Table of Contents

As filed with the Securities and Exchange Commission on April 5, 2007

Securities Act File No. 333-127272

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST-EFFECTIVE AMENDMENT NO. 2

TO REGISTRATION STATEMENT ON FORM S-1

UNDER

THE SECURITIES ACT OF 1933

Highbury Financial Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 6282 | 20-3187008 | ||

| (State or other jurisdiction of incorporation) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

999 Eighteenth Street, Suite 3000

Denver, CO 80202

303-357-4802

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Richard S. Foote, President and Chief Executive Officer

Highbury Financial Inc.

999 Eighteenth Street, Suite 3000

Denver, CO 80202

303-357-4802

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Ann F. Chamberlain

Floyd I. Wittlin

Bingham McCutchen LLP

399 Park Avenue

New York, NY 10022-4689

(212) 705-7000

(212) 752-5378—Facsimile

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

This post-effective Amendment No. 2 to Form S-1 is being filed to update the information in our Registration Statement, File No. 333-127272. This post-effective Amendment No. 2 relates to 15,486,666 shares of common stock issuable upon the exercise of outstanding warrants, 336,667 units underlying the unit purchase option issued to the underwriters of our initial public offering, 336,667 shares of common stock underlying the 336,667 units, 673,334 warrants underlying the 336,667 units and the 673,334 shares of common stock issuable upon the exercise of the 673,334 warrants.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED APRIL 5, 2007

PRELIMINARY PROSPECTUS

Highbury Financial Inc.

15,486,666 Shares

Common Stock

This prospectus relates to an aggregate of 15,486,666 shares of common stock, $0.0001 par value per share of Highbury, that may be issued upon the exercise of outstanding warrants. The warrants entitle the holders hereof, upon exercise, to purchase one share of our common stock at a price of $5.00 per share.

Our common stock is quoted on the OTC Bulletin Board under the trading symbol “HBRF.” On March 28, 2007, the last reported sale price of our common stock was $5.75.

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 5 of this prospectus for a discussion of information that should be considered in connection with an investment in our common stock.

| Public Offering Price | Underwriting Discount and Commission | Proceeds, Before Expenses, to Us | |||||||||

Per share | $ | 5.00 | (2) | $ | 0.00 | $ | 5.00 | (2) | |||

Total (1)(3) | $ | 77,433,330.00 | (2) | $ | 0.00 | $ | 77,433,330.00 | (2) | |||

| (1) | These amounts assume that all of our outstanding warrants are exercised. |

| (2) | The per share public offering price and proceeds to us for 15,486,666 shares is $5.00. |

| (3) | These amounts do not include the unit purchase option issued to the underwriters of our initial public offering. |

Neither the Securities and Exchange Commission, or the SEC, nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

__________, 2007

Table of Contents

| Page | ||

| 1 | ||

| 5 | ||

| 14 | ||

| 16 | ||

| 16 | ||

| 17 | ||

| 18 | ||

| 22 | ||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 25 | |

| 42 | ||

| 50 | ||

| 52 | ||

| 55 | ||

| 66 | ||

| 66 | ||

| 66 | ||

| 67 | ||

i

Table of Contents

You should rely only on the information contained or incorporated by reference in this prospectus and in an applicable prospectus supplement, if any, or in any amendment to this prospectus. We have not authorized any other person to provide you with different information, and if anyone provides, or has provided, you with different or inconsistent information, you should not rely on it. We will not make an offer to sell our common stock in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date of the document containing the information.

In this prospectus, references to “the Company,” “we,” “us,” “our,” and “registrant” refer to Highbury Financial Inc. and its subsidiary. References to Highbury refer solely to Highbury and references to Aston refer solely to Aston Asset Management LLC, a subsidiary of Highbury.

This prospectus relates to an aggregate of 15,486,666 shares of common stock, $0.0001 par value per share, of Highbury that may be issued upon the exercise of outstanding warrants. The warrants entitle the holders thereof, upon exercise, to purchase one share of our common stock at a price of $5.00 per share.

Highbury is an investment management holding company providing permanent capital solutions to mid-sized investment management firms. We pursue acquisition opportunities and seek to establish accretive partnerships with high quality investment management firms. Highbury’s strategy is to provide permanent equity capital to fund buyouts from corporate parents, buyouts of founding or departing partners, growth initiatives, or exit strategies for private equity funds. This strategy includes leaving material equity interests with management teams to align the interests of management and our shareholders and, in general, does not include integrating future acquisitions, although we may execute add-on acquisitions for our current or future affiliates. We will seek to augment and diversify our sources of revenue by asset class, investment style, distribution channel, client type and management team. We intend to fund future acquisitions with retained net income or the issuance of debt or equity.

Highbury was formed in July 2005 for the purpose of acquiring or acquiring control of, through a merger, capital stock exchange, asset acquisition, stock purchase or other similar business combination, one or more financial services businesses. Pursuant to the asset purchase agreement, dated as of April 20, 2006, referred to in this prospectus as the asset purchase agreement, among Highbury, Aston Asset Management LLC, and ABN AMRO Asset Management Holdings, Inc., ABN AMRO Investment Fund Services, Inc., ABN AMRO Asset Management, Inc., Montag & Caldwell, Inc., Tamro Capital Partners LLC, Veredus Asset Management LLC, and River Road Asset Management, LLC, collectively referred to herein as the sellers, on November 30, 2006, Highbury acquired substantially all of the sellers’ business of providing investment advisory, administration, distribution and related services to the U.S. mutual funds, referred to throughout this prospectus as the acquired business, specified in the asset purchase agreement. This transaction is referred to throughout this prospectus as the acquisition. In connection with the consummation of the acquisition, Aston entered into agreements with each of the sellers that managed the target funds prior to the acquisition, pursuant to which each such seller now acts as a sub-adviser to the applicable target fund, each of which is now rebranded an Aston Fund. Pursuant to the asset purchase agreement, the sellers have agreed not to terminate these agreements for a period of five years following the consummation of the acquisition.

At the closing of the acquisition, Highbury made a payment of $38.6 million to the sellers of the acquired business to pay the purchase price under the asset purchase agreement. Highbury then contributed the acquired business to Aston. Highbury formed Aston on April 19, 2006 and became the sole member of Aston. In connection with Highbury and Aston entering into the asset purchase agreement, the limited liability company agreement of Aston was amended and eight employees of the acquired business and ABN AMRO were admitted as members of Aston, collectively referred to herein as the Aston management members. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for information on the operating and ownership allocations of Highbury and Aston. As of December 31, 2006, Aston managed 20 no-load mutual funds, comprised of 16 equity funds and four fixed income funds, with approximately $5.5 billion of mutual fund assets under management.

1

Table of Contents

OUR CORPORATE INFORMATION

Our principal executive offices are located at 999 Eighteenth Street, Suite 3000, Denver, Colorado 80202. Our telephone number is (303) 357-4802.

