Filed Pursuant to Rule 424(b)(3)

Registration No. 333-147414

SUPPLEMENT NO. 6 DATED OCTOBER 23, 2008

TO PROSPECTUS DATED APRIL 25, 2008

APPLE REIT NINE, INC.

The following information supplements the prospectus of Apple REIT Nine, Inc. dated April 25, 2008 and is part of the prospectus. This Supplement updates the information presented in the prospectus.Prospective investors should carefully review the prospectus and this Supplement No. 6 (which is cumulative and replaces all prior Supplements).

| S-3 | ||

| S-3 | ||

| S-6 | ||

| S-7 | ||

| S-9 | ||

| S-11 | ||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | S-12 | |

| S-17 | ||

| F-1 |

Certain forward-looking statements are included in the prospectus and in this supplement. These forward-looking statements may involve our plans and objectives for future operations, including future growth and availability of funds. These forward-looking statements are based on current expectations, which are subject to numerous risks and uncertainties. Assumptions relating to these statements involve judgments with respect to, among other things, the continuation of our offering of units, future economic, competitive and market conditions and future business decisions, together with local, national and international events (including, without limitation, acts of terrorism or war, and their direct and indirect effects on travel and the economy). All of these matters are difficult or impossible to predict accurately and many of them are beyond our control. Although we believe the assumptions relating to the forward-looking statements, and the statements themselves, are reasonable, any of the assumptions could be inaccurate and, therefore, there can be no assurance that these forward-looking statements will prove to be accurate. In light of the significant uncertainties inherent in these forward-looking statements, the inclusion of this information should not be regarded as a representation by us or any other person that our objectives and plans, which we consider to be reasonable, will be achieved.

S-1

“Courtyard by Marriott,” “Fairfield Inn,” “TownePlace Suites,” “SpringHill Suites” and “Residence Inn” are each a registered trademark of Marriott International, Inc. or one of its affiliates. All references below to “Marriott” mean Marriott International, Inc. and all of its affiliates and subsidiaries, and their respective officers, directors, agents, employees, accountants and attorneys. Marriott is not responsible for the content of this prospectus supplement, whether relating to hotel information, operating information, financial information, Marriott’s relationship with Apple REIT Nine, Inc., or otherwise. Marriott is not involved in any way, whether as an “issuer” or “underwriter” or otherwise, in the offering by Apple REIT Nine, Inc. and receives no proceeds from the offering. Marriott has not expressed any approval or disapproval regarding this prospectus supplement or the offering related to this prospectus supplement, and the grant by Marriott of any franchise or other rights to Apple REIT Nine, Inc. shall not be construed as any expression of approval or disapproval. Marriott has not assumed, and shall not have, any liability in connection with this prospectus supplement or the offering related to this prospectus supplement.

“Hampton Inn,” “Hampton Inn & Suites,” “Homewood Suites,” “Hilton Garden Inn,” and “Embassy Suites” are each a registered trademark of Hilton Hotels Corporation or one of its affiliates. All references below to “Hilton” mean Hilton Hotels Corporation and all of its affiliates and subsidiaries, and their respective officers, directors, agents, employees, accountants and attorneys. Hilton is not responsible for the content of this prospectus supplement, whether relating to hotel information, operating information, financial information, Hilton’s relationship with Apple REIT Nine, Inc., or otherwise. Hilton is not involved in any way, whether as an “issuer” or “underwriter” or otherwise, in the offering by Apple REIT Nine, Inc. and receives no proceeds from the offering. Hilton has not expressed any approval or disapproval regarding this prospectus supplement or the offering related to this prospectus supplement, and the grant by Hilton of any franchise or other rights to Apple REIT Nine, Inc. shall not be construed as any expression of approval or disapproval. Hilton has not assumed, and shall not have, any liability in connection with this prospectus supplement or the offering related to this prospectus supplement.

S-2

We completed the minimum offering of units (with each unit consisting of one Common Share and one Series A Preferred Share) at $10.50 per unit on May 14, 2008. We are continuing the offering at $11 per unit in accordance with the prospectus.

As of October 1, 2008, we had closed on the following sales of units in the offering:

Price Per Unit | Number of Units Sold | Gross Proceeds | Proceeds Net of Selling Commissions and Marketing Expense Allowance | |||||

| $10.50 | 9,523,810 | $ | 100,000,000 | �� | $ | 90,000,000 | ||

| $11.00 | 19,542,556 | $ | 214,968,126 | $ | 193,471,313 | |||

Total | 29,066,366 | $ | 314,968,126 | $ | 283,471,313 | |||

Our distributions since initial capitalization through June 30, 2008 (before we completed the purchase of any hotels) totaled $893,000 and were paid at a monthly rate of $0.073334 per common share beginning in June 2008. For the same period our cash generated from operations was $304,000. Due to the inherent delay between raising capital and investing that same capital in income producing real estate, we have had significant amounts of cash earning interest at short term money market rates. As a result, the difference between distributions paid and cash generated from operations has been funded from proceeds from the offering of units, and this portion of distributions is expected to be treated as a return of capital for federal income tax purposes. We intend to continue paying dividends on a monthly basis, at an annualized dividend rate of $0.88 per common share. Since a portion of distributions has to date been funded with proceeds from the offering of units, our ability to maintain our current intended rate of distribution will be based on our ability to fully invest our offering proceeds and thereby increase our cash generated from operations. Since there can be no assurance of our ability to acquire properties that provide income at this level, there can be no assurance as to the classification or duration of distributions at the current rate. Proceeds of the offering which are distributed are not available for investment in properties. See “Risk Factors—We may be unable to make distributions to our shareholders,” on page 28 of the prospectus.

Purchase Summary

We currently own, through our subsidiaries, a total of 7 hotels. These hotels contain a total of 929 guest rooms. They were purchased for an aggregate gross purchase price of $124,617,440. Financial and operating information about these hotels is provided in another section below.

Loan Assumption

The purchase contract for one of our hotels required us to assume a loan secured by the hotel. The current outstanding principal balance of the assumed loan is $13,965,857. The assumed loan has a non-recourse structure, which means that the lender generally must rely on the property, rather than the borrower, as the lender’s source of repayment in any collection action. There are exceptions to the non-recourse structure in certain situations, such as misappropriation of funds and environmental liabilities. In these situations, the lender would be permitted to seek repayment from the guarantor or indemnitor of the loan, which is one of our wholly-owned subsidiaries.

S-3

Source of Funds and Related Party Payments

Our hotel purchases were funded by the proceeds from our ongoing offering of units. We also used our offering proceeds to pay $2,492,349, representing 2% of the gross purchase price for our hotel purchases, as a commission to Apple Suites Realty Group, Inc. This entity is owned by Glade M. Knight, who is one of our directors and our Chief Executive Officer.

We have entered into a property acquisition and disposition agreement with Apple Suites Realty Group, Inc. to acquire and dispose of our real estate assets. A fee of 2% of the gross purchase price or gross sale price in addition to certain reimbursable expenses will be payable for these services.

We have entered into an advisory agreement with Apple Nine Advisors, Inc. to manage us and our assets. An annual fee ranging from 0.1% to 0.25% of total equity proceeds received by us in addition to certain reimbursable expenses will be payable for these services. Apple Nine Advisors, Inc. has entered into an agreement with Apple REIT Six, Inc. to provide certain management services to us. We will reimburse Apple Nine Advisors, Inc. for the cost of the services provided by Apple REIT Six, Inc. Apple Nine Advisors, Inc. in turn will pay Apple REIT Six, Inc. for the cost of the services provided by Apple REIT Six, Inc. Total advisory fees and reimbursable expenses incurred by us under the advisory agreement are included in general and administrative expenses and totaled approximately $49,000 for the six months ended June 30, 2008. Apple Nine Advisors, Inc. is owned by Glade M. Knight, who is also the Chairman and Chief Executive Officer of Apple REIT Six, Inc.

