Exhibit 99.1

|

[GRAPHIC OMITTED] TENDA

Construindo felicidage

Contracting Party: Construtora Tenda S.A.

Subject Matters: Construtora Tenda S.A. and

Gafisa S.A.

THIS IS A FREE TRANSLATION OF THE REPORT PREPARED BY BANCO ITAU BBA S.A. ON

NOVEMBER 3rd, 2009. IN CASE OF ANY INCONSISTENCIES BETWEEN THIS REPORT AND ITS

PORTUGUESE VERSION, THE PORTUGUESE VERSION SHALL PREVAIL

[GRAPHIC OMITTED]

CONFIDENTIAL |November, 2009

slide01

|

|

Important Notes [GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

RELEVANT LEGAL INFORMATION - By accessing this Valuation Report, the person

confirms that he/she has read the following information and undertakes to fully

comply with all provisions below:

Banco Itau BBA S.A. ("Itau BBA") was engaged by Construtora Tenda S.A.

("Tenda") to prepare an economic and financial valuation report ("Valuation

Report") of Tenda and Gafisa S.A. ("Gafisa" and, jointly with Tenda,

"Companies"). This material is prepared within the context of a possible merger

of shares involving Tenda and Gafisa in accordance with the Material Fact

published on October 22, 2009 ("Transaction").

1. This Valuation Report was prepared for Tenda's exclusive use within the

context of its Independent Committee only, for Valuation of the Transaction,

and shall not be used or taken as a basis by anyone other than the persons for

whom this Report is expressly intended, as mentioned above, or for any purposes

other than those described herein. This Valuation Report, including its

analyses and conclusions, shall not be deemed as a recommendation or an

indication on how to proceed in relation to any decision. Any decisions that

may be taken by Tenda and/or its Independent Committee are their sole and

exclusive responsibility based on the risk and benefit analysis involved in the

Transaction. Thus, Tenda and its Independent Committee and any third party that

Itau BBA may authorize to verify this Valuation Report shall keep Itau BBA, its

directors, officers, employees and/or designees exempted, in a wide manner,

from any and all liabilities for losses, damages, expenses and judicial claims

directly or indirectly arising from the compilation of this Valuation Report,

including undertaking to promptly and fully indemnify Itau BBA for any loss

arising from issuance of this Valuation Report. Itau BBA does not take

responsibility and shall not be held liable for any direct or indirect damage

and/or loss or loss of profit that may arise from this Valuation Report from

time to time. The information contained herein is confidential and for the sole

use of Tenda and its Independent Committee. This Valuation Report shall not be

transmitted to any third party in any form not previously agreed upon with Itau

BBA or without the express consent of Itau BBA therefor. This Valuation Report

was completed and delivered on November 3, 2009.

2. For the issuance of this Valuation Report: (i) we used the consolidated

financial statements of Tenda and Gafisa as audited by Terco Grant Thornton

Auditores Independentes and by PricewaterhouseCoopers Auditores Independentes,

respectively, for the fiscal years ended on December 31, 2007 and December 31,

2008; (ii) we used public information on Tenda and Gafisa; (iii) we conducted

discussions with members of Tenda's Independent Committee about the business

and outlooks for the Companies; and (iv) we took into account other public

information, financial studies, analyses and researches, and financial,

economic and market criteria that we considered as relevant, including to

analyze, when and if applicable, the consistency of the information received

from Tenda (jointly, the "Information").

3. Within the scope of our work, we assume that all the Information is true,

accurate and complete and that no other information that might be relevant

within the scope of our works was not made available to use by Tenda and/or its

Independent Committee as applicable. In relation to the part of the Information

related to the future, we assumed that such Information reflects the best

estimates of Tenda's directors as currently available in relation to its future

performance. Additionally, within the scope of our work, we analyzed the

consistency of the Information based on our experience and good judgment, but

we do not undertake any responsibility for independent investigations of any

Information or independent verification or valuation of any assets or

liabilities (whether they are contingent or not) of the Companies. No such

valuation in this regard has been delivered to us either. We have not been

asked to conduct (and we have not conducted) any physical inspection of the

Companies' properties or facilities. Finally, we have not evaluated the

Companies' solvency or fair value considering the laws related to bankruptcy,

insolvency or similar issues.

4. Due to the limitations referred to in item 3 above, we have not and will not

provide, either expressly or implicitly, any representation or warranty in

relation to any Information used to prepare the Valuation Report. If any of the

related Information and/or assumptions is not fulfilled or if the Information

is somehow shown to be incorrect, incomplete or inaccurate, the conclusions may

be changed in a material manner.

5. The preparation of a financial analysis is a complex process that involves

several definitions related to the most appropriate and relevant financial

analysis methods as well as application of such methods. We reached a final

conclusion based on the results of the entire analysis carried out, considered

as a whole, and we did not reach any conclusions based on or related to any of

the factors or methods of our analyses considered alone. Thus, we believe that

our analysis must be considered as a whole and that the selection of parts of

our analysis and specific factors without considering all of our analysis and

conclusions may result in an incomplete and inaccurate understanding about the

processes used for our analyses and conclusions.

2

slide02

|

| Important Notes (Continued) [GRAPHIC OMITTED] - -------------------------------------------------------------------------------- 6. This Valuation Report indicates an estimate only, at our discretion, of the value obtained from application of valuation methodologies used in companies' financial valuations, and does not evaluate any other aspect or implication of the Transaction or any contract, agreement or understanding entered into in relation to the Transaction. We do not express our opinion in relation to the exchange ratio, amount to be paid for the shares under the Transaction or the value at which the Companies' shares may be traded in the security market at any time. Additionally, this Valuation Report may not be interpreted by any person obtaining access to the valuation report to constitute a fairness opinion or any indication of fairness from Itau BBA in relation to the Transaction. Additionally, this Valuation Report does not deal with the strategic and commercial merits of the Transaction, nor does it deal with any possible strategic and commercial decision of the Companies to carry out the Transaction. The results presented in this Valuation Report refer to the Transaction only and shall not be applied to any other present or future decision or operation related to the Companies, the economic group to which they belong or the market in which they operate. This Valuation Report does not constitute a judgment, opinion or recommendation to the management of Tenda and the Independent Committee or any third party in relation to the convenience and opportunity of the Transaction, as it is not intended to serve as a basis for any investment or any other decision. 7. Our Valuation Report is necessarily based on information that was made available to us until the date hereof and considering market, economic and other conditions as they are presented and as they may be evaluated on the date hereof. Although future events and other developments may affect the conclusions presented in this Valuation Report, we have no obligation to update, review, rectify or revoke this Valuation Report, in whole or in part, as a result of any subsequent development or due to any other reason whatsoever. 8. Our analyses do not include operating, tax or other benefits or losses of any type whatsoever, including any possible premium, nor do they include any synergies, incremental value and/or costs, if any, as of the closing of the Transaction, if closed, or of any other operation. Our analyses are not and shall not be considered as a recommendation in relation to how the Independent Committee, Tenda and/or Gafisa's shareholders must vote or perform in relation to the Transaction. We have not been requested to take part and we will not take part in the negotiation or structuring of the Transaction. 9. Tenda has agreed to reimburse us for our expenses and to indemnify us as well as some persons as a result of our engagement. We will receive a fee in relation to the preparation of this Valuation Report regardless of the Transaction completion. 10. We provided investment banking and banking services and financial services in general as well as other financial services to Tenda and to Gafisa and to their respective affiliates from time to time in the past, for which we were compensated, and we may, in the future, provide such services to Tenda and to Gafisa and to their respective affiliates, for which we expect to be compensated. We and our affiliates provide a variety of financial services and other services related to securities, brokerage and investment banking. In the usual course of our activities we may purchase, hold or sell, on our behalf or on the behalf and at the behest of our customers, shares, doubt instruments and other securities and financial instruments (including bank loans and other liabilities) of Tenda and Gafisa and of any other companies that may be involved in the Transaction, and we may provide investment banking services and other financial services to such companies and their respective subsidiaries or parent companies. The professionals of the securities analyses department (research) and other divisions of Itau Group, including Itau BBA, may base their analyses and publications on different operating and market assumptions and on different analysis methodologies when compared with those used in the preparation of this Valuation Report, so that the research reports and other publications prepared by them may contain results and conclusions that are different from those prepared herein, considering that such analyses and reports are performed by analysts who are independent from any relationship with the professionals who performed in the preparation of this Valuation Report. We adopt policies and procedures designed to protect the independence of our security analysts, whose views may differ from those of our investment banking department. We also adopt policies and procedures designed to protect the independence between the investment banking and the other areas and departments of Itau BBA and other companies of Itau Group, including but not limited to asset management, proprietary share trading desk, debt instruments, securities and other financial instruments. 11. We have not provided any accounting, auditing, legal, tax or fiscal services in relation to this Valuation Report. 12. The financial calculations contained in this Valuation Report may not always result in an accurate sum due to rounding. 13. This Valuation Report is the intellectual property of Itau BBA. Banco Itau BBA S.A. 3 slide03 |

