time, on , 2005, which is 20 business days after the commencement of the exchange offer, unless we extend the exchange offer. |

Exchange and Registration Rights | In an A/B exchange registration rights agreement dated February 11, 2005, the holders of the issuers’ 9.50% senior subordinated notes due 2013, series A, which are referred to in this prospectus as the “Original Notes,” were granted exchange and registration rights. This exchange offer is intended to satisfy these rights. You have the right to exchange the Original Notes that you hold for the issuers’ 9.50% senior subordinated notes due 2013, series B, which are referred to in this prospectus as the “New Notes,” with substantially identical terms. Once the exchange offer is complete, you will no longer be entitled to any exchange or registration rights with respect to your Original Notes. |

Accrued Interest on the New Notes and Original Notes | The New Notes will bear interest from February 11, 2005. Holders of Original Notes which are accepted for exchange will be deemed to have waived the right to receive any payment in respect of interest on those Original Notes accrued to the date of issuance of the New Notes. |

Conditions to the Exchange Offer | The exchange offer is conditioned upon some customary conditions which we may waive and upon compliance with securities laws. All conditions to which the exchange offer is subject must be satisfied or waived on or before the expiration of the offer. |

Procedures for Tendering Original Notes | Each holder of Original Notes wishing to accept the exchange offer must: |

| | • | | complete, sign and date the letter of transmittal, or a facsimile of the letter of transmittal; or |

| | • | | arrange for DTC to transmit required information in accordance with DTC’s procedures for transfer to the exchange agent in connection with a book-entry transfer. |

| | You must mail or otherwise deliver this documentation together with the Original Notes to the exchange agent. Original Notes tendered in the exchange offer must be in denominations of principal amount of $1,000 and any integral multiple thereof. |

Special Procedures for Beneficial Holders | If you beneficially own Original Notes registered in the name of a broker, dealer, commercial bank, trust company or other nominee and you wish to tender your Original Notes in the exchange offer, you should contact the registered holder promptly and instruct them to |

6

| | tender on your behalf. If you wish to tender on your own behalf, you must, before completing and executing the letter of transmittal for the exchange offer and delivering your Original Notes, either arrange to have your Original Notes registered in your name or obtain a properly completed bond power from the registered holder. The transfer of registered ownership may take considerable time. |

Guaranteed Delivery Procedures | You must comply with the applicable procedures for tendering if you wish to tender your Original Notes and: |

| | • | | time will not permit your required documents to reach the exchange agent by the expiration date of the exchange offer; or |

| | • | | you cannot complete the procedure for book-entry transfer on time; or |

| | • | | your Original Notes are not immediately available. |

Withdrawal Rights | You may withdraw your tender of Original Notes at any time by or prior to 12:00 midnight, New York City time, on the expiration date, unless previously accepted for exchange. |

Failure to Exchange Will Affect You Adversely | If you are eligible to participate in the exchange offer and you do not tender your Original Notes, you will not have further exchange or registration rights, and you will continue to be restricted from transferring your Original Notes. Accordingly, the liquidity of the Original Notes will be adversely affected. |

Federal Tax Considerations | We believe that the exchange of the Original Notes for the New Notes pursuant to the exchange offer will not be a taxable event for United States federal income tax purposes. A holder’s holding period for New Notes will include the holding period for Original Notes, and the adjusted tax basis of the New Notes will be the same as the adjusted tax basis of the Original Notes exchanged. |

Exchange Agent | Bank of New York, trustee under the indenture under which the New Notes will be issued, is serving as exchange agent. |

Use of Proceeds | We will not receive any proceeds from the exchange offer. |

7

SUMMARY TERMS OF NEW NOTES

The summary below describes the principal terms of the New Notes. Certain of the terms and conditions described below are subject to important limitations and exceptions.

Issuers | DynCorp International and DIV Capital Corporation. DIV Capital Corporation is a wholly owned subsidiary of DynCorp International with nominal assets and no active business or operations. DynCorp International and DIV Capital Corporation are collectively referred to in this prospectus as the “issuers.” |

Securities Offered | The form and terms of the New Notes will be the same as the form and terms of the Original Notes except that: |

| | • | | the New Notes will bear a different CUSIP number from the Original Notes; |

| | • | | the New Notes will have been registered under the Securities Act of 1933, or the Securities Act, and, therefore, will not bear legends restricting their transfer; and |

| | • | | you will not be entitled to any exchange or registration rights with respect to the New Notes. |

| | The New Notes will evidence the same debt as the Original Notes. They will be entitled to the benefits of the indenture governing the Original Notes and will be treated under the indenture as a single class with the Original Notes. |