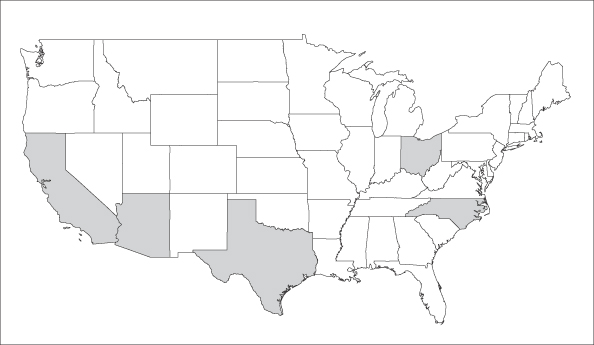

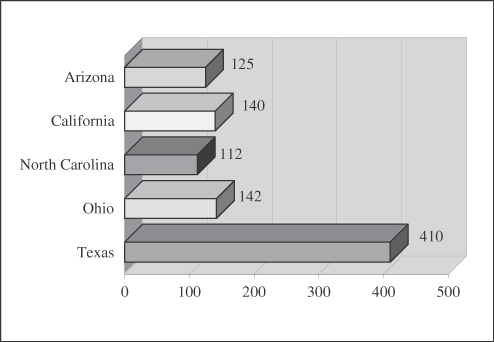

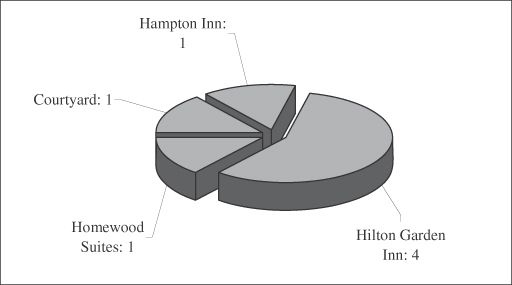

State and Franchise Summary

The below map shows the states in which our hotels are located, and the following charts summarize our room and franchise information.

States in which Our Hotels are Located

S-4

Number of Guest Rooms by State

Type and Number of Hotel Franchises

Ownership, Leasing and Management Summary

Each of our hotels has been leased to one of our wholly-owned subsidiaries, as the lessee, under a separate hotel lease agreement. For simplicity, the applicable lessee will be referred to below as the “lessee.”

Each hotel is managed under a separate management agreement between the applicable lessee and the manager. For simplicity, the applicable manager will be referred to below as the “manager.”

S-5

The hotel lease agreements and the management agreements are among the contracts described in another section below. The table below specifies the franchise, hotel owner, lessee and manager for our hotels:

Hotel | Franchise (a) | Hotel Owner/Lessor | Lessee | Manager | ||||||

| 1. | Tucson, Arizona | Hilton Garden Inn | Apple Nine Hospitality Ownership, Inc. | Apple Nine Hospitality Management, Inc. | Texas Western Management Partners, L.P. | |||||

| 2. | Charlotte, North Carolina | Homewood Suites | Apple Nine Hospitality Ownership, Inc. | Apple Nine Hospitality Management, Inc. | MHH Management, LLC | |||||

| 3. | Santa Clarita, California | Courtyard | Apple Nine Hospitality Ownership, Inc. | Apple Nine Hospitality Management, Inc. | Dimension Development Two, LLC | |||||

| 4. | Allen, Texas | Hampton Inn & Suites | Apple Nine Hospitality Ownership, Inc. | Apple Nine Hospitality Texas Services, Inc. | Gateway Hospitality Group, Inc. (b) | |||||

| 5. | Twinsburg, Ohio | Hilton Garden Inn | Apple Nine Hospitality Ownership, Inc. | Apple Nine Hospitality Management, Inc. | Gateway Hospitality Group, Inc. (b) | |||||

| 6. | Lewisville, Texas | Hilton Garden Inn | Apple Nine Hospitality Ownership, Inc. | Apple Nine Hospitality Texas Services, Inc. | Gateway Hospitality Group, Inc. (b) | |||||

| 7. | Duncanville, Texas | Hilton Garden Inn | Apple Nine SPE Duncanville, Inc. | Apple Nine Services Duncanville, Inc. | Gateway Hospitality Group, Inc. (b) |

Notes for Table:

| (a) | All brand and trade names, logos or trademarks contained, or referred to, in this prospectus supplement are the properties of their respective owners. These references shall not in any way be construed as participation by, or endorsement of, our offering by any of our franchisors or managers. |

| (b) | The hotels specified were purchased from an affiliate of the indicated manager. |

We have no material relationship or affiliation with the hotel sellers or managers, except for the relationship resulting from our purchases, our management agreements for the hotels we own, the pending purchase contracts and any related documents.

Purchase Contracts

We have entered into, or caused one of our wholly-owned subsidiaries to enter into, purchase contracts for 19 other hotels. These contracts are for direct hotel purchases or, in certain cases, a purchase of the entity that currently owns the hotel. The following table summarizes the hotel and contract information:

Purchase Contracts for Potential Acquisitions

Hotel | Franchise (a) | Date of Purchase Contract | Number of Rooms | Gross Purchase Price | |||||||

| 1. | Allen, Texas | Hilton Garden Inn | August 1, 2008 | 150 | $ | 18,500,000 | |||||

| 2. | Bristol, Virginia | Courtyard | August 7, 2008 | 175 | 18,650,000 | ||||||

| 3. | Santa Clarita, California | Hampton Inn | August 29, 2008 | 128 | 16,500,000 | ||||||

| 4. | Santa Clarita, California (a) | Residence Inn | August 29, 2008 | 90 | 16,000,000 | ||||||

| 5. | Santa Clarita, California (a) | Fairfield Inn | August 29, 2008 | 66 | 9,000,000 | ||||||

| 6. | Beaumont, Texas | Residence Inn | September 11, 2008 | 133 | 16,900,000 | ||||||

| 7. | Hillsboro, Oregon (b) | Embassy Suites | October 3, 2008 | 165 | 32,500,000 | ||||||

| 8. | Hillsboro, Oregon (b) | Hampton Inn & Suites | October 3, 2008 | 106 | 14,500,000 | ||||||

| 9. | Pueblo, Colorado | Hampton Inn & Suites | October 6, 2008 | 81 | 8,025,000 | ||||||

| 10. | Durham, North Carolina | Homewood Suites | October 10, 2008 | 122 | 19,050,000 | ||||||

| 11. | Clovis, California (b) | Hampton Inn & Suites | October 17, 2008 | 86 | 11,150,000 | ||||||

| 12. | Clovis, California (b) | Homewood Suites | October 17, 2008 | 83 | 12,435,000 | ||||||

| 13. | Panama City, Florida (b) | Hampton Inn & Suites | October 17, 2008 | 95 | 11,600,000 | ||||||

| 14. | Dothan, Alabama (b) | Hilton Garden Inn | October 20, 2008 | 104 | 11,600,836 | ||||||

| 15. | Albany, Georgia (b) | Fairfield Inn & Suites | October 20, 2008 | 87 | 7,919,790 | ||||||

| 16. | Hattiesburg, Mississippi (b) | Residence Inn | October 20, 2008 | 84 | 9,793,028 | ||||||

| 17. | Panama City, Florida (b) | TownePlace Suites | October 20, 2008 | 103 | 10,640,346 | ||||||

| 18. | Johnson City, Tennessee (b) | Courtyard | October 20, 2008 | 90 | 9,879,788 | ||||||

| 19. | Troy, Alabama (b) | Courtyard | October 20, 2008 | 90 | 8,696,456 | ||||||

| Total | 2,038 | $ | 263,340,244 | ||||||||

Notes for Table:

| (a) | The indicated hotels are subject to a single purchase contract. |

| (b) | The indicated hotels are currently under development. The table shows the expected number of rooms upon hotel completion and the expected franchise. |

S-6

In general, each purchase contract listed above required a deposit upon (or shortly after) execution. An additional deposit is typically due upon the expiration of the contract review period. If a closing occurs under a purchase contract, the initial and additional deposits are credited toward the purchase price. If a closing does not occur because the seller fails to satisfy a condition to closing or breaches the purchase contract, the applicable deposits would be refunded to us. The total of both the initial and additional deposits for the purchase contracts listed above is $3,840,000.

For each purchase contract listed above, there are material conditions to closing that presently remain unsatisfied. Accordingly, there can be no assurance at this time that a closing will occur under any of these purchase contracts.

Loan Information

Two of the purchase contracts listed above require our purchasing subsidiaries to assume loans that are secured by the hotels under contract. Each loan has a non-recourse structure, as previously described in another section above. The following table provides a summary of the loan information for the applicable hotels:

Loan Information for Potential Acquisitions (a)

Hotel | Franchise | Outstanding Principal Balance of Loan | Annual Interest Rate | Maturity Date | ||||||

Bristol, Virginia | Courtyard | $ | 9,793,768 | 6.59 | % | August 2016 | ||||

Allen, Texas | Hilton Garden Inn | 10,841,619 | 5.37 | % | October 2015 | |||||

| 20,635,387 | ||||||||||

Note for Table:

| (a) | The loans provide for monthly payments of principal and interest on an amortized basis. |

FOR OUR PROPERTIES

Hotel Lease Agreements

Each of our hotels is covered by a separate hotel lease agreement between the owner (one of our wholly-owned subsidiaries) and the applicable lessee (another one of our wholly-owned subsidiaries, as specified in the previous section). Each lease provides for an initial term of 10 years. The applicable lessee has the option to extend its lease term for two additional five-year periods, provided it is not in default at the end of the prior term or at the time the option is exercised.

