UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(RULE 14A-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| x | Definitive Additional Materials |

| ¨ | Soliciting Material Pursuant to §240.14a-12 |

Morgans Hotel Group Co.

(Exact Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ¨ | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

On June 3, 2013, Morgans Hotel Group Co., in connection with its 2013 Annual Meeting scheduled to be held on June 14, 2013, issued a press release relating to a letter distributed to shareholders identifying serious deficiencies in OTK Associates, LLC’s slate of director nominees. A copy of the press release is set forth below.

MORGANS HOTEL GROUP IDENTIFIES SERIOUS DEFICIENCIES IN OTK’S SLATE OF

NOMINEES THAT THREATEN SHAREHOLDER VALUE

OTK’s Nominees Are a Highly Conflicted Group of Family, Family Employees and Family Friends

Taubman and Olshan Families Seek to Take Control of Morgans without Paying a Premium

Morgans Urges Shareholders to Protect Their Investment by Voting the WHITE Proxy Card

NEW YORK, June 3, 2013 – Morgans Hotel Group Co. (NASDAQ: MHGC) (“Morgans” or the “Company”) today issued a letter to shareholders in connection with its 2013 Annual Meeting scheduled to be held on June 14, 2013. The text of the June 3 letter follows:

Dear Fellow Morgans Hotel Group Shareholder:

YOUR VOTE IS IMPORTANT – VOTE THE WHITE PROXY CARD TODAY

Your vote at the June 14, 2013 Morgans Hotel Group Annual Meeting is critical to the future of your investment.

THE TAUBMAN AND OLSHAN FAMILIES, THROUGH THEIR JOINTLY OWNED, SINGLE-PURPOSE VEHICLE, OTK ASSOCIATES, LLC (“OTK”), SEEK TO PLACE THEIR CHILDREN AT THE HELM OF MORGANS WHILE OFFERING NO CREDIBLE PLAN TO CREATE VALUE FOR SHAREHOLDERS.

There are serious deficiencies in the slate of directors nominated by a dissident shareholder named OTK, a vehicle controlled by the Taubman and Olshan families.

| • | The OTK slate isnot independent of OTK – it is a highly conflicted group of family, family employees and family friends beholden to the Olshan and Taubman families. |

| • | The Taubman and Olshan families seek to control Morgans’ Board with family members who are inexperienced and inappropriate to be directors of a public company, and whose only experience has been in furthering family interests in hand-picked roles at family-controlled businesses. |

| • | We believe that OTK and its nominees clearly do not understand the luxury, boutique hotel market in which Morgans operates. |

The election of this slate would turn the control of the Board over to the Olshan and Taubman families and their interests.

A closer look at the motivations of Taubman and Olshan controlled-OTK reveals that its own interests arenot aligned with those of the Company’s other shareholders and that it is not proposing a slate that will maximize value for all shareholders.

Filling Board Seats with Family –OTK rejected our offer of two Board seats and instead launched a costly proxy contest to fill all seven Board seats with its family (3), family employees (1) and family friends (3). We do not believe that such a slate of directors could act independently of the interests of OTK and the Olshan and Taubman families. This underscores the fact that OTK is attempting to take control of the Board to achieve its own objectives but without paying a premium or any other compensation to shareholders.

Personal Revenge and Objectives – OTK launched the proxy contest after an inexperienced and unqualified 34-year old Taubman trust fund heir, Jason Taubman Kalisman, was told he wouldn’t be handed the Morgans Board Chairmanship on the basis of his family’s influence alone. The Taubman and Olshan families that control OTK are now set on installing their heirs at the helm of our Company through an expensive and in our view unnecessary proxy contest.

Misaligned Cost Basis – OTK entered Morgans’ stock at an average cost of approximately $15.20 per share, raising serious questions about whether it would support a sale of the Company or other strategic transaction at a value below $15.20 per share. We are also concerned that OTK would not consider a sale or other value-maximizing alternative at a price that would publicly show a loss on itssole investment.

OTK: THE FAMILY TRUST FUND WITH A SINGLE INVESTMENT

Some of our shareholders have asked us “Who is OTK?” We thought it important to answer this question publicly in order to inform all of our shareholders of the facts about OTK.