|

Contents [GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Important Notes

SECTION 1 Executive Summary

SECTION 2 Information on Itau BBA

SECTION 3 Description of the Transaction

SECTION 4 Valuation of the Companies

SUB-SECTION 4A Market Price Metrics

SUB-SECTION 4B Balance Sheet Metrics

SUB-SECTION 4C Trading Multiples

EXHIBIT Overview of the Selected Comparables

4

slide04

|

|

[GRAPHIC OMITTED] TENDA

Construindo felicidage

5

slide05

|

|

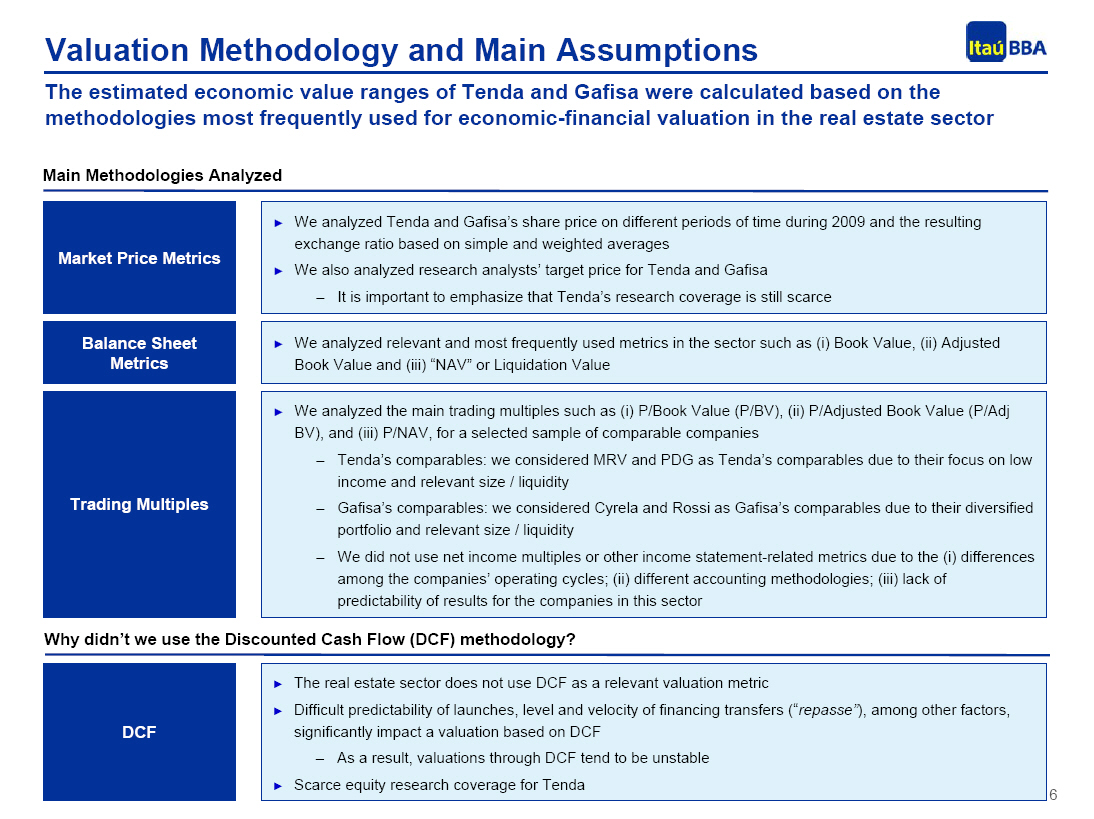

Valuation Methodology and Main Assumptions [GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

The estimated economic value ranges of Tenda and Gafisa were calculated based

on the methodologies most frequently used for economic-financial valuation in

the real estate sector

Main Methodologies Analyzed

[GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Market Price > We analyzed Tenda and Gafisa's share price on different

Metrics periods of time during 2009 and the resulting exchange

ratio based on simple and weighted averages

> We also analyzed research analysts' target price for

Tenda and Gafisa

- It is important to emphasize that Tenda's

research coverage is still scarce

- --------------------------------------------------------------------------------

Balance Sheet > We analyzed relevant and most frequently used metrics in

Metrics the sector such as (i) Book Value, (ii) Adjusted Book

Value and (iii) "NAV" or Liquidation Value

- --------------------------------------------------------------------------------

> We analyzed the main trading multiples such as (i) P/Book

Value (P/BV), (ii) P/Adjusted Book Value (P/Adj BV), and

(iii) P/NAV, for a selected sample of comparable companies

- Tenda's comparables: we considered MRV and PDG as

Tenda's comparables due to their focus on low

income and relevant size / liquidity

Trading - Gafisa's comparables: we considered Cyrela and

Multiples Rossi as Gafisa's comparables due to their

diversified portfolio and relevant size /

liquidity

- We did not use net income multiples or other

income statement-related metrics due to the (i)

differences among the companies' operating

cycles; (ii) different accounting methodologies;

(iii) lack of predictability of results for the

companies in this sector

- --------------------------------------------------------------------------------

Why didn't we use the Discounted Cash Flow (DCF) methodology?

- --------------------------------------------------------------------------------

- --------------------------------------------------------------------------------

> The real estate sector does not use DCF as a relevant

valuation metric

DCF > Difficult predictability of launches, level and velocity

of financing transfers ("repasse"), among other factors,

significantly impact a valuation based on DCF

- As a result, valuations through DCF tend to be

unstable

> Scarce equity research coverage for Tenda

- --------------------------------------------------------------------------------

6

slide06

|

|

Valuation Summary - Tenda [GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

The range of price per share for Tenda based on these methodologies results in

R$2.75 to R$8.51

Company's Value per Share (R$ / share)

- --------------------------------------------------------------------------------

[GRAPHIC OMITTED]

Source: Bloomberg and Companies' Reports as of October 27, 2009

2.50 4.00 5.50 7.00 8.50

Notes:

1 Based on the average closing price of the shares in the periods of 30d, 60d,

90d and 180d (through October 21, 2009)

2 Based on the weighted average price of the shares in the periods of 30d, 60d,

90d and 180d (through October 21, 2009)

3 Based on the target price for Tenda from JPM and Brascan Corretora

4 PDG and MRV are considered as comparable companies

5 We used Itau Corretora's methodology to calculate the NAV (receivables +

inventories + sales to be recognized - costs to be recognized - land bank

to be paid - net debt - minority interest)

6 Adjusted Book Value: shareholders' equity + sales to be recognized - costs to

be recognized

7

slide07

|

|

Valuation Summary - Gafisa [GRAPHIC OMITTED]

The range of price per share for Gafisa based on these methodologies results in

R$13.18 to R$44.60

Company's Value per Share (R$ / share)

- --------------------------------------------------------------------------------

[GRAPHIC OMITTED]

Source: Bloomberg and Companies' Reports as of October 27, 2009

13.00 18.00 23.00 28.00 33.00 38.00 43.00

Notes:

1 Based on the average closing price of the shares in the periods of 30d, 60d,

90d and 180d (through October 21, 2009)

2 Based on the weighted average price of the shares in the periods of 30d, 60d,

90d and 180d (through October 21, 2009)

3 Based on the target price for Gafisa from BofAML and Barclays

4 Cyrela and Rossi are considered as comparable companies

5 We used Itau Corretora's methodology to calculate the NAV (receivables +

inventories + sales to be recognized - costs to be recognized - land bank

to be paid - net debt - minority interest)

6 Adjusted Book Value: shareholders' equity + sales to be recognized -

costs to be recognized

8

slide08

|

|

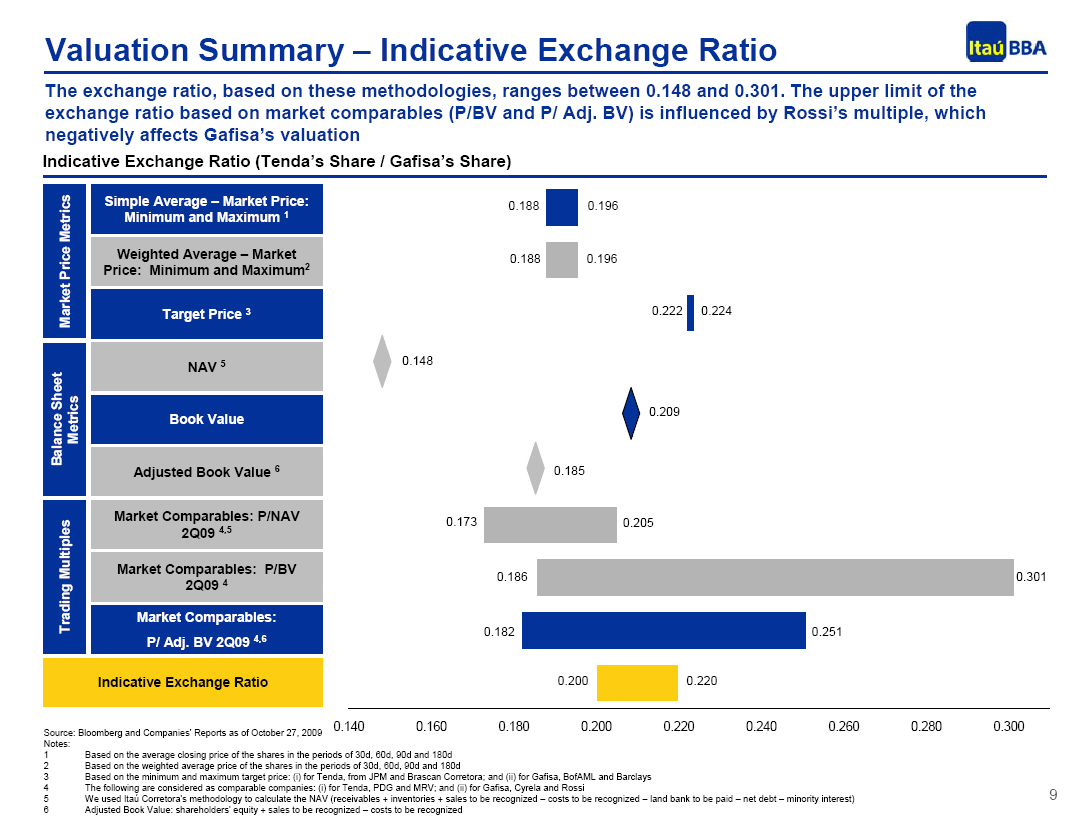

Valuation Summary - Indicative Exchange Ratio [GRAPHIC OMITTED]