Each lease provides for annual base rent and percentage rent. The annual base rent is payable in advance in equal monthly installments and will be adjusted each year in proportion to the Consumer Price Index (based on the U.S. City Average). Shown below is the annual base rent and the lease commencement date for our hotels:

Hotel | Franchise | Annual Base Rent | Date of Lease Commencement | ||||||

1. | Tucson, Arizona | Hilton Garden Inn | $ | 1,669,903 | July 31, 2008 | ||||

2. | Charlotte, North Carolina | Homewood Suites | 435,654 | September 24, 2008 | |||||

3. | Santa Clarita, California | Courtyard | 1,225,125 | September 24, 2008 | |||||

4. | Allen, Texas | Hampton Inn & Suites | 1,066,725 | September 26, 2008 | |||||

5. | Twinsburg, Ohio | Hilton Garden Inn | 1,478,217 | October 7, 2008 | |||||

6. | Lewisville, Texas | Hilton Garden Inn | 1,576,353 | October 16, 2008 | |||||

7. | Duncanville, Texas | Hilton Garden Inn | 1,435,865 | October 21, 2008 | |||||

S-7

The annual percentage rent depends on a formula that compares fixed “suite revenue breakpoints” with a portion of “suite revenue,” which is equal to gross revenue from guest rentals less sales and room taxes and credit card fees. The suite revenue breakpoints will be adjusted each year in proportion to the Consumer Price Index (based on the U.S. City Average). Specifically, the annual percentage rent is equal to the sum of (a) 17% of all suite revenue for the year, up to the applicable suite revenue breakpoint; plus (b) 55% of the suite revenue for the year in excess of the applicable suite revenue breakpoint, as reduced by base rent paid for the year.

Management Agreements

Each of our hotels is being managed by the manager under a separate management agreement between the manager and the applicable lessee (which is one of our wholly-owned subsidiaries, as specified in the previous section). The manager is responsible for managing and supervising the daily operations of the hotel and for collecting revenues for the benefit of the applicable lessee. The fees and other terms of these agreements are the result of commercial negotiations between otherwise unrelated parties. We believe that such fees and terms are appropriate for the hotels and the markets in which they operate.

Franchise Agreements

In general, for the hotels franchised by Marriott International, Inc. or one of its affiliates, there is a relicensing franchise agreement between the applicable lessee (as specified in a previous section) and Marriott International, Inc. or an affiliate. Each relicensing franchise agreement provides for the payment of royalty fees and marketing contributions to the franchisor. A percentage of gross room revenues is used to determine these payments. In addition, we have caused Apple Nine Hospitality, Inc. or another one of our subsidiaries to provide a separate guaranty of the payment and performance of the applicable lessee under the relicensing franchise agreement.

For the hotels franchised by Hilton Hotels Corporation or one of its affiliates, there is a franchise license agreement between the applicable lessee and Hilton Hotels Corporation or an affiliate. Each franchise license agreement provides for the payment of royalty fees and program fees to the franchisor. A percentage of gross room revenues is used to determine these payments. Apple Nine Hospitality, Inc. or another one of our subsidiaries has guaranteed the payment and performance of the lessee under the applicable franchise license agreement.

The fees and other terms of these agreements are the result of commercial negotiations between otherwise unrelated parties, and we believe that such fees and terms are appropriate for the hotels and the markets in which they operate. These agreements may be terminated for various reasons, including failure by the applicable lessee to operate in accordance with the standards, procedures and requirements established by the franchisor.

S-8

FINANCIAL AND OPERATING INFORMATION

FOR OUR PROPERTIES

Our hotels offer guest rooms and suites, together with related amenities, that are consistent with their operations. The hotels are located in developed or developing areas and in competitive markets. We believe the hotels are well-positioned to compete in their markets based on location, amenities, rate structure and franchise affiliation. In the opinion of management, each hotel is adequately covered by insurance. The following tables present further information about our hotels:

Table 1. General Information

Hotel | Franchise | Number of Rooms/ Suites | Gross Purchase Price | Average Daily Rate (Price) per Room/ Suite (a) | Federal Income Tax Basis for Depreciable Real Property Component of Hotel (b) | ||||||||||

1. | Tucson, Arizona | Hilton Garden Inn | 125 | $ | 18,375,000 | $ | 120-149 | $ | 17,397,150 | ||||||

2. | Charlotte, North Carolina | Homewood Suites | 112 | 5,750,000 | 129-189 | 4,729,410 | |||||||||

3. | Santa Clarita, California | Courtyard | 140 | 22,700,000 | 129-209 | 18,243,805 | |||||||||

4. | Allen, Texas | Hampton Inn & Suites | 103 | 12,500,000 | 144-159 | 11,100,086 | |||||||||

5. | Twinsburg, Ohio | Hilton Garden Inn | 142 | 17,792,440 | 134-161 | 16,387,690 | |||||||||

6. | Lewisville, Texas | Hilton Garden Inn | 165 | 28,000,000 | 149-176 | 24,529,875 | |||||||||

7. | Duncanville, Texas | Hilton Garden Inn | 142 | 19,500,000 | 143-199 | 17,779,620 | |||||||||

| Total | 929 | $ | 124,617,440 | ||||||||||||

Notes for Table 1:

| (a) | The amounts shown are subject to change, and exclude discounts that may be offered to corporate, frequent and other select customers. |

| (b) | The depreciable life is 39 years (or less, as may be permitted by federal tax laws) using the straight-line method. The modified accelerated cost recovery system will be used for the hotel’s personal property component. |

Table 2. Loan Information (a)

Hotel | Franchise | Outstanding Principal Balance of Loan | Annual Interest Rate | Maturity Date | ||||||||

Duncanville, Texas | Hilton Garden Inn | $ | 13,965,857 | 5.88 | % | May 2017 | ||||||

Note for Table 2:

| (a) | This table describes a loan that (i) pre-dated our purchase, (ii) is secured by the indicated hotel, and (iii) was assumed by our purchasing subsidiary. The loan provides for monthly payments of principal and interest on an amortized basis. |

S-9

Table 3. Operating Information (a)

PART A

| Avg. Daily Occupancy Rates (%) | ||||||||||||||||||||||||

Hotel | Franchise | 2003 | 2004 | 2005 | 2006 | 2007 | ||||||||||||||||||

1. | Tucson, Arizona | Hilton Garden Inn | — | — | — | — | — | |||||||||||||||||

2. | Charlotte, North Carolina | Homewood Suites | 66 | % | 63 | % | 78 | % | 76 | % | 71 | % | ||||||||||||

3. | Santa Clarita, California | Courtyard | — | — | — | — | 51 | % | ||||||||||||||||

4. | Allen, Texas | Hampton Inn & Suites | — | — | — | 51 | % | 68 | % | |||||||||||||||

5. | Twinsburg, Ohio | Hilton Garden Inn | 65 | % | 62 | % | 64 | % | 63 | % | 66 | % | ||||||||||||

6. | Lewisville, Texas | Hilton Garden Inn | — | — | — | — | 42 | % | ||||||||||||||||

7. | Duncanville, Texas | Hilton Garden Inn | — | — | 59 | % | 64 | % | 65 | % | ||||||||||||||

PART B

|

| |||||||||||||||||||||||

| Revenue per Available Room/Suite ($) | ||||||||||||||||||||||||

Hotel | Franchise | 2003 | 2004 | 2005 | 2006 | 2007 | ||||||||||||||||||

1. | Tucson, Arizona | Hilton Garden Inn | — | — | — | — | — | |||||||||||||||||

2. | Charlotte, North Carolina | Homewood Suites | $ | 46 | $ | 45 | $ | 55 | $ | 62 | $ | 67 | ||||||||||||

3. | Santa Clarita, California | Courtyard | — | — | — | — | $ | 59 | ||||||||||||||||

4. | Allen, Texas | Hampton Inn & Suites | — | — | — | $ | 53 | $ | 76 | |||||||||||||||

5. | Twinsburg, Ohio | Hilton Garden Inn | $ | 60 | $ | 57 | $ | 62 | $ | 64 | $ | 69 | ||||||||||||

6. | Lewisville, Texas | Hilton Garden Inn | — | — | — | — | $ | 50 | ||||||||||||||||

7. | Duncanville, Texas | Hilton Garden Inn | — | — | $ | 56 | $ | 66 | $ | 73 | ||||||||||||||

Note for Table 3:

| (a) | Information is shown for the last five years of hotel operations, if applicable. |

Table 4. Tax and Related Information

Hotel | Franchise | Tax Year | Real Property Tax Rate (c) | Real Property Tax | ||||||||||

1. | Tucson, Arizona | Hilton Garden Inn | 2007 | (a) | 2.5 | % | $ | 8,761 | (d) | |||||

2. | Charlotte, North Carolina | Homewood Suites | 2007 | (a) | 1.3 | % | 75,716 | |||||||

