UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: December 31, 2011

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______________ to _______________

Commission file number: 333-138465

| La Cortez Energy, Inc. |

| (Exact name of registrant as specified in its charter) |

| Nevada | | 20-5157768 |

| (State or other jurisdiction of | | (IRS Employer Identification No.) |

| incorporation or organization) | | |

| Calle 67 #7-35, Oficina 409 | | |

| Bogotá, Colombia | | None |

| (Address of principal executive offices) | | (Postal Code) |

Registrant’s telephone number, including area code: (941) 870-5433

Securities registered under Section 12(b) of the Act: None

Securities registered under Section 12(g) of the Act: Common stock, $0.001 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a smaller reporting company. See the definitions of the “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large Accelerated Filer ¨ | Accelerated Filer ¨ |

| Non-Accelerated Filer ¨ | Smaller reporting company x |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

On June 30, 2011, the last business day of the registrant’s most recently completed second fiscal quarter, 30,763,718 shares of its common stock, $0.001 par value per share (its only class of voting or non-voting common equity) were held by non-affiliates of the registrant. The market value of those shares was $14,151,310, based on the last sale price of $0.46 per share of the common stock on that date. For this purpose, shares of common stock beneficially owned by each executive officer and director of the registrant, and each person known to the registrant to be the beneficial owner of 10% or more of the common stock then outstanding, have been excluded because such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of April 10, 2012, there were46,467,849shares of the registrant’s common stock, par value $0.001 per share, issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

| Item Number and Caption | | Page |

| | | |

| Forward-Looking Statements | | 3 |

| | | |

| PART I | | 4 |

| | | | |

| 1. | Business | | 4 |

| 1A. | Risk Factors | | 16 |

| 1B. | Unresolved Staff Comments | | 31 |

| 2. | Properties | | 31 |

| 3. | Legal Proceedings | | 48 |

| 4. | Mine Safety Disclosures | | 48 |

| | | | |

| PART II | | 49 |

| | | | |

| 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | 49 |

| 6. | Selected Financial Data | | 50 |

| 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | | 51 |

| 8. | Financial Statements and Supplemental Data | | 61 |

| 9. | Changes in and Disagreements with Accountants on Accounting, and Financial Disclosure | | 61 |

| 9A. | Controls and Procedures | | 61 |

| | | | |

| PART III | | 62 |

| | | | |

| 10. | Directors, Executive Officers, and Corporate Governance | | 62 |

| 11. | Executive Compensation | | 68 |

| 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | 74 |

| 13. | Certain Relationships and Related Transactions and Director Independence | | 76 |

| 14. | Principal Accountant Fees and Services | | 77 |

| | | | |

| PART IV | | 78 |

| | | | |

| 15. | Exhibits and Financial Statement Schedules | | 78 |

| | | | |

| Financial Statements | | F-1 |

| | | | |

| Glossary of Oil and Gas Terms | | G-1 |

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K, particularly in Item 1, “Business”, and Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 (the Securities Act) and Section 21E of the Securities Exchange Act of 1934 (the Exchange Act). All statements other than statements of historical facts included in this Annual Report on Form 10-K including without limitation statements in the Management’s Discussion and Analysis of Financial Condition and Results of Operations regarding our financial position, estimated quantities and net present values of reserves, business strategy, plans and objectives of our management for future operations, covenant compliance, capital spending plans and those statements preceded by, followed by or that otherwise include the words “believe”, “expects”, “anticipates”, “intends”, “estimates”, “projects”, “target”, “goal”, “plans”, “objective”, “should”, or similar expressions or variations on such expressions are forward-looking statements. We can give no assurances that the assumptions upon which the forward-looking statements are based will prove to be correct and because forward-looking statements are subject to risks and uncertainties, actual results may differ materially from those expressed or implied by the forward-looking statements. There are a number of risks, uncertainties and other important factors that could cause our actual results to differ materially from the forward-looking statements, including, but not limited to, those set out in Part I, Item 1A “Risk Factors” in this Annual Report on Form 10-K. The information included herein is given as of the filing date of this Form 10-K with the Securities and Exchange Commission (“SEC”) and, except as otherwise required by the federal securities laws, we disclaim any obligations or undertaking to publicly release any updates or revisions to any forward-looking statement contained in this Annual Report on Form 10-K to reflect any change in our expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based.

All references in this Form 10-K to “La Cortez Energy,” the “Company,” “we,” “us” or “our” or similar terms are to La Cortez Energy, Inc., and its wholly owned subsidiaries.

PART I

For definitions of certain oil and gas industry terms used in this annual report on Form 10-K, please see the Glossary appearing on page G-1.

Overview of Our Business

We are an international, early-stage oil and gas exploration and production company focusing our business in South America. We have established our corporate headquarters in Bogota, Colombia, and have entered into two working interest agreements, with Petroleos del Norte S.A. (“Petronorte”), a subsidiary of PetroLatina Energy Limited (AIM: PELE), and with Emerald Energy Plc Sucursal Colombia (“Emerald”), a branch of Emerald Energy Plc. (discussed below). In addition, in March 2010, we acquired all of the outstanding capital stock of Avante Colombia S.à r.l. (“Avante Colombia”) from Avante Petroleum S.A. (“Avante”); Avante Colombia currently has a 50% participation interest in, and is the operator of, the Rio de Oro and Puerto Barco production contracts with Ecopetrol S.A. in the Catatumbo region of northeastern Colombia, under an operating joint venture with Vetra Exploración y Producción S.A. (“Vetra”).

Our plan was to build an oil and gas exploration and production company focused in select countries in South America. We concentrated our efforts in Colombia, where we believed good E&P opportunities existed with straightforward oil and gas contracting terms and conditions. Within the spectrum of the oil and gas business, we planned to focus on a blend between exploration and production of hydrocarbons through a variety of transactions. Our plan was to concentrate our efforts on lower risk exploration ventures and then seek to acquire oil and gas production fields to start building our reserves base.

In late 2010 and 2011, access to the credit and financial markets by small to mid-cap oil and gas exploration companies deteioratted considerably. As a result, in 2011, we were unable to access either the capital markets or obtain bank financing to obtain additional financing to fund our operations, which are highly capital intensive due to the costs involved in planning, permitting and drilling wells. While all of our rights flow through the working interest agreements described above, failure to pay our obligations under those agreements will result in a loss of all of our rights under those agreements, including our rights to share in any of the future oil or gas discoveries, should there be any. We anticipate, in the near term, that there will be mandatory capital calls made under these working interest agreements.

Due to this lack of availability to the financial and credit markets, and our historical operating losses, unless we raise additional capital by the end of May 2012, the Company will be required to take, and has been in the process of considering, actions to address this liquidity shortfall. Such actions include: deregistering our common stock under the Securities Exchange Act of 1934 to reduce accounting, auditing, legal and other associated public company costs which will have the adverse result in our stockholders being unable to sell their securities in the over-the-counter market; implementing further headcount reductions,which will make it difficult to operate our business; the sale of all or some of our interests in the Putumayo-4 (Petronorte), Maranta (Emerald), Rio de Oro or Puerto Barco projects at prices which may not reflect market value; the sale of the Company; and the sale of our equity or debt securities at discounted prices. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity” and “Risk Factors—Risks Related to Our Business and Financial Condition”.

