UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

| Form 10-K |

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the fiscal year ended December 31, 2016

or

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the transition period from to .

Commission File Number 001-35500

Oaktree Capital Group, LLC (Exact name of registrant as specified in its charter) | ||

| Delaware | 26-0174894 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

333 South Grand Avenue, 28th Floor Los Angeles, CA 90071 Telephone: (213) 830-6300 (Address, zip code, and telephone number, including area code, of registrant’s principal executive offices) | ||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered |

| Class A units representing limited liability company interests | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 and 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter periods that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer x | Accelerated filer ¨ | |

Non-accelerated filer ¨ | Smaller reporting company ¨ | |

| (Do not check if a smaller reporting company) | ||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the Class A units of the registrant held by non-affiliates as of June 30, 2016 was approximately $2.6 billion.

As of February 21, 2017, there were 62,994,591 Class A units and 91,547,128 Class B units of the registrant outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

TABLE OF CONTENTS

| Page | ||

| PART I. | ||

| PART II. | ||

| PART III. | ||

| PART IV. | ||

2

FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements within the meaning of Section 27A of the U.S. Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”), which reflect our current views with respect to, among other things, our future results of operations and financial performance. In some cases, you can identify forward-looking statements by words such as “anticipate,” “approximately,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “outlook,” “plan,” “potential,” “predict,” “seek,” “should,” “will” and “would” or the negative version of these words or other comparable or similar words. These statements identify prospective information. Important factors could cause actual results to differ, possibly materially, from those indicated in these statements. Forward-looking statements are based on our beliefs, assumptions and expectations of our future performance, taking into account all information currently available to us. Such forward-looking statements are subject to risks and uncertainties and assumptions relating to our operations, financial results, financial condition, business prospects, growth strategy and liquidity, including, but not limited to, changes in our anticipated revenue and income, which are inherently volatile; changes in the value of our investments; the pace of our raising of new funds; changes in assets under management; the timing and receipt of, and impact of taxes on, carried interest; distributions from and liquidation of our existing funds; the amount and timing of distributions on our Class A units; changes in our operating or other expenses; the degree to which we encounter competition; and general political, economic and market conditions. The factors listed in the item captioned “Risk Factors” in this annual report provide examples of risks, uncertainties and events that may cause our actual results to differ materially from the expectations described in our forward-looking statements.

Forward-looking statements speak only as of the date of this annual report. Except as required by law, we do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise.

MARKET AND INDUSTRY DATA

This annual report includes market and industry data and forecasts that are derived from independent reports, publicly available information, various industry publications, other published industry sources and our internal data, estimates and forecasts. Independent reports, industry publications and other published industry sources generally indicate that the information contained therein was obtained from sources believed to be reliable. We have not commissioned, nor are we affiliated with, any of the sources cited herein.

Our internal data, estimates and forecasts are based upon information obtained from investors in our funds, partners, trade and business organizations and other contacts in the markets in which we operate and our management’s understanding of industry conditions.

3

In this annual report, unless the context otherwise requires:

“Oaktree,” “OCG,” “we,” “us,” “our” or “our company” refers to Oaktree Capital Group, LLC and, where applicable, its subsidiaries and affiliates.

“Oaktree Operating Group,” or “Operating Group,” refers collectively to the entities in which we have a minority economic interest and indirect control that either (i) act as or control the general partners and investment advisers of our funds or (ii) hold interests in other entities or investments generating income for us.

“OCGH” refers to Oaktree Capital Group Holdings, L.P., a Delaware limited partnership, which holds an interest in the Oaktree Operating Group and all of our Class B units.

“OCGH unitholders” refers collectively to our senior executives, current and former employees and certain other investors who hold interests in the Oaktree Operating Group through OCGH.

“2007 Private Offering” refers to the sale completed on May 25, 2007 of 23,000,000 of our Class A units to qualified institutional buyers (as defined in the Securities Act) in a transaction exempt from the registration requirements of the Securities Act. Prior to our initial public offering, these Class A units traded on a private over-the-counter market developed by Goldman, Sachs & Co. for tradable unregistered equity securities.

“assets under management,” or “AUM,” generally refers to the assets we manage and equals the NAV (as defined below) of the assets we manage, the leverage on which management fees are charged, the undrawn capital that we are entitled to call from investors in our funds pursuant to their capital commitments, and the aggregate par value of collateral assets and principal cash held by our collateralized loan obligation vehicles (“CLOs”). Our AUM amounts include AUM for which we charge no management fees. Our definition of AUM is not based on any definition contained in our operating agreement or the agreements governing the funds that we manage. Our calculation of AUM and the two AUM-related metrics described below may not be directly comparable to the AUM metrics of other investment managers.

| • | “management fee-generating assets under management,” or “management fee-generating AUM,” is a forward-looking metric and reflects the beginning AUM on which we will earn management fees in the following quarter, as more fully described in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Segment and Operating Metrics—Assets Under Management—Management Fee-generating Assets Under Management.” |

| • | “incentive-creating assets under management,” or “incentive-creating AUM,” refers to the AUM that may eventually produce incentive income, as more fully described in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Segment and Operating Metrics—Assets Under Management—Incentive-creating Assets Under Management.” |

“consolidated funds” refers to the funds and CLOs that Oaktree is required to consolidate as of the applicable reporting date.

“funds” refers to investment funds and, where applicable, CLOs and separate accounts that are managed by us or our subsidiaries.

“initial public offering” refers to the listing of our Class A units on the New York Stock Exchange on April 12, 2012 whereby Oaktree sold 7,888,864 Class A units and selling unitholders sold 954,159 Class A units.

“Intermediate Holding Companies” collectively refers to the subsidiaries wholly owned by us.

“net asset value,” or “NAV,” refers to the value of all the assets of a fund (including cash and accrued interest and dividends) less all liabilities of the fund (including accrued expenses and any reserves established by us, in our discretion, for contingent liabilities) without reduction for accrued incentives (fund level) because they are reflected in the partners’ capital of the fund.

“Relevant Benchmark” refers, with respect to:

| • | our U.S. High Yield Bond strategy, to the Citigroup U.S. High Yield Cash-Pay Capped Index; |

| • | our Global High Yield Bond strategy, to an Oaktree custom global high yield index that represents 60% BofA Merrill Lynch High Yield Master II Constrained Index and 40% BofA Merrill Lynch Global Non-Financial High Yield European Issuers 3% Constrained, ex-Russia Index – USD Hedged from inception |

4

through December 31, 2012, and the BofA Merrill Lynch Non-Financial Developed Markets High Yield Constrained Index – USD Hedged thereafter;

| • | our European High Yield Bond strategy, to the BofA Merrill Lynch Global Non-Financial High Yield European Issuers excluding Russia 3% Constrained Index (USD Hedged); |

| • | our U.S. Senior Loan strategy (with the exception of the closed-end funds), to the Credit Suisse Leveraged Loan Index; |

| • | our European Senior Loan strategy, to the Credit Suisse Western European Leveraged Loan Index (EUR Hedged); |

| • | our U.S. Convertible Securities strategy, to an Oaktree custom convertible index that represents the Credit Suisse Convertible Securities Index from inception through December 31, 1999, the Goldman Sachs/Bloomberg Convertible 100 Index from January 1, 2000 through June 30, 2004, and the BofA Merrill Lynch All U.S. Convertibles Index thereafter; |

| • | our non-U.S. Convertible Securities strategy, to an Oaktree custom non-U.S. convertible index that represents the JACI Global ex-U.S. (Local) Index from inception through December 31, 2014 and the Thomson Reuters Global Focus ex-U.S. (USD hedged) Index thereafter; |

| • | our High Income Convertible Securities strategy, to the Citigroup U.S. High Yield Market Index; and |

| • | our Emerging Markets Equities strategy, to the Morgan Stanley Capital International Emerging Markets Index (Net). |

“senior executives” refers collectively to Howard S. Marks, Bruce A. Karsh, Jay S. Wintrob, John B. Frank, David M. Kirchheimer and Sheldon M. Stone.