2

Table of Contents

THE OFFERING

| Securities Offered: | 15,486,666 shares of common stock issuable upon exercise of the warrants | |

Number of shares of common stock outstanding before this offering: | 9,527,000 | |

| Warrants: | ||

Number of warrants outstanding before this offering: | 15,820,000 | |

Number of warrants to be outstanding after this offering: | 333,334 (assuming exercise in full of the warrants issued in our initial public offering) | |

Exercisability: | Each warrant is exercisable for one share of common stock. | |

Exercise price: | $5.00 | |

Exercise period: | The warrants became exercisable on January 25, 2007. | |

| The warrants will expire at 5:00 p.m., New York City time, on January 25, 2010, or earlier upon redemption. | ||

Redemption: | We may redeem the outstanding warrants: | |

• at any time after the warrants become exercisable; | ||

• in whole and not in part; | ||

• at a price of $0.01 per warrant; | ||

• upon a minimum of 30 days prior written notice of redemption; and | ||

• only if the last sales price of our common stock equals or exceeds $8.50 per share for any 20 trading days within a 30 trading day period ending three business days before we send the notice of redemption. | ||

| We have established these redemption criteria to provide warrant holders with a reasonable premium to the initial warrant exercise price as well as a reasonable cushion against a negative market reaction, if any, to our redemption call. If the foregoing conditions are satisfied and we call the warrants for redemption, each warrant holder will then be entitled to exercise his or her warrant prior to the date scheduled for redemption. There can be no assurance, however, that the price of the common stock will exceed the price at which the warrants may be called for redemption or the warrant exercise price after the redemption call is made. | ||

3

Table of Contents

OTC Bulletin Board symbols for our securities: | ||

Units: | HBRFU | |

Common Stock: | HBRF | |

Warrants: | HBRFW | |

Proceeds: | We intend to use the net proceeds for working capital or for other general corporate purposes. We may also use a portion of the net proceeds to fund acquisitions of investment management firms, to repurchase securities, if appropriate, or to repay outstanding borrowings, if any. | |

4

Table of Contents

An investment in our securities involves a high degree of risk. You should consider carefully all of the risks described below, together with the other information contained in this prospectus, before making a decision to invest in our common stock. If any of the following risks occur, our business, financial condition and results of operations may be materially adversely affected. In that event, the trading price of our securities could decline, and you could lose all or a part of your investment.

Risks Related to the Financial Services Industry and Aston

The financial services industry faces substantial regulatory risks and we may experience reduced revenues and profitability if our services are not regarded as compliant with the regulatory regime.

The financial services industry is subject to extensive regulation. Many regulators, including U.S. government agencies and self-regulatory organizations, as well as state securities commissions and attorneys general, are empowered to conduct administrative proceedings and investigations that can result in, among other things, censure, fine, the issuance of cease-and-desist orders, prohibitions against engaging in some lines of business or the suspension or expulsion of an investment adviser. The requirements imposed by regulators are designed to ensure the integrity of the financial markets and not to protect our stockholders.

Governmental and self-regulatory organizations, including the SEC, the NASD and national securities exchanges such as the New York Stock Exchange, impose and enforce regulations on financial services companies. The types of regulations to which investment advisers and managers are subject are extensive and include, among other things: recordkeeping, fee arrangements, client disclosure, custody of customer assets, and the conduct of officers and employees.

The regulatory environment in which we operate is also subject to modifications and further regulations. New laws or regulations or changes in the enforcement of existing laws or regulations applicable to us also may adversely affect our business, and our ability to function in this environment depends on our ability to constantly monitor and react to these changes. For example, the growing trend of separating the fees mutual fund managers pay brokerage firms for investment research from brokerage commissions may trigger restrictions under the Investment Advisers Act of 1940.

We may face legal liability that may result in reduced revenues and profitability.

In recent years, the volume of claims and amount of damages claimed in litigation and regulatory proceedings against financial services firms has been increasing. Aston’s investment advisory contracts include provisions designed to limit our exposure to legal claims relating to services, but these provisions may not protect us or may not be adhered to in all cases. We may also be subject to claims arising from disputes with employees for alleged discrimination or harassment, among other things. The risk of significant legal liability is often difficult to assess or quantify and its existence and magnitude often remain unknown for substantial periods of time. As a result, we may incur significant legal expenses in defending against litigation. Substantial legal liability or significant regulatory action against us could materially adversely affect our business, financial condition or results of operations or cause significant harm to our reputation, which could seriously harm our business.

There have been a number of highly publicized cases involving fraud or other misconduct by employees in the financial services industry in recent years, and we run the risk that employee misconduct could occur. It is not always possible to deter or prevent employee misconduct and the precautions we take to prevent and detect this activity may not be effective in all cases.

5

Table of Contents

We face strong competition from financial services firms, many of whom have the ability to offer clients a wider range of products and services than we offer, which could lead to pricing pressures that could have a material adverse affect on our revenue and profitability.

We compete with other firms – both domestic and foreign – in a number of areas, including the quality of our employees, transaction execution, products and services, innovation, reputation and price. We may fail to attract new business and may lose clients if, among other reasons, we are not able to compete effectively. We also face significant competition as a result of a recent trend toward consolidation in the investment management industry. In the past several years, there has been substantial consolidation and convergence among companies in this industry. In particular, a number of large commercial banks, insurance companies and other broad-based financial services firms have established or acquired broker-dealers or have merged with other financial institutions. Many of these firms have the ability to offer a wide range of products such as loans, deposit-taking and insurance, brokerage, investment management and investment banking services, which may enhance their competitive positions. They also have the ability to support investment management activity with commercial banking, investment banking, insurance and other financial services revenue in an effort to gain market share, which could result in pricing pressure on our business. The passage of the Gramm-Leach-Bliley Act in 1999 reduced barriers to large institutions’ providing a wide range of financial services products and services. We believe, in light of increasing industry consolidation and the regulatory overhaul of the financial services industry, that competition will continue to increase from providers of financial services products.

The investment advisory fees we receive may decrease in a market or general economic downturn, which would decrease our revenues and net income.

Because we are in the investment advisory business, our net income and revenues are likely to be subject to wide fluctuations, reflecting the effect of many factors on our assets under management, including: general economic conditions; securities market conditions; the level and volatility of interest rates and equity prices; competitive conditions; liquidity of global markets; international and regional political conditions; regulatory and legislative developments; monetary and fiscal policy; investor sentiment; availability and cost of capital; technological changes and events; outcome of legal proceedings; changes in currency values; inflation; credit ratings; and the size, volume and timing of transactions. These and other factors subject us to an increased risk of asset volatility.

As an investment management firm, our business could be expected to generate lower revenue in a market or general economic downturn. The investment advisory fees we receive are based on the market value of the assets under management. Accordingly, a decline in the prices of securities would be expected to cause our revenue and income to decline by:

| • | causing the value of the assets under management to decrease, which would result in lower investment advisory fees; or |

| • | causing some of our clients to withdraw funds from our investment management business in favor of investments they perceive as offering greater opportunity and lower risk, which also would result in lower investment advisory fees. |

Aston’s investment advisory contracts are subject to termination on short notice. Termination of a significant number of investment advisory contracts will have a material impact on our results of operations.

Aston derives almost all of its revenue from investment advisory contracts with the Aston Funds. These contracts are typically terminable by the target fund trustees without penalty upon relatively short notice (generally not longer than 60 days). We cannot be certain that we will be able to retain the target funds as clients. Because the Aston Funds all have the same trustees, it is possible that all the contracts with them could be terminated simultaneously. If the trustees of the Aston Funds terminate Aston’s investment advisory contracts we would lose substantially all of our revenues.

6

Table of Contents

To the extent Aston is forced to compete on the basis of price, it may not be able to maintain its current fee structure.

The investment management business is highly competitive and has relatively low barriers to entry. To the extent Aston is forced to compete on the basis of price, it may not be able to maintain its current fee structure. Although Aston’s investment management fees vary from product to product, historically the acquired business competed primarily on the performance of its products and not on the level of its investment management fees relative to those of its competitors. In recent years, however, there has been a trend toward lower fees in the investment management industry. In order to maintain its fee structure in a competitive environment, Aston must be able to continue to provide clients with investment returns and services that make investors willing to pay its fees. In addition, the board of trustees of the mutual funds managed by Aston must make certain findings as to the reasonableness of these fees. We cannot be certain that Aston will succeed in providing investment returns and service that will allow it to maintain its current fee structure. Fee reductions on existing or future new business could have an adverse effect on our profit margins and results of operations.

