Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

TABLE OF CONTENTS 3

TABLE OF CONTENTS 4

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| (Mark One) | |

o |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR |

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended March 31, 2008 |

OR |

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES ACT OF 1934 |

| For such transition period from to |

OR |

o |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Date of event requiring this shell company report |

| For such transition period from to |

Commission file number:333-137371

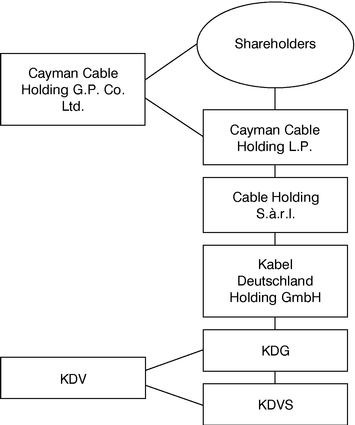

Kabel Deutschland GmbH

(Exact name of Co-Registrant as specified in its charter)

Kabel Deutschland Vertrieb und Service GmbH & Co. KG

(Exact name of Co-Registrant as specified in its charter)

Federal Republic of Germany

(Jurisdiction of incorporation or organization)

Betastraße 6-8

85774 Unterföhring

Germany

+49-89-960-100

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| |

|

|---|

Title of each class

| | Name of each exchange on which registered

|

| None | | n/a |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

€250 million 10.750% Senior Notes due 2014

$610 million 10.625% Senior Notes due 2014

(Title of Class)

As of March 31, 2008, the subscribed capital of KDG is held entirely by the sole shareholder Kabel Deutschland Holding GmbH and is represented by three shares in the following amounts:

Shareholders

| | €

|

|---|

| Kabel Deutschland Holding GmbH | | 24,750 |

| Kabel Deutschland Holding GmbH | | 250 |

| Kabel Deutschland Holding GmbH | | 1,000,000 |

| | |

|

| | | 1,025,000 |

| | |

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

o Yes ý No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

o Yes ý No

Note—Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

ý Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act. (Check one)

| Large accelerated filero | | Accelerated filero | | Non-accelerated filerý |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP o | | International Financial Reporting Standards as issued by the International Accounting Standards Board ý | | Other o |

If "Other" has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

o Item 17 o Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

o Yes ý No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

o Yes o No

TABLE OF CONTENTS

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. Selected Financial Data

In this annual report on Form 20-F, 'Issuer', 'Registrant', 'we', 'us', 'our', 'Company', 'KDG' and other similar terms refer to Kabel Deutschland GmbH and its consolidated subsidiaries, except where the context otherwise requires.

The selected consolidated statements of operations and cash flow data set forth below for the fiscal years ended March 31, 2004, 2005, 2006, 2007 and 2008 and the selected consolidated balance sheet data set forth below as of March 31, 2004, 2005, 2006, 2007 and 2008, in each case, for KDG have been derived from KDG's consolidated financial statements. KDG's consolidated financial statements for fiscal years ended March 31, 2006, 2007 and 2008 are included in ITEM 17 Financial Statements of this annual report.

The selected consolidated data presented below should be read in conjunction with our consolidated financial statements included in ITEM 17 Financial Statements of this annual report.

1

Consolidated Statement of Operations

| | Fiscal Year Ended March 31,

| |

|---|

| | 2004

| | 2005(1)

| | 2006(1)

| | 2007(1)

| | 2008

| |

|---|

| |

| | (as adjusted)

| | (as adjusted)

| |

| |

| |

|---|

| | (€ millions, except percentages)

| |

|---|

| | Cable Access Revenue | | 833.5 | | 850.1 | | 839.3 | | 845.6 | | 867.1 | |

| | TV/Radio Revenue | | 108.1 | | 126.4 | | 137.8 | | 163.0 | | 179.8 | |

| | Internet & Phone Revenue | | 1.2 | | 2.8 | | 9.8 | | 56.5 | | 121.4 | |

| | TKS Revenue | | 19.3 | | 23.9 | | 25.2 | | 28.1 | | 28.6 | |

| | |

| |

| |

| |

| |

| |

| Revenues | | 962.1 | | 1,003.2 | | 1,012.1 | | 1,093.2 | | 1,196.9 | |

| | Cost of Services Rendered(2) | | (616.5 | ) | (573.4 | ) | (490.1 | ) | (567.1 | ) | (588.5 | ) |

| | Other Operating Income | | 33.9 | | 17.9 | | 12.5 | | 13.2 | | 12.6 | |

| | Selling Expenses(3) | | (220.5 | ) | (262.5 | ) | (277.0 | ) | (318.7 | ) | (352.8 | ) |

| | General and Administrative Expenses(4) | | (115.5 | ) | (110.3 | ) | (102.4 | ) | (140.9 | ) | (128.7 | ) |

| | |

| |

| |

| |

| |

| |

| Profit from Ordinary Activities | | 43.5 | | 74.9 | | 155.1 | | 79.7 | | 139.5 | |

| | Interest Income | | 4.0 | | 11.4 | | 2.8 | | 3.6 | | 2.1 | |

| | Interest Expense | | (213.9 | ) | (186.3 | ) | (215.1 | ) | (155.7 | ) | (171.8 | ) |

| | Accretion/Depreciation on Investments and Other Securities | | 0.0 | | (0.3 | ) | (0.1 | ) | 0.3 | | (3.8 | ) |

| | Income from Associates | | 0.6 | | 0.7 | | 0.5 | | 0.4 | | 0.9 | |

| | |

| |

| |

| |

| |

| |

| Loss Before Taxes | | (165.8 | ) | (99.6 | ) | (56.8 | ) | (71.7 | ) | (33.1 | ) |

| Taxes on Income | | 13.9 | | (6.9 | ) | (11.7 | ) | (27.5 | ) | (0.7 | ) |

| | |

| |

| |

| |

| |

| |

| Net Loss | | (151.9 | ) | (106.5 | ) | (68.5 | ) | (99.2 | ) | (33.8 | ) |

| | |

| |

| |

| |

| |

| |

| Other Financial Data | | | | | | | | | | | |

| | Adjusted EBITDA(5) | | 428.0 | | 408.0 | | 401.3 | | 382.5 | | 457.8 | |

| | Adjusted EBITDA margin(6) | | 44.5 | % | 40.7 | % | 39.7 | % | 35.0 | % | 38.2 | % |

- (1)

- According to the update of the IFRIC agenda decision on IAS 39 accounting changes regarding assessing hedge effectiveness of interest rate swaps in a cash flow hedge have been made for the fiscal years ended March 31, 2005, 2006 and 2007. For a detailed description please refer to chapter Note 1.2 in the Notes to the consolidated financial statements of KDG and KDVS under ITEM 17 Financial Statements.

- (2)

- Includes €154.7 million of depreciation and amortization in FY 2008; €133.1 million in FY 2007; €117.4 million in FY 2006; €206.7 million in FY 2005; €261.8 million in FY 2004.

- (3)

- Includes €115.5 million of depreciation and amortization in FY 2008; €96 million in FY 2007; €88.2 million in FY 2006; €81.2 million in FY 2005; €92.4 million in FY 2004.

- (4)

- Includes €23.8 million of depreciation and amortization in FY 2008; €17.5 million in FY 2007; €15.2 million in FY 2006; €9.8 million in FY 2005; €10.1 million in FY 2004.

