UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | | | | | |

| | | (Mark One) | | |

| | | [ ü ] | | ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE | | |

| | | | | SECURITIES EXCHANGE ACT OF 1934 | | |

| | | | | For the fiscal year ended JUNE 29, 2008 | | |

| | | | | OR | | |

| | | [ ] | | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE | | |

| | | | | SECURITIES EXCHANGE ACT OF 1934 | | |

| | | | | For the transition period from to | | |

Commission file number 1-1370

BRIGGS & STRATTON CORPORATION

(Exact name of registrant as specified in its charter)

| | |

| A Wisconsin Corporation | | 39-0182330 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| |

12301 WEST WIRTH STREET WAUWATOSA, WISCONSIN | | 53222 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: 414-259-5333

Securities registered pursuant to Section 12(b) of the Act:

| | |

| Title of Each Class | | Name of Each Exchange on Which Registered |

| Common Stock (par value $0.01 per share) | | New York Stock Exchange |

| Common Share Purchase Rights | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ü No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No ü

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ü No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ü ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ü Accelerated filer Smaller reporting company

Non-accelerated filer (Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes No ü

The aggregate market value of Common Stock held by nonaffiliates of the registrant was approximately $1.08 billion based on the reported last sale price of such securities as of December 28, 2007, the last business day of the most recently completed second fiscal quarter.

Number of Shares of Common Stock Outstanding at August 25, 2008: 49,812,479.

DOCUMENTS INCORPORATED BY REFERENCE

| | |

| Document | | Part of Form 10-K Into Which Portions of Document are Incorporated |

Proxy Statement for Annual Meeting on October 15, 2008 | | Part III |

| |

| The Exhibit Index is located on page 62. | | |

BRIGGS & STRATTON CORPORATION

FISCAL 2008 FORM 10-K

TABLE OF CONTENTS

Cautionary Statement on Forward-Looking Statements

This release contains certain forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from those projected in the forward-looking statements. The words “anticipate”, “believe”, “estimate”, “expect”, “forecast”, “intend”, “may”, “objective”, “plan”, “project”, “seek”, “think”, “will”, and similar expressions are intended to identify forward-looking statements. The forward-looking statements are based on the Company’s current views and assumptions and involve risks and uncertainties that include, among other things, the ability to successfully forecast demand for our products and appropriately adjust our manufacturing and inventory levels; changes in our operating expenses; changes in interest rates; the effects of weather on the purchasing patterns of consumers and original equipment manufacturers (OEMs); actions of engine manufacturers and OEMs with whom we compete; the seasonal nature of our business; changes in laws and regulations, including environmental, tax, pension funding and accounting standards; work stoppages or other consequences of any deterioration in our employee relations; work stoppages by other unions that affect the ability of suppliers or customers to manufacture; acts of war or terrorism that may disrupt our business operations or those of our customers and suppliers; changes in customer and OEM demand; changes in prices of raw materials and parts that we purchase; changes in domestic economic conditions, including housing starts and changes in consumer disposable income and sentiment; changes in foreign economic conditions, including currency rate fluctuations; the actions of customers of our OEM customers; the ability to bring new productive capacity on line efficiently and with good quality; the ability to successfully realize the maximum market value of assets that may require disposal if products or production methods change; new facts that come to light in the future course of litigation proceedings which could affect our assessment of those matters; and other factors that may be disclosed from time to time in our SEC filings or otherwise, including the factors discussed in Item 1A, Risk Factors, of the Company’s Annual Report on Form 10-K and in its periodic reports on Form 10-Q. Some or all of the factors may be beyond our control. We caution you that any forward-looking statement reflects only our belief at the time the statement is made. We undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made.

PART I

Briggs & Stratton (the “Company”) is the world’s largest producer of air cooled gasoline engines for outdoor power equipment. Briggs & Stratton designs, manufactures, markets and services these products for original equipment manufacturers (OEMs) worldwide. These engines are aluminum alloy gasoline engines with displacements ranging from 31 cubic centimeters to 993 cubic centimeters.

Additionally, through its wholly owned subsidiary, Briggs & Stratton Power Products Group, LLC, Briggs & Stratton is a leading designer, manufacturer and marketer of generators (portable and home standby), pressure washers, air compressors, snow throwers, lawn and garden powered equipment (riding and walk behind mowers, tillers, chipper/shredders, leaf blowers and vacuums) and related accessories.

Briggs & Stratton conducts its operations in two reportable segments: Engines and Power Products. Further information about Briggs & Stratton’s business segments is contained in Note 6 of the Notes to Consolidated Financial Statements.

The Company’s Internet address is www.briggsandstratton.com. The Company makes available free of charge (other than an investor’s own Internet access charges) through its Internet website the Company’s Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as soon as reasonably practicable after it electronically files such material with, or furnishes such material to, the Securities and Exchange Commission. Charters of the Audit, Compensation, Nominating and Governance Committees; Corporate Governance Guidelines and code of business conduct and ethics contained in the Briggs & Stratton Business Integrity Manual are available on the Company’s website and are available in print to any shareholder upon request to the Corporate Secretary.

Engines

General

Briggs & Stratton’s engines are used primarily by the lawn and garden equipment industry, which accounted for 82% of the segment’s fiscal 2008 engine sales to OEMs. Major lawn and garden equipment applications include walk-behind lawn mowers, riding lawn mowers, garden tillers and snow throwers. The remaining 18% of engine sales to OEMs in fiscal 2008 were for use on products for industrial, construction, agricultural and other consumer applications, that include generators, pumps and pressure washers. Many retailers specify Briggs & Stratton’s engines on the powered equipment they sell, and the Briggs & Stratton name is often featured prominently on a product despite the fact that the engine is only a component.

In fiscal 2008, approximately 33% of Briggs & Stratton’s Engines Segment net sales were derived from sales in international markets, primarily to customers in Europe. Briggs & Stratton serves its key international markets through its European regional office in Switzerland, its distribution center in the Netherlands and sales and service subsidiaries and offices in Australia, Austria, Brazil, Canada, China, the Czech Republic, England, France, Germany, Italy, Japan, Mexico, New Zealand, Poland, Russia, South Africa, Spain, Sweden and the United Arab Emirates. Briggs & Stratton is a leading supplier of gasoline engines in developed countries where there is an established lawn and garden equipment market. Briggs & Stratton also exports engines to developing nations where its engines are used in agricultural, marine, construction and other applications. More detailed information about our foreign operations is in Note 6 of the Notes to Consolidated Financial Statements.

Briggs & Stratton engines are sold primarily by its worldwide sales force through direct calls on customers. Briggs & Stratton’s marketing staff and engineers in the United States provide support and technical assistance to its sales force.

Briggs & Stratton also manufactures replacement engines and service parts and sells them to sales and service distributors. Briggs & Stratton owns its principal international distributors. In the United States the distributors are independently owned and operated. These distributors supply service parts and replacement engines directly to independently owned, authorized service dealers throughout the world. These distributors and service dealers implement Briggs & Stratton’s commitment to reliability and service.

1

Customers

Briggs & Stratton’s engine sales are made primarily to OEMs. Briggs & Stratton’s three largest external engine customers in fiscal years 2008, 2007 and 2006 were Husqvarna Outdoor Products Group (HOP), MTD Products Inc. (MTD) and Deere & Company. Sales to the top three customers combined were 42%, 54% and 51% of Engines Segment net sales in fiscal 2008, 2007 and 2006, respectively. Under purchasing plans available to all of its gasoline engine customers, Briggs & Stratton typically enters into annual engine supply arrangements.

Briggs & Stratton believes that in fiscal 2008 more than 80% of all lawn and garden powered equipment sold in the United States was sold through mass merchandisers such as Sears Holdings Corporation (Sears), The Home Depot, Inc. (The Home Depot), Wal-Mart Stores, Inc. (Wal-Mart) and Lowe’s Companies, Inc. (Lowe’s). Given the buying power of the mass merchandisers, Briggs & Stratton, through its customers, has continued to experience pricing pressure; however, the Company attempts to recover increases in commodity costs through increased pricing. Briggs & Stratton believes that a similar trend has developed for its products in industrial and consumer applications outside of the lawn and garden market.

