Preliminary Materials Prepared for the Conflicts Committee of the Board of Directors of Crestwood Gas Services GP LLC Project Intrepid April 24, 2013 EXHIBIT (c)(2) DRAFT Preliminary and Subject to Change |

These materials have been prepared by Evercore Group L.L.C. (“Evercore”) for the Conflicts Committee of the Board of Directors (the “Conflicts Committee”) of Crestwood Gas Services GP LLC (the “Company”), the general partner of Crestwood Midstream Partners LP (the “Partnership”), to whom such materials are directly addressed and delivered and may not be used or relied upon for any purpose other than as specifically contemplated by a written agreement with Evercore. These materials are based on information provided by or on behalf of the Partnership and/or other potential transaction participants, from public sources or otherwise reviewed by Evercore. Evercore assumes no responsibility for independent investigation or verification of such information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates and forecasts of future financial performance prepared by or reviewed with the management of the Partnership and/or other potential transaction participants or obtained from public sources, Evercore has assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such management (or, with respect to estimates and forecasts obtained from public sources, represent reasonable estimates). No representation or warranty, express or implied, is made as to the accuracy or completeness of such information and nothing contained herein is, or shall be relied upon as, a representation, whether as to the past, the present or the future. These materials were designed for use by specific persons familiar with the business and affairs of the Partnership. These materials are not intended to provide the sole basis for evaluating, and should not be considered a recommendation with respect to, any transaction or other matter. These materials have been developed by and are proprietary to Evercore and were prepared for the benefit and internal use of the Conflicts Committee. These materials were compiled on a confidential basis for use by the Conflicts Committee in evaluating the potential transaction described herein and not with a view to public disclosure or filing thereof under state or federal securities laws, and may not be reproduced, disseminated, quoted or referred to, in whole or in part, without the prior written consent of Evercore. These materials do not constitute an offer or solicitation to sell or purchase any securities and are not a commitment by Evercore (or any affiliate) to provide or arrange any financing for any transaction or to purchase any security in connection therewith. Evercore assumes no obligation to update or otherwise revise these materials. These materials may not reflect information known to other professionals in other business areas of Evercore and its affiliates. Evercore and its affiliates do not provide legal, accounting or tax advice. Accordingly, any statements contained herein as to tax matters were neither written nor intended by Evercore or its affiliates to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on such taxpayer. Each person should seek legal, accounting and tax advice based on his, her or its particular circumstances from independent advisors regarding the impact of the transactions or matters described herein. DRAFT |

Table of Contents Section I II III IV V VI VII VIII IX Confidential DRAFT A. Weighted Average Cost of Capital Certain Benefits and Issues for Consideration With Respect to the Proposed Transaction Summary Pro Forma Impact Introduction Executive Summary Overview of CMLP Indicative Valuation of CMLP Overview of NRGM Indicative Valuation of NRGM Summary Analysis of the Proposed Consideration Appendix |

I. Introduction DRAFT |

DRAFT Evercore Partners (“Evercore”) is pleased to provide the materials herein to the Conflicts Committee of the Board of Directors (the “Conflicts Committee”) of Crestwood Gas Services GP LLC, the general partner of Crestwood Midstream Partners LP (“Crestwood”, “CMLP” or the “Partnership”), regarding the proposed merger of CMLP with and into Inergy Midstream, L.P. (“NRGM”) (the “Proposed Transaction” or “Project Intrepid”) – As part of the Proposed Transaction, each common unit and Class D Unit (1) of CMLP is to be exchanged for 1.061x NRGM units and $0.41 in cash (the “Proposed Consideration”) based on a proposed 5.0% premium to CMLP’s volume- weighted average unit price over the previous 20 trading days ending April 19, 2013 and an aggregate $25.0 million dollar one-time cash payment to CMLP unitholders – Pro forma for Project Intrepid, CMLP will survive as a wholly-owned subsidiary of NRGM – As part of the Proposed Transaction, NRGM will assume CMLP’s current debt outstanding – As a condition to the Proposed Transaction, Inergy, L.P. (“NRGY”) and Crestwood Holdings, LLC (“Crestwood Holdings”) will enter into a series of transactions to consolidate the general partner of both entities including: (i) NRGY distributing all its existing NRGM units to existing NRGY unitholders; (ii) Crestwood Holdings acquiring Inergy Holdings GP, LLC (“IHGP”) from NRGY principals and (iii) NRGY acquiring CMLP’s general partner and IDR interest from Crestwood Holdings Overview of Materials Introduction 1 (1) Class D Units are similar in certain respects to existing common units, except that CMLP has the option to pay distributions on Class D Units for the period from March 2013 to March 2014 with cash or by issuing additional paid-in-kind Class D Units based upon the volume weighted-average price of CMLP common units for the ten trading days immediately preceding the date the distribution is declared Confidential |

Confidential DRAFT As such, the materials herein review the following: – An executive summary including: (i) an overview of the Proposed Transaction, including summary proposed terms; (ii) a review of Evercore’s evaluation process to-date; (iii) Evercore’s remaining outstanding due diligence and evaluation items and (iv) a summary preliminary analysis of the value of the Proposed Consideration relative to the preliminary value of a CMLP unit and an analysis of the proposed pro forma ownership relative to each of CMLP’s and NRGM’s contribution to the proposed MLP based on various financial metrics – An overview of CMLP, including an overview of CMLP’s assets and operations, a review of CMLP’s market and capitalization data and historical and projected operating and financial results as provided by CMLP management (the “CMLP Management Financial Projections”), a review of the assumptions utilized by CMLP management in deriving such financial projections and a comparison of the CMLP Management Financial Projections to projected financial results per Wall Street Research analysts covering CMLP (the “CMLP Research Financial Projections”) – A preliminary valuation analysis of CMLP – An overview of NRGM, including an overview of NRGM’s assets and operations, a review of NRGM’s market and capitalization data and historical and projected operating and financial results as provided by NRGM management (the “NRGM Management Financial Projections”), a review of the assumptions utilized by NRGM management in deriving such financial projections and a comparison of the NRGM Management Financial Projections to projected financial results per Wall Street Research analysts covering NRGM (the “NRGM Research Financial Projections”) – A preliminary analysis of the Proposed Consideration, including an analysis of the proposed pro forma ownership relative to each of CMLP’s and NRGM’s contribution to the pro forma entity based on various financial metrics – A review of the pro forma financial impact of the Proposed Transaction to CMLP unitholders, including sensitivities assuming various adjustments to the assumptions underlying the CMLP Management Financial Projections and the NRGM Management Financial Projections – A review of certain benefits and issues for consideration with respect to the Proposed Transaction The materials herein are preliminary and are subject to potentially material changes Overview of Materials (cont’d) Introduction 2 |

DRAFT II. Executive Summary |

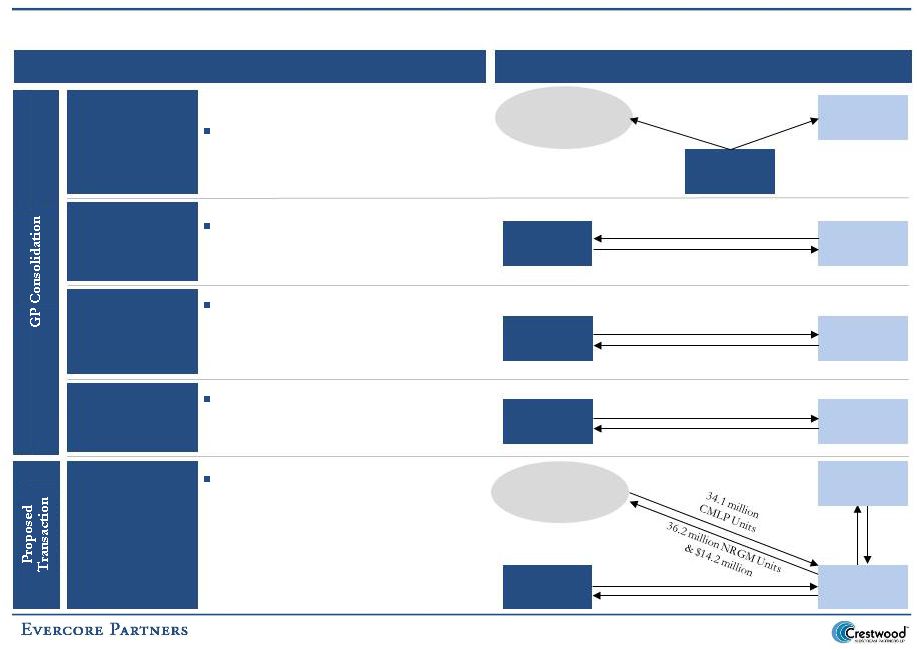

Overview of Project Intrepid 3 Executive Summary Confidential DRAFT Opinion Requested: Evercore has been asked by the Conflicts Committee, whether, in Evercore’s opinion, the Proposed Consideration to be received in the Proposed Transaction is fair, from a financial point of view, to the holders of the Partnership’s common units other than Crestwood Gas Services GP LLC, Crestwood Gas Services Holdings LLC and their respective affiliates As part of the Proposed Transaction, NRGM has proposed to acquire each CMLP common unit and Class D Unit outstanding in exchange for: (i) 1.061x NRGM common units and (ii) $0.41 cash assuming no more than a [5.0]% premium to CMLP’s volume-weighted average closing unit price over the 20 trading days prior to execution of a definitive agreement (“20- Day VWAP”) as described below and a one-time payment to CMLP unitholders not to exceed $[25.0] million in total – Represents an aggregate CMLP equity value of approximately $1.5 billion based on a 20-Day VWAP as of April 19, 2012 and, including NRGM’s assumption of CMLP’s approximately $787.4 million of net debt projected to be outstanding as of July 1, 2013, a CMLP enterprise value of approximately $2.3 billion – Pro forma for the Proposed Transaction, CMLP unitholders will own 42.7% of the pro forma entity – Expected announcement on May 6, 2013 Prior to the Proposed Transaction, it is anticipated that NRGY and Crestwood Holdings will enter into a series of transactions to consolidate the general partner of both entities (together the “GP Consolidation”), including: – Step 1: NRGY will distribute all of its 56.4 million NRGM units to NRGY unitholders – Step 2: Crestwood Holdings will acquire IHGP for a cash payment of [$70 million -$80 million], with the exact amount of such payment still to be determined based on certain tax and other considerations – Step 3: NRGY will acquire CMLP’s general partner and IDR interest on a debt-free basis from Crestwood Holdings in exchange for $450 million in NRGY units (41.6 million NRGY units based 20-Day VWAP as of April 19, 2012) – Step 4: Crestwood Holdings will contribute a portion of its CMLP units, currently proposed to be 5.5 million CMLP units, for an equivalent value of NRGY units such that Crestwood Holdings owns a 29.0% interest in NRGY on a pro forma basis While Steps 1 through 4 above are conditions precedent to closing of the Proposed Transaction, closing of the Proposed Transaction is not a condition precedent to the GP Consolidation |

Current NRGM Organizational Structure Note: Structure as of 4/1/13 4 Executive Summary NRGP Limited Partner, LLC Inergy Holdings GP , LLC Inergy Holdings, L.P. Inergy GP, LLC (Managing General Partner) IPCH Acquisition Corp. 847,415 Class A Units Inergy Partners, LLC 4,019,837 Class A Units Inergy Services, LLC Tres Palacios Midstream, LLC Inergy Pipeline East, LLC Inergy Gas Marketing, LLC Inergy Storage, Inc. Arlington Storage Company, LLC Finger Lakes LPG Storage, LLC Inergy Crude Logistics, LLC US Salt, LLC Inergy Terminals, LLC Inergy Dakota Pipeline, LLC Central New York Oil And Gas Company, L.L.C. Inergy , L.P. NYSE: NRGY 56,398,707 NRGM Common Units Incentive Distribution Rights Market Capitalization: $2,847 MM Net Debt: $345 MM Inergy Midstream, L.P. NYSE: NRGM Market Capitalization: $1,967 MM Net Debt: $680 MM Inergy Midstream Operations, LLC NRGY Public Unitholders NRGM Public Unitholders 99% L.P. Interest 1% L.P. Interest 100% Member Interest Non-Economic GP Interest 96.7% L.P. Interest 0.6% L.P. Interest 2.7% L.P. Interest 0.5% Class A Member Interest 100% Class A Member Interest 100% Member Interest 100% Member Interest 100% Member Interest 100% Member Interest 100% Member Interest 100% Member Interest 100% Ownership 99.9% Member Interest 0.1% Member Interest 100% Member Interest 100% Member Interest 100% Member Interest 100% Member Interest Non-economic GP interest 100% Member Interest 100% Member Interest Non-economic GP interest 100% Member Interest 100% Member Interest Tres Palacios Gas Storage, LLC 34.3% Ownership 65.7% Ownership Incentive Distribution Rights 100% L.P. Interest 100% Member Interest MGP GP, LLC Inergy Midstream Holdings, L.P. NRGM GP, LLC Inergy Operations, LLC Confidential DRAFT |