Maturity | February 15, 2013. |

Interest | The New Notes will bear cash interest at the rate of 9.50% per annum (calculated using a 360-day year), payable semi-annually in arrears. |

| | Payment frequency: every six months on February 15 and August 15. |

| | First payment: August 15, 2005. |

Ranking | The New Notes will be our general unsecured obligations, will be subordinated to our existing and future senior debt, and will rank equally with our future senior subordinated debt. The guarantees of the New Notes will be general unsecured obligations of each guarantor and will be structurally subordinated to all of the existing and future senior debt of our guarantor subsidiaries, and will rank equally with any of our senior subordinated debt. The New Notes will be structurally subordinated to all obligations of DynCorp International’s foreign subsidiaries, which will not guarantee the New Notes. As of July 1, 2005, we had $664.1 million of indebtedness, including the New Notes and excluding interest accrued thereon, of which $344.1 million was secured. As of July 1, 2005, approximately $344.1 million of our indebtedness would have ranked senior to, or |

8

| | pari passu with, the New Notes, excluding $5.1 million of outstanding letters of credit. For the fiscal year ended April 1, 2005 and the three months ended July 1, 2005, our non-guarantor subsidiaries represented 11.0% and 11.3% of our total revenues, respectively, and, as of July 1, 2005, 4.3% of our total assets. None of our foreign subsidiaries had any outstanding indebtedness as of July 1, 2005. |

Guarantees | Each of our existing and future domestic subsidiaries will guarantee the New Notes. Our foreign subsidiaries will not guarantee the New Notes. |

Optional Redemption | Prior to February 15, 2009, the issuers may redeem the New Notes, in whole or in part, at a price equal to (a) 100% of the principal amount of the notes plus the applicable premium, which is a component of the redemption price of the notes that is calculated to provide yield protection in the event that certain interest rates are lower than the interest rates on the New Notes at the date of redemption, as more fully described under “Description of New Notes—Definitions” under the defined term “Applicable Premium”), plus (b) accrued and unpaid interest and additional interest, or “Special Interest”, payable on the outstanding principal amount of any notes that constitute transfer restricted securities in the event that we fail to comply with certain obligations under the registration rights agreement, if any, to the redemption date. |

| | After February 15, 2009, the issuers may redeem the notes, in whole or in part, at the applicable redemption prices described under “Description of New Notes—Optional Redemption,” plus accrued and unpaid interest and Special Interest, if any, to the redemption date. |

Optional Redemption after Public Equity Offerings | The Issuers may redeem up to 35% of the original aggregate principal amount of the notes, at any time before February 15, 2008, with the net cash proceeds of certain equity offerings at a price equal to 109.500% of the principal amount of the notes, plus accrued and unpaid interest and Special Interest, if any, to the redemption date. |

Mandatory Offer to Repurchase | If we sell certain assets without applying the proceeds in a specified manner, or experience certain change of control events, each holder of the New Notes may require us to repurchase all or a portion of its New Notes at the purchase prices set forth in this prospectus, plus accrued and unpaid interest and Special Interest, if any, to the repurchase date. Our senior secured credit facility may restrict us from repurchasing any of the New Notes, including upon any repurchase we may be required to make as a result of a change of control or certain asset sales. |

9

Certain Indenture Provisions | The indenture governing the New Notes contains covenants that impose significant restrictions on our business. The restrictions that these covenants place on us and our restricted subsidiaries include limitations on our ability and the ability of our restricted subsidiaries to, among other things: |

| | • | | incur additional indebtedness or issue preferred stock or disqualified stock, which are equity interests that would mature or may be redeemable at the option of the holders, in whole or in part, on or prior to a date that is 91 days after the date the notes mature; |

| | • | | consolidate, merge, sell or otherwise dispose of all or substantially all of our assets; |

| | • | | enter into transactions with our affiliates; and |

| | • | | designate our subsidiaries as unrestricted subsidiaries. |

| | These covenants are subject to a number of important limitations and exceptions as described under “Description of the New Notes.” |

Exchange Offer; Registration Rights | You have the right to exchange the Original Notes for New Notes with substantially identical terms. This exchange offer is intended to satisfy that right. The New Notes will not provide you with any further exchange or registration rights. |

Resales Without Further Registration | We believe that the New Notes issued in the exchange offer in exchange for Original Notes may be offered for resale, resold and otherwise transferred by you without compliance with the registration and prospectus delivery provisions of the Securities Act, if: |

| | • | | you are acquiring the New Notes issued in the exchange offer in the ordinary course of your business; |

| | • | | you have not engaged in, do not intend to engage in, and have no arrangement or understanding with any person to participate in the distribution of the New Notes issued to you in the exchange offer; and |

| | • | | you are not our “affiliate,” as defined under Rule 405 of the Securities Act. |

| | Each broker dealer that receives New Notes pursuant to the Exchange Offer must deliver a prospectus in connection with any resale of the New Notes. If the broker dealer acquired the Original Notes as a result of market making or other trading activities, such broker dealer must use the prospectus for the exchange offer, as supplemented or amended in connection with the resales of the New Notes. We do not intend to list the New Notes on any securities exchange. |

10

Summary Consolidated Historical and Pro Forma Financial Data

On March 7, 2003, DynCorp and its subsidiaries, including DynCorp International, were acquired by Computer Sciences Corporation. The financial statements included in this prospectus for any period prior to March 7, 2003, the date of the CSC acquisition are referred to as the “original predecessor period” statements. We refer to the financial statements for the period March 8, 2003 to February 11, 2005, the date of the 2005 Acquisition, as the “immediate predecessor period.” On February 11, 2005, DynCorp International was acquired by Veritas Capital. The 2005 Acquisition has been accounted for using the purchase method of accounting, and the assets acquired and liabilities assumed have been accounted for at their fair market values at the date of consummation based on preliminary estimates. The final allocation of the purchase price may differ from the amount reflected herein, and that difference could be significant.