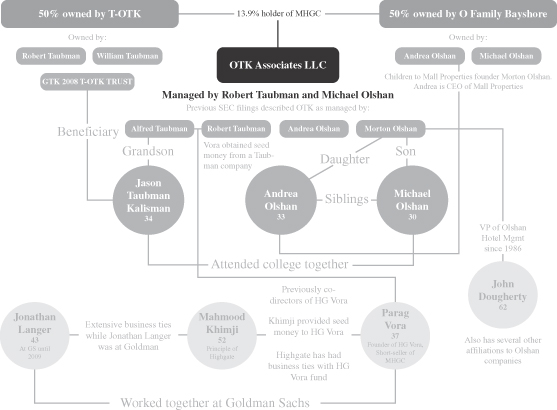

According to its own filings, OTK isa family partnership controlled 50% by the Olshan family and 50% by the Taubman family. The Olshan and Taubman families have been doing business and investing together for generations. According to an April 2013 Wall Street Journal article, “OTK’s origins go back four decades, when Mr. Olshan’s father, Mort Olshan, and Taubman family patriarch, A. Alfred Taubman, built the Fair Oaks Mall in Fairfax, Va. The next generation now oversees OTK, with Michael Olshan and Robert Taubman as managing principals.”

However, OTK is not an investment advisor, investment fund or other professional enterprise. OTK has no investment other than its position in Morgans’ common stock at an average cost basis of $15.20 per share. OTK claims it is “not an activist investor,” but it is currently taking an activist position in its only investment and several members of its slate of nominees have launched activist campaigns against other companies in the past.

The families now propose that the children (30-year old Michael Olshan, 33-year old Andrea Olshan and 34-year old Jason Taubman Kalisman) have the experience necessary to run Morgans’ Board. It is not clear to us why being a beneficiary of OTK’s family wealth and trust funds qualifies the heirs of Mort Olshan and Robert Taubman to serve as directors of Morgans.

OTK NOMINEES: THE CHILDREN, THE EMPLOYEE, THE SHORT-SELLER AND THE INTERDEPENDENTS

The Children

Michael Olshan – no experience outside of managing the family money. One of his claims is being a “manager” of OTK but by his own admission, this investment was acquired in 2008, and OTK has not sold a share and it has no other investments. We have difficulty understanding how being the beneficiary of a family investment qualifies as “management” experience. Mr. Olshan also manages family money through O-Cap Management LP, which has a track-record of activist investing but with mixed investment results.

Andrea Olshan – no experience outside of thefamily mall business. Her first reported job after college was “Chief Operating Officer” of the family business – when she was just 28 years old.

Jason Taubman Kalisman – the current OTK representative on the Morgans Board. Jason describes himself as a “founder” of OTK; however, in reality he wasbeneficiary of a family trust fund that is an indirect owner of OTK.

Other than Mr. Kalisman’s serving on our Board as OTK’s representative, the Olshan and Taubman family children have no relevant business, industry or public company experience that would qualify them to serve as directors of Morgans or any other public company. None of them have held a senior business position at any company other than to promote family business or investment interests.

The Employee

John Dougherty – has been the Vice President and Director of Olshan Hotel Management, an Olshan family business that operates a small number of hotels, since 1986. The hotels that Mr. Dougherty oversees for the Olshan family arenot luxury hotels, and his experience does not obviously translate to the luxury boutique hotel market in which Morgans operates.

But more importantly, Mr. Dougherty’s livelihood depends on the Olshan family. It is hard to imagine how Mr. Dougherty, a 25+ year employee of the Olshan family business, will exercise any independent judgment other than acting in the interests of OTK and the Olshans. He and the Olshan and Taubman family children will constitute a majority of the Board if OTK achieves its family goal.

We do not believe that the children and the long-time family employee can be expected to do anything other than represent OTK’s interests and do what Mort Olshan and Robert Taubman instruct them to do.

The Short-Seller

Parag Vora – the founder of a hedge fund in which the Taubman family is an investor. According to OTK’s proxy statement, Mr. Vora’s hedge fund executed more than 100 transactions in the Company’s stock, including many day-trades and short-sales over the last two years.

The Taubman investment in Mr. Vora’s hedge fund creates an apparent conflict of interest and would appear to undermine the ability of Mr. Vora to act as an independent director not beholden to the Taubman family. Unsurprisingly, Mr. Vora also has direct business ties to Mahmood Khimji, another OTK nominee, who has been a minority shareholder of HG Vora since its formation, an investor in the HG Vora funds and a director of HG Vora funds from 2009 to 2012.

Other Interdependents

Jonathan Langer – the former Goldman Sachs executive responsible for overseeing the firm’s proprietary real estate investment effort, including the Whitehall Street Real Estate Funds, which announced awrite down of $2.1 billion of the $3.7 billion invested between May 2007 and August 2008. Another one of his investments, American Casino & Entertainment Properties LLC (“ACEP”), where Mr. Langer was a director (and the initial investment into which Mr. Langer had championed in February 2008), posted anet loss of $31.4 million in 2009. Mr. Langer departed Goldman Sachs soon after this loss in 2009 to “pursue other opportunities.”