Competition

Briggs & Stratton’s major domestic competitors in engine manufacturing are Honda Motor Co., Ltd. (Honda), Kawasaki Heavy Industries, Ltd. (Kawasaki) and Kohler Co. (Kohler). Several Japanese and Chinese small engine manufacturers, of which Honda and Kawasaki are the largest, compete directly with Briggs & Stratton in world markets in the sale of engines to other OEMs and indirectly through their sale of end products.

Briggs & Stratton believes it has a significant share of the worldwide market for engines that power outdoor equipment.

Briggs & Stratton believes the major areas of competition from all engine manufacturers include product quality, brand strength, price, timely delivery and service. Other factors affecting competition are short-term market share objectives, short-term profit objectives, exchange rate fluctuations, technology, product support and distribution strength. Briggs & Stratton believes its product value and service reputation have given it strong brand name recognition and enhance its competitive position.

Seasonality of Demand

Sales of engines to lawn and garden OEMs are highly seasonal because of consumer buying patterns. The majority of lawn and garden equipment is sold during the spring and summer months when most lawn care and gardening activities are performed. Sales of lawn and garden equipment are also influenced by weather conditions. Engine sales in Briggs & Stratton’s fiscal third quarter have historically been the highest, while sales in the first fiscal quarter have historically been the lowest.

In order to efficiently use its capital investments and meet seasonal demand for engines, Briggs & Stratton pursues a relatively balanced production schedule throughout the year. The schedule is adjusted to reflect changes in estimated demand, customer inventory levels and other matters outside the control of Briggs & Stratton. Accordingly, inventory levels generally increase during the first and second fiscal quarters in anticipation of customer demand. Inventory levels begin to decrease as sales increase in the third fiscal quarter. This seasonal pattern results in high inventories and low cash flow for Briggs & Stratton in the second and the beginning of the third fiscal quarters. The pattern results in higher cash flow in the latter portion of the third fiscal quarter and in the fourth fiscal quarter as inventories are liquidated and receivables are collected.

Manufacturing

Briggs & Stratton manufactures engines and parts at the following locations: Auburn, Alabama; Statesboro, Georgia; Murray, Kentucky; Poplar Bluff, Missouri; Wauwatosa, Wisconsin; Chongqing, China; and Ostrava, Czech Republic. Briggs & Stratton has a parts distribution center in Menomonee Falls, Wisconsin.

As announced in April 2007, the Company discontinued operations at our Rolla, Missouri facility during the second fiscal quarter of 2008. Engine manufacturing performed in Rolla has been moved to the Chongqing, China and Poplar Bluff, Missouri plants.

Briggs & Stratton manufactures a majority of the structural components used in its engines, including aluminum die castings, carburetors and ignition systems. Briggs & Stratton purchases certain parts such as piston rings, spark plugs, valves, ductile and grey iron castings, plastic components, some stampings and

2

screw machine parts and smaller quantities of other components. Raw material purchases consist primarily of aluminum and steel. Briggs & Stratton believes its sources of supply are adequate.

Briggs & Stratton has joint ventures with Daihatsu Motor Company for the manufacture of engines in Japan, with Starting Industrial of Japan for the production of rewind starters and punch press components in the United States, and The Toro Company for the manufacture of two-cycle engines in China.

Briggs & Stratton has a strategic relationship with Mitsubishi Heavy Industries (MHI) for the global distribution of air cooled gasoline engines manufactured by MHI in Japan under Briggs & Stratton’s Vanguard™ brand.

Power Products

General

Briggs & Stratton Power Products Group, LLC’s (BSPPG) principal product lines include portable and standby generators, pressure washers, snow throwers and lawn and garden powered equipment. BSPPG sells its products through multiple channels of retail distribution, including consumer home centers, warehouse clubs, mass merchants and independent dealers. BSPPG product lines are marketed under various brands including Briggs & Stratton, Brute, Craftsman®, Ferris, Giant Vac, John Deere, Murray, Simplicity, Snapper and Troy-Bilt®.

BSPPG has a network of independent dealers worldwide for the sale and service of snow throwers and lawn and garden powered equipment.

To support its international business, BSPPG has leveraged the existing Briggs & Stratton worldwide distribution network.

Customers

Historically, BSPPG’s major customers have been Lowe’s, The Home Depot and Sears. Other U.S. customers include Wal-Mart, Deere & Company, Pace Inc., Tractor Supply Inc., Costco Wholesale, and a network of independent dealers.

Competition

The principal competitive factors in the power products industry include price, service, product performance, technical innovation and delivery. BSPPG has various competitors, depending on the type of equipment. Primary competitors include: Honda (portable generators, pressure washers and lawn and garden equipment), Generac Power Systems, Inc. (“Generac”) (standby generators), Alfred Karcher GmbH & Co. (pressure washers), Techtronic Industries (pressure washers), Deere & Company (commercial and consumer lawn mowers), MTD (consumer and commercial lawn mowers), the Toro Company (commercial and consumer lawn mowers), Scag Power Equipment, a Division of Metalcraft of Mayville, Inc. (commercial lawn mowers), and Husqvarna Outdoor Power Equipment (consumer and commercial lawn mowers).

BSPPG believes it has a significant share of the North American market for portable generators and consumer pressure washers.

Seasonality of Demand

Sales of BSPPG’s products are subject to seasonal patterns. Due to seasonal and regional weather factors, sales of pressure washers and lawn and garden powered equipment are typically higher during the fiscal third and fourth quarters than at other times of the year. Sales of portable generators and snow throwers are typically higher during the first and second fiscal quarters.

Manufacturing

BSPPG’s manufacturing facilities are located in Jefferson, Watertown and Port Washington, Wisconsin; McDonough, Georgia; Munnsville, New York; Newbern, Tennessee; and Qingpu, China. BSPPG also purchases certain powered equipment under contract manufacturing agreements.

BSPPG plans to close its Port Washington, Wisconsin manufacturing facility during the second quarter of fiscal 2009. Production will move to the McDonough, Georgia facility.

BSPPG manufactures core components for its products, where such integration improves operating profitability by providing lower costs.

3

BSPPG purchases engines from its parent, Briggs & Stratton, as well as from Honda, Kawasaki and Kohler. BSPPG has not experienced any difficulty obtaining necessary engines or other purchased components.

BSPPG assembles products for the international markets at its U.S. and China locations and through contract manufacturing agreements with other OEMs.

Consolidated

General Information

Briggs & Stratton holds patents on features incorporated in its products; however, the success of Briggs & Stratton’s business is not considered to be primarily dependent upon patent protection. The Company owns several trademarks which it believes significantly affect a consumer’s choice of outdoor powered equipment and therefore create value. Licenses, franchises and concessions are not a material factor in Briggs & Stratton’s business.

For the fiscal years ended June 29, 2008, July 1, 2007 and July 2, 2006, Briggs & Stratton spent approximately $26.5 million, $25.7 million and $28.8 million, respectively, on research activities relating to the development of new products or the improvement of existing products.

The average number of persons employed by Briggs & Stratton during fiscal 2008 was 7,202. Employment ranged from a low of 7,071 in October 2007 to a high of 7,388 in April 2008.

Export Sales

Export sales for fiscal 2008, 2007 and 2006 were $476.3 million (22% of net sales), $490.7 million (23% of net sales) and $527.0 million (21% of net sales), respectively. These sales were principally to customers in European countries. Refer to Note 6 of the Notes to Consolidated Financial Statements for financial information about geographic areas. Also, refer to Item 7A of this Form 10-K and Note 13 of the Notes to Consolidated Financial Statements for information about Briggs & Stratton’s foreign exchange risk management.

In addition to the risks referred to elsewhere in this Annual Report on Form 10-K, the following risks, among others, may have affected, and in the future could affect, the Company and its subsidiaries’ business, financial condition or results of operations. Additional risks not discussed or not presently known to the Company or that the Company currently deems insignificant may also impact its business and stock price.

Demand for products fluctuates significantly due to seasonality. In addition, changes in the weather and consumer confidence impact demand.

