Washington, D.C. 20549

For the transition period from ______________ to ______________.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.T

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

(1) Proxy Statement for the 2012 Annual Meeting of Stockholders of the Registrant (Part III).

First Guaranty Bancshares, Inc. (the “Company”) is a bank holding company headquartered in Hammond, Louisiana with one wholly owned subsidiary, First Guaranty Bank (the “Bank”). At December 31, 2011, the Company had consolidated assets of $1.4 billion with $126.6 million in consolidated stockholders’ equity. The Company’s executive office is located at 400 East Thomas Street, Hammond, Louisiana 70401. The telephone number is (985) 345-7685. The Company is subject to extensive regulation by the Board of Governors of the Federal Reserve System (“FRB”).

Our focus is on the bedroom communities of metropolitan markets, small cities and rural areas in southeast, southwest and north Louisiana. In southeast Louisiana, eight branches are located in Tangipahoa Parish in the towns of Amite, Hammond (2), Independence, Kentwood (2) and Ponchatoula (2). Three branches are located in Livingston Parish, with a branch in Denham Springs, Walker and Watson. In southwest Louisiana, we have branches in Abbeville and Jennings which are located in Vermillion Parish and Jefferson Davis Parish, respectively. The Company also has two branches in St. Helena Parish, one in Greensburg and the other in Montpelier. The remaining six branches are located in north Louisiana, in Haynesville and Homer, which are both in Claiborne Parish; in Oil City and Vivian, both in Caddo Parish; in Dubach in Lincoln Parish and Benton, in Bossier Parish. Our core market remains in the home parish of Tangipahoa where approximately 50.3% of deposits and 39.3% of net loans were based in 2011.

Our southeast Louisiana market is strategically located near the intersection of Interstates 12 and 55, which places it at a crossroads of commercial activity for the southeastern United States. In addition, this market area is largely populated by the work force of several nearby petrochemical refineries and other industrial plants and is a bedroom community for the urban centers of New Orleans and Baton Rouge, which are approximately 45 miles and 60 miles, respectively, from Hammond, where the main office is located. Hammond is home to one of the largest medical centers in the state of Louisiana and the third largest state university in Louisiana.

Our southwest Louisiana market benefits from a profitable casino gaming industry and substantial tourism revenue derived from the Louisiana Acadian culture. It also has a concentration of oil field and oil field services activity and is a thriving agricultural center for rice, sugarcane and crawfish. Timber cultivation and its related industries, including milling and logging, are key commercial activities in the north Louisiana market. It is also an agrarian center in which corn, cotton and soybeans are the primary crops. The poultry industry, including independent poultry grower farms that contract with national poultry processing companies, are also very important to the local economy.

The Company offers personalized commercial banking services to businesses, professionals and individuals. We offer a variety of deposit products including personal and business checking and savings accounts, time deposits, money market accounts and NOW accounts. Other services provided include personal and commercial credit cards, remote deposit capture, safe deposit boxes, official checks, traveler's checks, internet banking, online bill pay, mobile banking and lockbox services. Also offered is 24-hour banking through internet banking, voice response and thirty automated teller machines. Although full trust powers have been granted, we do not actively operate or have any present intention to activate a trust department.

The Bank is engaged in a diversity of lending activities to serve the credit needs of its customer base including commercial loans, commercial real estate loans, real estate construction loans, residential mortgage loans, agricultural loans, home equity lines of credit, equipment loans, inventory financing and student loans. In addition, the Bank provides consumer loans for a variety of reasons such as the purchase of automobiles, recreational vehicles or boats, investments or other consumer needs. The Bank issues MasterCard and Visa credit cards and provides merchant processing services to commercial customers. The loan portfolio is divided, for regulatory purposes, into four broad classifications: (i) real estate loans, which include all loans secured in whole or part by real estate; (ii) agricultural loans, comprised of all farm loans; (iii) commercial and industrial loans, which include all commercial and industrial loans that are not secured by real estate; and (iv) consumer loans.

The banking business in Louisiana is extremely competitive. We compete for deposits and loans with existing Louisiana and out-of-state financial institutions that have longer operating histories, larger capital reserves and more established customer bases. The competition includes large financial services companies and other entities in addition to traditional banking institutions such as savings and loan associations, savings banks, commercial banks and credit unions.

Many of our larger competitors have a greater ability to finance wide-ranging advertising campaigns through their greater capital resources. Marketing efforts depend heavily upon referrals from officers, directors and shareholders, selective advertising in local media and direct mail solicitations. We compete for business principally on the basis of personal service to customers, customer access to officers and directors and competitive interest rates and fees.

In the financial services industry, intense market demands, technological and regulatory changes and economic pressures have eroded industry classifications in recent years that were once clearly defined. Financial institutions have been forced to diversify their services, increase rates paid on deposits and become more cost effective, as a result of competition with one another and with new types of financial services companies, including non-banking competitors. Some of the results of these market dynamics in the financial services industry have been a number of new bank and non-bank competitors, increased merger activity, and increased customer awareness of product and service differences among competitors. These factors could affect business prospects.

The Company is a one-bank holding company with First Guaranty Bank as its subsidiary.

The Dodd-Frank Act made extensive changes in the regulation of depository institutions. For example, the Dodd-Frank Act creates a new Consumer Financial Protection Bureau as an independent bureau of the Federal Reserve Board. The Consumer Financial Protection Bureau will assume responsibility for the implementation of the federal financial consumer protection and fair lending laws and regulations, a function currently assigned to prudential regulators, and will have authority to impose new requirements. Institutions of less than $10 billion in assets, such as First Guaranty Bank, will continue to be examined for compliance with consumer protection and fair lending laws and regulations by, and be subject to the primary enforcement authority of, their federal prudential regulator rather than the Consumer Financial Protection Bureau.

In addition to creating the Consumer Financial Protection Bureau, the Dodd-Frank Act, among other things, directs changes in the way that institutions are assessed for deposit insurance, requires more stringent consolidated capital requirements for bank holding companies, requires originators of securitized loans to retain a percentage of the risk for the transferred loans, establishes regulatory rate-setting for certain debit card interchange fees, repeals restrictions on the payment of interest on commercial demand deposits, contains a number of reforms related to mortgage originations and requires public companies to give stockholders a non-binding vote on executive compensation and golden parachutes. Many of the provisions of the Dodd-Frank Act are subject to delayed effective dates and/or require the issuance of implementing regulations. Their impact on operations can not yet be fully assessed. However, there is significant possibility that the Dodd-Frank Act will, at a minimum, result in increased regulatory burden, compliance costs and interest expense for First Guaranty Bank.

General.

First Guaranty Bancshares, Inc. is a bank holding company registered with, and subject to regulation by, the FRB under the Bank Holding Company Act of 1956, as amended (the “Bank Holding Company Act”). The Bank Holding Company Act and other federal laws subject bank holding companies to particular restrictions on the types of activities in which they may engage, and to a range of supervisory requirements and activities, including regulatory enforcement actions for violations of laws and regulations. In accordance with FRB policy, a bank holding company, such as First Guaranty Bancshares, Inc., is expected to act as a source of financial strength to its subsidiary banks and commit resources to support its banks. This support may be required under circumstances when we might not be inclined to do so absent this FRB policy.

Dividends.

The Federal Reserve Bank has stated that generally, a bank holding company, should not maintain a rate of distributions to shareholders unless its available net income has been sufficient to fully fund the distributions, and the prospective rate of earnings retention appears consistent with the bank holding company’s capital needs, asset quality and overall financial condition. As a Louisiana corporation, the Company is restricted under the Louisiana corporate law from paying dividends under certain conditions. See Note 16 to the Consolidated Financial Statements for more information on dividend restrictions.

First Guaranty Bank may not pay dividends or distribute capital assets if it is in default on any assessment due to the FDIC. First Guaranty Bank is also subject to regulations that impose minimum regulatory capital and minimum state law earnings requirements that affect the amount of cash available for distribution. In addition, under the Louisiana Banking Law, dividends may not be paid if it would reduce the unimpaired surplus below 50% of outstanding capital stock in any year. The Bank is restricted under applicable laws in the payment of dividends to an amount equal to current year earnings plus undistributed earnings for the immediately preceding year, unless prior permission is received from the Commissioner of Financial Institutions for the State of Louisiana.