- -------------------------------------------------------------------------------

The exchange ratio, based on these methodologies, ranges between 0.148 and

0.301. The upper limit of the exchange ratio based on market comparables (P/BV

and P/ Adj. BV) is influenced by Rossi's multiple, which negatively affects

Gafisa's valuation

Indicative Exchange Ratio (Tenda's Share / Gafisa's Share)

- --------------------------------------------------------------------------------

[GRAPHIC OMITTED]

Source: Bloomberg and Companies' Reports as of October 27, 2009

0.140 0.160 0.180 0.200 0.220 0.240 0.260 0.280 0.300

Notes:

1 Based on the average closing price of the shares in the periods of 30d, 60d,

90d and 180d

2 Based on the weighted average price of the shares in the periods of 30d, 60d,

90d and 180d

3 Based on the minimum and maximum target price: (i) for Tenda, from JPM and

Brascan Corretora; and (ii) for Gafisa, BofAML and Barclays

4 The following are considered as comparable companies: (i) for Tenda, PDG

and MRV; and (ii) for Gafisa, Cyrela and Rossi 9

5 We used Itau Corretora's methodology to calculate the NAV (receivables +

inventories + sales to be recognized - costs to be recognized - land bank

to be paid - net debt - minority interest)

6 Adjusted Book Value: shareholders' equity + sales to be recognized - costs to

be recognized

9

slide09

|

|

Calculation of the Indicative Exchange Ratio [GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

The Indicative Exchange Ratio was achieved based on the assumptions and

criteria described below, which were discussed with Tenda's Independent

Committee. All terms and conditions referred to in the section "Important Notes

- - Relevant Legal Information" of this Report apply to the Indicative Exchange

Ratio. Specially, it should be emphasized that, if any of the following

assumptions and/or criteria used to establish the Indicative Exchange Ratio

change, the results may be materially different from those indicated in this

Report. The Indicative Exchange Ratio is Itau BBA's best indication. Itau BBA

does not take any responsibility in relation to this number to the Independent

Committee and/or any third party.

Methodology Used

- --------------------------------------------------------------------------------

Average of the > Given the importance of each criteria, their wide

Main Metrics use as well as their specificities, we believe

that the simple average of the minimum and

maximum values of each of the ranges is the best

methodology

- --------------------------------------------------------------------------------

Criteria - Rational

- --------------------------------------------------------------------------------

Market Price Metrics

- --------------------

Current and > Current and historical prices tend to be the ones

Historical Prices that best reflect the currently available

information and expectations. Since the simple and

weighted averages are equal, we will use the simple

average in order not to double this metric's weight

-------------------------------------------------------

Target Price > In addition to the topic above, this is an

independent metric, known in the market, and that

captures the expectation of share appreciation

(proxy for "fair value")

- --------------------------------------------------------------------------------

Balance Sheet Metrics

- ---------------------

Book Value and > The book value was considered as it reflects the

Adjusted Book Value current accounting position of both companies and

is a commonly used metric (used by the Corporation

Act ("Lei das S.A."). The adjusted book value was

not considered due to differences in the companies'

operating cycle

-------------------------------------------------------

> We did not consider the NAV, despite its being a

NAV relatively common metric, as we believe that it

fails to capture the growth potential as well as

the differences in the companies' operating cycles

- --------------------------------------------------------------------------------

Trading Multiples Metrics

- -------------------------

Market Comparables: > Due to the same reasons as above, we did not

P/NAV consider the P/NAV

-------------------------------------------------------

Market Comparables: > In spite of being used in the market (less

P/BV frequently), this metric fails to capture the

companies' growth potential. We also believe that

the upper limit of this range, calculated based on

Rossi's multiple, is an outlier and that the wide

range would distort the analysis

-------------------------------------------------------

Market Comparables: > After incorporating the backlog of results to be

P/ Adj. BV recognized to the calculation, so as to include the

growth outlook and minimize distortions, the P/Adj.

BV is a widely used metric

- --------------------------------------------------------------------------------

10

slide10

|

|

[GRAPHIC OMITTED] TENDA

Construindo Felicidage

SECTION 2

Information on Itau BBA

11

slide11

|

|

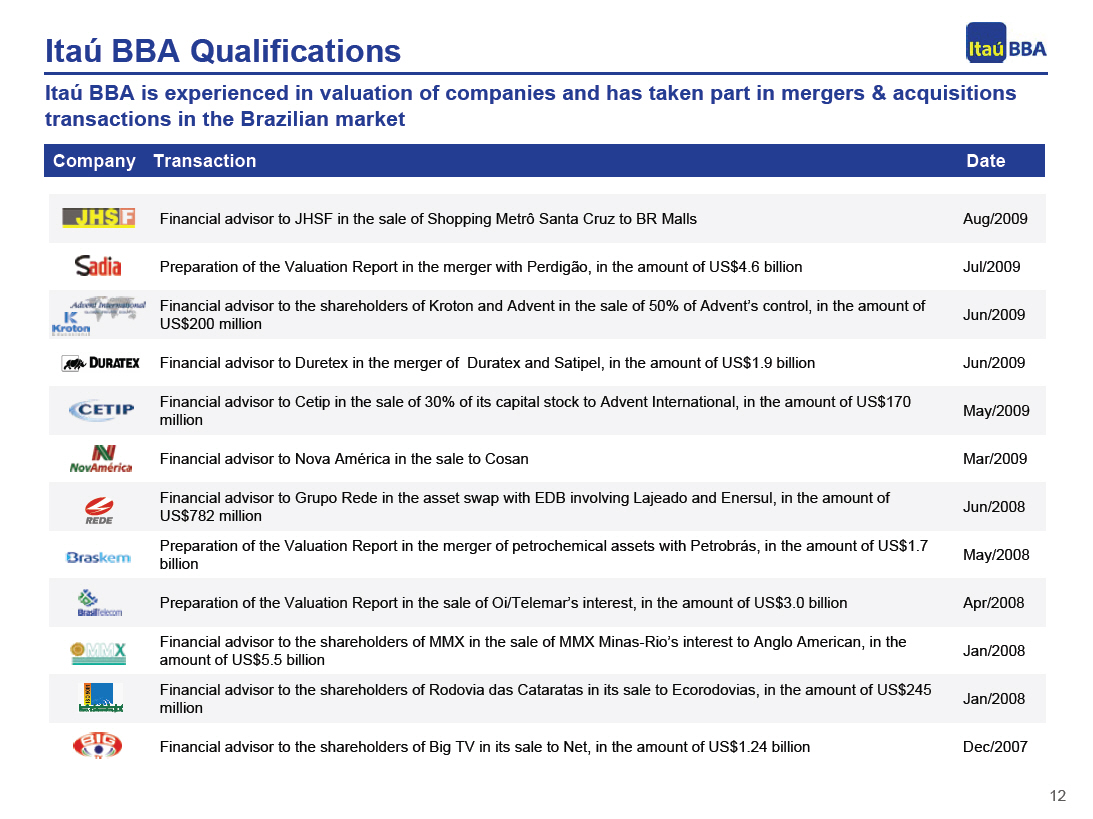

Itau BBA Qualifications [GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Itau BBA is experienced in valuation of companies and has taken part in mergers

& acquisitions transactions in the Brazilian market

- --------------------------------------------------------------------------------

Company Transaction

- --------------------------------------------------------------------------------

[GRAPHIC Financial advisor to JHSF in the sale of Shopping

OMITTED] Metro Santa Cruz to BR Malls Aug/2009

[GRAPHIC Preparation of the Valuation Report in the merger

OMITTED] with Perdigao, in the amount of US$4.6 billion Jul/2009

[GRAPHIC Financial advisor to the shareholders of Kroton

OMITTED] and Advent in the sale of 50% of Advent's control,

in the amount of US$200 million Jun/2009

[GRAPHIC Financial advisor to Duretex in the merger of Duratex and

OMITTED] Satipel, in the amount of US$1.9 billion Jun/2009

[GRAPHIC Financial advisor to Cetip in the sale of 30% of

OMITTED] its capital stock to Advent International, in the

amount of US$170 million May/2009

[GRAPHIC Financial advisor to Nova America in the sale to Cosan Mar/2009

OMITTED]

[GRAPHIC Financial advisor to Grupo Rede in the asset swap

OMITTED] with EDB involving Lajeado and Enersul, in the

amount of US$782 million un/2008

[GRAPHIC Preparation of the Valuation Report in the merger

OMITTED] of petrochemical assets with Petrobras, in the

amount of US$1.7 billion May/2008

[GRAPHIC Preparation of the Valuation Report in the sale

OMITTED] of Oi/Telemar's interest, in the amount of US$3.0

billion Apr/2008

[GRAPHIC Financial advisor to the shareholders of MMX in

OMITTED] the sale of MMX Minas-Rio's interest to Anglo

American, in the amount of US$5.5 billion Jan/2008

[GRAPHIC Financial advisor to the shareholders of Rodovia

OMITTED] das Cataratas in its sale to Ecorodovias, in the

amount of US$245 million Jan/2008

[GRAPHIC Financial advisor to the shareholders of Big TV

OMITTED] in its sale to Net, in the amount of US$1.24

billion Dec/2007

12

slide12

|

|

Itau BBA Qualifications (cont'd) [GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Company Transaction