- (5)

- Profit from ordinary activities before depreciation, amortization, non-cash compensation, which consists primarily of expenses related to our management equity programs and non-cash restructuring expenses ("Adjusted EBITDA"), is a measure used by management to measure our operating performance. Adjusted EBITDA is not a recognized accounting term, does not purport to be an alternative to profit from ordinary activities or cash flow from operating activities and should not be used as a measure of liquidity. We believe Adjusted EBITDA facilitates operating performance comparisons from period to period and company to company by eliminating potential differences caused by variations in tax positions (such as the impact on periods or companies of changes in effective tax rates or net operating losses) and the age and book depreciation of tangible assets (affecting relative depreciation expense). Because other companies may not calculate Adjusted EBITDA identically to us, our presentation of Adjusted EBITDA may not be comparable to similarly titled measures of other companies. In addition, Adjusted EBITDA is not calculated in the same way that "Consolidated EBITDA" is calculated under the indenture governing the Notes or under the terms of our Senior Credit Facilities. However, Adjusted EBITDA is a commonly used term to compare the operating activities of cable companies.

- (6)

- Adjusted EBITDA margin is a calculation of Adjusted EBITDA as a percentage of total revenues.

2

IFRS Reconciliation of Adjusted EBITDA to Profit from Ordinary Activities

| | Fiscal Year Ended March 31,

| |

|---|

| | 2004

| | 2005

| | 2006

| | 2007

| | 2008

| |

|---|

| | (€ millions)

| |

|---|

| Adjusted EBITDA | | 428.0 | | 408.0 | | 401.3 | | 382.5 | | 457.8 | |

| Depreciation and Amortization | | (364.3 | ) | (297.7 | ) | (220.8 | ) | (246.6 | ) | (294.0 | ) |

| MEP related non-cash Expenses | | (6.7 | ) | (35.4 | ) | (19.2 | ) | (41.8 | ) | (23.0 | ) |

| Restructuring Expenses | | (13.5 | ) | 0.0 | | (6.2 | ) | (14.4 | ) | (1.3 | ) |

| | |

| |

| |

| |

| |

| |

| Profit from Ordinary Activities | | 43.5 | | 74.9 | | 155.1 | | 79.7 | | 139.5 | |

| | |

| |

| |

| |

| |

| |

Consolidated Balance Sheet Data

| | As of March 31,

| |

|---|

| | 2004

| | 2005

| | 2006

| | 2007

| | 2008

| |

|---|

| |

| | (as adjusted)

| | (as adjusted)

| |

| |

| |

|---|

| | (€ millions)

| |

|---|

| | Cash & Cash Equivalents | | 184.7 | | 132.8 | | 225.1 | | 54.1 | | 15.5 | |

| | Other Current Assets | | 240.4 | | 128.0 | | 171.4 | | 162.5 | | 192.1 | |

| | Intangible Assets | | 630.6 | | 582.4 | | 519.7 | | 477.3 | | 431.9 | |

| | Tangible Assets | | 1,028.2 | | 900.5 | | 902.7 | | 986.6 | | 1,086.0 | |

| | Other Non-current Assets | | 6.6 | | 14.5 | | 7.0 | | 25.0 | | 26.8 | |

| | |

| |

| |

| |

| |

| |

| Total Assets | | 2,090.5 | | 1,758.2 | | 1,825.9 | | 1,705.5 | | 1,752.3 | |

| | |

| |

| |

| |

| |

| |

| | Liabilities to Banks/Bondholders | | 1,645.4 | | 1,952.2 | | 1,988.1 | | 1,895.8 | | 1,941.5 | |

| | Other Liabilities | | 524.7 | | 560.8 | | 647.2 | | 706.0 | | 743.4 | |

| | |

| |

| |

| |

| |

| |

| Total Liabilities | | 2,170.1 | | 2,513.0 | | 2,635.3 | | 2,601.8 | | 2,684.9 | |

| | |

| |

| |

| |

| |

| |

| | Subscribed Capital | | 1.0 | | 1.0 | | 1.0 | | 1.0 | | 1.0 | |

| Equity(7) | | (79.6 | ) | (754.8 | ) | (809.4 | ) | (896.3 | ) | (932.6 | ) |

| | |

| |

| |

| |

| |

| |

| Cash Flow Statement Data | | | | | | | | | | | |

| | Cash Flow from Operating Activities | | 354.6 | | 368.6 | | 399.3 | | 360.0 | | 444.7 | |

| | Cash Flow Used in Investing Activities | | (57.9 | ) | (124.7 | ) | (148.1 | ) | (276.4 | ) | (345.5 | ) |

| | Cash Flow Used in Financing Activities | | (280.5 | ) | (295.6 | ) | (158.8 | ) | (254.9 | ) | (137.9 | ) |

- (7)

- According to the update of the IFRIC agenda decision on IAS 39 accounting changes regarding assessing hedge effectiveness of interest rate swaps in a cash flow hedge have been made for the fiscal years ended March 31, 2005, 2006 and 2007. For a detailed description please refer to Note 1.2 in the Notes to the consolidated financial statements of KDG and KDVS under ITEM 17 Financial Statements.

3

Network Data, Subscribers and Revenue Generating Units

| | As of March 31,

| |

|---|

| | 2004

| | 2005

| | 2006

| | 2007

| | 2008

| |

|---|

| | (thousands, except percentages)

| |

|---|

| Homes passed | | 15,300 | | 15,600 | | 15,462 | | 15,333 | | 15,257 | |

| % penetration(8) | | 63 | % | 62 | % | 62 | % | 60 | % | 58 | % |

| Total Subscribers (Homes Connected) | | 9,626 | | 9,640 | | 9,581 | | 9,241 | | 8,884 | |

| —thereof Cable Access Subscribers | | 9,626 | | 9,640 | | 9,581 | | 9,241 | | 8,845 | |

| —thereof Kabel Internet und Phone Subscribers 'Solo'(9) | | n/a | | n/a | | n/a | | n/a | | 39 | |

| Cable Access RGUs (incl. TKS)(10) | | 9,626 | | 9,640 | | 9,597 | | 9,320 | | 8,980 | |

| Digital Video Recorder RGUs (Kabel Digital+) | | n/a | | n/a | | n/a | | 2 | | 60 | |

| Kabel Digital (pay TV) RGUs | | 81 | | 224 | | 479 | | 690 | | 779 | |

| Kabel Internet RGUs | | 5 | | 12 | | 61 | | 179 | | 393 | |

| Kabel Phone RGUs | | 0 | | 0 | | 40 | | 152 | | 361 | |

| | |

| |

| |

| |

| |

| |

| Total RGUs(11) | | 9,712 | | 9,876 | | 10,177 | | 10,343 | | 10,573 | |

| | |

| |

| |

| |

| |

| |

| Upgrade | | | | | | | | | | | |

| Homes Upgraded for 2-way-communication | | n/a | | n/a | | 4,000 | | 8,634 | | 10,901 | |

| Homes Connected Upgraded for 2-way-communication | | n/a | | n/a | | 2,669 | | 5,547 | | 6,577 | |

- (8)

- Number of subscribers at the end of the relevant period as a percentage of the number of Homes passed by KDG's network at the end of the relevant period.

- (9)

- Internet & Phone 'Solo' subscriber: Non-cable television access customers subscribing to Internet & Phone services only.

- (10)

- Includes CATV subscribers plus direct Digital Access customers within our B2B subscriber base.

- (11)

- Revenue generating units (RGU) relate to sources of revenue, which may not always be the same as subscriber numbers. For example, one person may subscribe to two different services, thereby accounting for only one subscriber, but two RGUs.

| | Fiscal Year Ended March 31,

|

|---|

| | 2004

| | 2005

| | 2006

| | 2007

| | 2008

|

|---|

| | (€)

|

|---|

| ARPU(12) | | | | | | | | | | |

| Cable Access(13) | | 7.07 | | 7.19 | | 7.26 | | 7.31 | | 7.79 |

| Kabel Digital+ | | n/a | | n/a | | n/a | | n/a | | 3.33 |

| Kabel Digital (pay TV) | | n/a | | 6.38 | | 6.97 | | 7.71 | | 7.73 |

| Kabel Internet | | n/a | | 26.40 | | 21.08 | | 16.30 | | 14.12 |

| Kabel Phone | | n/a | | n/a | | 27.40 | | 28.02 | | 24.79 |

| | |

| |

| |

| |

| |

|

| Total Blended ARPU(14) | | n/a | | 7.19 | | 7.30 | | 7.64 | | 8.32 |

| | |

| |

| |

| |

| |

|

- (12)

- Average revenue per unit (ARPU) is calculated by dividing the subscription revenue (excluding installation fees) for a period by the average number of RGUs for that period and the number of months in that period.

