UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21982

Claymore/Guggenheim Strategic Opportunities Fund

(Exact name of registrant as specified in charter)

2455 Corporate West Drive, Lisle, IL 60532

(Address of principal executive offices) (Zip code)

(Address of principal executive offices) (Zip code)

J. Thomas Futrell

2455 Corporate West Drive, Lisle, IL 60532

(Name and address of agent for service)

Registrant's telephone number, including area code: (630) 505-3700

Date of fiscal year end: May 31

Date of reporting period: May 31, 2010

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

Item 1. Reports to Stockholders.

The registrant's annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”), is as follows:

Annual Report May 31, 2010 | Claymore/Guggenheim Strategic Opportunities Fund | GOF | |

| |||

|  | ||

| www.claymore.com/gof | |

| ... your window to the LATEST, | |

| most up-to-date information about the | |

| Claymore/Guggenheim Strategic Opportunities Fund |

The shareholder report you are reading right now is just the beginning of the story. Online at www.claymore.com/gof, you will find:

| • | Daily, weekly and monthly data on share prices, net asset values, distributions and more |

| • | Portfolio overviews and performance analyses |

| • | Announcements, press releases and special notices |

| • | Fund and adviser contact information |

Guggenheim Partners Asset Management, LLC and Claymore are continually updating and expanding shareholder information services on the Fund’s website, in an ongoing effort to provide you with the most current information about how your Fund’s assets are managed, and the results of our efforts. It is just one more small way we are working to keep you better informed about your investment in the Fund.

2 | Annual Report | May 31, 2010

GOF | Claymore/Guggenheim Strategic Opportunities Fund

Dear Shareholder |

We thank you for your investment in the Claymore/Guggenheim Strategic Opportunities Fund (the “Fund”). This report covers the Fund’s performance for the fiscal year ended May 31, 2010.

The Fund’s investment objective is to maximize total return through a combination of current income and capital appreciation. The Fund’s sub-adviser is Guggenheim Partners Asset Management, LLC (“GPAM” or “the Sub-Adviser”), a wholly-owned subsidiary of Guggenheim Partners, LLC (“Guggenheim” or “Guggenheim Partners”). GPAM seeks to achieve that objective by combining a credit-managed fixed-income portfolio with access to a diversified pool of alternative investments and equity strategies. The Fund pursues a relative value-based investment philosophy, which utilizes quantitative and qualitative analysis to seek to identify securities or spreads between securities that deviate from their perceived fair value and/or historical norms.

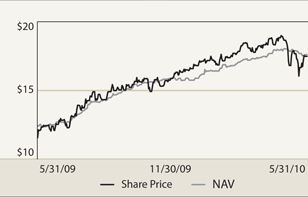

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the fiscal year ended May 31, 2010, the Fund generated a total return based on market price of 70.37% and a return of 59.06% based on NAV. As of May 31, 2010, the Fund’s last closing market price of $17.46 represented a discount of 0.57% to the Fund’s NAV of $17.56. Past performance is not a guarantee of future results. The market value of the Fund’s shares fluctuates from time to time, and it may be higher or lower than the Fund’s NAV. Investors should also be aware that these returns were primarily achieved during favorable market conditions and may not be sustainable.

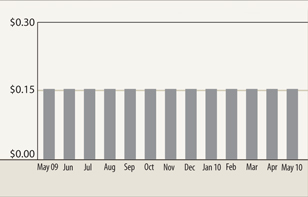

During the 2010 fiscal year the Fund paid monthly distributions of $0.154 per share. The most recent dividend represents an annualized distribution rate of 10.58% based on the Fund’s last closing market price of $17.46 as of May 31, 2010.

Claymore Advisors, LLC (“Claymore”) serves as the Investment Adviser to the Fund. Claymore Securities, Inc. is an affiliate of Claymore Advisors, LLC. Claymore Securities, Inc. offers strategic investment solutions for financial advisors and their clients. In total, Claymore entities provide supervision, management, or servicing on approximately $15.2 billion in assets as of May 31, 2010. Claymore and its associated entities are wholly-owned subsidiaries of Guggenheim Partners, a global, diversified financial services firm with more than $100 billion in assets under supervision.

As a result of the previously-announced Claymore/Guggenheim transaction, upon receiving the necessary shareholder approval on February 3, 2010, the Fund entered into a new investment advisory agreement with Claymore and a new investment sub-advisory agreement with Claymore and GPAM. These new agreements were necessary because the former agreements were automatically terminated upon the merger of Claymore Group Inc. (Claymore’s parent company) with Guggenheim Partners, which took place on October 14, 2009.

We encourage shareholders to consider the opportunity to reinvest their distributions from the Fund through the Dividend Reinvestment Plan (“DRIP”), which is described in detail on page 32 of the Fund’s annual report. When shares trade at a discount to NAV, the DRIP takes advantage of the discount by reinvesting the monthly dividend distribution in common shares of the Fund purchased in the market at a price less than NAV. Conversely, when the market price of the Fund’s common shares is at a premium above NAV, the DRIP reinvests participants’ dividends in newly-issued common shares at NAV, subject to an IRS limitation that the purchase price cannot be more than 5% below the market price per share. The DRIP provides a cost-effective means to accumulate additional shares and enjoy the benefits of compounding returns over time. Since the Fund endeavors to maintain a stable monthly distribution, the DRIP plan effectively provides an income averaging technique, which causes shareholders to accumulate a larger number of Fund shares when the market price is depressed than when the price is higher.

Annual Report | May 31, 2010 | 3

GOF | Claymore/Guggenheim Strategic Opportunities Fund | Dear Shareholder continued

To learn more about the Fund’s performance and investment strategy, we encourage you to read the Questions & Answers section of the report, which begins on page 5. You’ll find information on GPAM’s investment philosophy, its views on the economy and market environment, and detailed information about the factors that impacted the Fund’s performance.

We appreciate your investment and look forward to serving your investment needs in the future. For the most up-to-date information on your investment, please visit the Fund’s website at www. claymore.com/gof.

Sincerely,

J. Thomas Futrell

Chief Executive Officer

Claymore/Guggenheim Strategic Opportunities Fund

Update on Portfolio Management Team

Subsequent to the end of the reporting period, a member of the portfolio management team, Robert Daviduk, submitted his resignation from Guggenheim Partners Asset Management, LLC (“GPAM”). The Fund will continue to be managed by a team of professionals at GPAM, with the day to day responsibilities led by Anne Walsh.

4 | Annual Report | May 31, 2010

GOF | Claymore/Guggenheim Strategic Opportunities Fund

Questions & Answers |

Claymore/Guggenheim Strategic Opportunities Fund (the “Fund”) is managed by a team of seasoned professionals at Guggenheim Partners Asset Management, LLC. This team includes B. Scott Minerd, Chief Executive Officer and Chief Investment Officer; Anne Bookwalter Walsh, CFA, JD, Senior Managing Director; Michael Curcio, Managing Director; Robert N. Daviduk, CFA, Managing Director; Kerim Engin, Ph. D., Managing Director & Director of Risk Management; and Eric Silvergold, Managing Director. In the following interview, the investment team discusses the market environment and the Fund’s performance for the Fund’s fiscal year ended May 31, 2010.

Please remind us of this Fund’s objective and the way it is managed.

The Fund’s investment objective is to seek to maximize total return through a combination of current income and capital appreciation. The Fund pursues a relative value-based investment philosophy, which utilizes quantitative and qualitative analysis to seek to identify securities or spreads between securities that deviate from their perceived fair value and/or historical norms. GPAM seeks to combine a credit-managed fixed-income portfolio with access to a diversified pool of alternative investments and equity strategies. There is no guarantee that the perceived fair value will be achieved.

The Fund seeks to achieve its investment objective by investing in a wide range of fixed income and other debt and senior equity securities (“income securities”) selected from a variety of sectors and credit qualities, including, but not limited to, corporate bonds, loans and loan participations, structured finance investments, U.S. government and agency securities, mezzanine and preferred securities and convertible securities, and in common stocks, limited liability company interests, trust certificates and other equity investments (“common equity securities”) that GPAM believes offer attractive yield and/or capital appreciation potential, including employing a strategy of writing (selling) covered call and put options on such equities. GPAM believes the volatility (risk) of the Fund can be reduced by diversifying the portfolio across a large number of sectors and securities, many of which historically have not been highly correlated to one another.

| • | The Fund may invest, under normal market conditions, up to 60% of its total assets in income securities rated below investment grade (commonly referred to as “junk bonds”). |

| • | The Fund may invest up to 20% of its total assets in non-U.S. dollar-denominated fixed-income securities of corporate and governmental issuers located outside the U.S., including up to 10% of total assets in income securities of issuers located in emerging markets. |

| • | The Fund may invest up to 50% of its total assets in common equity securities consisting of common stock; and |

| • | The Fund may invest up to 30% of its total assets in investment funds that primarily hold (directly or indirectly) investments in which the Fund may invest directly and may invest up to 20% of the Fund’s total assets in investment funds that are registered as investment companies under the Investment Company Act of 1940, as amended (the “1940 Act”) to the extent permitted by applicable law and related interpretations of the staff of the U.S. Securities and Exchange Commission. |

GPAM’s investment process is a collaborative effort between its Portfolio Construction Group, which utilizes tools such as GPAM’s Dynamic Financial Analysis Model to determine allocation of assets among a variety of sectors, and its Sector Specialists, who are responsible for security selection within these sectors and for implementing securities transactions.

The Fund seeks to enhance the level of distributions by utilizing financial leverage through borrowings, reverse repurchase agreements or other forms of debt. As of May 31, 2010, the amount of leverage was approximately 30% of the Fund’s total assets.

Although the use of financial leverage by the Fund may create an opportunity for increased return for the common shares, it also results in additional risks and can magnify the effect of any losses. If the income and gains earned on securities purchased with the financial leverage proceeds are greater than the cost of the financial leverage, then the common shares’ return will be greater than if financial leverage had not been used. Conversely, if the income and gains from the securities purchased with the financial leverage is less than the cost of the financial leverage then the return on the common shares will be less than if financial leverage had not been used. There can be no assurance that a leveraging strategy will be implemented or that it will be successful during any period during which it is employed.

