Investor Presentation December 2014 Filed by Atlas Energy, L.P. Pursuant to Rule 425 under the Securities Act of 1933 and Deemed filed pursuant to Rule 14a-2 under the Securities Exchange Act of 1934 Subject Company: Atlas Energy, L.P. Commission File No. 001-32953 |

2 Safe Harbor Additional Information on the Transaction In connection with the proposed transaction, on November 20, 2014, Targa Resources Corp. (“TRGP”) filed with the U.S. Securities and Exchange Commission (the “SEC”) a registration statement on Form S-4 that included a preliminary joint proxy statement of Atlas Energy, L.P. (“ATLS”) and TRGP and a preliminary prospectus of TRGP (the “TRGP joint proxy statement/prospectus”). The registration statement has not yet become effective. After the registration statement has been declared effective by the SEC, TRGP plans to mail the definitive TRGP joint proxy statement/prospectus to its shareholders, and ATLS plans to mail the definitive TRGP joint proxy statement/prospectus to its unitholders. Also in connection with the proposed transaction, on November 20, 2014, Targa Resources Partners LP (“NGLS”) filed with the SEC a registration statement on Form S-4 that included a preliminary proxy statement of Atlas Pipeline Partners, L.P. (“APL”) and a preliminary prospectus of NGLS (the “NGLS proxy statement/prospectus”) . The registration statement has not yet become effective. After the registration statement has been declared effective by the SEC, APL plans to mail the definitive NGLS proxy statement/prospectus to its unitholders. INVESTORS, SHAREHOLDERS AND UNITHOLDERS ARE URGED TO READ THE TRGP JOINT PROXY STATEMENT/PROSPECTUS, THE NGLS PROXY STATEMENT/PROSPECTUS AND OTHER RELEVANT DOCUMENTS FILED OR TO BE FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT TRGP, NGLS, ATLS AND APL, AS WELL AS THE PROPOSED TRANSACTION AND RELATED MATTERS. This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. A free copy of the TRGP Joint Proxy Statement/Prospectus, the NGLS Proxy Statement/Prospectus and other filings containing information about TRGP, NGLS, ATLS and APL may be obtained at the SEC’s Internet site at www.sec.gov. In addition, the documents filed with the SEC by TRGP and NGLS may be obtained free of charge by directing such request to: Targa Resources, Attention: Investor Relations, 1000 Louisiana, Suite 4300, Houston, Texas 77002 or emailing InvestorRelations@targaresources.com or calling (713) 584-1133. These documents may also be obtained for free from TRGP’s and NGLS’s investor relations website at www.targaresources.com. The documents filed with the SEC by ATLS may be obtained free of charge by directing such request to: Atlas Energy, L.P., Attn: Investor Relations, 1845 Walnut Street, Philadelphia, Pennsylvania 19103 or emailing InvestorRelations@atlasenergy.com. These documents may also be obtained for free from ATLS’s investor relations website at www.atlasenergy.com. The documents filed with the SEC by APL may be obtained free of charge by directing such request to: Atlas Pipeline Partners, L.P., Attn: Investor Relations, 1845 Walnut Street, Philadelphia, Pennsylvania 19103 or emailing IR@atlaspipeline.com. These documents may also be obtained for free from APL’s investor relations website at www.atlaspipeline.com. Participants in Solicitation Relating to the Merger TRGP, NGLS, ATLS and APL and their respective directors, executive officers and other persons may be deemed to be participants in the solicitation of proxies from TRGP, ATLS or APL shareholders or unitholders, as applicable, in respect of the proposed transaction that will be described in the TRGP joint proxy statement/prospectus and NGLS proxy statement/prospectus. Information regarding TRGP’s directors and executive officers is contained in TRGP’s definitive proxy statement dated April 7, 2014, which has been filed with the SEC. Information regarding directors and executive officers of NGLS’s general partner is contained in NGLS’s Annual Report on Form 10-K for the year ended December 31, 2013, which has been filed with the SEC. Information regarding directors and executive officers of ATLS’s general partner is contained in ATLS’s definitive proxy statement dated March 21, 2014, which has been filed with the SEC. Information regarding directors and executive officers of APL’s general partner is contained in APL’s Annual Report on Form 10-K for the year ended December 31, 2013, which has been filed with the SEC. A more complete description will be available in the registration statement and the joint proxy statement/prospectus. |