- (13)

- Does not include TKS.

- (14)

- Total blended ARPU is calculated by dividing Cable Access, Pay TV, Kabel Digital+, Kabel Internet , Kabel Phone and TKS (cable television) subscription revenues (excluding installation fees) for the relevant period by the average number of RGUs for that period and the number of months in the period.

4

Operational Data

| | Fiscal Year Ended March 31,

| |

|---|

| | 2004

| | 2005

| | 2006

| | 2007

| | 2008

| |

|---|

| | (€ millions, except percentages)

| |

|---|

| Cable Access Revenue | | | | | | | | | | | |

| | Subscription Fees | | 817.0 | | 836.8 | | 829.1 | | 833.8 | | 854.1 | |

| | | % of Total Revenues | | 84.9 | % | 83.4 | % | 81.9 | % | 76.3 | % | 71.4 | % |

| | Installation Fees | | 11.1 | | 8.3 | | 5.7 | | 7.0 | | 7.6 | |

| | | % of Total Revenues | | 1.2 | % | 0.8 | % | 0.6 | % | 0.6 | % | 0.6 | % |

| | Other Revenue | | 5.4 | | 5.0 | | 4.5 | | 4.8 | | 5.4 | |

| | | % of total revenues | | 0.5 | % | 0.5 | % | 0.4 | % | 0.4 | % | 0.5 | % |

| | |

| |

| |

| |

| |

| |

| TV/Radio Revenue | | | | | | | | | | | |

| | Analog/Digital Carriage Fees | | 97.0 | | 97.7 | | 99.0 | | 99.6 | | 100.0 | |

| | | % of Total Revenues | | 10.1 | % | 9.7 | % | 9.8 | % | 9.1 | % | 8.4 | % |

| | Playout Facility revenues | | 7.6 | | 6.9 | | 3.4 | | 2.0 | | 1.0 | |

| | | % of Total Revenues | | 0.8 | % | 0.7 | % | 0.3 | % | 0.2 | % | 0.1 | % |

| | Pay TV subscription fees | | 3.5 | | 9.7 | | 27.7 | | 55.6 | | 69.9 | |

| | | % of Total Revenues | | 0.4 | % | 1.0 | % | 2.7 | % | 5.1 | % | 5.8 | % |

| | Other digital revenues | | 0.0 | | 12.1 | | 7.7 | | 5.8 | | 8.8 | |

| | | % of Total Revenues | | 0.0 | % | 1.2 | % | 0.7 | % | 0.5 | % | 0.7 | % |

| | |

| |

| |

| |

| |

| |

| Internet & Phone Revenue(15) | | 1.2 | | 2.8 | | 9.8 | | 56.5 | | 121.4 | |

| | | % of Total Revenues | | 0.1 | % | 0.3 | % | 1.0 | % | 5.2 | % | 10.1 | % |

| | |

| |

| |

| |

| |

| |

| TKS Revenue | | 19.3 | | 23.9 | | 25.2 | | 28.1 | | 28.6 | |

| | | % of Total Revenues | | 2.0 | % | 2.4 | % | 2.6 | % | 2.6 | % | 2.4 | % |

| | |

| |

| |

| |

| |

| |

| Total Revenues | | 962.1 | | 1,003.2 | | 1,012.1 | | 1,093.2 | | 1,196.9 | |

| | |

| |

| |

| |

| |

| |

- (15)

- Fiscal year ended March 31, 2006 was the first year to include revenues from Phone activities.

Exchange Rate Information

The functional and reporting currency of KDG is the Euro.

Foreign currency transactions were converted to Euros at the exchange rate applicable on the date of the transaction. Monetary assets and liabilities denominated in foreign currencies existing as of the balance sheet date are converted to Euros at the exchange rate of the European Central Bank on the balance sheet date. Currency differences resulting from these adjustments are recognized in the consolidated statement of operations.

5

Non-monetary assets and liabilities denominated in foreign currencies existing as of the balance sheet date, which are to be carried at fair value, were converted to Euros at the rate as of the balance sheet date. The Company used the following exchange rates (spot rates):

USD Exchange Rates (in EUR per USD)

| | Average

| | High

| | Low

| | Period-End

|

|---|

| Fiscal Year Ended March 31, | | | | | | | | |

| | 2004 | | 1.1796 | | 1.2630 | | 1.0927 | | 1.2224 |

| | 2005 | | 1.2647 | | 1.3621 | | 1.1947 | | 1.2964 |

| | 2006 | | 1.2117 | | 1.2957 | | 1.1769 | | 1.2104 |

| | 2007 | | 1.2912 | | 1.3318 | | 1.2537 | | 1.3318 |

| | | October | | 1.4227 | | 1.4447 | | 1.4037 | | 1.4447 |

| | | November | | 1.4684 | | 1.4874 | | 1.4423 | | 1.4761 |

| | | December | | 1.4570 | | 1.4741 | | 1.4349 | | 1.4721 |

| | 2008 | | 1.4328 | | 1.5812 | | 1.3453 | | 1.5812 |

| | | January | | 1.4718 | | 1.4895 | | 1.4482 | | 1.4870 |

| | | February | | 1.4748 | | 1.5167 | | 1.4513 | | 1.5167 |

| | | March | | 1.5527 | | 1.5812 | | 1.5196 | | 1.5812 |

| | | July 25, 2008 | | | | | | | | 1.5734 |

GBP Exchange Rates (in EUR per GBP)

| | Average

| | High

| | Low

| | Period-End

|

|---|

| Fiscal Year Ended March 31, | | | | | | | | |

| | 2004 | | 0.6926 | | 0.7196 | | 0.6659 | | 0.6659 |

| | 2005 | | 0.6834 | | 0.7051 | | 0.6626 | | 0.6885 |

| | 2006 | | 0.6823 | | 0.6964 | | 0.6742 | | 0.6964 |

| | 2007 | | 0.6783 | | 0.6942 | | 0.6633 | | 0.6798 |

| | | October | | 0.6961 | | 0.7010 | | 0.6913 | | 0.6973 |

| | | November | | 0.7090 | | 0.7203 | | 0.6924 | | 0.7146 |

| | | December | | 0.7206 | | 0.7348 | | 0.7107 | | 0.7334 |

| | 2008 | | 0.7116 | | 0.7958 | | 0.6740 | | 0.7958 |

| | | January | | 0.7473 | | 0.7600 | | 0.7413 | | 0.7477 |

| | | February | | 0.7509 | | 0.7652 | | 0.7416 | | 0.7652 |

| | | March | | 0.7749 | | 0.7958 | | 0.7605 | | 0.7958 |

| | | July 25, 2008 | | | | | | | | 0.7888 |

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

The risks described below are not the only risks we face. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially affect our business, financial condition or results of operations adversely. See also ITEM 4B Our Business—The Risk Management System for KDG.

6

Risks Relating to Our Business

We operate in highly competitive industries, and competitive pressures could have a material adverse effect on our business.

We face significant competition from established and new competitors. In some instances, we compete against companies subject to less regulation and with better access to financing, more comprehensive product offerings, greater personnel resources, greater brand name recognition and experience or longer-established relationships with regulatory authorities and customers.

