UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22106

Tortoise Power and Energy Infrastructure Fund, Inc.

(Exact name of registrant as specified in charter)

6363 College Boulevard, Suite 100A, Overland Park, KS 66211

(Address of principal executive offices) (Zip code)

P. Bradley Adams

Diane Bono

6363 College Boulevard, Suite 100A, Overland Park, KS 66211

(Name and address of agent for service)

913-981-1020

Registrant's telephone number, including area code

Date of fiscal year end: November 30

Date of reporting period: May 31, 2022

Item 1. Report to Stockholders.

(a) The report to Shareholders is attached herewithin.

Semi-Annual Report | May 31, 2022

2022 Semi-Annual Report

Closed-End Funds

| |

| |

| |

| |

| Tortoise |

| 2022 Semi-Annual Report to Stockholders |

| |

This combined report provides you with a comprehensive review of our funds that span essential assets.

| | | | | | | |

| Table of contents |

| | | | | | | |

| Closed-end Fund Comparison | 1 | | TPZ: | Fund Focus | 18 | |

| Letter to Stockholders | 2 | | TEAF: | Fund Focus | 21 | |

| TYG: | Fund Focus | 6 | | Financial Statements | 25 | |

| NTG: | Fund Focus | 9 | | Notes to Financial Statements | 62 | |

| TTP: | Fund Focus | 12 | | Additional Information | 79 | |

| NDP: | Fund Focus | 15 | | | | | |

| |

| TTP and TPZ distribution policies |

Tortoise Pipeline & Energy Fund, Inc. (“TTP”) and Tortoise Power and Energy Infrastructure Fund, Inc. (“TPZ”) are relying on exemptive relief permitting them to make long-term capital gain distributions throughout the year. Each of TTP and TPZ, with approval of its Board of Directors (the “Board”), has adopted a managed distribution policy (the “Policy”). Annual distribution amounts are expected to fall in the range of 7% to 10% of the average week-ending net asset value (“NAV”) per share for the prior fiscal semi-annual period. In accordance with its Policy, TTP distributes a fixed amount per common share, currently $.59, each quarter to its common shareholders. TPZ distributes a fixed amount per common share, currently $.105, each month to its common shareholders. Prior to February 2022, the monthly distribution rate was $.06. These amounts are subject to change from time to time at the discretion of the Board. Although the level of distributions is independent of TTP’s and TPZ’s performance, TTP and TPZ expect such distributions to correlate with its performance over time. Each quarterly and monthly distribution to shareholders is expected to be at the fixed amount established by the Board, except for extraordinary distributions in light of TTP’s and TPZ’s performance for the entire calendar year and to enable TTP and TPZ to comply with the distribution requirements imposed by the Internal Revenue Code. The Board may amend, suspend or terminate the Policy without prior notice to shareholders if it deems such action to be in the best interests of TTP, TPZ and their respective shareholders. For example, the Board might take such action if the Policy had the effect of shrinking TTP’s or TPZ’s assets to a level that was determined to be detrimental to TTP or TPZ shareholders. The suspension or termination of the Policy could have the effect of creating a trading discount (if TTP’s or TPZ’s stock is trading at or above net asset value), widening an existing trading discount, or decreasing an existing premium. You should not draw any conclusions about TTP’s or TPZ’s investment performance from the amount of the distribution or from the terms of TTP’s or TPZ’s distribution policy. Each of TTP and TPZ estimates that it has distributed more than its income and net realized capital gains; therefore, a portion of your distribution may be a return of capital. A return of capital may occur, for example, when some or all of the money that you invested in TTP or TPZ is paid back to you. A return of capital distribution does not necessarily reflect TTP’s or TPZ’s investment performance and should not be confused with “yield” or “income.” The amounts and sources of distributions reported are only estimates and are not being provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes will depend upon TTP’s and TPZ’s investment experience during their fiscal year and may be subject to changes based on tax regulations. TTP and TPZ will send you a Form 1099-DIV for the calendar year that will tell you how to report these distributions for federal income tax purposes.

| |

| |

| 2022 Semi-Annual Report | May 31, 2022 |

| |

| Closed-end Fund Comparison |

| | Name/Ticker | | Primary

focus | | Structure | | Total assets

($ millions)1 | | Portfolio mix

by asset type(1) | | Portfolio mix

by structure1 |

| | Tortoise Energy

Infrastructure Corp. NYSE: TYG

Inception: 2/2004 | | Energy

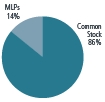

Infrastructure | | C-corp(2) | | $640.3 | |  | |  |

| Tortoise Midstream

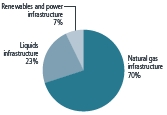

Energy Fund, Inc. NYSE: NTG

Inception: 7/2010 | | Natural Gas

Infrastructure | | C-corp(2) | | $328.5 | |  | |  |

| | Tortoise Pipeline

& Energy Fund, Inc. NYSE: TTP

Inception: 10/2011 | | North

American

pipeline

companies | | Regulated

investment

company | | $100.9 | |  | |  |

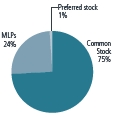

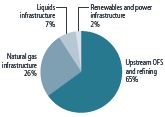

| | Tortoise Energy

Independence

Fund, Inc.NYSE: NDP

Inception: 7/2012 | | North

American

oil & gas

producers | | Regulated

investment

company | | $75.3 | |  | |  |

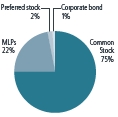

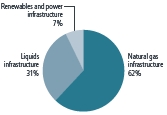

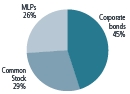

| | Tortoise Power

and Energy

Infrastructure

Fund, Inc. NYSE: TPZ

Inception: 7/2009 | | Power

& energy

infrastructure

companies

(Fixed income

& equity) | | Regulated

investment

company | | $132.9 | |  | |  |

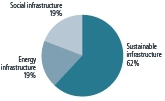

| | Ecofin Sustainable

and Social Impact

Term Fund NYSE: TEAF

Inception: 3/2019 | | Essential

assets | | Regulated

investment

company | | $264.3 | |  | |  |

| (1) | As of 5/31/2022 |

| (2) | TYG and NTG intend to qualify as regulated investment companies. See Note 2.E. to the financial statements for further disclosure. |

| |

| |

| |

| |

| Tortoise |

| 2022 Semi-Annual Report to closed-end fund stockholders |

| |

Dear stockholder

The first half of the 2022 fiscal year has proven to be a volatile environment with numerous headwinds for the broad market, including the renewable energy sector. Headwinds included recessionary concerns, rising inflation, as well as the anticipation of higher interest rates. The broad energy sector was an outlier with continued positive performance during the six-month period, although the sector pulled back significantly in June, following the fiscal period. Our social impact investments continued to improve post-COVID with educational facilities providing a stable environment for the first time since lockdown and senior living facilities seeing a recovery in occupancy rates.

Energy and power infrastructure

The broad energy sector, as represented by the S&P Energy Select Sector® Index returned 63.5% for the fiscal semi-annual period. After a strong start to the year, energy sold off along with the broader market on concerns about a looming recession. Concerns around energy security persisted, exacerbated by the impacts of the war in Ukraine and tightening global energy supply as demand rebounds post-COVID. Global underinvestment resulting from environmental, social and governance (ESG) commitments and energy transition is likely to keep global stock balances extremely tight for the foreseeable future, a dynamic that presents higher, but perhaps more volatile prices.

Despite higher commodity prices, global supply has not responded. OPEC+ production has continually undershot pledged production due to prolonged oil and gas underinvestment and rapidly shut-in production in 2020. The lack of supply coming to market is complicating assessments over the actual amount of OPEC spare capacity. Spare capacity is critical as it guards against prices rapidly rising should a market exogenous event occur. In addition to OPEC’s troubles, sanctions around exports of Russian energy started to take effect during the quarter. Russian volumes are projected to decline and/or face longer transit times to their end market. Given these disruptions, the focus has remained on the supply side of the equation. On the demand side, the scarcity of commodities comes at a time when the world is entering summer, or peak demand season. Global inventories continued to draw and are well below their 5-year averages to be drawn upon.

Global supply scarcity has created a renewed opportunity for short-cycle North American energy. U.S. oil production crossed 12 million (mm) barrels per day (b/d), a level not seen since April 2020. For 2022, the Energy Information Agency (EIA) forecasts that production will increase 1 mm b/d to 12.6 mm b/d, up from 11.6 mm b/d at the end of 2021. By the end of 2023, the EIA forecasts U.S. production growing to 13.4 mm b/d. The Permian, America’s biggest oil field, is expected to be the primary driver of production growth. During the second quarter, production within the basin surged to all-time highs of 5.2 mm b/d. Private operators continue to increase activity while major integrated energy companies have announced intentions to increase their production by 10-25%.