Sales to Major Customers

The Company, through its 20% interest share in the agreement with Emerald, sold oil representing 10% or more of total revenues for the years ended December 31, 2011 and 2010 to the customers shown below:

| | | December 31, | | | December 31, | |

| | | 2011 | | | 2010 | |

| HOCOL S.A. | | | 69 | % | | | 50 | % |

| Petrobras International Braspetro BV | | | 19 | % | | | 27 | % |

| Comercializadora International Exportecnicas Ltda. | | | 4 | % | | | 14 | % |

Industry Introduction

The oil and gas industry is a complex, multi-discipline sector that varies greatly across geographies. As a heavily regulated industry, operating conditions are subject to political regimes and changing legislation. Governments can either induce or deter investment in exploration and production, depending on legal requirements, fiscal and royalty structures, and regulation. Beyond the political considerations, exploration and production for hydrocarbons is an extremely risky business with countless perils, both endogenous and exogenous to the core business. Exploration and production wells require substantial amounts of investment and are long-term projects, sometimes exceeding twenty to thirty years. Regardless of the efforts spent on an exploration or production prospect, success is difficult to attain. Even though modern equipment including seismic and advanced software has helped geologists find producing sands and map reservoirs, they do not guarantee any particular outcome. Early oil & gas explorers relied on surface indicators to find reservoirs. Drilling is the only method to determine whether a prospect will be productive, and even then many complications can arise during drilling (e.g., those relating to drilling depths, pressure, porosity, weather conditions, permeability of the formation and rock hardness). Typically, there is a significant probability that a particular prospect will turn-up a dry-well, leaving investors with the cost of seismic and a dry well which during current times can total in the millions of dollars. Even if oil is produced from a particular well, there is always the possibility that treatment, at additional cost, may be required to make production commercially viable. Furthermore, most production profiles decline over time, which hinders any cost-benefit analysis. In sum, oil and gas is an industry with high risks and high entry barriers but significant potential for success.

Oil and gas prices determine the commercial feasibility of a project. Certain projects may become feasible with higher prices or, conversely, may falter with lower prices. Volatility in the pricing of oil, gas, and other commodities has increased during the last few years, and particularly in the last year, complicating the practicability of a proper assessment of revenue projections. Most governments have enforced strict regulations to uphold the highest standards of environmental awareness, thus, holding companies to the highest degree of responsibility and sensibility vis à vis protecting the environment. Aside from such environmental factors, oil and gas drilling is often conducted in populated areas. For a company to be successful in its drilling endeavors, working relationships with local communities are crucial, to promote its business strategies and to avoid any repercussions of disputes that might arise over local business operations.

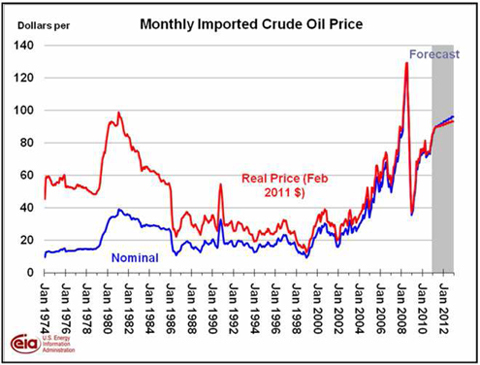

Global Recession, Volatility and Crude Oil Prices

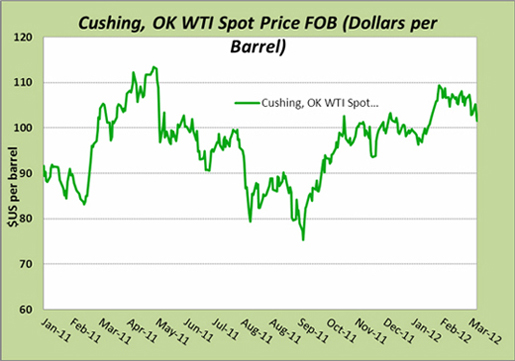

Aside from operational and regulatory issues that affect exploration and production (“E&P”) companies, every major market has been affected by the recent global recession and volatility over the past three years. The energy sector is no exception. West Texas Intermediate (“WTI”) crude prices, the standard oil benchmark for the western hemisphere, tumbled from over $140 per barrel in mid 2008 to less than $40 per barrel in early 2009, before rebounding. The lower price threshold made many previously economically viable opportunities less feasible. More recently, civil unrest and armed conflict in North Africa and the Middle East, relations between the international community and Iran and threats to the oil supply from the Persian Gulf,as well as economic fears regarding some of the European countries have driven oil pricesinto the range of $80 to $110 that prevailed through most of 2011and 2012 to date. Furthermore, the volatility in crude oil prices increases the risks involved. We cannot be sure that the projections we use in evaluating investment opportunities will be valid and in effect as conditions in the oil markets rapidly change. We compensate for this uncertainty by increasing the range of values for our assumptions and by working with numerous sensitivities that might be in line with the situation in the marketplace.

One-Year Daily Spot Price of WTI FOB Cushing, OK (U.S. Dollars per Barrel)*

* Source: U.S. Energy Information Administration

Twenty-Year Monthly Spot Price of WTI FOB Cushing, OK (U.S. Dollars per Barrel)*

* Source: U.S. Energy Information Administration

Inflation-Indexed Monthly Average U.S. Imported Crude Oil Price, January 1974 – January 2012

* Source: U.S. Energy information Administration

The availability of financing alternatives in the equity and debt capital markets, the most common financing vehicles for microcap international E&P companies like ours, has virtually disappearedduring the second half of 2011. The price decline experienced by most, if not all publicly traded microcap/small Colombian E&P companies was on average 42% over last 12 months (April 2011 to March 2012). Financing is now more accessible to companies that have a great base of proven reserves, steady production with some exploration risk, rather than to companies with a high exploration risk, modest production and proven reserves. Companies that are able to secure financing from existing and financially sound investor bases are in a position to take advantage of current business opportunities.

Business Plan and Strategic Outlook

Our initial plan was to build a successful oil and gas exploration and production company focused in select countries in South America. We concentrated our efforts in Colombia, where we believed good E&P opportunities existed with straightforward oil and gas contracting terms and conditions. Within the spectrum of the oil and gas business, we planned to focus on a blend between exploration and production of hydrocarbons through a variety of transactions. Our initial planwas to concentrate our efforts on lower risk explorationventures and later on to seek to acquire oil and gas production fields to start building our reserves base.

An integral part of our strategy has been to focus on building a competent and professional management and operations team that will enable us to successfully carry out our business plan. We have hired experienced personnel including technical specialists (e.g., geologists, geophysicists and petroleum engineers, as required by the scope of our operations), administrators, financial experts and functional specialists in fields such as environment and community relations, to encompass the different areas that are critical to our business. Because the focus of our business is in South America, the majority of our staff has been hired locally and resides in the region, which is consistent with our business plan and provides a significant competitive advantage in the region.

We motivated our employees through a positive, team oriented work environment and an incentive stock ownership plan. We believe that employee ownership, which is encouraged through our Amended and Restated 2008 Equity Incentive Plan, is essential for attracting, retaining and motivating qualified personnel.

We have concentrated our efforts in Colombia and we look at Peru as a potential target. Both countries have similar E&P contract terms and conditions as well as business opportunities that are appropriate for a small, early stage company such as La Cortez Energy. Ourrecent efforts have been concentrated in developing our current asset base as well as looking in obtaining financial support to grow via corporate transactions. We plan to adhere to this strategy, but reserve the option to be flexible if the right opportunity presents itself.

Execution of our Strategy to Date

In February 2008, Nadine C. Smith was appointed Chairman of our Board of Directors (sometimes referred to hereinafter as the “Board”). Ms. Smith was also appointed Interim Chief Financial Officer and Vice President at that time. Ms. Smith most recently served as a director of another publicly traded oil and gas exploration and production company, Gran Tierra Energy, Inc. (“Gran Tierra”), which also operates in South America.

On March 14, 2008, we closed a private placement of our common stock at a price of $1.00 per share pursuant to which we raised $2,400,000, or $2,314,895 net of offering expenses.

On September 10, 2008, we closed a private placement of 4,784,800 units at a price of $1.25 per unit, for an aggregate offering price of $5,981,000, or $5,762,126 after offering expenses. Each of these units consisted of (i) one share of our common stock and (ii) a common stock purchase warrant to purchase one-half share of our common stock, exercisable for a period of five years at an exercise price of $2.25 per share.

On June 1, 2008, Andrés Gutierrez Rivera became our President and Chief Executive Officer and a member of our Board of Directors. Mr. Gutierrez previously served as the senior executive officer of Lewis Energy Colombia Inc. and a vice president of Hocol, S.A. Both of these companies operate in the oil and gas sector in South America.