Please tell us about the market environment over the last 12 months.

Markets for both equity and fixed income securities have improved significantly over the last 12 months. This improvement followed an extremely volatile period for financial markets that began in the summer of 2007 and lasted until the early months of 2009. This difficult period was characterized by sharp declines in the market prices of most non-government securities. During that time, investors seemed to be pricing assets at levels that anticipated a very severe economic environment for an extended period—essentially another Great Depression. In the opinion of

Annual Report | May 31, 2010 | 5

GOF | Claymore/Guggenheim Strategic Opportunities Fund | Questions & Answers continued

GPAM, many securities were priced for a worst case economic outcome that did not come to pass. The U.S. economy did, in fact, experience the longest recession since the Great Depression, but it was far milder than the economic maelstrom that engulfed the world in the 1930s. In an effort to stem the very negative cycle that had begun, the federal government instituted several programs of fiscal stimulus financed by running budget deficits of about $1.5 trillion per year. In addition, the Federal Reserve (“Fed”) launched aggressive programs to improve liquidity and grow the money supply.

Beginning in March 2009, the outlook for the global economy began to improve, sparking a rally in virtually all asset classes that involved risk—including equities, corporate bonds, bank loans, asset-backed securities, non-Agency residential mortgage-backed securities, and commercial mortgage-backed securities among others. Market trends were generally positive during the Fund’s May 31, 2010, fiscal year. The Standard & Poor’s 500 (“S&P 500”) Index, which is generally regarded as an indicator of the broad U.S. stock market, returned 20.99% for the 12 months ended May 31, 2010. Most world equity markets were also strong: the Morgan Stanley Capital International (“MSCI”) World Index, which measures performance of world equity markets, returned 13.60%. Bonds also provided solid returns over this 12-month period: the Barclays Aggregate Bond Index, which is a proxy for the investment grade bond market, returned 8.4%. Reflecting investors’ increased appetite for risk, the return of the Barclays U.S. Corporate High Yield Index was 28.8% and the Barclays Commercial Backed Mortgage Securities Index also returned 28.8% over the 12-month period. Other non-government securities, such as investment grade corporate bonds, bank loans and asset backed securities have also performed very well. The return of the Barclays Capital 1-3 Month U.S. Treasury Bill Index was just 0.12%, a reflection of the record low Fed Funds target rate set between zero and 0.25%. Indices are unmanaged, reflect no expenses and it is not possible to invest directly in an index.

How did the Fund perform during this period?

The Fund performed very well over the last 12 months. All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the 12-month period ended May 31, 2010, the Fund returned 59.06% on an NAV basis and 70.37% on a market price basis. The closing price of the Fund’s shares as of May 31, 2010, was $17.46, which represented a discount of 0.57% to the NAV of $17.56. The market value of the Fund’s shares fluctuates from time to time and it may be higher or lower than the Fund’s NAV.

An important goal of the Fund is to provide long-term returns in line with equity returns but with volatility that is closer to that of bonds. For the period from the Fund’s inception date of July 27, 2007, through May 31, 2010, the Fund’s NAV return on an annualized basis was 9.05%, compared with the annualized return of - -7.7% for the S&P 500. Over this same period, the Fund’s annualized volatility has been approximately 10.1%. This compares with annualized volatility of the Barclays Aggregate Bond Index (a proxy for bonds) of approximately 4.8% and volatility of the S&P 500 Index of approximately 31.0% over the same period. Since inception, on an annualized basis, the Fund has outperformed equities (as measured by the S&P 500 Index) by 16.8 percentage points with slightly higher volatility than fixed income and less than one-third the volatility of equities. The volatility is measured by calculating the standard deviation of the percentage changes in the Fund’s daily NAV and then annualizing these percentage changes. The relatively low volatility of the Fund’s NAV is attributable to its high level of diversification across many different asset classes. Investors should also be aware that these returns were primarily achieved during favorable market conditions and may not be sustainable.

During the 12-month period ended May 31, 2010, the Fund paid monthly dividends of $0.154 per share. The most recent dividend represents an annualized distribution rate of 10.58% based on the Fund’s last closing market price of $17.46 as of May 31, 2010.

How was the Fund allocated among asset classes during this period and how did these decisions affect performance?

This Fund was created to provide investors the potential to realize a level of return similar to that achieved by equities, but with volatility more typical of fixed income securities. GPAM tracks a large number of equity and fixed income asset classes and, in constructing this portfolio, it seeks to use investments that historically have had low correlations to one another. GPAM has attempted to optimize the portfolio by analyzing the historical returns generated by GPAM’s management team in each sector, the volatility of each sector and the correlations among the sectors. GPAM does this in an effort to reduce the risk of the portfolio while providing the potential for an attractive long-term return to their investors. Throughout the period, the Fund has been highly diversified, generally with exposure to over a dozen broad sector classifications and dozens of subsectors within the major sectors.

Since the final months of 2008, GPAM recognized some unusual opportunities in the market, especially for structured securities, which were selling at extremely depressed prices because hedge funds and other levered investors were forced to sell securities at a

6 | Annual Report | May 31, 2010

GOF | Claymore/Guggenheim Strategic Opportunities Fund | Questions & Answers continued

time of very poor market liquidity. This forced selling created attractive opportunities for opportunistic investors such as GPAM.

In order to take advantage of these opportunities, the Fund’s position in U.S. government and U.S. government agency securities, which performed well during the financial crisis, was reduced substantially and was kept quite low throughout the fiscal year; these securities represented less than 1% of the Fund’s total investments as of May 31, 2010. This proved to be a good decision, as returns of government securities were just marginally positive during the recent strong market recovery, while most equity-related, corporate and structured finance securities held by the Fund have posted double digit returns; although there is no guarantee these securities will continue such performance, GPAM believes continued positive performance is possible.

In late 2009 and into 2010, GPAM sold some securities that had appreciated in value which in turn caused their market yields to decline to yields of 5% or less. GPAM reinvested the proceeds in securities that have the potential to provide much higher returns over the coming years. Examples of the types of securities sold include investment-grade corporate bonds, bank loans, various types of asset-backed securities (“ABS”) and non-traditional commercial mortgage-backed securities (“CMBS”), such as those backed by cell towers and timber. These securities were replaced with securities that GPAM believes are undervalued, such as conduit CMBS, non-agency residential mortgages, numerous types of ABS, select high yield bonds and preferred securities. These trades proved to be advantageous for the Fund. The securities purchased have appreciated and have outperformed the securities that were sold.

The Fund’s positioning proved to be a strong contributor to its performance over the 12-month period ended May 31, 2010. The Fund generated double digit total returns as well as attractive levels of income from nearly all asset classes. The best performing securities were equities, preferred securities, high yield corporate debt, and securitized assets including ABS, CMBS and non-Agency RMBS. One example of how the Fund capitalized on the financial crisis and some of the unprecedented programs that policymakers have put in place is an investment in a commercial mortgage backed security that utilized financing offered by the Federal Reserve (the “Fed”) via the term asset-backed lending facility (“TALF”). The TALF program was put in place by the Fed in an effort to restart the securitized asset market, which had virtually ceased to function during the financial market crisis and the accompanying deep recession. The securitized markets have become a critical component of capital formation and a cost effective source of credit for consumers and businesses alike. GPAM took advantage of very attractive terms being offered by the Fed that included lending to investors on a non-recourse basis. In a non-recourse loan the only source of repayment for the loan is the collateral, in this case the CMBS bond that the Fund has pledged to the Fed. Since the Fed provided a loan against the security, the Fund is at risk only for the difference between the security’s purchase price and the amount of the loan that was provided by the Fed (this amount is known as the haircut). Since making the investment in September 2009, this position has provided a return of approximately 49% after factoring in the cost of leverage.

The lowest returns came from the Fund’s very small position in U.S. government and U.S. government agency securities.

How did the Fund’s leverage affect performance during this period?

For the past year the Fund’s leverage has enhanced the return of the Fund. The purpose of leverage (borrowing) is to fund the purchase of additional securities that provide increased income and potentially greater appreciation to common shareholders than could be achieved from an unleveraged portfolio. Of course, leverage results in greater NAV volatility and entails more downside risk than an unleveraged portfolio. Since leverage adds to performance when the cost of leverage is less than the total return generated by investments, the use of leverage contributed to the Fund’s total return during this period.

As of May 31, 2010, the Fund’s leverage was approximately 30% of total assets. Leverage was increased from less than 20% during the recent financial crisis to its current level in an effort to take advantage of attractive investment opportunities.

From the Fund’s inception through late 2008, GPAM employed leverage through reverse repurchase agreements, under which they lend securities and receive cash in return which can be used for additional investments. In November 2008, the Fund entered into a committed financing facility through BNP Paribas, a leading European bank. GPAM currently employs leverage via both reverse repurchase agreements and the BNP Paribas facility, in addition to the TALF program discussed earlier.

What is the current outlook for the markets and the Fund, and how is the Fund positioned for this outlook?

GPAM’s expectations for the economy are somewhat stronger than the consensus, which is calling for real growth (real growth is measurement of GDP expectations less inflation) of about 2.0% to 3.0% for the full year 2010. Recent reports indicate that consumer confidence and business confidence are improving, and some surveys indicate businesses plan to increase hiring, which over time should help to reduce the unacceptably high level of

Annual Report | May 31, 2010 | 7

GOF | Claymore/Guggenheim Strategic Opportunities Fund | Questions & Answers continued

domestic unemployment. It is likely that there will be continued turbulence in the market, with bouts of selling pressure such as that experienced during the month of May 2010, but GPAM views these periods of weakness as opportunities to purchase select investments that have good long term potential at discounted prices.

Some of the securitized sectors continue to trade very cheap relative to historical experience, creating continued opportunities. As a bottom-up investor, GPAM evaluates each potential investment on its own merit, carefully analyzing the creditworthiness of the issuer and the security’s level of seniority in its issuer’s capital structure. GPAM intends to take advantage of market volatility and to purchase securities when there are periods of time when, in its opinion, securities can be purchased at prices that are below their true intrinsic values. When bonds or other investments are under unwarranted selling pressure, GPAM plans to take positions that have the potential for attractive returns.

