QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on June 22, 2007

Registration No. 333-143481

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1/A

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

PARAGON SHIPPING INC.

(Exact name of Registrant as specified in its charter)

| Marshall Islands (State or other jurisdiction of incorporation or organization | 4412 (Primary Standard Industrial Classification Code Number) Voula Center 102-104 V. Pavlou Street Voula 16673 Athens, Greece (011) (30) (210) 891 4600 | Inapplicable (I.R.S. Employer Identification No.) | ||

| (Address, including zip code, and telephone number, including area code, of registrant's principal executive offices) | ||||

| Seward & Kissel LLP Attn: Gary J. Wolfe, Esq. One Battery Park Plaza New York, New York 10004 (212) 574-1200 (Name, address, including zip code, and telephone number, including area code, of agent for service) | ||||

Copies of communications to:

Gary J. Wolfe, Esq.

Seward & Kissel LLP

One Battery Park Plaza

New York, New York 10004

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are being offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ý

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Amount to be Registered(2) | Proposed Maximum Aggregate Price Per Unit(1) | Proposed Maximum Aggregate Offering Price(1)(2) | Amount of Registration Fee | |||||

|---|---|---|---|---|---|---|---|---|---|

| Class A Common Shares, par value $0.001 per share, to be sold by selling shareholders | 11,097,187 | $9.11 | $101,095,373.57 | $3,103.63 | |||||

| Warrants to be sold by selling shareholders | 1,849,531 | $4.46 | $ 8,248,908.26 | $ 253.24 | |||||

| Total | $109,344,281.83 | $3,356.87* | |||||||

- *

- Previously paid.

- (1)

- Bona fide estimate pursuant to Rule 457(a) solely for the purpose of computing the amount of the registration fee.

- (2)

- Includes common shares issuable on exercise of Warrants.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrants shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Information contained herein is subject to completion or amendment. A registration statement relating to these securities has been filed with the Securities and Exchange Commission. These securities may not be sold nor may offers to buy be accepted prior to the time the registration statement becomes effective. This prospectus shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of these securities in any State in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such State.

SUBJECT TO COMPLETION DATED JUNE 22, 2007

1,849,531 Warrants

and

11,097,187 Class A Common Shares

This prospectus relates to the resale by the selling shareholders named herein of the Warrants and the Class A Common Shares, including the Class A Common Shares issuable to the selling shareholders on exercise of the Warrants. This prospectus also covers the Class A Common Shares issuable on exercise of the Warrants by persons other than the selling shareholders identified in this prospectus that will be identified in one or more supplements to this prospectus.

We will receive no proceeds from the sale of any of our Class A Common Shares or Warrants by the selling shareholders. We will receive proceeds to the extent the Warrants are exercised. However, the holders of the Warrants are under no obligation to do so.

Our Class A Common Shares are not currently traded on any securities exchange or on the OTC Bulletin Board. We will apply to have our Class A Common Shares and Warrants qualified for trading on the OTC Bulletin Board following the effectiveness of the registration statement of which this prospectus is a part.

SEE "RISK FACTORS" BEGINNING ON PAGE 11 FOR A DISCUSSION OF RISKS THAT YOU SHOULD CONSIDER IN CONNECTION WITH AN INVESTMENT IN OUR CLASS A COMMON SHARES OR IN OUR WARRANTS.

The initial offering price for our Class A Common Shares will be $9.11 and for our Warrants will be $4.46. Once a public market is established for our Class A Common Shares and Warrants, the offering price of our Class A Common Shares and our Warrants by the selling shareholders will be based on prevailing market or privately negotiated prices.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this Prospectus is , 2007.

DRYBULK SHIPPING INDUSTRY DATA

The discussions contained under the heading "The International Drybulk Shipping Industry" have been reviewed by Drewry Shipping Consultants, Ltd., or Drewry, which has confirmed to us that they accurately describe the international drybulk shipping market as of the date of this prospectus.

The statistical and graphical information we use in this prospectus has been compiled by Drewry from its database. Drewry compiles and publishes data for the benefit of its clients. Its methodologies for collecting data, and therefore the data collected, may differ from those of other sources, and its data does not reflect all or even necessarily a comprehensive set of the actual transactions occurring in the market.

i

Our disclosure and analysis in this prospectus pertaining to our operations, cash flows and financial position, including, in particular, the likelihood of our success in developing and expanding our business, include forward-looking statements. Statements that are predictive in nature, that depend upon or refer to future events or conditions, or that include words such as "expects," "anticipates," "intends," "plans," "believes," "estimates," "projects," "forecasts," "may," "should," and similar expressions are forward-looking statements.

All statements in this prospectus that are not statements of historical fact are forward-looking statements. Forward-looking statements include, but are not limited to, such matters as:

- •

- our future operating or financial results;

- •

- global and regional political conditions;

- •

- our pending acquisitions, our business strategy and expected capital spending or operating expenses, including drydocking and insurance costs;

- •

- competition in the shipping industry;

- •

- statements about shipping market trends, including charter rates and factors affecting supply and demand;

- •

- our financial position and liquidity, including our ability to obtain financing in the future to fund capital expenditures, acquisitions and other general corporate activities; and

- •

- our expectations of the availability of vessels to purchase and the time it may take to construct new vessels, or vessels' useful lives.

Many of these statements are based on our assumptions about factors that are beyond our ability to control or predict and are subject to risks and uncertainties that are described more fully under the "Risk Factors" section of this registration statement. Any of these factors or a combination of these factors could materially affect future results of operations and the ultimate accuracy of the forward-looking statements. Factors that might cause future results to differ include, but are not limited to, the following:

- •

- changes in governmental rules and regulations or actions taken by regulatory authorities;

- •

- changes in economic and competitive conditions affecting our business;

- •

- potential liability from future litigation;

- •

- length and number of off-hire periods and dependence on third party managers; and

- •

- other factors discussed under the "Risk Factors" section of this registration statement.

You should not place undue reliance on forward-looking statements contained in this registration statement, because they are statements about events that are not certain to occur as described or at all. All forward-looking statements in this registration statement are qualified in their entirety by the cautionary statements contained in this registration statement. These forward-looking statements are not guarantees of our future performance, and actual results and future developments may vary materially from those projected in the forward-looking statements.

Except to the extent required by applicable law or regulation, we undertake no obligation to release publicly any revisions to such forward-looking statements to reflect events or circumstances after the date of this registration statement or to reflect the occurrence of unanticipated events.

ii

| | PAGE | |

|---|---|---|

| PROSPECTUS SUMMARY | 1 | |

THE OFFERING | 8 | |

RISK FACTORS | 11 | |

USE OF PROCEEDS | 25 | |

CAPITALIZATION | 31 | |

OUR DIVIDEND POLICY | 32 | |

SELECTED FINANCIAL AND OTHER DATA | 34 | |

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 36 | |

INDUSTRY | 49 | |

BUSINESS | 62 | |

MANAGEMENT | 75 | |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS | 79 | |

RELATED PARTY TRANSACTIONS | 81 | |

SELLING SHAREHOLDERS | 82 | |

PLAN OF DISTRIBUTION | 86 | |

DESCRIPTION OF OUR CAPITAL STOCK AND WARRANTS | 89 | |

MARSHALL ISLANDS COMPANY CONSIDERATIONS | 96 | |

MATERIAL U.S. AND MARSHALL ISLANDS INCOME TAX CONSIDERATIONS | 100 | |

OTHER EXPENSES OF DISTRIBUTION | 109 | |

LEGAL MATTERS | 110 | |

EXPERTS | 110 | |

WHERE YOU CAN FIND ADDITIONAL INFORMATION | 110 | |

ENFORCEABILITY OF CIVIL LIABILITIES | 111 | |

GLOSSARY OF SHIPPING TERMS | 112 | |

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS | F-1 |

iii

This section summarizes some of the key information and financial statements that appear later in this prospectus. You should review carefully the risk factors and the more detailed information and financial statements included in this registration statement. Unless the context otherwise requires, when used in this registration statement, the terms "Paragon," the "Company," "we," "our" and "us" refer to Paragon Shipping Inc. and its subsidiaries. Unless otherwise indicated, all references to currency amounts in this registration statement are in U.S. dollars.

