SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

| Filed by the Registrant x | Filed by a Party other than the Registrant o |

Check the appropriate box:

| o | Preliminary Proxy Statement |

| | |

| o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| | |

| o | Definitive Proxy Statement |

| | |

| x | Definitive Additional Materials |

| | |

| o | Soliciting Material Pursuant to § 240.14a-12 |

Hampden Bancorp, Inc.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. |

| | | |

| o | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. |

| | | |

| | 1) | Title of each class of securities to which transaction applies: |

| | | |

| | 2) | Aggregate number of securities to which transaction applies: |

| | | |

| | 3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| | | |

| | 4) | Proposed maximum aggregate value of transaction: |

| | | |

| | 5) | Total fee paid: |

| | | |

| | | |

| o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| | | |

| | 1) | Amount Previously Paid: |

| | | |

| | 2) | Form, Schedule or Registration Statement No.: |

| | | |

| | 3) | Filing Party: |

| | | |

| | 4) | Date Filed: |

| | | |

On October 29, 2013, the Company provided the following letter to its shareholders:

HAMPDEN BANCORP, INC.

October 29, 2013

Dear Fellow Shareholder:

As you know a Dallas based-hedge fund manager, Johnny Guerry and the fund he controls, MHC Mutual Conversion Fund, L.P. (the “Clover Group”) are seeking to elect his nominees to our Board and approve his shareholder resolution both to advance his stated objective of forcing a sale or merger of Hampden. Your Board of Directors and management team believe this is the wrong path and is not in the best interests of Hampden shareholders. That is why we urge you to use the enclosed BLUE proxy card to vote IN FAVOR of the Board’s nominees and AGAINST the Clover Group’s proposal.

Your Board of Directors has nominated and unanimously recommends a vote IN FAVOR of our highly qualified slate of directors, including Thomas R. Burton, Arlene Putnam, Richard D. Suski, CPA and Linda Silva Thompson.

YOUR VOTE IS IMPORTANT TO PREVENT A FORCED SALE OR MERGER OF HAMPDEN

We believe the Clover Group misrepresents our total shareholder return, financial performance, compensation and other matters in its communications in order to further its own proposal to force a sale of Hampden. We believe that allowing Clover Group representatives on the Board would adversely affect long-term shareholder value by jeopardizing our progress and forcing a sale at the wrong time.

HAMPDEN BANCORP DELIVERING VALUE FOR SHAREHOLDERS BEFORE AND AFTER

CLOVER SCHEDULE 13D

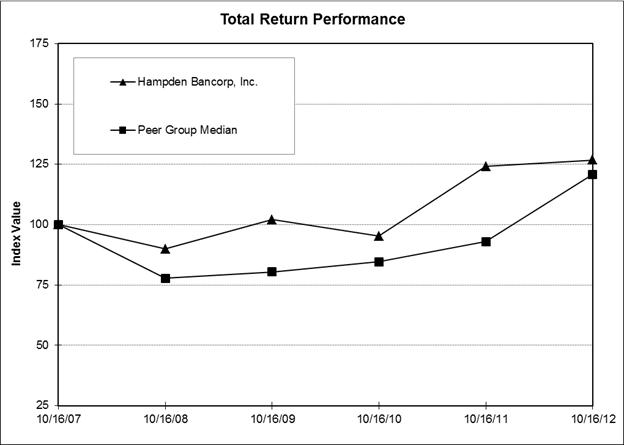

Our total shareholder return has outperformed the NASDAQ Bank Index, the SNL Bank Index and the median performance of our peer group stocks over the last five years. Our total shareholder return for the five years prior to October 17, 2012, the date of the Clover Group’s Schedule 13D, outperformed the median performance of our peer group stocks as seen below.

| | Period Ending |

| Index | 10/16/07 | 10/16/08 | 10/16/09 | 10/16/10 | 10/16/11 | 10/16/12 |

| Hampden Bancorp, Inc. | 100.00 | 89.89 | 102.10 | 95.22 | 124.06 | 126.72 |

| Peer Group Median | 100.00 | 77.79 | 80.45 | 84.56 | 93.01 | 120.86 |

Source: SNL Financial LC. The peer group used in the chart above, excluding mutual banking institutions, is the same peer group noted in our proxy statement, and was selected by our independent compensation consultant in order to prepare its compensation analysis for the Board of Directors.

THE CLOVER GROUP’S UNNECESSARY PROXY CONTEST

IS NOT IN THE BEST INTERESTS OF SHAREHOLDERS

The Clover Group has forced us into an unnecessary and distracting proxy fight, despite our willingness to listen to their views and address their proposals appropriately.

| ● | Clover Group Ignores Substantial Executive and Director Purchases of Hampden Stock. In the Clover Group’s letter to shareholders dated October 22, 2013, it describes a purported imbalance in purchases and sales of Company stock by insiders since 2008. Clover ignores the fact that in 2007, Company insiders purchased a total of $2,084,831 of Company stock, including purchases in our IPO, and made no sales. This amount is 150% of the transaction value noted in Clover’s letter. Our insiders’ interests are clearly aligned with stockholders. |

| ● | The Clover Group has Failed to Accurately Describe Executive Compensation. Based on our regulatory filings, Clover overstated the 2012 amount of Mr. Burton’s total compensation by $150,000 and understated the 2007 amount by $180,000. Accordingly, the change in compensation was actually a decrease of 7%, as opposed to the increase that Clover Group claims in its proxy statement. |

