|

UNITED STATES |

SECURITIES AND EXCHANGE COMMISSION |

Washington, D.C. 20549 |

|

FORM N-CSR |

|

CERTIFIED SHAREHOLDER REPORT OF REGISTERED |

MANAGEMENT INVESTMENT COMPANIES |

|

|

Investment Company Act file number | 811-21989 |

|

|

Nicholas-Applegate Equity & Convertible Income Fund |

(Exact name of registrant as specified in charter) |

|

|

1345 Avenue of the Americas, New York, | NY 10105 |

(Address of principal executive offices) | (Zip code) |

|

Lawrence G. Altadonna – 1345 Avenue of the Americas, New York, NY 10105 |

(Name and address of agent for service) |

|

|

Registrant’s telephone number, including area code: | 212-739-3371 |

|

|

|

Date of fiscal year: | January 31, 2010 |

|

|

|

Date of reporting period: | January 31, 2010 |

|

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-2001. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

ITEM 1. REPORT TO SHAREHOLDERS

|

|

|

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

|

| ||

| Nicholas-Applegate Equity & Convertible |

|

| Income Fund |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Annual Report |

|

| January 31, 2010 |

|

|

|

|

|

|

|

|

|

|

|

|

| Contents |

|

|

|

|

|

|

|

|

|

| 1 |

| |

|

|

|

|

|

|

| 2-5 |

| |

|

|

|

| |

| 6-18 |

| ||

|

|

|

| |

| 19 |

| ||

|

|

|

| |

| 20 |

| ||

|

|

|

| |

| 21 |

| ||

|

|

|

| |

| 22-30 |

| ||

|

|

|

| |

| 31-32 |

| ||

|

|

|

| |

| 33 |

| ||

|

|

|

| |

| 34 |

| ||

|

|

|

|

|

| Annual Shareholder Meeting Results/Changes in Board of Trustees |

| 35 |

|

|

|

|

|

|

|

| 36 |

| |

|

|

|

|

|

|

| 37 |

| |

|

|

|

|

|

|

| 38-39 |

| |

|

|

|

|

|

|

| 40 |

| |

|

|

|

|

|

|

| |||

|

NFJ Dividend, Interest & Premium Strategy Fund |

Nicholas-Applegate Equity & Convertible Income Fund Letter to Shareholders |

|

|

March 15, 2010 |

Dear Shareholder:

Please find enclosed the annual report for NFJ Dividend, Interest & Premium Strategy Fund and Nicholas-Applegate Equity & Convertible Income Fund (collectively the “Funds”) for the fiscal year ended January 31, 2010.

U.S. stocks advanced solidly during the fiscal period as investors moved capital into stocks and corporate bonds and away from lower yielding government bonds. The Russell 3000 Index, a broad measure of U.S. stock market performance, gained 35.05% during the twelve-month period. The Russell 1000 Value Index, a measure of large-cap value-style stocks, returned 31.44%; while its growth-style counterpart, the Russell 1000 Growth Index, advanced 37.85%. Convertible securities also rallied, as the Merrill Lynch All Convertibles Index advanced 46.62% during the twelve months ended January 31, 2010.

The Federal Reserve held the Federal Funds Rate, the key target rate on loans between member banks, to a historically low target range of 0.00% to 0.25% during the period and pursued other initiatives designed to inject liquidity into the financial system. Under its policy of quantitative easing, the U.S. monetary authority purchased large amounts of securities (such as mortgage-backed securities and U.S. Treasuries) from commercial banks to encourage lending to consumers and businesses.

Please refer to the following pages for specific information on the Funds. If you have any questions regarding the information provided, we encourage you to contact your financial advisor or call the Funds’ shareholder servicing agent at (800) 254-5197. You may also find a wide range of information and resources on our Web site, www.allianzinvestors.com/closedendfunds.

Together with Allianz Global Investors Fund Management LLC, the Funds’ investment manager, and NFJ Investment Group LLC, Nicholas-Applegate Capital Management LLC and Oppenheimer Capital LLC, the Funds’ sub-advisers, we thank you for investing with us.

We remain dedicated to serving your investment needs.

|

|

Sincerely, |

|

|

|

|

|

|

|

Hans W. Kertess | Brian S. Shlissel |

Chairman | President & Chief Executive Officer |

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

|

| 1.31.10 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 1 | |

|

NFJ Dividend, Interest & Premium Strategy Fund Fund Insights |

January 31, 2010 (unaudited) |

|

|

• | For the fiscal year ended January 31, 2010, the NFJ Dividend, Interest & Premium Strategy Fund returned 27.38% on net asset value and 17.31% on market price. |

|

|

• | U.S. equities advanced during the period. Among large cap value stocks, as represented by the Russell 1000 Value Index, all sectors posted positive returns. Index constituents in the recovering financials and consumer discretionary sectors contributed most significantly to overall gains for the index. On average, utility and energy companies underperformed the benchmark return. |

|

|

• | In energy, a gradual rise in crude oil prices during the period served to push share prices higher for exploration and production companies and for oilfield services firms. This benefited NFJ’s equity positions in offshore oil contractor Diamond Offshore Drilling and oilfield services firm Halliburton. Production-oriented energy company stocks are typically more sensitive to changes in energy commodity prices than are those of the larger, more vertically integrated refining and retail distribution companies. The Fund’s underweighting of integrated oil companies contributed to performance relative to the Russell 1000 Value Index for the period. |

|

|

• | In telecommunications, a position in wireless communications tower operator Crown Castle benefited performance relative to the Russell 1000 Value Index. During the period, the company delivered steady returns, outperforming the larger telecommunications services providers that waged a pitched battle for market share throughout the period. |

|

|

• | In the equity portion of the portfolio, underweight positions in financials and materials detracted from performance. |

|

|

• | After a solid fourth quarter in 2009, the convertible index enjoyed the best-performing year in history. The rally was constructive for the market, as it continued across all industries and qualities. Speculative grade issuers led performance over the time period and smaller-capitalized companies continued to outperform their large- and mid-cap counterparts While the underlying equity is starting to become a bigger driver of convertible performance, credit was the primary driver of convertible returns during the period. |

|

|

• | In addition to broad economic statistics and technical factors such as access to capital, corporate profits took center stage. Quarterly earnings reports were generally better than expected for the last two quarters of 2009. Initially, many companies performed better than they may have if not for more than a year of cost cutting initiatives. As the year progressed, demand emerged. |

|

|

• | In 2009, $37.2 billion was raised in the convertible new issuance market. In the first half of 2009, many companies accessed the corporate debt markets instead of the convertible markets in order to avoid shareholder dilution at depressed stock prices. As the equity markets gained during the second half of 2009, convertible new issuance increased. |

|

|

• | The Fund’s positions in the Automotive, Energy and Technology industries contributed to performance during the period. Automotive companies benefited from improved consumer demand and continued cost cutting. Ford Motor was a beneficiary. Energy companies were positive over the time period, as earnings and margins came in ahead of expectations. Chesapeake Energy and Whiting Petroleum benefited. Financial issuers Bank of America, Fifth Third Bancorp and Citigroup advanced as the companies improved their balance sheets and credit metric improved over the course of the year. |

|

|

• | The Fund’s positions in the Healthcare and Utility industries hindered relative performance during the reporting period due to rotation into higher beta industries. |

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

2 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 1.31.10 | |

|

NFJ Dividend, Interest & Premium Strategy Fund Performance & Statistics |

January 31, 2010 (unaudited) |

|

|

|

|

|

|

|

|

Total Return(1): |

| Market Price |

| Net Asset Value (“NAV”) | |||

1 year |

| 17.31 | % |

|

| 27.38 | % |

3 year |

| (10.53 | )% |

|

| (5.60 | )% |

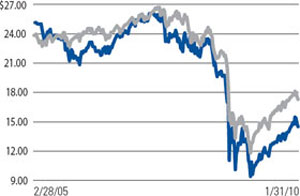

Commencement of Operations (2/28/05) to 1/31/10 |

| (2.83 | )% |

|

| 1.17 | % |

|

|

Market Price/NAV Performance: | |

Commencement of Operations (2/28/05) to 1/31/10 | |

| Market Price |

| NAV |

| |

|

|

|

|

|

Market Price/NAV: |

|

|

|

|

Market Price |

| $ | 14.50 |

|

NAV |

| $ | 17.30 |

|

Discount to NAV |

|

| (16.18 | )% |

Market Price Yield(2) |

|

| 4.14 | % |

|

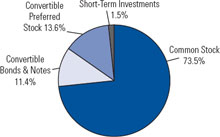

Investment Allocation |

|

(1) Past performance is no guarantee of future results. Total return is calculated by determining the percentage change in net asset value (“NAV”) or market price (as applicable) in the specified period. The calculation assumes that all income dividends and capital gain distributions, if any, have been reinvested. Total return does not reflect broker commissions or sales charges. Total return for a period of more than one year represents the average annual total return.

