UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21835

Name of Fund: BlackRock Long-Term Municipal Advantage Trust (BTA)

Fund Address: 100 Bellevue Parkway, Wilmington, DE 19809

Name and address of agent for service: John M. Perlowski, Chief Executive Officer, BlackRock Long-Term Municipal Advantage Trust, 55 East 52nd Street, New York, NY 10055

Registrant’s telephone number, including area code: (800) 882-0052, Option 4

Date of fiscal year end: 04/30/2017

Date of reporting period: 10/31/2016

Item 1 – Report to Stockholders

OCTOBER 31, 2016

| | | | |

SEMI-ANNUAL REPORT (UNAUDITED) | | | |  |

BlackRock Investment Quality Municipal Trust, Inc. (BKN)

BlackRock Long-Term Municipal Advantage Trust (BTA)

BlackRock Municipal 2020 Term Trust (BKK)

BlackRock Municipal Income Trust (BFK)

BlackRock Strategic Municipal Trust (BSD)

|

| Not FDIC Insured • May Lose Value • No Bank Guarantee |

| | | | | | |

| | | | | | | |

| 2 | | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | |

Dear Shareholder,

Central bank policy decisions have continued to provide support to financial markets, while changing economic outlooks and geopolitical risks have been major drivers of investor sentiment. After ending its near-zero interest rate policy at the end of 2015, the Federal Reserve (the “Fed”) remained in focus as investors considered the anticipated pace of future rate hikes. With the European Central Bank and the Bank of Japan having moved into stimulus mode, the divergence in global monetary policies drove heightened market volatility at the beginning of 2016 and caused the U.S. dollar to strengthen considerably.

Financial markets had a rough start to the year as the strong dollar challenged U.S. companies that generate revenues overseas and pressured emerging market currencies and commodities prices. Low and volatile oil prices and signs of slowing growth in China were also meaningful factors behind the decline in risk assets early in the year. However, as the first quarter wore on, these pressures abated and a more tempered outlook for U.S. rate hikes helped the markets rebound.

Volatility spiked in late June when the United Kingdom shocked investors with its vote to leave the European Union. Uncertainty around how the British exit might affect the global economy and political landscape drove investors to high-quality assets, pushing already low global yields to even lower levels. However, risk assets recovered swiftly in July as economic data suggested that the consequences had thus far been contained to the United Kingdom.

In a second episode of surprise vote results, equities fell sharply after the news of Donald Trump’s victory in the U.S. presidential election, but quickly recovered, and the yield curve steepened due to expectations for rising inflation. Broadly, a reflation theme has been building amid signs of rising price pressures, central banks signaling a greater tolerance to let inflation run hotter, and policy emphasis shifting from monetary to fiscal stimulus.

At BlackRock, we believe investors need to think globally, extend their scope across a broad array of asset classes and be prepared to adjust accordingly as market conditions change over time. We encourage you to talk with your financial advisor and visit blackrock.com for further insight about investing in today’s markets.

Sincerely,

Rob Kapito

President, BlackRock Advisors, LLC

Rob Kapito

President, BlackRock Advisors, LLC

| | | | | | | | |

| Total Returns as of October 31, 2016 | |

| | | 6-month | | | 12-month | |

U.S. large cap equities

(S&P 500® Index) | | | 4.06 | % | | | 4.51 | % |

U.S. small cap equities

(Russell 2000® Index) | | | 6.13 | | | | 4.11 | |

International equities

(MSCI Europe, Australasia,

Far East Index) | | | (0.16 | ) | | | (3.23 | ) |

Emerging market equities

(MSCI Emerging Markets Index) | | | 9.41 | | | | 9.27 | |

3-month Treasury bills

(BofA Merrill Lynch 3-Month

U.S. Treasury Bill Index) | | | 0.17 | | | | 0.31 | |

U.S. Treasury securities

(BofA Merrill Lynch

10-Year U.S. Treasury

Index) | | | 0.46 | | | | 4.24 | |

U.S. investment grade bonds

(Bloomberg Barclays U.S.

Aggregate Bond Index) | | | 1.51 | | | | 4.37 | |

Tax-exempt municipal

bonds (S&P Municipal

Bond Index) | | | 0.98 | | | | 4.53 | |

U.S. high yield bonds

(Bloomberg Barclays U.S. Corporate High Yield 2% Issuer

Capped Index) | | | 7.59 | | | | 10.16 | |

| Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. | |

| | | | | | |

| | | | | | | |

| | THIS PAGE NOT PART OF YOUR FUND REPORT | | | | 3 |

| | |

| Municipal Market Overview | | |

|

| For the Reporting Period Ended October 31, 2016 |

Municipal Market Conditions

Municipal bonds generated positive performance for the period, due to falling interest rates and a favorable supply-and-demand environment. Interest rates were volatile late in 2015 (bond prices rise as rates fall) leading up to a long-awaited rate hike from the U.S. Federal Reserve (the “Fed”) that ultimately came in December. However, ongoing reassurance from the Fed that rates would be increased gradually and would likely remain low overall resulted in strong demand for fixed income investments. Investors favored the relative yield and stability of municipal bonds amid bouts of volatility resulting from uneven U.S. economic data, volatile oil prices, global growth concerns, geopolitical risks (particularly the United Kingdom’s decision to leave the European Union and the contentious U.S. election), and widening central bank divergence — i.e., policy easing outside the United States while the Fed was posturing to commence policy tightening. During the 12 months ended October 31, 2016, municipal bond funds garnered net inflows of approximately $61 billion (based on data from the Investment Company Institute).

For the same 12-month period, total new issuance remained robust from a historical perspective at $439 billion (significantly above the $420 billion issued in the prior 12-month period). A noteworthy portion of new supply during this period was attributable to refinancing activity (roughly 60%) as issuers continued to take advantage of low interest rates and a flatter yield curve to reduce their borrowing costs.

|

S&P Municipal Bond Index |

Total Returns as of October 31, 2016 |

6 months: 0.98% |

12 months: 4.53% |

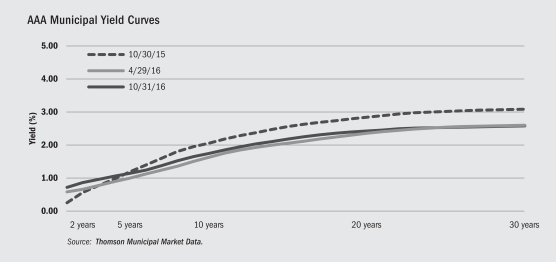

A Closer Look at Yields

From October 31, 2015 to October 31, 2016, yields on AAA-rated 30-year municipal bonds decreased by 51 basis points (“bps”) from 3.07% to 2.56%, while 10-year rates fell by 31 bps from 2.04% to 1.73% and 5-year rates decreased 4 bps from 1.17% to 1.13% (as measured by Thomson Municipal Market Data). The municipal yield curve experienced significant flattening over the 12-month period with the spread between 2- and 30-year maturities flattening by 81 bps and the spread between 2- and 10-year maturities flattening by 61 bps.

During the same time period, on a relative basis, tax-exempt municipal bonds broadly outperformed U.S. Treasuries with the greatest outperformance experienced in longer-term issues. In absolute terms, the positive performance of muni bonds was driven largely by falling interest rates as well as a supply/demand imbalance within the municipal market as investors sought income and incremental yield in an environment where opportunities became increasingly scarce. More broadly, municipal bonds benefited from the greater appeal of tax-exempt investing in light of the higher tax rates implemented in 2014. The asset class is known for its lower relative volatility and preservation of principal with an emphasis on income as tax rates rise.

Financial Conditions of Municipal Issuers

The majority of municipal credits remain strong, despite well-publicized distress among a few issuers. Four of the five states with the largest amount of debt outstanding — California, New York, Texas and Florida — have exhibited markedly improved credit fundamentals during the slow national recovery. However, several states with the largest unfunded pension liabilities have seen their bond prices decline noticeably and remain vulnerable to additional price deterioration. On the local level, Chicago’s credit quality downgrade is an outlier relative to other cities due to its larger pension liability and inadequate funding remedies. BlackRock maintains the view that municipal bond defaults will remain minimal and in the periphery while the overall market is fundamentally sound. We continue to advocate careful credit research and believe that a thoughtful approach to structure and security selection remains imperative amid uncertainty in a modestly improving economic environment.

The opinions expressed are those of BlackRock as of October 31, 2016, and are subject to change at any time due to changes in market or economic conditions. The comments should not be construed as a recommendation of any individual holdings or market sectors. Investing involves risk including loss of principal. Bond values fluctuate in price so the value of your investment can go down depending on market conditions. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. There may be less information on the financial condition of municipal issuers than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. Some investors may be subject to Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable.

