UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

| |

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

or

|

| |

| r | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 1-33100

Owens Corning

(Exact name of registrant as specified in its charter)

|

| | |

| | | |

| Delaware | | 43-2109021 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | |

One Owens Corning Parkway, Toledo, OH | | 43659 |

| (Address of principal executive offices) | | (Zip Code) |

(419) 248-8000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| | | |

| Title of each class | | Name of each exchange on which registered |

| Common Stock, par value $0.01 per share | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No r

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes r No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No r

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No r

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. r

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer þ Accelerated filer r Non-accelerated filer r Smaller reporting company r

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes r No þ

On June 30, 2015, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of $0.01 par value common stock (the voting stock of the registrant) held by non-affiliates (assuming for purposes of this computation only that the registrant had no affiliates) was approximately $4,850,794,039.

As of January 31, 2016, 115,540,535 shares of the registrant’s common stock, par value $0.01 per share, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of Owens Corning’s proxy statement to be delivered to stockholders in connection with the Annual Meeting of Stockholders to be held on April 21, 2016 (the “2016 Proxy Statement”) are incorporated by reference into Part III hereof.

|

| | |

| | | Page |

| | | |

| | |

| | | |

| ITEM 1. | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| ITEM 1A. | | |

| | | |

| ITEM 1B. | | |

| | | |

| ITEM 2. | | |

| | | |

| ITEM 3. | | |

| | | |

| ITEM 4. | | |

| | | |

| | | |

| | | |

| | |

| | | |

| ITEM 5. | | |

| | | |

| ITEM 6. | | |

| | | |

| ITEM 7. | | |

| | | |

| ITEM 7A. | | |

| | | |

| ITEM 8. | | |

| | | |

| ITEM 9. | | |

| | | |

| ITEM 9A. | | |

| | | |

| ITEM 9B. | | |

| | | |

| | |

| | | |

| ITEM 10. | | |

| | | |

| ITEM 11. | | |

| | | |

| ITEM 12. | | |

| | | |

| ITEM 13. | | |

| | | |

| ITEM 14. | | |

| | | |

| | |

| | | |

| ITEM 15. | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

PART I

OVERVIEW

Owens Corning was founded in 1938. Since then, the Company has continued to grow as a market-leading innovator of glass fiber technology. Owens Corning is a world leader in composite and building materials systems, delivering a broad range of high-quality products and services. Our products range from glass fiber used to reinforce composite materials for transportation, electronics, marine, infrastructure, wind-energy and other high-performance markets to insulation and roofing for residential, commercial and industrial applications.

Unless the context indicates otherwise, the terms “Owens Corning,” “Company,” “we” and “our” in this report refer to Owens Corning and its subsidiaries. References to a particular year mean the Company’s year commencing on January 1 and ending on December 31 of that year.

SEGMENT OVERVIEW

The Company has three reporting segments: Composites, which includes our Reinforcements and Downstream businesses; Insulation and Roofing. Our Composites, Insulation and Roofing reportable segments accounted for approximately 35%, 33% and 32% of our total reportable segment net sales, respectively, in 2015.

Note 2 to the Consolidated Financial Statements contains information regarding net sales to external customers and total assets attributable to each of Owens Corning’s reportable segments and geographic regions, earnings before interest and taxes for each of Owens Corning’s reportable segments, and information concerning the dependence of our reportable segments on foreign operations, for each of the years 2015, 2014, and 2013.

Composites

Owens Corning glass fiber materials can be found in over 40,000 end-use applications within five primary markets: building and construction, transportation, consumer, industrial, and power and energy. Such end-use applications include pipe, roofing shingles, sporting goods, consumer electronics, telecommunications cables, boats, aviation, defense, automotive, industrial containers and wind-energy. Our products are manufactured and sold worldwide. We primarily sell our products directly to parts molders and fabricators. Within the building and construction market, our Composites segment sells glass fiber and/or glass mat directly to a small number of major shingle manufacturers, including our own Roofing segment.

Our Composites segment is comprised of our Reinforcements and Downstream businesses. Within the Reinforcements business, the Company manufactures, fabricates and sells glass reinforcements in the form of fiber. Within the Downstream business, the Company manufactures and sells glass fiber products in the form of fabrics, non-wovens and other specialized products.

Demand for composites is driven by general global economic activity and, more specifically, by the increasing replacement of traditional materials such as aluminum, wood and steel with composites that offer lighter weight, improved strength, lack of conductivity and corrosion resistance. We estimate that over the last 30 years, on average, annual global demand for composite materials grew at about 1.6 times global industrial production growth.

We compete with composite manufacturers worldwide. According to various industry reports and Company estimates, our Composites segment is a world leader in the production of glass fiber reinforcement materials. Primary methods of competition include innovation, quality, customer service and global geographic reach. For our commodity products, price is also a method of competition. Significant competitors to the Composites segment include China Jushi Group Co., Ltd., Chongqing Polycom International Corporation Ltd ("CPIC"), Johns Manville, PPG Industries and Taishan Glass Fiber Co., Ltd.

Our manufacturing operations in this segment are generally continuous in nature, and we warehouse much of our production prior to sale since we operate primarily with short delivery cycles.

Insulation

Our insulating products help customers conserve energy, provide improved acoustical performance and offer convenience of installation and use, making them a preferred insulating product for new home construction and remodeling. These products include thermal and acoustical batts, loosefill insulation, foam sheathing and accessories, and are sold under well-recognized brand names and trademarks such as Owens Corning PINK® FIBERGLAS™ Insulation. Our Insulation segment also manufactures and sells glass fiber pipe insulation, energy efficient flexible duct media, bonded and granulated mineral fiber

-2-

|

| |

| ITEM 1. | BUSINESS (continued) |

insulation and foam insulation used in above- and below-grade construction applications. We sell our insulation products primarily to insulation installers, home centers, lumberyards, retailers and distributors in the United States and Canada.

Demand for Owens Corning’s insulating products is driven by new residential construction, remodeling and repair activity, commercial and industrial construction activity, increasingly stringent building codes and the growing need for energy efficiency. Sales in this segment typically follow seasonal home improvement, remodeling and renovation and new construction industry patterns. Demand for new residential construction typically follows on a three-month lagged basis. The peak season for home construction and remodeling in our geographic markets generally corresponds with the second and third calendar quarters and, therefore, our sales levels are typically higher during the second half of the year.

Our Insulation segment competes primarily with manufacturers in the United States. According to various industry reports and Company estimates, Owens Corning is North America’s largest producer of residential, commercial and industrial insulation, and the second-largest producer of extruded polystyrene foam insulation. Principal methods of competition include innovation and product design, service, location, quality, price and compatibility of systems solutions. Significant competitors in this segment include CertainTeed Corporation, Dow Chemical, Johns Manville, and Knauf Insulation.

Our Insulation segment includes a diverse portfolio with a geographic mix of United States, Canada, Asia-Pacific, and Latin America, a market mix of residential, commercial, industrial and other markets, and a channel mix of retail, contractor and distribution.

Working capital practices for this segment historically have followed a seasonal cycle. Typically, our insulation plants run continuously throughout the year. This production plan, along with the seasonal nature of the segment, generally results in higher finished goods inventory balances in the first half of the year. Since sales increase during the second half of the year, our accounts receivable balances are typically higher during this period.