Performance at market price will differ from its results at NAV. Although market price returns typically reflect investment results over time, during shorter periods returns at market price can also be influenced by factors such as changing views about the Fund, market conditions, supply and demand for the Fund’s shares, or changes in Fund dividends.

An investment in the Fund involves risk, including the loss of principal. Total return, market price, market yield and NAV asset will fluctuate with changes in market conditions. This data is provided for information purposes only and is not intended for trading purposes. Closed-end funds, unlike open-end funds, are not continuously offered. There is a onetime public offering and once issued, shares of closed-end funds are sold in the open market through a stock exchange. NAV is equal to total assets attributable to shareholders less total liabilities divided by the number of shares outstanding. Holdings are subject to change daily.

(2) Market Price Yield is determined by dividing the annualized current quarterly per share distribution (comprised of net investment income and short-term capital gains, if any) payable to shareholders by the market price per share at January 31, 2010.

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

|

| 1.31.10 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 3 | |

|

Nicholas-Applegate Equity & Convertible Income Fund Fund Insights |

January 31, 2010 (unaudited) |

|

|

• | For the fiscal year ended January 31, 2010, the Nicholas-Applegate Equity & Convertible Income Fund returned 40.81% on net asset value and 30.75% on market price. |

|

|

• | During the period equity markets rebounded from the lows experienced in March 2009. In 2008, convertible investors endured the worst-performing year in history. After a solid fourth quarter in 2009, the convertible index enjoyed the best-performing year in history. |

|

|

• | The rally was constructive for the equity and credit markets, as it continued across all market capitalizations, industries and qualities. The largest-capitalized companies in the Russell 1000 Growth Index outperformed. Convertible speculative grade issuers led performance over the time period and smaller- capitalized convertible companies continued to outperform their large- and mid-cap counterparts. While underlying equity became a more prominent driver of convertible performance, credit was the primary driver of convertible returns during the reporting period. |

|

|

• | In addition to broad economic statistics and technical factors such as access to capital, corporate profits took center stage. Quarterly earnings reports were generally better than expected for the last two quarters of 2009. Initially, many companies performed better than they may have if not for more than a year of cost cutting initiatives. As the year progressed, demand emerged. |

|

|

• | Equity positions in the Technology, Energy and Automotive industries benefitted Fund performance over the reporting period. Technology companies benefited from better end market demand and leaner inventories in the semiconductor and software markets. Energy companies benefited from better earnings as a result of improved operating efficiencies and higher commodity prices. Companies in the automotive supply chain benefited from re-ramping production expectations and leaner operations. |

|

|

• | Convertible positions in the Automotive, Energy, and Financial industries bolstered Fund performance during the reporting period. Automotive companies benefited from improved consumer demand and continued cost cutting. Energy companies contributed to performance during the reporting period, as earnings and margins came in ahead of expectations. Financial issuers advanced as companies improved their balance sheets and credit metrics improved over the course of the year. |

|

|

• | The Fund’s equity and convertible positions in the Healthcare and Utilities industries detracted from performance during the period due to a rotation into higher beta industries. |

|

|

• | Expectations of market volatility, as measured by the Chicago Board Options Exchange Volatility Index (“VIX”), averaged 29.7. The VIX Index began the reporting period at the mid forties, and declined to the mid twenties during the reporting period. The Fund was opportunistic and able to capture call option premiums on both index and stock-specific call options. |

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

4 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 1.31.10 | |

|

Nicholas-Applegate Equity & Convertible Income Fund Performance & Statistics |

January 31, 2010 (unaudited) |

|

|

|

|

|

|

|

Total Return(1): |

| Market Price |

| Net Asset Value (“NAV”) | ||

1 Year |

| 30.75 | % |

| 40.81 | % |

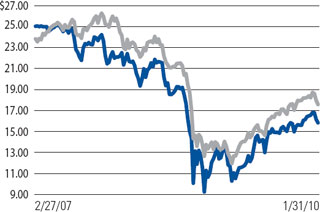

Commencement of Operations (2/27/07) to 1/31/10 |

| (5.71 | )% |

| (1.44 | )% |

|

|

Market Price/NAV Performance: | |

Commencement of Operations (2/27/07) to 1/31/10 | |

| Market Price |

| NAV |

| |

|

|

|

|

|

Market Price/NAV: |

|

|

|

|

Market Price |

| $ | 15.83 |

|

NAV |

| $ | 17.58 |

|

Discount to NAV |

|

| (9.95 | )% |

Market Price Yield(2) |

|

| 6.25 | % |

|

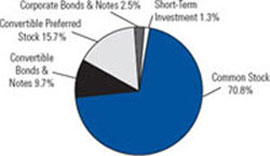

Investment Allocation |

|

(1) Past performance is no guarantee of future results. Total return is calculated by determining the percentage change in net asset value (“NAV”) or market price (as applicable) in the specified period. The calculation assumes that all income dividends and capital gain distributions, if any, have been reinvested. Total return does not reflect broker commissions or sales charges. Total return for a period of more than one year represents the average annual total return.

Performance at market price will differ from its results at NAV. Although market price returns typically reflect investment results over time, during shorter periods returns at market price can also be influenced by factors such as changing views about the Fund, market conditions, supply and demand for the Fund’s shares, or changes in Fund dividends.

An investment in the Fund involves risk, including the loss of principal. Total return, market price, market yield and NAV asset will fluctuate with changes in market conditions. This data is provided for information purposes only and is not intended for trading purposes. Closed-end funds, unlike open-end funds, are not continuously offered. There is a onetime public offering and once issued, shares of closed-end funds are sold in the open market through a stock exchange. NAV is equal to total assets attributable to shareholders less total liabilities divided by the number of shares outstanding. Holdings are subject to change daily.

(2) Market Price Yield is determined by dividing the annualized current quarterly per share distribution (comprised of net investment income and short-term capital gains, if any) payable to shareholders by the market price per share at January 31, 2010.