The following table sets forth summary historical consolidated financial and other operating data, and pro forma data for DynCorp International. The summary consolidated historical financial data as of July 1, 2005, and April 1, 2005, for the three months ended July 1, 2005, and the period February 12, 2005 through April 1, 2005 are derived from our consolidated financial statements for the successor period. The summary consolidated historical financial data for the period April 3, 2004 through February 11, 2005, the three months ended July 2, 2004 and as of and for the year ended April 2, 2004 and for the period March 8, 2003 through March 28, 2003 are derived from our consolidated financial statements for the immediate predecessor period. The summary consolidated financial information for the period March 30, 2002 through March 7, 2003 have been derived from our consolidated financial statements for the original predecessor period. The summary consolidated financial information as of and for the three month period ended July 1, 2005, and for the three month period ended July 2, 2004 have been derived from our unaudited consolidated financial statements during the successor and immediate predecessor period, respectively, which, in our opinion, have been prepared on the same basis as the audited financial statements and include all adjustments, consisting only of normal and recurring adjustments, necessary for a fair presentation of the information included therein.

The pro forma statement of operations data for the year ended April 1, 2005 includes the historical results of operations for the successor period February 12, 2005 to April 1, 2005 combined with the historical results of operations for the immediate predecessor period April 3, 2004 to February 11, 2005, and gives effect to the Transactions as if the Transactions had occurred on April 3, 2004. The pro forma statement of operations data for the three months ended July 2, 2004 gives effect to the Transactions as if the Transactions had occurred on April 3, 2004. The unaudited pro forma financial data does not necessarily reflect what our results of operations or financial position would have been had the transaction taken place on the date indicated and is not intended to project our results of operations or financial position for any future period or date.

The information set forth below should be read in conjunction with the information under “Capitalization,” “Pro Forma Financial Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes and the financial statements included elsewhere in this prospectus.

11

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Original

Predecessor

Period

| | | Immediate Predecessor Period

| | | Successor

Period

| | | Immediate

Predecessor

Period

| | | Successor

Period

| | | Pro Forma for the

| |

| | | March 30, 2002– March 7, 2003

| | | 21 Days Ended March 28, 2003

| | | Fiscal Year

Ended April 2, 2004

| | | | | | 49 Days

Ended

April 1,

2005

| | | Three

Months

Ended

July 2, 2004

| | | Three

Months

Ended

July 1, 2005

| | | Year Ended

April 1, 2005

| | | Twelve

Months

Ended

July 1, 2005

| |

| | | | | | April 3, 2004–

February 11, 2005

| | | | | | |

| | | (dollars in thousands, except for backlog, which is in millions) | |

STATEMENT OF OPERATIONS DATA: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Revenues | | $ | 859,112 | | | $ | 59,240 | | | $ | 1,214,289 | | | $ | 1,654,305 | | | $ | 266,604 | | | $ | 406,894 | | | $ | 425,055 | | | $ | 1,920,909 | | | $ | 1,939,070 | |

Costs of Services | | | 787,649 | | | | 53,482 | | | | 1,106,571 | | | | 1,496,109 | | | | 245,406 | | | | 367,021 | | | | 378,658 | | | | 1,741,515 | | | | 1,753,152 | |

Selling, General and Administrative | | | 40,316 | | | | 3,414 | | | | 48,350 | | | | 57,755 | | | | 8,408 | | | | 15,650 | | | | 19,159 | | | | 66,438 | | | | 69,872 | |

Depreciation and Amortization | | | 351 | | | | 265 | | | | 8,148 | | | | 5,922 | | | | 5,605 | | | | 1,773 | | | | 10,685 | | | | 40,969 | | | | 39,445 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Operating Income | | | 30,796 | | | | 2,079 | | | | 51,220 | | | | 94,519 | | | | 7,185 | | | | 22,450 | | | | 16,553 | | | | 71,987 | | | | 76,601 | |

Interest Expense | | | — | | | | — | | | | — | | | | — | | | | 8,054 | | | | — | | | | 13,837 | | | | 55,468 | | | | 55,468 | |

Interest Income | | | (43 | ) | | | (2 | ) | | | (64 | ) | | | (170 | ) | | | (7 | ) | | | (25 | ) | | | — | | | | (177 | ) | | | (152 | ) |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Net Income (Loss) Before Income Taxes | | | 30,839 | | | | 2,081 | | | | 51,284 | | | | 94,689 | | | | (862 | ) | | | 22,475 | | | | 2,716 | | | | 16,696 | | | | 21,285 | |