Roofing

Our primary products in the Roofing segment are laminate and strip asphalt roofing shingles. Other products include oxidized asphalt and roofing accessories. We have been able to meet the growing demand for longer lasting, aesthetically attractive laminate products with modest capital investment.

We sell shingles and roofing accessories primarily through home centers, lumberyards, retailers, distributors and contractors in the United States and sell other asphalt products internally to manufacture residential roofing products and externally to other roofing manufacturers. We also sell asphalt to roofing contractors and distributors for built-up roofing asphalt systems and to manufacturers in a variety of other industries, including automotive, chemical, rubber and construction.

Demand for products in our Roofing segment is generally driven by both residential repair and remodeling activity and by new residential construction. Roofing damage from major storms can significantly increase demand in this segment. As a result, sales in this segment do not always follow seasonal home improvement, remodeling and new construction industry patterns as closely as our Insulation segment.

Our Roofing segment competes primarily with manufacturers in the United States. According to various industry reports and Company estimates, Owens Corning’s Roofing segment is the second largest producer of asphalt roofing shingles in the United States. Principal methods of competition include innovation and product design, proximity to customers, quality and price. Significant competitors in the Roofing segment include CertainTeed Corporation, GAF and TAMKO.

Our manufacturing operations are generally continuous in nature, and we warehouse much of our production prior to sale since we operate with relatively short delivery cycles. One of the raw materials important to this segment is sourced from a sole supplier. We have a long-term supply contract for this material, and have no reason to believe that any availability issues will exist. If this supply was to become unavailable, our production could be interrupted until such time as the supplies again became available or the Company reformulated its products. Additionally, the supply of asphalt, another significant raw material in this segment, has been constricted at times. Although this has not caused an interruption of our production in the past, prolonged asphalt shortages would restrict our ability to produce products in this segment.

-3-

|

| |

| ITEM 1. | BUSINESS (continued) |

GENERAL

Major Customers

No one customer accounted for more than 10% of our consolidated net sales for 2015, 2014 or 2013. A significant portion of the net sales in our Insulation and Roofing segments are generated from large United States home improvement retailers.

Intellectual Property

The Company relies on a combination of intellectual property laws, as well as confidentiality procedures and contractual provisions, to protect our intellectual property, proprietary technology and our brands. Through continuous and extensive use of the color PINK since 1956, Owens Corning became the first owner of a single color trademark registration. In addition to our Owens Corning and PINK brands, the Company has registered, and applied for the registration of, U.S. and international trademarks, service marks, and domain names. Additionally, the Company has filed U.S. and international patent applications, including numerous issued patents, covering certain of our proprietary technology resulting from research and development efforts. Over time, the Company has assembled a portfolio of intellectual property rights including patents, trademarks, service marks, copyrights, domain names, know-how and trade secrets covering our products, services and manufacturing processes. Our proprietary technology is not dependent on any single or group of intellectual property rights and the Company does not expect the expiration of existing intellectual property to have a material adverse affect on the business as a whole. The Company believes the duration of our patents is adequate relative to the expected lives of our products. Although the Company protects its intellectual property and proprietary technology, any significant impairment of, or third-party claim against, our intellectual property rights could harm our business or our ability to compete.

Backlog

Our customer volume commitments are generally short-term, and the Company does not have a significant backlog of orders.

Research and Development

The Company’s research and development expense during each of the last three years is presented in the table below (in millions):

|

| | | |

| Period | Research and Development Expense |

| Twelve Months Ended December 31, 2015 | $ | 73 |

|

| Twelve Months Ended December 31, 2014 | $ | 76 |

|

| Twelve Months Ended December 31, 2013 | $ | 77 |

|

Environmental Control

Owens Corning has established policies and procedures to ensure that its operations are conducted in compliance with all relevant laws and regulations and that enable the Company to meet its high standards for corporate sustainability and environmental stewardship. Our manufacturing facilities are subject to numerous foreign, federal, state and local laws and regulations relating to the presence of hazardous materials, pollution and protection of the environment, including emissions to air, discharges to water, management of hazardous materials, handling and disposal of solid wastes, and remediation of contaminated sites. All Company manufacturing facilities operate using an ISO 14001 or equivalent environmental management system. The Company’s 2020 Sustainability Goals require significant global reductions in energy use, water consumption, waste to landfill, emissions of greenhouse gases, fine particulate matter and toxic air emissions. The Company is dedicated to continuous improvement in our environmental, health and safety performance and to achieving its 2020 Environmental Sustainability goals.

The Company has not experienced a material adverse effect upon our capital expenditures or competitive position as a result of environmental control legislation and regulations. Operating costs associated with environmental compliance were approximately $31 million in 2015. The Company continues to invest in equipment and process modifications to remain in compliance with applicable environmental laws and regulations worldwide.

Our manufacturing facilities are subject to numerous national, state and local environmental protection laws and regulations. Regulatory activities of particular importance to our operations include those addressing air pollution, water pollution, waste disposal and chemical control. The Company expects passage and implementation of new laws and regulations specifically

-4-

|

| |

| ITEM 1. | BUSINESS (continued) |

addressing climate change, toxic air emissions, ozone forming emissions and fine particulate matter during the next two to five years. New air pollution regulations could impact our ability to expand production or construct new facilities in certain regions of North America. However, based on information known to the Company, including the nature of our manufacturing operations and associated air emissions, at this time we do not expect any of these new laws, regulations or activities to have a material adverse effect on our results of current operations, financial condition or long-term liquidity.

Owens Corning is involved in remedial response activities and is responsible for environmental remediation at a number of sites, including certain of its currently owned or formerly owned plants. These responsibilities arise under a number of laws, including, but not limited to, the Federal Resource Conservation and Recovery Act (RCRA), and similar state or local laws pertaining to the management and remediation of hazardous materials and petroleum. The Company has also been named a potentially responsible party under the United States Federal Superfund law, or state equivalents, at a number of disposal sites. The Company became involved in these sites as a result of government action or in connection with business acquisitions. At the end of 2015, the Company was involved with a total of 19 sites worldwide, including 6 Superfund sites and 13 owned or formerly owned sites. None of the liabilities for these sites are individually significant to the Company.

Remediation activities generally involve a potential range of activities and costs related to soil and groundwater contamination. This can include pre-cleanup activities such as fact finding and investigation, risk assessment, feasibility studies, remedial action design and implementation (where actions may range from monitoring to removal of contaminants, to installation of longer-term remediation systems). A number of factors affect the cost of environmental remediation, including the number of parties involved in a particular site, the determination of the extent of contamination, the length of time the remediation may require, the complexity of environmental regulations, variability in clean-up standards, the need for legal action, and changes in remediation technology. Taking these factors into account, Owens Corning has predicted the costs of remediation reasonably estimated to be paid over a period of years. The Company accrues an amount on an undiscounted basis, consistent with the reasonable estimates of these costs when it is probable that a liability has been incurred. Actual cost may differ from these estimates for the reasons mentioned above. At December 31, 2015, the Company had an accrual totaling $3 million for these costs. Changes in required remediation procedures or timing of those procedures at existing legacy sites, or discovery of contamination at additional sites, could result in material increases to the Company’s environmental obligations.

Number of Employees

As of December 31, 2015, Owens Corning had approximately 15,000 employees. Approximately 7,000 of such employees are subject to collective bargaining agreements. The Company believes that its relations with employees are good.