- --------------------------------------------------------------------------------

[GRAPHIC OMITTED] Financial Advisor to Lopes in the merger with Patrimovel

in the amount of US$140 million Nov/2007

[GRAPHIC OMITTED] Financial Advisor to Klabin Segall in the merger with

Setin, in the amount of US$112 million Oct/2007

[GRAPHIC OMITTED] Financial Advisor to the shareholders of Suzano

Petroquimica in its merger with Petrobras, in the amount

of US$1.24 billion Aug/2007

[GRAPHIC OMITTED] Financial Advisor to Santos Brasil in the merge with

Mesquita, in the amount of US$51 million Aug/2007

[GRAPHIC OMITTED] Financial Advisor to Energisa in the sale of the

generation assets, including 11 PCHs and 4 projects, in

the amount of US$156 million Jul/2007

[GRAPHIC OMITTED] Financial Advisor to the shareholders of Serasa in the

sale of 65% of Serasa's interest to Experian, in the

amount of US$1.78 billion Jun/2007

[GRAPHIC OMITTED] Financial Advisor to MMX in the sale of 49% of interest

in MMX Minas-Rio to Anglo American, in the amount of

US$1.58 billion Apr/2007

[GRAPHIC OMITTED] Financial Advisor in the process of deverticalization of

CEEE's generation and distribution assets in the amount

of US$179 million Dec/2006

[GRAPHIC OMITTED] Financial Advisor to International Paper in the sale of

Amcel, in the amount of US$56 million Nov/2006

[GRAPHIC OMITTED] Financial Advisor to the shareholders of Vivax

in the merger with Net, in the amount of

US$676 million Oct/2006

[GRAPHIC OMITTED] Financial Advisor to Fertibras in the sale of

Fertibras' control to Yara International, in

the amount of US$339 million Jul/2006

[GRAPHIC OMITTED] Financial Advisor to CEMIG, Andrade

Gutierrez, JLA Part. and Pactual in the merger

with Light, in the amount of US$2.1 billion Mar/2006

13

slide13

|

|

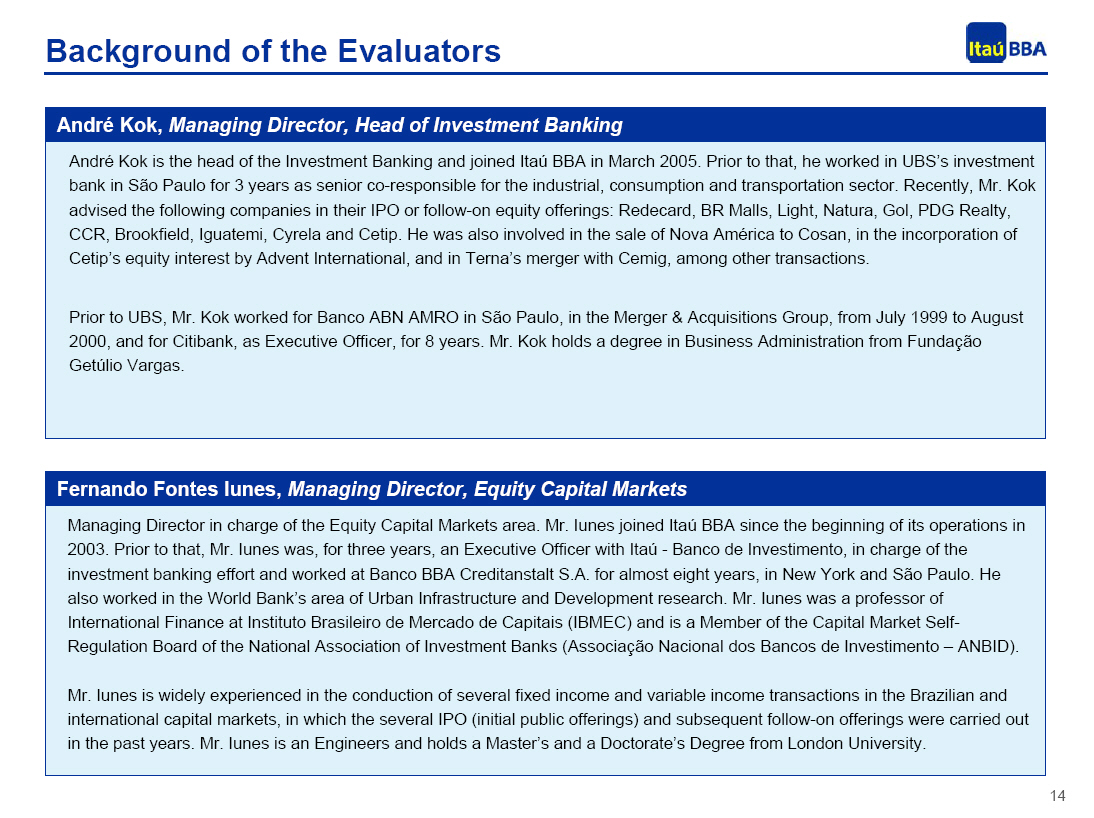

Background of the Evaluators [GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Andre Kok, Managing Director, Head of Investment Banking

- --------------------------------------------------------------------------------

Andre Kok is the head of the Investment Banking and joined Itau BBA in March

2005. Prior to that, he worked in UBS's investment bank in Sao Paulo for 3

years as senior co-responsible for the industrial, consumption and

transportation sector. Recently, Mr. Kok advised the following companies in

their IPO or follow-on equity offerings: Redecard, BR Malls, Light, Natura,

Gol, PDG Realty, CCR, Brookfield, Iguatemi, Cyrela and Cetip. He was also

involved in the sale of Nova America to Cosan, in the incorporation of Cetip's

equity interest by Advent International, and in Terna's merger with Cemig,

among other transactions.

Prior to UBS, Mr. Kok worked for Banco ABN AMRO in Sao Paulo, in the Merger &

Acquisitions Group, from July 1999 to August 2000, and for Citibank, as

Executive Officer, for 8 years. Mr. Kok holds a degree in Business

Administration from Fundacao Getulio Vargas.

- --------------------------------------------------------------------------------

- --------------------------------------------------------------------------------

Fernando Fontes Iunes, Managing Director, Equity Capital Markets

- --------------------------------------------------------------------------------

Managing Director in charge of the Equity Capital Markets area. Mr. Iunes

joined Itau BBA since the beginning of its operations in 2003. Prior to that,

Mr. Iunes was, for three years, an Executive Officer with Itau - Banco de

Investimento, in charge of the investment banking effort and worked at Banco

BBA Creditanstalt S.A. for almost eight years, in New York and Sao Paulo. He

also worked in the World Bank's area of Urban Infrastructure and Development

research. Mr. Iunes was a professor of International Finance at Instituto

Brasileiro de Mercado de Capitais (IBMEC) and is a Member of the Capital Market

Self- Regulation Board of the National Association of Investment Banks

(Associacao Nacional dos Bancos de Investimento - ANBID).

Mr. Iunes is widely experienced in the conduction of several fixed income and

variable income transactions in the Brazilian and international capital

markets, in which the several IPO (initial public offerings) and subsequent

follow-on offerings were carried out in the past years. Mr. Iunes is an

Engineers and holds a Master's and a Doctorate's Degree from London University.

- --------------------------------------------------------------------------------

14

slide14

|

|

Background of the Evaluators [GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Renato Polizzi, Vice-President

- --------------------------------------------------------------------------------

Renato Polizzi joined the Investment Banking team of Itau BBA in March 2005. In

2009, he conducted the follow-on equity offerings of BR Malls (US$432 MM), Gol

(US$542 MM), PDG Realty (US$532 MM), CCR (US$630 MM), Brookfield (US$331 MM)

and Iguatemi (US$224 MM). He also took part in the sale of Shopping Metro Santa

Cruz by JHSF to BR Malls (US$102 MM).

Prior to joining Itau BBA, Mr. Polizzi worked in the investment banking teams

of UBS and Merrill Lynch. He also worked in the equity research team of

Deutsche Bank. He is fluent in English and French languages and obtained his

degree in Business Administration from Fundacao Getulio Vargas (FGV) in 1998 as

the #1 student in his year.

- --------------------------------------------------------------------------------

- --------------------------------------------------------------------------------

Ana Carolina Shibata, Associate

- --------------------------------------------------------------------------------

Ana Carolina joined Itau BBA in May 2005. In 2009, she conducted the follow-on

equity offerings of Brookfield (US$ 331 MM), CCR (US$ 630 MM) and PDG (US$ 532

MM). She also took part in the sale of Nova America to Cosan (US$ 631 MM), in

the sale of equity stake in Cetip to Advent (US$ 170 MM), among others

transactions.

Before that, she worked for Banco Espirito Santo for two years in the Merger &

Acquisitions area. From September 2001 to April 2003, Mrs. Shibata worked for

JPMorgan Bank in the Treasury and Investment Banking areas. Mrs. Shibata holds

a degree in Business Administration from Fundacao Getulio Vargas.