3. | Santa Clarita, California | Courtyard | 2007 | (b) | 1.2 | % | 225,070 | |||||||

4. | Allen, Texas | Hampton Inn & Suites | 2007 | (a) | 2.4 | % | 192,282 | |||||||

5. | Twinsburg, Ohio | Hilton Garden Inn | 2007 | (a) | 2.0 | % | 237,637 | |||||||

6. | Lewisville, Texas | Hilton Garden Inn | 2007 | (a) | 2.6 | % | 262,740 | |||||||

7. | Duncanville, Texas | Hilton Garden Inn | 2007 | (a) | 2.7 | % | 296,354 | |||||||

Notes for Table 4:

| (a) | Represents calendar year. |

| (b) | Represents 12-month period from July 1, 2007 through June 30, 2008. |

| (c) | Property tax rate is an aggregate figure for county, city and other local taxing authorities (to the extent applicable). |

| (d) | The amount shown is the 2007 amount for the undeveloped land on which the hotel was constructed during 2008. The amount shown is not necessarily indicative of property taxes expected for the hotel in the future. |

S-10

| Three Months Ended | Six Months Ended | |||||||

(in thousands except per share and statistical data) | June 30, 2008 | June 30, 2008 | ||||||

| (unaudited) | ||||||||

Income Statement | ||||||||

General and administrative expenses | $ | 94 | $ | 111 | ||||

Interest (income) expense, net | $ | (388 | ) | $ | (385 | ) | ||

Net income | $ | 294 | $ | 274 | ||||

Per Share Data | ||||||||

Earnings per common share | $ | 0.05 | $ | 0.09 | ||||

Weighted-average common shares outstanding—basic and diluted | 6,392 | 3,196 | ||||||

Cash flow from (used in): | ||||||||

Operating activities | $ | 304 | ||||||

Investing activities | $ | (210 | ) | |||||

Financing activities | $ | 162,465 | ||||||

| June 30, 2008 | December 31, 2007 | |||||||

| (unaudited) | ||||||||

Balance Sheet Data | ||||||||

Cash and cash equivalents | $ | 162,579 | $ | 20 | ||||

Total assets | $ | 162,821 | $ | 337 | ||||

Note payable | $ | — | $ | 151 | ||||

Shareholders’ equity | $ | 162,770 | $ | 31 | ||||

S-11

MANAGEMENT’S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

(For the six months ended June 30, 2008)

Overview

The Company is a Virginia corporation that intends to qualify as a REIT for federal income tax purposes. The Company, which owns no properties and has no operating history, was formed to invest in hotels, residential apartment communities and other income-producing real estate in selected metropolitan areas in the United States. Initial capitalization occurred on November 9, 2007, when 10 Units, each Unit consisting of one common share and one Series A preferred share, were purchased by Apple Nine Advisors, Inc. (“A9A”) and 480,000 Series B convertible preferred shares were purchased by Glade M. Knight, the Company’s Chairman, Chief Executive Officer and President. The Company’s fiscal year end is December 31.

Related Party Transactions

The Company has significant transactions with related parties. These transactions cannot be construed to be at arms length and the results of the Company’s operations may be different than if conducted with non-related parties.

The Company has entered into a Property Acquisition and Disposition Agreement with Apple Suites Realty Group, Inc. (“ASRG”), to acquire and dispose of real estate assets for the Company. A fee of 2% of the gross purchase price or gross sale price in addition to certain reimbursable expenses will be payable for these services. There have been no amounts incurred by the Company under this agreement as of June 30, 2008.

The Company has entered into an advisory agreement with A9A to provide management of the Company and its assets. An annual fee ranging from 0.1% to 0.25% of total equity proceeds received by the Company in addition to certain reimbursable expenses will be payable for these services. A9A has entered into an agreement with Apple REIT Six, Inc. (“AR6”) to provide certain management services to the Company. The Company will reimburse A9A for the cost of the services provided by AR6. Total advisory fees and reimbursable expenses incurred by the Company under the advisory agreement are included in general and administrative expenses and totaled approximately $49,000 for the six months ended June 30, 2008.

ASRG and A9A are 100% owned by Glade M. Knight, Chairman, Chief Executive Officer and President of the Company. ASRG and A9A may purchase in the “best efforts” offering up to 2.5% of the total number of shares sold in the offering.

Mr. Knight is also Chairman and Chief Executive Officer of Apple REIT Six, Inc., Apple REIT Seven, Inc. and Apple REIT Eight, Inc., other REITS. Members of the Company’s Board of Directors are also on the Board of Directors of Apple REIT Six, Inc., Apple REIT Seven, Inc. and Apple REIT Eight, Inc.

Results of Operations

During the period from the Company’s initial formation on November 9, 2007 through June 30, 2008, the Company owned no properties, had no revenue, exclusive of interest income and was primarily engaged in capital formation activities.

Liquidity and Capital Resources

The Company’s principal source of liquidity will be the proceeds of the “best-efforts” offering and the cash flow generated from properties the Company will acquire and any short term investments. In addition, the Company may borrow funds, subject to the approval of the Company’s board of directors.

S-12

The Company is raising capital through a “best-efforts” offering of shares by David Lerner Associates, Inc., the managing dealer, which receives selling commissions and a marketing expense allowance based on proceeds of the shares sold. The minimum offering of 9,523,810 Units at $10.50 per Unit was sold as of May 14, 2008, with proceeds net of commissions and marketing expenses totaling $90 million. Subsequent to the minimum offering and through June 30, 2008, an additional 7.5 million Units, at $11 per Unit, were sold, with the Company receiving proceeds, net of commissions, marketing expenses and other offering costs of approximately $73.3 million. The Company is continuing its offering at $11.00 per Unit.

Each Unit consists of one common share and one Series A preferred share. The Series A preferred shares will have no voting rights, no conversion rights and no distribution rights. The only right associated with the Series A preferred shares will be a priority distribution upon the sale of the Company’s assets. The priority will be equal to $11.00 per Series A preferred share, and no more, before any distributions are made to the holders of any other shares. In the event the Company pays special dividends, the amount of the $11.00 priority will be reduced by the amount of any special dividends approved by the board. The Series A preferred shares will not be separately tradable from the common shares to which they relate.

Prior to the commencement of the Company’s “best-efforts” offering, the Company obtained an unsecured line of credit in a principal amount of $400,000 to fund certain start-up costs and offering expenses. The line of credit was fully paid during May 2008 with net proceeds from the Company’s “best-efforts” offering.

As of June 30, 2008, the Company had cash and cash equivalents totaling $162.6 million, primarily resulting from the sale of Units through that date. The Company intends to use funds generated from its “best-efforts” offering to invest in hotels, residential apartment communities and other income-producing real estate. As of June 30, 2008 the Company had entered into a purchase contract for the potential acquisition of a Hilton Garden Inn hotel located in Tucson, Arizona. The purchase price for the 125 guest room hotel is $18.4 million, and a refundable deposit of $150,000 was paid by the Company in connection with the contract. It is expected that the purchase price will be funded from the Company’s cash on hand. While the purchase of the hotel by the Company is expected to occur during 2008, there can be no assurance that all the conditions to closing will be satisfied.

To maintain its REIT status the Company is required to distribute at least 90% of its ordinary income. Although the Company owns no real estate, distributions since the initial capitalization through June 30, 2008 totaled approximately $893,000 and were paid at a monthly rate of $0.073334 per common share beginning in June 2008. For the same period the Company’s cash generated from operations was approximately $304,000. Due to the inherent delay between raising capital and investing that same capital in income producing real estate, the Company has had significant amounts of cash earning interest at short term money market rates. As a result, the difference between distributions paid and cash generated from operations has been funded from proceeds from the offering of Units, and this portion of distributions is expected to be treated as a return of capital for federal income tax purposes. The Company intends to continue paying dividends on a monthly basis, at an annualized dividend rate of $0.88 per common share. Since a portion of distributions has to date been funded with proceeds from the offering of Units, the Company’s ability to maintain its current intended rate of distribution will be based on its ability to fully invest its offering proceeds and thereby increase its cash generated from operations. Since there can be no assurance of the Company’s ability to acquire properties that provide income at this level, there can be no assurance as to the classification or duration of distributions at the current rate. Proceeds of the offering which are distributed are not available for investment in properties.

Series B Convertible Preferred Stock

The Company has authorized 480,000 shares of Series B convertible preferred stock. The Company has issued 480,000 Series B convertible preferred shares to Glade M. Knight, chairman, chief executive officer and president of the Company, in exchange for the payment by him of $0.10 per Series B convertible preferred share, or an aggregate of $48,000. The Series B convertible preferred shares are convertible into common shares pursuant to the formula and on the terms and conditions set forth below.

