Filed by Targa Resources Corp.

Pursuant to Rule 425 of the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

of the Securities Exchange Act of 1934

Subject Company: Atlas Energy, L.P.

Commission File No.: 001-32953

This filing relates to a proposed business combination involving Targa Resources Corp. and Atlas Energy, L.P.

Targa Resources All Employee Meeting December 12, 2014 2014 Proprietary and Confidential Information |

Today’s Discussion 2 2014 has been a good year From an industry standpoint, 2014 is finishing with challenges that will continue in 2015 Targa is well positioned to handle the challenges (that includes position after Targa/Atlas close) |

Preliminary Summary of Performance vs 2014 Business Priorities 2014 Business Priorities Execute on all business dimensions, including 2014 guidance for EBITDA and distribution/dividend growth as furnished from time to time Continue to control all costs—operating, capital and G&A Continue to attract and retain the operational and professional talent needed in our businesses Continue to manage tightly credit, inventory, interest rate and commodity price exposures Pursue commercial and financial approaches to achieve maximum value and manage risks Execute on major capital and development projects—finalizing negotiations, completing projects on time and on budget, and optimizing economics and capital funding Pursue selected growth opportunities including G&P build outs, fee-based capex projects, and potential purchases of strategic assets Continue the expansion of system capabilities and the commercialization of our Bakken shale midstream business including volume targets for 2014 Continue priority emphasis and strong performance relative to a safe workplace Reinforce business philosophy and mindset that promotes compliance in all aspects of our business including environmental and regulatory compliance 3 Continued strong HS&E track record and performance, industry recognition > 1700 contractor FTEs at our facilities with no significant safety incidents Execution and performance across our businesses 2014 continues transformation that was underway in 2013 to a diversified mid-stream company with increased scale Each reportable segment at or above Plan Distribution/dividend growth Fractionation and export volumes Balance sheet management and credit ratings Major project execution Capital markets execution, including equity ATM Expense control ~ Most business units above plan Credit, inventory, hedging Execution on capital projects continues long-term organic growth CBF Train 5 Low Ethane Exports Phase 2 High Plains / Longhorn Plant Startups Midland County Pipeline Little Missouri 40 & 200 MMcf/d Plants 300 MMcf/d Winkler County Plant Condensate Splitter Continued development of potential expansion project portfolio Ethane Exports Additional Condensate Splitter CBF Trains 6 and 7 Additional G&P and Badlands Expansions Targa/Atlas merger agreement structuring, negotiation and execution Adds attractive positions in active basins Increases scale and enhances credit profile Adds significant growth opportunities Creates significant long-term value |

Strong Execution Sustains Current and Long-Term Value Strong execution of business priorities combined with a disciplined growth strategy generate unitholder and shareholder value in the near-term, over the long-term and position Targa for the future 4 |

2014 Finishing with Challenges that Continue in 2015 5 Beginning in Q4, significant drop and significant uncertainty in commodity prices impacting producers – and therefore impacting Targa and other midstream companies Difficulty for producers to predict, plan and adjust to lower, uncertain prices – and therefore difficulty for Targa and other midstream companies Likely continued uncertainties associated with prices, future activity levels and future volume levels Resulting need for flexibility, cost control and capital expenditure efficiency |

Today’s Discussion 6 2014 has been a good year From an industry standpoint, 2014 is finishing with challenges that will continue in 2015 Targa is well positioned to handle the challenges (that includes position after Atlas close) |