Termination of Aston’s sub-advisory contracts could have a material adverse impact on the Aston Funds’ performance, and consequently, on our revenues and operating results.

As of December 31, 2006, Aston managed 20 no-load mutual funds, comprised of 16 equity funds and four fixed income funds, with approximately $5.5 billion of mutual fund assets under management. Aston currently utilizes nine different entities to manage the funds, of which five are affiliates of the sellers and four are independent. The sub-advisory contracts with the sellers’ affiliates, which are not terminable by the sub-advisers for five years from the consummation of the acquisition, include limited non-compete provisions and certain capacity guarantees in appropriate products to benefit the acquired business. While this arrangement is intended to ensure that the investment philosophy and process guiding the mutual funds in the future are consistent with their historical investment philosophy and process, there can be no assurances that this arrangement will remain in place. If one or more of these sub-advisory contracts is terminated, it could have a material adverse impact on the Aston Funds’ performance and on our revenues and operating results.

Aston depends on third-party distribution channels to market its investment products and access its client base. A substantial reduction in fees generated by third-party intermediaries could have a material adverse effect on its business.

The potential investor base for mutual funds and managed accounts is limited, and Aston’s ability to distribute mutual funds and access clients for managed accounts is highly dependent on access to the distribution systems and client bases of national and regional securities firms, banks, insurance companies, defined contribution plan administrators and other intermediaries, which generally offer competing internally and externally managed investment products. For open-end funds, such intermediaries are paid for their services to fund shareholders, in part, through Rule 12b-1 fees. Rule 12b-1 fees are those fees designated for promotions, sales, or any other activity connected with the distribution of the fund’s shares. In the case of no-load funds, Rule 12b-1 fees are usually, but not always, 0.25% of net assets and are used to cover advertising and marketing costs. Access to such distribution systems and client bases is substantially dependent upon our ability to charge Rule 12b-1 fees to our funds. To the extent that recent regulatory initiatives prohibit or limit the imposition of Rule 12b-1 or similar fees, our access to these distribution systems and client bases may be foreclosed in the future. To a lesser extent, the managed account business depends on referrals from financial planners and other professional advisers, as well as from existing clients. We cannot assure you that these channels and client bases will continue to be accessible to Aston. The inability to have such access could have a material adverse effect on our earnings.

While we expect Aston to continue to diversify and add new distribution channels for its mutual funds and managed accounts, a significant portion of the growth in the acquired business’ assets under management in recent years has been accessed through intermediaries. As of December 31, 2006, substantially all of the assets under management of the acquired business were attributable to accounts that it accessed through third-party intermediaries. These intermediaries generally may terminate their relationships on short notice. Loss of any of the distribution channels afforded by these intermediaries, and the inability to access clients through new distribution channels, could decrease assets under management and adversely affect our results of operations and growth. In addition, in the case of managed accounts offered through intermediaries to their customers, such intermediaries

7

Table of Contents

may reduce the fees that they remit to us as part of the arrangements they have with Aston. A substantial reduction in fees received from third-party intermediaries could have a material adverse affect on our business.

A change of control of our company would automatically terminate our investment management agreements with our clients, unless our managed account clients consent and, in the case of fund clients, the funds’ board of trustees and shareholders voted to continue the agreements.

Under the Investment Company Act, an investment management agreement with a fund must provide for its automatic termination in the event of its assignment. Under the Investment Advisers Act, a client’s investment management agreement may not be “assigned” by the investment adviser without the client’s consent. An investment management agreement is considered under both acts to be assigned to another party when a controlling block of the adviser’s securities is transferred. An assignment of our investment management agreements may occur if, among other things, we sell or issue a certain number of additional common shares in the future. We cannot be certain that our clients will consent to assignments of our investment management agreements or approve new agreements with us if a change of control occurs. This restriction may discourage potential purchasers from considering an acquisition of a controlling interest in Highbury.

If the adviser’s advisory contracts are assigned, the selling adviser may receive a benefit in connection with its sale of its business only if certain conditions are met.

If an adviser sells its business and, as a result, the adviser’s advisory contracts with registered investment companies are assigned, the selling adviser may receive a benefit in connection with its sale of its business only if certain conditions are met following the sale and assignment of the advisory contracts. Among these conditions is a requirement that no “unfair burden” be imposed on the investment companies as a result of the transaction. An unfair burden will be deemed to exist if, during the two years after the transaction, the predecessor or successor adviser or any interested person thereof is entitled to compensation from any person engaged in transactions with Highbury or from Highbury or its shareholders for other than bona fide advisory or administrative services. This restriction may discourage potential purchasers from considering an acquisition of a controlling interest in Highbury.

Investors in open-end funds can redeem their investments in these funds at any time without prior notice, which could adversely affect our earnings.

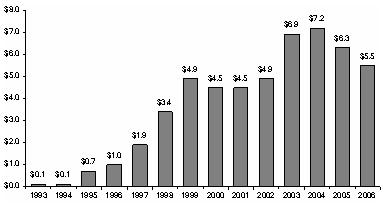

Open-end fund investors may redeem their investments in those funds at any time without prior notice. Investors may reduce the aggregate amount of assets under management for any number of reasons, including investment performance, changes in prevailing interest rates and financial market performance. Poor performance relative to other asset management firms tends to result in decreased purchases of mutual fund shares and increased redemptions of mutual fund shares. Cumulative net redemptions have reduced the mutual fund assets under management by the acquired business from $7.3 billion in 2004 to approximately $5.5 billion as of December 31, 2006, principally as a result of the net asset outflows in the Montag & Caldwell Growth Fund and the Veredus Aggressive Growth Fund, whose assets under management represent approximately 38% and 8% of the Aston Funds’ aggregate assets as of December 31, 2006. In a declining stock market, the pace of mutual fund redemptions could accelerate. The redemption of investments in mutual funds managed by the acquired business would adversely affect our revenues, which are substantially dependent upon the assets under management in our funds. If net redemptions of investments in the acquired business’ mutual funds increase, it would cause our revenues to decline, which would have a material adverse effect on our earnings.

A decline in the prices of securities, the performance of the Aston Funds or changes in investors’ preference of investing styles could lead to a decline in our assets under management, revenues and earnings.

Substantially all of our revenues are determined by the amount of assets under management. Under Aston’s investment advisory contracts with the Aston Funds, the investment management fee is typically based on the market value of assets under management. In addition, Aston receives asset-based distribution or service fees with respect to the open-end funds pursuant to distribution plans adopted under provisions of Rule 12b-1 under the Investment Company Act. Accordingly, a decline in the prices of securities generally may cause our revenues and net income to decline by either causing the value of our assets under management to decrease, which would result in lower investment advisory and Rule 12b-1 fees, or causing clients to withdraw funds in favor of investments or

8

Table of Contents

investment styles they perceive to offer greater opportunity or lower risk, which would also result in lower fees. For example, investors have withdrawn funds from the Montag & Caldwell Growth Fund and the Veredus Aggressive Growth Fund as a result of performance and changes in investors’ preferences for investing strategies. In addition, while the revenues of the acquired business are diversified across investment styles, the large capitalization growth style of investing accounts for approximately 54% of assets under management as of December 31, 2006. Large capitalization style implies a restriction imposed on the portfolio manager to select for investment by the fund predominantly equity securities of companies that have an average market capitalization of more than $10 billion and companies whose earnings are expected to grow at a rate that is above average for their industries or the overall market. The securities markets are highly volatile, and securities prices may increase or decrease for many reasons, including economic and political events and acts of terrorism beyond our control. If a decline in securities prices, fund performance or change in investors’ preference of investment styles were to cause our revenues to decline, it could have a material adverse effect on our earnings.