3 Cautionary Note Regarding Forward Looking Statements Certain statements contained herein are “forward-looking statements” that are subject to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements that involve a number of assumptions, risks and uncertainties that could cause actual results to differ materially from those contained in the forward-looking statements. Readers are cautioned that any forward-looking information is not a guarantee of future performance. Risks and uncertainties related to the proposed transaction (including the distribution of Atlas Energy Group, LLC units, or “the distribution”) include, among others: the risk that ATLS’s or APL’s unitholders or TRGP’s stockholders do not approve the mergers; the risk that the merger agreement is terminated as a result of a competing proposal, the risk that regulatory approvals required for the mergers are not obtained on the proposed terms and schedule or are obtained subject to conditions that are not anticipated; the risk that the other conditions to the closing of the mergers are not satisfied; potential adverse reactions or changes to business or employee relationships, including those resulting from the announcement or completion of the mergers or the distribution; uncertainties as to the timing of the mergers or the distribution; competitive responses to the proposed merger or the distribution; costs and difficulties related to the integration of ATLS’s and APL’s businesses and operations with TRGP’s and NGLS’s business and operations; the inability to obtain, or delays in obtaining, the cost savings and synergies contemplated by the mergers; uncertainty of the expected financial performance of the combined company or Atlas Energy Group, LLC following completion of the proposed transaction; unexpected costs, charges or expenses resulting from the mergers or the distribution; litigation relating to the merger; the outcome of potential litigation or governmental investigations; the inability to retain key personnel; and any changes in general economic and/or industry specific conditions; and other risks, assumptions and uncertainties detailed from time to time in ATLS', ARP's and APL's reports filed with the U.S. Securities and Exchange Commission, including quarterly reports on Form 10-Q, current reports on Form 8-K and annual reports on Form 10-K, as well as the TRGP joint proxy statement/prospectus and NGLS joint proxy statement/prospectus, and the Form 10 registration statement filed by Atlas Energy Group, LLC. Forward-looking statements speak only as of the date hereof, and we assumes no obligation to update such statements, except as may be required by applicable law. |

4 – A History of Value Creation • Atlas and its related companies have a track record of creating substantial value for stakeholders over the past several decades • The recently announced Targa transaction represents yet another milestone in delivering significant unitholder return • The newest opportunity, Atlas Energy Group, is positioned to continue this tradition Atlas Pre-Spinoff Stage 1999-2004 Shareholder return CAGR: 27% “Marcellus” Stage 2004-2011 Shareholder return CAGR: 41% “Post-Chevron” Stage 2011-2014 Shareholder return CAGR: 67% |

5 – A History of Value Creation Atlas has provided repeated substantial returns over the years in each of its various stages of growth and development Atlas Pipeline IPO Atlas America IPO Chevron acquires Atlas America, Inc.; New Atlas Energy, LP retains legacy assets 1999 Atlas America acquisition Targa agrees to acquire Atlas Pipeline and Atlas Energy; Atlas Energy Group is created CAGR: 27% CAGR: 41% CAGR: 67% Potential additional businesses and energy assets 2000 2004 2011 2014 Future |

6 Targa Transaction – Latest Significant Milestone Atlas Energy, L.P. and Atlas Pipeline Partners, L.P. have executed definitive agreements to be acquired by Targa Resources Targa Resources Corp. (TRGP) will acquire Atlas Energy (ATLS) for TRGP shares and cash in a transaction valued at $1.9 billion (1) , following Atlas Energy’s distribution of its non-midstream assets Targa Resources Partners, L.P. (NGLS) will acquire Atlas Pipeline for NGLS units and cash, valued at $5.8 billion (1) Upon closing of the transaction, ATLS will distribute common units representing a 100% LLC interest in Atlas Energy Group to ATLS unitholders Atlas Energy Group will own three General Partner interests and other additional assets: GP & IDR interests in Atlas Resource Partners, as well as 24.7 million limited partner units 80% GP & IDR interest in Atlas’ private E&P Development Subsidiary 16% GP interest and 12% limited partner interest in Lightfoot Capital, which owns a 40% limited partner interest in Arc Logistics, L.P. Net natural gas production of approximately 11.5 MMcf/d in the Arkoma basin Fundraising channel for new business creation (1) Based on market data as of October 10,2014, excluding transaction fees & expenses |