Given the Fund’s mandate and its ability to invest across many asset classes, it has been very well suited to take advantage of the opportunities that have prevailed since the summer of 2007 when the Fund was launched. In the name of this Fund—Claymore/Guggenheim Strategic Opportunities Fund—the key term is “opportunities.” The Fund was designed to invest across a broad array of sectors and securities, and to take advantage of the imbalances and dislocations that often exist in the financial markets. GPAM continues to believe that a portfolio that is highly diversified across many asset classes, such as those represented by the Fund, can be of great value to investors in a wide variety of market conditions.

Index Definitions

Indices are unmanaged, reflect no expenses and it is not possible to invest directly in an index.

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks. The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Morgan Stanley Capital International World Index is a float-adjusted capitalization-weighted index created by Morgan Stanley Capital International to measure equity market performance throughout the world.

The Barclays U.S. Aggregate Bond Index represents securities that are U.S. domestic, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

The Barclays U.S. Corporate High Yield Index is an unmanaged index of below investment grade bonds issued by U.S. corporations.

The Barclays Commercial Mortgage Backed Securities Index is an unmanaged index of securities secured by mortgages on commercial real estate.

The Barclays Capital 1-3 Month U.S. Treasury Bill Index tracks the performance of U.S. Treasury bills with a remaining maturity of one to three months. U.S. Treasury bills, which are short-term loans to the U.S. government, are full-faith-and-credit obligations of the U.S. Treasury and are generally regarded as being free of any risk of default.

Risks and Other Considerations

The views expressed in this report reflect those of the portfolio manager and Claymore only through the report period as stated on the cover. These views are subject to change at any time, based on market and other conditions and should not be construed as a recommendation of any kind. The material may also include forward looking statements that involve risk and uncertainty, and there is no guarantee that any predictions will come to pass. There can be no assurance that the Fund will achieve its investment objectives. The value of the Fund will fluctuate with the value of the underlying securities. Historically, closed-end funds often trade at a discount to their net asset value.

Below Investment-Grade Securities Risk: The Fund may invest in income securities rated below investment grade or, if unrated, determined by the Sub-Adviser to be of comparable credit quality, which are commonly referred to as “high-yield” or “junk” bonds. Investment in securities of below investment-grade quality involves substantial risk of loss. Income securities of below investment-grade quality are predominantly speculative with respect to the issuer’s capacity to pay interest and repay principal when due and therefore involve a greater risk of default or decline in market value due to adverse economic and issuer-specific developments.

Senior and Second Lien Secured Loans Risk: The Fund’s investments in senior loans and second lien secured floating-rate loans are typically below investment grade and are considered speculative because of the credit risk of their issuers. The risks associated with senior loans of below investment-grade quality are similar to the risks of other lower-grade income securities. Second lien loans are second in right of payment to senior loans and therefore are subject to the additional risk that the cash flow of the borrower and any property securing the loan may be insufficient to meet scheduled payments after giving effect to the senior-secured obligations of the borrower. Second lien loans are expected to have greater price volatility and exposure to losses upon default than senior loans and may be less liquid.

Structured Finance Investments Risk: The Fund’s structured finance investments may include residential and commercial mortgage-related and asset-backed securities issued by governmental entities and private issuers, collateralized debt obligations and risk-linked securities. These securities entail considerable risk, including many of the risks described above (e.g., market risk, credit risk, interest rate risk and prepayment risk). The value of collateralized debt obligations also may change because of changes in the market’s perception of the underlying collateral of the pool, the creditworthiness of the servicing agent for or the originator of the pool, or the financial institution or entity providing credit support for the pool. Returns on risk-linked securities are dependent upon such events as property or casualty damages which may be caused by such catastrophic events as hurricanes or earthquakes or other unpredictable events.

Mezzanine Investments Risk: Mezzanine investments are subject to the same risks associated with investment in senior loans, second lien loans and other lower-grade income securities. Mezzanine investments are expected to have greater price volatility than senior loans and second lien loans and may be less liquid.

8 | Annual Report | May 31, 2010

GOF | Claymore/Guggenheim Strategic Opportunities Fund | Questions & Answers continued

Preferred Stock Risk: Preferred stock is inherently more risky than the bonds and other debt instruments of the issuer, but typically less risky than its common stock. Preferred stocks may be significantly less liquid than many other securities, such as U.S. Government securities, corporate debt and common stock.

Convertible Securities Risk: As with all income securities, the market values of convertible securities tend to decline as interest rates increase and, conversely, to increase as interest rates decline. Convertible securities also tend to reflect the market price of the underlying stock in varying degrees, depending on the relationship of such market price to the conversion price in the terms of the convertible security.

Equity Risk: Common equity securities’ prices fluctuate for a number of reasons, including changes in investors’ perceptions of the financial condition of an issuer, the general condition of the relevant stock market, and broader domestic and international political and economic events.

Real Estate Securities Risk: Because of the Fund’s ability to invest in securities of companies in the real estate industry and to make indirect investments in real estate, it is subject to risks associated with the direct ownership of real estate, including declines in the value of real estate; general and local economic conditions; increased competition; and changes in interest rates. Because of the Fund’s ability to make indirect investments in natural resources and physical commodities, and in real property asset companies, the Fund is subject to risks associated with such real property assets, including supply and demand risk, depletion risk, regulatory risk and commodity pricing risk.

Personal Property Asset Company Risk: The Fund may invest in personal property asset companies such as special situation transportation assets. The risks of special situation transportation assets include cyclicality of supply and demand for transportation assets and risk of decline in the value of transportation assets and rental values. Private Securities Risk Private securities have additional risk considerations than with investments in comparable public investments.

Inflation/Deflation Risk: There is a risk that the value of assets or income from investments will be worth less in the future as inflation decreases the value of money.

Dividend Risk: Dividends on common stock and other common equity securities which the Fund may hold are not fixed but are declared at the discretion of an issuer’s board of directors. There is no guarantee that the issuers of the common equity securities in which the Fund invests will declare dividends in the future or that, if declared, they will remain at current levels or increase over time.

Portfolio Turnover Risk:The Fund’s annual portfolio turnover rate may vary greatly from year to year. A higher portfolio turnover rate results in correspondingly greater brokerage commissions and other transactional expenses that are borne by the Fund. High portfolio turnover may result in an increased realization of net short-term capital gains by the Fund which, when distributed to common shareholders, will be taxable as ordinary income. Additionally, in a declining market, portfolio turnover may create realized capital losses.

Derivatives Risk: The Fund may be exposed to certain additional risks should the Sub-Adviser use derivatives as a means to synthetically implement the Fund’s investment strategies. If the Fund enters into a derivative instrument whereby it agrees to receive the return of a security or financial instrument or a basket of securities or financial instruments, it will typically contract to receive such returns for a predetermined period of time. During such period, the Fund may not have the ability to increase or decrease its exposure. In addition, such customized derivative instruments will likely be highly illiquid, and it is possible that the Fund will not be able to terminate such derivative instruments prior to their expiration date or that the penalties associated with such a termination might impact the Fund’s performance in a material adverse manner. Furthermore, derivative instruments typically contain provisions giving the counterparty the right to terminate the contract upon the occurrence of certain events. If a termination were to occur, the Fund’s return could be adversely affected as it would lose the benefit of the indirect exposure to the reference securities and it may incur significant termination expenses.

Foreign Securities and Emerging Markets Risk: Investing in foreign issuers may involve certain risks not typically associated with investing in securities of U.S. issuers due to increased exposure to foreign economic, political and legal developments, including favorable or unfavorable changes in currency exchange rates, exchange control regulations, expropriation or nationalization of assets, imposition of withholding taxes on payments and possible difficulty in obtaining and enforcing judgments against foreign entities. Furthermore, issuers of foreign securities and obligations are subject to different, often less comprehensive, accounting, reporting and disclosure requirements than domestic issuers. The securities and obligations of some foreign companies and foreign markets are less liquid and at times more volatile than comparable U.S. securities, obligations and markets. These risks may be more pronounced to the extent that the Fund invests a significant amount of its assets in companies located in one region and to the extent that the Fund invests in securities of issuers in emerging markets. Heightened risks of investing in emerging markets include: smaller market capitalization of securities markets, which may suffer periods of relative illiquidity; significant price volatility; restrictions on foreign investment; and possible repatriation of investment income and capital.

Financial Leverage Risk: Although the use of Financial Leverage by the Fund may create an opportunity for increased after-tax total return for the Common Shares, it also results in additional risks and can magnify the effect of any losses. If the income and gains earned on securities purchased with Financial Leverage proceeds are greater than the cost of Financial Leverage, the Fund’s return will be greater than if Financial Leverage had not been used. Conversely, if the income or gains from the securities purchased with such proceeds does not cover the cost of Financial Leverage, the return to the Fund will be less than if Financial Leverage had not been used. Financial Leverage involves risks and special considerations for shareholders, including the likelihood of greater volatility of net asset value and market price of and dividends on the Common Shares than a comparable portfolio without leverage; the risk that fluctuations in interest rates on borrowings that the Fund must pay will reduce the return to the Common Shareholders; and the effect of Financial Leverage in a declining market, which is likely to cause a greater decline in the net asset value of the Common Shares than if the Fund were not leveraged, which may result in a greater decline in the market price of the Common Shares. There can be no assurance that a leveraging strategy will be implemented or that it will be successful during any period during which it is employed.

In addition to the risks described above, the Fund is also subject to: Income Securities Risk, Foreign Currency Risk, Risks Associated with the Fund’s Covered Call Option Strategy, Risks of Real Property Asset Companies, Risks of Personal Property Asset Companies, Private Securities Risk, Derivative Transactions Risks, Investment Funds Risk, Private Investment Funds Risk, Affiliated Investment Funds Risk, Synthetic Investments Risk, Inflation/Deflation Risk, Anti-Takeover Provisions, Market Discount Risk, and Current Developments Risks. Please see www.claymore.com/gof for a more detailed discussion about Fund risks and considerations.