S-13

There are no dividends payable on the Series B convertible preferred shares. Holders of more than two-thirds of the Series B convertible preferred shares must approve any proposed amendment to the articles of incorporation that would adversely affect the Series B convertible preferred shares.

Upon the Company’s liquidation, the holder of the Series B convertible preferred shares is entitled to a priority liquidation payment before any distribution of liquidation proceeds to the holders of the common shares. However, the priority liquidation payment of the holder of the Series B convertible preferred shares is junior to the holders of the Series A preferred shares distribution rights. The holder of a Series B convertible preferred share is entitled to a liquidation payment of $11 per number of common shares each Series B convertible preferred share would be convertible into according to the formula described below. In the event that the liquidation of the Company’s assets results in proceeds that exceed the distribution rights of the Series A preferred shares and the Series B convertible preferred shares, the remaining proceeds will be distributed between the common shares and the Series B convertible preferred shares, on an as converted basis.

Each holder of outstanding Series B convertible preferred shares shall have the right to convert any of such shares into common shares of the Company upon and for 180 days following the occurrence of any of the following events:

(1) substantially all of the Company’s assets, stock or business is sold or transferred through exchange, merger, consolidation, lease, share exchange, sale or otherwise, other than a sale of assets in liquidation, dissolution or winding up of the Company;

(2) the termination or expiration without renewal of the advisory agreement, or if the Company ceases to use ASRG to provide property acquisition and disposition services; or

(3) the Company’s common shares are listed on any securities exchange or quotation system or in any established market.

Upon the occurrence of any conversion event, each Series B convertible preferred share may be converted into a number of common shares based upon the gross proceeds raised through the date of conversion in the Company’s $2 billion offering according to the following table:

Gross Proceeds Raised from Sales of Units through Date of Conversion | Number of Common Shares through Conversion of One Series B Convertible Preferred Share | |

| $100 million | 0.92321 | |

| $200 million | 1.83239 | |

| $300 million | 3.19885 | |

| $400 million | 4.83721 | |

| $500 million | 6.11068 | |

| $600 million | 7.29150 | |

| $700 million | 8.49719 | |

| $800 million | 9.70287 | |

| $900 million | 10.90855 | |

| $ 1 billion | 12.11423 | |

| $ 1.1 billion | 13.31991 | |

| $ 1.2 billion | 14.52559 | |

| $ 1.3 billion | 15.73128 | |

| $ 1.4 billion | 16.93696 | |

| $ 1.5 billion | 18.14264 | |

| $ 1.6 billion | 19.34832 | |

| $ 1.7 billion | 20.55400 | |

| $ 1.8 billion | 21.75968 | |

| $ 1.9 billion | 22.96537 | |

| $ 2 billion | 24.17104 |

S-14

In the event that after raising gross proceeds of $2 billion, the Company raises additional gross proceeds in a subsequent public offering, each Series B convertible preferred share may be converted into an additional number of common shares based on the additional gross proceeds raised through the date of conversion in a subsequent public offering according to the following formula: (X/100 million) x 1.20568, where X is the additional gross proceeds rounded down to the nearest 100 million.

No additional consideration is due upon the conversion of the Series B convertible preferred shares. The conversion into common shares of the Series B convertible preferred shares will result in dilution of the shareholders’ interests.

Expense related to the issuance of 480,000 Series B convertible preferred shares to Mr. Knight will be recognized at such time when the number of common shares to be issued for conversion of the Series B shares can be reasonably estimated and the event triggering the conversion of the Series B shares to common shares occurs. The expense will be measured as the difference between the fair value of the common stock for which the Series B shares can be converted and the amounts paid for the Series B shares. Although the fair market value cannot be determined at this time, expense if the maximum offering is achieved could range from $0 to in excess of $127 million (assumes $11 per unit fair market value).

Recent Accounting Pronouncements

In September 2006, the Financial Accounting Standards Board (“FASB”) issued Statement No. 157,Fair Value Measurements (“SFAS 157”). SFAS 157 defines fair value, establishes a framework for measuring fair value and expands disclosures about fair value measurements. The Statement applies under other accounting pronouncements that require or permit fair value measurements. Accordingly, this Statement does not require any new fair value measurements. In February 2008, the FASB released FASB Staff Position (FSP) FAS 157-2 – Effective Date of FASB Statement No. 157, which defers the effective date of SFAS 157 to fiscal years beginning after November 15, 2008 for all nonfinancial assets and liabilities, except those items that are recognized or disclosed at fair value in the financial statements on a recurring basis (at least annually). The effective date of the statement related to those items not covered by the deferral (all financial assets and liabilities or nonfinancial assets and liabilities recorded at fair value on a recurring basis) is for fiscal years beginning after November 15, 2007. The adoption of this statement did not have and is not anticipated to have a material impact on the Company’s results of operations and financial position.

In February 2007, FASB issued SFAS No. 159,The Fair Value Option for Financial Assets and Financial Liabilities(“SFAS 159”). SFAS 159 permits entities to choose to measure many financial instruments and certain other items at fair value. The objective of the guidance is to improve financial reporting by providing entities with the opportunity to mitigate volatility in reported earnings caused by measuring related assets and liabilities differently without having to apply complex hedge accounting provisions. SFAS 159 is effective as of the beginning of the first fiscal year that begins after November 15, 2007. SFAS 159 is effective for the Company beginning January 1, 2008. The Company has elected not to use the fair value measurement provisions of SFAS 159 and therefore, adoption of this standard did not have an impact on the financial statements.

In March 2008, FASB issued SFAS No. 161,Disclosures about Derivative Instruments and Hedging Activities, an Amendment of FASB Statement No. 133 (“SFAS 161”). SFAS 161 is intended to improve transparency in financial reporting by requiring enhanced disclosures of an entity’s derivative instruments and hedging activities and their effects on the entity’s financial position, financial performance, and cash flows. SFAS 161 applies to all derivative instruments within the scope of SFAS No. 133,Accounting for Derivative Instruments and Hedging Activities (“SFAS 133”). It also applies to non-derivative hedging instruments and all hedged items designated and qualifying as hedges under SFAS 133. SFAS 161 is effective prospectively for financial statements issued for fiscal years and interim periods beginning after November 15, 2008, with early application encouraged. The Company does not currently have any instruments that qualify within the scope of SFAS 133, and therefore the adoption of this statement is not anticipated to have a material impact on the Company’s financial statements.

S-15

In May 2008, the FASB issued SFAS No. 162,The Hierarchy of Generally Accepted Accounting Principles (“SFAS 162”). SFAS 162 identifies the sources of accounting principles and the framework for selecting the principles to be used in the preparation of financial statements of nongovernmental entities that are presented in conformity with generally accepted accounting principles in the United States. SFAS 162 is effective 60 days following the Securities and Exchange Commission’s (“SEC”) approval of the Public Company Accounting Oversight Board amendments to AU Section 411, The Meaning of Present Fairly in Conformity with Generally Accepted Accounting Principles. The Company is currently evaluating the potential impact, if any, of the adoption of SFAS 162 on its financial statements.

Subsequent Events

In July 2008, the Company declared and paid approximately $1.2 million in dividend distributions to its common shareholders, or $0.073334 per outstanding common share.

During July 2008, the Company closed on the issuance of 4.2 million Units through its ongoing “best-efforts” offering, representing gross proceeds to the Company of $45.8 million and proceeds net of selling and marketing costs of $41.2 million.

On July 24, 2008, the Company entered into a purchase contract for the potential acquisition of a Courtyard hotel in Santa Clarita, California. The gross purchase price for the 140 room hotel is $22.7 million, and a refundable deposit of $200,000 was paid by the Company in connection with the contract.

On July 31, 2008, the Company closed on the purchase of a Hilton Garden Inn located in Tucson, Arizona. The gross purchase price for this hotel, which contains a total of 125 guest rooms, was $18.4 million.

On August 1, 2008, the Company entered into a purchase contract for the potential acquisition of a Homewood Suites hotel in Charlotte, North Carolina. The gross purchase price for the 112 room hotel is $5.8 million, and a refundable deposit of $200,000 was paid by the Company in connection with the contract.

On August 1, 2008, the Company entered into five separate purchase contracts with a group of related sellers for the potential acquisition of five hotels. The purchase contracts are for a 142 room Hilton Garden Inn in Twinsburg, Ohio with a purchase price of $16.5 million, a 165 room Hilton Garden Inn in Lewisville, Texas with a purchase price of $28.0 million, a 142 room Hilton Garden Inn in Duncanville, Texas with a purchase price of $19.5 million, a 103 room Hampton Inn and Suites in Allen, Texas with a purchase price of $12.5 million and a 150 room Hilton Garden Inn in Allen, Texas with a purchase price of $18.5 million. The initial refundable deposit under each separate contract was $200,000.