Transitioning to natural gas, the Russia-Ukraine conflict presents a large opportunity for U.S. liquefied natural gas (LNG). Entering 2022, Russian natural gas exports to Europe accounted for 13-15 billion cubic feet per day (Bcf/d) or 35-40% of the EU’s gas supply. With energy security a higher priority and low natural gas inventories, Europe has turned to U.S. LNG. During the first four months of 2022, the European Union (EU) accounted for 74% of total U.S. LNG exports per the EIA. The U.S. LNG market, while young, has grown from zero market share to the top export market in just over seven years. Throughout 2022, LNG exporters have contracted almost 5 Bcf/d of new contracts, signing 15-25-year contracts with European and Asian counterparties.

The midstream energy sector, represented by the Tortoise North American Pipeline IndexSM, returned 30.6% for the period. Investor sentiment rebounded with positive retail flows coupled with companies buying back stock in the open market. Beyond the constructive technical setup, we believe midstream serves as a hedge to many current risks investors face. Rising rates, inflation, higher commodity prices, and energy security all are key macro factors which could drive the global economy into recession.

It is important to note that a recession does not necessarily equate to a dip in energy demand. While there were several recessions in the last 40 years, energy demand increased in 38 out of the last 40 years (excluding 2008 and 2020). If any sector were to hold up in a near-term recession, we believe it would be energy. The world remains undersupplied in energy, we believe sector balance sheets are in much better shape than in past recessions including 2001, 2008, and 2020 and in our opinion, energy is the one part of the market where earnings have grown at an accelerated rate.

With inflation surging to 40-year highs, midstream can provide inflation protection. Pipelines typically have long-term contracts with inflation protection from regulated tariff escalators. Additionally, tariffs on regulated liquid pipelines often include an inflation escalator aligned with the Producer Price Index (PPI). Federal Energy Regulatory Commission (FERC) indexing could be a material driver of cash flows with rates potentially increasing over 13% next summer on top of an 8.7% increase already going into effect July 1, 2022.

Interest rates rose significantly in the first half of 2022 as the Federal Reserve took a more hawkish approach and started raising the Fed Funds rate. Midstream energy has displayed strong historical returns in rising rate environments. In the 15 time periods of rising rates since 2001, midstream energy, represented by the Tortoise North American Pipeline IndexSM, returned an average return of 8.5%, compared to a S&P 500 average return of 7.4%, and bond return of -1.9% represented by the Bloomberg Barclays U.S. Aggregate Bond Index.

Higher commodity prices are positive as midstream companies should expect more volumes flowing through pipeline systems. We expect the balanced return of capital story to continue for investors via debt reduction, share buybacks and increased distributions. The other use of capital has been mergers and acquisitions (M&A). In the first half

| |

| |

| 2022 Semi-Annual Report | May 31, 2022 |

| |

| |

| |

of 2022, there were several accretive bolt-on acquisitions of private assets completed by larger energy infrastructure companies. These assets expand the footprint of company existing assets and help operators keep volumes on systems across their value chains.

With energy supply short and energy security concerns emerging globally, investors are reminded how critical energy infrastructure is to daily life. Even before the Ukraine conflict, U.S. LNG cargoes were rapidly replenishing Europe’s low gas storage levels via LNG tankers. LPGs (liquid petroleum gases) were being exported to India and China, where demand is driven by global population growth and improvements in living standards. Whether it’s LNG, LPG, or crude oil, U.S. energy infrastructure companies have been signing long-term contracts and exporting energy all around the world.

On the regulatory front, it was a mixed quarter of news flow. Demand for low-cost U.S. natural gas created a need for additional natural gas pipelines and LNG export terminals. In the northeast Marcellus Basin, pipeline infrastructure is constrained. Despite this need, the one major pipeline which continues to be under construction is the Mountain Valley Pipeline (MVP). During the first half of 2022, the U.S. Court of Appeals for the Fourth Circuit overturned federal approval of a forest-crossing permit. Seeing the setback with MVP, companies are doing what they can to avoid the red-tape that comes with building new pipelines. For example, one company announced that its pipeline expansion will increase the mainline capacity from 2 billion cubic feet per day (Bcf/d) to 2.5 Bcf/d through the planned installation of three new compressor stations. Adding compression stations, for example, can help avoid the exhaustive permitting process affiliated with building new pipelines.

Sustainable infrastructure

Renewable energy

The beginning of the year has proven to be a volatile environment with numerous headwinds for the renewable sector. Europe’s accelerated pace in reducing fossil fuel generation, led by Germany’s decision to phase out nuclear and coal power plants, left the market highly dependent on Russian gas. In addition, French nuclear plants have faced unscheduled stops due to cracks and hydroelectric plants have been forced to operate at reduced levels due to poor hydro resources. The European power market was therefore tight. The Russian invasion of Ukraine then added geopolitical uncertainties to gas supply. Putting all these issues together, power prices across Europe have risen multiple times in the past 12 months. Supply constraints in global LNG and coal have had a spilling effect on power prices across the world as well.

Companies participating in the energy transition tend to benefit at the margin from higher power prices in the short-term. More importantly, higher fossil-fuel power prices highlight the imbedded value in operating renewables assets as well as in the renewables development pipeline providing affordable and stable power prices. On balance, we expect the events surrounding the invasion of Ukraine to result in a material acceleration of the energy transition.

High inflation and higher interest rates expectations, first in the U.S. and then in Europe, unnerved investors. As such, the companies in our investment universe couldn’t escape these fears even if their secular growth remains intact. However, unlike the broader market, earnings expectations for the majority of our portfolio companies have been revised up as a consequence of rising power prices and better renewables resources. In short, if anything, the fundamentals for the portfolio improved but concerns at the macro level and potential political intervention in some energy markets have been powerful headwinds.

In the midst of turbulence relating to supply chains, inflation, interest rates and geopolitics, the investment team remains focused on identifying long-term beneficiaries of the secular trends within the four master themes of the investment universe. In the medium term, inflation means higher electricity prices which is a material positive tailwind for the renewables sector. We would expect increased demand for renewable power purchase agreements (PPAs) at higher prices and longer tenors than we have seen in the past years.

We also expect an acceleration in renewables development activity as countries and companies want to ensure their security of supply at a predictable price. The macro environment remains a source of potential stress as inflation, interest rates, supply chain disruption and geopolitical tensions create a much tougher asset development environment for the companies we invest in. It is a supply issue and not a demand issue: as much as demand for renewables is strong and developers have pricing power, the industry is experiencing delays coming from bottlenecks (slow permitting process, equipment availability, shipping disruption). In the near-term, the elevated merchant power prices, higher contract prices and better generation volumes should more than offset all these issues and we expect 2022 to be a record year for most companies. At a time when the broader economy is affected by growth concerns and margin pressure, the secular growth in renewables and visibility on cash flows they provide become more sought-after attributes.

Waste transition

While the number of new projects under development in the waste transition sector continues to grow, bringing these projects to a financial closing remained challenging during the six-month period, largely due to continuing inflationary pressures and supply chain constraints. The result is an unusually large number of projects being delayed as developers re-evaluate elevated project construction budgets and their impact on pro-forma operating profitability.

The inflationary and supply chain impacts are three-fold. First, an increase in raw material prices for items such as steel has ballooned cost estimates for these capital-intensive projects. Second, the availability of critical equipment and systems components has been limited by supply-chain constraints, which has caused both price increases and delivery-time delays. Third, contractors that guarantee on-time and on-budget construction are demanding higher

premiums to offset against the potential for further price inflation and delivery-time delays. The combination of these issues — inflation, scarcity, and uncertainty — are leading to project cost increases of 25% or more in many cases.

In addition, development of renewable fuels projects was also adversely impacted by declining fuel credit prices, which generate a substantial portion of the pro-forma revenues for renewable fuels projects. In particular, projects being developed to produce renewable natural gas, renewable diesel, and sustainable aviation fuel saw significant declines in Federal Renewable Identification Number (or RIN) pricing and California Low Carbon Fuel Standard (or LCFS) pricing.

Regarding RIN pricing, D3 RINs, which support projects that convert cellulosic waste into renewable fuels, declined from $3.72 at end of 2021 to $3.30 at the end of the first quarter of 2022, a decline of more than 11%. During the same period, LCFS credits declined from $150 to $121, a decline of more than 19%. Fuel credit prices are expected to stabilize as the U.S. economy continues to recover toward full capacity, which would include higher demand for transportation fuels, and therefore higher demand for offset credits.