Again, unsurprisingly, Mr. Langer has extensive business ties to one of OTK’s other nominees, Mr. Khimji, including multiple related party dealings while Mr. Langer was a director of ACEP. Mr. Langer also used to work with another OTK nominee, Mr. Vora, at Goldman Sachs.

Mahmood Khimji – the co-founder of Highgate Holdings, a private hotel company. Highgate previously approached Morgans to make a proposal to take over the operations of Morgans’ hotel assets. The Board turned down a proposal that would have effectively handed over the management business to Highgate because the Board determined that the proposal was not in the best interests of shareholders.

Mr. Khimji shares offices with Mr. Vora and is an investor in his fund. Mr. Khimji also has long-standing business ties to Mr. Langer, which included consulting agreements with two public companies – ACEP and Colony Resorts LVH – while Mr. Langer was a director of these companies in 2009.

OTK’S SLATE IS CONFLICTED AND BEHOLDEN TO THE TAUBMAN AND OLSHAN FAMILIES

Turning control of the Board over to OTK’s proposed slate of nominees will effectively turn control of the Board over to OTK and the Olshan and Taubman families. The family and business ties that crisscross OTK’s slate demonstrate that the nominees are not remotely independent of their nominating shareholder. Morgans’ Board does not believe turning full control of the Board over to a 13.9% owner is in the best interests of all shareholders.

OTK’S COMMENTS REVEAL IT AND ITS PROPOSED SLATE DO NOT UNDERSTAND THE BOUTIQUE LUXURY HOTEL BUSINESS

Most importantly, OTK offers no credible plan for Morgans shareholders. The reality – it offers inexperienced directors, potential disruption to our business and significant downside risk.OTK’s nominees simply do not understand the luxury, boutique hotel business that Morgans operates, as evidenced by their comments and proposed slate of inexperienced nominees.

Each of our new boutique hotel projects starts as a blank canvass that requires our creative team to develop the concept, themes, layout and architectural design of the hotel with our partners that will bring a unique artistic and hip element to the hotel that will set it apart from the ordinary chain hotels. OTK’s comments illustrate to us that they have no idea what it takes to create a luxury brand.

OTK’S SLATE WOULD DIMINISH THE VALUE OF MORGANS’ BRANDS

Mr. Dougherty, the Olshan employee director nominee, has experience operating Courtyard by Marriott and other ordinary hotel brands –not luxury boutique hotels.Khimji’s Highgate Holdings similarly is an operator of hotels, but has only limited exposure to our luxury boutique hotel market segment.Their suggestion that that they are only interested in hotel projects with no or minimal capital outlay suggests that they have no understanding of our distinct brands, how this high-end segment of the hotel market operates or the intense competition for these

high-end projects. Our competitors certainly understand this and also offer and make significant key-money investments in their major high-end projects in key gateway cities worldwide.

Our management team has been able to negotiate eight new hotel projects with limited capital investment, attractive return on investment metrics, and long-term secure management agreements. Turning the entire Company over to OTK‘s proposed slate of nominees would disrupt the strategy and the work that the Board and its new management team has accomplished to transition Morgans into a world-class boutique brand and hotel management company.

Further, OTK’s suggestion that Morgans’ management agreements are not long-term and are cancellable at interim periods is simply and demonstrably false. This is something that Jason Taubman Kalisman knows – or should know – from representing OTK on our Board. Our new management contracts, negotiated by our new management team, are long-term – averaging 20+ years – and are not cancellable at interim periods. Our chief development officer has over 15 years of experience negotiating long-term hotel management agreements in accordance with industry best practices, and OTK’s suggestion that our management contracts are cancellable at interim periods or are otherwise not consistent with industry best practices, is simply false.

We believe the OTK nominees, if elected, would disrupt the momentum and progress that the Company has achieved in the last two years in its transition to a best-in-class brand and management platform in the luxury, high-end segment of the market. OTK is launching anopportunistic campaign as the Company is at its inflection point, with our first quarter results clearly demonstrating that the strategy the Board implemented in 2011, and that OTK and Jason Taubman Kalisman supported until Kalisman was not handed Chairmanship, is yielding significant results. The market has begun to appreciate management’s transition of the business, with the stock up approximately 75% over the past year. We believe the best is yet to come if we continue on this path.

YOUR VOTE IS IMPORTANT – VOTE THE WHITE PROXY CARD TODAY

The Taubman and Olshan families, through their jointly owned single-purpose vehicle, OTK Associates, seek to place their children at the helm of Morgans while offering no credible plan to create value for shareholders. They now conveniently seek to take full and complete control of Morgans at the very point in time when the strategic investments undertaken by the current management team are beginning to drive significant improvements in financial performance and growth of our pipeline of new hotel agreements.