Loss of key employees could lead to the loss of clients and a decline in revenue.

Aston’s ability to attract and retain personnel is important to attracting and retaining its clients. The market for qualified wholesalers, senior managers, compliance professionals, marketing professionals, key managers at the sub-advisers and other professionals is competitive. We and the sub-advisers may not be successful in our efforts to recruit and retain the required personnel to maintain or grow our business. Loss of a significant number of key personnel could have an adverse effect on us.

Any significant limitation or failure of Aston’s software applications and other technology systems that are critical to its operations could constrain its operations.

Aston is highly dependent upon the use of various proprietary and third-party software applications and other technology systems to operate the business. Aston uses its technology to, among other things, provide reports and other customer services to its clients. Any inaccuracies, delays or systems failures in these and other processes could subject Aston to client dissatisfaction and losses. Although Aston takes protective measures, its technology systems may be vulnerable to unauthorized access, computer viruses or other events that have a security impact, such as an authorized employee or vendor inadvertently causing Aston to release confidential information, which could materially damage Aston’s operations or cause the disclosure or modification of sensitive or confidential information. Moreover, loss of confidential customer identification information could cause harm to our reputation. Aston relies heavily on software and technology that are licensed from, and supported, upgraded and maintained by, third-party vendors. A suspension or termination of certain of these licenses or the related support, upgrades and maintenance could cause temporary system delays or interruption. Potential system failures or breaches and the cost necessary to correct them could result in material financial loss, regulatory action, breach of client contracts, reputational harm or legal claims and liability, which in turn could negatively impact our revenues and income.

We could suffer losses in earnings or revenue if our reputation is harmed or the Aston brand name is not recognized.

Aston’s reputation is important to the success of Highbury. Aston has strong relationships with intermediaries and continuity of these relationships is based on the intermediaries’ trust and confidence in Aston. If Aston’s reputation is harmed, existing clients of Aston may reduce amounts held in, or withdraw entirely from, funds that Aston advises or funds may terminate their investment advisory contracts which could reduce the amount of assets under management of Aston and cause us to suffer a corresponding loss in earnings or revenues. Reputational harm may also cause Aston to lose employees, and we may be unable to continue to attract new employees with similar qualifications, motivations or skills. If we fail to address, or appear to fail to address, successfully and promptly, the underlying causes of any reputational harm, we may be unsuccessful in repairing any existing harm to our reputation, and our future business prospects would likely be affected.

Aston co-brands the Aston Funds with the names of the sub-advisers. For example, the ABN AMRO Montag & Caldwell Growth Fund has been re-named the Aston/Montag & Caldwell Growth Fund. If investors and intermediaries fail to recognize the re-branded funds, Aston may suffer losses in assets under management, which would negatively impact our revenues and financial results.

9

Table of Contents

We rely on a few major clients for a significant majority of our business, and the loss of any of these clients, or adverse developments with respect to the financial condition of any of our major clients could reduce our revenue.

Relationships with a limited number of clients account for a significant majority of our revenue. We expect that Aston’s relationships with these clients will continue to account for a substantial portion of our total revenue in future periods. Aston’s client, the Aston Funds, a Delaware business trust, which accounts for approximately 96% of our assets under management, is comprised of 20 mutual funds that are currently managed by Aston. Because all these funds have the same trustees, it is possible that the contracts with them could be terminated simultaneously. Of these 20 funds, Aston/ABN AMRO Growth, Aston/Montag & Caldwell Growth, Aston/Optimum Mid Cap and Aston/Veredus Aggressive Growth each account for more than 10% of the revenues of Aston. Additionally, the assets under management that Aston sources through independent financial advisers using Schwab and Fidelity, as custodians, each generate more than 10% of revenues received by Aston. These various client concentrations leave us vulnerable to any adverse change in the financial condition of any of our major clients. The loss of any of these relationships may have a material adverse impact on our revenues.

Risks Related to the Structure of our Business

The agreed-upon expense allocation under our revenue sharing arrangement with Aston may not be large enough to pay for all of Aston’s operating expenses.

Pursuant to the limited liability company agreement of Aston, we receive a specified percentage of Aston’s gross revenue, and a percentage of revenue is retained for use in paying Aston’s operating expenses. We may not have anticipated and reflected in the agreement possible changes in Aston’s revenue and expense base, and the agreed-upon expense allocation may not be large enough to pay for all of Aston’s operating expenses. We may elect to defer the receipt of our share of Aston’s revenue to permit Aston to fund such operating expenses, or we may restructure our relationship with Aston with the aim of maximizing the long-term benefits to us. We cannot be certain, however, that any such deferral or restructured relationship would be of any greater benefit to us. Such a deferral or restructured relationship might have an adverse effect on our near-term or long-term profitability and financial condition.

The failure to receive regular distributions from Aston will adversely affect us and our holding company structure will result in substantial structural subordination that may affect our ability to make payments on our obligations.

Because we are a holding company, we receive substantially all of our cash from distributions made to us by Aston. Aston’s payment of distributions to us may be subject to claims by Aston’s creditors and to limitations applicable to Aston under federal and state laws, including securities and bankruptcy laws. Additionally, Aston may default on some or all of the distributions that are payable to us. As a result, we cannot guarantee we will always receive these distributions from Aston. The failure to receive the distributions to which we are entitled under our limited liability company agreement with Aston and the Aston management team would adversely affect us, and may affect our ability to make payments on our obligations.

Our right to receive any assets of Aston upon its liquidation or reorganization, and thus the right of our stockholders to participate in those assets, typically would be subordinated to the claims of Aston’s creditors. In addition, even if we were a creditor of Aston, our rights as a creditor would be subordinated to any security interest and indebtedness of Aston that is senior to us.

Aston’s autonomy limits our ability to alter its day-to-day activities, and we may be held responsible for liabilities it incurs.

Although our limited liability company agreement with Aston gives us the authority to control or vote with respect to Aston’s business activities, we generally are not directly involved in managing its day-to-day activities, including satisfaction of the contractual terms of the advisory, sub-advisory and other contracts, product development, client relationships, compensation programs and compliance activities. As a consequence, our financial condition and results of operations may be adversely affected by problems stemming from the day-to-day operations of Aston.

10

Table of Contents

In addition, we may be held liable in some circumstances as a control person for the acts of Aston or its employees. For example, if Highbury exercises or refuses to exercise its approval right as the manager member to settle potential litigation or Aston issues securities in violation of laws and does not use due care in exercising this authority, Highbury may be exposed to liability related to Aston’s actions. While Highbury maintains directors’ and officers’ insurance and Aston maintains errors and omissions and general liability insurance in amounts believed to be adequate to cover certain potential liabilities, we may have claims that exceed the limits of available insurance coverage. Furthermore, insurers may not remain solvent, meet their obligations to provide coverage, or coverage may not continue to be available with sufficient limits and at a reasonable cost. A judgment against us or Aston in excess of available insurance coverage could have a material adverse effect on us.

Risks Relating to Ownership of our Warrants

If we are unable to maintain a current prospectus relating to the common stock underlying our warrants, our warrants may have little or no value and the market for our warrants may be limited.