On June 19, 2009, we conducted an initial closing of a private placement of units. Each unit consisted of (i) one share of our common stock and (ii) a common stock purchase warrant to purchase one share of our common stock, exercisable for a period of five years at an exercise price of $2.00 per share. We offered these units at a price of $1.25 per unit and we derived total proceeds at the initial closing of $6,074,914 ($5,244,279 net after expenses) from the sale of 4,860,000 units. On July 31, 2009, we completed the final closing of this unit offering. At the final closing, we received gross proceeds of $256,250 from the sale of 205,000 units. In the aggregate, we received gross proceeds of $6,331,164 in this unit offering on the sale of a total of 5,065,000 units. This unit offering terminated on July 31, 2009.

In December 2009, January 2010, March 2010 and April 2010, we closed on a private placement offering of units. Each unit was sold at a price of $1.75 and consisted of (i) one share of our common stock, and (ii) a warrant representing the right to purchase one-half (1/2) of one share of our common stock, for a period of three years at an exercise price of $3.00 per whole share. On December 29, 2009, we closed on the sale of 1,428,571 Private Placing Offering (“PPO”) Units (as defined below) in a private placement offering for gross proceeds of $2.5 million; on January 29, 2010, we closed on the sale of 571,428 PPO Units in our PPO, for gross proceeds of $1.0 million; and on March 2, 2010, we closed on the sale of 857,144 in our PPO, for gross proceeds of $1.5 million. On April 19, 2010, we conducted the fourth and final closing of our PPO for an additional 5,905,121 PPO Units, for gross proceeds of $10.33 million. In the aggregate, in all four closings of the PPO, we sold 8,762,264 PPO Units, consisting of an aggregate of 8,762,264 shares of our common stock and warrants to purchase an aggregate of 4,381,138 shares of our common stock, for total gross proceeds of $15.33 million.

In connection with the acquisition of Avante Colombia, on March 2, 2010, Avante purchased (in addition to the shares of common stock issued to Avante in consideration for the acquisition) 2,857,143 shares of our common stock and three-year warrants to purchase 2,857,143 shares of our common stock at an exercise price of $3.00 per share (the “Avante Warrants”), for an aggregate purchase price of $5,000,000, or $1.75 per unit.

(The foregoing discussion does not include warrants issued to brokers and finders as compensation in connection with certain of the offerings.)

The funds raised in the private unit offerings (net of offering expenses) have been used to build our administrative and operations infrastructure and to invest in initial oil and gas development projects in Colombia. In addition, we have taken the following steps to ramp-up growth and development:

| | · | Added the following independent directors to our Board of Directors: Jaime Ruiz Llano, a former Colombian senator and a member of the Board of Directors of the World Bank; Jaime Navas Gaona, an experienced oil industry executive; Richard G. Stevens, an “audit committee financial expert”; and José Fernando Montoya Carrillo, a 27-year veteran of the oil industry in South America and former President of Hocol, S.A; |

| | · | Established a wholly owned subsidiary in the Cayman Islands, La Cortez Energy Colombia, Inc., to own our operating branch in Colombia; |

| | · | Established, organized, and staffed our corporate headquarters in Bogotá, Colombia; |

| | · | Redomiciliated Avante Colombia S.a.r.l from Luxembourg to Cayman Islands and changed its name to Avante Colombia, Inc.; |

| | · | Hired an Exploration Manager, Carlos Lombo, and administrative personnel; |

| | · | Signed a memorandum of understanding and joint operating agreement with one oil and gas exploration and production company in Colombia and a farm-in agreement with another, as further discussed below; |

| | · | Acquired a privately-held company that is the operator of, and owner of a 50% participation interest in, two production contracts with Ecopetrol S.A. in Colombia, as further discussed below; and |

| | · | Have been diligently working to identify, evaluate and finalize our participation in other potential oil and gas investment opportunities in Colombia. |

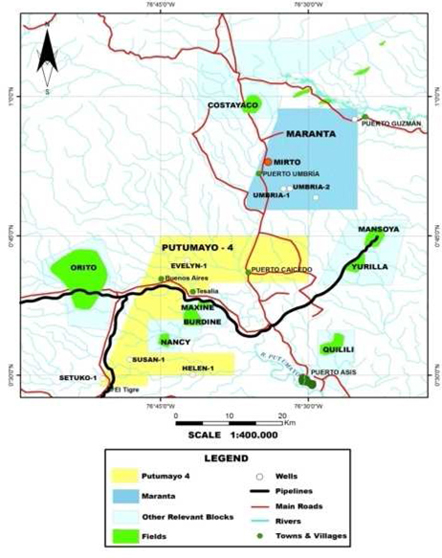

Putumayo 4 Block

The Putumayo 4 Block is an exploration block with no revenues or proven reserves at present. On December 22, 2008, we entered into a memorandum of understanding with Petronorte that entitles us to a 50% net working interest in the Putumayo 4 Block located in the south of Colombia. We executed a related joint operating agreement with Petronorte on October 14, 2009, effective as of February 23, 2009.

Petronorte was the successful bidder on the Putumayo 4 Block in the Colombia Mini Round 2008 conducted by the Agencia Nacional de Hidrocarburos (the “ANH”), Colombia’s hydrocarbon regulatory agency, and signed an E&P contract with the ANH on February 23, 2009. According to our memorandum of understanding and the joint operating agreement with Petronorte, we are entitled to the exclusive right to a fifty percent (50%) net participation interest in the Putumayo 4 Block and in the E&P contract (subject to approval by the ANH), after ANH royalties and an ANH one percent (1%) production participation. Petronorte will be the “operator” of the E&P contract.

The Putumayo 4 Block covers an area of 126,845 acres (51,333 hectares) located in the Putumayo Basin in southern Colombia and has over 1,000 km of pre-existing 2D seismic through which we and Petronorte have identified promising leads. We and Petronorte have reprocessed relevant seismic information that confirmed our initial evaluation of seven potential leads. During this initial stage, we and Petronorte have completed identification of the number of indigenous people and communities in the area, along with representatives from the Ministry of the Interior. A total of seven communities were identified, and the consultation process with these communities has been initiated.An agreement has been reached with four communities. In the southern area, the consultation process is ongoing with two communities. Based on reprocessed seismic information, the layout for the new seismic acquisition has also been completed, resulting in a 2D seismic acquisition plan of some 105 km in the north part of the block, where at least two leads have been determined with the reprocessed seismic. During 2010, we reprocessed approximately 1,000 km of 2D seismic covering the Putumayo-4 Block. During 2012, we plan to conduct two seismic acquisition campaigns. We plan to initiate shooting of the first 105 km of the 2D seismic campaign in April 2012, and the second 2D seismic acquisition of approximately 50 km in May 2012, upon completion of the preconsultation process with the remaining local communities for this acquisition. The preconsultation process was suspended for a period of seven months from December 2010 to July 2011 because no representative from the Colombian Ministry of Interior was available.

Results from the seismic acquisition will permit us to finalize the drill location for the first exploration well. Subject to completion of permitting and civil works at the drill-site, we, together with Petronorte, anticipate spudding the first Putumayo-4 exploration well early in 2013. We and Petronorte are also continuing to work and consult with the local communities to enable us to spud the first exploration well early in 2013. In addition, an Environmental Impact Study (Estudio de Impacto Ambiental - EIA) is ongoing and, when completed, will be presented to the relevant authorities to obtain the necessary exploration well drilling license. We remain optimistic on the potential of this block.

Under the terms of the contract signed with the ANH, we, together with Petronorte, must complete the acquisition of at least 103 km of seismic, the drilling of an exploratory well and additional work for a value of $1.6 million gross before August 25, 2012.We and Petronorte requested from the ANH an extension of the contract for a period of seven months due to problems encountered in the preconsultation process during 2010 and 2011. On February 23, 2012, the ANH approved a seven months and five day extension of the exploration Phase 1. The E&P contract consists of two three-year exploration phases and a twenty-four year production phase.

As criteria for awarding blocks in the 2008 Mini Round, the ANH considered proposed additional work commitments, comprised of capital expenditures and an additional production revenue payment after royalties, called the “X Factor.” In regards to capital expenditures, we and Petronorte offered to invest $1.6 million in additional seismic work in the Putumayo 4 Block, which we plan to accomplish with the seismic program anticipated during April and May 2012. Then, in regards to the “X Factor” mentioned above, we and Petronorte offered to pay ANH a 1% of net production revenues.

