As filed with the Securities and Exchange Commission on December 11, 2009

Registration No. 333-163119

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

FORM F-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

GAFISA S.A. (Exact Name of Registrant as Specified in Its Charter) |

Not applicable (Translation of Registrant’s name into English) |

| The Federative Republic of Brazil |

| (State or Other Jurisdiction of Incorporation or Organization) |

| 1520 |

| (Primary Standard Industrial Classification Code Number) |

| Not Applicable |

| (I.R.S. Employer Identification Number) |

Av. Nações Unidas No. 8,501, 19th floor 05425−070 − São Paulo, SP – Brazil Telephone: + 55 (11) 3025−9000 |

| (Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices) |

National Corporate Research, Ltd. 10 East 40th Street, 9th floor New York, NY 10016 Telephone: (212) 947-7200 |

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copies to: Diane G. Kerr, Esq. Manuel Garciadiaz, Esq. Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 (212) 450-4000 |

Approximate date of commencement of proposed offer to the public: As soon as practicable after this registration statement becomes effective.

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o __________

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

| CALCULATION OF REGISTRATION FEE | |||

Title of Each Class of Securities To Be Registered | Amount To Be Registered(1) | Proposed Maximum Aggregate Offering Price(2) | Amount of Registration Fee |

| Gafisa S.A. common shares, no par value | 16,442,296 | $264,499,068.80 | $14,759.05(3) |

| (1) | Calculated based on the maximum number of each registrant’s shares to be issued to U.S. holders of common shares of Construtora Tenda S.A., or Tenda, in connection with the Restructuring described in the accompanying preliminary prospectus / information statement assuming that none of the holders exercise their right of withdrawal in connection with the Restructuring. |

| (2) | The Proposed Maximum Aggregate Offering Price for registrant Gafisa (estimated solely for purposes of computing the amount of the registration fee pursuant to Rule 457(c) and Rule 457(f) under the U.S. Securities Act of 1933, as amended) is calculated in accordance with the exchange ratio of 0.205 common share to be exchanged in the Restructuring for each common share held directly by a U.S. resident of Tenda and the average of the high and low prices of the common shares of Tenda, as reported on the São Paulo Stock Exchange on December 9, 2009, converted into U.S. dollars at the exchange rate of R$1.7603 = US $1.00. |

| (3) | Includes an $2,810.68 registration fee previously paid with the intial filing of this Form F-4 on November 13, 2009. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the U.S. Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the U.S. Securities and Exchange Commission, acting pursuant to Section 8(a), may determine.

| The information in this preliminary prospectus/information statement is not complete and may be changed. Gafisa S.A. may not sell these securities until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This preliminary prospectus/information statement is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state or jurisdiction where the offer or sale is not permitted. |

PRELIMINARY PROSPECTUS/INFORMATION STATEMENT (Subject to Completion)

Dated December 11, 2009

| Gafisa S.A. Exchange of Common Shares for Common Shares of Construtora Tenda S.A. |  |

Gafisa S.A., or Gafisa, has proposed a corporate restructuring, or the Restructuring, the overall purpose of which is to consolidate at the Gafisa level all of its noncontrolling share ownership in its direct subsidiary, Construtora Tenda S.A., or Tenda. The Restructuring will be accomplished via a merger of shares (incorporaçăo de ações, under Brazilian law): a merger of all of the Tenda shares that Gafisa does not own into Gafisa in exchange for Gafisa shares, converting Tenda into a wholly-owned subsidiary of Gafisa.

If the Restructuring is approved by both the shareholders of Gafisa and the shareholders of Tenda, holders of common shares of Tenda will receive 0.205 common share, no par value, of Gafisa for each Tenda common share they hold.

The Restructuring will require the approvals of holders of common shares of Gafisa and Tenda as of the date of the shareholders’ meetings. The meetings of the shareholders of Gafisa and Tenda at which the Restructuring will be considered are currently scheduled for December 14, 2009; however, these meetings will not take place until after the registration statement, of which this preliminary prospectus/information statement is a part, has been declared effective by the U.S. Securities and Exchange Commission, or the SEC. Gafisa and its affiliates hold, directly or indirectly, all of the Tenda voting power necessary to approve the Restructuring at the Tenda level without the support of any other holders of common shares of Tenda.

Persons who were holders of record of common shares of Tenda as of October 21, 2009 will have withdrawal rights in connection with the Restructuring as described in this preliminary prospectus/information statement. Holders of Gafisa shares or American Depositary Shares, or ADSs representing Gafisa shares, will not have any withdrawal rights in connection with the Restructuring.

The common shares of Tenda and Gafisa are currently listed on the São Paulo Stock Exchange (BM&FBOVESPA S.A., Bolsa de Valores, Mercadorias e Futuros), or the BM&FBOVESPA. The ADSs of Gafisa are listed on the New York Stock Exchange, or the NYSE, and Gafisa is a foreign private issuer under U.S. securities laws. The common shares of Tenda are not listed or traded in the United States and Tenda has not previously been subject to the reporting requirements in the United States.

You should read this preliminary prospectus/information statement carefully. In particular, please read the section entitled “Part Three: Risk Factors” beginning on page 41 for a discussion of risks that you should consider in evaluating the transactions described in this preliminary prospectus/information statement.

Neither the SEC nor any state securities commission has approved or disapproved of the securities to be issued in connection with the Restructuring or determined if this preliminary prospectus/information statement is truthful or complete. Any representation to the contrary is a criminal offense.

IF YOU ARE A DIRECT HOLDER OF GAFISA OR TENDA SHARES OR GAFISA ADSs, NEITHER GAFISA NOR TENDA IS ASKING YOU FOR A PROXY AND YOU ARE REQUESTED NOT TO SEND GAFISA OR TENDA A PROXY. IF YOU ARE ENTITLED TO VOTE ON THE RESTRUCTURING, WHILE WE HAVE DESCRIBED GENERALLY THE PROCEDURE FOR VOTING YOUR SHARES IN THIS PRELIMINARY PROSPECTUS/INFORMATION STATEMENT, YOU ALSO SHOULD CONSULT BRAZILIAN COUNSEL.

This preliminary prospectus/information statement is dated December 11, 2009 and is expected to be mailed to the shareholders of Gafisa and Tenda beginning on or about that date.

This preliminary prospectus/information statement incorporates by reference important business and financial information about Gafisa and Tenda that is not included in or delivered with the document. This information is available without charge to security holders upon written or oral request. To obtain timely delivery, security holders must request the information no later than December 7, 2009, which is five business days before December 14, 2009, the scheduled date for the shareholders meeting of Gafisa and Tenda to approve the Restructuring. See “Part Seven: Additional Information for Shareholders—Incorporation by Reference.”

Page

| 1 | |

| 8 | |

| 8 | |

| 10 | |

| 11 | |

| 13 | |

| 15 | |

| 16 | |

| 17 | |

| 19 | |

| 19 | |

| 19 | |

| 19 | |

| 19 | |

| 20 | |

| 20 | |

| 21 | |

| 22 | |

| 37 | |

| 37 | |

| 39 | |

| 40 | |

| 41 | |

| 41 | |

| 45 | |

| 45 | |

| 57 | |

| 76 | |

| 76 | |

| 84 | |

| 84 | |

| 85 | |

| 87 | |

| 88 | |

| 88 | |

| 89 | |

| 105 | |

| 106 | |

| 106 | |

| 106 | |

| 107 | |

| 107 | |

| 107 | |

| 111 | |

| 115 | |

| 124 | |

| 126 | |

| 126 | |

| 127 |

i

| 127 | |

| 129 | |

| 129 | |

| 129 | |

| 130 | |

| 130 | |

| 130 | |

| 142 | |

| 142 | |

| 142 | |

| 143 | |

| 145 | |

| 145 | |

| 145 | |

| 145 | |

| 146 | |

| 146 | |

| 148 |

In this preliminary prospectus/information statement, “Gafisa,” “we,” “us” and “our” refer to Gafisa S.A. References to the “Companies” refer to Gafisa and Tenda.

