UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22037

Stone Harbor Investment Funds

(Exact name of registrant as specified in charter)

31 West 52nd Street, 16th Floor

New York, NY 10019

(Address of principal executive offices) (Zip code)

Adam J. Shapiro, Esq.

c/o Stone Harbor Investment Partners LP

31 West 52nd Street, 16th Floor

New York, NY 10019

(Name and address of agent for service)

With copies To:

Michael G. Doherty, Esq.

Ropes & Gray LLP

1211 Avenue of the Americas

New York, NY 10036

Registrant’s telephone number, including area code: (866) 699-8125

Date of fiscal year end: May 31

Date of reporting period: May 31, 2021

Item 1. Report to Stockholders.

(a)

As permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website at www.shiplp.com and you will be notified by mail each time a report is posted and provided with a website link to access the report.

You may, notwithstanding the availability of shareholder reports online, elect to receive all future shareholder reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Funds, you can call 1.866.699.8125 to let the Funds know you wish to continue receiving paper copies of your shareholder reports.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by enrolling at www.shiplp.com.

Table of Contents

| Shareholder Letter | 2 |

| Disclosure of Fund Expenses | 7 |

| Summaries of Portfolio Holdings | 8 |

| Growth of $10,000 Investment | |

| Stone Harbor Emerging Markets Debt Fund | 11 |

| Stone Harbor High Yield Bond Fund | 12 |

| Stone Harbor Local Markets Fund | 13 |

| Stone Harbor Emerging Markets Corporate Debt Fund | 14 |

| Stone Harbor Strategic Income Fund | 15 |

| Stone Harbor Emerging Markets Debt Allocation Fund | 16 |

| Report of Independent Registered Public Accounting Firm | 17 |

| Statements of Investments | |

| Stone Harbor Emerging Markets Debt Fund | 18 |

| Stone Harbor High Yield Bond Fund | 34 |

| Stone Harbor Local Markets Fund | 42 |

| Stone Harbor Emerging Markets Corporate Debt Fund | 48 |

| Stone Harbor Strategic Income Fund | 54 |

| Stone Harbor Emerging Markets Debt Allocation Fund | 62 |

| Statements of Assets & Liabilities | 64 |

| Statements of Operations | 66 |

| Statements of Changes in Net Assets | 68 |

| Financial Highlights | |

| Stone Harbor Emerging Markets Debt Fund | 72 |

| Stone Harbor High Yield Bond Fund | 73 |

| Stone Harbor Local Markets Fund | 74 |

| Stone Harbor Emerging Markets Corporate Debt Fund | 75 |

| Stone Harbor Strategic Income Fund | 76 |

| Stone Harbor Emerging Markets Debt Allocation Fund | 77 |

| Notes to Financial Statements | 78 |

| Additional Information | 100 |

| Board Approval of Investment Advisory Agreement | 103 |

| Liquidity Risk Management Program | 105 |

| Trustees & Officers | 106 |

| Stone Harbor Investment Funds Annual Report | May 31, 2021 | 1 |

| Stone Harbor Investment Funds | Shareholder Letter |

May 31, 2021 (Unaudited)

Dear Shareholder,

The past twelve months ending May 31, 20211 have seen very strong returns for risk assets generally as economies and markets recovered from the initial shock of the Covid-19 pandemic. The S&P 500 Index returned 40.30%; this strong return was further reflected in results of the high yield markets with U.S. high yield bonds returning 15.09%, and European high yield bonds returning 12.30%. Emerging markets (“EM”) debt (as represented by the JP Morgan EMBI Global Diversified Index), while positive, lagged behind the performance of these markets, returning 10.50% over the past twelve months. Emerging markets local currency debt and hard currency corporate debt indices returned 8.15% and 10.74%, respectively. These results, in large part, reflected two considerations: firstly, the extra exposure to U.S. duration imbedded in the asset class, and secondly, the different Covid-19 experiences realized around the world. Credit spreads tightened significantly over the reporting period. U.S. high yield spreads narrowed some 321 basis points (“bps”), ending May at 345 bps. Investment grade corporate spreads narrowed 91 bps, ending the period at 84 bps. Emerging markets external sovereign debt spreads tightened 184 bps over the course of the past twelve months. European high yield spreads narrowed 283 bps, ending the period at 295 bps.

Longer duration assets were exposed to a sharp rise in Treasury yields with the benchmark U.S. 10-year Treasury yield rising to 1.60% from 0.65% a year ago. This move in yields was in response to not only the success of economic policy in supporting the U.S. economy and encouraging recovery, with the goods side of the economy running arguably over 10% above trend, but also reflected the market’s concerns regarding the extent of fiscal policy stimulus with a new administration in place. Furthermore, signs of inflationary pressures emerged as unlocking of the economy highlighted disruptions in supply chains. German 10-Year Bund yields ended May at -0.18%, recording a comparatively very modest rise of 26 bps, reflecting the slower return to normality in Europe as Covid-19 vaccinations lagged the U.S., and also a sense that inflation pressures are significantly less marked. The constraining impact of rising yields on return was evident in the U.S. Treasury market and in investment grade corporates which, while positive, only returned 4.11%.

In foreign exchange (“FX”) markets, the U.S. dollar depreciated and the U.S. Dollar Index (“DXY”; an index of the value of the U.S. dollar relative to a basket of foreign currencies) posted a return of -8.49%. With support for the dollar lacking compared to previous years, the Euro posted a strong gain of over 10%. Emerging market currencies saw more mixed performance with over a 10% rally in the Mexican Peso, a stand out positive, while the Russian ruble and Turkish lira posted notable declines.

The economic outlook going forward seems more certain than it has at any point over the last twelve months. The success of Covid-19 vaccination programs in the U.S. and UK have allowed significant unlocking and it is likely that further unlocking will not only see economies grow but also rebalance them back towards services from the goods sector. Europe has lagged the U.S. in its vaccination progress, but the current rate of progress is substantial and, combined with low case rates, we expect to see further unlocking. Indeed it is notable that the relative performance of purchasing managers index (“PMI”) readings as of late suggest that Europe is in the process of catching up. While the outlook for economic growth seems relatively encouraging, the outlook for monetary policy seems less certain than it has for some time. The cause of this uncertainty is very much focused on the issues of how high inflation will get and whether or not it will be transitory. The Federal Reserve (“Fed”) has already moved to indicate that rates will likely rise in 2023 compared to a previous expectation of 2024. The Federal Open Market Committee (“FOMC”) appears quite split on this issue with a number of members indicating that they expect rates to rise in 2022.

We remain optimistic about the prospects for emerging markets debt. Our view is based on several factors, including: 1) our expectation of continued above-trend growth supported by expanding vaccine supply; 2) commodity price strength that provides many resource-rich developing countries powerful fiscal support; 3) emerging markets’ lower current account balances that have reduced external vulnerabilities; and 4) proactive steps emerging markets central banks have taken to insure against the risk of rising inflation by hiking policy interest rates.

At Stone Harbor Investment Partners LP (“Stone Harbor”), we will continue to focus on seeking to capture excess return from stable and improving credit situations in corporate and sovereign markets worldwide. As we continue to monitor these developments, please follow our progress through the year by visiting our website at www.shiplp.com. There you will find updates on our view of credit markets, as well as related news and research. We appreciate the confidence you have placed in Stone Harbor and look forward to providing you with another update in the next six months.

| (1) | Total returns and spread figures are as of May 28, 2021, due to the U.S. holiday on May 31, 2021. |

| 2 | www.shiplp.com |

| Stone Harbor Investment Funds | Shareholder Letter |

May 31, 2021 (Unaudited)

Market Review: Emerging Markets Debt

The recovery in global financial markets, following the most disruptive months of the pandemic in early 2020, continued throughout the reporting period, and global growth accelerated particularly in the last six months ended May 31, 2021. Increasing Covid-19 vaccine supply and distribution in developed countries and the subsequent spillover into emerging countries provided vital support for economic growth. As economies reopened and economic activity improved, commodity prices strengthened in response to high demand and constrained supply. The increase in oil and commodity prices positively impacted resource-rich developing countries and provided significant fiscal support. Another important source of support for emerging markets was ongoing commitment by the International Monetary Fund (“IMF”), which made available nearly US$1 trillion in aid to help countries manage through the pandemic. Towards the end of the reporting period, the yield on the ten-year U.S. Treasury note increased as U.S. markets priced expectations for rising inflation and higher growth rates. Unlike central banks from advanced economies, many EM central banks began to hike policy interest rates from low levels, proactively insuring against the risk of rising inflation.

The JPMorgan EMBI Global Diversified spread over comparable maturity U.S. Treasury securities tightened 184 bps, ending the reporting period at a spread of 331 bps and returning 10.50%. The JPMorgan CEMBI Broad Diversified credit spread tightened 212 bps, ending the period at a spread of 253 bps and returning 10.74%. The JPMorgan GBI-EM Global Diversified returned 8.15% during the period. According to Emerging Portfolio Fund Research (“EPFR”), global, mutual funds and ETFs recorded over US$12.6 billion of inflows into EM hard currency sovereign funds and US$17.4 billion into local currency sovereign funds. Demand for yield, combined with EM fundamentals, we believe, will continue to be drivers of inflows into the asset class.

Stone Harbor Emerging Markets Debt Fund

The total return of the Stone Harbor Emerging Markets Debt Fund (the “Fund”) for the 12-month period ended May 31, 2021(1) was 15.31% (net of expenses) and 16.04% (gross of expenses). This performance compares to a benchmark return of 10.50% for the JPMorgan EMBI Global Diversified Index. The Fund outperformed its benchmark as a result of both country selection and issue selection. Off-benchmark exposure in hard currency corporate bonds, particularly in Brazil, Colombia, Ghana, and Mexico also enhanced performance. Duration-adjusted returns that are explained by U.S. Treasury movements were negative, as were miscellaneous differences that represent pricing differences, among other factors.

