UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2013

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from_______to_______

Commission file number: 000-53012

FIRST CHOICE HEALTHCARE SOLUTIONS, INC.

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | | 90-0687379 (I.R.S. Employer Identification No.) |

| | | |

709 S. Harbor City Blvd., Suite 250, Melbourne, FL (Address of principal executive offices) | | 32901 (Zip Code) |

Registrant’s telephone number, including area code(321) 725-0090

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | | Name of each exchange on which registered |

| N/A | | N/A |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yeso Nox

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yeso Nox

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YesxNoo

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company��� in Rule 12b-2 of the Exchange Act.

Large accelerated filero Accelerated filer o Non-accelerated filer o Smaller reporting company x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yeso Nox

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold as of the last business day of the registrant’s most recently completed second fiscal quarter was $4,844,685.

As of March 27, 2014, there were 16,793,248 shares of common stock, par value $0.001 per share, outstanding.

FIRST CHOICE HEALTHCARE SOLUTIONS, INC.

TABLE OF CONTENTS

| | | | Page |

| | | | | |

| | PART I | | | |

| | | | | |

| Item 1. | Business | | | 1 |

| Item 1A. | Risk Factors | | | 12 |

| Item 1B. | Unresolved Staff Comments | | | 23 |

| Item 2. | Properties | | | 23 |

| Item 3. | Legal Proceedings | | | 24 |

| Item 4. | Mine Safety Disclosures | | | 24 |

| | | | | |

| | PART II | | | |

| | | | | |

| Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | | 24 |

| Item 6. | Selected Financial Data | | | 27 |

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | | | 27 |

| Item 7A. | Quantitative and Qualitative Disclosures about Market Risk | | | 34 |

| Item 8. | Financial Statements and Supplementary Data | | | 34 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | | | 34 |

| Item 9A. | Controls and Procedures | | | 34 |

| Item 9B. | Other Information | | | 35 |

| | | | | |

| | PART III | | | |

| | | | | |

| Item 10. | Directors, Executive Officers and Corporate Governance | | | 35 |

| Item 11. | Executive Compensation | | | 38 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | | 39 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | | | 42 |

| Item 14. | Principal Accounting Fees and Services | | | 43 |

| | | | | |

| | PART IV | | | |

| | | | | |

| Item 15. | Exhibits, Financial Statement Schedules | | | 44 |

PART I

This report may contain forward-looking statements within the meaning of Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended, or the Private Securities Litigation Reform Act of 1995. Investors are cautioned that such forward-looking state to all comments are based on our management’s beliefs and assumptions and on information currently available to our management and involve risks and uncertainties. Forward-looking statements include statements regarding our plans, strategies, objectives, expectations and intentions, which are subject to change at any time at our discretion. Forward-looking statements include our assessment, from time to time of our competitive position, the industry environment, potential growth opportunities and the effects of regulation. Forward-looking statements include all statements that are not historical facts and can be identified by terms such as “anticipates,” “believes,” “could,” “estimates,” “expects,” “hopes,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “should,” “will,” “would” or similar expressions.

Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. We discuss many of these risks in greater detail in “Risk Factors.” Given these uncertainties, you should not place undue reliance on these forward-looking statements. Also, forward-looking statements represent our management’s beliefs and assumptions only as of the date of this report. You should read this report and the documents that we reference in this report and have filed as exhibits to the report completely and with the understanding that our actual future results may be materially different from what we expect. Except as required by law, we assume no obligation to update these forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future.

ITEM 1. BUSINESS

History

First Choice Healthcare Solutions, Inc.’s (“FCHS,” “the Company,” “we,” “our” or “us”) mission is to transform, via acquisition and restructuring, multi-specialty clinics or physician-owned practices in the southeastern United States into world class, state-of-the-art medical centers of excellence, thereby establishing and extending ‘First Choice Healthcare Solutions’ brand and reputation as a profitable, well-managed enterprise committed to improving the quality of lives of the caregivers it employs and the health and wellness of the patients and families it serves.

We were incorporated in the State of Colorado on May 2007. In February 2012, we completed a merger with First Choice Healthcare Solutions, Inc., a Delaware corporation formed exclusively for the purpose of merging with the Company, pursuant to which (a) the Company’s state of incorporation changed from Colorado to Delaware (the “Reincorporation”) and (b) the Company’s name changed from Medical Billing Assistance, Inc. to First Choice Healthcare Solutions, Inc.

Our Business

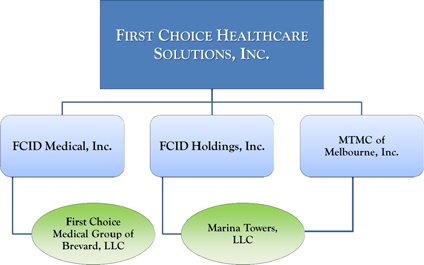

The Company operates in two segments, healthcare services and real estate, through five wholly-owned subsidiaries:

| · | FCID Medical, Inc., which is the subsidiary under which our present center of excellence is owned and operated and future centers of excellence will be owned and operated; |

| · | First Choice Medical Group of Brevard, LLC, which is the Company’s flagship medical center of excellence located in Melbourne, Florida, wholly-owned and operated by FCID Medical, Inc.; |

| · | FCID Holdings, Inc. which operates the Company’s real estate interests, and owns a 99% interest in Marina Towers, LLC; |

| · | MTMC of Melbourne, Inc., which owns a 1% ownership stake in Marina Towers, LLC; and |

| · | Marina Towers, LLC, which owns and operates Marina Towers, a Class A, 78,000 square foot, six-story building located on the Indian River in Melbourne, Florida. |

Diagram 1. First Choice Healthcare Solutions, Inc. Legal Corporate Structure

By distinguishing our medical centers of excellence as premier destinations for clinically superior, patient-centric care that is coordinated across a patient’s care continuum, we expect to deliver more meaningful and collaborative doctor-patient experiences, accurate diagnoses, effective treatment plans, faster recoveries and materially reduced costs. Currently, our strategic focus is to grow in the southeastern United States through selective employment of physicians and/or the acquisition of physician practices that fit our defined acquisition criteria, including the following:

| · | presents the opportunity for FCHS to introduce additional ancillary revenue channels (i.e. on-site magnetic resonance imaging (MRI), X-ray, physical therapy, diagnostic equipment, synergistic medical disciplines, durable medical equipment (DME), related health and wellness products, etc.) that will support and promote enhanced, well-coordinated, patient-centric care while supporting and promoting profitable business operations; |

| · | due diligence supporting economies of scale in billing, collections, purchasing, advertising and compliance that can be fully leveraged to reduce expenses and fuel income growth; and |

| · | creates the opportunity to increase awareness of FCHS’s brand; and aligns with and materially complements our Company’s inherent value proposition to patients, referring physicians and medical institutions, insurers, employers and other healthcare stakeholders in the local markets we serve. |