Cable Television. We may not be able to successfully compete in the cable television market. This market may also be adversely affected by competition from other means of transmission and entertainment mediums. The market is becoming increasingly competitive, especially as new technologies emerge as viable alternatives.

- •

- Satellite. In particular, we face competition from satellite distribution of free-to-air (FTA) television program streams, which has been gaining market share over recent years. Although data is limited, one satellite competitor source has published data indicating that the market share of satellite distribution increased from 37.2% to 42.6% between end of 2002 and 2007 while the market share of cable television decreased from 55.9% to 53.4% (according to AGF/GfK). In the same period, the number of our basic television access subscribers has declined.

Satellite has a number of competitive advantages over cable: among other things, it has a wider reach, especially in rural areas, and does not charge on-going subscription fees. Although cable television currently benefits from German zoning laws that restrict the installation of satellite dishes in certain areas, and housing association contracts with residents of multi-unit dwellings that frequently prohibit tenants from attaching satellite dishes to their apartments if cable is installed, these zoning laws may be changed in the future. As a result, this might ultimately further intensify competition with satellite providers. The acceptance of satellite dishes and technology to housing associations may also increase in the future.

- •

- Other delivery and entertainment systems. Our market share may also be adversely affected by terrestrial transmission of digital television, other means of TV signal delivery and emerging technologies (e.g. Internet Protocol TV, IPTV and mobile TV). The market share of digital terrestrial television (DTT), which is now available in most of Germany's urban regions and has replaced analog terrestrial broadcasting there, is not significant at present and its program offering is limited to between 12 and 24 programs depending on the region. Nevertheless, demand for digital terrestrial television may increase in the future as it charges no subscription fees, is likely to become more widely available and the price of the receiving equipment is likely to decrease. We expect digital terrestrial television to be a meaningful competitor to cable and satellite. So far, market share of terrestrial TV distribution does not exceed 5% (Source: AGF/GfK 2008). German state media authorities are promoting the switch-over from analog to digital terrestrial television, further promoting increased competition from digital terrestrial television. Improvements are also being made to alternative means of transmission, such as the provision of video signals by providers of digital subscriber line (DSL) services. The leading provider of these IPTV and video-on-demand (VoD) services in Germany is Deutsche Telekom AG (DTAG), which offers these services under the brand T-HOME and has increased marketing efforts. Furthermore, DTAG has currently built a VDSL network in 27 cities and plans to roll out VDSL in further cities. With this premium VDSL/ADSL2+ product offering they intend to reach up to 20 million homes by the end of 2008 according to DTAG's announced plans. DTAG claims that the VDSL network delivers speeds of up to 50 Mbit/s. In addition, other telecommunications network providers, which are regionally focused, also offer IPTV and VoD services, in particular video-over-DSL (VoDSL) services, in selected cities. Furthermore, there

7

are political considerations to free up frequencies currently devoted to broadcasting for mobile, stationary and/or wireless technologies in order to close existing gaps in broadband availability in Germany and to foster competition (the so called 'digital dividend'). Although these services are not yet comparable with the quality, breadth and user convenience of our service, they could develop into a major competitive force in the market for television distribution. Our services also compete to varying degrees with other entertainment media, including home entertainment systems and cinema. The full extent to which these media and alternative technologies will compete effectively with our cable television system may not be known for several years.

- •

- Level 4 operators. We also compete with alternative providers of television and radio signals over cable networks, principally Level 4 operators. As we continue to increase our number of direct customers, particularly within housing associations, we are in direct competition with the Level 4 operators, who for historical reasons are often the traditional providers of services to such customers and have existing contractual relationships with them. Level 4 operators typically enter into contracts with housing associations with an average term of ten to fifteen years, which limits our opportunities to win them as new customers and may hinder our efforts to market our services effectively to housing associations and their tenants. Level 4 operators and housing associations also seek opportunities to build their own Level 3 networks where economically viable hereby disconnecting from our network. Competition from Level 4 operators and housing associations could increase in the future as the industry undergoes ownership changes and potentially consolidates. In addition, Level 4 operators may have certain competitive advantages over our business, including the lack of regulation of their pricing. Over the recent quarters in our footprint Orion Cable (Orion) has formed a large entity by buying several Level 4 operators, i.e. EWT/Bosch (ewt), Tele Columbus GmbH (Telecolumbus) assets from Unity Media in our region and PrimaCom AG (Primacom).

Pay TV product providers. As we seek further subscribers to our new pay TV products, we may effectively be competing with those providers of pay TV products that currently utilize our network to reach their own subscribers, in particular a major pay television provider in Germany. As a consequence, these digital product providers may decide to use alternative distribution platforms, such as satellite, adversely affecting our ability to generate digital carriage fees, which we currently derive from digital product providers for distributing their signals over our network.

Digital playout facility. We face competition with respect to the services provided by our digital playout facility as other regional cable companies, Unity Media and Kabel Baden-Wuerttemberg (Kabel BW), have built their own playout facilities for packaging, encrypting and distribution of their digital television programming. For example, Unity Media phased out the use of our services during 2006 and 2007, Kabel BW started to phase out the use of our services in the first quarter of 2008 and is expected to discontinue using our services by the end of calendar year 2008.

Internet services. The Internet services business in Germany is highly competitive. We compete with companies that provide low-speed and low priced Internet access services over traditional fixed telephone lines as well as Internet access distributed mostly over DSL. The major DSL service provider in Germany is DTAG, the dominant and incumbent fixed-line telephony provider in Germany. We also compete with service providers that use other alternative technologies for Internet access, such as two-way satellite systems, power line connections and various wireless access, including: wireless local area networks (WLAN) or wireless fidelity (WiFi) access, Universal Mobile Telecommunication Services (UMTS), General Packet Radio Services (GPRS), an enlargement of global system for mobile communications (GSM) coverage areas, and point-to-multipoint wireless access. In the future, additional access technologies will be launched that will further increase competition.

Residential telephony market. The market for residential telephony is highly competitive. The fixed-line telephony market is increasingly under pressure from resellers, alternative carriers, declining

8

mobile phone charges and alternative access technologies like Voice over Internet Protocol (VoIP) and Internet telephony offered via DSL or other broadband connections. The German market for residential telephony services is relatively price sensitive and already on a low price level compared by international standards. We expect increasing competition, including price competition, from traditional and non-traditional telephony providers in the future. Most alternative carriers rely on regulated wholesale services from DTAG for their own telephony services. These wholesale services are currently subject to price regulation which commercially limits the ability of alternative carriers to lower prices on retail telephony markets. There can be no assurance that these price regulations or other market regulations will remain in effect.

Failure to control customer churn may adversely affect our business.

Customer churn refers to those customers who stop subscribing to our services. Churn arises mainly as a result of relocation or death of subscribers, price increases and competition. In addition, our customer churn rate may also increase as a result of competition from new technology access platforms or if we are unable to provide satisfactory service to our customers. Any increase in customer churn may lead to both reduced revenues from direct-subscribers, housing associations and Level 4 operators and reduced revenues from broadcasters whose carriage fees are related to the number of subscribers we reach with our network.

We may not be able to renew our existing contracts with Level 4 operators and housing associations upon their expiration on commercially attractive terms, if at all, or attract new subscribers by entering into new contracts with Level 4 operators and housing associations.

The successful implementation of our business strategy depends, in part, upon how successful we are in renewing our existing agreements with Level 4 operators and housing associations on favourable terms upon their expiration or in attracting Level 4 operators and housing associations to enter into new contracts. A number of our largest contracts with Level 4 operators are framework contracts and are due to expire between 2008 and 2012.

Under those framework contracts, the terms and conditions of the signal delivery are set out. These terms and conditions in most cases do not include an obligation of the Level 4 operator to purchase our signal for a certain number of houses. In such cases, the Level 4 operator can choose to disconnect from our signal and obtain their signal from alternative sources, such as a satellite provider, even before the end of the contract term.