We were incorporated in the Republic of the Marshall Islands in April 2006 to provide drybulk shipping services worldwide. We acquired our initial fleet of three Handymax and three Panamax drybulk carriers with the net proceeds of a private placement that closed in the fourth quarter of 2006, together with drawings under our senior secured credit facility and the proceeds of the sale by us of Class A Common Shares and Warrants to Innovation Holdings, S.A., or Innovation Holdings, a company beneficially owned by our founder and chief executive officer, Michael Bodouroglou, and members of his family. Accordingly, we have a limited history of operations. Allseas Marine S.A., or Allseas, a company controlled by Mr. Bodouroglou, provides the commercial and technical management of our vessels.

Our policy is to charter our vessels on time charters with durations of one to two years from the date of delivery, although we could engage in spot (voyage) charters or time charters with longer durations depending on our assessment of market conditions. From inception until December 31, 2006, our vessels achieved daily time charter equivalent rates of $25,460, and we generated net revenues of $4,729,160 and recorded net income of $461,764. We refer you to the section of this prospectus entitled "Forecasted Cash Available For Dividends, Reserves And Extraordinary Expenses For 2007" for information regarding the cash that we expect to have available to us during this period from the completion or our acquisition of our initial fleet.

Michael Bodouroglou, our founder and chief executive officer, has been involved in the shipping industry in various capacities for more than 25 years. Since 1993, Mr. Bodouroglou has co-owned and managed 30 vessels, including the six vessels in our initial fleet. Mr. Bodouroglou served as co-managing director of Eurocarriers S.A., or Eurocarriers, and Allseas, two ship management companies he co-founded in 1994 and 2000, respectively. Mr. Bodouroglou disposed of his interest in Eurocarriers in 2006. Since January 2006, Mr. Bodouroglou has been the sole managing director, and since September 2006 the sole owner, of Allseas, which currently manages eleven drybulk carriers, including the six vessels in our initial fleet.

We currently intend to pay quarterly dividends to the holders of our Class A Common Shares in February, May, August and November of each year in amounts substantially equal to our available cash from operations during the previous quarter, less cash expenses for that quarter and any reserves our board of directors determines we should maintain for reinvestment in our business. Our board of directors has declared a dividend in the amount of $0.4375 per Class A Common Share to shareholders of record on May 21, 2007 in respect of the period from the commencement of our operations through March 31, 2007.

From the closing of the private placement until the completion of a public offering of our Class A Common Shares that we may conduct in the future resulting in gross proceeds to us of at least $50 million, which we refer to as the subordination period, dividends will be declared on our Class B Common Shares in the same amount as on our Class A Common Shares but will not be payable on our Class B Common Shares until the later of (i) the conversion of our Class B Common Shares into Class A Common Shares and (ii) the payment date for dividends that were declared on the Class A Common Shares at the same time as dividends that were declared on the Class B Common Shares.

1

Accordingly, Innovation Holdings, as the holder of our Class B Common Shares, will receive the $0.4375 divided once its shares convert. For a more detailed summary of our dividend policy, please see "Our Dividend Policy" below.

We purchased the six secondhand Panamax and Handymax drybulk carriers in our initial fleet for an aggregate purchase price of $210.35 million, excluding certain pre-delivery expenses. We funded the acquisition of our initial fleet with the net proceeds of our private placement together with the net proceeds from the sale of Class A Common Shares and Warrants to Innovation Holdings, together with funds drawn under our senior secured credit facility. Please see "Business—our Fleet" for additional information regarding our fleet.

We have initially employed the vessels in our initial fleet under fixed rate time charters for approximately one to two-year periods from their respective delivery dates. The following table summarizes information about our initial fleet as of the date of this prospectus:

| | | | | | | Re-Delivery from Charterer(3) | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Vessel Name | Vessel Type | Year Built | Charterer Name | Charter Rate ($ per day)(1) | Vessel Delivery Date | |||||||||

| Earliest | Latest | |||||||||||||

| Blue Seas | Handymax | 1995 | STX Pan Ocean | 26,100 | October 4, 2006(2) | Aug. 21, 2007 | Nov. 20, 2007(4) | |||||||

Clean Seas | Handymax | 1995 | AS Klaveness | 20,000 | Jan. 8, 2007 | Oct. 24, 2008 | Feb. 24, 2009 | |||||||

Crystal Seas | Handymax | 1995 | San Juan Navigation | 24,000 | Jan 10, 2007 | Feb. 9, 2008 | July 8, 2008 | |||||||

Deep Seas | Panamax | 1999 | Morgan Stanley | 28,175 | October 12, 2006(2) | Aug. 28, 2007 | Nov. 28, 2007 | |||||||

Calm Seas | Panamax | 1999 | Morgan Stanley | 25,150 | Dec. 28, 2006 | Nov. 14, 2007 | Feb. 13, 2008 | |||||||

Kind Seas | Panamax | 1999 | Express Sea Transport | 23,600 | Dec. 21, 2006 | Sept. 4, 2008 | Feb. 18, 2009 | |||||||

- (1)

- This table shows gross charter rates and does not reflect commissions payable by us to third party chartering brokers and Allseas ranging from 2.5% to 6.25% including the 1.25% to Allseas.

- (2)

- The date shown represents the date our affiliate entities, Elegance Shipping Limited and Icon Shipping Limited, acquired the vessels. We acquired the vessels from our affiliates on December 28, 2006.

- (3)

- The date range provided represents the earliest and latest date on which the charterer may redeliver the vessel to us upon termination of the charter.

- (4)

- Upon the expiration of the current charter to STX Pan Ocean,Blue Seas is scheduled to be chartered to Korea Line Corp. at a gross daily rate of $28,500. The redelivery range for the charter to Korea Line Corp. is July 6, 2008 to February 14, 2009.

Please see "Business—Chartering" for additional information regarding our chartering arrangements.

Allseas is responsible for the technical and commercial management of our vessels. Allseas, which is based in Athens, Greece, was formed in 2000 as a ship management company and currently manages a fleet of 11 drybulk carriers including the six vessels in our fleet. The other five vessels are managed for affiliates of Allseas. We believe that Allseas has established a reputation in the international shipping industry for operating and maintaining a fleet with high standards of performance, reliability and safety.

2

Pursuant to separate management agreements that we have entered into with Allseas for each of our vessels, the terms of which have been approved by a majority of our independent directors, we are obligated to pay Allseas a technical management fee of $650 (based on a Euro/U.S. dollar exchange rate of 1.268:1.00) per vessel per day on a monthly basis in advance, pro rata for the calendar days the vessel is owned by us. The management fee is adjusted quarterly based on the Euro/U.S. dollar exchange rate as published by EFG Eurobank Ergasias S.A. two days prior to the end of the previous calendar quarter. The management fee will be increased commensurate with inflation on an annual basis, commencing on January 1, 2008 by reference to the official Greek inflation rate for the previous year, as published by the Greek National Statistical Office. We also pay Allseas a fee equal to 1.25% of the gross freight, demurrage and charter hire collected from the employment of our vessels. Allseas also earned a fee equal to 1.0% calculated on the price as stated in the relevant memorandum of agreement for any vessel bought or sold on our behalf, with the exception of the two vessels in our initial fleet that we acquired from entities affiliated with our founder and chief executive officer. Additional drybulk carriers that we may acquire in the future may be managed by Allseas or unaffiliated management companies. As of December 31, 2006, we have incurred $170,750 in management fees and $6,661 and $825,000 in chartering and vessel commissions, respectively, resulting in aggregate amount paid to Allseas by us during 2006 of $1,002,411.