Sales of our products are subject to seasonal and consumer buying patterns. Consumer demand in our markets can be reduced by unfavorable weather and weak consumer confidence. We manufacture throughout the year although our sales are concentrated in the second half of our fiscal year. This operating method requires us to anticipate demand of our customers many months in advance. If we overestimate or underestimate demand during a given year, we may not be able to adjust our production quickly enough to avoid excess or insufficient inventories, and that may in turn limit our ability to maximize our potential sales.

We have only a limited ability to pass through cost increases in our raw materials to our customers during the year.

We generally enter into annual purchasing plans with our largest customers, so our ability to raise our prices during a particular year to reflect increased raw materials costs is limited.

A significant portion of our net sales comes from major customers and the loss of any of these customers would negatively impact our financial results.

In fiscal 2008, our three largest customers accounted for 28% of our consolidated net sales. The loss of a significant portion of the business of one or more of these key customers would significantly impact our net sales and profitability.

4

Changes in environmental or other laws could require extensive changes in our operations or to our products.

Our operations and products are subject to a variety of foreign, federal, state and local laws and regulations governing, among other things, emissions to air, discharges to water, noise, the generation, handling, storage, transportation, treatment and disposal of waste and other materials and health and safety matters. Additional engine emission regulations were phased in through 2008 by the State of California, and will be phased in between 2009 and 2012 by the U.S. Environmental Protection Agency. We do not expect these changes to have a material adverse effect on us, but we cannot be certain that these or other proposed changes in applicable laws or regulations will not adversely affect our business or financial condition in the future.

Foreign economic conditions and currency rate fluctuations can reduce our sales.

In fiscal 2008, we derived approximately 26% of our consolidated net sales from international markets, primarily Europe. Weak economic conditions in Europe could reduce our sales and currency fluctuations could adversely affect our sales or profit levels in U.S. dollar terms.

Actions of our competitors could reduce our sales or profits.

Our markets are highly competitive and we have a number of significant competitors in each market. Competitors may reduce their costs, lower their prices or introduce innovative products that could hurt our sales or profits. In addition, our competitors may focus on reducing our market share to improve their results.

Disruptions caused by labor disputes or organized labor activities could harm our business.

A portion of our workforce is currently represented by labor unions. In addition, we may from time to time experience union organizing activities in our non-union facilities. Disputes with the current labor union or new union organizing activities could lead to work slowdowns or stoppages and make it difficult or impossible for us to meet scheduled delivery times for product shipments to our customers, which could result in loss of business. In addition, union activity could result in higher labor costs, which could harm our financial condition, results of operations and competitive position.

As of June 29, 2008, we had approximately $365.6 million of long-term debt. In addition, we have the ability to incur additional borrowings on our revolving credit facility. This level of debt could adversely affect our operating flexibility and put us at a competitive disadvantage.

Our level of debt and the limitations imposed on us by the indentures for the notes and our other credit agreements could have important consequences, including the following:

| • | | we will have to use a portion of our cash flow from operations for debt service rather than for our operations; |

| • | | we may not be able to obtain additional debt financing for future working capital, capital expenditures or other corporate purposes or may have to pay more for such financing; |

| • | | some or all of the debt under our current or future revolving credit facilities will be at a variable interest rate, making us more vulnerable to increases in interest rates; |

| • | | we could be less able to take advantage of significant business opportunities, such as acquisition opportunities, and to react to changes in market or industry conditions; |

| • | | we will be more vulnerable to general adverse economic and industry conditions; and |

| • | | we may be disadvantaged compared to competitors with less leverage. |

The terms of the indentures for the senior notes do not fully prohibit us from incurring substantial additional debt in the future and our revolving credit facilities permit additional borrowings, subject to certain conditions. If new debt is added to our current debt levels, the related risks we now face could intensify.

We expect to obtain the money to pay our expenses and to pay the principal and interest on the outstanding 8.875% senior notes, the credit facilities and other debt primarily from our operations. Our ability to meet our expenses thus depends on our future performance, which will be affected by financial, business, economic and other factors. We will not be able to control many of these factors, such as economic conditions in the markets where we operate and pressure from competitors. We cannot be certain that the money we earn will be sufficient to allow us to pay principal and interest on our debt and meet our other obligations. If we do not have enough money, we may be required to refinance all or part of our existing debt, sell assets or borrow more money. We cannot guarantee that we will be able to do so on terms acceptable to us. In addition, the

5

terms of existing or future debt agreements, including the revolving credit facilities and our indentures, may restrict us from adopting any of these alternatives.

We are restricted by the terms of the outstanding senior notes and our other debt, which could adversely affect us.

The indentures relating to the senior notes and our revolving credit agreement include a number of financial and operating restrictions, which may prevent us from capitalizing on business opportunities and taking some corporate actions. These covenants could adversely affect us by limiting our ability to plan for or react to market conditions or to meet our capital needs. These covenants include, among other things, restrictions on our ability to:

| • | | pay dividends or make distributions in respect of our capital stock or to make certain other restricted payments; |

| • | | incur indebtedness or issue preferred shares; |

| • | | make loans or investments; |

| • | | enter into sale and leaseback transactions; |

| • | | agree to payment restrictions affecting our restricted subsidiaries; |

| • | | consolidate, merge, sell or lease all or substantially all of our assets; |

| • | | enter into transactions with affiliates; and |

| • | | dispose of assets or the proceeds of sales of our assets. |

In addition, our revolving credit facility contains financial covenants that, among other things, require us to maintain a minimum interest coverage ratio and impose a maximum leverage ratio.

Our failure to comply with restrictive covenants under the indentures governing the senior notes and our revolving credit facility could trigger prepayment obligations.

Our failure to comply with the restrictive covenants described above could result in an event of default, which, if not cured or waived, could result in us being required to repay these borrowings before their due date. If we are forced to refinance these borrowings on less favorable terms, our results of operations and financial condition could be adversely affected by increased costs and rates.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

The corporate offices and one of Briggs & Stratton’s engine manufacturing facilities are located in Wauwatosa, Wisconsin. Briggs & Stratton also has engine manufacturing facilities in Auburn, Alabama; Statesboro, Georgia; Murray, Kentucky; Poplar Bluff, Missouri; Ostrava, Czech Republic and Chongqing, China. These are owned facilities containing approximately 2.9 million square feet of office and production area. Briggs & Stratton leases warehouse space in the localities of its engine manufacturing facilities, except China, totaling approximately 662,000 square feet. Additionally, a service parts distribution center consisting of approximately 299,000 square feet is leased in Menomonee Falls, Wisconsin.

BSPPG maintains office space and manufacturing facilities in Brookfield, Jefferson, Watertown and Port Washington, Wisconsin; McDonough, Georgia; Newbern, Tennessee; Munnsville, New York and Qingpu, China. Of these, the domestic facilities, except Brookfield, Wisconsin and Newbern, Tennessee, are owned and contain approximately 1.6 million square feet. The Brookfield, Wisconsin office space is leased and contains approximately 26,000 square feet; the Newbern, Tennessee office space and manufacturing facilities are also leased and contain approximately 267,500 square feet. BSPPG also leases warehouse space in Jefferson, Watertown and Fort Atkinson, Wisconsin; McDonough, Georgia; Grand Prairie, Texas; Greenville, Ohio; Reno, Nevada; and Sherrill, New York totaling approximately 1.8 million square feet. Additionally, the Qingpu, China facility is leased and contains approximately 47,000 square feet.

6

Briggs & Stratton leases approximately 312,000 square feet of space to house its foreign sales and service operations.

As Briggs & Stratton’s business is seasonal, additional warehouse space may be leased when inventory levels are at their peak. Briggs & Stratton’s owned properties are well maintained. Briggs & Stratton believes that its owned and leased facilities are adequate to perform its operations in a reasonable manner.

Briggs & Stratton is subject to various unresolved legal actions that arise in the normal course of its business. These actions typically relate to product liability (including asbestos-related liability), patent and trademark matters, and disputes with customers, suppliers, distributors and dealers, competitors and employees.