The top positive contributors to relative outperformance were overweights in Angola and Ecuador -- both oil exporting countries. In Angola, the government’s commitment to stabilize public finances through gains in revenue from improving economic growth and lower expenses from spending constraint has kept the country on track with its IMF program. The IMF approved a US$487.5 million disbursement in January following the fourth review of the IMF Extended Fund Facility (“EFF”). In addition, we believe Angola is likely to receive up to US$3.2 billion in debt relief in 2021 and another US$4 billion by the end of 2022 from China and other bilateral lenders. In Ecuador, despite the market’s fear that a populist with radical spending proposals would win the presidential election on 7 February, Ecuadorians ultimately elected a center-right conservative, Guillermo Lasso, who now faces a fragmented National Assembly. His victory improved the probability of achieving the goals of the recently approved 27 month, US$5 billion IMF EFF program. Other positive contributors to relative returns included overweight and issue selection in Mexico, and underweights in Peru, Poland, Russia, China, and Philippines.

The top detractors from relative returns included an overweight in Argentina and issue selection in Angola. Argentina’s bond prices fell to deeply depressed levels earlier this year on headlines that the country’s current Vice President (and former President) Cristina Fernandez de Kirchner and her allies wanted to delay negotiations with the IMF on a new lending program until after elections in the fall of 2021. We note that Argentina restructured approximately US$65 billion in its external sovereign debt last year and has only modest U.S. dollar coupon payments and amortizations due in the next two years. Current market pricing of the already-restructured debt is extreme, in our view, and recent news that Argentina has negotiated a payment plan for debt arrears with the Paris Club signals willingness to pay. An off-benchmark position in Angola floating rate debt underperformed fixed coupon benchmark securities.

The Fund uses various derivative instruments to implement its strategies. These derivatives may be utilized to attempt to manage the Fund’s credit risk, interest rate risk and foreign exchange risk. These derivative positions may increase or decrease the Fund’s exposure to these risks. At the end of the reporting period, the Fund had net market exposure to these derivatives of approximately $390,000. Over the course of the reporting period these derivative positions generated a net realized loss of approximately $10.3 million and $1.7 million in unrealized appreciation for a decrease in operations of $8.6 million. We plan to continue to utilize derivative instruments to implement our strategies related to credit risk, interest rate risk and foreign exchange risk.

Stone Harbor Local Markets Fund

The total return of the Stone Harbor Local Markets Fund (the “Fund”) for the 12-month period ended May 31, 2021(1) was 8.27% (net of expenses) and 9.28% (gross of expenses). This performance compares to a benchmark return of 8.15% for the JPMorgan GBI-EM Global Diversified. The Fund outperformed its benchmark as a result of both FX and duration positioning, as well as issue selection. Off-benchmark exposure in select U.S.-dollar denominated debt also enhanced performance. Miscellaneous differences that represent pricing differences, among other factors, were negative.

The top contributors to relative performance included Mexico (FX overweight, issue selection, and off-benchmark external sovereign debt), Thailand (FX and duration underweight), and South Africa (FX and duration overweight, issue selection). Mexico’s local bonds benefitted from the country’s close relationship with and proximity to the U.S. for trade and capital flows. The Fund’s exposure to U.S. dollar-denominated bonds of Pemex, Mexico’s state-owned oil company, outperformed, as the company benefitted from a recovery in oil prices and its bond spreads tightened, generating capital gains from higher oil prices. Peso-denominated exposure to America Movil, a telecommunications company, also enhanced performance. Banxico, Mexico’s central bank, provided a strong monetary policy anchor for domestic bond yields. The Fund’s exposure in South Africa enhanced relative returns as the rand appreciated and the average yield on local bonds fell. Thailand’s low-yielding currency and bond markets underperformed during the reporting period, allowing the Fund’s underweights in the country to generate excess returns. Other positive contributors to performance included Chile (duration underweight), Malaysia (FX and duration underweight), and Peru (FX underweight).

| Stone Harbor Investment Funds Annual Report | May 31, 2021 | 3 |

| Stone Harbor Investment Funds | Shareholder Letter |

May 31, 2021 (Unaudited)

Top detractors from relative returns were China (FX underweight, duration overweight, issue selection), Russia (FX and duration overweight, issue selection), and issue selection in Indonesia. China’s reminbi outperformed as the economy was the first to recover from the pandemic-driven downturn. Inflows from index-tracking investors also supported the reminbi following the inclusion of China’s local bond market in widely followed benchmarks. Domestic bond yields in China edged higher, counter to the trend in the broader market, as China’s central bank maintained its policy rate despite limited inflation pressure. The Fund’s positioning in Russia underperformed. Several factors weighed against Russian asset prices, including the country’s support for Armenia in geopolitical conflict with Azerbaijan and the ongoing case surrounding the poisoning and jailing of opposition leader Alexei Navalny. In Indonesia, local taxes, along with FX forwards detracted from excess returns. Exposure in Colombia (FX and duration overweight) also detracted from performance as local bond yields increased despite benign inflation.

The Fund uses various derivative instruments to implement its strategies. These derivatives may be utilized to attempt to manage the Fund’s credit risk, interest rate risk and foreign exchange risk. These derivative positions may increase or decrease the Fund’s exposure to these risks. At the end of the reporting period the Fund had net market exposure to these derivatives of approximately $351,000. Over the course of the reporting period, these derivative positions generated a net realized gain of approximately $368,000 and $516,000 in unrealized appreciation, for an increase in operations of $884,000. We plan to continue to utilize derivative instruments to implement our strategies related to credit risk, interest rate risk and foreign exchange risk.

Stone Harbor Emerging Markets Corporate Debt Fund

The total return of the Stone Harbor Emerging Markets Corporate Debt Fund (the “Fund”) for the 12-month period ended May 31, 2021(1) was 19.25% (net of expenses) and 20.26% (gross of expenses). This performance compares to a benchmark return of 10.74% for the JPMorgan CEMBI Broad Diversified Index. The index spread over comparable maturity U.S. Treasury securities tightened by 212 bps, ending the period at 253 bps. The high yield sub-sector outperformed, returning 16.63%, while the investment grade sub-sector returned 6.62%.

The Fund outperformed its benchmark due to issue selection decisions and country exposures. Overweight exposures in Argentina, Brazil, Colombia, Mexico, Ukraine, and Zambia, as well as an underweight exposure in South Korea enhanced performance during the reporting period. Argentinian assets were supported by higher oil prices and a comprehensive sovereign debt restructuring that suggested more clarity on regulatory regimes and the ability of corporates to refinance debt. Rising oil prices also helped boost bond prices of select oil and gas exploration and production companies, such as Colombia’s Geopark and Colombian-based independent oil and gas producer Gran Tierra. The company’s management team used proceeds from an asset sale to reduce debt and expects to generate significant free cash flow during 2021 to further reduce leverage. In Mexico, after defaulting in 2020 as a result of sharply lower air travel during the pandemic, Aero Mexico’s bonds rebounded during the first half of 2021 as the company worked through its U.S. bankruptcy filing. The judicial process is expected to culminate sometime later this year. Benefiting from the same theme of accelerating global recovery and air travel, the Fund’s exposure to Brazil’s GOL also enhanced performance as airlines rallied in the latter half of the reporting period. The recovery in prices of metals, including copper and iron ore, supported the outperformance of bonds of producers such as Metinvest (Ukraine) and First Quantum (Zambia/Panama).

Positive issue selection in Brazil, Colombia, Mexico, Peru, Saudi Arabia, South Africa, UAE, China, Hong Kong, and India contributed to relative returns.

From an industry perspective, overweights and issue selection in airlines, exploration & production, and metals/mining/steel contributed most to relative performance. These were industries that suffered the steepest decline during the initial phase of the Covid-19 pandemic and as oil prices dropped dramatically in the first quarter of 2020, but then rallied significantly as the economy began to reopen and restrictions eased. Issue selection in electric, as well as an underweight exposure and issue selection in financial/lease contributed positively to excess returns.

Attribution from credit rating was also positive, with overweights and issue selection in non-investment grade credits (B and CCC-rated), and underweights in investment grade credits (A and BBB-rated) contributing to excess returns.

Stone Harbor Emerging Markets Debt Allocation Fund

The total return of the Stone Harbor Emerging Markets Debt Allocation Fund (the “Fund”) for the 12-month period ended May 31, 2021(1) was 12.26% (net of direct and indirect expenses) and 13.11% (gross of direct and indirect expenses). This compares to a blended benchmark (50% JPMorgan EMBI Global Diversified Index / 50% JPMorgan GBI-EM Global Diversified Index) return of 9.34%.

The Fund outperformed its benchmark primarily as a result of country selection and issue selection in external sovereign debt. The portfolio’s allocation to local currency debt allocation and off-benchmark exposure in hard currency corporate bonds also enhanced excess returns. Duration-adjusted returns that are explained by U.S. Treasury movements were negative, as were miscellaneous differences that represent pricing differences, among other factors.

Asset allocation decisions contributed positively to relative performance. At the start of the reporting period, the Fund’s asset allocation favored hard currency assets given the persistent price dislocation in many countries’ sovereign bond markets. Following strong performance in the second quarter of 2020, we began reducing exposure to U.S. dollar-denominated sovereign assets, replacing them with high-quality corporate credits with relative value compared to sovereign debt, as well as local currency debt. In August and early September, we added to the Fund’s exposure in local currency debt, further increasing the exposure in January and maintaining the overweight through the end of the reporting period.

| 4 | www.shiplp.com |

| Stone Harbor Investment Funds | Shareholder Letter |

May 31, 2021 (Unaudited)

In hard currency sovereign debt, the top positive contributors to relative outperformance were overweights in Angola and Ecuador -- both oil exporting countries. In Angola, the government’s commitment to stabilize public finances through gains in revenue from improving economic growth and lower expenses from spending constraint has kept the country on track with its IMF program. The IMF approved a US$487.5 million disbursement in January following the fourth review of the IMF Extended Fund Facility (“EFF”). In addition, Angola is likely to receive up to US$3.2 billion in debt relief in 2021 and another US$4 billion by the end of 2022 from China and other bilateral lenders. In Ecuador, despite the market’s fear that a populist with radical spending proposals would win the presidential election on 7 February, Ecuadorians ultimately elected a center-right conservative, Guillermo Lasso. His victory improved the probability of achieving the goals of the recently approved 27-month, US$5 billion IMF EFF program. Other positive contributors to relative returns included overweight and issue selection in El Salvador, Mexico, and underweights in China, Peru, Philippines, Poland, and Russia.