The following are some questions that you may have regarding the Restructuring and brief answers to those questions. Gafisa urges you to read carefully the remainder of this document because the information in this section does not provide all the information that might be important to you with respect to the Restructuring. Additional important information is also contained in the documents incorporated by reference into this preliminary prospectus/information statement. See “Part Seven: Additional Information for Shareholders—Incorporation by Reference.”

| Q: | What is the Restructuring? |

| A: | Gafisa S.A., which we refer to in this preliminary prospectus/information statement as “Gafisa” or “we,” has proposed the Restructuring aiming at consolidating at the Gafisa level all of the noncontrolling share ownership in its subsidiary, Construtora Tenda S.A., or Tenda. The Restructuring will be accomplished via a merger of shares (called Incorporaçăo de Ações, under Brazilian law): a Brazilian business combination transaction where, subject to the approvals of the Gafisa shareholders and the Tenda shareholders, all of the Tenda shares not owned by Gafisa will be exchanged for Gafisa shares and Tenda will become a wholly-owned subsidiary of Gafisa. |

| Q: | What are the reasons for the Restructuring? |

| A: | Gafisa and Tenda believe the Restructuring: will be advantageous to the shareholders of both Companies, to the extent the Restructuring is likely to result in the creation of a national leader in the civil construction sector that is likely to derive benefits arising from scale and an increase in operational, commercial and administrative efficiencies, and permit the reduction of redundant costs and operational scale gains, allowing for larger investments to be made and a higher sustainable growth rate. For further details on the reasons for the Restructuring see “Part Two: Summary—Purposes of and Reasons for the Restructuring” and “Part Five: The Restructuring—Reasons for the Restructuring.” |

| Q: | What will happen to my shares in the Restructuring? |

| A: | If the Restructuring is approved and you are a direct holder of common shares of Tenda, you will receive 0.205 common share, no par value, of Gafisa for each common share of Tenda that you hold, respectively, plus, in each case, the cash value of any fractional shares. |

If you hold common shares of Tenda, no further action by you is required except that if you are not a resident of Brazil, you will be required to comply with the registration requirements of Instruction No. 325 of the Brazilian Securities Commission (Comissão de Valores Mobiliários), or CVM, and Resolution No. 2,689 of the Brazilian Monetary Council (Conselho Monetário Nacional), or CMN, or Law No. 4,131, as the case may be, as described below under “Part Two: Summary—Terms and Effects of the Restructuring.” To evidence your ownership of new shares of Gafisa, an entry or entries will be made in the share registry of Gafisa to evidence the common shares of Gafisa you will receive in the Restructuring. At that time, you will also receive cash in lieu of any fractional Gafisa shares to which you would have been entitled as a result of the Restructuring. See “When will I receive any cash attributable to any fractional Gafisa share?” below.

If you are a holder of Gafisa common shares or Gafisa ADSs, you will continue to hold these securities after the Restructuring.

| Q: | What shareholder approvals are needed? |

| A: | The Restructuring will require the affirmative vote of holders representing at least 50% of Tenda’s voting capital. Tenda’s extraordinarily general shareholders’ meeting, or EGM, is currently scheduled for December 14, 2009. |

The Restructuring is also subject to approval by the majority of Gafisa’s shareholders at an EGM also scheduled for December 14, 2009, which shall only occur if shareholders representing at least two thirds of Gafisa’s voting capital are in attendance. Pursuant to Brazilian law, if the attendance quorum is not reached on first call, the EGM of Gafisa may occur, on a second call, with any number of shareholders.

Gafisa and its affiliates hold, directly or indirectly, all of the voting power necessary to approve the Restructuring at the Tenda level without the support of any other holder of shares of Tenda.

| Q: | Do I have withdrawal rights? |

| A: | Persons who were holders of record of common shares of Tenda as of October 21, 2009, will be entitled to exercise withdrawal rights in connection with the Restructuring. |

If you have withdrawal rights, your withdrawal rights will lapse 30 days after publication of the minutes of Tenda’s EGM called to approve the Restructuring. If you have withdrawal rights you cannot exercise those withdrawal rights if you vote in favor of the Restructuring.

If Tenda’s shareholders exercise their withdrawal rights, they will receive from Tenda a cash amount for their shares, calculated in accordance with Brazilian law 6,404, dated December 15, 1976, or Brazilian corporate law, equal to the book value of their shares on the date of the last audited balance sheet approved by the shareholders of Tenda, i.e. December 31, 2008, unless they request Tenda to draw down a special and more recent balance sheet, as of no more than 60 days from the date of the EGM, in which case the requesting shareholder will receive its withdrawal rights based on such more recent balance sheet even if such value is lower than the value calculated as per Tenda’s December 31, 2008 balance sheet. On December 31, 2008, the book value of each share of Tenda amounted to R$2.65.

| Q: | Have the boards of directors or any committees of these boards taken any position relating to the Restructuring? |

| A: | The board of directors of each of the Companies has approved the merger agreement (Protocolo de Incorporação de Ações e Instrumento de Justificação, under Brazilian law) to which their Companies are parties and the calling of the EGMs required to obtain the requisite shareholder approvals. At the time the Restructuring was publicly announced, Tenda, adopting recently issued recommendations of the CVM, established, by one of the means recommended by the CVM, a special committee to negotiate the terms of the Restructuring with the management of Gafisa and to submit its recommendations to the board of directors of Tenda. The purpose of setting up the special committee was to protect the interests of noncontrolling shareholders of Tenda. This special committee, or the Special Committee, after having reviewed and negotiated the Gafisa proposals, having received advice from its own independent financial adviser and legal counsel and after having reached an agreement with the Gafisa management on the terms of the Restructuring, including the Exchange Ratio, unanimously recommended to the board of directors of Tenda the Exchange Ratio for the Restructuring set forth in this preliminary prospectus/information statement. On November 6, 2009, the board of directors of Tenda considered the recommendation of the Special Committee and other factors and approved the Restructuring. The Gafisa board of directors also approved the Restructuring on that day. For additional information regarding the factors and reasons considered by the board of directors of Gafisa and Tenda in approving the Restructuring, the manner in which these boards made their decision, including the decision of certain members of the boards to abstain from voting and the interest of certain directors and their affiliates in the Restructuring, see “Part Two: Summary—Background of the Restructuring” and “Part Five: The Restructuring—Background, the Special Committee and Board Positions—The Special Committee.” For additional information regarding the factors and reasons considered by the boards of directors of Gafisa and Tenda in approving the Restructuring, and the manner in which these boards made their decisions, including the decision of certain members of the boards to abstain from voting, see “Part Five: The Restructuring—Background, the Special Committee and Board Positions” and “Part Five: The Restructuring—Reasons for the Restructuring.” |

| Q: | Why am I receiving this document? |

| A: | This document is a preliminary prospectus/information statement of Gafisa relating to the merger of Tenda shares into Gafisa. If you hold common shares of Tenda you are receiving this preliminary prospectus/information statement because Gafisa may be deemed to be offering you securities for purposes of the U.S. Securities Act of 1933, as amended, or the Securities Act. If you hold common shares of either Gafisa or Tenda and you are a U.S. resident you are receiving this document to provide you with at least the same information relating to the shareholder meetings of the Companies as is being provided to other holders of the same class of securities in Brazil. If you are a holder of Gafisa ADSs, you are receiving this document to provide you with information about the Restructuring and the matters that will be considered at the EGM of Gafisa and with information regarding how you may exercise your voting rights in relation to these matters. |

| Q: | What will be the accounting treatment of the Restructuring? |

| A: | Under Brazilian GAAP, the accounting principles used to prepare Gafisa’s consolidated financial statements, the Restructuring is expected to be accounted for by the book value of the shares exchanged. |

Under U.S. GAAP, the merger of shares will be accounted for as equity transactions in accordance with Statement of Financial Accounting Standards (SFAS) No. 160, “Noncontrolling Interests in Consolidated Financial Statements, an Amendment of ARB No. 51” (U.S. GAAP codification: ASC 810 Consolidation), or SFAS 160. This standard requires that the carrying amount of a noncontrolling interest (formerly referred to as “a minority interest”) be adjusted to reflect the change in our ownership interest in the subsidiary. Any difference between fair value of the consideration received or paid and the amount by which the noncontrolling interests is adjusted shall be recognized in equity attributable to Gafisa.