On June 3, 2004, eight individuals who claim to have purchased lawnmowers in Illinois and Minnesota filed a lawsuit (Ronnie Phillips et al. v. Sears Roebuck Corporation et al., No. 04-L-334 (20th Judicial Circuit, St. Clair County, IL)) against Briggs & Stratton and other defendants alleging that the horsepower labels on the products they purchased were inaccurate. The plaintiffs sought an injunction, compensatory and punitive damages, and attorneys’ fees under various federal and state laws including the Racketeer Influenced and Corrupt Organization Act (RICO) on behalf of all persons in the United States who, beginning January 1, 1994 through the present, purchased a lawnmower containing a two-stroke or four-stroke gasoline combustion engine up to 30 horsepower that was manufactured by the defendants. On May 31, 2006, the defendants removed the case to the U.S. District Court for the Southern District of Illinois (No. 06-412-DRH).

The defendants subsequently filed a motion to dismiss the amended complaint, and two defendants (MTD Products, Inc. and American Honda Motor Company) notified the Court that they reached a settlement with the plaintiff class. On March 30, 2007, the Court issued an order granting the defendants’ motion to dismiss, and on May 8, 2008 the Court issued an opinion that (i) dismissed all the RICO claims with prejudice; (ii) dismissed all claims of the 93 non-Illinois plaintiffs with instructions to refile amended claims in individual state courts; (iii) ordered that any amended complaint for the three Illinois plaintiffs be refiled by May 30, 2008; and (iv) rejected the proposed class-wide settlement with MTD. The plaintiffs have filed new complaints in New Jersey and California federal courts, and refiled an amended complaint in Illinois. Each of these complaints allege, among other things, breach of each state’s consumer fraud laws and seek certification of a state-wide class.

On June 2, 2008, plaintiffs in the New Jersey action, the California action, and the Illinois action filed a motion with the Judicial Panel of Multidistrict Litigation seeking to transfer the three actions to the United States District Court for the District of New Jersey for coordinated pretrial proceedings. Counsel for plaintiffs have represented that they would be filing related actions across the country “and expect to have actions pending in all fifty states and the District of Columbia.” On August 12, 2008 the Multidistrict Litigation Panel denied plantiffs’ request for centralization of these various state proceedings. Defendents’ answers or responsive pleadings in each of the separate federal cases are currently due September 26, 2008.

Although it is not possible to predict with certainty the outcome of these unresolved legal actions or the range of possible loss, Briggs & Stratton believes the unresolved legal actions will not have a material effect on its financial position.

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

No matters were submitted to a vote of security holders, through the solicitation of proxies or otherwise, during the three months ended June 29, 2008.

7

| | |

Executive Officers of the Registrant | | |

| |

Name, Age, Position | | Business Experience for Past Five Years |

| |

JOHN S. SHIELY, 56 Chairman and Chief Executive Officer (1)(2)(3) | | Mr. Shiely was elected to his current position effective September 2008, after serving as Chairman, President and Chief Executive Officer since January 2003. |

| |

TODD J. TESKE, 43 President and Chief Operating Officer | | Mr. Teske was elected to his current position effective September 2008 after serving as Executive Vice President and Chief Operating Officer since September 2005. He previously served as Senior Vice President and President – Briggs & Stratton Power Products Group, LLC from September 2003 to August 2005. |

| |

JAMES E. BRENN, 60 Senior Vice President and Chief Financial Officer | | Mr. Brenn was elected to his current position in October 1998, after serving as Vice President and Controller since November 1988. |

| |

DAVID G. DEBAETS, 45 Vice President – North American Operations (Engine Power Products Group) | | Mr. DeBaets was elected to his current position effective September 2007. He has served as Vice President and General Manager – Large Engine Division since April 2000. |

| |

ROBERT F. HEATH, 60 Secretary | | Mr. Heath was elected to his current position in January 2002. In addition, Mr. Heath is Vice President and General Counsel and has served in these positions since January 2001. |

| |

HAROLD L. REDMAN, 44 Vice President and President – Home Power Products Group | | Mr. Redman was elected to his current position effective September 2006. He has served as Vice President and President – Home Power Products since May 2006. He also served as Senior Vice President – Sales & Marketing – Simplicity Manufacturing, Inc. since July 1995. |

| |

WILLIAM H. REITMAN, 52 Senior Vice President – Sales & Customer Support | | Mr. Reitman was elected to his current position effective September 2007, after serving as Senior Vice President – Sales & Marketing since May 2006, and Vice President – Sales & Marketing since October 2004. He also served as Vice President – Marketing since November 1995. |

| |

DAVID J. RODGERS, 37 Controller | | Mr. Rodgers was elected as an executive officer in September 2007 and has served as Controller since December 2006. He was previously employed by Roundy’s Supermarkets, Inc. as Vice President – Controller from September 2005 to November 2006 and Vice President – Retail Controller from May 2003 to August 2005. |

| |

THOMAS R. SAVAGE, 60 Senior Vice President – Administration | | Mr. Savage was elected to his current position effective July 1997. |

| |

MICHAEL D. SCHOEN, 48 Senior Vice President – Operations Support | | Mr. Schoen was elected to his current position effective December 2007 after serving as Senior Vice President and President – International Power Products Group since September 2005. He also served as Vice President – International Group since July 2001. |

| |

VINCENT R. SHIELY, 48 Senior Vice President and President – Yard Power Products Group (3) | | Mr. Shiely was elected to his current position effective May 2006, after serving as Vice President and President – Home Power Products Group since September 2005. He also served as Vice President and General Manager – Home Power Products Division October 2004 to September 2005. He previously served as Vice President and General Manager – Engine Products Group since September 2002. |

8

| | |

CARITA R. TWINEM, 53 Treasurer | | Ms. Twinem was elected to her current position in February 2000. In addition, Ms. Twinem is Tax Director and has served in this position since July 1994. |

| |

JOSEPH C. WRIGHT, 49 Senior Vice President and President – Engine Power Products Group | | Mr. Wright was elected to his current position in May 2006 after serving as Vice President and President – Yard Power Products Group since September 2005. He also served as Vice President and General Manager – Lawn and Garden Division from September 2004 to September 2005. He was elected an executive officer effective September 2002. |

(1) Officer is also a Director of Briggs & Stratton.

(2) Member of the Board of Directors Executive Committee.

(3) John S. Shiely and Vincent R. Shiely are brothers.

Officers are elected annually and serve until they resign, die, are removed, or a different person is appointed to the office.

PART II

| ITEM 5. | MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Briggs & Stratton common stock and its common share purchase rights are traded on the NYSE under the symbol “BGG”. Information required by this Item is incorporated by reference from the “Quarterly Financial Data, Dividend and Market Information” (unaudited) on page 60.

Changes in Securities, Use of Proceeds and Issuer Purchases of Equity Securities

Briggs & Stratton did not make any purchases of equity securities registered by the company pursuant to Section 12 of the Exchange Act during the fourth quarter of fiscal 2008.

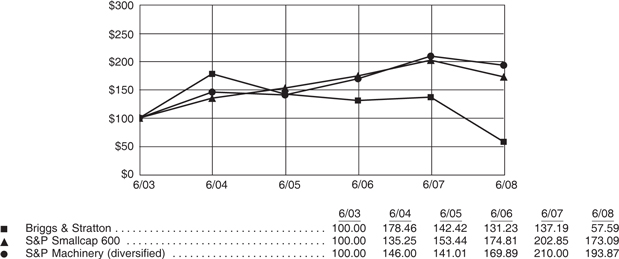

Five-year Stock Performance Graph

The chart below is a comparison of the cumulative return over the last five fiscal years had $100 been invested at the close of business on June 30, 2003 in each of Briggs & Stratton common stock, the Standard & Poor’s (S&P) Smallcap 600 Index and the S&P Machinery Index.