“Sharpe Ratio” refers to a metric used to calculate risk-adjusted return. The Sharpe Ratio is the ratio of excess return to volatility, with excess return defined as the return above that of a riskless asset (based on the three-month U.S. Treasury bill, or for our European Senior Loan strategy, the Euro Overnight Index Average) divided by the standard deviation of such return. A higher Sharpe Ratio indicates a return that is higher than would be expected for the level of risk compared to the risk-free rate.

This annual report and its contents do not constitute and should not be construed as an offer of securities of any Oaktree funds.

5

Part I.

Item 1. Business

Overview

Oaktree is a leader among global investment managers specializing in alternative investments, with $100.5 billion in assets under management (“AUM”) as of December 31, 2016. Our mission is to deliver superior investment results with risk under control and to conduct our business with the highest integrity. We emphasize an opportunistic, value-oriented and risk-controlled approach to investments in distressed debt, corporate debt (including high yield debt and senior loans), control investing, convertible securities, real estate and listed equities. Over three decades, we have developed a large and growing client base through our ability to identify and capitalize on opportunities for attractive investment returns in less efficient markets.

Our founders were pioneers in the management of high yield bonds, convertible securities and distressed debt. From those roots we have developed an array of specialized credit- and equity-oriented strategies. As of December 31, 2016, we had 297 investment professionals, including 170 senior investment professionals with an average 19 years of industry experience, who among them possess the investing, research, analytical, legal, trading and other skills, as well as relationships and experience, that are necessary for long-term success in our complex markets. Additionally, our compensation and other personnel practices foster a collaborative culture that facilitates complementary investment strategies benefiting from shared knowledge and insights.

We manage assets on behalf of many of the most significant institutional investors in the world. Our clientele includes 75 of the 100 largest U.S. pension plans, 38 states in the United States, over 400 corporations and/or their pension funds, over 350 university, charitable and other endowments and foundations, 16 sovereign wealth funds and over 350 other non-U.S. institutional investors. Our 25 largest clients participate in an average of four different investment strategies, reflecting the confidence engendered by our consistent firm-wide investment approach. Approximately 14% of our AUM represents high-net-worth individuals or sub-advisory relationships with mutual funds, indicating both the broadening appeal of alternatives to individual investors and our heightened focus on that market.

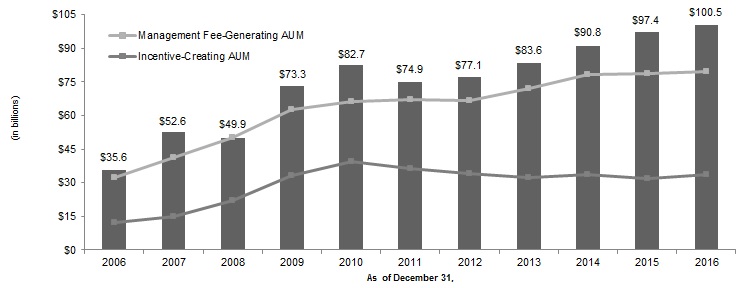

Since Oaktree’s founding in 1995, our AUM has grown significantly, even as we have distributed $87 billion from our closed-end funds. Although we limit our AUM when appropriate in order to better position us to generate superior risk-adjusted returns, we have a long-term track record of organically growing our investment strategies, increasing our AUM and expanding our client base. We have raised gross capital of $10 billion or more in each of the last 10 years, including $11.6 billion in 2016. As of December 31, 2016, uncalled capital commitments were $20.8 billion.

As shown in the chart below, our AUM has grown to $100.5 billion as of December 31, 2016 from $35.6 billion a decade earlier. Over the same period, management fee-generating assets under management (“management fee-generating AUM”) grew from $32.5 billion to $79.8 billion, and incentive-creating assets under management (“incentive-creating AUM”) increased from $12.2 billion to $33.6 billion.

Year-end AUM

6

We have systematically broadened employee ownership since our founding to help align interests among employees, our clients and other stakeholders, as well as to facilitate a smooth generational transfer of management and ownership. As of December 31, 2016, we had 939 employees, including 272 employee-owners, with offices in 18 cities across 13 countries, of which the largest offices are in Los Angeles (headquarters), London, New York City and Hong Kong.

Structure and Operation of Our Business

Our business is comprised of one segment, our investment management segment, which consists of the investment management services that we provide to our clients. Our segment revenue flows from the management fees and incentive income generated by the funds that we manage, as well as the investment income earned from the investments we make in our funds, third-party funds and other companies. The management fees that we receive are based on the contractual terms of the relevant fund and are typically calculated as a fixed percentage of the capital commitments (as adjusted for distributions during a fund’s liquidation period), drawn capital, cost basis or NAV of the particular fund. Incentive income represents our share (typically 20%) of the investors’ profits in most of the closed-end and evergreen funds. Investment income reflects the investment return on a mark-to-market basis and our equity participation on the amounts that we invest in Oaktree and third-party funds, as well as in collateralized loan obligation vehicles (“CLOs”) and other companies.

Structure of Funds

Closed-end Funds

Our closed-end funds are typically structured as limited partnerships that have a 10- or 11-year term and have a specified period during which clients can subscribe for limited partnership interests in the fund. Once a client is admitted as a limited partner, that client is required to contribute capital when called by us as the general partner, and generally cannot withdraw its investment. Our closed-end funds have an investment period that generally ranges from three to five years, during which we are permitted to call the committed capital of those funds to make investments. As closed-end funds liquidate their investments, we typically distribute the proceeds to the clients, although during the investment period we have the ability to retain or recall such proceeds to make additional investments. Once we have committed to invest approximately 80% of the capital in a particular fund, we typically raise a new fund in the same strategy, generally ensuring that we always have capital to invest in new opportunities. We may also provide discretionary management services for clients within our closed-end fund strategies through a separate account or through a limited partnership or limited liability company managed by us with the client as the sole limited partner or sole non-managing member (a “fund-of-one”).

Our closed-end funds also include CLOs for which we serve as collateral manager. CLOs are structured finance vehicles in which we make an investment and for which we are entitled to earn management fees. Investors in CLOs are generally unable to redeem their interests until the CLO liquidates, is called or otherwise terminates.

Open-end Funds

Our commingled open-end funds are typically structured as limited partnerships that are designed to admit clients as new limited partners (or accept additional capital from existing limited partners) on an ongoing basis during the fund’s life. Clients in commingled open-end funds typically contribute all of their committed capital upon being admitted to the fund. These funds do not have an investment period and do not distribute proceeds of realized investments to clients. We are permitted to commit the fund’s capital (including realized proceeds) to new investments at any time during the fund’s life. Clients in commingled open-end funds generally have the right to withdraw their capital from the fund on a monthly basis (with prior written notice of up to 90 days).

We also provide discretionary management services for clients through separate accounts within the open-end fund strategies. Clients establish accounts with us by depositing funds or securities into accounts maintained by qualified independent custodians and granting us discretionary authority to invest such funds pursuant to their investment needs and objectives, as stated in an investment management agreement. Separate account clients generally may terminate our services at any time by providing us with prior notice of 30 days or less.

Evergreen Funds

Our evergreen funds invest in marketable securities, private debt and equity, and in certain cases on a long or short basis. As with open-end funds, commingled evergreen funds are designed to accept new capital on an

7

ongoing basis and generally do not distribute proceeds of realized investments to clients. We also provide discretionary management services for clients through separate accounts or funds-of-one within our evergreen fund strategies. Clients in evergreen funds are generally subject to a lock-up, which restricts their ability to withdraw their entire capital for a certain period of time after their initial subscription.