S-16

Set forth below are the audited financial statements of the Tucson, Arizona-Hilton Garden Inn. These financial statements have been audited by Ernst & Young LLP, independent registered public accounting firm, as set forth in their report appearing elsewhere herein and are included in reliance upon such report given on the authority of such firm as experts in accounting and auditing.

Set forth below are the audited financial statements of Charlotte Lakeside Hotel, L.P. (previous owner of the Charlotte, North Carolina Homewood Suites). These financial statements have been included herein in reliance on the report, also set forth below, of Schneider & Company Certified Public Accountants, PC, an independent certified public accounting firm, and upon the authority of that firm as an expert in accounting and auditing.

Set forth below are the audited financial statements of the Santa Clarita, California Courtyard by Marriott Hotel. These financial statements have been included herein in reliance on the report, also set forth below, of L.P. Martin & Company, P.C., an independent certified public accounting firm, and upon the authority of that firm as an expert in accounting and auditing.

Set forth below are the separate audited financial statements of (i) Allen Stacy Hotel, Ltd. (previous owner of the Allen, Texas Hampton Inn & Suites), (ii) RSV Twinsburg Hotel, Ltd. (previous owner of the Twinsburg, Ohio Hilton Garden Inn), (iii) SCI Lewisville Hotel Ltd. (previous owner of the Lewisville, Texas Hilton Garden Inn), and (iv) SCI Duncanville Hotel, Ltd. (previous owner of the Duncanville, Texas Hilton Garden Inn). These financial statements have been included herein in reliance on the reports also set forth below, of Novogradac & Company LLP, an independent certified public accounting firm, and upon the authority of that firm as an expert in accounting and auditing.

S-17

F-1

F-2

(Unaudited) | ||

| F-99 | ||

Statements of Operations—Six months ended June 30, 2008 and 2007 | F-100 | |

Statements of Cash Flows—Six months ended June 30, 2008 and 2007 | F-101 | |

Pro Forma Financial Information | ||

Apple REIT Nine, Inc. (Unaudited) | ||

Pro Forma Condensed Consolidated Balance Sheet as of June 30, 2008 | F-102 | |

| F-104 | ||

| F-105 | ||

Notes to Pro Forma Condensed Consolidated Statement of Operations | F-108 | |

F-3

CONSOLIDATED BALANCE SHEETS

(in thousands, except share data)

| June 30, 2008 | December 31, 2007 | |||||||

| (unaudited) | ||||||||

ASSETS | ||||||||

Cash | $ | 162,579 | $ | 20 | ||||

Other assets | 242 | 317 | ||||||

Total Assets | $ | 162,821 | $ | 337 | ||||

LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||

Liabilities | ||||||||

Note payable | $ | — | $ | 151 | ||||

Accounts payable and accrued expenses | 51 | 155 | ||||||

Total Liabilities | 51 | 306 | ||||||

Shareholders’ Equity | ||||||||

Preferred stock, authorized 30,000,000 shares; none issued and outstanding | — | — | ||||||

Series A preferred stock, no par value, authorized 400,000,000 shares; issued and outstanding 17,004,557 and 10 shares | — | — | ||||||

Series B convertible preferred stock, no par value, authorized 480,000 shares; issued and outstanding 480,000 shares | 48 | 48 | ||||||

Common stock, no par value, authorized 400,000,000 shares; issued and outstanding 17,004,557 and 10 shares | 163,359 | — | ||||||

Distributions greater than net income | (637 | ) | (17 | ) | ||||

Total Shareholders’ Equity | 162,770 | 31 | ||||||

Total Liabilities and Shareholders’ Equity | $ | 162,821 | $ | 337 | ||||

See accompanying notes to consolidated financial statements.

The Company was initially capitalized on November 9, 2007.

F-4

CONSOLIDATED STATEMENTS OF OPERATIONS

(UNAUDITED)

(in thousands, except per share data)

| Three Months Ended June 30, 2008 | Six Months Ended June 30, 2008 | |||||||

Revenue | $ | — | $ | — | ||||

Expenses: | ||||||||

General and administrative | 94 | 111 | ||||||

Interest income, net | (388 | ) | (385 | ) | ||||

Net income | $ | 294 | $ | 274 | ||||

Basic and diluted earnings per common share | $ | 0.05 | $ | 0.09 | ||||

Weighted average common shares outstanding—basic and diluted | 6,392 | 3,196 | ||||||

Distributions declared and paid per common share | $ | 0.07 | $ | 0.07 | ||||

See accompanying notes to consolidated financial statements.

The Company was initially capitalized on November 9, 2007.

F-5

CONSOLIDATED STATEMENT OF CASH FLOWS

(UNAUDITED)

(in thousands)

| Six Months Ended June 30, 2008 | ||||

Cash flows from operating activities: | ||||

Net income | $ | 274 | ||

Adjustments to reconcile net income to cash provided by operating activities: | ||||

Stock option expense | 26 | |||

Changes in operating assets and liabilities: | ||||

Accounts payable and accrued expenses | 4 | |||

Net cash provided by operating activities: | 304 | |||

Cash flows used in investing activities: | ||||

Deposits and other disbursements for potential acquisitions | (210 | ) | ||

Net cash used in investing activities | (210 | ) | ||

Cash flows from financing activities: | ||||

Net proceeds from issuance of common shares | 163,509 | |||

Distributions paid to common shareholders | (893 | ) | ||

Payoff of the line of credit, net of borrowings | (151 | ) | ||

Net cash provided by financing activities | 162,465 | |||

Increase in cash and cash equivalents | 162,559 | |||

Cash and cash equivalents, beginning of period | 20 | |||

Cash and cash equivalents, end of period | $ | 162,579 | ||

See accompanying notes to consolidated financial statements.

The Company was initially capitalized on November 9, 2007.

F-6

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. BASIS OF PRESENTATION

The accompanying unaudited consolidated financial statements have been prepared in accordance with the rules and regulations for reporting on Form 10-Q. Accordingly, they do not include all of the information required by accounting principles generally accepted in the United States for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. These unaudited financials should be read in conjunction with the Company’s audited consolidated financial statements included in its registration statement filed on Form S-11 with the Securities and Exchange Commission (File No. 333-147414). Operating results for the three months and six months ended June 30, 2008 are not necessarily indicative of the results that may be expected for the twelve month period ending December 31, 2008.

2. ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Organization

Apple REIT Nine, Inc. together with its wholly owned subsidiaries (the “Company”) is a Virginia corporation that intends to qualify as a real estate investment trust (“REIT”) for federal income tax purposes. The Company, which owns no properties and has no operating history, was formed to invest in hotels, residential apartment communities and other income-producing real estate in selected metropolitan areas in the United States. Initial capitalization occurred on November 9, 2007, when 10 Units, each Unit consisting of one common share and one Series A preferred share, were purchased by Apple Nine Advisors, Inc. (“A9A”) and 480,000 Series B convertible preferred shares were purchased by Glade M. Knight, the Company’s Chairman, Chief Executive Officer and President (see Note 4 and 6). The Company’s fiscal year end is December 31. The consolidated financial statements include the accounts of the Company and its subsidiaries. All intercompany accounts and transactions have been eliminated.

Significant Accounting Policies

Cash and Cash Equivalents

Cash and cash equivalents consist of highly liquid investments with original maturities of three months or less. The fair market value of cash and cash equivalents approximates their carrying value. All cash and cash equivalents are currently held at two institutions, Wachovia Bank, N.A. and BB&T Corporation and the balances may at times exceed federal depository insurance limits.

Income Taxes

The Company intends to make an election to be treated, and expects to qualify, as a REIT under the Internal Revenue Code of 1986, as amended. As a REIT, the Company will be allowed a deduction for the amount of dividends paid to its shareholders, thereby subjecting the distributed net income of the Company to taxation only at the shareholder level. The Company’s continued qualification as a REIT will depend on its compliance with numerous requirements, including requirements as to the nature of its income and distribution of dividends.

The Company has established Apple Nine Hospitality Management, Inc. as a 100% owned taxable REIT subsidiary (“TRS”). The TRS will lease all hotels from the Company and be subject to income tax at regular corporate rates on any income that it would earn.

Start Up Costs

Start up costs are expensed as incurred.

F-7

Use of Estimates

The preparation of the financial statements in conformity with United States generally accepted accounting principles requires management to make estimates and assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes. Actual results could differ from those estimates.

Offering Costs

The Company is raising capital through a “best-efforts” offering of Units by David Lerner Associates, Inc., the managing underwriter, which receives a selling commission and a marketing expense allowance based on proceeds of the shares sold. Additionally, the Company has incurred other offering costs including legal, accounting and reporting services. These offering costs are recorded by the Company as a reduction of shareholders’ equity. Prior to the commencement of the Company’s offering, these costs were deferred and recorded as prepaid expense. As of June 30, 2008, the Company had sold 17.0 million Units for gross proceeds of $182.3 million and proceeds net of offering costs of $163.3 million.