7 Atlas Energy Group Valuation $9.12 $18.83 ~ $4.65 Current ATLS unit price (1) : $32.60 TRGP cash consideration TRGP share consideration (1) Implied value of Atlas Energy Group Atlas Energy Group’s current projected annual distribution: $1.25/unit Implied yield: ~ 27% The current implied value in ATLS for Atlas Energy Group is ~ $300MM, or ~ $4.65/unit, substantially below the value of the current cash flows which assume no strategic growth (1) Based on ATLS and TRGP trading prices on December 2, 2014; TRGP share consideration determined by TRGP unit price times merger exchange ratio of 0.1809 TRGP units for each unit of ATLS |

8 Atlas Energy Group Valuation 24.7MM ARP Limited Partner Units (2) (1) Assumes 52MM units outstanding at Atlas Energy Group (2) Total market value of ARP units owned by ATLS divided by 52MM units;; based on 12/2/14 ARP unit price (3) Based on net debt assumption of $140MM Current trading values (1) : Arkoma natural gas production Per Unit Values $6.35 $1.15 ($2.70) $4.80 $4.65 Total Current Value Total Current Implied Value of Atlas Energy Group Net debt expected at Atlas Energy Group (3) |

9 Atlas Energy Group Valuation – ADDITIONAL VALUE (1) Assumes 52MM units outstanding at Atlas Energy Group (2) Assumes 20x multiple on GP related cash flows for Minimum Value; 30x for Normalized ValueTotal market value of ARP units owned by ATLS divided by 52MM units; Minimum Value: 12/2/14 ARP unit price; Normalized Value: $20 ARP unit price (3) Assumes 14x multiple on ARCX GP related cash flows (4) Total market value of ARP units owned by ATLS divided by 52MM units;; Current Value based on 12/2/14 ARP unit price; Normalized Value based on $20 ARP unit price Total Per Unit Value Range of Atlas Energy Group Total Discount to Value Range Compared to Current Implied Value Current Normalized Value Value $6.50 $9.80 $0.60 $0.60 $1.20 $1.85 $ --- $ --- $4.80 $7.95 ~ $20.00 ~ $13.00 Per unit values (1) : $4.65 $4.65 Total Current Implied Value of Atlas Energy Group GP & LP interest in Lightfoot Capital (3) GP & LP interest in E&P Development Subsidiary; $3.2MM assumed annual run rate (2) ARP GP & IDR Cash Flow: $17MM FY15E annual run rate (2) Future potential LP’s and funds ARP LP units and Arkoma production (4) ~ 65% ~ 75% |

10 The New Atlas - Atlas Energy Group, LLC An energy general partner focused on growth of its enterprises with minimal capital investment Ability to grow cash flow from existing and future assets under management Atlas’ capital raising offers substantial ability to build new businesses Multiple General Partner cash flow streams Substantial potential for distribution growth with limited capital investment |

11 Atlas Fundraising Business Substantial Atlas internal sales force which raises capital in all 50 states Unique funding source: Partnership funds provide a non-traditional source of capital to develop limited partnerships and funds Over 40 years of raising funds through partnership channel Fundraising channel provides Atlas access to a $20 billion annual fundraising market |

