Targa Resources Goldman Sachs Global Energy Conference 2015 January 7-8, 2015 Filed by Targa Resources Corp. Pursuant to Rule 425 of the Securities Act of 1933 and deemed filed pursuant to Rule 14a-12 of the Securities Exchange Act of 1934 Subject Company: Atlas Energy, L.P. Commission File No.: 001-32953 This filing relates to a proposed business combination involving Targa Resources Corp. and Atlas Energy, L.P. |

2 Forward Looking Statements Certain statements in this presentation are "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, included in this presentation that address activities, events or developments that Targa Resources Partners LP (“TRP” or the “Partnership”) or Targa Resources Corp. (“TRC” or the “Company”) expect, believe or anticipate will or may occur in the future are forward-looking statements. These forward-looking statements rely on a number of assumptions concerning future events and are subject to a number of uncertainties, factors and risks, many of which are outside the Partnership’s and the Company’s control, which could cause results to differ materially from those expected by management of Targa Resources Partners LP and Targa Resources Corp. Such risks and uncertainties include, but are not limited to, weather, political, economic and market conditions, including declines in the production of natural gas or in the price and market demand for natural gas and natural gas liquids, the timing and success of business development efforts, the credit risk of customers and other uncertainties. These and other applicable uncertainties, factors and risks are described more fully in the Partnership's and the Company’s Annual Reports on Form 10-K for the year ended December 31, 2013 and other reports filed with the Securities and Exchange Commission. The Partnership and the Company undertake no obligation to update or revise any forward-looking statement, whether as a result of new information, future events or otherwise. |

3 Additional Information Additional Information and Where to Find It In connection with the proposed transaction, Targa Resources Corp. (“TRC”) will file with the U.S. Securities and Exchange Commission (the “SEC”) a registration statement on Form S-4 that will include a joint proxy statement of Atlas Energy, L.P. (“ATLS”) and TRC and a prospectus of TRC (the “TRC joint proxy statement/prospectus”). In connection with the proposed transaction, TRC plans to mail the definitive TRC joint proxy statement/prospectus to its shareholders, and ATLS plans to mail the definitive TRC joint proxy statement/prospectus to its unitholders. Also in connection with the proposed transaction, Targa Resources Partners LP (“TRP”) will file with the SEC a registration statement on Form S-4 that will include a proxy statement of Atlas Pipeline Partners, L.P. (“APL”) and a prospectus of TRP (the “TRP proxy statement/prospectus”). In connection with the proposed transaction, APL plans to mail the definitive TRP proxy statement/prospectus to its unitholders. INVESTORS, SHAREHOLDERS AND UNITHOLDERS ARE URGED TO READ THE TRC JOINT PROXY STATEMENT/PROSPECTUS, THE TRP PROXY STATEMENT/PROSPECTUS AND OTHER RELEVANT DOCUMENTS FILED OR TO BE FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT TRC, TRP, ATLS AND APL, AS WELL AS THE PROPOSED TRANSACTION AND RELATED MATTERS. This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. A free copy of the TRC Joint Proxy Statement/Prospectus, the TRP Proxy Statement/Prospectus and other filings containing information about TRC, TRP, ATLS and APL may be obtained at the SEC’s Internet site at www.sec.gov. In addition, the documents filed with the SEC by TRC and TRP may be obtained free of charge by directing such request to: Targa Resources, Attention: Investor Relations, 1000 Louisiana, Suite 4300, Houston, Texas 77002 or emailing InvestorRelations@targaresources.com or calling (713) 584-1133. These documents may be obtained for free from TRC’s and TRP’s investor relations website at www.targaresources.com. The documents filed with the SEC by ATLS may be obtained free of charge by directing such request to: Atlas Energy, L.P., Attn: Investor Relations, 1845 Walnut Street, Philadelphia, Pennsylvania 19103 or emailing InvestorRelations@atlasenergy.com. These documents may also be obtained for free from ATLS’s investor relations website at www.atlasenergy.com. The documents filed with the SEC by APL may be obtained free of charge by directing such request to: Atlas Pipeline Partners, L.P., Attn: Investor Relations, 1845 Walnut Street, Philadelphia, Pennsylvania 19103 or emailing IR@atlaspipeline.com. These documents may also be obtained for free from APL’s investor relations website at www.atlaspipeline.com. Participants in Solicitation Relating to the Merger TRC, TRP, ATLS and APL and their respective directors, executive officers and other persons may be deemed to be participants in the solicitation of proxies from TRC, ATLS or APL shareholders or unitholders, as applicable, in respect of the proposed transaction that will be described in the TRC joint proxy statement/prospectus and TRP proxy statement/prospectus. Information regarding TRC’s directors and executive officers is contained in TRC’s definitive proxy statement dated April 7, 2014, which has been filed with the SEC. Information regarding directors and executive officers of TRP’s general partner is contained in TRP’s Annual Report on Form 10-K for the year ended December 31, 2013, which has been filed with the SEC. Information regarding directors and executive officers of ATLS’s general partner is contained in ATLS’s definitive proxy statement dated March 21, 2014, which has been filed with the SEC. Information regarding directors and executive officers of APL’s general partner is contained in APL’s Annual Report on Form 10-K for the year ended December 31, 2013, which has been filed with the SEC. A more complete description will be available in the registration statement and the joint proxy statement/prospectus. |

4 Targa Resources’ Two Public Companies (1) 2010 covers time period from IPO (December 6, 2010) through December 31, 2010 Source: Bloomberg |