We refer you to "Business—Our Fleet" and "Chartering" for additional information about the vessels in our fleet.

We believe that we possess a number of competitive strengths in our industry, including:

- •

- Experienced management team. Our chief executive officer has more than 25 years of experience in the shipping industry, and our chief financial officer has over 20 years of experience in ship finance and has been the chief financial officer of American Stock Exchange and Nasdaq Global Market listed shipping companies. Our chief operating officer and commercial development officer each have 19 years of experience in shipping and have been working with our chief executive officer for the last ten years and four years, respectively.

- •

- Efficient and dependable manager. We believe Allseas has established its reputation as an efficient and dependable vessel operator, without compromising on safety, maintenance and operating performance. To our knowledge no vessel has suffered a total or constructive loss or suffered material damage while managed by Allseas. Mr. Bodouroglou, while at Allseas or Eurocarriers, has managed or co-managed 30 vessels since its inception.

- •

- Strong customer relationships. Our manager, Allseas, has established relationships with leading charterers and a number of chartering, sales and purchase brokerage houses around the world. Since its founding, Allseas and its affiliates have maintained relationships with major national and private industrial users, commodity producers and traders, including Cargill International and Glencore International, which have repeatedly chartered vessels managed by Allseas or by Eurocarriers. We intend to keep our vessels fully employed and to secure repeat business with charterers by providing well-maintained vessels and dependable service.

- •

- Established banking relationships. Our founder and chief executive officer has current banking relationships with some of the leading banks in ship finance, including HSH Nordbank, HSBC and HVB Bank. This is evidenced by the fact that the Company has closed a $109.5 million senior secured loan facility with HSH Nordbank to finance the acquisition of the initial fleet. All the banks named above expressed in writing their interest in financing a portion of the acquisition of our initial fleet.

3

Our strategy is to invest in the drybulk carrier industry, to generate stable cash flow through time charters and to grow through acquisitions that we expect to be accretive to our cash flow. As part of our strategy, we intend to:

- •

- Focus on all segments of the drybulk carrier sector. We intend to develop a diversified fleet of drybulk carriers in various size categories, including Capesize, Panamax, Handymax and Handysize, although we have initially focused on the Panamax and Handymax sectors. Larger drybulk carriers, such as Capesize and Panamax vessels, have historically experienced a greater degree of freight rate volatility, while smaller drybulk carriers, such as Handymax and Handysize vessels, have historically experienced greater charter rate stability. Furthermore, a diversified drybulk carrier fleet will enable us to serve our customers in both major and minor bulk trades, and to gain a worldwide presence in the drybulk carrier market by assembling a fleet capable of servicing virtually all major ports and routes used for the seaborne transportation of key commodities and raw materials. Our vessels are able to trade worldwide in a multitude of trade routes carrying a wide range of cargoes for a number of industries.

- •

- Generate stable cash flow through time charters. Our strategy is to employ our vessels primarily under one and two-year time charters from the date of delivery that we believe provide us with a stable cash flow base during the term of these charters. As of May 1, 2007, the current average remaining duration of our charters ranges from 13 to 17 months based on the earliest and latest redelivery dates. We believe that factors governing the supply of and demand for drybulk carriers may cause charter rates for drybulk carriers to strengthen in the near term, thereby providing us opportunities to renew our time charters or enter into new time charters at similar or higher rates following the expiration of their respective terms. When our vessels are not employed on time charters, we may enter into short term spot charters.

- •

- Disciplined growth through accretive secondhand vessel acquisitions. We intend to grow our fleet through timely and selective acquisitions of secondhand drybulk carriers. We will seek to identify potential secondhand vessel acquisition candidates among various size categories of drybulk carriers. We intend to use our cash flow from operations, the proceeds of future equity offerings and senior secured credit facilities to acquire additional drybulk carriers that we believe will be accretive to our cash flow. We believe that secondhand vessels, when operated in a cost efficient manner, currently provide better returns as compared with more expensive newbuilding vessels.

Our ability to successfully implement our business strategy is dependant on our ability to manage a number of risks relating to our industry and our operations. These risks include the following:

- •

- Cyclical nature of charter hire rates. The cyclical nature of the drybulk shipping industry and the volatility in charter hire rates for our vessels, which may affect our ability to successfully charter our vessels in the future or renew existing charters at rates sufficient to allow us to meet our obligations or to pay dividends. Charter rates are affected by, among other factors, the supply of drybulk vessels in the global fleet, which is expected to increase by approximately 20% by 2010 based on current newbuilding orders. Although charter hire rates and vessel values decreased slightly during 2005 and the first half of 2006, since July 2006, charter rates have risen sharply and are currently at or near their historical highs and the value of second hand vessels is currently at record high levels.

- •

- Our operations are subject to international laws and regulations. Our business and the operation of our vessels are materially affected by applicable government regulation in the form of international conventions and national, state and local laws and regulations. Because such conventions, laws, and regulations are often revised, we cannot predict the ultimate cost of

4

- •

- Servicing our current and future debt limits funds available for other purposes, including the payment of dividends. To finance our future fleet expansion, we expect to incur additional secured debt. We must dedicate a portion of our cash flow from operations to pay the principal and interest on our debt. These payments limit funds otherwise available for working capital, capital expenditures and other purposes and may limit funds available for other purposes, including distributing cash to our shareholders, and our inability to service debt could lead to acceleration of our debt payments and foreclosure on our fleet.

- •

- We are a recently-formed company with a limited operating history. We are a recently-formed company and have a limited performance record, operating history and limited financial information upon which you can evaluate our operations or our ability to implement and achieve our business strategy or our ability to pay dividends.

complying with them or with additional regulations that may be applicable to our operations that are adopted in the future.

Prospective investors in our Class A Common Shares and Warrants should also carefully consider the factors set forth in the section of this prospectus entitled "Risk Factors" beginning on page 11.

Drybulk Shipping Industry Trends

The maritime shipping industry is fundamental to international trade with ocean-going vessels representing the most efficient and often the only method of transporting large volumes of many essential commodities, finished goods and crude and refined petroleum products between the continents and across the seas. It is a global industry whose performance is closely tied to the level of economic activity in the world.