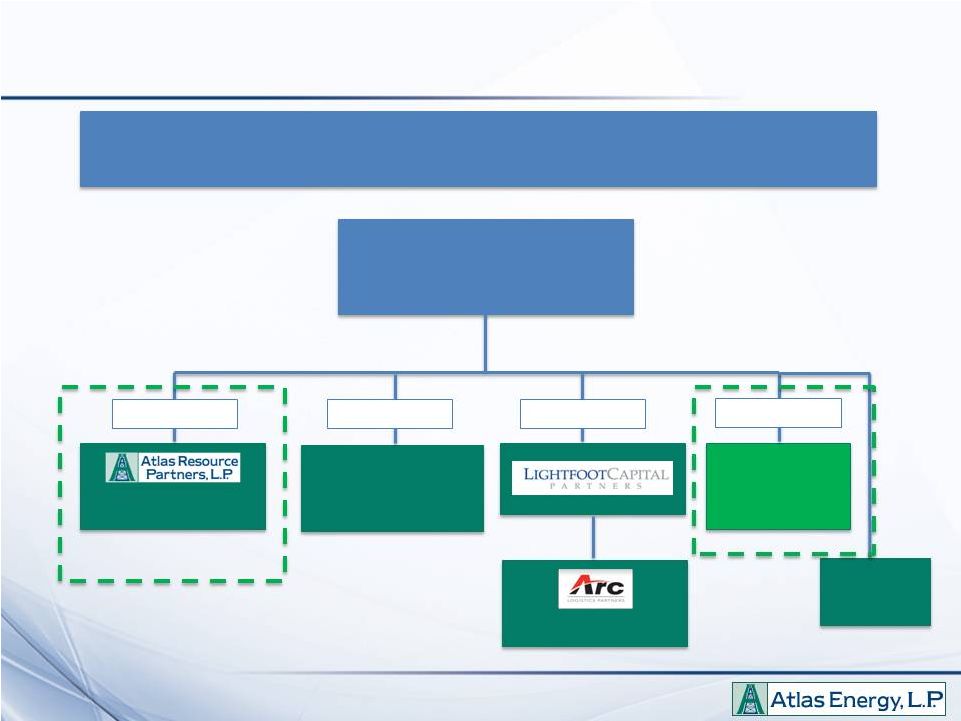

12 Pro Forma Atlas Family Corporate Structure Atlas Energy Group, LLC Future LPs/Funds 2.0% GP, 100% IDRs , 28% LP Private E&P Development Subsidiary 80% GP & IDRs, 3.1% LP NYSE: ARP 40% LP 16% GP & 12% LP NYSE: ARCX Atlas Energy Group will own multiple GP interests and cash flow streams following the Targa transaction Arkoma Production General Partner General Partner General Partner General Partner |