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

|

| 1.31.10 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 5 | |

|

NFJ Dividend, Interest & Premium Strategy Fund Schedule of Investments |

January 31, 2010 |

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

COMMON STOCK—74.0% |

|

|

| ||||

|

|

| Aerospace & Defense—2.6% |

|

|

|

|

| 700 |

| Boeing Co. (a) |

|

| $42,420,000 |

|

|

|

| Capital Markets—1.4% |

|

|

|

|

| 150 |

| Goldman Sachs Group, Inc. |

|

| 22,308,000 |

|

|

|

| Commercial Services & Supplies—1.6% |

|

|

|

|

| 400 |

| RR Donnelley & Sons Co. (a) |

|

| 7,928,000 |

|

| 573 |

| Waste Management, Inc. |

|

| 18,351,830 |

|

|

|

|

|

|

| 26,279,830 |

|

|

|

| Communications Equipment—0.5% |

|

|

|

|

| 200 |

| Harris Corp. |

|

| 8,584,000 |

|

|

|

| Diversified Financial Services—0.8% |

|

|

|

|

| 336 |

| JP Morgan Chase & Co. (a) |

|

| 13,083,334 |

|

|

|

| Diversified Telecommunication Services—8.2% |

|

|

|

|

| 1,200 |

| AT&T, Inc. (a) |

|

| 30,432,000 |

|

| 700 |

| CenturyTel, Inc. |

|

| 23,807,000 |

|

| 950 |

| Verizon Communications, Inc. (a) |

|

| 27,949,000 |

|

| 5,000 |

| Windstream Corp. (a) |

|

| 51,550,000 |

|

|

|

|

|

|

| 133,738,000 |

|

|

|

| Electric Utilities—1.1% |

|

|

|

|

| 204 |

| Edison International (a) |

|

| 6,797,280 |

|

| 152 |

| Entergy Corp. |

|

| 11,580,348 |

|

|

|

|

|

|

| 18,377,628 |

|

|

|

| Energy Equipment & Services—4.3% |

|

|

|

|

| 500 |

| Diamond Offshore Drilling, Inc. (a) |

|

| 45,765,000 |

|

| 810 |

| Halliburton Co. |

|

| 23,660,100 |

|

|

|

|

|

|

| 69,425,100 |

|

|

|

| Food & Drug Retailing—0.9% |

|

|

|

|

| 1,000 |

| SUPERVALU, Inc. |

|

| 14,710,000 |

|

|

|

| Food Products—1.1% |

|

|

|

|

| 633 |

| Kraft Foods, Inc.—Cl. A |

|

| 17,519,844 |

|

|

|

| Health Care Equipment & Supplies—0.5% |

|

|

|

|

| 200 |

| Medtronic, Inc. (a) |

|

| 8,578,000 |

|

|

|

| Household Durables—1.7% |

|

|

|

|

| 300 |

| Black & Decker Corp. (a) |

|

| 19,398,000 |

|

| 100 |

| Whirlpool Corp. |

|

| 7,518,000 |

|

|

|

|

|

|

| 26,916,000 |

|

|

|

| Household Products—1.3% |

|

|

|

|

| 350 |

| Kimberly-Clark Corp. |

|

| 20,786,500 |

|

|

|

| Industrial Conglomerates—2.4% |

|

|

|

|

| 200 |

| 3M Co. |

|

| 16,098,000 |

|

| 1,439 |

| General Electric Co. (a) |

|

| 23,137,785 |

|

|

|

|

|

|

| 39,235,785 |

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

6 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 1.31.10 | |

|

NFJ Dividend, Interest & Premium Strategy Fund Schedule of Investments |

January 31, 2010 |

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

| Insurance—6.2% |

|

|

|

|

| 700 |

| Allstate Corp. (a) |

|

| $20,951,000 |

|

| 1,303 |

| Lincoln National Corp. (a) |

|

| 32,017,908 |

|

| 680 |

| MetLife, Inc. |

|

| 24,016,223 |

|

| 490 |

| Travelers Cos, Inc. |

|

| 24,828,300 |

|

| 19 |

| XL Capital Ltd.—Cl. A |

|

| 322,487 |

|

|

|

|

|

|

| 102,135,918 |

|

|

|

| Leisure Equipment & Products—1.7% |

|

|

|

|

| 1,400 |

| Mattel, Inc. (a) |

|

| 27,608,000 |

|

|

|

| Machinery—1.3% |

|

|

|

|

| 400 |

| Caterpillar, Inc. (a) |

|

| 20,896,000 |

|

|

|

| Media—1.2% |

|

|

|

|

| 1,501 |

| CBS Corp.—Cl. B |

|

| 19,402,758 |

|

|

|

| Metals & Mining—1.3% |

|

|

|

|

| 325 |

| Freeport-McMoRan Copper & Gold, Inc. (a) |

|

| 21,674,250 |

|

|

|

| Multi-Utilities—1.3% |

|

|

|

|

| 800 |

| Ameren Corp. (a) |

|

| 20,440,000 |

|

|

|

| Office Electronics—1.1% |

|

|

|

|

| 2,125 |

| Xerox Corp. |

|

| 18,530,000 |

|

|

|

| Oil, Gas & Consumable Fuels—12.6% |

|

|

|

|

| 506 |

| Cenovus Energy, Inc. |

|

| 11,713,900 |

|

| 1,000 |

| Chesapeake Energy Corp. |

|

| 24,780,000 |

|

| 300 |

| Chevron Corp. (a) |

|

| 21,636,000 |

|

| 525 |

| ConocoPhillips (a) |

|

| 25,200,000 |

|

| 500 |

| EnCana Corp. |

|

| 15,295,000 |

|

| 900 |

| Marathon Oil Corp. (a) |

|

| 26,829,000 |

|

| 550 |

| Royal Dutch Shell PLC —Cl. A - ADR |

|

| 30,464,500 |

|

| 500 |

| Total SA - ADR |

|

| 28,795,000 |

|

| 1,200 |

| Valero Energy Corp. (a) |

|

| 22,104,000 |

|

|

|

|

|

|

| 206,817,400 |

|

|

|

| Pharmaceuticals—6.3% |

|

|

|

|

| 1,180 |

| GlaxoSmithKline PLC - ADR (a) |

|

| 46,035,701 |

|

| 169 |

| Johnson & Johnson |

|

| 10,599,327 |

|

| 2,500 |

| Pfizer, Inc. (a) |

|

| 46,650,000 |

|

|

|

|

|

|

| 103,285,028 |

|

|

|

| Real Estate Investment Trust—3.2% |

|

|

|

|

| 3,000 |

| Annaly Capital Management, Inc. |

|

| 52,140,000 |

|

|

|

| Specialty Retail—1.9% |

|

|

|

|

| 1,104 |

| Home Depot, Inc. (a) |

|

| 30,928,642 |

|

|

|

| Textiles, Apparel & Luxury Goods—0.9% |

|

|

|

|

| 200 |

| VF Corp. (a) |

|

| 14,406,000 |

|

|

|

| Thrifts & Mortgage Finance—3.6% |

|

|

|

|

| 2,000 |

| Hudson City Bancorp, Inc. (a) |

|

| 26,540,000 |

|

| 2,200 |

| New York Community Bancorp, Inc. (a) |

|

| 33,066,000 |

|

|

|

|

|

|

| 59,606,000 |

|

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

|

| 1.31.10 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 7 | |

|

NFJ Dividend, Interest & Premium Strategy Fund Schedule of Investments |

January 31, 2010 |

|

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Credit Rating |

| Value |

| ||

|

|

| Tobacco—3.0% |

|

|

|

|

|

|

| 1,300 |

| Altria Group, Inc. (a) |

|

|

|

| $25,818,000 |

|

| 450 |

| Reynolds American, Inc. (a) |

|

|

|

| 23,940,000 |

|

|

|

|

|

|

|

|

| 49,758,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Common Stock (cost- $1,501,533,438) |