Given, that some of these Level 4 operators are also our competitors in certain markets, it is possible, that we will experience continued disconnections from this customer group.

In addition, since 2007 we have been subject to the so called Market 18 (as defined below). This regulation currently limits our pricing flexibility, which may have a negative impact on the extension of existing contracts or new contracts with Level 4 operators.

When existing contracts expire, Level 4 operators and housing associations may attempt to negotiate discounts. Level 4 operators and housing associations may also choose to completely disconnect from our network and obtain their signal from alternative sources, such as a satellite provider. Some Level 4 operators and housing associations have chosen these alternatives in the past.

Our inability to renew our existing Level 4 and housing association contracts or enter into new contracts on commercially favorable terms, if at all, could lead to reduced sales and lower margins and could have a material adverse effect on our business, financial condition and results of operations.

9

Level 4 operators and large housing associations may seek to reduce their signal delivery costs through clustering, which could adversely affect our profitability.

Our subscription fees are based on our published rate card, according to which the standard rates are linked to the number of subscribers per connection point. Our fee schedule provides for higher discounts depending on the number of subscribers aggregated behind one connection point. In addition, Level 4 operators and large housing associations with large subscriber clusters may have a better bargaining position, allowing them to negotiate for discounts on our published rate card or establish their own head-end and disconnect from our network entirely.

If we fail to introduce and establish new or enhanced products and services successfully, our revenues and margins could be lower than expected.

Part of our business strategy is based on the expansion of the products and services we offer, including:

- •

- enhanced digital cable television services, including pay TV channels, pay-per-view, VoD offerings and PVR services;

- •

- Internet services;

- •

- Phone services; and

- •

- other bundled offers consisting of TV, Internet & Phone services.

Digital cable television. KDG has secured and aims to secure TV distribution rights including certain rights for its pay TV offering on a non-exclusive basis. We may not always be able to acquire the targeted rights or acquire them at economically attractive prices in the future. This might have a detrimental effect on our ability to gain and retain pay TV as well as basic cable subscribers.

Internet & Phone. Internet & Phone markets are very competitive and any of the new or enhanced products or services we introduce or have introduced may fail to achieve market acceptance or new or enhanced products or services introduced by our competitors may be more appealing to customers. As a consequence, for example, if our new Internet offering is not successful, our basic cable subscribers may decide to discontinue using our services altogether and choose other TV distribution platforms. This effect could be exacerbated by the fact that customer churn rates are generally higher for Internet & Phone services than for cable television services.

In addition, our Internet & Phone products and services may not generate profits for the time being and we may not be able to recover the investments, such as the costs of network upgrades and marketing expenses, made to launch new products and services. Moreover, these new products and services may result in a decline of ARPU (Average Revenue per Unit) related to those products and services, due to promotional offers that generate less revenue and result in lower margins, and Adjusted EBITDA, due to the costs of implementation, distribution and technology enhancement of such products.

Internet & Phone over broadband cable are relatively new products that might present unknown technological challenges both to our own systems and resources and to those of our suppliers. In connection with the rollout of Internet & Phone we rely on third parties to upgrade the hardware of the end customers and to connect our telephony customers to the German telephony networks. Demand for new products and services might exceed the capacities of these third parties creating a backlog of new customers to be connected and increased lead times which could in turn result in increased customer churn. Further, there can be no assurance that these third parties will meet our expectations with respect to quality and lead times.

10

Our move towards pay television services may erode our ability to generate revenue from carriage fees, as our pay television contracts would typically require us to pay for programs which we then resell to subscribers rather than having content providers pay us for transmission to the broadcaster's subscribers. If we fail to generate greater profits from our pay television subscription revenues than we would have achieved through providing carriage services to other operators, then our results of operations and financial condition, including our liquidity, will be adversely affected.

A number of contracts for access to pay TV programs require us to pay prices for programs based on a guaranteed minimum number of subscribers, notwithstanding a lower number of actual subscribers. Therefore, if we misjudge anticipated demand for programs, the profitability of our business may be impaired.

Consent of Level 4 operators and housing associations to market new products. We need the consent of Level 4 operators and housing associations in order to market our pay TV, Internet & Phone services to their end customers. Such marketing of pay television, Internet or phone access subscriptions is not generally covered by our standard cable television signal delivery agreements. We have entered into agreements permitting us to market our pay TV services directly to end customers with many of the Level 4 operators using our cable television services. With respect to the marketing of our Internet & Phone services we currently have an agreement with different Level 4 operators and a increasing number of housing associations. To the extent that we are unable to amend existing agreements or obtain new agreements with the remaining Level 4 operators and housing associations, we may market our new products and services to our direct end customers only, which may adversely affect the penetration of our new products and services and may make the offering of such new products and services uneconomical.

We rely on DTAG and certain of its affiliates for a significant part of our network.

While we compete with DTAG in a number of areas, we also rely on various long-term agreements with DTAG and certain of its affiliates that are significant to our business, including for the lease of cable duct space for approximately 13% of our cable network as well as the use of fiber optic transmission systems and facility space. In addition, we purchase the electrical power required for the operation of our network through DTAG. Our ability to offer our services to our customers depends on the performance of DTAG and its affiliates of their respective obligations under these arrangements. In particular, we rely on DTAG to provide us with timely access to co-located facilities, especially for the purposes of maintaining and repairing our network and avoiding or rectifying network outages. Our increasing direct competition with DTAG, caused by the introduction and growth of our Internet & Phone products, could potentially have a negative impact on DTAG's performance of its obligations under these arrangements. Our rights under the Service Level Agreements (SLAs) cannot be assigned without the consent of DTAG, other than in exceptional cases, as defined in the SLAs (see ITEM 10C Material Contracts). DTAG has the right to terminate such arrangements in certain circumstances and under certain conditions. For example, if DTAG decides to discontinue using cable ducts carrying our cable without replacing the ducts it may terminate our rights to use the ducts unless we exercise rights to purchase such ducts from DTAG. If DTAG replaces the ducts it must offer us space in the new ducts. If we fail to fulfill our payment obligations or are otherwise in breach of contract under the SLAs, DTAG would be entitled to terminate the SLAs. The termination of any material portion or all of the SLAs by DTAG would seriously affect the value of our network or business. Continuing our business upon such termination would, if possible at all, require a sizeable payment to purchase the relevant facility from DTAG or a sizeable investment to replicate the lost facilities or services and could have a material adverse effect on our business, financial condition or results of operations. In many cases we would not be able to find suitable alternative service providers at comparable cost or within a reasonable timeframe.

11

We will need to lease additional fibre optic transmission capacity to execute our Internet & Phone plan.

As our Internet & Phone customer base grows, we are in the process of leasing additional fibre optic transmission capacity. In two regions (Bavaria and Lower-Saxony), we have one sole supplier for leased lines. In other regions we may have to invest in constructing our own infrastructure to provide these services. Either of these options requires substantial capital expenditure. Furthermore, if the number of subscribers increases faster than anticipated or if the average usage per subscriber exceeds our expectations, we may need to increase our network capacity earlier than planned.

We depend on equipment and service suppliers that may discontinue their products or seek to charge us prices that are not competitive, either of which may adversely affect our business and profitability.

We have important relationships with several suppliers of hardware and services that we use to operate our cable network and systems. In many cases, we have made substantial investments in the equipment or software of a particular supplier, making it difficult for us in the short-term to change supply and maintenance relationships in the event that our initial supplier refuses to offer us favorable prices or ceases to produce equipment or provide the support that our cable network and systems require. If equipment or service suppliers were to discontinue their products or seek to charge us prices that are not competitive, our business and profitability could be materially and adversely affected. Furthermore, we rely upon outside contractors, many of which are small, locally operating companies, to install our Internet & Phone equipment in subscribers' homes. Delays caused by these contractors, or quality issues concerning these contractors, could lead to our customers' dissatisfaction and could produce additional churn or discourage potential new customers.