Current CMLP Organizational Structure 5 Executive Summary Source: Public partnership filings (1) Class D Units are similar in certain respects to existing common units, except that CMLP has the option to pay distributions to Class D unitholders for a period of one year with cash or by issuing additional paid-in-kind Class D units based upon the volume weighted-average price of CMLP common units for the ten trading days immediately preceding the date the distribution is declared 100% Public Unitholders 34,083,730 Common LP Units Crestwood Holdings Partners LLC Crestwood Gas Services Holdings LLC 17,210,377 Common LP Units 6,190,469 Class D LP Units Crestwood Holdings LLC 2,333,712 Common LP Units 55.8% Operating Subsidiaries Class D LP Units (1) 10.1% 100% GP 1.8% Crestwood Gas Services GP LLC 137,105 Common LP Units 1,112,674 GP Units Common LP Units 28.2% Crestwood Marcellus Midstream LLC Crestwood Midstream Partners LP Market Capitalization: $1,524.9 million Net Debt: $702.5 million B3 / B Crestwood Holdings II LLC Crestwood Marcellus Holdings LLC 3.8% LP 0.2% Confidential DRAFT 100% 100% |

Summary Transaction Structure 6 Executive Summary Summary Structure Step 2: Acquisition of Inergy Holdings GP Step 1: Distribution of NRGY’s NRGM Units to NRGY Unitholders Step 3: NRGY Acquires CMLP’s GP and IDR Interests for NRGY Units Crestwood Holdings acquires IHGP from NRGY principals for a cash payment of [$70 - $80] million NRGY distributes all of its existing NRGM units (56.4 million) to existing NRGY unitholders NRGY Principals Inergy Holdings GP, LLC and associated non-economic GP interest in NRGY [$70- $80] million cash NRGY NRGY Public Unitholders Crestwood Holdings NRGY Principals 56.4 million NRGM Units NRGY acquires CMLP’s general partner and IDR interests from Crestwood Holdings in exchange for $450 million of NRGY units (or 41.6 million NRGY units) NRGY CMLP’s General Partner and IDR Interest 41.6 million NRGY Units Crestwood Holdings Step 4: True-Up Contribution CMLP/NRGM Merger CMLP merges with and into NRGM at (i) an agreed upon premium not to exceed 5% for CMLP units and (ii) a one-time payment to CMLP unitholders not to exceed $25.0 million – As a result, NRGM issues 63.7 million new NRGM units and $25.0 million in cash Crestwood Holdings CMLP Public Unitholders 20.4 million CMLP Units NRGY acquires 5.5 million CMLP units from Crestwood Holdings in exchange for 12.2 million NRGY units NRGY 5.5 million CMLP Units 12.2 million NRGY Units Crestwood Holdings NRGM NRGY 5.5 million CMLP Units 5.8 million NRGM Units & $2.3 million 21.7 million NRGM Units & $8.5 million Confidential DRAFT |

Common LP Units 12.0 million 8.0% Common LP Units 26.7 million 14.4% 100% 100% 100% Common LP Units 105.0 million 56.6% Pro Forma Ownership Structure 7 Executive Summary 100% Crestwood Holdings Partners LLC Inergy Holdings, L.P. Public Unitholders Crestwood Holdings LLC 100% 100% 100% 100% Common LP Units 110.0 million 73.6% Inergy GP, LLC Inergy, L.P. Public Unitholders MGP GP, LLC NRGM GP, LLC Common LP Units 5.8 million 3.9% Non-Economic General Partner Interest Non-Economic General Partner Interest Inergy Midstream Holdings, L.P. Non-Economic General Partner Interest 100% Incentive Distribution Rights Non-Economic General Partner Interest Common LP Units 53.8 million 29.0% Management Management Common LP Units 21.7 million 14.5% Inergy Midstream, L.P. Crestwood Midstream Partners, LP 100% Crestwood Gas Services, LLC 100% Non-Economic General Partner Interest 100% Pro Forma Ownership Units (MM) % NRGY Public - NRGY 105.0 56.6% Crestwood Holdings 53.8 29.0% Management 26.7 14.4% Total NRGY Units 185.6 100.0% NRGM Public - NRGM 17.5 11.7% Public - CMLP 36.2 24.1% Crestwood Holdings 22.0 14.7% NRGY Unitholders 56.4 37.6% NRGY 5.8 3.9% Management 12.0 8.0% Total NRGM Units 149.9 100.0% Confidential DRAFT |

Pro Forma Asset Map 8 Executive Summary Gathering Systems (CMLP) Compression and Treating Facility (CMLP) Processing Facility (CMLP) Legend Gas Storage (NRGM) NGL Storage (NRGM) COLT Hub (NRGM) DRAFT Confidential |

Summary Side by Side Comparison ($ in millions, except per unit amounts) Executive Summary 9 Source: CMLP and NRGM management, respectively and CMLP and NRGM filings Note:: All entities listed on a fiscal year basis; NRGM fiscal year ends September 30 (1) Distribution per LP unit and Distributable Cash Flow per LP Unit for the three months ending September 30, 2013 NRGM CMLP NRGM Pro Forma Unit Price (as of 04/19/2013) $24.97 $22.90 $22.90 Total Equity Value $1,524.9 $1,967.2 $3,450.2 Plus: Net Debt $702.5 $679.8 $1,637.9 Plus: Minority Interest -- -- -- Enterprise Value $2,227.4 $2,647.0 $5,088.1 Adjusted EBITDA 2013E $173.3 $194.3 $377.5 2014E 214.8 228.6 458.4 Enterprise Value / Adjusted EBITDA 2013E 12.9x 13.6x 13.5x 2014E 10.4 11.6 11.1 Distributed Cash Flow Yield Current Annualized 8.2% 6.8% 7.4% 2013E 8.3% 6.9% 7.2% 2014E 8.6% 7.3% 8.1% Distributable Cash Flow Yield Current Annualized 7.8% 6.0% 7.6% 2013E 8.0% 6.7% 7.2% 2014E 8.6% 7.6% 8.3% Credit Rating B3 / B Ba3 / BB NA (1) (1) DRAFT Confidential |

Summary of Merger Agreement 10 Executive Summary Source: Draft of the Agreement and Plan of Merger by and among Inergy Midstream, L.P., NRGM GP, LLC, Intrepid Merger Sub, LLC, Inergy, L.P., Crestwood Midstream Partners LP and Crestwood Gas Services GP LLC dated April 19, 2013 (1) Subject to NRGM’s further confirmation of impact of merger transaction on CMLP equity awards Parties: CMLP Crestwood Gas Services GP, LLC (“CMLP GP”) NRGM; NRGM GP, LLC (“NRGM GP”) NRGY Intrepid Merger Sub, LLC (“Merger Sub”), a wholly-owned subsidiary of NRGM Mechanics: Provides for merger of CMLP with Merger Sub; CMLP remains as surviving entity post-closing, continuing as a wholly-owned subsidiary of NRGM NRGM will be sole limited partner of CMLP, CMLP GP will be sole general partner of CMLP, and NRGM GP will be sole member of CMLP GP Closing occurs within 3 business days of satisfaction or waiver of closing conditions (see page 11) Consideration: The Proposed Consideration (CMLP common units and Class D Units exchanged for NRGM units and cash) Merger Sub LLC interests convert into 100% LP interest in CMLP CMLP GP’s GP interest in CMLP converts into a non-economic GP interest in CMLP Outstanding CMLP Incentive Distribution Rights are cancelled [CMLP Restricted Common Units lapse; CMLP Phantom Units vest and restrictions thereon lapse] (1) Required Approvals After Merger Agreement is Executed: Majority of outstanding CMLP common units FTC/DOJ approval under the HSR Act (antitrust clearance) NYSE approval of listing of additional NRGM common units to be issued in connection with merger As a condition to execution of Merger Agreement, NRGM will require CMLP GP; Crestwood Gas Services Holdings LLC and Crestwood Holdings LLC to enter into a Voting Agreement (agreeing to support the Proposed Transaction) and an Option Agreement (giving NRGY the option to purchase these parties’ CMLP units in the event the Merger Agreement is terminated) – Confidential DRAFT |

Summary of Merger Agreement (cont’d) 11 Executive Summary Covenants: Parties agree to continue to conduct business in the ordinary course through Closing and abide by customary restrictions on issuance of equity, incurrence of debt, entry into material contracts, etc. No-Shop Clause: CMLP agrees not to solicit or otherwise agree to an alternative to the Proposed Transaction; includes fiduciary out allowing CMLP GP’s Board to agree to superior proposal Indemnification: NRGM must indemnify directors and officers of CMLP and related parties for 6 years after closing, including for claims relating to the Proposed Transaction Directors of CMLP Board (and related entities as NRGM may designate) must resign Securities Law Filings: Parties agree to cooperate in filing Joint Proxy Statement/Prospectus, Schedule 13E-3 (if needed), and other filings as required by the SEC Conditions to Closing: Customary closing conditions (including absence of Material Adverse Effect); GP Consolidation has occurred; and Required Approvals obtained (see page 10) Termination: Termination (i) by mutual consent of the parties; (ii) by either CMLP or NRGM if merger is not consummated [within one year of Merger Agreement execution], CMLP unitholder or requisite governmental approval not obtained, or material breach and failure to cure by the other party or (iii) by NRGM if CMLP GP Board changes its recommendation or willfully breaches non-solicitation provision Termination Fee: CMLP must pay termination fee of $[ ] if CMLP willfully breaches non-solicitation provision, CMLP GP Board changes its recommendation or CMLP agrees to a superior proposal Expense Reimbursement: CMLP must pay NRGM $[ ] million as expense reimbursement if CMLP unitholder approval is not obtained Controlling Law: Delaware Source: Draft of the Agreement and Plan of Merger by and among Inergy Midstream, L.P., NRGM GP, LLC, Intrepid Merger Sub, LLC, Inergy, L.P., Crestwood Midstream Partners LP and Crestwood Gas Services GP LLC dated April 19, 2013 DRAFT Confidential |

Confidential DRAFT Evercore Evaluation Process To-Date 12 Executive Summary In connection with its review of the Proposed Transaction as of April 24, 2013, Evercore has, among other things: – Reviewed certain publicly-available financial and operating data relating to CMLP and NRGM that we deemed to be relevant; – Reviewed publicly-available research analyst estimates for CMLP’s and NRGM’s future financial performance on a standalone basis; – Reviewed certain non-public projected financial and operating data relating to CMLP prepared and furnished to us by management of CMLP; – Discussed the past and current operations, financial projections and current financial condition of CMLP with management of CMLP (including management’s views of the risks and uncertainties of achieving such projections); – Reviewed certain non-public projected financial and operating data relating to NRGM prepared and furnished to us by management of NRGM; – Reviewed the past and current operations, financial projections and current financial condition of NRGM with CMLP management; – Reviewed the dynamics of each of the markets in which CMLP and NRGM participates with CMLP management; – Reviewed the Crestwood Management Presentation dated April 11, 2013 prepared for NRGY and NRGM by CMLP management – Reviewed the Inergy Management Presentation dated April 11, 2013 prepared for CMLP by NRGM management – Reviewed the Project Intrepid Due Diligence Presentation dated April 19, 2013 prepared by CMLP management – Reviewed a draft of the Agreement and Plan of Merger by and among Inergy Midstream, L.P., NRGM GP, LLC, Intrepid Merger Sub, LLC, Inergy, L.P., Crestwood Midstream Partners LP and Crestwood Gas Services GP LLC dated April 19, 2013 – Reviewed a draft of the Purchase and Sale Agreement among Crestwood Holdings LLC, Intrepid Holdings GP, LLC and NRGP Limited Partner, LLC dated April 19, 2013 – Reviewed a draft of the Contribution Agreement of Membership Interests of Crestwood Gas Services GP LLC among Crestwood Holdings LLC, Crestwood Gas Services Holdings LLC as Contributing Parties and Intrepid GP, LLC, Intrepid, L.P. as Recipient Parties dated April 19, 2013 |