In local currency debt, the top contributors to relative performance included overweight exposures in Mexico and South Africa, and underweight exposures in Peru and Turkey. Mexico’s local bonds benefitted from the country’s close relationship with and proximity to the U.S. for trade and capital flows. The Fund’s exposure to U.S. dollar-denominated bonds of Pemex, Mexico’s state-owned oil company, outperformed, as the company benefitted from a recovery in oil prices and its bond spreads tightened, generating capital gains. Peso-denominated exposure to America Movil, a telecommunications company, also enhanced performance. Banxico, Mexico’s central bank, provided a strong monetary policy anchor for domestic bond yields. The Fund’s exposure in South Africa enhanced relative returns as the rand appreciated and the average yield on local bonds fell.

Off-benchmark exposures to U.S. dollar-denominated corporate debt, particularly in Brazil, Colombia, Ghana, Mexico, and Ukraine, also contributed positively to performance.

Top detractors from relative returns in external sovereign debt included an overweight in Argentina and issue selection in Angola. Argentina’s bond prices fell to deeply depressed levels earlier this year on headlines that the country’s current Vice President (and former President) Cristina Fernandez de Kirchner and her allies wanted to delay negotiations with the IMF on a new lending program until after elections in the fall of 2021. We note that Argentina restructured approximately US$65 billion in its external sovereign debt last year and has only modest U.S. dollar coupon payments and amortizations due in the next two years. Current market pricing of the already-restructured debt is extreme, in our view, and recent news that Argentina has negotiated a payment plan for debt arrears with the Paris Club signals willingness to pay. An off-benchmark position in Angola floating rate debt underperformed fixed coupon benchmark securities.

In local currency debt, the top detractors from relative returns were overweight exposures in Colombia, where local bond yields increased despite benign inflation and the Colombian peso depreciated against the U.S. dollar. Interestingly, and we believe very important, Colombia is one of the few EM countries that has qualified for a Flexible Credit Line (“FCL”) with the IMF. The FCL, which requires the qualifying country to have very strong economic fundamentals and institutional policy frameworks, and a strong track record of implementing those policies comes with additional IMF support. In September 2020, the IMF increased Colombia’s access to IMF resources by approximately US$17.6 billion via the FCL. We continue to believe that Colombian policy-makers, in conjunction with the IMF’s technical advisors, are on the correct fiscal path and have maintained our position in Colombia’s local debt market.

The Fund uses various derivative instruments to implement its strategies. These derivatives are utilized to attempt to manage the Fund’s credit risk, interest rate risk and foreign exchange risk. These derivative positions may increase or decrease the Fund’s exposure to these risks. At the end of the reporting period the Fund had net market exposure to these derivatives of approximately $11,000. Over the course of the reporting period, these derivative positions generated a net realized gain of $21,000 and $4,000 in unrealized depreciation, for an increase in operations of approximately $17,000. We plan to continue to utilize derivative instruments to implement our strategies related to credit risk, interest rate risk and foreign exchange risk.

Stone Harbor High Yield Bond Fund

The total return of the Stone Harbor High Yield Bond Fund (the “Fund”) for the 12-month period ended May 31, 20211 was 13.19% (net of expenses) and 13.86% (gross of expenses). This compares to a benchmark return of 15.09% for the ICE BofA U.S. High Yield Constrained Index.

The high yield market posted considerable gains early in the reporting period as strong fiscal and monetary support spurred a quicker than expected rebound from the March lows, resulting in the economy and corporate profits outperforming expectations. Additionally, optimism for a Covid-19 vaccine and strong retail inflows contributed to the market recovery. Leading up to the U.S. elections in early November, the market fluctuated as positive events and sentiment mixed with rising virus cases, renewed lockdown restrictions, the absence of additional fiscal stimulus, and a heavy primary calendar as companies sought to boost liquidity or refinance to lower rates. The market resumed its strong recovery in November as election uncertainty gave way to a divided government and positive vaccine news. In 2021, the high yield market continues to perform well, despite a record-setting pace in the primary market, due to continued fiscal and monetary support and the reopening of the economy as vaccination rates improved. This resulted in a strong economic rebound, better than expected corporate profits, improving ratings trends, low levels of distressed debt, and a sharply lower default rate. Lower quality bonds outperformed during the period as bonds that suffered the steepest decline in early 2020 rallied significantly as the economy recovered and restrictions eased; nonetheless, stabilizing interest rates later in the reporting period led to a recovery in longer duration, higher quality credits. The recovery in commodity prices caused energy credits to outperform, and the global economic recovery contributed to a recovery in transportation and leisure-related industries.

| Stone Harbor Investment Funds Annual Report | May 31, 2021 | 5 |

| Stone Harbor Investment Funds | Shareholder Letter |

May 31, 2021 (Unaudited)

The Fund’s more defensive positioning in certain industries led to underperformance relative to the benchmark due to negative issue and industry selection. Negative security selection decisions in drillers and healthcare offset positive contributions from credit selection in exploration & production (“E&P”) and leisure. The underperformance in drillers came from avoiding the most distressed companies that do not generate free cash flow. Healthcare was negatively impacted by events in ongoing opioid litigation. E&P benefitted from an overweight to higher yielding energy bonds that outperformed with the oil prices rebound and an overweight position in cruise lines contributed positively in leisure. In industry selection decisions, underweights to retail and metals/mining and an overweight in building products and cable detracted the most from performance. This result was partially offset by an overweight in aerospace and an underweight in technology. From a credit quality perspective, an underweight in CCC-rated bonds and CCC-rated issue selection detracted from performance, while an underweight in BB-rated bonds enhanced positive performance.

Stone Harbor Strategic Income Fund

The total return of the Strategic Income Fund (the “Fund”) for the 12-month period ended May 31, 20211 was 10.05% (net of direct and indirect expenses) and 10.75% (gross of direct and indirect expenses). This performance compares to a benchmark return of 5.38% for the Bloomberg Barclays Global Credit Index (Hedged USD).

The Fund outperformed its benchmark as a result of certain asset allocation, duration, and individual credit decisions. The Fund’s duration positioning (short relative to the benchmark) generated a positive contribution during the period as developed market government rates moved higher, led by the U.S. 10-year Treasury yield rising 100 bps. The Fund’s broad asset allocation decisions were also a positive contributor taken as a whole. More than 100 basis points of excess return came from allocation decisions related to the Fund’s positioning in global high yield sectors. Within individual portfolio sectors, the Fund experienced outperformance in all major market segments with the exception of U.S. high yield corporates. Within investment grade, an overweight to corporate bonds led to incremental outperformance of approximately 100 basis points. In emerging markets hard currency debt, country overweights to Angola and Ecuador generated the largest positive contributions. Within emerging markets corporate debt, exposure to Columbian issuers was the largest single positive contributor. For the emerging markets local currency debt sector, both the foreign exchange and duration components provided relative outperformance.

The reporting period saw very strong returns for risk assets generally as economies and markets recovered from the initial shock of the Covid-19 pandemic. These strong results were reflected in results of the high yield markets with U.S. high yield bonds returning 15.09%, and European high yield bonds returning 12.30%. Credit spreads tightened significantly over the reporting period, with U.S. high yield spreads narrowing some 321 bps, ending May at 345 bps. Investment grade corporate spreads narrowed 91 bps, ending the period at 84 bps. European high yield spreads narrowed 283 bps, ending the period at 295 bps. As noted above, longer duration assets were exposed to a sharp rise in Treasury yields in response to not only the success of economic policy in supporting the U.S. economy and encouraging recovery, with the goods side of the economy running arguably over 10% above trend, but also reflected the market’s concerns regarding the extent of fiscal policy stimulus with a new administration in place.

The Fund uses various derivative instruments to implement its strategies. These derivatives are utilized to attempt to manage the Fund’s credit risk, interest rate risk and foreign exchange risk. These derivative positions may increase or decrease the Fund’s exposure to these risks. At the end of the reporting period the Fund had net market exposure of approximately $341,000 to these derivatives. Over the course of the reporting period, these derivative positions generated a net realized gain of $123,000 and $65,000 in unrealized appreciation, for an increase in operations of approximately $188,000. We plan to continue to utilize derivative instruments to implement our strategies related to credit risk, interest rate risk and foreign exchange risk.

Sincerely,

Peter J. Wilby, CFA

President and Chief Executive Officer

| (1) | Total returns and spread figures are as of May 28, 2021, due to the U.S. holiday on May 31, 2021. |

| 6 | www.shiplp.com |

| Stone Harbor Investment Funds | Disclosure of Fund Expenses |

May 31, 2021 (Unaudited)

Example. As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and/or redemption fees (if applicable) and (2) ongoing costs, including management fees and other Fund expenses. The below examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on December 1, 2020 and held until May 31, 2021.