Management Fees

We receive management fees monthly or quarterly based on annual fee rates for our investment advisory services. The contractual terms of those management fees generally vary by fund structure. For most closed-end funds, the management fee rate is applied against committed capital during the fund’s investment period and the lesser of total funded capital or cost basis of assets in the liquidation period. However, for certain closed-end funds, management fees during the investment period are calculated based on drawn capital or cost basis. Additionally, for those closed-end funds for which management fees are based on committed capital, we may elect to delay the start of the fund’s investment period and thus its full management fees, in which case we earn management fees based on drawn capital, and in certain cases outstanding borrowings under a fund-level credit facility made in lieu of drawing capital, until we elect to start the fund’s investment period. Our right to receive management fees typically ends after 10 or 11 years from either the initial closing date or the start of the investment period, even if assets remain in the fund. In the case of CLOs, a portion of our management fees is dependent on the sufficiency of the particular vehicle’s cash flow. For open-end and evergreen funds, the management fee is generally based on the NAV of the fund. In the case of certain open-end and evergreen fund accounts, we have the potential to earn performance-based fees, typically in reference to a relevant benchmark index or hurdle rate. From time to time, in our sole discretion we may afford certain investors in our funds or clients of separate accounts more favorable economic terms than other investors in the same investment strategy, including with respect to management and performance-based fees, generally based on the aggregate size of commitments of such investor or client, as applicable, to one or more funds or accounts managed by us.

Incentive Income

We have the potential to earn incentive income from closed-end funds, most of which follow the so-called European-style waterfall, whereby we receive incentive income only after the fund first distributes all contributed capital plus an annual preferred return, typically 8%. Once this occurs, we generally receive as incentive income 80% of all distributions otherwise attributable to our investors, and those investors receive the remaining 20% until we have received, as incentive income, 20% of all such distributions in excess of the contributed capital from the inception of the fund. Thereafter, all such future distributions attributable to our investors are distributed 80% to those investors and 20% to us as incentive income. As a result, we generally receive incentive income, if any, in the latter part of a fund’s life, although earlier in a fund’s term we may receive tax distributions, which we recognize as incentive income, to cover our allocable share of income taxes until we are otherwise entitled to payment of incentive income.

Certain evergreen funds pay annual incentive income equal to 10% to 20% of the year’s profits, subject to either a high-water mark or hurdle rate. The high-water mark refers to the highest historical NAV attributable to a limited partner’s account when either incentive income has been earned or the capital was contributed.

Investment Income

We earn segment investment income from our corporate investments in funds and companies, with Oaktree-managed funds constituting the bulk of our corporate investments. Our investments in Oaktree-managed funds generally fall into one of four categories: general partner interests in commingled funds or funds-of-one, investments in CLOs, seed capital for new investment strategies prior to third-party capital raising, and corporate cash management. In the case of general partner interests in our closed-end or evergreen funds, we typically invest the greater of 2.5% of committed capital or $20 million in each fund, not to exceed $100 million per fund. For CLOs, we generally invest 5%, but no more than 10%, of the CLO’s total par value. For strategic purposes, we also invest in a handful of third-party managed funds or companies.

Our investments in companies include a one-fifth equity stake in DoubleLine Capital LP and its affiliates (collectively, “DoubleLine”), a Southern California-based investment management firm that sought our start-up consulting and financial involvement shortly after its founding in December 2009 by Jeffrey Gundlach and others who had previously worked together for over 20 years. From first managing assets in April 2010, DoubleLine has grown to over $100 billion in assets under management as of December 31, 2016. DoubleLine invests across fixed income, equities and commodities through mutual funds, hedge funds and separate accounts.

8

Our Investment Approach

Our goal is excellence in investing. This means achieving attractive returns without commensurate risk, an imbalance which can only be achieved in markets that are not “efficient.” Although we strive for superior returns, our first priority is that our actions produce consistency, protection of capital and superior performance in bad times. At our core, we are contrarian, value-oriented investors focused on buying securities and companies at prices below their intrinsic value and selling or exiting those investments when they become fairly or fully valued. We believe we can do this best by investing in markets where specialization and superior analysis can offer an investing edge.

In our investing activities, we adhere to the following fundamental tenets:

| • | Focus on Risk-Adjusted Returns. Our primary goal is not simply to achieve superior investment performance, but to do so with less-than-commensurate risk. We believe that the best long-term records are built more through the avoidance of losses in bad times than the achievement of superior relative returns in good times. It is our overriding belief that, especially in the opportunistic markets in which we work, “if we avoid the losers, the winners will take care of themselves.” |

| • | Focus on Fundamental Analysis. We employ a bottom-up approach to investing, based on proprietary, company-specific research. We seek to generate consistent outperformance through superior knowledge of companies and their securities, not from macro-forecasting. We do not believe in the predictive ability required to correctly time markets. However, concern about the market climate may cause us to tilt toward more defensive investments, increase selectivity or act more deliberately. Our 297 investment professionals have developed a deep and thorough understanding of a wide number of companies and industries, providing us with a significant institutional knowledge base. |

| • | Specialization. We offer a broad array of specialized investment strategies. We believe this offers the surest path to the results we, and our clients, seek. Clients interested in a single investment strategy can limit themselves to the risk exposure of that particular strategy, while clients interested in more than one investment strategy can combine investments in our funds to achieve their desired mix. Our focus on specific strategies has allowed us to build investment teams with extensive experience and expertise. At the same time, our teams access and leverage each other’s expertise, affording us both the benefits of specialization and the strengths of a larger organization. |

9

Our Asset Classes and Investment Strategies

We manage investments in a number of strategies across six asset classes: Corporate Debt, Convertible Securities, Distressed Debt, Control Investing, Real Estate and Listed Equities. The diversity of our investment strategies allows us to meet a wide range of investor needs suited for different market environments globally and, for certain strategies, targeted regions, while providing us with a long-term diversified revenue base.

Our AUM by asset class and investment strategy as of December 31, 2016 is shown below:

| Strategy Inception | Strategy Inception | |||||||||||

| AUM | AUM | |||||||||||

| (in millions) | (in millions) | |||||||||||

| Corporate Debt: | Control Investing: | |||||||||||

| U.S. High Yield Bonds | 1986 | $ | 17,292 | Special Situations (1) | 1994 | $ | 5,547 | |||||

| Global High Yield Bonds | 2010 | 4,450 | European Principal | 2006 | 5,543 | |||||||

| European High Yield Bonds | 1999 | 1,316 | Infrastructure Investing (2) | 2014 | 2,762 | |||||||

| U.S. Senior Loans | 2007 | 7,735 | Power Opportunities | 1999 | 1,775 | |||||||

| European Senior Loans | 2009 | 3,048 | 15,627 | |||||||||

| European High Yield Bonds and Senior Loans | 2016 | 220 | Real Estate: | |||||||||

| Strategic Credit | 2012 | 3,281 | Real Estate Opportunities | 1994 | 6,557 | |||||||

| Mezzanine Finance | 2001 | 1,469 | Real Estate Debt | 2012 | 1,475 | |||||||

| European Private Debt | 2013 | 659 | Real Estate Value-Add | 2016 | 615 | |||||||

| Emerging Markets Debt Total Return | 2015 | 441 | 8,647 | |||||||||

| 39,911 | Listed Equities: | |||||||||||

| Convertible Securities: | Emerging Markets Equities | 2011 | 3,084 | |||||||||

| U.S. Convertibles | 1987 | 3,411 | Emerging Markets Absolute Return | 1997 | 131 | |||||||

| Non-U.S. Convertibles | 1994 | 1,456 | Value Equities | 2012 | 371 | |||||||

| High Income Convertibles | 1989 | 864 | Other | 69 | ||||||||

| 5,731 | 3,655 | |||||||||||

| Distressed Debt: | ||||||||||||

| Distressed Debt | 1988 | 24,751 | Total | $ | 100,504 | |||||||

| Value Opportunities | 2007 | 1,272 | ||||||||||

| Emerging Markets Opportunities | 2012 | 910 | ||||||||||

| 26,933 | ||||||||||||

| (1) | Effective November 2016, the Global Principal strategy was renamed Special Situations. |

| (2) | Oaktree acquired the Highstar Capital team in 2014, which represents the inception date of this strategy. Highstar’s inception date was 2000. |

We add an investment strategy when we identify a market with potential for attractive returns that we believe can be exploited in a risk-controlled fashion, and where we have access to the investment talent capable of producing the results we seek. We consider it far more important to avoid mistakes than to capture every opportunity. Because of the high priority we place on assuring that these requirements are met, we prefer that new products represent “step-outs” from our current investment strategies into related fields that are managed by people with whom we have had extensive experience or for whom we can validate qualifications.