Despite prior approval, the FRB has the authority to require a bank holding company to terminate an activity or terminate control of or liquidate or divest certain subsidiaries or affiliates when the FRB believes the activity or the control of the subsidiary or affiliate constitutes a significant risk to the financial safety, soundness or stability of any of its banking subsidiaries. A bank holding company that qualifies and elects to become a financial holding company is permitted to engage in additional activities that are financial in nature or incidental or complementary to financial activity. The Bank Holding Company Act expressly lists the following activities as financial in nature:

To qualify to become a financial holding company, First Guaranty Bancshares, Inc. and its subsidiary bank must be well-capitalized and well managed and must have a Community Reinvestment Act rating of at least satisfactory. Additionally, First Guaranty Bancshares, Inc. would be required to file an election with the FRB to become a financial holding company and to provide the FRB with 30 days’ written notice prior to engaging in a permitted financial activity. A bank holding company that falls out of compliance with these requirements may be required to cease engaging in some of its activities. First Guaranty Bancshares, Inc. currently has no plans to make a financial holding company election.

Bank holding companies and affiliates are prohibited from tying the provision of services, such as extensions of credit, to other services offered by a holding company or its affiliates.

First Guaranty Bank is a member of the Deposit Insurance Fund, which is administered by the FDIC. Deposit accounts in First Guaranty Bank are insured by the FDIC, previously up to a maximum of $100,000 for each separately insured depositor and $250,000 for self-directed retirement accounts. However, in view of the recent economic crisis, the FDIC temporarily increased the deposit insurance available on all deposit accounts to $250,000. The Dodd-Frank Act made that level of coverage permanent. In addition, the Dodd-Frank Act requires that certain non-interest-bearing transaction accounts maintained with depository institutions be fully insured, regardless of the dollar amount, until December 31, 2012.

The FDIC imposes an assessment for deposit insurance against all depository institutions. That assessment is based on the risk category of each institution, which is derived from examination and supervisory information. The FDIC first establishes an institution's initial base assessment rate based upon the risk category, with less risky institution paying lower rates. That initial base assessment rate ranged, from 12 to 45 basis points, depending upon the risk category of the institution. The initial base assessment was then adjusted (higher or lower) to obtain the total base assessment rate. The adjustments to the initial base assessment rate were generally based upon an institution's levels of unsecured debt, secured liabilities and brokered deposits. The total base assessment rate, as adjusted, ranges from 7 to 77.5 basis points of the institution's assessable deposits. The FDIC may adjust the scale uniformly, except that no adjustment may deviate more than three basis points from the base scale without notice and comment.

On May 22, 2009, the FDIC issued a final rule that imposed a special five basis point assessment on each FDIC-insured depository institution's assets minus its Tier 1 capital, on June 30, 2009, which was collected on September 30, 2009. The special assessment was capped at 10 basis points of an institution's domestic deposits. Subsequently the FDIC adopted a rule pursuant to which all insured depository institutions were required to prepay their estimated assessments for the fourth quarter of 2009, and for all of 2010, 2011 and 2012. That pre-payment, which was due on December 30, 2009, amounted to approximately $4.5 million for the Bank. The amount of prepayment was determined based on certain assumptions, including an annual 5% growth rate in the assessment base through the end of 2012. The pre-payment was recorded as a prepaid asset at December 31, 2009 and is being amortized to expense over three years.

In addition, the Dodd-Frank Act required the FDIC to revise its risk-based assessment schedule and procedures to base the assessment on each institution’s average total assets less tangible capital, rather than deposits. The FDIC has implemented that directive effective April 1, 2011. In so doing, the FDIC revised is assessment schedule so that it now ranges from 2.5 basis points for the institutions perceived as lest risky to 45 basis points for those perceived as riskiest.

The Federal Deposit Insurance Corporation has authority to increase insurance assessments. A significant increase in insurance premiums would likely have an adverse effect on the operating expenses and results of operations of First Guaranty Bank. Management cannot predict what insurance assessment rates will be in the future. Insurance of deposits may be terminated by the Federal Deposit Insurance Corporation upon a finding that an institution has engaged in unsafe or unsound practices, is in an unsafe or unsound condition to continue operations or has violated any applicable law, regulation, rule, order or condition imposed by the Federal Deposit Insurance Corporation. We do not currently know of any practice, condition or violation that may lead to termination of our deposit insurance.

In addition to the Federal Deposit Insurance Corporation assessments, the Financing Corporation (“FICO”) is authorized to impose and collect, with the approval of the Federal Deposit Insurance Corporation, assessments for anticipated payments, issuance costs and custodial fees on bonds issued by the FICO in the 1980s to recapitalize the former Federal Savings and Loan Insurance Corporation. The bonds issued by the FICO are due to mature in 2017 through 2019. For the quarter ended December 31, 2011, the annualized FICO assessment was 0.0165% of the Company's average assets less average equity.

Interest and other charges collected or contracted is subject to state usury laws and federal laws concerning interest rates. Loan operations are also subject to federal laws applicable to credit transactions, such as:

The Company is a legal entity separate and distinct from its subsidiary, First Guaranty Bank. The majority of the Company’s revenue is from dividends paid to the Company by the Bank. First Guaranty Bank may not pay dividends or distribute capital assets if it is in default on any assessment due to the FDIC. The FRB has indicated generally that it may be an unsafe or unsound practice for a bank holding company to pay dividends unless the bank holding company’s net income over the preceding year is sufficient to fund the dividends and the expected rate of earnings retention is consistent with the organization’s capital needs, asset quality and overall financial condition.

First Guaranty Bank is also subject to regulations that impose minimum regulatory capital and minimum state law earnings requirements that affect the amount of cash available for distribution. In addition, under the Louisiana Banking Law, dividends may not be paid if it would reduce the unimpaired surplus below 50% of outstanding capital stock in any year. If the Bank does not comply with these laws, regulations or policies it may materially affect the ability of the Company to pay dividends on its common stock.

The FRB monitors the capital adequacy of bank holding companies, such as First Guaranty Bancshares, Inc., and the OFI and FDIC monitor the capital adequacy of First Guaranty Bank. The federal bank regulators use a combination of risk-based guidelines and leverage ratios to evaluate capital adequacy and consider these capital levels when taking action on various types of applications and when conducting supervisory activities related to safety and soundness. The risk-based guidelines apply on a consolidated basis to bank holding companies with consolidated assets of $500 million or more and, generally, on a bank-only basis for bank holding companies with less than $500 million in consolidated assets. Each insured depository subsidiary of a bank holding company with less than $500 million in consolidated assets is expected to be “well-capitalized.”

The minimum guideline for the ratio of total capital to risk-weighted assets is 8%. Total capital consists of two components, Tier 1 Capital and Tier 2 Capital. Tier 1 Capital generally consists of common stock, minority interests in the equity accounts of consolidated subsidiaries, noncumulative perpetual preferred stock and a limited amount of qualifying cumulative perpetual preferred stock, less goodwill and other specified intangible assets. Tier 1 Capital must equal at least 4% of risk-weighted assets. Tier 2 Capital generally consists of subordinated debt, preferred stock (other than that which is included in Tier I Capital), and a limited amount of loan loss reserves. The total amount of Tier 2 Capital is limited to 100% of Tier 1 Capital.

The Dodd-Frank Act requires the Federal Reserve Board to issue consolidated regulatory capital requirements for bank holding companies that are at least as stringent as those applicable to insured depository institutions. Such regulations, when issued, will eliminate the use of certain instruments, such as cumulative preferred stock and trust preferred securities, from Tier 1 holding company capital. Instruments issued by May 19, 2010 by bank holding companies with consolidated assets of less than $15 billion (as of December 31, 2009) are grandfathered.

Failure to meet capital guidelines could subject a bank or bank holding company to a variety of enforcement remedies, including issuance of a capital directive, the termination of federal deposit insurance, a prohibition on accepting brokered deposits and other restrictions on its business.

The FRB and FDIC have promulgated guidance governing financial institutions with concentrations in commercial real estate lending. The guidance provides that a company has a concentration in commercial real estate lending if (i) total reported loans for construction, land development, and other land represent 100% or more of total capital or (ii) total reported loans secured by multifamily and non-farm residential properties and loans for construction, land development, and other land represent 300% or more of total capital and the outstanding balance of such loans has increased 50% or more during the prior 36 months. If a concentration is present, Management must employ heightened risk Management practices including board and Management oversight and strategic planning, development of underwriting standards, risk assessment and monitoring through market analysis and stress testing, and increasing capital requirements. The Company is subject to these regulations.