AVAILABILITY OF INFORMATION

Owens Corning makes available, free of charge, through its website the Company’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports as soon as reasonably practicable after such material is electronically filed with or furnished to the Securities and Exchange Commission. These documents are available through the Investor Relations page of the Company’s website at www.owenscorning.com.

RISKS RELATED TO OUR BUSINESS AND OUR INDUSTRY

Low levels of residential or commercial construction activity can have a material adverse impact on our business and results of operations.

A large portion of our products are used in the markets for residential and commercial construction, repair and improvement, and demand for certain of our products is affected in part by the level of new residential construction in the United States, although typically not until a number of months after the change in the level of construction. Lower demand in the regions and markets where our products are sold could result in lower revenues and lower profitability. Historically, construction activity has been cyclical and is influenced by prevailing economic conditions, including the level of interest rates and availability of financing, inflation, employment levels, consumer spending habits, consumer confidence and other macroeconomic factors outside our control.

-5-

|

| |

| ITEM 1A. | RISK FACTORS (continued) |

We face significant competition in the markets we serve and we may not be able to compete successfully.

All of the markets we serve are highly competitive. We compete with manufacturers and distributors, both within and outside the United States, in the sale of building products and composite products. Some of our competitors may have superior financial, technical, marketing and other resources than we do. In some cases, we face competition from manufacturers in countries able to produce similar products at lower costs. We also face competition from the introduction by competitors of new products or technologies that may address our customers’ needs in a better manner, whether based on considerations of pricing, usability, effectiveness, sustainability, quality or other features or benefits. If we are not able to successfully commercialize our innovation efforts, we may lose market share. Price competition or overcapacity may limit our ability to raise prices for our products when necessary, may force us to reduce prices and may also result in reduced levels of demand for our products and cause us to lose market share. In addition, in order to effectively compete, we must continue to develop new products that meet changing consumer preferences and successfully develop, manufacture and market these new products. Our inability to effectively compete could result in the loss of customers and reduce the sales of our products, which could have a material adverse impact on our business, financial condition and results of operations.

Our sales may fall rapidly in response to declines in demand because we do not operate under long-term volume agreements to supply our customers and because of customer concentration in certain segments.

Many of our customer volume commitments are short-term; therefore, we do not have a significant manufacturing backlog. As a result, we do not benefit from the hedge provided by long-term volume contracts against downturns in customer demand and sales. Further, we are not able to immediately adjust our costs in response to declines in sales. In addition, although no single customer represents more than 10% of our annual sales, our ability to sell some of the products in Insulation and Roofing are dependent on a limited number of customers, who account for a significant portion of such sales. The loss of key customers for these products, a consolidation of key customers or a significant reduction in sales to those customers, could significantly reduce our revenues from these products. In addition, if key customers experience financial pressure or consolidate, they could attempt to demand more favorable contractual terms, which would place additional pressure on our margins and cash flows. Lower demand for our products, loss of key customers and material changes to contractual terms could materially and adversely impact our business, financial condition and results of operations.

Worldwide economic conditions and credit tightening could have a material adverse impact on the Company.

The Company’s business may be materially and adversely impacted by changes in United States or global economic conditions, including global industrial production rates, inflation, deflation, interest rates, availability of capital, consumer spending rates, energy availability and commodity prices, trade laws, and the effects of governmental initiatives to manage economic conditions. Volatility in financial markets and the deterioration of national and global economic conditions could materially adversely impact the Company’s operations, financial results and/or liquidity including as follows:

| |

| • | the financial stability of our customers or suppliers may be compromised, which could result in reduced demand for our products, additional bad debts for the Company or non-performance by suppliers; |

| |

| • | one or more of the financial institutions syndicated under the credit agreement governing our revolving credit facility may cease to be able to fulfill their funding obligations, which could materially adversely impact our liquidity; |

| |

| • | it may become more costly or difficult to obtain financing or refinance the Company’s debt in the future; |

| |

| • | the value of the Company’s assets held in pension plans may decline; and/or |

| |

| • | the Company’s assets may be impaired or subject to write-down or write-off. |

Uncertainty about global economic conditions may cause consumers of our products to postpone spending in response to tighter credit, negative financial news and/or declines in income or asset values. This could have a material adverse impact on the demand for our products and on our financial condition and operating results. A deterioration of economic conditions would likely exacerbate these adverse effects and could result in a wide-ranging and prolonged impact on general business conditions, thereby negatively impacting our operations, financial results and/or liquidity.

-6-

|

| |

| ITEM 1A. | RISK FACTORS (continued) |

Our level of indebtedness could adversely impact our business, financial condition or results of operations.

Our debt level and degree of leverage could have important consequences, including the following:

| |

| • | our ability to obtain additional debt or equity financing for working capital, capital expenditures, debt service requirements, acquisitions and general corporate or other purposes may be limited; |

| |

| • | a substantial portion of our cash flow from operations could be required for the payment of principal and interest on our indebtedness, and may not be available for other business purposes; |

| |

| • | certain of our borrowings are at variable rates of interest, exposing us to the risk of increased interest rates; |

| |

| • | if due to liquidity needs we must replace any indebtedness upon maturity, we would be exposed to the risk that we may not be able to refinance such indebtedness; |

| |

| • | our ability to adjust to changing market conditions may be limited and place us at a competitive disadvantage compared to our competitors that have less debt; and |

| |

| • | we may be vulnerable in a downturn in general economic conditions or in our business, or we may be unable to carry out important capital spending. |

In addition, the credit agreement governing our senior credit facility, the indentures governing our senior notes and the receivables purchase agreement governing our receivables securitization facility contain various covenants that impose operating and financial restrictions on us and/or our subsidiaries. Additionally, instruments and agreements governing our future indebtedness may impose other restrictive conditions or covenants that could restrict our ability to conduct our business operations or pursue growth strategies.

Adverse weather conditions and the level of severe storms could have a material adverse impact on our results of operations.

Weather conditions and the level of severe storms can have a significant impact on the markets for residential and commercial construction, repair and improvement, which can in turn impact our business as follows:

| |

| • | generally, any weather conditions that slow or limit residential or commercial construction activity can adversely impact demand for our products; and |

| |

| • | a portion of our annual product demand is attributable to the repair of damage caused by severe storms. In periods with below average levels of severe storms, demand for such products could be reduced. |

Lower demand for our products as a result of either of these scenarios could adversely impact our business, financial condition and results of operations. Additionally, severely low temperatures may lead to significant and immediate spikes in costs of natural gas, electricity and other commodities that could negatively affect our results of operation.

Our operations require substantial capital, leading to high levels of fixed costs that will be incurred regardless of our level of business activity.

Our businesses are capital intensive, and regularly require capital expenditures to expand operations, maintain equipment, increase operating efficiency and comply with applicable laws and regulations, leading to high fixed costs, including depreciation expense. Also, increased regulatory focus could lead to additional or higher costs in the future. We are limited in our ability to reduce fixed costs quickly in response to reduced demand for our products and these fixed costs may not be fully absorbed, resulting in higher average unit costs and lower gross margins if we are not able to offset this higher unit cost with price increases. Alternatively, we may be limited in our ability to quickly respond to unanticipated increased demand for our products, which could result in an inability to satisfy demand for our products and loss of market share.

