ANNUAL INFORMATION FORM GEOVIC MINING CORP.

for the year ended December 31, 2006

Dated June 13, 2007

50555656.12

| TABLE OF CONTENTS |

| |

| |

| Item | | |

| | | Page |

| |

| METRIC CONVERSION TABLE | | 2 |

| CORPORATE STRUCTURE | | 3 |

| GENERAL DEVELOPMENT OF THE BUSINESS OF THE COMPANY | | 4 |

| DESCRIPTION OF THE BUSINESS | | 7 |

| RISK FACTORS | | 8 |

| MINERAL PROJECTS OF THE COMPANY | | 12 |

| DIVIDENDS | | 37 |

| DESCRIPTION OF CAPITAL STRUCTURE | | 37 |

| MARKET FOR SECURITIES | | 38 |

| ESCROWED SECURITIES | | 41 |

| DIRECTORS AND OFFICERS | | 42 |

| CEASE TRADE ORDERS, BANKRUPTCIES, PENALTIES OR SANCTIONS | | 44 |

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS | | 44 |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | | 45 |

| TRANSFER AGENTS AND REGISTRARS | | 45 |

| MATERIAL CONTRACTS | | 45 |

| INTEREST OF EXPERTS | | 46 |

| ADDITIONAL INFORMATION | | 46 |

50555656.12

| CURRENCY AND FINANCIAL INFORMATION |

All dollar references in this Annual Information Form (“AIF”) are in United States dollars, unless otherwise indicated. References to “$” or “US$” are to United States dollars and references to “Cdn$” are to Canadian dollars. The following table sets forth, for each period indicated, the exchange rates for United States dollars expressed in Canadian dollars and, in the case of yearly data, the average of such exchange rates on the last day of each month during such period, based on the inverse of the noon buying rate:

| | | Monthly Data | | |

| |

| |

|

| | | High | | Low |

| |

| |

|

| May 2007 | | 1.1136 | | 1.0663 |

| April 2007 | | 1.1584 | | 1.1067 |

| March 2007 | | 1.1811 | | 1.1529 |

| February 2007 | | 1.1853 | | 1.1585 |

| January 2007 | | 1.1824 | | 1.1649 |

| December 2006 | | 1.1652 | | 1.1415 |

| November 2006 | | 1.1474 | | 1.1275 |

| October 2006 | | 1.1385 | | 1.1155 |

| September 2006 | | 1.1190 | | 1.1131 |

| August 2006 | | 1.1315 | | 1.1066 |

| July 2006 | | 1.1416 | | 1.1061 |

| June 2006 | | 1.1245 | | 1.0990 |

| May 2006 | | 1.1233 | | 1.0990 |

| April 2006 | | 1.1719 | | 1.1133 |

| March 2006 | | 1.1724 | | 1.1322 |

| February 2006 | | 1.1578 | | 1.1380 |

| January 2006 | | 1.1726 | | 1.1439 |

| Yearly Data Year Ended December 31, |

|

| | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 |

| |

| |

| |

| |

| |

|

| Average Rate | | 1.1341 | | 1.2116 | | 1.3015 | | 1.4015 | | 1.5704 |

| High Rate | | 1.1726 | | 1.1427 | | 1.1746 | | 1.2839 | | 1.5028 |

| Low Rate | | 1.1190 | | 1.2734 | | 1.4003 | | 1.5777 | | 1.6184 |

On June 12, 2007, the inverse of the Noon Buying Rate was $1.00 = Cdn$1.0636.

50555656.12

METRIC CONVERSION TABLE

The following table sets out the applicable conversion information for imperial and metric measures:

| To convert from Metric | | To Imperial | | Divide By |

| |

| |

|

| Hectares | | Acres | | 0.404686 |

| |

| |

|

| Kilometers | | Miles | | 1.609344 |

| |

| |

|

| Kilograms | | Pounds | | 0.453592 |

| |

| |

|

| Tonnes | | Short tons | | 0.907185 |

| |

| |

|

| Metres | | Yards | | 0.9144 |

| |

| |

|

| Disclosure Regarding Forward-Looking Statements |

This AIF contains or incorporates by reference “forward looking information” which means disclosure regarding possible events, conditions, acquisitions, or results of operations that is based on assumptions about future conditions and courses of action and includes future oriented financial information with respect to prospective results of operations, financial position or cash flows that is presented either as a forecast or a projection, and also includes, but is not limited to, statements with respect to the future financial and operating performance of Geovic Mining Corp., its current and proposed subsidiaries and its current and proposed mineral projects, the estimation of mineral reserves and resources, the realization of mineral reserve estimates, the timing and amount of estimated future production, costs of production, working capital requirements, capital and exploration expenditures, costs and timing of mine de velopment, processing facility construction and the development of new deposits, costs and timing of future exploration, requirements for additional capital, government regulation of mining operations, environmental risks, reclamation expenses, title disputes or claims, limitations of insurance coverage and the timing and possible outcome of pending litigation and regulatory matters. Often, but not always, forward looking statements can be identified by the use of words such as “plans”, “proposes”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates ”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes” or variations (including negative variations) of such words and phrases, or state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, &# 147;occur” or “be achieved”. Forward looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company and/or its current and proposed subsidiaries to be materially different from any future results, performance or achievements expressed or implied by the forward looking statements. Such risks and factors include, among others, risks related to the integration of acquisitions, risks related to operations, risks related to joint venture operations, general business, economic, competitive, political and social uncertainties; the actual results of current exploration activities; actual results of reclamation activities; the outcome of negotiations, conclusions of economic evaluations and studies; changes in project parameters and returns as plans continue to be refined; future prices of metals; possible variations of ore reserves, grade or recovery rates; failure of plant, equipment or processes to op erate as anticipated; accidents, labour disputes and other risks of the mining industry; political instability; insurrection or war; political uncertainty; arbitrary changes in law; delays in obtaining governmental approvals or financing or in the completion of development or construction activities, as well as those factors discussed in the section entitled “Risk Factors” in this AIF. As a result, actual actions, events or results may differ materially from those described in forward looking statements, there may be other factors that cause actions, events or results to differ from those anticipated, estimated or intended. Forward looking statements contained herein are made as of the date of the AIF and the Company disclaims any obligation to update any forward looking statements, whether as a result of new information, future events or results or otherwise. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materi ally from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward looking statements due to the inherent uncertainty therein.

Forward looking statements and other information contained herein concerning the mining industry and our general expectations concerning the mining industry are based on estimates prepared by us using data from publicly available industry sources as well as from market research and industry analysis and on assumptions based on data

50555656.12

and knowledge of this industry which we believe to be reasonable. However, this data is inherently imprecise, although generally indicative of relative market positions, market shares and performance characteristics. While we are not aware of any misstatements regarding any industry data presented here, the industries involve risks and uncertainties and are subject to change based on various factors.

Geovic Mining Corp. (the “Company” or “Geovic Mining”) has its head office located at 743 Horizon Court, Suite 300A, Grand Junction, Colorado, USA, 81506. The registered and records office of the Company is located at Corporation Service Company, 2711 Centerville Road, Suite 400, Wilmington, Delaware, USA, 19808.

The Company was incorporated under the Business Corporations Act (Alberta) on August 27, 1984 and commenced business on March 1, 1988. The Company was continued into Ontario on November 8, 2001. On November 17, 2006, the Company consolidated all of its issued and outstanding shares on the basis of 2.344 common shares for each post-consolidated common share of the Company. On November 21, 2006, the Company continued its jurisdiction of incorporation into the State of Delaware and changed its name from “Resource Equity Ltd.” to “Geovic Mining Corp.”

