Confidential

Presentation to the

Board of Directors Regarding

Project MELODY

Strategic Alternatives Analysis

December, 2011

Confidential Important Information

Important Information

Confidential Material Presented to the Special Committee of the Board of Directors of MELODY

The following pages contain material that was prepared by William Blair & Company, L.L.C. (“William Blair”) and provided to the Special Committee of the Board of Directors of MELODY (the “Company”) in connection with their consideration of a potential business combination between the Company and an affiliate to Mr. Yingjie Gao and certain members of the management. The accompanying material was compiled or prepared on a confidential basis for use by the Special Committee of the Board of Directors and not with a view toward public disclosure. The information utilized in preparing this presentation was obtained from the Company and other public sources. Any estimates and projections for the Company contained herein have been prepared by or approved by senior management, or based upon such estimates and projections, and involve numerous and significant subjective determination, which may or may not prove to be correct. No representation or warranty, express or implied, is made as to the accuracy or completeness of such information and nothing contained herein is, or shall be relied upon as, a representation, whether as to the past or the future. Because this material was prepared for use in the context of an oral presentation to the Special Committee of the Board of Directors, which is familiar with the business and affairs of the Company, neither the Company nor William Blair nor any of their respective legal or financial advisors or accountants take any responsibility for the accuracy or completeness of any of the material if used by persons other than the Special Committee of the Board of Directors of the Company. Neither the Company nor William Blair undertakes any obligation to update or otherwise revise the accompanying materials. This presentation does not constitute an opinion and William Blair’s only opinion is the opinion that is to be rendered to the Special Committee of the Board of Directors of the Company.

1

Confidential Table of Contents

Table of Contents

I. Executive Summary

II. MELODY Business Overview III. MELODY Situation Overview IV. Valuation Analysis A. Summary of Transaction

B. Selected Public Companies Analysis C. Selected M&A Transactions Analysis D. Discounted Cash Flow Analysis E. Leveraged Buyout Analysis

F. Premiums Paid Analysis Appendix A. Supporting Financial Schedules

2

Confidential

Executive Summary

Confidential Executive Summary

Background

William Blair has been retained by the Special Committee of the Board of Directors of MELODY to provide certain analysis (the “Analysis”). This Analysis includes a review of the following:

Financial review of the Company: Historical financial performance Forecasted financial performance Preliminary valuation parameters

2

Confidential Executive Summary

Scope of Review and Analysis

In connection with this Analysis, Blair familiarized itself, to the extent it deemed appropriate, with the business, operations, financial condition and prospects of the Company Blair examined and relied upon information from several sources: Visited the Company’s headquarters in Shenzhen, Peoples Republic of China; Discussions with senior management regarding the Company’s historical financial results, current business operations and forecasted financial performance; Certain audited historical financial statements of the Company for the fiscal years ended December 2005 through December 2010; The unaudited financial statements of the Company for the nine months ended September 2010 and September 2011; Certain internal business, operating and financial information and forecasts for the years ended December 2011 through December 2016 (the “Forecasts”), prepared by the senior management of the Company; Financial terms of certain other transactions we deemed relevant and who’s information is publicly available; The financial position and operating results of the Company compared with those of certain other publicly traded companies we deemed relevant; Selected industry research and market analysis; Current and historical market prices and trading volumes of the Company common stock; and Certain other publicly available information relating to the Company Blair relied on the information furnished by the Company (and information available from public sources and other sources deemed reliable by Blair) without assuming any duty of independent verification thereof or independent appraisal of any of the assets of the Company Blair does not assume responsibility for the accuracy or completeness of the information or any other information regarding the Company Blair expressed no opinion with respect to the Company’s Forecasts or the estimates and judgments on which they are based

3

Confidential Executive Summary

Key Assumptions Underlying Our Review and Analysis

All information made available to Blair by the Company with respect to the Analysis was complete and correct in all material respects and that any projections, forecasts or other information provided by the Company to Blair was prepared in good faith and based upon reasonable assumptions The Forecasts examined by us have been reasonably prepared on bases reflecting the best currently available estimates and judgments of the senior management of MELODY, and we have assumed, with your consent, that the Forecasts will be achieved in the amounts and at the times contemplated thereby

4

Confidential Executive Summary

Summary of Valuation Analysis

Blair performed several analyses to assist in the development of its strategic alternatives analysis

Selected Public Companies Analysis

Trading multiple analysis based on companies that William Blair considered relevant

Selected Transaction Analysis

Transaction multiple analysis based on transactions that William Blair considered relevant

Discounted Cash Flow Analysis

Utilized MELODY’s forecasts to derive free cash flows for the Company for 2011E – 2016E. Employed a 11.0% –15.0% range of discount rates to determine the present values of such cash flows. Estimated a terminal value by utilizing 2016E EBITDA exit multiples of 5.3x – 6.3x

Leveraged Acquisition Analysis

Analyzed the purchase prices at which a leveraged acquisition of MELODY could occur based on a target IRR range of 20.0% – 30.0% and 2016E EBITDA exit multiples of 5.3x – 6.3x

M&A Premiums Paid Analysis

Reviewed the premiums derived by comparing the per share equity consideration paid to the trailing one day, one week, one month and 90 days trading prices for 728 public targets with 100% of target equity acquired for all cash and from $25M to $250M in deal size since January 1, 2006

5

Confidential Executive Summary

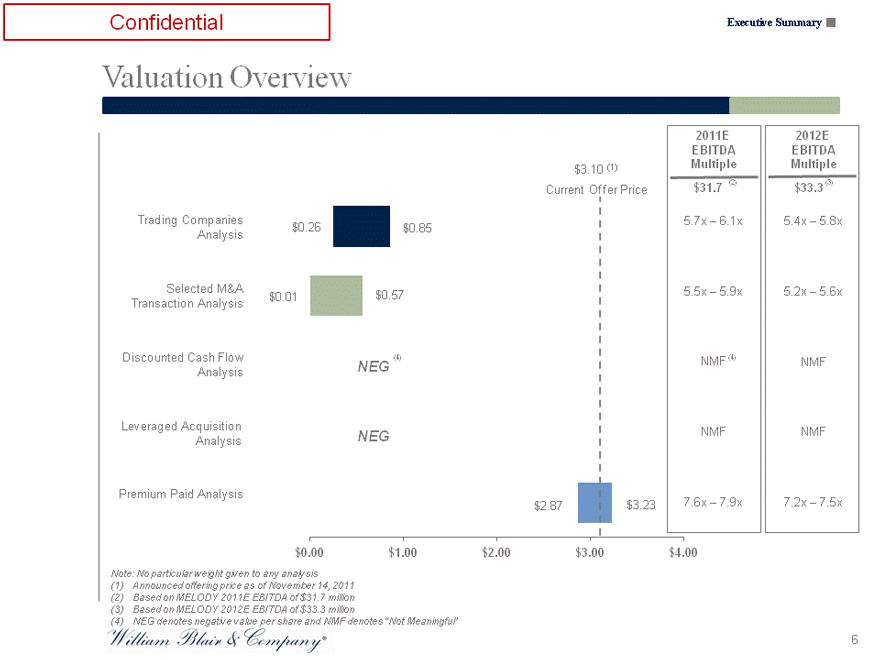

Valuation Overview

Trading Companies

Analysis

Selected M&A

Transaction Analysis

Discounted Cash Flow

Analysis

Leveraged Acquisition

Analysis

Premium Paid Analysis

$0.26

$0.01

$0.85

$0.57

(4)

NEG

NEG

$3.10 (1) Current Offer Price

2011E EBITDA Multiple $31.7 (2)

5.7x – 6.1x 5.5x – 5.9x NMF(4) NMF

2012E EBITDA Multiple

$33.3(3)

5.4x – 5.8x

5.2x – 5.6x NMF

NMF

$2.87 $3.23 7.6x – 7.9x 7.2x – 7.5x

$0.00 $1.00 $2.00 $3.00 $4.00

Note: No particular weight given to any analysis

(1) Announced offering price as of November 14, 2011 (2) Based on MELODY 2011E EBITDA of $31.7 million (3) Based on MELODY 2012E EBITDA of $33.3 million

(4) NEG denotes negative value per share and NMF denotes “Not Meaningful”

6

Confidential

MELODY Business Overview

Confidential

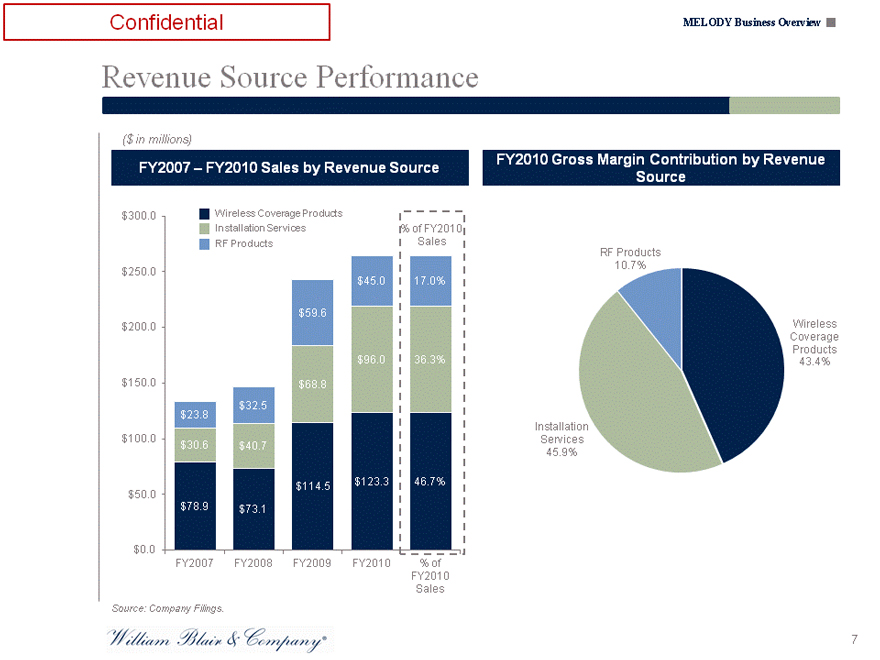

Revenue Source Performance

MELODY Business Overview

($ in millions)

FY2007 – FY2010 Sales by Revenue Source

$300.0 $250.0 $200.0 $150.0 $100.0 $50.0 $0.0

Wireless Coverage Products Installation Services RF Products

$45.0 17.0%

$59.6

$96.0 36.3%

$68.8

$23.8 $32.5

$30.6 $40.7

$114.5 $123.3 46.7%

$78.9 $73.1

% of FY2010 Sales

FY2007 FY2008 FY2009 FY2010 % of FY2010 Sales

Source: Company Filings.