|

|

|

| 1,209,590,017 |

|

|

|

|

|

|

|

|

|

|

|

CONVERTIBLE PREFERRED STOCK— 13.6% |

|

|

|

|

| ||||

|

|

| Airlines—0.0% |

|

|

|

|

|

|

| 24 |

| Continental Airlines Finance Trust II, 6.00%, 11/15/30 |

| Caa1/CCC |

|

| 620,575 |

|

|

|

| Capital Markets—0.2% |

|

|

|

|

|

|

|

|

| Lehman Brothers Holdings, Inc. (c)(g)(i), |

|

|

|

|

|

|

| 630 |

| 6.00%, 10/12/10, Ser. GIS (General Mills, Inc.) |

| WR/NR |

|

| 2,028,488 |

|

| 98 |

| 28.00%, 3/6/09, Ser. RIG (Transocean, Inc.) |

| WR/NR |

|

| 1,331,778 |

|

|

|

|

|

|

|

|

| 3,360,266 |

|

|

|

| Chemicals—0.3% |

|

|

|

|

|

|

| 130 |

| Celanese Corp., 4.25%, 2/1/10 (k) |

| NR/NR |

|

| 4,770,150 |

|

|

|

| Commercial Banks—0.9% |

|

|

|

|

|

|

| 42 |

| Fifth Third Bancorp, 8.50%, 6/30/13, Ser. G (k) |

| Baa3/BB |

|

| 5,742,326 |

|

| 10 |

| Wells Fargo & Co., 7.50%, 3/15/13, Ser. L (k) |

| Ba1/A- |

|

| 9,096,090 |

|

|

|

|

|

|

|

|

| 14,838,416 |

|

|

|

| Commercial Services & Supplies—0.4% |

|

|

|

|

|

|

| 62 |

| Avery Dennison Corp., 7.875%, 11/15/20 |

| NR/BB+ |

|

| 2,259,350 |

|

| 161 |

| United Rentals, Inc., 6.50%, 8/1/28 |

| Caa2/CCC |

|

| 4,562,842 |

|

|

|

|

|

|

|

|

| 6,822,192 |

|

|

|

| Consumer Finance—0.5% |

|

|

|

|

|

|

| 16 |

| SLM Corp., 7.25%, 12/15/10 |

| Ba3/BB- |

|

| 9,008,220 |

|

|

|

| Diversified Financial Services—4.5% |

|

|

|

|

|

|

|

|

| Bank of America Corp., |

|

|

|

|

|

|

| 10 |

| 7.25%, 1/30/13, Ser. L (k) |

| Ba3/BB |

|

| 8,597,500 |

|

| 189 |

| 10.00%, 2/3/11 (Gilead Sciences, Inc.) (i) |

| A2/A |

|

| 9,011,357 |

|

| 102 |

| Citigroup, Inc., 7.50%, 12/15/12 |

| NR/NR |

|

| 10,621,264 |

|

|

|

| Credit Suisse Securities USA LLC (i), |

|

|

|

|

|

|

| 367 |

| 10.00%, 9/1/10 (Bristol-Myers Squibb Co.) |

| Aa2/A- |

|

| 8,270,661 |

|

| 239 |

| 10.00%, 9/9/10 (Merck & Co., Inc.) |

| Aa2/A- |

|

| 8,008,291 |

|

| 879 |

| 10.00%, 1/22/11 (Ford Motor Co.) |

| Aa2/A- |

|

| 9,730,530 |

|

|

|

| JP Morgan Chase & Co. (i), |

|

|

|

|

|

|

| 577 |

| 10.00%, 1/14/11 (EMC Corp.) |

| Aa3/A+ |

|

| 9,828,914 |

|

| 518 |

| 10.00%, 1/20/11 (Symantec Corp.) |

| Aa3/A+ |

|

| 9,074,995 |

|

|

|

|

|

|

|

|

| 73,143,512 |

|

|

|

| Electric Utilities—0.0% |

|

|

|

|

|

|

| 18 |

| FPL Group, Inc., 8.375%, 6/1/12 |

| NR/NR |

|

| 925,650 |

|

|

|

| Food Products—0.9% |

|

|

|

|

|

|

| 99 |

| Archer-Daniels-Midland Co., 6.25%, 6/1/11 |

| NR/BBB+ |

|

| 4,262,973 |

|

|

|

| Bunge Ltd., |

|

|

|

|

|

|

| 96 |

| 4.875%, 12/1/11 (k) |

| Ba1/BB |

|

| 8,466,756 |

|

| 4 |

| 5.125%, 12/1/10 |

| NR/BB |

|

| 2,370,000 |

|

|

|

|

|

|

|

|

| 15,099,729 |

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

8 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 1.31.10 | |

January 31, 2010

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Credit Rating |

| Value |

| ||

|

|

| Household Durables—1.1% |

|

|

|

|

|

|

| 98 |

| Newell Financial Trust I, 5.25%, 4/19/10 |

| NR/BB |

|

| $3,438,738 |

|

| 16 |

| Stanley Works, 5.125%, 5/17/12 (h) |

| A3/BBB+ |

|

| 14,304,100 |

|

|

|

|

|

|

|

|

| 17,742,838 |

|

|

|

| Insurance—0.8% |

|

|

|

|

|

|

| 39 |

| Assured Guaranty Ltd., 8.50%, 6/1/12 |

| NR/NR |

|

| 3,616,305 |

|

| 347 |

| XL Capital Ltd., 10.75%, 8/15/11 |

| Baa2/BBB- |

|

| 8,984,745 |

|

|

|

|

|

|

|

|

| 12,601,050 |

|

|

|

| Media—0.2% |

|

|

|

|

|

|

| 4 |

| Interpublic Group of Cos, 5.25%, 10/15/10 (k) |

| NR/CCC+ |

|

| 2,993,550 |

|

|

|

| Metals & Mining—0.6% |

|

|

|

|

|

|

| 82 |

| Freeport-McMoRan Copper & Gold, Inc., 6.75%, 5/1/10 |

| NR/BB |

|

| 8,055,671 |

|

|

|

| Vale Capital Ltd., |

|

|

|

|

|

|

| 21 |

| 5.50%, 6/15/10, Ser. RIO (Compania Vale do Rio Doce) (i) |

| NR/NR |

|

| 1,085,875 |

|

|

|

|

|

|

|

|

| 9,141,546 |

|

|

|

| Multi-Utilities—0.7% |

|

|

|

|

|

|

| 244 |

| AES Trust III, 6.75%, 10/15/29 |

| B3/B |

|

| 11,179,780 |

|

|

|

| Oil, Gas & Consumable Fuels—0.7% |

|

|

|

|

|

|

| 45 |

| ATP Oil & Gas Corp., 8.00%, 10/1/14 (e)(f)(k) |

| NR/NR |

|

| 4,042,088 |

|

| 85 |

| Chesapeake Energy Corp., 5.00%, 11/15/10 (k) |

| NR/B |

|

| 7,220,750 |

|

|

|

|

|

|

|

|

| 11,262,838 |

|

|

|

| Pharmaceuticals—0.6% |

|

|

|

|

|

|

| 39 |

| Merck & Co., Inc., 6.00%, 8/13/10 |

| A2/A- |

|

| 9,880,943 |

|

|

|

| Real Estate Investment Trust—1.2% |

|

|

|

|

|

|

| 177 |

| Alexandria Real Estate Equities, Inc., 7.00%, 4/20/13 (k) |

| NR/NR |

|

| 3,801,200 |

|

| 602 |

| FelCor Lodging Trust, Inc., 1.95%, 12/31/49, Ser. A (c) |

| Caa3/C |

|

| 7,409,520 |

|

| 131 |

| Simon Property Group, Inc., 6.00%, 4/14/10, Ser. I (k) |

| Baa1/BBB |

|

| 8,078,770 |

|

|

|

|

|

|

|

|

| 19,289,490 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Convertible Preferred Stock (cost-$260,139,740) |

|

|

|

| 222,680,745 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CONVERTIBLE BONDS & NOTES — 11.5% | |||||||||