Provision (Benefit) for Income Taxes | | | 11,973 | | | | 852 | | | | 19,924 | | | | 34,956 | | | | 60 | | | | 8,577 | | | | 639 | | | | 6,161 | | | | 7,491 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Net Income (Loss) | | $ | 18,866 | | | $ | 1,229 | | | $ | 31,360 | | | $ | 59,733 | | | $ | (922 | ) | | $ | 13,898 | | | $ | 2,077 | | | $ | 10,535 | | | $ | 13,794 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| | | | | | | | | |

OTHER FINANCIAL DATA: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

EBITDA (1) (2) | | $ | 31,781 | | | $ | 2,382 | | | $ | 60,072 | | | $ | 101,326 | | | $ | 13,279 | | | $ | 24,467 | | | $ | 27,447 | | | $ | 114,330 | | | $ | 117,385 | |

Capital Expenditures | | | 1,011 | | | | 11 | | | | 2,047 | | | | 8,473 | | | | 244 | | | | 2,626 | | | | 446 | | | | 8,717 | | | | 2,626 | |

| | | | | | | | | |

SELECTED OPERATING INFORMATION: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Contract Recompete Win Rate (3) | | | 79 | % | | | NA | | | | 100 | % | | | — | | | | — | | | | N/A | | | | 100 | % | | | 100 | % | | | 100 | % |

New Contract Win Rate (3) | | | 93 | % | | | NA | | | | 72 | % | | | — | | | | — | | | | 49 | % | | | 67 | % | | | 74 | % | | | 73 | % |

Backlog (4) | | | NA | | | $ | 2,028 | | | $ | 2,164 | | | | NA | | | $ | 2,040 | | | | N/A | | | $ | 2,575 | | | $ | 2,040 | | | $ | 2,575 | |

| | | | | | | | | |

BALANCE SHEET DATA (5): | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Cash and Cash Equivalents | | | NA | | | $ | 4,541 | | | $ | 6,510 | | | | NA | | | $ | 13,474 | | | $ | 2,507 | | | $ | 28,589 | | | | N/A | | | | N/A | |

Working Capital (6) | | | NA | | | | 58,295 | | | | 104,335 | | | | NA | | | | 200,367 | | | | 110,636 | | | | 211,959 | | | | N/A | | | | N/A | |

Total Assets | | | NA | | | | 481,097 | | | | 579,829 | | | | NA | | | | 1,148,193 | | | | 587,835 | | | | 1,106,814 | | | | N/A | | | | N/A | |

Total Debt | | | NA | | | | — | | | | — | | | | NA | | | | 700,000 | | | | — | | | | 664,138 | | | | N/A | | | | N/A | |

Member’s Equity | | | NA | | | | 354,198 | | | | 396,573 | | | | NA | | | | 223,908 | | | | 403,514 | | | | 225,717 | | | | N/A | | | | N/A | |

Ratio of Earnings to Fixed

Charges | | | | 1.3x | | | | | |

| (1) | EBITDA is a primary component of certain covenants under our senior secured credit facility and is defined as net income (loss) before interest expense, income taxes, depreciation and amortization. EBITDA does not represent net income or cash flows from operations, as these terms are defined under generally accepted accounting principles, and should not be considered as an alternative to net income, operating income or any other performance measures derived in accordance with generally accepted accounting principles, or GAAP and EBITDA as presented in this prospectus are not necessarily comparable to similarly titled measures reported by other companies. |

12

| (2) | The following table presents a reconciliation of income to EBITDA for the periods included below. |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Original

Predecessor

Period

| | Immediate Predecessor Period

| | Successor

Period

| | | Immediate

Predecessor

Period

| | Successor

Period

| | Pro Forma for the

|

| | | March 30, 2002– March 7, 2003

| | 21 Days Ended March 28, 2003

| | Fiscal Year

Ended April 2, 2004

| | | | 49 Days

Ended

April 1,

2005

| | | Three

Months

Ended

July 2, 2004

| | Three

Months

Ended

July 1, 2005

| | Year

Ended

April 1,

2005

| | Twelve Months

Ended

July 1,

2005

|

| | | | | | April 3, 2004–

February 11, 2005

| | | | | |

| | | (dollars in thousands) |

RECONCILIATION OF NET INCOME TO EBITDA: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net Income (loss) | | $ | 18,866 | | $ | 1,229 | | $ | 31,360 | | $ | 59,733 | | $ | (922 | ) | | $ | 13,898 | | $ | 2,077 | | $ | 10,535 | | $ | 13,794 |

Income Taxes | | | 11,973 | | | 852 | | | 19,924 | | | 34,956 | | | 60 | | | | 8,577 | | | 639 | | | 6,161 | | | 7,491 |

Interest Expense | | | — | | | — | | | — | | | — | | | 8,054 | | | | — | | | 13,837 | | | 55,468 | | | 55,468 |