Our asset classes and investment strategies are described below:

Corporate Debt

High Yield Bonds

We view high yield bond investing as the conscious bearing of risk for potential profit, and we follow a defensive, downside-oriented strategy. Rather than stretching for higher yields, our primary focus is managing credit risk, avoiding dangerous concentrations and minimizing defaults. We have been managing high yield bonds for over three decades, starting in January 1986 with U.S. high yield bonds, and over that time our U.S. strategy has experienced an average default rate equal to approximately one-third the market as a whole. By controlling risk

10

and preserving profits, we seek to outperform our benchmark over full market cycles with less-than-commensurate risk.

We were among the first firms to establish a dedicated European high yield bond strategy, in 1999, when the European high yield bond market was still in its nascent stage. In recent years, the European high yield bond market has grown significantly, which has allowed us to construct diverse portfolios of bonds issued by credit-worthy companies from a variety of sectors across developed European countries. This strategy is managed by a dedicated team of leveraged-finance specialists in our London office and employs the same investment approach successfully applied by our U.S. High Yield Bond team.

Over the years, many of our U.S. clients invested in our Expanded High Yield Fund, which included an opportunistic allocation to our European High Yield Fund, to enhance performance and increase portfolio diversification. As a natural extension, in 2010 we established the Global High Yield Bond strategy, a single portfolio approach to investing in the lower-rated, yet credit-worthy performing bonds of North American and European companies. By employing a highly disciplined, credit-intensive research approach to construct a diversified, risk-controlled portfolio, this strategy targets the most attractive risk/return opportunities we identify across the developed world.

Senior Loans

In September 2007, we formed the U.S. Senior Loan strategy to capitalize on the backlog of unsold or “hung” bridge loans held by investment banks near the start of the global financial crisis. As the market environment changed, we expanded the strategy to include investing in senior bank loans. This strategy typically invests in broadly-syndicated, senior-secured loans or other senior, non-investment grade debt. In most instances, these instruments constitute the most senior position in the capital structure of the borrower. We employ a fundamental, bottom-up credit analysis when approaching potential loan investments. We rely on the same downside sensitivities in our models and proprietary credit scoring matrix that have been successfully applied for over three decades by our High Yield Bond team.

In May 2009, we capitalized on our experience in senior loans and European high yield bonds by forming the European Senior Loan strategy to invest in senior secured loans in the growing European bank loan market. The European Senior Loan strategy focuses on the senior-secured debt of issuers in Europe, and a majority of the portfolio consists of floating-rate obligations.

In 2012, we added a new product under the Senior Loan umbrella, Enhanced Income, to create a portfolio of below-investment grade loans using a moderate amount of leverage. Building on our experience in Senior Loans and Enhanced Income, in 2014 we added CLOs to our product offerings, both in the U.S. and Europe. CLOs are securities backed by a diversified pool of below-investment grade loans sold to investors often seeking credit-rated securities or the potential for higher-than-average returns. Both Enhanced Income and our fully-levered CLOs utilize the same investment approach as our Senior Loan strategy.

European High Yield Bonds and Senior Loans

Drawing on over 15 years of experience and expertise in European non-investment grade credits, in 2016 we launched our step-out European High Yield Bond and Senior Loan strategy as a distinct strategy. This strategy employs relative value analysis to construct optimized portfolios of European bonds and loans, focusing on the senior-secured debt of European issuers and companies with significant exposure to Europe, but may opportunistically invest in rated CLO tranches, direct loans/private placements, and stressed loans and bonds. As an absolute return strategy, the European High Yield Bond and Senior Loan strategy seeks to achieve superior risk-adjusted returns over credit cycles through selective investment in high quality borrowers, with an emphasis on income and long-term growth. Our flexibility to actively allocate between both asset classes provides us the opportunity to capitalize on differences in their relative values.

Strategic Credit

In 2012, we introduced Strategic Credit as a step-out from our Distressed Debt strategy, to capture attractive investment opportunities that appear to offer too little return for distressed debt investors, but may pose too much uncertainty for high yield bond investors. This strategy seeks to achieve an attractive, unlevered total return by investing in public and private performing debt of stressed U.S. and non-U.S. companies. Typical investments are in high yield bonds and senior loans entailing above average credit risk, loan portfolios, rescue financings and other capital solutions for companies experiencing financial stress.

11

Mezzanine Finance

In 2001, we established the Mezzanine Finance strategy to capitalize on our expertise in credit analysis after we observed a gap in the availability of mezzanine capital to many attractive companies that were considered too small for the high yield bond market. Our strong relationships with small-cap and mid-cap private equity sponsors constitute a major advantage in our Mezzanine investment process. The strategy targets middle market companies with enterprise values between $150 million and $750 million. We believe this part of the market presents attractive opportunities to help finance leveraged buyouts, recapitalizations, acquisitions and corporate growth. The Mezzanine Finance strategy seeks to earn an attractive current return and achieve long-term capital appreciation without subjecting principal to undue risk.

European Private Debt

We introduced European Private Debt in 2013 to capitalize on opportunities resulting from the decline in European bank lending and our significant industry experience, knowledge and deep relationships across the Continent. The strategy seeks to achieve attractive, risk-adjusted absolute returns by making primary investments in high-yielding debt or preferred equity of healthy European companies that require liquidity for acquisitions, buyouts of minority investors, debt restructurings, recapitalizations or acquisitions of hard assets. Our goal is to target a concentrated portfolio of direct loans to middle-market companies resulting from unique proprietary lending opportunities generated by the European Principal Group (the “EPG”). The strategy invests primarily in industries in which the EPG has existing portfolio companies or experience, with a particular emphasis on capital-intensive sectors where a lack of bank financing has created an opportunity to acquire assets at a significant discount or to extend credit at attractive rates. Typically we are the sole lender in our direct-lending transactions, and we rarely participate in sponsor-backed transactions or competitive auctions.

Emerging Markets Debt Total Return

As a step-out to our Emerging Markets Opportunities strategy, in 2015 we introduced Emerging Markets Debt Total Return to third-party investors to capitalize on the nascent market of stressed credits falling out of the investment-grade and high yield fixed income emerging markets universe. This strategy invests primarily in performing emerging market credit, seeking to achieve an attractive total return by taking advantage of market inefficiencies and geopolitical complexities in the emerging markets credit universe.

Convertible Securities

Convertible securities are part debt and part equity. By applying our risk-control investment approach to these securities, we attempt to capture most of the returns of equities in rising markets and to outperform equities in flat or down markets. Our goal is to capture the vast majority of the performance of equities over full market cycles with reduced volatility and/or substantially outperform straight bonds with similar levels of risk. To reduce risk, we broadly diversify and focus on convertibles that provide pronounced downside protection. We manage three convertible securities strategies that focus on different regions and market sections – U.S., non-U.S. and “high income” convertibles. High income, or “busted,” convertibles offer a unique combination of high current yield and yield-to-maturity, plus the potential for significant equity-driven capital appreciation.

Distressed Debt

Distressed Debt

Our Distressed Debt team was an industry pioneer and has been one of its leaders since the inception of the strategy in 1988. The team focuses primarily on investments in distressed companies that are perceived to have substantial asset values or business franchises, and are in industries going through periods of transition or dislocation. Our approach seeks to combine protection against loss, which generally comes from buying claims on assets at bargain prices, with the substantial gains to be achieved by returning companies to financial viability through restructuring. We take an opportunistic approach to investing, with the flexibility and expertise to choose from a broad range of investments, including leveraged loans, bonds, equity securities, companies or hard assets. Building on our Distressed Debt team’s experience in the U.S., we have established a significant presence in Europe to capitalize on opportunities in that region.