|

|

|

|

|

|

|

|

|

|

Principal |

|

|

|

|

|

|

|

| |

|

|

| Auto Components—0.2% |

|

|

|

|

|

|

$ | 2,200 |

| BorgWarner, Inc., 3.50%, 4/15/12 |

| NR/BBB |

|

| 2,769,250 |

|

|

|

| Automobiles—0.2% |

|

|

|

|

|

|

| 3,000 |

| Ford Motor Co., 4.25%, 12/15/36 |

| Caa1/CCC |

|

| 4,027,500 |

|

|

|

| Commercial Services & Supplies—0.5% |

|

|

|

|

|

|

| 7,000 |

| Covanta Holding Corp., 3.25%, 6/1/14 (e)(f) |

| Ba3/B |

|

| 7,910,000 |

|

|

|

| Communications Equipment—0.2% |

|

|

|

|

|

|

| 2,000 |

| Finisar Corp., 5.00%, 10/15/29 (e)(f) |

| NR/NR |

|

| 2,450,000 |

|

|

|

| Computers & Peripherals—0.6% |

|

|

|

|

|

|

| 8,125 |

| Maxtor Corp., 2.375%, 8/15/12 |

| NR/B |

|

| 9,018,750 |

|

|

|

| Diversified Consumer Services—0.1% |

|

|

|

|

|

|

| 2,000 |

| Coinstar, Inc., 4.00%, 9/1/14 |

| NR/BB |

|

| 1,925,000 |

|

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

|

| | 1.31.10 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 9 |

January 31, 2010

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Principal |

|

|

| Credit Rating |

| Value |

| ||

|

|

| Diversified Telecommunication Services—0.4% |

|

|

|

|

|

|

$ | 6,495 |

| tw telecom, Inc., 2.375%, 4/1/26 |

| B3/B- |

|

| $6,754,800 |

|

|

|

| Electrical Equipment—1.7% |

|

|

|

|

|

|

| 9,780 |

| EnerSys, 3.375%, 6/1/38 (d) |

| B2/BB |

|

| 8,410,800 |

|

| 7,510 |

| General Cable Corp., 0.875%, 11/15/13 |

| Ba3/B+ |

|

| 6,590,025 |

|

| 14,000 |

| JA Solar Holdings Co., Ltd., 4.50%, 5/15/13 |

| NR/NR |

|

| 11,532,500 |

|

| 1,000 |

| SunPower Corp., 4.75%, 4/15/14 |

| NR/NR |

|

| 1,041,250 |

|

|

|

|

|

|

|

|

| 27,574,575 |

|

|

|

| Energy Equipment & Services—0.4% |

|

|

|

|

|

|

| 8,480 |

| Hornbeck Offshore Services, Inc., 1.625%, 11/15/26 (d) |

| NR/BB- |

|

| 7,009,568 |

|

|

|

| Health Care Equipment & Supplies—0.2% |

|

|

|

|

|

|

| 1,000 |

| China Medical Technologies, Inc., 4.00%, 8/15/13, Ser. CMT |

| NR/NR |

|

| 618,750 |

|

| 3,000 |

| Inverness Medical Innovations, Inc., 3.00%, 5/15/16 |

| NR/B- |

|

| 3,420,000 |

|

|

|

|

|

|

|

|

| 4,038,750 |

|

|

|

| Hotels, Restaurants & Leisure—0.5% |

|

|

|

|

|

|

| 5,495 |

| International Game Technology, 3.25%, 5/1/14 (e)(f) |

| Baa2/BBB |

|

| 6,525,313 |

|

| 1,402 |

| Mandalay Resort Group, 1.003%, 3/21/33 (c)(g)(h) |

| Caa2/CCC+ |

|

| 1,513,970 |

|

|

|

|

|

|

|

|

| 8,039,283 |

|

|

|

| Household Durables—0.1% |

|

|

|

|

|

|

| 750 |

| Newell Rubbermaid, Inc., 5.50%, 3/15/14 |

| NR/BBB- |

|

| 1,295,625 |

|

|

|

| Internet Software & Services—0.3% |

|

|

|

|

|

|

| 4,200 |

| Equinix, Inc., 2.50%, 4/15/12 |

| NR/B- |

|

| 4,431,000 |

|

|

|

| IT Services—0.8% |

|

|

|

|

|

|

|

|

| Alliance Data Systems Corp., |

|

|

|

|

|

|

| 8,020 |

| 1.75%, 8/1/13 |

| NR/NR |

|

| 7,739,300 |

|

| 2,000 |

| 4.75%, 5/15/14 (e)(f) |

| NR/NR |

|

| 2,867,500 |

|

| 2,540 |

| DST Systems, Inc., 4.125%, 8/15/23 |

| NR/NR |

|

| 2,797,175 |

|

|

|

|

|

|

|

|

| 13,403,975 |

|

|

|

| Machinery—0.4% |

|

|

|

|

|

|

| 6,035 |

| AGCO Corp., 1.25%, 12/15/36 |

| NR/BB |

|

| 6,193,419 |

|

|

|

| Media—0.2% |

|

|

|

|

|

|

| 3,765 |

| Liberty Media LLC, 3.125%, 3/30/23 |

| B1/BB- |

|

| 3,906,187 |

|

|

|

| Metals & Mining—0.6% |

|

|

|

|

|

|

| 2,500 |

| Steel Dynamics, Inc., 5.125%, 6/15/14 |

| NR/BB+ |

|

| 2,887,500 |

|

| 4,000 |

| United States Steel Corp., 4.00%, 5/15/14 |

| Ba3/BB |

|

| 6,310,000 |

|

|

|

|

|

|

|

|

| 9,197,500 |

|

|

|

| Oil, Gas & Consumable Fuels—0.8% |

|

|

|

|

|

|

| 3,500 |

| Chesapeake Energy Corp., 2.50%, 5/15/37 |

| Ba3/BB |

|

| 2,988,125 |

|

| 9,675 |

| Peabody Energy Corp., 4.75%, 12/15/41 |

| Ba3/B+ |

|

| 9,662,906 |

|

|

|

|

|

|

|

|

| 12,651,031 |

|

|

|

| Pharmaceuticals—0.6% |

|

|

|

|

|

|

| 5,500 |

| Biovail Corp., 5.375%, 8/1/14 (e)(f) |

| NR/NR |

|

| 6,551,875 |

|

| 3,000 |

| Valeant Pharmaceuticals International, 4.00%, 11/15/13 |

| NR/B- |

|

| 3,682,500 |

|

|

|

|

|

|

|

|

| 10,234,375 |

|

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

|

10 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 1.31.10 | |

|

January 31, 2010

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Principal |

|

|

| Credit Rating |

| Value |

| ||

|

|

| Real Estate Investment Trust—1.1% |

|

|

|

|

|

|

$ | 2,950 |

| Boston Properties LP, 3.75%, 5/15/36 |

| NR/A- |

|

| $2,975,812 |

|

| 45 |

| Developers Diversified Realty Corp., 3.00%, 3/15/12 |

| NR/BB |

|

| 41,963 |

|

| 5,800 |

| Digital Realty Trust LP, 4.125%, 8/15/26 (e)(f) |

| NR/NR |

|

| 8,783,375 |

|

| 5,000 |

| Health Care REIT, Inc., 4.75%, 12/1/26 |

| Baa2/BBB- |

|

| 5,468,750 |

|

|

|

|

|

|

|

|

| 17,269,900 |

|

|

|

| Road & Rail—0.1% |

|

|

|

|

|

|

| 1,500 |

| Hertz Global Holdings, Inc., 5.25%, 6/1/14 |

| NR/CCC+ |

|

| 2,175,000 |

|

|

|

| Semiconductors & Semiconductor Equipment—0.7% |

|

|

|

|

|

|

| 11,785 |

| Advanced Micro Devices, Inc., 5.75%, 8/15/12 |

| NR/B- |

|

| 11,637,687 |

|

|

|

| Software—0.8% |

|

|

|

|

|

|

| 5,000 |

| Lawson Software, Inc., 2.50%, 4/15/12 |

| NR/NR |

|

| 4,950,000 |

|

| 8,500 |

| Nuance Communications, Inc., 2.75%, 8/15/27 |

| NR/B- |

|

| 8,893,125 |

|

|

|

|

|

|

|

|

| 13,843,125 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Convertible Bonds & Notes (cost-$180,737,461) |

|

|

|

| 187,756,300 |

|

|

|

|

|

|

|

|

|

|

|

SHORT-TERM INVESTMENTS—1.5% | |||||||||

| |||||||||

|

|

| Time Deposits—1.5% |

|

|

|

|

|

|

| 14,616 |

| Bank of America-Toronto, 0.03%, 2/1/10 |

|

|

|

| 14,615,822 |

|

| 10,433 |

| Societe Generale-Paris, 0.03%, 2/1/10 |

|

|

|

| 10,433,148 |

|

|

|

| (cost-$25,048,970) |

|

|

|

| 25,048,970 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Investments, before call options written |