Actual Expenses. The first table below provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in a Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect transactional costs, such as redemption fees, sales charges (loads) or exchange fees. Therefore, the second table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

BASED ON ACTUAL TOTAL RETURN

| Actual Total Return | Beginning Account Value December 1, 2020 | Ending Account Value May 31, 2021 | Expense Ratio(1) | Expenses Paid During Period(2) | |

| STONE HARBOR EMERGING MARKETS DEBT FUND | 1.20% | $ 1,000.00 | $ 1,012.00 | 0.73% | $ 3.66 |

| STONE HARBOR HIGH YIELD BOND FUND | 3.37 | 1,000.00 | 1,033.70 | 0.66 | 3.35 |

| STONE HARBOR LOCAL MARKETS FUND | 1.12 | 1,000.00 | 1,011.20 | 1.02 | 5.11 |

| STONE HARBOR EMERGING MARKETS CORPORATE DEBT FUND | 4.32 | 1,000.00 | 1,043.20 | 1.01 | 5.14 |

| STONE HARBOR STRATEGIC INCOME FUND | 1.97 | 1,000.00 | 1,019.70 | 0.09(3) | 0.45 |

| STONE HARBOR EMERGING MARKETS DEBT ALLOCATION FUND | 1.21 | 1,000.00 | 1,012.10 | 0.04(3) | 0.20 |

BASED ON HYPOTHETICAL TOTAL RETURN

| Hypothetical Annualized Total Return | Beginning Account Value December 1, 2020 | Ending Account Value May 31, 2021 | Expense Ratio(1) | Expenses Paid During Period(2) | |

| STONE HARBOR EMERGING MARKETS DEBT FUND | 5.00% | $ 1,000.00 | $ 1,021.29 | 0.73% | $ 3.68 |

| STONE HARBOR HIGH YIELD BOND FUND | 5.00 | 1,000.00 | 1,021.64 | 0.66 | 3.33 |

| STONE HARBOR LOCAL MARKETS FUND | 5.00 | 1,000.00 | 1,019.85 | 1.02 | 5.14 |

| STONE HARBOR EMERGING MARKETS CORPORATE DEBT FUND | 5.00 | 1,000.00 | 1,019.90 | 1.01 | 5.09 |

| STONE HARBOR STRATEGIC INCOME FUND | 5.00 | 1,000.00 | 1,024.48 | 0.09(3) | 0.45 |

| STONE HARBOR EMERGING MARKETS DEBT ALLOCATION FUND | 5.00 | 1,000.00 | 1,024.73 | 0.04(3) | 0.20 |

| (1) | Annualized, based on the Fund's most recent fiscal half-year expenses. |

| (2) | Expenses are equal to the Fund's annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (182), divided by 365. Note this expense example is typically based on a six-month period. |

| (3) | Ratio does not include expenses of the mutual funds held in the investment portfolio. |

| Stone Harbor Investment Funds Annual Report | May 31, 2021 | 7 |

| Stone Harbor Investment Funds | Summaries of Portfolio Holdings |

May 31, 2021 (Unaudited)

| STONE HARBOR EMERGING MARKETS DEBT FUND | |

| Country Breakdown(1) | % |

| Mexico | 6.30% |

| Colombia | 4.30% |

| Brazil | 4.17% |

| Russia | 3.48% |

| Qatar | 3.43% |

| Indonesia | 3.34% |

| Turkey | 3.29% |

| Argentina | 3.16% |

| United Arab Emirates | 3.10% |

| Panama | 2.98% |

| Malaysia | 2.77% |

| Saudi Arabia | 2.76% |

| Egypt | 2.66% |

| Dominican Republic | 2.61% |

| Oman | 2.55% |

| Peru | 2.52% |

| Ukraine | 2.49% |

| Bahrain | 2.48% |

| Kazakhstan | 2.41% |

| Ghana | 2.28% |

| Chile | 2.16% |

| South Africa | 2.16% |

| Angola | 2.15% |

| Philippines | 2.03% |

| Ecuador | 1.76% |

| Belarus | 1.64% |

| Nigeria | 1.64% |

| Romania | 1.44% |

| Uruguay | 1.27% |

| Sri Lanka | 1.18% |

| Zambia | 0.97% |

| El Salvador | 0.92% |

| Kenya | 0.88% |

| Pakistan | 0.86% |

| Iraq | 0.83% |

| Guatemala | 0.79% |

| Costa Rica | 0.76% |

| Mozambique | 0.73% |

| Morocco | 0.70% |

| Jordan | 0.64% |

| Benin | 0.63% |

| China | 0.59% |

| Tunisia | 0.56% |

| Ivory Coast | 0.48% |

| Venezuela | 0.45% |

| Trinidad & Tobago | 0.43% |

| Senegal | 0.42% |

| Azerbaijan | 0.38% |

| Israel | 0.38% |

| Lebanon | 0.33% |

| Gabon | 0.32% |

| Bahamas | 0.25% |

| Honduras | 0.21% |

| Georgia | 0.17% |

| Uzbekistan | 0.16% |

| Macau | 0.15% |

| Armenia | 0.14% |

| Vietnam | 0.14% |

| Cameroon | 0.10% |

| Papua New Guinea | 0.10% |

| Ethiopia | 0.09% |

| India | 0.09% |

| Total | 95.16% |

| Short Term Investments | 3.51% |

| Other Assets in Excess of Liabilities | 1.33% |

| Total Net Assets | 100.00% |

| STONE HARBOR LOCAL MARKETS FUND | |

| Country Breakdown(1) | % |

| China | 11.40% |

| Indonesia | 11.27% |

| Mexico | 11.06% |

| South Africa | 10.93% |

| Russia | 8.39% |

| Brazil | 6.64% |

| Colombia | 6.51% |

| Poland | 5.36% |

| Malaysia | 3.98% |

| Czech Republic | 3.68% |

| Romania | 3.07% |

| Thailand | 2.66% |

| Peru | 1.87% |

| Turkey | 1.72% |

| Chile | 1.67% |

| Egypt | 0.89% |

| Uruguay | 0.59% |

| Kazakhstan | 0.17% |

| Total | 91.86% |

| Short Term Investments | 1.19% |

| Other Assets in Excess of Liabilities | 6.95% |

| Total Net Assets | 100.00% |

| (1) | Country refers to country of primary risk exposure, as determined by Stone Harbor. In certain instances, a security’s country of incorporation may be different from its country of risk. |

| 8 | www.shiplp.com |

| Stone Harbor Investment Funds | Summaries of Portfolio Holdings |

May 31, 2021 (Unaudited)