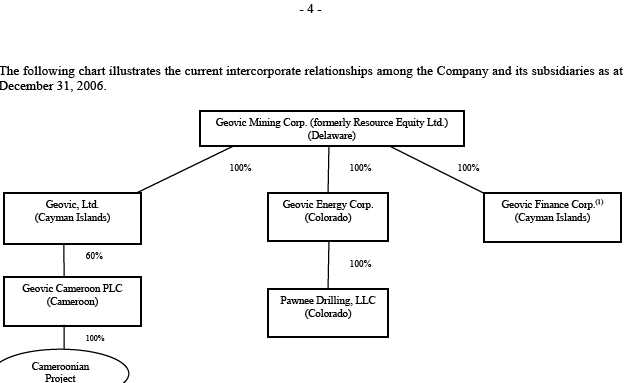

| Intercorporate Relationships |

On December 1, 2006, the Company completed a reverse take-over transaction (the “RTO” or the “Acquisition”) with the result that the Company holds 100% of the issued and outstanding shares in the capital of each of “Geovic, Ltd.” (“Geovic”) and “Geovic Finance Corp.” (“FinCo”). Geovic owns 60% of Geovic Cameroon PLC (“GeoCam”), a private corporation existing under the laws of Cameroon. The Acquisition was completed pursuant to an agreement (the “Arrangement Agreement”) dated as of September 20, 2006, as amended October 31, 2006, entered into between the Company, Geovic, FinCo and William A. Buckovic (“Buckovic”).

In anticipation of the RTO, the Company incorporated a new wholly-owned subsidiary, named Ironbark Capital Corporation (“Ironbark”) which subsequently assumed the historical business of the Company. On November 30, 2006, the Company completed a pro rata distribution to its shareholders on record as at September 22, 2006 of the shares of Ironbark (the “Ironbark Shares”), which held all of the Company’s then owned non cash assets, consisting of marketable securities and intellectual property related to its previous business activities. Accordingly, Geovic Mining no longer has an intercorporate relationship with Ironbark.

50555656.12

(1) FinCo is in the process of being voluntarily liquidated and dissolved.

On March 23, 2007, Geovic Mining incorporated “Geovic Energy Corp.” and on March 29, 2007, Geovic Energy Corp. formed “Pawnee Drilling, LLC” under the laws of the state of Colorado for the purpose of evaluating mineral deposits and opportunities and related surface rights in the United States.

GENERAL DEVELOPMENT OF THE BUSINESS OF THE COMPANY

On December 1, 2006, the Company completed the Acquisition, and currently operates the business previously operated by Geovic. Below is a summary of the development of the Company, Geovic and FinCo over the past three years.

| Geovic Mining Corp. (formerly Resource Equity Ltd). |

The original business objective of the Company was evaluating a wide variety of investment opportunities in Canada. It accumulated information on Canadian companies and industries on an ongoing basis, to assist its clients in finding investments. The Company completed industry and company specific studies on the wine industry and the impact of free trade, the dental supply industry and several resource industry studies. The Company derived revenue from fees for preparing the studies, locating investments for a number of local and foreign investors, and participating in investments.

The Company operated in two broad sectors. The first was the advisory and security related activities and services where it used both its own knowledge base and externally sourced data to provide information and implementation on a fee related basis or to exploit a trading opportunity. The second sector was specific projects, which could be internally or externally generated. Unlike the first sector, a specific project may span several years, and during this period, there may not be any revenue recognized. At the time of the Acquisition, the Company was involved in several long term projects.

50555656.12

The Company maintained an extensive database of information on companies and other business entities, which is a major component of the knowledge base. The Company used extensive paper files, microfiche records and several networked computers designed to store and organize data. The computers were equipped with peripheral accessories to permit capture of information and enable secure off site backup of the data files.

In addition to its own data storage, the Company maintained accounts with a number of other data service providers in Canada, the United States and France. The data provided by these suppliers was delivered either on compact discs, which were updated monthly, or through a password protected Internet site.

After the Company completed its initial assessment of investment opportunities in illiquid real estate syndicates, this became the major focus and Phoenix Capital Inc. (“Phoenix”) was established to focus on investing in illiquid real estate syndicates and to pursue opportunities initially with partners and subsequently as a listed public company. All of the business of Phoenix was based on information provided from the database owned by the Company.

With subsequent share issues to finance the growth of Phoenix, the Company’s ownership of Phoenix was diluted to a relatively small percentage. Phoenix has expanded significantly and in June 2005, converted to an income trust and announced the filing of a preliminary prospectus to raise up to an additional Cdn$50 million in capital to fund the expansion of the business. Historically, the profits generated by Phoenix were largely attributable to the access it had to the database of real estate syndicates that was owned by the Company. The access to the database provided by the Company was governed by a written contract. However, subsequent to the RTO, Geovic Mining no longer conducts any of the business previously conducted by the Company and the database utilized by Phoenix was part of the business that was transferred to Ironbark in anticipation of the RTO.

Prior to the Acquisition, Geovic was a private international mineral exploration and development company based in Grand Junction, Colorado with a focus on specialty and strategic metals, from project conception to production. Geovic was devoted to developing a primary cobalt deposit in Cameroon. Geovic owned 55.5% of GeoCam which entered into a mining convention with the Republic of Cameroon in 2002, and subsequently received a Mining Permit (the “Mining Permit”) in 2003 granting exclusive mining rights. In 2006, Geovic acquired 4.5% of GeoCam. GeoCam controls 100% of the Mining Permit for the Nkamouna Cobalt Project, the Mada Project and five other deposits located in Cameroon, Africa (the “Cameroon Properties”).

An independent engineering pre-feasibility study and National Instrument 43-101 technical reports were originally completed in 2006. From inception through 2005 Geovic raised approximately US$16 million from private investors and in 2006, Geovic raised an additional US$4.515 million of capital from private investors. Geovic’s sole business focus has been to advance its Cameroon Properties during this period. A bankable final feasibility study for the Nkamouna project was commissioned in July 2006.

- GeoCam signed a Mining Convention with the Republic of Cameroon in August of 2002.

- On April 14, 2003 the Republic of Cameroon granted the Mining Permit by Presidential Decree to GeoCam.

- GeoCam completed a draft Environmental and Social Impact Assessment (“ESIA”) and related documents in 2004. In 2006, GeoCam submitted the ESIA and related documents to the Government of Cameroon and completed 16 public hearings on the environmental aspects of the project in Cameroon.

- A pre-feasibility study was completed on the Nkamouna project in March 2006 and a Canadian 43-101 Technical Report in April 2006. In August 2006, a 43-101 Technical Report was completed on the Mada deposit.

50555656.12

FinCo was incorporated for the sole purpose of providing equity finance to the Company in connection with the Acquisition and is in the process of being voluntarily dissolved. FinCo is a private Cayman Islands corporation with no material assets, and has not carried on any operations since it was incorporated.

On December 1, 2006, pursuant to the RTO, the Company acquired: (a) all of the issued and outstanding securities of Geovic and of FinCo from the Geovic and FinCo securityholders; and (b) 45 shares, or 4.5% of the issued and outstanding shares of GeoCam, in the capital of GeoCam from Buckovic. The 45 GeoCam shares held by Buckovic were transferred to the Company and Buckovic received 1,250,010 common shares in the capital of the Company. Buckovic continues to hold five GeoCam shares, representing 0.5% of all issued and outstanding GeoCam shares. All common shares in the capital of Geovic were transferred to the Company and each holder of Geovic shares received two common shares in the capital of the Company for each Geovic share. All options to purchase Geovic shares were cancelled and for each Geovic option the Company issued two options, each entitling the holder to purchase one common share of the Company. All warrants to purchase Geovic shares were cancelled and for each Geovic warrant the Company issued a warrant entitling the holder to purchase one common share of the Company at a price of US$1.75 per share.

All common shares in the capital of FinCo were transferred to the Company and each holder of FinCo common shares received one common share in the capital of the Company for each FinCo common share held. All preferred shares of FinCo were transferred to the Company and each holder of a FinCo preferred share received one preferred share in the capital of the Company for each FinCo preferred share. All warrants to purchase FinCo common shares were cancelled and the Company issued to each FinCo warrantholder a warrant to purchase common shares of the Company with the same terms as the original FinCo warrants. All options to purchase FinCo common shares, which were issued by FinCo to the agents as part of the agents’ commission in connection with the Subscription Receipt Financing (as defined below) were cancelled and for each compensation option the Company issued an option to purchase a common share of the Company pursuant to the terms of the Acquisition.