The Standard & Poor’s Municipal Bond Index, a broad, market value-weighted index, seeks to measure the performance of the US municipal bond market. All bonds in the index are exempt from US federal income taxes or subject to the alternative minimum tax. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. It is not possible to invest directly in an index.

| | | | | | |

| | | | | | | |

| 4 | | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | |

| | | | |

| The Benefits and Risks of Leveraging | | |

The Trusts may utilize leverage to seek to enhance the distribution rate on, and net asset value (“NAV”) of, their common shares (“Common Shares”). However, these objectives cannot be achieved in all interest rate environments.

In general, the concept of leveraging is based on the premise that the financing cost of leverage, which is based on short-term interest rates, is normally lower than the income earned by a Trust on its longer-term portfolio investments purchased with the proceeds from leverage. To the extent that the total assets of the Trusts (including the assets obtained from leverage) are invested in higher-yielding portfolio investments, the Trusts shareholders benefit from the incremental net income. The interest earned on securities purchased with the proceeds from leverage is paid to shareholders in the form of dividends, and the value of these portfolio holdings is reflected in the per share NAV.

To illustrate these concepts, assume a Trust’s Common Shares capitalization is $100 million and it utilizes leverage for an additional $30 million, creating a total value of $130 million available for investment in longer-term income securities. If prevailing short-term interest rates are 3% and longer-term interest rates are 6%, the yield curve has a strongly positive slope. In this case, a Trust’s financing costs on the $30 million of proceeds obtained from leverage are based on the lower short-term interest rates. At the same time, the securities purchased by a Trust with the proceeds from leverage earn income based on longer-term interest rates. In this case, a Trust’s financing cost of leverage is significantly lower than the income earned on a Trust’s longer-term investments acquired from leverage proceeds, and therefore the holders of Common Shares (“Common Shareholders”) are the beneficiaries of the incremental net income.

However, in order to benefit Common Shareholders, the return on assets purchased with leverage proceeds must exceed the ongoing costs associated with the leverage. If interest and other costs of leverage exceed the Trusts’ return on assets purchased with leverage proceeds, income to shareholders is lower than if the Trusts had not used leverage. Furthermore, the value of the Trusts’ portfolio investments generally varies inversely with the direction of long-term interest rates, although other factors can influence the value of portfolio investments. In contrast, the value of the Trusts’ obligations under their respective leverage arrangements generally does not fluctuate in relation to interest rates. As a result, changes in interest rates can influence the Trusts’ NAVs positively or negatively. Changes in the future direction of interest rates are very

difficult to predict accurately, and there is no assurance that a Trust’s intended leveraging strategy will be successful.

The use of leverage also generally causes greater changes in each Trust’s NAV, market price and dividend rates than comparable portfolios without leverage. In a declining market, leverage is likely to cause a greater decline in the NAV and market price of a Trust’s Common Shares than if the Trust were not leveraged. In addition, each Trust may be required to sell portfolio securities at inopportune times or at distressed values in order to comply with regulatory requirements applicable to the use of leverage or as required by the terms of leverage instruments, which may cause the Trusts to incur losses. The use of leverage may limit a Trust’s ability to invest in certain types of securities or use certain types of hedging strategies. Each Trust incurs expenses in connection with the use of leverage, all of which are borne by Common Shareholders and may reduce income to the Common Shares. Moreover, to the extent the calculation of the Trusts’ investment advisory fees includes assets purchased with the proceeds of leverage, the investment advisory fees payable to the Trusts’ investment adviser will be higher than if the Trusts did not use leverage.

To obtain leverage, each Trust has issued Variable Rate Demand Preferred Shares (“VRDP Shares”) or Variable Rate Muni Term Preferred Shares (“VMTP Shares”) or Auction Market Preferred Shares (“AMPS”) (collectively, “Preferred Shares”) and/or leveraged its assets through the use of tender option bond trusts (“TOB Trusts”) as described in the Notes to Financial Statements.

Under the Investment Company Act of 1940, as amended (the “1940 Act”), each Trust is permitted to issue debt up to 33 1/3% of its total managed assets or equity securities (e.g., Preferred Shares) up to 50% of its total managed assets. A Trust may voluntarily elect to limit its leverage to less than the maximum amount permitted under the 1940 Act. In addition, a Trust may also be subject to certain asset coverage, leverage or portfolio composition requirements imposed by the Preferred Shares’ governing instruments or by agencies rating the Preferred Shares, which may be more stringent than those imposed by the 1940 Act.

If a Trust segregates or designates on its books and records cash or liquid assets having a value not less than the value of a Trust’s obligations under the TOB Trust (including accrued interest), a TOB Trust is not considered a senior security and is not subject to the foregoing limitations and requirements under the 1940 Act.

| | |

| Derivative Financial Instruments | | |

The Trusts may invest in various derivative financial instruments. These instruments are used to obtain exposure to a security, commodity, index, market, and/or other asset without owning or taking physical custody of securities, commodities and/or other referenced assets or to manage market, equity, credit, interest rate, foreign currency exchange rate, commodity and/or other risks. Derivative financial instruments may give rise to a form of economic leverage and involve risks, including the imperfect correlation between the value of a derivative financial instrument and the underlying asset, possible default of the counterparty

to the transaction or illiquidity of the instrument. The Trusts’ successful use of a derivative financial instrument depends on the investment adviser’s ability to predict pertinent market movements accurately, which cannot be assured. The use of these instruments may result in losses greater than if they had not been used, may limit the amount of appreciation a Trust can realize on an investment and/or may result in lower distributions paid to shareholders. The Trusts’ investments in these instruments, if any, are discussed in detail in the Notes to Financial Statements.

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | 5 |

| | |

| Trust Summary as of October 31, 2016 | | BlackRock Investment Quality Municipal Trust, Inc. |

BlackRock Investment Quality Municipal Trust, Inc.’s (BKN) (the “Trust”) investment objective is to provide high current income exempt from regular federal income tax consistent with the preservation of capital. The Trust seeks to achieve its investment objective by investing at least 80% of its assets in municipal obligations exempt from federal income taxes (except that the interest may be subject to the federal alternative minimum tax). Under normal market conditions, the Trust invests at least 80% of its assets in securities rated investment grade at the time of investment. The Trust may invest up to 20% of its assets in securities that are deemed by the investment adviser to be of comparable quality. The Trust may invest directly in such securities or synthetically through the use of derivatives.

No assurance can be given that the Trust’s investment objective will be achieved.

| | |

| Trust Information | | |

Symbol on New York Stock Exchange (“NYSE”) | | BKN |

Initial Offering Date | | February 19, 1993 |

Yield on Closing Market Price as of October 31, 2016 ($15.68)1 | | 5.51% |

Tax Equivalent Yield2 | | 9.73% |

Current Monthly Distribution per Common Share3 | | $0.072 |

Current Annualized Distribution per Common Share3 | | $0.864 |

Economic Leverage as of October 31, 20164 | | 36% |

| | 1 | | Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance does not guarantee future results. |

| | 2 | | Tax equivalent yield assumes the maximum marginal federal tax rate of 43.4%, which includes the 3.8% Medicare tax. Actual tax rates will vary based on income, exemptions and deductions. Lower taxes will result in lower tax equivalent yields. |

| | 3 | | The distribution rate is not constant and is subject to change. |

| | 4 | | Represents VMTP Shares and TOB Trusts as a percentage of total managed assets, which is the total assets of the Trust, including any assets attributable to VMTP Shares and TOB Trusts, minus the sum of accrued liabilities. For a discussion of leveraging techniques utilized by the Trust, please see The Benefits and Risks of Leveraging on page 5. |

Returns for the six months ended October 31, 2016 were as follows:

| | | | | | | | |

| | | Returns Based On | |

| | | Market Price | | | NAV | |

BKN1,2 | | | (5.04 | )% | | | 1.31 | % |

Lipper General & Insured Municipal Debt Funds (Leveraged)3 | | | (3.09 | )% | | | 1.30 | % |

| | 1 | | All returns reflect reinvestment of dividends and/or distributions. |

| | 2 | | The Trust moved from a premium to NAV to a discount during the period, which accounts for the difference between performance based on price and performance based on NAV. |

| | | | Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. |

The following discussion relates to the Trust’s absolute performance based on NAV:

| • | | The U.S. municipal bond market delivered modest gains in the period, with the bulk of the positive return occurring in May and June. During these two months, bond yields fell sharply (as prices rose) in reaction to the highly accommodative policies of the world’s central banks and the prospect of the Fed maintaining a gradual, data-dependent approach to raising rates. In the latter part of the period, however, the market gave back some ground as accelerating growth indicated an increased likelihood that the Fed would in fact start to raise rates before year end. Despite this headwind, the tax-exempt market closed in positive territory due to the combination of its attractive yields, a favorable supply-and-demand picture, and the continued health of state and local finances. |

| • | | The tax-exempt yield curve flattened, with short-term yields rising and longer-term yields moving lower. In this environment, the Trust’s longer-dated and longer-duration bonds provided the largest positive returns. (Duration is a measure of interest-rate sensitivity.) |