|

|

|

|

|

|

|

|

| (cost-$1,967,459,609—100.6%) |

|

|

|

| 1,645,076,032 |

|

|

|

|

|

|

|

|

|

|

|

CALL OPTIONS WRITTEN (b)—(0.4)% | |||||||||

| |||||||||

Contracts |

|

|

|

|

|

|

|

| |

|

|

| American Stock Exchange Morgan Stanley Cyclical Index, |

|

|

|

|

|

|

| 400 |

| strike price $880, expires 3/19/10 |

|

|

|

| (160,000 | ) |

|

|

| iShares Dow Jones U.S. Telecommunications, |

|

|

|

|

|

|

| 20,000 |

| strike price $19, expires 3/19/10 |

|

|

|

| (600,000 | ) |

|

|

| Morgan Stanley Cyclical Flex Index, |

|

|

|

|

|

|

| 400 |

| strike price $840, expires 2/5/10 |

|

|

|

| (2,080 | ) |

| 400 |

| strike price $865, expires 2/12/10 |

|

|

|

| (5,560 | ) |

| 350 |

| strike price $920, expires 3/5/10 |

|

|

|

| (7,735 | ) |

| 350 |

| strike price $925, expires 3/12/10 |

|

|

|

| (14,070 | ) |

|

|

| Morgan Stanley Cyclical Index |

|

|

|

|

|

|

| 400 |

| strike price $870, expires 2/19/10 |

|

|

|

| (164,000 | ) |

|

|

| New York Stock Exchange Arca Mini Oil Flex Index, |

|

|

|

|

|

|

| 6,000 |

| strike price $54, expires 2/12/10 |

|

|

|

| (24,000 | ) |

| 6,000 |

| strike price $55, expires 2/5/10 |

|

|

|

| — |

|

| 6,000 |

| strike price $56, expires 3/5/10 |

|

|

|

| (59,400 | ) |

| 6,000 |

| strike price $56, expires 3/12/10 |

|

|

|

| (91,800 | ) |

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

|

| | 1.31.10 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 11 |

January 31, 2010

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contracts |

|

|

|

|

| Value |

| ||

|

|

| New York Stock Exchange Arca Mini Oil Index, |

|

|

|

|

|

|

| 1,500 |

| strike price $52.50, expires 3/19/10 |

|

|

|

| $(172,500 | ) |

| 15,000 |

| strike price $55, expires 2/19/10 |

|

|

|

| (375,000 | ) |

| 4,500 |

| strike price $55, expires 3/19/10 |

|

|

|

| (157,500 | ) |

| 3,000 |

| strike price $57.50, expires 2/19/10 |

|

|

|

| (90,000 | ) |

|

|

| Philadelphia Stock Exchange KBW Bank Flex Index, |

|

|

|

|

|

|

| 7,000 |

| strike price $49.50, expires 3/12/10 |

|

|

|

| (589,400 | ) |

|

|

| Philadelphia Stock Exchange KBW Bank Index, |

|

|

|

|

|

|

| 2,000 |

| strike price $45, expires 2/19/10 |

|

|

|

| (485,000 | ) |

| 5,000 |

| strike price $46, expires 2/19/10 |

|

|

|

| (875,000 | ) |

| 9,500 |

| strike price $50, expires 3/19/10 |

|

|

|

| (878,750 | ) |

| 9,500 |

| strike price $51, expires 3/19/10 |

|

|

|

| (641,250 | ) |

|

|

| Standard & Poor’s 500 Flex Index, |

|

|

|

|

|

|

| 300 |

| strike price $1125, expires 2/12/10 |

|

|

|

| (25,530 | ) |

| 300 |

| strike price $1130, expires 2/5/10 |

|

|

|

| — |

|

| 250 |

| strike price $1160, expires 3/5/10 |

|

|

|

| (43,550 | ) |

|

|

| Standard & Poor’s 500 Index, |

|

|

|

|

|

|

| 300 |

| strike price $1120, expires 3/19/10 |

|

|

|

| (363,000 | ) |

| 300 |

| strike price $1130, expires 2/19/10 |

|

|

|

| (81,000 | ) |

| 600 |

| strike price $1130, expires 3/19/10 |

|

|

|

| (558,000 | ) |

| 300 |

| strike price $1135, expires 2/19/10 |

|

|

|

| (64,500 | ) |

|

|

| Total Call Options Written (premiums received-$15,703,026) |

|

|

|

| (6,528,625 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

| Total Investments, net of call options written |

|

|

|

|

|

|

|

|

| (cost-$1,951,756,583)—100.2% |

|

|

|

| 1,638,547,407 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Other liabilities in excess of other assets—(0.2)% |