Finally, a milestone achievement in terms of recycling efforts occurred in early March 2022, when 175 member-states of the United Nations Environment Assembly signed a resolution to establish a legally-binding treaty on the design, production, and disposal of petroleum-based plastics by the end of 2024. The so called Global Plastics Treaty is intended to dramatically reduce the amount of plastics waste for a more circular economy, and is being hailed as the most significant multilateral agreement since the Paris Agreement on Climate Change in 2015. Absent any coordinated effort, the production of plastics is expected to double by 2040, after already doubling since 2000.

Despite the challenging environment in terms of rising construction costs and lower fuel credit prices, the number of new projects planned or under development in the waste transition sector continues to grow and is at all-time high levels in many sub-sectors, as the demand for renewable or recycled content remains strong.

Social impact

Education

The public bond market for new issuance of K-12 charter school and private school revenue bonds in Q1 2022 was $532,995,000, a 6.1% decrease from the same period in 2021.1 One of the primary factors driving the 28.4% market growth for K-12 charter school and private school bonds in 2021 were more than $60 billion in municipal bond fund inflows, the most ever in a single year.

Robust new issuance in first quarter, despite municipal bond fund outflows exceeding $30 billion and an increase of 96 bps in the 30-yr Municipal Market Data tax-exempt bond benchmark, is a clear indicator that schools’ demand for reliable facility finance remains high, even in the face of significant market headwinds.2

The beginning of the calendar year provided students, parents and schools with a degree of stability and normalcy not seen since widespread lockdowns were put into place in March 2020. Fears the COVID-19 Omicron variant would surge, overwhelm schools and then force a return to remote learning proved unfounded. In January, more than 60% of the nation’s K-12 school districts mandated the use of masks for all students & teachers. By the end of March, that number had fallen to less than 5%. Schools not offering in-person instruction peaked at 7,463 on January 10th, falling to 345 by March 28, 2022.3

Not all of the news from the K-12 sector was as positive. The Brookings Institution reported in March that “schools have faced severe staff shortages, high rates of absenteeism and quarantines, and rolling school closures. Furthermore, students and educators continue to struggle with mental health challenges, higher rates of violence and misbehavior, and concerns about lost instructional time.”4 A recent working paper published by the Annenberg Institute stated drops in academic achievement “are significantly larger than estimated impacts from other large-school disruptions, such as after Hurricane Katrina.” It also noted, “income-based (academic achievement) gaps have indeed expanded substantively during the COVID-19 pandemic.”5

While achieving the unprecedented highs of 2021 seems unlikely, Ecofin believes the market for K-12 charter school and private school revenue bonds will remain strong. Rising interest rates and the likelihood of resulting municipal bond fund outflows should increase the number and quality of school facility funding opportunities available to investors highly focused on this segment of the market.

Senior Living

In the first quarter of 2022, the senior living industry continued its occupancy rebound after having established a “bottom” in occupancy deterioration about a year ago. Statistically, nationwide occupancy for independent living and assisted living is 83.1% and 77.9%, respectively. Occupancy has increased 1.4% for independent and 3.7% for assisted living from pandemic lows.6 Moreover, absorption is robust after Q3 2021 set the highest level ever recorded at more than 4 times the pace of absorption pre-pandemic. While there’s clearly ground to cover, it’s revitalizing to see the industry making strides to get back to pre-pandemic levels of 89.7% and 84.6% for independent and assisted living, respectively.

| |

| |

| 2022 Semi-Annual Report | May 31, 2022 |

| |

| |

| |

According to a recent NIC Lending Trends Report, construction lending dramatically increased in the third quarter of 2021, up 45% quarter over quarter on a same store basis. After over a year of slowing construction starts, this shows a significant reversal and renewed developer optimism especially in the face of rising construction costs and material shortages. That said, the pandemic related slowdown in new construction should help existing communities regain occupancy with the lowest inventory growth recorded since 2013.

From now until 2030, an average of 10,000 baby boomers will turn 65 every day.7 With the combination of occupancy on the rise, we remain confident in the senior living industry’s ability to rebound and prepare for the upcoming “Silver Tsunami” as the population continues to age.

Concluding thoughts

A renewed focus on energy security and independence should be a tailwind for the broad energy sector, particularly energy infrastructure as investors are reminded of its critical place in their daily lives and this should also benefit much of the energy transition universe. We expect improvement in renewables as 2021 was affected by poor wind speed hydro resources across the globe and many companies’ generation volumes were below normal. These renewables resources tend to normalize to long-term averages over time and we are seeing stronger volumes of electricity generation in the first few months of the year that we expect to continue. Our opportunities for investing in social impact projects are expanding for many reasons, primarily as our sectors continue to see robust growth and competing financing providers are forced to scale back allocations.

The S&P Energy Select Sector® Index is a capitalization-weighted index of S&P 500® Index companies in the energy sector involved in the development or production of energy products. The Tortoise North American Pipeline IndexSM is a float adjusted, capitalization-weighted index of energy pipeline companies domiciled in the United States and Canada. The Tortoise MLP Index® is a float-adjusted, capitalization-weighted index of energy master limited partnerships.

The Tortoise indices are the exclusive property of Tortoise Index Solutions, LLC, which has contracted with S&P Opco, LLC (a subsidiary of S&P Dow Jones Indices LLC) to calculate and maintain the Tortoise MLP Index® and Tortoise North American Pipeline IndexSM (the “Indices”). The Indices are not sponsored by S&P Dow Jones Indices or its affiliates or its third party licensors (collectively, “S&P Dow Jones Indices LLC”). S&P Dow Jones Indices will not be liable for any errors or omission in calculating the Indices. “Calculated by S&P Dow Jones Indices” and its related stylized mark(s) are service marks of S&P Dow Jones Indices and have been licensed for use by Tortoise Index Solutions, LLC and its affiliates. S&P® is a registered trademark of Standard & Poor’s Financial Services LLC (“SPFS”), and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”).

It is not possible to invest directly in an index.

Performance data quoted represent past performance; past performance does not guarantee future results. Like any other stock, total return and market value will fluctuate so that an investment, when sold, may be worth more or less than its original cost.

| 1 | EMMA & MuniOS |

| 2 | Bloomberg |

| 3 | https://about.burbio.com/school-mask-policies-by-state/ |

| 4 | https://www.brookings.edu/blog/brown-center-chalkboard/2022/03/03/ the-pandemic-has-had-devastating-impacts-on-learning-what-will-it-taketo-help-students-catch-up/ |

| 5 | https://edworkingpapers.com/sites/default/files/ai22-521.pdf |

| 6 | NIC |

| 7 | census.gov |

| |

| |

| |

| |

| Tortoise |

| Energy Infrastructure Corp. (TYG) |

| |

Fund description

TYG seeks a high level of total return with an emphasis on current distributions paid to stockholders. TYG invests primarily in equity securities in energy infrastructure companies. The fund is positioned to benefit from growing energy demand and accelerated efforts to reduce global CO2 emissions in energy production. Energy infrastructure companies generate, transport and distribute electricity, as well as process, store, distribute and market natural gas, natural gas liquids, refined products and crude oil.

Management’s discussion of fund performance

The midstream energy sector had strong performance for the period. Investor sentiment rebounded with positive retail flows coupled with companies buying back stock in the open market. Beyond the constructive technical setup, we believe midstream serves as a hedge to many current risks investors face. Rising rates, inflation, higher commodity prices, and energy security all are key macro factors that could drive the global economy into recession. Since the fund’s inception, it has paid out more than $147 in cumulative distributions to stockholders. The fund’s market-based and NAV-based returns for the fiscal period ending May 31, 2022 were 26.5 and 20.9%, respectively (including the reinvestment of distributions). The Tortoise MLP Index® returned 31.8% during the same period.

| 2022 mid-fiscal year summary | | |

| Distributions paid per share | | $0.7100 |

| Distribution rate (as of 5/31/2022) | | 8.4% |

| Quarter-over-quarter distribution increase (decrease) | | 0.0% |

| Year-over-year distribution increase (decrease) | | 93.2% |

| Cumulative distributions paid per share to | | |

| stockholders since inception in February 2004 | | $39.5875(1) |

| Market-based total return | | 29.5% |

| NAV-based total return | | 23.8% |

| Premium (discount) to NAV (as of 5/31/2022) | | (18.0)% |

| (1) | Distribution per share is unadjusted for the impact of reverse stock split. |

Key asset performance drivers

| Top five contributors | | Company type |

| Williams Companies, Inc. | | Natural gas pipelines company |

| Targa Resources Corp. | | Natural gas pipeline company |

| Energy Transfer LP | | Natural gas pipeline company |

| Western Midstream Partners LP | | Gathering & processing company |

| American Electric Power Company Inc. | | Power company |

| | | |

| Bottom five contributors | | Company type |

| NextEra Energy Partners | | Diversified infrastructure company |

| Atlantica Sustainable Infrastructure PLC | | Power company |

| ESS Tech Inc. | | Energy storage company |

| Clearway Energy, Inc. | | Diversified infrastructure company |

| NextEra Energy Inc. | | Diversified infrastructure company |

Unlike the fund return, index return is pre-expenses and taxes.