Under the prompt corrective action regulations, bank regulators are required and authorized to take supervisory actions against undercapitalized banks. For this purpose, a bank is placed in one of the following five categories based on its capital:

Federal banking regulators are required to take various mandatory supervisory actions and are authorized to take other discretionary actions with respect to institutions in the three undercapitalized categories. The severity of the action depends upon the capital category in which the institution is placed. Generally, subject to a narrow exception, banking regulators must appoint a receiver or conservator for an institution that is “critically undercapitalized.” The federal banking agencies have specified by regulation the relevant capital level for each category. An institution that is categorized as “undercapitalized”, “significantly undercapitalized” or “critically undercapitalized” is required to submit an acceptable capital restoration plan to its appropriate federal banking agency. A bank holding company must guarantee that a subsidiary depository institution meets its capital restoration plan, subject to various limitations. The controlling holding company’s obligation to fund a capital restoration plan is limited to the lesser of 5% of an “undercapitalized” subsidiary’s assets at the time it became “undercapitalized” or the amount required to meet regulatory capital requirements. An “undercapitalized” institution is also generally prohibited from increasing its average total assets, making acquisitions, establishing any branches or engaging in any new line of business, except under an accepted capital restoration plan or with regulatory approval. The regulations also establish procedures for downgrading an institution to a lower capital category based on supervisory factors other than capital.

The total amount of the above transactions is limited in amount, as to any one affiliate, to 10% of First Guaranty Bank’s capital and surplus and, as to all affiliates combined, to 20% of its capital and surplus. In addition to the limitation on the amount of these transactions, each of the above transactions must also meet specified collateral requirements. First Guaranty Bank is also subject to the provisions of Section 23B of the FRB Act and its implementing regulations, which, among other things, prohibit First Guaranty Bank from engaging in any transaction with an affiliate, such as First Guaranty Bancshares, Inc., unless the transaction is on terms substantially the same, or at least as favorable to First Guaranty Bank as those prevailing at the time for comparable transactions with nonaffiliated companies. First Guaranty Bank is also subject to restrictions on extensions of credit to its executive officers, directors, principal shareholders and their related interests. These types of extensions of credit must be made on substantially the same terms, including interest rates and collateral, as those prevailing at the time for comparable transactions with third parties and must not involve more than the normal risk of repayment or present other unfavorable features.

Financial institutions are required to establish anti-money laundering programs. In 2001, the USA PATRIOT Act was enacted. The USA PATRIOT Act significantly enhanced the powers of the federal government and law enforcement organizations to combat terrorism, organized crime and money laundering. While the USA PATRIOT Act imposed additional anti-money laundering requirements, these additional requirements are not material to our operations. Aside from the above, the USA PATRIOT Act also requires the federal banking regulators to assess the effectiveness of an institution’s anti-money laundering program in connection with merger and acquisition transactions. Failure to maintain an effective anti-money laundering program is grounds for the denial of merger or acquisition transactions.

First Guaranty Bancshares, Inc. common stock is registered with the Securities and Exchange Commission under the Securities Exchange Act of 1934. First Guaranty Bancshares, Inc. will continue to be subject to the information, proxy solicitation, insider trading restrictions and other requirements under the Securities Exchange Act of 1934.

Effective June 1, 1997, the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 permits state and national banks with different home states to operate branches across state lines with approval of the appropriate federal banking agency, unless the home state of a participating bank passed legislation “opting out” of interstate banking. The Dodd-Frank Act amended federal law to allow banks to branch de novo into another state if that state allows banks chartered by it to establish branches within its borders. First Guaranty Bank currently has no branches outside of Louisiana.

Under the Community Reinvestment Act, or CRA, a financial institution has a continuing and affirmative obligation, consistent with its safe and sound operation, to help meet the credit needs of its entire community, including low and moderate income neighborhoods. The FDIC assigns banks a CRA rating of “outstanding,” “satisfactory,” “needs to improve” or “substantial noncompliance,” and the bank must publicly disclose its rating. The FDIC rated the Bank as “satisfactory” in meeting community credit needs under the CRA at its most recent CRA performance examination.

Under the Gramm-Leach-Bliley Act, federal banking regulators have adopted new rules requiring disclosure of privacy policies and information sharing practices to consumers. These rules prohibit depository institutions from sharing customer information with nonaffiliated parties without the customer’s consent, except in limited situations, and require disclosure of privacy policies to consumers and, in some circumstances, enable consumers to prevent disclosure of personal information to nonaffiliated third parties. In addition, the Fair and Accurate Credit Transactions Act of 2003 requires banks to notify their customers if they report negative information about them to a credit bureau or if they grant credit to them on terms less favorable than those generally available. The Company has instituted risk Management systems to comply with all required privacy provisions and believes that the new disclosure requirements and implementation of the privacy laws will not materially increase operating expenses.

The Check 21 Act facilitates check truncation and electronic check exchange by authorizing a new negotiable instrument called a “substitute check”. The Act provides that a properly prepared substitute check is the legal equivalent of the original check for all purposes. This law supercedes contradictory state laws (i.e., state laws that allow customers to demand the return of original checks). Although the Check 21 Act does not require any bank to create substitute checks or to accept checks electronically, it does require banks to accept a legally equivalent substitute check in place of an original check after the Check 21 Act’s effective date of October 28, 2004.

The Company is also subject to the Sarbanes-Oxley Act of 2002, which has imposed corporate governance and accounting oversight restrictions and responsibilities on the board of directors, executive officers and independent auditors. The law has increased the time spent discharging responsibilities and costs for audit services. Beginning in 2007, Management was required to report on the effectiveness of internal controls and procedures. The Company is a smaller reporting company and is not required to get an attestation report from our external auditor on the effectiveness of our internal controls over financial reporting until our public float exceeds $75 million.

The difference between the interest rate paid on deposits and other borrowings and the interest rate received on loans and securities comprise most of a bank’s earnings. In order to mitigate the interest rate risk inherent in the industry, the banking business is becoming increasingly dependent on the generation of fee and service charge revenue. The earnings and growth of a bank will be affected by both general economic conditions and the monetary and fiscal policy of the United States Government and its agencies, particularly the Federal Reserve. The Federal Reserve sets national monetary policy such as seeking to curb inflation and combat recession. This is accomplished by its open-market operations in United States government securities, adjustments to the discount rates on borrowings and target rates for federal funds transactions. The actions of the Federal Reserve in these areas influence the growth of bank loans, investments and deposits and also affect interest rates on loans and deposits. The nature and timing of any future changes in monetary policies and their potential impact on the Company cannot be predicted. Our noninterest income and expenses can be affected by increasing rates of inflation; however, unlike most industrial companies, the assets and liabilities of financial institutions such as the Banks are primarily monetary in nature. Interest rates, therefore, have a more significant impact on the Bank’s performance than the effect of general levels of inflation on the price of goods and services.

Under the TARP, the United States Department of the Treasury authorized a voluntary capital purchase program (the “CPP”) to purchase up to $250 billion of senior preferred shares of qualifying financial institutions that elected to participate. Participating companies must adopt certain standards for executive compensation, including (a) prohibiting “golden parachute” payments as defined in the EESA to senior Executive Officers; (b) requiring recovery of any compensation paid to senior Executive Officers based on criteria that is later proven to be materially inaccurate; and (c) prohibiting incentive compensation that encourages unnecessary and excessive risks that threaten the value of the financial institution. The terms of the CPP also limit certain uses of capital by the issuer, including repurchases of company stock and increases in dividends.

On August 28, 2009, the Company entered into a Letter Agreement, which includes a Securities Purchase Agreement and a Side Letter Agreement (together, the “Purchase Agreement”), with the United States Department of the Treasury (“Treasury Department”) pursuant to which the Company issued and sold to the Treasury Department 2,069.9 shares of the Company’s Fixed Rate Cumulative Perpetual Preferred Stock, Series A, par value $1,000 per share for a total purchase price of $20.7 million. In addition to the issuance of the Series A Stock, as a part of the transaction, the Company issued to the Treasury Department a warrant to purchase 114.44444 shares of the Company’s Fixed Rate Cumulative Preferred Stock, Series B, and immediately following the issuance of the Series A stock, the Treasury Department exercised its rights and acquired 103 of the Series B shares through a cashless exercise. The newly issued Series A Stock, generally non-voting stock, pays cumulative dividends of 5% for five years, and a rate of 9% dividends, per annum, thereafter. The newly issued Series B Stock, generally non-voting, pays cumulative dividends at a rate of 9% per annum. Both the Series A Stock and the Series B Stock were issued in a private placement.