|

|

|

| (2,819,805 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

| Net Assets—100.0% |

|

|

|

| $1,635,727,602 |

|

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

|

12 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 1.31.10 | |

|

January 31, 2010

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares |

|

|

|

|

| Value |

| ||

COMMON STOCK—70.7% |

|

|

|

|

|

| |||

|

|

| Aerospace & Defense—1.6% |

|

|

|

|

|

|

| 74 |

| L-3 Communications Holdings, Inc. |

|

|

|

| $6,192,162 |

|

|

|

| Auto Components—1.6% |

|

|

|

|

|

|

| 226 |

| Johnson Controls, Inc. |

|

|

|

| 6,286,797 |

|

|

|

| Automobiles—1.4% |

|

|

|

|

|

|

| 497 |

| Ford Motor Co. (a)(b) |

|

|

|

| 5,391,816 |

|

|

|

| Beverages—5.1% |

|

|

|

|

|

|

| 149 |

| Coca-Cola Co. (a) |

|

|

|

| 8,056,125 |

|

| 127 |

| Molson Coors Brewing Co.—Cl. B |

|

|

|

| 5,346,600 |

|

| 114 |

| PepsiCo, Inc. |

|

|

|

| 6,796,680 |

|

|

|

|

|

|

|

|

| 20,199,405 |

|

|

|

| Biotechnology—2.0% |

|

|

|

|

|

|

| 164 |

| Gilead Sciences, Inc. (b) |

|

|

|

| 7,916,280 |

|

|

|

| Communications Equipment—6.0% |

|

|

|

|

|

|

| 39 |

| Aviat Networks, Inc. (b) |

|

|

|

| 277,735 |

|

| 314 |

| Cisco Systems, Inc. (b) |

|

|

|

| 7,048,839 |

|

| 156 |

| Harris Corp. |

|

|

|

| 6,674,060 |

|

| 142 |

| Qualcomm, Inc. |

|

|

|

| 5,557,142 |

|

| 61 |

| Research In Motion Ltd. (b) |

|

|

|

| 3,827,968 |

|

|

|

|

|

|

|

|

| 23,385,744 |

|

|

|

| Computers & Peripherals—4.7% |

|

|

|

|

|

|

| 25 |

| Apple, Inc. (a)(b) |

|

|

|

| 4,879,848 |

|

| 379 |

| EMC Corp. (a)(b) |

|

|

|

| 6,311,262 |

|

| 58 |

| International Business Machines Corp. (a) |

|

|

|

| 7,061,903 |

|

|

|

|

|

|

|

|

| 18,253,013 |

|

|

|

| Diversified Financial Services—0.8% |

|

|

|

|

|

|

| 84 |

| JP Morgan Chase & Co. |

|

|

|

| 3,263,172 |

|

|

|

| Diversified Telecommunication Services—1.5% |

|

|

|

|

|

|

| 202 |

| Verizon Communications, Inc. |

|

|

|

| 5,942,840 |

|

|

|

| Electric Utilities—1.1% |

|

|

|

|

|

|

| 54 |

| Entergy Corp. |

|

|

|

| 4,136,154 |

|

|

|

| Electronic Equipment, Instruments & Components—1.5% |

|

|

|

|

|

|

| 149 |

| Amphenol Corp.—Cl. A |

|

|

|

| 5,936,160 |

|

|

|

| Energy Equipment & Services—3.9% |

|

|

|

|

|

|

| 69 |

| Diamond Offshore Drilling, Inc. |

|

|

|

| 6,306,417 |

|

| 96 |

| National Oilwell Varco, Inc. |

|

|

|

| 3,918,220 |

|

| 81 |

| Schlumberger Ltd. |

|

|

|

| 5,165,644 |

|

|

|

|

|

|

|

|

| 15,390,281 |

|

|

|

| Health Care Equipment & Supplies—3.9% |

|

|

|

|

|

|

| 111 |

| Baxter International, Inc. |

|

|

|

| 6,398,249 |

|

| 27 |

| Intuitive Surgical, Inc. (b) |

|

|

|

| 8,847,778 |

|

|

|

|

|

|

|

|

| 15,246,027 |

|

|

|

| Health Care Providers & Services—4.2% |

|

|

|

|

|

|

| 140 |

| McKesson Corp. (a) |

|

|

|

| 8,234,800 |

|

| 133 |

| Medco Health Solutions, Inc. (a)(b) |

|

|

|

| 8,152,248 |

|

|

|

|

|

|

|

|

| 16,387,048 |

|

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

|

| 1.31.10 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 13 | |

January 31, 2010

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares |

|

|

|

|

| Value |

| ||

|

|

| Hotels Restaurants & Leisure—1.9% |

|

|

|

|

|

|

| 119 |

| McDonald’s Corp. (a) |

|

|

|

| $7,410,441 |

|

|

|

| Household Products—1.9% |

|

|

|

|

|

|

| 121 |

| Procter & Gamble Co. (a) |

|

|

|

| 7,472,170 |

|

|

|

| Independent Power Producers & Energy Traders—1.7% |

|

|

|

|

|

|

| 92 |

| Constellation Energy Group, Inc. |

|

|

|

| 2,969,760 |

|

| 154 |

| NRG Energy, Inc. (b) |

|

|

|

| 3,712,916 |

|

|

|

|

|

|

|

|

| 6,682,676 |

|

|

|

| Industrial Conglomerates—1.5% |

|

|

|

|

|

|

| 122 |

| General Electric Co. |

|

|

|

| 1,969,141 |

|

| 209 |

| Textron, Inc. (a) |

|

|

|

| 4,079,817 |

|

|

|

|

|

|

|

|

| 6,048,958 |

|

|

|

| Insurance—1.6% |

|

|

|

|

|

|

| 53 |

| MetLife, Inc. |

|

|

|

| 1,878,459 |

|

| 87 |

| Prudential Financial, Inc. |

|

|

|

| 4,349,130 |

|

|

|

|

|

|

|

|

| 6,227,589 |

|

|

|

| Internet Software & Services—1.9% |

|

|

|

|

|

|

| 14 |

| Google, Inc.—Cl. A (a)(b) |

|

|

|

| 7,411,880 |

|

|

|

| Machinery—4.2% |

|

|

|

|

|

|

| 176 |

| AGCO Corp. (a)(b) |

|

|

|

| 5,430,887 |

|

| 101 |

| Deere & Co. |

|

|

|

| 5,039,955 |

|

| 133 |

| Joy Global, Inc. (a) |

|

|

|

| 6,101,716 |

|

|

|

|

|

|

|

|

| 16,572,558 |

|

|

|

| Metals & Mining—1.8% |

|

|

|

|

|

|

| 105 |

| Freeport-McMoRan Copper & Gold, Inc. |

|

|

|

| 7,015,788 |

|

|

|

| Multiline Retail—1.8% |

|

|

|

|

|

|

| 139 |

| Target Corp. |

|

|

|

| 7,106,022 |

|

|

|

| Oil, Gas & Consumable Fuels—3.1% |

|

|

|

|

|

|

| 90 |

| Occidental Petroleum Corp. |

|

|

|

| 7,034,932 |

|

| 121 |

| Peabody Energy Corp. (a) |

|

|

|

| 5,100,732 |

|

|

|

|

|

|

|

|

| 12,135,664 |

|

|

|

| Pharmaceuticals—2.9% |

|

|

|

|

|

|

| 137 |

| Abbott Laboratories |

|

|

|

| 7,252,780 |

|

| 63 |

| Johnson & Johnson |

|

|

|

| 3,978,284 |

|

|

|

|

|

|

|

|

| 11,231,064 |

|

|

|

| Semiconductors & Semiconductor Equipment—3.4% |

|

|

|

|

|

|

| 355 |

| Intel Corp. (a) |

|

|

|

| 6,877,300 |

|

| 289 |

| Texas Instruments, Inc. |

|

|

|

| 6,498,000 |

|

|

|

|

|

|

|

|

| 13,375,300 |

|

|

|

| Software—3.7% |

|

|

|

|

|

|

| 261 |

| Microsoft Corp. (a) |

|

|

|

| 7,340,890 |

|

| 305 |

| Oracle Corp. (a) |

|

|

|

| 7,035,606 |

|

|

|

|

|

|

|

|

| 14,376,496 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Common Stock (cost-$374,808,443) |