As a result of the Acquisition, Geovic and FinCo became wholly owned subsidiaries of the Company and the Company subsequently transferred the GeoCam shares to Geovic.

| The Subscription Receipt Financing |

In connection with the Acquisition, FinCo and Geovic entered into an agency agreement with a syndicate of agents in connection with an offering on a best efforts basis by FinCo of up to 6,000,000 subscription receipts at a price of Cdn$1.95 per subscription receipt for gross proceeds of Cdn$11,700,000 (the “Subscription Receipt Financing”). Each subscription receipt was exchangeable, immediately prior to the completion of the Acquisition without payment of any further consideration into one FinCo common share and one half of a transferable warrant, each whole warrant (a “FinCo Financing Warrant”) entitling the holder to acquire one FinCo common share at a price of Cdn$2.75 per share for a period of five years from the closing of the Subscription Receipt Financing. The Subscription Receipt Financing was completed on November 3, 2006. In connection with the RTO, all securities issued in connection with the Subscription Receipt Financing were exchanged for similar securities issued by the Company.

On March 6, 2007, the Company closed its public offering of 21,600,000 units of the Company at a price of Cdn$2.50 per unit for gross proceeds of Cdn$54 million (the “March Equity Offering”). Canaccord Capital Corporation, Orion Securities Inc., and Desjardins Securities Inc. acted as agents for the offering. Each unit issued pursuant to the March Equity Offering consisted of one common share of the Company and one half of one common share purchase warrant, each whole warrant having an exercise price of Cdn$3.00 and being exercisable until March 6, 2012.

50555656.12

On April 27, 2007, the Company closed another public offering of 8,750,000 units of the Company at a price of Cdn$4.00 per unit for gross proceeds of Cdn $35 million (the “April Equity Offering”). Canaccord Capital Corporation and Orion Securities Inc. acted as underwriters for the offering. Each unit issued pursuant to the April Equity Offering consisted of one common share of the Company and one half of one common share purchase warrant, each whole warrant having an exercise price of Cdn$5.00 and being exercisable until April 27, 2012. In connection with the April Equity Offering, the Company granted the underwriters an option, exercisable for 30 days from closing, to purchase an additional 1,312,500 units on the same terms as those offered in the April Equity Offering, to cover over-allotments, if any (the “Over-Allotment Option). Subsequent to the closing of the April Equity Offering, the underwriters exercised the Over-Allotment Option and purchased an additional 834,200 units of the Company. With the exercise of the Over-Allotment Option, the April Equity Offering consisted of an aggregate 9,584,200 units resulting in total gross proceeds of Cdn$38,336,800.

| DESCRIPTION OF THE BUSINESS |

As a result of the Acquisition, the Company refocused its business and currently carries on the business formerly carried on by Geovic and focuses on specialty and strategic metals, from prospect conception to project development and production. Through Geovic, the Company is taking steps to advance its cobalt nickel laterite deposit in the Republic of Cameroon through final feasibility, project financing, construction and production in a socially responsive manner to maximize value for all stakeholders. The Company is focused primarily on development of the Nkamouna deposit and continued exploration and development of the other deposits within areas covered by the Mining Permit in the Cameroon Properties. The Company continues to evaluate other specialty metal and strategic mineral investment opportunities. The Company is evaluating selected acquisitions in the mining industry that would provide diversification. The Company’s success is dependent upon the ability of the Company to source the necessary funds to expeditiously explore and develop the mineral resources and reserves on its mineral properties. The Company has substantially no current revenue and continues to generate losses and negative cash flows from operations.

FinCo was incorporated for the sole purpose of providing equity finance to the Company in connection with the Acquisition and is in the process of being voluntarily liquidated.

The Company evaluates and is developing major cobalt nickel occurrences in southeastern Cameroon for production of high quality cobalt and nickel oxide products to meet rapidly expanding demand.

The Company competes with other cobalt nickel producers around the world. These other producers have operations and financial strength greater than the Company. These competitors include such current producers as Xstrata-Falconbridge, CVRD-Inco, Murrin Murrin (Minara) and significant new producers such as Ambatovy (Dynatec), Weda Bay (Eramet), Ravensthorpe (BHP), Goro (Inco) and others.

The environmental protection requirements affect the financial condition and operational performance and earnings of the Company as a result of the capital expenditures and operating costs needed to meet or exceed these requirements. These expenditures and costs may also have an impact on the competitive position of the Company to the extent that its competitors are subject to different requirements in other governmental jurisdictions. In the current financial year the effect of these requirements has been limited due to the development stage of the Company, but they are expected to have a larger effect in future years as the Company moves toward and commences production.

50555656.12

Geovic does not employ any former employees of the Company. As at December 31, 2006, Geovic employed six full time employees in its offices in the U.S. and GeoCam employed six full time employees in its offices in Yaounde, Cameroon.

Geovic Mining is a public corporation based in Grand Junction, Colorado. The Company’s material asset is its 60% interest in GeoCam, a private Cameroonian corporation that holds a 100% ownership of a cobalt nickel province in Cameroon.

Geovic manages the business of GeoCam, and has funded its operations since inception. To date Geovic exclusively funded the activities of GeoCam. The funding is recorded as debt repayable to Geovic. Accrued debt is structured as a series of loans corresponding to the respective fiscal year in which the funds were advanced.

The Company incorporated a wholly-owned subsidiary, Ironbark, prior to the Acquisition and then completed a pro rata distribution to its shareholders on record of the Ironbark Shares. See “Corporate Structure – Intercorporate Relationships” and see also “General Development of the Company - Significant Acquisitions”.

| Social or Environmental Policies |

In 2004 Geovic, on behalf of GeoCam, commissioned a site specific environmental study of the Nkamouna area, which was performed by the consulting firm Knight Piesold and presented as a Environmental and Social Assessment including an Environmental and Social Impact Assessment, and Environmental and Social Action Plan for the Nkamouna area. The Company will need to develop a site specific environmental study of the Mada area, which will include an Environmental and Social Assessment including an Environmental and Social Impact Assessment, and Environmental and Social Action Plan.

The directors of the Company consider the risks set out below to be the most significant risks facing the Company since completing the Acquisition. If any of these risks materialize into actual events or circumstances or other possible additional risks and uncertainties of which the directors are currently unaware or which they consider not to be material in relation to the Company business, actually occur, the Company’s assets, liabilities, financial condition, results of operations (including future results of operations), business and business prospects, are likely to be materially and adversely affected.

| Conflict of Interest of Management |

Certain of the Company’s directors and officers are also directors and officers of other natural resource companies. Consequently, there exists the possibility for such directors and officers to be in a position of conflict. Any decision made by any of such directors and officers relating to the Company will be made in accordance with their duties and obligations to deal fairly and in good faith with the Company and such other companies.

The Market Price of Shares May Be Subject to Wide Price Fluctuations

There can be no assurance that an active market for the securities of the Company will be sustained. Securities of small and mid-cap companies have experienced substantial volatility in the past, often based on factors unrelated to the financial performance or prospects of the companies involved. These factors include macroeconomic developments in North America and globally, and market perceptions of the attractiveness of particular industries.

50555656.12

The price of the securities of the Company is also likely to be significantly affected by short-term changes in commodity prices, other precious metal prices or other mineral prices, currency exchange fluctuation, changes in the business prospects of the Company, general economic conditions, changes in mineral reserve or resource estimates, results of exploration, changes in results of mining operations, legislative changes, the political environment in Cameroon, or in its financial condition or results of operations as reflected in its quarterly earnings reports and other events that are outside of the Company’s control. Other factors unrelated to the performance of the Company that may have an effect on the price of the securities of the Company include the following: the extent of analytical coverage available to investors concerning the business of the Company may be limited if investment banks with research capabilities do not follow the Company’s securities; lessening in trading volume and general market interest in the Company’s securities may affect an investor’s ability to trade significant numbers of securities of the Company; the size of the Company’s public float may limit the ability of some institutions to invest in the Company’s securities; and a substantial decline in the price of the securities of the Company that persists for a significant period of time could cause the Company’s securities, if listed on an exchange, to be delisted from such exchange, further reducing market liquidity. If an active market for the securities of the Company does not continue, the liquidity of an investor’s investment may be limited and the price of the securities of the Company may decline.