We may be exposed to increases in costs of energy, materials and transportation or reductions in availability of materials and transportation, which could reduce our margins and have a material adverse impact on our business, financial condition and results of operations.

Our business relies heavily on certain commodities and raw materials used in our manufacturing processes. Additionally, we spend a significant amount on natural gas inputs and services that are influenced by energy prices, such as asphalt, a large number of chemicals and resins and transportation costs. Price increases for these inputs could raise costs and reduce our margins if we are not able to offset them by increasing the prices of our products, improving productivity or hedging where

-7-

|

| |

| ITEM 1A. | RISK FACTORS (continued) |

appropriate. In particular, energy prices could increase as a result of climate change legislation or other environmental mandates. Availability of certain of the raw materials we use has, from time to time, been limited, and our sourcing of some of these raw materials from a limited number of suppliers, and in some cases a sole supplier, increases the risk of unavailability. For example, one of the raw materials important to our roofing segment is sourced from a sole supplier, and although we have a long-term supply contract for this material, our production could be interrupted until such time as the supplies again became available or we reformulated our products. Despite our contractual supply agreements with many of our suppliers, it is possible that we could experience a lack of certain raw materials which could limit our ability to produce our products, thereby materially and adversely impact our business, financial condition and results of operations.

We are subject to risks relating to our information technology systems, and any failure to adequately protect our critical information technology systems could materially affect our operations.

We rely on information technology systems across our operations, including for management, supply chain and financial information and various other processes and transactions. Our ability to effectively manage our business depends on the security, reliability and capacity of these systems. Information technology system failures, network disruptions or breaches of security could disrupt our operations, causing delays or cancellation of customer orders or impeding the manufacture or shipment of products, processing of transactions or reporting of financial results. An attack or other problem with our systems could also result in the disclosure of proprietary information about our business or confidential information concerning our customers or employees, which could result in significant damage to our business and our reputation.

We have put in place security measures designed to protect against the misappropriation or corruption of our systems, intentional or unintentional disclosure of confidential information, or disruption of our operations. However, advanced cyber-security threats, such as computer viruses, attempts to access information, and other security breaches, are persistent and continue to evolve making them increasingly difficult to identify and prevent. Protecting against these threats may require significant resources, and we may not be able to implement measures that will protect against all of the significant risks to our information technology systems. In addition, we rely on a number of third party service providers to execute certain business processes and maintain certain IT systems and infrastructure, any breach of security on their part could impair our ability to effectively operate. Moreover, our operations in certain geographic locations may be particularly vulnerable to security attacks or other problems. Any breach of our security measures could result in unauthorized access to and misappropriation of our information, corruption of data or disruption of operations or transactions, any of which could have a material adverse effect on our business.

We are subject to risks associated with our international operations.

We sell products and operate plants throughout the world. Our international sales and operations are subject to risks and uncertainties, including:

| |

| • | difficulties and costs associated with complying with a wide variety of complex and changing laws, including securities laws, tax laws, employment and pension-related laws, competition laws, U.S. and foreign export and trading laws, and laws governing improper business practices, treaties and regulations; |

| |

| • | limitations on our ability to enforce legal rights and remedies; |

| |

| • | adverse economic and political conditions, business interruption, war and civil disturbance; |

| |

| • | tax inefficiencies and currency exchange controls that may adversely impact our ability to repatriate cash from non-United States subsidiaries; |

| |

| • | the imposition of tariffs or other import or export restrictions; |

| |

| • | costs and availability of shipping and transportation; |

| |

| • | nationalization of properties by foreign governments; and |

| |

| • | currency exchange rate fluctuations between the United States dollar and foreign currencies. |

As we continue to expand our business globally, we may have difficulty anticipating and effectively managing these and other risks that our international operations may face, which may adversely impact our business outside the United States and our business, financial condition and results of operations.

In addition, we operate in many parts of the world that have experienced governmental corruption and we could be adversely affected by violations of the Foreign Corrupt Practices Act (“FCPA”) and similar worldwide anti-corruption laws. The FCPA

-8-

|

| |

| ITEM 1A. | RISK FACTORS (continued) |

and similar anti-corruption laws in other jurisdictions generally prohibit companies and their intermediaries from making improper payments to officials for the purpose of obtaining or retaining business. Although we mandate compliance with these anti-corruption laws and maintain an anti-corruption compliance program, we cannot provide assurance that these measures will necessarily prevent violations of these laws by our employees or agents. If we were found to be liable for violations of anti-corruption, we could be liable for criminal or civil penalties or other sanctions, which could have a material adverse impact on our business, financial condition and results of operations.

The Company’s income tax net operating loss carryforwards may be limited and our results of operations may be adversely impacted.

The Company has substantial deferred tax assets related to net operating losses (“NOLs”) for United States federal and state income tax purposes, which are available to offset future taxable income. However, the Company’s ability to utilize or realize the current carrying value of the NOLs may be impacted by certain events, such as changes in tax legislation or insufficient future taxable income prior to expiration of the NOLs or annual limits imposed under Section 382 of the Internal Revenue Code, or by state law, as a result of a change in control. A change in control is generally defined as a cumulative change of 50% or more in the ownership positions of certain stockholders during a rolling three year period. Changes in the ownership positions of certain stockholders could occur as the result of stock transactions by such stockholders and/or by the issuance of stock by the Company. Such limitations may cause the Company to pay income taxes earlier and in greater amounts than would be the case if the NOLs were not subject to such limitations.

Should the Company determine that it is likely that its recorded NOL benefits are not realizable, the Company would be required to reduce the NOL tax benefit reflected on its financial statements to the net realizable amount either by a direct adjustment to the NOL tax benefit or by establishing a valuation reserve and recording a corresponding charge to current earnings. The corresponding charge to current earnings would have an adverse effect on the Company’s financial condition and results of operations in the period in which it is recorded. Conversely, if the Company is required to increase its NOL tax benefit either by a direct adjustment or reversing any portion of the accounting valuation against its deferred tax assets related to its NOLs, such credit to current earnings could have a positive effect on the Company’s business, financial condition and results of operations in the period in which it is recorded.

Our intellectual property rights may not provide meaningful commercial protection for our products or brands and third parties may assert that we violate their intellectual property rights, which could adversely impact our business, financial condition and results of operations.

Owens Corning relies on its intellectual property, including numerous patents, registered trademarks, trade secrets, confidential information, as well as its licensed intellectual property. We monitor and protect against activities that might infringe, dilute, or otherwise harm our patents, trademarks and other intellectual property and rely on the patent, trademark and other laws of the United States and other countries. However, we may be unable to prevent third parties from using our intellectual property without our authorization. To the extent we cannot protect our intellectual property, unauthorized use and misuse of our intellectual property could harm our competitive position and have a material adverse impact on our business, financial condition and results of operations. In addition, the laws of some non-United States jurisdictions provide less protection for our proprietary rights than the laws of the United States and we therefore may not be able to effectively enforce our intellectual property in these jurisdictions. If we are unable to maintain certain exclusive licenses, our brand recognition and sales could be adversely impacted. Current employees, contractors and suppliers have, and former employees, contractors and suppliers may have, access to trade secrets and confidential information regarding our operations which could be disclosed improperly and in breach of contract to our competitors or otherwise used to harm us.

