Filed Pursuant to Rule 424(b)(3)

Registration No. 333-147414

Registration No. 333-147414

SUPPLEMENT NO. 14 DATED OCTOBER 21, 2010

TO PROSPECTUS DATED SEPTEMBER 21, 2009

APPLE REIT NINE, INC.

The following information supplements the prospectus of Apple REIT Nine, Inc. dated September 21, 2009 and is part of the prospectus. This Supplement updates the information presented in the prospectus.Prospective investors should carefully review the prospectus and this Supplement No. 14 (which is cumulative and replaces all prior Supplements).

TABLE OF CONTENTS

|

|

| |||||

|

| S-3 | |||||

|

| S-6 | |||||

|

| S-9 | |||||

|

| S-14 | |||||

Financial and Operating Information for Our Purchased Properties |

|

| S-17 | ||||

|

| S-23 | |||||

|

| S-28 | |||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

| S-30 | ||||

|

| S-31 | |||||

|

| S-33 | |||||

|

| F-1 | |||||

Certain forward-looking statements are included in the prospectus and this supplement. These forward-looking statements may involve our plans and objectives for future operations, including future growth and availability of funds. These forward-looking statements are based on current expectations, which are subject to numerous risks and uncertainties. Assumptions relating to these statements involve judgments with respect to, among other things, the continuation of our offering of Units, future economic, competitive and market conditions and future business decisions, together with local, national and international events (including, without limitation, acts of terrorism or war, and their direct and indirect effects on travel and the economy). All of these matters are difficult or impossible to predict accurately and many of them are beyond our control. Although we believe the assumptions relating to the forward-looking statements, and the statements themselves, are reasonable, any of the assumptions could be inaccurate and, therefore, there can be no assurance that these forward-looking statements will prove to be accurate. In light of the significant uncertainties inherent in these forward-looking statements, the inclusion of this information should not be regarded as a representation by us or any other person that our objectives and plans, which we consider to be reasonable, will be achieved.

S-1

“Courtyard by Marriott,” “Fairfield Inn,” “Fairfield Inn & Suites,” “TownePlace Suites,” “Marriott,” “SpringHill Suites” and “Residence Inn” are each a registered trademark of Marriott International, Inc. or one of its affiliates. All references below to “Marriott” mean Marriott International, Inc. and all of its affiliates and subsidiaries, and their respective officers, directors, agents, employees, accountants and attorneys. Marriott is not responsible for the content of this prospectus supplement, whether relating to hotel information, operating information, financial information, Marriott’s relationship with Apple REIT Nine, Inc., or otherwise. Marriott is not involved in any way, whether as an “issuer” or “underwriter” or otherwise, in the offering by Apple REIT Nine, Inc. and receives no proceeds from the offering. Marriott has not expressed any approval or disapproval regarding this prospectus supplement or the offering related to this prospectus supplement, and the grant by Marriott of any franchise or other rights to Apple REIT Nine, Inc. shall not be construed as any expression of approval or disapproval. Marriott has not assumed, and shall not have, any liability in connection with this prospectus supplement or the offering related to this prospectus supplement. “Hampton Inn,” “Hampton Inn & Suites,” “Homewood Suites,” “Embassy Suites,” “Hilton Garden Inn” and “Home2 by Hilton” are each a registered trademark of Hilton Worldwide or one of its affiliates. All references below to “Hilton” mean Hilton Worldwide and all of its affiliates and subsidiaries, and their respective officers, directors, agents, employees, accountants and attorneys. Hilton is not responsible for the content of this prospectus supplement, whether relating to hotel information, operating information, financial information, Hilton’s relationship with Apple REIT Nine, Inc., or otherwise. Hilton is not involved in any way, whether as an “issuer” or “underwriter” or otherwise, in the offering by Apple REIT Nine, Inc. and receives no proceeds from the offering. Hilton has not expressed any approval or disapproval regarding this prospectus supplement or the offering related to this prospectus supplement, and the grant by Hilton of any franchise or other rights to Apple REIT Nine, Inc. shall not be construed as any expression of approval or disapproval. Hilton has not assumed, and shall not have, any liability in connection with this prospectus supplement or the offering related to this prospectus supplement. S-2

We completed the minimum offering of Units (with each Unit consisting of one Common Share and one Series A Preferred Share) at $10.50 per Unit on May 14, 2008. We are continuing the offering at $11 per Unit in accordance with the prospectus. We registered to sell a total of 182,251,082 Units. As of September 30, 2010, 22,573,725 Units remained unsold. Our offering of Units expires on April 25, 2011, provided that the offering will be terminated if all of the Units are sold before then. As of September 30, 2010, we had closed on the following sales of Units in the offering: Price Per Number of Gross Proceeds Net of Selling $10.50 9,523,810 $ 100,000,000 $ 90,000,000 $11.00 150,153,547 1,651,689,025 1,486,520,123 Total 159,677,357 $ 1,751,689,025 $ 1,576,520,123 Our distributions since the initial capitalization through June 30, 2010 totaled approximately $119.9 million of which approximately $74.9 million was used to purchase additional Units under the Company’s best-efforts offering. In 2008 and 2009, our initial years of operations, over half of the $70.3 million in total distributions represented a return of capital (specifically, 53% and 58% in 2009 and 2008, respectively), as detailed below. Our distributions were paid at a monthly rate of $0.073334 per common share beginning in June 2008. Since the initial capitalization through June 30, 2010, our net cash generated from operations, from our Consolidated Statements of Cash Flows, was approximately $48.1 million, which exceeded the net cash distributions. The following is a summary of the distributions and cash generated by operations. Total Total Declared and Paid Net Cash Cash Reinvested Total 2nd Quarter 2008 $ 0.07 $ 300,000 $ 593,000 $ 893,000 $ 323,000 3rd Quarter 2008 0.22 1,694,000 3,094,000 4,788,000 966,000 4th Quarter 2008 0.22 2,582,000 4,749,000 7,331,000 2,047,000 1st Quarter 2009 0.22 3,624,000 6,265,000 9,889,000 2,204,000 2nd Quarter 2009 0.22 4,728,000 7,897,000 12,625,000 8,888,000 3rd Quarter 2009 0.22 5,956,000 9,790,000 15,746,000 8,908,000 4th Quarter 2009 0.22 7,240,000 11,830,000 19,070,000 9,137,000 1st Quarter 2010 0.22 8,656,000 14,160,000 22,816,000 3,963,000 2nd Quarter 2010 0.22 10,241,000 16,518,000 26,759,000 11,697,000 $ 1.83 $ 45,021,000 $ 74,896,000 $ 119,917,000 $ 48,133,000

Unit

Units Sold

Proceeds

Commissions and Marketing

Expense Allowance

Distributions

Declared and

Paid per Share

From

Operations(1)

| ||||||||||||||||||||

(1) |

|

| See complete consolidated statement of cash flows for the six months ending June 30, 2010 included in our most recent Form 10-Q for the quarter ended June 30, 2010, and the complete consolidated statements of cash flows for the years ended December 31, 2009 and 2008 included in our audited financial statements included in our most recent Form 10-K for the year ended December 31, 2009, incorporated by reference herein. See “Incorporation by Reference” on page S-6 of this Supplement. | |||||||||||||||||

The following table shows the amount of annual distributions per share to investors and the percentage that represented a return of capital and the percentage representing ordinary income as included in Note 1 to our audited consolidated financial statements in our most recent Form 10-K.

Year

Distributions

per Share

Percentage of

Distributions Classified as

Ordinary Income(1)

Percentage of

Distributions Classified as

Return of Capital(1)

2009

$

0.88

47

%

53

%

2008

$

0.51

42

%

58

%

| ||||||||||||||||||||

(1) |

|

| Percentages are based on earnings and profits of the Company as determined by federal income tax regulations. | |||||||||||||||||