| • | | At a time in which investors continued to search for yield, many of the largest contributors to Fund performance were its investments in lower-rated, higher-yielding sectors and securities. At the sector level, positions in tax-backed (school districts), housing, and education issues were the most significant contributors. The health care sector detracted from returns, as the purchases the Trust made during the course of the period underperformed once rates began to rise. |

| • | | The Trust’s exposure to lower-coupon issues and bonds with longer call dates also benefited returns, as both segments outpaced the broader market. |

| • | | During the period, the use of leverage helped augment the Fund’s returns. However, its use of U.S. Treasury futures contracts to manage exposure to a potential rise in interest rates had a slightly positive impact on performance given that Treasury yields fell during the period. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | | | | | |

| | | | | | | |

| 6 | | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | |

| | |

| | | BlackRock Investment Quality Municipal Trust, Inc. |

| | | | | | | | | | |

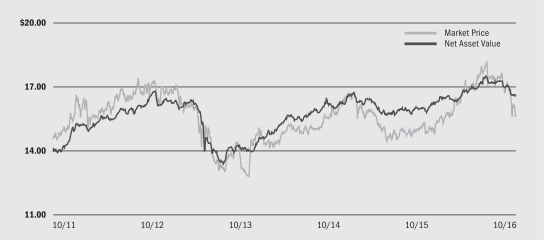

| Market Price and Net Asset Value Per Share Summary | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

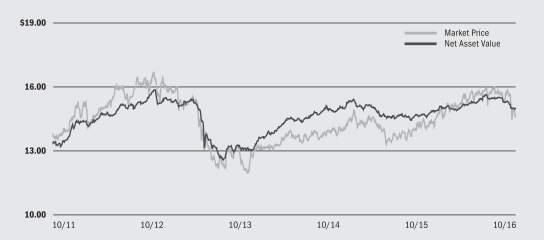

| | | 10/31/16 | | | 4/30/16 | | | Change | | | High | | | Low | |

Market Price | | $ | 15.68 | | | $ | 16.94 | | | | (7.44 | )% | | $ | 18.30 | | | $ | 15.53 | |

Net Asset Value | | $ | 16.62 | | | $ | 16.83 | | | | (1.25 | )% | | $ | 17.52 | | | $ | 16.55 | |

|

| Market Price and Net Asset Value History For the Past Five Years |

|

| Overview of the Trust’s Total Investments* |

| | | | | | | | |

| Sector Allocation | | 10/31/16 | | | 4/30/16 | |

Health | | | 28 | % | | | 23 | % |

Education | | | 15 | | | | 15 | |

County/City/Special District/School District | | | 14 | | | | 16 | |

Transportation | | | 14 | | | | 14 | |

Utilities | | | 11 | | | | 12 | |

State | | | 10 | | | | 10 | |

Corporate | | | 5 | | | | 7 | |

Tobacco | | | 3 | | | | 3 | |

For Trust compliance purposes, the Trust’s sector classifications refer to one or more of the sector subclassifications used by one or more widely recognized market indexes or rating group indexes, and/or as defined by the investment adviser. These definitions may not apply for purposes of this report, which may combine such sector subclassifications for reporting ease.

| | | | |

| | |

| Call/Maturity Schedule3 | | | |

Calendar Year Ended December 31, | | | | |

2016 | | | 2 | % |

2017 | | | 2 | |

2018 | | | 5 | |

2019 | | | 7 | |

2020 | | | 8 | |

| | 3 | | Scheduled maturity dates and/or bonds that are subject to potential calls by issuers over the next five years. |

| | * | | Excludes short-term securities. |

| | | | | | | | |

| Credit Quality Allocation1 | | 10/31/16 | | | 4/30/16 | |

AAA/Aaa | | | 6 | % | | | 6 | % |

AA/Aa | | | 45 | | | | 46 | |

A | | | 31 | | | | 28 | |

BBB/Baa | | | 11 | | | | 11 | |

BB/Ba | | | 2 | | | | 2 | |

B | | | 1 | | | | 1 | |

N/R2 | | | 4 | | | | 6 | |

| | 1 | | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either Standard & Poor’s (“S&P”) or Moody’s Investors Service (“Moody’s”) if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | 2 | | The investment adviser evaluates the credit quality of unrated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. Using this approach, the investment adviser has deemed certain of these unrated securities as investment grade quality. As of October 31, 2016 and April 30, 2016, the market value of unrated securities deemed by the investment adviser to be investment grade represents 2% and less than 1%, respectively, of the Trust’s total investments. |

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | 7 |

| | |

| Trust Summary as of October 31, 2016 | | BlackRock Long-Term Municipal Advantage Trust |

BlackRock Long-Term Municipal Advantage Trust’s (BTA) (the “Trust”) investment objective is to provide current income exempt from regular federal income tax. The Trust seeks to achieve its investment objective by investing, under normal market conditions, at least 80% of its assets in municipal obligations and derivative instruments with exposure to such municipal obligations, in each case that are exempt from federal income tax (except that the interest may be subject to the federal alternative minimum tax). The Trust invests, under normal market conditions, primarily in long-term municipal bonds with a maturity of more than ten years at the time of investment and, under normal market conditions, the Trust’s municipal bond portfolio will have a dollar-weighted average maturity of greater than 10 years. The Trust may invest directly in such securities or synthetically through the use of derivatives.

No assurance can be given that the Trust’s investment objective will be achieved.

| | |

| Trust Information | | |

Symbol on NYSE | | BTA |

Initial Offering Date | | February 28, 2006 |

Yield on Closing Market Price as of October 31, 2016 ($11.89)1 | | 5.50% |

Tax Equivalent Yield2 | | 9.72% |

Current Monthly Distribution per Common Share3 | | $0.0545 |

Current Annualized Distribution per Common Share3 | | $0.6540 |

Economic Leverage as of October 31, 20164 | | 38% |

| | 1 | | Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance does not guarantee future results. |

| | 2 | | Tax equivalent yield assumes the maximum marginal federal tax rate of 43.4%, which includes the 3.8% Medicare tax. Actual tax rates will vary based on income, exemptions and deductions. Lower taxes will result in lower tax equivalent yields. |

| | 3 | | The distribution rate is not constant and is subject to change. |

| | 4 | | Represents VRDP Shares and TOB Trusts as a percentage of total managed assets, which is the total assets of the Trust, including any assets attributable to VRDP Shares and TOB Trusts, minus the sum of accrued liabilities. For a discussion of leveraging techniques utilized by the Trust, please see The Benefits and Risks of Leveraging on page 5. |

Returns for the six months ended October 31, 2016 were as follows:

| | | | | | | | |

| | | Returns Based On | |

| | | Market Price | | | NAV | |

BTA1,2 | | | (0.61 | )% | | | 2.01 | % |

Lipper General & Insured Municipal Debt Funds (Leveraged)3 | | | (3.09 | )% | | | 1.30 | % |

| | 1 | | All returns reflect reinvestment of dividends and/or distributions. |

| | 2 | | The Trust’s discount to NAV, which widened during the period, accounts for the difference between performance based on price and performance based on NAV. |

| | | | Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. |

The following discussion relates to the Trust’s absolute performance based on NAV:

| • | | The U.S. municipal bond market delivered modest gains in the period, with the bulk of the positive return occurring in May and June. During these two months, bond yields fell sharply (as prices rose) in reaction to the highly accommodative policies of the world’s central banks and the prospect of the Fed maintaining a gradual, data-dependent approach to raising rates. In the latter part of the period, however, the market gave back some ground as accelerating growth indicated an increased likelihood that the Fed would in fact start to raise rates before year end. Despite this headwind, the tax-exempt market closed in positive territory due to the combination of its attractive yields, a favorable supply-and-demand picture, and the continued health of state and local finances. |

| • | | The Trust’s position in longer-dated securities, particularly those with maturities of 25 years and above, was a positive for performance given the relative strength in longer-term issues. The Trust was also aided by its positions in bonds rated BBB and below investment grade (BB and below), as higher-yielding, lower-quality markets segments generally outperformed higher-quality credits. |

| • | | At the sector level, exposure to utilities, project-financing, and health care issues were the largest contributors to performance. |

| • | | During the period, the use of leverage helped augment the Fund’s returns. The Trust utilized U.S. Treasury futures contracts to manage exposure to a potential rise in interest rates, and the Trust’s tactical shifts in this area contributed to its six-month results. |

| • | | Holdings in short and intermediate maturities detracted from performance, as yields rose on that part of the curve. Pre-refunded securities, which fall into this range, detracted relative to longer-dated bonds. |

| • | | The Trust’s more-seasoned holdings, while producing generous yields compared to current market rates, also detracted. The prices of many of these investments declined due to the premium amortization that occurred as the bonds approached their first call dates. (A call is when an issuer redeems a bond prior to its maturity date; premium is amount by which a bond trades above its $100 par value.) |