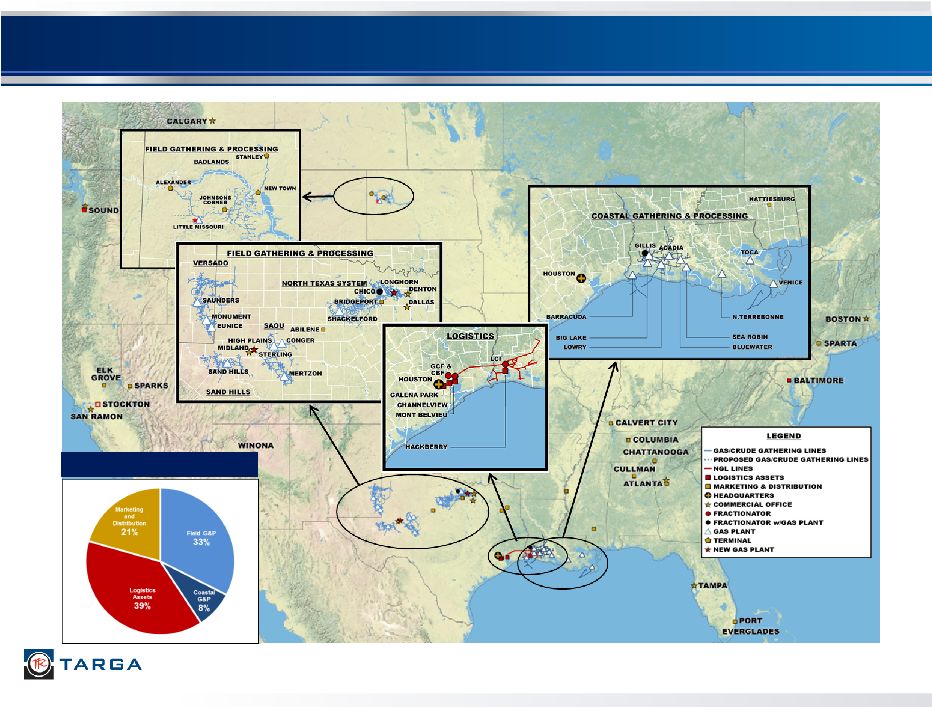

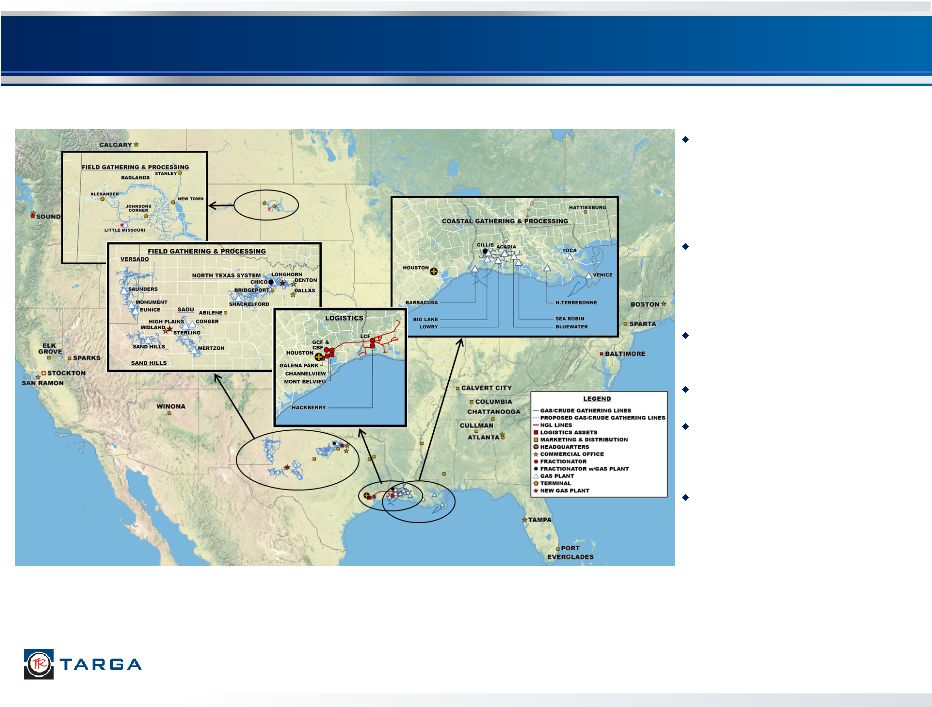

Targa’s Diversified Midstream Platform 5 (1) Operating margin percentages based on LTM as of September 30, 2014 Operating Margin (1) |

6 A Strong Footprint in Active Basins And a Leading Position at Mont Belvieu Drive Targa’s Long-Term Growth Leadership position in oil and liquids rich Permian Basin Bakken position capitalizes on strong crude oil fundamentals and active drilling activity Leadership position in the active portion of Barnett Shale “combo” play GOM and onshore Louisiana provide longer term upside potential for well positioned assets Mont Belvieu is the NGL hub of North America Increased domestic NGL production is driving capacity expansions into and at Mont Belvieu Second largest fractionation ownership position at Mont Belvieu One of only two operating commercial NGL export facilities on the Gulf Coast linked to Mont Belvieu Position not easily replicated Approximately $2.6 billion in announced organic capex projects completed or underway Increased capacity to support multiple U.S. shale / resource plays Additional fractionation expansion to support increased NGL supply Increased connectivity to U.S. end users of NGLs Expansion of export services capacity for global LPG markets at Galena Park marine terminal Positioning Pro Forma for Targa/Atlas Transaction: Expect to close Q1 2015 An even stronger footprint in active basins – modest change in fee based margin % and G&P % Additional NGL opportunities Better growth prospects than standalone December 10th Press Release: Maintaining pro forma 2015 estimates of 11-13% distribution growth at TRP and 35% dividend growth at TRC Expect distribution coverage of 1.0 to 1.2 times Commodity prices of $3.75/MMBtu for natural gas, $60/barrel for crude oil and $0.60/gallon for NGLs and related volume expectations Commodity prices of $4.00/MMBtu for natural gas, $80/barrel for crude oil and $0.80/gallon for NGLs and related volume expectations Well Positioned for 2014 and Beyond |