Earnings Per Common Share

Basic earnings per common share is computed as net income divided by the weighted average number of common shares outstanding during the year. Diluted earnings per share is calculated after giving effect to all potential common shares that were dilutive and outstanding for the year. There were no shares with a dilutive effect for the three months and six months ended June 30, 2008. Series B convertible preferred shares are not included in earnings per common share calculations until such time that such shares are converted to common shares (see Note 6).

Recent Accounting Pronouncements

In September 2006, the Financial Accounting Standards Board (“FASB”) issued Statement No. 157,Fair Value Measurements (“SFAS 157”). SFAS 157 defines fair value, establishes a framework for measuring fair value and expands disclosures about fair value measurements. The Statement applies under other accounting pronouncements that require or permit fair value measurements. Accordingly, this Statement does not require any new fair value measurements. In February 2008, the FASB released FASB Staff Position (FSP) FAS 157-2—Effective Date of FASB Statement No. 157, which defers the effective date of SFAS 157 to fiscal years beginning after November 15, 2008 for all nonfinancial assets and liabilities, except those items that are recognized or disclosed at fair value in the financial statements on a recurring basis (at least annually). The effective date of the statement related to those items not covered by the deferral (all financial assets and liabilities or nonfinancial assets and liabilities recorded at fair value on a recurring basis) is for fiscal years beginning after November 15, 2007. The adoption of this statement did not have and is not anticipated to have a material impact on the Company’s results of operations and financial position.

In February 2007, FASB issued SFAS No. 159,The Fair Value Option for Financial Assets and Financial Liabilities(“SFAS 159”). SFAS 159 permits entities to choose to measure many financial instruments and certain other items at fair value. The objective of the guidance is to improve financial reporting by providing entities with the opportunity to mitigate volatility in reported earnings caused by measuring related assets and liabilities differently without having to apply complex hedge accounting provisions. SFAS 159 is effective as of the beginning of the first fiscal year that begins after November 15, 2007. SFAS 159 is effective for the Company beginning January 1, 2008. The Company has elected not to use the fair value measurement provisions of SFAS 159 and therefore, adoption of this standard did not have an impact on the financial statements.

In March 2008, FASB issued SFAS No. 161,Disclosures about Derivative Instruments and Hedging Activities, an Amendment of FASB Statement No. 133 (“SFAS 161”). SFAS 161 is intended to improve transparency in financial reporting by requiring enhanced disclosures of an entity’s derivative instruments and hedging activities and their effects on the entity’s financial position, financial performance, and cash flows. SFAS 161 applies to all derivative instruments within the scope of SFAS No. 133,Accounting for Derivative

F-8

Instruments and Hedging Activities (“SFAS 133”). It also applies to non-derivative hedging instruments and all hedged items designated and qualifying as hedges under SFAS 133. SFAS 161 is effective prospectively for financial statements issued for fiscal years and interim periods beginning after November 15, 2008, with early application encouraged. The Company does not currently have any instruments that qualify within the scope of SFAS 133, and therefore the adoption of this statement is not anticipated to have a material impact on the Company’s financial statements.

In May 2008, the FASB issued SFAS No. 162,The Hierarchy of Generally Accepted Accounting Principles (“SFAS 162”). SFAS 162 identifies the sources of accounting principles and the framework for selecting the principles to be used in the preparation of financial statements of nongovernmental entities that are presented in conformity with generally accepted accounting principles in the United States. SFAS 162 is effective 60 days following the Securities and Exchange Commission’s (“SEC”) approval of the Public Company Accounting Oversight Board amendments to AU Section 411, The Meaning of Present Fairly in Conformity with Generally Accepted Accounting Principles. The Company is currently evaluating the potential impact, if any, of the adoption of SFAS 162 on its financial statements.

3. SUMMARY OF POTENTIAL ACQUISITIONS

On June 5, 2008, the Company entered into a purchase contract for the potential acquisition of a Hilton Garden Inn hotel located in Tucson, Arizona. The purchase price for the 125 guest room hotel is $18.4 million, and a refundable deposit of $150,000 was paid by the Company in connection with the contract and is included in other assets in the Company’s consolidated balance sheet as of June 30, 2008 and in deposits and other disbursements for potential acquisitions in the consolidated statement of cash flows. It is expected that the purchase price will be funded from the Company’s cash on hand. While the purchase of the hotel by the Company is expected to occur during 2008, there can be no assurance that all the conditions to closing will be satisfied.

4. RELATED PARTIES

The Company has significant transactions with related parties. These transactions cannot be construed to be at arms length and the results of the Company’s operations may be different than if conducted with non-related parties.

The Company has entered into a Property Acquisition and Disposition Agreement with Apple Suites Realty Group, Inc. (“ASRG”), to acquire and dispose of real estate assets for the Company. A fee of 2% of the gross purchase price or gross sale price in addition to certain reimbursable expenses will be payable for these services. There have been no amounts incurred by the Company under this agreement as of June 30, 2008.

The Company has entered into an advisory agreement with A9A to provide management of the Company and its assets. An annual fee ranging from 0.1% to 0.25% of total equity proceeds received by the Company in addition to certain reimbursable expenses will be payable for these services. A9A has entered into an agreement with Apple REIT Six, Inc. (“AR6”) to provide certain management services to the Company. The Company will reimburse A9A for the cost of the services provided by AR6. Total advisory fees and reimbursable expenses incurred by the Company under the advisory agreement are included in general and administrative expenses and totaled approximately $49,000 for the six months ended June 30, 2008.

ASRG and A9A are 100% owned by Glade M. Knight, Chairman, Chief Executive Officer and President of the Company. ASRG and A9A may purchase in the “best efforts” offering up to 2.5% of the total number of shares sold in the offering.

Mr. Knight is also Chairman and Chief Executive Officer of Apple REIT Six, Inc., Apple REIT Seven, Inc. and Apple REIT Eight, Inc., other REITS. Members of the Company’s Board of Directors are also on the Board of Directors of Apple REIT Six, Inc., Apple REIT Seven, Inc. and Apple REIT Eight, Inc.

F-9

5. STOCK INCENTIVE PLAN

During April 2008, the Company adopted a non-employee directors’ stock incentive plan (the “Directors’ Plan”) to provide incentives to attract and retain directors. The Directors’ Plan provides for the grant of options to purchase a specified number of shares of common stock (“Options”) to directors of the Company. A Compensation Committee (“Committee”) was established to administer the plan. The Committee is responsible for granting Options and for establishing the exercise price of Options. During the second quarter of 2008, the Company issued approximately 32,000 options under the Directors’ Plan and recorded approximately $26,000 in compensation expense.

6. SHAREHOLDERS’ EQUITY

Best-efforts Offering

The Company is currently conducting an on-going best-efforts offering. The Company registered its Units on Registration Statement Form S-11 (File No. 333-147414) filed on April 23, 2008 and was declared effective by the SEC on April 25, 2008. The Company began its best-efforts offering of Units the same day the registration statement was declared effective. The Offering is continuing as of the date of these financial statements. The managing underwriter is David Lerner Associates, Inc. and all of the Units are being sold for the Company’s account.

Each Unit consists of one common share and one Series A preferred share. The Series A preferred shares will have no voting rights, no conversion rights and no distribution rights. The only right associated with the Series A preferred shares will be a priority distribution upon the sale of the Company’s assets. The priority will be equal to $11.00 per Series A preferred share, and no more, before any distributions are made to the holders of any other shares. In the event the Company pays special dividends, the amount of the $11.00 priority will be reduced by the amount of any special dividends approved by the board. The Series A preferred shares will not be separately tradable from the common shares to which they relate.

Series B Convertible Preferred Stock

The Company has authorized 480,000 shares of Series B convertible preferred stock. The Company has issued 480,000 Series B convertible preferred shares to Glade M. Knight, Chairman, Chief Executive Officer and President of the Company, in exchange for the payment by him of $0.10 per Series B convertible preferred share, or an aggregate of $48,000. The Series B convertible preferred shares are convertible into common shares pursuant to the formula and on the terms and conditions set forth below.

There are no dividends payable on the Series B convertible preferred shares. Holders of more than two-thirds of the Series B convertible preferred shares must approve any proposed amendment to the articles of incorporation that would adversely affect the Series B convertible preferred shares.