First Guaranty Bancshares, Inc. and First Guaranty Bank have chosen to participate in the FDIC’s Temporary Liquidity Guarantee Program (the “TLGP”), which applies to, among other, all U.S. depository institutions insured by the FDIC and all United States bank holding companies, unless they have opted out. Under the TLPG, the FDIC guarantees certain senior unsecured debt of the holding company and bank, as well as non-interest bearing transaction account deposits at First Guaranty Bank. Under the debt guarantee component of the TLGP, the FDIC will pay the unpaid principal and interest on an FDIC-guaranteed debt instrument upon the uncured failure of the participating entity to make a timely payment of principal or interest. Neither First Guaranty Bancshares, Inc. nor First Guaranty Bank issued debt under the TLGP.

Under the transaction account guarantee component of the TLGP, all non-interest bearing transaction accounts maintained at First Guaranty Bank are insured in full by the FDIC until June 30, 2010, later extended to December 31, 2010, regardless of the standard maximum deposit insurance amounts. An annualized 10 basis point assessment on balances in noninterest-bearing transaction accounts that exceed the existing deposit insurance limit of $250,000 was assessed on a quarterly basis to insured depository institutions participating in this component of the TLGP. The Company chose to participate in this component of the TLGP. The Dodd-Frank Act extended unlimited coverage for certain non-interest bearing transaction accounts through December 31, 2012. The cost associated with that coverage will be part of the usual FDIC assessment.

American Recovery and Reinvestment Act of 2009.

On February 17, 2009, the American Recovery and Reinvestment Act of 2009 (the “ARRA”) was enacted. The ARRA is intended to provide a stimulus to the U.S. economy in the wake of the economic downturn brought about by the subprime mortgage crisis and the resulting credit crunch. The bill includes federal tax cuts, expansion of unemployment benefits and other social welfare provisions, and domestic spending in education, healthcare, and infrastructure, including the energy structure. The new law also includes numerous non-economic recovery related items, including a limitation on executive compensation in federally aided banks. Under the ARRA, an institution will be subject to the following restrictions and standards through out the period in which any obligation arising from financial assistance provided under the TARP remains outstanding:

The foregoing is a summary of requirements to be included in standards to be established by the Secretary of the Treasury. The chief executive officer and chief financial officer of each TARP recipient will be required to provide a written certification of compliance with these standards to the SEC. The foregoing is a summary of requirements to be included in standards to be established by the Secretary of the Treasury.

(references to “our,” “we” or similar terms under this subheading refer to First Guaranty Bancshares, Inc.)

We may be vulnerable to certain sectors of the economy.

Difficult market conditions have adversely affected the industry in which we operate.

None.

The Company is subject to various legal proceedings in the normal course of its business. It is Management’s belief that the ultimate resolution of such claims will not have a material adverse effect on the financial position or results of operations. At December 31, 2011, we were not involved in any material legal proceedings.

The following table sets forth the high and low bid quotations for First Guaranty Bancshares, Inc.’s common stock for the periods indicated. These quotations represent trades of which we are aware and do not include retail markups, markdowns, or commissions and do not necessarily reflect actual transactions. As of December 31, 2011, there were 6,294,227 shares of First Guaranty Bancshares, Inc. common stock issued and outstanding with a total of 1,407 shareholders of record.

Our stockholders are entitled to receive dividends when, and if declared by the Board of Directors, out of funds legally available for dividends. We have paid consecutive quarterly cash dividends on our common stock for each of the last 74 quarters dating back to the third quarter of 1993. The Board of Directors intends to continue to pay regular quarterly cash dividends. The ability to pay dividends in the future will depend on earnings and financial condition, liquidity and capital requirements, regulatory restrictions, the general economic and regulatory climate and ability to service any equity or debt obligations senior to common stock. There are legal restrictions on the ability of First Guaranty Bank to pay cash dividends to First Guaranty Bancshares, Inc. Under federal and state law, we are required to maintain certain surplus and capital levels and may not distribute dividends in cash or in kind, if after such distribution we would fall below such levels. Specifically, an insured depository institution is prohibited from making any capital distribution to its shareholders, including by way of dividend, if after making such distribution, the depository institution fails to meet the required minimum level for any relevant capital measure including the risk-based capital adequacy and leverage standards.

Additionally, under the Louisiana Business Corporation Act, First Guaranty Bancshares, Inc. is prohibited from paying any cash dividends to shareholders if, after the payment of such dividend, its total assets would be less than its total liabilities or where net assets are less than the liquidation value of shares that have a preferential right to participate in First Guaranty Bancshares, Inc.’s assets in the event First Guaranty Bancshares, Inc. were to be liquidated.

We have not repurchased any shares of our outstanding common stock during 2011.

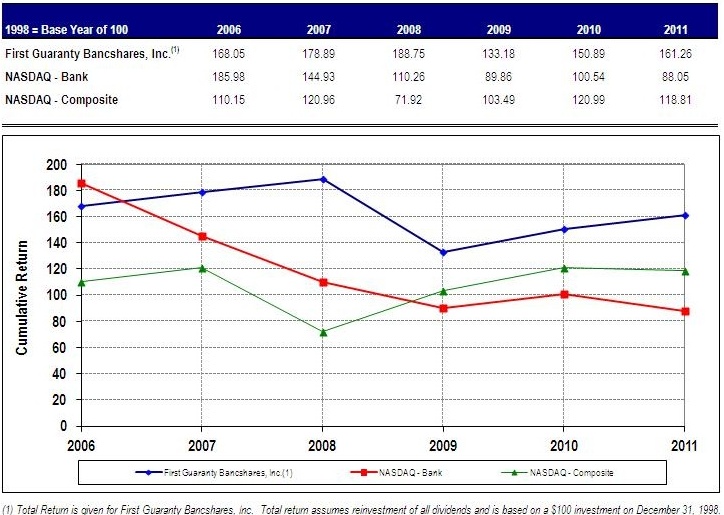

The line graph below compares the cumulative total return for the Company’s common stock with the cumulative total return of both the NASDAQ Stock Market Index for U.S. companies and the NASDAQ Index for bank stocks for the period December 31, 2006 through December 31, 2011. The total return assumes the reinvestment of all dividends and is based on a $100 investment on December 31, 1998. It also reflects the stock price on December 31st of each year shown, although this price reflects only a small number of transactions involving a small number of directors of the Company or affiliates or associates and cannot be taken as an accurate indicator of the market value of the Company’s common stock.

The following selected financial data should be read in conjunction with the financial statements, including the related notes, and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” which are included elsewhere in this Form 10-K. Except for the data under “Performance Ratios,” “Capital Ratios” and “Asset Quality Ratios,” the income statement data and share and per share data for the years ended December 31, 2011, 2010 and 2009 and the balance sheet data as of December 31, 2011 and 2010 are derived from the audited financial statements and related notes which are included elsewhere in this Form 10-K, and the income statement data and share and per share data for the years ended December 31, 2008 and 2007 and the balance sheet data as of December 31, 2009, 2008 and 2007 are derived from the audited financial statements and related notes that are not included in this Form 10-K.

Assets.

Total assets at December 31, 2011 were $1.4 billion, an increase of $221.1 million, or 19.5%, from $1.1 billion at December 31, 2010. Federal funds sold increased $59.5 million from December 31, 2010 to December 31, 2011 and total loans for the same period decreased $2.5 million. Cash and due from banks increased $8.1 million from 2010 to 2011. Additionally, total investment securities increased $151.2 million to $633.2 million from December 31, 2010 to December 31, 2011. Total deposits increased by $199.9 million or 19.8% from 2010 to 2011. At December 31, 2011, the Company had $3.2 million in long-term borrowings compared to no long-term borrowings at December 31, 2010.

Investment Securities.

The securities portfolio consisted principally of U.S. Government agency securities, corporate debt securities and mutual funds or other equity securities. The securities portfolio provides us with a relatively stable source of income and provides a balance to credit risks as compared to other categories of assets. The securities portfolio totaled $633.2 million at December 31, 2011, representing an increase of $151.2 million from December 31, 2010. The primary changes in the portfolio consisted of $858.7 million in purchases which was partially offset by maturities, calls and sales totaling $718.2 million. At December 31, 2011, approximately 2.1% of the securities portfolio (excluding Federal Home Loan Bank stock) matures in less than one year while securities with maturity dates over 10 years totaled 44.1% of the portfolio. At December 31, 2011, the average maturity of the securities portfolio was 7.8 years, compared to the average maturity at December 31, 2010 of 6.5 years.