- --------------------------------------------------------------------------------

15

slide15

|

|

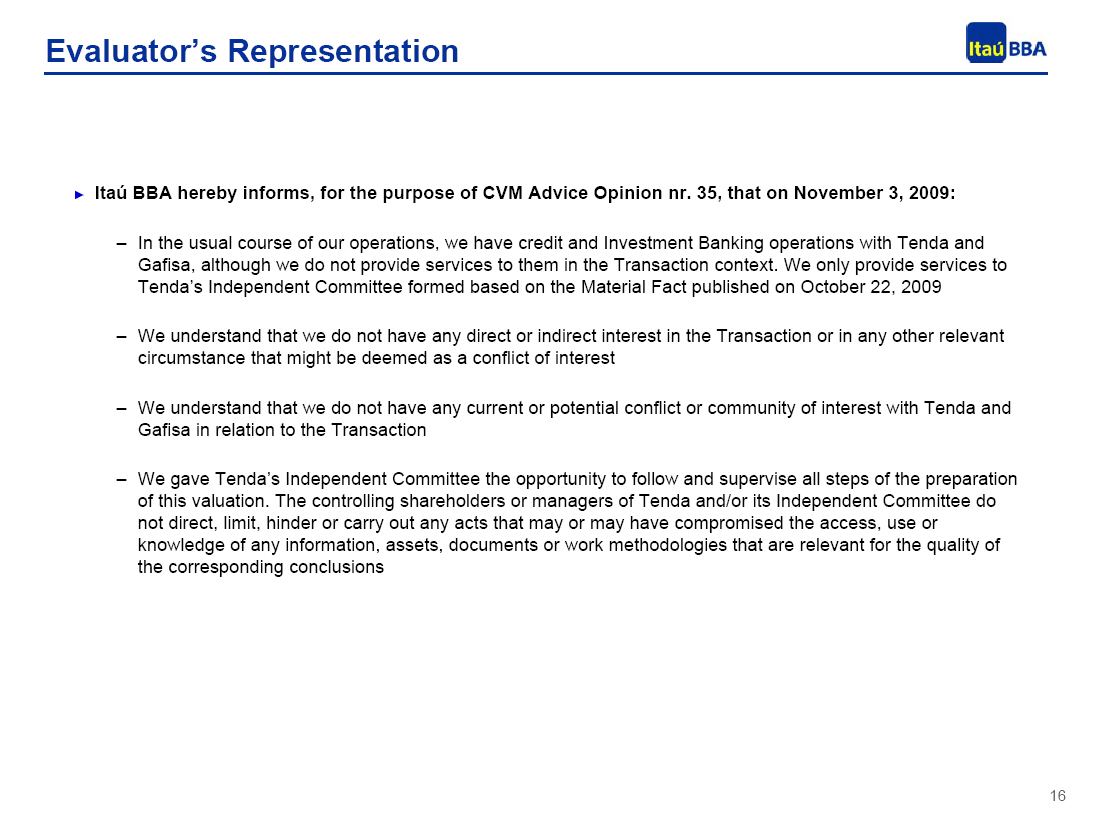

Evaluator's Representation [GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

> Itau BBA hereby informs, for the purpose of CVM Advice Opinion nr. 35,

that on November 3, 2009:

- In the usual course of our operations, we have credit and Investment

Banking operations with Tenda and Gafisa, although we do not provide

services to them in the Transaction context. We only provide services

to Tenda's Independent Committee formed based on the Material Fact

published on October 22, 2009

- We understand that we do not have any direct or indirect interest in

the Transaction or in any other relevant circumstance that might be

deemed as a conflict of interest

- We understand that we do not have any current or potential conflict

or community of interest with Tenda and Gafisa in relation to the

Transaction

- We gave Tenda's Independent Committee the opportunity to follow and

supervise all steps of the preparation of this valuation. The

controlling shareholders or managers of Tenda and/or its Independent

Committee do not direct, limit, hinder or carry out any acts that may

or may have compromised the access, use or knowledge of any

information, assets, documents or work methodologies that are

relevant for the quality of the corresponding conclusions

16

slide16

|

|

[GRAPHIC OMITTED] TENDA

Construindo Felicidage [GRAPHIC OMITTED]

SECTION 3

Description of the Transaction

17

slide17

|

|

Current Shareholder Structure of the Companies [GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Shareholder Structure (1): Tenda Shareholder Structure (1): Gafisa

- -------------------------------- ---------------------------------

[GRAPHIC OMITTED] [GRAPHIC OMITTED]

Source: Company's website Source: Company's website

(Updated on 09/22/2009) (Updated on 08/12/2009)

Note: Note:

1 Excludes treasury shares 1 Excludes treasury shares

18

slide18

|

|

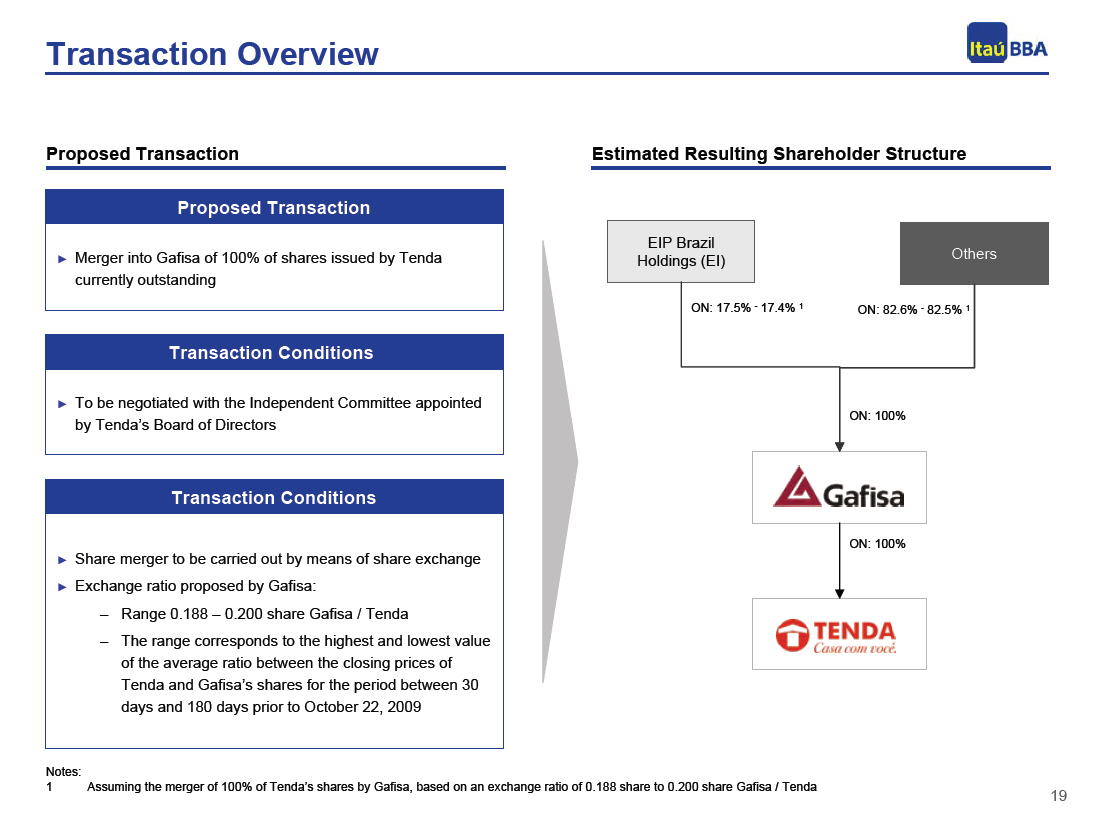

Transaction Overview [GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Proposed Transaction

- --------------------------

> Merger into Gafisa of 100% of shares issued by Tenda currently outstanding

Transaction Conditions

- ----------------------

> To be negotiated with the Independent Committee appointed

by Tenda's Board of Directors

Transaction Conditions

- ----------------------

> Share merger to be carried out by means of share exchange ? Exchange ratio

proposed by Gafisa:

- Range 0.188 - 0.200 share Gafisa / Tenda

- The range corresponds to the highest and lowest value of the average

ratio between the closing prices of Tenda and Gafisa's shares for

the period between 30 days and 180 days prior to October 22, 2009

- --------------------------------------------------------------------------------

Estimated Resulting Shareholder Structure

- -----------------------------------------

[GRAPHIC OMITTED]

Notes:

1 Assuming the merger of 100% of Tenda's shares by Gafisa, based on an

exchange ratio of 0.188 share to 0.200 share Gafisa / Tenda 19

19

slide 19

|

|

[GRAPHIC OMITTED] TENDA

Construindo Felicidage

SECTION 4

Valuation of the Companies

20

slide20

|

|

[GRAPHIC OMITTED] TENDA

Construindo Felicidage

SUB-SECTION 4A

Market Price Metrics

21

slide21

|

|

Tenda's Recent Performance [GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Tenda: Share Performance (R$ / share) (1)

- --------------------------------------------------------------------------------

[GRAPHIC OMITTED]

Source: Bloomberg as of October 27, 2009

Note:

1. Based on the closing price (December 31, 2008 = 100)

22

slide22

|

|

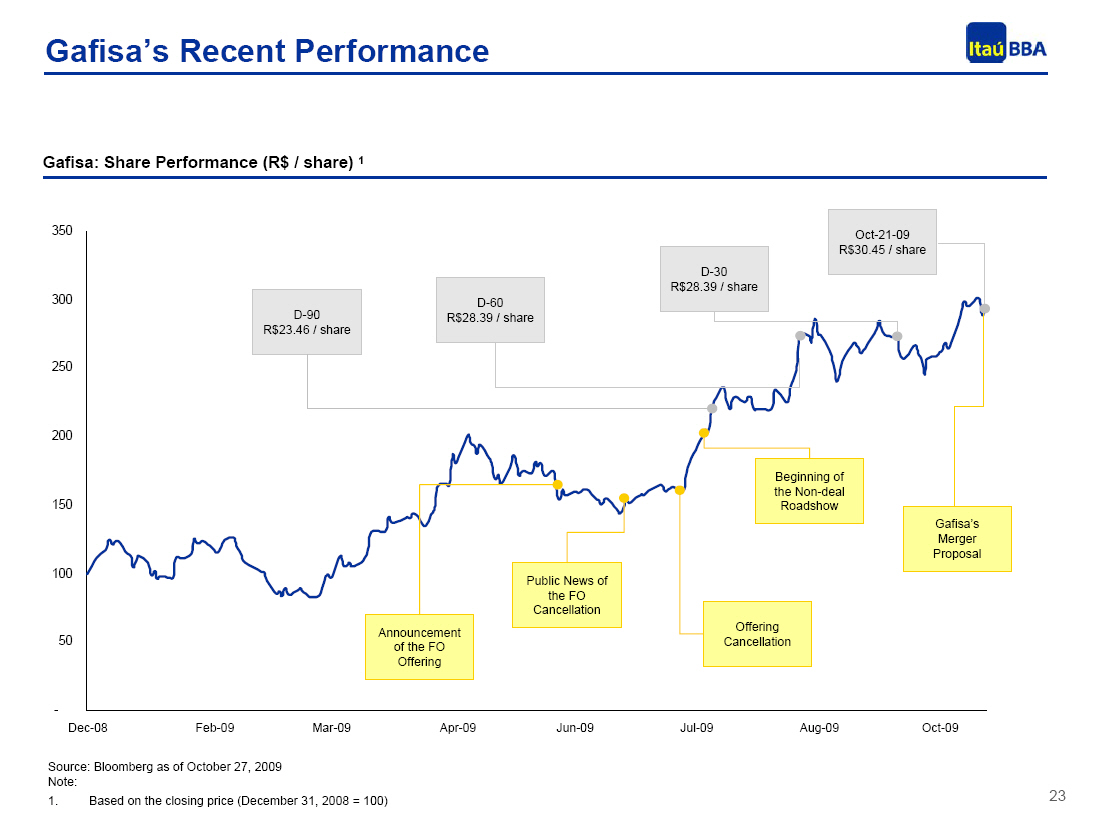

Gafisa's Recent Performance

Gafisa: Share Performance (R$ / share) (1)

[GRAPHIC]

Source: Bloomberg as of October 27, 2009 Note:

1. Based on the closing price (December 31, 2008 = 100)

23

|

|

Evolution of the Exchange Ratio: Closing Price

Evolution of the Exchange Ratio: Tenda / Gafisa (1)

[GRAPHIC]

Source: Bloomberg as of October 27, 2009 Tenda Note:

1. Based on the Companies' share closing price (up to October 21, 2009)

2. Performance on a 100 basis (December 31, 2008 = 100)

24

|

|

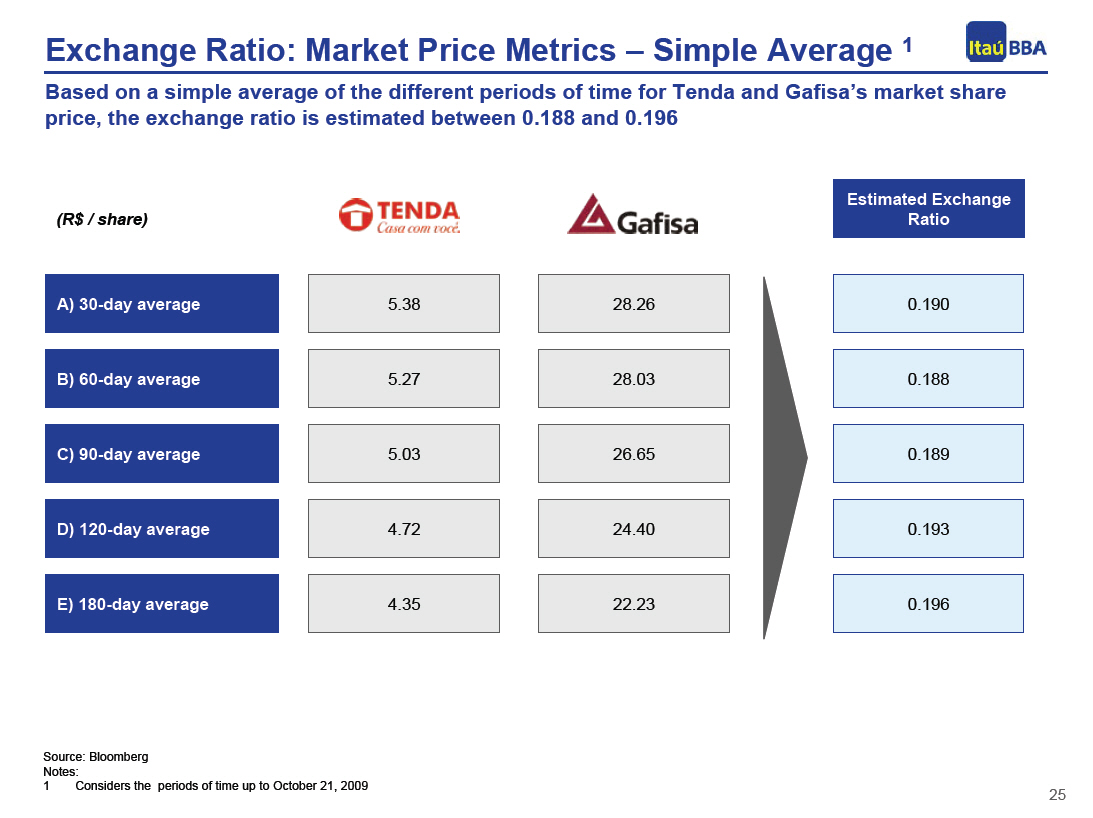

Exchange Ratio: Market Price Metrics -- Simple Average (1)

Based on a simple average of the different periods of time for Tenda and

Gafisa's market share price, the exchange ratio is estimated between 0.188 and

0.196

[GRAPHIC]

A) 30-day average 5.38 28.26 0.190

B) 60-day average 5.27 28.03 0.188

C) 90-day average 5.03 26.65 0.189

D) 120-day average 4.72 24.40 0.193

E) 180-day average 4.35 22.23 0.196

Source: Bloomberg Notes:

1 Considers the periods of time up to October 21, 2009

25

|

|

Exchange Ratio: Market Price Metrics -- Weighted Average 1

Based on a weighted average of the different periods of time for Tenda and

Gafisa's market share price, the exchange ratio is estimated between 0.188 and

0.196

A) 30-day average 5.38 28.30 0.190

B) 60-day average 5.28 28.07 0.188

C) 90-day average 5.03 26.62 0.189

D) 120-day average 4.72 24.34 0.194

E) 180-day average 4.35 22.20 0.196

Source: Bloomberg Notes:

1 Price average weighted by the trading volume. Considers the periods of time

up to October 21, 2009

26

|

|

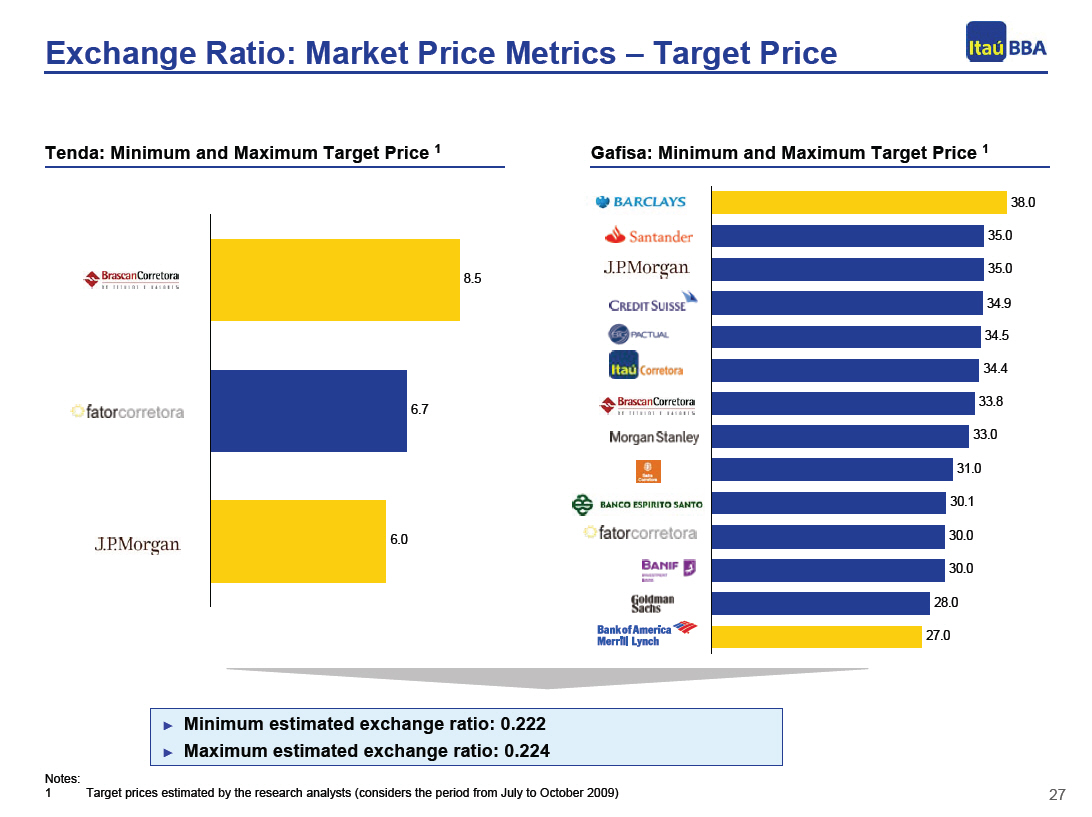

Exchange Ratio: Market Price Metrics -- Target Price

Tenda: Minimum and Maximum Target Price (1)