12

Value Opportunities

We launched Value Opportunities in 2007 for investors who had expressed interest in a more liquid version of the Distressed Debt strategy. The fund is managed by the Distressed Debt team and invests mainly in distressed debt, stressed debt and other value-oriented investments for which there is a liquid market. Inasmuch as this strategy is intended to be opportunistic, the composition of the portfolio is designed to capitalize on changing market conditions. In general, this strategy employs similar strategies and tactics with regard to distressed investments as the Distressed Debt strategy, but it may be more aggressive and more oriented to short selling and short-term trading (and may make greater use of leverage and derivatives) with respect to its non-distressed investments.

Emerging Markets Opportunities

We launched this strategy in 2012 as an expansion of our Distressed Debt strategy. The Emerging Markets Opportunities strategy targets stressed, distressed and other value-oriented fixed income, hybrid and equity investments in emerging markets. In contrast to developed markets, macroeconomic events, political crises and a misunderstanding among many investors of emerging market complexities give rise to more pronounced disruptions and an enhanced opportunity set for us to take advantage of such opportunities. This strategy is managed by a U.S.-based group that leverages our Distressed Debt team’s experience and expertise, and employs an established, flexible external network of local advisers to enhance deal flow, access local market intelligence and address the intricacies of jurisdictional differences and industry and local regulatory developments.

Control Investing

Special Situations

Our Special Situations strategy makes control-oriented debt and equity investments in middle-market companies that have an element of distress, dislocation or dysfunction and that we perceive to be undervalued. It seeks situations in which we can gain control of, or significant influence over, companies exhibiting such characteristics and then actively manages those businesses in an effort to deliver value as a private equity-like sponsor. The cornerstone of the Special Situations strategy is its flexibility to invest across capital structures, whether by purchasing secondary market debt (“distress-for-control”) or making direct debt or equity investments in distressed businesses. Importantly, the strategy does not require a distressed macro environment to invest successfully, relying instead on “situational” distress that can be uncovered in any industry, sector or individual company at any point in the economic cycle.

European Principal

The European Principal strategy targets control investing opportunities where dislocation or distress enable its funds to secure an attractive purchase price or creation value, and thus the potential for attractive returns. EPG’s diverse skillset enables the team to target “off-the-run” investment opportunities in which competition is limited, to assess the correlation between a company’s performance and the general economic cycle or specific industry trends, and to develop and implement bespoke operational, legal and financial solutions. We eschew competitive auctions, preferring instead to work closely with parties which have agreed in principle to the proposed transaction. This approach can improve information flow, reduce the risk and cost of competition, and translate into a more attractive investment opportunity. The team uses its local presence in multiple countries, coupled with its deal execution, operational and legal expertise, to craft customized solutions for situations that, in addition to capital, require complex operational or strategic improvements. Capital-intensive industries are an area of focus because the investment can be at least partially secured by the value of the assets, which creates downside protection and possibly substantial upside returns. We may also seek to acquire individual assets or smaller pools of assets in a single industry, consolidating them into a larger operating company. These so-called platform investments, which typically are managed by personnel identified by EPG, may benefit from operational, strategic and financial enhancements implemented by our in-house portfolio enhancement teams.

Power Opportunities

Beginning in 1996, our Control Investing strategies made a number of power- and energy-related investments jointly with an independent firm, GFI Energy Ventures (“GFI”), a firm founded in 1995. In 2009, GFI personnel joined us and, starting with Oaktree Power Opportunities Fund III, we became the sole manager of the strategy. The Power Opportunities funds seek to make controlling equity investments in companies providing equipment, software, and services used in the generation, transmission, distribution, marketing, trading, and

13

consumption of electricity, natural gas, and related energy services. The Power Opportunities team is comprised of seasoned energy sector professionals who work to identify key energy industry themes and then invest in companies well-positioned to benefit from such themes. The team then works closely with portfolio companies to strengthen operations, pursue new customers and market opportunities, recruit additional talent, and make complementary acquisitions, among other activities to increase shareholder value. The strategy invests in proven performers and market leaders, not start-up ventures or turnarounds.

Infrastructure Investing

In August 2014, we acquired the Highstar Capital team and certain Highstar entities (collectively “Highstar”) to facilitate the expansion of our Power Opportunities strategy and to help us capitalize on the growing need for private capital to support the renovation, replacement and creation of critical transportation and energy infrastructure. Highstar was founded in 2000 and was an early entrant to infrastructure investing, utilizing operating expertise to implement a value-added strategy to acquire, operate, fix and ultimately sell critical infrastructure assets and businesses, primarily in North America.

Real Estate

Real Estate Opportunities

The Real Estate team targets a diverse range of global opportunities across all areas of this asset class, with an emphasis on debt or equity investments in commercial real estate, corporate real estate, structured finance, commercial non-performing loans, residential real estate and non-U.S. real estate. Investments may include direct property investments; investments in real estate-related corporations; commercial mortgage-backed securities and related securities; residential land, assets and loan pools; small-balance commercial loan pools; and non-U.S. investments. With dedicated real estate professionals in the U.S., Japan, Hong Kong, South Korea and the U.K., the team benefits from Oaktree’s multi-disciplinary strengths and global footprint. The team also occasionally pursues development opportunities with aligned, high-quality partners.

Real Estate Debt

Our management of the Oaktree PPIP Fund, organized pursuant to the U.S. Treasury Department’s program to address troubled real estate-related assets during the global financial crisis, spurred us to offer Real Estate Debt as a successor strategy in 2012. The Real Estate Debt strategy seeks to achieve attractive risk-adjusted returns and produce current income by investing in real estate-related debt that is not anticipated to result in control of the underlying asset. This strategy specializes in debt-driven opportunities similar to that of the Real Estate strategy (e.g., commercial real estate, real estate-related corporate investments, structured finance, commercial non-performing loans, residential real estate and non-U.S. real estate), and invests in commercial mortgage-backed securities, commercial and residential mortgages, mezzanine loans and corporate debt.

Real Estate Value-Add

In 2016, we launched the Real Estate Value-Add strategy as a step-out of the Real Estate Opportunities strategy to expand the reach of our real estate platform through investments that have the potential to provide stable income and attractive risk-adjusted returns, but do not have the requisite distress or total return profile to be a candidate for our Real Estate Opportunities funds. This strategy seeks to achieve superior risk-adjusted returns through investments in high-quality real estate assets with an emphasis on income and long-term growth, and targets commercial real estate assets, with a particular emphasis on office, multifamily, industrial and retail properties. It also considers debt and other income-producing investments on a limited basis.

Listed Equities

Emerging Markets Equities

As a step-out from our Emerging Markets Absolute Return strategy, in 2011 we added the long-only Emerging Markets Equities strategy, which we manage through funds, mutual fund sub-advisory relationships and separate accounts. This strategy invests on a long-only basis in the equities of emerging market companies in the Asia Pacific region, Latin America, Eastern Europe, the Middle East, Africa and Russia.

14

Value Equities

We launched this strategy to third-party investors in 2014 as a step-out from our Distressed Debt platform. Similar to our Distressed Debt and Value Opportunities strategies, Value Equities employs a bottom-up, value-oriented investment approach focused on long-term principal appreciation and preservation of capital. This strategy seeks to achieve attractive, risk-adjusted returns by opportunistically assembling and managing an unleveraged, concentrated portfolio of stressed, post-reorganization and value equities that offer asymmetric return profiles across industries, market capitalizations and geographies within developed markets.

Our Investment Performance

Our investment professionals have generated impressive investment performance through multiple market cycles. As of December 31, 2016, our incentive-creating closed-end funds had produced a since-inception aggregate gross IRR of 18.9% on approximately $75 billion of drawn capital. Of the 56 such closed-end funds we manage that commenced before July 1, 2015, 55 had positive net IRRs as of December 31, 2016, an achievement that reflects, among many factors, our practice of sizing funds in proportion to our view of the supply of potential attractive investment opportunities.