FY2010 Gross Margin Contribution by Revenue Source

RF Products 10.7%

Installation Services 45.9%

Wireless Coverage Products 43.4%

7

Confidential MELODY Business Overview

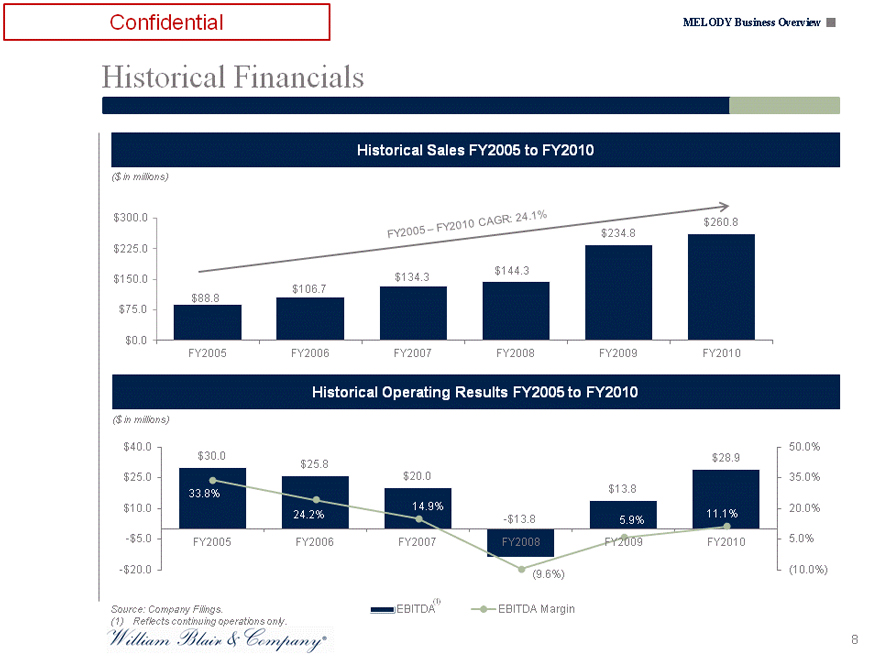

Historical Financials

Historical Sales FY2005 to FY2010

($ in millions)

$300.0 $225.0 $150.0 $75.0 $0.0

$260.8 $234.8

$144.3 $134.3 $106.7

$88.8

FY2005 FY2006 FY2007 FY2008 FY2009 FY2010

Historical Operating Results FY2005 to FY2010

($ in millions)

$40.0 $25.0 $10.0

-$5.0

-$20.0

$30.0 $28.9

$25.8

$20.0

$13.8

33.8%

14.9%

24.2% 11.1%

-$13.8 5.9%

FY2005 FY2006 FY2007 FY2008 FY2009 FY2010

(9.6%)

50.0% 35.0% 20.0% 5.0% (10.0%)

EBITDA (1) EBITDA Margin

Source: Company Filings.

(1) Reflects continuing operations only.

8

Confidential

MELODY Situation Overview

Confidential MELODY Situation Overview

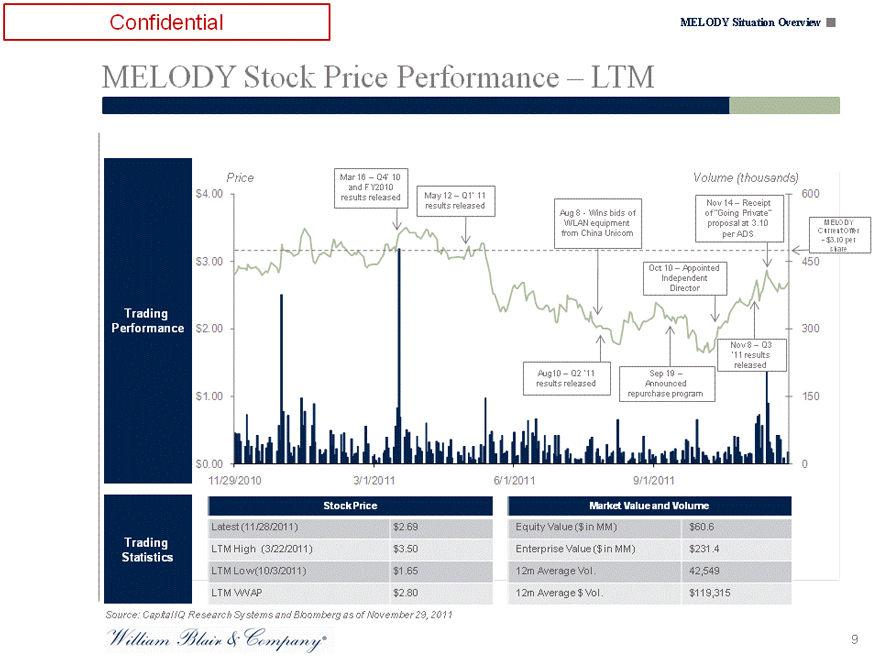

MELODY Stock Price Performance – LTM

Trading Performance

Trading Statistics

Price

Mar 16 – Q4’ 10 Volume (thousands)

and FY2010 results released May 12 – Q1’ 11 600 results released Nov 14 – Receipt Aug 8—Wins bids of of “Going Private”

WLAN equipment proposal at 3.10 MELODY from China Unicom per ADS Current Offer

- $3.10 per share

Oct 10 – Appointed Independent Director

Nov 8 – Q3 ‘11 results Aug10 – Q2 ‘11 Sep 19 – released results released Announced repurchase program

450 300 150

0

11/29/2010 3/1/2011 6/1/2011 9/1/2011

Trading Statistics

11/29/2010 3/1/2011 6/1/2011 9/1/2011

0

Stock Price

Latest (11/28/2011) $2.69 LTM High (3/22/2011) $3.50 LTM Low (10/3/2011) $1.65 LTM VWAP $2.80

Market Value and Volume

Equity Value ($ in MM) $60.6 Enterprise Value ($ in MM) $231.4 12m Average Vol. 42,549 12m Average $ Vol. $119,315

Source: Capital IQ Research Systems and Bloomberg as of November 29, 2011

9

Confidential MELODY Situation Overview

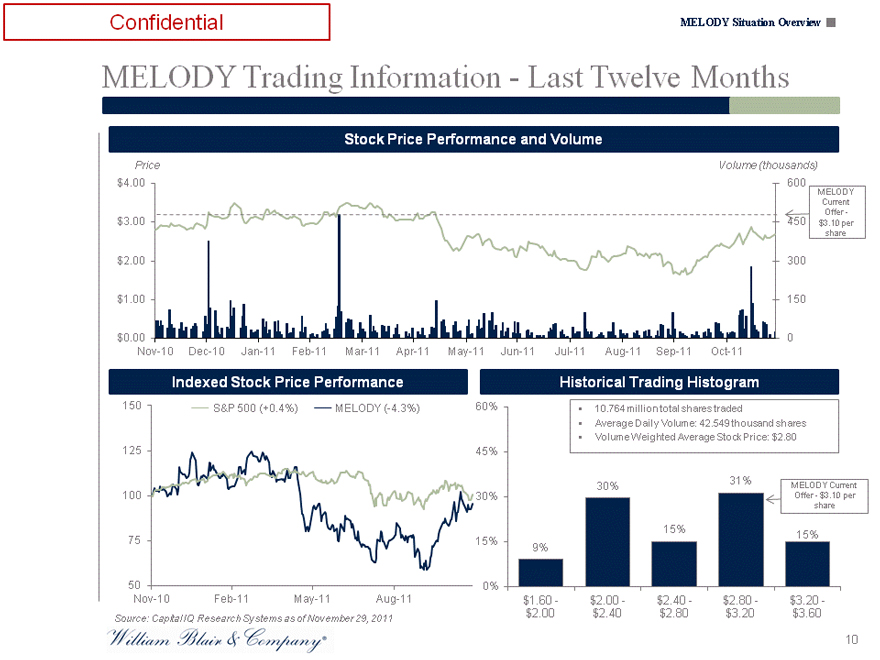

MELODY Trading Information—Last Twelve Months

Stock Price Performance and Volume

Price Volume (thousands)

$4.00 $3.00 $2.00 $1.00 $0.00

600 MELODY Current Offer -450 $3.10 per share

300 150 0

Nov-10 Dec-10 Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11

Indexed Stock Price Performance

150 125 100 75 50

S&P 500 (+0.4%) MELODY (-4.3%)

Nov-10 Feb-11 May-11 Aug-11

60% 45% 30% 15% 0%

Historical Trading Histogram

10.764 million total shares traded

Average Daily Volume: 42.549 thousand shares Volume Weighted Average Stock Price: $2.80