7 2014 End of Year Challenges Continue into 2015 Beginning in Q4 2014, the significant drop and resulting uncertainty in commodity prices is impacting producers, and therefore Targa and other midstream companies Resulting difficulty predicting, planning and adjusting for producers’ future activity and volume levels Targa is focused on: Cost management and flexibility Capital expenditure efficiency and flexibility Other opportunities in a challenging environment |

Major Announced Capital Projects and Preliminary 2015 CapEx 8 Over $1 billion of projects completed in 2013 and approximately $1 billion completed in 2014 Additional high quality growth projects under development for 2015 and beyond, with focus on capex efficiency CBF Train 5 Expansion (100 MBbl/d) New Badlands Infrastructure and Potential Plant, which may be downsized/delayed New Delaware Basin Plant, which may be downsized/delayed (1) 35 MBbl/d condensate splitter/alternative project expected to be in-service end of 2016 or early 2017, depending on permit timing and customer preference (2) Includes additional spending in both Permian Basin and North Texas (3) Additional gas processing plant will be in-service in Q1 2015 (4) ~$2.2-$2.4 billion of fee-based capital, ~74-76% of listed projects (4) Downstream Growth Projects Preliminary Total CapEx ($ millions) 2013 CapEx ($ millions) 2014 CapEx ($ millions) Preliminary 2015 CapEx ($ millions) Actual / Expected Completion Primarily Fee-Based Petroleum Logistics Projects - 2013 - 2015+ (1) $250 $40 $50 $30 2013 - 2015+ CBF Train 4 Expansion (100 MBbl/d) 385 120 20 0 Mid 2013 CBF Train 5 Expansion (100 MBbl/d) 385 0 50 200 Mid 2016 International Export Project 480 250 165 0 Q3 2013/Q3 2014 Other 130 30 50 25 Total Downstream Projects $1,630 $440 $335 $255 $1,630 G&P Growth Projects Preliminary Total CapEx ($ millions) 2013 CapEx ($ millions) 2014 CapEx ($ millions) Preliminary 2015 CapEx ($ millions) Actual / Expected Completion Primarily Fee-Based Gathering & Processing Expansion Program - 2013 - 2015+ (2) $185 $75 $110 $50 2013 - 2015+ North Texas Longhorn Project (200 MMcf/d) 150 40 20 0 May 2014 SAOU High Plains Plant (200 MMcf/d) 225 125 85 0 June 2014 Badlands Expansion Program - 2013 - Q1 2015 (3) 465 250 215 0 2013/Q1 2015 New Badlands Infrastructure and Potential Plant 150-320 0 0 125-250 YE 2015+ New Delaware Basin Plant (100-300 MMcf/d) 100-250 0 0 50-110 Mid 2016+ Other 40 25 15 10 Total G&P Projects $1,315 - $1,635 $515 $445 $235 - $420 $615 - $785 Total Projects $2,945 - $3,265 $955 $780 $490 - $675 $2,245 - $2,415 |

Additional Growth Opportunities Total CapEx ($ millions) Estimated Timing Primarily Fee-Based Badlands Expansion Program Permian Expansion Program Train 6 Expansion Train 7 Expansion Additional Condensate Splitter/Export Projects Ethane Export Project Other Projects primarily Total $2,000+ 2015 and beyond Major Capital Projects Under Development 9 In current environment, Targa is focused on capital efficiency and flexibility Over $2 billion of additional opportunities are in various stages of development Opportunities include additional infrastructure in both G&P and Downstream Increasing NGL supplies across the country will continue to drive the need for more processing, fractionation and connectivity |