Annual Report | May 31, 2010 | 9

GOF | Claymore/Guggenheim Strategic Opportunities Fund

Fund Summary |As of May 31, 2010 (unaudited)

| Fund Statistics | ||||

| Share Price | $ | 17.46 | ||

| Common Share Net Asset Value | $ | 17.56 | ||

| Premium/Discount to NAV | -0.57 | % | ||

| Net Assets Applicable to Common Shares ($000) | $ | 161,783 | ||

| Total Returns | ||||||||

| (Inception 7/27/07) | Market | NAV | ||||||

| One Year | 70.37 | % | 59.06 | % | ||||

| Since Inception - average annual | 7.91 | % | 9.05 | % | ||||

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown. For the most recent month-end performance figures, please visit www.claymore.com/gof. The investment return and principal value of an investment will fluctuate with changes in the market conditions and other factors so that an investor’s shares, when sold, may be worth more or less than their original cost. Investors should also be aware that these returns were primarily achieved during favorable market conditions and may not be sustainable.

| % of Long-Term | ||||

| Top Ten Holdings | Investments | |||

| Commercial Mortgage Pass Through Certificates, Ser. 2006-C7, | ||||

| Class A4, AAA, NR, | ||||

| 5.767%, 6/10/46 | 6.5 | % | ||

| Airplanes Pass Through Trust, Ser. 2001-1A, Class A9, CCC, B1, | ||||

| 0.887%, 3/15/19 | 3.7 | % | ||

| SPDR S&P 500 ETF Trust | 2.8 | % | ||

| Applebee’s Enterprises LLC, Ser. 2007-1A, Class A22A, AAA, Aa3, | ||||

| 6.427%, 12/20/37 | 2.8 | % | ||

| ProShares Ultra S&P500 | 1.7 | % | ||

| Telos CLO Ltd., Ser. 2006-1A, Class A2, AA+, Aa2, | ||||

| 0.694%, 10/11/21 (Cayman Islands) | 1.6 | % | ||

| Dominos Pizza Master Issuer LLC, Ser. 2007-1, Class A2, BBB-, Baa3, | ||||

| 5.261%, 4/25/37 | 1.6 | % | ||

| Aviation Capital Group Trust, Ser. 2003-2A, Class B1, BBB, A3, | ||||

| 3.340%, 9/20/33 | 1.6 | % | ||

| SPDR Dow Jones Industrial Average ETF Trust | 1.4 | % | ||

| Babcock & Brown Air Funding Ltd., Ser. 2007-1A, Class G1, | ||||

| BBB+, Baa2, | ||||

| 0.638%, 10/14/33 (Bermuda) | 1.4 | % | ||

Portfolio composition and holdings are subject to change daily. For more information, please visit www.claymore.com/gof. The above summaries are provided for informational purposes only and should not be viewed as recommendations. Past performance does not guarantee future results.

Share Price & NAV History

Monthly Dividends Per Share

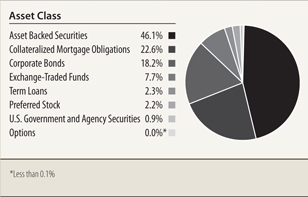

Portfolio Composition (% of Total Investments)

Credit Quality*

10 | Annual Report | May 31, 2010

GOF | Claymore/Guggenheim Strategic Opportunities Fund

Portfolio of Investments | May 31, 2010

| Principal | Optional Call | ||||||||||

| Amount | Description | Provision | Value | ||||||||

| Long-Term Investments – 131.7% | |||||||||||

| Corporate Bonds – 23.9% | |||||||||||

| Advertising – 0.3% | |||||||||||

| $ | 400,000 | MDC Partners, Inc., B+, B2 | |||||||||

| 11.000%, 11/1/16 (Canada) (a) (b) | 11/1/13 @ 105.50 | $ | 428,000 | ||||||||

| Aerospace/Defense – 0.8% | |||||||||||

| 785,000 | Global Aviation Holdings Ltd., BB-, Ba3, | ||||||||||

| 14.000%, 8/15/13 (United Kingdom) (a) (b) | 8/15/12 @ 110.50 | 792,850 | |||||||||

| 500,000 | Wyle Services Corp., B+, B3, | ||||||||||

| 10.500%, 4/1/18 (a) (b) | 4/1/14 @ 105.25 | 490,000 | |||||||||

| 1,282,850 | |||||||||||

| Airlines – 2.1% | |||||||||||

| 1,302,433 | America West Airlines 2001-1 Pass Through Trust, | ||||||||||

| Ser. 011G, BB+, B1, | |||||||||||

| 7.100%, 4/2/21 | N/A | 1,279,641 | |||||||||

| 2,000,000 | United Air Lines 2009-2A Pass Through Trust., BBB, Ba1, | ||||||||||

| 9.750%, 1/15/17 (a) | N/A | 2,150,000 | |||||||||

| 3,429,641 | |||||||||||

| Banks – 8.5% | |||||||||||

| 1,000,000 | Agfirst Farm Credit Bank, A, NR, | ||||||||||

| 7.300%, 10/31/49 (a) (b) | 7/2/10 @ 100.00 | 818,600 | |||||||||

| 1,250,000 | Barclays Bank PLC, A-, Baa3, | ||||||||||

| 6.278%, 12/29/49 (United Kingdom) (a) (c) | 12/15/34 @ 100.00 | 1,042,787 | |||||||||

| 1,200,000 | BNP Paribas, A, Baa1, | ||||||||||

| 7.195%, 6/29/49 (France) (a) (b) (c) | 6/25/37 @ 100.00 | 1,020,000 | |||||||||

| 1,000,000 | Credit Agricole SA, A-, A3, | ||||||||||

| 6.637%, 5/29/49 (France) (a) (b) (c) | 5/31/17 @ 100.00 | 710,000 | |||||||||

| 1,500,000 | Farm Credit Bank, Ser. 1, NR, A2, | ||||||||||

| 7.561%, 11/29/49 (a) (c) | 12/15/13 @100.00 | 1,233,180 | |||||||||

| 1,000,000 | Fifth Third Bancorp, BBB-, Baa2, | ||||||||||

| 8.250%, 3/1/38 (a) | N/A | 1,067,260 | |||||||||

| 1,000,000 | KeyCorp Capital III, BB, Baa3, | ||||||||||

| 7.750%, 7/15/29 (a) | N/A | 960,321 | |||||||||

| 1,250,000 | Mellon Capital IV, Ser. 1, A-, A3, | ||||||||||

| 6.244%, 6/29/49 (a) (c) | 6/20/12 @ 100.00 | 1,100,000 | |||||||||

| 1,250,000 | Northgroup Preferred Capital Corp., A, A2, | ||||||||||

| 6.378%, 1/29/49 (a) (b) (c) | 10/15/17 @ 100.00 | 1,152,288 | |||||||||

| 700,000 | PNC Preferred Funding Trust III, BBB, Baa3, | ||||||||||

| 8.700%, 3/29/49 (a) (b) (c) | 3/15/13 @ 100.00 | 711,186 | |||||||||

| 500,000 | Rabobank Nederland NV, AA-, A2, | ||||||||||

| 11.000%, 12/29/49 (Netherlands) (a) (b) (c) | 6/30/19 @ 100.00 | 606,549 | |||||||||

| 1,400,000 | Royal Bank of Scotland Group PLC, Ser. U, C, B3, | ||||||||||

| 7.640%, 3/31/49 (United Kingdom) (a) (c) | 9/29/17 @ 100.00 | 791,000 | |||||||||