Depreciation and Amortization | | | 942 | | | 301 | | | 8,788 | | | 6,637 | | | 6,087 | | | | 1,992 | | | 10,894 | | | 42,166 | | | 40,632 |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

| |

|

| |

|

| |

|

| |

|

|

EBITDA | | $ | 31,781 | | $ | 2,382 | | $ | 60,072 | | $ | 101,326 | | $ | 13,279 | | | $ | 24,467 | | $ | 27,447 | | $ | 114,330 | | $ | 117,385 |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

| |

|

| |

|

| |

|

| |

|

|

| (3) | Recompete and new contract win rates are calculated based on the dollar values of such contracts. “NA” reflects no new recompeted or new contract awards during the referenced periods. |

| (4) | Backlog data is as of the end of the applicable period. |

| (5) | Balance sheet data is as of the end of the applicable period. |

| (6) | Working capital is defined as current assets, net of current liabilities. |

13

RISK FACTORS

In addition to the other information set forth in this prospectus, you should carefully consider the following factors before tendering the Original Notes in exchange for the New Notes. The following risks could materially harm our business, financial condition or future results. If that occurs, the value of the New Notes could decline, and you could lose all or part of your investment.

Risks Relating to Our Indebtedness

Servicing our indebtedness requires a significant amount of cash. Our ability to generate sufficient cash depends on numerous factors beyond our control, and we may be unable to generate sufficient cash flow to service our debt obligations, including making payments on the New Notes.

Based on our indebtedness and other obligations as of July 1, 2005, we estimate that, our remaining contractual commitments including interest associated with our indebtedness and other obligations (assuming that our revolving credit facility will be undrawn at the close of fiscal 2006) will be $53.1 million and $229 million in the aggregate, respectively, for the remaining months of fiscal 2006 and the period between April 1, 2006 through the end of fiscal 2010. Our ability to make payments on and to refinance our indebtedness, including the New Notes, depends on our ability to generate cash. This, to a certain extent, is subject to general economic, political, financial, competitive, legislative, regulatory and other factors that are beyond our control.

We cannot assure you, however, that our business will generate sufficient cash flow from operations, or that future borrowings will be available to us under our senior secured credit facility in an amount sufficient to enable us to pay our indebtedness, including the New Notes, or to fund our other liquidity needs. We may need to refinance all or a portion of our indebtedness, including these New Notes, on or before maturity. We cannot assure you that we will be able to refinance any of our indebtedness, including these New Notes or our senior secured credit facility, on commercially reasonable terms or at all. In addition, the terms of existing or future debt agreements, including our senior secured credit facility and the indenture governing our New Notes, may restrict us from carrying out any of these alternatives. If we are unable to generate sufficient cash flow or refinance our debt on favorable terms, it could significantly adversely affect our financial condition, the value of the New Notes and our ability to pay principal and interest on the New Notes.

Our cash flows and capital resources may be insufficient to make required payments on our substantial indebtedness and future indebtedness.

We have substantial indebtedness. As of July 1, 2005, we had $664.1 million of total indebtedness including the New Notes and excluding interest accrued thereon, of which $344.1 was secured. On the same date we had approximately $69.9 million of availability under our senior secured credit facility (which gives effect to $5.1 million of outstanding letters of credit). As of July 1, 2005, approximately $344.1 million of our indebtedness would have ranked senior to or, pari passu with, the New Notes, excluding $5.1 million of outstanding letters of credit. In addition, subject to restrictions in the indenture and our senior secured credit facility, we may incur additional indebtedness.

Our substantial indebtedness could have important consequences to you, including the following:

| | • | | it may be more difficult for us to satisfy our obligations with respect to the New Notes; |

| | • | | our ability to obtain additional financing for working capital, debt service requirements, general corporate or other purposes may be impaired; |

| | • | | we must use a substantial portion of our cash flow to pay interest and principal on the New Notes and other indebtedness, which will reduce the funds available to us for other purposes; |

| | • | | we are more vulnerable to economic downturns and adverse industry conditions; |

14

| | • | | our ability to capitalize on business opportunities and to react to competitive pressures and adverse changes in our industry as compared to our competitors may be compromised due to our high level of indebtedness; and |

| | • | | our ability to refinance indebtedness may be limited. |

The indenture governing the Notes, our senior secured credit facility and preferred stock contain various covenants limiting the discretion of our management in operating our business.

Our indenture, senior secured credit facility and the certificates of designation governing our parent’s preferred stock contain various restrictive covenants that limit our management’s discretion in operating our business. As more fully discussed under the captions “Description of Material Indebtedness” and “Description of Notes”, these instruments, subject to certain limited exceptions, limit our ability to, among other things:

| | • | | incur additional indebtedness or guarantee obligations; |

| | • | | repay indebtedness (including the New Notes) prior to stated maturities; |

| | • | | pay dividends or make certain other restricted payments; |

| | • | | make investments or acquisitions; |

| | • | | create liens or other encumbrances; and |

| | • | | transfer or sell certain assets or merge or consolidate with another entity. |

In addition, our senior secured credit facility also requires us to maintain certain financial ratios and limits our ability to make capital expenditures. These financial ratios include a minimum interest coverage ratio and a leverage ratio. The interest coverage ratio is the ratio of EBITDA (as defined in our senior secured credit facility) to cash interest expense for the preceding four quarters. The leverage ratio is a ratio of our debt to our EBITDA for the preceding four quarters. The minimum interest coverage ratio increases from 2:1 to 3.2:1 during the term of the senior secured credit facility. The maximum leverage ratio decreases from 6:1 to 3:1 during the term of the senior secured credit facility. The senior secured credit facility also restricts the maximum amount of our capital expenditures during each year of the term of the senior secured credit facility.

If we fail to comply with the restrictions in the indenture or our senior secured credit facility or any other subsequent financing agreements, a default may allow the creditors under the relevant instruments, in certain circumstances, to accelerate the related debt and to exercise their remedies thereunder, which will typically include the right to declare the principal amount of such debt, together with accrued and unpaid interest and other related amounts immediately due and payable, to exercise any remedies such creditors may have to foreclose on any of our assets that are subject to liens securing such debt and to terminate any commitments they had made to supply us with further funds. Moreover, any of our other debt that has a cross-default or cross-acceleration provision that would be triggered by such default or acceleration would also be subject to acceleration upon the occurrence of such default or acceleration.

In addition, the terms of our parent’s preferred stock do not allow us or our parent to incur or become subject to any indebtedness if such indebtedness would be in excess of total indebtedness permitted to be incurred under a maximum debt incurrence test, which limits our maximum indebtedness to 7.5 times EBITDA, or $881.0 million as of July 1, 2005.

Our ability to comply with these covenants may be affected by events beyond our control, and an adverse development affecting our business could require us to seek waivers or amendments of covenants, alternative or additional sources of financing or reductions in expenditures. We cannot assure you that such waivers, amendments or alternative or additional financings could be obtained, or if obtained, would be on terms acceptable to us. In addition, the holders of the New Notes will have no control over any waivers or amendments with respect to any debt or preferred stock outstanding other than the debt contained in the indenture. Therefore,

15

we cannot assure you that even if the holders of the New Notes agree to waive or amend the covenants contained in the indenture, the holders of our other debt or preferred stock will agree to do the same with respect to their debt or preferred stock instruments.

Despite our current indebtedness level, we and our subsidiaries may still be able to incur substantially more debt, which could exacerbate the risks associated with our substantial leverage.

As of July 1, 2005, we had up to $69.9 million of additional availability under our senior secured credit facility (which gives effect to $5.1 million of outstanding letters of credit). The terms of the indenture and the senior secured credit facility do not fully prohibit us or our subsidiaries from incurring additional indebtedness, and we and our subsidiaries may also be able to incur substantial additional indebtedness in the future. Any senior debt incurred by us would be senior to the New Notes and any senior debt incurred by our subsidiaries would be structurally senior to the New Notes and senior to such subsidiary’s guarantee, as applicable. If we incur any additional indebtedness that ranks equal to the New Notes, the holders of that debt will be entitled to share ratably with the holders of the New Notes in any proceeds distributed in connection with any insolvency, liquidation, reorganization, dissolution or other winding up of us. If new debt is added to our or our subsidiaries’ current debt levels, the related risks that we now face could intensify. See “Description of Material Indebtedness.”

Risks Relating to the New Notes

Your right to receive payments on the New Notes is subordinated to our existing and future senior indebtedness, and the existing and future senior indebtedness of our subsidiary guarantors, including the senior secured credit facility.

The New Notes and the subsidiary guarantees will be subordinated in right of payment to the prior payment in full of our and our subsidiary guarantors’ respective current and future senior indebtedness, including our and their obligations under our senior secured credit facility. As a result of the subordination provisions of the New Notes, in the event of the bankruptcy, liquidation or dissolution of us or any subsidiary guarantor, our assets or the assets of the applicable subsidiary guarantor would be available to pay obligations under the New Notes and our other senior subordinated obligations only after all payments had been made on our senior indebtedness or the senior indebtedness of the applicable subsidiary guarantor. As of July 1, 2005, we had approximately $344.1 million of secured indebtedness under our senior secured credit facility, and up to $69.9 million of additional availability of revolving credit under our senior secured credit facility (which gives effect to $5.1 million of outstanding letters of credit). As more fully discussed under the caption “Description of Material Indebtedness”, borrowings under our senior secured credit facility are secured by substantially all of our and our subsidiaries’ assets. In addition, we and our subsidiaries may incur certain amounts of additional secured indebtedness in the future, as permitted by the indenture and the senior secured credit facility. Sufficient assets may not remain after all of these payments have been made to make any payments on the New Notes and our other senior subordinated obligations, including payments of interest when due.

In addition, we depend on our subsidiaries for substantially all of our cash flow. Pursuant to the terms of our senior secured credit facility, certain of our subsidiaries would be prohibited from paying dividends or making other distributions to us upon the occurrence of certain events of default under the senior secured credit facility. If any of our subsidiaries is not permitted to pay us dividends or other distributions, we may not have sufficient cash to fulfill our obligations under the New Notes. For fiscal 2005 and the three months ended July 1, 2005, subsidiary guarantors provided 17.9% and 12.1% of total revenue, respectively and as of July 1, 2005, represented 13.7% of total assets. For fiscal 2005 and the three months ended July 1, 2005, our subsidiary guarantors represented 6.7% and 5.2% of the net increase in cash and cash equivalents, respectively.

16

Not all of our subsidiaries will guarantee the New Notes. The New Notes will be structurally subordinated to indebtedness and other liabilities of our non-guarantor subsidiaries.

None of our foreign subsidiaries will guarantee the New Notes. Revenues from our non-guarantor subsidiaries for the fiscal 2005, and for the three months ended July 1, 2005, were $211.3 million and $48.2 million, respectively, and 11.0% and 11.3% of our total revenues for the same periods. As of July 1, 2005, assets associated with these operations were 4.3% of our total assets. As of July 1, 2005, the non-guarantor subsidiaries have no debt outstanding to third parties.

In the event that any of the non-guarantor subsidiaries becomes insolvent, liquidates, reorganizes, dissolves or otherwise winds up, holders of their indebtedness and their trade creditors will be entitled to payment on their claims from the assets of those subsidiaries before any such subsidiary would be able to distribute any of their assets to DynCorp International or any guarantor. Consequently, your claims in respect of the New Notes are structurally subordinated to all of the existing and future indebtedness and other liabilities of the non-guarantor subsidiaries.

We may not have the ability to raise the funds necessary to finance the change of control offer required by the indenture.

Upon the occurrence of certain specific change of control events, we will be required to offer to repurchase the New Notes at 101% of the principal amount thereof plus accrued and unpaid interest, if any, to the date of repurchase. Our failure to purchase, or give notice of the purchase of, the New Notes would be a default under the indenture, which would also be a default under our senior secured credit facility. A change of control is generally defined in the indenture as:

| | • | | the direct or indirect sale, or other disposition (other than by merger or consolidation) of all or substantially all of our properties or assets to any “person” other than to Veritas or its affiliates; |

| | • | | the adoption of a plan relating to our liquidation or dissolution; |

| | • | | the consummation of any transaction (including, any merger or consolidation), that would result in a third party other than Veritas or any of its affiliates becoming the beneficial owner of more than 50% of our voting stock; |

| | • | | after an initial public offering of our common stock or the common stock of our direct or indirect parent, the first day on which a majority of the members of our Board of Directors are not “Continuing Directors”, which generally means, as of the date of determination, any member of our parent’s board of directors who was a member on the date of the indenture; or was nominated for election or elected to the board of directors with the approval of a majority of the directors that were members of such board of directors at the time of the nomination or election. |

If a change of control occurs, it is possible that we may not have sufficient assets at the time of the change of control to make the required repurchase of the New Notes or to satisfy all obligations under our senior secured credit facility and the indenture. In order to satisfy our obligations, we could seek to refinance the indebtedness under our senior secured credit facility and the indenture or obtain a waiver from the lenders or you as a holder of the New Notes. We cannot assure you that we would be able to obtain a waiver or refinance our indebtedness on terms acceptable to us, if at all.

Federal and state laws permit courts to void guarantees under certain circumstances.

The New Notes will be guaranteed by all of our domestic subsidiaries. The guarantees may be subject to review under U.S. federal bankruptcy law and comparable provisions of state fraudulent conveyance laws if a bankruptcy or reorganization case or lawsuit is commenced by or on behalf of our or one of our guarantor’s unpaid creditors. Under these laws, a court could void the obligations under the guarantee, subordinate the guarantee of the New Notes to that guarantor’s other debt or take other action detrimental to holders of the New

17

Notes and the guarantees of the New Notes, if, among other things, the guarantor, at the time it incurred the indebtedness evidenced by its guarantee:

| | • | | issued the guarantee to delay, hinder or defraud present or future creditors; |

| | • | | received less than reasonably equivalent value or fair consideration for issuing the guarantee at the time it issued the guarantee; |

| | • | | was insolvent or rendered insolvent by reason of issuing the guarantee; |

| | • | | was engaged, or about to engage, in a business or transaction for which its remaining unencumbered assets constituted unreasonably small capital to carry on its business; or |

| | • | | intended to incur, or believed that it would incur, debts beyond its ability to pay as they mature. |

The measures of insolvency for purposes of these fraudulent transfer laws will vary depending upon the law applied in any proceeding to determine whether a fraudulent transfer has occurred. Generally, however, a guarantor would be considered insolvent if:

| | • | | the sum of its debts, including contingent liabilities, was greater than the fair saleable value of all of its assets; |

| | • | | the present fair saleable value of its assets was less than the amount that would be required to pay its probable liability on its existing indebtedness, including contingent liabilities, as they become absolute and mature; or |

| | • | | it could not pay its indebtedness as it becomes due. |

We cannot be sure as to the standard that a court would use to determine whether or not a guarantor was solvent at the relevant time or, regardless of the standard that the court uses, that the issuance of the guarantees would not be voided or the guarantees would not be subordinated to the guarantors’ other debt. If such a case were to occur, the guarantee could also be subject to the claim that, since the guarantee was incurred for our benefit and only indirectly for the benefit of the guarantor, the obligations of the applicable guarantor were incurred for less than fair consideration.

We are controlled by affiliates of Veritas Capital, whose interests may not be aligned with yours.

All of the voting power of our equity is held by DIV Holdings, LLC, a subsidiary of Veritas Capital. Accordingly, Veritas Capital controls the power to elect our managers and officers, to appoint new management and to approve all actions requiring the approval of the holders of our equity, including adopting amendments to our constituent documents and approving mergers, acquisitions or sales of all or substantially all of our assets. The managers have the authority, subject to the terms of our debt, to issue additional indebtedness or equity, implement equity repurchase programs, declare dividends and make other such decisions about our equity.

In addition, the interests of our controlling equity holders could conflict with your interests. For example, if we encounter financial difficulties or are unable to pay our debts as they mature, the interests of our controlling equity holders might conflict with your interests as a note holder. Our controlling equity holders also may have an interest in pursuing acquisitions, divestitures, financings or other transactions that, in their judgment, could enhance their equity investment, even though such transactions might involve risks to you, as holders of the New Notes.

There is no existing market for the New Notes, and we do not know if one will develop that will provide you with adequate liquidity.

The New Notes will be a new class of securities for which there currently is no established market, and we cannot be sure if an active or liquid trading market will develop for these notes. The issuers do not intend to apply for listing of the New Notes on any securities exchange or on any automated dealer quotation system. The initial purchasers of the Original Notes are not obligated to make a market in the New Notes and any market-

18

making may be discontinued at any time without notice. If a market for the New Notes were to develop, the New Notes could trade at prices that may be higher or lower than reflected by their initial offering price, depending on many factors, including, among other things:

| | • | | changes in the overall market for high-yield debt securities; |

| | • | | changes in our financial performance or prospects; |

| | • | | the prospects for companies in our industry generally; |

| | • | | the number of holders of the New Notes; |

| | • | | the interest of securities dealers in making a market for the New Notes; and |

| | • | | prevailing interest rates. |

In addition, the market for non-investment-grade debt has been historically subject to disruptions that have caused substantial volatility in the prices of securities similar to the New Notes. The market for the New Notes, if any, may be subject to similar disruptions. Any such disruption could adversely affect the value of your notes.

Risks Relating to Our Business

We rely on sales to U.S. government entities. A loss of contracts with the U.S. government, a failure to obtain new contracts or a reduction of sales under existing contracts could adversely affect our operating performance and our ability to generate cash flow to fund our operations and service our debt.

For fiscal 2005 and for the three months ended July 1, 2005, the Contract Field Teams, Civilian Police and International Narcotics and Law Enforcement contracts accounted for 18.0%, 27.4%, 8.1% and 19.3%, 30.3% and 8.7% of our revenues, respectively. The loss of any one of these contracts would significantly and adversely affect our future revenues and earnings. We derived substantially all of our revenues from contracts and subcontracts with the U.S. government and its agencies, primarily the Department of Defense and the Department of State. Contracts with agencies of the Department of Defense represented 49.7%, 49.0% and 63.1% of our revenues for the three months ended July 1, 2005, and for fiscal 2005 and 2004, respectively, and contracts with agencies of the Department of State represented 48.6%, 49.6% and 29.4% of our revenues over the same respective periods. The remainder of revenues represent commercial contracts, including contracts in which we serve as subcontractor to other contractors with U.S. government. We expect that U.S. government contracts, particularly with the Department of Defense and the Department of State, will continue to be our primary source of revenue for the foreseeable future. Continuation and renewal of our existing government contracts and new government contracts are, among other things, contingent upon the availability of adequate funding for various U.S. government agencies, including the Department of Defense and the Department of State. Changes in federal government spending could directly affect our operating performance and, as a result, we may not generate sufficient cash flow to satisfy our debt obligations, including the New Notes. Among the factors that could impact federal government spending and which would reduce our federal government contracting business are:

| | • | | a significant decline in, or reapportioning of, spending by the federal government, in general, or by the Department of Defense or the Department of State, in particular; |

| | • | | changes, delays or cancellations of U.S. government programs or requirements; |

| | • | | the adoption of new laws or regulations that affect companies that provide services to the federal government; |

| | • | | U.S. government shutdowns or other delays in the government appropriations process; |

| | • | | curtailment of the federal government’s outsourcing of services to private contractors; |

| | • | | changes in the political climate, including with regard to the funding or operation of the services we provide; and |

| | • | | general economic conditions. |

19