| Q: | What are the U.S. federal income tax consequences of the Restructuring? |

| A: | In the opinion of Davis Polk & Wardwell LLP, the Restructuring should qualify as a tax-free “reorganization” for U.S. federal income tax purposes. In order for the Restructuring to qualify as a reorganization for such purposes, among other things, Tenda shareholders must receive, from Gafisa, solely Gafisa voting stock in exchange for their Tenda shares. There is no authority under the U.S. tax laws expressly addressing whether the payment of cash to Tenda shareholders who exercise withdrawal rights pursuant to Brazilian law will prevent the Restructuring from satisfying this “solely for voting stock” requirement. However, based on the advice of Gafisa’s Brazilian counsel to the effect that solely Tenda, and not Gafisa, will be liable to make any cash payment to any Tenda shareholders who exercise withdrawal rights, and assuming that any such payments are not funded indirectly by Gafisa, the payment of such cash to Tenda shareholders who exercise withdrawal rights should not prevent the Restructuring from qualifying as a reorganization for U.S. federal income tax purposes. No ruling has been sought or will be obtained from the U.S. Internal Revenue Service on the U.S. federal income tax consequences of the transaction. |

If the Restructuring qualifies as a reorganization for U.S. federal income tax purposes, you generally will not recognize gain or loss for U.S. federal income tax purposes on the receipt of Gafisa shares in exchange for Tenda shares, except to the extent of gain attributable to cash received in lieu of a fractional Gafisa share. If the Restructuring is a taxable transaction, you generally will recognize gain or loss on the receipt of Gafisa shares in exchange for Tenda shares. Please review carefully the section under “Part Five: The Restructuring—Material Tax Considerations—United States Federal Income Tax Considerations.” Because the tax consequences of the Restructuring are uncertain, and will depend in part on your particular facts and circumstances, you should consult your tax adviser regarding the appropriate characterization of the Restructuring and the specific tax consequences to you.

| Q: | When will the Restructuring be completed? |

| A: | The EGM of Tenda will be held on December 14, 2009 at 9:00 a.m. (São Paulo time) and the EGM of Gafisa will be held on December 14, 2009 at 2:00 p.m. (São Paulo time). If either EGM is not convened |

| due to a lack of quorum, because the SEC shall not have declared effective the registration statement of which this preliminary prospectus/information statement is a part before that date or for any other reason, the EGMs will be convened on a later date and a call notice will be released at least eight days in advance of the rescheduled date of such EGM. Any changes to the abovementioned dates shall be disclosed in Brazil in accordance with Brazilian corporate law and by the issuance of a press release and the filing of an amendment to this prospectus/information statement with the SEC. The merger of shares will be legally effective upon approval of the Restructuring at the EGMs. However, new common shares will not be delivered to you in the Restructuring until a few days after the end of the period for the exercise of withdrawal rights, which period will end 30 days after publication of the minutes of Tenda’s EGM called to approve the Restructuring. See “Could the Restructuring be unwound?” below. |

| Q: | Can I sell my old shares during the 30-day period following publication of the minutes of the EGMs? |

| A: | There will continue to be negotiation under the ticker TEND3 on the BM&FBOVESPA, during the 30-day period. The shares of Gafisa will continue to be listed on the BM&FBOVESPA and the Gafisa ADSs will continue to be listed on the NYSE during and after that period until such time, if any, as Gafisa might decide to alter the listing of the Gafisa shares or ADSs. Gafisa does not currently have any plans of this nature. |

| Q: | Could the Restructuring be unwound? |

| A: | Under Brazilian law, if management believes that the total value of the withdrawal rights exercised by the shareholders of Tenda may place at risk the financial stability of the companies, management may, within 10 days after the end of the withdrawal rights period, call an EGM to either unwind or ratify the Restructuring. Payment relating to the exercise of the withdrawal rights will not be due if the Restructuring is unwound. See “When will I receive my Gafisa Common Shares?” below. |

| Q: | Are any other approvals necessary for the completion of the Restructuring? |

| A: | Yes. The EGMs of Tenda and Gafisa will not take place until after the SEC declares effective the registration statement of which this preliminary prospectus/information statement is a part. Completion of the Restructuring then is subject to (1) the occurrence of the Tenda EGM (which under Brazilian law must occur before the Gafisa EGM) and the approval of the Restructuring by the holders of at least 50% of Tenda’s common shares, (2) the occurrence of the Gafisa EGM (whether as currently scheduled or in a second call, due to minimum attendance requirements under Brazilian law) and the approval of the matters presented to the meeting by the holders of a majority of the Gafisa shares present or represented at the meeting. In addition, Tenda will seek approval of its debenture holders for the Restructuring and delisting from BM&FBOVESPA’s Novo Mercado. Acceleration of the debentures may result if either debenture holders decide without justification not to approve the Restructuring or if the debenture holders do not approve the delisting of Tenda from BM&FBOVESPA’s Novo Mercado. See “Part Four: Information on Gafisa and Tenda—Management’s Discussion and Analysis of Financial Condition and Results of Operations of Tenda—Indebtedness—Debenture Program.” |

| Q: | How will my rights as a shareholder change after the Restructuring? |

| A: | If you are a shareholder of Tenda, your rights as a shareholder of Gafisa will be substantially similar to your rights as a shareholder of Tenda. In exchange for your shares, you will be receiving exclusively Gafisa shares of the same class as your original shares plus any cash payable in respect of fractional shares as described below. The Gafisa common shares that you receive will be listed on BM&FBOVESPA as were your original Tenda shares, and on the New York Stock Exchange, or the NYSE, if later you decide to convert your Gafisa shares into Gafisa ADSs. See “Gafisa expects your new Gafisa securities to enjoy greater market liquidity when compared to your original securities” below. |

| Q: | When will I receive my Gafisa common shares? |

| A: | Assuming the Restructuring is completed, we will deliver common shares in connection with the Restructuring a couple of days after the end of the period for the exercise of withdrawal rights, which period will end 30 days after the publication of the minutes of Tenda’s EGM called to approve the Restructuring. During that period, the common shares of Gafisa and Tenda are expected to continue to trade on the BM&FBOVESPA under their existing ticker symbols and the Gafisa ADSs are expected to continue to trade on the NYSE, under their existing symbol. |

| Q: | Can I opt to receive Gafisa ADSs instead of Gafisa shares? |

A: | No. However, Citibank N.A., the depositary of Gafisa ADSs or the Gafisa Depositary, may create ADSs on your behalf if you or your broker deposit Gafisa shares with the custodian of Gafisa shares in Brazil, Itaú Unibanco S.A., or the Gafisa Custodian. The Gafisa Depositary will issue ADSs (in whole numbers only) and deliver such ADSs to the person indicated by you only after you pay any applicable issuance fees and any charges and taxes payable for the transfer of Gafisa shares to the Gafisa Custodian. Your ability to deposit Gafisa shares and receive Gafisa ADSs may be limited by U.S. and Brazilian legal considerations applicable at the time of deposit. Additional information on Gafisa ADSs, including exchange rights and conversion fees, are included in Gafisa’s Depositary Agreement, which is incorporated by reference herein. See “Part Five: The Restructuring—Conversion of Gafisa Common Shares into Gafisa ADSs.” |

| Q: | When will I receive any cash attributable to any fractional Gafisa share? |

| A: | If you hold shares of Tenda and the application of the Exchange Ratio in the “Restructuring would entitle you to receive a fractional Gafisa share, Gafisa will sell, in an auction on the BM&FBOVESPA, the aggregate of all fractional Gafisa shares. You will receive cash in lieu of any fractional Gafisa share to which you would have been entitled as a result of the Restructuring based on the net proceeds (after deducting applicable fees and expenses), from any sale on the BM&FBOVESPA of the aggregate number of fractional entitlements to Gafisa shares within thirty business days after the receipt of proceeds from the sale of all such fractional interests by Gafisa on the BM&FBOVESPA. The sale of such fractional interests in auctions on the BM&FBOVESPA will occur as soon as practicable after the completion of the Restructuring. |

| Q: | Will I have to pay brokerage commissions? |

| A: | You will not have to pay brokerage commissions as a result of the exchange of your Tenda shares for Gafisa shares in the Restructuring if your Tenda shares are registered in your name. If your securities are held through a bank or broker or a custodian linked to a stock exchange, you should consult with them as to whether or not they charge any transaction fee or service charges in connection with the Restructuring. Also, if you are not a Brazilian resident, you may be required to pay other costs in connection with complying with the Brazilian legal requirements described under “Part Five: The Restructuring—Brokerage Commission.” |