| 650,000 | Susquehanna Capital II, BB-, Ba2, | ||||||||||

| 11.000%, 3/23/40 (a) | 3/23/15 @ 100.00 | 680,875 | |||||||||

| 1,250,000 | US AgBank FCB, A, A2, | ||||||||||

| 6.110%, 4/29/49 (a) (b) (c) | 7/10/12 @ 100.00 | 891,113 | |||||||||

| 1,000,000 | Wells Fargo Capital XIII, Ser. GMTN, A-, Ba1, | ||||||||||

| 7.700%, 12/29/49 (a) (c) | 3/26/13 @ 100.00 | 985,000 | |||||||||

| 13,770,159 | |||||||||||

| Commercial Services – 0.4% | |||||||||||

| 280,000 | PharmaNet Development Group, Inc., B+, B3, | ||||||||||

| 10.875%, 4/15/17 (b) | 4/15/14 @ 105.44 | 274,400 | |||||||||

| 250,000 | R.R. Donnelley & Sons Co., BBB, Baa3, | ||||||||||

| 11.250%, 2/1/19 (a) | N/A | 316,219 | |||||||||

| 590,619 | |||||||||||

| Computers – 0.1% | |||||||||||

| 250,000 | Stratus Technologies, Inc., B-, B2, | ||||||||||

| 12.000%, 3/29/15 (b) | 4/15/13 @ 112.00 | 230,312 | |||||||||

| Distribution/Wholesale – 0.4% | |||||||||||

| 700,000 | Intcomex, Inc., B-, B3, | ||||||||||

| 13.250%, 12/15/14 (b) | 12/15/12 @ 106.63 | 717,500 | |||||||||

| Diversified Financial Services – 2.1% | |||||||||||

| Hampton Roads PPV LLC, NR, Baa2, (a) (b) | |||||||||||

| 1,000,000 | 6.071%, 12/15/41 | N/A | 829,220 | ||||||||

| 1,000,000 | 6.171%, 6/15/53 | N/A | 834,370 | ||||||||

| 2,000,000 | Svensk Exportkredit AB, A, NR, | ||||||||||

| 6.375%, 10/29/49 (Sweden) (a) (b) | 9/27/10 @ 100.00 | 1,716,676 | |||||||||

| 3,380,266 | |||||||||||

| Electric – 0.8% | |||||||||||

| 400,000 | United Maritime Group LLC/United Maritime Group | ||||||||||

| Finance Corp., B, B3, | |||||||||||

| 11.750%, 6/15/15 (a) (b) | 12/15/12 @ 105.88 | 392,000 | |||||||||

| 1,000,000 | Wisconsin Energy Corp., BBB-, Baa1, | ||||||||||

| 6.250%, 5/15/67 (a) (c) | 5/15/17 @ 100.00 | 910,000 | |||||||||

| 1,302,000 | |||||||||||

| Entertainment and Gaming – 1.9% | |||||||||||

| 1,000,000 | Agua Caliente Band of Cahuilla Indians, NR, NR, | ||||||||||

| 6.350%, 10/1/15 (b) | N/A | 953,400 | |||||||||

| 500,000 | Downstream Development Authority of the Quapaw | ||||||||||

| Tribe of Oklahoma, B-, Caa1, | |||||||||||

| 12.000%, 10/15/15 (b) | 10/15/11 @ 109.00 | 445,000 | |||||||||

| 500,000 | Indianapolis Downs LLC/Indiana Downs Capital Corp., | ||||||||||

| CCC, Caa3, | |||||||||||

| 11.000%, 11/1/12 (b) | 11/1/10 @ 105.50 | 357,500 | |||||||||

| 700,000 | Lions Gate Entertainment, Inc., B, B1, | ||||||||||

| 10.250%, 11/1/16 (b) | 11/1/13 @ 105.13 | 705,250 | |||||||||

| 700,000 | River Rock Entertainment Authority (The), B+, B2, | ||||||||||

| 9.750%, 11/1/11 (a) | 7/2/10 @ 100.00 | 652,750 | |||||||||

| 3,113,900 | |||||||||||

| Health Care – 0.2% | |||||||||||

| 250,000 | Apria Healthcare Group, Inc., BB+, Ba2, | ||||||||||

| 11.250%, 11/1/14 (a) (b) | 11/1/11 @ 105.63 | 263,125 | |||||||||

| Insurance – 4.7% | |||||||||||

| 1,000,000 | Allstate Corp. (The), BBB, Baa1, | ||||||||||

| 6.500%, 5/15/57 (a) (c) | 5/15/37 @ 100.00 | 875,000 | |||||||||

| 1,000,000 | American Financial Group, Inc., BBB, Baa2, | ||||||||||

| 9.875%, 6/15/19 (a) | N/A | 1,187,693 | |||||||||

See notes to financial statements.

Annual Report | May 31, 2010 | 11

GOF | Claymore/Guggenheim Strategic Opportunities Fund | Portfolio of Investments continued

| Principal | Optional Call | ||||||||||

| Amount | Description | Provision | Value | ||||||||

| Insurance (continued) | |||||||||||

| $ | 1,000,000 | AXA SA, BBB, Baa1, | |||||||||

| 6.463%, 12/14/49 (France) (a) (b) (c) | 12/14/18 @ 100.00 | $ | 780,000 | ||||||||

| 400,000 | Blue Coast Ltd., Ser. A, B+, NR, | ||||||||||

| 9.777%, 12/8/10 (Cayman Islands) (b) (d) (e) | N/A | 395,368 | |||||||||

| 700,000 | Blue Fin Ltd., BB+, NR, | ||||||||||

| 4.695%, 4/10/12 (Cayman Islands) (a) (b) (d) (e) | 7/8/10 @ 101.00 | 654,640 | |||||||||

| 800,000 | Ironshore Holdings US, Inc., BBB-, Baa3, | ||||||||||

| 8.500%, 5/15/20 (b) | N/A | 810,384 | |||||||||

| 1,000,000 | Metlife Capital Trust IV, BBB, Baa2, | ||||||||||

| 7.875%, 12/15/37 (a) (b) | 12/15/32 @ 100.00 | 980,000 | |||||||||

| 700,000 | National Life Insurance Co., BBB+, Baa1, | ||||||||||

| 10.500%, 9/15/39 (a) (b) | N/A | 788,318 | |||||||||

| 1,250,000 | Progressive Corp. (The), A-, A2, | ||||||||||

| 6.700%, 6/15/37 (a) (c) | 6/15/17 @ 100.00 | 1,140,462 | |||||||||

| 7,611,865 | |||||||||||

| Investment Companies – 0.6% | |||||||||||

| Allied Capital Corp., BBB, Ba1, (a) | |||||||||||

| 695,000 | 6.625%, 7/15/11 | N/A | 697,076 | ||||||||

| 290,000 | 6.000%, 4/1/12 | N/A | 290,401 | ||||||||

| 987,477 | |||||||||||

| Iron/Steel – 0.1% | |||||||||||

| 240,000 | Standard Steel LLC/Standard Steel Finance Corp., | ||||||||||

| B, Caa1, | |||||||||||

| 12.000, 5/1/15 (b) | 5/1/13 @ 106.00 | 241,469 | |||||||||

| Software – 0.2% | |||||||||||

| 400,000 | Open Solutions, Inc., CCC+, Caa2, | ||||||||||

| 9.750%, 2/1/15 (b) | 2/1/11 @ 104.88 | 312,000 | |||||||||

| Telecommunications – 0.7% | |||||||||||

| 1,086,000 | Clearwire Communications LLC/Clearwire Finance, | ||||||||||

| Inc., B-, Caa1, | |||||||||||

| 12.000%, 12/1/15 (b) | 12/1/12 @ 106.00 | 1,053,420 | |||||||||

| Total Corporate Bonds – 23.9% | |||||||||||

| (Cost $40,798,461) | 38,714,603 | ||||||||||

| Asset Backed Securities – 60.8% | |||||||||||

| Collateralized Debt Obligations – 4.0% | |||||||||||

| 1,897,459 | Aspen Funding I Ltd., Ser. 2002-1A, Class A1L, A, Ba1, | ||||||||||

| 0.894%, 7/10/37 (Cayman Islands) (b) (d) | 1,239,743 | ||||||||||

| 1,024,426 | Coronado CDO Ltd., Ser. 1A, Class A1, BB+, B3, | ||||||||||

| 0.772%, 9/4/38 (Cayman Islands) (b) (d) | 679,942 | ||||||||||

| 2,145,722 | Diversified Asset Securitization Holdings III, Ser. 1A, Class A2, BB+, Ba1, | ||||||||||

| 7.420%, 7/5/36 (Cayman Islands) (b) | 1,802,407 | ||||||||||

| 4,347,270 | Duke Funding Ltd., Ser. 2003-5A, Class 1W, CCC, Caa2, | ||||||||||

| 0.910%, 8/7/33 (Cayman Islands) (b) (d) | 1,549,765 | ||||||||||

| 608,584 | MWAM CBO Ltd., Ser. 2001-1A, Class A, AA, A3, | ||||||||||

| 0.936%, 1/30/31 (Cayman Islands) (b) (d) | 495,661 | ||||||||||

| 878,851 | Saybrook Point CBO Ltd., Ser. 2001-1A, Class A, BBB-, B3, | ||||||||||

| 0.977%, 2/25/31 (Cayman Islands) (b) (d) | 688,167 | ||||||||||

| 6,455,685 | |||||||||||

| Principal | |||||||

| Amount | Description | Value | |||||

| Collateralized Loan Obligations – 16.0% | |||||||

| $ | 635,902 | Armstrong Loan Funding Ltd., Ser. 2008-1A, Class B, AA+, Aa3, | |||||

| 1.344%, 8/1/16 (Cayman Islands) (b) (d) | $ | 580,483 | |||||

| 2,000,000 | Black Diamond CLO Ltd., Ser. 2006-1A, Class B, A+, Baa2, | ||||||

| 0.718%, 4/29/19 (Cayman Islands) (a) (b) (d) | 1,551,460 | ||||||

| 2,000,000 | Black Diamond CLO Ltd., Ser. 2006-1A, Class C, BBB+, Ba2, | ||||||

| 1.018%, 4/29/19 (Cayman Islands) (a) (b) (d) | 1,392,180 | ||||||

| 1,854,059 | Business Loan Express, Ser. 2006-AA, Class A, BBB-, Aa3, | ||||||

| 0.580%, 10/20/38 (b) (d) | 1,268,308 | ||||||

| 1,259,374 | Business Loan Express, Ser. 2007-AA, Class A, BBB-, A2, | ||||||

| 0.740%, 10/20/40 (b) (d) | 850,077 | ||||||

| 750,000 | CapitalSource Commercial Loan Trust, Ser. 2006-2A, Class A1B, AA+, Aaa, | ||||||

| 0.670%, 9/20/22 (b) (d) | 659,415 | ||||||

| 1,181,541 | Coast Investment Grade, Ser. 2002-1X, Class A, BBB-, Caa3, | ||||||

| 0.933% 7/30/17 (Cayman Islands) (d) | 590,770 | ||||||

| 500,000 | Emporia Preferred Funding, Ser. 2005-1A, Class B1, AA-, Aa3, | ||||||

| 0.844%, 10/12/2018 (Cayman Islands) (b) (d) | 341,275 | ||||||

| 1,000,000 | Friedbergmilstein Private Capital Fund, Ser. 2004-1A, Class B2, AA, A3, | ||||||

| 5.409%, 1/15/19 (Cayman Islands) (b) | 869,680 | ||||||

| 800,000 | Mountain View Funding CLO, Ser. 2007-3A, Class A2, AA, A1, | ||||||

| 0.644%, 4/16/21 (Cayman Islands) (b) (d) | 682,992 | ||||||

| 1,000,000 | Nantucket CLO Ltd., Ser. 2006-1A, Class B, AA, A3, | ||||||

| 0.904%, 11/24/20 (Cayman Islands) (b) (d) | 827,540 | ||||||

| 1,500,000 | Rosedale CLO Ltd., Ser. I-A, Class A1J, A+, Baa1, | ||||||

| 0.726%, 7/24/21 (Cayman Islands) (b) (d) | 1,351,755 | ||||||

| 2,000,000 | Stanfield Modena CLO Ltd., Ser. 2004-1A, Class C, BBB-, Ba2, | ||||||