Healthcare Services

Model for Medical Centers of Excellence

FCHS’s model for each medical center of excellence is strictly defined to ensure that our high standards for patient care and attention can be fostered and preserved. Ideally, a center will:

| · | employ, on average, ten specialty physicians – all of whom are subject to a rigorous qualification and hiring process; |

| · | provide for the combination of synergistic medical disciplines and supported by related in-house ancillary diagnostic services and technologies, i.e. orthopedics/neurology/interventional pain medicine; |

| · | be capable of generating $16-$20 million when operating at optimal economic capacity; and |

| · | be housed in a commercial building, in close geographic proximity to a primary hospital(s), and allows for 12,000-16,000 square feet of usable space for build-out consideration. |

Because FCHS’s leadership view themselves as guardians of their ideals relating to optimal patient experience of care, we continually reinforce the importance of hiring, training, evaluating, compensating and supporting a workforce committed to patient-centered care. Just as vital, we engage our employees in all aspects of process design and treat them with the same dignity and respect that they are expected to show patients and family members. Central to the success of our Company’s long term growth strategy is attracting and recruiting top tier physicians and care specialists that rank in the top percentile of performance in the local markets we serve; and creating a work environment and corporate culture that serves to engage, motivate and retain them.

Due to sweeping healthcare reform, increased regulatory and reimbursement mandates and the financial challenges each of these impose, remaining in private practice is quickly losing its appeal for many physicians. In fact, according to a nationwide survey published in 2013 by recruiting firm Jackson Healthcare, one-third of U.S. physicians plan to leave private medical practice within the next ten years in favor of employment by hospitals and multi-specialty medical groups. Thus, the opportunity for our Company to attract key medical talent has never been more robust.

Our systems of operation unburden the Company’s physicians from productivity-driven, assembly line medicine, and materially diminish the cognitive overload and exhaustion that makes medical care anything but caring or patient-centered. More specifically, the many advantages and benefits of choosing employment by FCHS are being enabled to focus exclusively on delivering excellent patient care; higher income potential; freedom from day-to-day practice administration, including marketing and generating new patient leads; access to state-of-the-art technology, diagnostics and services; and camaraderie and collaboration with a cadre of first rate caregivers dedicated to common, patient-centered goals and objectives. The requirements for running the day-to-day business functions of the centers are the sole responsibility of our management team – and not the physicians. Simply put, doctors get to be doctors.

Currently, we are actively engaged in identifying and pursuing discussions with prospective acquisitions in key target markets – with those being largely in the southeastern U.S. We anticipate investing $4-$6 million to acquire and/or develop one or more medical centers of excellence during the next 12 months, each center may require up to 6-12 months to achieve optimal economic capacity, depending on the number of physicians and physician assistants to be employed, the medical service mix and the type of diagnostic and ancillary services to be offered. However, there can be no assurance that we will be able to negotiate acceptable terms for, or find suitable candidates for, such acquisition.

Medical Service Mix

Like other successful business models for professional medical services, ours is designed to offer the most synergistic and profitable medical service mix. By their nature, some combinations of medical specialties can be more revenue positive than others. Physicians need access to diagnostic equipment and ancillary services, such as MRI, X-ray, DME and physical therapy. Moreover, patients expect their physicians to have access to the best diagnostic and service delivery equipment. Without diagnostic services, many medical practices will find it difficult to maintain their current margins of profitability.

We integrate both medical specialties and diagnostic/ancillary services in our centers to maintain or enhance our profits. While one specialty may have high reimbursements for their professional service but insufficient volume to profitably support the necessary ancillary services, another medical specialty may have a lower professional service reimbursement but high volume ancillary services use. Operating independently, each specialty group would face retreating profit margins and confront significant challenges to maintaining high service levels with adequate equipment and current technologies. However, operating together, they create the optimal mix of professional service fee income and ancillary services income. Since the combination is more profitable than either of its components, there is a favorable opportunity to sustain profit margins that will allow each center to maintain high service levels with state-of-the-art equipment and technologies.

Scalable Back Office and Economies of Scale

Fixed cost legacy administrative functions have subjected many established medical centers to a downward spiral of diminishing profit margins and losses. In legacy medical centers, administrative management, billing, compliance, accounting, marketing, advertising, scheduling, customer service and record keeping functions represent fixed overhead for the practice. The fixed administrative overhead of a practice has the effect of reducing profit margins as the practice experiences declining revenues as a result of lower patient volumes from increasing competition, lower pricing, lower reimbursements or loss of patients to competitors.

A key to our success is our ability to employ a highly experienced team of business managers supported by an array of professional, experienced and healthcare compliant subcontractors. Using the best project management practices, our business managers contract services for billing, compliance, accounting, marketing, advertising, legal, information technology and record keeping functions. The cost of our ‘back office operation’ does not increase in direct relation to our volume, allowing us to sustain profit margins with a cost effective and scalable back office. As the number of physicians increases, so do the economies of scale for our back office. The economies of scale support selecting the best in class subcontractors, while allowing our medical centers of excellence to operate cost effectively with higher service levels.

Specifically, we provide all of the administrative services to support the practice of medicine by our physicians and improve operating efficiencies of our medical centers of excellence:

| · | Recruiting and Credentialing. We have proven experience in locating, qualifying, recruiting and retaining experienced physicians. In addition to the verification of credentials, licenses and references of all prospective physician candidates, each caregiver undergoes level two background checks. We maintain a national database of practicing physicians In addition to our database of physicians, we recruit locally through trade advertising, the American Academy of Orthopaedic Surgeons and referrals from our physicians. |

| · | Billing, Collection and Reimbursement. We assume responsibility for contracting with third-party payors for all of our physicians; and we are responsible for billing, collection and reimbursement for services rendered by our physicians. In all instances, however, we do not assume responsibility for charges relating to services provided by hospitals or other referring physicians with whom we collaborate. Such charges are separately billed and collected by the hospitals or other physicians. The majority of our third party payors remit by EFT and wire transfers. Accordingly, every aspect of the business is positioned to achieve high productivity and lower administrative headcounts and per capita expense. We provide our physicians with a training curriculum that emphasizes detailed documentation of and proper coding protocol for all procedures performed and services provided, and we provide comprehensive internal auditing processes, all of which are designed to achieve appropriate coding, billing and collection of revenue for physician services. All of our billing and collection operations are controlled and will continue to be controlled from our business offices located at our corporate headquarters in Melbourne, Florida. |

| · | Risk Management and Other Services. We maintain a risk management program focused on reducing risk, including the identification and communication of potential risk areas to our medical staff. We maintain professional liability coverage for our group of healthcare professionals. Through our risk management staff, we conduct risk management programs for loss prevention and early intervention in order to prevent or minimize professional liability claims. In addition, we provide a multi-faceted compliance program that is designed to assist our multi-specialty centers of excellence in complying with increasingly complex laws and regulations. We also manage all information technology, facilities management, legal support, marketing support, regulatory compliance and other services. |

Developing and operating additional multi-specialty medical centers of excellence in other geographic areas will take advantage of the economies of scale for our administrative back office functions. Our plan calls for opening up multiple centers in multiple states and cities at a pace that will allow us to maintain the same levels of quality and acceptable profitability from each location. We believe that the scalable structure of our administrative back office functions will efficiently support our expansion plans.