S-3

As shown in the table above, for the years ended December 31, 2009 and 2008, 53% and 58%, respectively, of distributions made to investors represented a return of capital. The historical percentages may not be indicative of future return of capital percentages. We may use an unlimited amount of the offering proceeds to fund distributions in the future. Proceeds of the offering which are distributed are not available for investment in properties. Further, the payment of distributions from sources other than operating cash flow will decrease the cash available to invest in properties and will reduce the amount of distributions we may make in the future. See “Risk Factors”—“We may be unable to make distributions to our shareholders,” on page 28 of the prospectus, and “Our distributions to our shareholders have been sourced from operating cash flow and offering proceeds, and in the future we may fund distributions from offering proceeds or indebtedness, which (to the extent it occurs) will decrease our distributions in the future,” on page 16 of the prospectus. During the initial phase of our operations, we have had and may continue to have, due to the inherent delay between raising capital and investing that same capital in income producing real estate, a portion of our distributions funded from offering proceeds. Our objective in setting a distribution rate is to project a rate that will provide consistency over the life of the Company, taking into account acquisitions and capital improvements, ramp up of new properties and varying economic cycles. We anticipate that we may need to continue to use offering proceeds and cash from operations, and also utilize debt, to meet this objective. We evaluate the distribution rate on an ongoing basis and may make changes at any time if we feel the rate is not appropriate based on available cash resources. In May 2008, our Board of Directors established a policy for an annualized dividend rate of $0.88 per common share, payable in monthly distributions. Since there can be no assurance of our ability to acquire properties that provide income at this level, or that the properties already acquired will provide income at this level, there can be no assurance as to the classification or duration of distributions at the current rate. For the year ended December 31, 2009, as stated in Note 1 to our consolidated financial statements for that period, 53% of distributions made to investors represented a return of capital and the remaining 47% represented ordinary income. Proceeds of the offering which are distributed are not available for investment in properties. See “Risk Factors”—“We may be unable to make distributions to our shareholders,” on page 28 of the prospectus, and “Our distributions to our shareholders have been sourced from operating cash flow and offering proceeds, and in the future we may fund distributions from offering proceeds or indebtedness, which (to the extent it occurs) will decrease our distributions in the future,” on page 16 of the prospectus. Through July 31, 2010, we have received requests to redeem approximately 772,000 Units pursuant to our Unit Redemption Program for a total of $8.0 million. Through our last scheduled quarterly redemption date in 2010, July 20, 2010, we redeemed 100% of the redemption requests at an average per Unit redemption price of $10.30. We funded Unit redemptions for the periods noted above from the proceeds of dividends used to purchase additional Units under the Company’s best efforts offering of Units. Updated Risk Factor The following updated risk factor amends and replaces the current risk factor found on page 16 of our prospectus dated September 21, 2009. Our distributions to our shareholders have been sourced from operating cash flow and offering proceeds, and in the future we may fund distributions from offering proceeds or indebtedness, which (to the extent it occurs) will decrease our distributions in the future. Since we completed our minimum offering in May 2008 the Company has made monthly distributions to shareholders. We plan to continue to make such regular distributions. As a result, we have had, and early in our operations are more likely to have, a return of capital as a part of distributions to shareholders. This is because as proceeds are raised in the offering, it is not always possible immediately to invest them in real estate properties that generate our desired return on investment. There may be a “lag” or delay between the raising of offering proceeds and their investment in real estate properties. Persons who acquire Units relatively early in our offering, as S-4

compared with later investors, may receive a greater return of offering proceeds as part of the earlier distributions. In fiscal years 2009 and 2008, over half of our distributions to shareholders represented a return of capital. If investors receive different amounts of returns of offering proceeds as distributions based upon when they acquire Units, the investors will experience different rates of return on their invested capital and some investors may have less net cash per Unit invested after distributions than other investors. Further, offering proceeds that are returned to investors as part of distributions to them will not be available for investments in properties. The payment of distributions from sources other than operating cash flow will decrease the cash available to invest in properties and will reduce the amount of distributions we may make in the future. See “Plan of Distribution.” (Remainder of Page Intentionally Left Blank) S-5

We have elected to “incorporate by reference” certain information into this prospectus. By incorporating by reference, we are disclosing important information to you by referring you to documents we have filed separately with the Securities and Exchange Commission, or “SEC.” The following documents filed with the SEC are incorporated by reference in this prospectus (Commission File No. 333-147414), except for any document or portion thereof deemed to be “furnished” and not filed in accordance with SEC rules: • Annual Report on Form 10-K for the fiscal year ended December 31, 2009 filed with the SEC on March 5, 2010; • Definitive Proxy Statement filed on Schedule 14A filed with the SEC on April 2, 2010; • Quarterly report on Form 10-Q for the quarter ended March 31, 2010 filed with the SEC on May 5, 2010; • Quarterly report on Form 10-Q for the quarter ended June 30, 2010 filed with the SEC on August 4, 2010; • Current Report on Form 8-K/A filed with the SEC on October 10, 2008; includes the financial statements for the Tucson, Arizona Hilton Garden Inn Hotel and the required pro forma financial information; • Current Report on Form 8-K filed with the SEC on October 22, 2008; includes the financial statements for SCI Lewisville Hotel, Ltd. (previous owner of the Lewisville, Texas Hilton Garden Inn); SCI Duncanville Hotel, Ltd. (previous owner of the Duncanville, Texas Hilton Garden Inn) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on October 24, 2008; includes the financial statements for RSV Twinsburg Hotel, Ltd (previous owner of the Twinsburg, Ohio Hilton Garden Inn) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on October 24, 2008; includes the financial statements for Charlotte Lakeside Hotel, L.P. (previous owner of the Charlotte, North Carolina Homewood Suites); Santa Clarita Courtyard; Allen Stacy Hotel, Ltd. (previous owner of the Allen, Texas Hampton Inn & Suites) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on January 12, 2009; includes the financial statements for the Beaumont, Texas—Residence Inn by Marriott; Santa Clarita Hotels Portfolio; SCI Allen Hotel, Ltd. (previous owner of the Allen, Texas Hilton Garden Inn); Pueblo, Colorado Hampton Inn & Suites and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on January 12, 2009; includes the financial statements for the Bristol, Virginia—Courtyard Marriott and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on January 27, 2009; includes the financial statements for the Durham, North Carolina—Homewood Suites and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on January 27, 2009; includes the financial statements for RMRVH Jackson, LLC, CYRMR Jackson, LLC and VH Fort Lauderdale Investment Ltd (previous owners of the Jackson, Tennessee Courtyard; Jackson, Tennessee Hampton Inn & Suites and Fort Lauderdale, Florida Hampton Inn) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on January 27, 2009; includes the financial statements for RMRVH Jackson, LLC, CYRMR Jackson, LLC and VH Fort Lauderdale Investment Ltd (previous owners of the Jackson, Tennessee Courtyard; Jackson, Tennessee Hampton Inn & Suites and Fort Lauderdale, Florida Hampton Inn); Playhouse Square Hotel Associates and Playhouse Parking Associates, L.P. (previous owners of the Pittsburgh, Pennsylvania Hampton Inn) and the required pro forma financial information; S-6

• Current Report on Form 8-K filed with the SEC on April 15, 2009; includes the financial statements for Austin FRH, LTD, FRH Braker, LTD and RR Hotel Investment, LTD (previous owners of Round Rock, Texas Hampton Inn; Austin, Texas Homewood Suites and Austin, Texas Hampton Inn) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on April 15, 2009; includes the financial statements for Austin FRH, LTD, FRH Braker, LTD and RR Hotel Investment, LTD (previous owners of Round Rock, Texas Hampton Inn; Austin, Texas Homewood Suites and Austin, Texas Hampton Inn) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on September 1, 2009; includes the financial statements for Grove Street Orlando, LLC (previous owner of Orlando, Florida Fairfield Inn & Suites and Orlando, Florida SpringHill Suites) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on March 22, 2010; includes the financial statements for the Houston, Texas—Marriott Hotel and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on June 29, 2010; includes the financial statements for the Raymond Hotels Portfolio (which includes the Boise, Idaho Hampton Inn & Suites; Rogers, Arkansas Homewood Suites; St. Louis, Missouri Hampton Inn & Suites; Oklahoma City, Oklahoma Hampton Inn & Suites; Rogers, Arkansas Hampton Inn; St. Louis, Missouri Hampton Inn; and Kansas City, Missouri Hampton Inn), the Anchorage, Alaska—Embassy Suites Hotel and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on June 29, 2010; includes the financial statements for the Raymond Hotels Portfolio (which includes the Boise, Idaho Hampton Inn & Suites; Rogers, Arkansas Homewood Suites; St. Louis, Missouri Hampton Inn & Suites; Oklahoma City, Oklahoma Hampton Inn & Suites; Rogers, Arkansas Hampton Inn; St. Louis, Missouri Hampton Inn; and Kansas City, Missouri Hampton Inn) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on October 8, 2010; includes the financial statements for the Louisiana Hotels Portfolio (which includes the Lafayette, Louisiana Hilton Garden Inn and the West Monroe, Louisiana Hilton Garden Inn) and the required pro forma financial information; • The description of our Units contained in our Registration Statement filed on Form 8-A (File No. 000-53603), filed with the SEC on March 27, 2009; and • Current Reports on Form 8-K filed with the SEC on January 2, 2009, January 7, 2009, January 8, 2009, January 22, 2009, February 3, 2009, February 6, 2009, February 17, 2009, March 10, 2009, March 16, 2009, April 10, 2009, May 26, 2009, June 3, 2009, June 18, 2009, July 2, 2009, August 21, 2009, September 28, 2009, November 20, 2009, January 12, 2010, January 20, 2010, March 19, 2010, April 16, 2010, May 4, 2010, May 10, 2010, May 28, 2010, June 3, 2010, August 4, 2010, August 10, 2010, August 20, 2010, September 3, 2010, and September 15, 2010. All of the documents that we have incorporated by reference into this prospectus are available on the SEC’s website, www.sec.gov. In addition, these documents can be inspected and copied at the Public Reference Room maintained by the SEC at 100 F Street, NE, Washington, D.C. 20549. Copies also can be obtained by mail from the Public Reference Room at prescribed rates. Please call the SEC at (800) SEC-0330 for further information on the operation of the Public Reference Room. In addition, we will provide to each person, including any beneficial owner of our common shares, to whom this prospectus is delivered, a copy of any or all of the information that we have incorporated by reference into this prospectus, as supplemented, but not delivered with this prospectus. To receive a free copy of any of the documents incorporated by reference in this prospectus, other than exhibits, unless they are specifically incorporated by reference in those documents, call or write us at 814 East Main Street, Richmond, Virginia 23219, Attention: Kelly S-7

Clarke, (804) 344-8121. The documents also may be accessed on our website at www.applereitnine.com. The information relating to us contained in this prospectus does not purport to be comprehensive and should be read together with the information contained in the documents incorporated or deemed to be incorporated by reference in this prospectus. (Remainder of Page Intentionally Left Blank) S-8

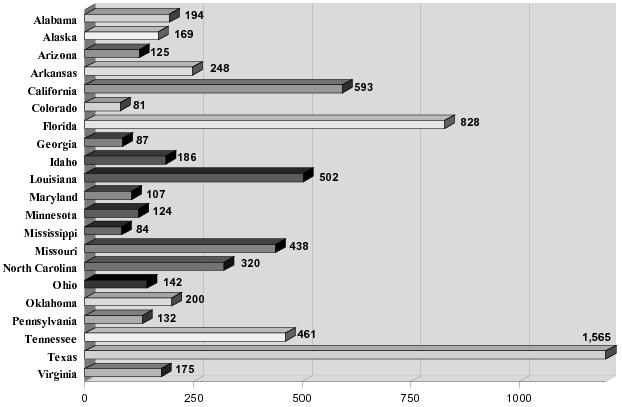

Summary of Real Estate Investments Since our prospectus dated September 21, 2009, we have purchased 23 additional hotels. Currently, through our subsidiaries, we own a total of 54 hotels. These hotels contain a total of 6,761 guest rooms. They were purchased for an aggregate gross purchase price of $933.2 million. Financial and operating information about our purchased hotels is provided in another section below. In addition, we currently own, through one of our subsidiaries, approximately 410 acres of land and land improvements located on 111 individual sites in the Ft. Worth, Texas area. The purchase price for this land was approximately $145 million. The land is leased to Chesapeake Energy Corporation for the production of natural gas. Under the ground lease, we receive monthly rental payments. Description of Real Estate Owned The map below shows the states in which our hotels are located, and the following charts summarize our room and franchise information. States in which Our Hotels are Located

S-9

Number of Guest Rooms by State

Type and Number of Hotel Franchises

S-10

Summary of Potential Acquisitions We have entered into, or caused one of our indirect wholly-owned subsidiaries to enter into, purchase contracts for 29 other hotels. These contracts are for direct hotel purchases. The following table summarizes the hotel and contract information: Hotel Location Franchise Date of Number of Gross 1. Holly Springs, North Carolina(a) Hampton Inn January 6, 2009 124 $ 14,880,000 2. Jacksonville, North Carolina Fairfield Inn & Suites December 11, 2009 79 7,800,000 3. Santa Ana, California(a) Courtyard February 1, 2010 155 24,800,000 4. Lafayette, Louisiana(a)(b) Spring Hill Suites March 29, 2010 103 10,232,110 5. Irving, Texas(c) Homewood Suites August 5, 2010 77 10,250,000 6. Tucson, Arizona(a)(b) TownePlace Suites August 10, 2010 124 15,851,974 7 El Paso, Texas(a)(b) Hilton Garden Inn August 10, 2010 145 19,973,526 8. Nashville, Tennessee(a) Home2 by Hilton August 13, 2010 110 15,400,000 9. Andover, Massachusetts SpringHill Suites August 30, 2010 136 6,500,000 10. Indianapolis, Indiana SpringHill Suites September 10, 2010 130 12,800,000 11. Mishawaka, Indiana Residence Inn September 10, 2010 106 13,700,000 12. Phoenix, Arizona Courtyard September 10, 2010 164 16,000,000 13. Phoenix, Arizona Residence Inn September 10, 2010 129 14,000,000 14. Lake Forest/Mettawa, Illinois Residence Inn September 10, 2010 130 23,500,000 15. Lake Forest/Mettawa, Illinois Hilton Garden Inn September 10, 2010 170 30,500,000 16. Austin, Texas Hilton Garden Inn September 10, 2010 117 16,000,000 17. Novi, Michigan Hilton Garden Inn September 10, 2010 148 16,200,000 18. Warrenville, Illinois Hilton Garden Inn September 10, 2010 135 22,000,000 19. Schaumburg, Illinois Hilton Garden Inn September 10, 2010 166 20,500,000 20. Salt Lake City, Utah SpringHill Suites September 10, 2010 143 17,500,000 21. Austin, Texas Fairfield Inn & Suites September 10, 2010 150 17,750,000 22. Austin, Texas Courtyard September 10, 2010 145 20,000,000 23. Chandler, Arizona Courtyard September 10, 2010 150 17,000,000 24. Chandler, Arizona Fairfield Inn & Suites September 10, 2010 110 12,000,000 25. Tampa, Florida Embassy Suites September 10, 2010 147 21,800,000 26. Philadelphia (Malvern), Pennsylvania (c) Courtyard October 1, 2010 127 21,000,000 27. Philadelphia (Collegeville), Pennsylvania Courtyard October 1, 2010 132 20,000,000 28. Texarkana, Texas (c) Hampton Inn & Suites October 18, 2010 81 9,100,000 29. Arlington, Texas Hampton Inn & Suites October 18, 2010 98 9,900,000 Total 3,731 $ 476,937,610

Purchase

Contract

Rooms

Purchase

Price

Notes for Table:

| ||||||||||||||||||||

(a) |

|

| The indicated hotels are currently under construction. The table shows the expected number of rooms upon hotel completion and the expected franchise. | |||||||||||||||||

| ||||||||||||||||||||

(b) |

| If the seller meets all of the conditions to closing, we are obligated to specifically perform under the purchase contract. As the property is under construction at this time, the seller has not met all conditions to closing. | ||||||||||||||||||

| ||||||||||||||||||||

(c) |

| Purchase contract for these hotels requires the assumption of loans secured by the hotels. Total outstanding principal is approximately $19.0 million. The loans have current interest rates of 5.83%, 6.50% and 6.90%, maturity dates of April 2017, October 2032 and July 2016, and require monthly payments of principal and interest on an amortized basis. | ||||||||||||||||||

In general, each purchase contract listed above required a deposit upon (or shortly after) execution. An additional deposit is typically due upon the expiration of the contract review period. If a closing occurs under a purchase contract, the initial and additional deposits are credited toward

S-11

the purchase price. If a closing does not occur because the seller fails to satisfy a condition to closing or breaches the purchase contract, the applicable deposits would be refunded to us. The total of both the initial and additional deposits for the purchase contracts listed above is approximately $32.9 million. For each purchase contract listed above, there are material conditions to closing that presently remain unsatisfied. Accordingly, there can be no assurance at this time that a closing will occur under any of these purchase contracts. On October 14, 2009, through one of our indirect wholly-owned subsidiaries, we entered into a ground lease for approximately one acre of land located in downtown Richmond, Virginia. The lease terminates on December 31, 2098, subject to our right to exercise two renewal periods of ten years each. We intend to use the land to build two nationally recognized brand hotels. Under the terms of the lease we have a “Study Period” to determine the viability of the hotels. We can terminate the lease for any reason during the Study Period, which originally ended on April 14, 2010. The Study Period was extended to April 2011. After the Study Period, the lease continues to be subject to various conditions, including but not limited to obtaining various permits, licenses, zoning variances and franchise approvals. If any of these conditions are not met we have the right to terminate the lease at any time. Rent payments are not required until we decide to begin construction on the hotels. Annual rent under the lease is $300,000 with adjustments throughout the lease term based on the Consumer Price Index. As there are many conditions to beginning construction on the hotels, there are no assurances that we will construct the hotels or continue the lease. Recent Terminations In December 2009 the Company terminated two purchase contracts for hotels in Hillsboro, Oregon. The contracts were initially entered into in October 2008. The seller was not able to begin construction of the hotels, and as a result the contracts were terminated by the Company and the initial aggregate deposit of $200,000 was returned to the Company. Source of Funds and Related Party Payments David Lerner Associates, Inc., Apple Suites Realty Group, Inc. and Apple Nine Advisors, Inc. earned the compensation and expense reimbursements shown below in connection with their services from inception through the period ending June 30, 2010 relating to our offering phase, acquisition phase and operations phase. David Lerner Associates, Inc. is not related to Apple Suites Realty Group, Inc. or Apple Nine Advisors, Inc. Apple Suites Realty Group, Inc. and Apple Nine Advisors, Inc. are owned by Glade M. Knight, our Chairman and Chief Executive Officer. As described on page 41 of our prospectus under the heading “Compensation” and as shown below, we pay certain fees and expenses as they are incurred, while others accrue and will be paid in future periods, subject in some cases to the achievement of performance criteria. We did not incur any amounts in connection with our disposition phase through June 30, 2010. Cumulative through June 30, 2010 Incurred Paid Accrued Offering Phase Selling commissions paid to David Lerner Associates, Inc. in connection with the offering $ 110,948,250 $ 110,948,250 $ — Marketing expense allowance paid to David Lerner Associates, Inc. in connection with the offering 36,982,750 36,982,750 — 147,931,000 147,931,000 — Acquisition Phase Acquisition commission paid to Apple Suites Realty Group, Inc. 18,037,000 18,037,000 — Operations Phase Asset management fee paid to Apple Nine Advisors, Inc. 1,516,000 1,516,000 — Reimbursement of costs paid to Apple Nine Advisors, Inc. 3,311,000 3,311,000 — S-12

Amendment to Our Unit Redemption Program On October 8, 2009, our Board of Directors adopted a resolution amending our Unit redemption program. The first full paragraph on page 128 of our prospectus describing the Unit redemption program is amended as follows: “If funds available for our Unit redemption program are not sufficient to accommodate all requests, Units will be redeemed as follows: first, pro rata as to redemptions upon the death or disability of a shareholder; next pro rata as to redemptions to shareholders who demonstrate, in the discretion of our board of directors, another involuntary exigent circumstance, such as bankruptcy; next pro rata as to redemptions to shareholders subject to a mandatory distribution requirement under such shareholder’s IRA; pro rata as to shareholders seeking redemption of all Units owned by them who beneficially or of record fewer than 100 Units; and, finally, pro rata as to other redemption requests. The board of directors, in its sole discretion, may choose to suspend or terminate the Unit redemption program or to reduce the number of Units purchased under the Unit redemption program if it determines the funds otherwise available to fund our Unit redemption program are needed for other purposes.” (Remainder of Page Intentionally Left Blank) S-13

SUMMARY OF CONTRACTS The following information updates the contract information included in our prospectus dated September 21, 2009 for our recently purchased hotels. These recent hotel purchases were funded by the proceeds from our ongoing best-efforts offering of Units. Ownership, Leasing and Management Summary Each of our recently purchased hotels has been leased to one of our indirect wholly-owned subsidiaries, as the lessee, under a separate hotel lease agreement. For simplicity, the applicable lessee will be referred to below as the “lessee.” Each hotel is managed under a separate management agreement between the applicable lessee and the manager. For simplicity, the applicable manager will be referred to below as the “manager.” The hotel lease agreements and the management agreements are among the contracts described in another section below. The table below specifies the franchise, hotel owner, lessee and manager for the hotels we have purchased since our prospectus dated September 21, 2009: Hotel Location Franchise(a) Hotel Lessee Manager 1. Baton Rouge, Louisiana SpringHill Suites Apple Nine Apple Nine Dimension 2. Johnson City, Tennessee Courtyard Sunbelt-CJT, Apple Nine LBAM-Investor 3. Houston, Texas Marriott Apple Nine Apple Nine Texas Western 4. Albany, Georgia Fairfield Inn & Suites Sunbelt-RAG, Apple Nine LBAM-Investor 5. Panama City, Florida TownePlace Suites Sunbelt-RPC, L.L.C. Apple Nine LBAM-Investor 6. Clovis, California Homewood Suites Apple Nine Apple Nine Dimension 7. Jacksonville, North Carolina TownePlace Suites Apple Nine Apple Nine LBAM-Investor 8. Miami, Florida Hampton Inn & Suites Apple Nine Apple Nine Dimension 9. Anchorage, Alaska Embassy Suites Apple Nine Apple Nine Stonebridge Realty 10. Boise, Idaho Hampton Inn & Suites Apple Nine Apple Nine Raymond 11. Rogers, Arkansas Homewood Suites Apple Nine Apple Nine Raymond 12. St. Louis, Missouri Hampton Inn & Suites Apple Nine Apple Nine Raymond 13. Oklahoma City, Oklahoma Hampton Inn & Suites Apple Nine Apple Nine Raymond 14. Fort Worth, Texas TownePlace Suites Apple Nine Apple Nine Texas 15. Lafayette, Louisiana Hilton Garden Inn Apple Nine Apple Nine LBAM-Investor S-14

FOR OUR RECENTLY PURCHASED PROPERTIES

Owner/Lessor

Hospitality

Ownership, Inc.

Hospitality

Management, Inc.

Development

Two, LLC

L.L.C.

Hospitality

Management, Inc.

Group, L.L.C.(b)

Hospitality

Ownership, Inc.

Hospitality

Texas Services II, Inc.

Management

Partners, L.P.(b)

L.L.C.

Hospitality

Management, Inc.

Group, L.L.C.(b)

Hospitality

Management, Inc.

Group, L.L.C.(b)

Hospitality

Ownership, Inc.

Hospitality

Management, Inc.

Development

Two, LLC

North

Carolina, L.P.

Hospitality

Management, Inc.

Group, L.L.C.

Hospitality

Ownership, Inc.

Hospitality

Management, Inc.

Development

Two, LLC

Hospitality

Ownership, Inc.

Hospitality

Management, Inc.

Advisors, Inc.(b)

Hospitality

Ownership, Inc.

Hospitality

Management, Inc.

Management

Company, Inc.(b)

Hospitality

Ownership, Inc.

Hospitality

Management, Inc.

Management

Company, Inc.(b)

Missouri, LLC

Hospitality

Management, Inc.

Management

Company, Inc.(b)

Oklahoma, LLC

Hospitality

Management, Inc.

Management

Company, Inc.(b)

Hospitality

Ownership, Inc.

Hospitality

Texas Services II, Inc.

Western

Management

Partners, L.P.(b)

Louisiana, LLC

Hospitality

Management, Inc.

Group, L.L.C.

Hotel Location Franchise(a) Hotel Lessee Manager 16. West Monroe, Louisiana Hilton Garden Inn Apple Nine Apple Nine Intermountain 17. Silver Spring, Maryland Hilton Garden Inn Apple Nine Apple Nine White Lodging 18. Rogers, Arkansas Hampton Inn Apple Nine Apple Nine Raymond 19. St. Louis, Missouri Hampton Inn Apple Nine Apple Nine Raymond 20. Kansas City, Missouri Hampton Inn Apple Nine Apple Nine Raymond 21. Alexandria, Louisiana Courtyard Sunbelt-CAL, LLC Apple Nine LBAM-Investor 22. Grapevine, Texas Hilton Garden Inn Apple Nine Apple Nine Texas 23. Nashville, Tennessee Hilton Garden Inn Apple Nine Apple Nine Vista Host, Inc.

Owner/Lessor

Louisiana, LLC

Hospitality

Management, Inc.

Management, LLC

Hospitality

Ownership, Inc.

Hospitality

Management, Inc.

Services

Corporation

SPE Rogers, Inc.

Services Rogers, Inc.

Management

Company, Inc.(b)

St. Louis, LLC

Services

St. Louis, Inc.

Management

Company, Inc.(b)

Kansas City, LLC

Services

Kansas City, Inc.

Management

Company, Inc.(b)

Hospitality

Management, Inc.

Group, L.L.C.(b)

Hospitality

Ownership, Inc.

Hospitality Texas

Services II, Inc.

Western

Management

Partners, L.P.

Hospitality

Ownership, Inc.

Hospitality

Management, Inc.

Notes for Table:

| ||||||||||||||||||||

(a) |

|

| All brand and trade names, logos or trademarks contained, or referred to, in this prospectus supplement are the properties of their respective owners. These references shall not in any way be construed as participation by, or endorsement of, our offering by any of our franchisors or managers. | |||||||||||||||||

| ||||||||||||||||||||

(b) |

| The hotel specified was purchased from an affiliate of the indicated manager. | ||||||||||||||||||

We have no material relationship or affiliation with the hotel sellers or managers, except for the relationship resulting from our purchases, our management agreements for the hotels we own and any related documents.

Hotel Lease Agreements

Each of our recently purchased hotels is covered by a separate hotel lease agreement between the owner (one of our indirect wholly-owned subsidiaries) and the applicable lessee (another one of our indirect wholly-owned subsidiaries, as specified in a previous section). Each lease provides for an initial term of 10 years. The applicable lessee has the option to extend its lease term for two additional five-year periods, provided it is not in default at the end of the prior term or at the time the option is exercised.

Each lease provides for annual base rent and percentage rent. The annual base rent is payable in advance in equal monthly installments and will be adjusted each year in proportion to the Consumer Price Index (based on the U.S. City Average). Shown below are the annual base rent and the lease commencement date for the hotels we have purchased since our prospectus dated September 21, 2009:

|

|

|

|

|

|

|

|

| |||||

| Hotel Location | Franchise | Annual | Date of Lease | |||||||||

1. | Baton Rouge, Louisiana | SpringHill Suites |

|

| $ |

| 974,274 | September 25, 2009 | |||||

2. | Johnson City, Tennessee | Courtyard |

|

| 723,153 | September 25, 2009 | |||||||

3. | Houston, Texas | Marriott |

|

| 2,367,460 | January 8, 2010 | |||||||

4. | Albany, Georgia | Fairfield Inn & Suites |

|

| 698,338 | January 14, 2010 | |||||||

S-15

Hotel Location Franchise Annual Date of Lease 5. Panama City, Florida TownePlace Suites $ 695,825 January 19, 2010 6. Clovis, California Homewood Suites 546,980 February 2, 2010 7. Jacksonville, North Carolina TownePlace Suites 1,046,227 February 16, 2010 8. Miami, Florida Hampton Inn & Suites 1,188,311 April 9, 2010 9. Anchorage, Alaska Embassy Suites 3,065,571 April 30, 2010 10. Boise, Idaho Hampton Inn & Suites 1,769,990 April 30, 2010 11. Rogers, Arkansas Homewood Suites 722,695 April 30, 2010 12. St. Louis, Missouri Hampton Inn & Suites 1,309,803 April 30, 2010 13. Oklahoma City, Oklahoma Hampton Inn & Suites 2,547,805 May 28, 2010 14. Fort Worth, Texas TownePlace Suites 1,436,528 July 19, 2010 15. Lafayette, Louisiana Hilton Garden Inn 1,602,354 July 30, 2010 16. West Monroe, Louisiana Hilton Garden Inn 1,428,300 July 30, 2010 17. Silver Spring, Maryland Hilton Garden Inn 991,262 July 30, 2010 18. Rogers, Arkansas Hampton Inn 805,911 August 31, 2010 19. St. Louis, Missouri Hampton Inn 1,778,985 August 31, 2010 20. Kansas City, Missouri Hampton Inn 1,072,218 August 31, 2010 21. Alexandria, Louisiana Courtyard 838,730 September 15, 2010 22. Grapevine, Texas Hilton Garden Inn 1,508,970 September 24, 2010 23. Nashville, Tennessee Hilton Garden Inn 3,084,122 September 30, 2010 The annual percentage rent depends on a formula that compares fixed “suite revenue breakpoints” with a portion of “suite revenue,” which is equal to gross revenue from guest rentals less sales and room taxes and credit card fees. The suite revenue breakpoints will be adjusted each year in proportion to the Consumer Price Index (based on the U.S. City Average). Specifically, the annual percentage rent is equal to the sum of (a) 17% of all suite revenue for the year, up to the applicable suite revenue breakpoint; plus (b) 55% of the suite revenue for the year in excess of the applicable suite revenue breakpoint, as reduced by base rent paid for the year. Management Agreements Each of our hotels is being managed by the manager under a separate management agreement between the manager and the applicable lessee (which is one of our indirect wholly-owned subsidiaries, as specified in the previous section). The manager is responsible for managing and supervising the daily operations of the hotel and for collecting revenues for the benefit of the applicable lessee. The fees and other terms of these agreements are the result of commercial negotiations between otherwise unrelated parties. We believe that such fees and terms are appropriate for the hotels and the markets in which they operate. Franchise Agreements In general, for our hotels franchised by Marriott International, Inc. or one of its affiliates, there is a relicensing franchise agreement between the applicable lessee (as specified in a previous section) and Marriott International, Inc. or an affiliate. Each relicensing franchise agreement provides for the payment of royalty fees and marketing contributions to the franchisor. A percentage of gross room revenues is used to determine these payments. In addition, we have caused Apple Nine Hospitality, Inc. or another one of our subsidiaries to provide a separate guaranty of the payment and performance of the applicable lessee under the relicensing franchise agreement. S-16

Base Rent

Commencement

For the hotels franchised by Hilton Worldwide or one of its affiliates, there is a franchise license agreement between the applicable lessee and Hilton Worldwide or an affiliate. Each franchise license agreement provides for the payment of royalty fees and program fees to the franchisor. A percentage of gross room revenues is used to determine these payments. Apple Nine Hospitality, Inc. or another one of our subsidiaries has guaranteed the payment and performance of the lessee under the applicable franchise license agreement. The fees and other terms of these agreements are the result of commercial negotiations between otherwise unrelated parties, and we believe that such fees and terms are appropriate for the hotels and the markets in which they operate. These agreements may be terminated for various reasons, including failure by the applicable lessee to operate in accordance with the standards, procedures and requirements established by the franchisors. FINANCIAL AND OPERATING INFORMATION Our hotels offer guest rooms and suites, together with related amenities, that are consistent with their operations. The hotels are located in developed or developing areas and in competitive markets. We believe the hotels are well-positioned to compete in their markets based on location, amenities, rate structure and franchise affiliation. In the opinion of management, each hotel is adequately covered by insurance. The following tables present further information about the hotels we have purchased: Table 1. General Information Hotel Location Franchise Number Gross Average Federal Purchase Date 1. Tucson, Arizona Hilton Garden Inn 125 $ 18,375,000 $120-149 $ 17,397,150 July 31, 2008 2. Charlotte, North Carolina Homewood Suites 112 5,750,000 129-189 4,729,410 September 24, 2008 3. Santa Clarita, California Courtyard 140 22,700,000 129-209 18,243,805 September 24, 2008 4. Allen, Texas Hampton Inn & Suites 103 12,500,000 144-159 11,100,086 September 26, 2008 5. Twinsburg, Ohio Hilton Garden Inn 142 17,792,440 134-161 16,387,690 October 7, 2008 6. Lewisville, Texas Hilton Garden Inn 165 28,000,000 149-176 24,529,875 October 16, 2008 7. Duncanville, Texas Hilton Garden Inn 142 19,500,000 143-199 17,779,620 October 21, 2008 8. Santa Clarita, California Hampton Inn 128 17,129,348 109 15,358,348 October 29, 2008 9. Santa Clarita, California Residence Inn 90 16,599,578 139-199 14,118,232 October 29, 2008 10. Santa Clarita, California Fairfield Inn 66 9,337,262 89-119 7,517,608 October 29, 2008 11. Beaumont, Texas(c) Residence Inn 133 16,900,000 159-179 15,752,641 October 29, 2008 12. Pueblo, Colorado Hampton Inn & Suites 81 8,025,000 149-199 7,157,264 October 31, 2008 13. Allen, Texas Hilton Garden Inn 150 18,500,000 129-149 16,405,653 October 31, 2008 14. Bristol, Virginia Courtyard 175 18,650,000 119-189 17,115,637 November 7, 2008 15. Durham, North Carolina Homewood Suites 122 19,050,000 144-209 17,846,600 December 4, 2008 16. Hattiesburg, Mississippi(c) Residence Inn 84 9,793,028 139-149 8,910,083 December 11, 2008 17. Jackson, Tennessee Courtyard 94 15,200,000 129-139 14,240,000 December 16, 2008 18. Jackson, Tennessee Hampton Inn & Suites 83 12,600,000 119-149 11,926,000 December 30, 2008 19. Fort Lauderdale, Florida Hampton Inn 109 19,290,434 149-169 18,080,922 December 31, 2008 20. Pittsburgh, Pennsylvania Hampton Inn 132 20,457,777 129-159 18,019,257 December 31, 2008 21. Frisco, Texas(c) Hilton Garden Inn 102 15,050,000 99-209 12,608,112 December 31, 2008 22. Round Rock, Texas Hampton Inn 93 11,500,000 119-139 10,658,652 March 6, 2009 23. Panama City, Florida(c) Hampton Inn & Suites 95 11,600,000 159-189 9,995,450 March 12, 2009 24. Austin, Texas Homewood Suites 97 17,700,000 149-189 15,866,419 April 14, 2009 25. Austin, Texas Hampton Inn 124 18,000,000 129-149 16,587,854 April 14, 2009 26. Dothan, Alabama(c) Hilton Garden Inn 104 11,600,836 119-169 10,564,205 June 1, 2009 27. Troy, Alabama(c) Courtyard 90 8,696,456 109-159 8,129,696 June 18, 2009 S-17

FOR OUR PURCHASED

PROPERTIES

of

Rooms/

Suites

Purchase

Price

Daily

Rate

(Price)

per

Room/

Suite(a)

Income Tax

Basis for

Depreciable

Real

Property

Component

Of Hotel(b)

Hotel Location Franchise Number Gross Average Federal Purchase Date 28. Orlando, Florida (c) Fairfield Inn & Suites 200 $ 25,800,000 89-109 $ 22,650,000 July 1, 2009 29. Orlando, Florida(c) SpringHill Suites 200 29,000,000 94-109 25,850,000 July 1, 2009 30. Clovis, California(c) Hampton Inn & Suites 86 11,150,000 99-139 9,860,000 July 31, 2009 31. Rochester, Minnesota(c) Hampton Inn & Suites 124 14,136,000 109-119 13,219,780 August 3, 2009 32. Baton Rouge, Louisiana(c) SpringHill Suites 119 15,100,000 99-134 13,820,000 September 25, 2009 33. Johnson City, Tennessee(c) Courtyard 90 9,879,788 119-169 8,774,788 September 25, 2009 34. Houston, Texas(c) Marriott 206 50,750,000 199-279 46,605,026 January 8, 2010 35. Albany, Georgia(c) Fairfield Inn & Suites 87 7,919,790 109 7,070,116 January 14, 2010 36. Panama City, Florida (c) TownePlace Suites 103 10,640,346 84-99 9,732,274 January 19, 2010 37. Clovis, California(c) Homewood Suites 83 12,435,000 119-139 10,932,060 February 2, 2010 38. Jacksonville, North Carolina TownePlace Suites 86 9,200,000 119-129 8,568,200 February 16, 2010 39. Miami, Florida Hampton Inn & Suites 121 11,900,000 139-159 9,927,800 April 9, 2010 40. Anchorage, Alaska Embassy Suites 169 42,000,000 174-299 39,040,017 April 30, 2010 41. Boise, Idaho Hampton Inn & Suites 186 22,370,000 119-179 21,034,240 April 30, 2010 42. Rogers, Arkansas Homewood Suites 126 10,900,000 109-139 9,514,300 April 30, 2010 43. St. Louis, Missouri Hampton Inn & Suites 126 16,000,000 139-149 15,240,730 April 30, 2010 44. Oklahoma City, Oklahoma Hampton Inn & Suites 200 32,656,898 144-199 31,227,392 May 28, 2010 45. Fort Worth, Texas(c) TownePlace Suites 140 18,434,940 139-169 16,353,092 July 19, 2010 46. Lafayette, Louisiana Hilton Garden Inn 153 17,261,340 129-149 17,261,340 July 30, 2010 47. West Monroe, Louisiana Hilton Garden Inn 134 15,638,660 133-153 14,806,866 July 30, 2010 48. Silver Spring, Maryland(c) Hilton Garden Inn 107 17,400,000 129-135 16,039,113 July 30, 2010 49. Rogers, Arkansas Hampton Inn 122 9,600,000 109-129 8,614,200 August 31, 2010 50. St. Louis, Missouri Hampton Inn 190 23,000,000 129-139 21,210,750 August 31, 2010 51. Kansas City, Missouri Hampton Inn 122 10,130,000 119-129 9,395,000 August 31, 2010 52. Alexandria, Louisiana(c) Courtyard 96 9,915,069 129 8,816,500 September 15, 2010 53. Grapevine, Texas Hilton Garden Inn 110 17,000,000 159-189 15,478,120 September 24, 2010 54. Nashville, Tennessee Hilton Garden Inn 194 42,667,000 144-194 38,729,591 September 30, 2010 Total 6,761 $ 933,181,990

of

Rooms/

Suites

Purchase

Price

Daily

Rate

(Price)

per

Room/

Suite(a)

Income Tax

Basis for

Depreciable

Real

Property

Component

Of Hotel(b)

Notes for Table 1:

| ||||||||||||||||||||

(a) |

|

| The amounts shown are subject to change, and exclude discounts that may be offered to corporate, frequent and other select customers. | |||||||||||||||||

| ||||||||||||||||||||

(b) |

| The depreciable life is 39 years (or less, as may be permitted by federal tax laws) using the straight-line method. The modified accelerated cost recovery system will be used for the hotel’s personal property component. | ||||||||||||||||||

| ||||||||||||||||||||

(c) |

| The date that the hotel was acquired was the date the hotel began operations. | ||||||||||||||||||

S-18

Table 2. Loan Information(a) Hotel Franchise Assumed Annual Maturity 1. Allen, Texas Hilton Garden Inn $ 10,786,698 5.37 % October 2015 2. Bristol, Virginia Courtyard 9,767,131 6.59 % August 2016 3. Duncanville, Texas Hilton Garden Inn 13,965,858 5.88 % May 2017 4. Round Rock, Texas Hampton Inn 4,175,225 5.95 % May 2016 5. Austin, Texas Homewood Suites 7,555,797 5.99 % March 2016 6. Austin, Texas Hampton Inn 7,553,015 5.95 % March 2016 7. Rogers, Arkansas Hampton Inn 8,336,824 5.20 % September 2015 8. St. Louis, Missouri Hampton Inn 13,914,689 5.30 % September 2015 9. Kansas City, Missouri Hampton Inn 6,517,413 5.45 % October 2015 $ 82,572,650

Principal

Balance of Loan

Interest

Rate

Date

Note for Table 2:

| ||||||||||||||||||||

(a) |

|

| This table summarizes loans that (i) pre-dated our purchase, (ii) are secured by our hotels, and (iii) were assumed by our purchasing subsidiary. Each loan provides for monthly payments of principal and interest on an amortized basis. | |||||||||||||||||

Table 3. Operating Information(a)

PART A

Hotel Location

Franchise

Avg. Daily Occupancy Rates (%)

2005

2006

2007

2008

2009

1.

Tucson, Arizona

Hilton Garden Inn

—

—

—

61

%

68

%

2.

Charlotte, North Carolina

Homewood Suites

78

%

76

%

71

%

53

%

52

%

3.

Santa Clarita, California

Courtyard

—

—

51

%

61

%

66

%

4.

Allen, Texas

Hampton Inn & Suites

—

51

%

68

%

69

%

60

%

5.

Twinsburg, Ohio

Hilton Garden Inn

64

%

63

%

66

%

66

%

62

%

6.

Lewisville, Texas

Hilton Garden Inn

—

—

42

%

63

%

61

%

7.

Duncanville, Texas

Hilton Garden Inn

59

%

64

%

65

%

66

%

58

%

8.

Santa Clarita, California

Hampton Inn

83

%

82

%

78

%

70

%

63

%

9.

Santa Clarita, California

Residence Inn

91

%

91

%

89

%

85

%

76

%

10.

Santa Clarita, California

Fairfield Inn

89

%

88

%

83

%

81

%

79

%

11.

Beaumont, Texas

Residence Inn

—

—

—

85

%

76

%

12.

Pueblo, Colorado

Hampton Inn & Suites

61

%

67

%

74

%

70

%

60

%

13.

Allen, Texas

Hilton Garden Inn

73

%

73

%

68

%

65

%

53

%

14.

Bristol, Virginia

Courtyard

54

%

65

%

67

%

57

%

61

%

15.

Durham, North Carolina

Homewood Suites

67

%

73

%

73

%

69

%

59

%

16.

Hattiesburg, Mississippi

Residence Inn

—

—

—

—

75

%

17.

Jackson, Tennessee

Courtyard

—

—

—

52

%

67

%

18.

Jackson, Tennessee

Hampton Inn & Suites

—

—

80

%

87

%

80

%

19.

Fort Lauderdale, Florida

Hampton Inn

85

%

85

%

89

%

85

%

73

%

20.

Pittsburgh, Pennsylvania

Hampton Inn

76

%

73

%

80

%

81

%

73

%

21.

Frisco, Texas

Hilton Garden Inn

—

—

—

—

45

%

22.

Round Rock, Texas

Hampton Inn

73

%

81

%

85

%

80

%

72

%

23.

Panama City, Florida

Hampton Inn & Suites

—

—

—

—

44

%

24.

Austin, Texas

Homewood Suites

82

%

89

%

80

%

81

%

77

%

25.

Austin, Texas

Hampton Inn

76

%

82

%

80

%

77

%

70

%

26.

Dothan, Alabama

Hilton Garden Inn

—

—

—

—

46

%

27.

Troy, Alabama

Courtyard

—

—

—

—

36

%

28.

Orlando, Florida

Fairfield Inn & Suites

—

—

—

—

56

%

29.

Orlando, Florida

SpringHill Suites

—

—

—

—

65

%

30.

Clovis, California

Hampton Inn & Suites

—

—

—

—

36

%

31.

Rochester, Minnesota

Hampton Inn & Suites

—

—

—

—

28

%

S-19

Hotel Location Franchise Avg. Daily Occupancy Rates (%) 2005 2006 2007 2008 2009 32. Baton Rouge, Louisiana SpringHill Suites — — — — 32 % 33. Johnson City, Tennessee Courtyard — — — — 49 % 34. Houston, Texas Marriott — — — — — 35. Albany, Georgia Fairfield Inn & Suites — — — — — 36. Panama City, Florida TownePlace Suites — — — — — 37. Clovis, California Homewood Suites — — — — — 38. Jacksonville, North Carolina TownePlace Suites — — — 83 % 90 % 39. Miami, Florida Hampton Inn & Suites 87 % 83 % 86 % 85 % 77 % 40. Anchorage, Alaska Embassy Suites — — — 69 % 72 % 41. Boise, Idaho Hampton Inn & Suites — — 64 % 71 % 73 % 42. Rogers, Arkansas Homewood Suites — 15 % 51 % 64 % 58 % 43. St. Louis, Missouri Hampton Inn & Suites — 72 % 76 % 74 % 75 % 44. Oklahoma City, Oklahoma Hampton Inn & Suites — — — — 75 % 45. Fort Worth, Texas TownePlace Suites — — — — — 46. Lafayette, Louisiana Hilton Garden Inn — 68 % 74 % 75 % 65 % 47. West Monroe, Louisiana Hilton Garden Inn — — 55 % 68 % 70 % 48. Silver Spring, Maryland Hilton Garden Inn — — — — — 49. Rogers, Arkansas Hampton Inn 66 % 66 % 59 % 62 % 60 % 50. St. Louis, Missouri Hampton Inn 63 % 65 % 67 % 67 % 71 % 51. Kansas City, Missouri Hampton Inn 77 % 79 % 79 % 77 % 73 % 52. Alexandria, Louisiana Courtyard — — — — — 53. Grapevine, Texas Hilton Garden Inn — — — — 44 % 54. Nashville, Tennessee Hilton Garden Inn — — — — 65 % PART B Hotel Location Franchise Revenue per Available Room/Suite ($) 2005 2006 2007 2008 2009 1. Tucson, Arizona Hilton Garden Inn — — — $ 65 $ 73 2. Charlotte, North Carolina Homewood Suites $ 55 $ 62 $ 67 $ 51 $ 46 3. Santa Clarita, California Courtyard — — $ 59 $ 70 $ 68 4. Allen, Texas Hampton Inn & Suites — $ 53 $ 76 $ 79 $ 63 5. Twinsburg, Ohio Hilton Garden Inn $ 62 $ 64 $ 69 $ 71 $ 63 6. Lewisville, Texas Hilton Garden Inn — — $ 50 $ 72 $ 65 7. Duncanville, Texas Hilton Garden Inn $ 56 $ 66 $ 73 $ 75 $ 59 8. Santa Clarita, California Hampton Inn $ 83 $ 91 $ 86 $ 72 $ 60 9. Santa Clarita, California Residence Inn $ 110 $ 120 $ 120 $ 110 $ 89 10. Santa Clarita, California Fairfield Inn $ 82 $ 95 $ 88 $ 78 $ 68 11. Beaumont, Texas Residence Inn — — — $ 133 $ 91 12. Pueblo, Colorado Hampton Inn & Suites $ 42 $ 51 $ 70 $ 72 $ 54 13. Allen, Texas Hilton Garden Inn $ 72 $ 77 $ 76 $ 74 $ 58 14. Bristol, Virginia Courtyard $ 50 $ 58 $ 66 $ 66 $ 65 15. Durham, North Carolina Homewood Suites $ 71 $ 81 $ 88 $ 85 $ 65 16. Hattiesburg, Mississippi Residence Inn — — — — $ 71 17. Jackson, Tennessee Courtyard — — — $ 58 $ 71 18. Jackson, Tennessee Hampton Inn & Suites — — $ 92 $ 105 $ 95 19. Fort Lauderdale, Florida Hampton Inn $ 90 $ 102 $ 112 $ 105 $ 85 20. Pittsburgh, Pennsylvania Hampton Inn $ 71 $ 75 $ 90 $ 101 $ 94 21. Frisco, Texas Hilton Garden Inn — — — — $ 47 22. Round Rock, Texas Hampton Inn $ 61 $ 72 $ 81 $ 85 $ 73 23. Panama City, Florida Hampton Inn & Suites — — — — $ 42 24. Austin, Texas Homewood Suites $ 79 $ 96 $ 103 $ 110 $ 97 25. Austin, Texas Hampton Inn $ 63 $ 74 $ 83 $ 93 $ 75 26. Dothan, Alabama Hilton Garden Inn — — — — $ 47 27. Troy, Alabama Courtyard — — — — $ 30 28. Orlando, Florida Fairfield Inn & Suites — — — — $ 37 S-20

Hotel Location Franchise Revenue per Available Room/Suite ($) 2005 2006 2007 2008 2009 29. Orlando, Florida SpringHill Suites — — — — $ 48 30. Clovis, California Hampton Inn & Suites — — — — $ 35 31. Rochester, Minnesota Hampton Inn & Suites — — — — $ 23 32. Baton Rouge, Louisiana SpringHill Suites — — — — $ 27 33. Johnson City, Tennessee Courtyard — — — — $ 42 34. Houston, Texas Marriott — — — — — 35. Albany, Georgia Fairfield Inn & Suites — — — — — 36. Panama City, Florida TownePlace Suites — — — — — 37. Clovis, California Homewood Suites — — — — — 38. Jacksonville, North Carolina TownePlace Suites — — — $ 79 $ 88 39. Miami, Florida Hampton Inn & Suites $ 79 $ 92 $ 108 $ 105 $ 80 40. Anchorage, Alaska Embassy Suites — — — $ 122 $ 111 41. Boise, Idaho Hampton Inn & Suites — — $ 65 $ 76 $ 72 42. Rogers, Arkansas Homewood Suites — $ 17 $ 59 $ 58 $ 53 43. St. Louis, Missouri Hampton Inn & Suites — $ 76 $ 90 $ 86 $ 79 44. Oklahoma City, Oklahoma Hampton Inn & Suites — — — — $ 83 46. Fort Worth, Texas TownePlace Suites — — — — — 46. Lafayette, Louisiana Hilton Garden Inn — $ 69 $ 80 $ 89 $ 74 47. West Monroe, Louisiana Hilton Garden Inn — — $ 57 $ 69 $ 75 48. Silver Spring, Maryland Hilton Garden Inn — — — — — 49. Rogers, Arkansas Hampton Inn $ 66 $ 70 $ 64 $ 66 $ 57 50. St. Louis, Missouri Hampton Inn $ 64 $ 65 $ 73 $ 72 $ 75 51. Kansas City, Missouri Hampton Inn $ 66 $ 72 $ 78 $ 77 $ 67 52. Alexandria, Louisiana Courtyard — — — — — 53. Grapevine, Texas Hilton Garden Inn — — — — $ 57 54. Nashville, Tennessee Hilton Garden Inn — — — — $ 69

Note for Table 3

| ||||||||||||||||||||

(a) |

|

| Operating data is presented for the last five years (or since the beginning of hotel operations). Hotels with no data for a period were under construction and not open at that time. The first year of data for a hotel reflects results only for the period of time open and may not be a reflection of results once established in its market. See Table 1. General Information on page S-17 for the date the hotel was acquired. | |||||||||||||||||

Table 4. Tax and Related Information

Hotel Location

Franchise

Tax Year

Real

Property

Tax Rate(f)

Real

Property

Tax

1.

Tucson, Arizona

Hilton Garden Inn

2009(a

)

3.0

%

$

182,214

2.

Charlotte, North Carolina

Homewood Suites

2009(a

)

1.3

%

75,716

3.

Santa Clarita, California

Courtyard

2009(b

)

1.2

%

244,355

4.

Allen, Texas

Hampton Inn & Suites

2009(a

)

2.4

%

165,942

5.

Twinsburg, Ohio

Hilton Garden Inn

2009(a

)

2.0

%

206,372

6.

Lewisville, Texas

Hilton Garden Inn

2009(a

)

2.3

%

173,620

7.

Duncanville, Texas

Hilton Garden Inn

2009(a

)

2.7

%

264,406

8.

Santa Clarita, California

Hampton Inn

2009(b

)

1.3

%

204,837

9.

Santa Clarita, California

Residence Inn

2009(b

)

1.3

%

140,814

10.

Santa Clarita, California

Fairfield Inn

2009(b

)

1.3

%

103,264

11.

Beaumont, Texas

Residence Inn

2009(a

)

2.6

%

266,990

12.

Pueblo, Colorado

Hampton Inn & Suites

2009(a

)

2.6

%

68,945

13.

Allen Texas

Hilton Garden Inn

2009(a

)

2.4

%

245,621

14.

Bristol, Virginia

Courtyard

2009(a

)

0.9

%

61,125

15.

Durham, North Carolina

Homewood Suites

2009(a

)

1.2

%

135,546

S-21

Hotel Location Franchise Tax Year Real Real 16. Hattiesburg, Mississippi Residence Inn 2009(a ) 2.3 % $ 119,504 17. Jackson, Tennessee Courtyard 2009(a ) 1.8 % 102,240 18. Jackson, Tennessee Hampton Inn & Suites 2009(a ) 1.8 % 78,504 19. Fort Lauderdale, Florida Hampton Inn 2009(a ) 2.0 % 208,760 20. Pittsburgh, Pennsylvania Hampton Inn 2009(a ) 2.9 % 229,625 21. Frisco, Texas Hilton Garden Inn 2009(a ) 2.2 % 249,005 22. Round Rock, Texas Hampton Inn 2009(a ) 2.4 % 148,293 23. Panama City, Florida Hampton Inn & Suites 2009(a )(e) 1.1 % 8,211 24. Austin, Texas Homewood Suites 2009(a ) 2.2 % 210,672 25. Austin, Texas Hampton Inn 2009(a ) 2.2 % 226,426 26. Dothan, Alabama Hilton Garden Inn 2009(c )(e) 3.3 % 6,831 27. Troy, Alabama Courtyard 2009(c )(e) 4.1 % 3,663 28. Orlando, Florida Fairfield Inn & Suites 2009(a )(e) 1.7 % 63,806 29. Orlando, Florida SpringHill Suites 2009(a )(e) 3.2 % 8,360 30. Clovis, California Hampton Inn & Suites 2009(b )(e) 1.2 % 40,312 31. Rochester, Minnesota Hampton Inn & Suites 2009(a )(e) 1.5 % 2,088 32. Baton Rouge, Louisiana SpringHill Suites 2009(a )(e) 10.7 % 22,454 33. Johnson City, Tennessee Courtyard 2009(a )(e) 1.4 % 14,962 34. Houston, Texas Marriott 2009(a )(e) 2.8 % 200,498 35. Albany, Georgia Fairfield Inn & Suites 2009(a )(e) 4.0 % 15,302 36. Panama City, Florida TownePlace Suites 2009(a )(e) 1.5 % 5,719 37. Clovis, California Homewood Suites 2009(b )(e) 1.2 % 12,458 38. Jacksonville, North Carolina TownePlace Suites 2009(a ) 1.2 % 42,741 39. Miami, Florida Hampton Inn & Suites 2009(a ) 1.9 % 165,510 40. Anchorage, Alaska Embassy Suites 2009(a ) 1.3 % 328,298 41. Boise, Idaho Hampton Inn & Suites 2009(a ) 1.5 % 167,968 42. Rogers, Arkansas Homewood Suites 2009(a ) 5.3 % 88,545 43. St. Louis, Missouri Hampton Inn & Suites 2009(a ) 8.3 % 245,869 44. Oklahoma City, Oklahoma Hampton Inn & Suites 2009(a ) 11.3 % 16,171 45. Fort Worth, Texas TownePlace Suites 2010(a )(e) 2.8 % 142,557 46. Lafayette, Louisiana Hilton Garden Inn 2009(a ) 10 % 44,067 47. West Monroe, Louisiana Hilton Garden Inn 2009(a ) 8 % 87,362 48. Silver Spring, Maryland Hilton Garden Inn 2010(d )(e) 1 % 11,365 49. Rogers, Arkansas Hampton Inn 2009(a ) 5.3 % 71,742 50. St. Louis, Missouri Hampton Inn 2009(a ) 9.3 % 103,588 51. Kansas City, Missouri Hampton Inn 2009(a ) 10.2 % 121,769 52. Alexandria, Louisiana Courtyard 2009(a )(e) 11.9 % 7,663 53. Grapevine, Texas Hilton Garden Inn 2009(a )(e) 2.3 % 132,601 54. Nashville, Tennessee Hilton Garden Inn 2009(a )(e) 2.8 % 262,297