| STONE HARBOR HIGH YIELD BOND FUND | |

| Industry Breakdown | % |

| Exploration & Production | 10.11% |

| Healthcare | 8.27% |

| Media Cable | 7.90% |

| Media Other | 6.26% |

| Gas Pipelines | 5.66% |

| Automotive | 5.46% |

| Building Products | 5.20% |

| Gaming | 4.44% |

| Electric | 3.43% |

| Leisure | 3.38% |

| Food and Beverage | 3.05% |

| Pharmaceuticals | 2.95% |

| Services Other | 2.63% |

| Chemicals | 2.59% |

| Aerospace/Defense | 2.45% |

| Industrial Other | 2.19% |

| Home Builders | 2.07% |

| Airlines | 2.05% |

| Satellite | 1.80% |

| Wirelines | 1.72% |

| Technology | 1.67% |

| Property & Casualty Insurance | 1.57% |

| Financial Other | 1.31% |

| Containers/Packaging | 1.18% |

| Pipelines | 1.16% |

| Drillers/Services | 1.06% |

| Consumer Products | 1.05% |

| Retail Food/Drug | 1.00% |

| Life | 0.93% |

| Wireless | 0.74% |

| Retail Non Food/Drug | 0.71% |

| Computers | 0.70% |

| Environmental Services | 0.59% |

| Diversified Manufacturing | 0.55% |

| Restaurants | 0.46% |

| Paper/Forest Products | 0.41% |

| Total | 98.70% |

| Short Term Investments | 1.85% |

| Other Liabilities in Excess of Other Assets | -0.55% |

| Total Net Assets | 100.00% |

| STONE HARBOR EMERGING MARKETS CORPORATE DEBT FUND | |

| Industry Breakdown | % |

| Electric | 12.75% |

| Oil & Gas | 10.73% |

| Telecommunications | 7.88% |

| Banks | 7.25% |

| Real Estate | 6.07% |

| Exploration & Production | 4.30% |

| Mining | 3.77% |

| Lodging | 3.61% |

| Industrial Other | 3.15% |

| Iron/Steel | 2.82% |

| Financial/Lease | 2.74% |

| Commercial Services | 2.42% |

| Pharmaceuticals | 2.32% |

| Pipelines | 2.15% |

| Airlines | 2.02% |

| Gas | 1.99% |

| Engineering & Construction | 1.77% |

| Metals/Mining/Steel | 1.75% |

| Media | 1.40% |

| Food | 1.38% |

| Energy-Alternate Sources | 1.30% |

| Wirelines | 1.20% |

| Transportation | 1.03% |

| Investment Companies | 0.98% |

| Metal Fabricate/Hardware | 0.96% |

| Forest Products & Paper | 0.93% |

| Gas Distributors | 0.87% |

| Packaging & Containers | 0.86% |

| Retail | 0.67% |

| Internet | 0.66% |

| Multi-National | 0.48% |

| Technology | 0.44% |

| Wireless | 0.44% |

| Food/Bev/Tobacco | 0.43% |

| Auto Parts & Equipment | 0.34% |

| Oil & Gas Services | 0.32% |

| Coal | 0.19% |

| Chemicals | 0.17% |

| Total | 94.54% |

| Short Term Investments | 5.18% |

| Other Assets in Excess of Liabilities | 0.28% |

| Total Net Assets | 100.00% |

| Stone Harbor Investment Funds Annual Report | May 31, 2021 | 9 |

| Stone Harbor Investment Funds | Summaries of Portfolio Holdings |

| May 31, 2021 (Unaudited) |

| STONE HARBOR STRATEGIC INCOME FUND | |

| Industry Breakdown | % |

| Government Entity | 14.33% |

| Banking | 3.55% |

| Financial Other | 1.61% |

| Electric | 1.29% |

| Gas Pipelines | 1.07% |

| Technology | 0.97% |

| Real Estate Investment Trust (REITs) | 0.83% |

| Healthcare | 0.62% |

| Wirelines | 0.62% |

| Automotive | 0.51% |

| Services Other | 0.46% |

| Chemicals | 0.36% |

| Gas Distributors | 0.36% |

| Wireless | 0.35% |

| Exploration & Production | 0.32% |

| Media Cable | 0.28% |

| Lodging | 0.25% |

| Aerospace/Defense | 0.24% |

| Refining | 0.24% |

| Building Products | 0.19% |

| Restaurants | 0.19% |

| Metals/Mining/Steel | 0.18% |

| Transportation Non Air/Rail | 0.18% |

| Gaming | 0.17% |

| Non Captive Finance | 0.17% |

| Pharmaceuticals | 0.17% |

| Construction Machinery | 0.16% |

| Diversified Manufacturing | 0.16% |

| Environmental Services | 0.16% |

| Industrial Other | 0.16% |

| Food And Beverage | 0.15% |

| Property & Casualty Insurance | 0.15% |

| Retail Non Food/Drug | 0.15% |

| Non Corporate | 0.14% |

| Media Other | 0.09% |

| Consumer Products | 0.08% |

| Affiliated Funds | 62.27% |

| Total | 93.18% |

| Short Term Investments | 13.86% |

| Other Liabilities in Excess of Assets | -7.04% |

| Total Net Assets | 100.00% |

| STONE HARBOR EMERGING MARKETS DEBT ALLOCATION FUND | |

| Fund of Fund Breakdown | % |

| Stone Harbor Local Markets Fund | 52.08% |

| Stone Harbor Emerging Markets Debt Fund | 47.17% |

| Short Term Investments | 1.00% |

| Other Liabilities in excess of Assets | -0.25% |

| Total Net Assets | 100.00% |

| 10 | www.shiplp.com |

| Stone Harbor Investment Funds | Growth of $10,000 Investment |

May 31, 2021 (Unaudited)

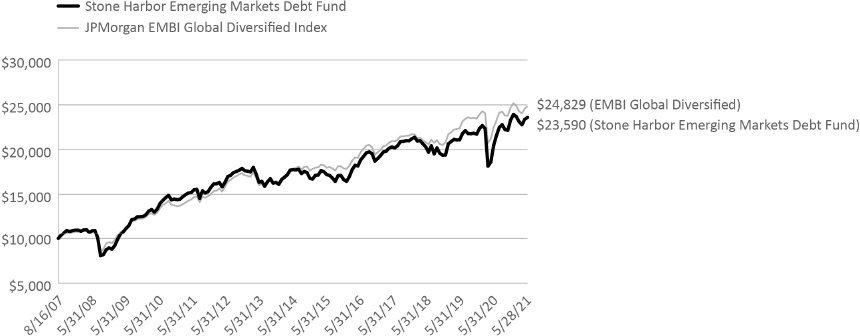

STONE HARBOR EMERGING MARKETS DEBT FUND

Comparison of Change in Value of $10,000 Investment in Stone Harbor Emerging Markets Debt Fund and the JPMorgan Emerging Markets Bond Index Global Diversified (JPMorgan EMBI Global Diversified Index). Please refer to the Additional Information section for detailed benchmark descriptions.

Total Returns (Inception Date, August 16, 2007)*

| Average Annual Return | |||||

| 1 Year | 3 Year | 5 Year | 10 Year | Since Inception | |

| Stone Harbor Emerging Markets Debt Fund | 15.31% | 5.10% | 5.35% | 4.53% | 6.42% |

| JPMorgan EMBI Global Diversified Index | 10.50% | 6.02% | 5.40% | 5.67% | 6.82% |

| * | As of 5/28/2021 |

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance quoted. Average annual total returns reflect the reinvestment of dividends and capital gains distributions and include all fee waivers and expense reimbursements. Without the fee waivers and expense reimbursements, total return figures would have been lower. The performance data quoted does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Index returns do not include the effects of sales charges, management fees and fund expenses or transaction costs. It is not possible to invest directly in an index.

| Stone Harbor Investment Funds Annual Report | May 31, 2021 | 11 |

| Stone Harbor Investment Funds | Growth of $10,000 Investment |

May 31, 2021 (Unaudited)

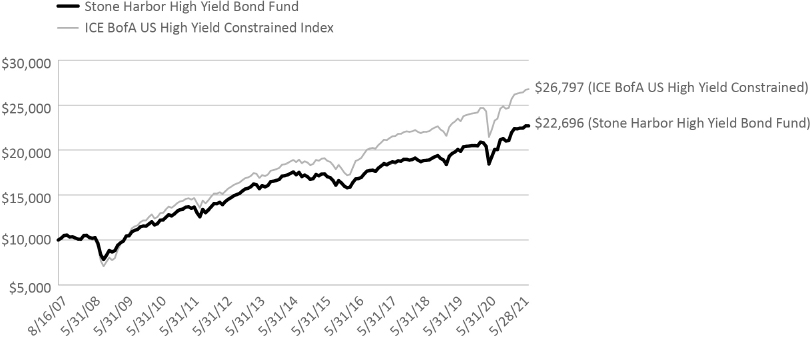

STONE HARBOR HIGH YIELD BOND FUND

Comparison of Change in Value of $10,000 Investment in Stone Harbor High Yield Bond Fund and the ICE BofAML US High Yield Constrained Index. Please refer to the Additional Information section for detailed benchmark descriptions.

Total Returns (Inception Date, August 16, 2007)*

| Average Annual Return | |||||

| 1 Year | 3 Year | 5 Year | 10 Year | Since Inception | |

| Stone Harbor High Yield Bond Fund | 13.19% | 6.39% | 6.15% | 5.19% | 6.12% |

| ICE BofA US High Yield Constrained Index | 15.09% | 6.76% | 7.22% | 6.24% | 7.41% |

| * | As of 5/28/2021 |

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance quoted. Average annual total returns reflect the reinvestment of dividends and capital gains distributions and include all fee waivers and expense reimbursements. Without the fee waivers and expense reimbursements, total return figures would have been lower. The performance data quoted does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Index returns do not include the effects of sales charges, management fees and fund expenses or transaction costs. It is not possible to invest directly in an index.

| 12 | www.shiplp.com |

| Stone Harbor Investment Funds | Growth of $10,000 Investment |

May 31, 2021 (Unaudited)

STONE HARBOR LOCAL MARKETS FUND

Comparison of Change in Value of $10,000 Investment in Stone Harbor Local Markets Fund and the JPMorgan Global Bond Index – Emerging Markets Global Diversified (JPMorgan GBI-EM Global Diversified Index). Please refer to the Additional Information section for detailed benchmark descriptions.

Total Returns (Inception Date, June 30, 2010)*

| Average Annual Return | |||||

| 1 Year | 3 Year | 5 Year | 10 Year | Since Inception | |

| Stone Harbor Local Markets Fund | 8.27% | 1.99% | 3.55% | -0.84% | 0.65% |

| JPMorgan GBI-EM Global Diversified Index | 8.15% | 3.47% | 4.65% | 0.62% | 2.19% |

| * | As of 5/28/2021 |

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance quoted. Average annual total returns reflect the reinvestment of dividends and capital gains distributions and include all fee waivers and expense reimbursements. Without the fee waivers and expense reimbursements, total return figures would have been lower. The performance data quoted does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Index returns do not include the effects of sales charges, management fees and fund expenses or transaction costs. It is not possible to invest directly in an index.

| Stone Harbor Investment Funds Annual Report | May 31, 2021 | 13 |

| Stone Harbor Investment Funds | Growth of $10,000 Investment |

May 31, 2021 (Unaudited)

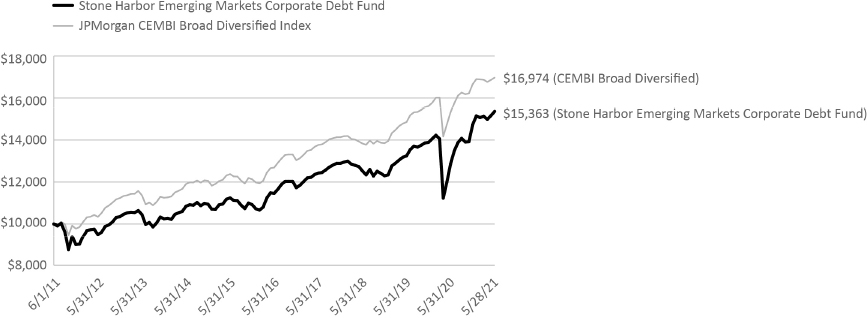

STONE HARBOR EMERGING MARKETS CORPORATE DEBT FUND

Comparison of Change in Value of $10,000 Investment in Stone Harbor Emerging Market Corporate Debt Fund and the JPMorgan Corporate Emerging Market Bond Index – Broad Diversified (JPMorgan CEMBI Broad Diversified Index). Please refer to the Additional Information section for detailed benchmark descriptions.