The Clover Group has presented compensation amounts from the SNL Financial data base. Such amounts are not calculated pursuant to accounting principles generally accepted in the United States (GAAP) which is required for all U.S. public companies.

| ● | The Cover Group has Failed to Accurately Describe the Number and Compensation of the Company’s Named Executive Officers. In the Clover Group’s October 16, 2013 and October 22, 2013 letters to stockholders it presents a table showing named executive compensation from 2008 to 2013. The October 16 letter inaccurately reflects an increased number of executives in 2012 and 2013, as explained below, and, in 2013, includes salaries and severance payment for employees who left the Company. |

The October 22 letter states the Clover Group’s concern about the increase in the Company’s officer positions. It fails to note that in 2013, our ex CEO, Mr. Burton, retired and two of our most highly paid executives left employment as part of our restructuring.

Under our regulatory disclosure rules, the Company must disclose compensation for named executive officers, who are the three most highly compensated executives. Such rules also require disclosure of compensation for anyone who served as CEO during the fiscal year and anyone who would have been one of the three highest paid executives but for the fact they were no longer serving as an executive at the end of such fiscal year, so that it appears as if there was an increase in the total number of executives and the total compensation paid to them. In reality, there was a decrease in the number of executives in 2013, which included three of our most highly paid executives, and Clover Group’s inclusion of two additional executives in 2012 and three in 2013 overstates our comparative compensation for those years and the total number of named executive officers.

| ● | Your Board formally considered last year’s shareholder proposal to consider strategic options and determined to continue to implement its strategy. Your Board of Directors formally considered a shareholder proposal that was substantially the same as that being proposed by the Clover Group, which was approved at last year’s annual meeting. Over a series of meetings, the Board of Directors consulted with two separate investment banks to analyze strategic options for the Company, including continuing to implement the strategic plan currently in effect and a potential sale or merger of the Company. As a result of that review and analysis the Board of Directors determined to continue to focus on building the long-term value of the Company and will continue to periodically evaluate means of enhancing shareholder value, including a sale or merger in the future. |

“Retaining” an independent financial advisory firm would have limited the scope of such review to one advisor and incurred additional expense.

Your Board and Management are better focused on serving the best interests of shareholders and continuing to grow the business and improve the performance of Hampden Bank.

VOTE THE BLUE PROXY CARD IN FAVOR OF THE COMPANY’S NOMINEES AND

AGAINST THE CLOVER GROUP’S PROPOSAL

Thank you again for you continued support.

Sincerely,

/s/ Glenn S. Welch

Glenn S. Welch

Chief Executive Officer and President

Your Vote Is Important, No Matter How Many Shares You Own.

If you have questions about how to vote your shares on the BLUE proxy card, or need additional assistance,

please contact the firm assisting us in the solicitation of proxies:

D.F. King

48 Wall Street

New York, New York 10005

For shareholder questions: 1-800-735-3591. For banks and brokers: 212-269-5550.

Email: info@dfking.com

Important Information

This material may be deemed to be solicitation material in respect of the solicitation of proxies from the Company’s shareholders in connection with the Company’s 2013 Annual Meeting of Stockholders (the “Annual Meeting”). The Company has filed with the Securities and Exchange Commission (the “SEC”) and mailed to its shareholders a proxy statement in connection with the Annual Meeting (the “Proxy Statement”), and advises its shareholders to read the Proxy Statement and any and all supplements and amendments thereto because they contain important information. Shareholders may obtain a free copy of the Proxy Statement and other documents that the Company files with the SEC at the SEC’s website at www.sec.gov. The Proxy Statement and these other documents may also be obtained upon request addressed to the Secretary of the Company at 19 Harrison Avenue, Springfield, MA 01103.

Certain Information Concerning Participants

The Company, its directors and its executive officers may be deemed to be participants in the solicitation of the Company’s shareholders in connection with the Annual Meeting. Shareholders may obtain information regarding the names, affiliations and interests of such individuals in the Company’s proxy statement related to its 2013 Annual Meeting of Stockholders, filed with the SEC on October 2, 2013.

Forward-Looking Statements

This letter contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are based on the beliefs and expectations of management, as well as the assumptions made using information currently available to management. Because these statements reflect the views of management concerning future events, these statements involve risks, uncertainties and assumptions. As a result, actual results may differ from those contemplated by these statements. Forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts. They often include words like “believe”, “expect”, “anticipate”, “estimate”, and “intend” or future or conditional verbs such as “will”, “would”, “should”, “could”, or “may.” Certain factors that could have a material adverse effect on the operations of Hampden Bank include, but are not limited to, increased competitive pressure among financial service companies, national and regional economic conditions, changes in interest rates, changes in consumer spending, borrowing and savings habits, legislative and regulatory changes, monetary and fiscal policies of the U.S. Government, including policies of the U.S. Treasury and Federal Reserve Board, adverse changes in the securities markets, inability of key third-party providers to perform their obligations to Hampden Bank and changes in relevant accounting principles and guidelines. These risks and uncertainties should be considered in evaluating forward-looking statements and undue reliance should not be placed on such statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Company disclaims any obligation to update any forward-looking statements, whether in response to new information, future events or otherwise.

5