13 In connection with its review of the Proposed Transaction, as of April 24, 2013 Evercore has the following remaining items to complete: – Reviewing certain additional sensitivity cases and other financial information as requested by Evercore on April 19, 2013 and not yet provided by CMLP management – Reviewing additional information from ongoing diligence with respect to NRGM as such information continues to be provided to CMLP management and Evercore – Reviewing certain tax information requested on April 21, 2013 Confidential DRAFT Executive Summary Evercore Remaining Due Diligence/Evaluation |

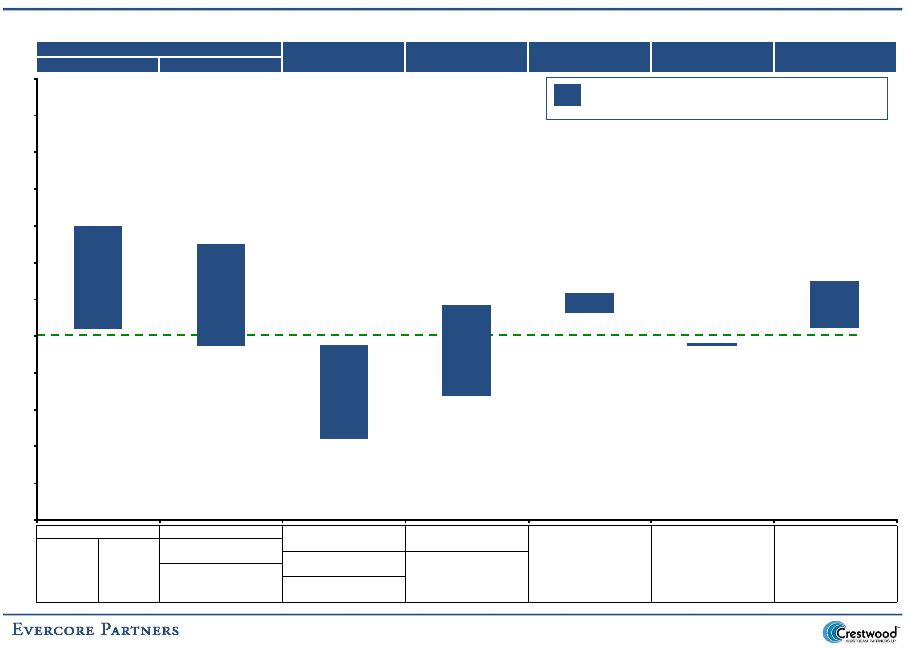

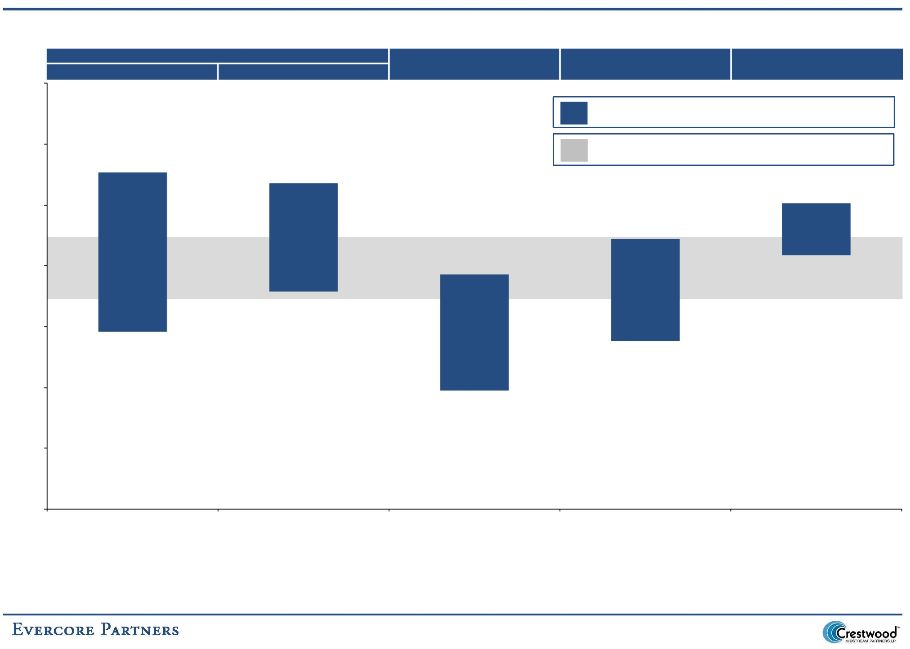

Summary Preliminary Valuation Analysis 14 Executive Summary Relevant Range of the Proposed Consideration $27.00 $22.00 Indicative Value per CMLP Common Unit Indicative Value of the Proposed Consideration to be Paid per CMLP Common Unit Crestwood Midstream Partners LP Indicative Valuation per LP Unit Indicative Valuation of Proposed Consideration Discounted Cash Flow Analysis Precedent M&A Peer Group Wall Street Discounted Cash Flow Analysis Precedent M&A Peer Group Wall Street Financial Distirbution Transactions Trading Research Price Financial Distirbution Transactions Trading Research Price Projections Per LP Unit Analysis Analysis Targets Projections Per LP Unit Analysis Analysis Targets 7.5% - 8.5% WACC 7.0% - 10.0% 2013E EBITDA 2013E EBITDA: Barclays 6.5% - 7.5% WACC 6.0% - 8.0% 2013E EBITDA: 2013E EBITDA: Barclays 2017E EBITDA Terminal Exit Yield $173.3 MM $173.3 MM Hilliard Lyons 2017E EBITDA Terminal Exit Yield $171.6 MM $171.6 MM Credit Suisse Exit Multiple of 8.5% - 9.5% CAPM 9.0x -12.5x 10.5x -13.5x Simmons Exit Multiple of 7.5% - 9.5% CAPM 11.5x -13.5x 14.0x -17.0x JP Morgan 9.0x -11.0x Equity Discount Rate EBITDA Multiple EBITDA Multiple Ladenburg Thalmann 11.5x -13.5x Equity Discount Rate EBITDA Multiple EBITDA Multiple Morgan Stanley Perpetuity Growth 13.5% -14.5% 2014E EBITDA: 2014E EBITDA: Wells Fargo Perpetuity Growth 9.0% - 11.0% 2014E EBITDA: 2014E EBITDA: Robert W. Baird & Co. Rate of Expected Market Return $214.8 MM $214.8 MM Rate of Expected Market Return $223.5 MM $223.5 MM Stifel Nicolaus 0.5% - 1.5% Equity Discount Rate 9.0x -12.5x 9.0x -12.0x 0.5% - 1.5% Equity Discount Rate 11.5x -13.5x 10.0x -13.0x EBITDA Multiple EBITDA Multiple EBITDA Multiple EBITDA Multiple Growth Capital Expenditures Growth Capital Expenditures Discounted @ 8.0% Discounted @ 7.0% $25.94 $23.70 $10.90 $16.81 $26.00 $19.55 $22.88 $14.77 $18.79 $25.89 $39.91 $37.49 $23.79 $29.16 $32.50 $32.70 $31.77 $24.29 $27.20 $30.13 $-- $10.00 $20.00 $30.00 $40.00 $50.00 $60.00 Confidential DRAFT 1.061x NRGM Units + $0.41 per unit of cash Current CMLP Unit Price: $24.97 |

Summary Contribution Analysis 15 Executive Summary (1) Adjusted for CMLP and NRGM net debt outstanding as of the most recent public disclosure. Equity value as of April 19, 2013 (2) Proposed exchange ratio excludes cash consideration of $0.41 per unit Management Financial Projections Implied Exchange Ratio Pro Forma Ownership Based on Proposed Exchange Ratio 1.061x 2013E Distributable Cash Flow 1.178x 2014E Distributable Cash Flow 1.290x 2015E Distributable Cash Flow 1.546x 2013E EBITDA (1) 1.178x 2014E EBITDA (1) 1.271x 2015E EBITDA (1) 1.585x DCF Equity Value 1.360x Precedent Transactions Equity Value 0.981x Peer Group Trading Equity Value 1.100x Relevant Range - - Implied Exchange Ratio - Proposed Exchange Ratio (2) 40.8% 1.061x 0.981x 1.585x 59.2% 47.3% 51.2% 40.8% 59.2% 52.0% 48.0% 45.2% 54.8% 47.1% 52.7% 52.9% Crestwood Inergy Midstream 45.2% 54.8% 47.5% 52.5% 42.7% 57.3% 43.6% 56.4% 52.7% 47.3% 48.8% DRAFT Confidential |

Confidential DRAFT Summary Pro Forma Accretion/Dilution Results 16 Executive Summary (1) Based on CMLP’s current 8.2% yield Standalone Pro Forma CMLP CMLP CMLP Breakeven Yield (1) CY 2014E CMLP DCF / LP Unit $2.14 $2.02 7.7% Accretion / (Dilution) - $ ($0.12) CY 2015E CMLP DCF / LP Unit $2.51 $2.22 7.7% Accretion / (Dilution) - $ ($0.29) CY 2016E CMLP DCF / LP Unit $2.78 $2.35 7.4% Accretion / (Dilution) - $ ($0.42) CY 2017E CMLP DCF / LP Unit $2.98 $2.48 7.1% Accretion / (Dilution) - $ ($0.50) CY 2014E CMLP Distribution / LP Unit $2.15 $1.96 7.4% Accretion / (Dilution) - $ ($0.19) CY 2015E CMLP Distribution / LP Unit $2.37 $2.16 7.5% Accretion / (Dilution) - $ ($0.20) CY 2016E CMLP Distribution / LP Unit $2.60 $2.31 7.2% Accretion / (Dilution) - $ ($0.29) CY 2017E CMLP Distribution / LP Unit $2.86 $2.39 6.8% Accretion / (Dilution) - $ ($0.47) CY 2014E - 2017E Distribution Growth 10.0% 6.9% Debt Metrics CY 2014E Debt/EBITDA 4.4x 3.8x CY 2015E Debt/EBITDA 3.7x 3.5x CY 2016E Debt/EBITDA 3.4x 3.2x CY 2017E Debt/EBITDA 3.2x 3.0x |