|

|

|

| 276,993,505 |

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

14 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 1.31.10 | |

January 31, 2010

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Credit Rating |

| Value |

| ||

CONVERTIBLE PREFERRED STOCK—15.7% |

|

|

|

|

|

| |||

|

|

| Capital Markets—0.3% |

|

|

|

|

|

|

|

|

| Lehman Brothers Holdings, Inc. (c)(g)(i), |

|

|

|

|

|

|

| 209 |

| 6.00%, 10/12/10, Ser. GIS (General Mills, Inc.) |

| WR/NR |

|

| $673,534 |

|

| 33 |

| 28.00%, 3/6/09, Ser. RIG (Transocean, Inc.) |

| WR/NR |

|

| 455,286 |

|

|

|

|

|

|

|

|

| 1,128,820 |

|

|

|

| Chemicals—0.5% |

|

|

|

|

|

|

| 49 |

| Celanese Corp., 4.25%, 2/1/10 (k) |

| NR/NR |

|

| 1,782,375 |

|

|

|

| Commercial Banks—1.1% |

|

|

|

|

|

|

| 14 |

| Fifth Third Bancorp, 8.50%, 6/30/13, Ser. G (k) |

| Baa3/BB |

|

| 1,957,455 |

|

| 3 |

| Wells Fargo & Co., 7.50%, 3/15/13, Ser. L (k) |

| Ba1/A- |

|

| 2,545,020 |

|

|

|

|

|

|

|

|

| 4,502,475 |

|

|

|

| Commercial Services & Supplies—1.2% |

|

|

|

|

|

|

| 49 |

| Avery Dennison Corp., 7.875%, 11/15/20 |

| NR/BB+ |

|

| 1,788,500 |

|

| 102 |

| United Rentals, Inc., 6.50%, 8/1/28 |

| Caa2/CCC |

|

| 2,900,615 |

|

|

|

|

|

|

|

|

| 4,689,115 |

|

|

|

| Consumer Finance—0.6% |

|

|

|

|

|

|

| 4 |

| SLM Corp., 7.25%, 12/15/10 |

| Ba3/BB- |

|

| 2,309,800 |

|

|

|

| Diversified Financial Services—3.0% |

|

|

|

|

|

|

| 4 |

| Bank of America Corp., 7.25%, 1/30/13, Ser. L (k) |

| Ba3/BB |

|

| 3,823,625 |

|

| 25 |

| Citigroup, Inc., 7.50%, 12/15/12 |

| NR/NR |

|

| 2,603,046 |

|

|

|

| Credit Suisse Securities USA LLC (i), |

|

|

|

|

|

|

| 70 |

| 10.00%, 9/1/10 (Bristol-Myers Squibb Co.) |

| Aa2/A- |

|

| 1,568,436 |

|

| 51 |

| 10.00%, 9/9/10 (Merck & Co., Inc.) |

| Aa2/A- |

|

| 1,719,120 |

|

| — | (j) | GMAC, Inc., 7.00%, 12/31/11, Ser. G (e)(f)(k) |

| NR/C |

|

| 71,475 |

|

|

|

| JP Morgan Chase & Co., |

|

|

|

|

|

|

| 113 |

| 10.00%, 1/20/11 (Symantec Corp.) (i) |

| Aa3/A+ |

|

| 1,978,630 |

|

|

|

|

|

|

|

|

| 11,764,332 |

|

|

|

| Electric Utilities—0.2% |

|

|

|

|

|

|

| 18 |

| FPL Group, Inc., 8.375%, 6/1/12 |

| NR/NR |

|

| 938,400 |

|

|

|

| Food Products—1.5% |

|

|

|

|

|

|

| 58 |

| Archer-Daniels-Midland Co., 6.25%, 6/1/11 |

| NR/BBB+ |

|

| 2,475,330 |

|

| 39 |

| Bunge Ltd., 4.875%, 12/1/11 (k) |

| Ba1/BB |

|

| 3,409,550 |

|

|

|

|

|

|

|

|

| 5,884,880 |

|

|

|

| Household Durables—1.2% |

|

|

|

|

|

|

| 5 |

| Stanley Works, 5.125%, 5/17/12 (h) |

| A3/BBB+ |

|

| 4,752,800 |

|

|

|

| Insurance—1.0% |

|

|

|

|

|

|

| 28 |

| Assured Guaranty Ltd., 8.50%, 6/1/12 |

| NR/NR |

|

| 2,583,075 |

|

| 53 |

| XL Capital Ltd., 10.75%, 8/15/11 |

| Baa2/BBB- |

|

| 1,363,918 |

|

|

|

|

|

|

|

|

| 3,946,993 |

|

|

|

| Multi-Utilities—1.2% |

|

|

|

|

|

|

| 102 |

| AES Trust III, 6.75%, 10/15/29 |

| B3/B |

|

| 4,692,210 |

|

|

|

| Oil, Gas & Consumable Fuels—1.1% |

|

|

|

|

|

|

| 20 |

| ATP Oil & Gas Corp., 8.00%, 10/1/14 (e)(f)(k) |

| NR/NR |

|

| 1,819,388 |

|

| 27 |

| Chesapeake Energy Corp., 5.00%, 11/15/10 (k) |

| NR/B |

|

| 2,324,750 |

|

|

|

|

|

|

|

|

| 4,144,138 |

|

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

|

| 1.31.10 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 15 | |

January 31, 2010

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Credit Rating |

| Value |

| ||

|

|

| Pharmaceuticals—1.1% |

|

|

|

|

|

|

| 8 |

| Merck & Co., Inc., 6.00%, 8/13/10 |

| A2/A- |

|

| $2,127,414 |

|

| 2 |

| Mylan, Inc., 6.50%, 11/15/10 |

| NR/B |

|

| 2,248,320 |

|

|

|

|

|

|

|

|

| 4,375,734 |

|

|

|

| Real Estate Investment Trust—1.7% |

|

|

|

|

|

|

| 121 |

| Alexandria Real Estate Equities, Inc., 7.00%, 4/20/13 (k) |

| NR/NR |

|

| 2,595,050 |

|

| 207 |

| FelCor Lodging Trust, Inc., 1.95%, 12/31/49, Ser. A (c) |

| Caa3/C |

|

| 2,549,790 |

|

| 24 |

| Simon Property Group, Inc., 6.00%, 4/14/10, Ser. I (k) |

| Baa1/BBB |

|

| 1,480,080 |

|

|

|

|

|

|

|

|

| 6,624,920 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Convertible Preferred Stock (cost-$83,759,033) |

|

|

|

| 61,536,992 |

|

|

|

|

|

|

|

|

|

|

|

CONVERTIBLE BONDS & NOTES—9.7% |

|

|

|

|

|

| |||

|

|

|

|

|

|

|

|

|

|

Principal |

|

|

|

|

|

|

|

| |

|

|

| Auto Components—0.5% |

|

|

|

|

|

|

| $1,425 |

| BorgWarner, Inc., 3.50%, 4/15/12 |

| NR/BBB |

|

| 1,793,719 |

|

|

|

| Commercial Services & Supplies—1.2% |

|

|

|

|

|

|

| 4,800 |

| Bowne & Co., Inc., 6.00%, 10/1/33 (d) |

| B3/CCC+ |

|

| 4,626,000 |

|

|

|

| Computers—1.3% |

|

|

|

|

|

|

| 4,925 |

| Maxtor Corp., 6.80%, 4/30/10 |

| Ba3/NR |

|

| 4,998,875 |

|

|

|

| Diversified Consumer Services—0.5% |

|

|

|

|

|

|

| 2,000 |

| Coinstar, Inc., 4.00%, 9/1/14 |

| NR/BB |

|

| 1,925,000 |

|

|

|

| Electrical Equipment—1.4% |

|

|

|

|

|

|

| 1,830 |

| EnerSys, 3.375%, 6/1/38 (d) |

| B2/BB |

|

| 1,573,800 |

|

| 4,605 |

| JA Solar Holdings Co., Ltd., 4.50%, 5/15/13 |

| NR/NR |

|

| 3,793,369 |

|

|

|

|

|

|

|

|

| 5,367,169 |

|

|

|

| Electronic Equipment, Instruments & Components—0.3% |

|

|

|

|

|

|

| 1,335 |

| Anixter International, Inc., 1.00%, 2/15/13 |

| NR/BB- |

|

| 1,228,200 |

|

|

|

| Energy Equipment & Services—0.3% |

|

|

|

|

|

|

| 1,625 |

| Hornbeck Offshore Services, Inc., 1.625%, 11/15/26 (d) |

| NR/BB- |

|

| 1,343,225 |

|

|

|

| Health Care Providers & Services—0.4% |

|

|

|

|

|

|

| 1,850 |

| Omnicare, Inc., 3.25%, 12/15/35, Ser. OCR |

| B3/B+ |

|

| 1,517,000 |

|

|

|

| Internet Software & Services—0.5% |

|

|

|

|

|

|

| 2,300 |

| VeriSign, Inc., 3.25%, 8/15/37 |

| NR/NR |

|

| 1,929,125 |

|

|

|

| IT Services—0.7% |

|

|

|

|

|

|

| 2,850 |

| Alliance Data Systems Corp., 1.75%, 8/1/13 |

| NR/NR |

|

| 2,750,250 |

|

|

|

| Pharmaceuticals—0.5% |

|

|

|

|

|

|

| 1,675 |

| Biovail Corp., 5.375%, 8/1/14 (e)(f) |

| NR/NR |

|

| 1,995,344 |

|

|

|

| Real Estate Investment Trust—1.0% |

|

|

|

|

|

|

| 2,000 |

| Boston Properties LP, 3.75%, 5/15/36 |

| NR/A- |

|

| 2,017,500 |

|

| 2,200 |

| Developers Diversified Realty Corp., 3.00%, 3/15/12 |

| NR/BB |

|

| 2,051,500 |

|

|

|

|

|

|

|

|

| 4,069,000 |

|

|

|

| Semiconductors & Semiconductor Equipment—0.4% |

|

|

|

|

|

|

| 1,950 |

| Micron Technology, Inc., 1.875%, 6/1/14 |

| NR/B- |

|

| 1,708,687 |

|

|

|

| NFJ Dividend, Interest & Premium Strategy Fund |

16 | Nicholas-Applegate Equity & Convertible Income Fund Annual Report | 1.31.10 | |

|

Nicholas-Applegate Equity & Convertible Income Fund Schedule of Investments |

January 31, 2010 |

|

|

|

|

|

|

|

|

|

|

|

Principal |

|

|

| Credit Rating |

| Value |

| ||

|

|

| Software—0.7% |

|

|

|

|

|

|

| $1,100 |

| Macrovision Corp., 2.625%, 8/15/11 |

| NR/B |

|

| $1,276,000 |

|

| 1,400 |

| Nuance Communications, Inc., 2.75%, 8/15/27 |

| NR/B- |

|

| 1,464,750 |

|

|

|

|

|

|

|

|

| 2,740,750 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Convertible Bonds & Notes (cost-$40,544,611) |

|

|

|

| 37,992,344 |

|

|

|

|

|

|

|

|

|

|

|

CORPORATE BONDS & NOTES—2.4% |

|

|

|

|

|

| |||

|

|

| Banks—0.1% |

|

|

|

|

|

|

| 400 |

| GMAC LLC, 6.75%, 12/1/14 |

| Ca/B |

|

| 393,000 |

|

|

|

| Paper & Forest Products—0.2% |

|

|

|

|

|

|

| 1,000 |

| Neenah Paper, Inc., 7.375%, 11/15/14 |

| B2/B+ |

|

| 935,000 |

|

|

|

| Pipelines—0.9% |

|

|

|

|

|

|

| 4,340 |

| Dynegy Holdings, Inc., 7.75%, 6/1/19 |

| B3/B |

|

| 3,493,700 |

|

|

|

| Wireless Telecommunication Services—1.2% |

|

|

|

|

|

|

| 4,600 |

| Millicom International Cellular S.A., 10.00%, 12/1/13 |

| B1/NR |

|

| 4,772,500 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Corporate Bonds & Notes (cost-$9,992,462) |

|

|

|

| 9,594,200 |

|

|

|

|

|

|

|

|

|

|

|

SHORT-TERM INVESTMENT—1.3% |

|

|

|

|

|

| |||

|

|

| Time Deposit—1.3% |

|

|

|

|

|

|

| 5,251 |

| Citibank-London, 0.03%, 2/1/10 (cost-$5,251,208) |

|

|

|

| 5,251,208 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Investments, before call options written |

|

|

|

| 391,368,249 |

|

|

|

|

|

|

|

| |||

CALL OPTIONS WRITTEN (b)—(0.0)% |

|

|

|

|

|

| |||

|

|

|

|

|

|

|

|

|

|

Contracts |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| AGCO Corp., |

|

|

|

|

|

|

| 270 |

| strike price $35, expires 2/19/10 |

|

|

|

| (5,670 | ) |

|

|

| Apple, Inc., |

|

|

|

|

|

|

| 175 |

| strike price $230, expires 2/19/10 |

|

|

|

| (3,325 | ) |

|

|

| EMC Corp., |

|

|

|

|

|

|

| 2,650 |

| strike price $19, expires 2/19/10 |

|

|

|

| (5,300 | ) |

|

|

| Ford Motor Co., |

|

|

|

|

|

|

| 3,480 |

| strike price $12, expires 2/19/10 |

|

|

|

| (45,240 | ) |