High Technology Infrastructure Supporting High Touch Patient Experiences

Successful retail models in other industries already effectively use telecommunications, remote computing, mobile computing, cloud computing, virtual networks and other leading-edge technologies to manage geographically diverse operating units. These technologies create the infrastructure to allow a central management team to monitor, direct and control geographically dispersed operating units and subcontractors, including national operations.

We believe that the FCHS business model incorporates the best of these technologies. A central management team monitors, directs and controls our multi-specialty medical centers of excellence and all the necessary support subcontractors. FCMG’s administrative operations center on a secure paperless practice management platform. We utilize a state-of-the-art, cloud-based electronic medical record (“EMR”) management system, which provides 24/7, secure, online access to each patient’s test results from virtually anywhere in world, including X-ray and MRI images, diagnosis, patient and doctor notes, visit reports, billing information, insurance coverage, patient identification and personalized care delivery requirements. Our EMR system fully complies with all stages of Meaningful Use standards defined by the Centers for Medicare & Medicaid Services Incentive Programs. These programs govern the use of electronic health records and allow us to earn incentive payments from the U.S. government, pursuant to the Health Information Technology for Economic and Clinical Health (HITECH) Act, which was enacted as part of the American Recovery and Reinvestment Act of 2009. See “HIPAA and Other Privacy Laws.”

We intend to grow by replicating our multi-specialty medical centers of excellence, supported by our standardized policies, procedures and clinic setup guidelines. The administrative functions can be quickly scaled to handle multiple additional centers. As we roll out our business model, we expect our administrative core and clinic retail model to maintain economies of scale for all of our multi-specialty medical centers of excellence.

Referral and Partnering Relationships

Our business model is influenced by the direct contact and daily interaction that our physicians have with their patients, and emphasizes a patient-centric, shared clinical approach that also serves to address the needs of our various “partners,” including hospitals, third-party payors and referring physicians, our physicians and, most importantly, our patients. Our relationships with all of our partners are important to our continued success.

Hospitals

Our relationships with our hospital partners are critical to our operations. We work with our hospital partners to enhance their reputation and market our services to referring physicians, an important source of hospital admissions, within the communities served by those hospitals. In addition, a majority of our physicians maintain regular hospital privileges, as well as trauma privileges where available, to ensure best in class is available to our patients and the community. Under our contracts with hospitals, we are responsible for billing patients and third-party payors for services rendered by our physicians separately from other related charges billed by the hospital or other physicians within the hospital to the same payors.

Third-Party Payors

Our relationships with government-sponsored plans, including Medicare and TRICARE, managed care organizations and commercial health insurance payors are vital to our business. We seek to maintain professional working relationships with our third-party payors, streamline the administrative process of billing and collection, and assist our patients and their families in understanding their health insurance coverage and any balances due for co-payments, co-insurance, deductibles or out-of-network benefit limitations. In addition, through our quality initiatives and continuing research and education efforts, we have sought to enhance clinical care provided to patients, which we believe benefits third-party payors by contributing to improved patient outcomes and reduced long-term health system costs.

We receive compensation for professional services provided by our physicians to patients based upon rates for specific services provided, principally from third-party payors. Our billed charges are substantially the same for all parties in a particular geographic area, regardless of the party responsible for paying the bill for our services. Approximately one-third of our net patient service revenue is received from government-sponsored plans, principally Medicare and TRICARE programs.

Medicare is a health insurance program primarily for individuals 65 years of age and older, certain younger people with disabilities and people with end-stage renal disease. The program is provided without regard to income or assets and offers beneficiaries different ways to obtain their medical benefits. The most common option selected today by Medicare beneficiaries is the traditional fee-for-service payment system. The other options include managed care, preferred provider organizations, private fee-for-service and specialty plans. TRICARE is the healthcare program for U.S. military service members (active, Guard/Reserve and retired) and their families around the world. TRICARE is managed by the Defense Health Agency under leadership of the Assistant Secretary of Defense. Both Medicare and TRICARE compensation rates are generally lower in comparison to commercial health plans. In order to participate in government programs, our center of medical excellence must comply with stringent and often complex enrollment and reimbursement requirements.

We also receive compensation pursuant to contracts with commercial payors that offer a wide variety of health insurance products, such as health maintenance organizations, preferred provider organizations and exclusive provider organizations that are subject to various state laws and regulations, as well as self-insured organizations subject to federal Employee Retirement Income Security Act (“ERISA”) requirements. We seek to secure mutually agreeable contracts with payors that enable our physicians to be listed as in-network participants within the payors’ provider networks

If we do not have a contractual relationship with a health insurance payor, we generally bill the payor our full billed charges. If payment is less than billed charges, we bill the balance to the patient, subject to state and federal laws regulating such billing. Although we maintain standard billing and collections procedures, we also provide discounts and/or payment option plans in certain hardship situations where patients and their families do not have financial resources necessary to pay the amount due at the time services are rendered. Any amounts written-off related to private-pay patients are based on the specific facts and circumstances related to each individual patient account.

Referring Physicians and Practice Groups

Our relationships with our referring physicians and referring practice groups are critical to our success. Our physicians seek to establish and maintain long-term professional relationships with referring physicians in the communities where we practice. We believe that our community presence, through our hospital coverage and medical centers of excellence, assists referring physicians with further enhancing their practices by providing well-coordinated and highly responsive care to their patients who require our musculoskeletal services, diagnostic services and rehabilitative care.

Government Regulation

The healthcare industry is governed by a framework of federal and state laws, rules and regulations that are extensive and complex and for which, in many cases, the industry has the benefit of only limited judicial and regulatory interpretation. If one of our physicians or physician practices is found to have violated these laws, rules or regulations, our business, financial condition and results of operations could be materially adversely affected. Moreover, the Affordable Care Act signed into law in March 2010 contains numerous provisions that are reshaping the United States healthcare delivery system, and healthcare reform continues to attract significant legislative interest, regulatory activity, new approaches, legal challenges and public attention that create uncertainty and the potential for additional changes. Healthcare reform implementation, additional legislation or regulations, and other changes in government policy or regulation may affect our reimbursement, restrict our existing operations, limit the expansion of our business or impose additional compliance requirements and costs, any of which could have a material adverse effect on our business, financial condition, results of operations, cash flows and the trading price of our common stock. See Item 1A. Risk Factors —“General Risks Relating to Our Business—The healthcare regulatory and political framework is uncertain and evolving.”

Fraud and Abuse Provisions

Existing federal laws governing Medicare, TRICARE and other federal healthcare programs (the “FHC Programs”), as well as similar state laws, impose a variety of fraud and abuse prohibitions on healthcare companies like us. These laws are interpreted broadly and enforced aggressively by multiple government agencies, including the Office of Inspector General of the Department of Health and Human Services, the Department of Justice (the “DOJ”) and various state authorities.