Information regarding our most significant and longest-managed closed-end funds is shown below, as of or for the periods ended December 31, 2016. Please see “Fund Data” below for more information regarding the performance of our closed-end funds.

| Strategy Inception | Total Drawn Capital | IRR Since Inception | Multiple of Drawn Capital | ||||||||||

| Gross | Net | ||||||||||||

| (in millions) | |||||||||||||

| Distressed Debt | 1988 | $ | 40,692 | 22.0 | % | 16.2 | % | 1.7x | |||||

| Real Estate Opportunities | 1994 | 7,283 | 15.5 | 11.9 | 1.7 | ||||||||

Special Situations (1) | 1994 | 10,283 | 13.3 | 9.6 | 1.9 | ||||||||

European Principal (2) | 2006 | 5,225 | 13.7 | 9.1 | 1.7 | ||||||||

| Power Opportunities | 1999 | 2,099 | 34.7 | 26.5 | 2.2 | ||||||||

| Mezzanine Finance | 2001 | 3,642 | 13.2 | 8.9 | 1.4 | ||||||||

| Sub-total | 69,224 | ||||||||||||

| Other funds | 18,755 | ||||||||||||

| Total | $ | 87,979 | |||||||||||

| (1) | Effective November 2016, the Global Principal strategy was renamed Special Situations. The figures shown include the performance of Oaktree Special Situations Fund, which commenced its investment period in November 2015. Excluding Oaktree Special Situations Fund, the aggregate gross and net IRRs as of December 31, 2016 were 13.3% and 9.5%, respectively. |

| (2) | All figures are based on the conversion of amounts or cash flows from euros to USD using the December 31, 2016 spot rate of $1.05. |

15

Performance of our open-end funds is in part measured in relation to applicable benchmark returns. Our emphasis on risk control and credit selection has generally led to outperformance in challenging markets and over full market cycles. Information regarding our open-end funds, together with relevant benchmark data, is set forth below as of or for the periods ended December 31, 2016. Please see “Fund Data” below for more information regarding the performance of our open-end funds.

| Strategy Inception | AUM | Since Inception | ||||||||||||||||

| Annualized Rates of Return | Sharpe Ratio | |||||||||||||||||

| Oaktree | Relevant Benchmark (Gross) | Oaktree Gross | Relevant Benchmark (Gross) | |||||||||||||||

| Gross | Net | |||||||||||||||||

| (in millions) | ||||||||||||||||||

| U.S. High Yield Bonds | 1986 | $ | 17,292 | 9.4 | % | 8.8 | % | 8.4 | % | 0.80 | 0.56 | |||||||

| Global High Yield Bonds | 2010 | 4,450 | 7.5 | 7.0 | 6.9 | 1.13 | 1.07 | |||||||||||

| European High Yield Bonds | 1999 | 1,316 | 8.1 | 7.6 | 6.3 | 0.71 | 0.44 | |||||||||||

| U.S. Convertibles | 1987 | 3,411 | 9.4 | 8.8 | 8.1 | 0.48 | 0.36 | |||||||||||

| Non-U.S. Convertibles | 1994 | 1,456 | 8.4 | 7.8 | 5.6 | 0.78 | 0.40 | |||||||||||

| High Income Convertibles | 1989 | 864 | 11.4 | 10.6 | 8.2 | 1.06 | 0.60 | |||||||||||

| U.S. Senior Loans | 2008 | 1,589 | 6.2 | 5.7 | 5.3 | 1.11 | 0.65 | |||||||||||

| European Senior Loans | 2009 | 1,422 | 8.5 | 7.9 | 9.2 | 1.72 | 1.73 | |||||||||||

| Emerging Markets Equities | 2011 | 3,084 | (1.7 | ) | (2.5 | ) | (2.7 | ) | (0.09) | (0.15) | ||||||||

Synergies

We emphasize cross-group cooperation and collaboration among our investment professionals. Many of our investment strategies are complementary, and our investment professionals often identify and communicate potential opportunities to other groups, allowing our funds to benefit from the synergies created by the scale of our business and our proprietary research. For example, the Distressed Debt group sometimes identifies companies emerging from bankruptcy that could be attractive to the High Yield Bond group.

This cross-pollination among our investment groups occurs both formally and informally. For example, representatives of different investment groups often attend each other’s meetings in order to keep abreast of the others’ activities and maintain access to specialized investment expertise. Groups periodically invest jointly, permitting us to make larger or more specialized investments than we could undertake in the absence of such collaboration. Our investment professionals also cooperate informally, consulting one another with respect to existing and proposed investments. Our culture encourages such cooperation, as does the broad Oaktree equity ownership among our investment professionals, which gives them an indirect stake in the success of all of our investment strategies.

We have a shared trading desk in the U.S. for many of our strategies, which provides the benefit of our traders’ deep experience with both performing and distressed securities, facilitates communication among the groups, and allows us to combine trades for larger orders with the preferential access and pricing that sometimes comes with larger orders. Additionally, the scale of our investing activities makes us a significant client of many investment banks, brokers and consultants, and thus helps each group access opportunities that might not be available were it not part of our larger organization. Finally, the scale of our activities has permitted us to create significant shared resources.

16

Marketing and Client Relations

Our client relationships are fundamental to our business. We believe our success is a byproduct of the success of our fund investors and thus always strive to achieve superior returns with risk under control, to charge fair and transparent management fees, and to behave with professionalism and integrity. We have developed a loyal following among many of the world’s most significant institutional investors, and believe that their and our other investors’ loyalty results from our superior investment record, our reputation for integrity, and the fairness and transparency of our fee structures.

As of December 31, 2016, our $100.5 billion of AUM was divided by client type and geographic origin as follows:

| AUM by Client Type | AUM | % | AUM by Client Location | AUM | % | ||||||||||

| (in millions) | (in millions) | ||||||||||||||

| Public funds | $ | 23,861 | 24 | % | Americas | $ | 71,831 | 72 | % | ||||||

| Corporate and corporate pension | 23,749 | 24 | Europe, Middle East & Africa | 15,568 | 15 | ||||||||||

| Insurance companies | 9,187 | 9 | Asia Pacific | 13,105 | 13 | ||||||||||

| Sub-advisory – mutual funds | 8,685 | 9 | Total | $ | 100,504 | 100 | % | ||||||||

| Sovereign wealth funds | 8,351 | 8 | |||||||||||||

| Endowments/foundations | 5,716 | 6 | |||||||||||||

| Private – high net worth/family office | 5,041 | 5 | |||||||||||||

| Oaktree & affiliates | 4,179 | 4 | |||||||||||||

| Fund of funds | 3,028 | 3 | |||||||||||||

| Unions | 2,038 | 2 | |||||||||||||

| Other | 6,669 | 6 | |||||||||||||

| Total | $ | 100,504 | 100 | % | |||||||||||

Our extensive in-house global Marketing and Client Relations group, consisting of 56 individuals dedicated to relationship management and sales, client service or sales strategy in Europe, the Middle East, Asia/Pacific and the Americas, appropriately reflects the global composition of our client base. This team is augmented by 46 dedicated marketing support, portfolio analytics and client reporting professionals.

Employees

We strive to maintain a work environment that fosters integrity, professionalism, excellence, candor and collegiality among our employees. We consider our labor relations to be good. As of December 31, 2016, we had 939 employees, categorized as follows:

| All Employees | Employee Owners (1) | Employees Located Outside the U.S. | ||||||

| Investment professionals | 297 | 177 | 106 | |||||

| Other professionals | 488 | 95 | 74 | |||||

| Support staff | 154 | — | 40 | |||||

| Total | 939 | 272 | 220 | |||||

(1) Represents employees that have received grants of Class A or OCGH units under our equity incentive plans.