We may not be able to accurately predict or fulfill customer demand for our digital cable television customer premises equipment ("CPE").

As access to our digital cable television and Internet & Phone offerings requires a set-top box and a modem, respectively, we must accurately predict the number of boxes or modems required to satisfy customer demand for these products. The long lead times between ordering and delivery make it more important to predict and more difficult to fulfill, the customer demand for set-top boxes and modems accurately. We cannot assure that our orders will match actual demand. If we are unable to successfully predict customer demand, we may be faced with a substantial amount of unsold set-top boxes or modems or alternatively missed sales opportunities. In response, we may be forced to rely on additional markdowns or promotional sales to dispose of excess or slow-moving inventory, which could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We do not have guaranteed access to programs and are dependent on agreements with certain program providers, which may adversely affect our profitability.

We do not produce our own content. For the provision of programs distributed via our cable television network we enter into agreements with program providers, such as public and commercial broadcasters or providers of pay TV channels or pay-per-view content, all of these contracts having different durations. We generally derive revenue under these contracts from "carriage fees" or "feed-in fees", in exchange for distributing the programs to our subscriber base. We cannot assure that we will be able to renew our existing contracts with program providers on commercially favorable terms, if at all. In particular, we believe that, as we are dependent upon such carriers for provision of programs in order to attract subscribers, program providers may have considerable power to renegotiate the fees that we charge for carriage of their product. Any lowering of the carriage fees that we receive from program providers would adversely affect our results of operations. In addition, the loss of programs could negatively affect attractiveness of the programming delivered to our subscribers, which could have a material adverse effect on our business and results of operations.

12

We conclude agreements with various broadcasters for our pay TV services. The pricing of such programs differs from the pricing of analog and digital FTA programs in that we pay the digital content providers for the digital programs they provide us at prices that may be affected by our ability to guarantee a minimum audience to such content providers or require us to guarantee a minimum audience generally. In addition, if we do not meet certain subscriber targets with respect to these program contracts within 12 to 18 months after their respective launch, the content providers may have the right to cancel or renegotiate these contracts. In the future, we will need to extend existing licenses and negotiate access to additional programs. Most premium content rights are already held by competing distributors and, to the extent such competitors obtain content on an exclusive basis, the availability of programs to us could be limited. As a consequence, we may be unable to obtain attractive content on favorable terms in the future, if at all which could have a material adverse effect on our business and results of operations. Our inability to obtain attractively priced competitive programs/channels would reduce demand for our existing and planned pay TV services, limiting our ability to maintain or increase revenues from these services.

Failure to reach agreement with owners of copyright protected broadcast content may adversely affect our business.

Until the end of 2006 copyright expenses were governed by two primary contracts. Since January 2007 we have made a conditional payment (i) to VG Media on the basis of a settlement agreement and (ii) to the former parties of the Kabelglobalvertrag on a voluntary basis. VG Media as well as the former parties of the Kabelglobalvertrag in 2007 published tariffs which would lead to significantly higher copyright expenses as compared to the past. Both tariffs are currently subject to arbitration proceedings which VG Media and the former parties of the Kabelglobalvertrag have started against us. In the meantime, we continue to make the above mentioned conditional payments on a voluntary basis. The amounts of these interim payments are less than the amounts that were paid until 2006 under the old contracts and would be payable under the aforementioned tariffs.

Our business is subject to rapid changes in technology and if we fail to respond to technological developments, our business may be adversely affected.

Technology in the cable television and telecommunications industry is changing rapidly. We will need to anticipate and react to these changes and to develop successful new and enhanced products and services quickly enough for the changing market. This could result in the need to make substantial investments in new or enhanced technologies, products or services, and we may not be able to adopt such technology due to insufficient funding to make the necessary capital expenditures or for other reasons, such as technological incompatibility with our systems. In addition, new technologies may become dominant in the future, rendering our current systems obsolete. These include the provision of video signals by DSL providers and also the provision of digital terrestrial television. Some of these technological changes may also be mandated by regulation. Our ability to adapt successfully to changes in technology in our industry and provide new or enhanced services in a timely and cost-effective manner, or successfully anticipate the demands of our customers, will determine whether we will be able to increase or maintain our subscriber base. If we fail to respond adequately to technological changes, we could lose subscribers and, as a result, our business would be materially and adversely affected.

Failure to upgrade or maintain our cable television network or make other network improvements could have a material adverse effect on our operations and impair our financial condition.

Our current assumptions regarding the costs associated with upgrades and maintenance of our cable television network may prove to be inaccurate. In particular, we intend to compete in providing Internet services on the basis of technologies that may be implemented with low costs and without

13

extensive upgrades to our existing network, which may not prove to be feasible on a network-wide basis. If capital expenditure exceeds our projections, for example because of the need to replace aging network components, or our operating cash flow is lower than expected, we may be required to seek additional financing. Our inability to secure additional financing on satisfactory terms (or at all) may adversely affect the maintenance of our cable television network and upgrades and other improvements to the network. This would negatively affect the service we provide to our subscribers, which could result in negative publicity and the loss of subscribers, and adversely affect our ability to attract new subscribers.

In addition, failure of Level 4 operators or housing associations to maintain their own networks could have adverse reputational consequences for us, as customers may assume that we are responsible for maintenance of these networks and may terminate their subscription with us. Any new or enhanced products or services we introduce, including Internet & Phone, may require an upgrade of these local and in-house networks, in which case we may be required to cover a portion, or all, of the costs of such upgrade.

The occurrence of events beyond our control could result in damage to our cable television network and digital playout facility.

If any part of our cable television network is subject to a flood, fire or other natural disaster, terrorism, a power loss or other catastrophe, our operations and customer relations could be materially and adversely affected. In general, our network consists of a large number of independent sub-networks. These sub-networks are usually built in a tree-structure. Although major casualties affecting individual sub-networks should not generally affect the entire network, this cannot be ruled out. Some of our network is built in resilient rings to promote the continuity of network availability in the event of damage to our underground fibers, however, if any ring is cut twice in different locations, transmission signals will not be able to pass through, which could cause significant damage to our business. Disaster recovery, security and service continuity protection measures that we have or may in the future undertake, and our monitoring of network performance, may be insufficient to prevent losses. A substantial part of our cable network is not insured. Any catastrophe or other damage that affects our network could result in substantial uninsured losses.

In case of a breakdown of a satellite transponder or a complete loss of the entire satellite system, our digital playout facility (which transmits signals via satellite to the head ends of our cable network) will be affected, interrupting the distribution of certain channels in the entire network until the transponder or system is fully operational again. Our transponder contract does not provide for back-up transponder capacity in the event of a breakdown of a satellite transponder. The satellite link between our playout facility in Frankfurt am Main/Rödelheim and the head ends is a particularly critical point as any failure of a transponder on this link or loss of control of the relevant satellite may affect all digital channels.

In the event of a power outage in our playout facility we may be unable to serve several or even all of our channels in the entire network even though we have back-up systems in place for most of our technical equipment. In the event of a power outage in our network or other shortage, we usually do not have a back-up or alternative supply source. A power outage in one segment of the network could cause sub-networks to shut down.

In addition, our business is dependent on certain sophisticated critical systems, including our playout facility and billing and customer service systems. The hardware supporting those systems is housed in a relatively small number of locations and if damage were to occur to any of these locations, or if those systems were to develop other problems, it could have a material adverse effect on our business.

14

The security of our encryption system is currently being compromised by illegal piracy.