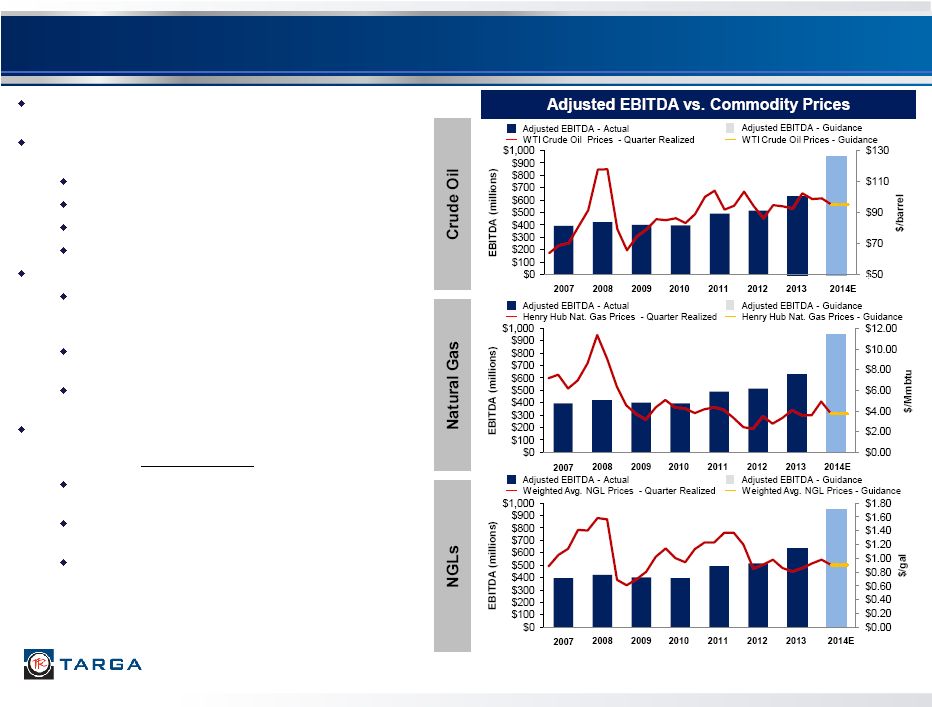

Diversity and Scale Mitigate Commodity Price Changes Growth has been driven by investing in the business, not by changes in commodity prices TRP benefits from multiple factors that help mitigate commodity price volatility, including: Scale Business and geographic diversity Increasing fee-based margin Hedging TRP’s current hedges include: Approximately 80% of 2014 natural gas and approximately 30% of 2014 combined NGL and condensate Approximately 50% to 60% of natural gas equity volumes for 2015 (1) and 20% to 30% for 2016 (1) Approximately 45% to 55% of condensate equity volumes for 2015 and 25% to 35% for 2016 Given our hedge position and our large fee-based operating margin, we estimate the following sensitivities for Targa Standalone 2015 EBITDA: A $5 drop in crude price would decrease EBITDA by ~$3 million A $0.05 drop in the weighted average NGLS price would decrease EBITDA by ~$12 million A $0.25 drop in natural gas price would result in an approximate $5 million decrease in EBITDA 10 (1) Will be towards bottom-end of range if there is significant ethane rejection in these years $120 $100 $80 $60 |

11 Targa Leverage and Liquidity (1) Includes TRP’s total availability under the revolver plus cash, less outstanding borrowings and letters of credit under the TRP revolver (2) Adjusts EBITDA to provide credit for material capital projects that are in process, but have not started commercial operation, and other items (2) Compliance Leverage Ratio Liquidity (1) Completed $800 million 4.125% unsecured notes offering in October 2014 Pro forma for offering, liquidity as of September 30, 2014 is $1.45 billion including capacity under accounts receivable securitization facility YTD through September 2014, raised net proceeds of $257 million from equity issuances under at-the-market (“ATM”) program Target compliance leverage 3x - 4x Debt/EBITDA Have historically been on low end of range Leverage increased at end of 2012 due to Badlands acquisition Q3 2014 compliance leverage was 2.7x |

12 Targa + Atlas: Transaction Overview Targa Resources Partners LP (NYSE: NGLS; “TRP” or the “Partnership”) has executed a definitive agreement to acquire Atlas Pipeline Partners, L.P. (NYSE: APL) for $5.8 billion (1) 0.5846 NGLS common units plus a one-time cash payment of $1.26 for each APL LP unit (implied premium (1) of 15%) $1.8 billion of debt at September 30, 2014 Targa Resources Corp. (NYSE: TRGP; “TRC” or the “Company”) has executed a definitive agreement to acquire Atlas Energy, L.P. (NYSE: ATLS), after its spin-off of non APL-related assets, for $1.9 billion (1) Prior to TRGP’s acquisition, all assets held by ATLS not associated with APL will be spun out to existing ATLS unitholders 10.35 million TRGP shares issued to ATLS unitholders $610 million of cash to ATLS Each existing ATLS (after giving effect to ATLS’ spin out) unit will receive 0.1809 TRGP shares and $9.12 in cash Accretive to NGLS and TRGP cash flow per unit and share, respectively, immediately and over the longer-term, while providing APL and ATLS unitholders increased value now and into the future Post closing (2) , NGLS plans to increase its quarterly distribution by $0.04 per LP unit ($0.16 per LP unit annualized rate) NGLS expects 11-13% distribution growth in 2015 compared to 7-9% in 2014 Post closing (2) , TRGP plans to increase its quarterly dividend by $0.10 per share ($0.40 per share annualized rate) TRGP expects approximately 35% dividend growth (3) in 2015 compared to 25%+ in 2014 Transactions are cross-conditional and subject to shareholder and regulatory approvals HSR clearance received Continue to expect transaction to close in Q1 2015 (1) Based on market data as of October 10, 2014, excluding transaction fees and expenses (2) Management intends to recommend this increase at the first regularly scheduled quarterly distribution declaration Board meeting after transaction closes (3) Assumes NGLS distribution growth of 11-13% |