III. Overview of CMLP DRAFT |

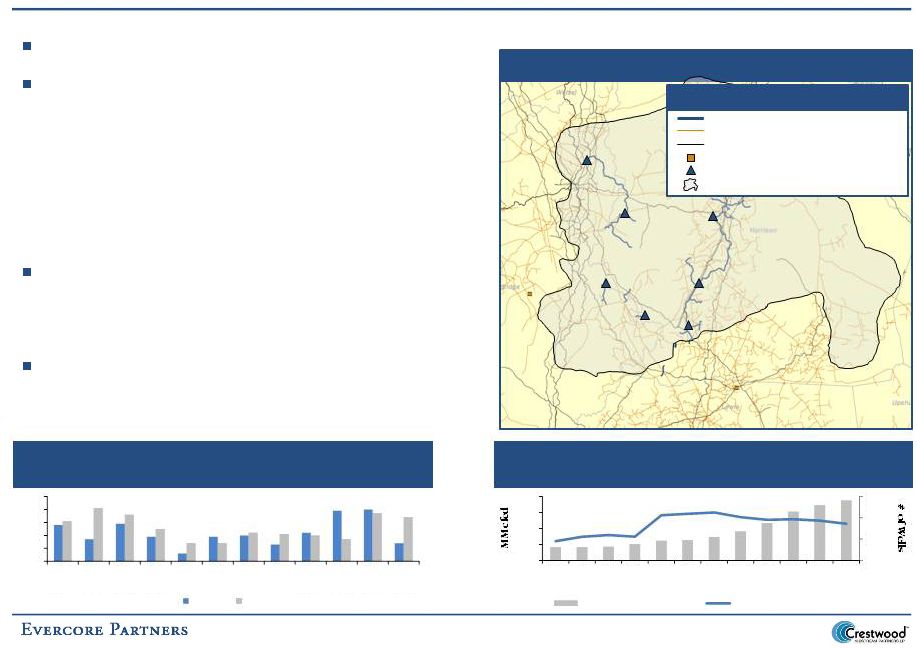

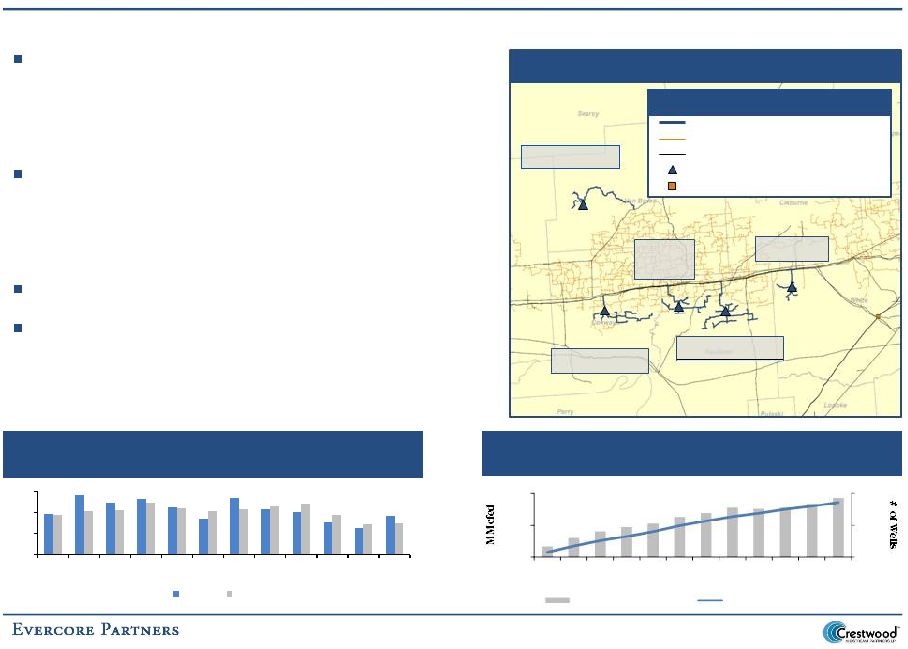

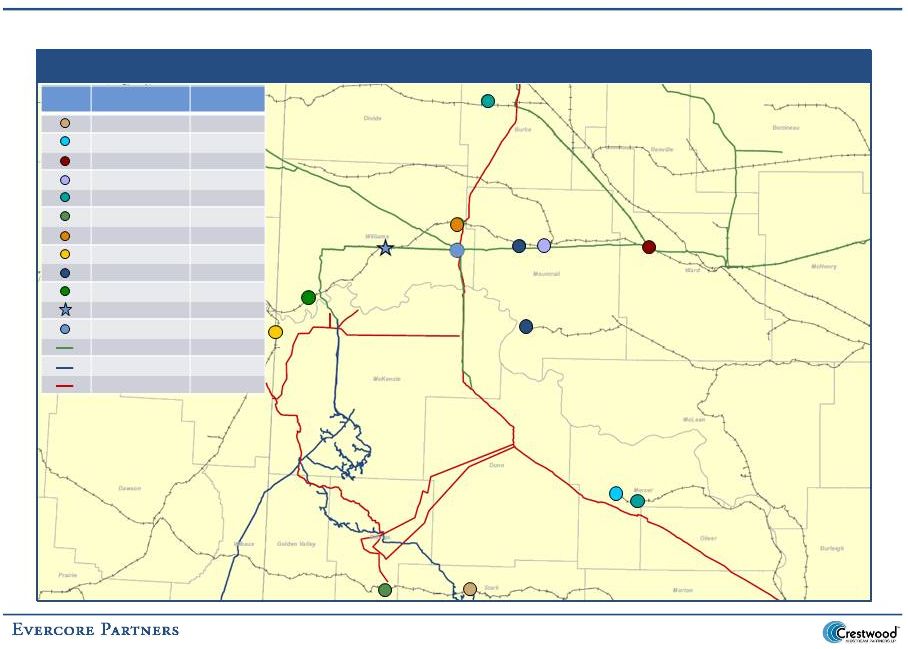

CMLP Asset Map ($ in millions) 17 Overview of CMLP Source: Public partnership filings (1) Excludes corporate expenses Acreage Dedication Summary Avalon Shale Barnett Shale Granite Wash Haynesville Shale Legend Fayetteville Shale Marcellus Shale 2012A to 2017E Gathering Volume Compound Annual Growth Rate by Basin (1) 2013E EBITDA by Basin (1) Confidential DRAFT Gathering Systems Compression and Treating Facility Processing Facility 40.0% 30.0% 20.0% 10.0% -- (10.0%) (20.0%) (30.0%) Barnett Shale Marcellus Shale Fayetteville Shale Granite Wash Haynesville Shale Avalon Shale 2.9% 28.1% 22.2% 32.6% (0.6%) (18.9%) Avalon Shale Granite Wash Fayetteville Shale Barnett Shale Haynesville Shale Marcellus Shale Contract Expiration 2017E 2020E 2021E 2022E 2024E 2032E 160,000 140,000 120,000 100,000 80,000 60,000 40,000 20,000 -- $21.2MM $3.7MM $3.0MM $111.2MM 55% 11% 2% 1% Avalon Shale Granite Wash Barnett Shale Fayetteville Shale Haynesville Shale Marcellus Shale $0.1MM 0% 31% $62.1MM |

Confidential DRAFT 1 Pipeline Nominal Capacity (MMcfd) Installed Compression Asset Miles Gathering Processing Treating Dehydration Compression (HP) Units Barnett Shale Owned: Cowtown System 298 425 425 -- 425 103,590 33 Lake Arlington System 10 230 -- -- 235 30,480 7 Alliance System 42 300 -- 340 240 43,680 7 Owned 350 955 425 340 900 177,750 47 Operated Non-Owned: Cowtown System 104 -- -- -- -- -- -- Lake Arlington System 10 -- -- -- -- -- -- Alliance System 35 -- -- -- -- -- -- Operated Non-Owned 149 -- -- -- -- -- -- Total Barnett Shale Assets 499 955 425 340 900 177,750 47 Fayetteville Shale Twin Groves/Prairie Creek/Woolly Hollow System 129 350 -- 185 180 26,635 14 Wilson Creek System 24 100 -- -- 5 425 1 Rose Bud System 15 60 -- -- 5 630 1 Total Fayetteville Shale Assets 168 510 -- 185 190 27,690 16 Granite Wash Total Granite Wash Assets 36 36 36 -- -- 10,890 10 Marcellus Shale Total Marcellus Shale Assets 42 420 -- -- 300 43,100 31 Other Las Animas System 47 50 -- -- 34 -- 1 Sabine System 57 100 -- 74 72 -- -- Total Other Assets 104 150 -- 74 106 -- Total CMLP 849 2,071 461 599 1,496 259,430 105 Asset Overview 18 Overview of CMLP Source: Public partnership filings |

Confidential DRAFT Asset Overview (cont’d) 19 Overview of CMLP Source: Public partnership filings (1) Excludes corporate expenses Located principally in Hood, Somervell and Johnson Counties, Texas in the southern portion of the Fort Worth Basin – The Cowtown Pipeline, which consists of NGL rich natural gas gathering systems, gathers natural gas for processing at the Cowtown Plant or Corvette Plant – The Cowtown Plant, which consists of two natural gas processing units, extracts NGLs from the natural gas stream and delivers residue gas and extracted NGLs to unaffiliated pipelines – The Corvette Plant extracts NGLs from the natural gas stream and delivers residue gas and extracted NGLs to unaffiliated pipelines Residue gas delivered to Atmos Energy Corporation, Enterprise Texas Pipeline LLC and/or Energy Transfer Partners, LP (“Energy Transfer”) Extracted NGLs delivered to West Texas Pipeline, LP and Lone Star NGL LLC for delivery to Mont Belvieu, Texas Acquired on August 24, 2012 from Devon Corporation and ceased operations on December 1, 2012 – CMLP is currently evaluating other potential uses for the 100 MMcfd West Johnson County Plant Located in eastern Tarrant County, Texas, the Lake Arlington System consists of a natural gas gathering system and related compression facility – Gathers natural gas for delivery to Energy Transfer Located in northern Tarrant and southern Denton Counties, Texas, the Alliance System consists of a natural gas gathering system and a related dehydration, compression and amine treating facility – Gathers natural gas for delivery to Energy Transfer and Crosstex Partners, LP (“Crosstex”) Barnett Shale 55.3% of 2013E EBITDA (1) Located in Harrison and Doddridge Counties, West Virginia, the Marcellus Systems consist of low pressure natural gas gathering systems and compression and dehydration facilities The Marcellus Systems interconnect with various interstate pipeline systems including Columbia Gas Transmission, Dominion Resources Inc. (“Dominion”) and Equitrans Pipeline The Marcellus Systems deliver high NGL content natural gas to MarkWest Energy Partners, L.P.’s Sherwood Natural Gas Processing Plant Antero’s assets consist of a 33-mile low pressure gathering system with 59 existing Antero horizontal Marcellus Shale well connections – Area of dedication located within the rich natural gas window of the southwestern core Marcellus Shale play in northern West Virginia Antero committed to deliver minimum annual throughput volumes for a seven-year period from January 1, 2012 to January 1, 2019, ranging from an average of 300 MMcfd in 2012 to an average of 450 MMcfd in 2018 EMAC’s assets consist of four compression and dehydration stations located on the acquired Antero gathering assets – Provide compression and dehydration services to Antero pursuant to a compression services agreement through 2018 Marcellus Shale 30.8% of 2013E EBITDA (1) Cowtown System West Johnson County System Lake Arlington System Alliance System Marcellus Systems Antero Resources Corporation (“Antero”) Acquisition E. Marcellus Asset Company, LLC (“EMAC”) Acquisition |

Confidential DRAFT Asset Overview (cont’d) 20 Overview of CMLP Source: Public partnership filings (1) Excludes corporate expenses Located in Roberts County, Texas, includes – The Indian Creek rich natural gas gathering system and related compression facility – The Indian Creek processing plant Gathers rich natural gas produced by Chesapeake Energy Corporation (“CHK”), Linn Energy, LLC and Sabine Oil and Gas LLC and interconnects with Mid-America Pipeline, a subsidiary of Enterprise Products Partners, L.P., for delivery of NGLs to Mont Belvieu, Texas The residue gas is delivered to ANR Pipeline and Northern Natural Gas Pipeline to provide access to the Mid-Continent natural gas markets Granite Wash 1.8% of 2013E EBITDA (1) Located in Eddy County, New Mexico, the Las Animas assets consist of three natural gas gathering systems located in the Morrow/Atoka reservoir and the Avalon Shale rich gas trend in the Permian Basin The Las Animas Systems include approximately 55,000 acres of dedication from Bass Oil Production Company through 2017 Located in Sabine Parish, Louisiana, the Sabine assets consist of high-pressure natural gas gathering pipelines Provides gathering and treating services for production from CHK, Comstock Resources, Inc., Forest Oil Corporation, Wildcat Sabine Pipeline LLC and Devon Corporation in the Haynesville/Bossier Shale with deliveries to Gulf South Pipeline and Tennessee Gas Pipeline Company, LLC – The Sabine System is supported by fixed-fee contracts with producers and approximately 20,000 dedicated acres Contracts have initial terms through 2019 to 2021 Other 1.6% of 2013E EBITDA (1) Located in Conway and Faulkner Counties, Arkansas, the Twin Groves/Prairie Creek/Woolly Hollow Systems consist of three natural gas gathering, compression, dehydration and treating facilities – Gather natural gas produced by BHP Billiton Petroleum, Plc. (“BHP”), BP and XTO Energy for delivery to Texas Gas Transmission, Ozark Gas Transmission and Fayetteville Express Pipeline Located in Van Buren County, Arkansas, the Wilson Creek System consists of a natural gas gathering system and a related compression facility. This system gathers natural gas produced by independent producers and delivers to Ozark Gas Transmission Located in White County, Arkansas, the Rose Bud System consists of a natural gas gathering system and a related compression facility. This system gathers natural gas produced by XTO Energy and delivers to Ozark Gas Transmission Fayetteville Shale 10.5% of 2013E EBITDA (1) Twin Groves / Prairie Creek / Woolly Hollow Systems Wilson Creek System Rose Bud System Granite Wash System Sabine System Los Animas Systems |

Confidential DRAFT Asset Overview – Barnett Shale (55.3% of 2013E EBITDA Excluding Corporate Expenses) 21 Source: Public partnership filings and CMLP management During the year ended December 31, 2012, CMLP’s Barnett Shale EBITDA declined $8.9 million from 2011 levels – Gathering volumes declined from 473.5 MMfcd in 2011 to 433.1 MMcfd in 2012 given reduced production from existing wells and well shut-ins on the Alliance System and Lake Arlington System – Such volume declines were partially offset by producers connecting 64 new wells during the year ended December 31, 2012 mostly on the Cowtown System – During the year ended December 31, 2011, Quicksilver Resources Inc.’s (“Quicksilver”) joint development agreement with Eni SpA resulted in an increase of approximately 75 MMcfd in gathered volumes and approximately $16.0 million in revenue Given the higher NGL content of the natural gas production in Johnson County, Texas, Devon Energy Corporation maintained an active drilling and development plan in 2012 Map – Barnett Shale Assets CMLP Natural Gas Gathering Pipeline Third-Party Natural Gas Gathering Pipeline Third-Party Natural Gas Takeaway Pipeline CMLP Natural Gas Processing Plants Third-Party Natural Gas Processing Plants CMLP Treating and Compression Facility Competitive Asset Legend Cowtown System Alliance System Lake Arlington System The primary producer on the system, Quicksilver, represented 71.6% of CMLP’s Barnett Shale gathering volumes On March 29, 2013, Quicksilver announced that it had executed an agreement to sell an undivided 25.0% interest in its Barnett Shale oil and gas assets for $485.0 million to TG Barnett Resources LP, a U.S. subsidiary of Tokyo Gas Co., Ltd. – Future development spending will be shared in proportion to each party’s working interest Overview of CMLP |