17

Competition

We compete with many other firms in every aspect of our business, including raising funds, seeking investments and hiring and retaining professionals. Many of our competitors are substantially larger than us and have considerably greater financial, technical and marketing resources. Certain of these competitors periodically raise significant amounts of capital in investment strategies that are similar to ours. Some of these competitors also may have a lower cost of capital and access to funding sources that are not available to us, which may create further competitive disadvantages for us with respect to investment opportunities. In addition, some of these competitors may have higher risk tolerances or make different risk assessments than we do, allowing them to consider a wider variety of investments and establish broader networks of business relationships. In short, we operate in a highly competitive business and many of our competitors may be better positioned than we are to take advantage of opportunities in the marketplace. For additional information regarding the competitive risks that we face, please see “Risk Factors—Risks Relating to Our Business—The investment management business is intensely competitive.”

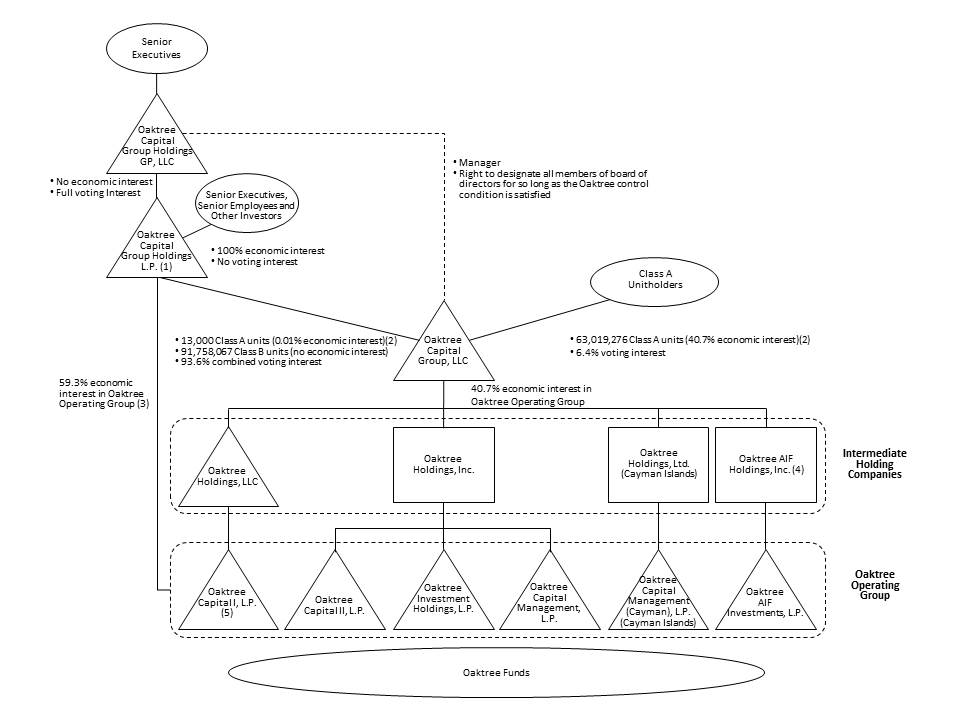

Organizational Structure

Oaktree Capital Group, LLC is a Delaware limited liability company that was formed on April 13, 2007. The Company is owned by its Class A and Class B unitholders. Oaktree Capital Group Holdings GP, LLC acts as the Company’s manager and is the general partner of Oaktree Capital Group Holdings, L.P., which owns 100% of the Company’s outstanding Class B units. OCGH is owned by the OCGH unitholders. The Company’s operations are conducted through a group of operating entities collectively referred to as the “Oaktree Operating Group.” OCGH has a direct economic interest in the Oaktree Operating Group and the Company has an indirect economic interest in the Oaktree Operating Group. We collectively refer to the interests in the Oaktree Operating Group as the “Oaktree Operating Group units.” An Oaktree Operating Group unit is not a separate legal interest but represents one limited partnership interest in each of the Oaktree Operating Group entities.

Class A units are entitled to one vote per unit. Class B units are entitled to ten votes per unit. However, if the Oaktree control condition (as defined below) is no longer satisfied, our Class B units will be entitled to only one vote per unit. Holders of our Class A units and Class B units generally vote together as a single class on the limited set of matters on which our unitholders have a vote. Such matters, which must be approved by a majority (or, in the case of election of directors when the Oaktree control condition is no longer satisfied, a plurality) of the votes entitled to be cast by all Class A units and Class B units present in person or represented by proxy at a meeting of unitholders, include a proposed sale of all or substantially all of our assets, certain mergers and consolidations, certain amendments to our operating agreement and an election by our board of directors to dissolve the company. The Class B units do not represent an economic interest in Oaktree Capital Group, LLC. The number of Class B units held by OCGH, however, increases or decreases with corresponding changes in OCGH’s economic interest in the Oaktree Operating Group.

Our operating agreement provides that so long as our senior executives, or their successors or affiliated entities (other than us or our subsidiaries), including OCGH, collectively hold, directly or indirectly, at least 10% of the aggregate outstanding Oaktree Operating Group units, our manager, Oaktree Capital Group Holdings GP, LLC, which is 100% owned and controlled by our senior executives, will be entitled to designate all the members of our board of directors. We refer to this ownership condition as the “Oaktree control condition.” Holders of our Class A units and Class B units have no right to elect our manager. So long as the Oaktree control condition is satisfied, our manager will control the membership of our board of directors, which will manage all of our operations and activities and will have discretion over significant corporate actions, such as the issuance of securities, payment of distributions, sale of assets, making certain amendments to our operating agreement and other matters.

18

The diagram below depicts our organizational structure as of December 31, 2016.

______________________

| (1) | Holds 100% of the Class B units and 0.02% of the Class A units, which together represent 93.6% of the total combined voting power of our outstanding Class A and Class B units. The Class B units have no economic interest in us. The general partner of Oaktree Capital Group Holdings, L.P. is Oaktree Capital Group Holdings GP, LLC, which is controlled by our senior executives. Oaktree Capital Group Holdings GP, LLC also acts as our manager and in that capacity has the authority to designate all the members of our board of directors for so long as the Oaktree control condition is satisfied. |

| (2) | The percent economic interest represents the applicable number of Class A units as a percentage of the Oaktree Operating Group units. As of December 31, 2016, there were 154,790,343 Oaktree Operating Group units outstanding. |

| (3) | The percent economic interest in Oaktree Operating Group represents the aggregate number of Oaktree Operating Group units held, directly or indirectly, as a percentage of the total number of Oaktree Operating Group units outstanding. |

| (4) | Oaktree Capital Group, LLC holds 1,000 shares of non-voting Class A common stock of Oaktree AIF Holdings, Inc., which are entitled to receive 100% of any dividends. Oaktree Capital Group Holdings, L.P. holds 100 shares of voting Class B common stock of Oaktree AIF Holdings, Inc., which do not participate in dividends or otherwise represent an economic interest in Oaktree AIF Holdings, Inc. |

| (5) | Owned indirectly by Oaktree Holdings, LLC through an entity not reflected in this diagram that is treated as a partnership for U.S. federal income tax purposes. Through this entity, each of Oaktree Holdings, Inc. and Oaktree Holdings, Ltd. owns a less than 1% indirect interest in Oaktree Capital I, L.P. |

19

Regulatory Matters and Compliance

Our business, as well as the financial services industry in general, is subject to extensive regulation in the United States and elsewhere. Our indirect subsidiary, Oaktree Capital Management, L.P., is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). Registered investment advisers are subject to the requirements and regulations of the U.S. Investment Advisers Act of 1940, as amended (the “Advisers Act”). These requirements relate to, among other things, fiduciary duties to clients, maintaining an effective compliance program, solicitation agreements, conflicts of interest, recordkeeping and reporting, disclosure, limitations on agency cross and principal transactions between an adviser and advisory clients and general anti-fraud prohibitions. In addition, Oaktree Capital Management, L.P. is registered as a commodity pool operator and a commodity trading adviser with the U.S. Commodity Futures Trading Commission (“CFTC”). Registered commodity pool operators and commodity trading advisers are each subject to the requirements and regulations of the U.S. Commodity Exchange Act, as amended (the “Commodity Exchange Act”). These requirements relate to, among other things, maintaining an effective compliance program, recordkeeping and reporting, disclosure, business conduct, and general anti-fraud prohibitions. In addition, as a registered commodity pool operator and a commodity trading adviser with the CFTC, we are also required to be a member of the National Futures Association (the “NFA”), a self-regulatory organization for the U.S. derivatives industry. The NFA also promulgates and enforces rules governing the conduct of, and examines the activities of, its member firms.