Total Returns (Inception Date, June 1, 2011)*

| Average Annual Return | ||||

| 1 Year | 3 Year | 5 Year | Since Inception | |

| Stone Harbor Emerging Markets Corporate Debt Fund | 19.25% | 7.04% | 6.04% | 4.39% |

| JPMorgan CEMBI Broad Diversified Index | 10.74% | 7.06% | 5.99% | 5.43% |

| * | As of 5/28/2021 |

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance quoted. Average annual total returns reflect the reinvestment of dividends and capital gains distributions and include all fee waivers and expense reimbursements. Without the fee waivers and expense reimbursements, total return figures would have been lower. The performance data quoted does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Index returns do not include the effects of sales charges, management fees and fund expenses or transaction costs. It is not possible to invest directly in an index.

| 14 | www.shiplp.com |

| Stone Harbor Investment Funds | Growth of $10,000 Investment |

May 31, 2021 (Unaudited)

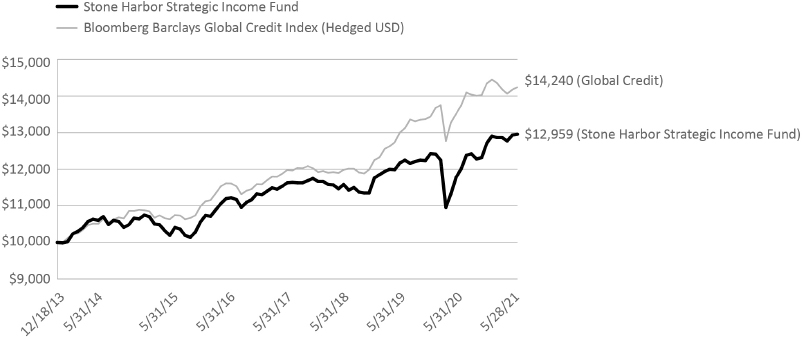

STONE HARBOR STRATEGIC INCOME FUND

Comparison of Change in Value of $10,000 Investment in Stone Harbor Strategic Income Fund and the Bloomberg Barclays Global Credit Index (Hedged USD). Please refer to the Additional Information section for detailed benchmark descriptions.

Total Returns (Inception Date, December 18, 2013)*

| Average Annual Return | ||||

| 1 Year | 3 Year | 5 Year | Since Inception | |

| Stone Harbor Strategic Income Fund | 10.05% | 3.85% | 3.88% | 3.54% |

| Bloomberg Barclays Global Credit Index (Hedged USD) | 5.38% | 6.11% | 5.01% | 4.86% |

| * | As of 5/28/2021 |

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance quoted. Average annual total returns reflect the reinvestment of dividends and capital gains distributions and include all fee waivers and expense reimbursements. Without the fee waivers and expense reimbursements, total return figures would have been lower. The performance data quoted does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Index returns do not include the effects of sales charges, management fees and fund expenses or transaction costs. It is not possible to invest directly in an index.

| Stone Harbor Investment Funds Annual Report | May 31, 2021 | 15 |

| Stone Harbor Investment Funds | Growth of $10,000 Investment |

May 31, 2021 (Unaudited)

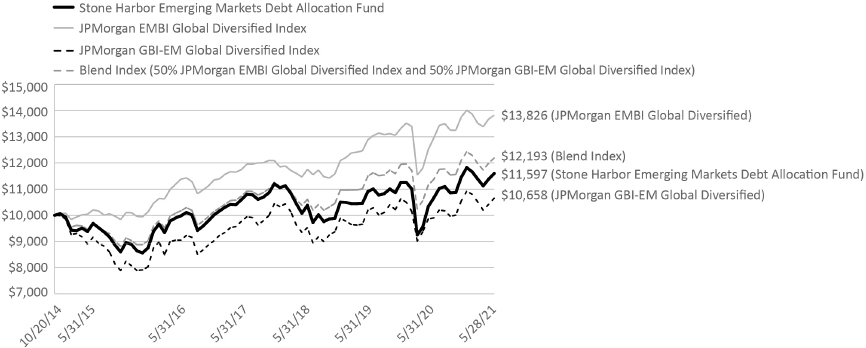

STONE HARBOR EMERGING MARKETS DEBT ALLOCATION FUND

Comparison of Change in Value of $10,000 Investment in Stone Harbor Emerging Markets Debt Allocation Fund, the JPMorgan EMBI Global Diversified Index, JPMorgan GBI-EM Global Diversified Index and the Blend Index (50% JPMorgan EMBI Global Diversified Index and 50% JPMorgan GBI-EM Global Diversified Index). Please refer to the Additional Information section for detailed benchmark descriptions.

Total Returns (Inception Date, October 20, 2014)*

| Average Annual Return | ||||

| 1 Year | 3 Year | 5 Year | Since Inception | |

| Stone Harbor Emerging Markets Debt Allocation Fund | 12.26% | 3.58% | 4.43% | 2.27% |

| JPMorgan EMBI Global Diversified Index | 10.50% | 6.02% | 5.40% | 5.02% |

| JPMorgan GBI-EM Global Diversified Index | 8.15% | 3.47% | 4.65% | 0.97% |

| Blend Index (50% JPMorgan EMBI Global Diversified Index and 50% JPMorgan GBI-EM Global Diversified Index) | 9.34% | 4.80% | 5.09% | 3.05% |

| * | As of 5/28/2021 |

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance quoted. Average annual total returns reflect the reinvestment of dividends and capital gains distributions and include all fee waivers and expense reimbursements. Without the fee waivers and expense reimbursements, total return figures would have been lower. The performance data quoted does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment return and principal value will vary, and shares, when redeemed, may be worth more or less than their original cost. Index returns do not include the effects of sales charges, management fees and fund expenses or transaction costs. It is not possible to invest directly in an index.

| 16 | www.shiplp.com |

| Report of Independent | |

| Stone Harbor Investment Funds | Registered Public Accounting Firm |

To the shareholders and the Board of Trustees of Stone Harbor Investment Funds

Opinion on the Financial Statements and Financial Highlights

We have audited the accompanying statements of assets and liabilities of Stone Harbor Investment Funds comprising Stone Harbor Emerging Markets Debt Fund, Stone Harbor High Yield Bond Fund, Stone Harbor Local Markets Fund, Stone Harbor Emerging Markets Corporate Debt Fund, Stone Harbor Strategic Income Fund, and Stone Harbor Emerging Markets Debt Allocation Fund (the “Funds”), including the statements of investments, as of May 31, 2021, the related statements of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, the financial highlights for each of the five years in the period then ended, and the related notes. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of each of the funds constituting the Stone Harbor Investment Funds as of May 31, 2021, and the results of their operations for the year then ended, the changes in their net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on the Funds’ financial statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Funds in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement, whether due to error or fraud. The Funds are not required to have, nor were we engaged to perform, an audit of their internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Funds’ internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements and financial highlights. Our procedures included confirmation of securities owned as of May 31, 2021, by correspondence with the custodian, transfer agent, agent banks, and brokers; when replies were not received from agent banks or brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

Denver, Colorado

July 30, 2021

We have served as the auditor of one or more Stone Harbor Investment Partners investment companies since 2008.

| Stone Harbor Investment Funds Annual Report | May 31, 2021 | 17 |

| Stone Harbor Emerging Markets Debt Fund | Statements of Investments |

May 31, 2021

| Currency | Rate | Maturity Date | Principal Amount/Shares* | Value (Expressed in USD) | ||||||||||||||

| SOVEREIGN DEBT OBLIGATIONS - 70.02% | ||||||||||||||||||

| Angola - 2.15% | ||||||||||||||||||

| Republic of Angola: | ||||||||||||||||||

| USD | 6M US L + 7.50% | 07/01/23 | 14,961,846 | $ | 14,887,037 | (1) | ||||||||||||

| USD | 6M US L + 4.50% | 12/07/23 | 2,730,000 | 2,675,400 | (1) | |||||||||||||

| USD | 6.93 | % | 02/19/27 | 6,642,857 | 6,186,161 | |||||||||||||

| USD | 9.38 | % | 05/08/48 | 5,991,000 | 6,227,045 | (2) | ||||||||||||

| 29,975,643 | ||||||||||||||||||

| Argentina - 3.07% | ||||||||||||||||||

| Republic of Argentina: | ||||||||||||||||||

| USD | 1.00 | % | 07/09/29 | 408,132 | 159,688 | |||||||||||||

| USD | 0.13 | % | 07/09/30 | 89,830,980 | 33,268,903 | (3) | ||||||||||||

| USD | 0.13 | % | 07/09/35 | 3,832,000 | 1,270,318 | (3) | ||||||||||||

| USD | 0.13 | % | 01/09/38 | 827,419 | 328,460 | (3) | ||||||||||||

| USD | 0.13 | % | 07/09/46 | 23,287,974 | 7,837,393 | (3) | ||||||||||||

| 42,864,762 | ||||||||||||||||||

| Armenia - 0.14% | ||||||||||||||||||

| Republic of Armenia | ||||||||||||||||||

| USD | 3.60 | % | 02/02/31 | 2,074,000 | 1,925,745 | (4) | ||||||||||||

| Bahamas - 0.25% | ||||||||||||||||||

| Commonwealth of Bahamas: | ||||||||||||||||||

| USD | 6.00 | % | 11/21/28 | 672,000 | 685,650 | (2) | ||||||||||||

| USD | 8.95 | % | 10/15/32 | 2,459,000 | 2,810,176 | (4) | ||||||||||||

| 3,495,826 | ||||||||||||||||||

| Bahrain - 1.80% | ||||||||||||||||||

| Kingdom of Bahrain: | ||||||||||||||||||

| USD | 7.38 | % | 05/14/30 | 4,915,000 | 5,526,156 | (2) | ||||||||||||

| USD | 5.63 | % | 09/30/31 | 2,458,000 | 2,477,314 | (4) | ||||||||||||

| USD | 5.45 | % | 09/16/32 | 7,352,000 | 7,257,802 | (4) | ||||||||||||

| USD | 5.25 | % | 01/25/33 | 7,392,000 | 7,140,210 | (4) | ||||||||||||

| USD | 6.00 | % | 09/19/44 | 2,968,000 | 2,781,476 | (2) | ||||||||||||

| 25,182,958 | ||||||||||||||||||

| Belarus - 1.64% | ||||||||||||||||||

| Development Bank Belarus | USD | 6.75 | % | 05/02/24 | 5,218,000 | 4,911,116 | (2) | |||||||||||