Third parties may also claim that we are infringing upon their intellectual property rights. If we are unable to successfully defend or license such alleged infringing intellectual property or if we are required to substitute similar technology from another source, our operations could be adversely affected. Even if we believe that such intellectual property claims are without merit, defending such claims can be costly, time consuming and require significant resources. Claims of intellectual property infringement also might require us to redesign affected products, pay costly damage awards, or face injunctions prohibiting us from manufacturing, importing, marketing or selling certain of our products. Even if we have agreements to indemnify us, indemnifying parties may be unable or unwilling to do so.

-9-

|

| |

| ITEM 1A. | RISK FACTORS (continued) |

Our hedging activities to address energy price fluctuations may not be successful in offsetting increases in those costs or may reduce or eliminate the benefits of any decreases in those costs.

In order to mitigate short-term variation in our operating results due to commodity price fluctuations, we hedge a portion of our near-term exposure to the cost of energy, primarily natural gas. The results of our hedging practices could be positive, neutral or negative in any period depending on price changes of the hedged exposures.

Our hedging activities are not designed to mitigate long-term commodity price fluctuations and, therefore, will not protect us from long-term commodity price increases. In addition, in the future, our hedging positions may not correlate to our actual energy costs, which would cause acceleration in the recognition of unrealized gains and losses on our hedging positions in our operating results.

Downgrades of our credit ratings could adversely impact us.

Our credit ratings are important to our cost of capital. The major debt rating agencies routinely evaluate our debt based on a number of factors, which include financial strength and business risk as well as transparency with rating agencies and timeliness of financial reporting. A downgrade in our debt rating could result in increased interest and other expenses on our existing variable interest rate debt, and could result in increased interest and other financing expenses on future borrowings. Downgrades in our debt rating could also restrict our access to capital markets and affect the value and marketability of our outstanding notes.

Increases in the cost of labor, union organizing activity, labor disputes and work stoppages at our facilities could delay or impede our production, reduce sales of our products and increase our costs.

The costs of labor are generally increasing, including the costs of employee benefit plans. We are subject to the risk that strikes or other types of conflicts with personnel may arise or that we may become the subject of union organizing activity at additional facilities. In particular, renewal of collective bargaining agreements typically involves negotiation, with the potential for work stoppages or increased costs at affected facilities.

We could face potential product liability and warranty claims, we may not accurately estimate costs related to such claims, and we may not have sufficient insurance coverage available to cover such claims.

Our products are used and have been used in a wide variety of residential and commercial applications. We face an inherent business risk of exposure to product liability or other claims in the event our products are alleged to be defective or that the use of our products is alleged to have resulted in harm to others or to property. We may in the future incur liability if product liability lawsuits against us are successful. Moreover, any such lawsuits, whether or not successful, could result in adverse publicity to us, which could cause our sales to decline.

In addition, consistent with industry practice, we provide warranties on many of our products and we may experience costs of warranty or breach of contract claims if our products have defects in manufacture or design or they do not meet contractual specifications. We estimate our future warranty costs based on historical trends and product sales, but we may fail to accurately estimate those costs and thereby fail to establish adequate warranty reserves for them. We maintain insurance coverage to protect us against product liability claims, but that coverage may not be adequate to cover all claims that may arise or we may not be able to maintain adequate insurance coverage in the future at an acceptable cost. Any liability not covered by insurance or that exceeds our established reserves could materially and adversely impact our business, financial condition and results of operations.

We may be subject to liability under and may make substantial future expenditures to comply with environmental laws and regulations.

Our manufacturing facilities are subject to numerous foreign, federal, state and local laws and regulations relating to the presence of hazardous materials, pollution and the protection of the environment, including those governing emissions to air, discharges to water, use, storage and transport of hazardous materials, storage, treatment and disposal of waste, remediation of contaminated sites and protection of worker health and safety.

Liability under these laws involves inherent uncertainties. Environmental liability estimates may be affected by changing determinations of what constitutes an environmental exposure or an acceptable level of cleanup. For example, remediation activities generally involve a potential range of activities and costs related to soil and groundwater contamination. This can

-10-

|

| |

| ITEM 1A. | RISK FACTORS (continued) |

include pre-cleanup activities such as fact finding and investigation, risk assessment, feasibility studies, remedial action design and implementation (where actions may range from monitoring to removal of contaminants, to installation of longer-term remediation systems). “Please see Item 7 - Management Discussion and Analysis - Environmental Controls” for information on costs and accruals related to environmental remediation. To the extent that the required remediation procedures or timing of those procedures change, additional contamination is identified, or the financial condition of other potentially responsible parties is adversely affected, the estimate of our environmental liabilities may change. Change in required remediation procedures or timing of those procedures at existing legacy sites, or discovery of contamination at additional sites, could result in increases to our environmental obligations. Violations of environmental, health and safety laws are subject to civil, and, in some cases, criminal sanctions. As a result of these uncertainties, we may incur unexpected interruptions to operations, fines, penalties or other reductions in income which could adversely impact our business, financial condition and results of operations. In addition, the Company expects passage and implementation of new laws and regulations specifically addressing climate change, toxic air emissions, ozone forming emissions and fine particulate matter during the next two to five years. New air pollution regulations could impact our ability to expand production or construct new facilities in certain regions of North America. Continued and increased government and public emphasis on environmental issues is expected to result in increased future investments for environmental controls at ongoing operations, which will be charged against income from future operations. Present and future environmental laws and regulations applicable to our operations, and changes in their interpretation, may require substantial capital expenditures or may require or cause us to modify or curtail our operations, which may have a material adverse impact on our business, financial condition and results of operations.

We will not be insured against all potential losses and could be seriously harmed by natural disasters, catastrophes or sabotage.

Many of our business activities globally involve substantial investments in manufacturing facilities and many products are produced at a limited number of locations. These facilities could be materially damaged by natural disasters such as floods, tornados, hurricanes and earthquakes or by sabotage. We could incur uninsured losses and liabilities arising from such events, including damage to our reputation, and/or suffer material losses in operational capacity, which could have a material adverse impact on our business, financial condition and results of operations.

We depend on our senior management team and other skilled and experienced personnel to operate our business effectively, and the loss of any of these individuals or the failure to attract additional personnel could adversely impact our financial condition and results of operations.

We are highly dependent on the skills and experience of our senior management team and other skilled and experienced personnel. These individuals possess sales, marketing, manufacturing, logistical, financial, business strategy and administrative skills that are important to the operation of our business. We cannot assure that we will be able to retain all of our existing senior management personnel. The loss of any of these individuals or an inability to attract additional personnel could prevent us from implementing our business strategy and could adversely impact our business and our future financial condition or results of operations.

We are subject to various legal and regulatory proceedings, including litigation in the ordinary course of business, and uninsured judgments or a rise in insurance premiums may adversely impact our business, financial condition and results of operations.

In the ordinary course of business, we are subject to various legal and regulatory proceedings, which may include but are not limited to those involving antitrust, tax, environmental and other matters, including general commercial litigation. Any claims raised in legal and regulatory proceedings, whether with or without merit, could be time consuming and expensive to defend and could divert management’s attention and resources. Additionally, the outcome of legal and regulatory proceedings may differ from our expectations because the outcomes of these proceedings are often difficult to predict reliably. Various factors and developments can lead to changes in our estimates of liabilities and related insurance receivables, where applicable, or may require us to make additional estimates, including new or modified estimates that may be appropriate due to a judicial ruling or judgment, a settlement, regulatory developments or changes in applicable law. A future adverse ruling, settlement or unfavorable development could result in charges that could have a material adverse effect on our results of operations in any particular period.