No warrants will be exercisable and we will not be obligated to issue shares of common stock unless at the time a holder seeks to exercise such warrant, a prospectus relating to the common stock issuable upon exercise of the warrants is current and the common stock has been registered or qualified or deemed to be exempt under the securities laws of the state of residence of the holder of the warrants. Under the terms of the warrant agreement between Continental Stock Transfer & Trust Company, as warrant agent, and us, we have agreed to use our best efforts to maintain a current prospectus relating to the common stock issuable upon exercise of our warrants until the expiration of our warrants. However, we cannot assure you that we will be able to do so. If the prospectus relating to the common stock issuable upon exercise of the warrants is not current or if the common stock is not qualified or exempt from qualification in the jurisdictions in which the holders of the warrants reside, our warrants may not be exercisable before they expire, and we will not net-cash settle the warrants. Thus, our warrants may be deprived of any value. The market for our warrants may be limited, and the warrants may expire worthless and unredeemed. Even if warrant holders are not able to exercise their warrants because there is no current prospectus or the common stock is not qualified or exempt from qualification in the jurisdictions in which the holders of the warrants reside, we can exercise our redemption rights.

There is no currently effective prospectus relating to the common stock issuable upon exercise of the warrants because certain audited financial statements of the business we acquired that are required to be included in the prospectus were not available prior to the filing of our Annual Report on Form 10-K on March 23, 2007. This post-effective amendment is subject to review by the SEC and must be declared effective before the warrants may be exercised. We cannot be certain when the SEC will declare this post-effective amendment effective and no warrants may be exercised until it does so.

We may choose to redeem our outstanding warrants when a prospectus relating to the common stock issuable upon exercise of such warrants is not current and the warrants are not exercisable.

We may redeem the warrants issued as a part of our units (including warrants issued and outstanding as a result of the exercise of the option to purchase units granted to ThinkEquity Partners LLC, or TEP, and EarlyBirdCapital Inc., or EBC, the underwriters of our initial public offering, and the warrants sold in the private placement to insiders of Highbury simultaneously with our initial public offering, referred to throughout this prospectus as the private placement) at any time after the warrants become exercisable in whole and not in part, at a price of $0.01 per warrant, upon a minimum of 30 days’ prior written notice of redemption, if and only if, the last sales price of our common stock equals or exceeds $8.50 per share for any 20 trading days within a 30 trading day period ending three business days before we send the notice of redemption. Redemption of the warrants could force the warrant holders (i) to exercise the warrants and pay the exercise price therefor at a time when it may be disadvantageous for the holders to do so, (ii) to sell the warrants at the then current market price when they might otherwise wish to hold the warrants or (iii) to accept the nominal redemption price which, at the time the warrants are called for redemption, is likely to be substantially less than the market value of the warrants. In addition, we may exercise our right to redeem outstanding warrants when a prospectus relating to the common stock issuable upon the exercise of such warrants is not current, thus rendering the warrants unexercisable.

11

Table of Contents

Our securities are registered only in specific states, and you may not be able to exercise your warrants if you are not located in one of such states.

Your ability to exercise a warrant will depend on the availability of a state securities exemption for such exercise or on our having registered or qualified the offer and sale of the shares to be issued upon exercise of the warrant under the securities laws of the state in which you reside. We registered the sale of our securities, including the issuance of shares of common stock upon exercise of the warrants, in Colorado, Delaware, Illinois, Indiana, New York, Rhode Island and Wyoming. In addition, we have sold our securities in Hawaii, where both the initial sale and the exercise of warrants is exempt under Hawaii law. If you are a resident of any state other than the above referenced states, and there is no available exemption from the registration requirement of the state in which you reside, we may not be able to issue to you shares of common stock upon the exercise of your warrants. As such, the value of your warrant will be significantly reduced and the market for warrants in states for which we have not registered or qualified or received an exemption from state securities laws may be significantly impaired. Holders are not entitled to any cash settlement or other compensation as a result of their residency in any state in which we have not registered or qualified or received an exemption from state securities laws.

Our outstanding warrants may be exercised in the future, which would increase the number of shares eligible for future resale in the public market and result in dilution to our stockholders. This might have an adverse effect on the market price of the common stock.

Outstanding redeemable warrants to purchase an aggregate of 15,820,000 shares of common stock became exercisable on January 25, 2007. To the extent warrants are exercised, additional shares of our common stock will be issued, which will result in dilution to our stockholders and increase the number of shares eligible for resale in the public market. Sales of substantial numbers of such shares in the public market could adversely affect the market price of our shares.

Risks Related to Ownership of our Common Stock

If our stockholders who acquired their shares prior to our initial public offering exercise their registration rights, it may have an adverse effect on the market price of our common stock.

Our stockholders who acquired their shares prior to our initial public offering, or our initial stockholders, are entitled to demand that we register the resale of their 1,725,000 shares of common stock owned prior to our initial public offering. The holders of the majority of these shares may elect to exercise these registration rights at any time after the date on which their shares of common stock are released from escrow, which will be January 31, 2009. In addition, our initial stockholders hold 166,667 shares that they purchased in a private placement contemporaneously with our initial public offering that are now eligible for registration. If all these shares are registered, there will be an additional 166,667 shares of common stock eligible for trading in the public market (and potentially another 333,334 shares of common stock issuable to our initial stockholders upon exercise of warrants). The presence of this additional number of shares of common stock eligible for trading in the public market may have an adverse effect on the market price of our common stock.

Our securities are quoted on the OTC Bulletin Board, which limits the liquidity and price of our securities more than if our securities were quoted or listed on The Nasdaq Stock Market or a national exchange.

Our securities are traded in the over-the-counter market. They are quoted on the OTC Bulletin Board, an inter-dealer automated quotation system for equity securities sponsored and operated by the National Association of Securities Dealers, Inc., or NASD, but not included in The Nasdaq Stock Market. Quotation of our securities on the OTC Bulletin Board limits the liquidity and price of our securities more than if our securities were quoted or listed on The Nasdaq Stock Market or a national exchange. Lack of liquidity limits the price at which you are able to sell our securities or your ability to sell our securities at all.

12

Table of Contents

The market price for our common stock could be volatile and could decline, resulting in a substantial or complete loss of your investment.

The stock markets on which our common stock trades have experienced significant price and volume fluctuations. As a result, the market price of our common stock could be similarly volatile and investors in our common stock may experience a decrease in the value of their shares, including decreases unrelated to our operating performance or prospects. The price of our common stock could be subject to wide fluctuations in response to a number of factors, including:

| • | our operating performance and the performance of other similar companies; |

| • | actual or anticipated differences in our operating results; |

| • | changes in our revenues or earnings estimates or recommendations by securities analysts; |

| • | publication of research reports about us or our industry by securities analysts; |

| • | additions and departures of key personnel; |

| • | speculation in the press or investment community; |

| • | actions by institutional or other shareholders; |

| • | changes in accounting principles; |

| • | terrorist acts; and |

| • | general market conditions, including factors unrelated to our performance. |

Future sales of our common stock may depress the price of our common stock.

As of March 15, 2007, there were 9,527,000 shares of our common stock outstanding. If the unit purchase option is exercised for cash, there will be 336,667 additional shares of our common stock outstanding. If the warrants underlying the units underlying the unit purchase option are exercised, there will be 673,334 additional shares of our common stock outstanding. On January 25, 2007, 15,820,000 warrants became exercisable. If all 15,820,000 warrants are exercised, 15,820,000 additional shares of our common stock may be issued. Sales of a substantial number of these shares in the public market could decrease the market price of our common stock. In addition, the perception that such sales might occur may cause the market price of our common stock to decline. Future issuances or sales of our common stock could have an adverse effect on the market price of our common stock.