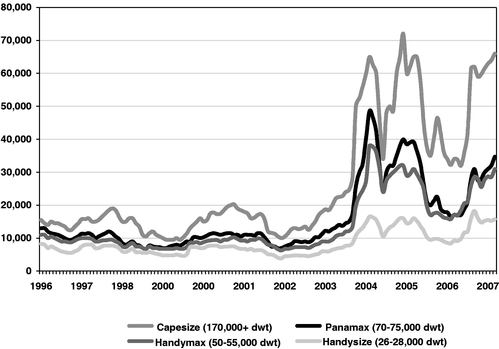

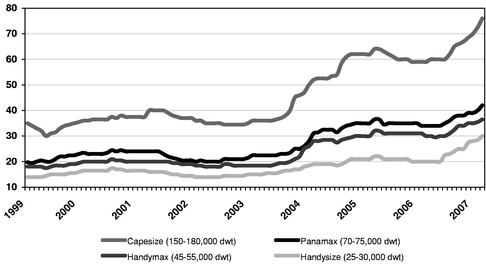

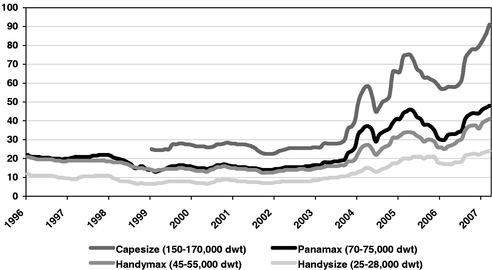

The drybulk shipping industry involves the carriage of bulk commodities. According to Drewry Shipping Consultants, Ltd., or Drewry, since the fourth quarter of 2002, the drybulk shipping industry has experienced the highest charter rates and vessel values in its modern history due to the favorable imbalance between the supply of drybulk carriers and demand for drybulk transportation service. Although charter hire rates and vessel values decreased slightly during 2005 and the first half of 2006, since July 2006, charter rates have risen sharply and are currently at or near their historical highs and the value of second hand vessels is currently at record high levels.

We were incorporated under the laws of the Republic of the Marshall Islands on April 26, 2006. Innovation Holdings currently holds 2,003,288 of our Class B Common Shares, representing approximately 15% of the aggregate of our total outstanding Class A Common Shares (excluding 185,656 Class A Common Shares issued to Cantor Fitzgerald & Co., CRT Capital Group LLC and Oppenheimer & Co., to whom we refer as the initial purchasers, as described below) and our total outstanding Class B Common Shares. We sold 9,062,000 of our Class A Common Shares and 1,812,400 of our Warrants, which were offered as a single unit, or a Unit, consisting of one Class A Common Share and one-fifth of one Warrant, at a price of $10.00 per Unit in our private placement. We completed the initial closing of our private placement on November 21, 2006 relating to the sale of 7,562,000 Units. Subsequent to the initial closing, the initial purchasers exercised an option we granted to them to purchase an additional 1,500,000 Units, which was completed on December 18, 2006. We received net proceeds from the private placement and the sale to Innovation Holdings in the amount of $109.5 million, after deducting offering fees and expenses of $3.6 million. In connection with our private placement, Innovation Holdings purchased an aggregate of 2,250,000 Units, consisting of 2,250,000 Class A Common Shares and 450,000 Warrants, at the same price per Unit paid by investors in the private placement. We also issued 185,656 Units, consisting of 185,656 Class A Common Shares and 37,131 Warrants, to the initial purchasers in the private placement for which we did not receive any

5

cash consideration. In addition, we issued 40,000 restricted Class A Common Shares pursuant to our equity incentive plan to certain individuals at the closing of the private placement. As a result of these transactions, Innovation Holdings owns approximately 31.5% of the aggregate of our total outstanding shares. Innovation Holdings also owns 450,000 Warrants to purchase our Class A Common Shares.

Our Class B Common Shares, which have not been issued to any shareholder other than Innovation Holdings, are subordinated to our Class A Common Shares until our completion of a public offering of our Class A Common Shares resulting in gross proceeds to us of at least $50 million, which we refer to as a qualified pubic offering. During the subordination period, dividends are declared on our Class B Common Shares in the same amount as on our Class A Common Shares but are not payable on our Class B Common Shares until the later of (i) the conversion of Class B Common Shares into Class A Common Shares and (ii) the payment date for dividends that were declared on the Class A Common Shares at the same time as dividends that were declared on the Class B Common Shares. The Class B Common Shares have no voting rights, and are subordinated to the Class A Common Shares with respect to ranking upon liquidation. Our Class B Common Shares will convert into Class A Common Shares upon the termination of the subordination period. Innovation Holdings acquired the Class B Common Shares for nominal consideration. We refer you to "Description of Capital Stock—Class B Common Shares" for additional information regarding the terms of our Class B Common Shares.

We maintain our principal executive offices at Voula Center, 102-104 V. Pavlou Street, Voula 16673, Athens, Greece. Our telephone number at that address is (011) (30) (210) 891 4600.

We intend to pay quarterly dividends to the holders of our Class A Common Shares in February, May, August and November of each year in amounts substantially equal to our available cash flow from operations during the previous quarter, less cash expenses for that quarter (principally vessel operating expenses and interest expense) and any reserves our board of directors determines we should maintain for reinvestment in our business. These reserves may cover, among other things, drydocking, intermediate and special surveys, liabilities and other obligations, interest expense and debt amortization, acquisitions of additional assets and working capital.

Our board of directors declared a dividend in the amount of $0.4375 per Class A Common Share to shareholders of record on May 21, 2007 in respect of the period from the commencement of our operations through March 31, 2007 which we paid to holders of our Class A Common Shares on May 31, 2007. Our board of directors has also declared a dividend with respect to the Class B Common Shares in the same amount as on our Class A Common Shares. However, we will not pay a dividend on our Class B Common Shares until the later of (i) the conversion of Class B Common Shares into Class A Common Shares and (ii) the payment date for dividends that were declared on the Class A Common Shares at the same time as dividends that were declared on the Class B Common Shares.

The declaration and payment of any dividend is subject to the discretion of our board of directors. The timing and amount of dividend payments will depend on our earnings, financial condition, cash requirements and availability, the restrictions in our senior secured credit facility, the provisions of Marshall Islands law affecting the payment of dividends and other factors. Because we are a holding company with no material assets other than the shares of our subsidiaries, which will directly own the vessels in our fleet, our ability to pay dividends will depend on the earnings and cash flow of our subsidiaries and their ability to pay dividends to us. We cannot assure you that, after the expiration or earlier termination of our charters, we will have any sources of income from which dividends may be paid. We refer you to "Our Dividend Policy" for additional information regarding our dividend policy.

6

Senior Secured Credit Facility

We have entered into a senior secured credit facility with HSH Nordbank AG of up to $109.5 million of which we drew down $108.25 million. Pursuant to the terms of the senior secured credit facility, we are permitted to draw up to 50% of the market value of the vessels in our initial fleet, up to the facility limit, to fund a portion of the acquisition of our initial fleet. The senior secured credit facility has a term of 3.5 years from the initial draw down date of December 21, 2006 and the amounts we draw under the senior secured credit facility are repayable in one balloon installment that are due 3.5 years from the initial borrowing date. The senior secured credit facility is secured by a first priority mortgage on our vessels as well as a first assignment of all earnings, insurances and cross default with each of our vessel owning subsidiaries. We refer you to "Senior Secured Credit Facility" for additional information regarding our senior secured credit facility.

7

| Outstanding Class A Common Shares offered by selling shareholders(1) | Up to 9,247,656 Class A Common Shares | |

Warrants offered by Selling Shareholders | Up to 1,849,531 Warrants | |

Class A Common Shares to be outstanding immediately after this offering(1) | 11,497,656 Class A Common Shares | |

Warrants to be outstanding immediately after this offering(1) | 2,299,531 Warrants | |

Use of proceeds | All of the shares of Class A Common Shares and Warrants offered hereby are being sold by the selling shareholders. We will not receive any proceeds from the sale of Class A Common Shares or Warrants by the selling shareholders. We will receive proceeds to the extent the Warrants are exercised. We intend to apply proceeds from those exercises, if any, to acquisitions, working capital and other corporate purposes. |

- (1)

- Assuming the sale of all Class A Common Shares and Warrants covered by this prospectus, and assuming no exercise of Warrants.