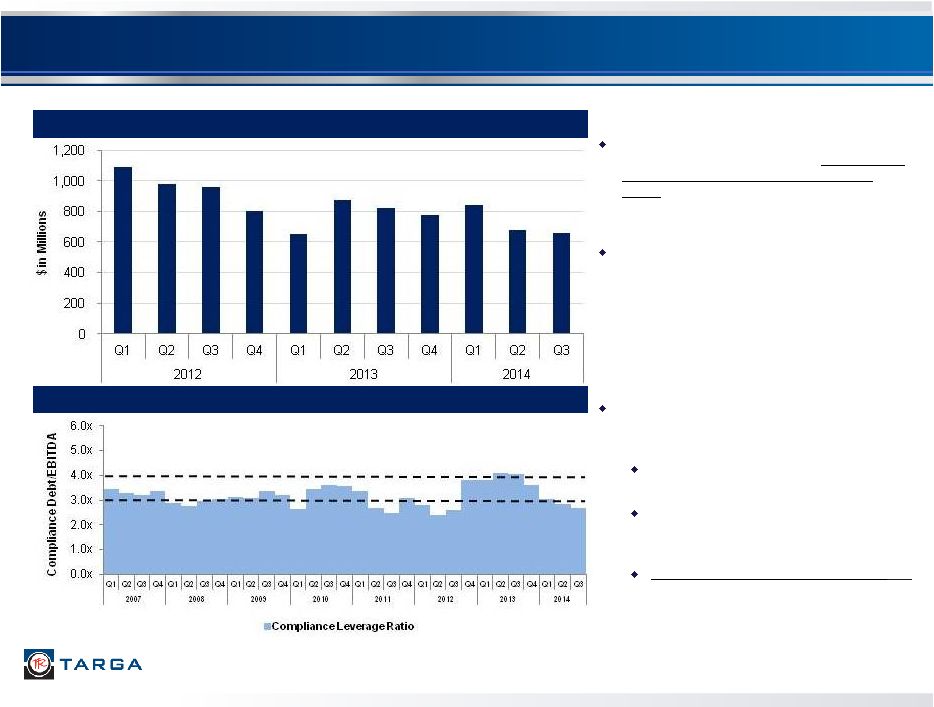

7 Targa Leverage and Liquidity Completed $800 million 4.125% unsecured notes offering in October 2014. Pro forma for offerings, liquidity as of Sept 30 is $1.45 billion including capacity under accounts receivable securitization YTD through September 2014, raised net proceeds of $257 million from equity issuances under at-the-market (“ATM”) program Target compliance leverage ratio 3x - 4x Debt/EBITDA Have historically been on low end of range Leverage increased at end of 2012 due to Badlands acquisition Q3 2014 compliance leverage ratio was 2.7x (1) Includes TRP’s total availability under the revolver plus cash, less outstanding borrowings and letters of credit under the TRP revolver (2) Adjusts EBITDA to provide credit for material capital projects that are in process, but have not started commercial operation, and other items Compliance Leverage Ratio Liquidity (1) |