In addition, stock markets have from time to time experienced extreme price and volume fluctuations, which, as well as general economic and political conditions, could adversely affect the market price for the common shares of the Company.

The Company is unable to predict whether substantial amounts of its common shares will be sold in the open market. Any sales of substantial amounts of common shares of the Company in the public market, or the perception that such sales might occur, could materially and adversely affect the market price of the common shares of the Company.

| Limited Operating History |

The Company has only a limited operating history upon which investors may base an evaluation its future performance. Although the directors and officers of the Company have extensive experience in mineral exploration, development, financing and operating businesses, there is no guarantee that this experience will result in future success. There can be no assurance that the Company will earn revenues or generate profits from the production of metals or from the sale of its properties.

The Company has no history of producing metals from its current portfolio of mineral exploration properties and none of the Company’s properties are currently under development. The future development of any properties found to be economically feasible will require board approval, the construction and operation of mines, processing plants and related infrastructure. There can be no assurance that the Company will be able to develop its mineral properties at a profit.

Historically, Geovic incurred losses, on an annual basis, since its inception and it is expected that the Company will incur losses unless and until such time as one or more of its properties enter into commercial production and generate sufficient revenues to fund continuing operations. The development of the Cameroonian Properties will require the commitment of substantial financial resources. The amount and timing of expenditures will depend on a number of factors, some of which are beyond the Company’s control, including the progress of ongoing exploration and development, the results of consultants’ analysis and recommendations, the rate at which operating losses are incurred, the execution of any joint venture agreements with strategic partners, and the Company’s acquisition of additional properties.

In respect of new properties, the Company will be subject to all of the risks associated with establishing new mining operations and business enterprises including: timing and cost of the construction of mining and processing facilities; the availability and costs of skilled labour and mining equipment; the availability and cost of appropriate processing materials and equipment; the need to obtain necessary environmental and other governmental approvals

50555656.12

and permits, and the timing of obtaining those approvals and permits; availability of off take agreements or metal sales contracts; and the availability of funds to finance construction and development activities.

The costs, timing and complexities of mine construction and development are increased by the remote location of the Company’s mining properties. It is common in new mining operations to experience unexpected problems and delays during construction, development, mine start up and ramp up to full designed commercial production. Accordingly, there are no assurances that the Company’s activities will result in profitable mining operations or that the Company will successfully establish mining operations or profitably produce metals at any of its properties.

| Reliance on External Financing |

The Company will need external financing to fund the exploration and any development on its mineral properties. The mineral properties that the Company is likely to develop are expected to require significant capital expenditures. The sources of external financing that the Company may use for these purposes include project debt, convertible notes and equity offerings. In addition, the Company may consider a sale of an interest in one of its mineral properties or may enter into a strategic alliance or may utilize a combination of some or all these alternatives. There can be no assurance that the financing option chosen by the Company will be available on acceptable terms, or at all. The failure to obtain financing could have a material adverse effect on the Company’s growth strategy and results of operations and financial condition.

| Sole Funder of Cameroon Properties |

To date Geovic has been contributing and it continues to contribute all of the funds necessary to advance the Cameroon Properties. It is expected that the Company will continue to contribute at least its share, and possibly all, of the funds necessary to advance the Cameroon Properties. If Geovic advances all of these future expenditures, these advances will be reflected as a debt owed to Geovic on the balance sheet of GeoCam. For this to occur, all of the financial statements of the Cameroon company must be approved and certified by an accredited state auditor. Once this debt is recognized on the balance sheet of the audited accounts, recapitalization of GeoCam may be required which might take the form of additions to the paid in capital or a dilution of interest for the minority shareholders. Geovic anticipates that it, rather than the Company, will provide its share of the funds necessary to advance the Cameroon Properties.

While Geovic entered into a loan agreement with GeoCam, there is no agreement that requires Geovic to be the sole source of funding for the Cameroon Properties. Further, the Board of Directors of GeoCam has approved a resolution that its Board recognizes that research, exploration expenses and other investments have been financed by Geovic and should be considered as debts of GeoCam to Geovic.

A shareholders agreement among GeoCam’s shareholders, being Geovic (60%), Societe Nationale d’Investissement du Cameroun (SNI) (20%), four Cameroon individuals (collectively, 19.5%), and Buckovic (0.5%) was entered into on April 9, 2007. The shareholders agreement reflects the historic arrangement between the shareholders and sets forth the terms, conditions and fiscal arrangement for continued participation in the Cameroonian Project. The Company believes that the shareholders agreement is consistent with international mining industry standards and is compliant with Western Africa business law. In addition, SNI has represented to the Company that SNI, on behalf of itself and the four Cameroonian individual shareholders, will contribute 39.5% of the equity funds needed to advance GeoCam’s operations in 2007 and in the future.

The Company competes with other cobalt nickel producers that have operations around the world, and many such companies have operations and financial strength far greater than the Company. The competition may temporarily lower prices to maintain market share and adversely affect the potential profits of the Company.

50555656.12

The Company’s profitability and long term viability depend, in large part, upon the market price of cobalt, nickel and other related products. The mining industry is highly competitive and subject to rapid changes in commodity prices. Conditions beyond the Company’s control could adversely affect the marketing of its cobalt, nickel and manganese (if produced). Conditions such as international financial crises, inflation, increasing interest rates, changing patterns in global cobalt and nickel consumption, and new competitive sources of cobalt and nickel and other potential products could adversely affect the demand and use of cobalt and related substances. There can be no assurance that the Company will be able to produce and sell these mineral products at a sufficient price for the Company to be profitable.

| Decrease in Commodity Prices |

Neither the Company nor Geovic has entered into forward sales arrangements to reduce the risk of exposure to volatility in commodity prices. Accordingly, the Company’s future operations are exposed to the impact of any significant decrease in commodity prices if the Company does not enter into such forward sales arrangements. Conversely, forward sales contracts limit potential upside market swings by setting price ceilings. Such upside price swings can have a significant benefit to companies taking added market risk by selling on the open spot metals market. Cobalt as a commodity, does not benefit from a futures market. If such prices decrease significantly at a time when the Company is producing, the Company would realize reduced revenues. The Company is not restricted from entering into forward sales arrangements at a future date.

The current and future development of the Cameroon Properties requires permits from various Cameroon governing authorities. Future operations will be subject to a number of existing laws and regulations such as labour standards, environmental reclamation, land use and safety.

GeoCam is, to the best of its knowledge, in compliance with all material laws and regulations that currently apply to its activities in Cameroon. There can be no assurance, however, that all permits required to construct and operate a mining and processing facility will be obtained by GeoCam or if obtained by GeoCam, they will be on reasonable terms and conditions or that such laws and regulations would not adversely affect the profitability of the operations.

| General Economic Conditions |

Both domestic and world economic conditions may affect the performance of the Company. Inflation, and deflation in certain geographic regions, continuously changing tax laws, and rapidly fluctuating interest rates may make mineral resource development more difficult. These factors have had a significant effect on Cameroon’s economy in recent years. There is no assurance that such general economic conditions will not have an adverse effect on the overall performance of the Company. In addition, general economic conditions could increase the risk that project financial projections may not occur as expected.

| Political and Country Risks |

The political risk in Sub Saharan Africa is significant. While GeoCam has been granted a Mining Convention and the Mining Permit by the Republic of Cameroon that gives GeoCam the exclusive right to mine, process and export cobalt and nickel on its permitted lands, there is no assurance that GeoCam will be able to finance or profit by this venture.

The business of mining is subject to certain types of risks and hazards, including reserve and resource estimates, processing risks, environmental hazards, industrial accidents, and periodic disruptions due to Force Majeure events,

50555656.12

inclement weather and so forth. Though each of these conditions is taken into consideration during preliminary planning and economic analysis, there is no assurance that disruption of development and production will not occur.