Performance data quoted represent past performance; past performance does not guarantee future results. Like any other stock, total return and market value will fluctuate so that an investment, when sold, may be worth more or less than its original cost. Portfolio composition is subject to change due to ongoing management of the fund. References to specific securities or sectors should not be construed as a recommendation by the fund or its adviser. See Schedule of Investments for portfolio weighting at the end of the fiscal quarter.

| |

| |

| 2022 Semi-Annual Report | May 31, 2022 |

| |

| Tortoise |

| Energy Infrastructure Corp. (TYG) (continued) |

| |

Value of $10,000 vs. Tortoise Energy Infrastructure Fund – Market (unaudited)

From May 31, 2012 through May 31, 2022

The chart assumes an initial investment of $10,000. Performance reflects waivers of fee and operating expenses in effect. In the absence of such waivers, total return would be reduced. Performance data quoted represents past performance and does not guarantee future results. Investment returns and principal value will fluctuate, and when sold, may be worth more or less than their original cost. Performance current to the most recent month-end may be lower or higher than the performance quoted and can be obtained by calling 866-362-9331. Performance assumes the reinvestment of capital gains and income distributions. The performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Annualized Rates of Return as of May 31, 2022

| | 1-Year | | 3-Year | | 5-Year | | 10-Year | | Since Inception(1) |

| Tortoise Energy Infrastructure Fund – NAV | | 29.35% | | -17.08% | | -10.95% | | -3.64% | | 2.80% |

| Tortoise Energy Infrastructure Fund – Market | | 33.46% | | -21.38% | | -16.24% | | -6.85% | | 1.43% |

| Tortoise MLP Index® | | 30.22% | | 7.96% | | 4.10% | | 4.41% | | 8.50% |

| (1) | Inception date of the Fund was February 25, 2004. |

Fund structure and distribution policy

The fund intends to qualify as a Regulated Investment Company (RIC) allowing it to pass-through to shareholders income and capital gains earned, thus avoiding double-taxation. To qualify as a RIC, the fund must meet specific income, diversification and distribution requirements. See Note 2E to the financial statements for further disclosure.

The fund has adopted a managed distribution policy (“MDP”). Annual distribution amounts are expected to fall in the range of 7% to 10% of the average week-ending net asset value (“NAV”) per share for the prior fiscal semi-annual period. Distribution amounts will be reset both up and down to provide a consistent return on trailing NAV. Under the MDP, distribution amounts will normally be reset in February and August, with no changes in distribution amounts in May and November.

Leverage

The fund’s leverage utilization increased $9.6 million during the six months ended Q2 2022, compared to the six months ended Q4 2021, and represented 22.6% of total assets at May 31, 2022. During the period, the fund maintained compliance with its applicable coverage ratios. 83.8% of the leverage cost was fixed, the weighted-average maturity was 2.8 years and the weighted-average annual rate on leverage was 3.39%. These rates will vary in the future as a result of changing floating rates, utilization of the fund’s credit facility and as leverage and swaps mature or are redeemed. During the six month period ended May 31, 2022, $8.0 million of Senior Notes and $16.6 million in preferred stock were paid in full upon maturity. In December 2021, the fund issued $10.0 million in Senior Note principal and $20.0 million in preferred stock.

Income taxes

As of May 31, 2022, the fund’s deferred tax asset was zero. The fund had capital loss carryforwards of $179.0 million for federal income tax purposes, which can be used to offset future capital gains.

Please see the Financial Statements and Notes to Financial Statements for additional detail regarding critical accounting policies, results of operations, leverage, taxes and other important fund information.

For further information regarding the calculation of distributable cash flow and distributions to stockholders, as well as a discussion of the tax impact on distributions, please visit www.tortoiseecofin.com.

| |

| |

| |

| |

| TYG Key Financial Data (supplemental unaudited information) |

| (dollar amounts in thousands unless otherwise indicated) |

| |

The information presented below is supplemental non-GAAP financial information, is not inclusive of required financial disclosures (e.g. Total Expense Ratio), and should be read in conjunction with the full financial statements.

| | 2021 | | 2022 |

| | | Q1(1) | | | | Q2(1) | | | | Q3(1) | | | | Q4(1) | | | | Q1(1) | | | | Q2(1) | |

| Selected Financial Information | | | | | | | | | | | | | | | | | | | | | | | | |

| Distributions paid on common stock | | $ | 3,757 | | | $ | 4,056 | | | $ | 4,353 | | | $ | 5,368 | | | $ | 8,469 | | | $ | 8,469 | |

Distributions paid on common stock

per share(2) | | | 0.3150 | | | | 0.3400 | | | | 0.3650 | | | | 0.4500 | | | | 0.7100 | | | | 0.7100 | |

| Total assets, end of period(3) | | | 523,106 | | | | 581,461 | | | | 555,604 | | | | 569,245 | | | | 607,077 | | | | 640,253 | |

| Average total assets during period(3)(4) | | | 479,525 | | | | 553,147 | | | | 576,902 | | | | 570,749 | | | | 584,250 | | | | 624,786 | |

| Leverage(5) | | | 154,427 | | | | 152,127 | | | | 140,293 | | | | 135,393 | | | | 146,087 | | | | 144,987 | |

| Leverage as a percent of total assets | | | 29.5 | % | | | 26.2 | % | | | 25.3 | % | | | 23.8 | % | | | 24.1 | % | | | 22.6 | % |

Operating expenses before leverage

costs and current taxes(6) | | | 1.10 | % | | | 1.05 | % | | | 1.06 | % | | | 1.11 | % | | | 1.12 | % | | | 1.07 | % |

| Net unrealized depreciation, end of period | | | (418,329 | ) | | | (353,117 | ) | | | (357,262 | ) | | | (358,544 | ) | | | (317,454 | ) | | | (268,736 | ) |

| Net assets, end of period | | | 357,783 | | | | 409,216 | | | | 400,314 | | | | 414,945 | | | | 451,671 | | | | 492,282 | |

| Average net assets during period(7) | | | 345,122 | | | | 391,953 | | | | 419,744 | | | | 432,282 | | | | 428,235 | | | | 482,183 | |

| Net asset value per common share(2) | | | 30.00 | | | | 34.31 | | | | 33.56 | | | | 34.79 | | | | 37.87 | | | | 41.27 | |

| Market value per share(2) | | | 25.25 | | | | 27.26 | | | | 26.81 | | | | 27.27 | | | | 30.25 | | | | 33.84 | |

| Shares outstanding (000's) | | | 11,928 | | | | 11,928 | | | | 11,928 | | | | 11,928 | | | | 11,928 | | | | 11,928 | |

| (1) | Q1 is the period from December through February. Q2 is the period from March through May. Q3 is the period from June through August. Q4 is the period from September through November. |

| (2) | Adjusted to reflect 1 for 4 reverse stock split effective May 1, 2020. |

| (3) | Includes deferred issuance and offering costs on senior notes and preferred stock. |

| (4) | Computed by averaging month-end values within each period. |

| (5) | Leverage consists of senior notes, preferred stock and outstanding borrowings under credit facilities. |

| (6) | As a percent of total assets. |

| (7) | Computed by averaging daily net assets within each period. |

| |

| |

| 2022 Semi-Annual Report | May 31, 2022 |

| |

Tortoise

Midstream Energy Fund, Inc. (NTG) |

|

| |

Fund description

NTG seeks to provide stockholders with a high level of total return with an emphasis on current distributions. NTG invests primarily in midstream energy equities that own and operate a network of pipeline and energy related logistical infrastructure assets with an emphasis on those that transport, gather, process and store natural gas and natural gas liquids (NGLs). NTG targets midstream energy equities, including MLPs benefiting from U.S. natural gas production and consumption expansion, with minimal direct commodity exposure.