| Q: | What do I need to do now? |

| A: | If you hold common shares of Tenda, no further action by you is required except that if you are not a resident of Brazil, you will be required to comply with the registration requirements of Instruction No. 325 of the CVM and Resolution No. 2,689 of the CMN, or Law No. 4,131, as the case may be, as described below under “Part Two: Summary—General Terms and Effects of the Restructuring” in order to receive Gafisa shares upon the consummation of the Restructuring. The Gafisa common shares are book-entry shares, and an entry or entries will be made in the share registry of Gafisa to evidence the common shares you will receive. See “Part Five: The Restructuring—Receipt of Shares of Gafisa” for more details. |

| Q: | When and where will the shareholders’ meetings take place? |

| A: | The EGM of Tenda is currently scheduled to take place at 9:00 a.m. (São Paulo time) on December 14, 2009 on the 10th floor of Tenda’s headquarters located at Avenida Engenheiro Luis Carlos Berrini, No. 1,376, 04571−000 − São Paulo, SP − Brazil. The EGM of Gafisa at which the Restructuring and certain related issues will be considered is currently scheduled to take place at 2:00 pm (São Paulo time) on December 14, 2009 on the 19th floor of Gafisa’s headquarters located at Avenida das Nações Unidas, No. 8,501, 05425−070 − São Paulo, SP − Brazil. However, these EGMs will not occur until after the SEC declares effective the registration statement of which this preliminary prospectus/information statements is a part. The CVM may suspend for up to 15 days the time period between the date of the call notice and the date of the EGM scheduled to approve the Restructuring. See “Part Three: Risk Factors—Risks Relating to the Restructuring—The CVM, the Brazilian securities regulator, may suspend for up to 15 days the shareholders’ meetings scheduled to approve the Restructuring.” |

| Q: | What do I need to do if I would like to vote my shares? |

| A: | Gafisa. If you hold common shares of Gafisa, you may attend the Gafisa EGM at which the Restructuring will be considered, and you may vote. Under Brazilian law, to vote shares at an EGM you must either appear at the meeting in person and vote your shares or grant an appropriate power of attorney to another shareholder, an executive officer of the applicable company or an attorney who will appear at the meeting and vote your shares. The power of attorney must have been granted, at most, one year prior to the shareholders’ meeting and must be certified by a notary public and legalized by the Brazilian consulate located in the domicile of the grantor. A corporation may be represented at the shareholders’ meeting by its officers. The powers of attorney granted by the shareholders of Gafisa for representation at the meeting should be deposited at the head office of Gafisa, located at Av. Nações Unidas No. 8,501, 19th floor, 05425−070 − São Paulo, SP − Brazil, at least 48 hours prior to the occurrence of the EGM. If you hold Gafisa ADSs, you are not entitled to attend the Gafisa EGM but will receive instructions from the Gafisa Depositary about how to instruct the Gafisa Depositary to vote the Gafisa common shares represented by your Gafisa ADSs. |

Tenda. If you hold common shares, you may attend the Tenda EGM at which the Restructuring will be considered, and you may vote. Under Brazilian law, to vote shares at an EGM you must either appear at the meeting in person and vote your shares or grant an appropriate power of attorney to another shareholder, an executive officer of the applicable company or an attorney who will appear at the meeting and vote your shares. The power of attorney must have been granted, at most, one year prior to the shareholders’ meeting and must be certified by a notary public and legalized by the Brazilian consulate located in the domicile of the grantor. A corporation may be represented at the shareholders’ meeting by its officers. The powers of attorney granted by the shareholders of Tenda for representation at the meeting should be deposited at the head offices of Tenda, located at Av. Engenheiro Luiz Carlos Berrini No. 1,376, 10th floor, 04571−000 − São Paulo, SP − Brazil, at least 48 hours prior to the occurrence of the EGM.

If you are a direct holder of shares that are entitled to vote at the EGMs relating to the Restructuring, you may either attend the relevant EGM personally or complete a power of attorney that complies with Brazilian law. While the form of power of attorney attached as an exhibit to the registration statement of which this preliminary prospectus/information statement is a part provides an example of a power of attorney, shareholders should confirm, with Brazilian counsel if necessary, that any power of attorney or revocation thereof satisfies the requirements of Brazilian law, as Gafisa and Tenda will not accept such forms if they do not comply with Brazilian law. Gafisa and Tenda encourage you to consult with Brazilian counsel if you wish to complete a power of attorney. Shareholders wishing to attend an EGM and who hold shares through the fungible custody of registered shares of the stock exchange must provide a statement containing their corresponding equity interest in the applicable company dated within 48 hours of the applicable EGM. The EGMs of Gafisa and Tenda are currently scheduled to be held as follows:

Gafisa S.A., December 14, 2009 2:00 p.m. (São Paulo time)

Av. Nações Unidas No. 8,501, 19th floor, 05425−070 − São Paulo, SP − Brazil

Construtora Tenda S.A., December 14, 2009 9:00 a.m. (São Paulo time)

Av. Engenheiro Luiz Carlos Berrini No. 1,376, 10th floor, 04571−000 − São Paulo, SP − Brazil

| Q: | Who can help answer my questions? |

| A: | If you have any questions about the Restructuring, you can contact: |

Gafisa S.A.

Attention: IR Department

Av. Nações Unidas No. 8,501, 19th floor

05425−070 − São Paulo, SP − Brazil

Telephone: + 55 (11) 3025−9000

e-mail: ri@gafisa.com.br

Construtora Tenda S.A.

Attention: IR Department

Av. Engenheiro Luiz Carlos Berrini No. 1,376, 9th floor

04571−000 − São Paulo, SP − Brazil

Telephone: + 55 (11) 3040−6426

e-mail: ri@tenda.com

| You may also contact the information agent for the Restructuring: |

D.F. King & Co., Inc.

48 Wall Street, 22nd floor

New York, N.Y. 10005 - USA

Toll Free: (800)207-3158

Collect – (212)269-5550

e-mail:proxy@dfking.com

| In addition, if you are a holder of Gafisa ADSs, you may also contact: |

Citibank, N.A.

Attention: Depositary Receipts Department

388 Greenwich Street

New York, N.Y. 10013 − USA

Calls within the United States: (800) 308−7887

Calls outside the United States: (781) 575−4555

The following summary highlights selected information from this preliminary prospectus/information statement and may not contain all the information that may be important to you. To understand the Restructuring more fully, you should read carefully this entire preliminary prospectus/information statement.

We use throughout this preliminary prospectus/information statement, specially under “—The Companies” and “Part Four: Information on Gafisa and Tenda,” the term “value of launches” as measure of the Companies performances. Value of launches is not a Brazilian GAAP measurement. Value of sales as used in this preliminary prospectus/registration statement is calculated by multiplying the total numbers of units in a real estate development by the unit sales price.

Overview of Gafisa

Gafisa is incorporated under the laws of the Federative Republic of Brazil under the name Gafisa S.A., known as Gafisa. Gafisa has the legal status of a sociedade por ações, or a stock corporation, operating under Brazilian law. Gafisa’s principal executive offices are located at Av. Nações Unidas No. 8,501, 19th floor, 05425−070 − São Paulo, SP − Brazil. Gafisa’s telephone number is +55 (11) 3025−9000, its facsimile number is +55(11) 3025−9348, and its website is www.gafisa.com.br. Gafisa’s agent for service of process in the United States is National Corporate Research, Ltd. located at 10 East 40th Street, 9th floor, New York, NY 10016.

We are one of Brazil’s leading homebuilders. Over the last 50 years, we have been recognized as one of the foremost high-quality homebuilders, having completed and sold more than 970 developments and constructed over 11 million square meters of housing under the Gafisa brand, which we believe is more than any other residential development company in Brazil. We believe our brands “Gafisa,” “Alphaville,” and “Tenda” are well-known brands in the Brazilian real estate development market, enjoying a reputation among potential homebuyers, brokers, lenders, landowners and competitors for quality, consistency and professionalism.

Our core business is the development of high-quality residential units in attractive locations. For the year ended December 31, 2008, approximately 50% of the value of our launches was derived from high and mid high-level residential developments under the Gafisa brand. We are also engaged in the development of land subdivisions, also known as residential communities, representing approximately 15% of the value of our launches, and affordable entry-level housing, which represents approximately 8% of the value of our total launches. Other mid-level and commercial buildings represent approximately 27% of the value of our total launches. In addition, we provide construction services to third parties.