[GRAPHIC]

Gafisa: Minimum and Maximum Target Price (1)

[GRAPHIC]

Minimum estimated exchange ratio: 0.222

Maximum estimated exchange ratio: 0.224

Notes:

1 Target prices estimated by the research analysts (considers the period from

July to October 2009)

27

|

|

[GRAPHIC]

Balance Sheet Metrics

28

|

|

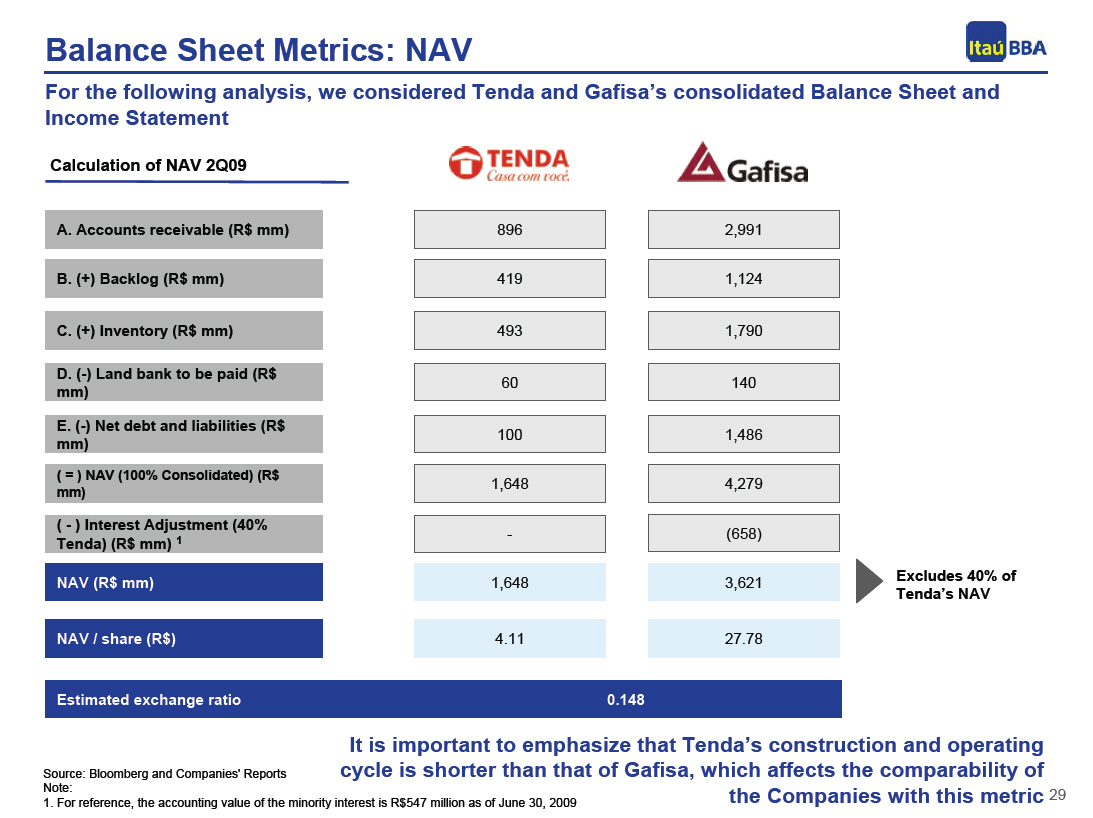

Balance Sheet Metrics: NAV

For the following analysis, we considered Tenda and Gafisa's consolidated

Balance Sheet and Income Statement

Calculation of NAV 2Q09

A. Accounts receivable (R$ mm) 896 2,991

B. (+) Backlog (R$ mm) 419 1,124

C. (+) Inventory (R$ mm) 493 1,790

D. (-) Land bank to be paid (R$ 60 140

mm)

E. (-) Net debt and liabilities (R$ 100 1,486

mm)

( = ) NAV (100% Consolidated) (R$ 1,648 4,279

mm)

( - ) Interest Adjustment (40% - (658)

Tenda) (R$ mm) (1)

NAV (R$ mm) 1,648 3,621

NAV / share (R$) 4.11 27.78

Excludes 40% of Tenda's NAV

Estimated exchange ratio 0.148

Source: Bloomberg and Companies' Reports Note:

1. For reference, the accounting value of the minority interest is R$547

million as of June 30, 2009

29

|

|

Balance Sheet Metrics: Simple and Adjusted Book Value

Book Value -- 2Q09 (R$ mm) 1,101 1,717

Book Value per share (R$) 2.75 13.18

Estimated exchange ratio = 0.209

A. Book Value -- 2Q09 (R$ mm) 1,101 1,717

B. ( + ) Backlog -- 2Q09 (R$ mm) 419 1,124

( = ) Adjusted Book Value 1,520 2,841

(100% Consolidated) (R$ mm)

( - ) Interest Adjustment (40% of - (168)

Tenda's Backlog) (R$ mm)

Adjusted Book Value (R$ mm) 1,520 2,674

Adjusted Book Value / share (R$) 3.79 20.52

Estimated exchange ratio = 0.185

Source: Bloomberg and Companies' Reports

30

|

|

[GRAPHIC]

SUB-SECTION 4C

Trading Multiples

31

|

|

Selected Comparables: Capitalization and Performance

We selected the companies below as a sample for the analysis of trading

multiples considering their focus and size / liquidity

Market Capitalization (R$ mm)

[GRAPHIC]

2009 YTD Performance

[GRAPHIC]

Source: Bloomberg as of October 27, 2009

32

|

|

Selected Comparables: Liquidity and Upside Potential

Based on the target price estimated by research analysts, the companies with

focus on low income have a higher upside potential

Free Float and Liquidity (1) (R$ mm)

[GRAPHIC]

Upside Potential: Target Price (2)

[GRAPHIC]

Source: Bloomberg as of October 27, 2009 Note:

1. Average volume traded within the past 30 days

2. Average target price estimated by research analysts (considers the period of

time from July to October 2009)

33

|

|

Trading Multiples

P / BV

[GRAPHIC]

P / Adj. BV(1)

[GRAPHIC]

P / NAV (2)

[GRAPHIC]

Source: Bloomberg as of October 27, 2009 Low Income Diversified Notes:

1. Adjusted book value: shareholders' equity + sales to be recognized -- costs

to be recognized

2. We used Ita Corretora's methodology to calculate the NAV (receivables +

inventories + sales to be recognized -- costs to be recognized -- land bank to

be paid -- net debt -- minority interest)

34

|

|

Trading Multiples: P/NAV

Selected Comparables

NAV (R$ mm) 1,648

( x ) P/NAV Multiple 1.8x 1.9x

( = ) Equity Value (R$ mm) 2,930 3,094

Price per Share (R$) 7.31 7.72

NAV (stand alone) (R$ mm) 2,630

( x ) P/NAV Multiple 1.1x 1.5x

( + ) 60% NAV Tenda X Tenda's 1,761 1,860

comparables' multiple (R$ MM)

( = ) Equity Value (R$ mm) 4,642 5,813

Price per Share (R$) 35.61 44.60

Estimated Exchange Ratio: 0.173 to 0.205

35

|

|

Trading Multiples: P/Book Value

[GRAPHIC]