Asset Overview – Barnett Shale (55.3% of 2013E EBITDA Excluding Corporate Expenses) (cont’d) 22 Overview of CMLP Source: Public partnership filings and HPDI Wells Spud and Permits by Quarter (Denton, Tarrant, Hood, Johnson, Somervell and Bosque Counties, Texas) -- 150 300 450 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Permits Spuds On August 24, 2012, CMLP acquired certain gathering and processing assets from Devon Corporation (“Devon”) in west Johnson County, Texas (the “West Johnson County System”) – The assets acquired consist of a 74-mile low pressure natural gas gathering system, a 100 MMcfd cryogenic processing facility and 23,100 horsepower of compression equipment – Additionally, CMLP entered into a 20-year, fixed-fee gathering, processing and compression agreement with Devon, pursuant to which CMLP will gather and process Devon’s natural gas production from a 20,500 acre dedication • Natural gas production gathered and processed pursuant to the agreement was approximately 96 MMcfd as of December 31, 2012 – The West Johnson County System was operational from August 24, 2012 to December 1, 2012 • On December 1, 2012, CMLP elected to cease operating the 100 MMcfd natural gas processing plant and consolidated natural gas volumes then on the West Johnson County System onto the Cowtown System – CMLP is currently evaluating other potential uses for the 100 MMcfd natural gas processing plant Producing Wells and Production by Quarter (Denton, Tarrant, Hood, Johnson, Somervell and Bosque Counties, Texas) Confidential DRAFT Production (MMcfed) Average Producing Wells 7,500 9,500 10,500 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 3,750 4,250 4,500 4,750 4,000 8,500 |

Asset Overview – Marcellus Shale (30.8% of 2013E EBITDA Excluding Corporate Expenses) 23 Overview of CMLP Antero Resources LLC (“Antero”) is the only producer on CMLP’s Marcellus Shale assets Based upon Antero’s current 2013 drilling plan in the eastern part of CMLP’s dedicated acreage: – CMLP management expects 60 to 70 new well connections in 2013 – CMLP management expects to expand its low pressure gathering systems with an additional 18 miles of pipeline – In addition to the four compressor stations acquired from Enerven in January 2013 for $95.0 million, CMLP also expects to add at least two new compressor stations during 2013 CMLP is in early discussions with Antero regarding the accelerated development of midstream infrastructure in the western part of CMLP’s dedicated acreage including the addition of incremental compressor stations to increase total gathering capacity CMLP’s Marcellus Shale assets gather natural gas production that Evercore believes, given well costs and production profile, generate 20.0% + IRRs for producers down to a $3.50 per MMBtu natural gas price Map – Marcellus Shale Assets Source: Public partnership filings and HPDI Wells Spud and Permits by Quarter (Harrison and Doddridge Counties, West Virginia) CMLP Natural Gas Gathering Pipeline Third-Party Natural Gas Gathering Pipeline Third-Party Natural Gas Takeaway Pipeline Third-Party Natural Gas Processing Plants CMLP Compression Station Antero Acreage Dedication Competitive Asset Legend Producing Wells and Production by Quarter (Harrison and Doddridge Counties, West Virginia) -- 10 20 30 40 50 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Permits Spuds 5,000 5,500 6,000 6,500 -- 100 200 300 400 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Production (MMcfed) Average Producing Wells Confidential DRAFT |

Asset Overview – Fayetteville Shale (10.5% of 2013E EBITDA Excluding Corporate Expenses) 24 Overview of CMLP Fayetteville segment EBITDA increased approximately $7.9 million during the year ended December 31, 2012 compared to 2011 and gathering volume increased by 22.5 MMcfd in 2012 compared to 2011 – During the year ended December 31, 2012, BHP connected six new wells on the Twin Groves System The Fayetteville System’s volumes are supported by long-term fixed-fee contracts with producers with approximately 100,000 acres dedicated to CMLP – These contracts have initial terms that extend through 2020 and include an option, by either party to the contract, to extend the contract through 2025 Primary producer, BHP, acquired CHK’s Fayetteville Shale upstream assets on February 22, 2011 for $4.25 billion On August 3, 2012, BHP took a $2.84 billion writedown on its Fayetteville assets, and BHP’s CEO Marius Kloppers stated, “The Fayetteville charge reflects the fall in United States domestic gas prices and the company’s decision to adjust its development plans by shifting drilling from dry gas to more liquids rich fields” Source: Public partnership filings and HPDI Wells Spud and Permits by Quarter (Van Buren, Conway, Faulkner and White Counties, Arkansas) -- 75 150 225 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Permits Spuds CMLP Natural Gas Gathering Pipeline Third-Party Natural Gas Gathering Pipeline Third-Party Natural Gas Takeaway Pipeline CMLP Treating and Compression Facility Third-Party Natural Gas Processing Plants Prairie Creek Twin Groves Woolly Hollow Producing Wells and Production by Quarter (Van Buren, Conway, Faulkner and White Counties, Arkansas) Confidential DRAFT Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Production (MMcfed) Average Producing Wells 1,500 2,000 2,500 1,750 2,750 3,750 Rose Bud Map – Fayetteville Shale Assets Competitive Asset Legend Wilson Creek |

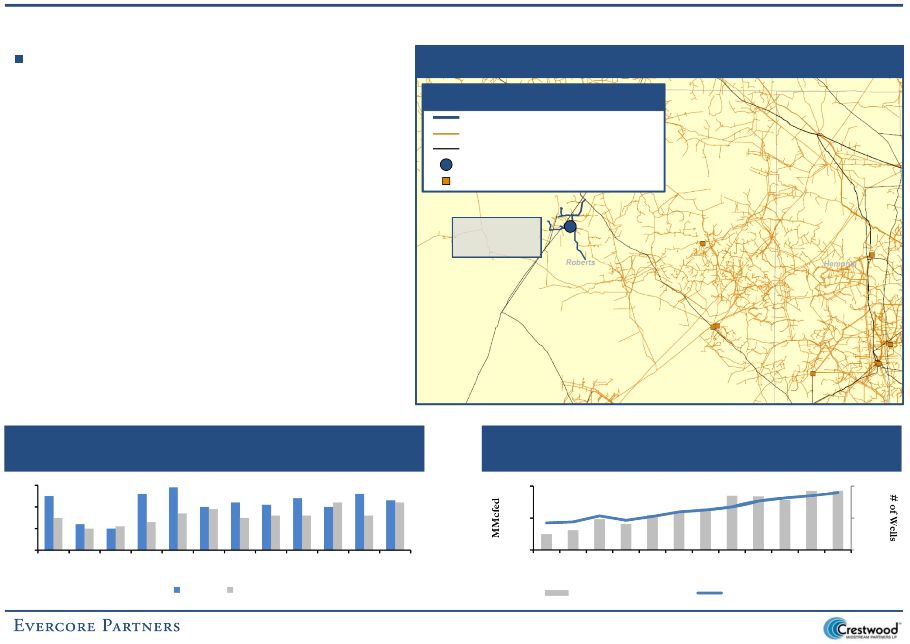

25 Overview of CMLP For the year ended December 31, 2012, the Granite Wash segment’s EBITDA was approximately $0.8 million lower than in 2011, primarily due to lower product sales margin and higher operations and maintenance expenses while volumes on the system increased by 5.2 MMcfd, or 41.4%, versus 2011 – Lower margins earned on percent-of- proceeds contracts, which primarily resulted from lower NGL and natural gas prices coupled with relatively consistent costs per volume – Higher gathering revenues from new wells connected by Sabine Oil and Gas LLC (“Sabine”) partially offset the decline in product sales margin in 2012 Source: Public partnership filings and HPDI CMLP Natural Gas Gathering Pipeline Third-Party Natural Gas Gathering Pipeline Third-Party Natural Gas Takeaway Pipeline CMLP Natural Gas Processing Plants Third-Party Natural Gas Processing Plants Indian Creek System Confidential DRAFT Wells Spud and Permits by Quarter (Roberts County, Texas) Producing Wells and Production by Quarter (Roberts County, Texas) Permits Spuds 30 20 10 -- Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Production (Mmcfed) Average Producing Wells 250 200 150 1,200 1,100 1,000 Map – Granite Wash Assets Competitive Asset Legend Asset Overview – Granite Wash (1.8% of 2013E EBITDA Excluding Corporate Expenses) |

Confidential Asset Overview – Haynesville Shale (1.5% of 2013E EBITDA Excluding Corporate Expenses) 26 Overview of CMLP Map – Haynesville Shale Assets Source: Public partnership filings and HPDI Wells Spud and Permits by Quarter (Sabine Parish, Louisiana) -- 25 50 75 100 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Permits Spuds On November 1, 2011, CMLP acquired Tristate Sabine, LLC (“Tristate”) from affiliates of Energy Spectrum Capital, Zwolle Pipeline, LLC and Tristate’s management for approximately $72.0 million in cash consideration comprised of $64.0 million paid at closing plus a deferred payment of approximately $8.0 million, which was paid during the fourth quarter of 2012 The Sabine System is supported by long-term, fixed- fee contracts with approximately 20,000 acres dedicated to CMLP – These contracts have various initial terms that extend through 2019 and 2021 The Sabine System had 50 MMcfd in gathered volumes for the year ended December 31, 2012, which resulted in approximately $10.0 million in revenues for the year ended December 31, 2012 CMLP Natural Gas Gathering Pipeline Third-Party Natural Gas Gathering Pipeline Third-Party Natural Gas Takeaway Pipeline CMLP Treating and Compression Facility Third-Party Natural Gas Processing Plants Competitive Asset Legend Sabine System Producing Wells and Production by Quarter (Sabine Parish, Louisiana) 275 375 475 575 -- 250 500 750 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Production (MMcfed) Average Producing Wells DRAFT |

Asset Overview – Avalon Shale (0.1% of 2013E EBITDA Excluding Corporate Expenses) 27 Overview of CMLP Effective February 1, 2011, CMLP acquired approximately 46 miles of natural gas gathering systems located in the Morrow/Atoka trend and the Avalon Shale for $5.1 million from a group of independent producers – Supported by long term, fixed-fee contracts which include existing Morrow/Atoka production and dedications of approximately 90,000 acres at the time of the acquisition – The Las Animas Systems currently has approximately 55,000 acres of dedication from Bass Oil Production Company through 2017 EBITDA related to the Las Animas System remained relatively unchanged for the year ended December 31, 2012 compared to 2011 as volumes decreased by 5.3% during the year Source: Public partnership filings and HPDI -- 100 200 300 400 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Permits Spuds CMLP Natural Gas Gathering Pipeline Third-Party Natural Gas Gathering Pipeline Third-Party Natural Gas Takeaway Pipeline CMLP Treating and Compression Facility Third-Party Natural Gas Processing Plants Wells Spud and Permits by Quarter (Eddy County, New Mexico) Producing Wells and Production by Quarter (Eddy County, New Mexico) Confidential DRAFT Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 1,500 1,000 500 -- 12,000 11,500 11,000 10,500 10,000 Production (MMcfed) Average Producing Wells Competitive Asset Legend Las Animas Systems Map – Avalon Shale Assets |