30% 31% MELODY Current Offer—$3.10 per share

15%

15% 9%

$1.60—$2.00—$2.40—$2.80—$3.20 -$2.00 $2.40 $2.80 $3.20 $3.60

Source: Capital IQ Research Systems as of November 29, 2011

10

Confidential MELODY Situation Overview

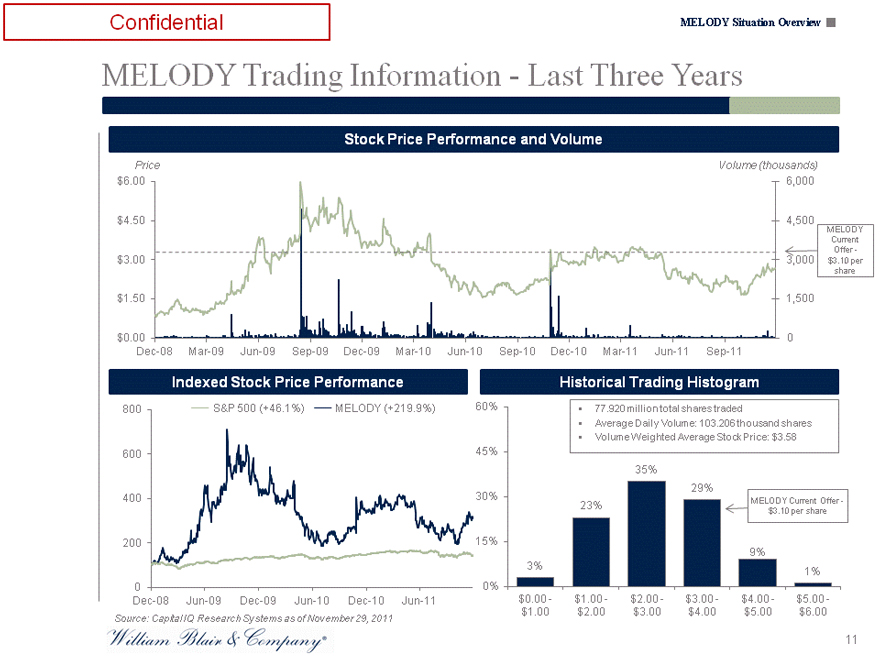

MELODY Trading Information—Last Three Years

Stock Price Performance and Volume

Price Volume (thousands)

$6.00 6,000

$4.50 4,500

MELODY

Current

Offer -

$3.00 3,000 $3.10 per

share

$1.50 1,500

$0.00 0

Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11

Indexed Stock Price Performance

800 S&P 500 (+46.1%) MELODY (+219.9%)

600

400

200

0

Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11

Historical Trading Histogram

60% 77.920 million total shares traded

Average Daily Volume: 103.206 thousand shares

Volume Weighted Average Stock Price: $3.58

45%

35%

29%

30% MELODY Current Offer -

23% $3.10 per share

15%

9%

3% 1%

0%

$0.00— $1.00— $2.00— $3.00— $4.00— $5.00 -

$1.00 $2.00 $3.00 $4.00 $5.00 $6.00

Source: Capital IQ Research Systems as of November 29, 2011

11

Confidential MELODY Situation Overview

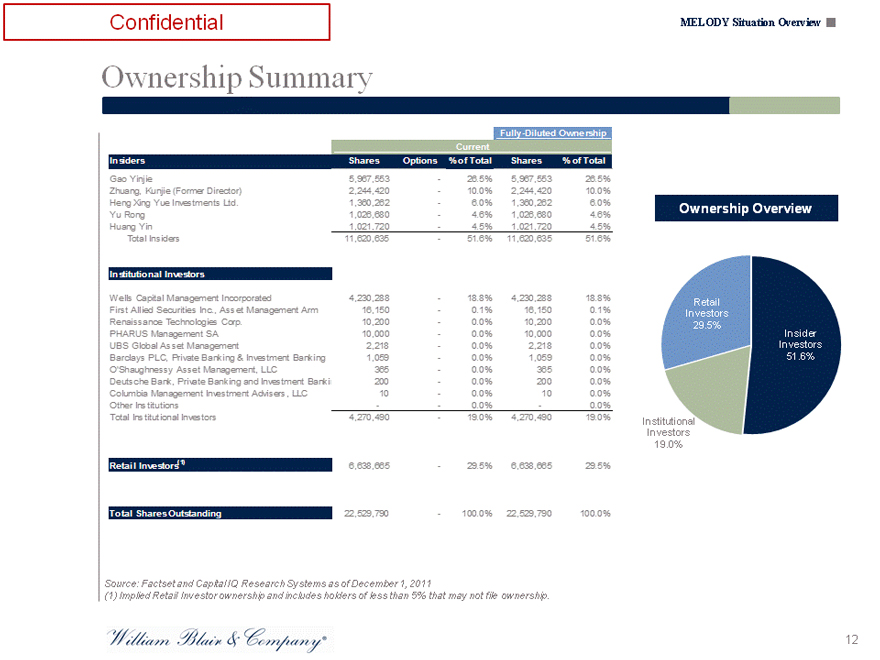

Ownership Summary

Fully-Diluted Ownership

Current

Insiders Shares Options % of Total Shares % of Total

Gao Yinjie 5,967,553 — 26.5% 5,967,553 26.5%

Zhuang, Kunjie (Former Director) 2,244,420 — 10.0% 2,244,420 10.0%

Heng Xing Yue Investments Ltd. 1,360,262 — 6.0% 1,360,262 6.0%

Yu Rong 1,026,680 — 4.6% 1,026,680 4.6%

Huang Yin 1,021,720 — 4.5% 1,021,720 4.5%

Total Insiders 11,620,635 — 51.6% 11,620,635 51.6%

Institutional Investors

Wells Capital Management Incorporated 4,230,288 — 18.8% 4,230,288 18.8%

First Allied Securities Inc., Asset Management Arm 16,150 — 0.1% 16,150 0.1%

Renaissance Technologies Corp. 10,200 — 0.0% 10,200 0.0%

PHARUS Management SA 10,000 — 0.0% 10,000 0.0%

UBS Global Asset Management 2,218 — 0.0% 2,218 0.0%

Barclays PLC, Private Banking & Investment Banking 1,059 — 0.0% 1,059 0.0%

O’Shaughnessy Asset Management, LLC 365 — 0.0% 365 0.0%

Deutsche Bank, Private Banking and Investment Bankin 200 — 0.0% 200 0.0%

Columbia Management Investment Advisers, LLC 10 — 0.0% 10 0.0%

Other Institutions —— 0.0% — 0.0%

Total Institutional Investors 4,270,490 — 19.0% 4,270,490 19.0%

Retail Investors(1) 6,638,665 — 29.5% 6,638,665 29.5%

Total Shares Outstanding 22,529,790 — 100.0% 22,529,790 100.0%

Source: Factset and Capital IQ Research Systems as of December 1, 2011

(1) Implied Retail Investor ownership and includes holders of less than 5% that may not file ownership.

Ownership Overview

Retail Investors 29.5% (1)

Insider Investors 51.6%

Institutional Investors

19.0%

12

Confidential MELODY Situation Overview

Research Coverage Overview

Limited number of research analysts cover MELODY

($ in millions) CY 2011 Estimate

Broker (Analyst) Rating Revenue EBITDA EPS Last Updated

China International Capital Corp. ACCUMULATE $308.9 NA $0.78 03/18/2011

MELODY Management (2) $287.0 $31.7 $0.63 12/02/2011

Sources: Thomson ONE Banker reports and Bloomberg. (1) Based on March 18, 2011 research report (2) MELODY management projections

13

Confidential MELODY Situation Overview

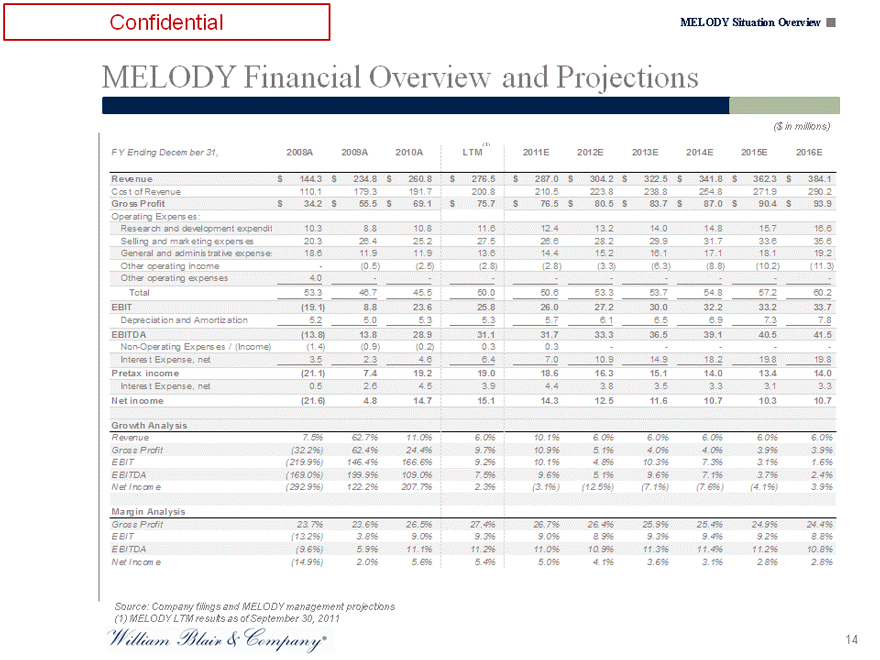

MELODY Financial Overview and Projections

($ in millions)

FY Ending December 31, 2008A 2009A 2010A LTM(1) 2011E 2012E 2013E 2014E 2015E 2016E

Revenue $ 144.3 $ 234.8 $ 260.8 $ 276.5 $ 287.0 $ 304.2 $ 322.5 $ 341.8 $ 362.3 $ 384.1

Cost of Revenue 110.1 179.3 191.7 200.8 210.5 223.8 238.8 254.8 271.9 290.2

Gross Profit $ 34.2 $ 55.5 $ 69.1 $ 75.7 $ 76.5 $ 80.5 $ 83.7 $ 87.0 $ 90.4 $ 93.9

Operating Expenses:

Research and development expendit 10.3 8.8 10.8 11.6 12.4 13.2 14.0 14.8 15.7 16.6

Selling and marketing expenses 20.3 26.4 25.2 27.5 26.6 28.2 29.9 31.7 33.6 35.6

General and administrative expenses 18.6 11.9 11.9 13.6 14.4 15.2 16.1 17.1 18.1 19.2

Other operating income — (0.5) (2.5) (2.8) (2.8) (3.3) (6.3) (8.8) (10.2) (11.3)