We are one of Brazil’s most geographically-diversified homebuilders currently operating in 94 cities, including São Paulo, Rio de Janeiro, Salvador, Fortaleza, Natal, Curitiba, Belo Horizonte, Manaus, Porto Alegre and Belém, across 18 states. Many of these developments are located in markets where few large competitors currently operate. For the year ended December 31, 2008, approximately 38% of the value of our launches were derived from our operations outside the states of São Paulo and Rio de Janeiro.

Overview of Tenda

Tenda is incorporated under the laws of the Federative Republic of Brazil under the name Construtora Tenda S.A., known as Tenda. Tenda has the legal status of a sociedade por ações, or a stock corporation, operating under Brazilian law. Tenda’s principal executive offices are located at Av. Engenheiro Luiz Carlos Berrini No. 1,376, 9th floor, 05425−070 − São Paulo, SP − Brazil. Tenda’s telephone number is +55 (11) 3040−6426, its facsimile number is +55 (11) 3040−6035, and its website is www.tenda.com.

Tenda is one of Brazil’s leading homebuilders focused in the development of affordable/entry-level residential buildings. Over the last 40 years, Tenda has been recognized as one of the foremost professionally-managed homebuilders in the affordable entry-level segment in Brazil, having completed and sold more than 230 developments and built and delivered more than 16,000 units.

On October 21, 2008, Tenda shareholders approved the merger into the company of FIT Residential Empreendimentos Imobiliários Ltda., or FIT, a company then controlled by Gafisa. As a result of the merger of FIT into Tenda, Gafisa became the controlling shareholder of Tenda. After the merger, the operations of Tenda further expanded into other markets in Brazil and, consequently, Tenda became one of the most diversified affordable/entry-level homebuilders in the country.

Tenda is currently present in 64 cities across 13 states in Brazil. Further, Tenda employs an in-house sales force, operating out of centralized retail centers in high traffic areas of the largest metropolitan regions with large housing deficits. Specifically, Tenda operates in cities and respective outskirts of high demographic density, including the cities and respective outskirts of São Paulo, Rio de Janeiro, Belo Horizonte, Salvador, Porto Alegre, Vitoria and Brasilia. According to IBGE, these seven Brazilian cities together account for approximately 110 million people and approximately 75% of the Brazilian GDP.

Tenda’s core business is the development of affordable/entry-level residential units in attractive locations targeted at lower-income population, which currently represents more than 90% of all families in Brazil. For the year ended December 31, 2008, approximately 88% of the value of Tenda sales were derived from affordable/entry-level residential developments.

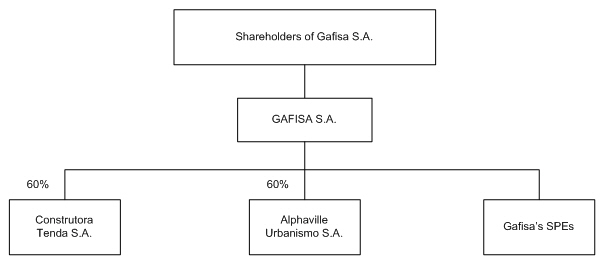

Current Corporate Structure of Gafisa

The following chart shows Gafisa’s corporate structure as of September 30, 2009:

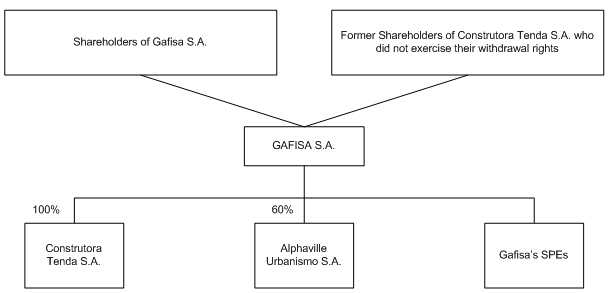

Post-Restructuring Corporate Structure

The following chart shows Gafisa’s expected corporate structure after the Restructuring:

Additional information about Gafisa and Tenda is included in our 2008 Annual Report on Form 20-F, which is incorporated by reference herein, except for the U.S. GAAP information included in items 3A, 8A and 18, which has been adjusted to reflect the retrospective adoption of the disclosures required by SFAS No. 160 and is incorporated by reference from our Form 6-K filed with the SEC on November 13, 2009.

Upon shareholder approvals on October 21, 2008, FIT Residential Empreendimentos Imobiliários Ltda., or FIT, a company previously controlled by Gafisa was merged into Tenda. As a result of the level of Gafisa’s pre-transaction ownership in FIT and the exchange ratio in the merger, Gafisa became the controlling shareholder of Tenda.

On September 10, 2009, Gafisa hired Estáter to study strategic options for its equity stake in Tenda. Based in part on Estáter’s advice, Gafisa concluded on October 16, 2009, that the Restructuring was the preferable option to be pursued. Representatives of Gafisa did not discuss the concept of the Restructuring with or disclose any proposed terms for the Restructuring to representatives of Tenda until after the closing of the market on October 21, 2009, at which time Gafisa’s officers, including Gafisa’s Chief Executive Officer and Investor Relations Officer, informed two of Tenda’s board members, Messrs. Mauricio Luchetti and Henrique Alves Pinto, of the proposed transaction. On October 22, 2009, Tenda’s Investors Relations Officer therefore decided to issue the first Tenda announcement in compliance with CVM’s regulations.

On October 22, 2009, the Companies announced their intention to consummate the Restructuring and stated that they would retain the services of specialized appraisal companies required under Brazilian corporate law to prepare the necessary reports and that they had retained and would retain other appropriate financial advisory services to assist in the determination of the Exchange Ratio and other terms of the Restructuring, as recommended by the CVM. In these public announcements of the Restructuring, the Companies also indicated that they would voluntarily comply with a recently issued CVM Release No. 35 (Parecer de Orientação No. 35), or CVM Release No. 35, making certain recommendations with respect to the negotiation and conduct of transactions between affiliated companies in order to enhance minority shareholder protection. Among other recommendations, CVM Release No. 35 suggests the establishment of special committees in connection with these transactions.

The Companies announced that Tenda would form a special committee to act in connection with the Restructuring and, specifically, to negotiate with Gafisa’s management and issue to the board of directors of Tenda its recommendation regarding an appropriate exchange ratio for the Restructuring. On October 22, 2009, the board of directors of Tenda appointed Messrs. Henrique de Freitas Alves Pinto, Mauricio Luis Luchetti and Eduardo B. Gentil to form a special committee, to negotiate, with the management of Gafisa, the terms and conditions of the Restructuring and to submit its recommendations relating to the Restructuring to the board of directors of Tenda. The Special Committee was formed, in accordance with one of CVM’s recommended methods for selecting the members of a special committee. A majority of the board of directors of Tenda chose two members, Mr. Maurício

Luis Luchetti and Mr. Henrique de Freitas Alves Pinto, both “independent members,” as such term is defined by the rules and regulations of the BM&FBOVESPA. Ms Henrique is a minority shareholder of Tenda and was appointed to the board of directors of Tenda by the noncontrolling shareholders thereof. Messrs. Henrique de Freitas Alves Pinto and Mauricio Luis Luchetti then selected Mr. Eduardo B. Gentil as the third member of the Special Committee. Mr. Gentil is not a member of the board of directors of either Gafisa or Tenda or an employee of either of the Companies and he is not otherwise affiliated with the Companies. By following a CVM recommended procedure and appointing these persons as the members of the Special Committee, Tenda assured that there would exist an independent group to negotiate with Gafisa regarding the terms of the Restructuring.

The Special Committee retained an independent financial advisor as well as an independent legal advisor in connection with the Restructuring and held meetings with such advisors as well as with representatives and advisors of Gafisa. With the assistance of its financial advisor, the Special Committee, after having negotiated with representatives of Gafisa, recommended an exchange ratio of 0.205 common share of Gafisa for each common share of Tenda for the Restructuring. On November 6, 2009 the Special Committee issued a written recommendation to the board of directors of Tenda recommending that the board adopt the Exchange Ratio set forth in this preliminary prospectus/information statement in connection with the Restructuring. On November 6, 2009, the boards of directors of Gafisa and Tenda voted to approve the terms and conditions of the merger agreement (Protocolo de Incorporação de Ações e Instrumento de Justificação, under Brazilian law), or the Merger Agreement, and scheduled EGMs of Gafisa and Tenda shareholders, respectively, in order to obtain the shareholder approvals required in connection with the Restructuring. Mr. Thomas McDonald recused himself from voting as a member of both the Tenda and the Gafisa board of directors. Mr. Gary Garrabrant recused himself from voting. Messrs. Wilson Amaral de Oliveira, Alceu Duilio Calciolari, Rodrigo Osmo and Fernando Cesar Calamita, recused themselves from voting with as members of Tenda board of directors. For additional information regarding the Restructuring, the Special Committee and the background of the Restructuring, see “Part Five: The Restructuring—Background, the Special Committee and Board Positions.” For additional information regarding the share ownership of Messrs. Thomas McDonald and Gary Garrabrant in both Tenda and Gafisa and regarding their other relationship with Tenda and Gafisa, see “Part Five: The Restructuring—Management of Gafisa” and “—Management of Tenda.”