8

Paragon Shipping Inc. Summary Financial Data

The following table sets forth summary consolidated financial data and other operating data of Paragon Shipping Inc. The summary financial data in the table as of and for the period from inception (April 26, 2006) to December 31, 2006, is derived from the audited consolidated financial statements of Paragon Shipping Inc. We refer you to the footnotes to our consolidated financial statements for a discussion of the basis upon which our consolidated financial statements are presented. The data should be read in conjunction with the consolidated financial statements, related notes and other financial information included herein.

| | Period from inception (April 26, 2006) to December 31, 2006 | ||||

|---|---|---|---|---|---|

| INCOME STATEMENT DATA | |||||

| Net revenue | $ | 4,729,160 | |||

| Voyage expenses | 18,970 | ||||

| Vessel operating expenses | 559,855 | ||||

| Management fees charged by a related third party | 170,750 | ||||

| Depreciation | 1,066,527 | ||||

| General and administrative expenses (including share based compensation of $1,476,717)(1) | 1,782,429 | ||||

| Operating Income | 1,130,629 | ||||

| Interest and finance costs | (951,798 | ) | |||

| Unrealized loss on interest rate swap | (117,965 | ) | |||

| Interest income | 404,409 | ||||

| Foreign currency losses | (3,511 | ) | |||

| Net Income | $ | 461,764 | |||

| Income allocable to Class B common shares | (259,036 | ) | |||

| Income available to Class A common shares | $ | 202,728 | |||

| Earnings per Class A common share, basic | $ | 0.14 | |||

| Earnings per Class A common share, diluted | $ | 0.14 | |||

| Earnings per Class B common share, basic and diluted | $ | 0.00 | |||

| Weighted average number of Class A common shares, basic | 1,441,887 | ||||

| Weighted average number of Class A common shares, diluted | 1,442,639 | ||||

| Weighted average number of Class B common shares, basic and diluted | 1,842,381 | ||||

BALANCE SHEET DATA | As of December 31, 2006 | ||||

| Current assets, including cash | $ | 33,410,044 | |||

| Total assets | 188,239,859 | ||||

| Current liabilities | 4,249,625 | ||||

| Long-term debt | 77,437,500 | ||||

| Obligations for warrants | 10,266,969 | ||||

| Shareholders' equity | 96,285,765 | ||||

| Net cash provided by operating activities | 1,621,892 | ||||

| Net cash used in investing activities | (155,355,447 | ) | |||

| Net cash provided by financing activities | 186,065,403 | ||||

FLEET DATA | |||||

| Average number of vessels(2) | 0.74 | ||||

| Total voyage days for fleet(3) | 185 | ||||

| Total calendar days for fleet(4) | 185 | ||||

| Fleet utilization(5) | 100% | ||||

9

AVERAGE DAILY RESULTS | |||||

| Time charter equivalent(6) | $ | 25,460 | |||

| Vessel operating expenses(7) | 3,026 | ||||

| Management fees | 923 | ||||

| General and administrative expenses(8) | 9,635 | ||||

- (1)

- We paid salaries and consulting fees to our senior management and remuneration to our non-executive directors that in total amounted $175,627 for the year ended December 31, 2006. The share based compensation from inception (April 26, 2006) through December 31, 2006 amounted to $1,476,717 and is included in the general and administrative expenses.

- (2)

- Average number of vessels is the number of vessels that constituted our fleet for the relevant period, as measured by the sum of the number of days each vessel was a part of our fleet during the period divided by the number of calendar days in that period.

- (3)

- Total voyage days for fleet are the total days the vessels were in our possession for the relevant period net of off hire days associated with major repairs, drydocks or special or intermediate surveys.

- (4)

- Calendar days are the total days the vessels were in our possession for the relevant period including off hire days associated with major repairs, drydockings or special or intermediate surveys.

- (5)

- Fleet utilization is the percentage of time that our vessels were available for revenue generating voyage days, and is determined by dividing voyage days by fleet calendar days for the relevant period.

- (6)

- Time charter equivalent, or TCE, is a measure of the average daily revenue performance of the vessels in our fleet. Our method of calculating TCE is consistent with industry standards and is determined by dividing voyage net revenue less of voyage expenses by voyage days for the relevant time period. Voyage expenses primarily consist of port, canal and fuel costs that are unique to a particular voyage, which would otherwise be paid by the charterer under a time charter contract, as well as commissions. TCE is a standard shipping industry performance measure used primarily to compare period-to-period changes in a shipping company's performance despite changes in the mix of charter types (i.e., spot charters, time charters and bareboat charters) under which the vessels may be employed between the periods.

- (7)

- Daily vessel operating expenses, which includes crew costs, provisions, deck and engine stores, lubricating oil, insurance, maintenance and repairs is calculated by dividing vessel operating expenses by fleet calendar days for the relevant time period.

- (8)

- Daily general and administrative expense is calculated by dividing general and administrative expense by fleet calendar days for the relevant time period.

10

You should carefully consider the following material risk factors and all other information contained in this prospectus before deciding to invest in our Class A Common Shares or Warrants. If any of the following risks occur, our business, financial condition and results of operations could be materially and adversely affected.

Industry Specific Risk Factors

Charter hire rates for drybulk carriers may decrease in the future, which may adversely affect our earnings

The drybulk shipping industry is cyclical with attendant volatility in charter hire rates and profitability. The degree of charter hire rate volatility among different types of drybulk carriers has varied widely. Although charter hire rates decreased slightly during 2005 and the first half of 2006, since July 2006, charter rates have risen sharply and are currently at or near their historical highs. Because we generally charter our vessels pursuant to one-year time charters, we are exposed to changes in spot market rates for drybulk carriers and such changes may affect our earnings and the value of our drybulk carriers at any given time. We cannot assure you that we will be able to successfully charter our vessels in the future or renew existing charters at rates sufficient to allow us to meet our obligations or to pay dividends to our shareholders. Because the factors affecting the supply and demand for vessels are outside of our control and are unpredictable, the nature, timing, direction and degree of changes in industry conditions are also unpredictable.

Factors that influence demand for vessel capacity include:

- •

- demand for and production of drybulk products;

- •

- global and regional economic and political conditions;

- •

- the distance drybulk is to be moved by sea;

- •

- environmental and other regulatory developments; and

- •

- changes in seaborne and other transportation patterns.

The factors that influence the supply of vessel capacity include:

- •

- the number of newbuilding deliveries;

- •

- port and canal congestion;

- •

- the scrapping rate of older vessels;

- •

- vessel casualties; and

- •

- the number of vessels that are out of service.

We anticipate that the future demand for our drybulk carriers will be dependent upon continued economic growth in the world's economies, including China and India, seasonal and regional changes in demand, changes in the capacity of the global drybulk carrier fleet and the sources and supply of drybulk cargo to be transported by sea. The capacity of the global drybulk carrier fleet seems likely to increase and there can be no assurance that economic growth will continue. Adverse economic, political, social or other developments could have a material adverse effect on our business and operating results.

An over-supply of drybulk carrier capacity may lead to reductions in charter hire rates and profitability

The market supply of drybulk carriers has been increasing, and the number of drybulk carriers on order are near historic highs. These newbuildings were delivered in significant numbers starting at the

11

beginning of 2006 and are expected to continue to be delivered in significant numbers through 2007. As of September 2006, newbuilding orders had been placed for an aggregate of more than 20.0% of the current global dry bulk fleet, with deliveries expected during the next 36 months. An over-supply of drybulk carrier capacity may result in a reduction of charter hire rates. If such a reduction occurs, upon the expiration or termination of our vessels' current charters, such as during 2007, when the charters under which our vessels will be employed expire, we may only be able to recharter our vessels at reduced or unprofitable rates or we may not be able to charter these vessels at all.