In accordance with customary practice, we maintain insurance against some, but not all, of these potential claims. In the future, we may not be able to maintain insurance at commercially acceptable premium levels. In addition, the levels of insurance we maintain may not be adequate to fully cover any and all losses or liabilities. If any significant judgment or claim is not fully

-11-

|

| |

| ITEM 1A. | RISK FACTORS (continued) |

insured or indemnified against, it could have a material adverse impact on our business, financial condition and results of operations.

If our efforts in acquiring and integrating other businesses, establishing joint ventures or expanding our production capacity are not successful, our business may not grow.

We have historically grown our business through acquisitions, joint ventures and the expansion of our production capacity. Our ability to grow our business through these investments depends upon our ability to identify, negotiate and finance suitable arrangements. If we cannot successfully execute on our investments on a timely basis, we may be unable to generate sufficient revenue to offset acquisition, integration or expansion costs, we may incur costs in excess of what we anticipate, and our expectations of future results of operations, including cost savings and synergies, may not be achieved. Acquisitions, joint ventures and production capacity expansions involve substantial risks, including:

| |

| • | unforeseen difficulties in operations, technologies, products, services, accounting and personnel; |

| |

| • | diversion of financial and management resources from existing operations; |

| |

| • | unforeseen difficulties related to entering geographic regions or markets where we do not have prior experience; |

| |

| • | risks relating to obtaining sufficient equity or debt financing; |

| |

| • | difficulty in integrating the acquired business’ standards, processes, procedures and controls with our existing operations; |

| |

| • | potential loss of key employees; |

| |

| • | potential loss of customers; and |

| |

| • | undisclosed or undiscovered liabilities or claims. |

Our failure to address these risks or other problems encountered in connection with our past or future acquisitions and investments could cause us to fail to realize the anticipated benefits of such acquisitions or investments, incur unanticipated liabilities, and harm our business generally. Future acquisitions and investments could also result in dilutive issuances of our equity securities, the incurrence of debt, contingent liabilities, or amortization expenses, or write-offs of goodwill, any of which could have a material adverse impact on our business, financial condition and results of operations. Also, the anticipated benefits of our investments may not materialize.

Our ongoing efforts to increase productivity and reduce costs may not result in anticipated savings in operating costs.

Our cost reduction and productivity efforts, including those related to our existing operations, production capacity expansions and new manufacturing platforms, may not produce anticipated results. Our ability to achieve cost savings and other benefits within expected time frames is subject to many estimates and assumptions. These estimates and assumptions are subject to significant economic, competitive and other uncertainties, some of which are beyond our control. If these estimates and assumptions are incorrect, if we experience delays, or if other unforeseen events occur, our business, financial condition and results of operations could be adversely impacted.

Significant changes in the factors and assumptions used to measure our defined benefit plan obligations, actual investment returns on pension assets and other factors could have a negative impact on our financial condition or liquidity.

We have certain defined benefit pension plans and other postretirement benefit (“OPEB”) plans. Our future funding requirements for defined benefit pension and OPEB plans depend upon a number of factors and assumptions, including our actual experience against assumptions with regard to interest rates used to determine funding levels; return on plan assets; benefit levels; participant experience (e.g., mortality and retirement rates); health care cost trends; and applicable regulatory changes. To the extent actual results are less favorable than our assumptions, there could be a material adverse impact on our financial condition and results of operations.

Additional risks exist due to the nature and magnitude of our investments, including the implementation of or changes to the investment policy, insufficient market capacity to absorb a particular investment strategy or high volume transactions, and the inability to quickly rebalance illiquid and long-term investments.

-12-

|

| |

| ITEM 1A. | RISK FACTORS (continued) |

As of December 31, 2015 and 2014, our U.S. and worldwide defined benefit pension plans were underfunded by a total of $392 million and $444 million, respectively and OPEB obligations were underfunded by $243 million and $254 million, respectively. If our cash flows and capital resources are insufficient to fund our pension or OPEB obligations, we could be forced to reduce or delay investments and capital expenditures, seek additional capital, or restructure or refinance our indebtedness.

If we were required to write down all or part of our goodwill or other indefinite-lived intangible assets, our results of operations or financial condition could be materially adversely affected in a particular period.

Declines in the Company’s business may result in an impairment of the Company’s tangible and intangible assets which could result in a material non-cash charge. A significant or prolonged decrease in the Company’s market capitalization, including a decline in stock price, or a negative long-term performance outlook, could result in an impairment of its tangible and intangible assets which results when the carrying value of the Company’s assets exceed their fair value. At least annually, the Company assesses goodwill and intangible assets for impairment. Since the Company utilizes a discounted cash flow methodology to calculate the fair value of its reporting units, weak demand for a specific product line or business could result in an impairment. Accordingly, any determination requiring the write-off of a significant portion of goodwill or intangible assets could negatively impact the Company’s results of operations.

RISKS RELATED TO OWNERSHIP OF OUR COMMON STOCK

The market price of our common stock is subject to volatility.

The market price of our common stock could be subject to wide fluctuations in response to numerous factors, many of which are beyond our control. These factors include actual or anticipated variations in our operational results and cash flow, our earnings relative to our competition, changes in financial estimates by securities analysts, trading volume, sales by holders of large amounts of our common stock, short selling, market conditions within the industries in which we operate, seasonality of our business operations, the general state of the securities markets and the market for stocks of companies in our industry, governmental legislation or regulation and currency and exchange rate fluctuations, as well as general economic and market conditions, such as recessions.

We are a holding company with no operations of our own and depend on our subsidiaries for cash.

As a holding company, most of our assets are held by our direct and indirect subsidiaries and we will primarily rely on dividends and other payments or distributions from our subsidiaries to meet our debt service and other obligations and to enable us to pay dividends. The ability of our subsidiaries to pay dividends or make other payments or distributions to us will depend on their respective operating results and may be restricted by, among other things, the laws of their jurisdiction of organization (which may limit the amount of funds available for the payment of dividends or other payments), agreements of those subsidiaries, agreements with any co-investors in non-wholly-owned subsidiaries, the terms of our credit facility and senior notes and the covenants of any future indebtedness we or our subsidiaries may incur.

Provisions in our amended and restated certificate of incorporation and bylaws or Delaware law might discourage, delay or prevent a change in control of our company or changes in our management and therefore depress the trading price of our common stock.

Our amended and restated certificate of incorporation and bylaws contain provisions that could depress the trading price of our common stock through provisions that may discourage, delay or prevent a change in control of our company or changes in our management that our stockholders may deem advantageous.

Additionally, we are subject to Section 203 of the Delaware General Corporation Law, which generally prohibits a Delaware corporation from engaging in any of a broad range of business combinations with any “interested” stockholder for a period of three years following the date on which the stockholder became an “interested” stockholder and which may discourage, delay or prevent a change in control of our company.

-13-

|

| |

| ITEM 1A. | RISK FACTORS (continued) |

Dividends on our common stock are declared at the discretion of our Board of Directors.