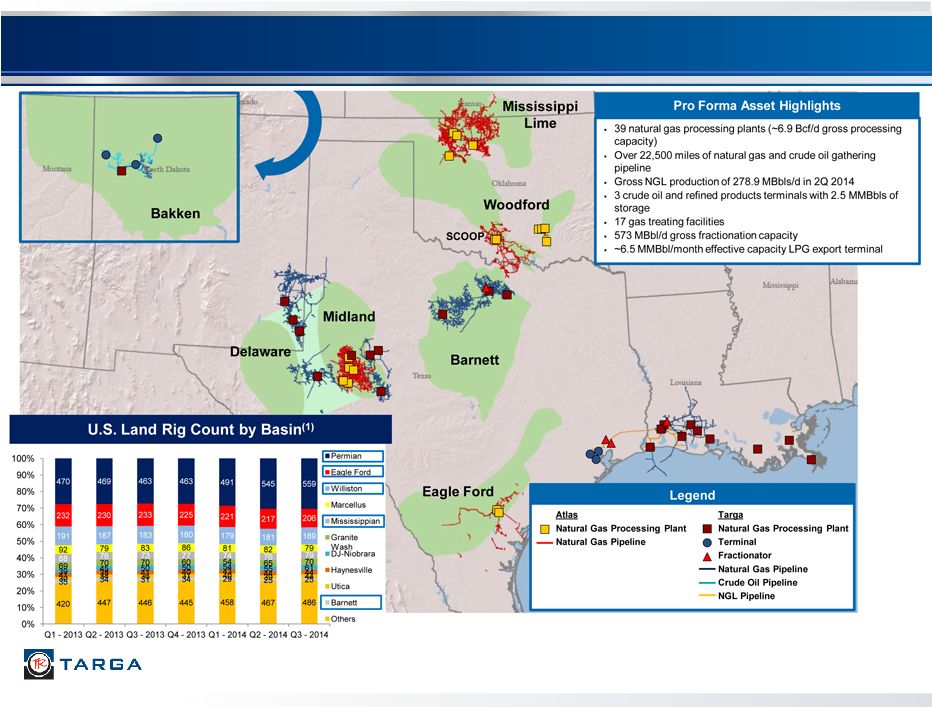

13 Targa + Atlas: Attractive Positions in Active Basins (1) Source: Baker Hughes Incorporated, as of October 20, 2014 |

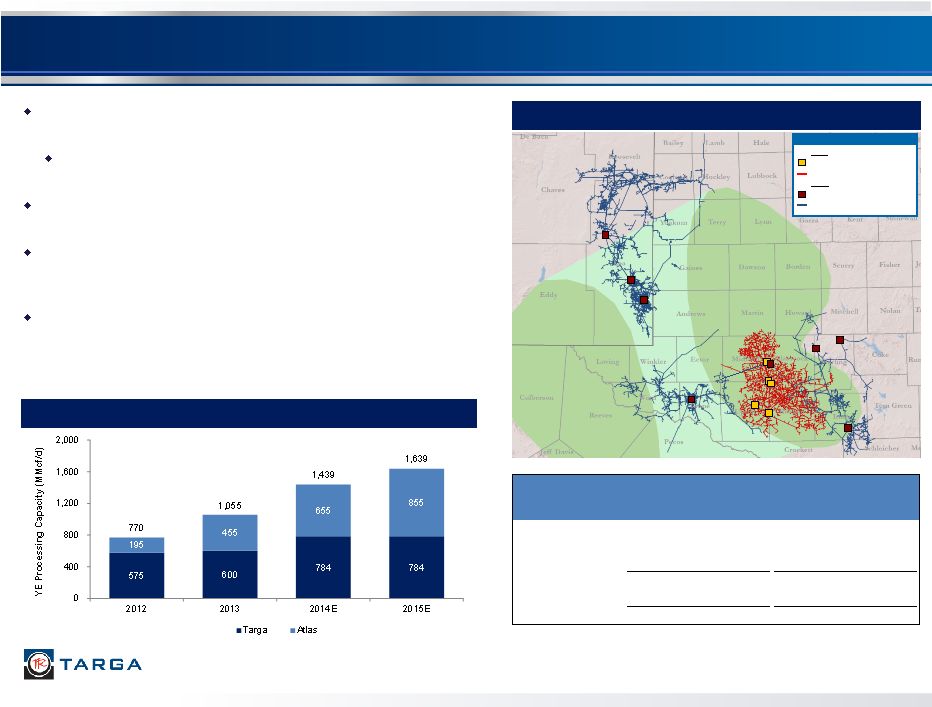

14 World Class Permian Footprint Atlas’ WestTX system sits in the core of the Midland Basin between Targa’s existing SAOU and Sand Hills systems More than 75% of the rigs currently running in the Midland Basin are in counties served by the combined systems Pro forma, NGLS will be the 2 nd largest Permian processor with 1.4 Bcf/d in gross processing capacity Recent activity includes Targa’s 200 MMcf/d High Plains plant placed in service June 2014 and Atlas’ 200 MMcf/d Edward plant placed in service September 2014 Announced expansions include Atlas’ 200 MMcf/d Buffalo plant (in service mid 2015) and Targa’s 300 MMcf/d Delaware Basin plant (in service mid 2016) Combined Permian Footprint Year-End Permian Gross Processing Capacity Legend Atlas Natural Gas Processing Plant Natural Gas Pipeline Targa Natural Gas Processing Plant Natural Gas Pipeline Current Permian Gross Processing Capacity (MMcf/d) Miles of Pipeline SAOU 369 1,800 Sand Hills 175 1,500 Versado 240 3,350 Total: Targa 784 6,650 Atlas WestTX 655 3,600 Total: PF Targa 1,439 10,250 Delaware Midland |