13

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD LOOKING STATEMENTS

We believe that some of the information in this prospectus constitutes forward-looking statements within the definition of the Private Securities Litigation Reform Act of 1995. You can identify these statements by forward-looking words such as “may,” “expect,” “anticipate,” “contemplate,” “believe,” “estimate,” “intends,” and “continue” or similar words. You should read statements that contain these words carefully because they:

| • | discuss future expectations; |

| • | contain projections of future results of operations or financial condition; or |

| • | state other “forward-looking” information. |

We believe it is important to communicate our expectations to our stockholders. However, there may be events in the future that we are not able to predict accurately or over which we have no control. The risk factors and cautionary language discussed in this prospectus provide examples of risks, uncertainties and events that may cause actual results to differ materially from the expectations described by us in such forward-looking statements, including among other things:

| • | the impact of legislative and regulatory actions and reforms and regulatory, supervisory or enforcement actions of government actions relating to us; |

| • | changes in political, economic or industry conditions, the interest rate environment or financial and capital markets, which could result in changes in demand for products or services or in the value of assets under management; |

| • | terrorist activities and international hostilities, which may adversely affect the general economy, financial and capital markets, specific industries, and us; |

| • | changing conditions in global financial markets generally and in the equity markets particularly, and decline or lack of sustained growth in these markets; |

| • | our business strategy and plans; |

| • | the introduction, withdrawal, success and timing of business initiatives and strategies; |

| • | harm to our reputation; |

| • | fluctuations in customer demand; |

| • | management of rapid growth; |

| • | the impact of fund performance on redemptions; |

| • | changes in investors’ preference of investing styles; |

| • | changes in or loss of sub-advisers; |

| • | the impact of increased competition; |

| • | the results of future financing efforts; |

| • | the impact of future acquisitions or divestitures; |

| • | the relative and absolute investment performance of our investment products; |

14

Table of Contents

| • | investment advisory agreements subject to termination or non-renewal; |

| • | a substantial reduction in fees received from third parties; |

| • | our success in finding or acquiring additional investment management firms on favorable terms and consummating acquisitions of investment management firms; |

| • | the ability to retain major clients; |

| • | the ability to attract and retain highly talented professionals; |

| • | significant limitations or failure of software applications; |

| • | expenses subject to significant fluctuations; and |

| • | the impact, extent and timing of technological changes and the adequacy of intellectual property protection. |

You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this prospectus.

All forward-looking statements included herein are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Except to the extent required by applicable laws and regulations, Highbury and Aston undertake no obligation to update these forward-looking statements to reflect events or circumstances after the date of this prospectus or to reflect the occurrence of unanticipated events.

15

Table of Contents

The amount of the proceeds we will receive from the shares covered by this prospectus depends on the number of warrants covered by this prospectus that are exercised. If all of the warrants are exercised, our gross proceeds from the sale of the shares of common stock pursuant to the exercise of the warrants will be $77,433,330. We expect net proceeds, which are what we will receive after paying the estimated expenses of this offering, to be approximately $77,333,330. For the purpose of estimating net proceeds, we estimate that our offering expenses in this offering will be approximately $100,000. See “Plan of Distribution,” below. We intend to use the net proceeds for working capital, or for other general corporate purposes. We may also use a portion of the net proceeds to fund acquisitions of investment management firms over time or to repurchase securities, if appropriate.

DETERMINATION OF OFFERING PRICE

The offering price for the shares covered by this prospectus is the exercise price of the warrants, which was determined at the time the warrants were issued. The exercise price of the warrants exercisable for the shares of common stock is $5.00 per share.

The securities covered by this prospectus will be distributed solely to existing warrantholders upon exercise of their warrants. The warrants are immediately exercisable as of the effective date of the registration statement. The shares of common stock issued upon exercise of the warrants will be freely tradable, except that sales by warrantholders who are our affiliates will be subject to Rule 144 as promulgated under the Securities Act.

We do not know if or when the warrants will be exercised. We also do not know whether any of the shares acquired upon exercise will be sold.

16

Table of Contents

The following table sets forth our capitalization at December 31, 2006 and as adjusted to give effect to the sale of our common stock and the application of the estimated net proceeds delivered from the sale of our common stock in this offering.

| December 31, 2006 | ||||||||

| Actual | Adjusted | |||||||

| (unaudited) | ||||||||

Total liabilities | $ | 2,511,559 | $ | 2,511,559 | ||||

Minority interest | 626,901 | 626,901 | ||||||

Common stock | ||||||||

Stockholders’ equity | ||||||||

Preferred stock, $0.0001 par value, 1,000,000 shares authorized; none issued and outstanding | — | — | ||||||

Common stock, $0.0001 par value, 50,000,000 shares authorized; 9,527,000 shares issued and outstanding, 25,013,666 shares issued and outstanding, as adjusted | 953 | 2,501 | ||||||

Additional paid-in capital | 56,693,484 | 134,025,266 | ||||||

Accumulated deficit | (12,465,658 | ) | (12,465,658 | ) | ||||

Total stockholders’ equity | 44,228,779 | 121,562,109 | ||||||

Total capitalization | $ | 47,367,239 | $ | 124,700,569 | ||||

17

Table of Contents

COMBINED FINANCIAL STATEMENTS

The following unaudited pro forma condensed combined statements of operations combine the historical statement of operations of Highbury for its fiscal year ended December 31, 2006 and the historical combined statement of operations of the acquired business for the eleven months ended November 30, 2006, the date of the acquisition, giving effect to the acquisition as if it had occurred on January 1, 2006. The unaudited pro forma condensed combined statements of operations assume Highbury’s initial public offering was consummated on the first day of the reporting period, so that the presentation of shares outstanding is consistent across the periods presented.

We are providing this information to aid you in your analysis of the financial aspects of our business. The unaudited pro forma condensed combined financial statements described above should be read in conjunction with the historical financial statements of Highbury and the historical combined statement of the acquired business and the related notes thereto. The unaudited pro forma information is not necessarily indicative of the financial position or results of operations that may have actually occurred had the acquisition taken place on the dates noted, or the future financial position or operating results of Highbury.

18

Table of Contents

UNAUDITED PRO FORMA CONDENSED COMBINED

STATEMENT OF OPERATIONS

JANUARY 1, 2006 - DECEMBER 31, 2006 (HIGHBURY)

JANUARY 1, 2006 – NOVEMBER 30, 2006 (ACQUIRED BUSINESS)

| Acquired Business | Highbury Financial Inc. | Pro Forma Adjustments | Pro Forma Combined | ||||||||||||

Revenue | $ | 38,476,882 | $ | 3,828,100 | $ | — | $ | 42,304,982 | |||||||

Distribution and sub-advisory fees | 28,830,231 | 1,796,910 | — | 30,627,141 | |||||||||||

| 9,646,651 | 2,031,190 | — | 11,677,841 | ||||||||||||

Operating expenses: | |||||||||||||||

Compensation and related expenses | 3,999,963 | 21,109,331 | — | 25,109,294 | |||||||||||

Other operating expenses | 3,552,847 | 1,162,875 | — | 4,715,722 | |||||||||||

Depreciation and other amortization | — | — | 88,057 | (a) | 88,057 | ||||||||||

| 7,552,810 | 22,272,206 | 88,057 | 29,913,073 | ||||||||||||

Operating income (loss) | 2,093,841 | (20,241,016 | ) | (88,057 | ) | (18,235,232 | ) | ||||||||

Non-operating income: | |||||||||||||||

Interest income (expense) | 314,695 | 1,744,907 | (1,744,907 | )(b) | 314,695 | ||||||||||

Income (loss) before minority interest and income taxes | 2,408,536 | (18,496,109 | ) | (1,832,964 | ) | (17,920,537 | ) | ||||||||

Minority interest | — | (6,647,715 | ) | (626,900 | )(c) | (7,274,615 | ) | ||||||||

Income (loss) before income taxes | 2,408,536 | (11,848,394 | ) | (1,206,064 | ) | (10,645,922 | ) | ||||||||

Income taxes – current | — | 702,088 | (702,088 | )(d) | 161,434 | ||||||||||

| 161,434 | (e) | ||||||||||||||

Income taxes – intangible-related deferred | — | 74,989 | 824,884 | (e) | 899,873 | ||||||||||

Income taxes – other deferred | — | (162,265 | ) | 162,265 | (d) | — | |||||||||

Net income (loss) | $ | 2,408,536 | $ | (12,463,206 | ) | $ | (1,652,559 | ) | $ | (11,707,229 | ) | ||||

Weighted average shares outstanding – basic and diluted | 9,045,773 | 9,527,000 | |||||||||||||

Net loss per share – basic and diluted | $ | (1.38 | ) | $ | (1.23 | ) | |||||||||

See notes to unaudited pro forma condensed combined financial statements.