We use a conditional access system to encrypt TV, radio and data that either form part of our free and pay TV offerings or that are marketed by third parties, such as the above mentioned pay TV operator. A compromised security of the conditional access system might have a negative impact on the revenue generation of such services. As the security of our current conditional access system is believed to be compromised by illegal piracy, we have decided to migrate to a new conditional access system, to be provided by our current supplier Nagravision S.A. (Nagravision). Even though we require Nagravision to provide state-of-the-art security for the new conditional access system, the security of the system could be compromised again by illegal piracy at some point in time.

The installation of a new information technology system and changes to our financial accounting systems and personnel may result in higher costs than expected.

Higher expenses than initially anticipated can occur when assumptions turn out to be unrealistic or wrong regarding high time pressure, problems with data migration, factual change requests during realization, changing ancillary conditions during the development, potential wrong adaptation of business processes or even lack of training related to the new processes.

Our subscriber data may not be representative of our actual results and data.

As subscriber data (contracts, cancellation etc.) is partly entered manually in the systems, eg. by call center agents, process errors may occur. There might also be erroneous subscriber data in the historical data set (previous system migration errors, data entry errors) of the source system. Subscriber figures are reported automatically by data warehouse systems. As no software can be proven to be fault free, system anomalies/errors might affect reported data. Likewise, the extraction of subscriber data out of the source system might extract erroneous data.

We depend on key personnel and may not be able to retain those employees or recruit additional qualified personnel.

As of March 31, 2008, approximately 15% of our workforce were civil servants and still have the right to cease working for us and return to DTAG or its affiliates. An additional approximately 18% of our workforce has the right to return to DTAG or its affiliates until the end of 2008. However, this right can be exercised only under certain circumstances such as corporate restructurings, reorganizations or insolvency.

Strikes or other industrial actions could disrupt our operations or make it more costly to operate our facilities.

We are exposed to the risk of strikes and other industrial actions. Approximately 22% of our employees are members of a labor union. Historically, we have enjoyed good labor relationships and we are committed to maintaining these relationships. We take a constructive approach to union relationships, and have been able to secure the cooperation of the unions and our workforce with regard to significant changes and the process of continuous improvements. We have negotiated various collective bargaining agreements directly with the labor union. These collective bargaining agreements cover the general labor conditions of our employees (other than executives), such as working hours, holidays, termination, provisions and general payment schemes for wages.

In April 2008, we entered into a new 24-month collective bargaining agreement with the labor union representing our unionized employees. As a result, wages for employees increased by 3.7% from June 1, 2008 and will increase another 3.3% from April 1, 2009.

15

U.S. military redeployment may adversely impact our TKS business.

Our TKS business operates a broadband and telephony telecommunications business that mainly serves NATO military bases in Germany. TKS is permitted to build and maintain its networks on U.S. military bases located on premises owned by the Federal Republic of Germany pursuant to agreements with an agency representing the Federal Republic of Germany. In the event that any of the U.S. military bases are vacated, the Federal Republic of Germany may terminate the applicable agreement with TKS. The U.S. military has announced that it is planning to restructure its operations in Germany, which could lead to a significant reduction in the number of American troops stationed in Germany. Any such reduction in U.S. military personnel or the closure of U.S. military bases in Germany would likely have an adverse effect on TKS' results of operations.

Termination of Services for Deutsche Telekom AG (DTAG) may adversely affect our TKS business.

TKS is in discussions to extend the contract with DTAG but there is no assurance an agreement can be reached. If the contract is not extended it would be detrimental to the TKS business.

We are acquiring assets which could potentially deliver less revenue and earnings than anticipated and we may not be able to integrate these assets in a timely manner which may delay the roll out of Internet & Phone and not allow us to recognize anticipated synergies.

The anticipated synergies out of recent acquistions have not yet been validated. As of today the due dilligence as well as the appraisal of financials is still ongoing. Differing network structures and underlying channel allocations could turn out to become major obstacles in the timing of the network upgrade and the roll-out of voice and internet services.

Risks Relating to Regulatory and Legislative Matters

We are subject to significant government regulation which may increase our costs and otherwise adversely affect our business and further changes could also adversely affect our business.

Our existing and planned activities as a cable network operator in Germany (including our Internet & Phone services) are subject to significant regulation and supervision by various regulatory bodies, including state, federal and European Union (EU) authorities. Such governmental regulation and supervision as well as future changes in laws, regulations or government policy (or in the interpretation or enforcement of existing laws or regulations) that affect us, our competitors or our industry, generally strongly influence our viability and how we operate our business. Complying with existing regulations is burdensome and future changes may increase our operational and administrative expenses and limit our revenues. In particular, we are subject to:

- •

- licensing and notification requirements;

- •

- price regulation for certain services that we provide, in particular with respect to carriage fees to broadcasters and fees for the delivery of signals to other operators;

- •

- rules regarding the interconnection of our telecommunications cable network with those of other network operators and, under certain circumstances, the granting of access to our network to competitors or the resale of our services on a wholesale basis;

- •

- requirements that a cable network operator carries certain channels;

- •

- rules relating to data and customer protection, as well as protection of minors;

- •

- rules regarding the allocation of frequencies and analog and digital transmission capacities;

- •

- rules regarding the fair, reasonable and non-discriminating treatment of broadcasters;

16

- •

- rules regarding fair trade and competition;

- •

- rules relating to conditional access systems and application interfaces;

- •

- rules regarding the duty to disclose personal data of our customers to copyright holders in the case of copyright infringements (as of September 1, 2008) and

- •

- other requirements covering a variety of operational areas such as environmental protection, technical standards and subscriber service requirements:

Our business would be materially and adversely affected if there were any adverse changes in relevant laws or regulations (or in their interpretation or enforcement) regarding, for example, the imposition of access or resale obligations, price regulation, interconnection agreements, frequency allocation requirements or the imposition of universal service obligations, or any change in policy allowing more favorable conditions for other operators. Our ability to introduce new products and services may also be affected if we cannot predict how existing or future laws, regulations or policies would apply to such product or service.

In the future, our Internet access and telephony business may be subject to new laws and regulations, the impacts of which are difficult to predict.

Furthermore, the copyright holders, particularly certain collecting societies try to impose an obligation to block URLs if copyright infringements are committed on the underlying web pages. Recently, similar political discussions have developed with respect to mandatory blocking by access providers of illegal content harmful to minors. Any new laws or regulations affecting the Internet, or amendments to or new interpretations of existing laws and regulations to cover Internet related activities, could increase the costs of regulatory compliance to us or force us to change our business practices or otherwise have a material adverse effect on our business.

Under the current regulatory regime based on federal and European legislation, the Federal Network Agency (FNA) is entitled to impose certain obligations on operators of telecommunications networks which have significant market power or which, despite the absence of significant market power, control end user access. Amongst other things, it may impose the obligation on such operators to grant access to, or interconnection with, their telecommunications networks and to offer third parties the re-sale of their telecommunications services on a wholesale basis. Moreover, the prices that operators with significant market power or operators controlling end user access charge to their competitors and customers may be subject to regulation.

In 2003, the European Commission had issued a recommendation identifying a number of markets potentially susceptible to ex-ante regulation. One of these markets concerned broadcasting transmission services to deliver broadcast content to end-users (Market 18). In 2006 the FNA performed an analysis of this Market 18 as periodical part coming to the conclusions described in the next paragraph. At the end of 2007, the European Commission has revised the recommendation and has, inter alia, removed Market 18 from the list of markets warranting special observation. This should have consequences for the review of the market analysis to be performed periodically by the FNA which is due in fall 2008. Depending on the outcome of such analysis, this could lead to less strict regulation. However, it is too early to predict the consequences of such removal of Market 18 as of now.