| • | | The Trust’s yield declined during the period, as the proceeds of called bonds were reinvested at much lower prevailing rates. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | | | | | |

| | | | | | | |

| 8 | | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | |

| | |

| | | BlackRock Long-Term Municipal Advantage Trust |

|

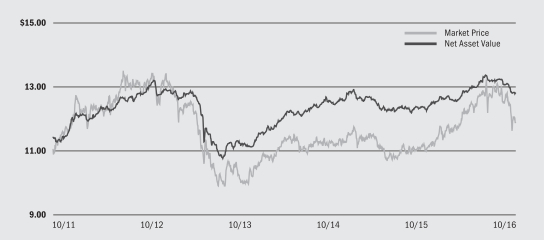

| Market Price and Net Asset Value Per Share Summary |

| | | | | | | | | | | | | | | | | | | | |

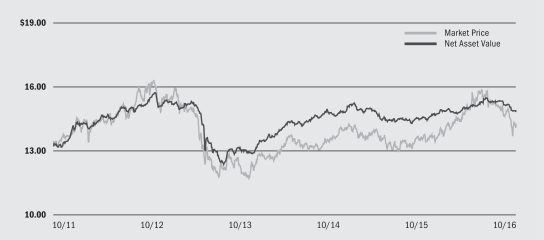

| | | 10/31/16 | | | 4/30/16 | | | Change | | | High | | | Low | |

Market Price | | $ | 11.89 | | | $ | 12.28 | | | | (3.18 | )% | | $ | 13.44 | | | $ | 11.60 | |

Net Asset Value | | $ | 12.81 | | | $ | 12.89 | | | | (0.62 | )% | | $ | 13.37 | | | $ | 12.79 | |

|

| Market Price and Net Asset Value History For the Past Five Years |

|

| Overview of the Trust’s Total Investments* |

| | | | | | | | |

| Sector Allocation | | 10/31/16 | | | 4/30/16 | |

Health | | | 20 | % | | | 19 | % |

Utilities | | | 15 | | | | 16 | |

Transportation | | | 15 | | | | 15 | |

County/City/Special District/School District | | | 13 | | | | 12 | |

Education | | | 12 | | | | 11 | |

Tobacco | | | 10 | | | | 10 | |

State | | | 8 | | | | 8 | |

Corporate | | | 6 | | | | 8 | |

Housing | | | 1 | | | | 1 | |

For Trust compliance purposes, the Trust’s sector classifications refer to one or more of the sector subclassifications used by one or more widely recognized market indexes or rating group indexes, and/or as defined by the investment adviser. These definitions may not apply for purposes of this report, which may combine such sector subclassifications for reporting ease.

| | | | |

| | |

| Call/Maturity Schedule3 | | | |

Calendar Year Ended December 31, | | | | |

2016 | | | 4 | % |

2017 | | | 4 | |

2018 | | | 3 | |

2019 | | | 16 | |

2020 | | | 12 | |

| | 3 | | Scheduled maturity dates and/or bonds that are subject to potential calls by issuers over the next five years. |

| | * | | Excludes short-term securities. |

| | | | | | | | |

| Credit Quality Allocation1 | | 10/31/16 | | | 4/30/16 | |

AAA/Aaa | | | 5 | % | | | 5 | % |

AA/Aa | | | 41 | | | | 42 | |

A | | | 15 | | | | 16 | |

BBB/Baa | | | 16 | | | | 16 | |

BB/Ba | | | 7 | | | | 7 | |

B | | | 6 | | | | 4 | |

N/R2 | | | 10 | | | | 10 | |

| | 1 | | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P’s or Moody’s if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | 2 | | The investment adviser evaluates the credit quality of unrated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. Using this approach, the investment adviser has deemed certain of these unrated securities as investment grade quality. As of October 31, 2016 and April 30, 2016, the market value of unrated securities deemed by the investment adviser to be investment grade each represents 1% of the Trust’s total investments. |

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | 9 |

| | |

| Trust Summary as of October 31, 2016 | | BlackRock Municipal 2020 Term Trust |

BlackRock Municipal 2020 Term Trust’s (BKK) (the “Trust”) investment objectives are to provide current income exempt from regular federal income tax and to return $15 per Common Share (the initial offering price per Common Share) to holders of Common Shares on or about December 31, 2020. The Trust seeks to achieve its investment objectives by investing, under normal market conditions, at least 80% of its managed assets in municipal bonds exempt from federal income taxes (except that the interest may be subject to the federal alternative minimum tax). The Trust invests, under normal market conditions, at least 80% of its managed assets in municipal bonds that are investment grade, or deemed to be of comparable quality by the investment adviser, at the time of investment. The Trust may invest directly in such securities or synthetically through the use of derivatives. There is no assurance that the Trust will achieve its investment objective of returning $15.00 per Common Share.

| | |

| Trust Information | | |

Symbol on NYSE | | BKK |

Initial Offering Date | | September 30, 2003 |

Termination Date (on or about) | | December 31, 2020 |

Yield on Closing Market Price as of October 31, 2016 ($16.27)1 | | 3.30% |

Tax Equivalent Yield2 | | 5.83% |

Current Monthly Distribution per Common Share3 | | $0.0448 |

Current Annualized Distribution per Common Share3 | | $0.5376 |

Economic Leverage as of October 31, 20164 | | 9% |

| | 1 | | Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance does not guarantee future results. |

| | 2 | | Tax equivalent yield assumes the maximum marginal federal tax rate of 43.4%, which includes the 3.8% Medicare tax. Actual tax rates will vary based on income, exemptions and deductions. Lower taxes will result in lower tax equivalent yields. |

| | 3 | | The distribution rate is not constant and is subject to change. |

| | 4 | | Represents AMPS and TOB Trusts as a percentage of total managed assets, which is the total assets of the Trust, including any assets attributable to AMPS and TOB Trusts, minus the sum of accrued liabilities. For a discussion of leveraging techniques utilized by the Trust, please see The Benefits and Risks of Leveraging on page 5. |

Returns for the six months ended October 31, 2016 were as follows:

| | | | | | | | |

| | | Returns Based On | |

| | | Market Price | | | NAV | |

BKK1,2 | | | 2.47 | % | | | 0.34 | % |

Lipper Intermediate Municipal Debt Funds3 | | | (1.81 | )% | | | 0.78 | % |

| | 1 | | All returns reflect reinvestment of dividends and/or distributions. |

| | 2 | | The Trust moved from a discount to NAV to a premium during the period, which accounts for the difference between performance based on price and performance based on NAV. |

| | | | Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. |

The following discussion relates to the Trust’s absolute performance based on NAV:

| • | | The U.S. municipal bond market delivered modest gains in the period, with the bulk of the positive return occurring in May and June. During these two months, bond yields fell sharply (as prices rose) in reaction to the highly accommodative policies of the world’s central banks and the prospect of the Fed maintaining a gradual, data-dependent approach to raising rates. In the latter part of the period, however, the market gave back some ground as accelerating growth indicated an increased likelihood that the Fed would in fact start to raise rates before year end. Despite this headwind, the tax-exempt market closed in positive territory due to the combination of its attractive yields, a favorable supply-and-demand picture, and the continued health of state and local finances. |

| • | | The Trust’s exposure to lower-rated credits aided performance as yield spreads for higher-yielding issues generally tightened over the period. At the sector level, exposure to health care, development districts and tax-backed issues were the largest contributors. Additionally, the use of leverage helped augment returns at time of positive market performance. |

| • | | Select holdings in the corporate municipal bond sector detracted from results, as deteriorating credit fundamentals resulted in multiple-notch ratings downgrades for certain issuers. |

| • | | The Trust’s shorter duration profile and exposure to bonds maturing inside of five years was a drag on performance at a time in which longer-term bonds outpaced shorter-term issues. (Duration is a measure of interest-rate sensitivity.) The Trust’s more-seasoned holdings, while producing generous yields compared to current market rates, also detracted. The prices of many of these investments declined due to the premium amortization that occurred as the bonds approached their first call dates. (A call is when an issuer redeems a bond prior to its maturity date; premium is amount by which a bond trades above its $100 par value.) |

| • | | Reinvestment was a drag on performance, as the proceeds of mature or called bonds were reinvested at much lower prevailing rates. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | | | | | |

| | | | | | | |

| 10 | | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | |

| | |

| | | BlackRock Municipal 2020 Term Trust |

|

| Market Price and Net Asset Value Per Share Summary |

| | | | | | | | | | | | | | | | | | | | |

| | | 10/31/16 | | | 4/30/16 | | | Change | | | High | | | Low | |

Market Price | | $ | 16.27 | | | $ | 16.14 | | | | 0.81 | % | | $ | 17.01 | | | $ | 15.90 | |