CMLP – Summary Market Data ($ in millions, except per unit amounts) Market Capitalization Balance Sheet and Credit Data Unit Price and Distribution Information Overview of CMLP 28 Source: Public partnership filings and Factset (1) Includes 6,190,469 Class D Units (2) Excludes 6,190,469 Class D Units General Partner Incentive Distribution Rights As of April 19, 2013 Total Units Outstanding (1) 61.1 Common Unit Price $24.97 Total Equity Value $1,524.9 Plus: Total Debt 702.7 Less: Cash (0.1) Total Enterprise Value $2,227.4 IBES Yield/ Data Multiple Distribution Yield Current $2.04 8.2% 2013E 2.07 8.3% 2014E 2.15 8.6% 2015E 2.26 9.1% TEV / EBITDA 2013E $179.1 12.4x 2014E 229.5 9.7 2015E 296.3 7.5 As of December 31, 2012 Cash and Marketable Securities $0.1 Short-term Debt 3.9 Long-term Debt 698.8 Total Debt $702.7 Net Debt 702.5 Plus: Partners' Capital 978.6 Net Book Capitalization $1,681.2 Revolver Availability / Revolver Capacity $406 / $750 Net Debt / Net Book Cap 41.8% Net Debt / 2013E EBITDA 3.9x Net Debt / 2014E EBITDA 3.1x Current Ratings: Moody's B3 S&P B $34.00 $30.00 $26.00 $22.00 $18.00 4/19/11 9/12/11 2/5/12 6/30/12 11/23/12 4/19/13 $2.10 $2.00 $1.90 $1.80 $1.70 $1.60 $1.50 DRAFT Confidential Distribution per Unit Unit Price Quarterly Distribution per LP Unit $0.5100 Quarterly Total Total Total Total LP Quarterly Quarterly Distribution Total Quarterly Quarterly Annual Annual Distribution Distribution to GP LP Units (2) Distribution Distribution Distribution Distribution % to LP % to GP Range Within Range per LP Unit Outstanding to LPs to GP to LPs to GP 98.2% 1.8% $0.0000 $0.3450 $0.3450 $0.0064 53.8 $18.5 $0.3 $74.2 $1.4 85.2% 14.8% 0.3450 0.3750 0.0300 0.0052 53.8 1.6 0.3 6.5 1.1 75.2% 24.8% 0.3750 0.4500 0.0750 0.0248 53.8 4.0 1.3 16.1 5.3 50.2% 49.8% 0.4500 0.4500 0.0600 0.0596 53.8 3.2 3.2 12.9 12.8 $27.4 $5.2 $109.7 $20.6 % of Total Distributions to the GP 15.8% % of Total Distributions to the IDRs 14.0% |

Confidential DRAFT Trading Performance 29 Overview of CMLP Source: Public partnership filings and Factset 12/8/2008: Purchased Lake Arlington Dry System for $42.0 million 12/10/2009: Announced purchase of Alliance system midstream gathering and treating assets from Quicksilver Resources Inc for $87.1 million 7/22/2010: Announced sale by Quicksilver Resources Inc of all of its interest in Quicksilver Gas Services to Crestwood Holdings Partners LLC for $701.0 million 10/04/2010: Changed name from Quicksilver Gas Services LP to Crestwood Midstream Partners LP 2/01/2011: Acquired natural gas gathering pipelines located in Avalon Shale for $5.1 million from a group of independent producers 2/18/2011: Announced agreement to acquire midstream assets in Fayetteville Shale and Granite Wash from Frontier Gas Services, LLC for $345.0 million 12/13/2011: Announced signing of memorandum of understanding with Mountaineer Keystone LLC to construct 42- mile, 16-inch natural gas gathering system to serve Marcellus Shale development program 4/01/2011: Issued 6.24 million Class C Units in private placement for $24.50 per unit 10/18/2011: Announced agreement to acquire Tristate Sabine, LLC from affiliates of Energy Spectrum Capital, Zwolle Pipeline LLC and Tristate management for $73.0 million 7/23/2012: Announced agreement to acquire midstream assets in the Barnett Shale from Devon Corporation for $90.0 million 11/26/2012: CMM agrees to acquire natural gas compression and dehydration assets from Enerven Compression, LLC for $95.0 million 2/27/2012: Announced agreement with Crestwood Holdings Partners LLC and Antero Resources Appalachian Corporation through newly-formed JV, Crestwood Marcellus Midstream (“CMM”), to acquire certain of Antero’s Marcellus Shale assets for $375.0 million 1/8/2013: Agrees to acquire remaining 65.0% interest in CMM from Crestwood Holdings Partners LLC for $258.0 million 0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 $20.00 $22.50 $25.00 $27.50 $30.00 $32.50 $35.00 $37.50 $40.00 6/20/08 12/13/08 6/7/09 12/1/09 5/26/10 11/19/10 5/14/11 11/6/11 5/1/12 10/24/12 4/19/13 $17.50 $15.00 $12.50 $10.00 $7.50 $5.00 $2.50 $-- |

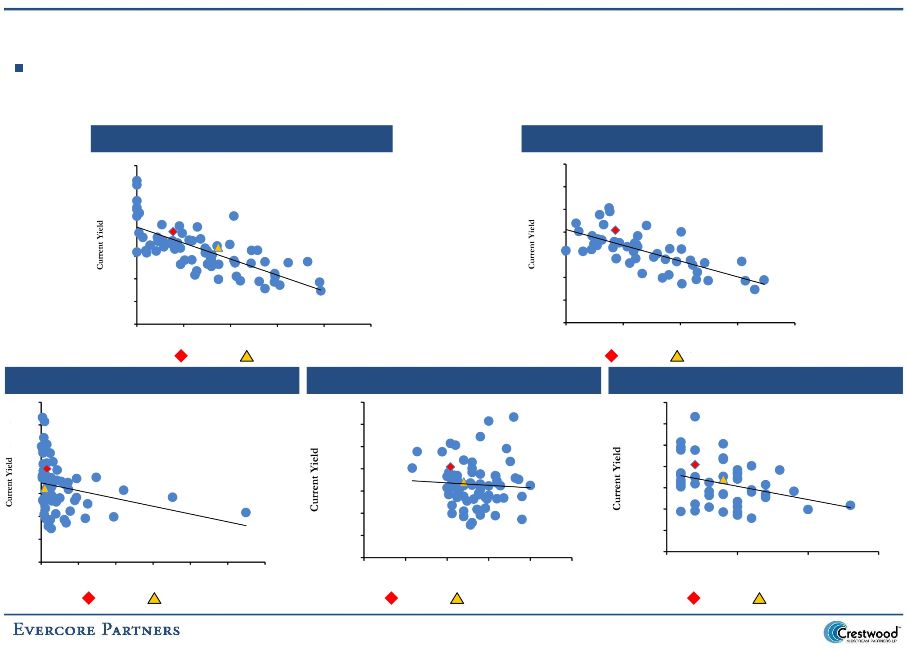

Confidential DRAFT Overview of CMLP 30 Relevant Relative Trading Metrics ($ in millions, except per unit amounts) Source: Partnership filings, FactSet, IBES Enterprise Value / Price Equity Enterprise EBITDA Distribution Yield Distribution Total Partnership (04/19/2013) Value Value 2013E 2014E Current 2013E 2014E Growth Return Natural Gas Gathering and Processing MLPs American Midstream Partners, LP $17.09 $159.9 $370.1 12.5x 11.6x 10.1% 10.1% 11.0% 2.9% 13.0% Atlas Pipeline Partners, L.P. 35.55 2,341.9 3,585.6 10.3 8.5 6.5% 7.1% 8.0% 9.9% 16.4% Access Midstream Partners, L.P. 40.41 7,814.3 10,360.9 12.8 10.0 4.5% 4.9% 5.6% 10.6% 15.0% Crosstex Energy, L.P. 19.12 1,828.0 2,864.2 12.2 9.3 6.9% 7.3% 7.9% 5.3% 12.2% DCP Midstream Partners, LP 47.62 2,946.1 4,600.5 12.6 9.2 5.8% 6.0% 6.5% 8.4% 14.2% MarkWest Energy Partners, L.P. 60.68 9,046.7 11,550.2 16.6 12.2 5.4% 5.7% 6.2% 9.2% 14.6% Regency Energy Partners LP 26.07 5,360.4 8,213.9 13.1 10.5 7.1% 7.4% 7.9% 5.0% 12.0% Southcross Energy Partners, L.P. 20.86 520.1 962.3 18.2 16.9 7.7% 8.5% 8.9% 5.0% 12.7% Summit Midstream Partners, LP 26.92 1,341.0 1,532.4 13.2 10.8 6.1% 6.4% 7.1% 8.0% 14.1% Targa Resources Partners LP 48.53 5,040.6 7,516.4 11.8 9.2 5.6% 5.9% 6.5% 8.5% 14.1% Western Gas Partners, LP 58.10 6,231.5 8,029.5 18.3 13.4 3.7% 3.9% 4.5% 11.6% 15.3% Mean 13.8x 11.1x 6.3% 6.7% 7.3% 7.7% 14.0% Median 12.8 10.5 6.1% 6.4% 7.1% 8.4% 14.1% Crestwood Midstream Partners LP $24.97 $1,524.9 $2,256.4 12.6x 9.8x 8.2% 8.3% 8.6% 4.1% 12.3% |

Confidential DRAFT Wall Street Research Price Targets ($ in millions, except per unit amounts) Summary Price Targets 31 Analyst Recommendations Source: Bloomberg, IBES Distribution Per Unit Estimates EBITDA Estimates Overview of CMLP Hold (2) 33.3% Buy (4) 66.7% $2.09 $2.17 $2.26 $2.12 $2.24 $2.36 $2.04 $2.14 $2.07 $2.10 $2.20 $2.07 $2.15 $2.26 $1.80 $1.90 $2.00 $2.10 $2.20 $2.30 $2.40 2013E 2014E 2015E $178.0 $258.0 $307.0 $179.1 $209.0 $180.7 $229.0 $178.6 $248.8 $316.4 $179.1 $229.5 $296.3 $-- $50.0 $100.0 $150.0 $200.0 $250.0 $300.0 $350.0 2013E 2014E 2015E Barclays Ladenburg Thalmann RBC Wells Fargo IBES Target Firm Analyst Date Recommendation Price Ladenburg Thalmann Eduardo Seda 02/27/13 Buy $32.50 Hilliard Lyons Joel K. Havard 02/27/13 Long-term Buy 32.00 Simmons Mark L. Reichman 03/21/13 Overweight 30.00 Barclays Richard Gross 02/28/13 Equalweight 27.00 RBC T.J. Schultz 02/27/13 Sector Perform 26.00 Wells Fargo Michael J. Blum 02/28/13 Outperform NA Median: $30.00 Mean: 29.50 Low: 26.00 High: 32.50 |

Research Analyst Commentary Overview of CMLP 32 “In our opinion, given our assumption of an improving sector growth outlook, a weak natural gas but strong crude oil and NGL commodity price environment, additional organic growth projects coming on-line, as well as contributions from the recent acquisitions and CMLP’s increased growth capex budget, we believe CMLP is well positioned to achieve a distribution growth rate of 5.6% CAGR over the 2013-15 period, and thereafter at a higher rate.” – Ladenburg Thalmann, Eduardo Seda; February 27, 2013 ���We expect CMLP's valuation to improve as investors better appreciate the partnership's growing geographic footprint, stable cash flow (98% fee-based), strong sponsor support, and potential upside tied to future acquisitions and organic investments. We forecast CMLP to grow distributions at a 5-year CAGR of approximately 4% supported by volume growth in liquids-rich areas.” – Wells Fargo Securities, Ronald F. Londe; February 28, 2013 “We forecast 5-year distribution CAGR of 3.9%. We believe CMLP will be able to raise distribution at a moderate pace, but expect near-term coverage to be impacted (and light) from Class C and D unit conversions in 2Q13 and 1Q14, respectively. Risks to the upside include potential parent-led drop downs, a recovery in dry gas volumes or new oil / rich gas projects” – Barclays Capital, Richard Gross; February 28, 2013 Price Target: $32.50 Price Target: NA Price Target: $27.00 DRAFT Confidential |

Confidential DRAFT Ratings Agency Commentary 33 Overview of CMLP Standard & Poor’s – B/Stable (Nora Pickens & Michael V. Grande – March 29, 2013) – “CMLP’s aggressive growth strategy, customer concentration to Quicksilver Resources Inc., and potential cash flow volatility due to lower natural gas throughput characterize the partnership's “weak” business profile. High financial leverage and the master limited partnership structure, which gives CMLP much incentive to pay out most of its cash flow after maintenance capital spending to unitholders each quarter, reflect the aggressive financial profile. CMLP’s mostly fee-based contract mix and minimal direct commodity exposure partly offset these risks.” – “We could lower the rating if a debt-financed acquisition or a decrease in volumes causes cash flow to decline and financial ratios to deteriorate, stand-alone and fully consolidated basis, respectively, for an extended period” – “A higher rating is unlikely at this time because of CMLP’s limited scale and high consolidated leverage, but is attainable if we believe it will maintain consolidated leverage at 4x or less.” Moody’s – B2/Stable (Jonathan Kalmanoff & Steven Wood – March 28, 2013) – “Crestwood's B2 corporate family rating is supported by fixed fee contracts that avoid direct commodity price exposure, a moderate degree of basin and customer diversification, exposure to producing basins with liquids production, minimum volume commitments for a portion of throughput, a management team with extensive experience in the midstream sector, and a private equity sponsor with the industry knowledge and financial capacity to support the company's growth ambitions. concentration relative to rated midstream peers, volumes driven by E&P drilling activity which is indirectly tied to commodity prices, and high consolidated leverage.” such that debt to EBITDA remains above 5.5x and 7.0x on a The rating is restrained by business line |