Management’s discussion of fund performance

The midstream energy sector had strong performance for the period. Investor sentiment rebounded with positive retail flows coupled with companies buying back stock in the open market. Beyond the constructive technical setup, we believe midstream serves as a hedge to many current risks investors face. Rising rates, inflation, higher commodity prices, and energy security all are key macro factors that could drive the global economy into recession. The fund’s market-based and NAV-based returns for the fiscal period ending May 31, 2022 were 29.8% and 28.5%, respectively (including the reinvestment of distributions). The Tortoise MLP Index® returned 31.8% during the same period.

| 2022 mid-fiscal year summary | | | | |

| Distributions paid per share | | | $0.7700 |

| Distribution rate (as of 5/31/2022) | | | 8.1 | % |

| Quarter-over-quarter distribution increase (decrease) | | | 0.0 | % |

| Year-over-year distribution increase (decrease) | | | 87.2 | % |

Cumulative distributions paid per share to

stockholders since inception in July 2010 | | $ | 19.5000 | (1) |

| Market-based total return | | | 30.6 | % |

| NAV-based total return | | | 29.4 | % |

| Premium (discount) to NAV (as of 5/31/2022) | | | (17.8 | )% |

| (1) | Distribution per share is unadjusted for the impact of reverse stock split. |

Key asset performance drivers

| Top five contributors | | Company type |

| Williams Companies, Inc. | | Natural gas pipelines company |

| Targa Resources Corp. | | Natural gas pipeline company |

| Kinder Morgan Inc. | | Natural gas pipeline company |

| Energy Transfer LP | | Natural gas pipeline company |

| Pembina Pipeline Corporation | | Crude oil pipeline company |

| | | |

| Bottom five contributors | | Company type |

| NextEra Energy Partners | | Diversified infrastructure

company |

Atlantica Sustainable

Infrastructure PLC | | Power company |

| Clearway Energy, Inc. | | Diversified infrastructure

company |

| ESS Tech Inc. | | Energy storage company |

| Altus Midstream Company | | Natural gas pipeline company |

Unlike the fund return, index return is pre-expenses and taxes.

Performance data quoted represent past performance; past performance does not guarantee future results. Like any other stock, total return and market value will fluctuate so that an investment, when sold, may be worth more or less than its original cost. Portfolio composition is subject to change due to ongoing management of the fund. References to specific securities or sectors should not be construed as a recommendation by the fund or its adviser. See Schedule of Investments for portfolio weighting at the end of the fiscal quarter.

(unaudited)

| |

| |

| |

| |

Tortoise

Midstream Energy Fund, Inc. (NTG) (continued) |

|

| |

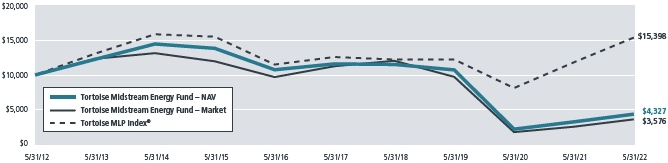

Value of $10,000 vs. Tortoise Midstream Energy Fund – Market (unaudited)

From May 31, 2012 through May 31, 2022

The chart assumes an initial investment of $10,000. Performance reflects waivers of fee and operating expenses in effect. In the absence of such waivers, total return would be reduced. Performance data quoted represents past performance and does not guarantee future results. Investment returns and principal value will fluctuate, and when sold, may be worth more or less than their original cost. Performance current to the most recent month-end may be lower or higher than the performance quoted and can be obtained by calling 866-362-9331. Performance assumes the reinvestment of capital gains and income distributions. The performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Annualized Rates of Return as of May 31, 2022

| | 1-Year | | 3-Year | | 5-Year | | 10-Year | | Since Inception(1) |

| Tortoise Midstream Energy Fund – NAV | | 36.04 | % | | -25.01 | % | | -17.15 | % | | -7.63 | % | | -5.68 | % |

| Tortoise Midstream Energy Fund – Market | | 42.33 | % | | -28.36 | % | | -20.50 | % | | -9.77 | % | | -7.59 | % |

| Tortoise MLP Index® | | 30.22 | % | | 7.96 | % | | 4.10 | % | | 4.41 | % | | 5.78 | % |

| (1) | Inception date of the Fund was July 27, 2010. |

Fund structure and distribution policy

The fund intends to qualify as a Regulated Investment Company (RIC) allowing it to pass-through to shareholders income and capital gains earned, thus avoiding double-taxation. To qualify as a RIC, the fund must meet specific income, diversification and distribution requirements. See Note 2E to the financial statements for further disclosure.

The fund has adopted a managed distribution policy (“MDP”). Annual distribution amounts are expected to fall in the range of 7% to 10% of the average week-ending net asset value (“NAV”) per share for the prior fiscal semi-annual period. Distribution amounts will be reset both up and down to provide a consistent return on trailing NAV. Under the MDP, distribution amounts will normally be reset in February and August, with no changes in distribution amounts in May and November.

Leverage

The fund’s leverage utilization increased approximately $6.1 million during the six months ended Q2 2022 compared to the six months ended Q4 2021, and represented 20.2% of total assets at May 31, 2022. During the period, the fund maintained compliance with its applicable coverage ratios. 78.2% of the leverage cost was fixed, the weighted-average maturity was 4.0 years and the weighted-average annual rate on leverage was 3.17%. These rates will vary in the future as a result of changing floating rates, utilization of the fund’s credit facility and as leverage matures or is redeemed. During the six month period ended May 31, 2022, the fund issued $25.0 million in Senior Note principal and $7.5 million in preferred stock.

Income taxes

As of May 31, 2022, the fund’s deferred tax asset was zero. The fund had capital loss carryforwards of $459.0 million for federal income tax purposes, which can be used to offset future capital gains.

Please see the Financial Statements and Notes to Financial Statements for additional detail regarding critical accounting policies, results of operations, leverage, taxes and other important fund information.

For further information regarding the calculation of distributable cash flow and distributions to stockholders, as well as a discussion of the tax impact on distributions, please visit www.tortoiseecofin.com.

| |

| |

| 2022 Semi-Annual Report | May 31, 2022 |

| |

| NTG Key Financial Data (supplemental unaudited information) |

| (dollar amounts in thousands unless otherwise indicated) |

| |

The information presented below is supplemental non-GAAP financial information, is not inclusive of required financial disclosures (e.g. Total Expense Ratio), and should be read in conjunction with the full financial statements.

| | 2021 | | 2022 |

| | | Q1(1) | | | | Q2(1) | | | | Q3(1) | | | | Q4(1) | | | | Q1(1) | | | | Q2(1) | |

| Selected Financial Information | | | | | | | | | | | | | | | | | | | | | | | | |

| Distributions paid on common stock | | $ | 1,862 | | | $ | 2,032 | | | $ | 2,172 | | | $ | 3,217 | | | $ | 4,345 | | | $ | 4,345 | |

Distributions paid on common stock

per share(2) | | | 0.3300 | | | | 0.3600 | | | | 0.3850 | | | | 0.5700 | | | | 0.7700 | | | | 0.7700 | |

| Total assets, end of period(3) | | | 257,953 | | | | 287,686 | | | | 277,673 | | | | 279,404 | | | | 307,035 | | | | 328,526 | |

| Average total assets during period(3)(4) | | | 237,709 | | | | 271,839 | | | | 287,464 | | | | 281,278 | | | | 289,590 | | | | 317,967 | |

| Leverage(5) | | | 68,640 | | | | 71,869 | | | | 67,969 | | | | 60,269 | | | | 63,069 | | | | 66,369 | |

| Leverage as a percent of total assets | | | 26.6 | % | | | 25.0 | % | | | 24.5 | % | | | 21.6 | % | | | 20.5 | % | | | 20.2 | % |

Operating expenses before leverage

costs and current taxes(6) | | | 1.28 | % | | | 1.10 | % | | | 1.21 | % | | | 1.25 | % | | | 1.22 | % | | | 1.07 | % |

Net unrealized appreciation (depreciation),

end of period | | | 44,946 | | | | 82,670 | | | | 81,302 | | | | 93,436 | | | | 129,068 | | | | 154,849 | |

| Net assets, end of period | | | 176,826 | | | | 206,310 | | | | 202,684 | | | | 210,018 | | | | 241,033 | | | | 260,924 | |

| Average net assets during period(7) | | | 171,201 | | | | 221,422 | | | | 213,041 | | | | 221,422 | | | | 221,176 | | | | 254,706 | |

| Net asset value per common share(2) | | | 31.34 | | | | 36.56 | | | | 35.92 | | | | 37.22 | | | | 42.71 | | | | 46.24 | |

| Market value per common share(2) | | | 27.00 | | | | 28.71 | | | | 28.55 | | | | 30.31 | | | | 34.81 | | | | 37.99 | |

| Shares outstanding (000's) | | | 5,643 | | | | 5,643 | | | | 5,643 | | | | 5,643 | | | | 5,643 | | | | 5,643 | |

| (1) | Q1 is the period from December through February. Q2 is the period from March through May. Q3 is the period from June through August. Q4 is the period from September through November. |

| (2) | Adjusted to reflect 1 for 10 reverse stock split effective May 1, 2020. |

| (3) | Includes deferred issuance and offering costs on senior notes and preferred stock. |

| (4) | Computed by averaging month-end values within each period. |

| (5) | Leverage consists of senior notes, preferred stock and outstanding borrowings under the credit facility. |

| (6) | Computed as a percent of total assets. |

| (7) | Computed by averaging daily net assets within each period. |

| |

| |

| |

| |

Tortoise

Pipeline & Energy Fund, Inc. (TTP) |

|

| |

Fund description

TTP seeks a high level of total return with an emphasis on current distributions paid to stockholders. TTP invests primarily in equity securities of North American pipeline companies that transport natural gas, natural gas liquids (NGLs), crude oil and refined products and, to a lesser extent, in other energy infrastructure companies.