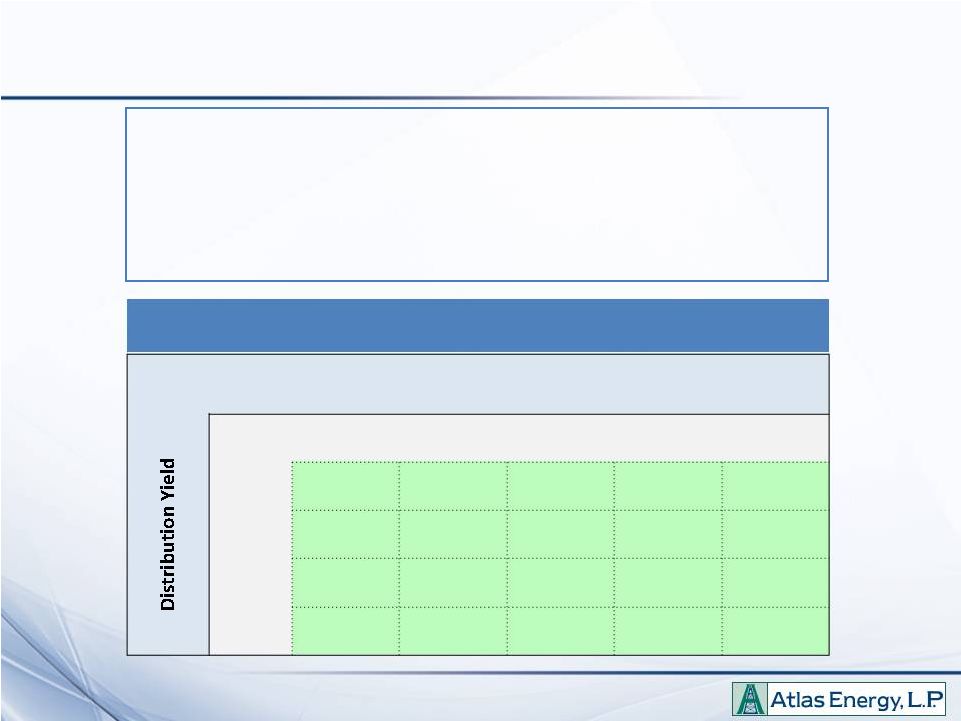

13 Atlas Energy Group – Substantial Embedded Value • Atlas expects to expand its interests and cash flow through future strategic activities, which could include: • New energy asset opportunities • Build out of ARP’s production assets, possibly through strategic partnerships • Growth of Atlas’ private E&P Development Subsidiary Atlas Energy Group per unit value scenarios, compared to current implied unit price of ~ $4.65/unit Atlas Energy Group Distribution Growth 0% 5% 10% 20% 30% 10% $ 12.50 $ 13.13 $ 13.75 $ 15.00 $ 16.25 8% $ 15.63 $ 16.41 $ 17.19 $ 18.75 $ 20.31 6% $ 20.83 $ 21.88 $ 22.92 $ 25.00 $ 27.08 4% $ 31.25 $ 32.81 $ 34.38 $ 37.50 $ 40.63 |

14 Strategic Opportunities Atlas Resource Partners Future growth opportunities Atlas Energy Group will have the ability to substantially increase cash flow and distributions through several potential strategic activities |

15 Strategic Opportunities - ARP Atlas Resource Partners Potential “drop down” partnership Visibility to asset growth Improved liquidity and credit profile at ARP IDR high splits offer incentive to JV partner Continued increases to fundraising activity to provide capital for future growth Atlas Energy Group, LLC ARP General Partner Atlas Resource Partners, LP % interest in ARP GP ARP LP units + cash Multiple drop down assets Potential Drop Down Partner Long lived oil & gas production Potential Drop Down Scenario Example |

16 Strategic Opportunities – Future Growth Additional opportunities — Increased capital and organic growth in Atlas’ E&P Development subsidiary — New enterprises to be cultivated within Atlas Energy Group, utilizing Atlas’ fundraising capabilities — E.g. $1 billion of fundraising for new assets could potentially generate an additional $0.35 per unit plus incentive distribution rights, or a ~ 30% increase to initial annual distributions of $1.25 |

17 ATLAS RESOURCE PARTNERS |

18 ARP Overview Well-balanced production between oil & natural gas — ~ 75% natural gas on over 285 Mmcfe/d of net production Diversified cash flow streams — Balance between production from multiple regions as well as fee income Strong hedge portfolio protecting production margins — ~ 70% of 2015 natural gas and oil production is hedged — Natural gas at increasing prices each year through 2018 Growth with minimal capital investment Atlas Resource Partners is an oil & gas production MLP, which manages stable producing assets from over 14,000 wells in 16 different states in the U.S. |