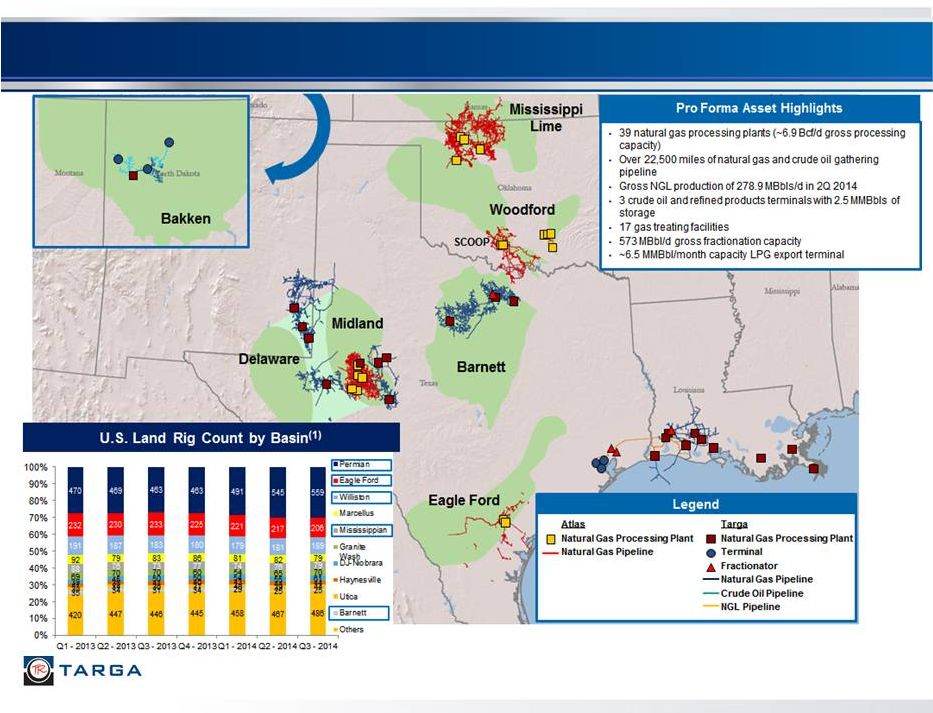

8 A Strong Footprint in Active Basins And a Leading Position at Mont Belvieu Drive Targa’s Long-Term Growth Leadership position in oil and liquids rich Permian Basin Bakken position capitalizes on strong crude oil fundamentals and active drilling activity Leadership position in the active portion of Barnett Shale “combo” play GOM and onshore Louisiana provide longer term upside potential for well positioned assets Mont Belvieu is the NGL hub of North America Increased domestic NGL production is driving capacity expansions into and at Mont Belvieu Second largest fractionation ownership position at Mont Belvieu One of only two operating commercial NGL export facilities on the Gulf Coast linked to Mont Belvieu Position not easily replicated Approximately $2.6 billion in announced organic capex projects completed or underway Increased capacity to support multiple U.S. shale / resource plays Additional fractionation expansion to support increased NGL supply Increased connectivity to U.S. end users of NGLs Expansion of export services capacity for global LPG markets at Galena Park marine terminal Well Positioned for 2014 and Beyond Targa prior to Targa/Atlas Close Positioning with close of Targa/Atlas Transaction An even stronger footprint in active basins Additional NGL opportunities Growth prospects – better than stand alone Maintaining pro forma 2015 distribution and dividend growth with 1.0-1.2 times coverage under $3.75/$60/$0.60 pricing and related volume expectations $4.00/$80/$0.80 pricing and related volume expectations Expect close Q1 2015 Press Release 12/10/14 |

Management Perspectives on Targa/Atlas Transaction 9 Received HSR clearance; expected timing first quarter 2015 Although we are in a different commodity price world – this is still a strategic and value creating transaction Long-term view of businesses being acquired and asset fit Sharing general principles and governing thoughts for combination |

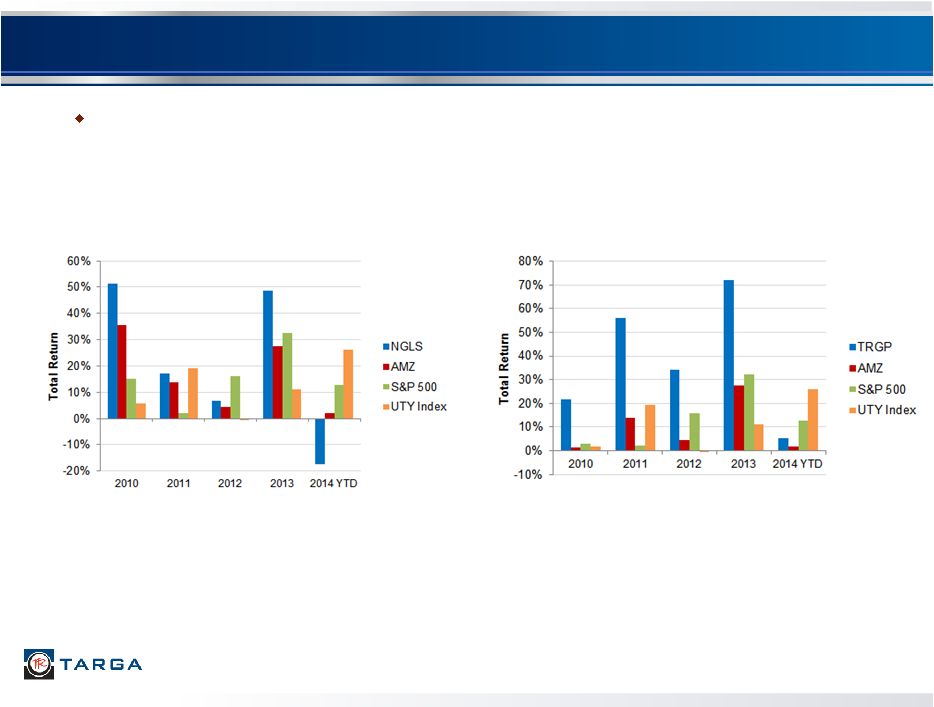

Commodity Price Performance Since Targa/Atlas Announcement Crude Oil Natural Gas Ethane Propane Normal Butane Iso-Butane Natural Gasoline Mont Belvieu NGL Components ($/Gallon) 10 Note: Pricing data through December 1, 2014 |