| 1.521%, 9/22/16 (Cayman Islands) (a) (b) (d) | 1,484,040 | ||||||

| 600,000 | Start CLO Ltd., Ser 2006-2, Class C, A+, Baa1, | ||||||

| 1.038%, 6/29/12 (Cayman Islands) (d) | 559,602 | ||||||

| 1,000,000 | Start CLO Ltd., Ser 2006-2, Class D, BBB+, Baa3, | ||||||

| 2.138%, 6/29/12 (Cayman Islands) (d) | 932,890 | ||||||

| 400,000 | Start CLO Ltd., Ser. 2006-3A, Class C, A-, A1, | ||||||

| 0.952%, 6/7/11 (Cayman Islands) (b) (d) | 399,524 | ||||||

| 550,000 | Start CLO Ltd., Ser. 2006-3A, Class D, BBB, Baa1, | ||||||

| 2.002%, 6/7/11 (Cayman Islands) (b) (d) | 543,758 | ||||||

| 100,000 | Start CLO Ltd., Ser 2006-3X, Class F, NR, NR, | ||||||

| 17.252%, 6/7/11 (Cayman Islands) (d) | 99,817 | ||||||

| 500,000 | Start CLO Ltd., Ser. 2007-4A, Class D, BBB+, Baa1, | ||||||

| 1.835%, 12/26/11 (Cayman Islands) (a) (b) (d) | 483,445 | ||||||

| 1,000,000 | Start CLO Ltd., Ser. 2007-4A, Class E, BB+, Ba1, | ||||||

| 3.885%, 12/26/11 (Cayman Islands) (a) (b) (d) | 966,060 | ||||||

| 100,000 | Start CLO Ltd., Ser 2007-4X, Class E, BB+, Ba1, | ||||||

| 3.885%, 12/26/11 (Cayman Islands) (d) | 96,606 | ||||||

| 2,000,000 | TCW Global Project Fund, Ser. 2004-1A, Class A1, NR, NR, | ||||||

| 1.203%, 6/15/16 (Cayman Islands) (b) (d) (f) | 1,704,200 | ||||||

| 2,000,000 | TCW Global Project Fund, Ser. 2004-1A, Class B1, NR, NR, | ||||||

| 2.253%, 6/15/16 (Cayman Islands) (a) (b) (d) (f) | 1,420,320 | ||||||

| 1,000,000 | TCW Global Project Fund, Ser. 2005-1A, Class B2, A, NR, | ||||||

| 5.793%, 9/1/17 (Cayman Islands) (b) | 771,230 | ||||||

See notes to financial statements.

12 | Annual Report | May 31, 2010

GOF | Claymore/Guggenheim Strategic Opportunities Fund | Portfolio of Investments continued

| Principal | |||||||

| Amount | Description | Value | |||||

| Collateralized Loan Obligations (continued) | |||||||

| $ | 4,000,000 | Telos CLO Ltd., Ser. 2006-1A, Class A2, AA+, Aa2, | |||||

| 0.694%, 10/11/21 (Cayman Islands) (b) (d) | $ | 3,513,280 | |||||

| 2,500,000 | Telos CLO Ltd., Ser. 2006-1A, Class B, A+, A2, | ||||||

| 0.784%, 10/11/21 (Cayman Islands) (b) (d) | 1,975,425 | ||||||

| 25,916,132 | |||||||

| Commercial Real Estate – 1.0% | |||||||

| 2,000,000 | Wrightwood Capital Real Estate CDO Ltd., Ser. 2005-1A, Class A1, BB, Aa3, | ||||||

| 0.798%, 11/21/40 (Cayman Islands) (b) (d) (f) | 1,507,380 | ||||||

| Commercial Receivables – 2.6% | |||||||

| 500,000 | FCC Financing Subsidiary LLC, Ser. 2010-1A, Class B, NR, NR, | ||||||

| 15.68%, 3/31/17 (d) | 502,500 | ||||||

| 2,000,000 | HFG Healthco-4 LLC, Ser. 2006-1A, Class A, NR, Aa2, | ||||||

| 0.680%, 6/5/12 (b) (d) | 1,849,460 | ||||||

| 2,000,000 | Sealane Trade Finance, Ser. 2007-1A, Class E, NR, NR, | ||||||

| 15.497%, 11/25/12 (Cayman Islands) (a) (b) (d) | 1,889,860 | ||||||

| 4,241,820 | |||||||

| Corporate Debt Obligations – 0.4% | |||||||

| 575,866 | Muzinich CBO II Ltd., Ser. A2-A, AA+, B1, | ||||||

| 7.150%, 10/15/13 (Bermuda) (b) | 546,900 | ||||||

| 112,680 | Phoenix Funding Ltd., Ser. 2001-1, AA, Aa2, | ||||||

| 0.753%, 4/15/13 (d) | 99,458 | ||||||

| 646,358 | |||||||

| Credit Cards – 2.8% | |||||||

| 500,000 | 1st Financial Bank USA, Ser. 2009-B, Class D, BBB-, NR, | ||||||

| 11.000%, 4/15/15 (b) | 500,153 | ||||||

| 1,000,000 | LCP Rights Trust, Ser. 2010-1, Class A, NR, NR, | ||||||

| 14.550%, 7/17/17 | 999,960 | ||||||

| 500,000 | LCP Rights Trust, Ser. 2010-1, Class C, NR, NR, | ||||||

| 19.210%, 7/17/17 | 499,955 | ||||||

| 1,000,000 | LCP Rights Trust, Ser. 2010-1, Class D, NR, NR, | ||||||

| 14.550%, 1/15/16 | 999,970 | ||||||

| 1,500,000 | LCP Rights Trust, Ser. 2010-1, Class F, NR, NR, | ||||||

| 19.210%, 1/15/16 | 1,499,895 | ||||||

| 4,499,933 | |||||||

| Financials – 0.0%* | |||||||

| 42,012 | Blue Falcon, Ser. A-2, NR, NR, | ||||||

| 5.460%, 12/25/16 (b) | 41,595 | ||||||

| Insurance – 2.3% | |||||||

| 1,758,677 | 321 Henderson Receivables I LLC, Ser. 2007-3A, Class A, BBB, Baa1, | ||||||

| 6.150%, 10/15/48 (a) (b) | 1,724,559 | ||||||

| 443,118 | 321 Henderson Receivables I LLC, Ser. 2008-1A, Class A, AA+, Aaa, | ||||||

| 6.190%, 1/15/44 (a) (b) | 446,073 | ||||||

| 500,000 | 321 Henderson Receivables I LLC, Ser. 2008-1A, Class B, AA, NR, | ||||||

| 8.370%, 1/15/46 (a) (b) | 518,215 | ||||||

| 500,000 | 321 Henderson Receivables I LLC, Ser. 2008-1A, Class C, A, NR, | ||||||

| 9.360%, 1/15/48 (b) | 505,820 | ||||||

| 500,000 | 321 Henderson Receivables I LLC, Ser. 2008-1A, Class D, BBB, NR, | ||||||

| 10.810%, 1/15/50 (b) | 535,420 | ||||||

| 3,730,087 | |||||||

| Residential Loans – 0.2% | |||||||

| 500,000 | GSAA Trust, Ser. 2007-5, Class 1F2A, CCC, Caa1, | ||||||

| 5.788%, 3/25/47 (a) (d) | 305,439 | ||||||

| Student Loans – 0.2% | |||||||

| 391,570 | MRU Student Loan Trust, Ser. 2008-A, Class A1A, AAA, NR, | ||||||

| 7.400%, 1/25/41 (b) | 197,391 | ||||||

| 202,567 | MRU Student Loan Trust, Ser. 2008-A, Class B, AA, NR, | ||||||

| 5.816%, 1/25/41 (b) (d) | 49,748 | ||||||

| 202,567 | MRU Student Loan Trust, Ser. 2008-A, Class C, A, NR, | ||||||

| 7.816%, 1/25/41 (b) (d) | 43,724 | ||||||

| 290,863 | |||||||

| Timeshares – 2.5% | |||||||

| 2,593,604 | Diamonds Resort Owner Trust, Ser. 2009-1, Class A, A, NR, | ||||||

| 9.310%, 3/20/26 (a) (b) | 2,595,760 | ||||||

| 1,369,941 | Sierra Receivables Funding Co., Ser. 2006-1A, Class A1, BBB-, Baa3, | ||||||

| 5.840%, 5/20/18 (a) (b) | 1,393,113 | ||||||

| 3,988,873 | |||||||

| Transportation – 18.0% | |||||||

| 1,907,592 | Aircraft Certificate Owner Trust, Ser. 2003-1A, Class D, BB+, Ba3, | ||||||

| 6.455%, 9/20/22 (b) | 1,735,909 | ||||||

| 2,000,000 | Aircraft Certificate Owner Trust, Ser. 2003-1A, Class E, BB+, Ba3, | ||||||

| 7.001%, 9/20/22 (b) | 1,645,020 | ||||||

| 2,311,685 | Aircraft Lease Securitisation Ltd., Ser. 2007-1A, Class G3, A-, Baa1, | ||||||

| 0.540%, 5/10/32 (Jersey) (b) (d) | 2,039,461 | ||||||

| 766,783 | Airplanes Pass Through Trust, Ser. 1R, Class A8, BB-, Baa3, | ||||||

| 0.712%, 3/15/19 (d) | 751,448 | ||||||

| 15,000,000 | Airplanes Pass Through Trust, Ser. 2001-1A, Class A9, CCC, B1, | ||||||

| 0.887%, 3/15/19 (d) | 7,837,500 | ||||||

| 1,087,247 | Aviation Capital Group Trust, Ser. 2000-1A, Class A1, BB, Ba3, | ||||||

| 0.817%, 11/15/25 (b) (d) | 595,964 | ||||||

| 5,813,296 | Aviation Capital Group Trust, Ser. 2003-2A, Class B1, BBB, A3, | ||||||

| 3.340%, 9/20/33 (b) (d) | 3,494,140 | ||||||

| 3,883,199 | Babcock & Brown Air Funding Ltd., Ser. 2007-1A, Class G1, BBB+, Baa2, | ||||||

| 0.638%, 10/14/33 (Bermuda) (a) (b) (d) | 2,912,400 | ||||||

| 894,145 | Blade Engine Securitization Ltd., Ser. 2006-1A, Class B, BBB+, Baa2, | ||||||

| 3.337%, 9/15/2041 (Cayman Islands) (b) (d) | 585,527 | ||||||

| 567,248 | CLI Funding LLC, Ser. 2006-1A, Class A, BBB, Baa3, | ||||||

| 0.518%, 8/18/21 (b) (d) | 461,308 | ||||||

| 267,307 | Helios Finance LP, Ser. 2007-S1, Class B1, BBB, Baa3, | ||||||

| 1.040%, 10/20/14 (Cayman Islands) (b) (d) | 260,670 | ||||||

| 3,221,236 | Lease Investment Flight Trust, Ser. 1, Class A3, B+, Baa3, | ||||||

| 0.767%, 7/15/16 (a) (d) | 2,844,319 | ||||||

| 5,200,000 | Pegasus Aviation Lease Securitization, Ser. 2001-1A, Class A1, NR, B2, | ||||||

| 0.777%, 5/10/31 (b) (d) | 1,924,000 | ||||||

| 500,000 | Pegasus Aviation Lease Securitization, Ser. 2001-1A, Class A2, NR, B2, | ||||||

| 0.877%, 5/10/31 (b) (d) | 185,000 | ||||||

See notes to financial statements.