Upon the Company’s liquidation, the holder of the Series B convertible preferred shares is entitled to a priority liquidation payment before any distribution of liquidation proceeds to the holders of the common shares. However, the priority liquidation payment of the holder of the Series B convertible preferred shares is junior to the holders of the Series A preferred shares distribution rights. The holder of a Series B convertible preferred share is entitled to a liquidation payment of $11 per number of common shares each Series B convertible preferred share would be convertible into according to the formula described below. In the event that the liquidation of the Company’s assets results in proceeds that exceed the distribution rights of the Series A preferred shares and the Series B convertible preferred shares, the remaining proceeds will be distributed between the common shares and the Series B convertible preferred shares, on an as converted basis.

F-10

Each holder of outstanding Series B convertible preferred shares shall have the right to convert any of such shares into common shares of the Company upon and for 180 days following the occurrence of any of the following events:

(1) substantially all of the Company’s assets, stock or business is sold or transferred through exchange, merger, consolidation, lease, share exchange, sale or otherwise, other than a sale of assets in liquidation, dissolution or winding up of the Company;

(2) the termination or expiration without renewal of the advisory agreement, or if the Company ceases to use ASRG to provide property acquisition and disposition services; or

(3) the Company’s common shares are listed on any securities exchange or quotation system or in any established market.

Upon the occurrence of any conversion event, each Series B convertible preferred share may be converted into a number of common shares based upon the gross proceeds raised through the date of conversion in the Company’s $2 billion offering according to the following table:

Gross Proceeds Raised from Sales of Units through Date of Conversion | Number of Common Shares through Conversion of One Series B Convertible Preferred Share | |

| $100 million | 0.92321 | |

| $200 million | 1.83239 | |

| $300 million | 3.19885 | |

| $400 million | 4.83721 | |

| $500 million | 6.11068 | |

| $600 million | 7.29150 | |

| $700 million | 8.49719 | |

| $800 million | 9.70287 | |

| $900 million | 10.90855 | |

| $1 billion | 12.11423 | |

| $1.1 billion | 13.31991 | |

| $1.2 billion | 14.52559 | |

| $1.3 billion | 15.73128 | |

| $1.4 billion | 16.93696 | |

| $1.5 billion | 18.14264 | |

| $1.6 billion | 19.34832 | |

| $1.7 billion | 20.55400 | |

| $1.8 billion | 21.75968 | |

| $1.9 billion | 22.96537 | |

| $2 billion | 24.17104 |

In the event that after raising gross proceeds of $2 billion, the Company raises additional gross proceeds in a subsequent public offering, each Series B convertible preferred share may be converted into an additional number of common shares based on the additional gross proceeds raised through the date of conversion in a subsequent public offering according to the following formula: (X/100 million) x 1.20568, where X is the additional gross proceeds rounded down to the nearest 100 million.

No additional consideration is due upon the conversion of the Series B convertible preferred shares. The conversion into common shares of the Series B convertible preferred shares will result in dilution of the shareholders’ interests.

Expense related to the issuance of 480,000 Series B convertible preferred shares to Mr. Knight will be recognized at such time when the number of common shares to be issued for conversion of the Series B shares

F-11

can be reasonably estimated and the event triggering the conversion of the Series B shares to common shares occurs. The expense will be measured as the difference between the fair value of the common stock for which the Series B shares can be converted and the amounts paid for the Series B shares. Although the fair market value cannot be determined at this time, expense if the maximum offering is achieved could range from $0 to in excess of $127 million (assumes $11 per unit fair market value).

7. LINE OF CREDIT

Prior to the commencement of the Company’s “best-efforts” offering, the Company obtained an unsecured line of credit in a principal amount of $400,000 to fund certain start-up costs and offering expenses. The lender was Wachovia Bank, N.A. The line of credit bore interest at a variable rate based on the London Interbank Borrowing Rate (LIBOR). The line of credit was fully paid during May 2008 with net proceeds from the Company’s “best-efforts” offering.

8. SUBSEQUENT EVENTS

In July 2008, the Company declared and paid approximately $1.2 million in dividend distributions to its common shareholders, or $0.073334 per outstanding common share.

During July 2008, the Company closed on the issuance of 4.2 million Units through its ongoing “best-efforts” offering, representing gross proceeds to the Company of $45.8 million and proceeds net of selling and marketing costs of $41.2 million.

On July 24, 2008, the Company entered into a purchase contract for the potential acquisition of a Courtyard hotel in Santa Clarita, California. The gross purchase price for the 140 room hotel is $22.7 million, and a refundable deposit of $200,000 was paid by the Company in connection with the contract.

On July 31, 2008, the Company closed on the purchase of a Hilton Garden Inn located in Tucson, Arizona. The gross purchase price for this hotel, which contains a total of 125 guest rooms, was $18.4 million.

On August 1, 2008, the Company entered into a purchase contract for the potential acquisition of a Homewood Suites hotel in Charlotte, North Carolina. The gross purchase price for the 112 room hotel is $5.8 million, and a refundable deposit of $200,000 was paid by the Company in connection with the contract.

On August 1, 2008, the Company entered into five separate purchase contracts with a group of related sellers for the potential acquisition of five hotels. The purchase contracts are for a 142 room Hilton Garden Inn in Twinsburg, Ohio with a purchase price of $16.5 million, a 165 room Hilton Garden Inn in Lewisville, Texas with a purchase price of $28.0 million, a 142 room Hilton Garden Inn in Duncanville, Texas with a purchase price of $19.5 million, a 103 room Hampton Inn and Suites in Allen, Texas with a purchase price of $12.5 million and a 150 room Hilton Garden Inn in Allen, Texas with a purchase price of $18.5 million. The initial refundable deposit under each separate contract was $200,000.

F-12

REPORT OF INDEPENDENT AUDITORS

Board of Directors

Apple REIT Nine, Inc.

We have audited the accompanying balance sheet of the Tucson, AZ—Hilton Garden Inn Hotel (the “Hotel”) as of December 31, 2007, and the related statement of operations, cash flows, and owners’ equity for the year then ended. These financial statements are the responsibility of the Hotel’s management. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. We were not engaged to perform an audit of the Hotel’s internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Hotel’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Tucson, AZ—Hilton Garden Inn Hotel as of December 31, 2007 and the results of its operations and its cash flows for the year then ended in conformity with U.S. generally accepted accounting principles.

/s/ Ernst & Young LLP

Richmond, Virginia

September 29, 2008

F-13

TUCSON, AZ—HILTON GARDEN INN HOTEL

BALANCE SHEET

| December 31 2007 | |||

ASSETS | |||

Cash and cash equivalents | $ | 205,722 | |

Prepaid expenses and other assets, net | 139,991 | ||

Investment in real estate | 13,097,129 | ||

Total assets | $ | 13,442,842 | |

LIABILITIES AND OWNERS’ EQUITY | |||

Accounts payable and other liabilities | $ | 2,196,567 | |

Mortgage payable | 8,328,567 | ||

Total liabilities | 10,525,134 | ||

Owners’ equity | 2,917,708 | ||

Total liabilities and owners’ equity | $ | 13,442,842 | |

See accompanying notes.

F-14

TUCSON, AZ—HILTON GARDEN INN HOTEL

STATEMENT OF OPERATIONS

| Year Ended December 31 2007 | ||||

REVENUES | ||||

Rooms | $ | — | ||

Other income | — | |||

Total revenues | — | |||

OPERATING EXPENSES | ||||

Real estate taxes, insurance and other | 807 | |||

Administrative | 6,298 | |||

Total operating expenses | 7,105 | |||

OTHER INCOME | ||||

Interest income | 1,413 | |||

Net loss | $ | (5,692 | ) | |

See accompanying notes.

F-15

TUCSON, AZ—HILTON GARDEN INN HOTEL

OWNERS’ EQUITY

| Year Ended December 31 2007 | ||||

Owners’ equity at beginning of period | $ | 2,728,244 | ||

Contributions by owners | 195,156 | |||

Net loss | (5,692 | ) | ||

Owners’ equity at end of period | $ | 2,917,708 | ||

See accompanying notes.

F-16

TUCSON, AZ—HILTON GARDEN INN HOTEL

STATEMENT OF CASH FLOWS

| Year Ended December 31 2007 | ||||

CASH FLOWS FROM OPERATING ACTIVITIES | ||||

Net loss | $ | (5,692 | ) | |

Adjustments to reconcile net loss to net cash provided by operating activities: | ||||

Changes in operating assets and liabilities: | ||||

Prepaid expenses and other assets | 23,908 | |||

Net cash provided by operating activities | 18,216 | |||

CASH FLOWS FROM INVESTING ACTIVITIES | ||||

Purchase of property and equipment, including construction-in-progress | (7,958,358 | ) | ||

Net cash used in investing activities | (7,958,358 | ) | ||

CASH FLOWS FROM FINANCING ACTIVITIES | ||||

Proceeds from mortgage payable | 7,468,195 | |||

Capital contributions | 195,156 | |||

Net cash provided by financing activities | 7,663,351 | |||