Net Asset Value | | $ | 16.06 | | | $ | 16.27 | | | | (1.29 | )% | | $ | 16.35 | | | $ | 16.06 | |

|

| Market Price and Net Asset Value History For the Past Five Years |

|

| Overview of the Trust’s Total Investments* |

| | | | | | | | |

| Sector Allocation | | 10/31/16 | | | 4/30/16 | |

Utilities | | | 17 | % | | | 17 | % |

Transportation | | | 16 | | | | 15 | |

County/City/Special District/School District | | | 15 | | | | 14 | |

State | | | 13 | | | | 13 | |

Health | | | 13 | | | | 12 | |

Education | | | 11 | | | | 10 | |

Corporate | | | 9 | | | | 12 | |

Tobacco | | | 4 | | | | 4 | |

Housing | | | 2 | | | | 3 | |

For Trust compliance purposes, the Trust’s sector classifications refer to one or more of the sector subclassifications used by one or more widely recognized market indexes or rating group indexes, and/or as defined by the investment adviser. These definitions may not apply for purposes of this report, which may combine such sector subclassifications for reporting ease.

| | | | |

| | |

| Call/Maturity Schedule3 | | | |

Calendar Year Ended December 31, | | | | |

2016 | | | 1 | % |

2017 | | | 5 | |

2018 | | | 5 | |

2019 | | | 19 | |

2020 | | | 50 | |

| | 3 | | Scheduled maturity dates and/or bonds that are subject to potential calls by issuers over the next five years. |

| | * | | Excludes short-term securities. |

| | | | | | | | |

| Credit Quality Allocation1 | | 10/31/16 | | | 4/30/16 | |

AAA/Aaa | | | 4 | % | | | 6 | % |

AA/Aa | | | 30 | | | | 25 | |

A | | | 33 | | | | 37 | |

BBB/Baa | | | 17 | | | | 19 | |

BB/Ba | | | 3 | | | | 4 | |

B | | | 4 | | | | — | |

N/R2 | | | 9 | | | | 9 | |

| | 1 | | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P’s or Moody’s if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | 2 | | The investment adviser evaluates the credit quality of unrated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. Using this approach, the investment adviser has deemed certain of these unrated securities as investment grade quality. As of October 31, 2016 and April 30, 2016, the market value of unrated securities deemed by the investment adviser to be investment grade represents 6% and 4%, respectively, of the Trust’s total investments. |

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | 11 |

| | |

| Trust Summary as of October 31, 2016 | | BlackRock Municipal Income Trust |

BlackRock Municipal Income Trust’s (BFK) (the “Trust”) investment objective is to provide current income exempt from regular federal income tax. The Trust seeks to achieve its investment objective by investing primarily in municipal bonds exempt from federal income taxes (except that the interest may be subject to the federal alternative minimum tax). The Trust invests, under normal market conditions, at least 80% of its assets in municipal bonds that are investment grade, or deemed to be of comparable quality by the investment adviser, at the time of investment. The Trust may invest directly in such securities or synthetically through the use of derivatives.

No assurance can be given that the Trust’s investment objective will be achieved.

| | |

| Trust Information | | |

Symbol on NYSE | | BFK |

Initial Offering Date | | July 27, 2001 |

Yield on Closing Market Price as of October 31, 2016 ($14.68)1 | | 5.81% |

Tax Equivalent Yield2 | | 10.27% |

Current Monthly Distribution per Common Share3 | | $0.0711 |

Current Annualized Distribution per Common Share3 | | $0.8532 |

Economic Leverage as of October 31, 20164 | | 40% |

| | 1 | | Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance does not guarantee future results. |

| | 2 | | Tax equivalent yield assumes the maximum marginal federal tax rate of 43.4%, which includes the 3.8% Medicare tax. Actual tax rates will vary based on income, exemptions and deductions. Lower taxes will result in lower tax equivalent yields. |

| | 3 | | The distribution rate is not constant and is subject to change. |

| | 4 | | Represents VMTP Shares and TOB Trusts as a percentage of total managed assets, which is the total assets of the Trust, including any assets attributable to VMTP Shares and TOB Trusts, minus the sum of accrued liabilities. For a discussion of leveraging techniques utilized by the Trust, please see The Benefits and Risks of Leveraging on page 5. |

Returns for the six months ended October 31, 2016 were as follows:

| | | | | | | | |

| | | Returns Based On | |

| | | Market Price | | | NAV | |

BFK1,2 | | | (2.22 | )% | | | 1.49 | % |

Lipper General & Insured Municipal Debt Funds (Leveraged)3 | | | (3.09 | )% | | | 1.30 | % |

| | 1 | | All returns reflect reinvestment of dividends and/or distributions. |

| | 2 | | The Trust moved from a premium to NAV to a discount during the period, which accounts for the difference between performance based on price and performance based on NAV. |

| | | | Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. |

The following discussion relates to the Trust’s absolute performance based on NAV:

| • | | The U.S. municipal bond market delivered modest gains in the period, with the bulk of the positive return occurring in May and June. During these two months, bond yields fell sharply (as prices rose) in reaction to the highly accommodative policies of the world’s central banks and the prospect of the Fed maintaining a gradual, data-dependent approach to raising rates. In the latter part of the period, however, the market gave back some ground as accelerating growth indicated an increased likelihood that the Fed would in fact start to raise rates before year end. Despite this headwind, the tax-exempt market closed in positive territory due to the combination of its attractive yields, a favorable supply-and-demand picture, and the continued health of state and local finances. |

| • | | The Trust’s positions in lower-rated investment-grade securities generally made the largest contributions to performance, as elevated investor risk appetites led to robust demand for higher-yielding issues. Holdings in bonds with maturities of 20 years in longer also aided performance given that longer-term debt benefited from both stronger price performance and higher income relative to shorter-dated securities. At the sector level, the Trust was helped by its positions in transportation, utilities and local tax-backed issues. |

| • | | The Trust’s more-seasoned holdings, while producing generous yields compared to current market rates, detracted from performance. The prices of many of these investments declined due to the premium amortization that occurred as the bonds approached their first call dates. (A call is when an issuer redeems a bond prior to its maturity date; premium is amount by which a bond trades above its $100 par value.) |

| • | | The Trust utilized U.S. Treasury futures contracts to manage exposure to a potential rise in interest rates, and its tactical shifts in this area contributed to the Trust’s six-month results. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | | | | | |

| | | | | | | |

| 12 | | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | |

| | |

| | | BlackRock Municipal Income Trust |

| | | | | | | | | | |

| Market Price and Net Asset Value Per Share Summary | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | 10/31/16 | | | 4/30/16 | | | Change | | | High | | | Low | |

Market Price | | $ | 14.68 | | | $ | 15.44 | | | | (4.92 | )% | | $ | 16.02 | | | $ | 14.34 | |

Net Asset Value | | $ | 15.00 | | | $ | 15.21 | 1 | | | (1.38 | )% | | $ | 15.64 | | | $ | 14.97 | |

| | 1 | | The net asset value does not reflect adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles and therefore differs from amount reported in the Financial Highlights. |

|

| Market Price and Net Asset Value History For the Past Five Years |

|

| Overview of the Trust’s Total Investments* |

| | | | | | | | |

| Sector Allocation | | 10/31/16 | | | 4/30/16 | |

Transportation | | | 21 | % | | | 21 | % |

Utilities | | | 15 | | | | 15 | |

Health | | | 14 | | | | 14 | |

County/City/Special District/School District | | | 14 | | | | 12 | |

State | | | 11 | | | | 11 | |

Education | | | 11 | | | | 10 | |

Corporate | | | 7 | | | | 11 | |

Tobacco | | | 7 | | | | 6 | |

For Trust compliance purposes, the Trust’s sector classifications refer to one or more of the sector subclassifications used by one or more widely recognized market indexes or rating group indexes, and/or as defined by the investment adviser. These definitions may not apply for purposes of this report, which may combine such sector subclassifications for reporting ease.

| | | | |

| | |

| Call/Maturity Schedule3 | | | |

Calendar Year Ended December 31, | | | | |

2016 | | | 4 | % |

2017 | | | 4 | |

2018 | | | 3 | |

2019 | | | 17 | |

2020 | | | 13 | |

| | 3 | | Scheduled maturity dates and/or bonds that are subject to potential calls by issuers over the next five years. |

| | * | | Excludes short-term securities. |

| | | | | | | | |

| Credit Quality Allocation1 | | 10/31/16 | | | 4/30/16 | |

AAA/Aaa | | | 7 | % | | | 8 | % |

AA/Aa | | | 44 | | | | 41 | |

A | | | 20 | | | | 21 | |

BBB/Baa | | | 17 | | | | 16 | |

BB/Ba | | | 4 | | | | 4 | |

B | | | 2 | | | | 1 | |

N/R2 | | | 6 | | | | 9 | |

| | 1 | | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P’s or Moody’s if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | 2 | | The investment adviser evaluates the credit quality of unrated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. Using this approach, the investment adviser has deemed certain of these unrated securities as investment grade quality. As of October 31, 2016 and April 30, 2016, the market value of unrated securities deemed by the investment adviser to be investment grade each represents 2% of the Trust’s total investments. |

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | 13 |

| | |

| Trust Summary as of October 31, 2016 | | BlackRock Strategic Municipal Trust |

BlackRock Strategic Municipal Trust’s (BSD) (the “Trust”) investment objectives are to provide current income that is exempt from regular federal income tax and to invest in municipal bonds that over time will perform better than the broader municipal bond market. The Trust seeks to achieve its investment objective by investing, under normal market conditions, at least 80% of its assets in investments exempt from federal income taxes (except that the interest may be subject to the federal alternative minimum tax). The Trust invests at least 80% of its assets in securities that are investment grade, or deemed to be of comparable quality by the investment adviser, at the time of investment and, under normal market conditions, primarily invests in municipal bonds with long-term maturities in order to maintain a weighted average maturity of 15 years or more. The Trust may invest directly in such securities or synthetically through the use of derivatives.