The fraud and abuse laws include extensive federal and state regulations applicable to our financial relationships with hospitals, referring physicians and other healthcare entities. In particular, the federal anti-kickback statute prohibits the offer, payment, solicitation or receipt of any remuneration in return for either referring Medicare, TRICARE or other FHC Program business, or purchasing, leasing, ordering or arranging for or recommending any service or item for which payment may be made by an FHC Program. In addition, federal physician self-referral legislation, commonly known as the “Stark Law,” prohibits a physician from ordering certain designated health services reimbursable by Medicare from an entity with which the physician has a prohibited financial relationship. These laws are broadly worded and, in the case of the anti-kickback statute, have been broadly interpreted by federal courts, and potentially subject many healthcare business arrangements to government investigation and prosecution, which can be costly and time consuming. See Item 1A.Risk Factors —“General Risks Relating to Our Business—Stark Law prohibition on physician referrals may be interpreted so as to limit our prospects.”

Violations of these laws are punishable by substantial penalties, including monetary fines, civil penalties, administrative remedies, criminal sanctions (in the case of the anti-kickback statute), exclusion from participation in FHC Programs and forfeiture of amounts collected in violation of such laws, any of which could have an adverse effect on our business and results of operations. Many of the states in which we operate also have anti-kickback and self-referral laws which are applicable to our government and non-government business and which also authorize substantial penalties for violations.

There are a variety of other types of federal and state fraud and abuse laws, including laws authorizing the imposition of criminal, civil and administrative penalties for filing false or fraudulent claims for reimbursement with government healthcare programs. These laws include the civil False Claims Act (“FCA”), which prohibits the submitting of or causing to be submitted false claims to the federal government or federal government programs, including Medicare, the TRICARE program for military dependents and retirees, and the Federal Employees Health Benefits Program. Substantial civil fines and multiple damages, along with other remedies, can be imposed for violating the FCA. Furthermore, proving a violation of the FCA requires only that the government show that the individual or company that submitted or caused to be submitted an allegedly false claim acted in “reckless disregard” of the truth or falsity of the claim, notwithstanding that there may have been no intent to defraud the government program and no actual knowledge that the claim was false (which typically are required to be shown to sustain a criminal conviction). The FCA also applies to the improper retention of known overpayments and includes “whistleblower” provisions that permit private citizens to sue a claimant on behalf of the government and thereby share in the amounts recovered under the law and to receive additional remedies. In recent years, many cases have been brought against healthcare companies by such “whistleblowers,” which have resulted in judgments or, more often, settlements involving substantial payments to the government by the companies involved. It is anticipated that the number of such actions against healthcare companies will continue to increase with the enactment of a growing number of state false claims acts and certain amendments to the FCA recently enacted by Congress and enhanced government enforcement.

In addition, federal and state agencies that administer healthcare programs have at their disposal statutes, commonly known as “civil money penalty laws,” that authorize substantial administrative fines and exclusion from government programs in cases where an individual or company that filed a false claim, or caused a false claim to be filed, knew or should have known that the claim was false or fraudulent. As under the FCA, it often is not necessary for the agency to show that the claimant had actual knowledge that the claim was false or fraudulent in order to impose these penalties.

The civil and administrative false claims statutes are being applied in an increasingly broader range of circumstances. For example, government authorities have asserted that claiming reimbursement for services that fail to meet applicable quality standards may, under certain circumstances, violate these statutes. Government authorities also often take the position, now with support from recent amendments to the FCA, that claims for services that were induced by kickbacks, Stark Law violations or other illicit marketing schemes are fraudulent and, therefore, violate the false claims statutes. Many of the laws and regulations referenced above can be used in conjunction with each other.

If we were excluded from any government-sponsored healthcare programs, not only would we be prohibited from submitting claims for reimbursement under such programs, but we also would be unable to contract with other healthcare providers, such as hospitals, to provide services to them. It could also adversely affect our ability to contract with, or to obtain payment from, non-governmental payors.

Although we diligently conduct our business in compliance with all applicable federal and state fraud and abuse laws, many of the laws and regulations applicable to us, including those relating to billing and those relating to relationships with referring physicians and hospitals, are broadly worded and may be interpreted or applied by prosecutorial, regulatory or judicial authorities in ways that we cannot predict. Accordingly, we cannot assure you that our arrangements or business practices will not be subject to government scrutiny or be alleged or found to violate applicable fraud and abuse laws. Moreover, the standards of business conduct expected of healthcare companies under these laws and regulations have become more stringent in recent years, even in instances where there has been no change in statutory or regulatory language. If there is a determination by government authorities that we have not complied with any of these laws and regulations, our business, financial condition and results of operations could be materially adversely affected. See “Government Investigations.”

Government Reimbursement Requirements

In order to participate in the Medicare program, we must comply with stringent and often complex enrollment and reimbursement requirements. While our compliance program requires that we adhere to the laws and regulations applicable to the government programs in which we participate, our failure to comply with these laws and regulations could negatively affect our business, financial condition and results of operations. See “Government Regulation—Fraud and Abuse Provisions,” “Government Regulation—Compliance Program,” “Government Investigations” and “Other Legal Proceedings,” and Item 1A. Risk Factors—“General Risks Relating to Our Business—The healthcare industry is highly regulated, and government authorities may determine that we have failed to comply with applicable laws or regulation;” “Federal and state laws that protect the privacy and security of protected health information may increase our costs and limit our ability to collect and use that information and subject us to penalties if we are unable to fully comply with such laws;” and “Changes in the rates or methods of third-party reimbursements for medical services could result in reduced demand for our services or create downward pricing pressure, which would result in a decline in our revenues and harm to our financial position.”

In addition, Medicare, TRICARE and other government healthcare programs are subject to statutory and regulatory changes, administrative rulings, interpretations and determinations, requirements for utilization review and new governmental funding restrictions, all of which may materially increase or decrease program payments as well as affect the cost of providing services and the timing of payments to providers. Moreover, because these programs generally provide for reimbursement on a fee-schedule basis rather than on a charge-related basis, we generally cannot increase our revenue by increasing the amount we charge for our services. To the extent our costs increase, we may not be able to recover our increased costs from these programs, and cost containment measures and market changes in non-governmental insurance plans have generally restricted our ability to recover, or shift to non-governmental payors, these increased costs. In attempts to limit federal and state spending, there have been, and we expect that there will continue to be, a number of proposals to limit or reduce Medicare reimbursement for various services. Our business may be significantly and adversely affected by any such changes in reimbursement policies and other legislative initiatives aimed at reducing healthcare costs associated with Medicare, TRICARE and other government healthcare programs.

Our business also could be adversely affected by reductions in or limitations of reimbursement amounts or rates under these government programs, reductions in funding of these programs or elimination of coverage for certain individuals or treatments under these programs.

Antitrust

The healthcare industry is subject to close antitrust scrutiny. In recent years, the Federal Trade Commission (the “FTC”), the Department of Justice (“DOJ”) and state Attorney General have increasingly taken steps to review and, in some cases, taken enforcement action against business conduct and acquisitions in the healthcare industry. Violations of antitrust laws may be punishable by substantial penalties, including significant monetary fines, civil penalties, criminal sanctions, consent decrees and injunctions prohibiting certain activities or requiring divestiture or discontinuance of business operations. Any of these penalties could have a material adverse effect on our business, financial condition and results of operations. We consider the antitrust laws in connection with the acquisition of physician practices and the operation of our business, and we believe our operations are in compliance with applicable laws.

HIPAA and Other Privacy Laws

Numerous federal and state laws, rules and regulations govern the collection, dissemination, use and confidentiality of protected health information, including the federal Health Insurance Portability and Accountability Act of 1996, as amended (“HIPAA”), and its implementing regulations, violations of which are punishable by monetary fines, civil penalties and, in some cases, criminal sanctions. As part of our medical record keeping, third-party billing, research and other services, we and our affiliated practices collect and maintain protected health information on the patients that we serve.

Pursuant to HIPAA, the U.S. Department of Health and Human Services (“HHS”) has adopted standards to protect the privacy and security of individually identifiable health information, known as the Privacy Standards and Security Standards. HHS’s Privacy Standards apply to medical records and other individually identifiable health information in any form, whether electronic, paper or oral, that is used or disclosed by healthcare providers, hospitals, health plans and healthcare clearinghouses, which are known as “Covered Entities.” We have implemented privacy policies and procedures, including training programs, designed to be compliant with the HIPAA Privacy Standards.

HHS’s Security Standards require healthcare providers to implement administrative, physical and technical safeguards to protect the integrity, confidentiality and availability of individually identifiable health information that is electronically received, maintained or transmitted (including between us and our affiliated practices). We have implemented security policies, procedures and systems designed to facilitate compliance with the HIPAA Security Standards.

In February 2009, Congress enacted the Health Information Technology for Economic and Clinical Health Act (“HITECH”) as part of the American Recovery and Reinvestment Act (“ARRA”). Among other changes to the law governing protected health information, HITECH strengthens and expands HIPAA, increases penalties for violations, gives patients new rights to restrict uses and disclosures of their health information, and imposes a number of privacy and security requirements directly on our “Business Associates,” which are third-parties that perform functions or services for us or on our behalf. Specifically, HITECH requires that Covered Entities and Business Associates alike report any unauthorized use or disclosure of individually identifiable health information that meets the definition of a breach, to the affected individuals, HHS and, depending on the number of affected individuals, the media for the affected market. HITECH also authorizes state Attorneys General to bring civil actions in response to violations of HIPAA that threaten the privacy of state residents. As a result, we have made revisions to our privacy policies and procedures so that we are compliant with HITECH requirements.

In addition to the federal HIPAA and HITECH requirements, numerous other state and certain other federal laws protect the confidentiality of patient information, including state medical privacy laws, state social security number protection laws, human subjects research laws and federal and state consumer protection laws. In some cases, state laws are more stringent than HIPAA and therefore, are not preempted by HIPAA.

Environmental Regulations

Our healthcare operations generate medical waste that must be disposed of in compliance with federal, state and local environmental laws, rules and regulations. Our office-based operations are subject to compliance with various other environmental laws, rules and regulations. Such compliance does not, and we anticipate that such compliance will not, materially affect our capital expenditures, financial position or results of operations.

Compliance Program

We maintain a compliance program that reflects our commitment to complying with all laws, rules and regulations applicable to our business and that meets our ethical obligations in conducting our business (the “Compliance Program”). We believe our Compliance Program provides a solid framework to meet this commitment and our obligations as a provider of health care services, including:

| • | a Compliance Committee consisting of our senior executives; |

| • | ourCode of Ethics, which is applicable to our employees, officers and directors; |

| • | a disclosure program that includes a mechanism to enable individuals to disclose on a confidential or anonymous basis to our Chief Executive Officer, or any person who is not in the disclosing individual’s chain of command, issues or questions believed by the individual to be a potential violation of criminal, civil, or administrative laws; |

| • | an organizational structure designed to integrate our compliance objectives into our corporate offices and centers of medical excellence; and |

| • | education, monitoring and corrective action programs, including a disclosure policy designed to establish methods to promote the understanding of our Compliance Program and adherence to its requirements. |

The foundation of our Compliance Program is ourCode of Ethics which is intended to be a comprehensive statement of the ethical and legal standards governing the daily activities of our employees, affiliated professionals, independent contractors, officers and directors. All our personnel are required to abide by, and are given thorough education regarding, ourCode of Ethics. In addition, all employees are expected to report incidents that they believe in good faith may be in violation of ourCode of Ethics.

Government Investigations

We expect that audits, inquiries and investigations from government authorities, agencies, contractors and payors will occur in the ordinary course of business. Such audits, inquiries and investigations and their ultimate resolutions, individually or in the aggregate, could have a material adverse effect on our business, financial condition, results of operations, cash flows and the trading price of our common stock. To the best of our knowledge, as of this time, our health care business is not the subject of any pending audit, inquiry or investigation by any governmental authority.

Other Legal Proceedings

In the ordinary course of our business, we may become involved in pending and threatened legal actions and proceedings, most of which might involve claims of medical malpractice related to medical services provided by our physicians. Our contracts with hospitals generally require us to indemnify them and their affiliates for losses resulting from the negligence of our physicians. We may also become subject to other lawsuits that could involve large claims and significant defense costs. We believe, based upon a review of pending actions and proceedings, that the outcome of such legal actions and proceedings will not have a material adverse effect on our business, financial condition or results of operations. The outcome of such actions and proceedings, however, cannot be predicted with certainty and an unfavorable resolution of one or more of them could have a material adverse effect on our business, financial condition, results of operations, cash flows and the trading price of our common stock.

Although we currently maintain liability insurance coverage intended to cover professional liability and certain other claims, we cannot assure that our insurance coverage will be adequate to cover liabilities arising out of claims asserted against us in the future where the outcomes of such claims are unfavorable to us. Liabilities in excess of our insurance coverage, including coverage for professional liability and certain other claims, could have a material adverse effect on our business, financial condition and results of operations. See “Professional and General Liability Coverage.”

Professional and General Liability Coverage

We maintain professional and general liability insurance policies with third-party insurers on a claims-made basis, subject to deductibles, self-insured retention limits, policy aggregates, exclusions, and other restrictions, in accordance with standard industry practice. We believe that our insurance coverage is appropriate based upon our claims experience and the nature and risks of our business. However, we cannot assure that any pending or future claim will not be successful or if successful will not exceed the limits of available insurance coverage.

FCID Medical, Inc.

FCID Medical, Inc. (FCID) is our wholly-owned subsidiary under which our present center of excellence is owned and operated and future centers of excellence will be owned and operated. FCID managed First Choice Medical Group of Brevard, LLC from November 2011 until we acquired the Company in April 2012. Since acquiring the practice, we have succeeded in increasing monthly patient visits, improving management of account payables/receivables, and expanding the number of physicians and care specialists on staff.

Based in Melbourne, Florida, FCMG is our flagship multi-specialty medical center of excellence that specializes in the delivery of musculoskeletal medicine, diagnostic services and rehabilitative care with multiple quality-focused goals centered on enriching its patients’ care experience. Our physicians and care specialists are recruited and retained with an emphasis on best practices and attitude: that being committed to meeting and exceeding the needs of patients and their families. We currently employ eight best in class physicians who represent what FCHS believes rank as the best clinicians in their respective medical disciplines in Brevard County, Florida. Moreover, all employees of FCMG, from the receptionists to the doctors, are considered caregivers whoput the patient first. All caregivers cooperate with one another through a common focus on the best interests and personal goals of each patient. Moreover, families and friends of each patient are considered vital components of the care team.

Care is focused on each patient’s full continuum of care, which requires a more ‘personalized’ approach to treatment. Care is customized to ensure that each patient’s needs, values and choices are always considered, which squarely aligns with FCHS’s slogan of “transforming healthcare delivery, one patient at a time.”

Diagram 2. First Choice Medical Group’s Patient-Centric Care Delivery Model

We strive every day to ensure that our patients are never kept waiting to see our physicians. Based upon FCMG’s patient exit polling results collected in 2013, our patient wait time has remained consistently below the industry average of approximately 23 minutes (source: Vitals.com).

Care providers listen to and honor patients and family perspectives and choices. Moreover, our caregivers intend to continue to communicate and share complete and unbiased information with patients and families in ways that are affirming and useful in decision-making processes. Our care delivery practices exemplify the very definition of patient-centric care, explicitly recognizing the importance of human interaction in terms of personalized care, kindness and being ‘present’ with patients.

FCMG’s patient-centric culture strives to include providing an inviting, easily accessible, peaceful, healing environment that is aesthetically pleasing and designed specifically to allay patient fear, anxiety and discomfort. The design and décor of FCMG’s lobby and diagnostic and treatment areas are intended to define and reinforce a strong and relevant brand image of quality, patient-centered care. Capitalizing on sweeping views of the Indian River, FCMG’s spa-like decor provides a seamless connection to nature and promotes a palpable sense of good health and wellness.

FCMG also engages the most advanced diagnostic technologies coupled with the latest in individualized care, including trigger point injections and pharmacological, physical, neurological, orthopedic, chiropractic and massage therapy treatments. Our care facilities house both a digital GE X-Ray system and a GE 450 MRI Gem Suite system, which is physically positioned to capitalize on the expansive waterfront view of the Indian River, promoting patient relaxation and soothing fear and anxiety.

Our physicians currently have hospital and surgical privileges at several hospitals serving Brevard County, Florida, and include:

| · | Health First, Inc. – an integrated healthcare delivery system comprising: |

| o | Holmes Regional Medical Center; |

| o | Cape Canaveral Hospital; |

| · | Melbourne Same-Day Surgery Center; |

| · | Merritt Island Surgery Center; |

| · | Crane Creek Surgery Center; and |

| · | Wuestoff Medical Centers in Rockledge and Melbourne. |

Geographic Service Region

Currently, 100% of our revenues are generated from our business interests operating in Melbourne, located in Brevard County, Florida along the coast of the Atlantic Ocean. As of the 2010 Census, the population of Brevard was 543,376, making it the ninth most populous county in the state. Influenced by the presence of the John F. Kennedy Space Center, Brevard County is also known as the “Space Coast.” Military installations in Brevard County include Patrick Air Force Base, Cape Canaveral Air Force Station and the U.S. Air Force Malabar Test Facility. In addition, the U.S. Navy maintains a Trident turning basin at Port Canaveral for ballistic missile submarines.

Real Estate

Marina Towers, LLC

Marina Towers, LLC is our subsidiary which owns and operates Marina Towers, a Class A 78,000 square foot, six-story building located on the Indian River in Melbourne, Florida. The address is 709 South Harbor City Boulevard, Melbourne, Florida 32901. In addition to housing our corporate headquarters and First Choice Medical Group, the building, which averages 95% annual occupancy, also leases commercial office space to tenants that include UBS Financial, Support Systems and Modus Operandi.

Our wholly owned subsidiary FCID Holdings, Inc. holds a 99% ownership stake in Marina Towers, LLC; and our wholly owned subsidiary MTMC of Melbourne, Inc. holds the remaining 1% ownership.

Our Headquarters

Our corporate headquarters is located on the shore of the Indian River at 709 S. Harbor City Boulevard, Suite 250, Melbourne, Florida 32901 in Marina Towers, which is owned by Marina Towers, LLC, a subsidiary owned by FCID Holdings, Inc. and MTMC of Melbourne, Inc., both wholly owned subsidiaries of the Company.

Employees

As of December 31, 2013, we employed approximately 40 employees, which included eight physicians and two physician assistants.

Merger, Re-Incorporation and Name Change

We were incorporated in the State of Colorado on May 30, 2007 to act as a holding corporation for I.V. Services Ltd., Inc. (“IVS”), a Florida corporation engaged in providing billing services to providers of medical services. IVS was incorporated in the State of Florida on September 28, 1987, and on June 30, 2007, 2,429,000 common shares were issued to Mr. Michael West and other IVS shareholders in exchange for 100% of the capital stock of IVS. In the second quarter of 2011, we disposed of IVS, which, at the time, was an inactive, wholly-owned subsidiary of the Company. The consideration for the disposition was the net liability assumption by the purchaser.

On December 29, 2010, we entered into a Share Exchange Agreement (the “Share Exchange Agreement”) with FCID Medical, Inc., a Florida corporation (“FCID Medical”) and FCID Holdings, Inc., a Florida corporation (“FCID Holdings)”, which together will be referred to herein with FCID Medical as “FCID”, and the shareholders of FCID (the “FCID Shareholders”). Pursuant to the terms of the Share Exchange Agreement, the FCID Shareholders exchanged 100% of the outstanding common stock of FCID for a total of 10,000,000 common shares of the Company, resulting in FCID Medical and FCID Holdings being 100% owned subsidiaries of the Company (the “Share Exchange”).

On or about February 13, 2012, we obtained stockholder consent for (i) the approval of an agreement and plan of merger (the “Merger Agreement”) with First Choice Healthcare Solutions, Inc., (“FCHS Delaware”), a Delaware corporation formed exclusively for the purpose of merging with the Company, pursuant to which (a) the Company’s state of incorporation changed from Colorado to Delaware (the “Reincorporation”) (b) the Company’s name changed from Medical Billing Assistance, Inc. to First Choice Healthcare Solutions, Inc. (the “Name Change”), (c) every four shares of Company’s common stock was exchanged for one share of FCHS Delaware common stock (effectively resulting in a four-to-one reverse split of the Company’s common stock) (the “Reverse Split”), and (d) FCHS Delaware inherited the rights and property of the Company and assumed the liabilities of the Company and (ii) the approval of the Medical Billing Assistance, Inc. 2011 Incentive Stock Plan. The effective date for the Reincorporation and the Reverse Split was April 4, 2012. The Company changed its name to be more closely aligned with its target market.

Our address is 709 S. Harbor City Blvd., Suite 250, Melbourne, Florida, 32901 and our phone number is (321) 725-0090. Our website address is www.myfchs.com. Information contained in our website is not incorporated by reference herein.

Where You Can Find Additional Information

The Company is subject to the reporting requirements under the Exchange Act. The Company files with, or furnishes to, the SEC quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports and will furnish its proxy statement. These filings are available free of charge on the Company’s website, www.myfchs.com, shortly after they are filed with, or furnished to, the SEC. The SEC maintains an Internet website,www.sec.gov, which contains reports and information statements and other information regarding issuers.

ITEM 1A. RISK FACTORS

The risk factors discussed below could cause our actual results to differ materially from those expressed in any forward-looking statements. Although we have attempted to list comprehensively these important factors, we caution you that other factors may in the future prove to be important in affecting our results of operations. New factors emerge from time to time and it is not possible for us to predict all of these factors, nor can we assess the impact of each such factor on the business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statement.

The risks described below set forth what we believe to be the most material risks associated with the purchase of our common stock. Before you invest in our common stock, you should carefully consider these risk factors, as well as the other information contained in this prospectus.

General Risks Regarding Our Business

We have a limited operating history that impedes our ability to evaluate our potential future performance and strategy.

Our Company implemented its unique business model in 2012 and we continue to enhance the strategy of the business plan. Our limited operating history in our present format makes it difficult for us to evaluate our future business prospects and make decisions based on estimates of our future performance. To address these risks and uncertainties, we must do the following:

| · | Successfully execute our business strategy; |

| · | Respond to competitive developments; |

| · | Effectively and efficiently integrate new acquisitions; and |

| · | Attract, integrate, retain and motivate qualified personnel. |

We cannot be certain that our business strategy will be successful or that we will successfully address these risks. In the event that we do not successfully address these risks, our business, prospects, financial condition and results of operations may be materially and adversely affected.

We are implementing a strategy to grow our business, which is expensive and may not generate income.

We intend to grow our business, and we plan to incur expenses associated with our growth and expansion. Although we are taking steps to raise funds through equity offerings to implement our growth strategy, these funds may not be adequate to offset all of the expenses we incur in expanding our business. We will need to generate revenues to offset expenses associated with our growth, and we may be unsuccessful in achieving sufficient revenues, despite our attempts to grow our business. If our growth strategies do not result in sufficient revenues and income, we may have to abandon our plans for further growth and/or cease operations, which could have a material and adverse effect on our business, prospects and financial condition.

We may need to raise additional capital. If we are unable to raise additional capital, our business may fail.

If we require additional capital, we may need to borrow money or sell more securities. Under these circumstances, we may be unable to secure additional financing on favorable terms or at all.

Selling additional stock, either privately or publicly, would dilute the equity interests of our stockholders. If we borrow money, we will have to pay interest and may also have to agree to restrictions that limit our operating flexibility. If we are unable to obtain required capital for operations or growth, we may have to curtail business operations which would have a material negative effect on operating results and most likely result in a lower stock price.

Adverse changes in general domestic and worldwide economic conditions and instability and disruption of credit markets could adversely affect our operating results, financial condition, or liquidity.

We are subject to risks arising from adverse changes in general domestic and global economic conditions, including recession or economic slowdown and disruption of credit markets. Recent global market and economic conditions have been unprecedented and challenging with tighter credit conditions and recession in most major economies. Continued concerns about the systemic impact of potential long-term and wide-spread recession, inflation, energy costs, geopolitical issues, the availability and cost of credit, the United States mortgage market and a declining real estate market in the United States have contributed to increased market volatility and diminished expectations for the United States economy. Added concerns fueled by the United States government financial assistance to certain companies and other federal government’s interventions in the United States financial system has led to increased market uncertainty and instability in both United States and international capital and credit markets. These conditions, combined with volatile oil prices, declining business and consumer confidence, increased unemployment, increased tax rates and governmental budget deficits and debt levels have contributed to volatility of unprecedented levels. We believe our healthcare clinics may be impacted by unemployment rates, the number of under-insured or uninsured patients and other conditions arising from the global economic conditions described above. At this time, it is unclear what impact this might have on our future revenues or business.

As a result of these market conditions, the cost and availability of credit has been and may continue to be adversely affected by illiquid credit markets and wider credit spreads. Concern about the stability of the markets generally and the strength of counterparties specifically has led many lenders and institutional investors to reduce, and in some cases, cease to provide funding to borrowers.

Continued turbulence in the United States and international markets and economies may adversely affect our liquidity and financial condition, and the liquidity and financial condition of our patients. If these market conditions continue, they may limit our ability, and the ability of our patients, to timely replace maturing liabilities, and access the capital markets to meet liquidity needs, resulting in material and adverse effects on our business, prospects, financial condition and results of operations.

While the majority of the cost of medical care is typically reimbursed by third-party payers such as commercial healthcare insurance companies or government programs, including Medicare and TRICARE, the consumer pays a portion of health care costs and we are affected by changes in the consumer’s disposal revenue.

After payments by commercial healthcare insurance companies or government programs, including Medicare and TRICARE, the remaining portion of the cost of medical care is paid by the patient. Accordingly, our operating results may vary based upon the impact of changes in the disposable income of consumers interested in healthcare, among other economic factors. A significant decrease in consumer disposable income in a weak economy may result in a decrease in the number of medical procedures performed and a decline in our revenues and profitability. In addition, weak economic conditions may cause some of our patients to experience financial distress or declare bankruptcy, which may negatively impact our accounts receivable collection experience.

Since a significant percentage of our operating expenses are fixed, a relatively small decrease in revenues could have a significant negative impact on our financial results.

A significant percentage of our expenses will be fixed - meaning they do not vary significantly with the increase or decrease in revenues. Such expenses include, but will not be limited to, debt service and capital lease payments, rent and operating lease payments, salaries, maintenance and insurance. As a result, a small reduction in the prices we charge for our services or procedure volume could have a disproportionately negative effect on our financial results.

Loss of key executives, limited experience in operating a public company and failure to attract qualified managers and sales persons could limit our growth and negatively impact our operations.

We depend upon our management team to a substantial extent. In particular, we depend upon Christian Charles Romandetti, our President and Chief Executive Officer for his skills, experience and knowledge of our Company and industry contacts. The loss of Mr. Romandetti or other members of our management team could have a material adverse effect on our business, results of operations or financial condition.

Our limited experience in dealing with the increasingly complex laws pertaining to public companies could be a significant disadvantage to us in that it is likely that an increasing amount of management’s time will be devoted to these activities which will result in less time being devoted to the management and growth of our company. It is possible that we will be required to expand our employee base and hire additional employees to support our operations as a public company which will increase our operating costs in future periods.