| Republic of Belarus: | ||||||||||||||||||

| USD | 5.88 | % | 02/24/26 | 6,324,000 | 5,958,394 | (2) | ||||||||||||

| USD | 7.63 | % | 06/29/27 | 275,000 | 274,542 | (4) | ||||||||||||

| USD | 7.63 | % | 06/29/27 | 8,734,000 | 8,719,458 | (2) | ||||||||||||

| USD | 6.20 | % | 02/28/30 | 420,000 | 381,477 | (4) | ||||||||||||

| USD | 6.20 | % | 02/28/30 | 2,866,000 | 2,603,123 | (2) | ||||||||||||

| 22,848,110 | ||||||||||||||||||

| Benin - 0.63% | ||||||||||||||||||

| Republic of Benin: | ||||||||||||||||||

| EUR | 4.88 | % | 01/19/32 | 3,297,000 | 3,991,638 | (4) | ||||||||||||

| See Notes to Financial Statements. | |

| 18 | www.shiplp.com |

| Stone Harbor Emerging Markets Debt Fund | Statements of Investments |

May 31, 2021

| Currency | Rate | Maturity Date | Principal Amount/Shares* | Value (Expressed in USD) | ||||||||||||||

| Benin (continued) | ||||||||||||||||||

| Republic of Benin: (continued) | ||||||||||||||||||

| EUR | 6.88 | % | 01/19/52 | 3,806,000 | $ | 4,834,138 | (4) | |||||||||||

| 8,825,776 | ||||||||||||||||||

| Brazil - 2.94% | ||||||||||||||||||

| Fed Republic of Brazil: | ||||||||||||||||||

| USD | 6.00 | % | 04/07/26 | 1,713,000 | 2,015,203 | |||||||||||||

| USD | 4.63 | % | 01/13/28 | 5,626,000 | 6,131,060 | |||||||||||||

| USD | 3.88 | % | 06/12/30 | 17,404,000 | 17,619,897 | |||||||||||||

| USD | 5.63 | % | 02/21/47 | 2,414,000 | 2,603,064 | |||||||||||||

| State of Minas Gerais: | ||||||||||||||||||

| USD | 5.33 | % | 02/15/28 | 1,295,700 | 1,411,503 | (4) | ||||||||||||

| USD | 5.33 | % | 02/15/28 | 10,365,600 | 11,292,026 | (2) | ||||||||||||

| 41,072,753 | ||||||||||||||||||

| Cameroon - 0.10% | ||||||||||||||||||

| Republic of Cameroon | USD | 9.50 | % | 11/19/25 | 1,170,000 | 1,344,780 | (4) | |||||||||||

| Chile - 0.12% | ||||||||||||||||||

| Republic of Chile | USD | 3.10 | % | 05/07/41 | 1,675,000 | 1,642,338 | ||||||||||||

| Colombia - 3.67% | ||||||||||||||||||

| Republic of Colombia: | ||||||||||||||||||

| USD | 8.13 | % | 05/21/24 | 2,703,000 | 3,205,049 | |||||||||||||

| USD | 3.00 | % | 01/30/30 | 9,006,000 | 8,717,988 | |||||||||||||

| USD | 3.13 | % | 04/15/31 | 22,057,000 | 21,251,699 | |||||||||||||

| USD | 3.25 | % | 04/22/32 | 6,384,000 | 6,157,368 | |||||||||||||

| USD | 6.13 | % | 01/18/41 | 2,118,000 | 2,468,375 | |||||||||||||

| USD | 4.13 | % | 02/22/42 | 1,001,000 | 954,203 | |||||||||||||

| USD | 5.00 | % | 06/15/45 | 3,766,000 | 3,895,720 | |||||||||||||

| USD | 5.20 | % | 05/15/49 | 2,392,000 | 2,545,208 | |||||||||||||

| USD | 3.88 | % | 02/15/61 | 2,410,000 | 2,071,244 | |||||||||||||

| 51,266,854 | ||||||||||||||||||

| Costa Rica - 0.76% | ||||||||||||||||||

| Costa Rica Government: | ||||||||||||||||||

| USD | 4.38 | % | 04/30/25 | 1,800,000 | 1,883,318 | (2) | ||||||||||||

| USD | 6.13 | % | 02/19/31 | 540,000 | 578,192 | (2) | ||||||||||||

| USD | 5.63 | % | 04/30/43 | 195,000 | 184,452 | (4) | ||||||||||||

| USD | 7.00 | % | 04/04/44 | 2,835,000 | 2,975,272 | (4) | ||||||||||||

| USD | 7.16 | % | 03/12/45 | 2,434,000 | 2,574,265 | (4) | ||||||||||||

| USD | 7.16 | % | 03/12/45 | 2,331,000 | 2,465,330 | (2) | ||||||||||||

| 10,660,829 | ||||||||||||||||||

| Dominican Republic - 2.61% | ||||||||||||||||||

| Dominican Republic: | ||||||||||||||||||

| USD | 6.60 | % | 01/28/24 | 1,632,000 | 1,827,840 | (2) | ||||||||||||

| USD | 5.88 | % | 04/18/24 | 2,537,000 | 2,719,810 | (4) | ||||||||||||

| USD | 5.95 | % | 01/25/27 | 2,152,000 | 2,436,468 | (2) | ||||||||||||

| USD | 4.50 | % | 01/30/30 | 6,873,000 | 7,063,915 | (4) | ||||||||||||

| USD | 4.88 | % | 09/23/32 | 2,045,000 | 2,108,267 | (4) | ||||||||||||

| See Notes to Financial Statements. | |

| Stone Harbor Investment Funds Annual Report | May 31, 2021 | 19 |

| Stone Harbor Emerging Markets Debt Fund | Statements of Investments |

| May 31, 2021 |

| Currency | Rate | Maturity Date | Principal Amount/Shares* | Value (Expressed in USD) | ||||||||||||||

| Dominican Republic (continued) | ||||||||||||||||||

| Dominican Republic: (continued) | ||||||||||||||||||

| USD | 4.88 | % | 09/23/32 | 4,457,000 | $ | 4,594,888 | (2) | |||||||||||

| USD | 6.50 | % | 02/15/48 | 6,526,000 | 7,146,133 | |||||||||||||

| USD | 6.40 | % | 06/05/49 | 3,389,000 | 3,647,106 | (2) | ||||||||||||

| USD | 5.88 | % | 01/30/60 | 4,957,000 | 4,898,136 | (4) | ||||||||||||

| 36,442,563 | ||||||||||||||||||

| Ecuador - 1.76% | ||||||||||||||||||

| Republic of Ecuador: | ||||||||||||||||||

| USD | 0.50 | % | 07/31/30 | 16,733,738 | 14,558,352 | (3)(4) | ||||||||||||

| USD | 0.00 | % | 07/31/30 | 5,211,766 | 2,959,306 | (4)(5) | ||||||||||||

| USD | 0.50 | % | 07/31/35 | 10,014,323 | 7,047,580 | (3)(4) | ||||||||||||

| 24,565,238 | ||||||||||||||||||

| Egypt - 2.66% | ||||||||||||||||||

| Republic of Egypt: | ||||||||||||||||||

| USD | 5.88 | % | 06/11/25 | 936,000 | 1,009,705 | (4) | ||||||||||||

| USD | 5.25 | % | 10/06/25 | 1,451,000 | 1,540,327 | (4) | ||||||||||||

| USD | 3.88 | % | 02/16/26 | 4,130,000 | 4,105,478 | (4) | ||||||||||||

| EUR | 4.75 | % | 04/16/26 | 2,252,000 | 2,899,144 | (4) | ||||||||||||

| USD | 7.05 | % | 01/15/32 | 1,753,000 | 1,833,147 | (4) | ||||||||||||

| USD | 7.63 | % | 05/29/32 | 9,043,000 | 9,826,011 | (4) | ||||||||||||

| USD | 8.50 | % | 01/31/47 | 3,169,000 | 3,374,335 | (2) | ||||||||||||

| USD | 7.90 | % | 02/21/48 | 4,503,000 | 4,574,294 | (4) | ||||||||||||

| USD | 7.90 | % | 02/21/48 | 2,099,000 | 2,132,233 | (2) | ||||||||||||

| USD | 8.70 | % | 03/01/49 | 1,115,000 | 1,203,751 | (4) | ||||||||||||

| USD | 8.88 | % | 05/29/50 | 1,149,000 | 1,266,040 | (4) | ||||||||||||

| USD | 8.15 | % | 11/20/59 | 3,335,000 | 3,409,662 | (4) | ||||||||||||

| 37,174,127 | ||||||||||||||||||

| El Salvador - 0.92% | ||||||||||||||||||

| Republic of El Salvador: | ||||||||||||||||||

| USD | 5.88 | % | 01/30/25 | 987,000 | 971,578 | (2) | ||||||||||||

| USD | 6.38 | % | 01/18/27 | 3,032,000 | 2,992,205 | (2) | ||||||||||||

| USD | 8.25 | % | 04/10/32 | 867,000 | 909,808 | (4) | ||||||||||||

| USD | 8.25 | % | 04/10/32 | 2,468,000 | 2,589,858 | (2) | ||||||||||||

| USD | 7.63 | % | 02/01/41 | 296,000 | 293,225 | (4) | ||||||||||||

| USD | 7.63 | % | 02/01/41 | 4,341,000 | 4,300,303 | (2) | ||||||||||||

| USD | 9.50 | % | 07/15/52 | 720,000 | 777,600 | (2) | ||||||||||||

| 12,834,577 | ||||||||||||||||||

| Ethiopia - 0.09% | ||||||||||||||||||

| Republic of Ethiopia | USD | 6.63 | % | 12/11/24 | 1,319,000 | 1,224,978 | (4) | |||||||||||