Other operating expenses 4.0 — ——— — — — — -

Total 53.3 46.7 45.5 50.0 50.6 53.3 53.7 54.8 57.2 60.2

EBIT (19.1) 8.8 23.6 25.8 26.0 27.2 30.0 32.2 33.2 33.7

Depreciation and Amortization 5.2 5.0 5.3 5.3 5.7 6.1 6.5 6.9 7.3 7.8

EBITDA (13.8) 13.8 28.9 31.1 31.7 33.3 36.5 39.1 40.5 41.5

Non-Operating Expenses / (Income) (1.4) (0.9) (0.2) 0.3 0.3 — — — — -

Interest Expense, net 3.5 2.3 4.6 6.4 7.0 10.9 14.9 18.2 19.8 19.8

Pretax income (21.1) 7.4 19.2 19.0 18.6 16.3 15.1 14.0 13.4 14.0

Interest Expense, net 0.5 2.6 4.5 3.9 4.4 3.8 3.5 3.3 3.1 3.3

Net income (21.6) 4.8 14.7 15.1 14.3 12.5 11.6 10.7 10.3 10.7

Growth Analysis

Revenue 7.5% 62.7% 11.0% 6.0% 10.1% 6.0% 6.0% 6.0% 6.0% 6.0%

Gross Profit (32.2%) 62.4% 24.4% 9.7% 10.9% 5.1% 4.0% 4.0% 3.9% 3.9%

EBIT (219.9%) 146.4% 166.6% 9.2% 10.1% 4.8% 10.3% 7.3% 3.1% 1.6%

EBITDA (169.0%) 199.9% 109.0% 7.5% 9.6% 5.1% 9.6% 7.1% 3.7% 2.4%

Net Income (292.9%) 122.2% 207.7% 2.3% (3.1%) (12.5%) (7.1%) (7.6%) (4.1%) 3.9%

Margin Analysis

Gross Profit 23.7% 23.6% 26.5% 27.4% 26.7% 26.4% 25.9% 25.4% 24.9% 24.4%

EBIT (13.2%) 3.8% 9.0% 9.3% 9.0% 8.9% 9.3% 9.4% 9.2% 8.8%

EBITDA (9.6%) 5.9% 11.1% 11.2% 11.0% 10.9% 11.3% 11.4% 11.2% 10.8%

Net Income (14.9%) 2.0% 5.6% 5.4% 5.0% 4.1% 3.6% 3.1% 2.8% 2.8%

Source: Company filings and MELODY management projections (1) MELODY LTM results as of September 30, 2011

14

Confidential MELODY Situation Overview

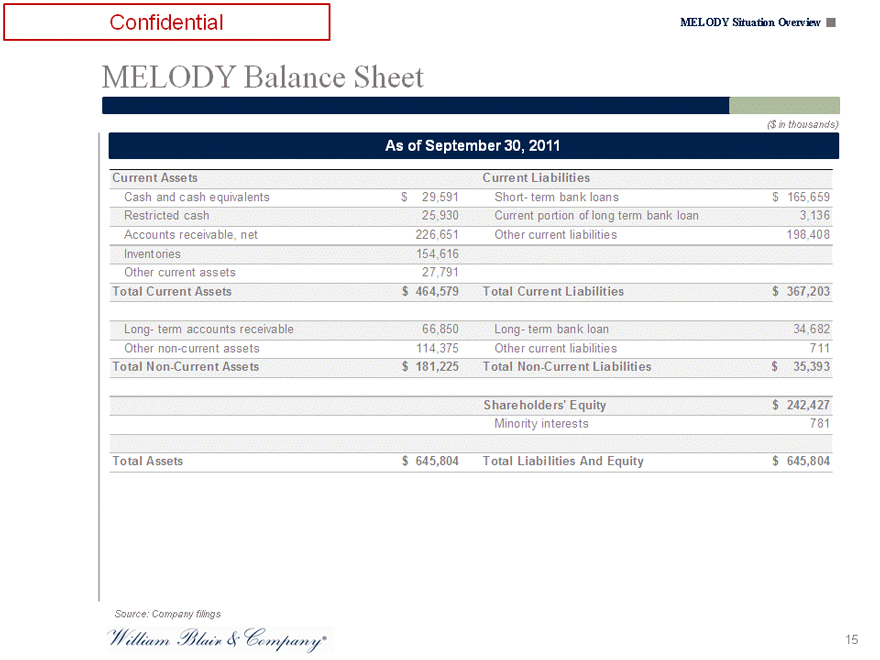

MELODY Balance Sheet

($ in thousands)

As of September 30, 2011

Current Assets Current Liabilities

Cash and cash equivalents $ 29,591 Short- term bank loans $ 165,659

Restricted cash 25,930 Current portion of long term bank loan 3,136

Accounts receivable, net 226,651 Other current liabilities 198,408

Inventories 154,616

Other current assets 27,791

Total Current Assets $ 464,579 Total Current Liabilities $ 367,203

Long- term accounts receivable 66,850 Long- term bank loan 34,682

Other non-current assets 114,375 Other current liabilities 711

Total Non-Current Assets $ 181,225 Total Non-Current Liabilities $ 35,393

Shareholders’ Equity $ 242,427

Minority interests 781

Total Assets $ 645,804 Total Liabilities And Equity $ 645,804

Source: Company filings

15

Confidential

Valuation Analysis

Confidential

Summary of Transaction

Confidential Summary of Transaction

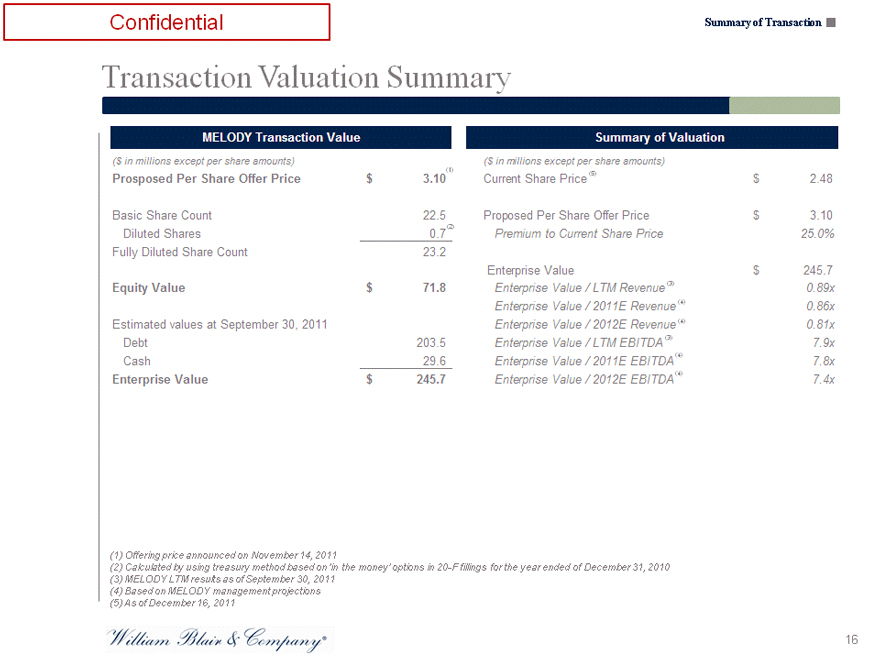

Transaction Valuation Summary

MELODY Transaction Value

($ in millions except per share amounts)

Prosposed Per Share Offer Price $ 3.10(1)

Basic Share Count 22.5

Diluted Shares 0.7 (2)

Fully Diluted Share Count 23.2

Equity Value $ 71.8

Estimated values at September 30, 2011

Debt 203.5

Cash 29.6

Enterprise Value $ 245.7

Summary of Valuation

($ in millions except per share amounts)

Current Share Price (5) $ 2.48

Proposed Per Share Offer Price $ 3.10

Premium to Current Share Price 25.0%

Enterprise Value $ 245.7

Enterprise Value / LTM Revenue (3) 0.89x

Enterprise Value / 2011E Revenue (4) 0.86x

Enterprise Value / 2012E Revenue (4) 0.81x

Enterprise Value / LTM EBITDA (3) 7.9x

Enterprise Value / 2011E EBITDA (4) 7.8x

Enterprise Value / 2012E EBITDA (4) 7.4x

(1) Offering price announced on November 14, 2011

(2) Calculated by using treasury method based on ‘in the money’ options in 20-F fillings for the year ended of December 31, 2010

(3) MELODY LTM results as of September 30, 2011 (4) Based on MELODY management projections (5) As of December 16, 2011

