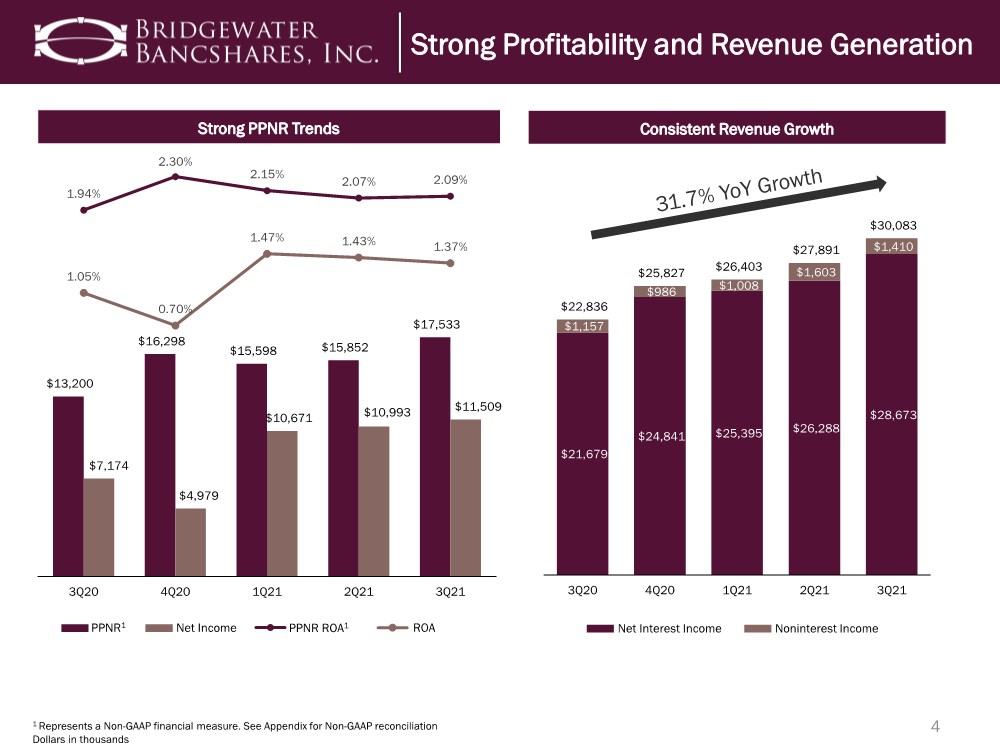

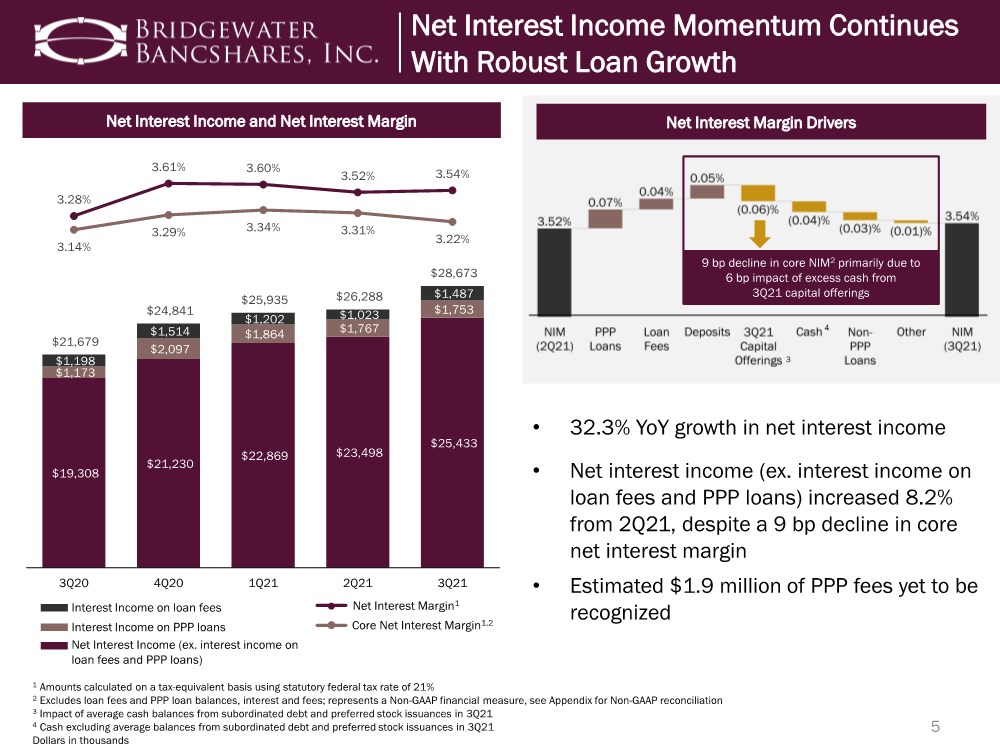

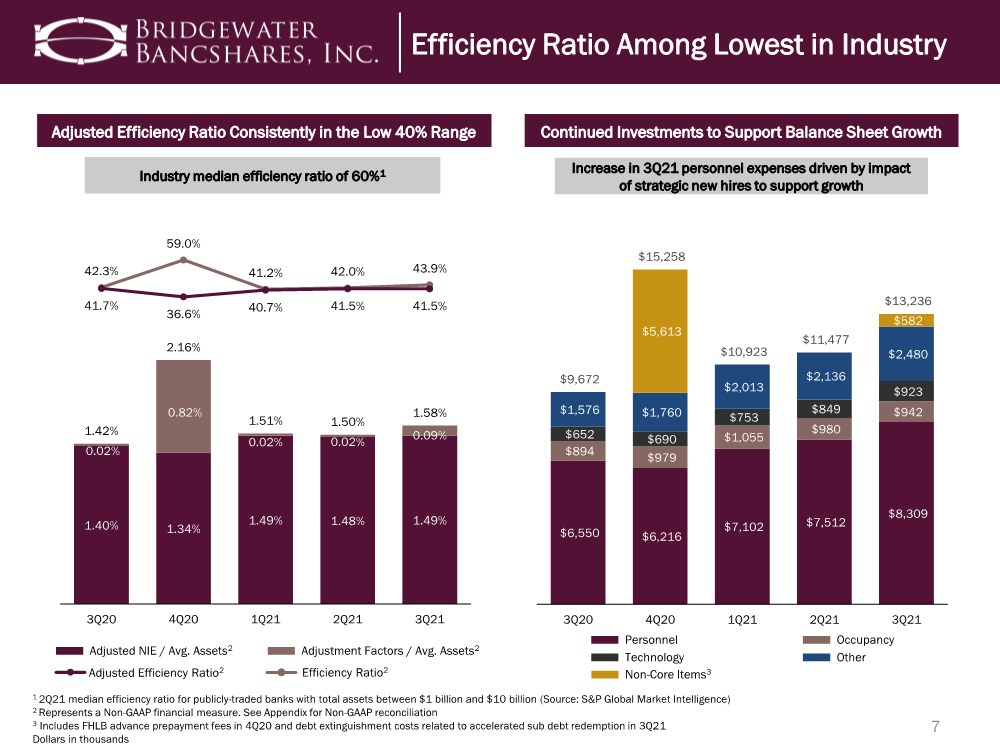

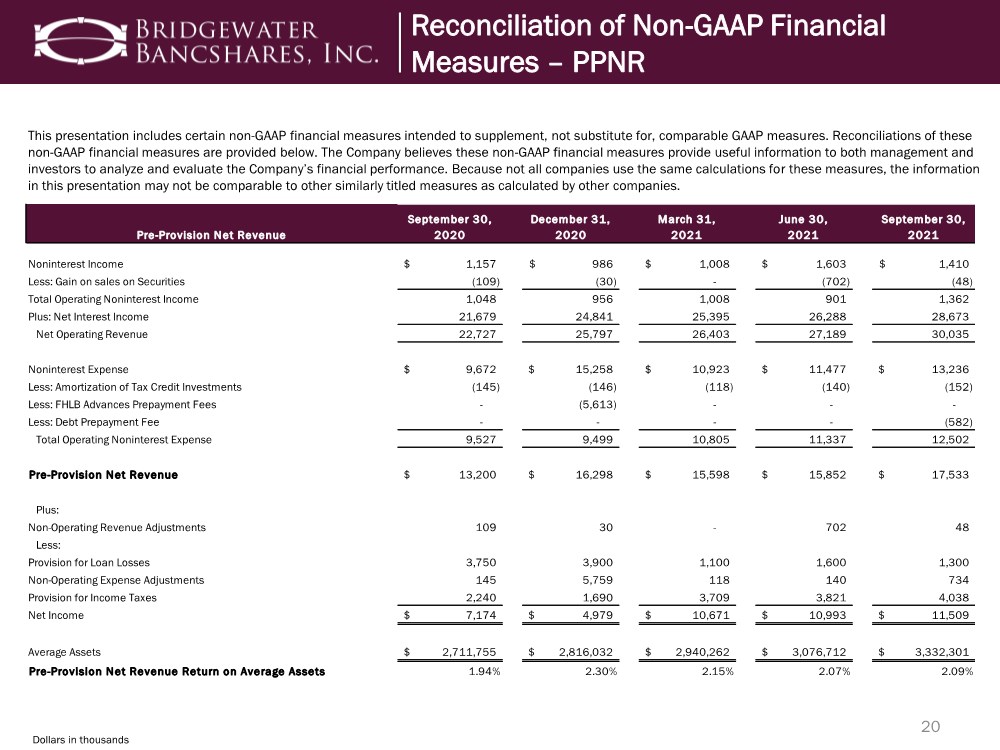

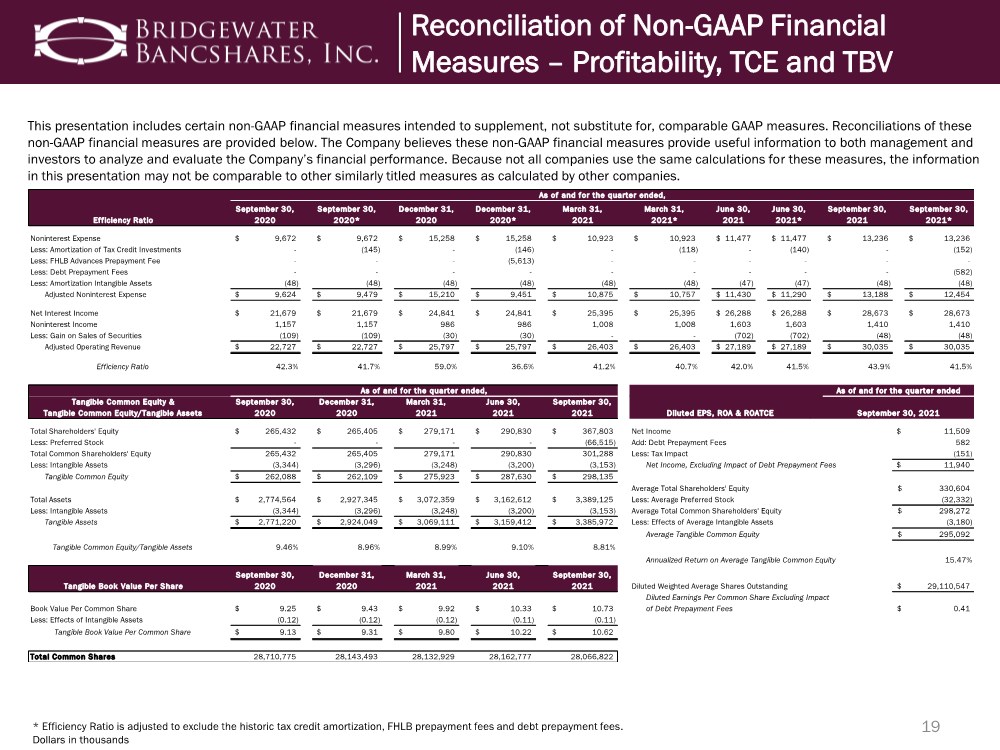

| 19 This presentation includes certain non-GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures. Reconciliations of these non-GAAP financial measures are provided below. The Company believes these non-GAAP financial measures provide useful information to both management and investors to analyze and evaluate the Company’s financial performance. Because not all companies use the same calculations for these measures, the information in this presentation may not be comparable to other similarly titled measures as calculated by other companies. * Efficiency Ratio is adjusted to exclude the historic tax credit amortization, FHLB prepayment fees and debt prepayment fees. Dollars in thousands Reconciliation of Non-GAAP Financial Measures – Profitability, TCE and TBV Efficiency Ratio