No assurance can be given that the Trust’s investment objectives will be achieved.

| | |

| Trust Information | | |

Symbol on NYSE | | BSD |

Initial Offering Date | | August 25, 1999 |

Yield on Closing Market Price as of October 31, 2016 ($14.25)1 | | 5.47% |

Tax Equivalent Yield2 | | 9.66% |

Current Monthly Distribution per Common Share3 | | $0.065 |

Current Annualized Distribution per Common Share3 | | $0.780 |

Economic Leverage as of October 31, 20164 | | 38% |

| | 1 | | Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance does not guarantee future results. |

| | 2 | | Tax equivalent yield assumes the maximum marginal federal tax rate of 43.4%, which includes the 3.8% Medicare tax. Actual tax rates will vary based on income, exemptions and deductions. Lower taxes will result in lower tax equivalent yields. |

| | 3 | | The distribution rate is not constant and is subject to change. |

| | 4 | | Represents VMTP Shares and TOB Trusts as a percentage of total managed assets, which is the total assets of the Trust, including any assets attributable to VMTP Shares and TOB Trusts, minus the sum of accrued liabilities. For a discussion of leveraging techniques utilized by the Trust, please see The Benefits and Risks of Leveraging on page 5. |

Returns for the six months ended October 31, 2016 were as follows:

| | | | | | | | |

| | | Returns Based On | |

| | | Market Price | | | NAV | |

BSD1,2 | | | (2.59 | )% | | | 1.58 | % |

Lipper General & Insured Municipal Debt Trusts (Leveraged)3 | | | (3.09 | )% | | | 1.30 | % |

| | 1 | | All returns reflect reinvestment of dividends and/or distributions. |

| | 2 | | The Trust’s discount to NAV, which widened during the period, accounts for the difference between performance based on price and performance based on NAV. |

| | | | Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. |

The following discussion relates to the Trust’s absolute performance based on NAV:

| • | | The U.S. municipal bond market delivered modest gains in the period, with the bulk of the positive return occurring in May and June. During these two months, bond yields fell sharply (as prices rose) in reaction to the highly accommodative policies of the world’s central banks and the prospect of the Fed maintaining a gradual, data-dependent approach to raising rates. In the latter part of the period, however, the market gave back some ground as accelerating growth indicated an increased likelihood that the Fed would in fact start to raise rates before year end. Despite this headwind, the tax-exempt market closed in positive territory due to the combination of its attractive yields, a favorable supply-and-demand picture, and the continued health of state and local finances. |

| • | | The Trust’s position in longer-dated securities, particularly those with maturities of 25 years and above, was a positive for performance given the relative strength in longer-term issues. The Trust was also aided by its positions in bonds rated A and BBB, as higher-yielding, lower-quality markets segments generally outperformed higher-quality credits. |

| • | | At the sector level, exposure to transportation, corporate-backed, and utilities issues were the largest contributors to performance. |

| • | | During the period, the use of leverage helped augment the Fund’s returns. The Trust utilized U.S. Treasury futures contracts to manage exposure to a potential rise in interest rates, and its tactical shifts in this area contributed to the Trust’s six-month results. |

| • | | Holdings in short and intermediate maturities detracted from performance, as yields rose on that part of the curve. Pre-refunded securities, which fall into this range, detracted relative to longer-dated bonds. |

| • | | The Trust’s more-seasoned holdings, while producing generous yields compared to current market rates, also detracted. The prices of many of these investments declined due to the premium amortization that occurred as the bonds approached their first call dates. (A call is when an issuer redeems a bond prior to its maturity date; premium is amount by which a bond trades above its $100 par value.) |

| • | | The Trust’s yield declined during the period, as the proceeds of called bonds were reinvested at much lower prevailing rates. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | | | | | |

| | | | | | | |

| 14 | | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | |

| | |

| | | BlackRock Strategic Municipal Trust |

| | | | | | | | | | |

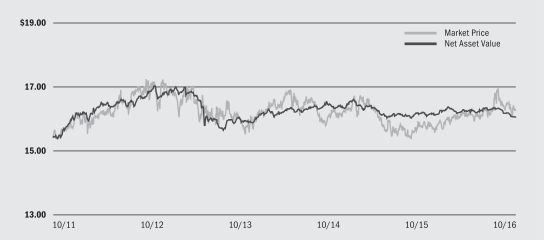

| Market Price and Net Asset Value Per Share Summary | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | 10/31/16 | | | 4/30/16 | | | Change | | | High | | | Low | |

Market Price | | $ | 14.25 | | | $ | 15.02 | | | | (5.13 | )% | | $ | 15.98 | | | $ | 13.66 | |

Net Asset Value | | $ | 14.88 | | | $ | 15.04 | | | | (1.06 | )% | | $ | 15.50 | | | $ | 14.86 | |

|

| Market Price and Net Asset Value History For the Past Five Years |

|

| Overview of the Trust’s Total Investments* |

| | | | | | | | |

| Sector Allocation | | 10/31/16 | | | 4/30/16 | |

Transportation | | | 23 | % | | | 24 | % |

Health | | | 20 | | | | 18 | |

Utilities | | | 12 | | | | 14 | |

Education | | | 11 | | | | 11 | |

County/City/Special District/School District | | | 11 | | | | 10 | |

State | | | 10 | | | | 9 | |

Corporate | | | 7 | | | | 9 | |

Tobacco | | | 6 | | | | 5 | |

For Trust compliance purposes, the Trust’s sector classifications refer to one or more of the sector subclassifications used by one or more widely recognized market indexes or rating group indexes, and/or as defined by the investment adviser. These definitions may not apply for purposes of this report, which may combine such sector subclassifications for reporting ease.

| | | | |

| | |

| Call/Maturity Schedule3 | | | |

Calendar Year Ended December 31, | | | | |

2016 | | | 5 | % |

2017 | | | 4 | |

2018 | | | 6 | |

2019 | | | 17 | |

2020 | | | 12 | |

| | 3 | | Scheduled maturity dates and/or bonds that are subject to potential calls by issuers over the next five years. |

| | * | | Excludes short-term securities. |

| | | | | | | | |

| Credit Quality Allocation1 | | 10/31/16 | | | 4/30/16 | |

AAA/Aaa | | | 8 | % | | | 9 | % |

AA/Aa | | | 42 | | | | 41 | |

A | | | 23 | | | | 25 | |

BBB/Baa | | | 13 | | | | 11 | |

BB/Ba | | | 4 | | | | 4 | |

B | | | 2 | | | | 1 | |

N/R2 | | | 8 | | | | 9 | |

| | 1 | | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P’s or Moody’s if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | 2 | | The investment adviser evaluates the credit quality of unrated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. Using this approach, the investment adviser has deemed certain of these unrated securities as investment grade quality. As of October 31, 2016 and April 30, 2016, the market value of unrated securities deemed by the investment adviser to be investment grade each represents 2% of the Trust’s total investments. |

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | 15 |

| | |

Schedule of Investments October 31, 2016 (Unaudited) | | BlackRock Investment Quality Municipal Trust, Inc. (BKN) (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Municipal Bonds | | Par (000) | | | Value | |

Alabama — 1.9% | | | | | | | | |

City of Birmingham Alabama Special Care Facilities Financing Authority, RB, Children’s Hospital (AGC),

6.00%, 6/01/19 (a) | | $ | 1,745 | | | $ | 1,966,231 | |

UAB Medicine Finance Authority, Refunding RB,

Series B, 3.50%, 9/01/39 (b) | | | 3,560 | | | | 3,488,444 | |

| | | | | | | | |

| | | | | | | | 5,454,675 | |

Arizona — 8.0% | | | | | | | | |

Arizona Health Facilities Authority, Refunding RB, Phoenix Children’s Hospital, Series A,