Annual Report | May 31, 2010 | 13

GOF | Claymore/Guggenheim Strategic Opportunities Fund | Portfolio of Investments continued

| Principal | |||||||

| Amount | Description | Value | |||||

| Transportation (continued) | |||||||

| $ | 2,106,000 | Triton Container Finance LLC, Ser. 2006-1A, BBB, Baa2, | |||||

| 0.515%, 11/26/21 (b) (d) | $ | 1,884,013 | |||||

| 29,156,679 | |||||||

| Trust Preferred Stocks – 3.5% | |||||||

| 6,000,000 | Attentus CDO Ltd., Ser. 2007-3A, Class A1B, AAA, Aa3, | ||||||

| 0.554%, 10/11/42 (Cayman Islands) (b) (d) | 2,785,080 | ||||||

| 4,772,600 | Preferred Term Securities XXIII Ltd., BBB-, B1, | ||||||

| 0.567%, 12/22/36 (Cayman Islands) (b) (d) | 2,911,286 | ||||||

| 5,696,366 | |||||||

| Whole Business – 7.3% | |||||||

| 6,424,030 | Applebee’s Enterprises LLC, Ser. 2007-1A, Class A22A, AAA, Aa3, | ||||||

| 6.427%, 12/20/37 (a) (b) | 5,979,679 | ||||||

| 3,760,000 | Dominos Pizza Master Issuer LLC, Ser. 2007-1, Class A2, BBB-, Baa3, | ||||||

| 5.261%, 4/25/37 (a) (b) | 3,506,096 | ||||||

| 2,000,000 | IHOP Franchising LLC, Ser. 2007-1A, Class A1, BBB-, Baa2, | ||||||

| 5.144%, 3/20/37 (a) (b) | 1,822,720 | ||||||

| 600,000 | NuCO2 Funding LLC, Ser. 2008-1A, Class A1, NR, Baa2, | ||||||

| 7.250%, 6/25/38 (b) | 545,826 | ||||||

| 11,854,321 | |||||||

| Total Asset Backed Securities – 60.8% | |||||||

| (Cost $91,838,654) | 98,331,531 | ||||||

| Collateralized Mortgage Obligations – 29.8% | |||||||

| 500,000 | Banc of America Commercial Mortgage, Inc., Ser. 2003-2, Class G, A-, NR, | ||||||

| 5.333%, 3/11/41 (b) (d) | 422,554 | ||||||

| 1,000,000 | Banc of America Commercial Mortgage, Inc., Ser. 2004-5, Class B, AA+, Aa2, | ||||||

| 5.058%, 11/10/41 (a) (d) | 720,686 | ||||||

| 600,000 | Banc of America Commercial Mortgage, Inc., Ser. 2005-5, Class AJ, BBB+, Aaa, | ||||||

| 5.154%, 10/10/45 (a) (d) | 507,830 | ||||||

| 1,500,000 | Bear Stearns Commercial Mortgage Securities, Ser. 2005-PW10, Class AJ, BB+, NR, | ||||||

| 5.463%, 12/11/40 (a) (d) | 1,156,325 | ||||||

| 500,000 | Citigroup Commercial Mortgage Trust, Ser. 2004-C2, Class E, A-, A3, | ||||||

| 5.023%, 10/15/41 (b) (d) | 388,684 | ||||||

| 1,200,000 | Citigroup Commercial Mortgage Trust, Ser. 2007-C6, Class AM, A, NR, | ||||||

| 5.700%, 12/10/49 (d) | 1,021,904 | ||||||

| 2,000,000 | Citigroup/Deutsche Bank Commercial Mortgage Trust, Ser. 2005-CD1, Class AJ, | ||||||

| A-, Aa1, | |||||||

| 5.223%, 7/15/44 (a) (d) | 1,683,356 | ||||||

| 13,500,000 | Commercial Mortgage Pass Through Certificates, Ser. 2006-C7, Class A4, AAA, NR, | ||||||

| 5.767%, 6/10/46 (d) (g) | 13,928,007 | ||||||

| 1,000,000 | Commercial Mortgage Pass Through Certificates, Ser. 2006-C7, Class AM, A, NR, | ||||||

| 5.792%, 6/10/46 (a) (d) | 900,141 | ||||||

| 1,000,000 | Commercial Mortgage Pass Through Certificates, Ser. 2006-CN2A, Class F, CCC+, NR, | ||||||

| 5.570%, 2/5/19 (a) (b) (d) | 884,671 | ||||||

| 4,144,928 | Countrywide Alternative Loan Trust, Ser. 2006-OA19, Class A1, CCC, Ba2, | ||||||

| 0.520%, 2/20/47 (a) (d) | 2,078,101 | ||||||

| 3,001,260 | Countrywide Home Equity Loan Trust, Ser. 2004-S, Class 1A, CCC, B3, | ||||||

| 0.577%, 2/15/30 (d) | 1,586,703 | ||||||

| 1,599,910 | Countrywide Home Loan Mortgage Pass Through Trust, Ser. 2005-HYB8, | ||||||

| Class 4A1, B-, Caa3, | |||||||

| 5.383%, 12/20/35 (d) | 1,201,463 | ||||||

| 1,187,500 | Credit Suisse First Boston Mortgage Securities Corp., Ser. 2005-TFLA, | ||||||

| Class K, AA+, Aaa, | |||||||

| 1.637%, 2/15/20 (a) (b) (d) | 1,123,473 | ||||||

| 1,500,000 | Credit Suisse Mortgage Capital Certificates, Ser. 2006-C3, Class AM, BBB-, Aaa, | ||||||

| 5.825%, 6/15/38 (a) (d) | 1,331,004 | ||||||

| 121,885 | Deutsche ALT-A Securities, Inc., Alternate Loan Trust, Ser. 2006-AB4, | ||||||

| Class A1A, D, Caa1, | |||||||

| 6.005%, 10/25/36 (d) | 76,221 | ||||||

| 2,000,000 | Greenwich Capital Commercial Funding Corp., Ser. 2005-GG3, | ||||||

| Class AJ, AAA, Aa2, | |||||||

| 4.859%, 8/10/42 (a) (d) | 1,694,853 | ||||||

| 1,000,000 | Greenwich Capital Commercial Funding Corp., Ser. 2005-GG5, | ||||||

| Class AJ, BBB, Aaa, | |||||||

| 5.301%, 4/10/37 (a) (d) | 822,963 | ||||||

| 600,000 | GS Mortgage Securities Corp. II, Ser. 2001-GL3A, Class E, NR, A3, | ||||||

| 6.852%, 8/5/18 (b) (d) | 578,637 | ||||||

| 1,039,312 | Indymac Index Mortgage Loan Trust, Ser. 2006-AR9, Class 3A1, AAA, B3, | ||||||

| 5.640%, 6/25/36 (d) | 827,340 | ||||||

| 700,000 | JP Morgan Chase Commercial Mortgage Securities Corp., Ser. 2002-C1, | ||||||

| Class E, A-, A2, | |||||||

| 6.135%, 7/12/37 (b) | 649,147 | ||||||

| 1,000,000 | JP Morgan Chase Commercial Mortgage Securities Corp., Ser. 2005-LDP3, | ||||||

| Class AJ, BBB, A2, | |||||||

| 4.965%, 8/15/42 (a) (d) | 816,448 | ||||||

| 2,600,000 | JP Morgan Chase Commercial Mortgage Securities Corp., Ser. 2007-LD11, | ||||||

| Class AM, BB+, A3, | |||||||

| 5.818%, 6/15/49 (a) (d) | 1,937,098 | ||||||

| 2,000,000 | Morgan Stanley Capital I, Ser. 2005-HQ6, Class AJ, A-, NR, | ||||||

| 5.073%, 8/13/42 (a) (d) | 1,756,896 | ||||||

| 1,000,000 | Morgan Stanley Capital I, Ser. 2006-HQ10, Class AM, NR, Aaa, | ||||||

| 5.360%, 11/12/41 (a) | 922,407 | ||||||

| 1,250,000 | Morgan Stanley Capital I, Ser. 2006-IQ12, Class AM, A, NR, | ||||||

| 5.370%, 12/15/43 (a) | 1,064,239 | ||||||

| 1,000,000 | Morgan Stanley Capital I, Ser. 2006-T23, Class AM, A+, NR, | ||||||

| 5.810%, 8/12/41 (a) (d) | 912,135 | ||||||

| 436,711 | New Century Home Equity Loan Trust, Ser. 2004-A, Class AII9, B, A2, | ||||||

| 5.364%, 8/25/34 (d) | 353,970 | ||||||

| 1,088,000 | TBW Mortgage Backed Pass Through Certificates, Ser. 2006-6, | ||||||

| Class A3, D, Caa2, | |||||||

| 5.750%, 1/25/37 (h) | 629,458 | ||||||

| 2,500,000 | TBW Mortgage Backed Pass Through Certificates, Ser. 2006-6, | ||||||

| Class A5B, D, Caa3, | |||||||

| 6.040%, 1/25/37 (h) | 1,169,860 | ||||||

See notes to financial statements.