In 2014, we launched our first Oaktree-branded mutual funds, which are subject to the rules and regulations applicable to investment companies under the U.S. Investment Company Act of 1940 (as amended, the “Investment Company Act”). We are required to invest our mutual funds’ assets in accordance with limitations under the Investment Company Act and applicable provisions of the U.S. Internal Revenue Code of 1986, as amended (the “Code”). In addition, we are required to file periodic and annual reports on behalf of the mutual funds with the SEC. Furthermore, advisers to mutual funds have a fiduciary duty under the Investment Company Act not to charge excessive compensation, and the Investment Company Act grants shareholders of mutual funds a direct private right of action against investment advisers to seek redress for alleged violations of this fiduciary duty.

One of our indirect subsidiaries, OCM Investments, LLC, is registered as a broker-dealer with the SEC and in all 50 states, the District of Columbia and Puerto Rico, and is a member of the U.S. Financial Industry Regulatory Authority (“FINRA”). As a broker-dealer, this subsidiary is subject to regulation and oversight by the SEC and state securities regulators. In addition, FINRA, a self-regulatory organization that is subject to oversight by the SEC, promulgates and enforces rules governing the conduct of, and examines the activities of, its member firms. Due to the limited authority granted to our subsidiary in its capacity as a broker-dealer, it is not required to comply with certain regulations covering trade practices among broker-dealers and the use and safekeeping of customers’ funds and securities. As a registered broker-dealer and member of a self-regulatory organization, we are, however, subject to the SEC’s uniform net capital rule. Rule 15c3-1 of the Exchange Act specifies the minimum level of net capital a broker-dealer must maintain and also requires that a significant part of a broker-dealer’s assets be kept in relatively liquid form. The SEC and FINRA impose rules that require notification when net capital falls below certain predefined criteria, limit the ratio of subordinated debt to equity in the regulatory capital composition of a broker-dealer and constrain the ability of a broker-dealer to expand its business under certain circumstances. Additionally, the SEC’s uniform net capital rule imposes certain requirements that may have the effect of prohibiting a broker-dealer from distributing or withdrawing capital and requiring prior notice to the SEC for certain withdrawals of capital.

Another of our subsidiaries, Oaktree Capital Management (UK) LLP, is authorized and regulated by the U.K. Financial Conduct Authority (“FCA”) as an investment manager in the United Kingdom. The U.K. Financial Services and Markets Act 2000 (“FSMA”) and rules promulgated thereunder govern all aspects of the U.K. investment business, including sales, research and trading practices, the provision of investment advice, the use and safekeeping of client funds and securities, regulatory capital, recordkeeping, margin practices and procedures, the approval standards for individuals, anti-money laundering, periodic reporting, and settlement procedures. Similarly, we have a number of other non-U.S. subsidiaries that are regulated by the applicable regulators in their respective jurisdictions.

The SEC and other regulators have in recent years aggressively increased their regulatory activities in respect of asset management firms. The Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”), among other things, imposes significant regulations on nearly every aspect of the U.S. financial services industry, including oversight and regulation of systemic market risk (including the power to liquidate certain institutions); authorizing the Federal Reserve to regulate nonbank institutions that are deemed systemically important; generally prohibiting insured depository institutions and their affiliates from conducting proprietary trading

20

and investing in private equity funds and hedge funds; and imposing new registration, recordkeeping and reporting requirements on private fund investment advisers. Some of these provisions are still subject to further rulemaking and to the discretion of regulatory bodies. The Dodd-Frank Act also prohibits investments in private equity and hedge funds by certain banking entities and covered nonbank companies. While certain of our subsidiaries are already registered investment advisers and registered broker-dealers and subject to SEC and FINRA examinations, compliance with any additional legal or regulatory requirements, including the need to register other subsidiaries as investment advisers, could make compliance more difficult and expensive and affect the manner in which we conduct business.

Certain of our activities are subject to compliance with laws and regulations of U.S. federal, state and municipal governments, non-U.S. governments, their respective agencies and/or various self-regulatory organizations or exchanges relating to, among other things, antitrust laws, anti-money laundering laws, anti-bribery laws relating to foreign officials, and privacy laws with respect to client information, and some of our funds invest in businesses that operate in highly regulated industries. Any failure to comply with these rules and regulations could expose us to liability and/or reputational damage. Our business has operated for many years within a legal framework that requires our being able to monitor and comply with a broad range of legal and regulatory developments that affect our activities. However, additional legislation, changes in rules or changes in the interpretation or enforcement of existing laws and rules, either in the United States or elsewhere, may directly affect our mode of operation and profitability. Please see “Risk Factors—Risks Relating to Our Business—Regulatory changes in the United States, regulatory compliance failures and the effects of negative publicity surrounding the financial industry in general could adversely affect our reputation, business and operations.”

Financial and Other Information by Segment

Financial and other information by segment for the years ended December 31, 2016, 2015 and 2014 are set forth in the “Segment Reporting” note in our consolidated financial statements included elsewhere in this annual report.

Available Information

Our website address is www.oaktreecapital.com. Information on our website is not a part of this annual report and is not incorporated by reference herein. We make available free of charge on our website or provide a link on our website to our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, as soon as reasonably practicable after those reports are electronically filed with, or furnished to, the SEC. To access these filings, go to the “Unitholders—Investor Relations” section of our website and then click on “SEC Filings.” You may also read and copy any document we file at the SEC’s public reference room located at 100 F Street, N.E., Washington, DC 20549. Please call the SEC at 1-800-SEC-0330 for further information on the public reference room. In addition these reports and the other documents we file with the SEC are available at a website maintained by the SEC at www.sec.gov.

Investors and others should note that we use the Unitholders – Investor Relations section of our corporate website to announce material information to investors and the marketplace. While not all of the information that we post on our corporate website is of a material nature, some information could be deemed to be material. Accordingly, we encourage investors, the media, and others interested in Oaktree to review the information that we share on our corporate website at the Unitholders – Investor Relations section of our website, http://ir.oaktreecapital.com/. Information contained on, or available through, our website is not incorporated by reference into this document.

21

Fund Data

Information regarding our closed-end, open-end and evergreen funds, together with benchmark data where applicable, is set forth below. For our closed-end and evergreen funds, no benchmarks are presented in the tables as there are no known comparable benchmarks for these funds’ investment philosophy, strategy and implementation.

Closed-end Funds

| As of December 31, 2016 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Investment Period | Total Committed Capital | % Invested (1) | % Drawn (2) | Fund Net Income Since Inception | Distri- butions Since Inception | Net Asset Value | Manage- ment Fee-gener- ating AUM | Oaktree Segment Incentive Income Recog- nized | Accrued Incentives (Fund Level) (3) | Unreturned Drawn Capital Plus Accrued Preferred Return (4) | IRR Since Inception (5) | Multiple of Drawn Capital (6) | |||||||||||||||||||||||||||||||||||||

| Start Date | End Date | Gross | Net | ||||||||||||||||||||||||||||||||||||||||||||||

| (in millions) | |||||||||||||||||||||||||||||||||||||||||||||||||

| Distressed Debt | |||||||||||||||||||||||||||||||||||||||||||||||||

| Oaktree Opportunities Fund Xb | TBD | — | $ | 8,063 | — | % | — | % | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | n/a | n/a | n/a | ||||||||||||||||||||||||