16

Confidential

Selected Public Companies Analysis

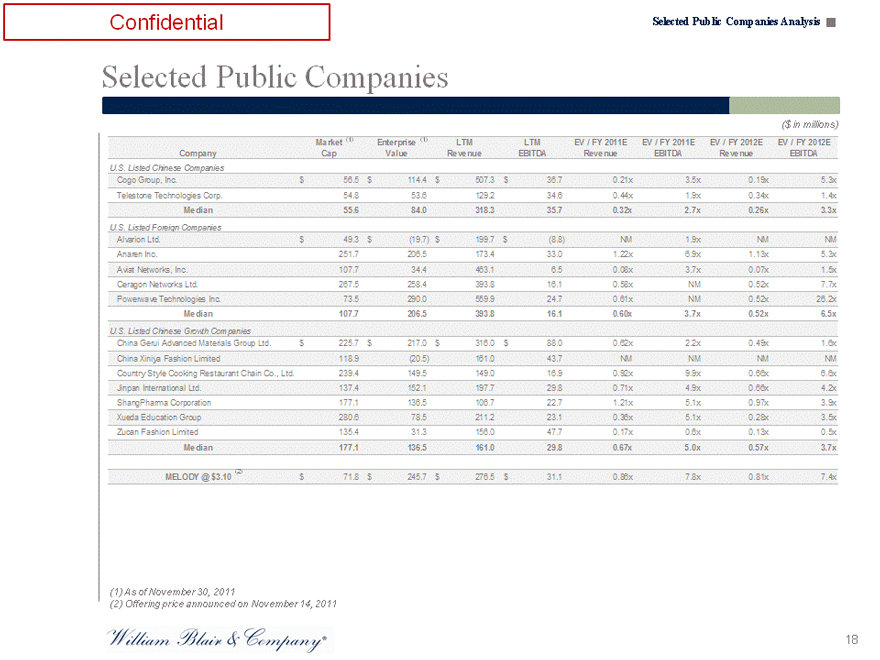

Confidential Selected Public Companies Analysis

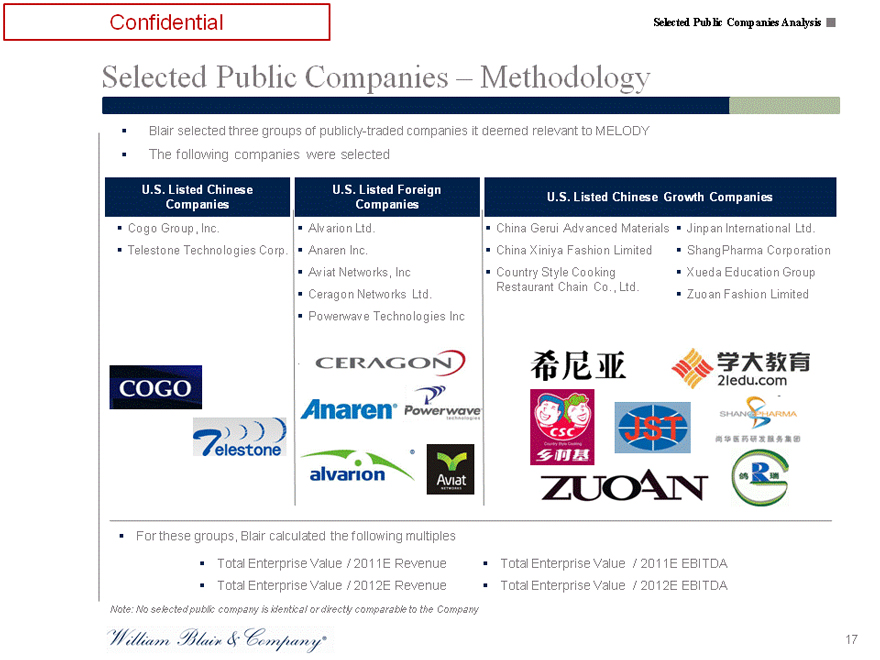

Selected Public Companies – Methodology

Blair selected three groups of publicly-traded companies it deemed relevant to MELODY The following companies were selected

U.S. Listed Chinese U.S. Listed Foreign U.S. Listed Chinese Growth Companies

Companies Companies

Cogo Group, Inc. Alvarion Ltd. China Gerui Advanced Materials Jinpan International Ltd.

Telestone Technologies Corp. Anaren Inc. China Xiniya Fashion Limited ShangPharma Corporation

Aviat Networks, Inc Country Style Cooking Xueda Education Group

Restaurant Chain Co., Ltd.

Ceragon Networks Ltd. Zuoan Fashion Limited

Powerwave Technologies Inc

.

For these groups, Blair calculated the following multiples

Total Enterprise Value / 2011E Revenue Total Enterprise Value / 2011E EBITDA

Total Enterprise Value / 2012E Revenue Total Enterprise Value / 2012E EBITDA

Note: No selected public company is identical or directly comparable to the Company

17

Confidential Selected Public Companies Analysis

Selected Public Companies

($ in millions)

Market (1) Enterprise (1) LTM LTM EV / FY 2011E EV / FY 2011E EV / FY 2012E EV / FY 2012E

Company Cap Value Revenue EBITDA Revenue EBITDA Revenue EBITDA

U.S. Listed Chinese Companies

Cogo Group, Inc. $ 56.5 $ 114.4 $ 507.3 $ 36.7 0.21x 3.5x 0.19x 5.3x

Telestone Technologies Corp. 54.8 53.6 129.2 34.6 0.44x 1.9x 0.34x 1.4x

Median 55.6 84.0 318.3 35.7 0.32x 2.7x 0.26x 3.3x

U.S. Listed Foreign Companies

Alvarion Ltd. $ 49.3 $ (19.7) $ 199.7 $ (8.8) NM 1.9x NM NM

Anaren Inc. 251.7 206.5 173.4 33.0 1.22x 6.9x 1.13x 5.3x

Aviat Networks, Inc. 107.7 34.4 463.1 6.5 0.08x 3.7x 0.07x 1.5x

Ceragon Networks Ltd. 267.5 258.4 393.8 16.1 0.58x NM 0.52x 7.7x

Powerwave Technologies Inc. 73.5 290.0 559.9 24.7 0.61x NM 0.52x 26.2x

Median 107.7 206.5 393.8 16.1 0.60x 3.7x 0.52x 6.5x

U.S. Listed Chinese Growth Companies

China Gerui Advanced Materials Group Ltd. $ 225.7 $ 217.0 $ 316.0 $ 88.0 0.62x 2.2x 0.49x 1.6x

China Xiniya Fashion Limited 118.9 (20.5) 161.0 43.7 NM NM NM NM

Country Style Cooking Restaurant Chain Co., Ltd. 239.4 149.5 149.0 16.9 0.92x 9.9x 0.66x 6.6x

Jinpan International Ltd. 137.4 152.1 197.7 29.8 0.71x 4.9x 0.66x 4.2x

ShangPharma Corporation 177.1 136.5 106.7 22.7 1.21x 5.1x 0.97x 3.9x

Xueda Education Group 280.6 78.5 211.2 23.1 0.36x 5.1x 0.28x 3.5x

Zuoan Fashion Limited 135.4 31.3 156.0 47.7 0.17x 0.6x 0.13x 0.5x

Median 177.1 136.5 161.0 29.8 0.67x 5.0x 0.57x 3.7x

MELODY @ $3.10 (2) $ 71.8 $ 245.7 $ 276.5 $ 31.1 0.86x 7.8x 0.81x 7.4x

(1) | | As of November 30, 2011 |

(2) | | Offering price announced on November 14, 2011 |

18

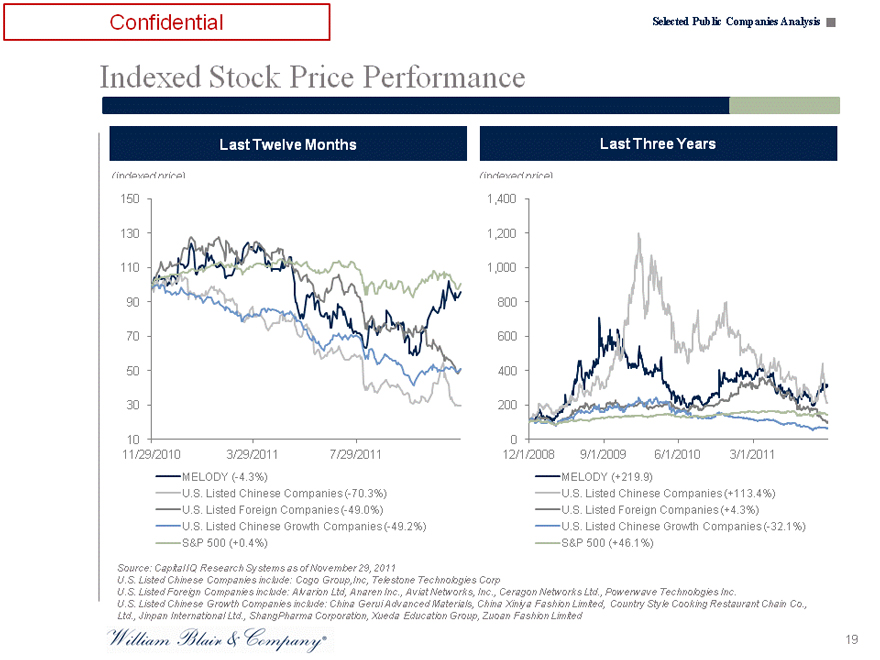

Confidential Selected Public Companies Analysis

Indexed Stock Price Performance

Last Twelve Months

(indexed price)

150

130

110

90

70

50

30

10

11/29/2010 3/29/2011 7/29/2011

MELODY (-4.3%)

U.S. Listed Chinese Companies (-70.3%)

U.S. Listed Foreign Companies (-49.0%)

U.S. Listed Chinese Growth Companies (-49.2%) S&P 500 (+0.4%)

Last Three Years

(indexed price)

1,400

1,200

1,000

800

600

400

200

0

12/1/2008 9/1/2009 6/1/2010 3/1/2011

MELODY (+219.9)

U.S. Listed Chinese Companies (+113.4%)

U.S. Listed Foreign Companies (+4.3%)

U.S. Listed Chinese Growth Companies (-32.1%) S&P 500 (+46.1%)

Source: Capital IQ Research Systems as of November 29, 2011

U.S. Listed Chinese Companies include: Cogo Group,Inc, Telestone Technologies Corp

U.S. Listed Foreign Companies include: Alvarion Ltd, Anaren Inc., Aviat Networks, Inc., Ceragon Networks Ltd., Powerwave Technologies Inc.

U.S. Listed Chinese Growth Companies include: China Gerui Advanced Materials, China Xiniya Fashion Limited, Country Style Cooking Restaurant Chain Co., Ltd., Jinpan International Ltd., ShangPharma Corporation, Xueda Education Group, Zuoan Fashion Limited