5.00%, 2/01/42 | | | 3,300 | | | | 3,603,138 | |

City of Phoenix Arizona IDA, Refunding RB, Basis Schools, Inc. Projects, 5.00%, 7/01/45 (c) | | | 455 | | | | 481,190 | |

County of Maricopa Industrial Development Authority, Refunding RB, Banner Health Obligation

Group (b): | | | | | | | | |

3.25%, 1/01/37 | | | 2,895 | | | | 2,762,756 | |

4.00%, 1/01/38 | | | 2,000 | | | | 2,100,240 | |

County of Pinal Arizona Electric District No. 3, Refunding RB, Electric System, 4.75%, 7/01/31 | | | 3,750 | | | | 4,216,125 | |

Salt Verde Financial Corp., RB, Senior: | | | | | | | | |

5.00%, 12/01/32 | | | 1,035 | | | | 1,247,423 | |

5.00%, 12/01/37 | | | 4,585 | | | | 5,497,232 | |

University Medical Center Corp., RB,

6.50%, 7/01/19 (a) | | | 750 | | | | 856,343 | |

University Medical Center Corp., Refunding RB,

6.00%, 7/01/21 (a) | | | 1,600 | | | | 1,945,072 | |

| | | | | | | | |

| | | | | | | | 22,709,519 | |

Arkansas — 3.2% | | | | | | | | |

City of Benton Arkansas, RB, 4.00%, 6/01/39 | | | 1,355 | | | | 1,458,658 | |

City of Fort Smith Arkansas Water & Sewer Revenue, Refunding RB, 4.00%, 10/01/40 | | | 1,850 | | | | 1,968,418 | |

City of Hot Springs Arkansas, RB, Wastewater,

5.00%, 12/01/38 | | | 1,800 | | | | 2,056,518 | |

City of Little Rock Arkansas, RB, 4.00%, 7/01/41 | | | 2,955 | | | | 3,147,607 | |

County of Pulaski Arkansas Public Facilities Board, RB, 5.00%, 12/01/42 | | | 465 | | | | 530,230 | |

| | | | | | | | |

| | | | | | | | 9,161,431 | |

California — 18.1% | | | | | | | | |

California Health Facilities Financing Authority, RB, Sutter Health: | | | | | | | | |

Series A, 3.25%, 11/15/36 | | | 1,230 | | | | 1,224,600 | |

Series B, 5.88%, 8/15/31 | | | 2,300 | | | | 2,684,031 | |

California Health Facilities Financing Authority, Refunding RB, Adventist Health System West, Series A, 3.00%, 3/01/39 | | | 1,130 | | | | 1,028,153 | |

California Infrastructure & Economic Development Bank, Refunding RB, 4.00%, 11/01/45 | | | 3,330 | | | | 3,536,693 | |

California Statewide Communities Development Authority, RB, Loma Linda University Medical Center, Series A, 5.25%, 12/01/56 (c) | | | 705 | | | | 786,505 | |

Carlsbad California Unified School District, GO, Election of 2006, Series B, 0.00%, 5/01/34 (d) | | | 1,500 | | | | 1,598,070 | |

City of San Jose California, Refunding ARB, Series A-1, AMT, 5.75%, 3/01/34 | | | 3,000 | | | | 3,496,350 | |

| | | | | | | | |

| Municipal Bonds | | Par (000) | | | Value | |

California (continued) | | | | | | | | |

Dinuba California Unified School District, GO, Election of 2006 (AGM), 5.75%, 8/01/19 (a) | | $ | 535 | | | $ | 604,871 | |

Hartnell Community College District California, GO, CAB, Election of 2002, Series D, 0.00%, 8/01/34 (d) | | | 2,475 | | | | 2,497,448 | |

Norwalk-La Mirada Unified School District, GO, Refunding, CAB, Election of 2002, Series E (AGC), 0.00%, 8/01/38 (e) | | | 12,000 | | | | 5,235,600 | |

Palomar Community College District, GO, CAB,

Election of 2006, Series B: | | | | | | | | |

0.00%, 8/01/30 (e) | | | 2,270 | | | | 1,495,136 | |

0.00%, 8/01/33 (e) | | | 4,250 | | | | 1,704,250 | |

0.00%, 8/01/39 (d) | | | 3,000 | | | | 2,778,150 | |

San Diego Community College District, GO, CAB, Election of 2002, 0.00%, 8/01/33 (d) | | | 4,200 | | | | 4,773,258 | |

State of California, GO, Refunding, Various Purposes: | | | | | | | | |

5.00%, 2/01/38 | | | 2,000 | | | | 2,321,460 | |

4.00%, 10/01/44 | | | 2,520 | | | | 2,690,856 | |

State of California, GO, Various Purposes: | | | | | | | | |

5.75%, 4/01/31 | | | 3,000 | | | | 3,331,200 | |

6.00%, 3/01/33 | | | 2,270 | | | | 2,634,812 | |

6.50%, 4/01/33 | | | 2,900 | | | | 3,275,405 | |

5.50%, 3/01/40 | | | 3,650 | | | | 4,144,830 | |

| | | | | | | | |

| | | | | | | | 51,841,678 | |

Colorado — 0.3% | | | | | | | | |

Park Creek Metropolitan District, Refunding RB, Senior Limited Property Tax (AGM),

6.00%, 12/01/20 (a) | | | 750 | | | | 892,860 | |

Connecticut — 1.2% | | | | | | | | |

Connecticut State Health & Educational Facility Authority, Refunding RB: | | | | | | | | |

Lawrence & Memorial Hospital, Series F,

5.00%, 7/01/36 | | | 950 | | | | 1,042,540 | |

Trinity Health Corp., 3.25%, 12/01/36 | | | 150 | | | | 150,120 | |

South Central Connecticut Regional Water Authority, Refunding RB, Thirty Second,

Series B,

4.00%, 8/01/36 | | | 1,980 | | | | 2,160,239 | |

| | | | | | | | |

| | | | | | | | 3,352,899 | |

Delaware — 2.5% | | | | | | | | |

County of Sussex Delaware, RB, NRG Energy, Inc., Indian River Power LLC Project, 6.00%, 10/01/40 | | | 1,800 | | | | 1,986,894 | |

Delaware Transportation Authority, RB: | | | | | | | | |

5.00%, 6/01/45 | | | 3,000 | | | | 3,478,080 | |

5.00%, 6/01/55 | | | 1,430 | | | | 1,621,820 | |

| | | | | | | | |

| | | | | | | | 7,086,794 | |

Florida — 6.1% | | | | | | | | |

Capital Trust Agency Inc., RB, M/F Housing, The Gardens Apartment Project, Series A,

4.75%, 7/01/40 | | | 900 | | | | 916,596 | |

County of Miami-Dade Florida, RB: | | | | | | | | |

CAB, Subordinate Special Obligation,

0.00%, 10/01/32 (e) | | | 5,000 | | | | 2,793,550 | |

| | | | | | | | | | |

| AGC | | Assured Guarantee Corp. | | COP | | Certificates of Participation | | LRB | | Lease Revenue Bonds |

| AGM | | Assured Guaranty Municipal Corp. | | EDA | | Economic Development Authority | | M/F | | Multi-Family |

| AMBAC | | American Municipal Bond Assurance Corp. | | EDC | | Economic Development Corp. | | NPFGC | | National Public Finance Guarantee Corp. |

| AMT | | Alternative Minimum Tax (subject to) | | GARB | | General Airport Revenue Bonds | | PILOT | | Payment in Lieu of Taxes |

| ARB | | Airport Revenue Bonds | | GO | | General Obligation Bonds | | RB | | Revenue Bonds |

| BAM | | Build America Mutual Assurance Co. | | HDA | | Housing Development Authority | | SAN | | State Aid Notes |

| CAB | | Capital Appreciation Bonds | | IDA | | Industrial Development Authority | | S/F | | Single-Family |

| CHF | | Swiss Franc | | ISD | | Independent School District | | | | |

See Notes to Financial Statements.

| | | | | | |

| | | | | | | |

| 16 | | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | |

| | |

Schedule of Investments (continued) | | BlackRock Investment Quality Municipal Trust, Inc. (BKN) |

| | | | | | | | |

| Municipal Bonds | | Par (000) | | | Value | |

Florida (continued) | | | | | | | | |

County of Miami-Dade Florida, RB (continued): | | | | | | | | |

CAB, Subordinate Special Obligation,

0.00%, 10/01/33 (e) | | $ | 15,375 | | | $ | 8,228,239 | |

Series B, AMT, 6.00%, 10/01/32 | | | 3,000 | | | | 3,656,670 | |

County of Miami-Dade Florida Educational Facilities Authority, Refunding RB, University of Miami,

Series A, 5.00%, 4/01/45 | | | 1,390 | | | | 1,602,100 | |

County of Orange Florida Health Facilities Authority, Refunding RB, Mayflower Retirement Center,