Since February 2014, the Board has declared a quarterly dividend on our common stock. The payment of any future cash dividends to our stockholders is not guaranteed and will depend on decisions that will be made by our Board of Directors and will depend on then existing conditions, including our operating results, financial conditions, contractual restrictions, corporate law restrictions, capital agreements, applicable laws of the State of Delaware and business prospects.

|

| |

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

Composites

Our Composites segment operates out of 28 manufacturing facilities. We expect to begin operations in our recently constructed Gastonia, North Carolina facility in 2016. Principal manufacturing facilities for our Composites segment, all of which are owned, include the following:

|

| |

| Amarillo, Texas | Kimchon, Korea |

| Anderson, South Carolina | L’Ardoise, France |

| Besana, Italy | Rio Claro, Brazil |

| Chambery, France | Taloja, India |

| Gous, Russia | Tlaxcala, Mexico |

| Jackson, Tennessee | Yuhang, China |

Insulation

Our Insulation segment operates out of 31 manufacturing facilities. We have recently begun construction of our Joplin, Missouri facility, and we expect this new capacity to be available in 2017. Principal manufacturing facilities for our Insulation segment, all of which are owned, include the following:

|

| |

| Delmar, New York | Newark, Ohio |

| Edmonton, Alberta, Canada | Rockford, Illinois |

| Fairburn, Georgia | Santa Clara, California |

| Guangzhou, Guandong, China | Tallmadge, Ohio |

| Kansas City, Kansas | Toronto, Ontario, Canada |

| Mexico City, Mexico | Wabash, Indiana |

| Mt. Vernon, Ohio | Waxahachie, Texas |

Roofing

Our Roofing segment operates out of 29 manufacturing facilities. Principal manufacturing facilities for our Roofing segment, all of which are owned by the Company, include the following:

|

| |

| Atlanta, Georgia | Kearny, New Jersey |

| Compton, California | Medina, Ohio |

| Denver, Colorado | Portland, Oregon |

| Irving, Texas | Savannah, Georgia |

| Jacksonville, Florida | Summit, Illinois |

We believe that these properties are in good condition and well maintained, and are suitable and adequate to carry on our business. The capacity of each plant varies depending upon product mix.

Our principal executive offices are located in the Owens Corning World Headquarters, Toledo, Ohio, an owned facility of approximately 400,000 square feet.

Our research and development activities are primarily conducted at our Science and Technology Center, located on approximately 500 acres of land owned by the Company outside of Granville, Ohio. It consists of approximately 20 structures totaling more than 650,000 square feet. In addition, we have application development and other product and market focused research and development centers in various locations.

The Company is involved in legal and regulatory proceedings from time to time in the regular course of its business. The Company believes that adequate provisions for resolution of all contingencies, claims and pending litigation have been made for probable losses that are reasonably estimable. The Company does not believe that the ultimate outcome of these actions will have a material adverse effect on its financial condition, but could have a material adverse effect on its results of operations, cash flows, or liquidity in a given quarter or year.

|

| |

| ITEM 4. | MINE SAFETY DISCLOSURES |

Not applicable.

EXECUTIVE OFFICERS OF OWENS CORNING

The name, age and business experience during the past five years of Owens Corning’s executive officers as of January 1, 2016 are set forth below. Each executive officer holds office until his or her successor is elected and qualified or until his or her earlier resignation, retirement or removal. All those listed have been employees of Owens Corning during the past five years except as indicated.

|

| | |

| Name and Age | | Position* |

| Brian D. Chambers (49) | | President, Roofing and Asphalt since October 2014; formerly Vice President and General Manager, Roofing and Asphalt (2013); Vice President and Managing Director, CSB (2011). |

| | | |

| Julian Francis (49) | | President, Insulation Business since October 2014; formerly Vice President and General Manager, Residential Insulation (2012); Vice President and General Manager, Glass Reinforcements (2011). |

| | | |

| Arnaud Genis (51) | | Group President, Composite Solutions since December 2010. |

| | | |

Ava Harter (46)

| | Senior Vice President, General Counsel and Secretary since May 2015; formerly General Counsel, Chief Compliance Officer and Corporate Secretary, Taleris America LLC, an operating service provider to airlines and cargo carriers (2012), General Counsel, General Electric Aviation's Avionics Business, General Electric (2009). |

| | |

| Michael C. McMurray (50) | | Senior Vice President and Chief Financial Officer since August 2012; formerly Vice President Finance, Building Materials Group (2011). |

| | |

| Kelly J. Schmidt (50) | | Vice President, Controller since April 2011. |

| | |

| Daniel T. Smith (50) | | Senior Vice President, Organization and Administration since November 2014; formerly Senior Vice President, Information Technology and Human Resources since September 2009. |

| | |

| Michael H. Thaman (51) | | President and Chief Executive Officer since December 2007 and Chairman of the Board since April 2002; Director since 2002. |

|

| |

| * | Information in parentheses indicates year during the past five years in which service in position began. The last item listed for each individual represents the position held by such individual at the beginning of the five-year period. |

Part II

|

| |

| ITEM 5. | MARKET FOR OWENS CORNING’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information

Owens Corning’s common stock trades on the New York Stock Exchange under the symbol “OC.” The following table sets forth the high and low sales prices per share of, and dividends declared on, Owens Corning common stock for each quarter from January 1, 2014 through December 31, 2015:

|

| | | | | | | | | | | |

| Period | High | | Low | | Declared Dividend |

| First Quarter 2014 | $ | 46.64 |

| | $ | 36.80 |

| | $ | 0.16 |

|

| Second Quarter 2014 | $ | 44.04 |

| | $ | 38.10 |

| | $ | 0.16 |

|

| Third Quarter 2014 | $ | 39.44 |

| | $ | 31.52 |

| | $ | 0.16 |

|

| Fourth Quarter 2014 | $ | 37.16 |

| | $ | 28.38 |

| | $ | 0.16 |

|

| First Quarter 2015 | $ | 43.67 |

| | $ | 34.73 |

| | $ | 0.17 |

|

| Second Quarter 2015 | $ | 45.70 |

| | $ | 37.29 |

| | $ | 0.17 |

|

| Third Quarter 2015 | $ | 47.90 |

| | $ | 38.95 |

| | $ | 0.17 |

|

| Fourth Quarter 2015 | $ | 48.50 |

| | $ | 41.59 |

| | $ | 0.17 |

|

Holders of Common Stock

The number of stockholders of record of Owens Corning’s common stock on January 31, 2016 was 466.

Cash Dividends

The payment of any future cash dividends to our stockholders will depend on decisions that will be made by our Board of Directors and will depend on then existing conditions, including our operating results, financial conditions, contractual restrictions, corporate law restrictions, capital agreements, applicable laws of the State of Delaware and business .prospects.

Under the credit agreement applicable to our senior revolving credit facility, the Company may not declare a cash dividend if a default or event of default exists or would come to exist at the time of declaration or if a dividend declaration violates the provisions of our formation documents or other material agreements.

The Company’s subsidiaries are subject to certain restrictions on their ability to pay dividends under the agreements governing our senior revolving credit facility and our receivables securitization facility.

Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities

None.

