Exhibit 99.4

JAGUAR MINING INC.

Annual Information Form

for the year ended December 31, 2008

Dated February 11, 2009

TABLE OF CONTENTS

| CAUTIONARY NOTE REGARDING FORWARD LOOKING STATEMENTS | | | 3 | |

| CORPORATE STRUCTURE | | | 4 | |

| GENERAL DEVELOPMENT OF THE BUSINESS | | | 5 | |

| DESCRIPTION OF THE BUSINESS | | | 14 | |

| JAGUAR GOLD OPERATIONS AND PROJECTS | | | 20 | |

| RISK FACTORS | | | 73 | |

| DIVIDENDS | | | 79 | |

| DESCRIPTION OF CAPITAL STRUCTURE | | | 80 | |

| MARKET FOR SECURITIES | | | 81 | |

| DIRECTORS AND EXECUTIVE OFFICERS | | | 83 | |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | | | 88 | |

| TRANSFER AGENTS AND REGISTRAR | | | 89 | |

| MATERIAL CONTRACTS | | | 90 | |

| INTERESTS OF EXPERTS | | | 91 | |

| ADDITIONAL INFORMATION | | | 92 | |

| APPENDIX A CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS | | | 93 | |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain information contained herein and in the documents incorporated by reference herein constitutes forward-looking statements. Forward-looking statements are frequently characterized by words such as “plan”, “goal”, “strategy”, “budget”, “estimates”, “schedule”, “expect”, “project”, “intend”, “believe”, “anticipate” and other similar words, or statements that certain events or conditions “may”, “could”, “might”, or “will” occur. Statements relating to “mineral reserves” or “mineral resources” are deemed to be forward-looking statements, as they involve the implied assessment, based on certain estimates and assumptions, that the mineral reserves and mineral resources described can be profitably produced in the future. Forward-looking statements are based on the opinions and estimates of management at the date the statements are made, and are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking statements. These factors include the inherent risks involved in the exploration and development of mineral properties, the uncertainties involved in interpreting drilling results and other ecological data, fluctuating metal prices, the possibility of project cost overruns or unanticipated costs and expenses, uncertainties relating to the availability and costs of financing needed in the future, political risks and other factors described in this annual information form under the heading “Risk Factors”.

Actual results and developments are likely to differ, and may differ materially, from those expressed or implied by the forward-looking statements contained in this annual information form. Such statements are based on a number of assumptions which may prove to be incorrect, including, but not limited to, the following assumptions: that there is no material deterioration in general business and economic conditions; that there is no unanticipated fluctuation of interest rates and foreign currency exchange rates; that the supply and demand for, deliveries of, and the level and volatility of prices of gold as well as oil and petroleum products develop as expected; that Jaguar receives regulatory and governmental approvals for its development projects and other operations on a timely basis; that Jaguar is able to obtain financing for its development projects on reasonable terms; that there is no unforeseen deterioration in Jaguar’s costs of production or Jaguar’s production and productivity levels; that Jaguar is able to procure mining equipment and operating supplies in sufficient quantities and on a timely basis; that engineering and construction timetables and capital costs for Jaguar’s development and expansion projects are not incorrectly estimated or affected by unforeseen circumstances; that costs of closure of various operations are accurately estimated; that unforeseen changes to the political stability or government regulation in the country in which Jaguar operates do not occur; that there are no unanticipated changes to market competition, that Jaguar’s reserve estimates are within reasonable bounds of accuracy (including with respect to size, grade and recoverability) and that the geological, operational and price assumptions on which these are based are reasonable; that Jaguar realizes expected premiums over London Metal Exchange cash and other benchmark prices; and that Jaguar maintains its ongoing relations with its employees and business partners and joint venturers; as well as those risk factors set out in this annual information form.

All of the forward-looking information in this annual information form, and the documents incorporated by reference herein, is qualified by these cautionary statements. Forward-looking information contained herein is made as of the date of this annual information form and Jaguar disclaims any obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. There can be no assurance that the forward-looking information will prove to be accurate as actual results and future events could differ materially from those anticipated in making such statements containing forward-looking information. Accordingly, readers should not place undue reliance on forward-looking information.

CORPORATE STRUCTURE

Jaguar Mining Inc. (“Jaguar”) was incorporated on March 1, 2002 pursuant to the Business Corporations Act (New Brunswick). On March 30, 2002, Jaguar issued initial common shares to Brazilian Resources, Inc. (“Brazilian”) and IMS Empreendimentos Ltda. (“IMS”) in exchange for property. In that transaction, Brazilian contributed to Jaguar all of the issued and outstanding shares in Mineração Serras do Oeste Ltda. (“MSOL”), a Brazilian mining company that controlled the mineral rights, concessions and licenses to certain property located near the community of Sabará, east of Belo Horizonte in the state of Minas Gerais, Brazil (the “Sabará Property”), and IMS contributed to Jaguar a 1,000-tonne per day production facility located near the community of Caeté east of Belo Horizonte in the state of Minas Gerais, Brazil (the “Caeté Plant”) and the mineral rights to a nearby property related to National Department of Mineral Production (“DNPM”) Mineral Exploration Request no. 831.264/87 and DNPM Mineral Exploration Request nos. 830.590/83 and 830.592/83 (the “Rio de Peixe Property”). Jaguar was continued into Ontario in October 2003 pursuant to the Business Corporations Act (Ontario) and is currently a corporation existing under the laws of Ontario. Jaguar’s head office is located at 125 North State Street, Concord, New Hampshire (USA) 03301, and its registered office is located at 1 First Canadian Place, 100 King Street West, Suite 4400, Box 63, Toronto, Ontario, Canada M5X 1B1.

On October 9, 2003, pursuant to an amalgamation agreement dated July 16, 2003, Jaguar amalgamated with Rainbow Gold Ltd. (“Rainbow”), a New Brunswick corporation and a then inactive reporting issuer listed on the TSX Venture Exchange (the “TSX-V”), through a reverse take-over. Each shareholder of Rainbow received one common share of Jaguar (a “Common Share”) for every 14 common shares of Rainbow owned. The amalgamated entity adopted the name “Jaguar Mining Inc.” Jaguar was approved for listing on the TSX-V on October 14, 2003 and began trading on October 16, 2003. Jaguar subsequently graduated from the TSX-V to the Toronto Stock Exchange (the “TSX”) and began trading on the TSX on February 17, 2004 under the symbol “JAG”. On July 23, 2007, trading of Jaguar’s common shares commenced on the NYSE Arca Exchange (“NYSE Arca”) under the symbol “JAG”.

Jaguar has two wholly-owned direct subsidiaries, MSOL and Mineração Turmalina Ltda. (“MTL”), both incorporated under the laws of the Republic of Brazil. The registered and head office of each of MSOL and MTL is located at Rua Fernandes Tourinho, 487, 7th Floor, Bairro Savassi, Belo Horizonte, Minas Gerais, CEP 30.112-000, Brazil.

GENERAL DEVELOPMENT OF THE BUSINESS

Corporate History

In 2001, the principals of Brazilian and IMS recognized that an opportunity existed to create a mid-sized gold producer in the Quadrilátero Ferrífero (“Iron Quadrangle”) region of Brazil by acquiring various late-stage gold exploration properties with existing resources and relatively new plant and equipment, at prices reflecting the comparatively distressed state of the gold mining industry at that time. Gold prices were depressed compared to historical levels and, for different reasons, Mineração AngloGold Ltda., a subsidiary of AngloGold Ashanti Limited (“AngloGold Ashanti”), Vale (or Companhia Vale do Rio Doce until 2007) and Rio Tinto Desenvolvimentos Minerais Ltda. (“RTZ”) were all contemplating the rationalization of their gold property and equipment portfolios. Brazilian and IMS believed that no junior mining companies operating in the region were in a strong enough financial condition to broadly negotiate to acquire the available properties.

Mining Exploration, Production History and Corporate Transactions

Mining Properties Generally

Jaguar’s properties, except for the Pedra Branca Project, are located in or adjacent to the Iron Quadrangle region of Brazil, a greenstone belt located east of the city of Belo Horizonte in the state of Minas Gerais. Jaguar has three operations currently in production, located at the Turmalina, Paciência and Sabará properties, respectively. In addition, Jaguar has one property under development: the Caeté Project. Jaguar has also entered into a joint venture agreement with Xstrata plc. (“Xstrata”) to explore the Pedra Branca Project in northeastern Brazil, as further described under “Pedra Branca Project”, below.

Jaguar commissioned TechnoMine Services, LLC (“TechnoMine”) and Scott Wilson Roscoe Postle Associates Inc. (formerly Roscoe Postle Associates Inc.) (“Scott Wilson RPA”) to prepare technical reports in accordance with National Instrument 43-101 Standards of Disclosure for Mineral Properties (“NI 43-101”) to set forth the mineral resources and reserves of all Jaguar’s concessions in the Iron Quadrangle. All of the NI 43-101 compliant technical reports prepared on behalf of Jaguar can be found at www.sedar.com. The Scott Wilson RPA technical reports referred to herein have been updated and superseded by technical reports prepared by TechnoMine, except with respect to Ore Body B on the Turmalina property, and as such are no longer current.

Additional information regarding each property is set forth below.

Turmalina

On September 30, 2004, Jaguar acquired MTL and the 13,183 acre Turmalina gold project located in Minas Gerais, Brazil from AngloGold Ashanti. Jaguar, through MSOL, agreed to pay US$1.35 million over three years for 100 percent ownership and operational control of the Turmalina concessions, which amount has been paid in full.