We require medical clinic managers, medical professionals and marketing persons with experience in our industry to operate and market our medical clinic services. It is impossible to predict the availability of qualified persons or the compensation levels that will be required to hire them. The loss of the services of any member of our senior management or our inability to hire qualified persons at economically reasonable compensation levels could adversely affect our ability to operate and grow our business.

We may have difficulties managing growth which could lead to higher losses.

Rapid growth could strain our human and capital resources, potentially leading to higher operating losses. Our ability to manage operations and control growth will be dependent upon our ability to raise and spend capital to successfully attract, train, motivate, retain and manage new employees and continue to update and improve our management and operational systems, infrastructure and other resources, financial and management controls, and reporting systems and procedures. Should we be unsuccessful in accomplishing any of these essential aspects of our growth in an efficient and timely manner, then management may receive inadequate information necessary to manage our operations, possibly causing additional expenditures and inefficient use of existing human and capital resources or we otherwise may be forced to grow at a slower pace that could slow or eliminate our ability to achieve and sustain profitability. Such slower than expected growth may require us to restrict or cease our operations and go out of business.

We may not receive payment from some of our healthcare patients because of their financial circumstances.

Some of our healthcare provider patients may not have significant financial resources, liquidity or access to capital. If these patients experience financial difficulties they may be unable to pay for the healthcare services that we will provide. A significant deterioration in general or local economic conditions could have a material adverse effect on the financial health of our healthcare provider patients. As a result, this may adversely affect our financial condition and results of operations.

We may be subject to medical professional liability risks, which could be costly and could negatively impact our business and financial results.

We may be subject to professional liability claims. Although there currently are no known hazards associated with any of our procedures or technologies when performed or used properly, hazards may be discovered in the future. For example: there is a risk of harm to a patient during an MRI if the patient has certain types of metal implants or cardiac pacemakers within his or her body. Although patients are screened to safeguard against this risk, screening may nevertheless fail to identify the hazard. There also is potential risk to patients treated with therapy equipment secondary to inadvertent or excessive over- or under- exposure to radiation — a topic on which the U.S. House of Representatives Committee on Energy and Commerce Subcommittee on Health held a hearing on February 26, 2010. We maintain professional liability insurance with coverage that we believe is consistent with industry practice and appropriate in light of the risks attendant to our business. However, any claim made against us could be costly to defend against, resulting in a substantial damage award against us and divert the attention of our management team from our operations, which could have an adverse effect on our financial performance.

We may not be able to achieve the expected benefits from future acquisitions, which would adversely affect our financial condition and results.

We plan to rely on acquisitions as a method of expanding our business. If we do not successfully integrate acquisitions, we may not realize anticipated operating advantages and cost savings. The integration of companies that have previously operated separately involves a number of risks, including:

| · | Demands on management related to the increase in our size after an acquisition; |

| · | The diversion of management’s attention from the management of daily operations to the integration of operations; |

| · | Difficulties in the assimilation and retention of employees; |

| · | Potential adverse effects on operating results; and |

| · | Challenges in retaining patients. |

We may not be able to maintain the levels of operating efficiency acquired companies have achieved or might achieve separately. Successful integration of each of their operations will depend upon our ability to manage those operations and to eliminate redundant and excess costs. Difficulties in combining operations may not be able to achieve the cost savings and other size-related benefits that we hoped to achieve from these acquisitions, which would harm our financial condition and operating results.

The healthcare regulatory and political framework is uncertain and evolving.

Healthcare laws and regulations may change significantly in the future which could adversely affect our financial condition and results of operations. We continuously monitor these developments and modify our operations from time to time as the legislative and regulatory environment changes.

In March 2010, President Barack Obama signed one of the most significant health care reform measures in decades providing healthcare insurance for approximately 30 million more Americans. The Patient Protection and Affordable Care Act, as amended by the Health Care and Education Affordability Reconciliation Act (collectively, the “PPACA”), substantially changes the way health care is financed by both governmental and private insurers, including several payment reforms that establish payments to hospitals and physicians based in part on quality measures, and may significantly impact our industry. The PPACA requires, among other things, payment rates for services using imaging equipment that costs over $1 million to be calculated using revised equipment usage assumptions and reduced payment rates for imaging services paid under the Medicare Part B fee schedule. We are unable to predict what effect the PPACA or other healthcare reform measures that may be adopted in the future will have on our business.

The healthcare industry is highly regulated, and government authorities may determine that we have failed to comply with applicable laws or regulations.

The healthcare industry and physicians’ medical practices, including the healthcare and other services that we and our affiliated physicians provide, are subject to extensive and complex federal, state and local laws and regulations, compliance with which imposes substantial costs on us. Of particular importance are the provisions summarized as follows:

| · | federal laws (including the federal False Claims Act) that prohibit entities and individuals from knowingly or recklessly making claims to Medicare and other government programs that contain false or fraudulent information or from improperly retaining known overpayments; |

| · | a provision of the Social Security Act, commonly referred to as the “anti-kickback” law, that prohibits the knowing and willful offer, payment, solicitation or receipt of any bribe, kickback, rebate or other remuneration, in cash or in kind, in return for the referral or recommendation of patients for items and services covered, in whole or in part, by federal healthcare programs, such as Medicare; |

| · | a provision of the Social Security Act, commonly referred to as the Stark Law, that, subject to limited exceptions, prohibits physicians from referring Medicare patients to an entity for the provision of certain “designated health services” if the physician or a member of such physician’s immediate family has a direct or indirect financial relationship (including a compensation arrangement) with the entity; |

| · | similar state law provisions pertaining to anti-kickback, fee splitting, self-referral and false claims issues, which typically are not limited to relationships involving federal payors; |

| · | provisions of HIPAA that prohibit knowingly and willfully executing a scheme or artifice to defraud a healthcare benefit program or falsifying, concealing or covering up a material fact or making any material false, fictitious or fraudulent statement in connection with the delivery of or payment for healthcare benefits, items or services; |

| · | state laws that prohibit general business corporations from practicing medicine, controlling physicians’ medical decisions or engaging in certain practices, such as splitting fees with physicians; |

| · | federal and state laws that prohibit providers from billing and receiving payment from Medicare and TRICARE for services unless the services are medically necessary, adequately and accurately documented and billed using codes that accurately reflect the type and level of services rendered; |

| · | federal and state laws pertaining to the provision of services by non-physician practitioners, such as advanced nurse practitioners, physician assistants and other clinical professionals, physician supervision of such services and reimbursement requirements that may be dependent on the manner in which the services are provided and documented; and |

| · | federal laws that impose civil administrative sanctions for, among other violations, inappropriate billing of services to federally funded healthcare programs, inappropriately reducing hospital care lengths of stay for such patients, or employing individuals who are excluded from participation in federally funded healthcare programs. |

In addition, we believe that our business will continue to be subject to increasing regulation, the scope and effect of which we cannot predict. See Item 1. Business—“Government Regulation.”

We may in the future become the subject of regulatory or other investigations or proceedings, and our interpretations of applicable laws, rules and regulations may be challenged.