11 Attractive Positions in Active Basins (1) Source: Baker Hughes Incorporated, as of October 20, 2014 |

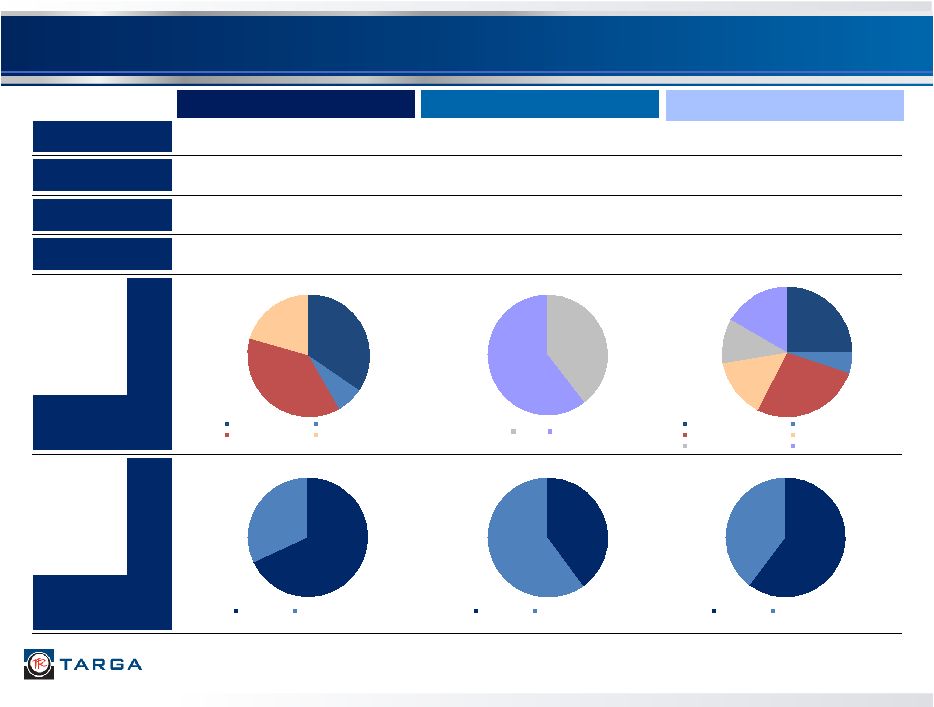

Market Cap ~ $12 Billion (1) ~ $5 Billion (2) ~ $17 Billion (1) Enterprise Value ~ $15 Billion (1) ~ $8 Billion (2) ~ $23 Billion (1) 2014E EBITDA ($MM) $925 - $975 Million $400 - $425 Million $1,325 - $1,400 Million 2014E Capital Expenditures ($MM) $780 Million $400 - $450 Million $1,180 - $1,230 Million 2014E Operating Margin by Segment YE 2014E % Fee- Based 68% 32% Fixed Fee Percent of Proceeds 35% 7% 38% 20% Field G&P Coastal G&P Logistics Marketing and Dist. 40% 60% Texas Oklahoma 25% 5% 27% 15% 11% 17% Field G&P - Targa Coastal G&P - Targa Logistics - Targa Marketing and Dist. - Targa Texas - Atlas Oklahoma - Atlas 40% 60% Fixed Fee Percent of Proceeds 60% 40% Fixed Fee Percent of Proceeds 12 Increased Size and Scale Enhance Credit Profile Targa Atlas Pro Forma Targa *As disclosed at time of announcement (1) Represents combined market cap and enterprise value for NGLS and TRGP as of October 10, 2014, less the value of NGLS units or PF NGLS units owned by TRGP (2) Represents combined market cap and enterprise value for APL and ATLS as of October 10, 2014 based on transaction consideration (3) Includes keep-whole at 1% of total margin (3) * * * * * * |

13 Targa + Atlas: Strategic Highlights Attractive Positions in Active Basins Creates World-Class Permian Footprint Complementary Assets with Significant Growth Opportunities Enhances Credit Profile Significant Long-Term Value Creation Increased Size and Scale |

General Principals and Governing Thoughts for the Combination 14 The overall philosophy in preparing for closing of the Atlas Mergers is to keep both organizations in place and motivated to continue to execute Continue execution of Targa and APL business strategies and growth plans without disruption Retain a talented midstream G&P organization with different geographic locations Manage the acquired businesses through Tulsa and through a Tulsa leadership team Minimize the potential burdens and distractions for the Targa team in connection with the merger Our goal is to keep all the talent we can across companies and locations The APL leadership team in Tulsa has agreed to remain in place Pat McDonie reporting to Mike Heim Trey Karlovich reporting to Matt Meloy Jack Wygle reporting to Jeff McParland Jerry Shrader reporting to Paul Chung Both organizations are short people and fully loaded managing and executing business growth and business performance Obviously, some corporate and technical functions will need to coordinate to establish common policies and philosophies But please note that “coordination” is not the same as “integration” or “consolidation” |

Conclusions 15 Once the Targa/Atlas Mergers close, Targa will be a larger, more diversified midstream company About 40% larger in enterprise value and headcount One of larger, more diversified MLPs Great presence in more producing basins with more potential Y-grade supply Stronger position to continue to grow; stronger position to withstand cycles Investment grade sooner Targa is well positioned to handle the challenges associated with commodity prices (that includes position after Atlas close) What questions or suggestions do you have today? |