Reserve and resource estimates are expressions of judgement based on knowledge, experience and industry practice. Estimates, which were valid when made, may change significantly when new information becomes available. Accordingly, development and mining plans may have to be altered in a way that adversely affects the Company’s operation and profitability. An estimation of reserves, resources and future production is included in this AIF together with the projected profitability of the operation. These projections are based on a number of existing material facts and certain assumptions. Many of the assumptions are based on future estimates of metal prices and market demands over which the Company will have little or no control. In addition, while metallurgical testing on the Cameroon mineralization performed by the Company’s independent consultants has been successful for agitation leaching, there is a risk that final testing may indicate technical and commercial shortcomings. Consequently, actual results may vary materially from the projected values given herein. Once in production, additional factors can influence the profitability of the Cameroonian Properties including civil strife and environmental compliance issues.

Completion of the development of Cameroonian Properties is subject to various requirements, including the availability and timing of acceptable arrangements for power, water and transportation facilities. The lack of availability on acceptable terms or the delay in the availability of any one or more of these items could prevent or delay development of the Cameroonian Properties. If adequate infrastructure is not available in a timely manner, there can be no assurance that the development of the Cameroonian Properties will be commenced or completed on a timely basis, if at all, or that the resulting operations will achieve the anticipated production or the construction costs and ongoing operating costs associated with the development of the Cameroonian Properties will not be higher than anticipated.

| Mining is Inherently Dangerous |

Mining involves various types of risks and hazards, including, but not limited to, environmental hazards, industrial accidents, metallurgical and process risks, flooding, fire, metal theft, inclement weather, access problems and transport accidents. Workers are subject to risks associated with large mining equipment operations, slope instability, exposure to indigenous disease, steam and hazardous chemicals as well as local social unrest.

These risks could result in damage to, or destruction of mine properties, production facilities or other properties, personal injury, and cause delays in mining, increased production costs, monetary losses and possible legal liabilities unforeseen by financial planners. The Company may not be able to obtain insurance to cover part or all of these risks at economically feasible premiums. Insurance against certain environmental risks, including potential liability for pollution or other hazards as a result of the disposal of waste products occurring from production, is not generally available to the Company or to other companies within the mining industry. The Company may suffer a material adverse effect on its business if it incurs losses related to any significant events that are not covered by such an insurance policy.

| MINERAL PROJECTS OF THE COMPANY |

Description Of Mineral Projects

Nkamouna and Mada Projects |

Unless stated otherwise, information in this section is summarized, compiled or extracted from the Technical Report, Nkamouna and Mada Cobalt Projects, Cameroon dated March 12, 2007 (the “Technical Report”) prepared for Geovic Mining and Geovic by Frederick Barnard, Richard Lambert and Alan Noble, each a “Qualified Person”, as defined in National Instrument 43-101 (“NI 43-101”). Messrs. Barnard, Lambert and Noble are currently employed by Pincock, Allen & Holt (“PAH”) and are independent of Geovic. The Technical Report was prepared in accordance with the requirements of NI 43-101.

50555656.12

Portions of the following information are based on assumptions, qualifications and procedures which are set out only in the full Technical Report. For a complete description of assumptions, qualifications and procedures associated with the following information, reference should be made to the full text of the Technical Report which is available electronically from the Company’s website at www.geovic.net and on SEDAR at www.sedar.com. References to “Geovic” in this section entitled “Mineral Projects of the Company” include GeoCam, as applicable.

| Project Description and Location |

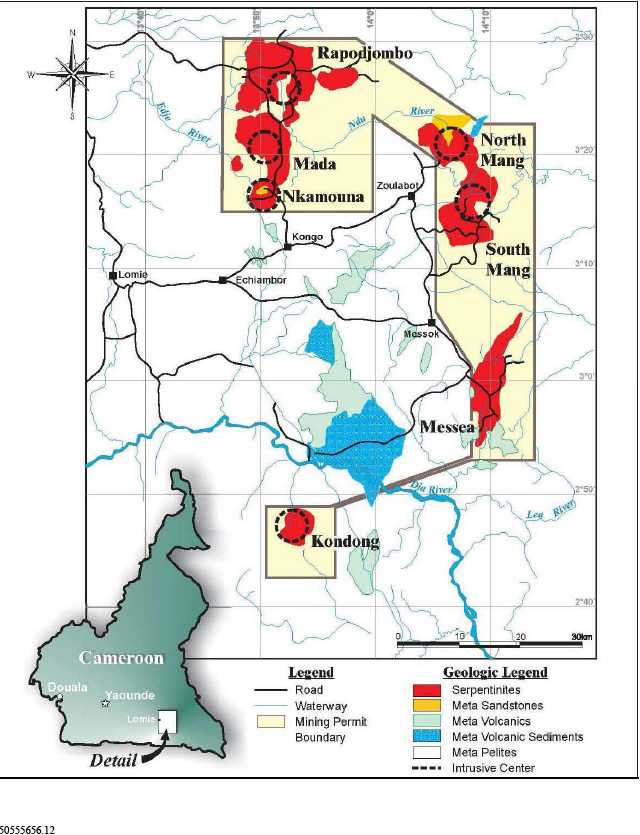

Geovic, through its 60% owned subsidiary GeoCam, has exclusive rights to a large cobalt-nickel laterite province in southeastern Cameroon (the “Cobalt-Nickel Project”). There are seven laterite plateaus within the Cobalt-Nickel Project: Nkamouna, Mada, Rapodjombo, North Mang, South Mang, Messea and Kondong (collectively, the “Plateaus”).

The Nkamouna project (the “Nkamouna Project”), one of the Plateaus, is located in southeastern Cameroon, approximately 640 road kilometers east of the port city of Douala and 400 road kilometres east of the capitol of Yaounde.. The Mada Project (the “Mada Project”) is another one of the Plateaus, approximately 10 kilometers north of the Nkamouna Project.

The mineral rights are held by GeoCam under the Mine Permit and administered under the Mining Convention. Figure A shows the Mine Permit boundary. Although the Mining Permit decree states the area of the Cobalt-Nickel Project as 1,250 square kilometers, the area within the coordinate boundary of the Cobalt-Nickel Project measures approximately 1,600 square kilometers of “multiple use” forestlands, while the Plateaus within the Cobalt-Nickel Project constitute over 300 square kilometers of known mineralized or potentially mineralized terrain within lands designated as “mineral exclusive lands”.

50555656.12

Figure A

Location Map and Mine Permit Area

Geovic’s Cobalt-Nickel Project is located in the Haut Nyong district, East Province of Cameroon, Africa. The Project’s site is 640 kilometers by road from the seaport of Douala, and about 400 kilometers from the capital city of Yaounde. The closest town to the Project site is Lomie, at approximately 26 kilometers to the west – southwest. The closest railroad transport to the Project is at the town of Belabo, at a distance of approximately 250 kilometers. Transportation from Yaounde to the Project is by paved highway to Ayos, improved public road to Abong Mbang and private logging roads or public roads to the project site.

Fifty-nine percent of the Eastern Province, where the Cobalt-Nickel Project is situated, is dominated by forests zoned “multiple-use.” Over 64 logging concessions are designated in the province that surround GeoCam’s “mineral exclusive zone”. A significant portion of the area is also dedicated to protected forests, wildlife reserves and general “evergreen forest” habitat (22%) that are located well away from planned operations. A small proportion of the district is zoned for mineral development (1.6%), part of which includes “mineral exclusive lands” (0.35%) . Indigenous community lands dominated by subsistence gardening and “community forest” developments form the remainder of the district lands which covers about 18% of the province. These lands are located principally along the main access routes developed when the province was first opened to plantation farming in the late 19th Century.

The Mining Convention was signed on July 31, 2002 by the Ministry of Mines, Water, and Power of the Republic of Cameroon. On April 11, 2003, GeoCam was issued the Mining Permit, granting GeoCam the exclusive rights to exploit the deposits within the Cobalt Nickel Project. The Mining Permit will remain in force for the duration of the mineable resource and has an initial term of 25 years. The Mining Permit and Mining Convention are renewable every 10 years thereafter until the depletion of resources. The Mining Permit is the main operating permit for the commercial GeoCam facilities.

In 1999, GeoCam was granted an Exploration Permit, PDR 67, on an area of 5,000 square kilometers. A Mining Convention was entered into between GeoCam and the Republic of Cameroon in 2002. In 2003, Mine Permit 33 was issued by decree granting an exclusive right to Geovic to exploit the deposits within the permitted area. Geovic’s program was initially based entirely on manually-dug test pits, and later incorporated drilling and limited trenching. The program began at Nkamouna and was later extended to the other Plateaus, which were identified by satellite images and air photos. Geologists from the Cameroon Ministry of Mines, Water and Energy participated in the work initially to provide government oversight as well as training.