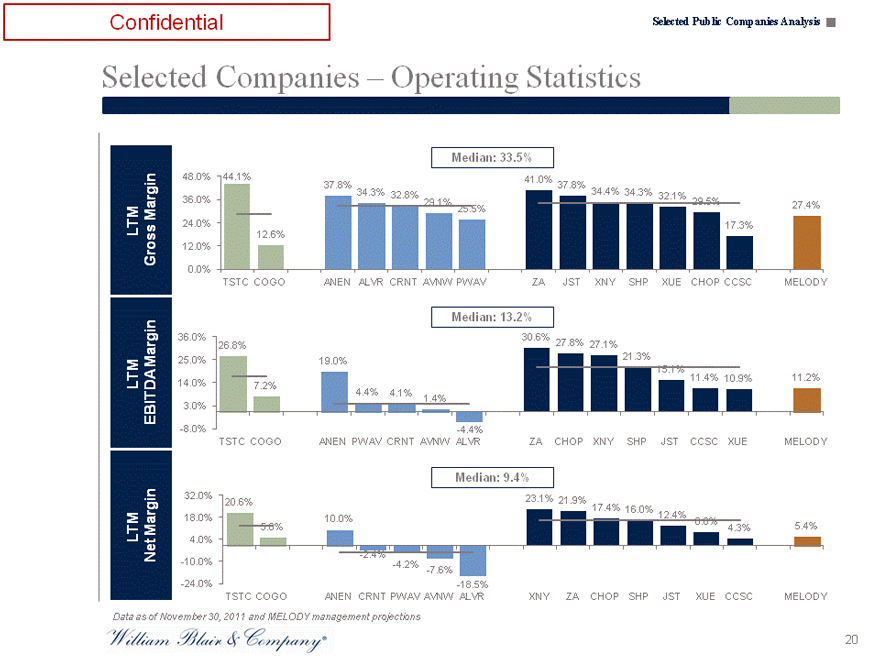

Confidential Selected Public Companies Analysis

Selected Companies – Operating Statistics

Median: 33.5%

LTM Gross Margin

48.0% 44.1% 41.0%

37.8% 37.8%

34.3% 32.8% 34.4% 34.3% 32.1%

36.0% 29.1% 29.5% 27.4%

25.5%

24.0% 17.3%

12.6%

12.0%

0.0%

TSTC COGO ANEN ALVR CRNT AVNW PWAV ZA JST XNY SHP XUE CHOP CCSC MELODY

Median: 13.2%

LTM EBITDA Margin

36.0% 30.6%

26.8% 27.8% 27.1%

25.0% 19.0% 21.3%

15.1% 11.4% 10.9% 11.2%

14.0% 7.2%

4.4% 4.1% 1.4%

3.0%

-8.0% -4.4%

TSTC COGO ANEN PWAV CRNT AVNW ALVR ZA CHOP XNY SHP JST CCSC XUE MELODY

Median: 9.4%

LTM Net Margin

32.0% 20.6% 23.1% 21.9%

17.4% 16.0% 12.4%

18.0% 10.0% 8.8%

5.0% 4.3% 5.4%

4.0%

-2.4%

-10.0% -4.2% -7.6%

-24.0% -18.5%

TSTC COGO ANEN CRNT PWAV AVNW ALVR XNY ZA CHOP SHP JST XUE CCSC MELODY

Data as of November 30, 2011 and MELODY management projections

20

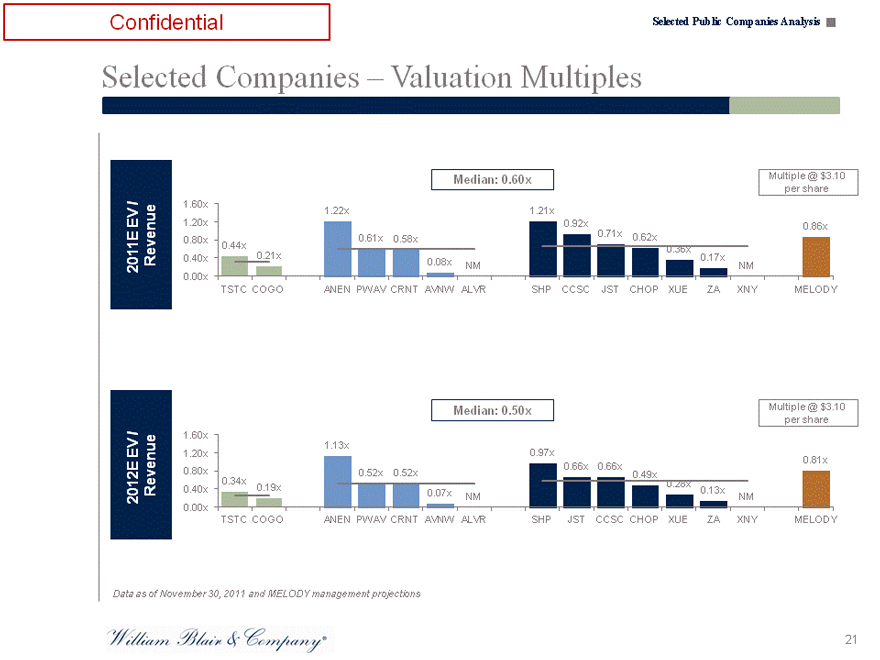

Confidential Selected Public Companies Analysis

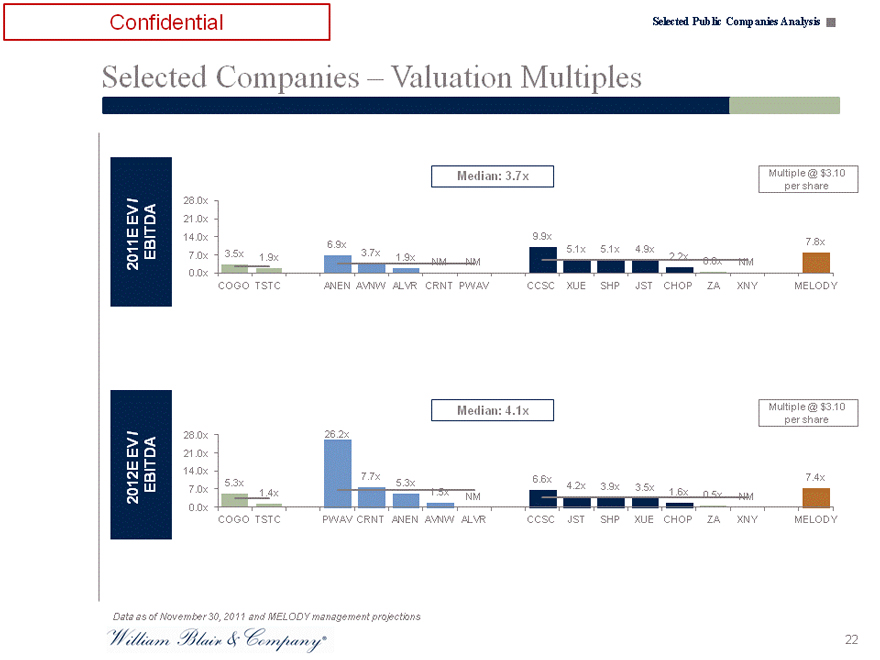

Selected Companies – Valuation Multiples

2011E EV / Revenue

2012E EV / Revenue

Median: 0.60x

Multiple @ $3.10 per share

1.60x 1.20x 0.80x 0.40x 0.00x

0.44x 0.21x

1.22x

0.61x 0.58x

0.08x NM

1.21x

0.92x 0.71x

0.62x

0.36x

0.17x NM

0.86x

TSTC COGO ANEN PWAV CRNT AVNW ALVR SHP CCSC JST CHOP XUE ZA XNY MELODY

Median: 0.50x

Multiple @ $3.10 per share

1.60x 1.20x 0.80x 0.40x 0.00x

0.34x 0.19x

1.13x

0.52x 0.52x

0.07x NM

0.97x

0.66x 0.66x

0.49x 0.28x

0.13x NM

0.81x

TSTC COGO ANEN PWAV CRNT AVNW ALVR SHP JST CCSC CHOP XUE ZA XNY MELODY

Data as of November 30, 2011 and MELODY management projections

21

Confidential Selected Public Companies Analysis

Selected Companies – Valuation Multiples

2011E EV / EBITDA

2012E EV / EBITDA

Median: 3.7x

Multiple @ $3.10 per share

28.0x 21.0x 14.0x 7.0x 0.0x

6.9x

3.5x 1.9x 3.7x 1.9x NM NM

9.9x

5.1x 5.1x 4.9x

2.2x 0.6x NM

7.8x

COGO TSTC ANEN AVNW ALVR CRNT PWAV CCSC XUE SHP JST CHOP ZA XNY MELODY

Median: 4.1x

Multiple @ $3.10 per share

28.0x 21.0x 14.0x 7.0x 0.0x

5.3x 1.4x

26.2x

7.7x

5.3x 1.5x NM

6.6x

4.2x 3.9x 3.5x

1.6x 0.5x NM

7.4x

COGO TSTC PWAV CRNT ANEN AVNW ALVR CCSC JST SHP XUE CHOP ZA XNY MELODY

Data as of November 30, 2011 and MELODY management projections

22

Confidential Selected Public Companies Analysis

Summary – Selected Public Companies

Public Company Metrics

Enterprise Value / Revenue Median Mean Minimum Maximum Transaction (1)

FY 2011E 0.60x 0.59x 0.08x 1.22x 0.86x

FY 2012E 0.50x 0.50x 0.07x 1.13x 0.81x

Enterprise Value / EBITDA Median Mean Minimum Maximum Transaction

FY 2011E 3.7x 4.1x 0.6x 9.9x 7.8x

FY 2012E 4.1x 5.6x 0.5x 26.2x 7.4x

(1) | | Based on MELODY management projections |

23

Confidential

Selected M&A Transactions Analysis

Confidential Selected M&A Transactions Analysis

Summary – Selected M&A Transactions

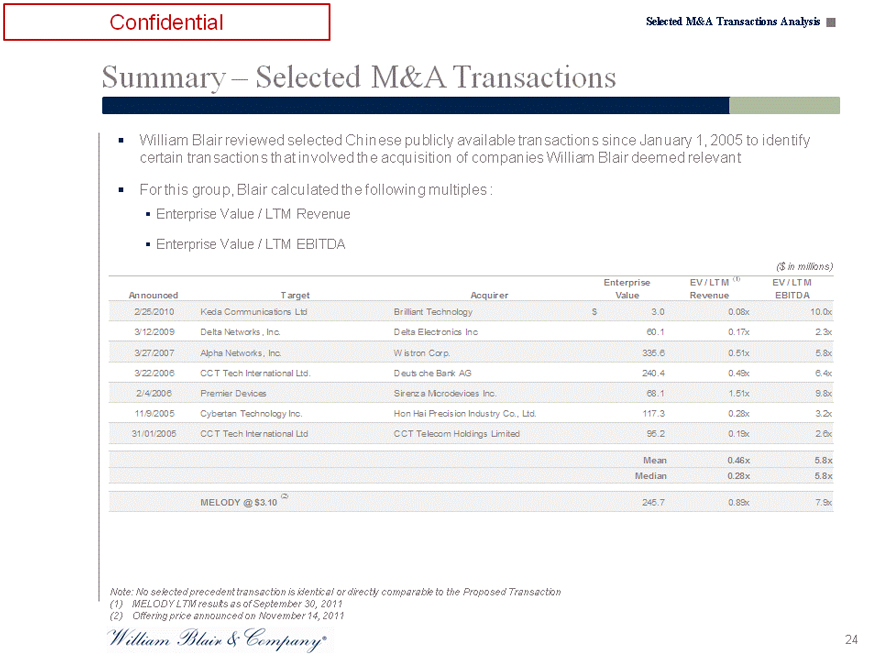

William Blair reviewed selected Chinese publicly available transactions since January 1, 2005 to identify certain transactions that involved the acquisition of companies William Blair deemed relevant