An economic slowdown in the Asia Pacific region could have a material adverse effect on our business, financial position and results of operations

We anticipate a significant number of the port calls made by our vessels will involve the loading or discharging of drybulk commodities in ports in the Asia Pacific region. As a result, a negative change in economic conditions in any Asia Pacific country, but particularly in China, may have an adverse effect on our business, financial position and results of operations, as well as our future prospects. In recent years, China has been one of the world's fastest growing economies in terms of gross domestic product, which has had a significant impact on shipping demand. We cannot assure you that such growth will be sustained or that the Chinese economy will not experience negative growth in the future. Moreover, any slowdown in the economies of the United States, the European Union or certain Asian countries may adversely affect economic growth in China and elsewhere. Our business, financial position, results of operations, ability to pay dividends as well as our future prospects, will likely be materially and adversely affected by an economic downturn in any of these countries.

The market values of our vessels may decrease, which could limit the amount of funds that we can borrow under our senior secured credit facility or cause us to breach covenants in our senior secured credit facility and adversely affect our operating results

The fair market values of drybulk carriers have generally experienced high volatility. The market prices for secondhand drybulk carriers declined from historically high levels during 2005 and the first half of 2006, and have rose sharply in 2006 nearing historical highs and have remained firm in 2007. You should expect the market value of our vessels to fluctuate depending on general economic and market conditions affecting the shipping industry and prevailing charter hire rates, competition from other shipping companies and other modes of transportation, types, sizes and ages of vessels, applicable governmental regulations and the cost of newbuildings. If the market value of our fleet declines, we may not be able to draw down the full amount of our senior secured credit facility that we have entered into and we may not be able to obtain other financing or incur debt on terms that are acceptable to us or at all. Further, while we believe that the current aggregate market value of our drybulk vessels will be in excess of amounts required under the senior secured credit facility that we have entered into, a decrease in these values could cause us to breach some of the covenants that are contained in our senior secured credit facility and in future financing agreements that we may enter into from time to time. If we do breach such covenants and we are unable to remedy the relevant breach, our lenders could accelerate our debt and foreclose on our fleet. In addition, if the book value of one of our vessels is impaired due to unfavorable market conditions or a vessel is sold at a price below its book value, we would incur a loss that could adversely affect our operating results. Please see the section of this prospectus entitled "The International Drybulk Shipping Industry" for information concerning historical prices of drybulk carriers.

World events could affect our results of operations and financial condition

Terrorist attacks such as those in New York on September 11, 2001, the bombings in Spain on March 11, 2004 and in London on July 7, 2005 and the continuing response of the United States to these attacks, as well as the threat of future terrorist attacks in the United States or elsewhere,

12

continues to cause uncertainty in the world's financial markets and may affect our business, operating results and financial condition. The continuing conflict in Iraq may lead to additional acts of terrorism and armed conflict around the world, which may contribute to further economic instability in the global financial markets. These uncertainties could also adversely affect our ability to obtain additional financing on terms acceptable to us or at all. In the past, political conflicts have also resulted in attacks on vessels, mining of waterways and other efforts to disrupt international shipping, particularly in the Arabian Gulf region. Acts of terrorism and piracy have also affected vessels trading in regions such as the South China Sea. Any of these occurrences could have a material adverse impact on our operating results, revenues and costs.

Our operating results will be subject to seasonal fluctuations, which could affect our operating results and the amount of available cash with which we can pay dividends

We operate our vessels in markets that have historically exhibited seasonal variations in demand and, as a result, in charter hire rates. This seasonality may result in quarter to quarter volatility in our operating results, which could affect the amount of dividends that we pay to our shareholders from quarter to quarter. The drybulk carrier market is typically stronger in the fall and winter months in anticipation of increased consumption of coal and other raw materials in the northern hemisphere during the winter months. In addition, unpredictable weather patterns in these months tend to disrupt vessel scheduling and supplies of certain commodities. As a result, revenues of drybulk carrier operators in general have historically been weaker during the fiscal quarters ended June 30 and September 30, and, conversely, been stronger in fiscal quarters ended December 31 and March 31. While this seasonality is not likely to materially affect our operating results, it could materially affect our operating results and cash available for distribution to our shareholders as dividends in the future.

We are subject to regulation and liability under environmental laws that could require significant expenditures and affect our cash flows and net income and could subject us to increased liability under applicable law or regulation

Our business and the operation of our vessels are materially affected by government regulation in the form of international conventions and national, state and local laws and regulations in force in the jurisdictions in which the vessels operate, as well as in the countries of their registration. Because such conventions, laws, and regulations are often revised, we cannot predict the ultimate cost of complying with them or their impact on the resale prices or useful lives of our vessels. Additional conventions, laws and regulations may be adopted that could limit our ability to do business or increase the cost of our doing business and that may materially adversely affect our operations. We are required by various governmental and quasi-governmental agencies to obtain certain permits, licenses, certificates, and financial assurances with respect to our operations.

The operation of our vessels is affected by the requirements set forth in the United Nations' International Maritime Organization's International Management Code for the Safe Operation of Ships and Pollution Prevention, or ISM Code. The ISM Code requires shipowners, ship managers and bareboat charterers to develop and maintain an extensive "Safety Management System" that includes the adoption of a safety and environmental protection policy setting forth instructions and procedures for safe operation and describing procedures for dealing with emergencies. The failure of a shipowner or bareboat charterer to comply with the ISM Code may subject it to increased liability, may invalidate existing insurance or decrease available insurance coverage for the affected vessels and may result in a denial of access to, or detention in, certain ports.

13

The operation of drybulk carriers has certain unique operational risks which could affect our earnings and cash flow

The operation of certain ship types, such as drybulk carriers, has certain unique risks. With a drybulk carrier, the cargo itself and its interaction with the vessel can be an operational risk. By their nature, drybulk cargoes are often heavy, dense, easily shifted, and react badly to water exposure. In addition, drybulk carriers are often subjected to battering treatment during unloading operations with grabs, jackhammers (to pry encrusted cargoes out of the hold) and small bulldozers. This treatment may cause damage to the vessel. Vessels damaged due to treatment during unloading procedures may be more susceptible to breach to the sea. Hull breaches in drybulk carriers may lead to the flooding of the vessels' holds. If a drybulk carrier suffers flooding in its forward holds, the bulk cargo may become so dense and waterlogged that its pressure may buckle the vessel's bulkheads leading to the loss of a vessel. If we are unable to adequately maintain our vessels we may be unable to prevent these events. Any of these circumstances or events could negatively impact our business, financial condition, results of operations and ability to pay dividends. In addition, the loss of any of our vessels could harm our reputation as a safe and reliable vessel owner and operator.

Maritime claimants could arrest one or more of our vessels, which could interrupt our cash flow

Crew members, suppliers of goods and services to a vessel, shippers of cargo and other parties may be entitled to a maritime lien against a vessel for unsatisfied debts, claims or damages. In many jurisdictions, a claimant may seek to obtain security for its claim by arresting a vessel through foreclosure proceedings. The arrest or attachment of one or more of our vessels could interrupt our cash flow and require us to pay large sums of money to have the arrest or attachment lifted. In addition, in some jurisdictions, such as South Africa, under the "sister ship" theory of liability, a claimant may arrest both the vessel which is subject to the claimant's maritime lien and any "associated" vessel, which is any vessel owned or controlled by the same owner. Claimants could attempt to assert "sister ship" liability against one vessel in our fleet for claims relating to another of our vessels.