19

Table of Contents

NOTES TO UNAUDITED PRO FORMA CONDENSED

COMBINED FINANCIAL STATEMENTS

PRO FORMA ADJUSTMENTS

Adjustments included in the column under the heading “Pro Forma Adjustments” include the following:

| a. | To reflect depreciation of fixed assets of the acquired business according to the following schedule: |

Type of Asset | Fair Value of Assets | Useful Life (years) | |||

Information technology | $ | 175,000 | 4 | ||

Furniture and equipment | 250,000 | 11 | |||

Other | 107,900 | 5 | |||

| $ | 532,900 | ||||

| b. | To reflect pro forma interest income earned by the combined business for the period presented. Highbury’s cash balances are eligible to earn interest, however, given the uncertainty regarding the use of cash after the acquisition, interest income earned by Highbury has been excluded and no interest income (in excess of interest income earned by the acquired business in the applicable period) has been included in the pro forma financial statements. |

| c. | To reflect Aston management’s 35% share of the membership interests in the acquired business. All items of income and loss have been allocated between Highbury and the Aston management members according to the terms of the Aston limited liability company agreement. Upon consummation of the acquisition, as a result of the amendment to the Aston limited liability company agreement to admit the Aston management members, Aston incurred a one-time, non-cash compensation charge of approximately $20.8 million. This non-recurring item is included in Highbury’s statement of operations and the accompanying pro forma statements of operations for the period ended December 31, 2006. |

| d. | To remove income taxes of Highbury as a stand-alone entity. |

| e. | Highbury’s estimated income tax liabilities for both GAAP and cash purposes are based on assumed federal and Colorado state income tax rates of 34.00% and 4.63%, respectively. Since Colorado state income taxes are deductible for federal income tax purposes, Highbury’s estimated effective tax rate is 37.06%. On the statement of operations, income taxes – current are equal to the total tax liability calculated on a cash basis. These calculations are shown in the following tables, and the results are indicated in the line entitled “total tax liability – current.” On the statement of operations, income taxes – deferred are equal to the difference between total tax liability calculated for GAAP purposes and the total tax liability calculated on a cash basis. These calculations are also shown in the following tables. The results of the calculations of the total tax liability calculated for GAAP purposes are indicated in the line entitled “Total tax liability (benefit) – GAAP” and the difference between these first two calculations is indicated in the line entitled “deferred tax liability (benefit).” |

This deferred tax liability is created as a result of the amortization of intangibles for cash tax purposes going forward. Highbury recorded goodwill and intangible assets to the balance sheet of the acquired business to reflect the value of the assets acquired in the acquisition. Highbury intends to amortize the intangible assets for income tax purposes which will reduce Highbury’s annual income taxes and create a recurring tax benefit. Furthermore, Highbury has determined that the acquired mutual fund client relationships meet the indefinite life criteria outlined in FAS No. 142, “Goodwill and Other Intangible Assets,” and as such, Highbury will not amortize these

20

Table of Contents

intangible assets for GAAP purposes, but will instead review these assets at least annually for impairment and to ensure the indefinite life conclusion is still appropriate. Highbury expects this difference in amortization schedules will create an annual deferred tax liability for GAAP purposes. Because Highbury does not anticipate impairment of the acquired assets in the future, Highbury does not expect this recurring tax benefit to reverse. Although the acquired business has historically provided a full valuation allowance for its deferred tax asset, Highbury will not make such a provision after the acquisition as a result of the increased profitability of the acquired business.

RECONCILIATION OF CURRENT AND DEFERRED INCOME TAXES

| Year Ended December 31, 2006 | ||||

Income (loss) before income taxes - GAAP | $ | (10,645,922 | ) | |

Permanent differences: | ||||

Compensation expense for grant of 35% interest in Aston | 20,784,615 | |||

Goodwill impairment | — | |||

Intangible asset impairment | — | |||

Minority interest adjustment | (7,274,615 | ) | ||

Taxable income – GAAP | 2,864,078 | |||

Colorado state income tax liability | 132,607 | |||

Federal income tax liability | 928,700 | |||

Total tax liability – GAAP | 1,061,307 | |||

Net income (loss) – GAAP | $ | (11,707,229 | ) | |

Income (loss) before income taxes – GAAP | $ | (10,645,922 | ) | |

Addback: compensation expense for grant of 35% interest in Aston | 20,784,615 | |||

Addback: goodwill impairment | — | |||

Addback: intangible asset impairment | — | |||

Less: minority interest adjustment | (7,274,615 | ) | ||

Less: goodwill amortization | (2,428,427 | ) | ||

Cash taxable income | 435,651 | |||

Colorado state income tax liability | 20,171 | |||

Federal income tax liability | 141,263 | |||

Total tax liability - current | 161,434 | |||

Deferred tax liability for goodwill amortization | 899,873 | |||

Total tax liability - GAAP | $ | 1,061,307 | ||

21

Table of Contents

SELECTED HISTORICAL CONSOLIDATED FINANCIAL OPERATING DATA

The following table sets forth our selected historical consolidated financial operating data as of the dates and for the periods indicated. The selected historical consolidated statements of income and balance sheets as of and for each of the fiscal years ended December 31, 2003, 2004 and 2005 and for the 11 month period ended November 30, 2006 for the acquired business and for the fiscal years ended December 31, 2005 and 2006 for Highbury are derived from, and are qualified in their entirety by, the historical financial statements of the acquired business and Highbury. Historical results are not necessarily indicative of the results to be expected in the future. You should read the following data together with “Business,” “Unaudited Pro Form Condensed Combined Financial Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the historical financial statements of the acquired business and Highbury and the related notes.

| Acquired Business | Highbury | Combined(5) | ||||||||||||||||||||||||||

| Year Ended December 31, 2003 | Year Ended December 31, 2004 | Year Ended December 31, 2005 | Eleven Months Ended November 30, 2006 | Period from July 13, 2005 (inception) to December 31, 2005 | Year Ended December 31, 2006 | Year Ended December 31, 2006 | ||||||||||||||||||||||

Statement of Income Data | ||||||||||||||||||||||||||||

Operating revenue | $ | 39,677,535 | $ | 49,247,963 | $ | 48,927,074 | $ | 38,476,882 | $ | — | $ | 3,828,100 | $ | 42,304,982 | ||||||||||||||

Distribution and advisory costs | $ | (33,531,069 | ) | $ | (40,918,617 | ) | $ | (40,405,752 | ) | $ | (28,830,231 | ) | $ | — | $ | (1,796,910 | ) | $ | (30,627,141 | ) | ||||||||