Under the memorandum of understanding and the joint operating agreement with PetroNorte, we will be responsible for fifty percent (50%) of the costs incurred under the E&P contract, entitling us to fifty percent (50%) of the revenues originated from the Putumayo 4 Block, net of royalty and production participation interest payments to the ANH, except that we will be responsible for paying two-thirds (2/3) of the costs originated from the first 103 kilometers of 2D seismic to be performed in the Putumayo 4 Block, in accordance with the expected Phase 1 minimum exploration program under the E&P contract. If a prospective Phase 1 well in a prospect in the Putumayo 4 Block proves productive, Petronorte will reimburse us for its share of these seismic costs paid by us (one-sixth (1/6)) with their revenues from production from the Putumayo 4 Block. We expect that our capital commitments to Petronorte will be approximately $4.6million in 2012 for Phase 1 seismic reprocessing, seismic acquisition and permitting activities. The drilling of the referred well was deferred to the first quarter of 2013.

Petronorte filed a request with the ANH for the official assignment of the 50% working interest in the Putumayo-4 block to La Cortez and is obligated to assist La Cortez Energy in obtaining assignment of its working interest from the ANH through reasonable means.The ANHhas recently informed Petronorte that it requires La Cortez to provide an additional financial guarantee. We are evaluating various options to decide whether to provide the additional guarantee or submit a new request later in 2012.In the event that ANH will not approve the assignment, La Cortez will continue to be a private working interest party under the agreement with Petronorte.

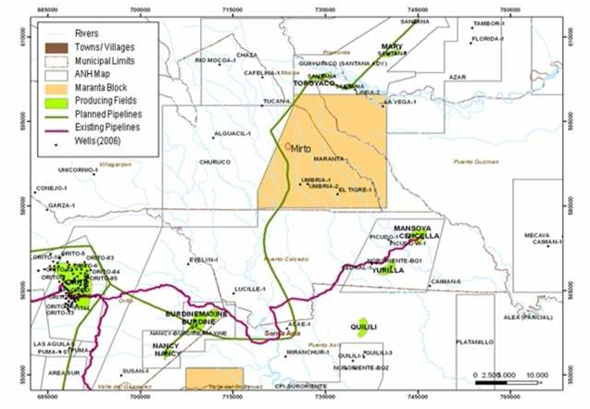

Maranta Block

The Maranta Block was our original entry into our oil and gas business, and all revenue and proved oil reserves from inception through December 31, 2011 are associated with this block. On February 6, 2009, La Cortez Energy Colombia, Inc., our wholly owned Cayman Islands operating subsidiary (“La Cortez Colombia”), entered into a farm-in agreement with Emerald for a 20% participating interest in the Maranta E&P block in the Putumayo Basin in Southwest Colombia.

Emerald signed an E&P contract for the Maranta Block with the ANH on September 12, 2006. La Cortez Colombia executed a joint operating agreement with Emerald with respect to the Maranta Block on February 4, 2010, having met its Phase 1 and Phase 2 (drilling and completion of the Mirto-1 exploratory well) payment obligations described below. Under the farm-in agreement and the joint operating agreement, Emerald will remain the operator for the block. If the ANH does not approve the assignment of this participating interest to us, we, together with Emerald, have agreed to use our best endeavors to seek in good faith a legal way to enter into an agreement with terms equivalent to the farm-in agreement and the joint operating agreement, that shall privately govern the relations between the parties with respect to the Maranta Block and which will not require ANH approval.

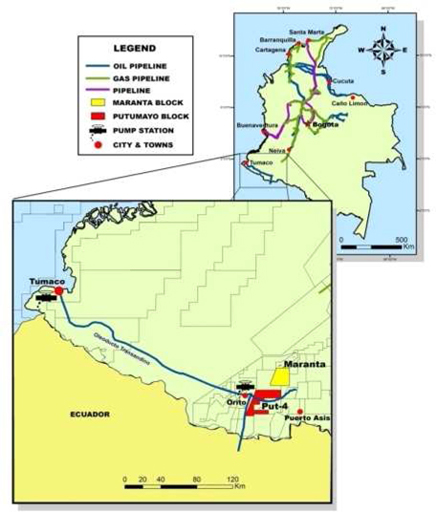

The Maranta Block covers an area of 90,459 acres (36,608 hectares) in the foreland of the Putumayo Basin in southwest Colombia. Emerald completed the first phase exploratory program for the Maranta Block by acquiring 71 square kilometers of new 2D seismic and reprocessing 40 square kilometers of existing 2D seismic, identifying several promising prospects and leads. Emerald identified the Mirto prospect, namely the Mirto-1 well, as the first exploratory well in the Maranta Block. The Maranta Block is adjacent to Gran Tierra’s Chaza block and close to both the Orito and Santana crude oil receiving stations, allowing transportation by truck directly to either station (depending on going rates and capacity), and consequently tying into the pipeline to Colombia’s Pacific Ocean port at Tumaco.

As consideration for its 20% participating interest, we reimbursed Emerald in 2009 $7.28 million of its Phase 1 sunk costs. In 2010, we paid an additional $1.1 million to Emerald, to cover exploration costs associated with the Mirto-1 well, as well as $5.09 million for several projects such as appraisal seismic, drilling of the Mirto-2 well, production facilities and operating costs. In 2011, we paid an additional $1.69 million for activities such as workover of Mirto-1 well and operating costs.

Emerald reached the intended total depth of 11,578 feet on the Mirto-1 exploration well in July 2009, with oil and gas shows recorded across the four target reservoirs. Following the completion of operations in the Mirto-1 well, the drilling rig was released from the location. On July 23, 2009, based on the preliminary results of the drilling of the Mirto-1 well, we decided to participate with Emerald in the completion and evaluation of Mirto-1. In accordance with the terms of the farm-in agreement, we have borne 65% ($1.2 million) of the $1.8 million Mirto-1 completion costs. We made this $1.2 million payment to Emerald on July 27, 2009. Additional Phase 2 costs were paid by us as needed, following cash calls by Emerald, as follows: $948,044 for seismic on the Mirto-1 well (equivalent to 60% share) and $7,440,354 for drilling cost on the Mirto-1 well (equivalent to 65% share), totaling $8,388,398. With Phase 2 work completed, we will pay 20% of all subsequent costs related to the Maranta Block.

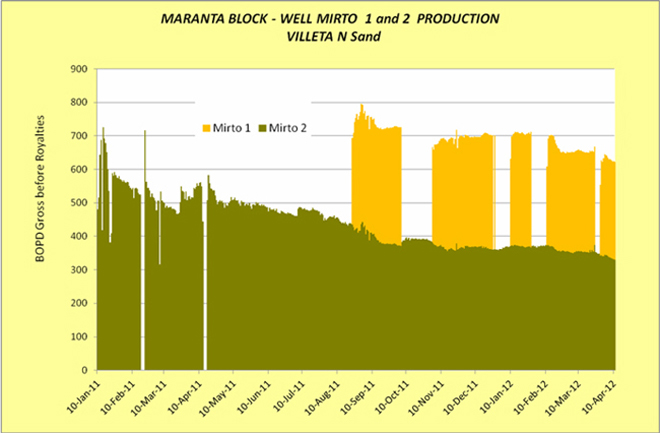

During production testing on Mirto-1, the Villeta N sand interval produced an average oil rate of 247 bopd of 15 degree API oil under artificial lift over a 48 hour period (average water cut of 64%), and the Villeta U sand produced 32 degree API oil at an average rate of 731 bopd (average water cut of 26%) during the same production test. After an unsuccessful workover attempt to isolate the water production, the Mirto-1 well production decreased to an average rate of 60 bopd exclusively from the U sand with water cut close to 90%. Subsequently, the Mirto-1 well was shut in on September 27, 2010, due to mechanical problems, pending evaluation of the technical and operational feasibility to be completed in the Villeta N sand formation.

