UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): October 15, 2021 (October 12, 2021)

Appgate, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | | 000-52776 | | 20-3547231 |

(State or other jurisdiction

of incorporation) | | (Commission File Number) | | (I.R.S. Employer

Identification) |

2333 Ponce De Leon Blvd., Suite 900, Coral Gables, FL 33134

(Address of principal executive offices) (Zip Code)

(866) 524-4782

(Registrant’s Telephone Number, Including Area Code)

Newtown Lane Marketing, Incorporated

c/o Graubard Miller

405 Lexington Avenue, 11th Floor

New York, New York 10174

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

| ☐ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☐ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a -12) |

| ☐ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d -2(b)) |

| ☐ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e -4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| N/A | | N/A | | N/A |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

INTRODUCTORY NOTE

Unless the context otherwise requires, “we,” “us,” “our,” “Appgate” and the “Company” refer to Appgate, Inc., a Delaware corporation (f/k/a Newtown Lane Marketing, Incorporated), and its consolidated subsidiaries following the Closing (as defined below). Unless the context otherwise requires, references to “Newtown Lane” refer to Newtown Lane Marketing, Incorporated prior to the Closing. All references herein to the “Board” refer to the board of directors of the Company.

This Current Report on Form 8-K (this “Report”) is being filed by the Company in connection with the completion of the transactions contemplated by that certain agreement and plan of reorganization, dated February 8, 2021 (the “Merger Agreement”), entered into by and among Newtown Lane, Newtown Merger Sub. Corp., a Delaware corporation and wholly owned subsidiary of Newtown Lane (“Merger Sub”), and Cyxtera Cybersecurity, Inc. (d/b/a AppGate), a Delaware corporation (“Legacy Appgate”). Pursuant to the Merger Agreement, Merger Sub was merged with and into Legacy Appgate (the “Merger”), with Legacy Appgate surviving the Merger and becoming a wholly-owned subsidiary of the Company. The Merger was consummated on October 12, 2021 (the “Closing” and such date the “Closing Date”).

In connection with the Closing, we experienced a change of control (the “Change of Control”), as:

| ● | SIS Holdings LP (“SIS Holdings”), the sole stockholder of Legacy Appgate immediately prior to the Closing, received an aggregate of 117,149,920 shares of the Company’s common stock, par value $0.001 per share (the “Common Stock”), which resulted in SIS Holdings owning an aggregate of approximately 89% of the Company’s issued and outstanding Common Stock as of the date of this Report; |

| ● | The size of the Board was increased to five and four new directors were elected (as further described in this Report); and |

| ● | Jonathan J. Ledecky resigned from his position as President of the Company and Manuel D. Medina became the Executive Chairman of the Company, Barry Field became the Chief Executive Officer of the Company, Jawahar Sivasankaran became the President and Chief Operating Officer of the Company, Rene A. Rodriguez became the Chief Financial Officer of the Company, and Jeremy M. Dale became the General Counsel and Secretary of the Company. |

As a result of the foregoing, the Change of Control occurred with respect to the Company’s stock ownership and management upon the Closing. Therefore, we have determined to treat the Merger as a reverse merger and recapitalization for accounting purposes, with Legacy Appgate as the acquirer for accounting purposes. As such, the financial information, including the operating and financial results and audited financial statements included in this Report will be that of Legacy Appgate rather than that of our Company prior to the completion of the transactions described herein.

Item 1.01 Entry into a Material Definitive Agreement.

As disclosed previously in Newtown Lane’s Current Report on Form 8-K as filed with the Securities and Exchange Commission (the “SEC”) on February 9, 2021 by Newtown Lane (the “Merger Agreement 8-K”), Newtown Lane entered into the Merger Agreement with Merger Sub and Legacy Appgate. The Merger, together with the other transactions contemplated by the Merger Agreement, are referred to herein as the “Transactions”.

The summary of the Merger Agreement is included in Item 1.01 of the Merger Agreement 8-K and is incorporated herein by reference. The summary of the Merger Agreement is qualified in its entirety by reference to the full text of the Merger Agreement, a copy of which is filed as Exhibit 2.1 to this Report, and incorporated herein by reference.

Pursuant to the terms and subject to the conditions set forth in the Merger Agreement, the Transactions were consummated on the Closing Date.

Item 2.01 of this Report discusses the consummation of the Transactions and the entry into of the agreements relating thereto and is incorporated herein by reference.

Support Agreements

Summaries of the support agreements entered into by Newtown Lane in connection with the execution of the Merger Agreement are included in Item 1.01 of the Merger Agreement 8-K and are incorporated herein by reference.

The summaries of the support agreements are qualified in their entirety by reference to the form of each support agreement, attached as Exhibits 10.2 and 10.3 to this Report, respectively, and incorporated herein by reference.

Merger Registration Rights Agreement

On October 12, 2021, in connection with, and as a condition to, the Closing, Newtown Lane entered into a registration rights agreement (the “Merger Registration Rights Agreement”) with SIS Holdings and Ironbound Partners Fund, LLC, the owner of the majority of the outstanding Common Stock of Newtown Lane prior to the Closing (“Ironbound”, and together with SIS Holdings, the “Holders”), and, solely with respect to Section 3.1 of the Merger Registration Rights Agreement, Medina Capital Fund II – SIS Holdco, LP. Pursuant to the Merger Registration Rights Agreement, the Holders have the right to require us to file one or more registration statements with the SEC for the sale of our Common Stock held by the Holders, subject to certain exceptions. The Company is obligated to use its commercially reasonable best efforts to have a resale “shelf” registration statement declared effective with the SEC by February 9, 2022 (or May 10, 2022 if the SEC notifies the Company that it will “review” the registration statement). The Company will also be required to facilitate “takedown” offerings from the shelf upon demand by the Holders, provided that (i) the Company is eligible to use Form S-3 and (ii) the offering (x) has an anticipated offering price, net of the underwriters’ discount, in excess of $50.0 million or (y) constitutes the total aggregate registrable securities then held by all the Holders. The Holders may also require the Company to file an S-1 or S-3 registration statement for any registrable securities not included in the aforementioned “shelf” registration statement, provided the offering (i) has an anticipated offering price, net of the underwriters’ discount, in excess of $50.0 million or (ii) constitutes the total aggregate registrable securities then held by all the Holders. All holders of registrable securities party to the Merger Registration Rights Agreement are entitled to certain “piggyback” registration rights in subsequent offerings. Such holders are entitled to notice of a registered offering by the Company or by stockholders other than the Holders and to have their shares included on a pro rata basis. The Merger Registration Rights Agreement also provides that the Company will pay certain expenses of the Holders relating to the registrations and indemnify them against certain liabilities which may arise under the Securities Act and other federal or state securities laws.

The foregoing description of the Merger Registration Rights Agreement is qualified in its entirety by reference to the full text of the Merger Registration Rights Agreement, a copy of which is filed as Exhibit 10.1 to this Report, and incorporated herein by reference.

SIS Holdings and Ironbound Lock-up Agreement

On October 12, 2021, in connection with, and as a condition to, the Closing, SIS Holdings and Ironbound entered into a lock-up agreement with Newtown Lane (the “Lock-Up Agreement”), providing that the Company’s Common Stock held by such persons may not be transferred for a period of 12 months following the Closing, except to certain permitted transferees or pursuant to certain customary exceptions.

The foregoing description of the Lock-Up Agreement is qualified in its entirety by reference to the full text of the Lock-Up Agreement, a copy of which is filed as Exhibit 10.4 to this Report, and incorporated herein by reference.

Magnetar Convertible Senior Notes

Note Purchase Agreement

Concurrently with the execution of the Merger Agreement, Legacy Appgate entered into a note purchase agreement (the “Note Purchase Agreement”) with the lenders named on the Schedule of Lenders (as defined in the Note Purchase Agreement) attached thereto. Pursuant to the Note Purchase Agreement, Legacy Appgate agreed to sell, and the Initial Holders (as defined below) agreed to purchase, upon the terms and subject to the conditions contained in the Note Purchase Agreement, (i) $50.0 million aggregate principal amount of Legacy Appgate’s 5.00% Convertible Senior Notes due 2024 (the “Notes”) on the date of the initial closing (the “Initial Closing”), (ii) $25.0 million aggregate principal amount of Notes (the “Additional Notes”) on the Closing Date and (iii) at the election of Magnetar, up to $25.0 million additional Notes in one or more subsequent transactions, on or prior to February 8, 2022.

Under the terms of the Note Purchase Agreement, Magnetar shall have the right to fund up to 25% of certain issuances of indebtedness of Legacy Appgate or any of its subsidiaries that is either (i) convertible or exchangeable for capital stock of Legacy Appgate or any of its subsidiaries or (ii) issued with warrants or a similar equity component convertible or exchangeable for capital stock of Legacy Appgate or any of its subsidiaries. The Note Purchase Agreement also grants to Magnetar certain preemptive rights in respect to future issuances of equity of Legacy Appgate or any of its subsidiaries.

The Initial Closing and the issuance of $50.0 million aggregate principal amount of Notes in connection therewith took place on February 9, 2021. The Additional Notes (in an aggregate principal amount of $25.0 million) were issued on the Closing Date. The Notes and Additional Notes were issued under and are governed by the terms of the Note Issuance Agreement (as defined and described below).

The foregoing description of the Note Purchase Agreement is qualified in its entirety by reference to the full text of the Note Purchase Agreement, a copy of which is filed as Exhibit 10.5 to this Report, and incorporated herein by reference.

Note Issuance Agreement

Concurrently with the execution of the Merger Agreement, on the date of the Initial Closing, Legacy Appgate entered into a note issuance agreement (the “Note Issuance Agreement”) together with Legacy Appgate’s wholly-owned domestic subsidiaries (each, a “Guarantor”) and Magnetar Financial LLC (collectively, with its affiliates, “Magnetar”), as representative of the several initial holders named therein (“Initial Holders”). The terms of the Note Issuance Agreement and the Notes are summarized below; capitalized terms used in this section but not otherwise defined herein shall have the respective definitions ascribed to them in the Note Issuance Agreement:

Interest and Maturity. The Notes bear interest at 5.00% per annum if paid in cash and 5.50% per annum if paid in kind, payable, at the election of Legacy Appgate, entirely in cash, entirely in kind or a combination of in cash and in kind, which interest accrues from February 9, 2021, and will be payable semiannually in arrears on February 1 and August 1 of each year, beginning on August 1, 2021. The Notes will mature on February 9, 2024 unless earlier redeemed or repurchased.

Conversion upon Change of Control. If Legacy Appgate undergoes a Change of Control other than the Merger prior to maturity, each holder of Notes shall have the option to convert all or any portion of such Notes into Legacy Appgate common stock or, following entry into the Supplemental Agreement (as defined below), our Common Stock, subject to and in accordance with the terms of the Note Issuance Agreement, including the applicable conversion rate thereunder.

Conversion. Other than upon a Change of Control, prior to maturity, each holder of Notes shall have the option to convert all or any portion of such Notes into Legacy Appgate common stock or, following entry into the Supplemental Agreement, our Common Stock, subject to and in accordance with the terms of the Note Issuance Agreement, including the applicable conversion rate thereunder.

Guarantees; Conversion Obligations. The Notes are guaranteed by each of Legacy Appgate’s wholly-owned domestic subsidiaries. Upon the consummation of certain events resulting in Legacy Appgate becoming a direct or indirect subsidiary of any person (including the Merger), such acquiring person, any direct or indirect parent company thereof and each subsidiary thereof (immediately prior to such event) shall unconditionally guarantee Legacy Appgate’s Obligations and assume all of Appgate’s Conversion Obligations and Change of Control Conversion Obligations and, upon such assumption, Legacy Appgate shall be released from its Conversion Obligations and Change of Control Conversion Obligations.

Repurchase Upon a Fundamental Change. Upon the occurrence of a Fundamental Change at any time after a Public Company Event, each holder of Notes shall have the option to require Legacy Appgate to repurchase for cash all or any portion of such Notes, at a repurchase price equal to 100% of the principal amount thereof, plus accrued and unpaid interest thereon, subject to and in accordance with the terms of the Note Issuance Agreement.

Repurchase Upon a Change of Control. Upon the occurrence of a Change of Control other than the Merger at any time before a Public Company Event, each holder of Notes shall have the option to require Legacy Appgate to repurchase for cash all or any portion of such Notes, at a repurchase price equal to 102% of the principal amount thereof, plus accrued and unpaid interest thereon, subject to and in accordance with the terms of the Note Issuance Agreement.

Covenants. The Note Issuance Agreement contains restrictive covenants that, among other things, generally limit the ability of Legacy Appgate and certain of its subsidiaries (subject to certain exceptions) to: (i) incur additional debt and issue Disqualified Stock; (ii) create liens; (iii) pay dividends, acquire shares of capital stock, or make investments; (iv) issue guarantees; (v) sell assets and (vi) enter into transactions with affiliates. The foregoing restrictive covenants are subject to a number of important exceptions and qualifications, as set forth in the Note Issuance Agreement.

Events of Default. The Note Issuance Agreement provides for customary events of default which include (subject in certain cases to customary grace and cure periods), among others: (i) nonpayment of principal or interest; (ii) breach of covenants or other agreements in the Note Issuance Agreement; (iii) defaults in failure to pay certain other indebtedness; and (iv) certain events of bankruptcy or insolvency. Generally, if an event of default occurs and is continuing under the Note Issuance Agreement, Magnetar or the holders of at least 25% in aggregate principal amount of the Note then outstanding may declare the principal of, premium, if any, and accrued interest on all the Notes immediately due and payable.

The foregoing description of the Note Issuance Agreement is qualified in its entirety by reference to the full text of the Note Issuance Agreement, a copy of which is filed as Exhibit 10.6 to this Report, and incorporated herein by reference.

Supplemental Agreement

On October 12, 2021, in connection with Closing, Newtown Lane entered into a supplemental agreement (the “Supplemental Agreement”) with Legacy Appgate and Magnetar, as representative of the holders of the Notes, pursuant to which Newtown Lane, among other things, unconditionally guaranteed all of Legacy Appgate’s Obligations, including the Notes, and assumed all of Legacy Appgate’s Conversion Obligations and Change of Control Conversion Obligations.

The foregoing description of the Supplemental Agreement is qualified in its entirety by reference to the full text of the Supplemental Agreement, a copy of which is filed as Exhibit 10.7 to this Report, and incorporated herein by reference.

Magnetar Registration Rights Agreement

Concurrently with the execution of the Merger Agreement, Legacy Appgate and the holders of Notes entered into a registration rights agreement (the “Magnetar Registration Rights Agreement”), pursuant to which, following a Public Company Event (as defined therein), Legacy Appgate would be obligated to file a registration statement to register the resale of certain securities of Legacy Appgate (including Legacy Appgate common stock, or, following entry into the Supplemental Agreement, our Common Stock, issued upon conversion of the Notes) held by such holders of Notes.

The Company has assumed these registration obligations pursuant to the Supplemental Agreement described above.

The foregoing description of the Magnetar Registration Rights Agreement is qualified in its entirety by reference to the full text of the Magnetar Registration Rights Agreement, a copy of which is filed as Exhibit 10.8 to this Report, and incorporated herein by reference.

Indemnification Agreements

On October 12, 2021, in connection with Closing, the Company entered into an indemnification agreement with each of the current directors and executive officers of the Company. Each indemnification agreement provides, among other things, for indemnification to the fullest extent permitted by applicable law and our A&R Charter (as defined herein) and A&R Bylaws (as defined herein) against any and all expenses, judgments, fines, penalties and amounts paid in settlement of any claim. The indemnification agreements provide for the advancement or payment of all expenses to the indemnitee and for the reimbursement to us if it is found that such indemnitee is not entitled to such indemnification under applicable law and our A&R Charter and A&R Bylaws.

The foregoing description of the indemnification agreements is qualified in its entirety by reference to the full text of the form of indemnification agreement between the Company and each of indemnitee, a copy of which is filed as Exhibit 10.9 to this Report, and incorporated herein by reference.

Item 2.01 Completion of Acquisition or Disposition of Assets.

The disclosure in Item 1.01 of this Report discusses the consummation of the Transactions and the entry into agreements relating thereto and is incorporated herein by reference.

FORM 10 INFORMATION

Item 2.01(f) of Form 8-K states that if the registrant was a shell company, as Newtown Lane was immediately before the Merger, then the registrant must disclose the information that would be required if the registrant were filing a general form for registration of securities on Form 10. Accordingly, the Company is providing below the information that would be included in a Form 10 if it were to file a Form 10. Please note that the information provided below relates to the Company after the consummation of the Merger, unless otherwise specifically indicated or the context otherwise requires.

Cautionary Note Regarding Forward-Looking Statements

This Report, including the documents incorporated by reference into this Report, contain forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and Section 27A of the Securities Act of 1933, as amended. Statements that do not relate strictly to historical or current facts are forward-looking and can be identified by the use of words such as “anticipate,” “estimate,” “could,” “would,” “should,” “will,” “may,” “forecast,” “approximate,” “expect,” “project,” “seek,” “predict,” “potential,” “intend,” “plan,” “believe,” and other words of similar meaning. Without limiting the generality of the foregoing, forward-looking statements contained in this Report include statements regarding the Company and its industry relating to matters such as anticipated future financial and operational performance, business prospects, the percentage of the Company’s future revenue derived from subscription term-based licenses compared to revenue from services, expected future increases in revenue and sales, including increasing the Company’s customer base, sales to existing customers, the U.S. federal government and through the Company’s channel partners, expected increases in gross profit and gross margin, the Company’s expected future net loss position, planned investments in sales and marketing and related increases in operating and general and administrative expenses and planned investments in research and development as a result of the Company’s expected growth, the expected future growth of the cybersecurity industry, including the growth in adoption of Zero Trust security solutions, the Company’s ability to innovate and add new functionality to existing products through research and development, the Company’s ability to fund working capital and capital expenditures for the next 12 months, potential future investments in the Company by Magnetar Financial, LLC under the Notes, the Company’s ability to remain in compliance with covenants under the Notes, the impact of foreign currency exchanges and inflation on the Company’s business, strategy and plans and similar matters.

The forward-looking statements included in this Report involve risks and uncertainties that could cause actual results to differ materially from projected results. Accordingly, investors should not place undue reliance on forward-looking statements as a prediction of actual results. The Company has based these forward-looking statements on current expectations and assumptions about future events, taking into account all information currently known by the Company. While the Company considers these expectations and assumptions to be reasonable, they are inherently subject to significant business, economic, competitive, regulatory and other risks and uncertainties, many of which are difficult to predict and beyond our control. These risks and uncertainties include, but are not limited to:

| ● | our future financial performance, including our expectations regarding our total revenue, cost of revenue, gross profit or gross margin, operating expenses, including changes in operating expenses and our ability to achieve and maintain future profitability; |

| ● | the effects of increased competition in our markets and our ability to compete effectively; |

| ● | market acceptance of our products and services and our ability to increase adoption of our products; |

| ● | our ability to maintain the security and availability of our products; |

| ● | our ability to develop new products, or enhancements to our existing products, and bring them to market in a timely manner; |

| ● | our ability to maintain and expand our customer base, including by attracting new customers; |

| ● | the potential impact on our business of the ongoing COVID-19 pandemic; |

| ● | our ability to maintain, protect and enhance our intellectual property rights; |

| ● | our ability to comply with laws and regulations that currently apply or become applicable to our business both in the United States and internationally; |

| ● | our ability to maintain an effective system of disclosure controls and internal control over financial reporting; |

| ● | SIS Holdings’ significant influence over our business and affairs; |

| ● | the future trading prices and liquidity of our Common Stock; |

| ● | our indebtedness, which may increase risk to our business; and |

| ● | other risks and uncertainties, including those described under the section below entitled “Risk Factors.” |

The forward-looking statements contained in this Report are based on the Company’s current expectations and beliefs concerning future developments and their potential effects on the Transactions and the Company. There can be no assurance that future developments affecting the Company will be those that the Company has anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond the Company’s control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the heading “Risk Factors” below. Should one or more of these risks or uncertainties materialize, or should any of the assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. The Company will not and does not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

Business

Mission Statement

Our mission is to empower and protect how people work and connect by enabling any user on any device to securely access any application, use any network, and perform any transaction.

Overview

Appgate is a cybersecurity company that protects against breaches and fraud through innovative, identity-centric, context-aware, Zero Trust1 solutions. Zero Trust is an approach to cybersecurity that shifts defenses from static, network-based perimeters to a dynamic security model based on users, assets, and resources. Appgate exists to provide modern organizations with a solution to the growing cyber crisis, against which their traditional cybersecurity tools are proving ineffective. The need for Appgate is growing as enterprise information technology (“IT”) changes with the adoption of new digital technologies, evolving IT architectures, and the increasing need to accommodate users’ preference to “work from anywhere.” While these changes are necessary for organizations to work efficiently and effectively, they introduce new security challenges. The corporate network is no longer consolidated and neatly protected behind a firewall, but rather has expanded into sprawling, distributed, hybrid environments, often with access to multiple clouds, that are more vulnerable to attacks. Adversaries have simultaneously grown stealthier, more sophisticated, and more determined, and have a track record of outmaneuvering legacy cybersecurity tools and wreaking havoc on organizations. Taken together, these changes have created a perfect storm which required a fundamentally different solution, Zero Trust, of which we have been a pioneer and recognized industry leader.

Appgate’s purpose-built solutions uniquely apply the principles of Zero Trust to protect organizations against growing cyber threats by applying the right access policies, and in the event of a security breach, limiting adversaries’ ability to cause widespread damage. Our solutions also reduce operational complexity by integrating with existing enterprise software and distinctively protecting users and networks across all IT infrastructure environments, whether cloud, hybrid, or on-premises, thus providing a ubiquitous, dynamic, user-centered foundation for organizations’ Zero Trust cybersecurity initiatives. Appgate enables businesses to meet both their immediate need to make their organizations resilient to adversaries without slowing down business, as well as their long-term need to develop a more modern, proactive cybersecurity approach essential for future success.

Appgate operated as a subsidiary of Cyxtera Technologies, Inc. (“Cyxtera”) until December 31, 2019, at which time Cyxtera spun out Appgate to become a standalone company. Appgate is headquartered in Coral Gables, Florida and had 423 full time employees across thirteen global offices as of June 30, 2021.

The Problem

Digital transformation, driven by growth in cloud computing, Software as a Service (“SaaS”), mobile devices, Internet of Things (“IoT”), and similar technologies, as well as increasing remote work, has changed the nature of cybersecurity risks by proliferating the number of entry points to organizations’ networks (often referred to as “increasing the attack surface”). Simultaneously, the number and sophistication of cyberattacks is ever-increasing. This combination of more vulnerable networks and more malicious activity has created a cybersecurity crisis, forever changing the threat landscape organizations face. According to Cybersecurity Ventures, cybersecurity breaches are expected to cause a record $6 trillion in aggregate damages in 2021 alone.

Traditional cybersecurity tools are not designed for today’s distributed, heterogeneous, and hybrid IT architectures. In large part, this is because traditional cybersecurity tools are perimeter-centric, or focused on the boundary between a private network and the public internet. This approach worked better historically when there were fewer entry points into an enterprise network. The perimeter-centric model is particularly problematic because it is built on a notion of implicit trust, which is the assumption that traffic initiated from within a network does not represent a risk. As a result, if there is a security breach, infiltrators can remain undetected, move laterally (i.e., after gaining initial access, progressively move through a network in search of sensitive and valuable data) across a network, and cause widespread damage.

Some of these traditional cybersecurity technologies have existed for well over two decades with little innovative change over that period of time. Many vendors of traditional cybersecurity tools have simply refreshed their product portfolios with better hardware, leaving the core security mechanism unchanged. For instance, virtual private network (“VPN”) technology has existed largely unchanged since the 1990s, and VPNs continue to be exploited regularly by adversaries.

These traditional security technologies are also often ineffective in newer cloud-based environments because they were not designed for the cloud and typically do not map well to cloud-based systems, causing friction and introducing security gaps. As organizations increasingly adopt cloud environments, security teams are facing a difficult choice – either mis-apply traditional security and networking tools to the cloud or introduce a new silo of cloud-only security and operational tools. Neither of these choices is secure or efficient.

| 1 | ZeroTrust enhances security by eliminating the implicit trust that is often granted based on physical or network location, instead requiring that all access be earned via dynamic attributes and strong authentication. Unlike traditional security models in which users are given overprivileged access and can easily move laterally within a network, Zero Trust only grants users access to resources that are needed to do their job at a particular time and place. Users are continuously monitored so that if their context or device changes, access can be revoked. This approach makes organizations much more resilient to attacks. |

Our Solution

Appgate’s software solutions and services, discussed in detail in the following paragraphs, use a fundamentally different identity-centric and context-aware approach grounded in the principles of Zero Trust to protect corporate users and consumers of online services. Zero Trust recognizes that the entire extended network is the attack surface, that no user, device, or application should be implicitly trusted, and that organizations must be resilient to attacks. We believe we have built the premiere pure-play Zero Trust platform capable of facilitating secure interactions between all devices, from all locations, in all IT environments.

Software:

Software Defined Perimeter (“SDP”) enables fast, secure connections for users and devices using the principles of Zero Trust. SDP offers comprehensive network security by segmenting resources and making them invisible to a user or device until trust is established. SDP uses adaptive and dynamic access policies based on user identity and device posture to continuously monitor users and limit lateral movement. This pioneering solution was the first SDP product to be Common Criteria Certified, which is the international “gold standard” for IT security. We believe that adoption of our SDP product is among the most pivotal steps an organization can take towards moving to a Zero Trust posture.

Risk Based Authentication (“RBA”) provides secure access between financial institutions and their customers to prevent transaction and financial fraud. RBA combines advanced authentication techniques and threat intelligence to authorize access and transactions. It allows for customizable and dynamic Zero Trust policy enforcement which enables seamless workflow processes.

Digital Threat Protection (“DTP”) offers digital threat visibility and comprehensive risk management to identify and eliminate attacks before they occur, across social media, phishing attacks, bogus websites, and malicious mobile apps. Its curated threat intelligence and continuous threat monitoring complements SDP and RBA to provide Zero Trust based protection throughout the threat lifecycle. It protects users against phishing attacks and account takeover attempts and provides business leaders with valuable reporting functionality.

Services:

Our Threat Advisory Services provide a dedicated, highly pedigreed team of consultants who provide breach and attack simulation in the form of customized vulnerability assessments and penetration testing, helping customers validate the effectiveness of their security infrastructure. In addition to providing a valuable service to our clients, their work allows us to stay at the cutting edge of cybersecurity threats and better understand the needs of our customers. This, in turn, provides us with feedback we can leverage to make our software products better. These advisory services also generate leads for our software solutions for organizations looking to achieve a Zero Trust posture.

We believe customers choose Appgate for the following six reasons:

| ● | Reduce network security risk: Appgate not only reduces the attack surface, which makes it harder for a hacker to penetrate, but it also limits an attacker’s ability to move laterally once in the network and applies continuous monitoring so that if a breach occurs, it is easier and faster to detect. |

| | | |

| ● | Integrate with their existing IT environments: We serve all IT environments, from legacy infrastructure to the cloud, and perform especially well against our competition in complex, hybrid environments that are pervasive in large enterprises and government agencies. |

| | | |

| ● | Improve the user’s experience: Our solutions provide a seamless and consistent user experience across all locations and devices, without the need for users to frequently re-authenticate themselves as they would using tools such as a VPN. Our solutions also make it easy for administrators to deploy and manage with a unified policy model active across all environments. |

| ● | Enhance existing security technologies: We have built a rich set of application programming interfaces (“APIs”) that integrate with organizations’ existing IT tools and allow us to extract useful context and, in turn, often extend the useful life of legacy systems by increasing their ability to defend against modern threats. |

| | | |

| ● | Prevent complex fraud: We offer a complete set of tools to prevent fraud for financial institutions and other consumer-facing organizations. Most attacks go through a multi-step process before causing significant damage to an organization. Appgate has solutions to address each phase, including planning and targeting, setup and launch and cashing out. Our solutions can be seamlessly tied together using risk orchestration, which allows customers to easily integrate protection layers based on risk tolerance and protect their consumers throughout the fraud attack lifecycle. |

| | | |

| ● | Proactively harden defenses: Understanding how threat actors operate enables us to proactively harden customer defenses. Our threat advisory services use advanced penetration testing, adversary simulation, and deep knowledge of evasion techniques to validate organizations’ defenses and uncover weaknesses before attackers do. |

We are a recognized market leader, given the quality of our offering and the strength of our vision. Examples of our industry recognition include the following:

| ● | Appgate was named a “Leader” in the Forrester New Wave™ for Zero Trust Network Access (Q3 2021). The report highlighted Appgate’s ability to address cloud, on-premises and hybrid IT models, noting that Appgate SDP "Is the best fit for companies that need high security and a self-hosted option. Appgate offers its Zero Trust Network Access (“ZTNA”) as a SaaS, but also as a self-hosted option for enterprises and agencies that need it." |

| | | |

| ● | Appgate was named a “Leader” in the Forrester Wave™ Zero Trust eXtended Ecosystem (Q3 2020). The report noted that Appgate already serves mega-enterprises and Department of Defense (“DoD”) customers, which is a testament to our capabilities and positions us well to benefit from the rising demand for Zero Trust solutions. |

| | | |

| ● | We were recognized by Forrester in their “New Tech: Zero Trust Network Access, 2021” report, where we were listed as a mature or “Late-Stage” vendor, indicating significant company tenure, number of customers, employees, and funding level as compared to our peers. |

| | | |

| ● | As of October 12, 2021, we have received 4.7 out of 5 stars from customer reviews on Gartner Peer Insights, with 95% of reviewers stating they would recommend Appgate to peers. |

| | | |

| ● | A 2021 Nemertes Research user survey rated Appgate a 9.5 out of 10 in its level of strategic importance to Zero Trust initiatives and further recognized Appgate SDP for “dramatically advancing strategic initiatives focused on implementing Zero Trust security, enabling digital transformation, supporting hybrid work-from-anywhere environments and improving employee satisfaction”. |

| | | |

| ● | Our Risk-Based Authentication solution was named a “Leader” in Quadrant Solutions’ SPARK Matrix™: Risk Based Authentication (RBA), 2021 report. |

| | | |

| ● | Appgate was 1 of 18 cybersecurity leaders selected from a list of hundreds of companies to participate in the National Institute of Standards and Technology (“NIST”) National Cybersecurity Center of Excellence, an initiative designed to provide guidance to organizations on how to implement Zero Trust architecture. |

| | | |

| ● | Our products and services serve some of the largest and most security-conscious organizations, including Fortune 10 enterprises, the US government, and many of the world’s largest financial institutions. We have authority to operate within the DoD, we’re certified for the Department of Homeland Security (“DHS”), and our Software Defined Perimeter (SDP) product is Common Criteria certified, indicating we meet the most stringent security requirements of government entities. |

| | | |

Currently, we serve over 600 organizations, including domestic and international government agencies and Fortune 500 enterprises that include at least one of the top-five largest companies in the defense contracting, telecommunications, and oil and gas sectors. We serve a global customer base across 40 countries. For the twelve months ending June 30, 2021, Appgate generated approximately $37 million of revenue and net losses of approximately $47 million. We expect losses to continue for the foreseeable future as we prioritize growth.

Industry Background

Cybersecurity attacks are increasing in severity and frequency as lateral movement, ransomware, and insecure remote access are pervasive.

Cyber threats are rising as adversaries are highly motivated and increasingly sophisticated in their approach. According to a report by Cybersecurity Ventures, breaches are expected to cost $6 trillion in damages in 2021, an aggregate cost greater than the GDP of any country in the world except the US and China. Cybersecurity Ventures predicts that in 2021, a ransomware attack will occur every 11 seconds, up nearly four times since 2016. One of the leading drivers behind the increasing costs of breaches is an attacker’s ability to remain undetected in a network for a long period of time and move laterally across it. According to IBM, the average breach in 2020 took 207 days to detect and another 73 days to contain, giving an attacker plenty of time to cause significant financial and reputational damage to an organization. Stopping lateral movement is essential to any security posture and is at the core of Appgate’s Zero Trust strategy.

The 2020 “SolarWinds” attack is an example of how costly a breach can be. A nation-state breached the networks of thousands of organizations, including as many as 425 of the Fortune 500 and all branches of the U.S. military, after clients of SolarWinds downloaded a software update that was infected with malicious code. The breach occurred sometime between March and June of 2020 and went undetected by traditional perimeter-based network security solutions until December of that year. The perpetrators moved laterally within the networks of these organizations, gathering sensitive data, and installing more malware. It will take years to contain the vast damages that are expected to cost up to $100 billion.

Following the SolarWinds attack, guidance was released by NIST, the National Security Agency (“NSA”), and the Cybersecurity and Infrastructure Security Agency (“CISA”) recommending a Zero Trust security approach. Additionally, on May 12, 2021, President Joe Biden issued an Executive Order explicitly calling for the adoption of a Zero Trust Architecture to improve the nation’s response to “persistent and increasingly sophisticated malicious cyber campaigns that threaten the public sector, the private sector, and ultimately the American people’s security and privacy.” The federal government continues to lead the industry in setting standards with the September 2021 release of a Zero Trust maturity model and Zero Trust strategy documents.

In addition to threats caused by external actors, insider threats, typically coming from employees or third-party contractors, also pose a growing security threat to organizations. According to IBM, non-malicious insiders caused 23% of organizational data breaches in 2020. While insider breaches are most frequently caused by simple human error, these non-malicious breaches are still expensive, with an average cost of $3 million per breach in 2020. Therefore, it is critical to limit access to only those resources individuals require to do their job.

Finally, identity fraud is also on the rise as cyber criminals are directly targeting consumers and financial institutions. According to Javelin Strategy & Research’s 2021 Identity Fraud Study, total identity fraud losses soared to a record $56 billion in 2020. Commercial banks are a frequent target of criminals, who use targeted email phishing, social media, and other strategies to induce bank employees and their consumers to inadvertently share their credentials. The COVID-19 pandemic has accelerated this trend, as more consumers moved to online and mobile channels to execute banking transactions. As consumers increasingly rely on these channels, financial institutions must rely on best-in-class authentication and security protocols to protect against fraud.

Because of the ever-evolving threat landscape, the cybersecurity market is experiencing significant growth as “next-generation” security solutions are designed to address these many challenges.

Traditional security tools are being rendered ineffective by the move to distributed IT environments, the growing prevalence of remote workforces, persistent human error, and increased consumer engagement on digital platforms.

Historically, security has centered around network perimeters, not users. Traditional perimeter-centric security tools, such as VPNs, firewall equipment, and network access control equipment were designed for a network infrastructure and threat landscape that no longer exist. Many vendors of these perimeter-centric technologies have simply refreshed hardware without altering the flawed security paradigm on which these legacy solutions are based. While the perimeter-centric approach used by these technologies made sense previously, it’s ineffective and easily exploitable in a modern environment for several reasons.

First, the network perimeter has evaporated as organizations’ infrastructures and people’s ways of working have evolved. Today’s hybrid networks now include on-premises, public and private cloud resources, or a combination of these (i.e., hybrid). The wide adoption of Infrastructure-as-a-Service (“IaaS”), SaaS, mobile devices, IoT, and large-scale remote working underscore just how far organizations have moved from traditional networking. Organizations now expect their workers to securely move from place-to-place and device-to-device without losing productivity. These factors have dramatically increased the attack surface, the scope of network vulnerabilities, and the likelihood of network infiltration, as each new user, connection, device, or online interaction introduces risk.

Second, the network is vulnerable and therefore the likelihood of a breach continues to grow. Not only are the number of attacks and sophistication of adversaries increasing, but also there is risk coming from the impacts of human error, which account for a large portion of data breaches. Even as network security technology improves, you can never fully solve the human element, as people reuse passwords, click links, download files, and don’t update software.

Finally, the perimeter-centric model was built on the notion of implicit trust, in which users, once inside the network, are granted access to more resources than they need. As a result, if a breach occurs and an attacker is inside the network, they are easily able to perform reconnaissance, exploit vulnerable systems, and live undetected while they carry out their mission and cause widespread damage.

This context indicates why specific security technologies need to be replaced. VPNs provide remote access, not security. In fact, VPN entry points represent well-known and widely exploited vulnerabilities. VPNs also perpetuate the outdated model of a single network perimeter entry point (i.e., not a distributed network architecture) and broad network access privileges. Network access control solutions are similarly outdated. For instance, because they are hardware-based and require physical proximity to users, they have been rendered ineffective by the shift to work-from-home. They also have an inherently “coarse-grained” access control model – allowing or denying access only to broad sections of the network, rather than to individual resources, thus frequently giving users access to more resources than they need. While traditional firewalls will always have a place in organizations’ network infrastructure, they are not suited for controlling access by remote users with granularity or fidelity. Firewall policy models are oriented around IP addresses, not users, therefore limiting their ability to adapt to today’s identity-centric security needs.

Organizations have adopted a complex set of cybersecurity tools that do not always integrate well.

Many organizations struggle with a large set of mismatched and overlapping cybersecurity tools. In 2020, IBM estimated that the average large enterprise uses an average of 45 cybersecurity tools, with some large organizations operating with in excess of 100 tools. Unfortunately, many of these tools do not integrate well, resulting in significant performance issues and leaving organizations with operational complexity and management difficulties. Some larger legacy security providers have tried to address this issue by creating portfolios of products that have generally been compiled through the acquisition of disparate solutions. While tools in these portfolios are usually easier to manage, the mix of products typically are not all “best of breed” and often require a complete system overhaul that can be time consuming and expensive. This drives the need for organizations to adopt a solution that simplifies and integrates technologies together.

Our Solution

Appgate offers software solutions and services to address these changing cybersecurity threats:

Appgate SDP: In traditional IT architectures, employees, contractors, and vendors have overprivileged access across multiple IT environments, exposing many attack surfaces. Appgate SDP is designed to ensure trusted network access for all corporate users across all devices and IT environments, including cloud, hybrid, or on-premises. We empower organizations to defend their network from wrongful access and continuously monitor for changes in user behavior once a connection is made. The network remains invisible until a user is authenticated and connected, so that no ports are exposed and open to attacks. Once authenticated and on the network, SDP employs the principles of least-privileged access, which dictate that users can only access resources they need to do their job. Access is conditional, based on many factors, and if any one of them change during the online session, the user can be denied access in part or in full to resources and applications. The most common Appgate SDP use cases include VPN replacement for remote access, cloud and hybrid deployments, cloud migrations, securely providing third-party access, secure Development and Operations (“DevOps”), and integrating Merger & Acquisition (“M&A”) assets into a secure network environment.

Digital Threat Protection: Consumers are increasingly reliant on digital platforms to conduct daily tasks, which creates greater opportunities for fraud. Appgate helps organizations minimize the impact of fraud for themselves and for their consumers. Most cyberattacks start with a phishing attempt and rapidly escalate from there. Appgate’s DTP solution helps combat external threats, including phishing links, malicious mobile apps, and fraudulent websites, targeting consumers. It illuminates threats lurking online, continuously monitors activity, and takes swift action to stop attacks before damage is done, and often before intended victims are even aware.

Risk-Based Authentication: In order to augment weak authentication measures, like the password, organizations have unintentionally created friction for their customers. RBA offers an intelligent and data informed approach to authenticating users without friction. Our solution uses real-time behavioral risk assessments, context-based authentication, and machine learning to protect individuals against targeted attacks. It employs strong authentication and transaction monitoring to determine if the person attempting to access their account is legitimate, and if not, access is denied. During an online session, the user’s activity is constantly monitored for changes in behavior. Transactions can be blocked or challenged in real-time, preventing account takeover.

Appgate Threat Advisory Services: Because no cybersecurity system is infallible, it is critical for an organization to address weaknesses in their network before an attacker does. Appgate’s Threat Advisory Services proactively identifies vulnerabilities and validates defenses. We use highly sophisticated, bespoke processes based on the individual needs of our customers to simulate nation-state-level and other complex attacks. These engagements help organizations test and validate the security investments they’ve made and can lead to the implementation of our software solutions based on remediation recommendations as we help our customers accelerate their Zero Trust journey. Another benefit is that we can use real-time information from our services engagements to stay up to date on the evolving cybersecurity threats to inform our software technology roadmap, helping us more rapidly address our customers’ evolving needs.

Key Benefits

We believe we provide unique and innovative cybersecurity solutions to address the security challenges faced by any modern organization and are a preferred security vendor for the following reasons:

| ● | Pure-play Zero Trust security provider. As a pioneer, leader, and one of the earliest proponents of Zero Trust, we have built and honed a pure-play platform based on Zero Trust principles to facilitate secure interactions for organizations, their devices, and their consumers. Our leading software solutions are, and have always been, rooted in Zero Trust principles and provide organizations with a strong foundation in their shift towards this modern cybersecurity posture. |

| ● | Effective across all environments. Modern organizations require infrastructure to support on-premises, hybrid, cloud, IoT, bring your own device (“BYOD”), and other disparate platforms. Most of our competitors provide solutions for some of these platforms and none of our competitors provide an effective solution that can dynamically adjust for changes in context across all environments. The result in most organizations is a patchwork of products that often do not integrate well, thereby creating additional complexity, security gaps, and administrative burden. We believe we were among the first to identify the need for and deliver an enterprise class, software-based, unifying solution that dynamically works across all environments. |

| ● | A better approach to network security. Our solutions use the principles of Zero Trust to strengthen network security, making it harder for adversaries to attack a network. Additionally, if a breach were to occur, an attacker’s lateral movement would be restricted so they can be identified and contained swiftly and overall damages could be limited. |

| ● | Prevents complex fraud. We offer financial institutions and other consumer-facing organizations a complete set of solutions based on Zero Trust principles to prevent fraud. Unlike traditional rules-based products, our solutions incorporate machine learning and behavioral analytics to identify and stop fraudulent activities, and dynamically assess risk to make decisions about when to authenticate connections. Our proprietary technology is also focused on detecting and deactivating targeted external threats which utilize phishing links, malicious mobile apps, or fraudulent websites. We continuously analyze and monitor an array of digital channels to identify threats, and execute site take-downs, often before intended victims are even aware. Finally, we provide rich insights on victims, so organizations are better prepared to stop future complex fraud campaigns. |

| ● | Supports business growth. Appgate’s solutions provide a strong, secure foundation allowing customers to grow at the pace of their business, unconstrained by cybersecurity worries. Appgate’s security solutions are easily extendable, enabling customers to onboard new customers, vendors, and M&A assets without compromising security. |

| ● | Allows secure “work from anywhere”. Appgate’s solutions offer fast, secure, direct connections from any location, enabling increasingly popular remote workforce models. Unlike perimeter-based approaches, our SDP platform uses a uniform identity-centric policy model to connect users from any device in any location. While remote workforce models typically invite security risk, Appgate’s security architecture is designed to ensure that increased workforce mobility does not create additional vulnerable access points. |

| ● | Strong integration capabilities. Our solutions can be easily deployed alongside existing security systems and across the entire IT environment. We utilize what we believe is the richest set of APIs amongst our peers to enable our solution to coordinate and communicate with other IT systems and improve the interoperability with other security products. Our approach allows customers to both extend the reach and value of their existing security and non-security tools by integrating them into our Zero Trust security solutions. We believe this value proposition enables a faster purchasing decision and differs from “next generation” security solutions that require an overhaul of a customer’s existing security system. |

| ● | Empowers digital transformation. Because our solutions are highly compatible with other technologies, Appgate customers are emboldened to adopt new, transformative non-security solutions without fear of integration issues. Unlike many legacy security tools, Appgate’s solutions are highly conducive to digital transformation and empower customers to continue on their digital journey. |

| ● | Enhanced customer experience. Our products provide an enhanced, agile experience for end users and administrators for the following reasons: |

| | | |

| o | Seamless end user experience: We provide automatic, dynamic access without having to frequently engage with the end user or disrupt workflow processes. Users are authenticated the same way regardless of where they are located or what device they are using. This approach differs from, and can be a replacement for, inflexible tools like VPNs and static multi-factor authentication systems, which often require users to re-authenticate themselves routinely, frustrating users. Our fraud protection suite is designed to stop attacks as they are unfolding and before the user is even aware. It is designed to fully protect them from phishing attacks, malware downloads and fraudulent transactions. |

| | | |

| o | Uniform policy model: We allow system administrators to create a single set of access policies that can be used uniformly across multiple disparate environments, increasing ease of use, operational efficiency, and security. This is in sharp contrast to not only traditionally siloed products (e.g., VPNs, NACs), but also many other ZTNA providers, who utilize static (versus dynamic) security rules or who cannot secure access for on-premises users. |

| o | Customer support and innovation: We partner with our customers on their Zero Trust journeys to ensure they receive maximum value from our products. We do so by providing first-class customer support and continually innovating to meet our customers’ needs. Our customer success team works closely with our customers throughout their entire life cycle, maintaining an open line of communication, frequently requesting feedback to ensure we are meeting their needs, and supporting them as new needs arise. By doing so, we become an extension to our customers’ teams. Partnering with our customers also influences how we prioritize our technology roadmap and enhances the value of our products to meet their changing needs. We collect customer feedback systematically, including quarterly feedback from our Customer Advisory Board, a panel comprised of select customers who are among the heaviest users of our solutions. |

| | | |

| o | Improved Operational Efficiency: Adoption of Appgate’s user-friendly software solutions frequently leads to improved operational efficiency for organizations. A recent Nemertes survey concluded that all respondents reported improvements in one or more key operational metrics, including average user provisioning time, average login time, and number of access-related security tickets, after adopting Appgate’s solutions. |

Competitive Strengths

Our competitive strengths include:

| ● | Leading Zero Trust product providing differentiated efficacy and user experience. Our solutions were purpose-built to meet the needs of modern organizations, whose networks are transforming with the expansion of cloud, SaaS, mobile, IoT, and remote working. Appgate’s SDP Zero Trust Network Access was designed to function and integrate across all IT environments, including cloud, hybrid, and on-premises, and as a result, it is the only product to do so effectively. Our user-friendly product allows system administrators to create a single set of access policies that can be used uniformly across multiple environments, reducing risk and administrative resources. Our solutions also integrate well with many existing security systems. We accomplish this through our broad set of APIs, which not only can be quickly deployed to extend the usefulness of existing systems, but also extract threat data and context from other technologies which we in turn can use to enrich our risk scoring and authentication decisions. |

| ● | Industry leading reputation. Our SDP product was named a “Leader” in the Forrester New Wave™ for Zero Trust Network Access (Q3 2021) and, as of October 12, 2021, received 4.7 out of 5 stars from customer reviews on Gartner Peer Insights. SDP was also recognized by Forrester in their “New Tech: Zero Trust Network Access, 2021” report, as a mature or “Late-Stage” vendor, indicating significant company tenure, number of customers, employees, and funding level as compared to our peers. Our Risk-Based Authentication solution was named a “Leader” in Quadrant Solutions’ SPARK Matrix™: Risk Based Authentication (RBA), 2021 report. We believe these high-profile recognitions received from trusted industry experts have elevated our reputation with existing and prospective customers. |

| ● | Strong customer focus. We are a trusted, long-term partner to our customers and are devoted to offering exceptional service. Our customer success team not only works with customers during the sales and renewal process, but also works with and supports our customers throughout their entire journey. They accomplish this through frequent communication and quarterly business reviews, helping them through new issues/use cases as they arise, and consistently seeking feedback to improve our products and services. Appgate also runs a Customer Advisory Board to enhance the open dialogue across customers to ensure we understand their changing needs. Our customers’ feedback is used as a direct input to our innovation roadmap so that we can quickly rollout the changes that we know are the most critical to our customers. Our goal is to become a true partner to our customers, involved in their day-to-day operations, going above and beyond a transactional vendor relationship. We continue to invest in our channel partners to increase customer adoption and satisfaction. A recent Nemertes survey of our customers revealed that 100% of respondents said Appgate accelerated their digital transformation. Of those implementing Zero Trust, they ranked Appgate’s importance to their strategy 9.5 out of 10. |

��

| ● | Demonstrated “license to win” with proven integrated sales and engineering approach. Our robust product offerings currently serve over 600 customers including Fortune 100 enterprises and domestic and international government agencies. We attract blue chip private and public sector organizations due to our integrated technical sales approach. We extend our customer reach through our trusted channel partners, such as Lumen, Optiv, Presidio, Guidepoint Security, DXC, TechMatrix, SageNet, Q2, Alkami, GBM, CLM, Kite, and Cybernet using a sell-with approach to avoid conflicts and increase win rate. Our customer acquisition engine is complemented by our strong sales engineering team which can powerfully demonstrate the value of our product to even the largest, most complex prospective customers. While our solutions have proven suitable for these large customers, they are also affordable and can meet the needs of organizations of any size. |

| ● | Highly experienced management team with a singular focus on cybersecurity threats. Our senior management team is composed of experienced executives with extensive expertise in the cybersecurity industry as well as knowledge of the markets in which we operate. The members of our senior management team have an average of over 20 years of experience in the enterprise technology and cybersecurity spaces and have a strong historical track record of success. Our seasoned executives were among the earliest pioneers in the Zero Trust security movement and are devoted to the continued growth of our business. |

Our Opportunity

The need for Zero Trust access and authentication solutions is increasing as more organizations expand their predominantly hybrid IT infrastructures to account for cloud computing, SaaS, mobility, IoT, BYOD, and remote working, thus introducing new attack vectors that traditional perimeter-based solutions cannot protect. Digital fraud is also on the rise as digital transaction volumes continue to grow. While these shifts were well underway prior to the COVID-19 pandemic, its impact has only accelerated these trends. For example:

| ● | According to 451 Research in 2020, hybrid IT environments are the most common amongst organizations, with approximately 60% of organizations currently operating or planning to operate using hybrid IT environments. |

| ● | Gartner estimates that public cloud services end user spend will grow at a 21% compound annual growth rate (“CAGR”) over the next three years. |

| ● | At the end of 2021, 99% of organizations will be using one or more SaaS solutions. |

| ● | Ericsson expects mobile data traffic to grow 4.5x over the next 6 years, representing a 28% CAGR. |

| ● | The number of connected IoT devices is expected to increase from approximately 9 billion in 2020 to approximately 14 billion in 2024, implying a 12% CAGR, according to 451 Research. |

| ● | BYOD has been normalized, evidenced by a 2012 Cisco study that found over 95% of organizations have allowed employee-owned devices in the workplace. |

| ● | PricewaterhouseCoopers estimates that over 50% of US enterprises will adopt a permanent hybrid (remote / in-office) workweek following the COVID-19 pandemic. |

| ● | The Federal Trade Commission reports that Americans lost over $3 billion to fraud in 2020. Key factors contributing to this large loss include COVID-19-related acceleration of e-commerce and online food delivery. |

| ● | Over 70% of Americans reported use of peer-to-peer (“P2P”) payment applications in 2020, ultimately prompting the Federal Communications Commission (“FCC”) to issue a warning about potential fraud in 2021. |

With these changes and the fact that cyber threats are on the rise, the need for organizations to adopt Zero Trust solutions is becoming more urgent.

Our Zero Trust SDP product can provide seamless secure network access across all environments, including cloud, hybrid, and on-premises. Therefore, we believe it is well positioned to continue to displace and take share from traditional network security solutions, such as firewalls, VPNs, NACs, and intrusion detection systems, as these legacy solutions are not built for cloud or hybrid IT environments and thus increase the risk of network exposure. We are also well positioned against cloud only cybersecurity providers given the prevalence of hybrid IT environments.

Our total addressable market encompasses hybrid, cloud, and on-premises network security, which Gartner estimates is a combined $39 billion market opportunity in 2021, expected to grow at a 14% CAGR to reach $57 billion by 2024. As more organizations migrate their IT to the cloud and embrace hybrid architectures, the need for a new network security approach will become increasingly apparent, and we believe we are well positioned to grow and take share in this market for the reasons discussed above.

We believe we are also well positioned to benefit from the recent rising interest in the idea of a Secure Access Service Edge (“SASE”). This term, recently created by the analyst firm Gartner, encompasses the trend of integrating many security and network technologies to secure hybrid, cloud, and on-premises environments. Appgate SDP is a recognized leader in ZTNA, which we believe is the most critical element of SASE because there cannot be security without securing access to the network first. Given our positioning, we believe our Zero Trust platform will be among the earliest beneficiaries of the SASE trend.

Our RBA and DTP solutions address Fraud Detection and Prevention (“FDP”). According to Global Market Insights, FDP was a $20 billion market in 2018 and expected to grow at a 23% CAGR from 2019-2025, which implies a total market size of $30 billion in 2020. The continued growth of online banking, e-commerce and P2P payment applications underpins the need for robust solutions to defend against pervasive, complex, and always-evolving fraud schemes. While growth in digital transactions has been ongoing, the COVID-19 pandemic has further accelerated this trend as more people have moved online to complete transactions, providing even greater opportunity for increased fraud.

Additionally, our DTP offerings are well-positioned to capitalize on the growing set of active and targeted phishing campaigns, as well as the increasing use of malicious websites and mobile apps for criminal purposes. Zero Trust should extend to the set of digital properties owned by the organization; ensuring that their customers aren’t deceived by fraudulent websites, phishing campaigns, or mobile apps is critical to these businesses’ reputations.