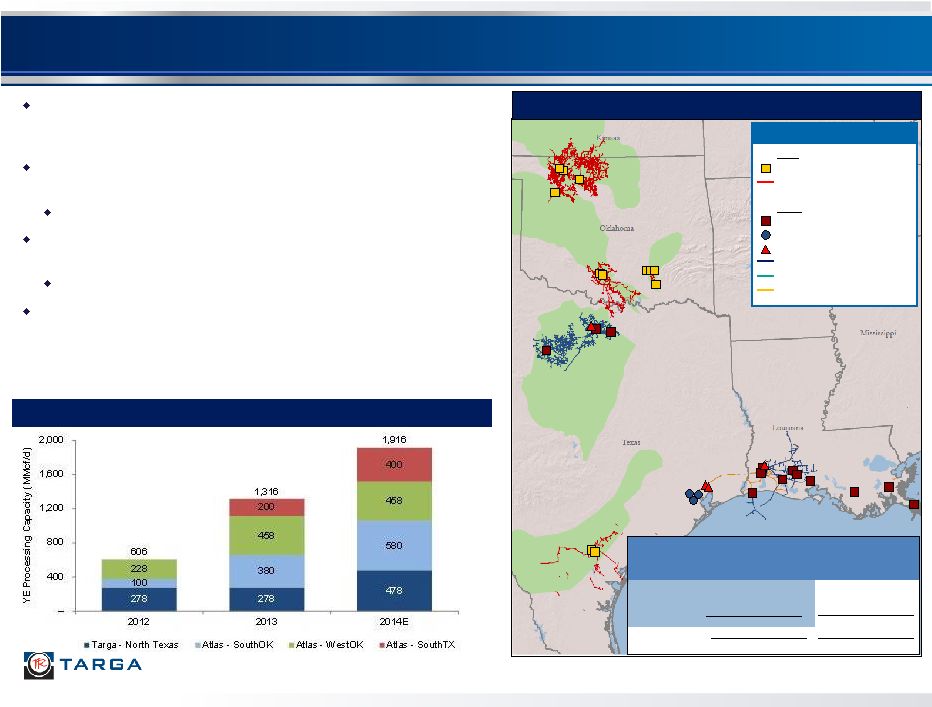

15 Leading Positions in Active Basins Combined Footprint Year-End NorthTX/SouthTX/OK Gross Processing Capacity Atlas Natural Gas Processing Plant Natural Gas Pipeline Targa Natural Gas Processing Plant Terminal Fractionator Natural Gas Pipeline Crude Oil Pipeline NGL Pipeline Legend Barnett Eagle Ford Woodford Mississippi Lime Atlas’ assets also provide exposure to significant drilling activity in the Mississippi Lime, SCOOP, Arkoma Woodford and Eagle Ford plays Largest gathering and processing footprint in the Mississippi Lime with 458 MMcf/d of nameplate capacity System remains full with volumes offloaded to third parties Current project underway to connect Velma & Arkoma systems to create a gathering and processing super-system Further potential to connect to Targa’s North Texas assets Long-term contracts with active producers in the Eagle Ford SCOOP Current North Texas/SouthTX/OK Gross Processing Capacity (MMcf/d) Miles of Pipeline SouthOK 500 1,300 WestOK 458 5,700 SouthTX 400 500 Total: Atlas 1,358 7,500 Targa North Texas 478 4,500 Total: PF Targa 1,836 12,000 |

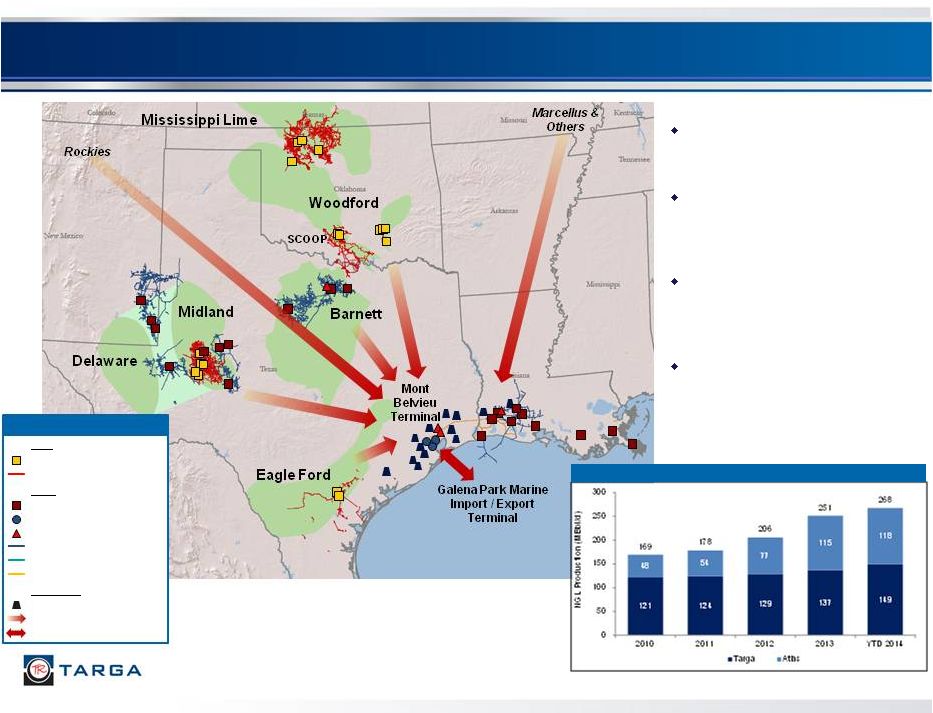

16 16 Producer Activity Drives NGL Flows to Mont Belvieu Growing field NGL production increases NGL flows to Mont Belvieu Increased NGL production could support Targa’s existing and expanding Mont Belvieu and Galena Park presence Petrochemical investments, fractionation and export services will continue to clear additional supply Targa’s Mont Belvieu and Galena Park businesses very well positioned Combined NGL Production (MBbl/d) Atlas Natural Gas Processing Plant Natural Gas Pipeline Targa Natural Gas Processing Plant Terminal Fractionator Natural Gas Pipeline Crude Oil Pipeline NGL Pipeline Third Party Ethylene Cracker Illustrative Y-Grade Flows Import / Export Legend |