Equity Ownership Summary Overview of CMLP Includes 6,190,469 Class D Units and 1,112,674 GP units Source: NASDAQ National Markets as of March 28, 2013 34 Institutional Top 10: Kayne Anderson Capital Advisors LP 5,807,677 9.5% Tortoise Capital Advisors LLC 2,676,178 4.4% ClearBridge Investments LLC 2,481,349 4.1% Center Coast Capital Advisors LP 2,463,613 4.0% Tiverton Asset Management LLC 600,000 1.0% JPMorgan Securities LLC 512,084 0.8% UBS Global Asset Management 279,425 0.5% Advisors Asset Management, Inc. 159,065 0.3% Wells Fargo Advisors LLC 115,524 0.2% Fidelity Management & Research Co. 95,332 0.2% Other 888,299 1.5% Total Institutional Ownership 16,078,546 26.3% Insiders First Reserve Corp. 27,135,412 44.4% Other 448,596 0.7% Total Insiders 27,584,008 45.2% Retail / Other 17,405,513 28.5% Total Units Outstanding (1) 61,068,067 100.0% Short Interest (2) 639,653 1.0% Current Unitholders Units % of Total (1) Confidential DRAFT Source: FactSet (1) (2) |

Confidential DRAFT Overview of CMLP 35 CMLP Management Financial Projections – Assumptions The CMLP Management Financial Projections as provided by CMLP management and utilized herein by Evercore, incorporate the following assumptions: – Marcellus volumes are expected to increase 101.2% year-over-year from 227.2 MMcfd in 2012A to 457.1 MMcfd in 2013E based on Antero’s volume forecast provided to CMLP management – Barnett rich natural gas volumes are expected to increase 32.2% year-over-year from 163.5 MMcfd in 2012A to 216.1 MMcfd in 2013E based on a full year contribution from Devon and increasing offload point volumes from Empire Pipeline Corporation (“Empire”) Empire is as a natural gas utility serving Parker, western Tarrant, northern Hood and western Johnson Counties, Texas operating over 240 miles of low-pressure gathering and transmission pipeline – Barnett dry natural gas volumes are expected to decline by 12.5% year-over-year from 268.4 MMcfd in 2012A to 234.9 MMcfd in 2013E due to limited anticipated 2013E drilling activity and no well completions by Quicksilver – Fayetteville dry natural gas volumes are expected to increase by 12.9% year-over-year from 86.7 MMcfd in 2012A to 97.9 MMcfd in 2013E due to 23 new BHP wells expected to be connected to the CMLP gathering system – Rich natural gas volumes from the Marcellus, Barnett, Granite Wash and Avalon are expected to grow at a 5-year compound annual growth rate (“CAGR”) of 10.9% based on forecasts provided by producers and management’s estimates of drilling activity corresponding to current 5-year commodity strip pricing – Dry natural gas volumes are expected to grow at a 5-year CAGR of 11.6% based on management’s estimate of two to three rigs working in the Fayetteville Shale for BHP beginning in 2014E, one to two rigs working in the Barnett Shale beginning in 2014E and an average of one half of one rig per year working in the Haynesville beginning in 2014E – Operations and maintenance expenses were derived from a bottom-up forecast provided by CMLP operations managers 2013E includes full-year expenses for CMM, West Johnson County and Enerven assets and a partial year of expenses for new Marcellus compressor stations in addition to the incremental costs of 18 new full time employees Fixed costs assumed to increase at 3% per year after 2013E |

Overview of CMLP 36 – General and administrative expenses were also derived from a bottom-up forecast provided by CMLP operations managers 2013E includes incremental costs for 23 additional full-time employees and additional equity compensation and amortization expenses General and administrative expenses assumed to increase at 4% per annum after 2013E – Similarly, 2013E maintenance and growth capital expenditure estimates were also derived from a bottom-up forecast provided by CMLP operations managers and include: 2013E maintenance capital expenditures are projected to be $9.3 million including compressor overhauls and a new compressor warehouse – Five year maintenance capital expenditures based on 2013E budget and consist primarily of compressor overhauls 2013E growth capital expenditures are projected to be $126.8 million and include $77.1 million of new pipeline and compressor stations in the Marcellus, $22.0 million for the West Union Compressor Station in Doddridge County, West Virginia, $5.1 million for the upgrade of Enerven compressor stations with the remaining $22.7 million primarily related to new well connections – Five year growth capital expenditures based on forecasted well connections and associated pipeline capital projects, as well as additional Marcellus compressor stations and Fayetteville and Granite Wash facility expansions Excludes potential other growth capital expenditure opportunities, including: – The potential acquisition of RKI Exploration & Production, LLC’s (“RKI”) 50.0% non-operating interest in the Jackalope Gas Gathering System (“JGGS”) in the Niobrara Basin, and the further development of that system for $199.1 million in 2013E – The potential acquisition of 41 miles of high-pressure pipeline and two compressor stations in the Marcellus from MarkWest Energy Partners, L.P. (the “MarkWest Marcellus Bolt-On Acquisition”) for $125 million – The potential acquisition of certain pipeline assets pursuant to CMM’s seven-year right of first offer to acquire any midstream assets sold by Antero in an area of approximately 100,000 acres adjacent to Antero’s current area of dedication (“Antero Western AOD Acquisition”) for $250 million CMLP Management Financial Projections – Assumptions (cont’d) DRAFT Confidential |

Confidential DRAFT – Growth capital expenditures to be financed with revolver borrowings at an interest rate of 3.60%, 3.75%, 4.50%, 5.00% and 5.50% in 2013E, 2014E, 2015E, 2016E and 2017E, respectively – Assumes CMLP’s Class D Units distributions are paid in-kind with additional Class D Units until conversion into 6.8 million CMLP common units in March 2014 on a one-for-one basis – $200.0 million senior note offering on June 30, 2014 assumed to be issued at an 8.0% interest rate with proceeds utilized to reduce borrowings from CMLP’s revolving credit facility – Distribution per LP unit of $2.07 and $2.15 in 2013E and 2014E, respectively, and a target 10.0% distribution per LP unit growth rate in 2015E, 2016E and 2017E – No interest income on cash balances Overview of CMLP 37 CMLP Management Financial Projections – Assumptions (cont’d) Assumes CMLP yield of 9.0%, 8.5%, 8.0% and 7.5% in the first, second, third and fourth quarter of 2013E, respectively LP distribution coverage of 1.10x, 1.10x and 1.06x for 2015E, 2016E and 2017E, respectively |

2013E Growth Capital Expenditures – Summary 38 Overview of CMLP Source: CMLP management ($ in millions) For the Quarter Ending Fiscal Year Budgeted Growth Capital Expenditures 3/31/13E 6/30/13E 9/30/13E 12/31/13E 2013E Marcellus: Zinnia Mainlines $-- $30.1 $7.1 $-- $37.2 Perkins/Morgan Stations 5.0 12.7 6.4 4.9 29.0 Other Marcellus Laterals -- 3.5 6.7 0.7 10.9 Enerven Engine Upgrades 1.3 2.5 1.3 -- 5.1 Mackey Wolfe Lateral 1.8 1.8 -- -- 3.6 West Union Station 14.7 3.8 0.4 3.1 22.0 Total Marcellus $22.8 $54.4 $21.9 $8.7 $107.8 Barnett 1.8 2.4 3.7 2.5 10.4 Fayetteville 0.8 0.2 0.9 -- 1.9 Granite Wash 1.5 -- -- -- 1.5 Haynesville 0.1 0.3 -- -- 0.4 Avalon -- -- -- -- -- Corporate (Oracle/SAP) 0.2 2.2 1.2 1.2 4.8 Total Budgeted Growth Capital Expenditures $27.2 $59.5 $27.7 $12.4 $126.8 Upside Growth Capital Expenditures Q1 2013 Q2 2013 Q3 2013 Q4 2013 2013E RKI Niobrara Development $91.5 $12.0 $47.8 $47.8 $199.1 MarkWest Marcellus Bolt-On Acquisition -- 125.0 -- -- 125.0 Antero Western AOD Acquisition -- -- 250.0 -- 250.0 Identified Incremental Capital Expenditures $91.5 $137.0 $297.8 $47.8 $574.1 Total Potential Capital Expenditures (Budget + Potential) $118.7 $196.5 $325.5 $60.2 $700.9 Confidential DRAFT |

CMLP Management Financial Projections 39 Overview of CMLP The following sets forth selected operating projections provided by CMLP management utilized in deriving the CMLP Management Financial Projections herein: Confidential DRAFT For the Year Ended December 31, For the Years Ending December 31, CAGR 2010A 2011A 2012A 2013E 2014E 2015E 2016E 2017E 2013E - 2017E Gathering Volumes (MMcfd) Barnett Rich 129.5 143.9 163.5 216.1 211.6 210.6 212.9 215.9 (0.0%) Granite Wash -- 16.6 17.6 29.7 46.1 58.4 66.4 72.1 24.8% Avalon -- 11.5 9.0 6.8 5.2 4.3 3.6 3.1 (17.4%) Marcellus -- -- 227.2 457.1 572.5 692.0 740.5 783.3 14.4% Total Rich Gathering Volumes 129.5 172.0 417.2 709.7 835.3 965.3 1,023.4 1,074.4 10.9% Barnett Dry 213.8 329.7 268.4 234.9 256.6 275.7 277.8 283.2 4.8% Fayetteville -- 85.2 86.7 97.9 117.1 160.6 205.7 235.7 24.6% Haynesville -- 60.1 50.5 33.6 32.4 42.4 46.0 48.9 9.8% Total Dry Gathering Volumes 213.8 475.0 405.6 366.4 406.1 478.8 529.5 567.8 11.6% Total Gathering 343.3 647.0 822.8 1,076.1 1,241.5 1,444.0 1,552.9 1,642.2 11.1% Processing Volumes (MMcfd) Barnett 127.8 131.8 155.7 207.0 202.6 201.6 203.8 206.8 (0.0%) Granite Wash -- 12.3 17.5 29.4 45.6 57.8 65.7 71.3 24.8% Total Processing Volumes 127.8 144.1 173.2 236.4 248.2 259.4 269.6 278.1 4.1% Compression Volumes (MMcfd) Marcellus -- -- 6.4 331.8 543.9 702.9 752.0 794.8 24.4% Well Connections Barnett Rich NA NA 43.0 60.0 68.0 68.0 68.0 68.0 Granite Wash NA NA 5.0 10.0 16.0 16.0 15.0 15.0 Avalon NA NA -- -- -- -- -- -- Marcellus NA NA 60.0 65.0 102.0 69.0 73.0 73.0 Total Rich Well Connections NA NA 108.0 135.0 186.0 153.0 156.0 156.0 Barnett Dry NA NA 23.0 8.0 41.0 35.0 32.0 32.0 Fayetteville NA NA 18.0 23.0 35.0 60.0 60.0 60.0 Haynesville NA NA 1.0 -- 5.0 5.0 5.0 5.0 Total Dry Well Connections NA NA 42.0 31.0 81.0 100.0 97.0 97.0 Total Well Connections NA NA 150.0 166.0 267.0 253.0 253.0 253.0 |