Selected Comparables

Book Value (R$ mm) 1,101

( x ) P/Book Value Multiple 2.1x 2.4x

( = ) Equity Value (R$ mm) 2,299 2,659

Price per Share (R$) 5.74 6.64

Book Value (R$ mm) 1,717

( x ) P/Book Value Multiple 1.4x 2.7x

( = ) Equity Value (R$ mm) 2,483 4,652

Price per Share (R$) 19.05 35.69

Estimated Exchange Ratio: 0.186 to 0.301

36

|

|

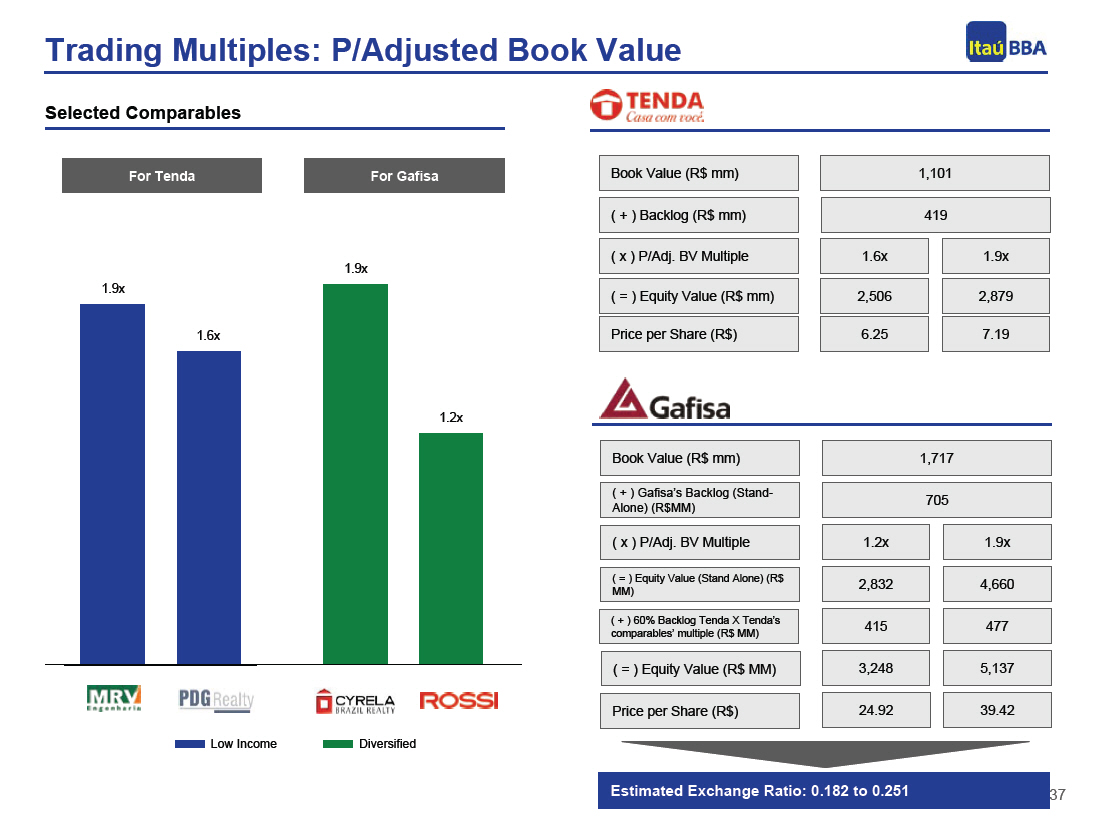

Trading Multiples: P/Adjusted Book Value

[GRAPHIC]

Selected Comparables

Book Value (R$ mm) 1,101

( + ) Backlog (R$ mm) 419

( x ) P/Adj. BV Multiple 1.6x 1.9x

( = ) Equity Value (R$ mm) 2,506 2,879

Price per Share (R$) 6.25 7.19

Book Value (R$ mm) 1,717

( + ) Gafisa's Backlog (Stand- 705

Alone) (R$MM)

( x ) P/Adj. BV Multiple 1.2x 1.9x

( = ) Equity Value (Stand Alone) (R$ 2,832 4,660

MM)

( + ) 60% Backlog Tenda X Tenda's 415 477

comparables' multiple (R$ MM)

( = ) Equity Value (R$ MM) 3,248 5,137

Price per Share (R$) 24.92 39.42

Estimated Exchange Ratio: 0.182 to 0.251

37

|

|

Research Analysts' View

"In our view, this is positive as company should further boost its operational

scale as well as market liquidity. Furthermore, Gafisa will consolidate under

its umbrella a stake that it was already controlling, without paying any

premium (and paying with cash), and Tenda's shareholder will come to own a

stock of a large company, with much higher liquidity, without any dilution

penalty. " (October 22, 2009)

"We believe that this is negative news for Tenda's shareholders, due to the

fact that they will be migrated to a company with a higher financial and

operating risk, and with a growth potential lower than that of Tenda without

Gafisa. Our target prices for the companies (as reported yesterday), of R$ 8.51

for Tenda and R$ 33.80 for Gafisa, imply a more favorable exchange ratio for

Tenda's shares, which takes the fair ratio to 0.2518, in our opinion. "

(October 22, 2009)

"Although we view the move as positive from a strategic standpoint as, in our

opinion, it made little sense to keep two separate investment vehicles, we

believe the transaction should be neutral in terms of economic value. In our

view, the proposed ratio is fair, close to the market ratio, and values both

companies at similar P/BV ratios." (October 22, 2009

"We think the management of both companies would be more efficient with Tenda

100%-owned by Gafisa, as it reduces costs and conflicts in dealing with two

separate entities with different shareholders. The merger would also enhance

the exposure of Gafisa, the only builder with ADRs and the strongest share

liquidity in the sector, to the fastest growing housing market in Brazil. Our

Neutral rating and price target are unchanged. " (October 22, 2009)

38

|

|

[GRAPHIC]

EXHIBIT

Overview of the Selected Comparable Companies

39

|

|

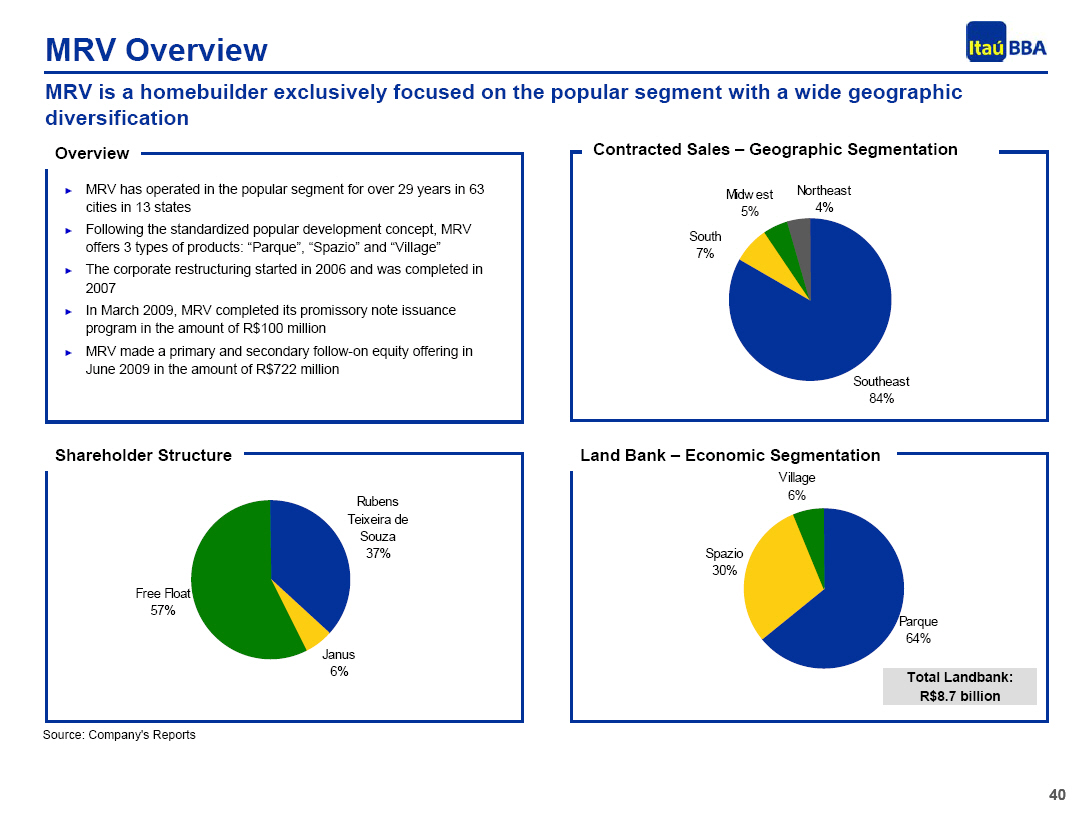

MRV Overview

MRV is a homebuilder exclusively focused on the popular segment with a wide

geographic diversification

Overview

MRV has operated in the popular segment for over 29 years in 63 cities in 13

states Following the standardized popular development concept, MRV offers 3

types of products: "Parque", "Spazio" and "Village" The corporate

restructuring started in 2006 and was completed in 2007 In March 2009, MRV

completed its promissory note issuance program in the amount of R$100 million

MRV made a primary and secondary follow-on equity offering in June 2009 in the

amount of R$722 million

Contracted Sales -- Geographic Segmentation

[GRAPHIC]

Shareholder Structure

[GRAPHIC]

Land Bank -- Economic Segmentation

[GRAPHIC]

40

|

|

PDG Realty Overview

PDG Realty is one of the largest homebuilders in the country, focused on the

popular segment

Overview

PDG Realty operates in the economic, medium, medium -high and high income

segments In April 2009, PDG completed its debenture issuance program in the

amount of R$276 million In August 2009, PDG closed its repurchase program and

carried out the cancellation of its treasury shares In September 2009, the

share split of PDG's capital stock was approved in the proportion of 1:2 PDG

made a primary and secondary follow-on equity offering in October 2009 in the

amount of R$941 million

Land Bank

[GRAPHIC]

Shareholder Structure

[GRAPHIC]

41

|

|

Cyrela Overview

Cyrela is the largest residential real estate developer in Brazil

Overview

Cyrela is the largest homebuilder in Brazil, with around 50 years of history

In 2006 the subsidiary Living was created to operate in the economic and

super-economic segments In September 2009, Cyrela sold the total of its

interest in the capital stock of Agra Additionally, the 3(rd) issuance of

debentures was approved in the total limit amount of R$350 million Cyrela made

a primary follow-on equity offering in October 2009 in the amount of R$1

billion

Land Bank

[GRAPHIC]

Shareholder Structure

[GRAPHIC]

42

|

|

Rossi Overview

Rossi has been present in the real estate sector for almost 30 years, with a

distinguished performance in all economic segments

Overview

Rossi is one of the oldest companies in this market, with over 29 years of

operations It has 4 product segments: High-End, Medium -High, Medium and

Economic In October 2008 the shareholders announced a capital increase of

R$150 million, at R$4.35 / share In May 2009 the company announced the release

of the brand Ideal for the economic segment, with launches aimed at the segment

with average income of up to 10 minimum salaries and average development price

of R$ 90,000 Rossi made a primary follow-on equity offering in October 2009 in

the amount of R$825 million

Shareholder Structure

[GRAPHIC]

Land Bank

[GRAPHIC]

Source: Company's Reports

43

|