FIVE YEAR CUMULATIVE TOTAL RETURN COMPARISON*

Briggs & Stratton versus Published Indices

| | * | Total return calculation is based on compounded monthly returns with reinvested dividends. |

9

| ITEM 6. | SELECTED FINANCIAL DATA |

| | | | | | | | | | | | | | | | |

| Fiscal Year | | 2008 | | Restated 2007 | | | Restated 2006 | | Restated 2005 | | Restated 2004 |

(dollars in thousands, except per share data) | | | | | | | | | | | | | | | | |

| | | | | |

SUMMARY OF OPERATIONS (1) (2) (3) | | | | | | | | | | | | | | | | |

NET SALES | | $ | 2,151,393 | | $ | 2,156,833 | | | $ | 2,539,671 | | $ | 2,651,975 | | $ | 1,947,364 |

GROSS PROFIT ON SALES | | | 307,316 | | | 295,198 | | | | 495,345 | | | 508,691 | | | 441,697 |

PROVISION (CREDIT) FOR INCOME TAXES | | | 7,009 | | | (3,399 | ) | | | 52,533 | | | 59,890 | | | 71,294 |

INCOME BEFORE EXTRAORDINARY GAIN | | | 22,600 | | | 6,701 | | | | 105,981 | | | 120,525 | | | 137,643 |

INCOME BEFORE EXTRAORDINARY GAIN PER SHARE OF COMMON STOCK: | | | | | | | | | | | | | | | | |

Basic Earnings | | | 0.46 | | | 0.13 | | | | 2.06 | | | 2.34 | | | 3.04 |

Diluted Earnings | | | 0.46 | | | 0.13 | | | | 2.05 | | | 2.32 | | | 2.72 |

PER SHARE OF COMMON STOCK: | | | | | | | | | | | | | | | | |

Cash Dividends | | | .88 | | | .88 | | | | .88 | | | .68 | | | .66 |

Shareholders’ Investment | | $ | 16.90 | | $ | 16.94 | | | $ | 20.47 | | $ | 18.28 | | $ | 17.02 |

WEIGHTED AVERAGE NUMBER OF SHARES OF COMMON STOCK OUTSTANDING (in 000’s) | | | 49,549 | | | 49,715 | | | | 51,479 | | | 51,472 | | | 45,286 |

DILUTED NUMBER OF SHARES OF COMMON STOCK OUTSTANDING (in 000’s) | | | 49,652 | | | 49,827 | | | | 51,594 | | | 51,954 | | | 50,680 |

| | | | | |

OTHER DATA (1) (2) | | | | | | | | | | | | | | | | |

SHAREHOLDERS’ INVESTMENT | | $ | 837,523 | | $ | 838,454 | | | $ | 1,045,492 | | $ | 943,837 | | $ | 868,522 |

LONG-TERM DEBT | | | 365,555 | | | 384,048 | | | | 383,324 | | | 486,321 | | | 360,562 |

CAPITAL LEASES | | | 1,677 | | | 2,379 | | | | 1,385 | | | 1,988 | | | - |

TOTAL ASSETS | | | 1,833,294 | | | 1,884,468 | | | | 2,049,436 | | | 2,072,538 | | | 1,724,341 |

PLANT AND EQUIPMENT | | | 1,012,987 | | | 1,006,402 | | | | 1,008,164 | | | 1,005,644 | | | 867,987 |

PLANT AND EQUIPMENT, NET OF RESERVES | | | 391,833 | | | 388,318 | | | | 430,288 | | | 447,255 | | | 356,542 |

PROVISION FOR DEPRECIATION | | | 65,133 | | | 70,379 | | | | 72,734 | | | 66,348 | | | 59,816 |

EXPENDITURES FOR PLANT AND EQUIPMENT | | | 65,513 | | | 68,000 | | | | 69,518 | | | 86,075 | | | 52,962 |

WORKING CAPITAL | | $ | 644,935 | | $ | 519,023 | | | $ | 680,606 | | $ | 761,037 | | $ | 677,832 |

Current Ratio | | | 2.9 to 1 | | | 2.1 to 1 | | | | 3.0 to 1 | | | 3.1 to 1 | | | 3.2 to 1 |

NUMBER OF EMPLOYEES AT YEAR-END | | | 7,145 | | | 7,260 | | | | 8,701 | | | 9,073 | | | 7,732 |

NUMBER OF SHAREHOLDERS AT YEAR-END | | | 3,545 | | | 3,693 | | | | 3,874 | | | 4,058 | | | 4,230 |

QUOTED MARKET PRICE: | | | | | | | | | | | | | | | | |

High | | $ | 33.40 | | $ | 33.07 | | | $ | 40.38 | | $ | 44.50 | | $ | 44.22 |

Low | | $ | 12.80 | | $ | 24.29 | | | $ | 30.01 | | $ | 30.83 | | $ | 24.68 |

| (1) | The amounts include the acquisitions of Simplicity Manufacturing, Inc. since July 7, 2004 and certain assets of Murray, Inc. since February 11, 2005. |

| (2) | Share data adjusted for effect of 2-for-1 stock split effective October 29, 2004. |

| (3) | As discussed in Note 3 to the Notes to Consolidated Financial Statements, the Company has restated its prior years’ financial statements for a change in accounting principle related to its defined benefit pension plan, which occurred in the first quarter of fiscal 2008, and for the correction of certain errors which were identified in the third quarter of fiscal 2008. The impact of these items was a reduction in fiscal 2005 net sales of approximately $2.9 million. There was no impact on fiscal 2004 net sales. The impact of these items was an increase in fiscal 2005 and 2004 income before extraordinary gain of $3.8 million ($.07 per diluted share) and $1.5 million ($.03 per diluted share), respectively. The impact to the fiscal 2006, 2005 and 2004 balance sheet data was negligible. |

10

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Results of Operations

FISCAL 2008 COMPARED TO FISCAL 2007

Net Sales

Fiscal 2008 consolidated net sales were approximately $2.15 billion, a decrease of $5.4 million compared to the previous year. The decrease is due to the net effect of lower sales volumes in both segments offset by a favorable mix of product and currency exchange rates in the Engines Segment.

Engines Segment net sales were $1.46 billion compared to $1.45 billion in the prior year, an increase of $12.8 million or 1%. This increase reflects the impact of a favorable mix of shipped products and a favorable currency exchange rate offset by a 4% reduction of engine shipments. The decrease in unit volume was primarily due to the lower demand for engine powered lawn and garden equipment in the U.S.

Power Products Segment net sales were $870.4 million in fiscal 2008 compared to $890.0 million in fiscal 2007, a decrease of $19.6 million or 2%. This decrease was due to a reduction in unit shipments in each product category except shipments of lawn and garden equipment to mass retailers, which reflected product placement that the Company did not have in the prior year. Generally, these sales decreases reflect weak consumer demand for outdoor power equipment.

Gross Profit

Consolidated gross profit was $307.3 million in fiscal 2008 compared to $295.2 million in fiscal 2007, an increase of $12.1 million or 4%. In fiscal 2008, the Company recorded a $13.3 million pretax ($8.1 million after tax) gain associated with the reduction of certain post closing employee benefit costs related to the closing of the Port Washington, Wisconsin manufacturing facility and a $19.8 million pretax ($13.5 million after tax) expense from a snow engine recall. In fiscal 2007, the Company recorded impairment charges of $43.1 million ($26.2 million, net of taxes) related to write-downs of assets primarily associated with the announced rationalization of two manufacturing plants and $5.0 million pretax ($3.4 million after tax) expense from the snow engine recall. After considering the impact of these items, consolidated gross profit declined $29.5 million, primarily the result of lower sales volumes and lower utilization of production facilities.

Engines Segment gross profit increased to $271.0 million in fiscal 2008 from $216.9 million in fiscal 2007, an increase of $54.1 million. Engines Segment gross profit margins increased to 18.6% in fiscal 2008 from 15.0% in fiscal 2007. Approximately $20.4 million of the improvement is due to fiscal 2007 expenses incurred with the write-down of assets associated primarily with the rationalization of a major manufacturing plant in the United States that were not incurred in fiscal 2008, offset by the increased expense of the snow engine recall in fiscal 2008. The balance of the improvement resulted primarily from $23.1 million of manufacturing cost reductions primarily from the rationalization of the manufacturing plant in the United States. A favorable product mix and favorable currency exchange rates were offset by decreases in unit volume.