Emerald, as operator of the Maranta Block, decided to enter the exploration commitment in the Maranta Block, which entailed the drilling of an additional exploratory/appraisal well, Mirto-2. We, together with Emerald, acquired about 25 km of 3D seismic in the area. Emerald completed drilling operations of the Mirto-2 exploratory well on August 15, 2010, after having conducted a sidetrack on the well to a “measured depth” (“MD”) of 11,590 feet. Mirto-2 production tests initiated on September 23, 2010 for a 5-day period on the Villeta U sand had an average production of 29 bopd and water cut of 95.9%. The well was put back on an extended production test from October 16, 2010 until December 10, 2010. During that period, the well produced on average 89.08 bopd gross with an average water cut of 88.4%.

The workover rig on Mirto-2 was used to run cased-hole logs to confirm the appropriate perforation positions. This activity was completed on January 2, 2011, and after N Sand production testing was initiated on January 9, 2011, the well has been on production since then with the following results: Average oil production over the testing period (January 9, 2011 to December 31, 2011) was 450 bopd gross (90 bopd net to La Cortez before royalties) with an average Base Sediment and Water (BS&W) of 0.57% over the same period. Cumulative oil gross production from Mirto-2 is 197,010 bbls from the N reservoir as of April 10, 2012.

On August 23, 2011 the Mirto-1 well was put back in production from the Villeta N sand formation. The well has been on production since August 23rd, 2011 having an ESP (Electric Submersible Pump) failure in early October, which was corrected during the month, in addition to other minor mechanical problems during this year, which were corrected in the same month. The well has showed an average rate of 330 bopd gross (66 bopd net to La Cortez before royalties). The well will continue to be produced under a long term test. The table below summarizes the Mirto Field production and production on a gross basis and net to our interest (after royalties).

| Cumulative Production Mirto-1 | |

| | |

| Formation | | Date | | | Total Fluids

(bls) | | | Oil (bls)

Gross | | | Oil net after

royalties (bls) | |

| Test U, T, N | | | August 9, 2009 | | | | September 29, 2009 | | | | 8,969 | | | | 4,173 | | | | 768 | |

| Sandstone U | | | October 1, 2009 | | | | September 17, 2010 | | | | 210,995 | | | | 41,514 | | | | 7,639 | |

| Sandstone N | | | August 23, 2011 | | | | December 31, 2011 | | | | 30,769 | | | | 32,971 | | | | 6,067 | |

| Sandstone N | | | January 1, 2012 | | | | April 10, 2012 | | | | 23,738 | | | | 23,063 | | | | 4,244 | |

| TOTAL | | | | | | | | | | | 274,471 | | | | 101,721 | | | | 18,718 | |

| Cumulative Production Mirto-2 | |

| | |

| Formation | | Date | | | Total Fluids

(bls) | | | Oil (bls)

Gross | | | Oil net after

royalties (bls) | |

| Sandstone U | | | September 24, 2010 | | | | December 31, 2010 | | | | 46,221 | | | | 5,281 | | | | 972 | |

| Sandstone N | | | January 9, 2011 | | | | December 31, 2011 | | | | 158,775 | | | | 160,658 | | | | 29,561 | |

| Sandstone N | | | January 1, 2012 | | | | April 10, 2012 | | | | 36,465 | | | | 36,352 | | | | 6,689 | |

| TOTAL | | | | | | | | | | | 241,461 | | | | 202,291 | | | | 37,222 | |

| Cumulative Production Mirto Field (Mirto-1 and Mirto-2) | |

| | |

| Date | | Total Fluids

(bls) | | | Oil (bls)

Gross | | | Oil net after

royalties (bls) | |

| October 1, 2009 | | April 10, 2012 | | | 515,932 | | | | 304,012 | | | | 55,940 | |

| TOTAL (bbl) | | | 515,932 | | | | 304,012 | | | | 55,940 | |

Emerald, as operator of the Block, has received authorization from the Colombian Ministry of Mines to continue production from the well under a long-term test. This period will be used to conduct well pressure testing and to gather other information that will be used to define the potential of this reservoir and to optimize production rates.

With the drilling of the Mirto-2 well, Phase 3 of the exploration program has been completed. Both Emerald and La Cortez have complied with the exploration obligations on this block in accordance with the contract signed with the ANH. Under the contract terms and conditions, and after completion of this phase, both La Cortez and Emerald are required to relinquish 50% of the area of the block, as selected by both parties, and the option to continue exploration activities in the remaining 50% of the area was exercised by committing to additional exploration activities with the ANH, such as new seismic acquisition or drilling a new exploration well. This is a normal procedure and in accordance with the contracts entered into with the ANH.

Emerald presented to the ANH the area to be relinquished along with the work commitments to be conducted in the remaining area of the Maranta Block during the first additional exploration phase. The work commitment suggested in for Phase 1 is either a new seismic acquisition (120 km of 2D seismic) or the drilling of an exploration well, which have been accepted by the ANH. The Agapanto-1 well was presented to the ANH to comply with activity required under Phase 1. Emerald is expecting an answer from the ANH before May 2012. If the drilling of the Agapanto-1 well is not approved as an activity commitment for the additional exploration phase, the Company and Emerald plan to carry on with seismic acquisition.

Emerald filed a request with the ANH for the assignment of the 20% working interest in the Maranta Block to La Cortez. To qualify as a contractor with ANH, we have submitted legal, operating, technical and financial information to be reviewed by ANH. Because the financial information required audited financial statements for the last three years, the ANH granted La Cortez until April 15, 2011 to present the 2010 audited financial statements along with other financial information required. Accordingly, we submitted the audited financial statements and the ANH initiated the review process for the assignment to La Cortez of the 20% participation interest in the contract. However, the ANH denied the assignment of the 20% to La Cortez Energy because our financial indicators did not comply with the minimum requirements set out by the ANH, mainly arising from the classification of derivative warrants instruments as a current liability in the Company’s balance sheet under US GAAP (Generally Accepted Accounting Principles) rules. The Company will ask Emerald to present an application for assignment to the ANH once our financial condition meets the ANH criteria. In the meantime, La Cortez will continue to be a private interest holder under agreement with Emerald.

The activity plan for 2012 includes the drilling of the Agapanto 1 well, which is located 1.7 km south of Mirto-1 and Mirto-2, the construction of permanent production facilities, the potential acquisition of additional seismic and a workover on the Umbria-1 well, which is contingent on obtaining the required permits. The Umbria-1 well was drilled in the Maranta Block in 1967 and encountered oil in the Villeta formation. The drilling of the Agapanto-1 well or the acquisition of additional seismic must be executed before the end of the additional phase 1 exploration (by the end of August of 2012). The activity budget for 2012 in this block is $4.97 million, excluding the contingent items such as the seismic and the Umbria workover.

Both Emerald and La Cortez believe that based on the testing results from the Mirto-2 well, and despite the mechanical problems encountered in the Mirto-1 well, there could be sufficient accumulation of hydrocarbons in the area to merit the proposed work commitments.

On March 22, 2012, Emerald submitted to the ANH the report of the evaluation program and declaration of commerciality of the Mirto field. ANH approval is currently pending.

Rio de Oro and Puerto Barco Fields

On March 2, 2010, we acquired all of the outstanding capital stock of Avante Colombia, which became our wholly owned subsidiary. The Rio de Oro and Puerto Barco fields are production projects, the costs of which are currently classified as unproved properties. As consideration for the acquisition, we issued an aggregate of 10,285,819 shares of our common stock to the Avante shareholders.

Avante Colombia currently has a 50% participation interest (acquired in late 2005) in, and is the operator of, the Rio de Oro and Puerto Barco production contracts with Ecopetrol S.A. in the Department of North Santander in the Catatumbo region of northeastern Colombia, under an operating joint venture with Vetra. The Rio de Oro field covers 5,590 acres (2,262 hectares), and the Puerto Barco field covers 5,945 acres (2,406 hectares). Both production contracts are for a ten-year term expiring at the end of 2013.

The Catatumbo basin is the southern-most extension of the Maracaibo basin of Venezuela, the second most prolific basin in the world according to the US Department of Energy and Petroleos de Venezuela. This sub-basin has produced over 800 million barrels of oil to-date from numerous fields.