For this group, Blair calculated the following multiples : Enterprise Value / LTM Revenue

Enterprise Value / LTM EBITDA

($ in millions)

Enterprise EV / LTM (1) EV / LTM

Announced Target Acquirer Value Revenue EBITDA

2/25/2010 Keda Communications Ltd Brilliant Technology $ 3.0 0.08x 10.0x

3/12/2009 Delta Networks, Inc. Delta Electronics Inc 60.1 0.17x 2.3x

3/27/2007 Alpha Networks, Inc. Wistron Corp. 335.6 0.51x 5.8x

3/22/2006 CCT Tech International Ltd. Deutsche Bank AG 240.4 0.49x 6.4x

2/4/2006 Premier Devices Sirenza Microdevices Inc. 68.1 1.51x 9.8x

11/9/2005 Cybertan Technology Inc. Hon Hai Precision Industry Co., Ltd. 117.3 0.28x 3.2x

31/01/2005 CCT Tech International Ltd CCT Telecom Holdings Limited 95.2 0.19x 2.6x

Mean 0.46x 5.8x

Median 0.28x 5.8x

MELODY @ $3.10 (2) 245.7 0.89x 7.9x

Note: No selected precedent transaction is identical or directly comparable to the Proposed Transaction (1) MELODY LTM results as of September 30, 2011 (2) Offering price announced on November 14, 2011

24

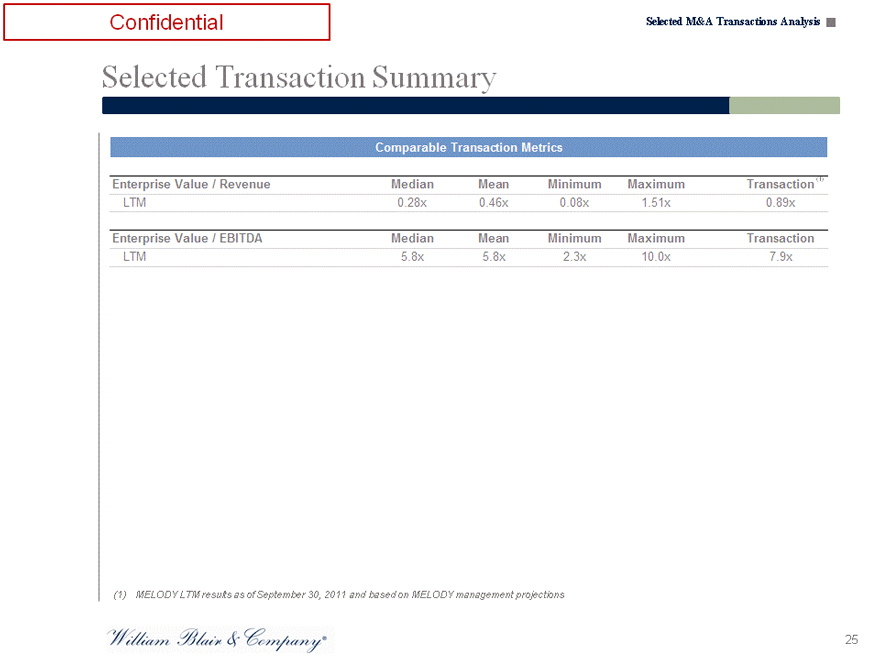

Confidential Selected M&A Transactions Analysis

Selected Transaction Summary

Comparable Transaction Metrics

Enterprise Value / Revenue Median Mean Minimum Maximum Transaction (1)

LTM 0.28x 0.46x 0.08x 1.51x 0.89x

Enterprise Value / EBITDA Median Mean Minimum Maximum Transaction

LTM 5.8x 5.8x 2.3x 10.0x 7.9x

(1) MELODY LTM results as of September 30, 2011 and based on MELODY management projections

25

Confidential

Discounted Cash Flow Analysis

Confidential Discounted Cash Flow Analysis

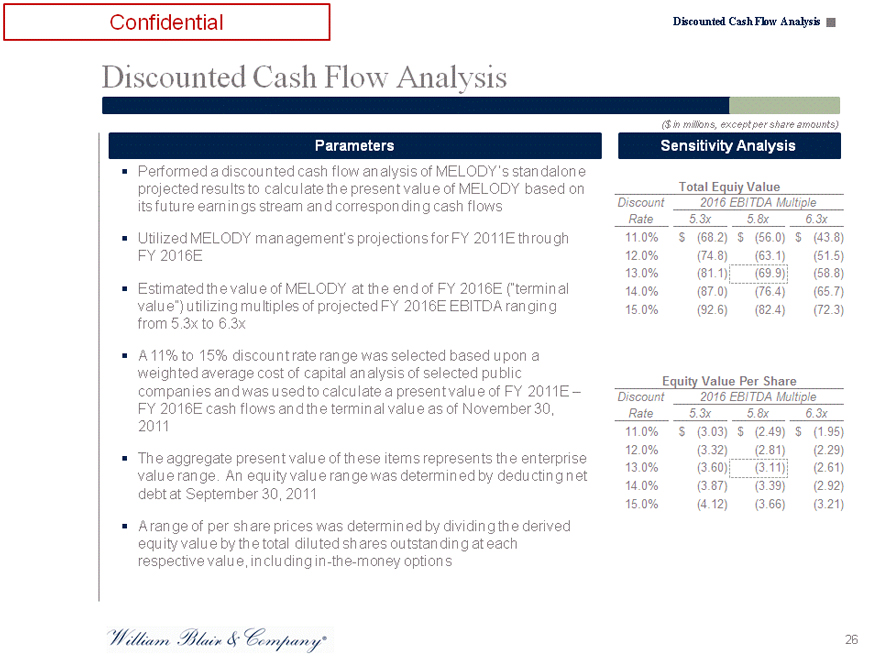

Discounted Cash Flow Analysis

Parameters

Performed a discounted cash flow analysis of MELODY’s standalone projected results to calculate the present value of MELODY based on its future earnings stream and corresponding cash flows

Utilized MELODY management’s projections for FY 2011E through FY 2016E

Estimated the value of MELODY at the end of FY 2016E (“terminal value”) utilizing multiples of projected FY 2016E EBITDA ranging from 5.3x to 6.3x

A 11% to 15% discount rate range was selected based upon a weighted average cost of capital analysis of selected public companies and was used to calculate a present value of FY 2011E –

FY 2016E cash flows and the terminal value as of November 30, 2011

The aggregate present value of these items represents the enterprise value range. An equity value range was determined by deducting net debt at September 30, 2011

A range of per share prices was determined by dividing the derived equity value by the total diluted shares outstanding at each respective value, including in-the-money options

($ in millions, except per share amounts)

Sensitivity Analysis

Total Equiy Value

Discount 2016 EBITDA Multiple

Rate 5.3x 5.8x 6.3x

11.0% $ (68.2) $ (56.0) $ (43.8)

12.0% (74.8) (63.1) (51.5)

13.0% (81.1) (69.9) (58.8)

14.0% (87.0) (76.4) (65.7)

15.0% (92.6) (82.4) (72.3)

Equity Value Per Share

Discount 2016 EBITDA Multiple

Rate 5.3x 5.8x 6.3x

11.0% $ (3.03) $ (2.49) $ (1.95)

12.0% (3.32) (2.81) (2.29)

13.0% (3.60) (3.11) (2.61)

14.0% (3.87) (3.39) (2.92)

15.0% (4.12) (3.66) (3.21)

26

Confidential

Leveraged Buyout Analysis

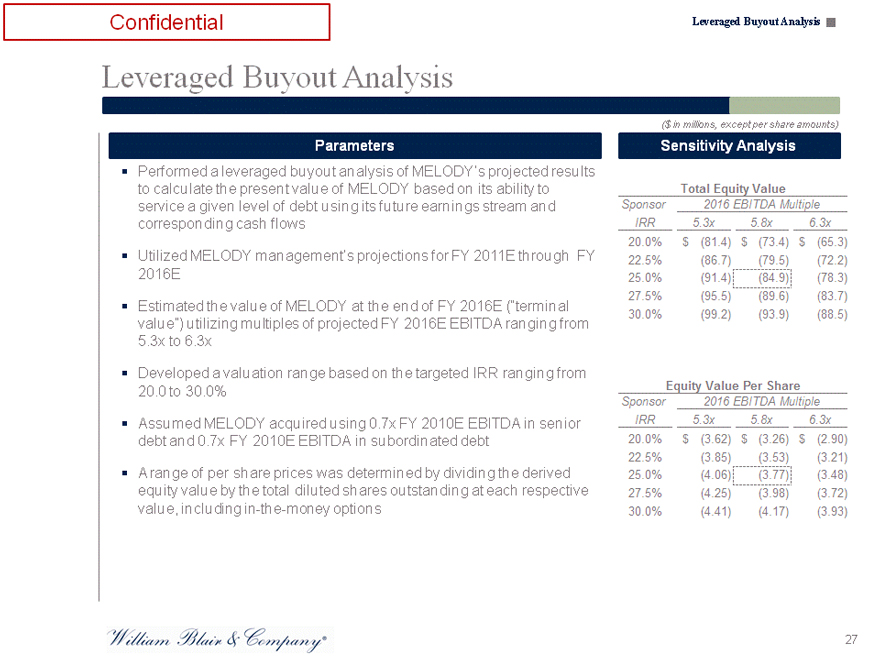

Confidential Leveraged Buyout Analysis

Leveraged Buyout Analysis

Parameters

Performed a leveraged buyout analysis of MELODY’s projected results to calculate the present value of MELODY based on its ability to service a given level of debt using its future earnings stream and corresponding cash flows

Utilized MELODY management’s projections for FY 2011E through FY 2016E

Estimated the value of MELODY at the end of FY 2016E (“terminal value”) utilizing multiples of projected FY 2016E EBITDA ranging from 5.3x to 6.3x

Developed a valuation range based on the targeted IRR ranging from 20.0 to 30.0%

Assumed MELODY acquired using 0.7x FY 2010E EBITDA in senior debt and 0.7x FY 2010E EBITDA in subordinated debt