Lands held within the Mining Permit are designated “multiple-use”, with the principal mineralized areas set aside for “exclusive mine” development. Mining Permit lands were specifically established to exclude village lands in order to avoid conflicts with local communities.

Specific sites that will be impacted by mining and mine related activities will be leased under a government prescribed expropriation process and will have “site specific” environmental plans designed and approved by governing agencies prior to mining. This inventory, valuation and registration process requires local government approval, following a review of each site by district leaders.

The principal remaining permits required by GeoCam before the initiation of construction at Nkamouna include:

| 1) | Land Lease for development sites. |

| |

| 2) | Environmental Permit and Bond, and |

| |

| 3) | Water Use Permit. |

| |

The land lease will be registered and issued to Geovic. Geovic will pay for the cost of leasing the land and compensation for the loss of alternative resources.

50555656.12

Geovic will have the right to occupy, build roads, remove vegetation and mine and process cobalt, nickel and associated substances covered in the Mining Convention once the land is leased, in accordance to the GeoCam Mining Convention of August 1, 2002.

Geovic’s Mine Permit area is totally contained in areas zoned for logging concessions and “multiple use.” All planned mine developments are in logged over areas and are exclusive of “primary forest” designations. Geovic’s mining operations will result in partial deforestation during the mining phase, which represents less than 0.5% of the annual deforested area within the region.

A comprehensive Environmental and Social Impact Assessment (“ESIA”) for the Nkamouna area, describing the existing conditions and project impacts along with the related Environmental and Social Impact Action Plan (“ESAP”) describing appropriate mitigation measures was recently submitted to the Environmental Ministry in Cameroon and is under review.

The ESIA identified several potential environmental and social impacts for which the mitigation measures may be broadly categorized as: reclamation of disturbed land to forest/wildlife habitat, protecting and enhancing biodiversity, offsetting greenhouse gas emissions, ensuring adequate water supplies, and economic diversification and sustainable community development. The ESAP for the Nkamouna Project impacts defines the specific actions that must occur to implement these mitigation measures and who is responsible for their implementation. It also defines specific monitoring programs aimed at documenting the implementation and adequacy of control systems and mitigation measures and the reporting that is required to assure transparency.

With the effective implementation of the mitigation measures and monitoring programs defined in the ESAP, GeoCam can prevent or minimize its project impacts in a manner consistent and in compliance with applicable regulations.

No site specific work has been performed for the Mada area. Geovic will need to develop a site specific environmental study of the Mada area, which will include an Environmental and Social Assessment including an Environmental and Social Impact Assessment and Environmental and Social Action Plan prior to any construction activity in the Mada area.

Principal legislative, regulatory and policy considerations relating to the Cobalt-Nickel Project are as follows:

| A) | Environmental Protection: Law No. 96/12 relating to environmental management outlines the general legal framework for environmental management in Cameroon. The law requires that any development must carry out an “impact assessment study”. The new mining code specifies that bonds are required before mine development can commence. The project’s proposed environmental mitigation and rehabilitation practices are reviewed once every four years to determine if the bond is sufficient to cover annual impacts caused by mining activities. The bond is based on an estimated annual cost of environmental impact mitigation of disturbed sites. |

| |

| B) | Law 94/01(Decree No. 94/436) pertains to forest developments. Article 9 prescribes that cutting trees in a state forest can be performed only after an impact study has been conducted. This study will be carried out as part of Geovic’s “site specific” environmental impact assessment report and environmental rehabilitation plan. |

| |

| C) | Law No. 81-13 regulates fishing, hunting and the issuance of related licenses. Also, the law controls the possession or trade in wild animals and trophy hunting and provides for the protection of endangered species. Enforcement measures and penalties are defined in this law, as described in the Geovic environmental plan. |

| |

| D) | Law No. 89/027 addresses specific waste disposal regulations. It pertains to storage, transportation and disposal of hazardous waste. Businesses must declare the volumes and nature of each waste product and ensure elimination of waste without undue risk to people and the environment. |

| |

50555656.12

| E) | Law 84/13 regulates water resources. The government manages and protects state waters such as rivers, lakes and groundwater. Non-state waters include spring, well and drill holes not used by the public, and rainwater falling on private land or collected artificially from roof systems. The use of water for commercial purposes may be sold by the State authority and is subject to permitting, exploitation and conservation taxes. |

| |

| F) | Decree No. 85/758 regulates water use by committee. This committee provides advice in implementing the water code that will include issues such as inventory, conservation, protection, use, effluent treatment and taxation. |

| |

The current statutory income tax rates in Cameroon are 38.5% for corporations. Dividend tax rates are 16.5% for residents and 25% for non-residents. Thus, the effective income plus dividend tax rate is 53.875% for non-residents and 48.648% for residents.

Among other specific benefits, GeoCam’s Strategic Enterprise Regime awarded on December 16, 2002, provides a 50% reduction to these two tax rates for five years during the installation phase, plus 12 years during the exploitation phase. As a result, GeoCam’s tax rates are 19.25% for corporation and 12.5% dividend (8.25% for residents), or a net 29.34% overall tax for the first 17 years of full production. Since approximately 40% of the shareholders are Cameroon residents, the weighted average dividend tax rate for the first 17 years is 10.8% and the effective rate is 27.97% . Dividend tax is based on cash flow after the initial capital is repaid. Pursuant to provisions in the Strategic Enterprise Regime, 25% of the base salaries and wages paid to Cameroonian employees is credited to GeoCam to further reduce taxable income and provide incentives to employ local workers.

In addition, Article 144 of the Mining Code now in effect calls for an ad valorem tax of 2.5% on metals. This is treated as a production tax expense and reduces net income for income tax purposes.

Based on interpretations of the Mining Code by Geovic and its Cameroonian attorney, Mr. Pierre Christian Nsegbe, value-added taxes will not be applied to Geovic’s operations during the exploration phase of the Cobalt-Nickel Project. The value added taxes will apply during the construction and production phase of the Cobalt Nickel Project and are expected to be recovered against exports and are not expected to have a major impact on the project economics.

Accessibility, Climate, Local Resources, Infrastructure, And Physiography

The closest town to the Cobalt-Nickel Project site is Lomie, at approximately 26 kilometers to the west – southwest. The closest railroad transport to the Cobalt-Nickel Project is at the town of Belabo, at a distance of approximately 250 kilometers. International airports and modern telecommunication facilities exist at Yaounde and Douala. Suitable shipping and receiving facilities exist at the international seaport of Douala. Driving from Yaounde to the Nkamouna Project takes approximately 8 hours.

Access to the Cobalt-Nickel Project site is from the seaport of Douala by a well-maintained provincial highway via Yaounde and Ayos. After Ayos and across the Nyong River, the highway to Central African Republic deteriorates rapidly to a well-traveled 90-kilometer per hour two-lane gravel road to Abong Mbang, with a population of approximately 30,000 people. This section of the road is currently prepared for paving. Abong Mbang is the provincial Division headquarters of the Prefect and main administrative and commercial center for the Hyaut Nyong Division. The town hosts a local trade school, service stations, hotels, restaurants and phone service. It is the main administrative center for the Ministry of Environment and Protection of Nature and the Ministry of Industry, Mining and Technological Development. Turning south from Abong Mbang towards Lomie, the road narrows and is frequented by log and lumber trucks over the next 127-kilometer distance to Lomie. The road from Lomie to Kongo village, the site of the GeoCam field camp, supports heavy log and lumber transports, as does the road from Kongo village to the project site.

50555656.12

Lomie is the Subdivision administrative center that hosts the Cobalt-Nickel Project and has been the staging area for Geovic’s activities. Lomie has about 3,500 inhabitants, a limited local electrical supply, and very basic services and supplies. There is new telephone service, but no airstrip or approved heliport, and only rudimentary medical facilities. Geovic’s field operations are based from the Kongo Camp, a fully-contained compound near the village of Kongo. The compound has adequate working and sleeping quarters, a diesel generator, satellite-phone facilities, diesel fuel storage, a kitchen with refrigerators, repair shop and sample preparation and storage facilities.