The principal factors or reasons that caused the Gafisa management and the Tenda management to approve and recommend the Restructuring to their respective boards of directors are the following:

| · | Gafisa and Tenda believe the Restructuring is likely to result in the creation of a Brazilian national leader in the civil construction sector; and |

| · | Gafisa and Tenda believe the Restructuring is likely to (1) permit Gafisa and Tenda to derive economic benefits as a result of the larger scale of their combined operations, (2) to increase operational, commercial and administrative efficiencies and (3) to permit the reduction of redundant costs, and thereby allowing for the possibility of larger future investments by Gafisa in its own business and the possibility of a higher sustainable growth rate. |

| o | Gafisa and Tenda management believe that in the Brazilian real estate sector it is important to have scale. A typical project, from launch to delivery, usually takes 36 months and 20 months to complete for Gafisa and Tenda, respectively, and payments received prior to delivery, only represent up to 30% of the unit cost (the remaining 70% is usually financed by a third party bank or financial institution). Therefore, the cash needs of the companies are high — a characteristic of the business that has only been exacerbated by Gafisa’s increasing sales volume (which grew from R$995 million in 2006 to R$2,194 million in the first nine months of 2009). By managing both companies together, Gafisa management expects to be able to manage its cash needs more effectively by utilizing the strenght of the combined balance sheet of Gafisa and Tenda and by being able to allocate capital more freely between the two companies. Management also expects to realize cost savings as a result of the Restructuring because it should be possible to eliminate duplicative activities at the two companies and avoid the costs related to maintaining Tenda as a publicly listed company. |

| o | The management of Gafisa and Tenda also believe that the affordable entry level housing market in which Tenda is focused has the potential for high-growth and that the mid and mid/high housing sectors in which Gafisa operates are also performing very well at the present time; however, at times, either of these markets may outperform the other. Gafisa and Tenda management believe that having a diversified platform is the best way to mitigate risk. As a result of the Restructuring, Tenda’s shareholders will no longer be exposed to only one segment of the Brazilian real estate market, but to the various sectors of the housing market in Brazil, and Tenda and Gafisa management believe that this diversification will be valuable to both Tenda and Gafisa shareholders. Tenda and Gafisa management believe that the ability to switch investments according to demand across all sectors of the housing market in Brazil, will likely produce a higher sustainable growth rate for Gafisa. Prior to the Restructuring, Gafisa’s 60% ownership of Tenda was not sufficient as to allow Gafisa to easily switch investments between the companies. |

When they approved the Restructuring, members of the boards of directors of Gafisa and Tenda considered the following factors:

| · | the views of the management of Gafisa and Tenda, described above, to the effect that (1) the Restructuring is likely to result in the creation of a Brazilian national leader in the civil construction sector and (2) the Restructuring is likely to result in economic benefits as a result of the increased scale of the business, operational and administrative efficiencies, and the ability to easily swich investments according to demand across all sectors of the housing market in Brazil. In considering these views, the Board considered the likelihood that management’s predictions would be realized and risks that these predictions might fail to be realized as a result of, among other matters, changes in macro-economic conditions in and changes in the competitive environment in which Gafisa and Tenda operate. Each board concluded that, in its opinion, the views presented by management were, as of the date of the board meetings, based on reasonable assumptions and that achievement of management’s objectives would be beneficial to all of the Gafisa shareholders, including those receiving Gafisa shares as a result of the Restructuring. |

| · | that the final terms of the Restructuring approved by the boards were consistent with the recommendations made by the Special Committee to the Tenda board of directors. |

| · | that the Restructuring will allow holders of common shares of Tenda to exchange their securities at an equitable exchange ratio, as recommended by the Special Committee and as determined by independent financial advisors. |

| · | that the Restructuring will allow holders of common shares of Tenda to receive Gafisa common shares having substantially the same rights as their common shares of Tenda but that instead are expected to enjoy greater liquidity than the securities previously held by them. In reaching this conclusion, the boards received advice from their respective Brazilian legal advisors to the effect that, under Brazilian law and the respective bylaws of Gafisa and Tenda, the common shares of each company had substantially the same voting rights, dividend rights and other material shareholder rights. The boards recognized that the nature of the businesses represented by each of the respective classes of stock differed in certain respects, with the Tenda business being focused on affordable entry-level residential buildings and the Gafisa business being focused on high quality homes and that certain shareholders might prefer one over the other; however, the boards also noted that other shareholders might well prefer diversification and that both management and the boards view diversification as an appropriate means to mitigate risk. More importantly, the boards noted that, because the Gafisa shares are traded both on BM&FBOVESPA and, on the NYSE, in the form of ADSs, there is a larger trading market for the Gafisa shares than exists for the Tenda shares. For example, in October 2009, Gafisa’s average daily trading volume (ADTV) was equivalent to R$ 60 million on the BM&FBOVESPA and approximately R$ 76.7 million on the NYSE, resulting in a consolidated ADTV of close to R$137 million. In the same period, Tenda’s ADTV was R$14.4 million, or 11% of Gafisa’s ADTV. After the Restructuring, the potential combined liquidity would be approximately R$ 150 million and this fact might facilitate sales by shareholders no longer interested in maintaining their investment in the business at prices deemed acceptable by those shareholders. |

| · | that the Restructuring will allow Tenda shareholders who do not want to become shareholders in Gafisa a right to exercise withdrawal rights, but the Restructuring will offer those Tenda shareholders who do not |

exercise withdrawal rights an Exchange Ratio with an equivalent market price for the Tenda shares that is likely to be higher than the value of the withdrawal rights offered to dissenting Tenda shareholders. The value of the withdrawal rights is based on Tenda's equity value (book value) per share on December 31, 2008. Based on Tenda’s book value as of December 31, 2008 of R$1,062,213,828.91 and the 400,804,117 outstanding shares, a holder of a single Tenda share would receive R$2.65, if such holder were to exercise his withdrawal rights. On the other hand, the Exchange Ratio of 0.205 and the market price of Gafisa's shares as of December 8, 2009 (R$28.84 per share) imply an equivalent market price of R$5.91 to be received by a holder of a single Tenda share who does not exercise his withdrawal rights. Although the actual value of Gafisa shares (and therefore the equivalent value to be received by Tenda shareholders based on the Exchange Ratio) will fluctuate between the date of this Registration Statement and the date that Tenda shareholders will receive Gafisa shares following the Restructuring, the value of withdrawal rights will be greater than the value of the Gafisa shares received based on the Exchange Ratio only if the market price of Gafisa shares falls below R$12.93 per share (a decline of more than 55% from the market price on December 8, 2009.

Under Brazilian corporate law, Tenda shareholders dissenting from the Restructuring may request that withdrawal rights be calculated based on a balance sheet prepared within no more than 60 days as of the date of the Tenda EGM. Even applying the most recent public information available (i.e. the interim balance sheet dated September 30, 2009), Tenda’s shareholders exercising withdrawal rights would only receive approximately R$2.80 per Tenda share, which would still be less than the value likely to be received based on the Exchange Ratio. The book value of Tenda shares is unlikely to have varied sufficiently since September 30, 2008 so as to provide Tenda shareholders who choose to exercise withdrawal rights with a greater value than that which they would receive if they participate in the Restructuring. For more information on how the withdrawal value is calculated, see “Part Five—The Restructuring—Withdrawal Rights.”