Under the Puerto Barco production contract, Ecopetrol has a 6% participation in production, Vetra a 47% participation in production and a 50% working interest, and Avante Colombia a 47% participation on production and a 50% working interest, in each case after royalties. Royalties payable are 20% of audited production. The operator is Avante Colombia. Production on the field began in 1958 and was stopped in July 2008, as a result of insurgent activity. Total historical production was 811,000 barrels of oil.

Under the Rio de Oro production contract, Ecopetrol has a 12% production participation, Vetra a 44% production participation and a 50% working interest, and Avante Colombia a 44% production participation and a 50% working interest, in each case after royalties. Royalties payable are 20% of audited production. The operator is Avante Colombia. Production on the field began in 1950 and was stopped in June 1999, as a result of insurgent activity. Total historical production was 11.3 million barrels of oil and 27,041 million cubic feet of gas.

In the Rio de Oro field, the remediation of certain historical environmental conditions generated prior to our acquisition will be the responsibility of the previous operators. In addition to the contractual responsibility of the previous operators for these liabilities, Avante has agreed in the stock purchase agreement (“SPA”) to indemnify us for 50% of any environmental losses we incur, up to a maximum of $2.5 million.

Under the terms of the SPA, we and Avante have also agreed to pursue certain opportunities in the Catatumbo area on a joint venture basis. If we enter into such a joint venture with Avante, then we would own 70% of the joint venture and commit to pay 70% of the geological and geophysical costs, and Avante would own 30% of the joint venture and commit to pay 30% of the geological and geophysical costs, up to a maximum commitment by Avante of $1,500,000. If the total costs of the venture exceed $5,000,000, then Avante may elect either (a) not to pay any additional costs of the venture and incur dilution of its ownership percent from future payments by us, (b) to continue to pay additional costs of the venture at 30% or (c) to pay a larger proportion of the costs of the venture, in which case Avante’s ownership percent would be increased in proportion to the percentage of total venture costs paid by each party, up to a maximum ownership interest for Avante of 50%.

Our plans with respect to Avante Colombia’s business depend, among other things, on obtaining an extension of the term of the existing contracts between Avante Colombia and Ecopetrol, which expires in December 2013. We believe that, to negotiate a term extension, we will have to commit to additional investment in the area. We are actively engaged with Ecopetrol regarding these issues, but there can be no assurance that we will be able to negotiate a term extension with Ecopetrol or to do so on favorable terms. If we fail to obtain a sufficient extension, or to do so on sufficiently favorable terms, it would have a material adverse effect on our planned operations for Avante Colombia.

Avante Colombia, as operator of the Rio de Oro and Puerto Barco Fields, has completed the technical evaluation of these fields, which is encouraging as to future upside potential. Avante Colombia has also completed the program to re-initiate the Puerto Barco field in conjunction with our joint venture partner Vetra. We have met with representatives from the local communities and with several local and regional government officials, who we believe are supportive of the initiatives to reinitiate operations in the fields.

Avante Colombia has performed a detailed evaluation of the current road conditions, which will allow the Company to determine cost and timing for the necessary road improvements. Our technical evaluation has identified several attractive workover opportunities, andas previously anticipated, the 2011 activity was concentrated on the re-establishment of production in the Puerto Barcofield’s PB-2 well. Activities were carried out at the end of 2011 in this field, and the Company conducted a field evaluation and test of a well. The well test resulted in oil produced at natural flow with 43.3degrees API gravity oil. No further tests were conducted due to lack of production facilities at the site. Despiteoperating conditions in the area remaining challenging due to weather, security and infrastructure constraints, we estimatethat if an agreement is reached with Ecopetrol by May 2012,initiation of future activitycoild start in the second half of this year.The Company continues to work with the communities in the area, and we believe we have developed an excellent relation with the local communities and their leaders.

We have been in discussions with Ecopetrol with regard to contract terms and conditions modifications, and we presented to Ecopetrol a proposal to commit to new investment in the area, which is being evaluated at this time.We expect a definitive resolution on this negotiation during 2012. This plan assumes that the Company will obtain additional funding. If no additional funds are obtained, the Company may be obligated to default on its obligations which may cause the loss of its rights in the agreement.

Governmental Regulation

The oil and gas industry in Colombia is broadly regulated. Rights and obligations with regard to exploration, development and production activities are explicit for each project; economics are governed by a royalty/tax regime. Various government approvals are required for acquisitions and transfers of exploration and exploitation rights, including meeting financial, operational, legal and technical qualification criteria. Oil and gas concessions are typically granted for fixed terms with opportunity for extension.

Colombia

In Colombia, state owned Ecopetrol was formerly responsible for all activities related to the exploration, production, refining, transportation and marketing of oil for export. Historically, all oil and gas exploration and production was governed by agreements granted to local and foreign operators, under Association or Shared Risk Contracts with companies and joint ventures which generally provided Ecopetrol with back-in rights that allowed for Ecopetrol to acquire a working interest share in any commercial discovery by paying its share of the costs for that discovery. Alternatively, exploration and production of certain areas and of those areas relinquished by operators were operated directly by Ecopetrol.

Effective January 1, 2004, the regulatory regime in Colombia underwent a significant change with the formation of the ANH. The ANH is now exclusively responsible for regulating the Colombian oil industry, including managing all exploration areas not subject to a previously existing Association contract and collecting royalty payments on behalf of the Colombian government. The former state oil company, Ecopetrol, maintains title to agreements executed before January 1, 2004 and its own operated exploration, production, refining and transportation activities across the country. It also continues to internationally market its oil related products and has become a direct competitor of private operators in E&P projects.

Ecopetrol is a Mixed Economy company (private and public equity), established as a stock corporation, with a commercial orientation.

In conjunction with this change, the ANH developed a new exploration risk contract that took effect during the first quarter of 2005. This exploration and production contract has significantly changed the way the industry views Colombia. In place of the earlier Association contracts in which Ecopetrol had a direct co-management of the contract together with the associate and an immediate back-in to production, the new ANH agreement provides full risk/reward benefits for the contractor. Under the terms of the contract, the E&P operator retains the rights to all reserves, production and income from any new exploration block, subject to an existing royalty (variable royalty from 8% to 25% depending upon daily production rates) and an additional royalty for the ANH, payable beginning when total production reaches 5 million barrels.

E&P companies have to comply with certain minimum requirements (legal, operational, financial, and technical) to become eligible to be granted an ANH Exploration and Production contract. Companies can also apply for Technical Evaluation Agreements (TEA). Domiciled and non-domiciled oil companies may participate in the various bidding rounds for E&P contracts on and offshore in Colombia. In a bidding round, the companies that offer greater investment programs in the initial exploration phase (Phase 1) and, in some cases, that provide ANH with a higher participation in production will be the ones to be awarded E&P contracts.

Colombia, in the last few years has become very attractive to foreign oil, gas and mining investors as a result of political and regulation stability, perceived good contract terms and conditions and improved security. It is, therefore, a competitive environment for us, with good business opportunities available.

See “Risk Factors” for information regarding the regulatory risks that we face.

Environmental Regulation – Community Relations

Our activities will be subject to existing laws and regulations governing environmental quality and pollution control in the foreign countries where we expect to maintain operations. Our activities with respect to exploration, drilling and production from wells, facilities, including the operation and construction of pipelines, plants and other facilities for transporting, processing, treating or storing crude oil and other products, will be subject to stringent environmental regulation by regional, provincial and federal authorities in Colombia. Such regulations relate to, for example, environmental impact studies, permissible levels of air and water emissions, control of hazardous wastes, construction of facilities, recycling requirements and reclamation standards. Risks are inherent in oil and gas exploration, development and production operations, and we can give no assurance that significant costs and liabilities will not be incurred in connection with environmental compliance issues. There can be no assurance that all licenses and permits which may be required to carry out exploration and production activities will be obtainable on reasonable terms or on a timely basis, or that such laws and regulations would not have an adverse effect on any project that we may wish to undertake.