The Power Products Segment gross profit decreased to $39.4 million in fiscal 2008 from $80.4 million in fiscal 2007, a decrease of $41.0 million. The Power Products Segment gross profit margins decreased to 4.5% in fiscal 2008 from 9.0% in fiscal 2007. As previously mentioned, a $13.3 million gain associated with the reduction of certain post closing employee benefit costs related to the closing of the Port Washington, Wisconsin manufacturing facility was recorded in fiscal 2008. In fiscal 2007, asset impairment charges of $9.2 million were recorded, primarily related to the write-down of assets at this same facility. After considering the impact of these items, gross margins decreased $63.5 million, primarily the result of $22.8 million of manufacturing cost increases due to under utilization of production facilities, $16.5 million of inefficiencies related to the initial year of a plant start-up and $19.2 million of increased costs for raw materials and components.

Engineering, Selling, General and Administrative Costs

Engineering, selling, general and administrative costs increased to $281.0 million in fiscal 2008 from $263.0 million in fiscal 2007, an increase of $17.9 million. Engineering, selling, general and administrative costs as a percent of sales increased to 13.1% in fiscal 2008 from 12.2% in fiscal 2007.

The increase in engineering, selling, general and administrative expenses is due to planned increases in salaries and benefits of $10.0 million, $2.2 million of increased engineering costs and increased selling, marketing and advertising expenses of $1.4 million.

11

Interest Expense

Interest expense decreased $5.6 million in fiscal 2008 compared to fiscal 2007. The decrease is attributable to lower average borrowings between years for working capital requirements and lower average interest rates.

Other Income

Other income increased $26.6 million in fiscal 2008 as compared to fiscal 2007. This increase is primarily due to the $8.6 million gain on the redemption of preferred stock and $18.3 million of additional dividends received on this stock compared to the prior year.

Provision for Income Taxes

The effective tax rate was 23.7% for fiscal 2008 and 102.9% for fiscal 2007. The fiscal 2008 effective tax rate is less than the statutory 35% rate primarily due to the Company’s ability to exclude from taxable income a portion of the distributions received from investments and the benefit from research credits. In 2007, the combination of similar exclusion, the research credit and production activity deduction with a small pre-tax financial loss effectively increased the total tax (benefit) by an amount greater than the pre-tax loss.

FISCAL 2007 COMPARED TO FISCAL 2006

Net Sales

Fiscal 2007 consolidated net sales were approximately $2.16 billion, a decrease of $383 million compared to the previous year. The decrease is primarily due to lower sales volumes in both segments.

Engines Segment net sales were $1.45 billion compared to $1.65 billion in the prior year, a decrease of $201.2 million or 12%. The decrease is primarily the result of a 12% decrease in engine unit shipments between years. The shipment decline is due to a 66% reduction of engine shipments for portable generators caused by a lack of events, such as hurricanes, that cause power outages. The remainder of the decrease is due to lower retail demand for lawn and garden equipment in the U.S. along with a smaller market share in Europe. Unfavorable weather conditions and various economic factors contributed to difficult market conditions for lawn and garden products. Pricing improvements and the impact of favorable Euro exchange rates in fiscal 2007 were almost entirely offset by an unfavorable mix shift to smaller displacement, lower priced engines.

Power Products Segment net sales were $890.0 million in fiscal 2007 compared to $1.18 billion in fiscal 2006, a decrease of $293.5 million or 25%. Approximately $113.0 million of the decrease was the result of the anticipated reduction of Murray branded lawn and garden product sold to retailers. Excluding Murray branded product, lawn and garden equipment sales were comparable between years. The remainder of the net sales decrease was primarily due to a 58% reduction of portable generator unit shipments because of no landed hurricane activity in fiscal 2007 and lower pre-hurricane season sales. These sales decreases were partially offset by an increase in pressure washer unit shipments compared to the same period in the prior year and the introduction of new air compressor and home standby generator products.

Gross Profit

Consolidated gross profit was $295.2 million in fiscal 2007 compared to $495.3 million in fiscal 2006, a decrease of $200.1 million or 40%. In fiscal 2007, the Company recorded impairment charges of $43.1 million ($26.2 million, net of taxes) related to write-downs of assets primarily associated with the announced rationalization of two manufacturing plants. The remainder of the decrease is the result of lower sales and production volumes in both segments.

Engines Segment gross profit decreased to $216.9 million in fiscal 2007 from $388.1 million in fiscal 2006, a decrease of $171.2 million. Engines Segment gross profit margins decreased to 15.0% in fiscal 2007 from 23.5% in fiscal 2006. Approximately $33.9 million of the decline is attributable to expense incurred with the write-down of assets primarily associated with the rationalization of a major operating plant in the United States. The balance of the reduction resulted primarily from lower sales and production volumes, and increased costs for raw materials. Lower unit sales negatively impacted fiscal 2007 margins by approximately $70.0 million. Pricing improvements and the impact of favorable Euro exchange rates in fiscal 2007 were almost entirely offset by an unfavorable mix shift to smaller displacement, lower priced engines. Raw material cost increases primarily related to aluminum, steel, and zinc also negatively impacted margins. Engine production volumes decreased 18.9% in fiscal 2007 compared to fiscal 2006 reducing fixed cost absorption by approximately $45.0 million. In addition, fiscal 2006 included gains of approximately $12.2 million associated with certain asset sales that were not recurring in fiscal 2007.

12

The Power Products Segment gross profit decreased to $80.4 million in fiscal 2007 from $110.7 million in fiscal 2006, a decrease of $30.3 million. The Power Products Segment gross profit margins decreased to 9.0% in fiscal 2007 from 9.4% in fiscal 2006. Asset impairment charges of $9.2 million primarily related to the write-down of assets associated with a plan to close the Port Washington manufacturing facility by October 2008 accounted for a gross profit margin decline of approximately 1.0%. Portable generator production volume declines of 65% offset by increased production of pressure washers decreased fixed cost absorption by approximately $13.6 million. These declines were offset by a decrease of $19 million of 2006 expenses associated with the wind down of operations at the Murray, Inc. operating facility and the write-off of excess inventory related to Murray product.

Engineering, Selling, General and Administrative Costs

Engineering, selling, general and administrative costs decreased to $263.0 million in fiscal 2007 from $313.2 million in fiscal 2006, a decrease of $50.2 million. Engineering, selling, general and administrative costs as a percent of sales decreased to 12.2% in fiscal 2007 from 12.3% in fiscal 2006.

The decrease in engineering, selling, general and administrative expenses is due to planned reductions in salaries and benefits of $14 million, reduced professional services and legal fees of $21 million and reduced selling, marketing and advertising expenses of $12 million.

Interest Expense

Interest expense increased $1.6 million in fiscal 2007 compared to fiscal 2006. The increase is attributable to higher average borrowings between years to support higher average working capital requirements.

Other Income

Other income decreased $3.7 million in fiscal 2007 as compared to fiscal 2006. The decrease in other income is due to lower dividends received as well as the Company’s portion of lower earnings at its joint venture investments.

Provision for Income Taxes

The effective tax rate was 102.9% for fiscal 2007 and 33.1% for fiscal 2006. The fiscal 2007 effective tax rate results primarily from our ability to exclude from taxable income a portion of the distributions received from investments and the benefit from the research credit and the production activities deduction.

Liquidity and Capital Resources

FISCAL YEARS 2008, 2007 AND 2006

Cash flows from operating activities were $61 million, $88 million and $155 million in fiscal 2008, 2007 and 2006, respectively.

The fiscal 2008 cash flows from operating activities were $27 million less than the prior year. This decrease is primarily due to lower cash operating earnings that resulted from increased manufacturing costs, offset by $32 million less of working capital requirements between years.

The fiscal 2007 cash flows from operating activities were $67 million less than the prior year. The primary reason for the decrease is due to net income being lower by $99 million in fiscal 2007 compared to fiscal 2006. The decrease in net income was partially offset by non-cash impairment charges of $43 million in fiscal 2007. In addition, higher fourth quarter sales within our Engines Segment increased working capital requirements for accounts receivable by $54 million partially offset by higher accounts payable and accrued liabilities.