Gafisa and Tenda do not generally publish their business plans and strategies or make external disclosures of their anticipated financial position or results of operations. However, the management of each of Tenda and Gafisa has provided historical financial information set forth in valuation reports and financial analyses issued for the benefit of the Special Committee by Banco Itaú BBA S.A., Estáter Assessoria Financeira Ltda., N.M. Rothschild & Sons (Brasil) Ltda. and APSIS Consultoria Empresarial Ltda., as described below. The assumptions and estimates underlying the prospective financial information are inherently uncertain and, though considered reasonable by the management of the Companies as of the date of its preparation, are subject to a wide variety of significant business, economic, and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information, including, among other things, risks and uncertainties. See “Part Three: Risk Factors.” Accordingly, there can be no assurance that the prospective results are indicative of the future performance of Gafisa and Tenda or that actual results will not differ materially from those presented in the prospective financial information. The accompanying prospective financial information was not prepared with a view toward public disclosure or with a view toward complying with the guidelines established by the American Institute of Certified Public Accountants with respect to prospective financial information. Inclusion of any prospective financial information in this registration statement should not be regarded as a representation by any person that the results contained in such prospective financial information will be achieved. None of Gafisa’s or Tenda’s independent public accountants, nor any other independent accountants, have compiled, examined, or performed any procedures with respect to the prospective financial information contained herein or therein, nor have they expressed any opinion or any other form of assurance on such information or its achievability, and assume no responsibility for, and disclaim any association with, the prospective financial information. The reports of those independent registered public accounting firms included in this prospectus relate to Gafisa’s and Tenda’s historical financial information. They do not extend to the prospective financial information and should not be read to do so.

Banco Itaú BBA S.A.

In connection with the Restructuring, the Special Committee received a valuation report from Banco Itaú BBA S.A., or Itaú BBA, expressing the view that, as of the date of that report and based on and subject to the considerations, limitations and assumptions of Itaú BBA’s analysis described in that report, as well as other matters Itaú BBA considered relevant, Itaú BBA determined for the exclusive benefit of the Special Committee, after carefully hearing and discussing the new assumptions and arguments presented by the Special Committee, that the indicative exchange ratio should be between 0.200 to 0.220 shares of Gafisa per share of Tenda, therefore increasing its initial analysis of an indicative exchange ratio between 0.196 and 0.210.

Estáter Assessoria Financeira Ltda.

In connection with the Restructuring, Gafisa received a presentation of financial analyses from Estáter Assessoria Financeira Ltda., or Estáter, expressing, as of the date of that presentation and based on and subject to the considerations and limitations of Estáter’s analysis described in that presentation and based on other matters as Estáter considered relevant, that if the exchange ratio recommended by Gafisa and approved by the boards of directors of Gafisa and Tenda with respect to the Restructurings was within the range of implied exchange ratios derived from the financial analyses performed by Estáter with respect to Gafisa and Tenda, applied on a consistent basis, then such exchange ratio, as of November 4, 2009, would constitute equitable treatment as understood in the manner described in such presentation. The boards of directors of Gafisa and Tenda and the Special Committee confirmed that the exchange ratio falls within the range derived from the financial analyses performed by Estáter.

N.M. Rothschild & Sons (Brasil) Ltda.

In connection with the Restructuring, Gafisa’s board of directors was advised by N.M. Rothschild & Sons (Brasil) Ltda., or Rothschild, which provided an additional analysis as to the appropriate range for the Exchange Ratio in the Restructuring and provided the Gafisa board of directors with its assessment of the Estáter financial analyses. Rothschild stated that it considered the Estáter financial analyses to be thorough, professionally prepared and based on reasonable assumptions. Rothschild then noted that while its valuation methodology differed in certain respects from that of Estáter, the range for the exchange ratio derived by Rothschild and the range derived by Estáter were substantially consistent. Rothschild also noted that the Estáter’s range fell within the Rothschild’s range. Rothschild thus reported to the board of directors of Gafisa and Tenda and to the Special Committee that any exchange ratio between 0.188 Gafisa shares per Tenda share to 0.259 Gafisa shares per Tenda share for the Restructuring would be equitable from the perspective of the noncontrolling shareholders.

APSIS Consultoria Empresarial Ltda.

In connection with the Restructuring, the board of directors of Gafisa received from APSIS Consultoria Empresarial Ltda., or APSIS, an appraisal report for purposes of Article 8 of Brazilian corporate law, which is the Brazilian law that requires an appraisal of the shares of Tenda used to determine the capital increase of Gafisa. APSIS concluded that, as of September 30, 2009, the book value of the common shares of Tenda for this purpose was R$2.80 per share.

In addition, the boards of directors of Gafisa and Tenda and the Special Committee received from APSIS an appraisal report for purposes of Article 264 of Brazilian corporate law which is the Brazilian law that requires an appraisal of the net worth of Gafisa and Tenda at market prices as of September 30, 2009 and disclosure of the outcome of that appraisal so that shareholders have a parameter against which to judge the Exchange Ratio. APSIS expressed the view that, as of the date of its reports and based on and subject to the assumptions and considerations described in those reports and based on other matters as APSIS considered relevant (1) the value of the net equity of Tenda as of September 30, 2009, calculated as if all of its assets and liabilities had been sold at fair market value was approximately R$3.04 per common share, (2) the value of the net equity of Gafisa as of September 30, 2009, calculated as if all of its assets and liabilities had been sold at fair market value was approximately R$16.32 per common share of Gafisa and (3) these net equity values of Tenda and Gafisa implied an exchange ratio of 0.186199 share of Gafisa per share of Tenda as compared to the Exchange Ratio of 0.205 share of Gafisa per common share of Tenda.

Uses of the Valuation Reports and Appraisals

Only the APSIS appraisals, prepared for purposes of sections 227, 8 and 264 of the Brazilian corporate law, were required pursuant to the Brazilian corporate law. One of the APSIS appraisals is intended, as required by Brazilian regulations, to confirm that the capital increase in Gafisa resulting from the Restructuring is supported by the net worth of Tenda. The other report, also required by statute is intended only to compare the proposed exchange ratio to another theoretical exchange ratio based on the market value of the assets and liabilities of both companies. Neither of those appraisals refers to the fairness of the exchange ratio nor were they required to have done so pursuant to Brazilian corporate law.

The Special Committee was selected in accordance with the recommendations of CVM Release No. 35 and therefore complies with such recommendations of CVM Release No. 35 so as to adequately fulfill the fiduciary duties of directors related to a transaction with an affiliate. While the CVM Release No. 35 acknowledges that there are other means to comply with the fiduciary duties of the directors in such cases, it indicates that the creation of a Special Committee in compliance with the recommendations of CVM Release No. 35 is an adequate way of having the applicable fiduciary duties fulfilled.

The reports presented by Rothschild and Estater were prepared at the request of Gafisa’s Board of Directors and the report presented by Itaú BBA was prepared at the request of Tenda’s Special Committee, to support their respective evaluation and negotiation of the terms and conditions of the transaction. Whereas such reports do not express any opinion with respect to the fairness of transaction, they confirm that the proposed exchange ratio is supported by the common methodologies of financial valuation standards as described in each of the reports.

The Board of Directors of Gafisa recommended the approval of the Restructuring based on the appraisal prepared by APSIS and on the reports presented by Rothschild and Estater, after having considered the recommendations of the Special Committee of Tenda, including, specifically, the Exchange Ratio, which Gafisa’s Board of Directors considered to be fair and adequately justified.

The Board of Directors of Tenda recommended the approval of the Restructuring to the shareholders of Tenda based on the appraisal prepared by APSIS and the recommendation of the Special Committee (which was advised by Itaú BBA).

We urge you to read carefully the summary of the reports set forth in “Part Five: The Restructuring—Valuation Reports of Itaú BBA,” “Part Five: The Restructuring—Financial Analyses of Estáter,” “Part Five: The Restructuring—Valuation Reports of Rothschild” and “Part Five: The Restructuring—Valuation Reports of APSIS,” which includes information on how to obtain copies of the full reports.

If the Restructuring is approved holders of common shares of Tenda will receive, without any further action, except if they are not residents of Brazil, 0.205 common share, no par value, of Gafisa for each Tenda common share they hold, plus, in each case, cash instead of any fractional shares.

Tenda shareholders residing outside of Brazil will receive their shares in accordance with their current investment regime. Hence, such shareholders will receive their shares, either (1) as a portfolio investment pursuant to the registration requirements of the Instruction No. 325 of the CVM, or Instruction No. 325, and Resolution No. 2,689 of the CMN, or Resolution No. 2,689; or (2) as a foreign direct investment in accordance with Law No. 4,131/62, depending on how they hold their shares of Tenda.