To protect your investment, vote the WHITE proxy card for the highly qualified and experienced Morgans director nominees. Your vote is critical to ensure Morgans’ Board can continue its drive to maximize value for all shareholders.

Whether or not you plan to attend the Annual Meeting, you have the opportunity to protect your investment by promptly voting the WHITE PROXY CARD. We urge you to vote today by telephone, by Internet, or by signing, dating and returning the enclosed WHITE PROXY CARD in the postage-paid envelope provided.

On behalf of the Board of Directors, we thank you for your continued support.

Sincerely,

Michael Gross

Chief Executive Officer

ABOUT MORGANS HOTEL GROUP

Morgans Hotel Group Co. (NASDAQ: MHGC) is widely credited as the creator of the first “boutique” hotel and a continuing leader of the hotel industry’s boutique sector. Morgans Hotel Group operates Delano in South Beach and Marrakech, Mondrian in Los Angeles, South Beach and New York, Hudson in New York, Morgans and

Royalton in New York, Shore Club in South Beach, Clift in San Francisco, Ames in Boston and Sanderson and St Martins Lane in London. Morgans Hotel Group has ownership interests or owns several of these hotels. Morgans Hotel Group has other property transactions in various stages of completion, including Delano properties in Las Vegas, Nevada; Cesme, Turkey and Moscow, Russia; Mondrian properties in London, England; Istanbul, Turkey; Doha, Qatar and Baha Mar in Nassau, The Bahamas; and a Hudson in London, England. Morgans Hotel Group also owns a 90% controlling interest in The Light Group, a leading lifestyle food and beverage company. For more information please visit www.morganshotelgroup.com.

FORWARD-LOOKING AND CAUTIONARY STATEMENTS

This letter may contain certain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements relate to, among other things, the operating performance of our investments and financing needs. Forward-looking statements are generally identifiable by use of forward-looking terminology such as “may,” “will,” “should,” “potential,” “intend,” “expect,” “endeavor,” “seek,” “anticipate,” “estimate,” “overestimate,” “underestimate,” “believe,” “could,” “project,” “predict,” “continue” or other similar words or expressions. These forward-looking statements reflect our current views about future events and are subject to risks, uncertainties, assumptions and changes in circumstances that may cause our actual results to differ materially from those expressed in any forward-looking statement. Important risks and factors that could cause our actual results to differ materially from those expressed in any forward-looking statements include, but are not limited to economic, business, competitive market and regulatory conditions such as: a sustained downturn in economic and market conditions, both in the U.S. and internationally, particularly as it impacts demand for travel, hotels, dining and entertainment; our levels of debt, our ability to refinance our current outstanding debt, repay outstanding debt or make payments on guaranties as they may become due, our ability to access the capital markets and the ability of our joint ventures to do the foregoing; our history of losses; our ability to compete in the “boutique” or “lifestyle” hotel segments of the hospitality industry and changes in the competitive environment in our industry and the markets where we invest; our ability to protect the value of our name, image and brands and our intellectual property; risks related to natural disasters, terrorist attacks, the threat of terrorist attacks and similar disasters; and other risk factors discussed in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2012, which was filed with the Securities and Exchange Commission (the “SEC”) on March 6, 2013, as amended by the Form 10-K/A filed on April 30, 2013, and other documents filed by the Company with the SEC from time to time. All forward-looking statements in this letter are made as of the date hereof, based upon information known to management as of the date hereof, and the Company assumes no obligations to update or revise any of its forward-looking statements even if experience or future changes show that indicated results or events will not be realized.

IMPORTANT ADDITIONAL INFORMATION

On May 23, 2013, the Company filed a definitive proxy statement and WHITE proxy card with the SEC in connection with the solicitation of proxies for its 2013 Annual Meeting of Stockholders. Stockholders are strongly advised to read the Company’s 2013 proxy statement because it contains important information. Stockholders may obtain a free copy of the 2013 proxy statement and other documents that the Company files with the SEC from the SEC’s website at www.sec.gov or the Company’s website at www.morganshotelgroup.com.

CONTACTS

Investors:

Richard Szymanski, Morgans Hotel Group Co., (212) 277-4188

Richard H. Grubaugh, D.F. King & Co., Inc., (212) 493-6950, rgrubaugh@dfking.com

Media:

Lex Suvanto or Neil Maitland, Abernathy MacGregor, (212) 371-5999, lex@abmac.com or nam@abmac.com