17

On the basis of the above analysis, the FNA has declared within a regulatory ordinance as of April 2007 that we have significant market power (SMP) in the regional, network-based cable television markets in which we operate. In its decision the FNA has imposed certain remedies for the feed-in market for broadcasters (Einspeisemarkt) and the signal delivery market to Level 4 operators (Signallieferungsmarkt). We have filed complaints against this regulatory ordinance with the competent court. These cases are pending.

These regulatory obligations (remedies) include for our feed-in market:

- (1)

- A transparency obligation with regard to technical specifications, network features, provisional conditions and fees. This information on all different kinds of our feed-in offers must be published for interested parties (but not for the public).

- (2)

- Feed-in fees are subject to ex-post regulation, but there is no obligation to disclose fees in advance to the FNA.

For our signal delivery market to Level 4 operators the remedies include:

- (1)

- An access obligation for the delivery of broadcasting signals to downstream operators (Level 4) for connection point (Übergabepunkt) clusters up to 500 households (Wohneinheiten) including a shared use of connection points. Therefore access to our network cannot be denied to Level 4 operators if technically feasible.

- (2)

- A non-discrimination obligation. Access agreements must be impartial, comprehensible, and adequate and include equal opportunities for all Level 4 operators. Individual deviations are feasible for "objective" reasons only.

- (3)

- A separate accounting obligation: Access prices and internal transfer prices for signal delivery must be configured transparently. On request, sales volumes and revenues of external and internal signal delivery products must be provided to the FNA.

- (4)

- Signal delivery fees are subject to ex post regulation including an obligation to disclose fees in advance to the FNA.

- (5)

- We are obligated to publish a reference offer (Standardangebot) for our signal delivery products to Level 4 operators. The reference offer must include all necessary technical and commercial information including prices and shall enable Level 4 operators to accept such offer without any further negotiations.

Furthermore, in the future, it cannot be ruled out that we may be required to offer our services to third parties for resale on a wholesale basis. Granting such access or interconnection would limit the bandwidth available for us to provide other products and services to customers served by our networks.

The actual and possible future regulation could:

- •

- impair our ability to use our bandwidth in ways that would generate maximum revenue;

- •

- create a shortage of capacity on our networks, which could limit the types and variety of services we seek to provide our customers;

- •

- strengthen our competitors by granting them access and lowering their costs to enter into our markets; and

- •

- have a material adverse impact on our profitability.

18

Due to regulation, we do not have complete control over the prices that we charge to broadcasters or wholesale offers to Level 4 operators, and this may adversely affect our future cash flows and profitability. This may also affect our pricing flexibility for housing associations and subscribers.

In the case of an ex post review of our feed-in or signal delivery fees, the FNA may declare our fees invalid if it finds that they are abusive and may either direct us to adjust our fees or provide for fees that are not abusive. Therefore, we may not be able to enforce future changes to our carriage and signal delivery fees. This may have an adverse impact on our revenues, profitability of new products and services and ability to respond to changes in the cable television market.

We presently utilize a range of rebate or volume-related pricing mechanisms. Due to actual regulation with regard to the feed-in and signal delivery market we may be restricted from imposing or enforcing certain pricing mechanism. There is a potential risk that broadcasters may try to seek help from or initiate review proceedings by the FNA with respect to the carriage fees charged by us. Volume-based discounts reflecting cost savings, one means of avoiding churn to competing infrastructures, are not affected. We cannot entirely rule out the possibility, however, that, if other clauses were subjected to challenge within a regulatory proceeding, these clauses would be found to be unenforceable. In such cases, we could, under certain circumstances, be found liable for fines or damages if these clauses were successfully challenged. This could adversely affect our competitiveness, financial condition and results of operations.

According to the State Broadcasting Treaty, our analog and digital carriage fees are, in addition to the price regulation by FNA mentioned above, subject to certain notification obligations to the state media authorities. The state media authorities are entitled to review whether the prices we apply are restrictive or discriminatory with respect to certain content providers. As a result, we may be further constrained in respect of the pricing models we agree with content providers for both analog and digital products and our results of operations may be adversely affected.

In addition, we are prohibited from charging carriage fees to certain legally privileged radio and television channels operated by non-profit organizations.

We are required to carry certain programs on our network, which may adversely affect our competitive position and results of operations.

We are required to carry certain broadcasting and other channels on our cable system that we might not necessarily carry voluntarily. In the digital range, these must-carry obligations currently apply to the bandwidth equivalent of four analog television channels. It is unclear whether as a consequence of changes in the law currently under discussion, the must-carry obligations will encompass even greater portions of bandwidth in the future. In the analog range, the scope of the "must-carry" obligation varies from state to state. In some states also television channels broadcasted via DTT fall, as asserted by the respective media authorities, within the scope of the must carry obligation, which therefore takes up a significant portion of our analog bandwidth in such states.

We may become subject to more onerous must-carry rules upon a change in the current regulatory regimes. In the case of one federal state (Saarland), this risk has materialized as the state legislator has remodeled the previously more liberal regime in favor of a stricter one. Re-allocation of analog capacity in various German federal states requires at least to reach informal understandings with the competent state media authority, which decreases planning reliability and could have a material adverse effect on our business, considering that both the digitization of a channel earmarked for future transmission of broadcasting or other media content and each network upgrade to establish Internet require a re-allocation of analog capacity.

19

Analog television and radio distribution may be phased out, which may adversely affect our competitive position and could result in increased costs or a loss of revenue.

The German federal and state governments aim at a general switch-over from analog to digital distribution for all terrestrial television distribution platforms. In accordance with the Telecommunications Act and the regulations promulgated thereunder, the FNA is generally required to revoke all allocations of terrestrial frequencies for analog television transmission by 2010, and for analog terrestrial frequency-modulated radio transmission by 2015. Even though the relevant provisions of the Telecommunications Act and related regulations are not directly applicable to us, as the operation of cable television networks, in principle, does not require frequency allocations, we may be required to invest in the exchange of some of our head end equipment as some broadcasters could cease to deliver their signals in analog format. In addition, future legislation or market needs may require us to digitize our entire cable network and may also require a hard switch-over. Recent proposed changes in the law with potential adverse effects on our business aim at the mandatory digitization or even complete switch-off of a specified number of analog channels in the lower frequency spectrum for security reasons (mitigating interference with air traffic etc.). The proposal provides for a digitization or switch-off in steps until the year 2012. It is unclear as of now, to what extent and at which point in time the proposed steps will have to be realized.

The advent of digitization may promote new technologies that compete with us. For instance, although DTT has failed to become a strong competitor in the past, the German federal state media authorities are currently promoting a switch-over from analog to digital terrestrial television. In all regions in which we operate our telecommunications cable networks (Berlin, Brandenburg, Bremen, Lower Saxony, Hamburg, Schleswig-Holstein, Rhineland-Palatinate, Saarland, Bavaria, Mecklenburg-Western Pomerania, Saxony, Saxony-Anhalt and Thuringia) digital terrestrial television is meanwhile available in both metropolitan and rural areas (in some parts of the latter confined to the transmission of public broadcasting channels). Plans announced by the public broadcasters aim for a provision of 90% of the population with their channels via DTT by the end of 2008. The digital terrestrial television therefore covers almost all of the most densely populated metropolitan areas in the regions in which we operate our cable networks. Hence, digital terrestrial television has to some extent and may continue to grow to a new competitive delivery system for television programs. This in turn could adversely affect our results of operations and financial condition.

In addition, we are dependent upon program providers for the provision of programming and, as the market moves towards digital transmission and a multiplication of digital platforms by facility-based and/or non-facility based operators, we may find that we are unable to generate carriage fees for carrying digital programming at similar levels to those we obtain for carrying analog programming, or at all. This could adversely affect our results of operations and financial condition.

Risks Relating to Our Indebtedness and Our Structure

Our high leverage and debt service obligations could materially and adversely affect our business, financial condition or results of operations.