Property

Tax Rate(f)

Property

Tax

Notes for Table 4:

| ||||||||||||||||||||

(a) |

|

| Represents calendar year. | |||||||||||||||||

| ||||||||||||||||||||

(b) |

| Represents 12-month period from July 1, 2009 through June 30, 2010. | ||||||||||||||||||

| ||||||||||||||||||||

(c) |

| Represents 12-month period from October 1, 2008 through September 30, 2009. | ||||||||||||||||||

| ||||||||||||||||||||

(d) |

| Represents 12-month period from July 1, 2010 through June 30, 2011. | ||||||||||||||||||

| ||||||||||||||||||||

(e) |

| The hotel property consisted of undeveloped land for a portion of the tax year, and the real property tax is not necessarily indicative of property taxes expected for the hotel in the future. | ||||||||||||||||||

| ||||||||||||||||||||

(f) |

| Property tax rate is an aggregate figure for county, city and other local taxing authorities (to the extent applicable). | ||||||||||||||||||

S-22

We are expanding our discussion in the prospectus to include the subsections and information below. Ownership of Equity Securities by Management The determination of “beneficial ownership” for purposes of this Supplement has been based on information reported to the Company and the rules and regulations of the Securities and Exchange Commission. References below to “beneficial ownership” by a particular person, and similar references, should not be construed as an admission or determination by the Company that Common Shares in fact are beneficially owned by such person. As of September 30, 2010, the Company had a total of 158,905,339 issued and outstanding Common Shares. There are no shareholders known to the Company who beneficially owned more than 5% of its outstanding voting securities on such date. The following table sets forth the beneficial ownership of the Company’s securities by its directors and executive officers as of March 19, 2010: Title of Class(1) Name of Beneficial Owner Amount and Percent Common Shares Lisa B. Kern 20,402 * (voting) Bruce H. Matson 20,402 * Michael S. Waters 20,402 * Robert M. Wily 20,402 * Glade M. Knight 10 * Above directors and executive officers as a group 81,618 * Series A Lisa B. Kern 20,402 * (non-voting) Bruce H. Matson 20,402 * Michael S. Waters 20,402 * Robert M. Wily 20,402 * Glade M. Knight 10 * Above directors and executive officers as a group 81,618 * Series B Convertible Glade M. Knight 480,000 100 % (non-voting)

Nature of

Beneficial

Ownership(2)

of Class

Preferred Shares

Preferred Shares

| ||||||||||||||||||||

* |

|

| Less than one percent of class. | |||||||||||||||||

| ||||||||||||||||||||

(1) |

| Executive officers not listed above for a particular class of securities hold no securities of such class. The Series A Preferred Shares are being issued as part of the Company’s best efforts offering of Units. Each Unit consists of one Common Share and one Series A Preferred Share. The Series A Preferred Shares have no voting rights and are not separately tradable from the Common Shares to which they relate. | ||||||||||||||||||

| ||||||||||||||||||||

(2) |

| Amounts shown for individuals other than Glade M. Knight consist entirely of securities that may be acquired upon the exercise of options, although no options have been exercised to date. The Series B Convertible Preferred Shares are convertible into Common Shares upon the occurrence of certain events, under a formula which is based on the gross proceeds raised by the Company during its best-efforts offering of Units. | ||||||||||||||||||

Information regarding the Company’s equity compensation plan is set forth in note 5 to the Company’s audited consolidated financial statements, which are incorporated by reference into this Supplement.

S-23

Corporate Governance Board of Directors The Company’s Board of Directors has determined that all of the Company’s directors, except Mr. Knight, are “independent” within the meaning of the rules of the New York Stock Exchange (which the Company, although not listed on a national exchange, has adopted for purposes of determining such independence). In making this determination, the Board considered all relationships between the director and the Company, including commercial, industrial, banking, consulting, legal, accounting, charitable and familial relationships. The Board has adopted a categorical standard that a director is not independent (a) if he or she receives any personal financial benefit from, on account of or in connection with a relationship between the Company and the director (excluding directors fees and options), (b) if he or she is a partner, officer, employee or managing member of an entity that has a business or professional relationship with, and that receives compensation from, the Company, or (c) if he or she is a non-managing member or shareholder of such an entity and owns 10% or more of the membership interests or common stock of that entity. The Board may determine that a director with a business or other relationship that does not fit within the categorical standard described in the immediately preceding sentence is nonetheless independent, but in that event, the Board is required to disclose the basis for its determination in the Company’s then current annual proxy statement. In addition, the Board has voluntarily adopted, based on rules of the New York Stock Exchange, certain conditions that prevent a director from being considered independent while the condition lasts and then for three years thereafter. Compensation of Directors During 2009, the directors of the Company were compensated as follows: All Directors in 2009. All directors were reimbursed by the Company for travel and other out-of-pocket expenses incurred by them to attend meetings of the directors or a committee and in conducting the business of the Company. Independent Directors in 2009. The independent directors (classified by the Company as all directors other than Mr. Knight) received annual directors’ fees of $15,000, plus $1,000 for each meeting of the Board attended and $1,000 for each committee meeting attended. Additionally, the Chair of the Audit Committee receives an additional fee of $2,500 per year and the Chair of the Compensation Committee receives an additional fee of $1,500 per year. Under the Company’s Non-Employee Directors’ Stock Option Plan, each non-employee director received options to purchase 12,466 Units, exercisable at $11 per Unit. Non-Independent Director in 2009. Mr. Knight received no compensation from the Company for his services as a director. Director Summary Compensation Director Year Fees Option Total Lisa B. Kern 2009 $ 25,500 $ 16,198 $ 41,698 Bruce H. Matson 2009 20,500 16,198 36,698 Michael S. Waters 2009 23,000 16,198 39,198 Robert M. Wily 2009 23,000 16,198 39,198 Glade M. Knight 2009 — — —

Earned

Awards(1)

| ||||||||||||||||||||

(1) |

|

| The amounts in this column reflect the grant date fair value determined in accordance with FASB ASC Topic 718. | |||||||||||||||||

S-24

Stock Option Grants in Last Fiscal Year In 2008, the Company adopted a Non-Employee Directors’ Stock Option Plan (the “Directors’ Plan”). The Directors’ Plan provides for automatic grants of options to acquire Units. The Directors’ Plan applies to directors of the Company who are not employees of the Company. Since adoption of the Directors’ Plan, none of the participants have exercised any of their options to acquire Units. The following table shows the options to acquire Units that were granted under the Directors Plan in 2009: Option Grants in Last Fiscal Year

Name(1)

Number of Units

Underlying Options

Granted in 2009(2)

Glade M. Knight

—

Lisa B. Kern

12,466

Bruce H. Matson

12,466

Michael S. Waters

12,466

Robert M. Wily

12,466

| ||||||||||||||||||||

(1) |

|

| Glade M. Knight is not eligible under the Directors’ Plan. | |||||||||||||||||

| ||||||||||||||||||||

(2) |

| Options granted in 2009 are exercisable for ten years from the date of grant at an exercise price of $11 per Unit. | ||||||||||||||||||

Certain Relationships and Agreements

The Company has significant transactions with related parties. These transactions may not have arms-length terms, and the results of the Company’s operations might be different if these transactions had been conducted with unrelated parties. The Company’s independent members of the Board of Directors oversee the existing related party relationships and are required to approve any material modifications to the existing contracts. At least one member of the Company’s senior management team approves each related party transaction.

The Company has contracted with Apple Suites Realty Group, Inc. (“ASRG”) to provide brokerage services for the acquisition and disposition of real estate assets. ASRG is wholly-owned by Glade M. Knight, the Company’s Chairman and Chief Executive Officer. In accordance with the contract, ASRG is paid a fee equal to 2% of the gross purchase or sales price (as applicable) of any acquisitions or dispositions of real estate investments, subject to certain conditions. Total amounts earned and paid through December 31, 2009 to ASRG for services under the terms of this contract were approximately $13.6 million. Amounts earned in 2009 were approximately $6.7 million.

The Company also has contracted with Apple Nine Advisors, Inc. (“A9A”), a company wholly-owned by Glade M. Knight to advise the Company and provide day-to-day management services and due-diligence services on acquisitions. In accordance with the contract, the Company pays A9A a fee equal to 0.1% to 0.25% of the total equity contributions to the Company, in addition to certain reimbursable expenses. The aggregate amount paid by the Company to A9A in 2009 was approximately $2.4 million. This amount includes a fee of $.7 million and costs of $1.7 million which were reimbursed by A9A to Apple REIT Six, Inc. who provides the resources for these services.

Compensation Discussion and Analysis

General Philosophy

The Company’s executive compensation philosophy is to attract, motivate and retain a superior management team. The Company’s compensation program rewards each senior manager for their contribution to the Company. In addition, the Company uses annual incentive benefits that are designed to be competitive with comparable employers and to align management’s incentives with the interests of the Company and its shareholders.

S-25