5.00%, 6/01/32 | | | 200 | | | | 215,760 | |

| | | | | | | | |

| | | | | | | | 17,412,915 | |

Hawaii — 0.2% | | | | | | | | |

Hawaii State Department of Budget & Finance, Refunding RB, Special Purpose, Senior Living, Kahala Nui, 5.25%, 11/15/37 | | | 600 | | | | 660,816 | |

Idaho — 1.2% | | | | | | | | |

Idaho Health Facilities Authority, RB, St. Lukes Health System Project, Series A, 5.00%, 3/01/39 | | | 3,000 | | | | 3,402,780 | |

Illinois — 8.4% | | | | | | | | |

Chicago Public Building Commission, RB, Series A (NPFGC), 7.00%, 1/01/20 (f) | | | 5,000 | | | | 5,728,950 | |

City of Chicago Illinois, Refunding ARB, O’Hare International Airport Passenger Facility Charge, Series B, AMT, 4.00%, 1/01/29 | | | 2,400 | | | | 2,510,496 | |

City of Chicago Illinois Midway International Airport, Refunding GARB, 2nd Lien, Series A,

5.00%, 1/01/41 | | | 1,735 | | | | 1,926,475 | |

City of Chicago Illinois Transit Authority, RB, Sales Tax Receipts, 5.25%, 12/01/40 | | | 1,000 | | | | 1,103,840 | |

Illinois Finance Authority, RB, Rush University Medical Center, Series C, 6.63%, 5/01/19 (a) | | | 1,200 | | | | 1,366,572 | |

Illinois Finance Authority, Refunding RB: | | | | | | | | |

OSF Heallthcare System, 6.00%, 5/15/20 (a) | | | 955 | | | | 1,115,717 | |

OSF Heallthcare System, 6.00%, 5/15/39 | | | 535 | | | | 608,150 | |

Roosevelt University Project, 6.50%, 4/01/44 | | | 1,500 | | | | 1,625,850 | |

Railsplitter Tobacco Settlement Authority, RB: | | | | | | | | |

6.25%, 6/01/24 | | | 5,000 | | | | 5,057,050 | |

6.00%, 6/01/28 | | | 1,700 | | | | 1,996,225 | |

State of Illinois, GO, 5.00%, 2/01/39 | | | 1,000 | | | | 1,034,950 | |

| | | | | | | | |

| | | | | | | | 24,074,275 | |

Iowa — 1.4% | | | | | | | | |

Iowa Higher Education Loan Authority, Refunding RB, Private College Facility: | | | | | | | | |

Drake University Project, 3.00%, 4/01/34 | | | 1,000 | | | | 1,003,220 | |

Upper Iowa University Project,

5.75%, 9/01/20 (a) | | | 965 | | | | 1,129,648 | |

Upper Iowa University Project,

6.00%, 9/01/20 (a) | | | 1,500 | | | | 1,769,955 | |

| | | | | | | | |

| | | | | | | | 3,902,823 | |

Kansas — 3.5% | | | | | | | | |

County of Johnson Unified School District No. 512 Shawnee Mission, GO, Refunding Series B,

3.00%, 10/01/37 | | | 1,940 | | | | 1,859,315 | |

County of Seward Kansas Unified School District No. 480, GO, Refunding,

5.00%, 9/01/22 (a) | | | 6,000 | | | | 6,812,760 | |

Kansas Development Finance Authority, Refunding RB, Sisters Leavenworth: | | | | | | | | |

5.00%, 1/01/20 (a) | | | 1,005 | | | | 1,126,303 | |

5.00%, 1/01/28 | | | 150 | | | | 165,146 | |

| | | | | | | | |

| | | | | | | | 9,963,524 | |

| | | | | | | | |

| Municipal Bonds | | Par (000) | | | Value | |

Kentucky — 5.7% | | | | | | | | |

County of Louisville & Jefferson Kentucky Metropolitan Government, Refunding RB, Norton Healthcare, Inc.,

4.00%, 10/01/35 | | $ | 2,100 | | | $ | 2,239,902 | |

Kentucky Bond Development Corp., Refunding RB, Saint Elizabeth Medical Center, Inc.,

4.00%, 5/01/35 | | | 875 | | | | 931,954 | |

Kentucky Economic Development Finance Authority, RB, Catholic Health Initiatives, Series A,

5.38%, 1/01/40 | | | 3,400 | | | | 3,841,184 | |

Kentucky Economic Development Finance Authority, Refunding RB, Norton Healthcare, Inc., Series B (NPFGC), 0.00%, 10/01/23 (e) | | | 8,500 | | | | 7,129,885 | |

Kentucky Public Transportation Infrastructure Authority, RB, Downtown Crossing Project, Convertible CAB, 1st Tier, Series C (d): | | | | | | | | |

0.00%, 7/01/34 | | | 1,000 | | | | 868,360 | |

0.00%, 7/01/39 | | | 1,395 | | | | 1,183,336 | |

| | | | | | | | |

| | | | | | | | 16,194,621 | |

Louisiana — 2.0% | | | | | | | | |

City of Alexandria Louisiana Utilities, RB,

5.00%, 5/01/39 | | | 1,790 | | | | 2,028,840 | |

Louisiana Local Government Environmental Facilities & Community Development Authority, RB, Westlake Chemical Corp. Project, Series A-1,

6.50%, 11/01/35 | | | 1,565 | | | | 1,810,924 | |

Louisiana Public Facilities Authority, RB, Belle Chasse Educational Foundation Project, 6.50%, 5/01/31 | | | 600 | | | | 687,240 | |

Louisiana Public Facilities Authority, Refunding RB,

4.00%, 11/01/45 | | | 1,040 | | | | 1,059,708 | |

| | | | | | | | |

| | | | | | | | 5,586,712 | |

Maryland — 0.8% | | | | | | | | |

County of Anne Arundel Maryland Consolidated, Special Taxing District, Villages at Two Rivers Project: | | | | | | | | |

5.13%, 7/01/36 | | | 260 | | | | 269,280 | |

5.25%, 7/01/44 | | | 260 | | | | 268,811 | |

County of Montgomery Maryland, RB, Trinity Health Credit Group, 5.00%, 12/01/45 | | | 1,500 | | | | 1,771,515 | |

| | | | | | | | |

| | | | | | | | 2,309,606 | |

Massachusetts — 1.7% | | | | | | | | |

Massachusetts Development Finance Agency, RB, Dana-Farber Cancer Institute Issue, Series N,

5.00%, 12/01/46 | | | 625 | | | | 728,912 | |

Massachusetts Development Finance Agency, Refunding RB: | | | | | | | | |

Emmanuel College Issue, Series A,

4.00%, 10/01/46 | | | 1,380 | | | | 1,395,760 | |

International Charter School, 5.00%, 4/15/40 | | | 600 | | | | 669,558 | |

WGBH Educational Foundation Issue,

3.00%, 1/01/42 | | | 2,280 | | | | 2,132,393 | |

| | | | | | | | |

| | | | | | | | 4,926,623 | |

Michigan — 3.6% | | | | | | | | |

Michigan Finance Authority, RB, Detroit Water & Sewage Disposal System, Senior Lien, Series 2014 C-2, AMT, 5.00%, 7/01/44 | | | 360 | | | | 387,141 | |

Michigan Finance Authority, Refunding RB, Henry Ford Health System, 4.00%, 11/15/46 | | | 2,305 | | | | 2,322,057 | |

Michigan State Building Authority, Refunding RB, Facilities Program Series, 6.25%, 10/15/38 | | | 60 | | | | 65,803 | |

Michigan State Hospital Finance Authority, Refunding RB, Trinity Health Credit Group, Series C,

4.00%, 12/01/32 | | | 4,150 | | | | 4,370,531 | |

See Notes to Financial Statements.

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | OCTOBER 31, 2016 | | 17 |

| | |

Schedule of Investments (continued) | | BlackRock Investment Quality Municipal Trust, Inc. (BKN) |

| | | | | | | | |

| Municipal Bonds | | Par (000) | | | Value | |

Michigan (continued) | | | | | | | | |

Royal Oak Hospital Finance Authority Michigan, Refunding RB, William Beaumont Hospital,

Series V, 8.25%, 9/01/18 (a) | | $ | 2,750 | | | $ | 3,118,445 | |

| | | | | | | | |

| | | | | | | | 10,263,977 | |

Minnesota — 2.1% | | | | | | | | |

City of Minneapolis Minnesota, Refunding RB, Fairview Health Services, Series B (AGC), 6.50%, 11/15/38 | | | 1,905 | | | | 2,094,033 | |

City of St. Cloud Minnesota, Refunding RB, CentraCare Health System, Series A, 3.25%, 5/01/39 | | | 695 | | | | 684,075 | |

Minnesota Higher Education Facilities Authority, RB, College of St. Benedict, Series 8-K: | | | | | | | | |