A range of per share prices was determined by dividing the derived equity value by the total diluted shares outstanding at each respective value, including in-the-money options

($ in millions, except per share amounts)

Sensitivity Analysis

Total Equity Value

Sponsor 2016 EBITDA Multiple

IRR 5.3x 5.8x 6.3x

20.0% $ (81.4) $ (73.4) $ (65.3)

22.5% (86.7) (79.5) (72.2)

25.0% (91.4) (84.9) (78.3)

27.5% (95.5) (89.6) (83.7)

30.0% (99.2) (93.9) (88.5)

Equity Value Per Share

Sponsor 2016 EBITDA Multiple

IRR 5.3x 5.8x 6.3x

20.0% $ (3.62) $ (3.26) $ (2.90)

22.5% (3.85) (3.53) (3.21)

25.0% (4.06) (3.77) (3.48)

27.5% (4.25) (3.98) (3.72)

30.0% (4.41) (4.17) (3.93)

27

Confidential

Premiums Paid Analysis

Confidential Preliminary Paid Analysis

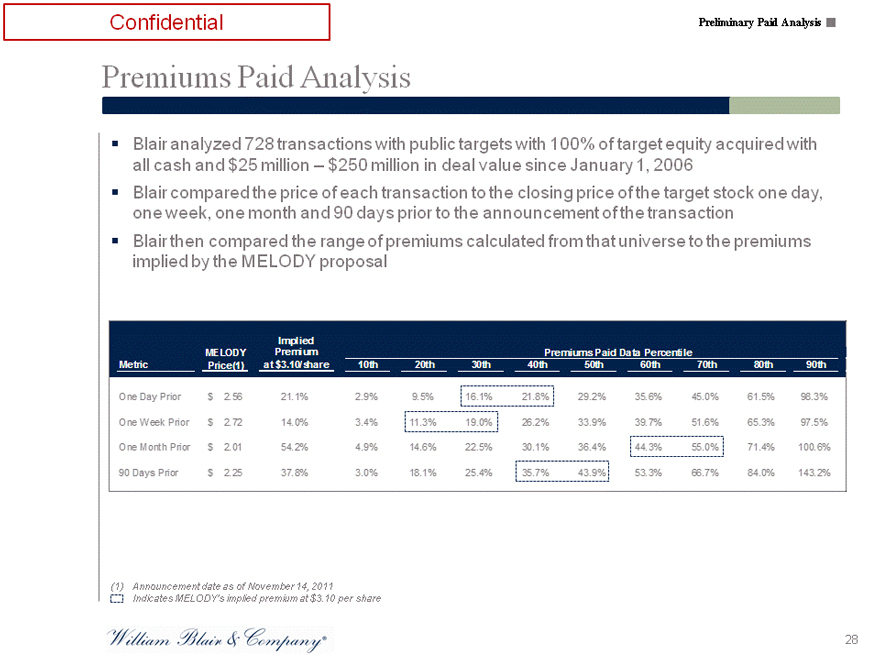

Premiums Paid Analysis

Blair analyzed 728 transactions with public targets with 100% of target equity acquired with all cash and $25 million – $250 million in deal value since January 1, 2006

Blair compared the price of each transaction to the closing price of the target stock one day, one week, one month and 90 days prior to the announcement of the transaction Blair then compared the range of premiums calculated from that universe to the premiums implied by the MELODY proposal

Implied

MELODY Premium Premiums Paid Data Percentile

Metric Price(1) at $3.10/share 10th 20th 30th 40th 50th 60th 70th 80th 90th

One Day Prior $ 2.56 21.1% 2.9% 9.5% 16.1% 21.8% 29.2% 35.6% 45.0% 61.5% 98.3%

One Week Prior $ 2.72 14.0% 3.4% 11.3% 19.0% 26.2% 33.9% 39.7% 51.6% 65.3% 97.5%

One Month Prior $ 2.01 54.2% 4.9% 14.6% 22.5% 30.1% 36.4% 44.3% 55.0% 71.4% 100.6%

90 Days Prior $ 2.25 37.8% 3.0% 18.1% 25.4% 35.7% 43.9% 53.3% 66.7% 84.0% 143.2%

(1) Announcement date as of November 14, 2011

Indicates MELODY’s implied premium at $3.10 per share

28

Confidential

Supporting Financial Schedules

Confidential Supporting Financial Schedules

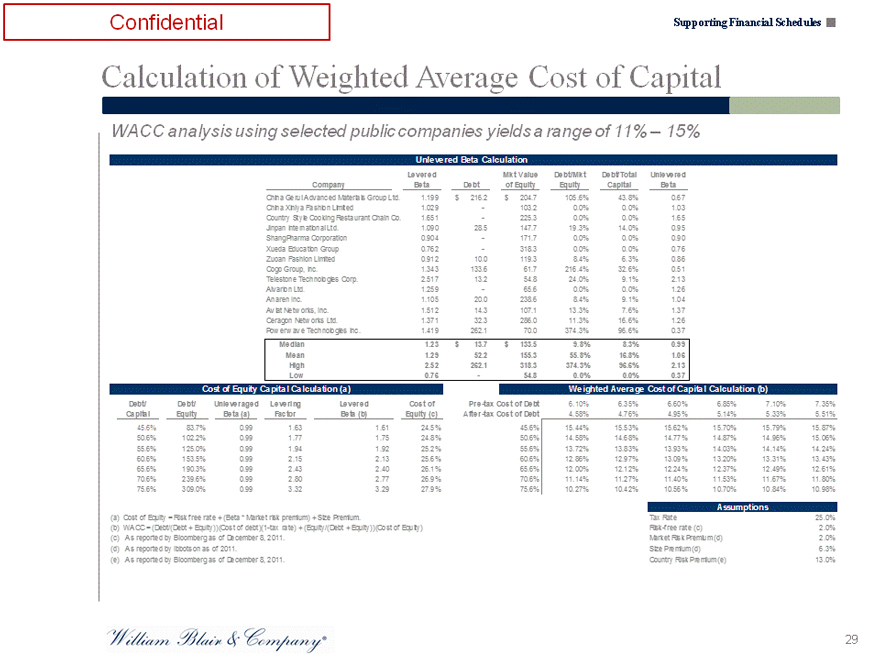

Calculation of Weighted Average Cost of Capital

WACC analysis using selected public companies yields a range of 11% – 15%

Unlevered Beta Calculation

Levered Mkt Value Debt/Mkt Debt/Total Unlevered

Company Beta Debt of Equity Equity Capital Beta

China Gerui Advanced Materials Group Ltd. 1.199 $ 216.2 $ 204.7 105.6% 43.8% 0.67

China Xiniya Fashion Limited 1.029 — 103.2 0.0% 0.0% 1.03

Country Style Cooking Restaurant Chain Co. 1.651 — 225.3 0.0% 0.0% 1.65

Jinpan International Ltd. 1.090 28.5 147.7 19.3% 14.0% 0.95

ShangPharma Corporation 0.904 — 171.7 0.0% 0.0% 0.90

Xueda Education Group 0.762 — 318.3 0.0% 0.0% 0.76

Zuoan Fashion Limited 0.912 10.0 119.3 8.4% 6.3% 0.86

Cogo Group, Inc. 1.343 133.6 61.7 216.4% 32.6% 0.51

Telestone Technologies Corp. 2.517 13.2 54.8 24.0% 9.1% 2.13

Alvarion Ltd. 1.259 — 65.6 0.0% 0.0% 1.26

Anaren Inc. 1.105 20.0 238.6 8.4% 9.1% 1.04

Aviat Netw orks, Inc. 1.512 14.3 107.1 13.3% 7.6% 1.37

Ceragon Netw orks Ltd. 1.371 32.3 286.0 11.3% 16.6% 1.26

Pow erw ave Technologies Inc. 1.419 262.1 70.0 374.3% 96.6% 0.37

Median 1.23 $ 13.7 $ 133.5 9.8% 8.3% 0.99

Mean 1.29 52.2 155.3 55.8% 16.8% 1.06

High 2.52 262.1 318.3 374.3% 96.6% 2.13

Low 0.76 — 54.8 0.0% 0.0% 0.37

Cost of Equity Capital Calculation (a)

Debt/ Debt/ Unleveraged Levering Levered Cost of

Capital Equity Beta (a) Factor Beta (b) Equity (c)

45.6% 83.7% 0.99 1.63 1.61 24.5%

50.6% 102.2% 0.99 1.77 1.75 24.8%

55.6% 125.0% 0.99 1.94 1.92 25.2%

60.6% 153.5% 0.99 2.15 2.13 25.6%

65.6% 190.3% 0.99 2.43 2.40 26.1%

70.6% 239.6% 0.99 2.80 2.77 26.9%

75.6% 309.0% 0.99 3.32 3.29 27.9%

Weighted Average Cost of Capital Calculation (b)

Pre-tax Cost of Debt 6.10% 6.35% 6.60% 6.85% 7.10% 7.35%

After-tax Cost of Debt 4.58% 4.76% 4.95% 5.14% 5.33% 5.51%

45.6% 15.44% 15.53% 15.62% 15.70% 15.79% 15.87%

50.6% 14.58% 14.68% 14.77% 14.87% 14.96% 15.06%

55.6% 13.72% 13.83% 13.93% 14.03% 14.14% 14.24%

60.6% 12.86% 12.97% 13.09% 13.20% 13.31% 13.43%

65.6% 12.00% 12.12% 12.24% 12.37% 12.49% 12.61%

70.6% 11.14% 11.27% 11.40% 11.53% 11.67% 11.80%

75.6% 10.27% 10.42% 10.56% 10.70% 10.84% 10.98%

(a) Cost of Equity = Risk free rate + (Beta * Market risk premium) + Size Premium.

(b) WACC = (Debt/(Debt + Equity))(Cost of debt)(1-tax rate) + (Equity/(Debt + Equity))(Cost of Equity)

(c) As reported by Bloomberg as of December 8, 2011.

(d) As reported by Ibbotson as of 2011.

(e) As reported by Bloomberg as of December 8, 2011.

Assumptions

Tax Rate 25.0%

Risk-free rate (c) 2.0%

Market Risk Premium (d) 2.0%

Size Premium (d) 6.3%

Country Risk Premium (e) 13.0%

29