The fiscal 2006 cash flows from operating activities were $6 million higher than the prior year. The primary reason for the increase is lower working capital requirements in fiscal 2006. Lower fourth quarter sales in fiscal 2006 resulted in higher inventory levels offset by lower receivables and accrued liabilities including rebates, incentive compensation and income taxes. The reduction in net income between years was more than offset by a series of increased non-cash items in fiscal 2006 including non-cash pension charges, stock compensation expense, gains on fixed asset sales, the deferred tax credit, and the elimination of the extraordinary gain.

Cash provided by investing activities was $0.7 million in fiscal 2008. Cash used in investing activities was $67 million and $55 million in fiscal 2007 and 2006, respectively. These cash flows include capital expenditures of $66 million, $68 million and $70 million in fiscal 2008, 2007 and 2006, respectively. The capital expenditures

13

relate primarily to reinvestment in equipment, capacity additions and new products. During fiscal 2007, the Company increased its Engines Segment capacity by opening a new plant in Ostrava, Czech Republic which accounted for $15 million of capital expenditures. This new plant began production in December 2006. In addition, the Power Products Segment added lawn and garden product capacity with a new plant in Newbern, Tennessee that accounted for $14 million and $6 million of capital expenditures in fiscal 2008 and 2007, respectively. This plant began production in the second quarter of fiscal 2008.

In fiscal 2008, the Company received $66 million in proceeds on the sale of an investment in preferred stock including the final dividends paid on this preferred stock.

In fiscal 2006, Briggs & Stratton received $12 million in cash from the sale of certain operating assets. In addition, Briggs & Stratton received $6 million as a refund of a portion of the cash paid for certain assets of Murray, Inc. in fiscal 2006.

Briggs & Stratton used cash of $63 million, $89 million and $169 million in financing activities in fiscal 2008, 2007 and 2006, respectively.

The Company paid common stock dividends of $44 million, $44 million and $45 million in fiscal 2008, 2007 and 2006, respectively. In fiscal 2007, Briggs & Stratton repurchased $48 million of its common shares outstanding as part of a $120 million share repurchase program authorized by the Board of Directors in fiscal 2007. Briggs & Stratton repurchased $35 million of its common shares in fiscal 2006.

In fiscal 2006, the Company paid off $104 million of its long term debt, including $90 million of its term notes due in fiscal 2008.

The Company received $1 million, $4 million and $12 million in fiscal years 2008, 2007 and 2006, respectively, from the exercise of stock options. The stock option activity is a direct reflection of the market value of the Company’s stock and option strike prices that encourage the exercise of the options.

Future Liquidity and Capital Resources

On July 12, 2007, the Company entered into a $500 million amended and restated multicurrency credit agreement. The Amended Credit Agreement (“Revolver”) provides a revolving credit facility for up to $500 million in revolving loans, including up to $25 million in swing-line loans. The Company used the proceeds of the Revolver to pay off the remaining amounts outstanding under the Company’s variable rate term notes issued in February 2005 with various financial institutions, retire the 7.25% senior notes that were due in September 2007 and fund seasonal working capital requirements and other financing needs. At any time during the term of the Revolver, the Company may, so long as no event of default has occurred and is continuing and certain other conditions are satisfied, elect to increase the maximum amount available under the Revolver from $500 million by up to an amount not to exceed $250 million through, at the Company’s election, increases of commitments by existing lenders and/or the addition of new lenders. The Revolver has a term of five years and all outstanding borrowings on the Revolver will be due and payable on July 12, 2012. As of June 29, 2008, borrowings on the Revolver totaled $99.1 million.

On August 10, 2006, Briggs & Stratton announced its intent to initiate repurchases of up to $120 million of its common stock through open market transactions during fiscal 2007 and fiscal 2008. The Company repurchased approximately $48 million of common stock under this plan, which expired in February 2008.

Briggs & Stratton expects capital expenditures to be approximately $50 million in fiscal 2009. These anticipated expenditures reflect our plans to continue to reinvest in equipment, new products, and capacity enhancements.

Management believes that available cash, the credit facility, cash generated from future operations and existing lines of credit will be adequate to fund Briggs & Stratton’s capital requirements for the foreseeable future.

Financial Strategy

Management believes that the value of Briggs & Stratton is enhanced if the capital invested in operations yields a cash return that is greater than the cost of capital. Consequently, management’s first priority is to reinvest capital into physical assets and products that maintain or grow the global cost leadership and market positions that Briggs & Stratton has achieved, and drive the economic value of the Company. Management’s next financial objective is to identify strategic acquisitions or alliances that enhance revenues and provide a superior economic return. Finally, management believes that when capital cannot be invested for returns greater than the cost of capital, we should return capital to the capital providers through dividends and/or share repurchases.

14

Off-Balance Sheet Arrangements

Briggs & Stratton has no off-balance sheet arrangements or significant guarantees to third parties not fully recorded in our Balance Sheets or fully disclosed in our Notes to Consolidated Financial Statements. Briggs & Stratton’s significant contractual obligations include our debt agreements and certain employee benefit plans.

Briggs & Stratton is subject to financial and operating restrictions in addition to certain financial covenants under its domestic debt agreements. As is fully disclosed in Note 8 of the Notes to Consolidated Financial Statements, these restrictions could limit our ability to: pay dividends; incur further indebtedness; create liens; enter into sale and/or leaseback transactions; consolidate, sell or lease all or substantially all of our assets; and dispose of assets or the proceeds of our assets. We believe we will remain in compliance with these covenants in fiscal 2009. Briggs & Stratton has obligations concerning certain employee benefits including its pension plans, postretirement benefit obligations and deferred compensation arrangements. All of these obligations are recorded on our Balance Sheets and disclosed more fully in the Notes to Consolidated Financial Statements.

Contractual Obligations

A summary of the Company’s expected payments for significant contractual obligations as of June 29, 2008 is as follows (in thousands):

| | | | | | | | | | | | | | | | | | | | | | | |

| | | Total | | | | 2009 | | | | 2010-2011 | | | | 2012-2013 | | | | Thereafter |

Long-Term Debt | | $ | 367,077 | | | | $ | - | | | | $ | 268,000 | | | | $ | 99,077 | | | | $ | - |

Interest on Long-Term Debt | | | 83,640 | | | | | 28,541 | | | | | 50,145 | | | | | 4,954 | | | | | - |

Capital Leases | | | 2,077 | | | | | 524 | | | | | 992 | | | | | 561 | | | | | - |

Operating Leases | | | 59,303 | | | | | 14,981 | | | | | 23,570 | | | | | 12,766 | | | | | 7,986 |

| | | | | | | | | | | | | | | | | | | | | | | |

| | $ | 512,097 | | | | $ | 44,046 | | | | $ | 342,707 | | | | $ | 117,358 | | | | $ | 7,986 |

| | | | | | | | | | | | | | | | | | | | | | | |

Other Matters

Labor Agreement

Briggs & Stratton has collective bargaining agreements with its unions. These agreements expire at various times ranging from 2008-2013.

Emissions

The U.S. Environmental Protection Agency (EPA) has developed national emission standards under a two-phase process for small air cooled engines. Briggs & Stratton currently has a complete product offering that complies with the EPA’s Phase II engine emission standards.

The EPA issued proposed Phase III standards to further reduce engine exhaust emissions and to control evaporative emissions from small off-road engines and equipment they are used in. The proposed standards are similar to those adopted by the California Air Resources Board (CARB). The proposed Phase III program would require some evaporative controls in 2009 and go into full effect in 2011 for Class II engines (225 cubic centimeter displacement and larger) and 2012 for Class I engines (less than 225 cubic centimeter displacement). Briggs & Stratton does not believe compliance with the new standards will have a material adverse effect on its financial position or results of operations.