At present it takes about one hour to drive the 40 kilometers between Lomie and the Nkamouna Project site. The economy of Lomie is largely undeveloped, except for a large sawmill and surrounding timber harvesting operations. Local businesses include the Lomie Subdivision’s government headquarters of the sub-prefecture, police station, hospital, parochial schools, shops, three general mercantile stores and the Raffia Motel. Most business activity centers around logging and the local saw mill that is located east of town. Other activities include road maintenance, palm oil production, limited agricultural activities and general commerce. Lomie’s municipality has provided diesel electric power (200kW) to those who can afford it, since 1997. Lomie is the site of a number of domestic and international non-governmental organizations that monitor the 1.3 million acre World Heritage Dja Biosphere reserve and other reserves within the region.

From Lomie, the road passes east to the village of Echiambot where it branches northeast to the Edje River and Kongo village. The first mine site at the Nkamouna Project is located 10 kilometers north of this village. The second mining plateau is the Mada Project which is located 20 kilometres north of the Kongo village. The trip from Yaounde to Kongo village takes about 8 hours by vehicle.

Transport infrastructure in Lomie includes the Huat Nyong Express that carries people four times per day to Yaounde (18 per bus) and 10 busses per day to Abong Mbang. Motorcycle taxis transport individuals in the Lomie area. Geovic intends to provide, or arrange, scheduled bus and van service between the project and main towns and villages around the project site. Geovic will improve the existing roads and a small, private airstrip will be constructed to service project needs.

The climate of the region is classified as an “Equatorial Guinea” sub-type characterized by two main seasonal types, namely the “main wet” season and “main dry” season, and two minor seasonal types designated as “mini wet” and “mini dry.” The site is located on the northwestern margin of the Congo River tropical zone. The annual maximum monthly temperature ranges from 24° to 33° centigrade. The lowest daily minimum temperature recorded is 12° centigrade, but temperatures normally do not fall below 18° centigrade.

The average annual precipitation over a 32-year period is 1,580 millimeters and the humidity is typically high and evaporation rates high on an annual basis. Maximum annual precipitation measured to date totals 2,200 millimeters. The main wet season occurs between September and early November, and the main dry season occurs from November to May. The mini wet season lasts about eight weeks in March to May, and the mini dry season extends from June to mid-September. Limited amounts of rainfall occur throughout the year, except during the months of December and January. The average number of rain-free days at site was 229 and days receiving a total of at least 25 mm of precipitation at Nkamouna are 28 per year. Average monthly evaporation rates exceed rainfall during the two dry seasons. Data for 2004 show total precipitation at 1,820 millimeters, evaporation at 1,951 millimeters, for a net evaporation of 131 millimeters. The prevailing wind direction is from the south and southwest, and averages less than 4-kilometers per hour. Wind gusts rarely exceed 8 kilometers per hour, and are commonly undetectable beneath the tree canopy near the proposed Plant site. The operating season is year-round.

As currently envisioned, there are four waste and low-grade streams generated from the tailings disposal process. The two main waste streams from the metal recovery plant (the “MRP”) are manganese precipitate and the counter-current decantation (the “CCD”) leach tails. The manganese precipitate will be stored in a segregated area of the mine (55 tonnes per day (“tpd”)) and the CCD leach tails (1,385 tpd per day) will be co-disposed with the physical upgrades (the “PUG”) tails in the Napene Creek tailings storage facility (the “TSF”).

Geovic had previously planned to backfill all mine waste rock and process tailings into the mine backfill. This option appeared to have many advantages compared to disposing slurry tailings in a separate impoundment.

50555656.12

However, it also presented significant engineering, scheduling, environmental and other challenges during project development, operations and reclamation. As a result, the Napene Creek TSF became the preferred option.

An overall water balance was prepared from material balances for the PUG plant, MRP, and Napene Creek TSF. Except for the TSF, all flows are constant throughout the year. Knight Piesold and Co. (“Knight Piesold”) estimated water flows in and out of the TSF on a monthly basis, including excess water generated by consolidation of settled tailings, seasonal rainfall, and evaporation.

The overall water balance shows that the need to divert surplus water around the tailings dam is a rare event. Alternatively, tailings supernatant water can be accumulated during these periods to reduce the demand for Edje River water makeup. The overall water balance is simplified as all water in the mine and infrastructure areas are currently planned to be diverted around such facilities and placed in natural drainages. In this manner, the Napene Creek TSF water balance will be independent of external variations.

Demand for Edje River water over the project life was estimated from the overall water balance. Impound volumes were also estimated on a quarterly basis by adding solids volumes to water impound volumes.

Water available from the TSF for pumping back to the PUG plant and the MRP varies seasonally and yearly. The rate of water impounding in the TSF declines during the project life due to gradual consolidation of solids. The overall water balance shows that the need to divert surplus water around the tailings dam is a rare event. The overall water balance is simplified as all water in the mine and infrastructure areas will be diverted around such facilities and placed in natural drainages. In this manner, the Napene Creek TSF water balance will be independent of other project components.

To support the mining and milling operations at Nkamouna, a number of ancillary facilities will be required. These include energy generation, a mobile equipment maintenance shop, warehouse, reagent storage building, laboratory, and administration offices.

Combined Heat and Power (“CHP”) units fuelled by locally harvested wood will produce total project requirements of 2.5 MW of electrical energy and 11 MW of thermal energy. A temporary 300-man construction camp will be installed and used until permanent housing can be obtained to meet project operating requirements. On-site accommodations will be provided for expatriate staff, most of who will be scheduled for about 6 weeks on site and two to three weeks to their destination of choosing. Housing and other community assistance will be provided to local employees, who will be drawn from nearby villages.

Abundant water is available from shallow wells to be completed in the Edje River floodplain; however, much of the process water will be recycled from the TSF. Mining, processing and housing facilities will each be provided with sewage collection and treatment systems.

The vegetation in plateau areas is typical of an “evergreen equatorial forest” characterized by diverse endemic plant species. The forest area is stratified in three layers, including the 40-meter tall tree canopy characterized by broad-crown diameters and straight limbless trunks; shorter, more slender, fast-growing, narrow crown-diameter, fragile trees form the intermediate layer; and the scanty undergrowth layer consisting of vines, brush and ferns. Trees of local economic importance include Ayos, Sapelli, Wengive, Iroka, Bubinga, Azobe, and Obeche. Other diverse species occur in swamplands and patches of dense wet-substrate dominated valley floors.

Recent logging has occurred throughout most of the mineralized areas within the Mine Permit. The extent of this logging is documented on satellite images and by ground surveys. These logging activities are independent of Geovic’s operations and were part of pre-existing timber leases within the Mine Permit area.

The central part of the cobalt-nickel mineral district is dominated by a series of rolling upland plateaus that are isolated by several river systems that feed into the main Congo River drainage basin. Elevations in the province range from about 450 meters along the lower Dja River to 927 meters above sea level at Mount Guimbiri, located east of Abong Mbang. The local upland plateau in the vicinity of the Nkamouna mine site presents an elevation of about 700 meters.

50555656.12

The Nkamouna ore deposit is relatively flat and has an average depth of 15 meters. The majority of the deposit is situated downslope from the process plant and has a natural grade of approximately 5 % with upper elevations around 760 meters and lower elevations near 610 meters. The deposit is a crescent shape about 4 kilometers from east to west and 2 kilometers from north to south. The process plant is adjacent to the mine and near the top of a saddle at an approximate elevation of 700 meters above sea level.

The Mada deposit is relatively flat. There is a swamp and small depression in the center of the deposit. The deposit is a crescent shape about 8 kilometers from east to west and 14 kilometers from north to south. The perimeter of the deposit has an approximate elevation of 760 meters above sea level, with the lower central depression of 680 meters.