Management’s discussion of fund performance

The midstream energy sector had strong performance for the period. Investor sentiment rebounded with positive retail flows coupled with companies buying back stock in the open market. Beyond the constructive technical setup, we believe midstream serves as a hedge to many current risks investors face. Rising rates, inflation, higher commodity prices, and energy security all are key macro factors that could drive the global economy into recession. The fund’s market-based and NAV-based returns for the fiscal period ending May 31, 2021 were 35.7% and 29.8%, respectively (including the reinvestment of distributions). The Tortoise North American Pipeline IndexSM returned 30.6% for the same period.

2022 mid-fiscal year summary

| Distributions paid per share | | | $0.5900 |

| Distribution rate (as of 5/31/2022) | | | 7.9 | % |

| Quarter-over-quarter distribution increase (decrease) | | | 0.0 | % |

| Year-over-year distribution increase (decrease) | | | 122.6 | % |

Cumulative distributions paid per share to

stockholders since inception in October 2011 | | $ | 16.1175 | (1) |

| Market-based total return | | | 33.8 | % |

| NAV-based total return | | | 32.9 | % |

| Premium (discount) to NAV (as of 5/31/2022) | | | (16.5 | )% |

| (1) | Distribution per share is unadjusted for the impact of reverse stock split. |

Please refer to the inside front cover of the report for important information about the fund’s distribution policy.

The fund utilizes a covered call strategy when appropriate, which seeks to generate income while reducing overall volatility. No covered calls were written during the period.

Key asset performance drivers

| Top five contributors | | Company type |

| Williams Companies, Inc. | | Natural gas pipeline company |

| Enbridge Inc. | | Crude oil pipeline company |

| Kinder Morgan Inc. | | Natural gas pipeline company |

| Pembina Pipeline Corporation | | Crude oil pipeline company |

| TC Energy Corp. | | Natural gas pipeline company |

| | | |

| Bottom five contributors | | Company type |

| Equitrans Midstream | | Gathering & processing |

| Corporation | | company |

| NextEra Energy Partners | | Diversified infrastructure

company |

| ESS Tech Inc. | | Energy storage company |

| Clearway Energy, Inc. | | Diversified infrastructure

company |

| Altus Midstream Company | | Natural gas pipeline company |

Unlike the fund return, index return is pre-expenses.

Performance data quoted represent past performance; past performance does not guarantee future results. Like any other stock, total return and market value will fluctuate so that an investment, when sold, may be worth more or less than its original cost. Portfolio composition is subject to change due to ongoing management of the fund. References to specific securities or sectors should not be construed as a recommendation by the fund or its adviser. See Schedule of Investments for portfolio weighting at the end of the fiscal quarter.

(unaudited)

| |

| |

| 2022 Semi-Annual Report | May 31, 2022 |

| |

| Tortoise |

Pipeline & Energy Fund, Inc. (TTP) (continued) |

| |

Value of $10,000 vs. Tortoise Pipeline and Energy Fund – Market (unaudited)

From May 31, 2012 through May 31, 2022

The chart assumes an initial investment of $10,000. Performance reflects waivers of fee and operating expenses in effect. In the absence of such waivers, total return would be reduced. Performance data quoted represents past performance and does not guarantee future results. Investment returns and principal value will fluctuate, and when sold, may be worth more or less than their original cost. Performance current to the most recent month-end may be lower or higher than the performance quoted and can be obtained by calling 866-362-9331. Performance assumes the reinvestment of capital gains and income distributions. The performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Annualized Rates of Return as of May 31, 2022

| | 1-Year | | 3-Year | | 5-Year | | 10-Year | | Since Inception(1) |

| Tortoise Pipeline and Energy Fund – NAV | | | 32.38 | % | | | | -11.35 | % | | | | -8.68 | % | | | | -2.15 | % | | | | -1.76 | % | |

| Tortoise Pipeline and Energy Fund – Market | | | 40.97 | % | | | | -13.37 | % | | | | -11.06 | % | | | | -3.69 | % | | | | -3.85 | % | |

| Tortoise North American Pipeline Index | | | 30.64 | % | | | | 12.12 | % | | | | 9.15 | % | | | | 8.72 | % | | | | 8.68 | % | |

(1) | Inception date of the Fund was October 26, 2011. |

Fund structure and distribution policy

The fund is structured to qualify as a Regulated Investment Company (RIC) allowing it to pass-through to shareholders income and capital gains earned, thus avoiding double-taxation. To qualify as a RIC, the fund must meet specific income, diversification and distribution requirements. Regarding income, at least 90 percent of the fund’s gross income must be from dividends, interest and capital gains. The fund must meet quarterly diversification requirements including the requirement that at least 50 percent of the assets be in cash, cash equivalents or other securities with each single issuer of other securities not greater than 5 percent of total assets. No more than 25 percent of total assets can be invested in any one issuer other than government securities or other RIC’s. The fund must also distribute at least 90 percent of its investment company income. RIC’s are also subject to excise tax rules which require RIC’s to distribute approximately 98 percent of net income and net capital gains to avoid a 4 percent excise tax.

The fund has adopted a distribution policy which is included on the inside front cover of this report. To summarize, the fund has adopted a managed distribution policy (“MDP”). Annual distribution amounts are expected to fall in the range of 7% to 10% of the average week-ending net asset value (“NAV”) per share for the prior fiscal semi-annual period. Distribution amounts will be reset both up and down to provide a consistent return on trailing NAV. Under the MDP, distribution amounts will normally be reset in February and August, with no changes in distribution amounts in May and November. The fund may designate a portion of its distributions as capital gains and may also distribute additional capital gains in the last quarter of the year to meet annual excise distribution requirements. Distribution amounts are subject to change from time to time at the discretion of the Board.

Leverage

The fund’s leverage utilization increased approximately $2.8 million during the six months ended Q2 2022, compared to the six months ended Q4 2021, and represented 20.6% of total assets at May 31, 2022. During the period, the fund maintained compliance with its applicable coverage ratios. 48.0% of the leverage cost was fixed, the weighted-average maturity was 1.5 years and the weighted-average annual rate on leverage was 3.86%. These rates will vary in the future as a result of changing floating rates, utilization of the fund’s credit facility and as leverage matures or is redeemed.

Please see the Financial Statements and Notes to Financial Statements for additional detail regarding critical accounting policies, results of operations, leverage and other important fund information.

For further information regarding the calculation of distributable cash flow and distributions to stockholders, as well as a discussion of the tax impact on distributions, please visit www.tortoiseecofin.com.

| |

| |

| |

| |

| TTP Key Financial Data (supplemental unaudited information) |

| (dollar amounts in thousands unless otherwise indicated) |

| |

The information presented below is supplemental non-GAAP financial information, is not inclusive of required financial disclosures (e.g. Total Expense Ratio), and should be read in conjunction with the full financial statements.