At December 31, 2011, securities totaling $520.5 million were classified as available for sale and $112.7 million were classified as held to maturity as compared to $322.1 million and $159.8 million, respectively at December 31, 2010. Securities classified as available for sale are measured at fair market value. For these securities, the Company obtains fair value measurements from an independent pricing service. The fair value measurements consider observable data that may include dealer quotes, market spreads, cash flows, market yield curves, prepayment speeds, credit information and the instrument’s contractual terms and conditions, among other things. Securities classified as held to maturity are measured at book value. The held to maturity portfolio is principally used to collateralize public funds deposits. The Company believes that it has the ability to maintain the current level of securities in the portfolio. The Company has maintained public funds in excess of $175.0 million since 2007. The book yields on securities available for sale ranged from 0.2% to 9.6% at December 31, 2011, exclusive of the effect of changes in fair value reflected as a component of stockholders’ equity. The book yields on held to maturity securities ranged from 1.0% to 4.0%. See Note 5 to the Consolidated Financial Statements for additional information.

Securities classified as available for sale had gross unrealized losses totaling $1.6 million at December 31, 2011. The gross unrealized gains for our available for sale securities totaled $8.3 million at December 31, 2011 compared to $5.1 million for the same period in 2010. The Company believes that it will collect all amounts contractually due and has the intent and the ability to hold these securities until the fair value is at least equal to the carrying value. At December 31, 2010, securities classified as available for sale had gross unrealized losses totaling $5.5 million. See Note 5 to the Consolidated Financial Statements for additional information.

Average securities as a percentage of average interest-earning assets were 46.7% and 35.5% at December 31, 2011 and 2010, respectively. At December 31, 2011 and 2010, $428.6 million and $290.0 million in securities were pledged, respectively.

The origination of loans is a primary use of our financial resources and represented 48.9% of average earning assets for 2011. At December 31, 2011, the loan portfolio (loans, net of unearned income) totaled $573.1 million, a decrease of approximately $2.5 million, or 0.4%, from the December 31, 2010 level of $575.6 million. The decrease in net loans primarily includes a reduction of $8.6 million in commercial and industrial loans, a reduction of $24.2 million in non-farm non-residential loans secured by real estate, partially offset by an increase of $13.0 million in construction and land development loans and an increase of $16.0 million in one to four family loans. Loans represented 47.5% of deposits at December 31, 2011, compared to 57.1% of deposits at December 31, 2010. Loans secured by real estate increased $5.5 million to $464.9 million at December 31, 2011. Non-real estate loans decreased $8.1 million to $108.8 million at December 31, 2011. Real estate and related loans comprised 81.0% of the portfolio in 2011 as compared to 79.7% in 2010. Non-real estate loans comprised 19.0% of the portfolio in 2011 as compared to 20.3% in 2010. Loan charge-offs taken during 2011 totaled $10.4 million, compared to charge-offs of $5.6 million in 2010. Of the loan charge-offs in 2011, approximately $8.0 million were loans secured by real estate, $1.7 million were commercial and industrial loans and $0.7 million were consumer and other loans. In 2011, recoveries of $0.7 million were recognized on loans previously charged off as compared to $0.4 million in 2010.

Non-performing Assets.

Nonperforming assets were $28.9 million, or 2.1% of total assets at December 31, 2011, compared to $31.0 million, or 2.7% of total assets at December 31, 2010. The decrease resulted from a $6.3 million decrease in non-accrual loans which was partially offset by an increase in other real estate. The decrease in nonaccrual loans was primarily in construction and land development, multifamily, and non-farm non-residential loans. These decreases reflect the strategy of Management to combat non-performing assets and strengthen the Company's balance sheet.

Deposits.

Total deposits increased by $199.9 million or 19.8%, to $1.2 billion at December 31, 2011 from $1.0 billion at December 31, 2010. In 2011, noninterest-bearing demand deposits increased $37.0 million, interest-bearing demand deposits increased $97.3 million and savings deposits increased $10.8 million. Time deposits increased $54.8 million, or 8.6%. The increase in deposits was principally due to an increase of $75.8 million in public funds deposits. Public fund deposits totaled $431.9 million or 35.8% of total deposits at December 31, 2011. Seven public entities comprised $371.8 million or 86.1% of the total public funds as of December 31, 2011. At December 31, 2010, public fund deposits represented 35.4% of total deposits with a balance of $356.2 million.

Borrowings.

Short-term borrowings decreased $0.4 million in 2011 to $12.2 million at December 31, 2011 from $12.6 million at December 31, 2010. Short-term borrowings are used to manage liquidity on a daily or otherwise short-term basis. The short-term borrowings at December 31, 2011 and 2010, respectively was solely comprised of repurchase agreements. Overnight repurchase agreement balances are monitored daily for sufficient collateralization. Long-term borrowings increased to $3.2 million in 2011. Long-term borrowings consisted of a $3.5 million term loan to the Company originally obtained for the purpose of the Greensburg acquisition. There were no long-term borrowings in 2010. See Note 12 of the Consolidated Financial Statements for additional information.

Stockholders’ Equity.

Total stockholders’ equity increased $28.7 million or 29.3% to $126.6 million at December 31, 2011 from $97.9 million at December 31, 2010. The increase in stockholders’ equity is attributable to the $8.0 million in consolidated earnings, $39.4 million in capital received from the issuance of preferred stock under the U.S. Department of Treasury Small Business Lending Fund Program, $3.0 million in common stock issued for the acquisition of Greensburg Bancshares and $4.7 million change in accumulated other comprehensive income. The increases were partially offset by $3.6 million in dividends on common stock, $1.8 million in dividends on preferred stock, and $21.1 million in redemption of preferred stock issued under the U.S. Department of Treasury Capital Purchase Program.

Loan Portfolio Composition.

The following table sets forth the composition of our loan portfolio, excluding loans held for sale, by type of loan at the dates indicated.

| | December 31, 2011 | | December 31, 2010 | |

| (in thousands except for %) | Balance | | As % of Category | | Balance | | | |

| Real Estate: | | | | | | | | |

| Construction & land development | $ | 78,614 | | 13.7 | % | $ | 65,570 | | 11.4 | % |

| Farmland | | 11,577 | | 2.0 | % | | 13,337 | | 2.3 | % |

| 1- 4 Family | | 89,202 | | 15.6 | % | | 73,158 | | 12.7 | % |

| Multifamily | | 16,914 | | 2.9 | % | | 14,544 | | 2.5 | % |

| Non-farm non-residential | | 268,618 | | 46.8 | % | | 292,809 | | 50.8 | % |

| Total Real Estate | $ | 464,925 | | 81.0 | % | $ | 459,418 | | 79.7 | % |

| Non-real Estate: | | | | | | | | | | |

| Agricultural | $ | 17,338 | | 3.0 | % | $ | 17,361 | | 3.0 | % |

| Commercial and industrial | | 68,025 | | 11.9 | % | | 76,590 | | 13.3 | % |

| Consumer and other | | 23,455 | | 4.1 | % | | 22,970 | | 4.0 | % |

| Total Non-real Estate | $ | 108,818 | | 19.0 | % | $ | 116,921 | | 20.3 | % |

Total loans before unearned income | $ | 573,743 | | 100.0 | % | $ | 576,339 | | 100.0 | % |

| Less: Unearned income | | (643 | ) | | | | (699 | ) | | |

Total loans net of unearned income | $ | 573,100 | | | | $ | 575,640 | | | |

| | December 31, 2009 | | December 31, 2008 | | December 31, 2007 | |

| (in thousands except for %) | Balance | | As % of Category | | Balance | | | | Balance | | As % of Category | |

| Real Estate: | | | | | | | | | | | | | |

| Construction & land development | $ | 78,686 | | 13.3 | % | $ | 92,029 | | 15.2 | % | $ | 98,127 | | 17.0 | % |

| Farmland | | 11,352 | | 1.9 | % | | 16,403 | | 2.7 | % | | 23,065 | | 4.0 | % |

| 1- 4 Family | | 77,470 | | 13.1 | % | | 79,285 | | 13.1 | % | | 84,640 | | 14.7 | % |

| Multifamily | | 8,927 | | 1.5 | % | | 15,707 | | 2.6 | % | | 13,061 | | 2.3 | % |

| Non-farm non-residential | | 300,673 | | 51.0 | % | | 261,744 | | 43.0 | % | | 236,474 | | 41.1 | % |

| Total Real Estate | $ | 477,108 | | 80.8 | % | $ | 465,168 | | 76.6 | % | $ | 455,367 | | 79.1 | % |

| Non-real Estate: | | | | | | | | | | | | | | | |

| Agricultural | $ | 14,017 | | 2.4 | % | $ | 18,536 | | 3.0 | % | $ | 16,816 | | 2.9 | % |

| Commercial and industrial | | 82,348 | | 13.9 | % | | 105,555 | | 17.4 | % | | 81,073 | | 14.1 | % |

| Consumer and other | | 17,226 | | 2.9 | % | | 17,926 | | 3.0 | % | | 22,517 | | 3.9 | % |

| Total Non-real Estate | $ | 113,591 | | 19.2 | % | $ | 142,017 | | 23.4 | % | $ | 120,406 | | 20.9 | % |