Compensation and related expenses | $ | (3,920,966 | ) | $ | (4,416,624 | ) | $ | (5,194,449 | ) | $ | (3,999,963 | ) | $ | — | $ | (21,109,331 | ) | $ | (25,109,294 | ) | ||||||||

Goodwill impairment | $ | — | $ | — | $ | (13,344,050 | ) | $ | — | $ | — | $ | — | $ | — | |||||||||||||

Intangible asset impairment | $ | — | $ | — | $ | (10,425,533 | ) | $ | — | $ | — | $ | — | $ | — | |||||||||||||

Other expenses | $ | (1,625,837 | ) | $ | (2,398,696 | ) | $ | (3,318,263 | ) | $ | (3,552,847 | ) | $ | (2,452 | ) | $ | (1,162,875 | ) | $ | (4,715,722 | ) | |||||||

Operating income (loss) | $ | 599,663 | $ | 1,514,026 | $ | (23,760,973 | ) | $ | 2,093,841 | $ | (2,452 | ) | $ | (20,241,016 | ) | $ | (18,147,175 | ) | ||||||||||

Interest income | $ | 20,432 | $ | 31,140 | $ | 133,524 | $ | 314,695 | $ | — | $ | 1,744,907 | $ | 2,059,602 | ||||||||||||||

Minority interest | $ | — | $ | — | $ | — | $ | — | $ | — | $ | 6,647,715 | $ | 6,647,715 | ||||||||||||||

Income taxes | $ | — | $ | — | $ | — | $ | — | $ | — | $ | (614,812 | ) | $ | (614,812 | ) | ||||||||||||

Net income (loss) | $ | 620,095 | $ | 1,545,166 | $ | (23,627,449 | ) | $ | 2,408,536 | $ | (2,452 | ) | $ | (12,463,206 | ) | $ | (10,054,670 | ) | ||||||||||

Earnings per share – basic and diluted | n/a | n/a | n/a | n/a | $ | (0.00 | ) | $ | (1.38 | ) | ||||||||||||||||||

Average shares outstanding – basic and diluted | n/a | n/a | n/a | n/a | 1,725,000 | 9,045,773 | ||||||||||||||||||||||

Balance Sheet Data | ||||||||||||||||||||||||||||

Cash and cash equivalents | n/a | $ | 3,158,266 | $ | 5,239,747 | $ | 7,966,323 | $ | 36,902 | $ | 6,248,705 | |||||||||||||||||

Accounts receivable | n/a | $ | 4,193,370 | $ | 4,074,486 | $ | 3,480,736 | $ | — | $ | 3,646,422 | |||||||||||||||||

Intangible assets(1) | n/a | $ | 56,333,333 | $ | 32,563,750 | $ | 32,563,750 | $ | — | $ | 36,426,412 | |||||||||||||||||

Other non-current assets | n/a | $ | 3,159 | $ | 1,635 | $ | 1,635 | $ | 483,492 | $ | 810,810 | |||||||||||||||||

22

Table of Contents

| Acquired Business | Highbury | Combined(5) | |||||||||||||||||||||||

| Year Ended December 31, 2003 | Year Ended December 31, 2004 | Year Ended December 31, 2005 | Eleven Months Ended November 30, 2006 | Period from July 13, 2005 (inception) to December 31, 2005 | Year Ended December 31, 2006 | Year Ended December 31, 2006 | |||||||||||||||||||

Total assets(2) | n/a | $ | 63,688,128 | $ | 41,879,618 | $ | 44,012,444 | $ | 520,394 | $ | 47,367,239 | ||||||||||||||

Liabilities | n/a | $ | 4,266,990 | $ | 3,869,502 | $ | 3,597,720 | $ | 497,846 | $ | 2,511,559 | ||||||||||||||

Senior debt | n/a | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||||||

Senior convertible debt | n/a | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||||||

Mandatory convertible securities | n/a | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||||||

Other long-term obligations | n/a | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||||||

Stockholders’ equity | n/a | $ | 59,421,138 | $ | 38,010,116 | $ | 40,414,724 | $ | 22,548 | $ | 44,228,779 | ||||||||||||||

Cash Flow Data | |||||||||||||||||||||||||

Operating activities | $ | 280,014 | $ | 1,420,696 | $ | (134,946 | ) | $ | 2,730,504 | — | $ | (12,229 | ) | ||||||||||||

Investing activities | $ | — | $ | — | $ | — | $ | — | — | $ | (36,923,503 | ) | |||||||||||||

Financing activities | $ | 1,407,219 | $ | (833,060 | ) | $ | 2,216,427 | $ | (3,928 | ) | $ | 36,902 | $ | 43,147,535 | |||||||||||

Other Financial Data | |||||||||||||||||||||||||

Adjusted EBITDA(3) | n/a | n/a | n/a | n/a | $ | (2,452 | ) | $ | 1,661,606 | ||||||||||||||||

Cash Net Income(4) | n/a | n/a | n/a | n/a | $ | (2,452 | ) | $ | 1,121,783 | ||||||||||||||||

Assets under management (at period end, in millions) | |||||||||||||||||||||||||

Mutual funds | $ | 6,906 | $ | 7,223 | $ | 6,329 | $ | 5,308 | $ | — | $ | 5,454 | |||||||||||||

Separate accounts | — | 22 | 149 | 119 | — | 199 | |||||||||||||||||||

Total | $ | 6,906 | $ | 7,245 | $ | 6,478 | $ | 5,427 | $ | — | $ | 5,653 | |||||||||||||

| (1) | Intangible assets have increased as a result of our acquisition of the U.S. mutual fund business of ABN AMRO on November 30, 2006. This acquisition is discussed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” |

| (2) | Total assets have increased as a result of our initial public offering which was consummated on January 31, 2006. Our initial public offering is discussed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” |

| (3) | Adjusted EBITDA means the sum of (a) net income determined in accordance with GAAP, plus (b) amortization of intangible assets, plus (c) interest expense, plus (d) depreciation, plus (e) other non-cash expenses, plus (f) taxes. This definition of Adjusted EBITDA is consistent with the definition of EBITDA used in our credit facility. We consider non-cash expenses to be expenses which we incur for financial reporting purposes for which there is no corresponding current or future cash expense. As a measure of liquidity, we believe that Adjusted EBITDA is useful as an indicator of our ability to service debt, make |

23

Table of Contents

new investments and meet working capital requirements. Adjusted EBITDA is not a measure of liquidity under GAAP and should not be considered an alternative to cash flow from operations. Adjusted EBITDA, as calculated by us, may not be consistent with computations of EBITDA by other companies. Our use of Adjusted EBITDA, including reconciliations to cash flow from operations and Net Income, is discussed in greater detail in “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” |

| (4) | Cash Net Income means the sum of (a) net income determined in accordance with GAAP, plus (b) amortization of intangible assets, plus (c) deferred taxes related to intangible assets, plus (d) affiliate depreciation, plus (e) other non-cash expenses. We consider Cash Net Income an important measure of our financial performance, as we believe it best represents operating performance before non-cash expenses relating to the acquisition of our interest in our affiliated investment management firm. Cash Net Income is not a measure of financial performance under GAAP and, as calculated by us, may not be consistent with computations of Cash Net Income by other companies. Our use of Cash Net Income, including a reconciliation of Cash Net Income to Net Income, is discussed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” |

| (5) | The information presented in the “Combined” column for 2006 is the arithmetic sum of the operating results of Highbury for the year ended December 31, 2006, which includes the acquired business’ results from December 1, 2006, and the operating results of the acquired business for the 11 months ended November 30, 2006, which is prior to the date of acquisition. No pro forma or other adjustments have been made in the presentation of the “Combined” financial results. |

24

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS