UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| (Mark One) | ||

ý | ANNUAL REPORT UNDER SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

FOR THE FISCAL YEAR ENDED: DECEMBER 31, 2010 | ||

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to | ||

Commission File Number: 0-51430

STW RESOURCES HOLDING CORP.

(Exact name of registrant as specified in its charter)

Nevada (State or Other Jurisdiction of Incorporation or Organization) | 20-3678799 (I.R.S. Employer Identification No.) |

619 West Texas Avenue, Suite 126, Midland, Texas 79701

(Address of principal executive offices) (Zip Code)

(432) 686-7777

(Registrant's telephone number)

(Former Name, Former Address and Former Fiscal Year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| None |

Securities registered pursuant to section 12(g) of the Act:

Title of class: Common Stock, par value $0.001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 (the "Exchange Act") during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | o | Accelerated filer | o | |

Non-accelerated filer (Do not check if a smaller reporting company) | o | Smaller reporting company | ý |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No ý

The aggregate market value of the voting and non-voting common equity held by non-affiliates as of June 30, 2010 was $7,569,296 based upon an offering price of $0.25 per share of common stock sold to investors on or about June 30, 2010 . For purposes of the above statement only, all directors, executive officers and 10% shareholders are assumed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for any other purpose

As of April 15, 2011 the registrant had 43,836,849 shares of common stock, par value $0.001 per share outstanding.

STW RESOURCES HOLDING CORP.

FORM 10-K

INDEX

| Page | ||

1 | ||

13 | ||

19 | ||

19 | ||

19 | ||

19 | ||

20 | ||

21 | ||

22 | ||

30 | ||

30 | ||

31 | ||

32 | ||

32 | ||

33 | ||

36 | ||

38 | ||

38 | ||

39 | ||

40 | ||

| SIGNATURES | 41 | |

| FINANCIAL STATEMENTS | F-1 | |

PART I

This Annual Report on Form 10-K for the fiscal year ended December 31, 2010 filed by STW Resources Holding Corp. (f/k/a Woozyfly Inc. and STW Global, Inc.) with the Securities and Exchange Commission contains forward looking statements and information that are based upon beliefs of, and information currently available to, the Company's management as well as estimates and assumptions made by the Company's management. When used in the filings the words "anticipate", "believe", "estimate", "expect", "future", "intend", "plan" or the negative of these terms and similar expressions as they relate to the Company’s or Company’s management identify forward looking statements. Such statements reflect the current view of the Company with respect to future events and are subject to risks, uncertainties, assumptions and other factors (including the risks contained in the section of this report entitled "Risk Factors") relating to the Company’s industry, the Company’s operations and results of operations and any businesses that may be acquired by the Company. Should one or more of these risks or uncertainties materialize, or should the underlying assumptions prove incorrect, actual results may differ significantly from those anticipated, believed, estimated, expected, intended or planned.

Although the Company’s management believes that the expectations reflected in the forward looking statements are reasonable, the Company cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, the Company does not intend to update any of the forward-looking statements to conform these statements to actual results. The following discussion should be read in conjunction with the Company's financial statements and the related notes filed with this Annual Report on Form 10-K.

In this Annual Report on Form 10-K, references to "we," "our," "us," the "Company," “STW”, refer to STW Resources Holding Corp. (f/k/a Woozyfly Inc. and STW Global, Inc.), a Nevada corporation.

ITEM 1. BUSINESS.

Corporate History

The Company was organized September 11, 2003 (Date of Inception) under the laws of the State of Nevada, as GPP Diversified, Inc. The business of the Company was to sell pet products via the Internet. We were initially authorized to issue 25,000,000 shares of its no par value common stock. On November 9, 2005, we amended our articles of incorporation to increase our authorized capital to 100,000,000 shares with a par value of $0.001. Concurrently, we changed our name from GPP Diversified, Inc. to Pet Express Supplies, Inc. On July 28, 2008, Pet Express Supply, Inc. entered into an Exchange Agreement with each of the shareholders of CJ Vision Enterprises, Inc., a Delaware corporation doing business as Woozyfly.com, pursuant to which we changed our corporate name to Woozyfly, Inc. , authorized the issuance of 10,000,000 blank check preferred shares and effectuated a 6:1 stock split. On January 15, 2009, we ceased operations.

On May 12, 2009, the Company filed a voluntary petition in the United States Bankruptcy Court for the Southern District of New York (the “Bankruptcy Court”) seeking reorganization relief under the provisions of Chapter 11 of Title 11 of the United States Code (the “Bankruptcy Code”). The Chapter 11 case is being administered under the caption In re Woozyfly, Inc. Case No. 09-13022 (JMP) (the “Chapter 11 Case”). The Company continued to operate its business as debtor in possession under the jurisdiction of the Bankruptcy Court and in accordance with the applicable provisions of the Bankruptcy Code and orders of the Bankruptcy Court. In connection with the Chapter 11 Case, the Bankruptcy Court approved the arrangement pursuant to which MKM Opportunity Master Fund Ltd agreed to provide a DIP loan in the amount up to $100,000 (the “DIP Loan”).

The filing of the Chapter 11 Case constituted an event of default or otherwise triggered repayment obligations under the Company's 6% Secured Convertible Notes due June 30, 2011 ("Convertible Notes"). As a result, all indebtedness outstanding under these facilities and the notes became automatically due and payable, subject to an automatic stay of any action to collect, assert, or recover a claim against the Company and the application of applicable bankruptcy law.

On January 17, 2010, we entered into an Agreement and Plan of Merger (“Merger Agreement”) with STW Acquisition, Inc. (“Acquisition Sub”), a wholly owned subsidiary of the Company, STW Resources, Inc. (“Acquiree” ) and certain shareholders of Acquiree controlling a majority of the issued and outstanding shares of STW Resources, Inc. Pursuant to the Merger Agreement, Acquiree merged into the Acquisition Sub resulting in an exchange of all of the issued and outstanding shares of STW Resources, Inc. for shares of the Company on a one for one basis. At such time, STW will become a wholly owned subsidiary of the Company.

On February 9, 2010, the Court entered an order confirming the Second Amended Plan of Reorganization (the “Plan”) pursuant to which the Plan and the Merger was approved. The Plan was effective February 19, 2010 (the “Effective Date”). The principal provisions of the Plan are as follows:

| · | MKM, the DIP Lender, shall receive 400,000 shares of common stock and 2,140,000 shares of preferred stock; |

| · | the holders of the Convertible Notes shall receive 1,760,000 shares of common stock; |

| · | general unsecured claims shall received 100,000 shares of common stock; and |

| · | the Company’s equity interest shall be extinguished and cancelled. |

On February 12, 2010, pursuant to the terms of the Merger Agreement, STW Resources, Inc. merged with and into Acquisition Sub, which became a wholly-owned subsidiary of the Company (the “Merger”). In consideration for the Merger and STW Resources, Inc. becoming a wholly-owned subsidiary of the Company, the Company issued an aggregate of 31,780,004 (the “STW Acquisition Shares”) shares of common stock to the shareholders of STW Resources, Inc. at the closing of the merger and all derivative securities of STW as of the Merger became derivative securities of the Company including options and warrants to acquire 12,613,002 shares of common stock at an exercise price ranging from $3.00 to $8.00 with an exercise period ranging from July 31, 2011 through November 12, 2014 and convertible debentures in the principal amount of $1,467,903 with a conversion price of $0.25 and maturity dates ranging from April 24, 2010 through November 12, 2010.

Overview

The Company, based in Midland, Texas, provides customized water reclamation services. STW’s core expertise is an understanding of water chemistry and its application to the analysis and remediation of complex water reclamation issues. STW provides a complete solution throughout all phases of a water reclamation project including analysis, design, evaluation, implementation and operations.

STW’s expertise is applicable to several market segments including:

| · | Gas shale hydro-fracturing flowback; |

| · | Oil and gas produced water; |

| · | Acid mine drainage (“AMD”); |

| · | Desalination; |

| · | Brackish water; and |

| · | Municipal waste water. |

Understanding water chemistry is the foundation of STW’s expertise. STW will provide detailed chemical analysis of the input stream and of the process output that conforms to the various environmental and legal requirements. STW becomes an integral part of the water management process and provides a customized solution that encompasses analysis, design and operations including pretreatment and transportation. Simultaneously, STW evaluates the economic impact of this process to the customer. These processes will use technologies that fit our customer’s need: fixed, mobile or portable; evaporation, reverse-osmosis or membrane technology, and any necessary pre-treatment, crystallization and post-treatment. STW will also supervise construction, testing, and operation of these systems. Our keystone is determining and optimizing the most appropriate technology to effectively and economically address our customers’ particular requirements. As an independent solutions provider STW is manufacturer-agnostic and is committed to the use of the right technology demanded by the design process.

Market Opportunities

Gas shale fracturing flowback water

STW is actively pursuing opportunities in all the major shale formations in the United States. The initial focus, in this sector, is the Marcellus Shale in Pennsylvania. Presently, we believe there are about 800 producing wells, the majority being simple vertical wells, and over sixty new wells in Pennsylvania are being drilled each month. Most of the new wells being drilled are horizontal, requiring about 3.5 million gallons of water per well. There are 28 producers in the Marcellus, with the four largest being Range Resources, Chesapeake Energy, Atlas Energy Resources and Seneca Resources.

Unconventional tight gas shales such as Marcellus require millions of gallons of fresh water to drill and stimulate a new well. The water returns during the fracture flowback (“frac”) and production (“production”) with salts or Total Dissolved Solids (“TDS”) at levels unfit for human consumption. This flowback or produced water is typically disposed of through various means such as controlled dilution to a river, or lost from the ecosystem by injection into disposal wells. STW will target the frac water market in the tight gas formations first, and approach the produced water market for coal bed methane and oil and gas production subsequently.

Oil and gas reservoirs are usually found in porous rocks, which also contain saltwater. Cross linked gel fracture fluids with high “proppant” loading (additives that prop open fissures in the geological formation caused by hydraulic fracturing) have been utilized to fracture these zones in order to gain permeability, allowing the oil and gas to flow to the well bore. The unconventional shale formations have been common knowledge for decades, but the cost of gas production was always considered to be uneconomical. The wells were drilled and fractured with the same crossed linked system as discussed above.

All of the wells were vertical and required stimulation about every three years with a new fracture. Around 2001, the “slick water fracture” technique was developed. This change required larger volumes of fresh water (1.2 million gallons per fracture on a vertical well) to be used in the fracturing process, a friction reducing polymer additive, and low concentrations of a proppant in the hydraulic fracture fluid. Wells using this modified technique now can economically produce gas for over eight years without re-stimulation. The fresh water is believed to dissolve salts from the shale over time and open up the natural fractures and fissures in the rock, allowing more gas to be produced. In 2003, horizontal drilling rigs were brought into the Barnett Shale and the slick water fracture volume increased from one to eight plus million gallons per well. The slick water fracture technique has become the standard for all of the shale formations for stimulation of the wells.

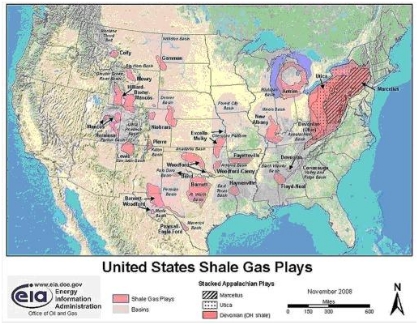

This map illustrates the location of the major shale formations that are discussed below:

The Marcellus Shale

The Marcellus Shale formation, located in the Appalachian regions of Pennsylvania, New York and West Virginia, is the major focus of the Company. The Marcellus covers the largest land mass of any of the known shale zones to date, and it is located close to the densely populated north-eastern corridor of the United States. The water returns from the slick water fracture contain significantly higher TDS levels than the Barnett Shale and also include, in certain cases, extremely high levels of calcium, barium, strontium and chloride ions.

At approximately 200,000 parts per million in TDS, the produced water from these regions is nearly seven times the salinity of the ocean. The most common practice utilized by the gas production industry in Pennsylvania for the disposal of waste water streams produced by gas wells is to remove the oil, some of the heavy metals and simply discharge this water to the rivers and streams. The volume of water used in the gas well fracture process has grown substantially over recent years with growth in both the absolute number of active wells and with increased volumes of water in each well. STW believes that today, the initial daily returns of one Marcellus fracture well often exceed the volume of thousands of older oil and gas wells.

While there are about 800 Marcellus gas wells in operation in the Marcellus shale formation today, gas producers in the region are primarily engaged in exploratory drilling process activities. The northern portion of the state reportedly has some of the best geological formations for gas production, but drilling activity has been curtailed as a result of limited water supply and limited capacity to dispose of waste water. Because of economic considerations in local communities, the investment of several billion dollars by producers in lease acquisition for drilling purposes, and proximity to high population areas, management believes that drilling activity utilizing hydraulic fracturing methods will increase significantly in the future.

The Marcellus Shale Formation is believed to be approximately 30 million plus acres in size. In comparison, the Barnett Shale Formation is approximately 2 million acres in size and approximately 140 million barrels of produced water are disposed of in deep disposal wells annually. Each one of the stationary systems proposed by STW will be able to process approximately 23,000 barrels of water per day, and the mobile systems will be capable of processing 1,700 barrels per day. This is therefore a high priority focus for STW.

With the mountainous terrain in the Appalachian region, STW believes mobile or portable evaporation units may provide a key part of the solution in this market by helping gas producers minimize trucking in and out of production locations and their neighboring communities. These systems may also be airlifted in and out of drilling locations. Central evaporation and crystallization would then be required to handle the remaining water and residual brine. The central plants would also be equipped to generate calcium chloride and sodium chloride salts. The sodium chloride would be processed as rock salt for use in de-icing highways for public safety. As discussed above, revenue from these salts would impact the overall cost of reclamation, reinforcing the Company’s competitiveness in the region.

The Fayetteville Shale

Producers in Arkansas’ Fayetteville Shale face similar problems as those operating in the Marcellus, as there are very limited brine disposal options. Most disposal wells in the Fayetteville shale are located near Ft. Smith; over a three hour drive from most of the producing gas wells. Although new disposal wells are being permitted and are under evaluation in the Conway area, gas producers remain uncertain as to whether the permitted volumes for these brine injection wells will be sufficient for current and future production needs.

The fracture system typically utilizes 50,000 to 65,000 barrels, or 2.0 to 2.8 million gallons of water. These wells typically flow back 1,000 to 1,500 bpd of contaminated frac water for the first few days and then decline to under 100 bpd for the next three months before finally declining to a rate of five bpd or less. All of this flowback water is disposed of at land farms and disposal wells. Recently the land farms have come under scrutiny due to claims that these operations fail to comply with applicable regulations and laws. Several land farm operations have been shut down because of contamination of the areas surrounding these operations, significantly raising the cost of disposal to the producers.

Water quality varies with the location of the wells and can range from approximately 20,000 mg/l TDS for wells in the Searcy area to over 70,000 mg/l TDS for wells in the northern and western portions. The Company believes water reclamation coupled with deep well injection could provide a very cost effective solution to producers in the Fayetteville zone. The lower TDS in this shale, relative to other shales, would allow water recovery at rates in excess of 90% at 20,000 mg/l TDS, and 75% at TDS levels of approximately 70,000 mg/l. These rates will dramatically reduce trucking cost to disposal wells, and will provide fresh water for new wells or other applications such as steam generation.

As part of the STW’s strategy in this region, the Company is actively seeking to educate gas producers on the advantages of water reclamation.

The Barnett Shale

As discussed above, the Barnett Shale, located in central and west-central Texas, was the first shale formation to be developed with production starting nearly 25 years ago. In 2009, drilling activity was flat in the Barnett Shale at current gas prices. A large influence for this leveling is the increasing activity in the other gas formations such as the Haynesville, Fayetteville and Marcellus.

The Piceance Basin

The conventional frac process in the Piceance has been to incorporate the typically low TDS flowback and produced waters as fracture fluids in new wells. Previously, drilling has been completed throughout the year; however, several producers only fracture in the summer months. For these producers, excess water produced in the winter required storage in surface containment facilities that created substantial environmental risk. Treatment of this water prior to storage addressed this risk and resulted in a seasonally high demand for water reclamation during winter months.

Today, producers in the Piceance Basin are generally slowing down drilling activity while natural gas prices remain depressed. Whatever produced water is currently generated is being hauled to other states for disposal.

Eagleford ShaleFormation

The Eagleford Shale is a recently discovered formation located in South Texas. Several experimental wells have been completed and to date appear to be very profitable. This area has limited supplies of fresh water, leading the Company to believe water reclamation will be a required solution in order for producers to access a sufficient supply of frac water in this market. Production of natural gas has been reported at levels in excess of 10 million cubic feet (“Mcf”) per day, and hundreds of barrels of condensate at some of the wells. The Company expects to intensify its efforts to address this market opportunity.

The Haynesville Shale

This shale formation covers the northern half of Louisiana, southern Arkansas and extends into northeastern Texas. It is the highest pressure zone of all the shale formations discovered to date. Most of the wells are horizontal, utilize the slick water fracture system, and each require about 6.5 million gallons of water. Production of natural gas has been reported at levels in excess of 25 million cubic feet (“Mcf”) per day at some of the wells in the Haynesville shale formation.

Once production starts at typical gas wells in this region, a surge of water production occurs for a few days before water production declines to ten bpd or less. There appears to be sufficient disposal well capacity in the Haynesville to handle present production needs. The Company believes that more disposal wells are being added in southern Arkansas and northeastern Texas as needed. STW believes that legislators in Louisiana are currently reviewing policies on disposal wells and may alter these to increase the deep injection well disposal capacity.

The Cotton Valley zone actually produces most of the water in the area. It has a TDS content of over 200,000 mg/l and therefore does not lend itself to economical water reclamation. Crystallization would be required, which is more expensive and would generate a salt cake that is not required in the area. Consequently, this region is not a high priority market for STW at this time.

Produced Water

Shale zones are typically dry geological formations devoid of any formation or connate water, and hence the fracture flowback water comprises most of water that returns following gas production. Outside of shale formations, where most gas and oil production occurs, there is typically a reservoir of connate water in the production zone that generates “produced” water. Produced water is primarily salty water trapped in the reservoir rock and brought up along with oil and/or gas during production, and is the most common oil field waste. The quality of produced water varies significantly in different parts of the world depending on the geology of the underlying formation.

In a large number of the oil fields in the USA, secondary or tertiary means of handling produced water storage, such as water floods and steam floods, are typically utilized. These are operations where the produced water is used to maintain reservoir pressure, prevent subsidence, and sweep the zone to remove the oil. Most of these water floods utilize a fresh water source as a supply so that sufficient volumes are available. As these fields age, less water is required for the flood, so excess contaminated brines concentrate and require disposal. As this water could be reclaimed with Thermal Evaporative Technologies, STW believes that the market for reclaiming produced water outside the shale reclamation projects represents a considerable opportunity for the Company.

Texas is the largest oil and gas production state in the nation and the produced water is unfit for use, poses a threat to the environment and is typically injected into deep injection wells. In accordance with Texas Railroad Commission regulations, water placed in these disposal wells is rendered permanently unavailable for re-use or consumption. The reclaimed water would available for many beneficial uses, including agricultural and environmental applications, as well as re-use in hydraulic fracturing operations. Deep injection well practices in every gas and oil producing region in the world pose the same detrimental environmental and resource conservation issues. The water reclamation products and services offered by the Company could provide a significant part of the solution to all constituencies concerned.

In the steam floods of California, a large portion of the water is recycled through the water treatment facility and converted back to steam. There are some fields that there is excess water in the millions of gallons per day that is low in TDS and could very economically be converted back to environmentally usable water.

Acid mine drainage (AMD)

AMD is another sensitive environmental issue in the Appalachian Mountain regions. We believe it has impaired more than 4,600 miles of waterways in Pennsylvania alone. Drainage from old abandoned coal mines is acidic, and insoluble metal oxides precipitate when the drainage enters a river, lake or stream, damaging the marine ecosystem. The AMD discharge from a single mine or coal tailing pile can range from 10 to more than 10,000 gallons per minute. In just one example, the Lackawanna River in northeastern Pennsylvania is being contaminated from at least seven monitored AMD locations with estimated peak flow of 40 million gallons per day. STW has identified the state of Pennsylvania as a customer for AMD purification and the Marcellus producers (eg Range Resources, Chesapeake Energy, Atlas Energy Resouces and Seneca Resources) as potential customers for the resultant reclaimed water.

Acid Mine Drainage is the number one environmental water issue throughout most of the Appalachian Mountains. Coal was one of the largest industries in the region. Unproductive and unprofitable mines were abandoned. Over time a large number of these mining companies have gone out of business leaving the residual “dirty coal” and the water flowing from the mines as a responsibility of the states and federal government. Dirty coal is the coal that lies near the edge of the main coal seam and contains a high concentration of dirt.

As the mines fill up with water overtime, the excess water flows out. Due to contact with the minerals contained in the dirt, coal, salts and gases, the water tends to become acidic. This lower pH tends to dissolve more ions or salts such as iron, aluminum, calcium, and sulfate. Iron and other metals upon oxidation form insoluble salts such as iron oxide or rust. Once the acid mine drainage enters a river, lake or stream, the water precipitates these metal oxides. This forms an impervious film on the bed of the water destroying the marine ecosystem.

The Pennsylvania Department of Environmental Protection (“DEP”) typically constructs passive treatment plants that require large acreage, where the process is oxidation in large lagoons allowing the solids to precipitate and altering the pH level by adding certain chemicals such as lime. The water leaving these systems will support the growth of plants and animals. This process is inherently more time-consuming and expensive, and because of the land requirements, not suitable for all locations.

STW can provide AMD treatment using a specially-designed mobile unit and sell the processed AMD to the producers. The state will retain ownership of the AMD, with STW having ownership rights to the processed water.

The mobile unit available to STW can handle about 250 gpm or about 360,000 gallons per day. This mobile unit provides the same functionality as the current passive system, but in minutes compared to weeks and months and with a much smaller footprint. The state may provide incentives in the form of grants and/or subsidies that cover the cost of AMD processing. The DEP has permits in place for the disposal of the filter-pressed sludge. STW is also reviewing all of the present passive system flow-rates and water quality for potential use as supply water to producers

Brackish Water

World-wide, there are brackish water zones that contain large volumes of water. The water contains dissolved salts in the 0.5 to 2% (5,000 to 20,000 mg/l TDS) range and hence unfit for human use. This water can be treated to reduce the TDS below 500 mg/l or 0.05% TDS making the water fit for human consumption. Factors such as decreasing supplies of fresh ground and surface water, increased competition for surface water resources, and changes in population/demand centers are driving the need for brackish water for water supply. STW’s potential customers are private companies and municipalities serving fast growing metropolitan areas where demand for water is outpacing the available supply. For example, aquifers in the Texas Gulf Coast contain a large volume of brackish water (less than 10,000 ppm TDS) that, with desalinization, will help meet increasing demand in the region.

Legislative and Regulatory:

Progressively tighter regulations are demanding a thorough review of the entire water-use cycle in industrial applications with the ultimate goal of encouraging and/or mandating reclamation and re-use of water. STW works closely with Federal, State and local regulators and environmental agencies to share our expertise and knowledge on this complex issue and discuss our views on potential solutions. The Company’s intimate knowledge of this process is a key tool to assist their customers to better understand the legislative and regulatory elements related to water management and advise them of various alternatives

Process

STW’s process is predicated upon a thorough understanding of the customer’s water needs and related issues. This understanding is developed through a series of interactive discussions with the customer. The next phase is data gathering and analysis. STW collects samples at various locations and at different time intervals which are then tested at independent laboratories and analyzed by STW. Based upon this analysis, STW would recommend a solution using the most appropriate technologies and negotiate the acquisition and financing of these technologies as well as contracts with engineering procurement construction (“EPC”). Finally, STW oversees the EPC process and operates the facility.

STW’s process is based upon a fundamental understanding of the core issue and developing an appropriate solution using our experience and expertise. It includes sampling and testing, analysis, design and as required by customers, implementation and operation. Some of the steps involved are described below:

| · | The inlet water quality must be determined and measurement of Total Dissolved Solids (TDS), hardness, barium, strontium, bromine, sulfate and hydrocarbon concentrations are critical. |

| · | Multiple samples over time are taken to ensure consistency and accuracy of inlet water quality measurement. |

| · | An understanding and analysis of potential uses for the reclaimed water. |

| · | A site inspection to determine the various vessels needed such as tanks, pumps, pits, truck off loading racks, and engineering testing of the land. |

| · | An analysis of fluid volumes and their variability over time. |

| · | Length of time the water needs to be reclaimed at this site. |

| · | Determination of appropriate technology: fixed or mobile, evaporation, reverse osmosis or other. |

| · | Permitting as needed |

| · | An investigation of the handling of the concentrated brines and any other residue from the reclamation process. |

| · | Disposal options on the residue including potential use of the by-products. |

Technology

STW has developed relationships with a number of manufacturers that offer best-of-class technologies applicable to its customer base. These technologies include thermal evaporation, membrane technology and reverse osmosis and are available as fixed or mobile units with varying capacities. Various pre and post-treatment options are available as necessary including crystallizers that process very high TDS (>150,000 mg/l).

Thermal Evaporation: This process is capable of handling waters that contain up to 150,000 mg/l TDS, with fresh water recovery rates from 50 to 90% or greater depending on inlet water quality. The recovered fresh water, or “distillate”, is highly purified water from the evaporative process and has multiple re-use applications. It is particularly applicable in the gas shale and oil production facilities for reclaiming frac and produced waters.

The technology is scalable and can be deployed as mobile units that can process 72,000 gallons per day (“gpd”), or as portable units that can process 216,000 gpd, or as fixed central units capable of processing up to 2,880,000 gpd.

Residual brine concentrate can, depending on local conditions and producer’s priorities, either be disposed off in deep injection wells or be treated further through a Crystallizer that reduces it into distillate and commercially valuable salt residuals.

Reverse Osmosis: Waters that are below 34,000 mg/l of total dissolved solids and contain low levels of barium, strontium, bromine, and sulfate can be reclaimed through a reverse osmosis unit (RO). Reverse osmosis is the process of forcing a solvent from a region of high solute concentration through a semi-permeable membrane to a region of low solute concentration by applying a pressure in excess of the osmotic pressure. The membranes used for reverse osmosis are generally designed to allow only water to pass through while preventing the passage of solutes (such as salt ions). This process is best known for its use in desalination (removing the salt from sea water to get fresh water), but it has also been used to purify fresh water for medical, industrial and domestic applications. Recovery rates for seawater to drinking water are about 50%.

A stream of concentrated brine or higher TDS is the by-product. This brine can be properly disposed of or utilized as a feed solution to a brine concentrator or crystallizer. The latter ensures higher quality water with lower TDS levels for industrial Uses.

Most oilfield waters cannot be processed through an RO membrane since they contain barium, strontium, or bromine. The barium and strontium are very large molecules and they plug the membrane and create damage or permanent fouling of the membrane. Bromine and other such halogens react with the membrane and destroy its integrity. There are few oil field waters that could be processed through this technology but a thorough study is required to ensure success. STW Resources will utilize this technology where the water chemistry can be processed through RO membranes.

Membrane Bioreactor: A Membrane BioReactor (“MBR”) is a combination of biological and ultrafiltration technologies. The biological area provides the same process utilized in all sewage treatment facilities. Bacteria are maintained in an aerobic condition which cause decay in all of the organic materials contained in the water, and oxidizing these organic materials into low molecular weight acids, usually acetic acid. Maintaining the bacteria in an oxygen rich environment prevents mutatation or growth of any anaerobic bacteria, which would produce inorganic acids such as hydrogen sulfide.

A filter membrane removes the water fraction from the unit. The membrane provides filtration in the 0.01 microns or lower range which is sufficient enough to remove viruses, bacteria, and other colloidal materials. The water exiting the units is potable water and safe for human consumption.

Joint Venture with Aqua Verde, LLC

On August 5, 2010, the Company entered into a Joint Venture Agreement (the “JV Agreement”) with Aqua Verde, LLC (“AV”). Pursuant to the JV Agreement, STW and AV agreed to collectively work together through the joint venture to procure water reclamation contracts with natural gas drilling companies in the states of Colorado and Texas. In addition, AV shall assign all of its existing master services agreements and master services contracts to the joint venture.

The joint venture is named Water Reclamation Partners, LLC, and is owned 51% by the Company and 49% by AV, with the Company having exclusive control and management of the business of the joint venture. In addition, a steering committee was established for the purpose of managing and directing the joint pursuits of the joint venture, and is comprised of two representatives from the Company and two representatives of AV. As of December 31, 2010, there have been no operations within the joint venture, and AV has not contributed the master services contracts to the joint venture, therefore the joint venture had no impact on the current consolidated financial statements.

Marketing & Sales

STW’s business proposition is to provide comprehensive, necessary water treatment solutions. We will work closely with our customers to evaluate their water treatment needs, understand how these may change over time, assess the regulatory and economic factors and then design an optimal solution. As illustrated in the chart to the right, STW offers a broad array of technical solutions coupled with a service suite and financial structuring options that provide our customers with the ability to obtain a turnkey solution to their waste water disposal challenges.

Gas Shales: Most of the natural gas producers in each of the shale formations are already well known to the Company. STW personnel have developed many, and in some cases, long standing relationships with key personnel responsible for well completion and remedial operations at each gas producer. STW monitors production plans at the producer level, the acreage acquisitions at the shale formations and trends that relate to the demand for water reclamation by region. In addition, the Company maintains detailed databases that monitor drilling permits, rig counts and other key statistics that forecast gas production rates by geography. These activities allow the Company to anticipate demand for its services and to prioritize its sales calling effort on those producers for whom fresh water supply is an issue or where shale water disposal pose the greatest challenges.

The foundation of the Company’s sales strategy is to become an integral part of its customer’s water management function. This involves identifying and finding solutions to customer needs through a multi–step, consultative approach:

| · | Evaluate drilling program and production expansion plans. |

| · | Identify and define fracture water supply needs and waste brine generation levels. |

· | Study the flowback water volumes and chemistry over time. |

· | Generate economic models jointly with producers, with full consideration of all costs of obtaining, utilizing, and disposing of the water. |

· | Evaluate various water reclamation options, from equipment to logistics, and develop financial models for all the options. |

· | Provide a customized presentation comparing present practices to all of the options of water reclamation available to the customer, for buy-in to the best scenarios. |

· | Jointly develop a presentation of the best scenarios for water management (present and future) for use by upper management. Support the presentation as required. |

· | Review and determine optimal system design, location and financial structure. |

· | Develop a time line for water reclamation implementation. |

· | Execute definitive off-take and/or other agreements satisfactory to all parties. |

STW is able to facilitate this part of the sales process through its detailed knowledge of the gas production process and economics, shale formation geology, frac water chemistry, well completion techniques and logistics and regional regulatory landscapes. This expertise reduces the time required during the evaluative stage of the sales process and fosters a positive working relationship with our customers. STW then works together with its manufacturing partners to complete the technical solution, develop ancillary system requirements (balance of plant) evaluate cost and operating data, model the financial performance of the system and define remaining project parameters and an installation timeline.

Water reclamation is a new paradigm for natural gas producers. Educating them about the economic, environmental and political benefits is key to long-term adoption.

Some of the issues that operators are facing currently in the Marcellus Shale are:

| · | Water consumption and usage restrictions on the Susquehanna River are very restrictive. |

| · | There are only 8 deep injection wells in Pennsylvania, all of which are already at or close to capacity. New deep wells are being drilled, but the permitting process and actual drilling costs are proving to be expensive. |

| · | Trucking costs from $3.10 to over $10 / barrel, and generate a number of complaints about truck traffic, noise and the associated wear and tear on the roads. The cost to dispose of the water into the commercial disposal wells is $1.50 to $3.00 per barrel in addition to the trucking costs. |

| · | Reclaimed water will not require a consumption permit for use, as it has already been consumed once. Trucks can bring brine to the Water Reclamation facility and return with fresh water for the next fracture. |

| · | The crystallization process will produce rock salt that meets the requirements of ASTM Standards for road salt. PennDOT purchases between 600,000 and 1,000,000 tons of road salt each year and local municipalities purchase an additional 500,000 tons. An STW 1 million gal/day facility will produce approximately 88,500 to 106,000 tons of rock salt per year. |

| · | By 2011 any new permits for disposal to the rivers will require total dissolved solids (TDS) removal. |

At this time, in the Marcellus Shale, only a couple of operators have the necessary scale for a captive facility. Most operators are still in the exploratory drilling stage, with single wells being drilled over a wide region.

Based on the geographical mountainous terrain, the producers are constructing the well sites on the higher elevations so that they do not interfere with the agricultural and cattle ranch business conducted in the valleys. In a large number of examples a multiple well pad is constructed and then the wells are directional drilled and completed in the Marcellus. One central water pit is permitted to hold the drilling and fracture water. As the fracture is conducted, the flowback and produced water is presently trucked to an approved disposal facility. In some cases the producers are recycling some of the early low TDS flowback water by filtration and then blending into the new fresh water. All of the fresh water utilized by all of the wells must be trucked to the site and then all of the flowback and produced water is trucked away.

STW would locate mobile evaporation equipment at the well site. The flowback water would be processed and the distilled water generated would be placed into the fracture water pit. The residual brine from the evaporation process would be trucked to an approved disposal facility or taken to a STW central crystallizer. The crystallizer would provide additional fresh water that could be trucked (2 way freight) back to the fracture pit. About 98% of the available water from the residual brine or the high TDS produced water would be recovered. Additional bi-products of sodium chloride for use in Highway deicing and a solution of calcium chloride would be generated.

Competition

In the oil and gas industry, current fracturing and produced water disposal methods – deep injection wells and surface water disposal – represent the Company’s greatest source of competition.

Brine Discharge / Deep Injection Wells

In many gas shale fields, disposal through a deep injection well offers a cost-effective (though environmentally questionable) alternative to water reclamation. If suitable geology exists, high TDS flowback waters can be disposed by injection into a deep discharge brine well. There are operative brine discharge wells in each of the major shale formations, particularly in the Barnett shale formation in Texas where many empty oil wells are converted for brine discharge use. There are only eight such discharge wells in the state of Pennsylvania. Management believes these are presently operating at close to capacity.

Surface Water Disposal

Similarly, surface water disposal facilities (rivers, streams and drainage creeks) offer a competitive alternative to water reclamation. At river discharge facilities, flowback and produced waters are treated to remove naturally occurring radioactive materials, some suspended solids and well completion chemicals before discharge. Dissolved salts are not removed and therefore are added to surface water systems where they degrade water quality, pollute the environment and disrupt wildlife habits. Many states have taken action to reduce or eliminate altogether the availability of surface water disposal for gas well waste water streams.

In the Marcellus shale, there are several treatment facilities that remove only the oil and heavy metals, then discharge the water to certain rivers (where permitted), and range in size from 20,000 to 200,000 gallons per day. The treatment does not remove salts, so the waters that are being discharged into the river system retain high TDS contamination levels. In April of 2009, the Pennsylvania DEP regulated this type of treatment by limiting it to existing permitted facilities only through January 2011, at which time treatment to remove the TDS (salts) will have to be implemented.

The following companies provide pre-discharge brine treatment solutions:

The Company accepts flowback and produced waters from gas producers operating in the Marcellus and other regions in Pennsylvania, removes the oil, heavy metals, and discharges the water to certain rivers in Pennsylvania. Advanced Waste operates one discharge facility in the western part of the Pennsylvania. Sunbury operates an experimental river discharge site in conjunction with the Pennsylvania Department of Environmental Protection. Sunbury’s primary business is the operation of waste coal fired power plants, and it has obtained a permit to discharge significant volumes of contaminated water into certain rivers in Pennsylvania. Acid Mine Drainage is presently processed through large acreage passive systems. These systems provide oxidation followed by a long settling time for the heavy metals to precipitate and possibly some pH adjustment before the water enters the river or stream. There are several companies that construct such facilities under contract with the governmental agency. At this time there is no one that provides mobile AMD processing.

Number of Employees

As of April 15, 2011, other than our directors and officers, presently we do not have any full time employees.

Our Website

Our website address is www.stwresources.com; Information found on our website is not incorporated by reference into this report.

ITEM 1A. RISK FACTORS.

You should carefully consider the following risk factors and the other information included in this annual report on Form 10-K, as well as the information included in other reports and filings made with the SEC, before investing in our common stock. If any of the following risks actually occurs, our business, financial condition or results of operations could be harmed. The trading price of our common stock could decline due to any of these risks, and you may lose part or all of your investment.

Our limited operating history makes it difficult for us to evaluate our future business prospects and make decisions based on those estimates of our future performance .

We did not begin operations of our business until February 2008. We have a limited operating history and have generated limited revenue. As a consequence, it is difficult, if not impossible, to forecast our future results based upon our historical data. Reliance on the historical results may not be representative of the results we will achieve, particularly in our combined form. Because of the uncertainties related to our lack of historical operations, we may be hindered in our ability to anticipate and timely adapt to increases or decreases in revenues or expenses. If we make poor budgetary decisions as a result of unreliable historical data, we could be less profitable or incur losses, which may result in a decline in our stock price.

STW’s results of operations have not resulted in profitability and we may not be able to achieve profitability going forward.

STW incurred a net loss amounting to $16,184,248 for the period from inception (January 28, 2008) through December 31, 2010. In addition, as of December 31, 2010, STW has liabilities of $4,845,222. If we incur additional significant operating losses, our stock price, may decline, perhaps significantly.

Our management is developing plans to alleviate the negative trends and conditions described above. Our business plan is speculative and unproven. There is no assurance that we will be successful in executing our business plan or that even if we successfully implement our business plan, that we will be able to curtail our losses now or in the future. Further, as we are a new enterprise, we expect that net losses will continue and our working capital deficiency will exacerbate.

We depend upon key personnel and need additional personnel.

Our success depends on the continuing services of Stanley Weiner, our chief executive officer and director. The loss of Mr. Weiner could have a material and adverse effect on our business operations. Additionally, the success of the Company’s operations will largely depend upon its ability to successfully attract and maintain competent and qualified key management personnel. As with any company with limited resources, there can be no guaranty that the Company will be able to attract such individuals or that the presence of such individuals will necessarily translate into profitability for the Company. Our inability to attract and retain key personnel may materially and adversely affect our business operations.

We must effectively manage the growth of our operations, or our company will suffer.

To manage our growth, we believe we must continue to implement and improve our operational and marketing departments. We may not have adequately evaluated the costs and risks associated with this expansion, and our systems, procedures, and controls may not be adequate to support our operations. In addition, our management may not be able to achieve the rapid execution necessary to successfully offer our products and services and implement our business plan on a profitable basis. The success of our future operating activities will also depend upon our ability to expand our support system to meet the demands of our growing business. Any failure by our management to effectively anticipate, implement, and manage changes required to sustain our growth would have a material adverse effect on our business, financial condition, and results of operations.

Our business requires substantial capital, and if we are unable to maintain adequate financing sources our profitability and financial condition will suffer and jeopardize our ability to continue operations.

We require substantial capital to support our operations. If we are unable to maintain adequate financing or other sources of capital are not available, we could be forced to suspend, curtail or reduce our operations, which could harm our revenues, profitability, financial condition and business prospects.

Our Operations are Subject to Comprehensive Regulation Which May Cause Substantial Delays or Require Capital Outlays in Excess of Those Anticipated Causing an Adverse Effect on Us.

Our operations are subject to federal, state, and local laws relating to the protection of the environment, including laws regulating removal of natural resources from the ground and the discharge of materials into the environment. Various permits from government bodies are required for our operations to be conducted; no assurance can be given that such permits will be received. Environmental standards imposed by federal, provincial, or local authorities may be changed and any such changes may have material adverse effects on our activities. Moreover, compliance with such laws may cause substantial delays or require capital outlays in excess of those anticipated, thus causing an adverse effect on us. Additionally, we may be subject to liability for pollution or other environmental damages. We generally maintain insurance coverage customary to the industry; however, we are not fully insured against all possible environmental risks. To date we have not been required to spend any material amount on compliance with environmental regulations. However, we may be required to do so in future and this may affect our ability to expand or maintain our operations.

Risks associated with the collection, treatment and disposal of wastewater may impose significant costs.

Our wastewater collection, treatment and disposal operations of our subsidiaries are subject to substantial regulation and involve significant environmental risks. If collection systems fail, overflow or do not operate properly, untreated wastewater or other contaminants could spill onto nearby properties or into nearby streams and rivers, causing damage to persons or property, injury to aquatic life and economic damages, which may not be recoverable in rates. Liabilities resulting from such damage could adversely and materially affect our business, results of operations and financial condition. Moreover, in the event that we are deemed liable for any damage caused by overflow, our losses might not be covered by insurance policies, and such losses may make it difficult for us to secure insurance in the future at acceptable rates.

We will require significant capital requirements for equipment, commercialization and overall success.

We will require additional financing for our operations, to purchase equipment and to establish a customer base. We anticipate that we will require a minimum of $10.0 to $15.0 million in additional capital over the next six months to pursue our business plan. We cannot assure you that we will obtain any additional financing through any other means. Additional financing may not be available to us on acceptable terms, if at all. Unless we raise additional financing, we will not have sufficient funds to complete the purchase of equipment and commercialization of our services.

Our additional financing requirements could result in dilution to existing stockholders.

We will require additional financings obtained through one or more transactions which effectively dilute the ownership interests of holders of our Common Stock. We have the authority to issue additional shares of Common Stock and Preferred Stock as well as additional classes or series of ownership interests or debt obligations which may be convertible into any class or series of ownership interests in the Company. The Company is authorized to issue 100,000,000 shares of Common Stock and 10,000,000 shares of Preferred Stock. Such securities may be issued without the approval or other consent of the holders of the Common Stock.

A small number of existing shareholders own a significant amount of our Common Stock, which could limit your ability to influence the outcome of any shareholder vote.

Our executive officers, directors and shareholders holding in excess of 5% of our issued and outstanding shares, beneficially own over 38.1% of our Common Stock. Under our Articles of Incorporation and Nevada law, the vote of a majority of the shares outstanding is generally required to approve most shareholder action. As a result, these individuals will be able to significantly influence the outcome of shareholder votes for the foreseeable future, including votes concerning the election of directors, amendments to our Articles of Incorporation or proposed mergers or other significant corporate transactions.

We face competition.

We face competition from existing companies in reclamation of oil and gas waste water space that provide similar services to the Company’s. Our competitors may have longer operating histories, greater name recognition, broader customer relationships and industry alliances and substantially greater financial, technical and marketing resources than we do. Our competitors may be able to respond more quickly than we can to new or emerging technologies and changes in customer requirements.

We rely on confidentiality agreements that could be breached and may be difficult to enforce.

Although we believe that we take reasonable steps to protect our intellectual property, including the use of agreements relating to the non-disclosure of our confidential information to third parties, as well as agreements that provide for disclosure and assignment to us of all rights to the ideas, developments, discoveries and inventions of our employees and consultants while we employ them, such agreements can be difficult and costly to enforce. Although we generally seek to enter into these types of agreements with our consultants, advisors and research collaborators, to the extent that such parties apply or independently develop intellectual property in connection with any of our projects, disputes may arise concerning allocation of the related proprietary rights. If a dispute were to arise enforcement of our rights could be costly and the result unpredictable. In addition, we also rely on trade secrets and proprietary know-how that we seek to protect, in part, through confidentiality agreements with our employees, consultants, advisors or others.

Despite the protective measures we employ, we still face the risk that: agreements may be breached; agreements may not provide adequate remedies for the applicable type of breach; our trade secrets or proprietary know-how may otherwise become known; our competitors may independently develop similar technology; or our competitors may independently discover our proprietary information and trade secrets.

There has not been an active public market for our common stock so the price of our common stock could be volatile and could decline at a time when you want to sell your holdings.

Our common stock is traded on the Over-the-Counter Bulletin Board under the symbol STWS.OB. Our common stock is not actively traded and the price of our common stock may be volatile. Numerous factors, many of which are beyond our control, may cause the market price of our common stock to fluctuate significantly. These factors include:

| • | expiration of lock-up agreements; |

| • | our earnings releases, actual or anticipated changes in our earnings, fluctuations in our operating results or our failure to meet the expectations of financial market analysts and investors; |

| • | changes in financial estimates by us or by any securities analysts who might cover our stock; |

| • | speculation about our business in the press or the investment community; |

| • | significant developments relating to our relationships with our customers or suppliers; |

| • | stock market price and volume fluctuations of other publicly traded companies and, in particular, those that are in the oil and gas industry; |

| • | customer demand for our products; |

| • | investor perceptions of the oil and gas industry in general and our company in particular; |

| • | the operating and stock performance of comparable companies; |

| • | general economic conditions and trends; |

| • | major catastrophic events; |

| • | announcements by us or our competitors of new products, significant acquisitions, strategic partnerships or divestitures; |

| • | changes in accounting standards, policies, guidance, interpretation or principles; |

| • | sales of our common stock, including sales by our directors, officers or significant stockholders; and |

| • | additions or departures of key personnel. |

Securities class action litigation is often instituted against companies following periods of volatility in their stock price. This type of litigation could result in substantial costs to us and divert our management’s attention and resources.

Moreover, securities markets may from time to time experience significant price and volume fluctuations for reasons unrelated to operating performance of particular companies. These market fluctuations may adversely affect the price of our common stock and other interests in our company at a time when you want to sell your interest in us.

Our Common Stock is subject to the “penny stock” rules of the Securities and Exchange Commission.

The Securities and Exchange Commission has adopted Rule 15g-9 which establishes the definition of a "penny stock," for the purposes relevant to us, as any equity security that has a market price of less than $5.00 per share or with an exercise price of less than $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, the rules require:

| • | that a broker or dealer approve a person's account for transactions in penny stocks; and |

| • | the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased. |

In order to approve a person's account for transactions in penny stocks, the broker or dealer must:

| • | obtain financial information and investment experience objectives of the person; and |

| • | make a reasonable determination that the transactions in penny stocks are suitable for that person and the person has sufficient knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks. |

The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prescribed by the Commission relating to the penny stock market, which, in highlight form:

| • | sets forth the basis on which the broker or dealer made the suitability determination; and |

| • | that the broker or dealer received a signed, written agreement from the investor prior to the transaction. |

Generally, brokers may be less willing to execute transactions in securities subject to the "penny stock" rules. This may make it more difficult for investors to dispose of our common stock and cause a decline in the market value of our stock.

Disclosure also has to be made about the risks of investing in penny stocks in both public offerings and in secondary trading and about the commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.

Because certain of our stockholders control a significant number of shares of our common stock, they may have effective control over actions requiring stockholder approval.

Our directors, executive officers and principal stockholders, and their respective affiliates, will beneficially own approximately 38.1% of our outstanding shares of common stock. As a result, these stockholders, acting together, would have the ability to control the outcome of matters submitted to our stockholders for approval, including the election of directors and any merger, consolidation or sale of all or substantially all of our assets. In addition, these stockholders, acting together, would have the ability to control the management and affairs of our company. Accordingly, this concentration of ownership might harm the market price of our common stock by:

| • | delaying, deferring or preventing a change in corporate control; |

| • | impeding a merger, consolidation, takeover or other business combination involving us; or |

| • | discouraging a potential acquirer from making a tender offer or otherwise attempting to obtain control of us. |

Any adjustment in the conversion price of our convertible notes or the exercise price of our warrants could have a depressive effect on our stock price and the market for our stock.

If we are required to adjust the warrant exercise price pursuant to any of the adjustment provisions of the agreements relating to any of our prior financing transaction, the adjustment or the perception that an adjustment may be required, may have a depressive effect on both our stock price and the market for our common stock.

Failure to maintain effective internal controls in accordance with Section 404 of the Sarbanes-Oxley Act could have a material adverse effect on our business and operating results and stockholders could lose confidence in our financial reporting.

Effective internal controls are necessary for us to provide reliable financial reports and effectively prevent fraud. If we cannot provide reliable financial reports or prevent fraud, our operating results could be harmed. Failure to achieve and maintain an effective internal control environment, regardless of whether we are required to maintain such controls, could also cause investors to lose confidence in our reported financial information, which could have a material adverse effect on our stock price. Although we are not aware of anything that would impact our ability to maintain effective internal controls, we have not obtained an independent audit of our internal controls and, as a result, we are not aware of any deficiencies which would result from such an audit. Further, at such time as we are required to comply with the internal controls requirements of the Sarbanes-Oxley Act, we may incur significant expenses in having our internal controls audited and in implementing any changes which are required.

We have not paid dividends on our common stock in the past and do not expect to pay dividends on our common stock for the foreseeable future. Any return on investment may be limited to the value of our common stock.

No cash dividends have been paid on our common stock. We expect that any income received from operations will be devoted to our future operations and growth. We do not expect to pay cash dividends on our common stock in the near future. Payment of dividends would depend upon our profitability at the time, cash available for those dividends, and other factors as our board of directors may consider relevant. If we do not pay dividends, our common stock may be less valuable because a return on an investor’s investment will only occur if our stock price appreciates.

The requirements of being a public company may strain our resources, divert management’s attention and affect our ability to attract and retain qualified board members.

We recently became a public company and subject to the reporting requirements of the Securities Exchange Act of 1934, as amended, the Sarbanes-Oxley Act. Prior to February 2010, we had not operated as a public company and the requirements of these rules and regulations will likely increase our legal and financial compliance costs, make some activities more difficult, time-consuming or costly and increase demand on our systems and resources. The Exchange Act requires, among other things, that we file annual, quarterly and current reports with respect to our business and financial condition. The Sarbanes-Oxley Act requires, among other things, that we maintain effective disclosure controls and procedures and internal controls for financial reporting. For example, Section 404 of the Sarbanes-Oxley Act of 2002 requires that our management report on, and our independent auditors attest to, the effectiveness of our internal controls structure and procedures for financial reporting. Section 404 compliance may divert internal resources and will take a significant amount of time and effort to complete. We may not be able to successfully complete the procedures and certification and attestation requirements of Section 404 by the time we will be required to do so. If we fail to do so, or if in the future our chief executive officer, chief financial officer or independent registered public accounting firm determines that our internal controls over financial reporting are not effective as defined under Section 404, we could be subject to sanctions or investigations by the SEC or other regulatory authorities. Furthermore, investor perceptions of our company may suffer, and this could cause a decline in the market price of our common stock. Irrespective of compliance with Section 404, any failure of our internal controls could have a material adverse effect on our stated results of operations and harm our reputation. If we are unable to implement these changes effectively or efficiently, it could harm our operations, financial reporting or financial results and could result in an adverse opinion on internal controls from our independent auditors. We may need to hire a number of additional employees with public accounting and disclosure experience in order to meet our ongoing obligations as a public company, which will increase costs. Our management team and other personnel will need to devote a substantial amount of time to new compliance initiatives and to meeting the obligations that are associated with being a public company, which may divert attention from other business concerns, which could have a material adverse effect on our business, financial condition and results of operations. In addition, because our management team has limited experience managing a public company, we may not successfully or efficiently manage our transition into a public company.

If securities or industry analysts do not publish research or reports about our business, or if they change their recommendations regarding our stock adversely, our stock price and trading volume could decline.

The trading market for our common stock will be influenced by the research and reports that industry or securities analysts publish about us or our business. We do not currently have and may never obtain research coverage by industry or financial analysts. If no or few analysts commence coverage of us, the trading price of our stock would likely decrease. Even if we do obtain analyst coverage, if one or more of the analysts who cover us downgrade our stock, our stock price would likely decline. If one or more of these analysts cease coverage of our company or fail to regularly publish reports on us, we could lose visibility in the financial markets, which in turn could cause our stock price or trading volume to decline.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

Not Applicable.

ITEM 2. PROPERTIES.

Our principal offices are located at 619 West Texas Avenue, Suite 126, Midland, Texas 79701, which includes 1,250 square feet in office space. We pay $1,200 per month in rent and our lease is month to month.

ITEM 3. LEGAL PROCEEDINGS.

From time to time, the Company may become a party to litigation or other legal proceedings that it considers to be a part of the ordinary course of its business. The Company is not involved currently in legal proceedings that could reasonably be expected to have a material adverse affect on its business, prospects, financial condition or results of operations. The Company may become involved in material legal proceedings in the future.

ITEM 4. REMOVED AND RESERVED.

PART II

ITEM 5. MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUERS PURCHASES OF EQUITY SECURITES.

Our common stock qualified for quotation on the Over-the-Counter Bulletin Board under the symbol “STWS.OB” on November 19, 2010. The quotations reflect inter-dealer prices, without retail mark-ups, mark-downs, or commissions and may not necessarily represent actual transactions.

The closing price of our common stock on the OTC Bulletin Board on April 14, 2011, was $0.17 per share.

The following table sets forth the range of high and low bid quotations as reported on the OTC Bulletin Board for the periods indicated.

Year Ended December 31, 2010 | High | Low | ||||||

| Fourth quarter ended December 31, 2010 | $ | 1.00 | $ | 0.50 | ||||

Holders of Common Stock

As of April 15, 2011, we had 209 holders of record of our common stock.

Dividends

We have never paid any cash dividends on our common stock and do not anticipate paying any cash dividends on our common stock in the foreseeable future. We currently intend to retain any future earnings to fund the development and growth of our business. There are no restrictions in our certificate of incorporation or by-laws on declaring dividends.

As long as any shares of our series A convertible preferred stock are outstanding, no dividend may be declared or paid for payment on our common stock or any other class of our capital stock (other than the series A convertible preferred stock) without the prior express written consent of our holders of the series A convertible preferred stock representing not less than a majority of the aggregate number of the then outstanding shares of series A convertible preferred stock.

Recent Sales of Unregistered Securities

There were no sales of unregistered securities that were not previously reported in 8-K.

Equity Compensation Information

The following table summarizes information about our equity compensation plans as of December 31, 2010.

| Plan Category | Number of Shares of Common Stock to be Issued upon Exercise of Outstanding Options (a) | Weighted- Average Exercise Price of Outstanding Options | Number of Options Remaining Available for Future Issuance Under Equity Compensation Plans (excluding securities reflected in column (a)) (c) | ||||||

| Equity Compensation Plans Approved by Stockholders | - | $ | - | ||||||

| Equity Compensation Plans Not Approved by Stockholders | - | ||||||||

| Total | - | $ | - | ||||||

ITEM 6. SELECTED FINANCIAL DATA

Not Applicable.

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following information should be read in conjunction with STW Resources Holding Corp. (f/k/a/ Woozyfly, Inc.) (the “Company”) consolidated audited financial statements and the notes thereto contained elsewhere in this report. Information in this Item 2, "Management's Discussion and Analysis of Financial Condition and Results of Operations," and elsewhere in this Form 10-K that does not consist of historical facts, are "forward-looking statements." Statements accompanied or qualified by, or containing words such as "may," "will," "should," "believes," "expects," "intends," "plans," "projects," "estimates," "predicts," "potential," "outlook," "forecast," "anticipates," "presume," and "assume" constitute forward-looking statements, and as such, are not a guarantee of future performance. The statements involve factors, risks and uncertainties including those discussed in the “Risk Factors” section included herein, the impact or occurrence of which can cause actual results to differ materially from the expected results described in such statements. Risks and uncertainties can include, among others, fluctuations in general business cycles and changing economic conditions; changing product demand and industry capacity; increased competition and pricing pressures; advances in technology that can reduce the demand for the Company's products, as well as other factors, many or all of which may be beyond the Company's control. Consequently, investors should not place undue reliance on forward-looking statements as predictive of future results. The Company disclaims any obligation to update the forward-looking statements in this report.

Overview