Governments could requisition our vessels during a period of war or emergency, resulting in a loss of earnings

A government could requisition one or more of our vessels for title or for hire. Requisition for title occurs when a government takes control of a vessel and becomes her owner, while requisition for hire occurs when a government takes control of a vessel and effectively becomes her charterer at dictated charter rates. Generally, requisitions occur during periods of war or emergency, although governments may elect to requisition vessels in other circumstances. Although we would be entitled to compensation in the event of a requisition of one or more of our vessels, the amount and timing of payment would be uncertain. Government requisition of one or more of our vessels may negatively impact our revenues and reduce the amount of cash we have available for distribution as dividends to our shareholders.

Company Specific Risk Factors

We are a recently-formed company with no history of operations on which investors may assess our performance or our ability to pay dividends

We are a recently-formed company and have no performance record, operating history or historical financial statements upon which you can evaluate our operations or our ability to implement and achieve our business strategy or our ability to pay dividends. We cannot assure you that we will be successful in implementing our business strategy.

14

Our earnings may be adversely affected if we do not successfully employ our vessels

We employ our drybulk carriers on one and two-year time charters. Period charters provide relatively steady streams of revenue, but vessels committed to period charters may not be available for spot voyages during periods of increasing charter hire rates, when spot voyages might be more profitable. Charter hire rates for drybulk carriers are volatile, and in the past charter hire rates for drybulk carriers have declined below operating costs of vessels. If our vessels become available for employment in the spot market or under new period charters during periods when market prices have fallen, we may have to employ our vessels at depressed market prices, which would lead to reduced or volatile earnings. We cannot assure you that future charter hire rates will enable us to operate our drybulk carriers profitably.

Investment in derivative instruments such as freight forward agreements could result in losses

From time to time, we may take positions in derivative instruments including freight forward agreements, or FFAs. FFAs and other derivative instruments may be used to hedge a vessel owner's exposure to the charter market by providing for the sale of a contracted charter rate along a specified route and period of time. Upon settlement, if the contracted charter rate is less than the average of the rates, as reported by an identified index, for the specified route and time period, the seller of the FFA is required to pay the buyer an amount equal to the difference between the contracted rate and the settlement rate, multiplied by the number of days in the specified period. Conversely, if the contracted rate is greater than the settlement rate, the buyer is required to pay the seller the settlement sum. If we take positions in FFAs or other derivative instruments and do not correctly anticipate charter rate movements over the specified route and time period, we could suffer losses in the settling or termination of the FFA. This could adversely affect our results of operation and cash flow.

Our charterers may terminate or default on their charters, which could adversely affect our results of operations and cash flow

Our charters may terminate earlier than the dates indicated in this registration statement. The terms of our charters vary as to which events or occurrences will cause a charter to terminate or give the charterer the option to terminate the charter, but these generally include a total or constructive total loss of the related vessel, the requisition for hire of the related vessel or the failure of the related vessel to meet specified performance criteria. In addition, the ability of each of our charterers to perform its obligations under a charter will depend on a number of factors that are beyond our control. These factors may include general economic conditions, the condition of the drybulk shipping industry, the charter rates received for specific types of vessels and various operating expenses. The costs and delays associated with the default by a charterer of a vessel may be considerable and may adversely affect our business, results of operations, cash flows and financial condition and our ability to pay dividends.

We cannot predict whether our charterers will, upon the expiration of their charters, recharter our vessels on favorable terms or at all. If our charterers decide not to re-charter our vessels, we may not be able to recharter them on terms similar to the terms of our current charters or at all. In the future, we may also employ our vessels on the spot charter market, which is subject to greater rate fluctuation than the time charter market.

If we receive lower charter rates under replacement charters or are unable to recharter all of our vessels, the amounts available, if any, to pay dividends to our shareholders may be significantly reduced or eliminated.

15

We may be unable to effectively manage our growth

We intend to continue to grow our fleet. Our growth will depend on:

- •

- locating and acquiring suitable drybulk carriers;

- •

- identifying and consummating acquisitions or joint ventures;

- •

- integrating any acquired business successfully with our existing operations;

- •

- enhancing our customer base;

- •

- managing our expansion; and

- •

- obtaining required financing.

Growing any business by acquisition presents numerous risks such as undisclosed liabilities and obligations, difficulty experienced in obtaining additional qualified personnel and managing relationships with customers and suppliers and integrating newly acquired operations into existing infrastructures. We cannot give any assurance that we will be successful in executing our growth plans or that we will not incur significant expenses and losses in connection therewith.

The expansion of our fleet may impose significant additional responsibilities on our management and staff, and the management and staff of Allseas, and may necessitate that we, and they, increase the number of personnel. Allseas may have to increase its customer base to provide continued employment for our fleet, and such costs will be passed on to us by Allseas.

We may be unable to attract and retain key management personnel and other employees in the shipping industry, which may negatively affect the effectiveness of our management and our results of operations

Our success depends to a significant extent upon the abilities and efforts of our management team. We have entered into employment agreements with each of our founder and chief executive officer, Michael Bodouroglou, our chief operating officer, George Skrimizeas, and our chief financial officer, Christopher Thomas, for work performed in Greece and separate consulting agreements with companies owned by each of them for work performed outside of Greece. Our success will depend upon our ability to hire and retain key members of our management team. The loss of any of these individuals could adversely affect our business prospects and financial condition. Difficulty in hiring and retaining personnel could adversely affect our business, results of operations and ability to pay dividends. We do not intend to maintain "key man" life insurance on any of our officers.

We are entirely dependent on Allseas to manage and charter our fleet

The only employees we currently have are Mr. Bodouroglou, our chief executive officer, George Skrimizeas, our chief operating officer, Christopher Thomas, our chief financial officer, and Anthony Smith, our commercial development officer, and we currently have no plans to hire additional employees. We currently subcontract the commercial and technical management of our fleet, including crewing, maintenance and repair, to Allseas, the loss of Allseas' services or its failure to perform its obligations to us could materially and adversely affect the results of our operations. Although we may have rights against Allseas if it defaults on its obligations to us, you will have no recourse directly against Allseas. Further, we expect that we will need to seek approval from our lenders to change our commercial and technical manager. Allseas will also be providing similar services for vessels owned by other shipping companies including companies with which they are affiliated. These responsibilities and relationships could create conflicts of interest between Allseas' performance of its obligations to us, on the one hand, and Allseas' performance of its obligations to its other clients on the other hand. These conflicts may arise in connection with the crewing, supply provisioning and operations of the vessels in our fleet versus vessels owned by other clients of Allseas. In particular, Allseas may give preferential

16

treatment to vessels owned by other clients whose arrangements provide for greater economic benefit to Allseas. These conflicts of interest may have an adverse effect on our results of operations.

Allseas is a privately held company and there is little or no publicly available information about it

The ability of Allseas to continue providing services for our benefit will depend in part on its own financial strength. Circumstances beyond our control could impair Allseas' financial strength, and because it is privately held it is unlikely that information about its financial strength would become public unless Allseas began to default on its obligations. As a result, an investor in our shares might have little advance warning of problems affecting Allseas, even though these problems could have a material adverse effect on us.