Total loans before unearned income | $ | 590,699 | | 100.0 | % | $ | 607,185 | | 100.0 | % | $ | 575,773 | | 100.0 | % |

| Less: Unearned income | | (797 | ) | | | | (816 | ) | | | | (517 | ) | | |

Total loans net of unearned income | $ | 589,902 | | | | $ | 606,369 | | | | $ | 575,256 | | | |

The four most significant categories of our loan portfolio are construction and land development real estate loans, 1-4 family residential loans, non-farm non-residential real estate loans and commercial and industrial loans. The Company’s credit policy dictates specific loan-to-value and debt service coverage requirements. The Company generally requires a maximum loan-to-value of 85.0% and a debt service coverage ratio of 1.25x to 1.0x for non-farm non-residential real estate loans. In addition, personal guarantees of borrowers are required as well as applicable hazard, title and flood insurance. Loans may have a maximum maturity of five years and a maximum amortization of 25 years. The Company may require additional real estate or non-real estate collateral when deemed appropriate to secure the loan.

The Company generally requires all 1-4 family residential loans to be underwritten based on the Fannie Mae guidelines provided through Desktop Underwriter. These guidelines include the evaluation of risk and eligibility, verification and approval of conditions, credit and liabilities, employment and income, assets, property and appraisal information. It is required that all borrowers have proper hazard, flood and title insurance prior to a loan closing. Appraisals and Desktop Underwriter approvals are good for six months. The Company has an in-house underwriter review the final package for compliance to these guidelines.

The Company generally requires a maximum loan-to value of 80.0% and a debt service coverage ratio of 1.25x to 1.0x for construction land development loans. In addition, detailed construction cost breakdowns, personal guarantees of borrowers and applicable hazard, title and flood insurance are required. Loans may have a maximum maturity of 24 months for the construction phase and a maximum maturity of 24 months for land development or 60 months for commercial construction. The Company may require additional real estate or non-real estate collateral when deemed appropriate to secure the loan.

The Company has specific guidelines for the underwriting of commercial and industrial loans that is specific for the collateral type and the business type. Commercial and industrial loans are secured by non-real estate collateral such as equipment, inventory, accounts receivable, or may be unsecured. Each of these collateral types has maximum loan to value ratios. Commercial and industrial loans have the same debt service coverage ratio requirements as other loans, which is 1.25x to 1.0x.

The Company will allow exceptions to each of the above policies with appropriate mitigating circumstances and approvals. The Company has a defined credit underwriting process for all loan requests. The Company actively monitors loan concentrations by industry type and will make adjustments to underwriting standards as deemed necessary. The Company has a loan review department that monitors the performance and credit quality of loans. The Company has a special assets department that manages loans that have become delinquent or have serious credit issues associated with them.

For new loan originations, appraisals and evaluations on all properties shall be valid for a period not to exceed two calendar years from the effective appraisal date for non-residential properties and one calendar year from the effective appraisal date for residential properties. However, an appraisal may be valid longer if there has been no material decline in the property condition or market condition that would negatively affect the bank’s collateral position. This must be supported with a “Validity Check Memorandum”.

For renewals, any commercial appraisal greater than two years or greater than one year for residential appraisals must be updated with a Validity Check Memorandum. Any renewal loan request, in which new money will be disbursed, whether commercial or residential, and the appraisal is older than five years a new appraisal must be obtained. The Company does not require new appraisals between renewals unless the loan becomes impaired and is considered collateral dependent. At this time, an appraisal may be ordered in accordance with the Company’s Allowance for Loan Losses policy. The Company does not mitigate risk using products such as credit default agreements and/or credit derivatives. These, accordingly, have no impact on our financial statements. The Company does not offer loan products with established loan-funded interest reserves.

The following table summarizes the scheduled repayments of our loan portfolio including non-accruals at December 31, 2011. Loans having no stated repayment schedule or maturity and overdraft loans are reported as being due in one year or less. Maturities are based on the final contractual payment date and do not reflect the effect of prepayments and scheduled principal amortization.

| | December 31, 2011 | |

| (in thousands) | One Year or Less | | One Through Five Years | | After Five Years | | Total | |

| Real Estate: | | | | | | | | | | | | |

| Construction & land development | $ | 46,005 | | $ | 23,357 | | $ | 9,252 | | $ | 78,614 | |

| Farmland | | 4,608 | | | 4,688 | | | 2,281 | | | 11,577 | |

| 1 - 4 family | | 27,473 | | | 35,931 | | | 25,798 | | | 89,202 | |

| Multifamily | | 11,603 | | | 4,032 | | | 1,279 | | | 16,914 | |

| Non-farm non-residential | | 107,697 | | | 149,898 | | | 11,023 | | | 268,618 | |

| Total Real Estate | $ | 197,386 | | $ | 217,906 | | $ | 49,633 | | $ | 464,925 | |

| Non-real Estate: | | | | | | | | | | | | |

| Agricultural | $ | 6,804 | | $ | 3,015 | | $ | 7,519 | | $ | 17,338 | |

| Commercial and industrial | | 39,604 | | | 25,147 | | | 3,274 | | | 68,025 | |

| Consumer and other | | 10,226 | | | 13,196 | | | 33 | | | 23,455 | |

| Total Non-Real Estate | $ | 56,634 | | $ | 41,358 | | $ | 10,826 | | $ | 108,818 | |

Total loans before unearned income | $ | 254,020 | | $ | 259,264 | | $ | 60,459 | | $ | 573,743 | |

| Less: unearned income | | | | | | | | | | | (643 | ) |

| Total loans net of unearned income | | | | | | | | | | $ | 573,100 | |

| | December 31, 2010 | |

| (in thousands) | One Year or Less | | One Through Five Years | | After Five Years | | Total | |

| Real Estate: | | | | | | | | | | | | |

| Construction & land development | $ | 50,377 | | $ | 11,979 | | $ | 3,214 | | $ | 65,570 | |

| Farmland | | 6,647 | | | 3,863 | | | 2,827 | | | 13,337 | |

| 1 - 4 family | | 19,745 | | | 24,098 | | | 29,315 | | | 73,158 | |

| Multifamily | | 7,815 | | | 5,426 | | | 1,303 | | | 14,544 | |

| Non-farm non-residential | | 114,034 | | | 172,283 | | | 6,492 | | | 292,809 | |

| Total Real Estate | $ | 198,618 | | $ | 217,649 | | $ | 43,151 | | $ | 459,418 | |

| Non-real Estate: | | | | | | | | | | | | |

| Agricultural | $ | 7,080 | | $ | 3,414 | | $ | 6,867 | | $ | 17,361 | |

| Commercial and industrial | | 46,185 | | | 23,869 | | | 6,536 | | | 76,590 | |

| Consumer and other | | 7,767 | | | 15,054 | | | 149 | | | 22,970 | |

| Total Non-Real Estate | $ | 61,032 | | $ | 42,337 | | $ | 13,552 | | $ | 116,921 | |

Total loans before unearned income | $ | 259,650 | | $ | 259,986 | | $ | 56,703 | | $ | 576,339 | |

| Less: unearned income | | | | | | | | | | | (699 | ) |

| Total loans net of unearned income | | | | | | | | | | $ | 575,640 | |

The following table sets forth the scheduled contractual maturities at December 31, 2011 and December 31, 2010 of fixed- and floating-rate loans excluding non-accrual loans.

| | December 31, 2011 | | December 31, 2010 | |

| (in thousands) | Fixed | | Floating | | Total | | Fixed | | Floating | | Total | |

| One year or less | $ | 108,276 | | $ | 124,052 | | $ | 232,328 | | $ | 67,944 | | $ | 167,399 | | $ | 235,343 | |

| One to five years | | 160,191 | | | 98,972 | | | 259,163 | | | 127,401 | | | 132,345 | | | 259,746 | |

| Five to 15 years | | 8,393 | | | 36,891 | | | 45,284 | | | 2,456 | | | 30,953 | | | 33,409 | |

| Over 15 years | | 8,464 | | | 6,054 | | | 14,518 | | | 9,735 | | | 9,388 | | | 19,123 | |

| Subtotal | $ | 285,324 | | $ | 265,969 | | $ | 551,293 | | $ | 207,536 | | $ | 340,085 | | $ | 547,621 | |

| Nonaccrual loans | | | | | | | | 22,450 | | | | | | | | | 28,718 | |

Total loans before unearned income | | | | | | | $ | 573,743 | | | | | | | | $ | 576,339 | |

| Less: Unearned income | | | | | | | | (643 | ) | | | | | | | | (699 | ) |

Total loans net of unearned income | | | | | | | $ | 573,100 | | | | | | | | $ | 575,640 | |

At December 31, 2011, fixed rate loans totaled $285.3 million or 51.8% of total loans excluding non-accrual loans and variable rate loans totaled $266.0 or 48.2% of total loans excluding non-accrual loans. Throughout 2011, Management added floors to floating rate loans, primarily tied to the prime rate. As of December 31, 2011, the portfolio consisted of $266.0 million in variable rate loans with $257.4 million or 96.8% at the floor rate.

Non-Performing Assets.

The table below sets forth the amounts and categories of our non-performing assets at the dates indicated.

(in thousands) | December 31, 2011 | | December 31, 2010 | | December 31, 2009 | | December 31, 2008 | | December 31, 2007 | |

| Non-accrual loans: | | | | | | | | | | | | |

| Real Estate: | | | | | | | | | | | | |

| Construction and land development | $ | 1,520 | | $ | 3,383 | | $ | 2,841 | | $ | 1,644 | | $ | 1,841 | |

| Farmland | | 562 | | | - | | | 54 | | | 182 | | | 419 | |

| 1 - 4 family residential | | 5,647 | | | 1,480 | | | 2,814 | | | 1,445 | | | 1,819 | |

| Multifamily | | - | | | 1,357 | | | - | | | - | | | 2 | |

| Non-farm non-residential | | 12,400 | | | 21,944 | | | 7,439 | | | 5,263 | | | 4,950 | |

| Total Real Estate | $ | 20,129 | | $ | 28,164 | | $ | 13,148 | | $ | 8,534 | | $ | 9,031 | |

| Non-Real Estate: | | | | | | | | | | | | | | | |

| Agricultural | $ | 315 | | $ | 446 | | $ | - | | $ | - | | $ | - | |

| Commercial and industrial | | 1,986 | | | 76 | | | 830 | | | 275 | | | 978 | |

| Consumer and other | | 20 | | | 32 | | | 205 | | | 320 | | | 279 | |

| Total Non-Real Estate | $ | 2,321 | | $ | 554 | | $ | 1,035 | | $ | 595 | | $ | 1,257 | |

Total non-accrual loans | $ | 22,450 | | $ | 28,718 | | $ | 14,183 | | $ | 9,129 | | $ | 10,288 | |

| | | | | | | | | | | | | | | | |

| Loans 90 days and greater delinquent & accruing: | | | | | | | | | | | | | | | |

| Real Estate: | | | | | | | | | | | | | | | |

| Construction and land development | $ | - | | $ | - | | $ | - | | $ | - | | $ | - | |

| Farmland | | - | | | - | | | - | | | - | | | - | |

| 1 - 4 family residential | | 309 | | | 1,663 | | | 757 | | | 185 | | | 544 | |

| Multifamily | | - | | | - | | | - | | | - | | | - | |

| Non-farm non-residential | | 419 | | | - | | | - | | | - | | | - | |

| Total Real Estate | $ | 728 | | $ | 1,663 | | $ | 757 | | $ | 185 | | $ | 544 | |

| Non-Real Estate: | | | | | | | | | | | | | | | |

| Agricultural | $ | - | | $ | - | | $ | - | | $ | - | | $ | - | |

| Commercial and industrial | | - | | | - | | | - | | | 17 | | | - | |

| Consumer and other | | 8 | | | 10 | | | 28 | | | 3 | | | 3 | |

| Total Non-Real Estate | $ | 8 | | $ | 10 | | $ | 28 | | $ | 20 | | $ | 3 | |

Total loans 90 days and greater delinquent & accruing | $ | 736 | | $ | 1,673 | | $ | 785 | | $ | 205 | | $ | 547 | |

| | | | | | | | | | | | | | | | |

| Total non-performing loans | $ | 23,186 | | $ | 30,391 | | $ | 14,968 | | $ | 9,334 | | $ | 10,835 | |

| | | | | | | | | | | | | | | | |

| Real Estate Owned: | | | | | | | | | | | | | | | |

| Real Estate Loans: | | | | | | | | | | | | | | | |

| Construction and land development | $ | 1,161 | | $ | 231 | | $ | - | | $ | 89 | | $ | 84 | |

| Farmland | | - | | | - | | | - | | | - | | | - | |

| 1 - 4 family residential | | 1,342 | | | 232 | | | 292 | | | 223 | | | 170 | |

| Multifamily | | - | | | - | | | - | | | - | | | - | |

| Non-farm non-residential | | 3,206 | | | 114 | | | 366 | | | 256 | | | 119 | |

| Total Real Estate | $ | 5,709 | | $ | 577 | | $ | 658 | | $ | 568 | | $ | 373 | |

| Non-Real Estate Loans: | | | | | | | | | | | | | | | |

| Agricultural | $ | - | | $ | - | | $ | - | | $ | - | | $ | - | |

| Commercial and industrial | | - | | | - | | | - | | | - | | | - | |

| Consumer and other | | - | | | - | | | - | | | - | | | - | |

| Total Non-Real Estate | $ | - | | $ | - | | $ | - | | $ | - | | $ | - | |

| Total Real Estate Owned | $ | 5,709 | | $ | 577 | | $ | 658 | | $ | 568 | | $ | 373 | |

| | | | | | | | | | | | | | | | |

| Total non-performing assets | $ | 28,895 | | $ | 30,968 | | $ | 15,626 | | $ | 9,902 | | $ | 11,208 | |

| | | | | | | | | | | | | | | | |

| Restructured Loans in compliance with modified terms | $ | 17,547 | | $ | 9,382 | | $ | - | | $ | - | | $ | - | |

| | | | | | | | | | | | | | | | |

| Non-performing assets to total loans | | 5.04 | % | | 5.38 | % | | 2.65 | % | | 1.63 | % | | 1.95 | % |

| Non-performing assets to total assets | | 2.13 | % | | 2.73 | % | | 1.68 | % | | 1.14 | % | | 1.85 | % |

Nonperforming assets totaled $28.9 million or 2.1% of total assets at December 31, 2011, a decrease of $2.1 million from $31.0 million in December 31, 2010. Management has not identified additional information on any loans not already included in impaired loans or the nonperforming asset total that indicates possible credit problems that could cause doubt as to the ability of borrowers to comply with the loan repayment terms in the future.

Nonperforming assets includes $4.2 million in remaining acquired non-accrual loans and $1.7 million in remaining acquired OREO from Greensburg Bancshares.

Nonperforming assets without those assets acquired by Greensburg totaled $23.0 million at December 31, 2011, a decline of $5.9 million from December 31, 2010.

Non-accrual loans totaled $22.5 million as of December 31, 2011. The nonaccrual loan balance is concentrated in five credit relationships that total approximately $11.7 million or 50.0% of the nonaccrual balance. This nonaccrual loan total includes approximately $3.8 million in a participation loan secured by a hotel, $3.8 million secured by two motels, $2.7 million secured by an entertainment complex, and $1.4 million secured by equipment and real estate.