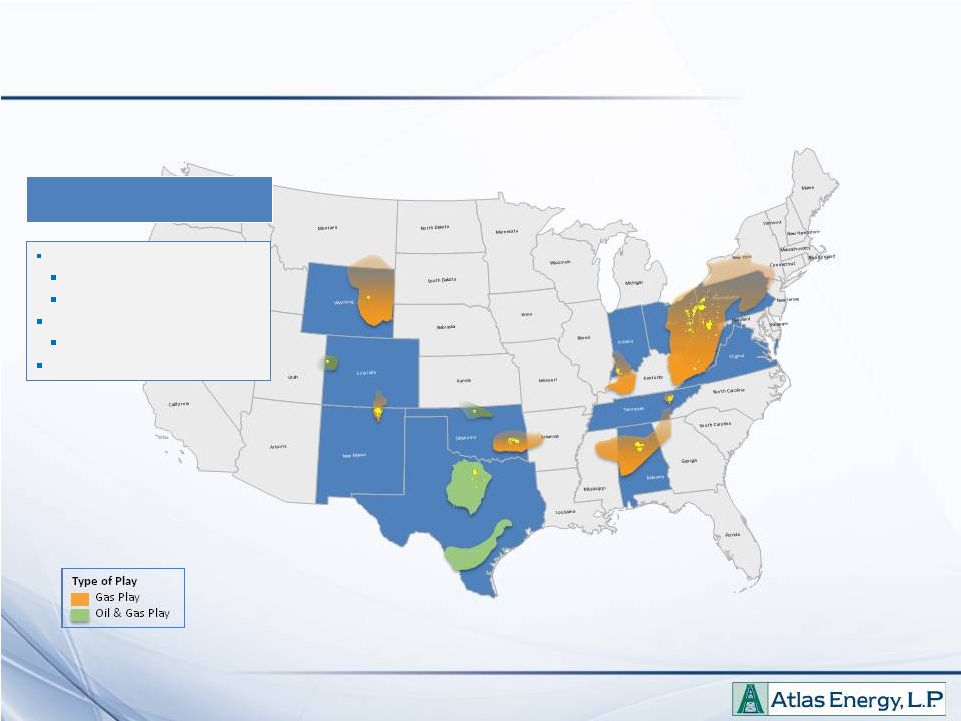

19 (1) 2014 Mid-year reserves pro forma for announced acquisitions ARP Asset Overview Powder River Basin Uinta Basin Mississippi Lime Black Warrior Basin Chattanooga New Albany Marcellus, Utica, Devonian ~1.7 Tcfe proved reserves (1) 65% gas 65% developed > 285 MMcfe/d net production ~75% gas Over 13,000 wells operated ARP Asset Summary Raton Basin Barnett / Marble Falls Arkoma Eagle Ford |

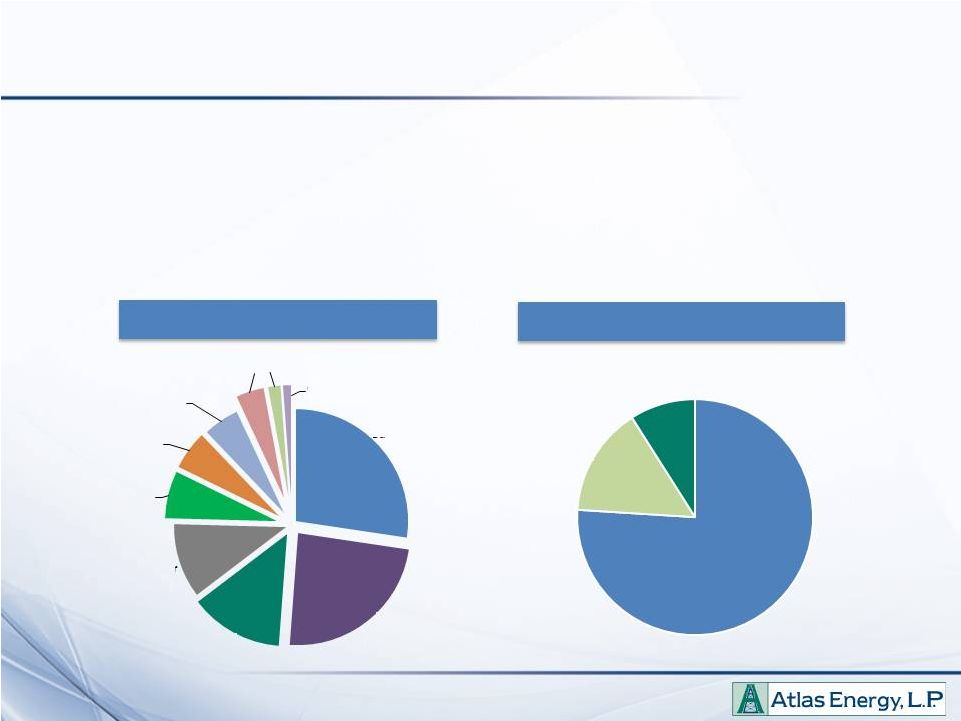

20 Geographic & Commodity Diversification Geographic Profile (1) • ARP has robust geographic coverage – operations in 16 states • Production is diversified across numerous sales points which helps mitigate basis differential risk and stabilize cash flow • Scale of operations and expertise creates opportunities for future expansion Balanced Commodity Profile (2) 15% 76% 9% (1) Based on Q3 2014 production levels (2) Based on FY 2015E production levels Barnett / Marble Falls 27% Raton 24% Appalachia 13% Black Warrior 11% WV CBM 7% Rangely 6% Eagle Ford 5% MS Lime/Hunton 4% Other 1% County Line < 1% Natural Gas Oil NGLs |

21 |