In some countries in South America, it is usually required for oil and gas E&P companies to present their operational plans to local communities or indigenous populations living in the area of a proposed project before project activities can be initiated. Usually, E&P companies try to benefit the community in which they are operating by hiring local, unskilled labor or contracting locally for services such as workers’ transportation. For La Cortez Energy, working with local communities is an essential part of our work program for the development of any of our E&P projects in the region.

Competition

The oil and gas industry is highly competitive. We face competition from both local and international companies in matters such as acquiring properties, contracting for drilling equipment and securing trained personnel. Many of these competitors have financial and technical resources that exceed ours, and we believe that these companies have a competitive advantage in these areas. Others are smaller, and we believe our technical and managerial capabilities give us a competitive advantage over these companies.

Research and Development

We have not spent any amounts on research and development activities during either of the last two fiscal years.

Employees

We currently have 14 full time employees, all of whom, including our Chief Executive Officer, Andrés Gutierrez, our Exploration Manager, Mr. Carlos Lombo,and our Operations and Production Manager, Luis Eduardo Goyeneche,are based in our corporate headquarters location in Bogotá, Colombia.Our Chairman, Ms. Nadine Smith, is currently acting as our Interim Chief Financial Officer.

We intend to maintain our experienced leadership team of energy industry veterans with direct exploration and production experience in the region combined with an efficient managerial and administrative staff, to enable us to achieve our strategic and operational goals. Our ability to provide continued employment to such individuals is dependent upon our ability to raise additional funds to support our ongoing operations, and we may be forced to implement headcount reductions if we are unable to do so.

Additionally, we strive to maintain a highly competitive assembly of experienced and technically proficient employees, motivating them through a positive, team oriented work environment and our incentive stock ownership plan. We believe that employee ownership, which is encouraged through our 2008 Equity Incentive Plan, is essential for attracting, retaining and motivating qualified personnel.

THIS ANNUAL REPORT ON FORM 10-K CONTAINS CERTAIN STATEMENTS RELATING TO FUTURE EVENTS OR THE FUTURE FINANCIAL PERFORMANCE OF OUR COMPANY. YOU ARE CAUTIONED THAT SUCH STATEMENTS ARE ONLY PREDICTIONS AND INVOLVE RISKS AND UNCERTAINTIES, AND THAT ACTUAL EVENTS OR RESULTS MAY DIFFER MATERIALLY. IN EVALUATING SUCH STATEMENTS, YOU SHOULD SPECIFICALLY CONSIDER THE VARIOUS FACTORS IDENTIFIED IN THIS ANNUAL REPORT ON FORM 10-K, INCLUDING THE MATTERS SET FORTH BELOW, WHICH COULD CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE INDICATED BY SUCH FORWARD-LOOKING STATEMENTS.

RISKS RELATED TO OUR BUSINESS AND FINANCIAL CONDITION

Our operations have resulted in negative cash flows, we are seeking to raise additional funds to fund our operating expenses and capital obligations as soon as possible, which could cause us to have to accept terms that are harmful to our business, dilutive to our stockholders or otherwise disadvantageous to our existing stockholders, and if we are unable to secure additional funding, or enter into a sales agreement, we may be required to significantly scale back our operations, seek protection under the provisions of the U.S. Bankruptcy Code, or discontinue many of our activities which could negatively affect our business and prospects.

As of April 10, 2012, we had cash and cash equivalents of $2,289,010. Our current cash resources are not sufficient to fund our operations.

We have agreed to fund an additional $1.32 million for the acquisition of Phase 1 2D seismic on the Putumayo-4 Block by the end of May, 2012. On the Maranta block, we expect the operator to make a cash call on us by May-June, 2012 of $1.71 million for the drilling of the Agapanto-1 well, and $0.70 million for the construction of production facilities.

Over the remainder of 2012, we expect to use, in addition to the above immediate requirements:

| · | approximately $3.29 million to bear our share of commitments with respect to the Putumayo-4 Block, related to Phase 1 seismic acquisition, permitting activities and exploration activities; |

| · | approximately $2.56 million for our share of the costs on the Maranta block for drilling the Agapanto-1 well, which is located 1.7 km south of Mirto-1 and Mirto-2, and the community consultation for the acquisition of additional seismic; |

| · | approximately $0.30 million for community and social programs in the Catatumbo area; and |

| · | up to an additional $4.32 million to cover our administrative expenses and for general working capital to continue to execute our business plan and build our operations, this amount includes a provision for potential strategic transaction costs of $ 0.75 million and approximately $ 0.66 million for tax payments. |

Our total cash capital requirements for the remainder of 2012 are anticipated to be approximately $14.2 million. With our cash and cash equivalents on hand, we will require additional capital by the end of May 2012. We currently do not have any available credit, bank financing or other external sources of liquidity. Due to our brief history and historical operating losses, our operations have not been a source of liquidity.

If we raise additional funds through the issuance of debt securities, these securities would have rights that are senior to holders of our common stock and could contain covenants that restrict our operations. Any additional equity financing would likely be substantially dilutive to our stockholders, particularly given the prices at which our common stock has been recently trading. In addition, if we raise additional funds through the sale of equity securities, new investors could have rights superior to our existing stockholders. This could also result in a decrease in the fair market value of our equity securities because our assets would be owned by a larger pool of outstanding equity. There can be no assurance that we will be successful in obtaining additional funding, in sufficient amounts or on terms acceptable to us, if at all.

If we are unable to raise sufficient additional funds when needed, we would be required to further reduce operating expenses by, among other things, curtailing significantly or delaying or eliminating part or all of our operations and properties, or we may need to seek protection under the provisions of the U.S. Bankruptcy Code.

If we are not able to raise the required funds, we will not be able to meet our funding commitments on the Putumayo-4 Block, the Maranta Block and the Rio de Oro and Puerto Barco fields. As a result, we may lose our interests in these projects and all previously invested capital.

We may have to sell our assets or enter into a transaction upon terms that are disadvantageous to us and which could negatively affect our business and prospects.

We may seek to raise additional funds through the sale of our interests in the Putumayo-4 (Petronorte), Maranta (Emerald), Rio de Oro or Puerto Barco projects, or a sale of the Company. If we raise funds through a farm-out or sale of any of our rights in Putumayo-4, Maranta, Rio de Oro or Puerto Barco projects, we may be required to relinquish, on terms that are not favorable to us, our interests in those projects. Our need to raise capital soon may require us to accept terms that may harm our business or be disadvantageous to our current stockholders, particularly in light of the current illiquidity. There can be no assurance that we will be successful selling or farming-out assets, in sufficient amounts or on terms acceptable to us, if at all. Additionally, our ability to sell or farm-out our rights under our existing joint operating agreements is subject to rights of first refusal or similar rights of our joint venture partners.

We have recorded significant impairments to goodwill and to our oil properties

During 2011, we recorded both a goodwill impairment loss of $5,591,422 (eliminating the goodwill attributed to our acquisition of Avante Colombia in 2010), and an impairment expense on our oil properties of $4,201,385. The circumstances leading to our goodwill assessment and subsequent impairment charges are attributed to the impact of changes in the forecasted results of our business operations, discussions with potential investors regarding possible investments in our securities, our current market capitalization, and as a consequence of proposals from various parties regarding potential corporate strategic transactions.

We assess the carrying value of our unproved properties for impairment periodically. If the results of an assessment indicate that an unproved property is impaired (which was assessed in connection with our evaluation of goodwill impairment), then the carrying value of our unproved properties is added to the proved oil property costs to be amortized and subject to the ceiling test. During the fourth quarter of 2011, we transferred approximately $7.8 million in unproved properties to proved oil properties as a result of this assessment. Subsequent to the transfer, we recorded an impairment expense on our oil properties of $4,201,385 as the unamortized costs for proved oil properties exceeded the cost ceiling limitation.

There is substantial doubt as to the Company’s ability to continue as a going concern.