| | | 2021 | | 2022 |

| | Q1(1) | | Q2(1) | | Q3(1) | | Q4(1) | | Q1(1) | | Q2(1) |

| Selected Financial Information | | | | | | | | | | | | | | | | | | | | | | | | |

| Distributions paid on common stock | | $ | 371 | | | $ | 365 | | | $ | 831 | | | $ | 824 | | | $ | 1,314 | | | $ | 1,314 | |

| Distributions paid on common stock | | | | | | | | | | | | | | | | | | | | | | | | |

| per share(2) | | | 0.1600 | | | | 0.1600 | | | | 0.3700 | | | | 0.3700 | | | | 0.5900 | | | | 0.5900 | |

| Total assets, end of period(3) | | | 75,473 | | | | 88,149 | | | | 83,133 | | | | 80,898 | | | | 92,230 | | | | 100,901 | |

| Average total assets during period(3)(4) | | | 71,333 | | | | 81,731 | | | | 86,656 | | | | 84,993 | | | | 86,730 | | | | 96,706 | |

| Leverage(5) | | | 20,557 | | | | 20,557 | | | | 20,557 | | | | 18,143 | | | | 20,143 | | | | 20,943 | |

| Leverage as a percent of total assets | | | 27.2 | % | | | 23.3 | % | | | 24.7 | % | | | 22.4 | % | | | 21.8 | % | | | 20.8 | % |

| Operating expenses before leverage costs(6) | | | 1.78 | % | | | 1.66 | % | | | 1.60 | % | | | 1.03 | % | | | 1.57 | % | | | 1.44 | % |

| Net unrealized appreciation (depreciation), | | | | | | | | | | | | | | | | | | | | | | | | |

| end of period | | | (11,507 | ) | | | 1,568 | | | | (313 | ) | | | 1,003 | | | | 11,927 | | | | 20,208 | |

| Net assets, end of period | | | 53,891 | | | | 66,024 | | | | 62,043 | | | | 62,289 | | | | 71,653 | | | | 79,443 | |

| Average net assets during period(7) | | | 52,929 | | | | 61,405 | | | | 66,284 | | | | 67,014 | | | | 66,721 | | | | 76,749 | |

| Net asset value per common share(2) | | | 23.35 | | | | 28.96 | | | | 27.70 | | | | 27.96 | | | | 32.16 | | | | 35.66 | |

| Market value per common share(2) | | | 21.32 | | | | 22.69 | | | | 23.05 | | | | 23.16 | | | | 26.44 | | | | 29.76 | |

| Shares outstanding (000's) | | | 2,308 | | | | 2,279 | | | | 2,239 | | | | 2,228 | | | | 2,228 | | | | 2,228 | |

| (1) | Q1 is the period from December through February. Q2 is the period from March through May. Q3 is the period from June through August. Q4 is the period from September through November. |

| (2) | Adjusted to reflect 1 for 4 reverse stock split effective May 1, 2020. |

| (3) | Includes deferred issuance and offering costs on senior notes and preferred stock. |

| (4) | Computed by averaging month-end values within each period. |

| (5) | Leverage consists of senior notes, preferred stock and outstanding borrowings under the revolving credit facility. |

| (6) | Computed as a percent of total assets. |

| (7) | Computed by averaging daily net assets within each period. |

| |

| |

| 2022 Semi-Annual Report | May 31, 2022 |

| |

| Tortoise |

Energy Independence Fund, Inc. (NDP) |

| |

Fund description

NDP seeks a high level of total return with an emphasis on current distributions paid to stockholders. NDP invests primarily in equity securities of upstream North American energy companies that engage in the exploration and production of crude oil, condensate, natural gas and natural gas liquids that generally have a significant presence in North American oil and gas fields, including shale reservoirs.

Management’s discussion of fund performance

Concerns around energy security persisted, exacerbated by the impacts of the war in Ukraine and tightening global energy supply as demand rebounds post-COVID. Despite higher commodity prices, global supply has not responded. OPEC+ production has continually undershot pledged production due to prolonged oil and gas underinvestment and rapidly shut-in production in 2020. Global underinvestment resulting from environmental, social and governance (ESG) commitments and energy transition is likely to keep global stock balances extremely tight for the foreseeable future, a dynamic that presents higher, but perhaps more volatile prices. The fund’s market-based and NAV-based returns for the fiscal period ending May 31, 2022 were 51.3% and 55.5%, respectively (including the reinvestment of distributions).

| 2022 mid-fiscal year summary | | | | |

| Distributions paid per share | | | $0.4800 |

| Distribution rate (as of 5/31/2022) | | | 5.9 | % |

| Quarter-over-quarter distribution increase (decrease) | | | 0.0 | % |

| Year-over-year distribution increase (decrease) | | | 209.7 | % |

| Cumulative distributions paid per share to | | | | |

| stockholders since inception in July 2012 | | $ | 13.6925 | (1) |

| Market-based total return | | | 50.6 | % |

| NAV-based total return | | | 58.8 | % |

| Premium (discount) to NAV (as of 5/31/2022) | | | (16.1 | )% |

(1) | Distribution per share is unadjusted for the impact of reverse stock split. |

The fund utilizes a covered call strategy when appropriate, which seeks to generate income while reducing overall volatility. No covered calls were written during the period.

Key asset performance drivers

| Top five contributors | | Company type |

| EQT Corp. | | Oil & gas production company |

| Devon Energy Corporation | | Oil & gas production company |

| Pioneer Natural Resources Co. | | Oil & gas production company |

| Occidental Petroleum Corp. | | Oil & gas production company |

| EOG Resources Inc. | | Oil & gas production company |

| | | |

| Bottom five contributors | | Company type |

| ESS Tech Inc. | | Energy storage company |

| Denbury Inc. | | Independent energy company |

| NextEra Energy Inc. | | Diversified infrastructure |

| | company |

| Clean Energy Fuels Corp. | | Renewables and power |

| | infrastructure company |

| Archaea Energy Inc. | | Renewables and power |

| | infrastructure company |

Unlike the fund return, index return is pre-expenses.

Performance data quoted represent past performance: past performance does not guarantee future results. Like any other stock, total return and market value will fluctuate so that an investment, when sold, may be worth more or less than its original cost. Portfolio composition is subject to change due to ongoing management of the fund. References to specific securities or sectors should not be construed as a recommendation by the fund or its adviser. See Schedule of Investments for portfolio weighting at the end of the fiscal quarter.

| |

| |

| |

| |

| Tortoise |

Energy Independence Fund, Inc. (NDP) (continued) |

| |

Value of $10,000 vs. Tortoise Energy Independence Fund – Market (unaudited)

Since inception on July 26, 2012 through May 31, 2022

The chart assumes an initial investment of $10,000. Performance reflects waivers of fee and operating expenses in effect. In the absence of such waivers, total return would be reduced. Performance data quoted represents past performance and does not guarantee future results. Investment returns and principal value will fluctuate, and when sold, may be worth more or less than their original cost. Performance current to the most recent month-end may be lower or higher than the performance quoted and can be obtained by calling 866-362-9331. Performance assumes the reinvestment of capital gains and income distributions. The performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Annualized Rates of Return as of May 31, 2022 |

| | | | | | | | | | | | | | | | | | | |

| | 1-Year | | 3-Year | | 5-Year | | Since Inception(1) |

| Tortoise Energy Independence Fund - NAV | | | 78.28 | % | | | | -1.87 | % | | | | -10.33 | % | | | | -6.42 | % | |

| Tortoise Energy Independence Fund - Market | | | 73.55 | % | | | | -13.99 | % | | | | -14.40 | % | | | | -8.50 | % | |

| S&P 500 Energy Select Sector Index | | | 74.76 | % | | | | 20.96 | % | | | | 11.20 | % | | | | 6.20 | % | |

(1) | Inception date of the Fund was July 26, 2012. |

Fund structure and distribution policy

The fund is structured to qualify as a Regulated Investment Company (RIC) allowing it to pass-through to shareholders income and capital gains earned, thus avoiding double-taxation. To qualify as a RIC, the fund must meet specific income, diversification and distribution requirements. Regarding income, at least 90 percent of the fund’s gross income must be from dividends, interest and capital gains. The fund must meet quarterly diversification requirements including the requirement that at least 50 percent of the assets be in cash, cash equivalents or other securities with each single issuer of other securities not greater than 5 percent of total assets. No more than 25 percent of total assets can be invested in any one issuer other than government securities or other RIC’s. The fund must also distribute at least 90 percent of its investment company income. RIC’s are also subject to excise tax rules which require RIC’s to distribute approximately 98 percent of net income and net capital gains to avoid a 4 percent excise tax.

The fund has adopted a managed distribution policy (“MDP”). Annual distribution amounts are expected to fall in the range of 7% to 10% of the average week-ending net asset value (“NAV”) per share for the prior fiscal semi-annual period. Distribution amounts will be reset both up and down to provide a consistent return on trailing NAV. Under the MDP, distribution amounts will normally be reset in February and August, with no changes in distribution amounts in May and November. The fund may designate a portion of its distributions as capital gains and may also distribute additional capital gains in the last quarter of the year to meet annual excise distribution requirements. Distribution amounts are subject to change from time to time at the discretion of the Board.

Leverage

The fund’s leverage utilization increased $0.9 million during the six months ended Q2 2022 as compared to the six months ended Q4 2021. The fund utilizes all floating rate leverage that had an interest rate of 2.22% and represented 4.8% of total assets at year-end. During the period, the fund maintained compliance with its applicable coverage ratios. The interest rate on the fund’s leverage will vary in the future along with changing floating rates.

Please see the Financial Statements and Notes to Financial Statements for additional detail regarding critical accounting policies, results of operations, leverage and other important fund information.