September 30, 2020 September 30, 2020* December 31, 2020 December 31, 2020* March 31, 2021 March 31, 2021* June 30, 2021 June 30, 2021* September 30, 2021 September 30, 2021* Noninterest Expense 9,672 $ 9,672 $ 15,258 $ 15,258 $ 10,923 $ 10,923 $ 11,477 $ 11,477 $ 13,236 $ 13,236 $ Less: Amortization of Tax Credit Investments - (145) - (146) - (118) - (140) - (152) Less: FHLB Advances Prepayment Fee - - - (5,613) - - - - - - Less: Debt Prepayment Fees - - - - - - - - - (582) Less: Amortization Intangible Assets (48) (48) (48) (48) (48) (48) (47) (47) (48) (48) Adjusted Noninterest Expense 9,624 $ 9,479 $ 15,210 $ 9,451 $ 10,875 $ 10,757 $ 11,430 $ 11,290 $ 13,188 $ 12,454 $ Net Interest Income 21,679 $ 21,679 $ 24,841 $ 24,841 $ 25,395 $ 25,395 $ 26,288 $ 26,288 $ 28,673 $ 28,673 $ Noninterest Income 1,157 1,157 986 986 1,008 1,008 1,603 1,603 1,410 1,410 Less: Gain on Sales of Securities (109) (109) (30) (30) - - (702) (702) (48) (48) Adjusted Operating Revenue 22,727 $ 22,727 $ 25,797 $ 25,797 $ 26,403 $ 26,403 $ 27,189 $ 27,189 $ 30,035 $ 30,035 $ Efficiency Ratio 42.3% 41.7% 59.0% 36.6% 41.2% 40.7% 42.0% 41.5% 43.9% 41.5% Tangible Common Equity & Tangible Common Equity/Tangible Assets September 30, 2020 December 31, 2020 March 31, 2021 June 30, 2021 September 30, 2021 Total Shareholders' Equity 265,432 $ 265,405 $ 279,171 $ 290,830 $ 367,803 $ Net Income Less: Preferred Stock - - - - (66,515) Add: Debt Prepayment Fees Total Common Shareholders' Equity 265,432 265,405 279,171 290,830 301,288 Less: Tax Impact Less: Intangible Assets (3,344) (3,296) (3,248) (3,200) (3,153) Net Income, Excluding Impact of Debt Prepayment Fees Tangible Common Equity 262,088 $ 262,109 $ 275,923 $ 287,630 $ 298,135 $ Average Total Shareholders' Equity Total Assets 2,774,564 $ 2,927,345 $ 3,072,359 $ 3,162,612 $ 3,389,125 $ Less: Average Preferred Stock Less: Intangible Assets (3,344) (3,296) (3,248) (3,200) (3,153) Average Total Common Shareholders' Equity Tangible Assets 2,771,220 $ 2,924,049 $ 3,069,111 $ 3,159,412 $ 3,385,972 $ Less: Effects of Average Intangible Assets Average Tangible Common Equity Tangible Common Equity/Tangible Assets 9.46% 8.96% 8.99% 9.10% 8.81% Annualized Return on Average Tangiible Common Equity Tangible Book Value Per Share September 30, 2020 December 31, 2020 March 31, 2021 June 30, 2021 September 30, 2021 Diluted Weighted Average Shares Outstanding Diluted Earnings Per Common Share Excluding Impact Book Value Per Common Share 9.25 $ 9.43 $ 9.92 $ 10.33 $ 10.73 $ of Debt Prepayment Fees Less: Effects of Intangible Assets (0.12) (0.12) (0.12) (0.11) (0.11) Tangible Book Value Per Common Share 9.13 $ 9.31 $ 9.80 $ 10.22 $ 10.62 $ Total Common Shares 28,710,775 28,143,493 28,132,929 28,162,777 28,066,822 (32,332) (3,180) 15.47% As of and for the quarter ended, As of and for the quarter ended, As of and for the quarter ended September 30, 2021 Diluted EPS, ROA & ROATCE 295,092 $ 29,110,547 $ 11,509 $ 582 (151) 11,940 $ 330,604 $ 298,272 $ 0.41 $ |