The Turmalina concessions are subject to a participation interest as follows: (i) for production obtained as a result of washing of dragline-mined placers, open pit hydraulic mining or other similar method, MSOL shall pay a royalty to AngloGold Ashanti equal to (a) ten percent of annual net revenue up to US$500,000, (b) five percent of annual net revenue between US$500,000 and US$1,000,000, and (c) two and a half percent of annual net revenue over US$1,000,000; and (ii) for production obtained as a result of in situ mineral reserves, in fresh or altered rocks, via underground or open pit mining, MSOL shall pay a royalty to AngloGold Ashanti equal to (a) two percent of net revenue for the first six operational months, (b) two percent of net revenue during the 7th through 48th operational months (however, at least US$200,000 shall be paid every twelve months after the seventh month of production), (c) five percent after the first four years of production sale up to and including US$10,000,000, and (d) three percent after the first four years of production sale in excess of US$10,000,000.

During 2006, Jaguar completed a feasibility study on Turmalina and commissioned Scott Wilson RPA to audit it and issue a technical report in compliance with NI 43-101. Scott Wilson RPA issued its report on September 16, 2005, revised it on March 10, 2006, supplemented it on March 14, 2006 and, upon the completion of Phase II of the Turmalina exploration program in the Main and Northeast Targets (Ore Bodies A and B, respectively), further updated the report on July 31, 2006.

Commissioning at Turmalina began in November 2006 and the first gold pour was conducted in January 2007. Turmalina is an underground mine utilizing the "sublevel stoping" and the "cut and fill" mining methods with paste fill. Turmalina is currently processing 1,300 tonnes per day of ore in the carbon-in-pulp ("CIP") plant.

Additional exploration efforts by Jaguar in the area surrounding Ore Bodies A and B have led to the discovery of a third mineralized area, referred to as the Satinoco Target, where three new areas of mineralization have been identified. The Satinoco Target is located approximately 300 meters from Ore Body A at the Turmalina Mine.

Jaguar initially completed a two-phase diamond drilling program at the Satinoco Target and commissioned TechnoMine to prepare a resource estimate technical report. A technical report was issued in October 2007, based on exploration data achieved until July 2007. Jaguar completed an additional, Phase III exploration campaign in December 2007. The results generated during Phase III program were integrated to the previous exploration database and gave rise to a re-evaluation of the Satinoco Target resource base. In February 2008, Jaguar filed a technical report in accordance with NI 43-101 in connection with the upgrade of inferred to measured and indicated resources at the Satinoco Target.

During the fourth quarter of 2007, Jaguar completed the underground crosscut to access the Satinoco mineralization through the existing ramp developed by Jaguar to mine Ore Bodies A and B at Turmalina. The crosscut will be utilized to transport ore from the Satinoco Target out the Turmalina Mine entrance. During the excavation process of the crosscut to the Satinoco Target, economic grades of gold were discovered in channel samples. During 2008, Jaguar conducted a complementary 12,000 meter in-fill diamond drill program as part of the feasibility work in an effort to convert resources to reserves to expand Turmalina’s operation.

In September 2008, TechnoMine completed the NI 43-101 compliant feasibility study technical report on the Turmalina Phase I expansion, which converted the Satinoco mineral resources to reserves. Jaguar expects this will be the first of a planned three-phase expansion program at the Turmalina operations. The Phase I expansion is expected to increase Turmalina production by 25% from its present design rate of approximately 80,000 ounces per year to 100,000 ounces per year. Jaguar expects to complete the Phase I expansion by the third quarter of 2009.

Jaguar’s reported mineral resources for Turmalina are to a depth of approximately 500 meters where the mineralized structure is open at depth and along strike. As part of a recent drill program to prove the continuity of the mineralization at Ore Body A to a depth of over 800 meters, Jaguar drilled four holes to depths ranging from 850 meters to 1,100 meters. Two of these drill holes intersected the mineralized structure in the Ore Body A to a depth of approximately 800 meters. A grade of approximately seven grams per tonne was encountered in a narrow zone at depth thereby confirming the extension of the mineralized structure. Jaguar’s team believes the size of the mineralized structure and mineralization is similar to the existing reserve base in this ore body to the depth of 500 meters. This is also consistent with the characteristics of other gold mines in the Iron Quadrangle, some of which have operated to depths of 2,400 meters. Jaguar intends to update the inferred resources category at Turmalina using the information from these recent drill results but does not have any plans to conduct further deep drilling at Turmalina at this time.

As part of the surface exploration to estimate resource potential in a newly discovered oxide zone at Ore Body B, several trenches were opened in the outcropping to expose and sample the mineralized zone. Channel samples revealed two separate mineralized areas with average surface grades ranging from 3 grams per tonne to 5 grams per tonne. Jaguar’s team intends to update the geological model to incorporate this new data into the overall mine model. The oxide ore from this new zone would be blended with sulfide ore and processed through Turmalina Plant, providing immediate additional lower cost ore.

At the Satinoco Target (Ore Body C) and Satinoco Extension (Zone D), additional gold bearing oxide ore has been identified in the weathered rock above the sulfide zone, as well as within the sulfide zone. During 2008, 11,698 meters of drilling for a total of 62 drill holes were drilled in the Satinoco structure to estimate oxide and sulfide mineral resources. Jaguar expects to complete the resource estimate by the third quarter of 2009.

Jaguar has also discovered a new target at the Turmalina mining complex, the Fazenda Experimental Target, which management believes has significant potential and is unrelated to the mineralized on-strike zone associated with Ore Bodies A, B and C and Zone D. The Fazenda Experimental Target is located in a structure parallel to the existing ore bodies and zones, where historic mining work at shallow depths can be seen, approximately 5 kilometers from the Turmalina Plant. Jaguar has conducted limited soil sampling, trenching and other geo-chemical work in the area over the past two years.

During the third quarter of 2008, four drill holes in 716 meters were carried out, which entailed 200 meters along strike. Three drill holes intercepted mineralized structures. Intersection grades varied from 2.9 grams per tonne to 6.5 grams per tonne at intervals of 3 meters or less. Additional trenching has provided evidence that the continuity near the surface extends well beyond areas where no drilling has taken place.

During 2009, Jaguar intends to conduct additional underground exploration as part of the forward development of Turmalina’s Ore Bodies A, B and C, as well as in Zone D and at the Fazenda Experimental Target to increase resources with the objective of generating reserves to further expand Turmalina’s annual production beyond the current plan of 100,000 ounces.

Paciência

In November 2003, Jaguar acquired the Paciência concessions from AngloGold Ashanti.

In March 2004, TechnoMine completed an NI 43-101 technical report on its Iron Quadrangle properties, which included the Paciência/Santa Isabel Mine resources. This technical report was revised in September 2004 and further revised in December 2004.

In 2005, Jaguar acquired rights from IAMGold with respect to properties located on approximately 2,307 acres in the aggregate in Rio Acima and Itabirito, Brazil. These concessions, known as the Conglomerates, represent an opportunity for Jaguar to eventually further explore, upgrade and expand Paciência’s aggregate mineral resources and overall production. Since 2007, Jaguar has been conducting exploration work at the Conglomerates as detailed below.

During 2007, Jaguar successfully concluded a land swap agreement with another gold producer whereby Jaguar expanded the concession package at the Paciência mining complex to a contiguous 20 kilometers area adjacent to the São Vicente lineament. This land area was first mined in the 17th century by the Portuguese and the old works are highly visible, even from satellite photography. Jaguar’s exploration efforts today are along this same strike at depths deeper than the Portuguese could access without modern mining equipment.

In August 2007, TechnoMine completed an NI 43-101 compliant feasibility study for the Paciência Project Santa Isabel Mine and processing plant.

Construction of the CIP processing plant began immediately after the completion of the feasibility study. Mining operations at the Santa Isabel Mine commenced in April 2008 as the new Paciência Plant entered the commissioning phase. Jaguar uses the cut-and-fill mining method at the Santa Isabel Mine.

Commissioning of the Paciência operation was interrupted late in the second quarter of 2008 to repair a seam in the tailings pond liner which was improperly installed by a contractor. During the initial charging and testing of the tailings facility, a leak was detected by sub-surface monitors and ramp-up was delayed. There was no discharge from the tailings pond. It took approximately four weeks to properly repair and test the affected portion of the liner. Commissioning operations at Paciência resumed in July 2008.

On July 24, 2008, Paciência reported its first gold pour and operations were deemed commercial during the latter part of the fourth quarter of 2008 based on throughput rates.

During 2008, Jaguar conducted extensive underground development and exploration activities at the NW01 Target (Marzagão) and the Conglomerates Target (Palmital) to add additional tonnes vertically as well as horizontally in an effort to increase the resource base for the Paciência operation. As part of the exploration effort at these two targets, a total of 9,152 meters was drilled in 42 drill holes during 2008.

Grades observed at the NW01 Target are similar to those observed at the Santa Isabel Mine. The main access ramp, which is 4 meter x 5 meter in size, was completed early in 2008. A total of 1,191 meters in ramp and drifts have been developed toward the Santa Isabel Mine located 2 kilometers to the south of the NW01 portal. This cross cut will eventually intersect the second level of the Santa Isabel Mine. During this development, two new mineralized zones were encountered. Channel samples were taken and Jaguar decided to develop a drift across the zone. Jaguar’s management believes blind ore shoots likely exist along the 20-kilometer contiguous concession base. By extending the ramp to the second level of the Santa Isabel Mine, Jaguar’s management believes the tonnes per vertical meter that will be identified over the 2 kilometers will rise.

The mineralized zones are partially exposed, with approximately 30 meters in length and 1 meter to 3 meters in width. Channel sampling in this area gave rise to grades ranging from 1 gram per tonne to 10 grams per tonne. The extension is open towards the North West and laterally towards the North East. Surface drill holes at the drift level indicate the presence of an additional mineralized zone. A drill hole from the area had an unusually high amount of “free” gold and a grade of 595 grams per tonne over 0.7 meter. The shape and other characteristics of this structure suggest that other mineralized zones might be located in the vicinity of the NW01 Target. Two surface rigs are presently drilling in the South East extension of the drift with the objective of intercepting these new zones.

A second zone of mineralization at Paciência, not related to the São Vicente lineament where Jaguar has a resource and reserve base, is referred to as the Conglomerates Target. The zone entails several concessions, which are located approximately 12 kilometers east of the Paciência processing plant. The property’s previous owners, the Anschutz Group and Western Mining, carried out exploration campaigns between 1985 and 1990, which included underground development and channel sampling, surface and underground diamond drilling and geological mapping. Based on their efforts, a pre NI 43-101 gold resource of approximately 110,000 ounces was estimated.

In order to estimate the resources held in the Conglomerates Target consistent with NI 43-101 standards, Jaguar conducted a 7,191 meter in-fill drilling program inside this target zone that consisted of 30 drill holes. Jaguar also opened a portal into the host rock and developed 60 meters of a 4 meter x 5 meter ramp, which was concrete lined. During 2008, Jaguar carried out 1,306 meters of ramp and drifts to reach mining areas Level I and Level II.

At Level I, the conglomerate layer was identified to extend over 100 meters, confirming the grades and widths obtained through surface drilling. At the exposed section, the mineralized conglomerate shows thicknesses that vary from less than 1 meter to 2.5 meters and grades of up to 200 grams per tonne. Partial channel results in the drift already defined a mineralized zone with an average grade of 6.8 grams per tonne over a 150 m2 conglomerate layer area.

The development of exploration drifts in Level I will continue to laterally expose the conglomerate layer. Through additional drilling, Jaguar’s team expects to estimate the resource potential in one known 300-meter section and trace the geometry of the conglomerate reef to depth. Jaguar is currently developing a new resource estimate and views this new geological setting as additional feed for the Paciência processing plant.

At Level II, further underground development is being carried out to provide access to the mineralized zone for further in-fill drilling.

Sabará

In 2003, Jaguar commissioned TechnoMine to produce studies of its Sabará property. Jaguar filed a feasibility study on the Zone B Mine of the Sabará property on SEDAR on June 30, 2003 and filed a revised study on January 28, 2004, both of which can be found at http://www.sedar.com.

In July 2003, Jaguar commenced pre-mining operations at the Sabará Zone B Mine. In December 2003, Jaguar began pouring gold from the Sabará Zone B Mine at the Caeté Plant. Mining operations at the Sabará Zone B Mine concluded in the fourth quarter of 2005.

MSOL and AngloGold Ashanti owned adjacent properties, known together as Lamego, in the Sabará property area of the Iron Quadrangle region in Brazil. On November 21, 2003, MSOL entered into an agreement with an AngloGold Ashanti subsidiary, Mineração Morro Velho Ltda. (“Morro Velho”) regarding exploration at the adjacent properties. AngloGold Ashanti applied for concession of mining rights for sulfide mineral resources on its property, and MSOL received concessions for oxide mineral resources on its property. Through Morro Velho, AngloGold Ashanti granted to MSOL the right to explore for oxide resources on AngloGold Ashanti’s Lamego property, and in exchange MSOL granted to AngloGold Ashanti the right to explore for sulfide resources on MSOL’s Lamego property. On November 21, 2007, Jaguar and AngloGold Ashanti entered into an agreement, pursuant to which Jaguar transferred its interests in the Lamego property (valued at US$8,060,560) to AngloGold Ashanti in consideration of (i) satisfaction of the US$350,000 note payable related to the purchase of quota shares of MTL, (ii) elimination of US$153,960 payable in connection with leaching services provided by AngloGold Ashanti, and (iii) a reduction in future net smelter royalty payments for the Paciência Mine equal to US$7,556,600 (net smelter royalty payments are generally due on a monthly basis on a sliding scale from 1.5% to 4.5% on gross revenues from gold produced, the percentage of such royalty being determined based on the US$ price of gold at a given time).

In January 2005, Jaguar completed a feasibility study on the remaining gold oxides at Sabará, which included Zones A and B and Lamego, and commissioned Scott Wilson RPA to audit the feasibility study and issue a technical report in accordance with NI 43-101. Scott Wilson RPA’s report was issued on February 17, 2006 and can be found at http://www.sedar.com.

In December 2005, Jaguar began crushing ore from Zone A at its new gold oxide heap leach facility and recovery plant at Sabará (the “Sabará Plant”).

During the third quarter of 2007, Jaguar concluded drilling activities at the Serra Paraíso Target, an oxide zone near the Sabará mining and processing complex. After carrying out metallurgical recovery tests and completing its analysis of the Serra Paraíso Target drill program, Jaguar initiated stripping operations at the Serra Paraíso mineralized zone and is now moving its ore to the Sabará Plant. Management is currently reducing mining operations in the Zone A Mine in favor of higher grade ore from the Serra Paraíso Target.

In order to add oxide resources to feed the Sabará Plant and thereby increase its mine life, Jaguar developed an exploration program at its Sabará and Caeté properties in a 15,000 hectare area. In addition to the Serra Paraíso Target mentioned above, Jaguar is conducting channel sampling, soil geochemistry and trenching at three different targets near the Sabará operations. Preliminary results of such exploration identified new targets, which have given rise to a drill program that began in the first quarter of 2009.

Caeté Project

The Caeté Project consists of two main targets, the Roça Grande Target and the Pilar Target.

In November 2005, Jaguar entered into a mutual exploration and option agreement with Vale for the Roça Grande Target with respect to seven concessions located on 9,500 acres of highly prospective gold properties along 25 kilometers of a key geological trend in the Iron Quadrangle. The contract between Jaguar and Vale provided Jaguar with the exclusive right over a twenty-eight month period beginning November 28, 2005 to explore and conduct feasibility studies and to acquire gold mining rights in the Vale properties if the studies supported economical mining operations. The contract granted corresponding rights for Vale to explore the Jaguar property for iron and acquire mineral rights in the property during a three-year period. In November 2007, Jaguar notified Vale of its intent to exercise the option to acquire all seven Roça Grande concessions. The legal procedures necessary to execute the final transfer agreement in connection with the acquisition of the Roça Grande concessions started in 2008 and are expected to conclude by the second quarter of 2009.

Jaguar has been exploring its Pilar Target since 2006 and initially contemplated building a sulfide plant on site, but the acquisition of the Roça Grande Target created an opportunity to develop a project with greater plant capacity to receive ore from several mineral properties. Jaguar contemplates mining underground non-refractory sulfide ore at the Pilar Target and truck the ore for processing at the expanded Caeté Plant, which will also process sulfide ore from the Roça Grande Target.

During 2007, a number of key events occurred with respect to the expansion of the Caeté Project, including:

| | • | Jaguar commissioned TechnoMine to prepare technical studies with respect to the expansion, |

| | • | TechnoMine completed a scoping study on the Caeté Project, |

| | • | Jaguar received the Implementation License (LI) for the Caeté Project, |

| | • | Jaguar secured the power contract for a 2009 start-up of the Caeté Project, and |

| | • | TechnoMine completed an NI 43-101 technical report on the Caeté Project resources. |

In September 2008, expansion plans at the Caeté Project continued as TechnoMine completed the NI 43-101 feasibility study technical report. Based on the feasibility study, processing facilities will include crushing and grinding circuits followed by a gravity separation circuit along with a leaching and CIP-ADR (carbon-in-pulp adsorption/desorption/recovery) plant, which will process the sulfide ore from Pilar, Roça Grande, and other nearby targets. This new plant is expected to utilize much of the existing infrastructure of the previously closed Caeté heap leach and carbon-in-column (“CIC”) facility. Jaguar intends to use a combination of "cut and fill" and "selective stoping" methods at both mines, which contemplates a treated tailings backfill system.

By the end of the third quarter in 2008 all necessary permits and licenses for the construction and commissioning phase had been received and Jaguar initiated civil works for the milling and treatment circuits.

However, in November 2008, due to the retraction in gold prices, financial markets and worldwide equity values, including the gold sector, Jaguar temporarily suspended development of the Caeté Project pending an assessment of market conditions and the availability of capital to move the project forward.

Consistent with the decision to suspend the development of the Caeté Project, underground work at the Roça Grande Target has been temporarily suspended; however, development at the Pilar Mine continued. Beginning in December 2008, Jaguar began transporting ore by truck from the Pilar Mine to the Paciência processing plant to supplement the ore being supplied from Paciência’s Santa Isabel Mine. Jaguar expects to continue this practice until such time as the ore from the Pilar Mine would be needed at the future Caeté processing plant.

As part of Jaguar’s effort to identify and add to the estimated gold resources reported in the November 2007 technical report, 75,000 meters of additional drilling are planned over the next five years in the mineral properties identified to supply the Caeté Plant.

During 2008, Jaguar completed 31,501 meters of drilling for a total of 92 drill holes in the exploration concessions that are part of the Caeté Project mining complex.

Pedra Branca Project

In March 2007, Jaguar entered into a joint venture agreement with Xstrata to explore the Pedra Branca gold project (the “Pedra Branca Project”) in the State of Ceará in northern Brazil (the “Joint Venture Agreement”). Under the Joint Venture Agreement, a new company or companies will be formed to mine economic gold deposits. Jaguar shall pay an aggregate fee of US$150,000 over a two year period in exchange for an option to hold a 51 percent ownership interest in the new company or companies by investing an aggregate of US$3.85 million in exploration expenditures within the next four years. Jaguar is subject to annual exploration expenditure targets for each year in which it maintains such option. Furthermore, Jaguar may increase its ownership interest in certain gold deposits to 60 percent through an additional investment of US$3 million by the fifth anniversary of the Joint Venture Agreement, subject to the rights of Xstrata to return to their 49 percent interest through additional contributions to the joint venture for certain properties which have gold deposits of two million ounces or more. Certain properties within the Pedra Branca Project that are dominated by base metal deposits, or which have gold deposits of less than one million ounces, may be held in different ownership percentages and be subject to different conditions, or removed from the joint venture.

The Pedra Branca Project has mineral rights to 37 concessions totaling approximately 159,000 acres in a 65-kilometer shear zone. The concessions are located in and around municipal areas with good infrastructure.

Xstrata carried out a preliminary exploration program that covered only 25 kilometers of the shear zone. The program identified 10 kilometers of soil anomalies, including two large anomalies referred to as Coelho and Mirador targets. For the most part, the mineralized formations uncovered by Xstrata’s preliminary efforts are open along the extremity and lead both companies’ geologists to believe the area has significant potential for gold mineralization, which could include the presence of both oxide and sulfide formations in large structures.

Jaguar is currently conducting a comprehensive exploration program at the Pedra Branca Project, including extensive geological mapping, drainage and soil geochemistry, detailing of zones with anomalies, trenching and diamond drilling. During the third quarter of 2007, Jaguar began a diamond drill program to test the continuity of the mineralization at depth. To date, 57 drill holes totaling 5,561 meters have been completed.

Contracts with AngloGold Ashanti

On November 21, 2003, MSOL entered an agreement with AngloGold Ashanti’s subsidiary, Morro Velho, pursuant to which MSOL is provided with certain ore treatment services at the Queiróz plant of AngloGold Ashanti ("Queiróz Plant"), gold refining services and marketing services. The treatment operations began in the first quarter of 2006. MSOL agreed to deliver for treatment a certain number of metric tons of gold each year for four years starting in January 2006 and ending in 2009. If AngloGold Ashanti fails to treat the scheduled amount of ore, it will pay a penalty to MSOL. AngloGold Ashanti will provide gold refining services and each year will refine the amount of gold agreed upon by the parties by December 30th of the preceding year. AngloGold Ashanti further agreed to market MSOL’s gold. As a fee for the refining and marketing aspects of the contract, MSOL will pay one percent of the gross income from sales resulting from the refining and marketing services. The agreement is in effect with respect to the treatment services until December 31, 2009, and with respect to the refining and marketing services until 2017, or a previous date if the sources of natural resources are exhausted. MSOL may terminate the agreement if it determines through a mineral survey that the exploitation of certain specified deposits is not feasible. In January 2007, Jaguar notified AngloGold Ashanti that it elected not to exercise its rights to process non-refractory ore at the Queiróz Plant. This decision was based on an internal assessment of other production alternatives, which Jaguar has determined should generate a greater level of profitability in the future by processing available ore through a Jaguar-owned facility.

On November 21, 2003, Jaguar acquired its Paciência, Catita, Juca Vieira (Catita II), Bahú, Marzagão, Camará and Morro do Adão properties in the Iron Quadrangle region from AngloGold Ashanti. Under the terms of such transaction, AngloGold Ashanti has the right, following exhaustion of the reserves developed from the known resources at the Paciência, Juca Vieira, Catita, Bahú, Marzagão, Camará and Morro do Adão properties, to develop a full valuation of any of such properties, including drilling works. If the valuation identifies the existence, in one or more areas, of measured and indicated resources of a minimum of 750,000 ounces, AngloGold Ashanti will have the right to reacquire up to 70 percent of any of such properties at an ascribed value of US$10.50 per ounce of the new measured and indicated resources.

AngloGold Ashanti’s rights pertain to only three of the twelve concessions at Jaguar’s Paciência property (Paciência, Bahú and Marzagão) and four concessions at the Sabará property (Catita, Catita II, Camará and Morro do Adão). The mineralization potential at Sabará is not considered substantial. These seven concessions represent only 16% of the hectares of Jaguar’s concession base in Minas Gerais. At this time, none of Jaguar’s resources, operations and projections for the next five years are impacted by this provision nor expected to be in the next several years.

Laboratory

During the third quarter of 2005, Jaguar began construction of its own testing laboratory adjacent to the Caeté Plant. The laboratory was completed and became operational in the fourth quarter of 2005. Jaguar’s on-site testing laboratory expedites process control and certain exploration testing and alleviates some of the delays experienced by excessive demand on the independent laboratories due to surging mining activity. Jaguar also utilizes the services of a local, independent laboratory.

Corporate Transactions

On December 20, 2005, MTL obtained a secured financing facility from RMB International (“RMB”) in an amount of up to US$14,000,000 (the “Turmalina Facility”) which was used primarily to finance the construction and start-up of the Turmalina Mine. In connection with the Turmalina Facility, (i) MTL and MSOL provided security interests in the cash flow, equipment and other assets of Turmalina and Sabará operations and a pledge, (ii) Jaguar issued a guaranty of MTL’s obligations under the Turmalina Facility, and (iii) Jaguar issued 1,093,835 unlisted warrants to the Turmalina Facility lenders (which had an exercise price of Cdn.$4.50 and an expiry date between June 30, 2009 and March 31, 2010 have all been exercised), 350,000 listed warrants to the lenders’ agent (all of such warrants were exercised at a price of Cdn.$4.50), and 300,000 unlisted warrants to Auramet Trading, LLC in its capacity as an advisor to Jaguar with respect to the Turmalina Facility (all of such warrants were exercised at a price of Cdn.$3.90), in each case with each warrant entitling the holder to purchase one common share of Jaguar. In the fourth quarter of 2005, Jaguar entered into a forward sales contract agreement with the lender under the Turmalina Facility to implement a risk management strategy to manage commodity price exposure on gold sales. In September 2007, Jaguar received an amendment to the loan facility agreement from RMB, which allowed Jaguar to close the forward sales contracts. In March 2008, Jaguar paid RMB US$9.8 million plus US$181,000 accrued interest to repay the Turmalina Facility agreement in full, paid RMB US$22.1 million to close the forward sales contracts and closed the forward purchase contracts realizing a gain of US$7.4 million, thereby effectively reducing the net loss of the forward contracts to US$14.8 million (of which US$14.5 million was accrued as of December 31, 2007). No additional charges were realized during 2008 for the forward contracts.

On March 27, 2006, Jaguar completed a public offering in Canada and private placement offering in the United States of 10,100,000 common shares at a price of Cdn.$5.25 pursuant to an Underwriting Agreement dated March 9, 2006 among Jaguar and Blackmont Capital Inc. (“BCI”), BMO Nesbitt Burns Inc. (“BMO”), RBC Dominion Securities Inc. (“RBC”), TD Securities Inc. (“TD Securities”) and Paradigm Capital Inc. as underwriters. The underwriters received a cash commission equal to 5.5 percent of the gross proceeds of the offering, underwriter options to purchase up to 1,335,000 common shares at a price of Cdn.$5.25, which they exercised at the closing on March 27, 2006, and compensation warrants to purchase up to 343,050 common shares at a price of Cdn.$5.25 with an expiry date of March 27, 2008. As of January 31, 2008, 198,969 common shares were purchased as a result of the exercise of such compensation warrants.

On February 1, 2007, Jaguar’s Board of Directors adopted a shareholder rights plan (the “Shareholder Rights Plan”) which is intended to ensure the fair treatment of shareholders in connection with any take-over bid for common shares. The Shareholder Rights Plan was not being adopted in response to any proposal to acquire control of Jaguar. The Shareholder Rights Plan seeks to provide shareholders with adequate time to properly assess a take-over bid without undue pressure. It also is intended to provide the Board with more time to fully consider an unsolicited take-over bid and, if considered appropriate, to identify, develop and negotiate other alternatives to maximize shareholder value. The rights issued under the Shareholder Rights Plan will become exercisable only when a person, including its affiliates and associates and persons acting jointly or in concert with it, acquires or announces its intention to acquire beneficial ownership of common shares which when aggregated with its current holdings total 20 percent or more of the outstanding common shares (determined in the manner set out in the Shareholder Rights Plan) without complying with the “Permitted Bid” provisions of the Shareholder Rights Plan or without approval of the Board. Under the Shareholder Rights Plan those bids that meet certain requirements intended to protect the interests of all shareholders deemed to be “Permitted Bids”. Permitted Bids must be made by way of a take-over bid circular prepared in compliance with applicable securities laws and, among other conditions, must remain open for at least sixty (60) days. In the event a take-over bid does not meet the Permitted Bid requirements of the Shareholder Rights Plan, the rights will entitle shareholders, other than the person making the take-over bid and its affiliates and associates and persons acting jointly or in concert with it, to purchase additional common shares at a substantial discount to the market price of the common shares at that time. The TSX accepted notice of the Shareholder Rights Plan and the shareholders ratified the adoption of the Shareholder Rights Plan on May 10, 2007.

On February 27, 2007, Jaguar filed a final short form prospectus to issue up to 340,090 common shares to the holders of 5,398,250 common share purchase warrants, upon early exercise of the warrants. Each warrant entitled the holder thereof to acquire one common share of Jaguar at a price of Cdn.$4.50 at any time prior to 5:00 p.m. (Eastern Standard Time) on December 31, 2007. Each warrant entitled the holder thereof to acquire an additional 0.063 of one common share if such holder exercised his or her warrants during the thirty (30) day early exercise period commencing on February 28, 2007, and ending at 5:00 p.m. (Eastern Standard Time) on March 30, 2007.

The additional 0.063 of a common share issued upon the exercise of the warrants during the early exercise period represented a value of Cdn.$0.43 based on the closing price on February 26, 2007 of Cdn.$6.79. If at least 66 2/3 percent of the warrants outstanding on February 28, 2007 were exercised at or before the early warrant expiry time, each warrant that had not been so exercised during the early exercise period (except in limited circumstances with respect to U.S. warrant holders) would be exchanged, without any further action on the part of the warrant holder, including payment of the exercise price thereof or any other additional consideration, for a fraction of a common share equal to: (A) one plus (B) 0.063 multiplied by 50 percent minus (C) Cdn.$4.50 divided by the lesser of (i) the volume weighted average trading price of the common shares on the TSX for the five trading days ending on the early exercise expiry date, and (ii) the closing price of the common shares on the early exercise expiry date. As a result of the early exercise program described in this paragraph, 4,818,852 warrants were exercised resulting in the issuance of 5,122,428 common shares to the warrant holders. No agency fee was paid by Jaguar in connection with the distribution of the early exercise shares or the exchange shares being qualified under the short form prospectus. BCI acted as financial advisor and soliciting dealer manager to Jaguar in connection with the issuance of the early exercise shares and the exchange shares. Jaguar paid BCI a financial advisory fee of 3 percent of the exercise price for each warrant that is submitted for exercise in connection with the early exercise and automatically exchanged for exchange shares. The early exercise warrant transaction was approved by shareholders on February 27, 2007 and by warrant holders on February 28, 2007.

On March 22, 2007, Jaguar closed a private placement of 75,000 units. The units were sold by a syndicate led by TD Securities and included BCI, BMO and RBC. The underwriters exercised their option to purchase an additional 15 percent of the number of the units offered to cover over-allotments, resulting in aggregate gross proceeds of Cdn.$86.3 million (US$74.5 million) from the sale of 86,250 units. The units are comprised of a secured note in the principal amount of Cdn.$1,000, bearing a coupon of 10.5 percent, payable semi-annually in arrears, and 25 common shares of Jaguar. A total of 2.16 million new shares were issued relating to the private placement. The notes were listed on the TSX on July 26, 2007, under the symbol “JAG.NT”.

On July 23, 2007, Jaguar common shares began trading under the symbol “JAG” on the NYSE Arca Exchange.

On February 21, 2008, Jaguar issued 8,250,000 common shares at a price of Cdn.$13.40 per share for proceeds of Cdn.$110,550,000. The offering price was determined by negotiation between Jaguar and a syndicate led by RBC and included TD Securities, BCI, BMO, and Raymond James Ltd. Jaguar granted the underwriters an over-allotment option, exercisable in whole or in part up to 30 days following the closing of the transaction, to purchase up to an additional 1,237,500 common shares at a price of Cdn.$13.40 per common share, which would have increased the aggregate proceeds of the offering to Cdn.$127,132,500 if the over-allotment option had been fully exercised. The over-allotment option was not exercised and no additional shares were issued subsequent to the closing.

DESCRIPTION OF THE BUSINESS

General

Jaguar is a gold mining company currently engaged in gold production and in the acquisition, exploration, development and operation of gold mineral properties in Brazil. In addition, Jaguar may consider the acquisition and subsequent exploration, development and operation of other gold properties in Brazil.

Jaguar’s wholly-owned gold producing properties and projects are located in the Iron Quadrangle region near Belo Horizonte, Minas Gerais, Brazil: Turmalina, Paciência, Sabará and the Caeté Project. Through its wholly-owned subsidiaries, MSOL and MTL, Jaguar has interests in, and controls the mineral rights, concessions and licenses to the mineral resources and reserves presented in Tables 1 and 2 under the section entitled “Mineral Resources and Reserves”.

The technical report on the Turmalina Gold Project dated October 29, 2004, revised on December 16, 2004 and further revised on December 20, 2004, which covers the Turmalina property, the Scott Wilson RPA Turmalina Technical Report and the TechnoMine Turmalina Expansion Technical Report, as defined below, contain further details with respect to reported gold reserves and gold resources at Turmalina - See “Scott Wilson RPA Turmalina Technical Report” and “TechnoMine Turmalina Expansion Technical Report” below.

The TechnoMine Paciência Technical Report, as defined below, contains additional details regarding currently reported gold resources and reserves at Paciência - See “TechnoMine Paciência Technical Report” below.

The TechnoMine Quadrilátero Technical Report and the Scott Wilson RPA Sabará Technical Report, as defined below, contains additional details regarding reported gold resources and reserves at Sabará - See “TechnoMine Quadrilátero Technical Report” and “Scott Wilson RPA Sabará Technical Report” below.

The TechnoMine Caeté Project Technical Report, as defined below, contains additional details regarding currently reported gold resources in the Caeté Project - See “TechnoMine Caeté Technical Report” below.

In addition to the mining properties described in the preceding paragraph, in March 2007, Jaguar entered into the Joint Venture Agreement with Xstrata with respect to the Pedra Branca Project located in the State of Ceará in northeastern Brazil. Pursuant to the Joint Venture Agreement, Jaguar is currently conducting a comprehensive exploration program at the Pedra Branca Project.

The Technical Reports (as defined below) contain additional information regarding gold reserves and gold resources on Jaguar’s properties. See “Mining Projects” below.

Gold production and sales

Jaguar began pouring gold in December 2003. During 2008, Jaguar produced a total of 115,348 ounces of gold at an average cash operating cost of US$429 per ounce compared to 70,113 ounces produced at an average cash operating cost of US$346 per ounce during 2007. For the year ended December 31, 2008, gold sales totaled 108,944 ounces at an average price of US$860 per ounce compared to 67,350 ounces sold at an average price of US$710 per ounce for the year ended December 31, 2007. Increases in gold production during 2008 primarily resulted from the commencement of gold production at Paciência, which was under construction during fiscal 2007 and commenced gold production in July 2008.

The table below provides greater detail regarding total gold production at Turmalina, Paciência and Sabará for the year ended December 31, 2008:

| | Ore processed (000 tonnes) | Feed Grade (grams per tonne) | Plant Recovery Rate (%) | Production (ounces) | Cash operating cost per tonne (US$) | Cash operating cost per ounce (US$) |

| Turmalina | 481 | 5.46 | 88 | 72,785 | 55.30 | 364.00 |

| Paciência | 277 | 3.28 | 92 | 24,364 | 43.00 | 443.00 |

| Sabará | 475 | 1.54 | 66 | 18,199 | 22.50 | 667.00 |

| Total | 1,233 | 3.46 | 85 | 115,348 | 39.90 | 429.00 |

During 2009, Jaguar estimates it will produce 165,000-175,000 ounces of gold as follows:

| | Estimated | Estimated |

| | FY 2009 | FY 2009 |

| Operation | Production | Cash Operating Cost |

| | (ounces) | (US$/ounce) |

| Turmalina | 80,000-85,000 | $354-387 |

| Paciência | 65,000-70,000 | $362-398 |

| Sabará | 20,000 | $374-411 |

| Total | 165,000-175,000 | $360-394 |

Operating cash cost estimates for 2009 are based on an average exchange rate of R$2.00 to R$2.20 per US$1.00. As of January 30, 2009, the exchange rate was R$2.31 per US$1.00.

With respect to the Caeté Project, Jaguar targets initial gold production will commence approximately 18 months after the project is re-started and will be expanded to approximately 160,000 ounces per year in 2013.

All of Jaguar’s production facilities are, or will be, near Jaguar’s mineral concessions and are accessible via existing roads. Jaguar believes it has an advantage over other gold mine operators due to the clustered nature of its resource concessions and the proximity of its concessions to its processing facilities and existing infrastructure.

Jaguar has contracted with AngloGold Ashanti for AngloGold Ashanti to arrange sales of Jaguar’s gold bullion with gold brokers at Jaguar’s request and direction, which provides Jaguar with ready access to gold markets at limited costs and risks.

Specialized Skill and Knowledge

Jaguar is staffed by an experienced senior management team with over 100 years of collective experience exploring, developing and operating gold mines in Brazil. Jaguar’s Chief Executive Officer and President, Daniel R. Titcomb, has been involved in continuous mining exploration and development in Brazil since 1993. Jaguar’s Chief Operating Officer, Lúcio Cardoso, was formerly superintendent of AngloGold Ashanti's gold division and has over 35 years experience in the Brazilian mining sector. Jaguar’s Vice President of Exploration and Engineering, Adriano L. Nascimento, also has approximately 30 years experience in the Brazilian mining industry and held the position of senior engineer at AngloGold Ashanti for 11 years, where he was responsible for the production department of several mines, including Mina Grande, the deepest and one of the oldest mines in Brazil. Jaguar’s Chief Geologist, Jaime Duchini, has over 25 years experience in exploration in the Iron Quadrangle.

Competitive Conditions

The gold exploration and mining business is a competitive business in all its phases. Jaguar competes with numerous other companies and individuals in the search for and the acquisition of mineral licenses, permits and other mineral interests, as well as for acquisition of equipment and the recruitment and retention of qualified employees. There is also significant competition for the limited number of gold property acquisition opportunities. The ability of Jaguar to acquire gold mineral properties in the future will depend not only on its ability to develop its present properties, but also on its ability to select and acquire suitable producing properties or prospects for gold development or mineral exploration.

Jaguar has an ongoing relationship with AngloGold Ashanti through contractual royalty rights in certain of the properties and an agreement to provide Jaguar’s operating company with gold refining and marketing services.

Jaguar has built its base upon the acquisition of later-stage gold exploration properties in the Iron Quadrangle region of Brazil at relatively depressed prices. Jaguar believes that its asset acquisition costs combined with the clustered nature of its mineral assets and production facilities gives it an advantage over other similarly-sized competitors.

Employees

Jaguar had 1,328 employees as at December 31, 2008.

Foreign Operations

All of Jaguar’s mineral projects are owned and operated though its wholly-owned subsidiaries, MSOL and MTL. All of the wholly-owned properties are located near Belo Horizonte, Minas Gerais, Brazil. Jaguar is entirely dependent on its foreign operations for the exploration and development of gold properties and for production of gold.

Mineral Projects

Except as otherwise noted, the following descriptions and summaries of Jaguar’s material projects, are derived from the following Technical Reports:

| | (i) | The Technical Report on the Turmalina Gold Project dated September 10, 2005 and revised on March 10, 2006, as supplemented by a Technical Report on Turmalina Gold Project dated March 14, 2006 and as further revised on July 31, 2006, which cover the Turmalina property (the “Scott Wilson RPA Turmalina Technical Report”); |

| | (ii) | The Technical Report on the Turmalina Expansion Feasibility Study dated September 9, 2008 (the “TechnoMine Turmalina Expansion Technical Report”), which covers the Satinoco property; |

| | (iii) | The Technical Report on the Paciência Gold Project Santa Isabel Mine dated August 7, 2007 (the “TechnoMine Paciência Technical Report”), which covers the Paciência-Santa Isabel property; |

| | (iv) | The Technical Report on Jaguar’s initial concessions on the Quadrilátero dated September 17, 2004 and revised on December 20, 2004 (the “TechnoMine Quadrilátero Technical Report”), which covers the Sabará, Paciência and Santa Bárbara properties; |

| | (v) | The Technical Report on the Sabará Project dated February 17, 2006 (the “Scott Wilson RPA Sabará Technical Report”), which covers Zones A and B and Lamego (also called Zone C) and Queimada properties; and |

| | (vi) | The Technical Report on the Caeté Expansion Feasibility Study dated September 15, 2008 (the “TechnoMine Caeté Technical Report” and together with the technical reports in items (i)-(v), the "Technical Reports"), which covers the Pilar and Roça Grande properties. |

This Annual Information Form contains only summary information regarding Jaguar’s properties. A complete description of Jaguar’s properties and associated maps, photographs and references can be found in the Technical Reports filed on SEDAR (at www.sedar.com), and such reports are hereby incorporated by reference herein.

The Qualified Person, as such term is defined in NI 43-101, who prepared the TechnoMine Turmalina Expansion Technical Report, the TechnoMine Paciência Technical Report, the TechnoMine Quadrilátero Technical Report, and the TechnoMine Caeté Technical Report referred to above was Ivan C. Machado, M.Sc., P.E., P.Eng. Mr. Machado is a principal of TechnoMine and is independent for the purposes of NI 43-101.

The Qualified Persons who prepared the Scott Wilson RPA Turmalina Technical Report and the Scott Wilson RPA Sabará Technical Report were Graham G. Clow, P.Eng., and Wayne W. Valliant, P.Geo. Mr. Clow is a principal of Scott Wilson RPA, and Mr. Clow and Mr. Valliant are independent for the purposes of NI 43-101.

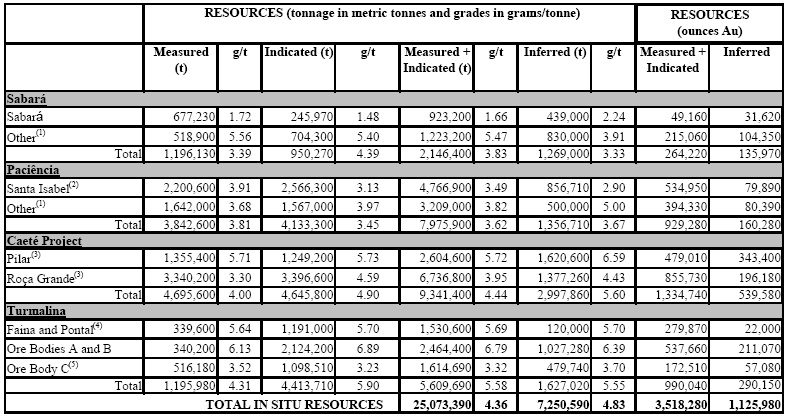

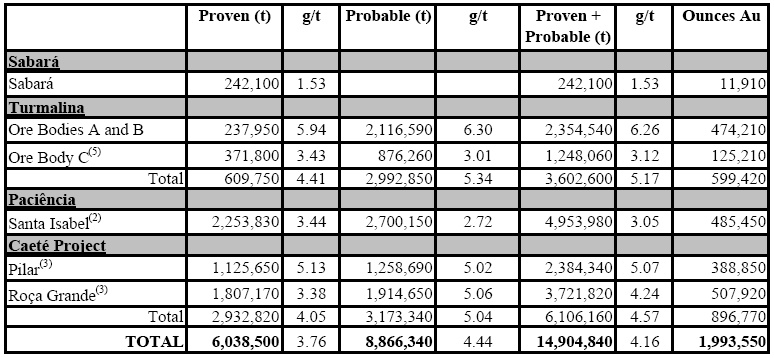

Mineral Resources and Reserves

During 2008, Jaguar retained TechnoMine to prepare feasibility studies for its Caeté Project and expansion of the Turmalina operation. TechnoMine completed the NI 43-101 compliant feasibility study technical reports on September 15, 2008 and September 9, 2008, respectively.

TechnoMine completed the feasibility studies and in concert with Jaguar reviewed the information and prepared a table of mineral resources and reserves (the “September 2008 Review”). Ivan C. Machado, M.Sc., P.E., P.Eng. audited the September 2008 Review. Mr. Machado is a Qualified Person as such term is defined in NI 43-101.

Based on the September 2008 Review, Jaguar reported (i) measured and indicated resources of 23,095,210 tonnes with an average grade of 4.74 grams per tonne containing 3,517,860 ounces of gold and (ii) 6,704,750 tonnes of inferred resources with an average grade of 5.15 grams per tonne containing 1,109,030 ounces of gold. Jaguar’s proven and probable mineral reserves, which are included in the measured and indicated mineral resource figure above, were 13,510,470 tonnes with an average grade of 4.69 grams per tonne containing 2,033,620 ounces of gold. The figures reported in the September 2008 Review did not consider 2007 and 2008 production from the Turmalina operations and a small test mining production at Paciência in 2006.

In consideration of the significant improvement in global gold prices, Jaguar and TechnoMine redefined the design criteria to reflect stronger gold markets. Based on the review recently completed, as of December 31, 2008, Jaguar’s mineral resources are (i) measured and indicated resources of 25,073,390 tonnes with an average grade of 4.36 grams per tonne containing 3,518,270 ounces of gold and (ii) 7,250,590 tonnes of inferred resources with an average grade of 4.83 grams per tonne containing 1,125,970 ounces of gold. Jaguar’s proven and probable mineral reserves, which are included in the measured and indicated mineral resource figure above, are 14,904,840 tonnes with an average grade of 4.16 grams per tonne containing 1,993,550 ounces of gold.

See below detailed tables of Jaguar’s mineral resources and reserves as at December 31, 2008.

Table 1 - Summary of Estimated Mineral Resources*

Table 2 - Summary of Estimated Mineral Reserves*

* Mineral resources listed in Table 1 include mineral reserves listed in Table 2. Totals reflect depletion from production through December 31, 2008. Some columns and rows may not total due to rounding.

(1) TechnoMine NI 43-101 Technical Report on the Quadrilátero Gold Project filed on SEDAR on December 20, 2004.

| (2) TechnoMine NI 43-101 Technical Report on the Paciência Gold Project Sta. Isabel Mine filed on SEDAR on August 9, 2007. |

(3) TechnoMine NI 43-101 Technical Report on the Caeté Gold Project filed on SEDAR on September 17, 2008.

(4) TechnoMine NI 43-101 Technical Report on the Turmalina Gold Project filed on SEDAR on December 20, 2004.

(5) TechnoMine NI 43-101 Technical Report on the Turmalina Expansion filed on SEDAR on September 11, 2008.

Although Jaguar has carefully prepared and verified the mineral resource and reserve figures presented herein, such figures are estimates, which are, in part, based on forward-looking information, and no assurance can be given that the indicated level of gold will be produced. Estimated reserves may have to be recalculated based on actual production experience. Market price fluctuations of gold as well as increased production costs or reduced recovery rates, and other factors may render the present proven and probable reserves unprofitable to develop at a particular site or sites for periods of time. See “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements”.

Mining Concession and Exploration Permitting Requirements and Status

In Brazil mining activity requires the grant of concessions from the DNPM, an agency of the Brazilian federal government responsible for controlling and applying the Brazilian Mining Code. Government concessions consist of exploration awards, exploration licenses, and mining permits. Exploration awards permit the holder to begin exploration of the property, exploration licenses allow the holder to proceed with exploration to determine feasibility of mining the property, and mining permits allow the holder to mine the property.

Applications for mining concessions must include an independently-prepared environmental plan that deals with water treatment, soil erosion, air quality control, re-vegetation and reforestation (where necessary) and reclamation. Mining concessions will not be granted unless the mining plan, including the environmental plan, is approved by the state authorities.

Based on the experience of management in obtaining licenses, Jaguar has made estimates anticipated time frames for receiving licenses, upon which it has based projections for capital expenditures, revenues and earnings. The time frames in which licenses are issued are dependent upon the actions of regulatory authorities and third parties.

The following table lists the status of Jaguar’s awards, licenses and permits.

| Property | Permits |

| | Phase | Status |

| Sabará |

| Sabará Plant | Implementation License | Received September 2005 |

| Sabará Plant | Operation License | Received December 2006 |

| Sabará Zone A Mine | Implementation License | Received September 2006 |

| Sabará Zone A Mine | Operation License | Received November 2006 |

| Paciência |

| Santa Isabel Mine and Plant | Implementation License | Received May 2007 |

| Santa Isabel Mine and Plant | Operation License | Received October 2008 |

| Caeté Project |

| Caeté Plant | Implementation License | Received July 2007 |

| Caeté Plant | Operation License | Expected June 2010 |

| Caeté Tailing Dam | Previous License | Received November 2007 |

| Caeté Tailing Dam | Implementation License | Expected March 2009 |

| Caeté Tailing Dam | Operation License | Expected December 2009 |

| Roça Grande Mine | Operation License | Received April 2008 |

| Pilar Mine | Implementation License | Received August 2008 |

| Pilar Mine | Operation License | Expected June 2010* |

| Turmalina |

| Turmalina Mine and Plant | Implementation License | Received August 2006 |

| Turmalina Mine and Plant | Operation License | Received March 2007 |

| Turmalina Mine and Plant Expansion I | Operation License | Expected April 2009 |

| Turmalina Tailing Dam Expansion I | Implementation License | Expected February 2009 |

*An AAF permit has been granted to the Pilar Mine for production of up to 100,000 tonnes per year.

JAGUAR GOLD OPERATIONS AND PROJECTS

In the state of Minas Gerais in Brazil, Jaguar has three operating properties (Turmalina, Paciência and Sabará) and one property under development (the Caeté Project). See detailed description of each property below.

| Turmalina Operations | Paciência Operations | Sabará Operations | Caeté Project |

| Turmalina Plant | Paciência Plant | Sabará Plant | Caeté Plant |

| Turmalina Mine (Ore Bodies A and B) | Santa Isabel Mine | Sabará Zone A Mine | Roça Grande Mine |

| Satinoco (Ore Body C) | Bahú Target | Serra Paraíso Target | Pilar Mine |

| Satinoco Extension (Ore Body D) | NW01 Target | Rio de Peixe Oxide | Catita II Target |

| Faina and Pontal Targets | Rio de Peixe Sulfide | Catita Oxide | Morro do Adão Target |

| Fazenda Experimental Target | Conglomerates Target | Boa Vista Target | Camará/Trindade Targets |

Scoot Wilson RPA Turmalina Technical Report

Background

Scott Wilson RPA prepared a NI 43-101 Technical Report for Turmalina, dated July 31, 2006, filed on SEDAR August 1, 2006. This report is no longer current in that two years of production have taken place and it has not been updated to reflect any new information since the date of the report, including, but not limited to, resources and reserves, mine and plant production, metallurgy, operating and capital costs and environmental data. The following description of the Turmalina Project is derived from the summary contained in the Scott Wilson RPA Turmalina Technical Report.

Gold was first discovered in the Turmalina area in the sixteenth century. AngloGold Ashanti explored the area extensively between 1979 and 1988 utilizing geochemistry, trenching, drilling and 3.9 kilometers of underground development. This exploration program led to the discovery of the following mineralized bodies: Turmalina, Satinoco, Faina and Pontal. During 1992 and 1993, AngloGold Ashanti mined 373,000 tonnes of oxide mineralization from an open pit on the Turmalina zone and recovered 35,500 ounces of gold using heap leach technology. Subsequently, AngloGold Ashanti explored a possible downward sulphide extension by driving a ramp beneath the pit and drifting on two levels in the mineralized zone at approximately 50 and 75 meters below the pit floor. Jaguar acquired the Turmalina Gold Project from AngloGold Ashanti on September 30, 2004.

Mining Status and Permitting

Jaguar received an implementation license for the Turmalina Gold Project in December 2005. In the fourth quarter of 2005 Jaguar commenced construction of the 60,000 ounce per year Turmalina facility. The majority of the infrastructure, such as roads, power, ramp and access to the underground orebody, was in place as of the date of the Scott Wilson RPA Turmalina Technical Report. Jaguar received the operation license with respect to the Turmalina Gold Project in March 2007.

Jaguar submitted environmental plans for the Turmalina Gold Project and received approval prior to the issuance of its Turmalina operation license. The Turmalina operation license was received in March 2007.

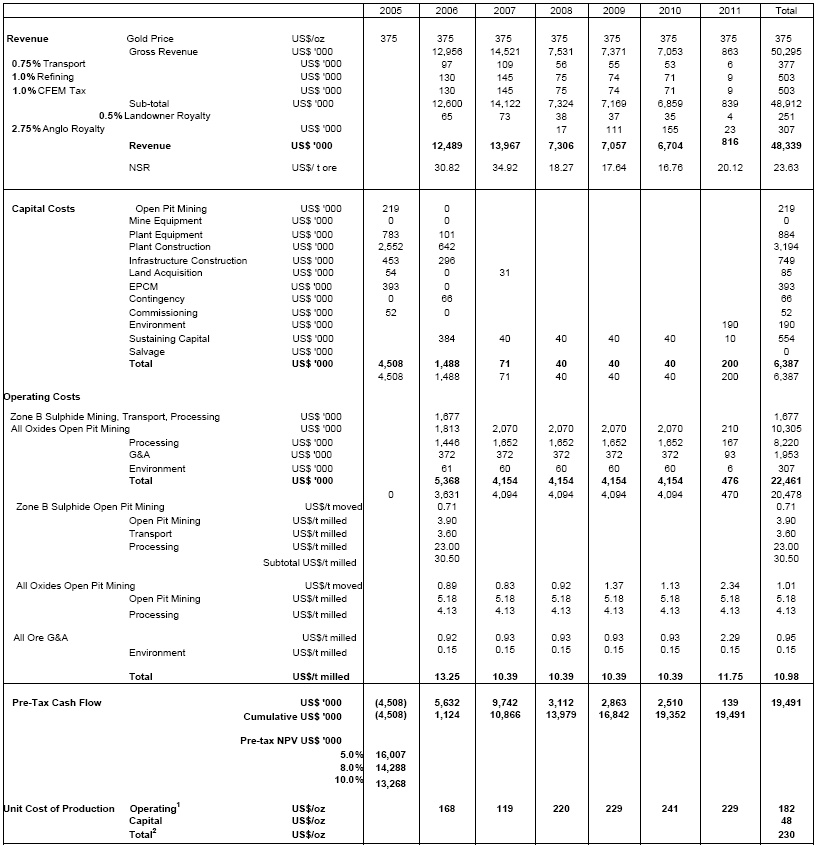

Economic Analysis

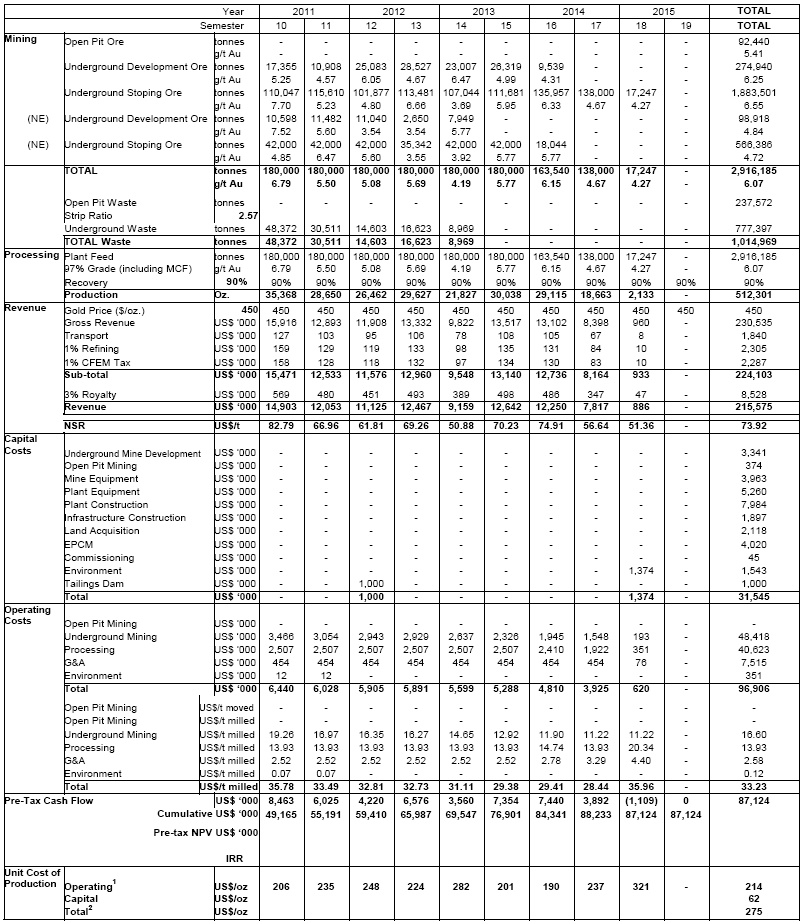

A pre-tax Cash Flow Projection has been generated from the Life of Mine production schedule and capital and operating cost estimates, and is summarized in Table 1-1. A summary of the key criteria is provided below.