The Cobalt-Nickel Project consists of an enriched cobalt-nickel-manganese-iron lateritic deposit located within an extensive mineral province in southeastern Cameroon, Africa. Nkamouna, Mada, and several other nickeliferous laterite deposits in southeast Cameroon were first discovered and investigated by the United Nations Development Programme (the “UNDP”) during 1981-1986, in a cooperative project with the Cameroon Ministry of Mines, Water and Energy to evaluate mineral potential in southeastern Cameroon. Following a regional stream sediment geochemical survey which indicated the likely presence of laterite nickel mineralization, the UNDP project drilled eleven core holes in the Nkamouna area, which was the most accessible laterite area at that time.

Several of the UNDP holes intersected laterite and saprolite with interesting nickel and cobalt values. The first hole, KG-S-1, traversed 56 meters of lateritic profile and fresh serpentinite, with nickel values up to 1.00% and cobalt values up to 0.19% . Due to the remote location and the low nickel prices at the time, the discovery did not draw much attention.

William Buckovic became aware of the nickel discovery in 1988, subsequent to submitting a proposal in 1986 to explore for minerals to the Cameroon Ministry of Mines. No recorded exploration or mining had taken place on the property since the UNDP work. After assaying samples he was able to obtain from the deposit, Mr. Buckovic noted in 1994 a higher than typical cobalt:nickel ratio characterizing the Cameroon deposits. This high ratio was confirmed by the assay results from the UN coring program. Mr. Buckovic was also aware of recent advances in Australia and elsewhere in the hydrometallurgical processing of previously sub-economic nickel laterite deposits. As a result, in 1995 he helped form a new company, GeoCam, to investigate this unusual but potentially promising occurrence.

By 2004, Geovic had largely completed the reconnaissance sampling and had undertaken pitting and drilling patterns of varying spacing at Nkamouna where access was greater due to recent logging operations, with an eye toward defining deposit parameters for an eventual feasibility study. Between 1995 and 2003, Geovic carried out extensive pitting at Mada.

Most of the work at Nkamouna and Mada has been performed by Geovic employees and consultants on behalf of GeoCam. Early geological and sampling oversight was provided by Buckovic and by Duncan and Associates of Perth, Australia. Mintec, Inc., of Tucson, Arizona (“Mintec”), and by geologist and Qualified Person, Nikolai R. Burcham, provided oversight during 2003. Metallurgical and other testing has been performed from time to time by Bateman Engineering, Inc of Tucson, Arizona, METCON Research, Inc. of Tucson, Pittsburgh Metallurgical and Environmental Inc. (“PMET”) of Pittsburgh, Pennsylvania, Hazen Research of Golden, Colorado, Knight Piesold of Denver, Colorado, and others.

The Nkamouna and Mada properties are undeveloped, as are those of the adjacent laterite Plateaus.

Geology Setting

Regional Setting |

Southeastern Cameroon lies within a region of metamorphosed Proterozoic rocks ranging in age from 1800 to 600 million years and extending across parts of several west-central African countries. In southeastern Cameroon,

50555656.12

several assemblages of such metamorphic rocks have been mapped and named. In the Cobalt-Nickel Project area, the Mbalmayo-Bengbis Series, one of several “series” comprising the Intermediate Series, consists principally of chloritic and sericitic schists and quartzites. Also included in the series are extensive metamorphosed felsic, mafic volcanic and volcaniclastic rocks. These rocks are post-Eburnean (i.e. younger than 1800 million years) and are cut by basic dikes. The original depositional age of the sediments was probably 1800 to 1400 million years, with metamorphism to almandine-amphibolite facies occurring about 1200 million years ago, likely coincident with the Kibaran Orogeny.

The schists and quartzites contain inliers of ultramafic rock, which were probably emplaced long after deposition of the original sedimentary rocks. Due to poor exposures, the contact relations are unclear, but the ultramafic bodies appear to be emplaced along north-trending regional fractures, which apparently allowed emplacement of ultramafic rocks of deep-seated origin.

The region within a 300-km radius of the Cobalt-Nickel Project Area in Cameroon, Gabon, Congo, and Central African Republic has few producing mineral deposits and few with near-term production potential. Most of this region of west-central Africa is underlain by Proterozoic granite-gneiss-schist terrains, broadly similar to the rocks in the Cobalt-Nickel Project Area. Within the region, ultramafic rocks, the original source of the cobalt and nickel, are confined to the Cobalt-Nickel Project Area. There has been no previous production of minerals from the Cobalt-Nickel Project Area.

Alluvial gold is exploited on a small scale from stream gravels in various parts of Cameroon, Gabon, Congo, and Central African Republic. Few statistics are available because all production in the region is from artisanal sources. In the southwest part of the Central African Republic, alluvial gold is accompanied by small quantities of alluvial diamonds in streams which drain Cretaceous sandstone and conglomerates exposed further east. The Cretaceous formations do not extend into Cameroon.

Deposits of iron ore are reported to exist in south-central Cameroon, north of the Gabon border, but little information is available about these deposits. The UNDP also evaluated several iron ore and limestone deposits. At Belinga in northeast Gabon, a stratiform iron deposit contains several hundred million tonnes of 64% iron, but with high phosphorus content (+0.1% P). This deposit has not been exploited on an appreciable scale.

Small amounts of alluvial tin and rutile are extracted from streams in the region, also in quantities that are locally important to village economies but are not industrially significant. Limestone deposits occur in the Proterozoic rocks, about 50 km southeast of Lomie. These deposits were drilled by the UNDP in 1981, but they have not been exploited on a large scale.

Elsewhere in Cameroon, mining of non-fuel minerals is in its infancy, with one cement plant being the only sizeable mineral producer. Occurrences or resources of bauxite exist in northern and western Cameroon. An aluminium smelter near Douala processes only imported alumina. There is little in the way of a mining culture or infrastructure in the country at present.

The cobalt-nickel deposits are hosted in residual laterites which have formed by prolonged tropical weathering of serpentinites. Large areas of mineralized laterite, each several square kilometers in extent, have been preserved on low-relief mesas or plateaus underlain by ultramafic rocks that stand above the surrounding dissected lowlands. Nkamouna and Mada are two such plateaus. Most of the plateaus are underlain by ultramafic rocks, with some areas of schist, phyllite, and quartzite. The surrounding lowlands are underlain by schists, phyllites, quartzites, and meta-volcanics of the Intermediate Series. The bedrock geology at Nkamouna has been mapped by Geovic geologists through a combination of natural exposures, soil mapping, and, most importantly, observation of weathered or fresh rock encountered in pits and drillholes. Mapping of detailed structures, attitudes of foliation or fractures, etc. is generally not practical except in the deeper pits. Rock from pits, drillholes, and rare exposures indicate that the fresh underlying rock at Nkamouna is a pervasively-sheared serpentinite.

50555656.12

The bedrock geology at Mada has also been developed through a combination of natural exposures, soil mapping, and rock encountered in pits.

Most serpentinites form from parental ultramafic rocks, as a result of hydration and shearing at moderate temperatures, either during emplacement of the ultramafic or during post-emplacement tectonism. At Nkamouna, petrographic evidence suggests that the parent rock to the serpentinite was probably a dunite (rock containing +90 percent olivine). Minor amounts of chrysotile asbestos, a common accessory mineral in serpentinites, are reported from one pit in the Mada area located beneath the mineralized zone. Metasedimentary rocks (quartz-muscovite schist, phyllite, and quartzite) occupy the borders of the serpentinite, and also occur as inliers within the serpentinites. Locally, lateritic soils with schist fragments overlie serpentinite bedrock due to the gravity-induced creep of soils down-slope.

Nickeliferous laterite deposits in southeast Cameroon were first discovered and investigated by the UNDP during 1981-1986, in a cooperative project with the Cameroon Ministry of Mines, Water and Energy. Following a regional stream sediment geochemical survey which indicated the likely presence of laterite nickel mineralization, the UNDP project drilled eleven core holes in the Nkamouna area, which was the most accessible laterite area at that time.

Several of the UNDP holes intersected laterite and saprolite with interesting nickel and cobalt values. The first hole, KG-S-1, traversed 56 meters of lateritic profile and fresh serpentinite, with nickel values up to 1.00% and cobalt values up to 0.19% . Due to the remote location and the low nickel prices at the time, the discovery did not draw much attention.