In the course of our development activities, we have sustained losses and expect such losses to continue through at least the end of April 2013. In addition, during the fourth quarter of 2011, we recorded significant impairments of our oil properties and goodwill.We expect to finance our operations primarily through our existing cash and any future financing. However, there exists substantial doubt about our ability to continue as a going concern for at least the next twelve months, because we will be required to obtain additional capital in the future to continue our operations and there is no assurance that we will be able to obtain such capital, through equity or debt financing, or any combination thereof, or on satisfactory terms or at all. Our independent auditors have included an explanatory paragraph in their report on our consolidated financial statements included in this report that raises substantial doubt about our ability to continue as a going concern. Our audited consolidated financial statements have been prepared in accordance with generally accepted accounting principles applicable to a going concern, which implies we will continue to meet our obligations and continue our operations for the next twelve months. Realization values may be substantially different from carrying values as shown, and our consolidated financial statements do not include any adjustments relating to the recoverability or classification of recorded asset amounts or the amount and classification of liabilities that might be necessary as a result of the going concern uncertainty.

Our long-term business plans and prospects will also require us to obtain additional capital.

We require additional capital to continue to operate our business beyond the initial phase, and we will need additional capital to develop and expand our exploration and development programs. We may be unable to obtain the additional capital required. Furthermore, inability to obtain capital may damage our reputation and credibility with industry participants and government agencies in the event we cannot close previously announced transactionsor meet or ongoing operating commitments under our joint venture agreements.

If our negotiations with Ecopetrol regarding extending the contract terms for Rio de Oro and Puerto Barco are successful, then we expect to require up to $18.5 million of additional funds to pay for our share of costs with respect to additional seismic in the area and, depending upon seismic results, drilling of an additional well during the next three years.

Because we are an early stage exploration and development company with limited resources, we may not be able to compete in the capital markets with much larger, established companies that have ready access to large sums of capital.

We will need to raise additional funds and/or generate cash flow to meet various objectives, including but not limited to:

| · | complying with funding obligations under our existing contractual commitments; |

| · | pursuing growth opportunities, including more rapid expansion; |

| · | acquiring complementary businesses; |

| · | making capital improvements to improve our infrastructure; |

| · | hiring qualified management and key employees; |

| · | responding to competitive pressures; |

| · | meeting administrative requirements (such as salaries, insurance expenses and general overhead expenses, as well as legal compliance costs and accounting expenses) |

| · | complying with licensing, registration and other requirements; and |

| · | maintaining compliance with applicable laws. |

We plan to pursue sources of such capital through various financing transactions or arrangements, including corporate transactions, joint venturing of projects, debt financing, equity financing or other means. We may not be successful in locating suitable financing transactions in the time period required or at all, and we may not obtain the capital we require by other means. Although improving considerably, the turmoil in the world capital markets over the past couple of years has made it difficult for companies to raise funds. If we do succeed in raising additional capital, the capital received may not be sufficient to fund our operations going forward without obtaining further, additional capital financing.

Furthermore, future financings are likely to be dilutive to our stockholders, as we will most likely issue additional shares of our common stock or other equity to investors in future financing transactions. This could also result in a decrease in the fair market value of our equity securities because our assets would be owned by a larger pool of outstanding equity. The terms of securities we issue in future capital transactions may be more favorable to our new investors, and may include preferences, superior voting rights, the issuance of warrants or other derivative securities, and issuances of incentive awards under equity employee incentive plans, which may have a further dilutive effect. In addition, debt and other mezzanine financing may involve a pledge of assets and may be senior to interests of equity holders.

We may incur substantial costs in pursuing future capital financing, including investment banking fees, legal fees, accounting fees, securities law compliance fees, printing and distribution expenses and other costs. We may also be required to recognize non-cash expenses in connection with certain securities we may issue, such as convertible notes and warrants, which will adversely impact our financial condition.

Our ability to obtain needed financing may be impaired by such factors as conditions in the capital markets (both generally and in the oil and gas industry in particular), our status as a new enterprise without a demonstrated operating history, the location of our prospective oil and natural gas properties in developing countries and prices of oil and natural gas on the commodities markets (which will impact the amount of asset-based financing available to us) and/or the loss of key management. Further, if oil and/or natural gas prices on the commodities markets decrease, then our potential revenues will likely decrease, and such decreased future revenues may increase our requirements for capital. Some of the contractual arrangements governing our operations may require us to maintain minimum capital, and we may lose our contract rights (including exploration, development and production rights) if we do not have the required minimum capital. If the amount of capital we are able to raise from financing activities, together with our revenues from operations, is not sufficient to satisfy our capital needs (even to the extent that we reduce our operations), we may be required to cease our operations.

We are an early stage oil and gas exploration and production company with very limited operating history for you to evaluate our business. We may never attain profitability.

We are an early stage oil and gas exploration and production company with very limited oil and no natural gas operations. We do not have a full management team in place. As an early stage oil and gas exploration and development company with very limited operating history, it is difficult for potential investors to evaluate our business. Our proposed operations are therefore subject to all of the risks inherent in light of the expenses, difficulties, complications and delays frequently encountered in connection with the formation of any new business, as well as those risks that are specific to the oil and gas industry and to that industry in South America, in particular. Investors should evaluate us in light of the delays, expenses, problems and uncertainties frequently encountered by companies developing markets for new products, services and technologies. We may never overcome these obstacles.

We may be unable to obtain development rights that we need to build our business, and our financial condition and results of operations may deteriorate.

Our business plan focuses on international exploration and production opportunities in South America, initially in Colombia. Thus far, we have signed two participation interest agreements with partners in Colombia, only one of which (Maranta) is operational, and have acquired one non-producing company (Avante Colombia). In the event that these initial projects do not proceed successfully or we do not succeed in negotiating any other property acquisitions, our future prospects will likely be substantially limited, and our financial condition and results of operations may deteriorate.

Our business is speculative and dependent upon the implementation of our business plan and our ability to enter into agreements with third parties for the rights to exploit potential oil and gas reserves on terms that will be commercially viable for us.

We may not be able to renegotiate Avante Colombia’s agreements with Ecopetrol in a manner that would permit us to successfully execute our plans with respect to the affected projects.

Our plans with respect to Avante Colombia’s business depend, among other things, on our ability to successfully obtain a modification to the terms and conditions of the existing contract between Avante Colombia and Ecopetrol, which expires in December 2013. We believe that to negotiate a change in the contract terms, as well as to acquire additional exploration acreage, we will have to commit to additional investment in the area. There can be no assurance that we will be able to negotiate these items with Ecopetrol or to do so on favorable terms or that we will be able to obtain enough cash to fulfill our commitments. If we fail to obtain sufficient changes to the contract or new exploration acreage, or to do so on sufficiently favorable terms, it would have a material adverse effect on our financial condition and planned operations for Avante Colombia.

Our lack of diversification will increase the risk of an investment in our common stock.

Our business will focus on the oil and gas industry in a limited number of properties, initially in Colombia, with the intention of expanding elsewhere in South America. Larger companies have the ability to manage their risk by diversification. However, we will lack diversification, in terms of both the nature and geographic scope of our business. As a result, factors affecting our industry or the regions in which we operate will likely impact us more acutely than if our business were more diversified.

Strategic relationships upon which we may rely are subject to change, which may diminish our ability to conduct our operations.

Our ability to successfully bid on and acquire properties, to discover reserves, to participate in drilling opportunities and to identify and enter into commercial arrangements with customers will depend on developing and maintaining close working relationships with industry participants and on our ability to select and evaluate suitable properties and to consummate transactions in a highly competitive environment. These realities are subject to change and may impair La Cortez Energy’s ability to grow.

To develop our business, we endeavor to use the business relationships of our management and our Board of Directors to enter into strategic relationships, which may take the form of joint ventures with other private parties or with local government bodies, or contractual arrangements with other oil and gas companies, including those that supply equipment and other resources that we will use in our business. We may not be able to establish these strategic relationships, or if established, we may not be able to maintain them. In addition, the dynamics of our relationships with strategic partners may require us to incur expenses or undertake activities we would not otherwise be inclined pursue to in order to fulfill our obligations to these partners or maintain our relationships. If we fail to make the cash calls required by our joint venture partners in the joint ventures we do not operate, we may be required to forfeit our interests in these joint ventures. If our strategic relationships are not established or maintained, our business prospects may be limited, which could diminish our ability to conduct our operations.