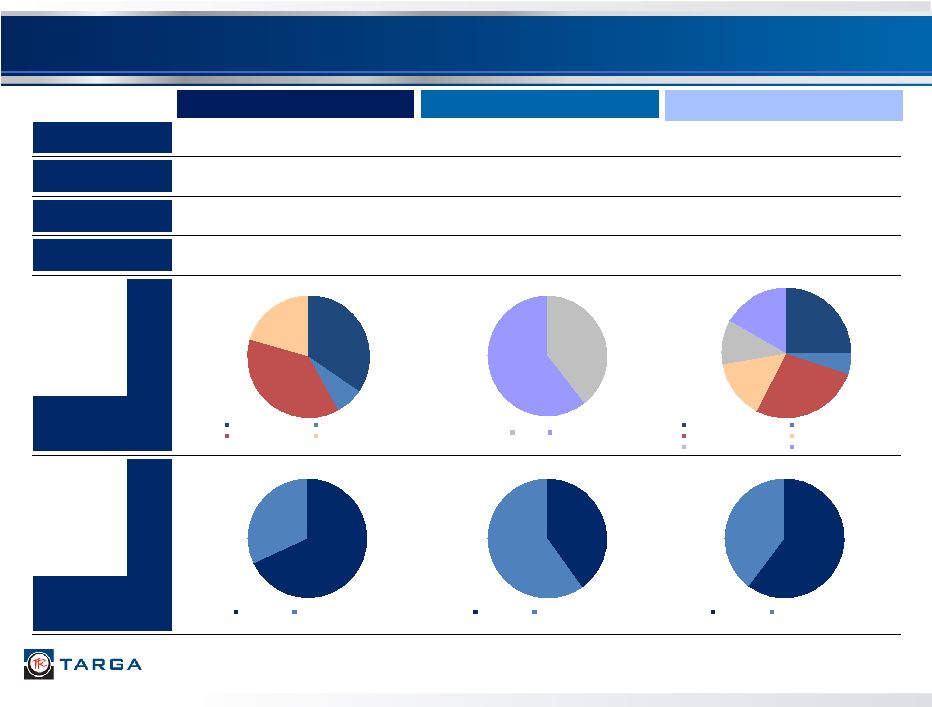

Market Cap ~ $10 Billion (1) ~ $3 Billion (2) ~ $13 Billion (1) Enterprise Value ~ $13 Billion (1) ~ $6 Billion (2) ~ $19 Billion (1) 2014E EBITDA ($MM) $925 - $975 Million $400 - $425 Million $1,325 - $1,400 Million 2014E Growth CAPEX ($MM) $780 Million $400 - $450 Million $1,180 - $1,230 Million 2014E Operating Margin by Segment YE 2014E % Fee- Based 68% 32% Fixed Fee Percent of Proceeds 35% 7% 38% 20% Field G&P Coastal G&P Logistics Marketing and Dist. 40% 60% Texas Oklahoma 25% 5% 27% 15% 11% 17% Field G&P - Targa Coastal G&P - Targa Logistics - Targa Marketing and Dist. - Targa Texas - Atlas Oklahoma - Atlas 40% 60% Fixed Fee Percent of Proceeds 60% 40% Fixed Fee Percent of Proceeds 17 Targa + Atlas: Increased Size and Scale Enhance Credit Profile Targa Atlas Pro Forma Targa (1) Represents combined market cap and enterprise value for NGLS and TRGP as of December 31, 2014, less the value of NGLS units or PF NGLS units owned by TRGP (2) Represents combined market cap and enterprise value for APL and ATLS as of December 31, 2014 based on transaction consideration (3) Includes keep-whole at 1% of total margin (3) |

18 Targa + Atlas: Strategic Highlights Attractive Positions in Active Basins Creates World- Class Permian Footprint Complementary Assets with Significant Growth Opportunities Enhances Credit Profile Significant Long- Term Value Creation Already strong positions in Permian and Bakken enhanced with entry into Mississippi Lime and Eagle Ford 4 of the top 5 basins by active rig count and unconventional well spuds (1) Top 3 basins by oil production (1) Also exposed to emerging SCOOP play and continued development of NGL-rich Barnett Shale Adds diversity and leadership position in all basins/plays Combines strong Permian Basin positions to create a premier franchise Provides new customer relationships with the most active operators in each basin Current combined processing capacity of 1,439 MMcf/d Significant organic growth project opportunities 2014 pro forma growth capex of ~$1.2 billion Additional projects under development of over $3 billion NGL production to support Targa’s leading NGL position in Mont Belvieu and Galena Park Estimated pro forma leverage ratio of 3.3x Total Debt / 2014E EBITDA (4) at NGLS Increased size and scale move NGLS credit metrics closer to investment grade over time Immediately accretive to distributable cash flow at both NGLS and TRGP Increases FY 2015 vs FY 2014 distribution growth at NGLS to 11-13% and at TRGP to approximately 35% Provides larger asset base with additional long-term growth opportunities Higher long-term distribution/dividend growth profile than Targa standalone (1) Source: Oil & Gas Investor (2) Based on market data as of December 31, 2014, less the value of 16.3 MM PF NGLS units owned by TRGP (3) Based on NGLS and APL guidance ranges (4) Based on estimated compliance ratio Increased Size and Scale Combined partnership will be one of the largest diversified MLPs Pro forma enterprise value (2) of $19 billion Pro forma 2014E EBITDA of approximately $1.3-$1.4 billion (3) |