Our founder and chief executive officer has affiliations with Allseas which may create conflicts of interest

Our founder and chief executive officer is the beneficial owner of all of the issued and outstanding capital stock of Allseas. These responsibilities and relationships could create conflicts of interest between us, on the one hand, and Allseas, on the other hand. These conflicts may arise in connection with the chartering, purchase, sale and operations of the vessels in our fleet versus vessels managed for other companies affiliated with Allseas and Mr. Bodouroglou. Allseas may give preferential treatment to vessels that are beneficially owned by related parties because Mr. Bodouroglou and members of his family may receive greater economic benefits. In particular, Allseas currently provides management services to five drybulk carriers, other than the vessels in our initial fleet, that are owned by entities affiliated with Mr. Bodouroglou, and such entities may acquire additional vessels that will compete with our vessels in the future. Mr. Bodouroglou has granted to us the right to purchase the remaining five vessels for which Allseas provides management services as well as a right of first refusal over future vessels that he or entities affiliated with him may seek to acquire in the future. However, we may not exercise our right to acquire all or any of these vessels in the future, and such vessels may compete with our fleet. These conflicts of interest may have an adverse effect on our results of operations.

In the highly competitive international drybulk shipping industry, we may not be able to compete for charters with new entrants or established companies with greater resources

We employ our vessels in a highly competitive market that is capital intensive and highly fragmented. Competition arises primarily from other vessel owners, some of whom have substantially greater resources than we do. Competition for the transportation of drybulk cargoes can be intense and depends on price, location, size, age, condition and the acceptability of the vessel and its managers to the charters. Due in part to the highly fragmented market, competitors with greater resources could enter and operate larger fleets through consolidations or acquisitions that may be able to offer better prices and fleets than we are able to offer.

Our vessels may suffer damage and we may face unexpected drydocking costs, which could affect our cash flow and financial condition

If our vessels suffer damage, they may need to be repaired at a drydocking facility. The costs of drydocking repairs are unpredictable and can be substantial. We may have to pay drydocking costs that our insurance does not cover. The loss of earnings while these vessels are being repaired and repositioned, as well as the actual cost of these repairs, would decrease our earnings.

Purchasing and operating previously owned, or secondhand, drybulk carriers may result in increased operating costs and off-hire days for our vessels, which could adversely affect our earnings

Our inspection of secondhand vessels prior to purchase does not provide us with the same knowledge about their condition and cost of any required (or anticipated) repairs that we would have

17

had if these vessels had been built for and operated exclusively by us. While we normally inspect secondhand vessels prior to purchase, this does not provide us with the same knowledge about their condition that we would have had if these vessels had been built for and operated exclusively by us, and accordingly, we may not discover defects or other problems with such vessels prior to purchase. If this were to occur, such hidden defects or problems, when detected, may be expensive to repair, and if not detected, may result in accidents or other incidents for which we may become liable to third parties. Generally, we do not receive the benefit of Warranties on secondhand vessels.

The aging of our fleet may result in increased operating costs in the future, which could adversely affect our earnings

In general, the costs to maintain a drybulk carrier in good operating condition increase with the age of the vessel. The average age of the vessels comprising our initial fleet is approximately 9.2 years. Older vessels are typically less fuel-efficient and more costly to maintain than more recently constructed drybulk carriers due to improvements in engine technology. Cargo insurance rates increase with the age of a vessel, making older vessels less desirable to charterers.

Rising fuel prices may adversely affect our profits

The cost of fuel is a significant factor in negotiating charter rates. As a result, an increase in the price of fuel beyond our expectations may adversely affect our profitability. The price and supply of fuel is unpredictable and fluctuates based on events outside our control, including geo-political developments, supply and demand for oil, actions by members of the Organization of the Petroleum Exporting Countries and other oil and gas producers, war and unrest in oil producing countries and regions, regional production patterns and environmental concerns and regulations.

We cannot assure you that we will pay dividends

Our policy is to pay quarterly dividends in February, May, August and November of each year as described in "Our Dividend Policy." However, we may incur other expenses or liabilities that would reduce or eliminate the cash available for distribution as dividends. Our loan agreements, including our senior secured credit facility, may also prohibit our declaration and payment of dividends under some circumstances.

In addition, the declaration and payment of dividends will be subject at all times to the discretion of our board of directors. The timing and amount of dividends will depend on our earnings, financial condition, cash requirements and availability, fleet renewal and expansion, restrictions in our loan agreements, the provisions of Marshall Islands law affecting the payment of dividends and other factors. Marshall Islands law generally prohibits the payment of dividends other than from surplus or while a company is insolvent or would be rendered insolvent upon the payment of such dividends. There can be no assurance that dividends will be paid in the anticipated amounts and frequency set forth in this registration statement or at all.

We are a holding company, and we will depend on the ability of our subsidiaries to distribute funds to us in order to satisfy our financial obligations or to make dividend payments

We are a holding company and our subsidiaries, all of which are, wholly-owned by us either directly or indirectly, will conduct all of our operations and own all of our operating assets. We will have no significant assets other than the equity interests in our wholly-owned subsidiaries. As a result, our ability to make dividend payments depends on our subsidiaries and their ability to distribute funds to us. If we are unable to obtain funds from our subsidiaries, our board of directors may exercise its discretion not to pay dividends.

18

Anti-takeover provisions in our amended and restated articles of incorporation could make it difficult for our shareholders to replace or remove our current board of directors or could have the effect of discouraging, delaying or preventing a merger or acquisition, which could adversely affect the market price of our common shares

Several provisions of our amended and restated articles of incorporation and bylaws could make it difficult for our shareholders to change the composition of our board of directors in any one year, preventing them from changing the composition of our management. In addition, the same provisions may discourage, delay or prevent a merger or acquisition that shareholders may consider favorable.

These provisions include those that:

- •

- authorize our board of directors to issue "blank check" preferred stock without shareholder approval;

- •

- provide for a classified board of directors with staggered, three-year terms;

- •

- prohibit cumulative voting in the election of directors;

- •

- authorize the removal of directors only for cause and only upon the affirmative vote of the holders of at least 662/3% of the outstanding common shares entitled to vote for those directors; and

- •

- restrict business combinations with interested shareholders.

These anti-takeover provisions could substantially impede the ability of shareholders to benefit from a change in control and, as a result, may adversely affect the market price of our common shares and your ability to realize any potential change of control premium.

Servicing future debt would limit funds available for other purposes such as the payment of dividends

To finance our future fleet expansion, we expect to incur additional secured debt. While we do not intend to use operating cash to pay down principal, we must dedicate a portion of our cash flow from operations to pay the principal and interest on our debt. These payments limit funds otherwise available for working capital, capital expenditures and other purposes. We will have to incur debt in order to acquire and later expand our fleet, which could increase our ratio of debt to equity. The need to service our debt may limit funds available for other purposes, including distributing cash to our shareholders, and our inability to service debt could lead to acceleration of our debt and foreclosure on our fleet.

Our senior secured credit facility contains restrictive covenants that may limit our liquidity and corporate activities

Our senior secured credit facility imposes operating and financial restrictions on us. These restrictions may limit our ability to:

- •

- incur additional indebtedness;

- •

- create liens on our assets;

- •

- sell capital stock of our subsidiaries;

- •

- make investments;

- •

- engage in mergers or acquisitions;

- •

- pay dividends;

- •

- make capital expenditures;

19

- •

- compete effectively to the extent our competitors are subject to less onerous financial restrictions;

- •

- change the management of our vessels or terminate or materially amend the management agreement relating to each vessel; and

- •

- sell our vessels.

Therefore, our discretion is limited because we may need to obtain consent from our lenders in order to engage in certain corporate actions. Our lenders' interests may be different from ours, and we cannot guarantee that we will be able to obtain our lenders' consent when needed. This may prevent us from taking actions that are in our shareholders' best interest.

Our senior secured credit facility imposes certain conditions on the payment of dividends