CARB’s Tier 3 regulation requires additional reductions to engine exhaust emissions and new controls on evaporative emissions from small engines. The Tier 3 regulation was fully phased in during fiscal year 2008. While Briggs & Stratton believes the cost of the regulation may increase engine costs per unit, Briggs & Stratton does not believe the regulation will have a material effect on its financial condition or results of operations. This assessment is based on a number of factors, including revisions the CARB made to its adopted regulation from the proposal published in September 2003 in response to recommendations from Briggs & Stratton and others in the regulated category and intention to pass increased costs associated with the regulation on to consumers.

The European Commission adopted an engine emission Directive regulating exhaust emissions from small air cooled engines. The Directive parallels the Phase 1 and 2 regulations adopted by the U.S. EPA. Stage 1 was effective in February 2004 and Stage 2 phases in between calendar years 2005 and 2007, with some limited extensions available for specific size and type engines until 2010. Briggs & Stratton has a full product line compliant with Stage 2. Briggs & Stratton does not believe compliance with the Directive will have a material adverse effect on its financial position or results of operations.

15

Critical Accounting Policies

Briggs & Stratton’s critical accounting policies are more fully described in Note 2 and Note 14 of the Notes to Consolidated Financial Statements. As discussed in Note 2, the preparation of financial statements in conformity with accounting principles generally accepted in the U.S. (“GAAP”) requires management to make estimates and assumptions about future events that affect the amounts reported in the financial statements and accompanying notes. Future events and their effects cannot be determined with absolute certainty. Therefore, the determination of estimates requires the exercise of judgment. Actual results inevitably will differ from those estimates, and such differences may be material to the financial statements.

The most significant accounting estimates inherent in the preparation of our financial statements include a goodwill assessment, estimates as to the recovery of accounts receivable and inventory reserves, and estimates used in the determination of liabilities related to customer rebates, pension obligations, postretirement benefits, warranty, product liability, litigation and taxation.

The carrying amount of goodwill is tested annually and whenever events or circumstances indicate that impairment may have occurred. Impairment testing is performed in accordance with Statement of Financial Accounting Standard (SFAS) No. 142, “Goodwill and Other Intangible Assets.” The Company performs impairment reviews for its reporting units, which have been determined to be one level below the Company’s reportable segments, using a fair value method. The reporting units are Engine Power Products, Home Power Products and Yard Power Products. The fair value represents the amount at which a reporting unit could be bought or sold in a current transaction between willing parties on an arms-length basis. To estimate fair value, the Company periodically retains independent third party valuation experts. Fair value is estimated using a valuation methodology that incorporates three approaches in estimating fair value including the public guideline company method, the guideline transaction method and the discounted cash flow method. The determination of fair value requires significant management judgment including estimating future sales volumes, selling prices and costs, changes in working capital, investments in property and equipment and the selection of an appropriate discount rate. The estimated fair value is then compared with the carrying value of the reporting unit, including the recorded goodwill. The Company is subject to financial statement risk to the extent that the carrying amount exceeds the estimated fair value. The impairment testing performed by the Company at June 29, 2008 indicated that the estimated fair value of each reporting unit exceeded its corresponding carrying amount, including recorded goodwill and as such, no impairment existed. Other intangible assets with definite lives continue to be amortized over their estimated useful lives and are subject to impairment testing if events or changes in circumstances indicate that an asset may be impaired. Indefinite lived intangible assets are also subject to impairment testing on at least an annual basis. At June 29, 2008 there was no impairment of intangible assets.

The reserves for customer rebates, warranty, product liability, inventory and doubtful accounts are fact specific and take into account such factors as specific customer situations, historical experience, and current and expected economic conditions.

The Company’s estimate of income taxes payable, deferred income taxes, and the effective tax rate is based on a complex analysis of many factors including interpretations of federal, state and foreign income tax laws, the difference between tax and financial reporting bases of assets and liabilities, estimates of amounts currently due or owed in various jurisdictions, and current accounting standards. We review and update our estimates on a quarterly basis as facts and circumstances change and actual results are known. In addition, Federal, state and foreign taxing authorities periodically review the Company’s estimates and interpretation of income tax laws. Adjustments to the effective income tax rate and recorded tax related assets and liabilities may occur in future periods if actual results differ significantly from original estimates and interpretations.

The pension benefit obligation and related pension expense or income are calculated in accordance with SFAS No.158, “Employer’s Accounting for Defined Benefit Pension and Other Postretirement Plans - an amendment of FASB Statements No. 87, 88, 106 and 132 (R)”, and are impacted by certain actuarial assumptions, including the discount rate and the expected rate of return on plan assets. These rates are evaluated on an annual basis considering such factors as market interest rates and historical asset performance. Actuarial valuations at June 29, 2008 used a discount rate of 7.0% and an expected rate of return on plan assets of 8.75%. Our discount rate was selected using a methodology that matches plan cash flows with a selection of Moody’s Aa or higher rated bonds, resulting in a discount rate that better matches a bond yield curve with comparable cash flows. A 0.25% decrease in the discount rate would decrease annual pension expense by approximately $0.5 million. A 0.25% decrease in the expected return on plan assets would increase our annual pension expense by approximately $2.3 million. In estimating the expected return on plan assets, the Company considers the historical returns on

16

plan assets, adjusted for forward looking considerations, including inflation assumptions and active management of the plan’s invested assets. Changes in the discount rate and return on assets can have a significant effect on the funded status of our pension plans, stockholders’ equity and expense. We cannot predict these changes in discount rates or investment returns and, therefore, cannot reasonably estimate whether the impact in subsequent years will be significant.

The funded status of the Company’s pension plan is the difference between the projected benefit obligation and the fair value of its plan assets. The projected benefit obligation is the actuarial present value of all benefits expected to be earned by the employees’ service adjusted for future potential wage increases. At June 29, 2008 the fair value of plan assets exceeded the projected benefit obligation by approximately $52 million.

The other postretirement benefits obligation and related expense or income are also calculated in accordance with SFAS No. 158, “Employer’s Accounting for Defined Benefit Pension and Other Postretirement Plans – an amendment of FASB Statements No. 87, 88, 106 and 132 (R)” and are impacted by certain actuarial assumptions, including the health care trend rate. An increase of one percentage point in health care costs would increase the accumulated postretirement benefit obligation by $10.0 million and would increase the service and interest cost by $0.8 million. A corresponding decrease of one percentage point, would decrease the accumulated postretirement benefit by $9.2 million and decrease the service and interest cost by $0.7 million.

For pension and postretirement benefits, actuarial gains and losses are accounted for in accordance with GAAP. Refer to Note 14 of the Notes to the Consolidated Financial Statements for additional discussion.

New Accounting Pronouncements

In March 2008, the Financial Accounting Standards Board (“FASB”) issued Statement No. 161, “Disclosures about Derivative Instruments and Hedging Activities – an amendment of FASB Statement No. 133” (“SFAS 161”). SFAS 161 is intended to help investors better understand how derivative instruments and hedging activities affect an entity’s financial position, financial performance and cash flows through enhanced disclosure requirements. SFAS 161 is effective for fiscal years and interim periods beginning after November 15, 2008. At this time, the impact of adoption of SFAS 161 on our consolidated financial position is being assessed.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial Statements – an amendment of ARB No. 51,” (SFAS 160). SFAS 160 amends ARB 51 to establish accounting and reporting standards for the noncontrolling interest in a subsidiary and for the deconsolidation of a subsidiary. It clarifies that a noncontrolling interest in a subsidiary is an ownership interest in the consolidated entity that should be reported as equity in the consolidated financial statements. SFAS 160 is effective for fiscal years beginning on or after December 15, 2008. At this time, the impact of adoption of SFAS 160 on our consolidated financial position is being assessed.

In December 2007, the FASB issued SFAS No. 141 (revised 2007), “Business Combinations” (SFAS No. 141R). SFAS No. 141R will significantly change the accounting for business combinations in a number of areas including the treatment of contingent consideration, contingencies, acquisition costs, in-process research and development, and restructuring costs. In addition, under SFAS No. 141R, changes in deferred tax asset valuation allowances and acquired income tax uncertainties in a business combination after the measurement period will impact income taxes. SFAS No. 141R is effective for fiscal years beginning after December 15, 2008, and will impact the accounting for any business combinations entered into after the effective date.