Physicals

| | Mine life: | | 8.6 years, beginning in October 2006 |

| | Total millfeed: | | 2,916,000 tonnes at a grade of 6.1 grams per tonne Au |

| | Operations: | | 360 days per year |

| | Open pit production: | | 92,400 tonnes at a grade of 5.4 grams per tonne Au |

| | Strip Ratio: | | 2.57 |

| | Underground production: | | 1,000 tonnes per day at a grade of 6.1 grams per tonne Au |

| | Mill throughput: | | 1,000 tonnes per day, 360,000 tons per year |

| | Gold recovery: | | 90% to doré |

| | Total gold produced: | | 512,000 ounces |

Revenue

| | Gold price: | | US$450 per ounce |

| | Transport and insurance: | | US$3.60 per ounce |

| | Refining: | | 1% of gross sales |

| | CFEM (federal) royalty: | | 1% of gross sales |

| | Royalty to landowner: | | 5% NSR on first US$10 M/year, 3% on remainder |

| | Operating cost: | | US$33.23 per tonne milled |

| | Pre-production Capital cost: | | US$28.7 million |

| | Sustaining capital: | | US$2.8 million (includes closure) |

| | Exchange Rate: | | reverting from current rates to long-term rate of US$1.00 = R $2.501 |

1 The long-term exchange rate used for the Turmalina Project is US$1.00 = R$2.50, compared to the rate as of the date of the Scott Wilson RPA Turmalina Technical Report of US$1.00 = R$2.29. The long-term rate was chosen based on economic forecasts by Brazilian banks. For Base Case cash flow estimation, actual exchange rates were used for costs incurred up to June 30, 2006. The remainder of pre-production capital to be spent was converted using an exchange rate of US$1.00 = R$2.19. As of March 11, 2008, the exchange rate is US$1.00 = R$1.70.

| TABLE 1-1 PRE-TAX CASH FLOW $450/OUNCES GOLD |

JAGUAR MINING INC. - TURMALINA PROJECT

Notes: 1. Equivalent to Gold Institute Total Cash Cost.

2. Equivalent to Gold Institute Total Production Cost.

3. Working capital estimated at $0.9 M by Jaguar Mining Inc. has been excluded.

4. Salvage estimated at $3.4 M by Jaguar Mining Inc.

TABLE 1-1 PRE-TAX CASH FLOW $450/OUNCES GOLD

JAGUAR MINING INC. - TURMALINA PROJECT

Notes: 1. Equivalent to Gold Institute Total Cash Cost.

2. Equivalent to Gold Institute Total Production Cost.

3. Working capital estimated at $0.9 M by Jaguar Mining Inc. has been excluded.

4. Salvage estimated at $3.4 M by Jaguar Mining Inc.

Considering the Turmalina Project on a stand-alone basis, the Base Case undiscounted pre-tax cash flow totals US$87.1 million over the mine life, and simple payback occurs near the mid-point of 2008 (approximately 21 months from start of production).

The Gold Institute Total Cash Cost is US$214 per ounce of gold. The mine life capital unit cost is US$62 per ounce, for a Gold Institute Total Production Cost of US$275 per ounce of gold. Average annual gold production during operations is 60,000 ounces per year.

At a discount rate of 12%, the pre-tax NPV at the time of the Scott Wilson RPA Turmalina Technical Report was US$33.0 million and the IRR is 47.5%.

Jaguar’s after-tax NPV estimate at 12% discount rate at the time of the Scott Wilson RPA Turmalina Technical Report was US$14.2 million, with a project IRR of 30.7%. Scott Wilson RPA did not review Jaguar’s tax model.

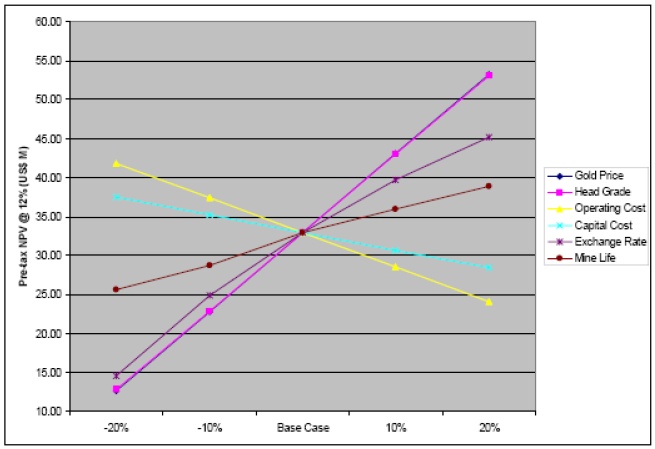

Sensitivity Analysis

Figure 1-1 shows the project sensitivity to various factors, including:

• Head Grade

• Gold Price

• Operating Cost

• Capital Cost

• Exchange Rate

• Mine Life

FIGURE 1-1 SENSITIVITY ANALYSIS

The Turmalina Project is most sensitive to gold price and head grade. The break even gold price resulting in zero pre-tax NPV at 12% at the time of the Scott Wilson RPA Turmalina Technical Report was approximately US$300 per ounce. At a gold price of US$635 per ounce (July 27, 2006), the pre-tax NPV at 12% was US$74.7 million. Possible impacts on head grades include assay bias and increased dilution. If assaying proves to be biased 10% low, head grades may be 10% higher, which would result in a pre-tax NPV at 12% of US$43 million. If dilution rates are 20% (AngloGold Ashanti test results) rather than 15% (Base Case estimate), head grades will be reduced by 5%, which would result in a pre-tax NPV at 12% of approximately US$28 million.

The long-term exchange rate used for the Turmalina Project is US$1.00 = R$2.50, compared to the rate as of the date of the Scott Wilson RPA Turmalina Technical Report of US$1.00 = R$2.29. The long-term rate was chosen based on economic forecasts by Brazilian banks. For Base Case cash flow estimation, actual exchange rates were used for costs incurred up to June 30, 2006. The remainder of pre-production capital to be spent was converted using an exchange rate of US$1.00 = R$2.19. Sustaining capital and operating costs use the long-term exchange rate.

Other key sensitivities, in addition to the aforementioned, are operating costs, and capital cost, and mine life. The sensitivities are summarized in the following table as pre-tax NPV at 12% discount.

TABLE 1-2 SENSITIVITY DATA

Jaguar Mining Inc - Turmalina Project

| | -20% | -10% | Base Case | +10% | +20% |

Gold Price (US$/ounces) Pre-tax NPV (US$ million) | 360 $ 12.7 | 405 $ 22.8 | 450 $ 33.0 | 495 $ 43.1 | 540 $53.2 |

Grade (grams per tonne) Pre-tax NPV (US$ million) | 4.86 $ 12.8 | 5.46 $ 22.9 | 6.07 $ 33.0 | 6.68 $ 43.0 | 7.28 $53.1 |

Operating Costs (US$ million) Pre-tax NPV (US$ million) | $ 62.0 $ 41.8 | $ 78.5 $ 37.4 | $ 96.9 $ 33.0 | $ 117.3 $ 28.5 | $ 139.6 $ 24.1 |

Capital Costs (US$ million) Pre-tax NPV (US$ million) | $ 20.2 $ 37.5 | $ 25.6 $ 35.2 | $ 31.6 $ 33.0 | $ 38.2 $ 30.7 | $ 45.4 $ 28.4 |

Exchange Rate (R$/US$) Pre-tax NPV (US$ million) | 2.00 $ 14.5 | 2.25 $ 24.9 | 2.50 $ 33.0 | 2.75 $ 39.7 | 3.00 $ 45.2 |

Mine Life (Mt) Pre-tax NPV (US$ million) | 2.3 $ 25.6 | 2.6 $ 28.7 | 2.9 $ 33.0 | 3.2 $ 36.0 | 3.5 $ 38.9 |

The base case sensitivity to discount rate is shown as follows:

• 12% - - pre-tax NPV = US$33.0 million

• 10% - - pre-tax NPV = US$38.6 million

• 7.5% - - pre-tax NPV = US$47.2 million

• 5% - - pre-tax NPV = US$57.7 million

Technical Summary

The Turmalina Project lies approximately 120 kilometers northwest of Belo Horizonte and six kilometers south of the town of Pitangui, Minas Gerais, Brazil. The Turmalina Project comprises seven contiguous concessions covering an area of 5,337 hectares and was acquired from AngloGold Ashanti in September 2004 for US$4.0 million, payable in three equal installments of US$1.35 million. Jaguar has 100% ownership subject to a 5% net revenue interest up to US$10 million, and 3% thereafter, to an unrelated third party. In addition, there is a 0.5% net revenue interest payable to the legal landowner.

Gold was first discovered in the area in the 16th century. During 1992 and 1993, AngloGold Ashanti mined 373,000 tonnes of oxide mineralization from an open pit on the Turmalina Zone and recovered 35,500 ounces of gold using heap leach technology. Subsequently, AngloGold Ashanti explored a possible downward sulphide extension by driving a ramp beneath the pit and drifting on two levels in the mineralized zone at approximately 50 meters and 75 meters below the pit floor.

The Turmalina Deposit is hosted by rocks of the Archaean Rio das Velhas greenstone belt in the Iron Quadrangle region, one of the major gold provinces in the world. The Pitangui area is underlain by rocks of Archaean and Proterozoic age. Archaean units include a granitic basement, overlain by the Pitangui Group, a sequence of ultramafic to intermediate volcanic flows and pyroclastics, and associated sediments. The predominant rock types in the deposit are metamorphosed pelites and tuffs. Gold mineralization is associated with higher levels of sericite, quartz, and biotite. Some fraction of the gold mineralization in the Turmalina Deposit may be due to primary, exhalative deposition associated with the banded iron formation, however, the deposit can be broadly classified as epigenetic, related to a mesothermal system that localized auriferous silicification in local structural features within a wider shear zone.

The Turmalina Deposit comprises three ore bodies: Principal Zone (Ore Body A), NE Zone (Ore Body B) and the CD Zone. Ore Body A strikes azimuth 110° and dips at 55°-60°. Gold grade zoning indicates a SE plunge of approximately 65°. The body is 200 m to 250 m long and ranges in horizontal width from two meters to 30 meters, averaging approximately eight meters. Ore Body B lies 50 meters to 100 meters east of the Ore Body A and has a similar attitude. It is approximately 200 meters long and ranges from one meter to 12 meters in horizontal width, averaging approximately three meters. Mineralization extends to at least 350 meters below surface. The CD Zone includes two narrow sub-zones approximately 50 meters vertically by 50 meters horizontally, ten meters in the hangingwall and ten meters in the footwall of the Ore Body A.