For further information regarding the calculation of distributable cash flow and distributions to stockholders, as well as a discussion of the tax impact on distributions, please visit www.tortoiseecofin.com.

| |

| |

| 2022 Semi-Annual Report | May 31, 2022 |

| |

| NDP Key Financial Data (supplemental unaudited information) |

(dollar amounts in thousands unless otherwise indicated) |

| |

The information presented below is supplemental non-GAAP financial information, is not inclusive of required financial disclosures (e.g. Total Expense Ratio), and should be read in conjunction with the full financial statements.

| | 2021 | | 2022 |

| | Q1(1) | | Q2(1) | | Q3(1) | | Q4(1) | | Q1(1) | | Q2(1) |

| Selected Financial Information | | | | | | | | | | | | | | | | | | | | | | | | |

| Distributions paid on common stock | | $ | — | | | $ | — | | | $ | 572 | | | $ | 572 | | | $ | 886 | | | $ | 886 | |

| Distributions paid on common stock | | | | | | | | | | | | | | | | | | | | | | | | |

| per share(2) | | | — | | | | — | | | | 0.3100 | | | | 0.3100 | | | | 0.4800 | | | | 0.4800 | |

| Total assets, end of period | | | 43,206 | | | | 46,930 | | | | 43,973 | | | | 51,135 | | | | 62,500 | | | | 75,288 | |

| Average total assets during period(3) | | | 37,831 | | | | 44,909 | | | | 45,851 | | | | 49,036 | | | | 55,216 | | | | 67,737 | |

| Leverage(4) | | | 4,400 | | | | 3,600 | | | | 3,100 | | | | 2,700 | | | | 3,200 | | | | 3,600 | |

| Leverage as a percent of total assets | | | 10.2 | % | | | 7.7 | % | | | 7.0 | % | | | 5.3 | % | | | 5.1 | % | | | 4.8 | % |

| Operating expenses before leverage | | | | | | | | | | | | | | | | | | | | | | | | |

| costs as a percent of total assets | | | 2.27 | % | | | 2.02 | % | | | 2.12 | % | | | 1.30 | % | | | 1.80 | % | | | 1.49 | % |

| Net unrealized appreciation (depreciation), | | | | | | | | | | | | | | | | | | | | | | | | |

| end of period | | | 2,902 | | | | 7,043 | | | | 5,595 | | | | 9,327 | | | | 22,097 | | | | 32,340 | |

| Net assets, end of period | | | 38,160 | | | | 42,560 | | | | 40,604 | | | | 46,398 | | | | 58,650 | | | | 71,407 | |

| Average net assets during period(5) | | | 34,528 | | | | 41,089 | | | | 42,801 | | | | 46,787 | | | | 51,521 | | | | 64,733 | |

| Net asset value per common share(2) | | | 20.67 | | | | 23.06 | | | | 22.00 | | | | 25.13 | | | | 31.77 | | | | 38.68 | |

| Market value per common share(2) | | | 17.74 | | | | 19.88 | | | | 19.49 | | | | 22.24 | | | | 27.59 | | | | 32.47 | |

| Shares outstanding (000's) | | | 1,846 | | | | 1,846 | | | | 1,846 | | | | 1,846 | | | | 1,846 | | | | 1,846 | |

| (1) | Q1 is the period from December through February. Q2 is the period from March through May. Q3 is the period from June through August. Q4 is the period from September through November. |

| (2) | Adjusted to reflect 1 for 8 reverse stock split effective May 1, 2020. |

| (3) | Computed by averaging month-end values within each period. |

| (4) | Leverage consists of outstanding borrowings under the revolving credit facility. |

| (5) | Computed by averaging daily net assets within each period. |

| |

| |

| |

| |

| Tortoise |

| Power and Energy Infrastructure Fund, Inc. (TPZ) |

| |

Fund description

TPZ seeks to provide a high level of current income to stockholders, with a secondary objective of capital appreciation. TPZ seeks to invest primarily in fixed income and dividend-paying equity securities of power and energy infrastructure companies that provide stable and defensive characteristics throughout economic cycles.

Management’s discussion of fund performance

The midstream energy sector had strong performance for the period. Investor sentiment rebounded with positive retail flows coupled with companies buying back stock in the open market. Beyond the constructive technical setup, we believe midstream serves as a hedge to many current risks investors face. Rising rates, inflation, higher commodity prices, and energy security all are key macro factors that could drive the global economy into recession. The fund’s market-based and NAV-based returns for the fiscal period ending May 31, 2022 were 7.4% and 9.9%, respectively (including the reinvestment of distributions). Comparatively, the TPZ Benchmark Composite* returned -1.3% for the same period. The fund’s equity holdings outperformed its fixed income holdings for the period on a total return basis.

| 2022 mid-fiscal year summary | | |

| Distributions paid per share | | $0.3150 |

| Monthly distributions paid per share | | $0.105 |

| Distribution rate (as of 5/31/2022) | | 8.9% |

| Quarter-over-quarter distribution increase (decrease) | | 40.0% |

| Year-over-year distribution increase (decrease) | | 96.9% |

| Cumulative distribution to stockholders | | |

| since inception in July 2009 | | $19.005 |

| Market-based total return | | 13.7% |

| NAV-based total return | | 12.6% |

| Premium (discount) to NAV (as of 5/31/2022) | | (13.5)% |

| * | The TPZ Benchmark Composite includes the BofA Merrill Lynch U.S. Energy Index (CIEN), the BofA Merrill Lynch U.S. Electricity Index (CUEL) and the Tortoise MLP Index® (TMLP). It is comprised of a blend of 70% fixed income and 30% equity securities issued by companies in the power and energy infrastructure sectors. |

Please refer to the inside front cover of the report for important information about the fund’s distribution policy.

Key asset performance drivers

| Top five contributors | | Company type |

| Williams Companies, Inc. | | Natural gas pipelines company |

| Enterprise Products Partners | | Natural gas pipeline company |

| Energy Transfer LP | | Natural gas pipeline company |

| Western Midstream Partners LP | | Gathering & processing

company |

| | |

| DCP Midstream LP | | Natural gas pipeline company |

| | | |

| Bottom five contributors | | Company type |

| NextEra Energy, Inc. | | Diversified infrastructure |

| 4.800% Due 12/1/2077 | | company |

| Enbridge Inc. | | Crude oil pipeline company |

| 5.500% Due 7/15/2077 | | |

| ONEOK Inc. | | Natural gas pipeline company |

| 6.350% Due 1/15/2031 | | |

| Buckeye Partners LP | | Refined products pipeline |

| 5.850% Due 11/15/2043 | | company |

| ESS Tech Inc | | Energy storage company |

Unlike the fund return, index return is pre-expenses.

Performance data quoted represent past performance; past performance does not guarantee future results. Like any other stock, total return and market value will fluctuate so that an investment, when sold, may be worth more or less than its original cost. Portfolio composition is subject to change due to ongoing management of the fund. References to specific securities or sectors should not be construed as a recommendation by the fund or its adviser. See Schedule of Investments for portfolio weighting at the end of the fiscal quarter.

| |

| |

| 2022 Semi-Annual Report | May 31, 2022 |

| |

| Tortoise |

| Power and Energy Infrastructure Fund, Inc. (TPZ) (continued) |

| |

| Value of $10,000 vs. Tortoise Power and Energy Infrastructure Fund – Market (unaudited) |

| From May 31, 2012 through May 31, 2022 |

The chart assumes an initial investment of $10,000. Performance reflects waivers of fee and operating expenses in effect. In the absence of such waivers, total return would be reduced. Performance data quoted represents past performance and does not guarantee future results. Investment returns and principal value will fluctuate, and when sold, may be worth more or less than their original cost. Performance current to the most recent month-end may be lower or higher than the performance quoted and can be obtained by calling 866-362-9331. Performance assumes the reinvestment of capital gains and income distributions. The performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Annualized Rates of Return as of May 31, 2022

| | 1-Year | | 3-Year | | 5-Year | | 10-Year | | Since Inception(2) |

| Tortoise Power and Energy Infrastructure Fund – NAV | | 11.01 | % | | 0.75 | % | | 0.69 | % | | 3.25 | % | | | 5.93 | % | |

| Tortoise Power and Energy Infrastructure Fund – Market | | 13.94 | % | | -0.85 | % | | -0.98 | % | | 2.29 | % | | | 4.74 | % | |

| TPZ Benchmark Composite(1) | | 10.02 | % | | 7.45 | % | | 5.51 | % | | 4.92 | % | | | 6.86 | % | |

| (1) | The TPZ Benchmark Composite includes the BofA Merrill Lynch U.S. Energy Index (CIEN), the BofA Merrill Lynch U.S. Electricity Index (CUEL) and the Tortoise MLP Index® (TMLP). |

| (2) | Inception date of the Fund was July 29, 2009. |

Fund structure and distribution policy