CMLP Management Financial Projections (cont’d) ($ in millions) 40 Overview of CMLP The following sets forth the CMLP Management Financial Projections utilized by Evercore in its analysis herein: For the Years Ending December 31, CAGR 2013E 2014E 2015E 2016E 2017E 2013E - 2017E Revenue, Less Purchases: Barnett Rich $90.5 $93.7 $101.5 $108.4 $115.1 Granite Wash 5.9 10.2 14.0 16.5 18.4 Avalon 0.4 0.3 0.3 0.2 0.2 Marcellus 69.9 100.1 127.6 140.4 152.3 Total Rich Natural Gas Revenue $166.7 $204.3 $243.3 $265.6 $285.9 14.4% Barnett Dry 49.5 52.5 59.1 62.4 65.8 Fayetteville 30.6 36.5 49.7 66.1 78.2 Haynesville 5.3 5.6 7.9 8.2 9.0 Total Dry Natural Gas Revenue $85.4 $94.7 $116.7 $136.7 $153.0 15.7% Total Revenue, Less Purchases $252.1 $299.0 $360.0 $402.3 $439.0 14.9% Operating Expense: CMLP Operating Expense $42.9 $44.9 $48.6 $51.7 $54.1 CMM Operating Expense 7.9 9.8 10.6 10.9 11.2 Total Operating Expense $50.8 $54.7 $59.2 $62.6 $65.3 6.5% General and Administrative Expense: CMLP General and Administrative Expense $25.4 $26.4 $27.4 $28.5 $29.7 CMM General and Administrative Expense 2.9 3.0 3.2 3.3 3.4 Total General and Administrative Expense 28.3 29.4 30.6 31.8 33.1 4.0% Plus: Other Corporate Adjustments 0.3 -- -- -- -- Adjusted EBITDA $173.3 $214.8 $270.3 $307.9 $340.6 18.4% Confidential DRAFT |

Confidential DRAFT CMLP Management Financial Projections (cont’d) ($ in millions, except per unit amounts) 41 Overview of CMLP The following sets forth the CMLP Management Financial Projections utilized by Evercore in its analysis herein: For the Years Ending December 31, CAGR 2013E 2014E 2015E 2016E 2017E 2013E - 2017E Distributable Cash Flow Adjusted EBITDA $173.3 $214.8 $270.3 $307.9 $340.6 18.4% Less: Cash Interest Expense, net (43.0) (52.4) (62.8) (67.6) (72.8) Less: Maintenance Capital Expenditures (9.3) (7.2) (7.7) (8.9) (11.8) Plus: Non-Cash Equity Compensation 3.8 4.5 4.7 4.9 5.2 Distributable Cash Flow $124.7 $159.8 $204.5 $236.3 $261.1 20.3% Distributed Cash Flow Common Units (Public) $70.6 $73.3 $80.6 $88.7 $97.6 Common Units (Crestwood Holdings) 40.7 57.0 62.7 69.0 75.9 GP 22.2 30.3 43.3 57.7 73.4 Total $133.5 $160.6 $186.7 $215.4 $246.9 16.6% % to GP 16.6% 18.9% 23.2% 26.8% 29.7% GP IDRs $20.1 $27.6 $40.4 $54.5 $69.9 Weighted Average LP Units Outstanding 60.2 60.6 60.6 60.6 60.6 DCF / LP Unit $1.99 $2.14 $2.51 $2.78 $2.98 10.7% Distribution / LP Unit $2.07 $2.15 $2.37 $2.60 $2.86 8.4% LP Coverage 0.96x 1.00x 1.06x 1.07x 1.04x Total Coverage 0.93x 0.99x 1.10x 1.10x 1.06x Distributable Cash Flow Surplus / (Shortfall) ($8.7) ($0.9) $17.8 $20.9 $14.2 |

CMLP Management Financial Projections (cont’d) ($ in millions) 42 The following sets forth the funding assumptions utilized in the CMLP Management Financial Projections and CMLP’s resulting capital structure and credit statistics Overview of CMLP For the Years Ending December 31, 2013E 2014E 2015E 2016E 2017E Sources: Equity Issued (Public) $119.0 $-- $-- $-- $-- Equity Issued (Crestwood Holdings) -- -- -- -- -- GP Contribution (Crestwood Holdings) -- -- -- -- -- Class D Units Issued for Acquisition of 65.0% of CMM 129.0 -- -- -- -- Revolver Draw for Acquisition of 65.0% of CMM 129.0 -- -- -- -- CMM Debt Issued 32.1 45.0 40.0 40.0 40.0 CMLP Debt Issued/(Repaid), net of Surplus/(Shortfall) 49.8 69.3 14.0 10.7 9.0 DCF Surplus / (Shortfall) (8.7) (0.9) 17.8 20.9 14.2 Contribution from CMLP to CMM 50.0 -- -- -- -- Less: Financing Fees (0.5) -- -- -- -- Total Funding $499.6 $113.4 $71.8 $71.7 $63.3 Debt Issued/(Repaid), net of Surplus/(Shortfall) $92.3 $114.3 $54.0 $50.7 $49.0 Total Equity Issued 248.0 -- -- -- -- Uses: Acquisition of 65.0% of CMM $258.0 $-- $-- $-- $-- Debt Paydown from 5.175 MM Units Issuance 118.5 -- -- -- -- (Increase) / Decrease in Working Capital (3.7) 5.3 -- -- -- Growth Capital Expenditures 126.8 108.1 71.8 71.7 63.3 Total Uses $499.6 $113.4 $71.8 $71.7 $63.3 Credit Statistics Debt / Adjusted EBITDA 4.8x 4.4x 3.7x 3.4x 3.2x Net Debt / Adjusted EBITDA 4.8x 4.4x 3.7x 3.4x 3.2x Capital Structure Cash $0.1 $0.1 $0.1 $0.1 $0.1 Total Debt 826.0 940.3 994.4 1,045.1 1,094.1 Net Debt $825.9 $940.2 $994.3 $1,045.0 $1,094.0 Confidential DRAFT |

Overview of CMLP 43 CMLP Management Financial Projections Comparison to Wall Street Research Estimates The following sets forth a comparison of the CMLP Management Financial Projections and Wall Street Research consensus estimates EBITDA Distribution per LP Unit DCF per LP Unit $2.07 $2.07 $2.15 $2.15 $2.37 $2.60 $2.86 $2.26 $2.35 $2.43 $-- $0.50 $1.00 $1.50 $2.00 $2.50 $3.00 $3.50 2013E 2014E 2015E 2016E 2017E CMLP Management Financial Projections Wall Street Research Distribution Coverage 0.93x 0.99x 1.10x 1.10x 1.06x 0.98x 1.07x 1.27x 1.38x 1.47x -- 0.20x 0.40x 0.60x 0.80x 1.00x 1.20x 1.40x 1.60x 2013E 2014E 2015E 2016E 2017E CMLP Management Financial Projections Wall Street Research $173.3 $214.8 $270.3 $307.9 $340.6 $179.1 $229.5 $296.3 $370.1 $446.5 $-- $100.0 $200.0 $300.0 $400.0 $500.0 2013E 2014E 2015E 2016E 2017E CMLP Management Financial Projections Wall Street Research $1.99 $2.14 $2.51 $2.78 $2.98 $2.05 $2.24 $2.64 $2.93 $3.19 $-- $0.50 $1.00 $1.50 $2.00 $2.50 $3.00 $3.50 2013E 2014E 2015E 2016E 2017E CMLP Management Financial Projections Wall Street Research ($ in millions, except per unit amounts) DRAFT Confidential |

Wall Street Research vs. CMLP Management Financial Projections 44 Overview of CMLP Barclays - February 28, 2013 (Price Target: $27.00) CMLP Management Financial Projections Difference: Research vs. CMLP For the Years Ending December 31, For the Years Ending December 31, For the Years Ending December 31, 2013E 2014E 2015E 2016E 2017E 2013E 2014E 2015E 2016E 2017E 2013E 2014E 2015E 2016E 2017E Adjusted EBITDA $177.5 $257.7 $306.8 $358.5 NA $173.3 $214.8 $270.3 $307.9 $340.6 $4.2 $42.9 $36.5 $50.6 NA Less: Cash Interest Expense, net (50.7) (68.7) (76.8) (84.9) NA (43.0) (52.4) (62.8) (67.6) (72.8) (7.7) (16.3) (14.0) (17.3) NA Less: Maintenance Capital Expenditures (10.0) (14.0) (16.8) (19.8) NA (9.3) (7.2) (7.7) (8.9) (11.8) (0.7) (6.8) (9.1) (10.9) NA Plus: Other 4.0 4.0 4.0 4.0 NA 3.8 4.5 4.7 4.9 5.2 0.2 (0.5) (0.7) (0.9) NA Distributable Cash Flow $120.8 $179.0 $217.2 $257.8 NA $124.7 $159.8 $204.5 $236.3 $261.1 ($3.9) $19.2 $12.7 $21.5 NA DCF / LP Unit $2.10 $2.21 $2.45 $2.70 NA $1.99 $2.14 $2.51 $2.78 $2.98 $0.11 $0.07 ($0.06) ($0.08) NA Distribution / LP Unit $2.09 $2.17 $2.26 $2.35 NA $2.07 $2.15 $2.37 $2.60 $2.86 $0.02 $0.02 ($0.11) ($0.25) NA Growth Capital Expenditures / Acquisitions $583.0 $300.0 $300.0 $300.0 NA $126.8 $108.1 $71.8 $71.7 $63.3 $456.2 $191.9 $228.2 $228.4 NA Wells Fargo - February 28, 2013 (Price Target: $25.00 - $27.00) CMLP Management Financial Projections Difference: Research vs. CMLP For the Years Ending December 31, For the Years Ending December 31, For the Years Ending December 31, 2013E 2014E 2015E 2016E 2017E 2013E 2014E 2015E 2016E 2017E 2013E 2014E 2015E 2016E 2017E Adjusted EBITDA $178.6 $248.8 $316.4 $381.6 $446.5 $173.3 $214.8 $270.3 $307.9 $340.6 $5.3 $34.0 $46.1 $73.7 $105.9 Less: Cash Interest Expense, net (54.2) (71.5) (85.3) (105.7) (127.2) (43.0) (52.4) (62.8) (67.6) (72.8) (11.2) (19.1) (22.5) (38.1) (54.4) Less: Maintenance Capital Expenditures (9.7) (13.1) (16.6) (20.0) (23.3) (9.3) (7.2) (7.7) (8.9) (11.8) (0.4) (5.9) (8.9) (11.1) (11.5) Plus: Other 8.3 8.3 8.3 8.3 8.3 3.8 4.5 4.7 4.9 5.2 4.5 3.8 3.6 3.4 3.1 Distributable Cash Flow $122.9 $172.5 $222.8 $264.2 $304.3 $124.7 $159.8 $204.5 $236.3 $261.1 ($1.8) $12.7 $18.3 $27.9 $43.2 DCF / LP Unit $1.84 $2.15 $2.50 $2.65 $2.77 $1.99 $2.14 $2.51 $2.78 $2.98 ($0.15) $0.01 ($0.01) ($0.13) ($0.21) Distribution / LP Unit $2.07 $2.10 $2.20 $2.32 $2.43 $2.07 $2.15 $2.37 $2.60 $2.86 ($0.00) ($0.05) ($0.17) ($0.28) ($0.43) Growth Capital Expenditures / Acquisitions $375.0 $375.0 $375.0 $375.0 $375.0 $126.8 $108.1 $71.8 $71.7 $63.3 $248.2 $266.9 $303.2 $303.4 $311.8 RBC - February 27, 2013 (Price Target: $26.00) CMLP Management Financial Projections Difference: Research vs. CMLP For the Years Ending December 31, For the Years Ending December 31, For the Years Ending December 31, 2013E 2014E 2015E 2016E 2017E 2013E 2014E 2015E 2016E 2017E 2013E 2014E 2015E 2016E 2017E Adjusted EBITDA $180.7 $229.0 NA NA NA $173.3 $214.8 $270.3 $307.9 $340.6 $7.4 $14.2 NA NA NA Less: Cash Interest Expense, net (45.4) (55.3) NA NA NA (43.0) (52.4) (62.8) (67.6) (72.8) (2.4) (2.9) NA NA NA Less: Maintenance Capital Expenditures (10.0) (12.6) NA NA NA (9.3) (7.2) (7.7) (8.9) (11.8) (0.7) (5.4) NA NA NA Plus: Other 4.1 4.1 NA NA NA 3.8 4.5 4.7 4.9 5.2 0.3 (0.4) NA NA NA Distributable Cash Flow $129.4 $165.2 NA NA NA $124.7 $159.8 $204.5 $236.3 $261.1 $4.7 $5.4 NA NA NA DCF / LP Unit $2.23 $2.27 NA NA NA $1.99 $2.14 $2.51 $2.78 $2.98 $0.24 $0.13 NA NA NA Distribution / LP Unit $2.04 $2.14 NA NA NA $2.07 $2.15 $2.37 $2.60 $2.86 ($0.03) ($0.01) NA NA NA Growth Capital Expenditures / Acquisitions NA NA NA NA NA $126.8 $108.1 $71.8 $71.7 $63.3 NA NA NA NA NA Wall Street Research Analyst CMLP Management Financial Projections Comparison ($ in millions, except per unit amounts) Confidential DRAFT |

IV. Indicative Valuation of CMLP DRAFT |