With certain limited exceptions, Resolution No. 2,689 investors are permitted to carry out any type of transaction in the Brazilian financial capital market involving securities traded on a Brazilian stock, futures or securities traded in organized over-the-counter markets. Investments and remittances outside of Brazil of gains, dividends, profits or other payments related to such securities are made through the foreign exchange market.

In order to become a Resolution No. 2,689 investor, an investor residing outside Brazil must:

| · | appoint a representative in Brazil with powers to take actions relating to the investment; |

| · | obtain a taxpayer identification number from the Brazilian tax authorities; |

| · | appoint an authorized custodian in Brazil for the investments, which must be a financial institution duly authorized by the Brazilian Central Bank and CVM; and |

| · | through its representative, register itself as a foreign investor with the CVM and the investment with the Brazilian Central Bank. |

Securities and other financial assets held by foreign investors pursuant to Resolution No. 2,689 must be registered or maintained in deposit accounts or under the custody of an entity duly licensed by the Central Bank or the CVM. In addition, securities trading by foreign investors is generally restricted to transactions involving securities listed on the Brazilian stock exchanges or traded in organized over-the-counter markets licensed by the CVM.

Foreign direct investors under Law No. 4,131 may sell their shares in both private and open market transactions, but these investors are currently subject to less favorable tax treatment on gains.

A foreign direct investor under Law No. 4,131 must:

| · | register as a foreign direct investor with the Central Bank; |

| · | obtain a taxpayer identification number from the Brazilian tax authorities; |

| · | appoint a tax representative in Brazil; and |

| · | appoint a representative in Brazil for service of process in respect of suits based on the Brazilian corporate law. |

As a result of the Restructuring:

| · | Gafisa will be a significantly larger company and will own 100% of the capital stock of Tenda. Gafisa’s interest in the net book value and net income (loss) of Tenda will therefore increase to 100%; |

| · | subject to satisfying applicable legal requirements, the Restructuring will provide holders of Tenda shares with an opportunity to own ADSs instead of shares by exchanging the Gafisa shares that they receive in the Restructuring for Gafisa ADSs in accordance with the terms of the Gafisa Deposit Agreement, a copy of which is included as exhibit 3.2 to the registration statement of which this preliminary prospectus/information statement is a part and which is incorporated by reference herein; |

| · | the holders of common shares of Tenda will receive common shares of Gafisa which will be listed on the BM&FBOVESPA, and any such Gafisa shares that are exchanged for Gafisa ADSs pursuant to the terms of the Gafisa Deposit Agreement will be listed on the NYSE; |

| · | the common shares of Tenda will be delisted from the “Novo Mercado” of BM&FBOVESPA, however Tenda will remain registered as a publicly-held company with the CVM, until further decision from Gafisa on the subject; |

| · | the common shares of Gafisa will continue to be listed on the BM&FBOVESPA and the Gafisa ADSs will continue to be listed on the NYSE and Gafisa will continue to file periodic reports with the SEC pursuant to the Securities Exchange Act of 1934, or the Exchange Act; and |

| · | the holders of common shares of Tenda that do not vote favorably to from the Restructuring will have, for a period of 30 days from the date of the publication of the minutes of Tenda’s EGM relating to the Restructuring, the right to withdraw from Tenda and be reimbursed for the value of the shares for which they are record holders on October 21, 2009. For more information on withdrawal rights, see “Part Five: The Restructuring—Withdrawal Rights.” |

Despite the benefits of and reasons for the Restructuring as well as the effects of the Restructuring all listed above, in considering the Restructuring, noncontrolling shareholders should consider the following factors:

| · | Gafisa will be considerably more leveraged than Tenda was previously. The Restructuring will not, however, cause Gafisa to absorb any properties, rights, assets, obligations or responsibilities of Tenda, which shall keep its legal identity in full without succession. See “Part Three: Risk Factors—Risks Relating to the Restructuring.” |

| · | Because Gafisa will be a larger company than Tenda, holders of Tenda shares will generally have a lower ownership percentage in Gafisa than they currently have in Tenda. Also, Gafisa shareholders’ ownership percentage in Gafisa will be diluted as a result of the issuance of the new Gafisa shares in the Restructuring. See “Part Three: Risk Factors—Risks Relating to the Restructuring.” |

| · | While the Exchange Ratio was determined in accordance with all applicable laws and regulations in Brazil and was recommended by the Special Committee, this ratio may be higher or lower, from the perspective of value to unaffiliated shareholders, than those that could be achieved through arm’s length negotiations between unrelated parties. See “Part Five: The Restructuring— Past Contacts, Transactions, Negotiations and Agreements” and “Part Five: The Restructuring—Transactions and Arrangements Concerning the Common Shares of Tenda.” |

| · | The Exchange Ratio reflects the fact that Gafisa already owns, directly or indirectly, a majority of the outstanding shares of Tenda and, accordingly, the Restructuring does not involve a change of control. As a result, the Exchange Ratio should not be expected to, and does not, reflect a control premium. |

| · | The Special Committee relied on the valuation reports of Itaú BBA and, together with its financial adviser, reviewed the financial analyses of Estáter and the appraisal report of APSIS. Furthermore, Estáter’s exchange ratio range fell within Rothschild’s exchange ratio range. APSIS’ fees will be paid entirely by the Companies, Itaú BBA’s fees will be paid entirely by Tenda and Estáter’s and Rothschild’s fees will be paid entirely by Gafisa. |

In the opinion of Davis Polk & Wardwell LLP, the Restructuring should qualify as a tax-free “reorganization” for U.S. federal income tax purposes. In order for the Restructuring to qualify as a reorganization for such purposes, among other things, Tenda shareholders must receive, from Gafisa, solely Gafisa voting stock in exchange for their Tenda shares. There is no authority under the U.S. tax laws expressly addressing whether the payment of cash to Tenda shareholders who exercise withdrawal rights pursuant to Brazilian law will prevent the Restructuring from satisfying this “solely for voting stock” requirement. However, based on the advice of Gafisa’s Brazilian counsel to the effect that solely Tenda, and not Gafisa, will be liable to make any cash payment to any Tenda shareholders who exercise withdrawal rights, and assuming that any such payments are not funded indirectly by Gafisa, the payment of such cash to Tenda shareholders who exercise withdrawal rights should not prevent the Restructuring from qualifying as a reorganization for U.S. federal income tax purposes. No ruling has been sought or will be obtained from the U.S. Internal Revenue Service on the U.S. federal income tax consequences of the transaction.

If the Restructuring qualifies as a reorganization for U.S. federal income tax purposes, you generally will not recognize gain or loss for U.S. federal income tax purposes on the receipt of Gafisa shares in exchange for Tenda shares, except to the extent of gain attributable to cash received in lieu of a fractional Gafisa share. If the Restructuring is a taxable transaction, you generally will recognize gain or loss on the receipt of Gafisa shares in exchange for Tenda shares. Please review carefully the section under “Part Five: the Restructuring—Material Tax Considerations—United States Federal Income Tax Considerations.”

The Restructuring may also have Brazilian tax implications, as described under “Part Five: The Restructuring—Material Tax Considerations—Brazilian Tax Considerations.”

The Restructuring will require the affirmative vote of holders representing at least 50% of the Tenda common shares at the EGM of Tenda, to take place after the declaration of effectiveness of the registration statement to which

this preliminary prospectus/information statement is a part to by the SEC and the distribution of this preliminary prospectus/information statement to the shareholders of Tenda.

The Restructuring will be also subject to approval by the majority of Gafisa’s shareholders present at a duly convened EGM of Gafisa to take place promptly after the Tenda EGM, provided that such EGM shall only occur on a first call if shareholders representing at least two thirds of Gafisa’s voting capital attend. If the attendance quorum is not reached, the EGM may occur, on a second call, with any number of shareholders. The EGMs of Gafisa and Tenda are currently scheduled to be held as follows:

Gafisa S.A., December 14, 2009 2:00 p.m. (São Paulo time)

Av. Nações Unidas No. 8,501, 19th floor, 05425−070 − São Paulo, SP − Brazil

Construtora Tenda S.A., December 14, 2009 9:00 a.m. (São Paulo time)

Av. Engenheiro Luiz Carlos Berrini No. 1,376, 10th floor, 04571−000 − São Paulo, SP − Brazil