| Gabon - 0.32% | ||||||||||||||||||

| Republic of Gabon: | ||||||||||||||||||

| USD | 6.38 | % | 12/12/24 | 937,000 | 993,157 | (2) | ||||||||||||

| USD | 6.63 | % | 02/06/31 | 3,521,000 | 3,527,566 | (4) | ||||||||||||

| 4,520,723 | ||||||||||||||||||

| See Notes to Financial Statements. | |

| 20 | www.shiplp.com |

| Stone Harbor Emerging Markets Debt Fund | Statements of Investments |

May 31, 2021

| Currency | Rate | Maturity Date | Principal Amount/Shares* | Value (Expressed in USD) | ||||||||||||||

| Georgia - 0.17% | ||||||||||||||||||

| Republic of Georgia | USD | 2.75 | % | 04/22/26 | 2,366,000 | $ | 2,394,836 | (4) | ||||||||||

| Ghana - 1.76% | ||||||||||||||||||

| Republic of Ghana: | ||||||||||||||||||

| USD | 8.13 | % | 01/18/26 | 1,616,000 | 1,745,054 | (4) | ||||||||||||

| USD | 6.38 | % | 02/11/27 | 1,308,000 | 1,321,018 | (4) | ||||||||||||

| USD | 7.88 | % | 03/26/27 | 5,098,000 | 5,404,033 | (4) | ||||||||||||

| USD | 7.63 | % | 05/16/29 | 396,000 | 406,177 | (4) | ||||||||||||

| USD | 7.63 | % | 05/16/29 | 1,268,000 | 1,300,588 | (2) | ||||||||||||

| USD | 8.88 | % | 05/07/42 | 2,037,000 | 2,075,194 | (4) | ||||||||||||

| USD | 8.63 | % | 06/16/49 | 2,077,000 | 2,033,611 | (4) | ||||||||||||

| USD | 8.63 | % | 06/16/49 | 600,000 | 587,466 | (2) | ||||||||||||

| USD | 8.95 | % | 03/26/51 | 1,500,000 | 1,499,156 | (4) | ||||||||||||

| USD | 8.95 | % | 03/26/51 | 2,200,000 | 2,198,762 | (2) | ||||||||||||

| USD | 8.75 | % | 03/11/61 | 6,160,000 | 5,997,453 | (4) | ||||||||||||

| 24,568,512 | ||||||||||||||||||

| Guatemala - 0.79% | ||||||||||||||||||

| Republic of Guatemala: | ||||||||||||||||||

| USD | 4.50 | % | 05/03/26 | 400,000 | 440,810 | (2) | ||||||||||||

| USD | 4.38 | % | 06/05/27 | 3,000,000 | 3,268,732 | (2) | ||||||||||||

| USD | 5.38 | % | 04/24/32 | 2,181,000 | 2,506,825 | (2) | ||||||||||||

| USD | 6.13 | % | 06/01/50 | 3,986,000 | 4,812,607 | (2) | ||||||||||||

| 11,028,974 | ||||||||||||||||||

| Honduras - 0.21% | ||||||||||||||||||

| Honduras Government | USD | 5.63 | % | 06/24/30 | 2,825,000 | 2,979,520 | (4) | |||||||||||

| Indonesia - 0.99% | ||||||||||||||||||

| Republic of Indonesia: | ||||||||||||||||||

| USD | 2.85 | % | 02/14/30 | 7,584,000 | 7,881,672 | |||||||||||||

| USD | 8.50 | % | 10/12/35 | 834,000 | 1,320,920 | (2) | ||||||||||||

| USD | 5.25 | % | 01/17/42 | 1,380,000 | 1,685,767 | (2) | ||||||||||||

| USD | 6.75 | % | 01/15/44 | 948,000 | 1,369,614 | (2) | ||||||||||||

| USD | 5.13 | % | 01/15/45 | 670,000 | 808,615 | (2) | ||||||||||||

| USD | 5.25 | % | 01/08/47 | 664,000 | 826,620 | (4) | ||||||||||||

| 13,893,208 | ||||||||||||||||||

| Iraq - 0.24% | ||||||||||||||||||

| Republic of Iraq | USD | 5.80 | % | 01/15/28 | 3,517,500 | 3,398,186 | (2) | |||||||||||

| Ivory Coast - 0.48% | ||||||||||||||||||

| Ivory Coast Government: | ||||||||||||||||||

| EUR | 5.25 | % | 03/22/30 | 1,720,000 | 2,214,282 | (2) | ||||||||||||

| EUR | 6.88 | % | 10/17/40 | 1,965,000 | 2,620,314 | (2) | ||||||||||||

| EUR | 6.63 | % | 03/22/48 | 1,446,000 | 1,866,666 | (4) | ||||||||||||

| 6,701,262 | ||||||||||||||||||

See Notes to Financial Statements.

| Stone Harbor Investment Funds Annual Report | May 31, 2021 | 21 |

| Stone Harbor Emerging Markets Debt Fund | Statements of Investments |

May 31, 2021

| Currency | Rate | Maturity Date | Principal Amount/Shares* | Value (Expressed in USD) | ||||||||||||||

| Jordan - 0.64% | ||||||||||||||||||

| Kingdom of Jordan: | ||||||||||||||||||

| USD | 5.85 | % | 07/07/30 | 5,738,000 | $ | 5,980,072 | (4) | |||||||||||

| USD | 7.38 | % | 10/10/47 | 531,000 | 563,682 | (4) | ||||||||||||

| USD | 7.38 | % | 10/10/47 | 2,325,000 | 2,468,098 | (2) | ||||||||||||

| 9,011,852 | ||||||||||||||||||

| Kazakhstan - 0.14% | ||||||||||||||||||

| Republic of Kazakhstan | USD | 4.88 | % | 10/14/44 | 1,560,000 | 1,933,640 | (4) | |||||||||||

| Kenya - 0.88% | ||||||||||||||||||

| Republic of Kenya: | ||||||||||||||||||

| USD | 6.88 | % | 06/24/24 | 3,675,000 | 4,092,875 | (4) | ||||||||||||

| USD | 7.00 | % | 05/22/27 | 1,055,000 | 1,165,121 | (4) | ||||||||||||

| USD | 7.25 | % | 02/28/28 | 1,510,000 | 1,681,151 | (2) | ||||||||||||

| USD | 8.00 | % | 05/22/32 | 1,980,000 | 2,238,024 | (2) | ||||||||||||

| USD | 8.25 | % | 02/28/48 | 2,861,000 | 3,173,850 | (4) | ||||||||||||

| 12,351,021 | ||||||||||||||||||

| Lebanon - 0.33% | ||||||||||||||||||

| Lebanese Republic: | ||||||||||||||||||

| USD | 8.25 | % | 04/12/21 | 5,803,000 | 793,502 | (2)(6) | ||||||||||||

| USD | 6.00 | % | 01/27/23 | 3,176,000 | 435,700 | (6) | ||||||||||||

| USD | 6.40 | % | 05/26/23 | 1,400,000 | 190,249 | (6) | ||||||||||||

| USD | 6.65 | % | 04/22/24 | 4,700,000 | 643,500 | (6) | ||||||||||||

| USD | 6.60 | % | 11/27/26 | 4,525,000 | 622,097 | (6) | ||||||||||||

| USD | 6.65 | % | 02/26/30 | 4,400,000 | 603,438 | (6) | ||||||||||||

| USD | 8.20 | % | 05/17/33 | 9,575,000 | 1,263,661 | (6) | ||||||||||||

| 4,552,147 | ||||||||||||||||||

| Malaysia - 2.55% | ||||||||||||||||||

| 1mdb Global Investments | USD | 4.40 | % | 03/09/23 | 35,300,000 | 35,641,969 | (2) | |||||||||||

| Mexico - 2.28% | ||||||||||||||||||

| United Mexican States: | ||||||||||||||||||

| USD | 4.75 | % | 04/27/32 | 17,395,000 | 19,817,471 | |||||||||||||

| USD | 6.05 | % | 01/11/40 | 3,354,000 | 4,183,075 | |||||||||||||

| USD | 4.28 | % | 08/14/41 | 1,549,000 | 1,619,480 | |||||||||||||

| USD | 4.75 | % | 03/08/44 | 2,446,000 | 2,677,508 | |||||||||||||

| USD | 3.77 | % | 05/24/61 | 3,840,000 | 3,533,030 | |||||||||||||

| 31,830,564 | ||||||||||||||||||

| Morocco - 0.70% | ||||||||||||||||||

| Kingdom of Morocco | USD | 3.00 | % | 12/15/32 | 10,218,000 | 9,844,404 | (2) | |||||||||||

| Mozambique - 0.73% | ||||||||||||||||||

| Republic of Mozambique | USD | 5.00 | % | 09/15/31 | 12,437,000 | 10,177,664 | (3)(4) | |||||||||||

See Notes to Financial Statements.

| 22 | www.shiplp.com |

| Stone Harbor Emerging Markets Debt Fund | Statements of Investments | |

| May 31, 2021 | ||

| Currency | Rate | Maturity Date | Principal Amount/Shares* | Value (Expressed in USD) | ||||||||||||||

| Nigeria - 1.56% | ||||||||||||||||||

| Republic of Nigeria: | ||||||||||||||||||

| USD | 6.50 | % | 11/28/27 | 2,019,000 | $ | 2,155,010 | (4) | |||||||||||

| USD | 7.88 | % | 02/16/32 | 13,364,000 | 14,515,743 | (4) | ||||||||||||

| USD | 7.70 | % | 02/23/38 | 1,880,000 | 1,947,957 | (4) | ||||||||||||

| USD | 7.70 | % | 02/23/38 | 3,012,000 | 3,120,876 | (2) | ||||||||||||

| 21,739,586 | ||||||||||||||||||

| Oman - 2.55% | ||||||||||||||||||

| Oman Government: | ||||||||||||||||||

| USD | 4.88 | % | 02/01/25 | 4,237,000 | 4,440,217 | (4) | ||||||||||||