Growth Strategies

We expect to work with new and existing customers to support their Zero Trust journeys and beyond. Key elements of our growth strategy include:

| ● | Continue to grow customer base. While our solutions are uniquely positioned to serve large, regulated, security-conscious organizations with complex, hybrid IT environments, our solutions also offer value to medium and small sized customers. We believe we can continue to grow our customer base as we scale our sales team and increase our investment in channels and strategic partners. |

| ● | Expand with existing customers. We utilize a land and expand strategy through which we typically expand a customer account by adding new use cases or more users, including third-party users as contractors. We continue to invest in our customer success function, focused on retention and increased customer cross-selling. |

| ● | Grow our global footprint. We currently have customers across over 40 countries and have offices in 8 countries, reflecting our investment to be a global company and our success selling products internationally. In the twelve months ended June 30, 2021, international sales represented 52% of our revenue. While we expect our international markets to continue to grow, we anticipate the growth in the United States to outpace that of international markets. |

| ● | Expand our channel and product partnerships. Our Zero Trust solutions are highly complementary to a number of other security products, and as such, we have built a number of highly strategic product and go-to-market partnerships. Our products are easy to deploy and can be distributed by value-added resellers and service providers. We have strong growing channel partnerships with Lumen, Optiv, Presidio, Guidepoint Security, DXC, TechMatrix, SageNet, Q2, Alkami, GBM, CLM, Kite, and Cybernet, among others and work closely with federal systems integrators such as Raytheon, Northrop Grumman, and ManTech, who are building out solutions around our products for wider distribution. |

| ● | Expand our presence with U.S. federal government. With NIST, The White House, and other agencies endorsing the adoption of Zero Trust, we expect to have ample opportunities to leverage our early and continued success with the Department of Defense and Department of Homeland Security and to build trust with other government agencies and departments. Our solution was the first SDP product to be Common Criteria Certified, which is the international “gold standard” for Information Technology security. Common Criteria is recognized by 30 nations and was developed by the United States, United Kingdom, Canada, France, Germany, and the Netherlands. |

| ● | Innovate to add new functionality and use cases. We invested 28% of our revenue in research and development in the twelve months ended June 30, 2021 and maintain a robust product and technology roadmap. Our roadmap incorporates customer feedback which gives us confidence that we will be able to monetize our development efforts. We seek to offer highly scalable, flexible, and user-friendly products to address a variety of high-impact use cases. |

Our Technology and Architecture

Appgate’s cybersecurity solutions empower and protect how people work and connect. Our solutions are designed to enhance security, limit the ability of attackers to succeed, and minimize damage in the event of a breach. We recognize that IT, business, and security infrastructures are complex and can act as impediments to innovation, security, efficiency, and effectiveness. Organizations need security solutions that can be easily and effectively deployed and integrated into their existing environments.

Our solutions are designed with customer integration and customer success in mind, and this philosophy has influenced our technology architectures. We believe that customers should retain the choice of where and how to deploy their security infrastructure, enforce access, and route traffic. As such, we have designed and architected our solutions to support secure access to the cloud and on-premises.

Appgate SDP

Our Zero Trust Network Access solution, Appgate SDP, is purpose-built to secure enterprise environments by applying the core principles of Zero Trust. With Appgate SDP, our customers have successfully achieved enterprise Zero Trust security, at scale and at speed, integrated into their IT and security teams, business processes, and technologies.

The Appgate SDP architecture is fully aligned with the NIST Zero Trust model, which contains the following fundamental principles:

| ● | No implicit trust. There is no inherent trust (or access) granted to assets or user accounts based solely on their physical or network location, instead assuming a network has already been breached. |

| ● | Authentication and authorization required before access is granted. Authentication and authorization are discrete functions performed before any access to an enterprise resource is permitted. This applies to users, servers and devices. |

| ● | Minimal attack surface (principle of least privilege). All users, devices, and networks must only permit access to the minimal set of resources, and only for authenticated and authorized users. This applies to all users (remote and on-premises), all devices (enterprise-issued and BYOD), and all resource types (on-premises, cloud-based, physical, or virtual). |

| ● | Dynamic, identity-centric policies. The focus is on protecting specific resources (assets, services, workflows, network accounts, etc.), not broad network segments. Access policies dynamically evaluate user, device, network, and resource attributes to make decisions about whether access should be permitted at any given point in time. |

Deployment Architecture

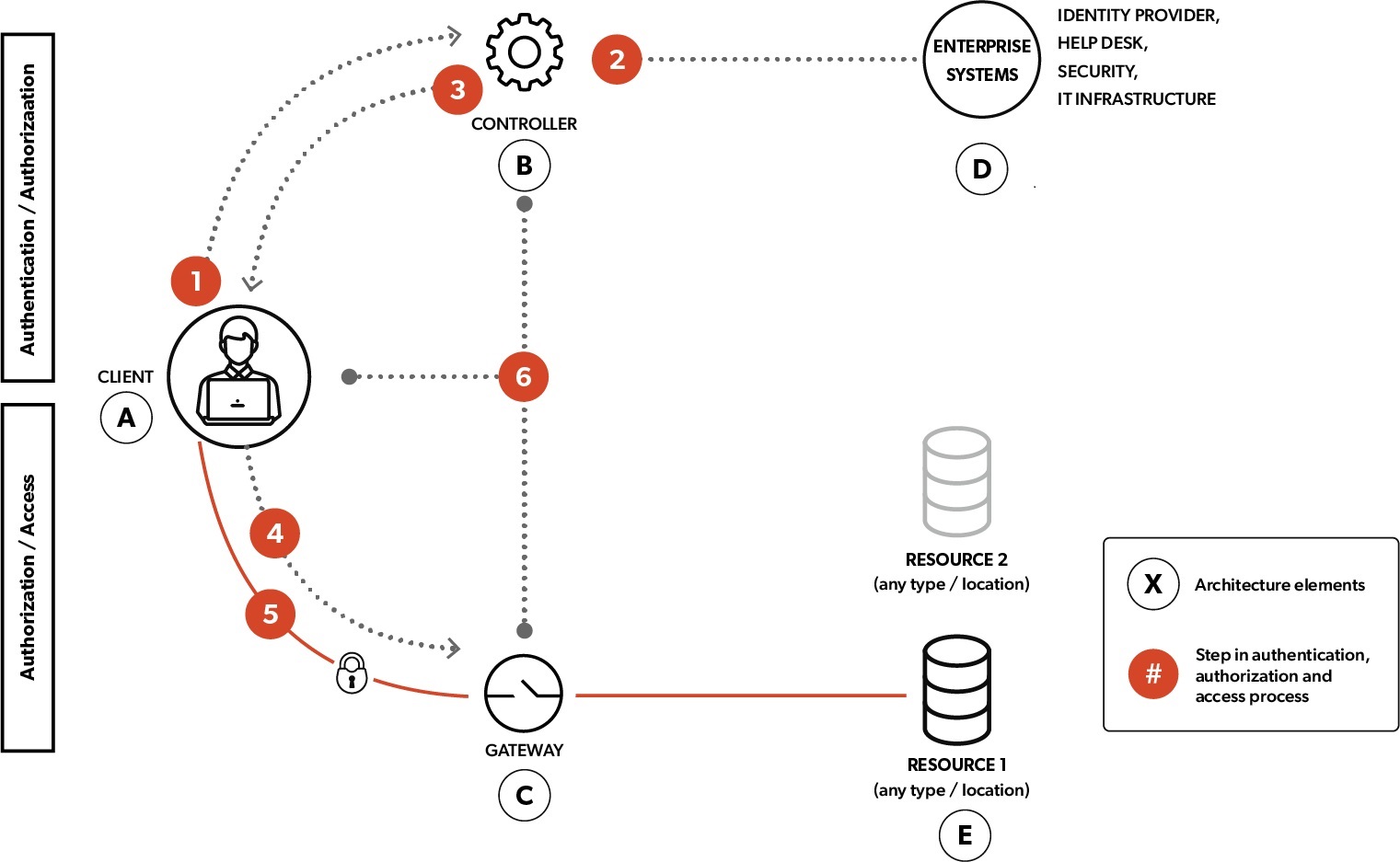

The Appgate SDP deployment architecture is comprised of the following five elements.

| A. | Client. The user of a resource (described below). In the typical Appgate SDP use case, the client is an organization’s employee seeking to access an application from a PC or mobile device. |

| B. | Controller. Effectively the brain of the system, the controller houses the enterprise policy model (the rules used to determine which users should have access to which resources), aggregates the information required to enforce the enterprise policy model, and then makes an authentication and authorization decision. |

| | | |

| C. | Gateway. Policy enforcement points that restrict access to resources until a client is authorized. |

| | | |

| D. | Enterprise Systems. Sources of information about a user and context used to make authentication and authorization decisions. |

| | | |

| E. | Resource. Any application, server, network, IoT device, containerized workload, etc. that can be located in any cloud or on-premises environment. |

| | | |

A conceptional depiction and description of the Appgate SDP deployment architecture are as follows:

| 1. | The Client (or user) first connects to the Controller. |

| | | |