-18-

|

| |

| ITEM 5. | MARKET FOR OWENS CORNING’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES (continued)

|

Issuer Purchases of Equity Securities

The following table provides information about Owens Corning’s purchases of its common stock during the three months ended December 31, 2015:

|

| | | | | | | | | | | | | |

| Period | Total Number of Shares (or Units) Purchased | | | Average Price Paid per Share (or Unit) | | Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs** | | Maximum Number of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs** |

| October 1-31, 2015 | 153,640 |

| | | $ | 42.05 |

| | 150,000 |

| | 5,449,165 |

|

| November 1-30, 2015 | 500,603 |

| | | 46.54 |

| | 499,962 |

| | 4,949,203 |

|

| December 1-31, 2015 | 344,650 |

| | | 47.18 |

| | 343,199 |

| | 4,606,004 |

|

| Total | 998,893 |

| * | | $ | 46.07 |

| | 993,161 |

| | 4,606,004 |

|

|

| |

| * | The Company retained 3,640, 665, and 1,451 shares surrendered to satisfy tax withholding obligations in connection with the vesting of restricted shares granted to our employees in October, November and December, respectively. |

|

| |

| ** | On April 19, 2012, the Company approved a share buy-back program under which the Company is authorized to repurchase up to 10 million shares of Owens Corning's outstanding common stock. Under the buy-back program, shares may be repurchased through open market, privately negotiated, or other transactions. The timing and actual number of shares repurchased will depend on market conditions and other factors and will be at the Company's discretion. |

-19-

|

| |

| ITEM 5. | MARKET FOR OWENS CORNING’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES (continued)

|

Performance Graph

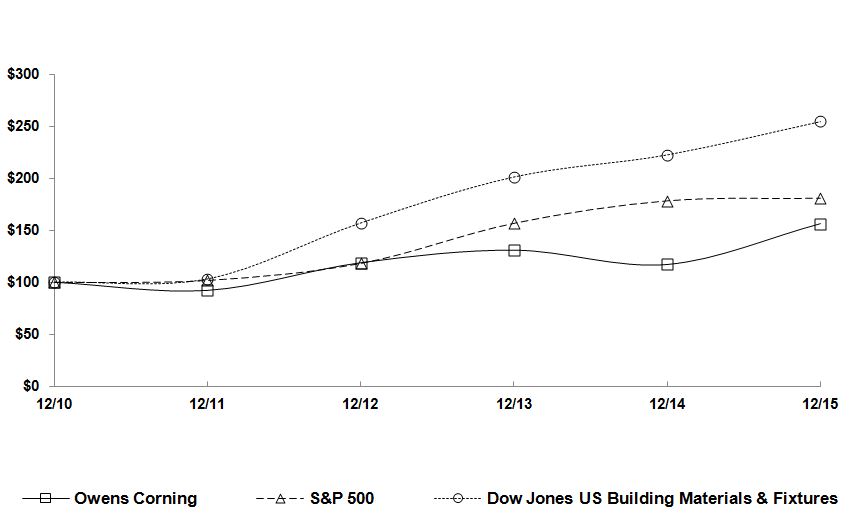

The annual changes for the five-year period shown in the graph on this page are based on the assumption that $100 had been invested in Owens Corning stock ("OC"), the Standard & Poor’s 500 Stock Index ("S&P 500") and the Dow Jones U.S. Building Materials & Fixtures Index ("DJ Bld. Mat.") on December 31, 2010, and that all quarterly dividends were reinvested. The total cumulative dollar returns shown on the graph represent the value that such investments would have had on December 31, 2015.

Performance Graph

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | 2010 | | 2011 | | 2012 | | 2013 | | 2014 | | 2015 |

| OC | $ | 100 |

| | $ | 92 |

| | $ | 119 |

| | $ | 131 |

| | $ | 117 |

| | $ | 156 |

|

| S&P 500 | $ | 100 |

| | $ | 102 |

| | $ | 118 |

| | $ | 157 |

| | $ | 178 |

| | $ | 181 |

|

| DJ Bld. Mat. | $ | 100 |

| | $ | 103 |

| | $ | 157 |

| | $ | 201 |

| | $ | 223 |

| | $ | 255 |

|

|

| |

| ITEM 6. | SELECTED FINANCIAL DATA |

|

| | | | | | | | | | | | | | | | | | | |

| | Twelve Months Ended |

| | December 31, 2015(a) | | December 31, 2014(b) | | December 31, 2013(c) | | December 31, 2012(d) | | December 31, 2011 |

| | (in millions, except per share amounts) |

| Statement of Earnings (Loss) Data | | | | | | | | | |

| Net sales | $ | 5,350 |

| | $ | 5,260 |

| | $ | 5,295 |

| | $ | 5,172 |

| | $ | 5,335 |

|

| Gross margin | $ | 1,153 |

| | $ | 976 |

| | $ | 966 |

| | $ | 797 |

| | $ | 1,028 |

|

| Marketing and administrative expenses | $ | 525 |

| | $ | 487 |

| | $ | 530 |

| | $ | 509 |

| | $ | 525 |

|

| Earnings before interest and taxes | $ | 548 |

| | $ | 392 |

| | $ | 385 |

| | $ | 148 |

| | $ | 461 |

|

| Interest expense, net | $ | 100 |

| | $ | 114 |

| | $ | 112 |

| | $ | 114 |

| | $ | 108 |

|

| Loss (gain) on extinguishment of debt | $ | (5 | ) | | $ | 46 |

| | $ | — |

| | $ | 74 |

| | $ | — |

|

| Income tax expense (benefit) | $ | 120 |

| | $ | 5 |

| | $ | 68 |

| | $ | (28 | ) | | $ | 74 |

|

| Net earnings (loss) | $ | 334 |

| | $ | 228 |

| | $ | 205 |

| | $ | (16 | ) | | $ | 281 |

|

| Net earnings (loss) attributable to Owens Corning | $ | 330 |

| | $ | 226 |

| | $ | 204 |

| | $ | (19 | ) | | $ | 276 |

|

| Earnings (loss) per common share attributable to Owens Corning common stockholders | | | | | | | | | |

| Basic | $ | 2.82 |

| | $ | 1.92 |

| | $ | 1.73 |

| | $ | (0.16 | ) | | $ | 2.25 |

|

| Diluted | $ | 2.79 |

| | $ | 1.91 |

| | $ | 1.71 |

| | $ | (0.16 | ) | | $ | 2.23 |

|

| Dividend | $ | 0.68 |

| | $ | 0.64 |

| | $ | — |

| | $ | — |

| | $ | — |

|

| Weighted-average common shares | | | | | | | | | |

| Basic | 117.2 |

| | 117.5 |

| | 118.2 |

| | 119.4 |

| | 122.5 |

|

| Diluted | 118.2 |

| | 118.3 |

| | 119.1 |

| | 119.4 |

| | 123.5 |

|

| Balance Sheet Data | | | | | | | | | |

| Total assets | $ | 7,380 |

| | $ | 7,542 |

| | $ | 7,635 |

| | $ | 7,556 |

| | $ | 7,517 |

|

| Long-term debt, net of current portion | $ | 1,702 |

| | $ | 1,978 |

| | $ | 2,012 |

| | $ | 2,064 |

| | $ | 1,920 |

|

| Total equity | $ | 3,779 |

| | $ | 3,730 |

| | $ | 3,830 |

| | $ | 3,575 |

| | $ | 3,741 |

|

| |

| (a) | During 2015, the Company recorded $2 million of charges related to cost reduction actions and related items. This was comprised of a $(6) million benefit in charges related to cost reduction actions, mainly due to changes in severance estimates and pension-related adjustments, and $8 million in other related charges, inclusive of $3 million in accelerated depreciation and $5 million in other related charges. |

| |