14 | Annual Report | May 31, 2010

GOF | Claymore/Guggenheim Strategic Opportunities Fund | Portfolio of Investments continued

| Principal | |||||||

| Amount | Description | Value | |||||

| Collateralized Mortgage Obligations (continued) | |||||||

| $ | 2,000,000 | TIAA Seasoned Commercial Mortgage Trust, Ser. 2007-C4, Class AJ, A+, NR, | |||||

| 6.072%, 8/15/39 (d) | $ | 1,818,309 | |||||

| 750,000 | Timberstar Trust, Ser. 2006-1A, Class C, A, A3, | ||||||

| 5.884%, 10/15/36 (a) (b) | 764,954 | ||||||

| 2,000,000 | Wachovia Bank Commercial Mortgage Trust, Ser. 2005-C20, Class AJ, BBB-, Aaa, | ||||||

| 5.139%, 7/15/42 (a) (d) | 1,667,477 | ||||||

| 1,000,000 | Wachovia Bank Commercial Mortgage Trust, Ser. 2005-C21, Class AJ, A-, Aa2, | ||||||

| 5.208%, 10/15/44 (a) (d) | 873,269 | ||||||

| Total Collateralized Mortgage Obligations – 29.8% | |||||||

| (Cost $50,030,593) | 48,270,583 | ||||||

| Number | |||||||

| of Shares | Value | ||||||

| Preferred Stock – 2.8% | |||||||

| Banks – 1.3% | |||||||

| 40,000 | BB&T Capital Trust VI, 9.600% (a) | 1,111,200 | |||||

| 50,000 | Santander Finance Preferred SA Unipersonal, 6.500% (Spain) (a) | 990,500 | |||||

| 2,101,700 | |||||||

| Diversified Financial Services – 0.6% | |||||||

| 50,000 | Deutsche Bank Contingent Capital Trust II, 6.550% (a) | 1,009,500 | |||||

| 37,600 | Lehman Brothers Holdings, Inc., Ser. J, 7.950% (i) | 827 | |||||

| 1,010,327 | |||||||

| Insurance – 0.2% | |||||||

| 20,000 | Aegon NV, 6.375% (Netherlands) (a) | 341,400 | |||||

| 3,800 | ING Groep NV, 7.050% (Netherlands) (a) | 68,134 | |||||

| 409,534 | |||||||

| Telecommunication – 0.7% | |||||||

| 1,000 | Centaur Funding Corp., 9.080% (Cayman Islands) (b) | 1,058,437 | |||||

| Total Preferred Stock – 2.8% | |||||||

| (Cost $5,817,313) | 4,579,998 | ||||||

| Exchange-Traded Funds – 10.1% | |||||||

| 55,000 | Powershares QQQ (a) (j) | 2,509,100 | |||||

| 27,500 | ProShares Ultra Dow30 (a) (j) | 1,144,825 | |||||

| 100,000 | ProShares Ultra S&P500 (a) (j) | 3,624,000 | |||||

| 30,000 | SPDR Dow Jones Industrial Average ETF Trust (a) (j) | 3,044,100 | |||||

| 55,000 | SPDR S&P 500 ETF Trust (a) (j) | 6,019,200 | |||||

| Total Exchange-Traded Funds – 10.1% | |||||||

| (Cost $16,018,936) | 16,341,225 | ||||||

| Principal | |||||||

| Amount | Description | Value | |||||

| U.S. Government and Agency Securities – 1.2% | |||||||

| $ | 2,000,000 | Freddie Mac, Ser. 1, AAA, Aaa, | |||||

| 6.500%, 6/3/24 (a) (d) | |||||||

| (Cost $2,000,000) | $ | 1,960,000 | |||||

| Term Loans (k) – 3.1% | |||||||

| Consumer Products – 0.3% | |||||||

| 447,659 | Navisite, Inc., B-, B3, | ||||||

| 9.150%, 9/19/14 (d) | 425,276 | ||||||

| Electronics – 0.2% | |||||||

| 283,064 | Clientlogic Corp., B+, B3, | ||||||

| 5.795%, 1/30/14 (d) | 277,403 | ||||||

| Healthcare, Education & Childcare – 0.4% | |||||||

| 843,384 | Embanet, B, B2, | ||||||

| 3.310%, 6/28/12 (d) | 691,574 | ||||||

| Home & Office Furnishings – 0.4% | |||||||

| 692,502 | Centaur LLC, CCC+, B2, | ||||||

| 11.250%, 11/9/14 (d) | 626,715 | ||||||

| Leisure – 0.8% | |||||||

| 1,448,876 | Bushnell Performance Optics, BB-, Ba3, | ||||||

| 4.540%, 8/24/13 (d) | 1,372,810 | ||||||

| Retail Stores – 1.0% | |||||||

| 1,078,241 | Deb Shops, Inc., B-, B3, | ||||||

| 7.000%, 4/23/14 (d) | 733,204 | ||||||

| 972,500 | Mattress Firm, B, Ba3, | ||||||

| 2.690%, 10/23/14 (d) | 802,313 | ||||||

| 1,535,517 | |||||||

| Total Term Loans – 3.1% | |||||||

| (Cost $5,609,694) | 4,929,295 | ||||||

| Total Long-Term Investments – 131.7% | |||||||

| (Cost $212,113,651) | 213,127,235 | ||||||

See notes to financial statements.

Annual Report | May 31, 2010 | 15

GOF | Claymore/Guggenheim Strategic Opportunities Fund | Portfolio of Investments continued

| Expiration | Exercise | ||||||||||||||

| Contracts | Options Purchased | Date | Price | Value | |||||||||||

| Call Options Purchased – 0.0%* | |||||||||||||||

| 32 | CBOE S&P 500 Volatility Index (j) (l) (m) | ||||||||||||||

| (Cost $38,080) | June 2010 | $ | 20.00 | $ | 32,000 | ||||||||||

| Total Investments – 131.7% | |||||||||||||||

| (Cost $212,151,731) | 213,159,235 | ||||||||||||||

| Other Assets in excess of Liabilities - 11.3% | 18,332,722 | ||||||||||||||

| Total Options Written - (0.3%) | (591,684 | ) | |||||||||||||

| Borrowings - (16.6%) | (26,865,369 | ) | |||||||||||||

| Reverse Repurchase Agreements - (19.5%) | (31,621,245 | ) | |||||||||||||

| TALF Loan – (6.6%) | (10,630,271 | ) | |||||||||||||

| Net Assets Applicable to Common Shareholders - 100.0% | $ | 161,783,388 | |||||||||||||

* Less than 0.1%

AB - Stock Company

CBO - Collateralized Bond Obligation

CDO - Collateralized Debt Obligation

CLO - Collateralized Loan Obligation

FCB - Farmers Credit Bureau

LLC - Limited Liability Company

LP - Limited Partnership

N/A - Not Available

NV - Publicly Traded Company

PLC - Public Limited Company

SA - Corporation

| (a) | All or a portion of this security has been physically segregated in connection with swap agreements, line of credit, options and reverse repurchase agreements. As of May 31, 2010, the total amount segregated was $109,614,982. |

| (b) | Securities are exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At May 31, 2010, these securities amounted to $106,936,897 which represents 66.1% of net assets applicable to common shares. |

| (c) | Security has a fixed rate coupon which will convert to a floating or variable rate coupon on a future date. |

| (d) | Floating or Variable Rate Coupon. Rate shown is in effect at May 31, 2010. |

| (e) | Risk-Linked Security – A risk-linked security is a form of derivative issued by insurance companies and insurance related special purpose vehicles that apply securitization techniques to catastrophic property and casualty damages. The security is typically a debt obligation for which the return of principal and the payment of interest are contingent on the non-occurrence of a pre-defined “trigger event.” Depending on the specific terms and structure of the security, this trigger could be the result of a hurricane, earthquake or some other catastrophic event. |

| (f) | Security is valued in accordance with Fair Valuation procedures established in good faith by the Board of Trustees and is based, in part on significant unobservable inputs. The total market value of such securities is $4,631,900 which represents 2.9% of net assets applicable to common shares. |

| (g) | All or a portion of this security was acquired, and has been physically segregated in connection with the Fund’s participation in the Term Asset-Backed Securities Loan Facility program(the “TALF program”) operated by the Federal Reserve Bank of New York. As of May 31, 2010, the total amount physically segregated was $13,928,007. See notes to financial statements. |

| (h) | Security is a “step-up” bond where the coupon increases or steps up at a predetermined date. |

| (i) | Non-income producing as security is in default. |

| (j) | All or a portion of this security position represents cover for outstanding options written. |

| (k) | Term loans held by the Fund have a variable interest rate feature which is periodically adjusted based on an underlying interest rate benchmark. In addition, term loans may include mandatory and/or optional prepayment terms. As a result, the actual maturity dates of the loans may be different than the amounts disclosed in the portfolio of investments. Term loans may be considered restricted in that the Fund may be contractually obligated to receive approval from the Agent Bank and/or Borrower prior to the sale or disposition of loan. |

| (l) | Non-income producing security. |

| (m) | Represents 100 shares per contract. |

Ratings (unaudited) shown are per Standard & Poor’s and Moody’s. Securities classified as NR are not rated.

| Expiration | Exercise | ||||||||||||||

| Contracts | Options Written (l) | Date | Price | Value | |||||||||||

| Call Options Written – (0.3%) | |||||||||||||||

| 32 | CBOE S&P 500 Volatility Index (m) | June 2010 | $ | 30.00 | $ | 11,200 | |||||||||

| 550 | Powershares QQQ (m) | June 2010 | 46.00 | 52,525 | |||||||||||

| 275 | ProShares Ultra Dow30 (m) | June 2010 | 42.00 | 50,187 | |||||||||||

| 1,000 | ProShares Ultra S&P500 (m) | June 2010 | 37.00 | 151,500 | |||||||||||

| 900 | S&P 500 Index | June 2010 | 1,120.00 | 11,430 | |||||||||||

| 6,900 | S&P 500 Index | June 2010 | 1,100.00 | 151,800 | |||||||||||

| 300 | SPDR Dow Jones Industrial Average | ||||||||||||||

| ETF Trust (m) | June 2010 | 102.00 | 61,650 | ||||||||||||

| 550 | SPDR S&P 500 ETF Trust (m) | June 2010 | 111.00 | 101,200 | |||||||||||

| Total Value of Call Options Written | |||||||||||||||