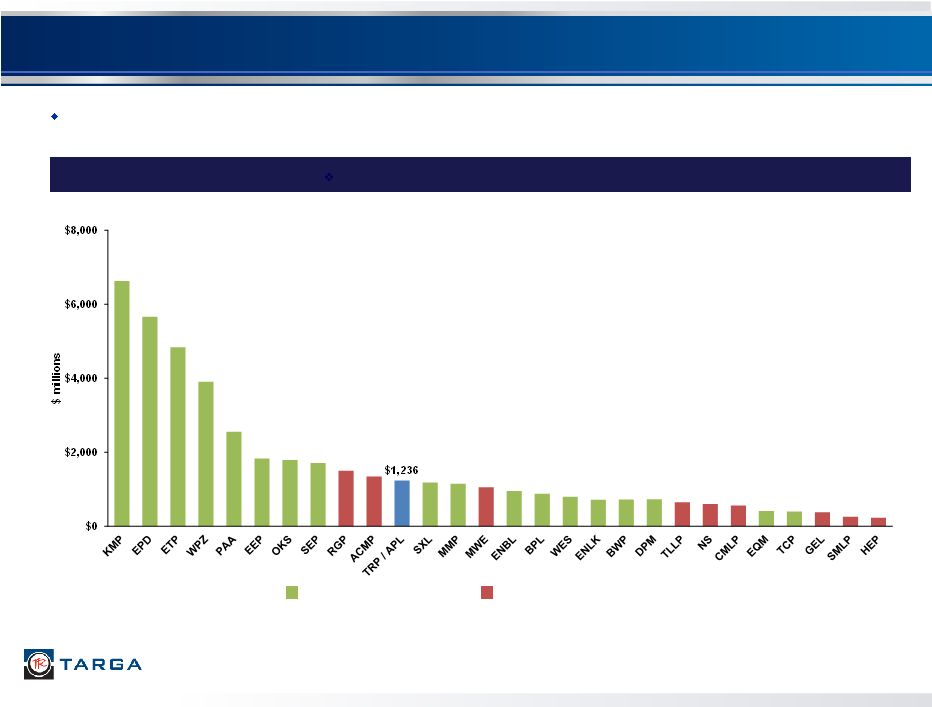

Targa Resources – Diversified MLP with Increased Scale 19 MLPs Ranked by 2015E EBITDA (1) Creates 11th largest diversified MLP on EBITDA basis (upper mid-cap / lower large-cap MLP) Note: TRP/APL combination includes $20 million of synergies (1) Source: Wall Street research estimates Investment Grade MLPs Non-Investment Grade MLPs |

20 Targa + Atlas: Current Commodity Price Environment Despite the current and forward commodity price environment being weaker than when the Targa/Atlas transaction was announced on October 13, 2014, we maintain the pro forma distribution and dividend growth estimates originally provided: 2015 distribution growth for TRP of 11% to 13% 2015 dividend growth for TRC of 35% TRP currently expects the above referenced pro forma distribution growth range for 2015, along with pro forma distribution coverage of approximately 1.0 to 1.2 times, under a range of possible scenarios: (i) (a) commodity prices of $3.75 per MMBtu for natural gas, $60 per barrel for crude oil and $0.60 per gallon for NGLs; (b) current expectations of activity levels at these prices, resulting in low single digit annual volume growth for pro forma TRP and APL field gathering and processing businesses compared to current estimated fourth quarter 2014 volumes; and (c) only LPG export volumes that are currently under contract (ii) (a) commodity prices of $4.00 per MMBtu for natural gas, $80 per barrel for crude oil and $0.80 per gallon for NGLs; (b) volume growth in line with historical growth rates as expected at the time of announcement for pro forma TRP and APL field gathering and processing businesses; and (c) a modest level of export volumes above those currently under contract |

Targa Investment Highlights 21 Well positioned in U.S. shale / resource plays, with an even stronger footprint in active basins with close of the Targa/Atlas transaction Leadership position at Mont Belvieu and associated LPG export facility at Houston Ship Channel Increasing scale, diversity and fee-based margin Strong financial profile Strong track record of distribution and dividend growth Experienced management team |

Appendix |

23 This presentation includes the non-GAAP financial measure of Adjusted EBITDA. The presentation provides a reconciliation of this non-GAAP financial measures to its most directly comparable financial measure calculated and presented in accordance with generally accepted accounting principles in the United States of America ("GAAP"). Our non-GAAP financial measures should not be considered as alternatives to GAAP measures such as net income, operating income, net cash flows provided by operating activities or any other GAAP measure of liquidity or financial performance. Non-GAAP Measures Reconciliation |

24 Adjusted EBITDA – The Partnership and Targa define Adjusted EBITDA as net income attributable to Targa Resources Partners LP before: interest; income taxes; depreciation and amortization; gains or losses on debt repurchases and redemptions; early debt extinguishment and asset disposals; non-cash risk management activities related to derivative instruments; changes in the fair value of the Badlands acquisition contingent consideration and the non-controlling interest portion of depreciation and amortization expenses. Adjusted EBITDA is used as a supplemental financial measure by our management and by external users of our financial statements such as investors, commercial banks and others. The economic substance behind management’s use of Adjusted EBITDA is to measure the ability of our assets to generate cash sufficient to pay interest costs, support our indebtedness and make distributions to our investors. Adjusted EBITDA is a non-GAAP financial measure. The GAAP measures most directly comparable to Adjusted EBITDA are net cash provided by operating activities and net income (loss) attributable to Targa Resources Partners LP. Adjusted EBITDA should not be considered as an alternative to GAAP net cash provided by operating activities or GAAP net income. Adjusted EBITDA has important limitations as an analytical tool. Investors should not consider Adjusted EBITDA in isolation or as a substitute for analysis of our results as reported under GAAP. Because Adjusted EBITDA excludes some, but not all, items that affect net income and net cash provided by operating activities and is defined differently by different companies in our industry, our definition of Adjusted EBITDA may not be comparable to similarly titled measures of other companies. Management compensates for the limitations of Adjusted EBITDA as an analytical tool by reviewing the comparable GAAP measures, understanding the differences between the measures and incorporating these insights into management’s decision-making processes. Non-GAAP Measures Reconciliation |

25 1000 Louisiana Suite 4300 Houston, TX 77002 Phone: (713) 584-1000 Email: InvestorRelations@targaresources.com Website: www.targaresources.com |