Non-accrual loans decreased in aggregate $6.3 million from December 31, 2010 to December 31, 2011. The decrease was a combination of loans returning to accrual status, the foreclosure of several loans whose collateral was moved to other real estate owned and charge-offs of losses. The largest credit relationship that returned to accrual status in the first quarter was an $8.6 million loan secured by a climate controlled warehouse and a commercial building. The largest credit that was partially charged off by $2.7 million was secured by two motels.

Construction and land development nonaccrual loans decreased by $1.9 million from $3.4 million in 2010 to $1.5 million in 2011.

One-to-four family residential nonaccrual loans increased $4.2 million primarily due to several loans many of which were acquired from the purchase of Greensburg.

Multifamily non-accrual loans decreased by $1.4 million in the year end of 2011. The decrease was concentrated in one relationship that was secured by a condominium complex. Due to an extended probate process that resulted from the death of a guarantor, the loan went into nonaccrual during the fourth quarter of 2010. The loan returned to accrual status in the first quarter of 2011.

Non-farm non-residential nonaccrual decreased $9.5 million from $21.9 million in December 31, 2010 to $12.4 million in December 31, 2011. The decrease in this category was due in part to the previously mentioned relationship secured by a climate controlled warehouse that returned to accrual status in the first quarter of 2011. The decrease was also the result of a partial charge off for $2.7 million for a loan secured by two motels. In addition, the collateral for several loans was moved into other real estate owned.

Commercial and industrial non-accrual loans increased by $1.9 million principally due to the addition of three loans secured primarily by equipment and accounts receivables.

Other Real Estate Owned (OREO) totaled approximately $5.7 million as of December 31, 2011. OREO is composed of several one to four family residential properties totaling $1.3 million, construction and land development lots of approximately $1.2 million, and commercial properties totaling $3.2 million. Out of this total, approximately $0.9 million of the one-to-four family properties, $0.6 million of the construction and land development properties, and $0.7 million of the commercial properties were acquired with the acquisition of the Bank of Greensburg.

Restructured loans totaled $17.5 million as of December 31, 2011. Restructured loans were concentrated in three credit relationships. The largest credit relationship for $8.9 million is secured by commercial real estate and land development properties. The second largest credit relationship for $6.0 million is secured by an apartment complex. The third credit relationship of $1.7 million was secured by a large single family residence which become a restructured loan in the third quarter of 2011. The modifications were concessions on the interest rate charged for these loans. The effect of the modifications to the Company was a reduction in interest income. These loans still have an allocated reserve in the Company's reserve for loan losses.

Impaired loans totaled $51.1 million as of December 31, 2011. Impaired loans with a valuation allowance totaled $39.9 million and impaired loans without a valuation allowance totaled $11.2 million. Included in the impaired loan total were $17.5 million in restructured loans that are performing under their new terms. For more information, see Note 7 to Consolidated Financial Statements.

Allowance for Loan Losses.

The allowance for loan losses is maintained at a level considered sufficient to absorb potential losses embedded in the loan portfolio. The allowance is increased by the provision for anticipated loan losses as well as recoveries of previously charged off loans and is decreased by loan charge-offs. The provision is the necessary charge to current expense to provide for current loan losses and to maintain the allowance at an adequate level commensurate with Management’s evaluation of the risks inherent in the loan portfolio. Various factors are taken into consideration when determining the amount of the provision and the adequacy of the allowance. These factors include but are not limited to:

| ● | past due and nonperforming assets; |

| ● | specific internal analysis of loans requiring special attention; |

| ● | the current level of regulatory classified and criticized assets and the associated risk factors with each; |

| ● | changes in underwriting standards or lending procedures and policies; |

| ● | charge-off and recovery practices; |

| ● | national and local economic and business conditions; |

| ● | nature and volume of loans; |

| ● | overall portfolio quality; |

| ● | adequacy of loan collateral; |

| ● | quality of loan review system and degree of oversight by its Board of Directors; |

| ● | competition and legal and regulatory requirements on borrowers; |

| ● | examinations of the loan portfolio by federal and state regulatory agencies and examinations; |

| ● | and review by our internal loan review department and independent accountants. |

The data collected from all sources in determining the adequacy of the allowance is evaluated on a regular basis by Management with regard to current national and local economic trends, prior loss history, underlying collateral values, credit concentrations and industry risks. An estimate of potential loss on specific loans is developed in conjunction with an overall risk evaluation of the total loan portfolio. This evaluation is inherently subjective as it requires estimates that are susceptible to significant revision as new information becomes available.

The allowance consists of specific, general and unallocated components. The specific component relates to loans that are classified as doubtful, substandard or special mention. For such loans that are also classified as impaired, an allowance is established when the discounted cash flows (or collateral value or observable market price) of the impaired loan is lower than the carrying value of that loan. The general component covers non-classified loans and is based on historical loss experience adjusted for qualitative factors. An unallocated component is maintained to cover uncertainties that could affect Management's estimate of probable losses.

Provisions made pursuant to these processes totaled $10.2 million for 2011 as compared to $5.7 million for 2010. The provisions made for 2011 were taken to provide for current loan losses and to maintain the allowance at a level commensurate with Management’s evaluation of the risks inherent in the loan portfolio. In addition, the level of provisions reflects management's decision to aggressively address non-performing assets by charging off loans that were not performing. Total charge-offs were $10.4 million for 2011 as compared to $5.6 million for 2010. Recoveries totaled $0.7 million for 2011 and $0.4 million for 2010.

Charged-off real estate construction and land development loans totaled $1.1 million for the year of 2011. There were $0.1 million in charged-off farmland loans for the year of 2011. Charged-off 1-4 family residential loans totaled $1.6 million for the year of 2011. There were no charged-off multifamily loans in the year of 2011. Charged off non-farm non-residential loans totaled $5.2 million in the year of 2011. Included in the non-farm non-residential charge offs was a $2.7 million charge off for a loan secured by two motels. Charged-off agricultural loans totaled $23,000 for the year of 2011. Charged off commercial and industrial loans totaled $1.6 million for the year of 2011. Charged-off consumer loans and credit cards totaled $0.7 million for the year of 2011. Included in the $1.5 million in charge-offs in the commercial and industrial loan category was one credit relationship for $1.4 million that was charged off in the second quarter of 2011. The credit relationship was primarily secured by accounts receivables that were determined by the Company to be fraudulent. The Company is currently pursuing recourse against the guarantor. For more information, see Note 7 to Consolidated Financial Statements.

Allocation of Allowance for Loan Losses.

In prior years, the Company used an internal method to calculate the allowance for loan losses which categorized loans by risk rather than by type. We do not have the ability to accurately and efficiently provide the allocation of the allowance for loan losses by loan type for a five-year historical period. Beginning in 2008, the Company modified the allowance calculation to segregate loans by category and allocate the allowance for loan losses accordingly. The allowance for loan losses calculation considers both qualitative and quantitative risk factors. The quantitative risk factors include, but are not limited to, past due and nonperforming assets, adequacy of collateral, changes in underwriting standings or lending procedures and policies, specific internal analysis of loans requiring special attention and the nature and volume of loans. Qualitative risk factors include, but are not limited to, local and regional business conditions and other economic factors.

The following table shows the allocation of the allowance for loan losses by loan type as of December 31, 2011, 2010, 2009, and 2008.

| | December 31, 2011 | |

| | Real Estate Loans: | | Non-Real Estate Loans: | | | |

| (in thousands except for %) | Construction and Land Development | | Farmland | | 1-4 Family | | Multi-family | | Non-farm non-residential | | Agricultural | | Commercial and Industrial | | Consumer and other | | Unallocated | | Total | |

| Allowance for Loan Loss | $ | 1,002 | | $ | 65 | | $ | 1,917 | | $ | 780 | | $ | 2,980 | | $ | 125 | | $ | 1,407 | | $ | 314 | | $ | 289 | | $ | 8,879 | |

| % of Allowance to Total Allowance for Loan Losses | | 11.3 | % | | 0.7 | % | | 21.6 | % | | 8.8 | % | | 33.6 | % | | 1.4 | % | | 15.8 | % | | 3.5 | % | | 3.3 | % | | 100.0 | % |

| % of Loans in Each Category to Total Loans | | 13.7 | % | | 2.0 | % | | 15.6 | % | | 2.9 | % | | 46.8 | % | | 3.0 | % | | 11.9 | % | | 4.1 | % | | N/A | % | | 100.0 | % |

| | December 31, 2010 | |

| | Real Estate Loans: | | Non-Real Estate Loans: | | | |