[LETTERHEAD OF WACHTELL, LIPTON, ROSEN & KATZ]

March 29, 2010

Anne Nguyen Parker

Tracey McNeil

Division of Corporation Finance

Securities and Exchange Commission

100 F Street, N.E.

Washington, D.C. 20549-7010

| Re: | Noranda Aluminum Holding Corporation |

Amendment No. 4 to Registration Statement on Form S-1

Filed March 2, 2010

File Number 333-150760

Dear Ms. Parker and Ms. McNeil:

Set forth below are the responses of Noranda Aluminum Holding Corporation (“Noranda” or the “Company”) to the comments of the Staff of the Division of Corporation Finance (the “Staff”) that were set forth in your letter dated March 19, 2010, regarding Amendment No. 4 (“Amendment No. 4”) to the Company’s Registration Statement on Form S-1 (the “Registration Statement”). In connection with this letter responding to the Staff’s comments, we are filing Amendment No. 5 to the Registration Statement (“Amendment No. 5”), and we have enclosed six courtesy copies of such Amendment No. 5 marked to show changes from Amendment No. 4 as filed on March 2, 2010. Capitalized terms used but not defined herein have the meanings specified in Amendment No. 5.

For your convenience, the Staff’s comments are set forth in bold, followed by responses on behalf of the Company. All page references in the responses set forth below refer to pages of Amendment No. 5.

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 2

General

| 1. | Please continue to monitor your requirements to provide updated financial statements with your next amendment. Please refer to Rule 3-12 of Regulation S-X. |

Response: The Company acknowledges the Staff’s comment and will continue to monitor its requirements pursuant to Rule 3-12 of Regulation S-X.

| 2. | Please provide updated consents with your next amendment. |

Response: The Company has filed updated consents with Amendment No. 5. Please see exhibits 23.2, 23.3, 23.4 and 23.5 to Amendment No. 5.

Prospectus Summary, page 1

General

| 3. | We remind you of our prior comment 11 from our letter dated February 16, 2010. Please revise your prospectus summary to discuss and quantify the “significant negative” impact of the recent global recession and credit crisis on your financial results. We note the revised risk factor on page 25 and the revised disclosure on pages 54-55. |

Response: The Company has revised the Registration Statement in response to the Staff’s comment. Please see pages 1 and 3.

Overview, page 1

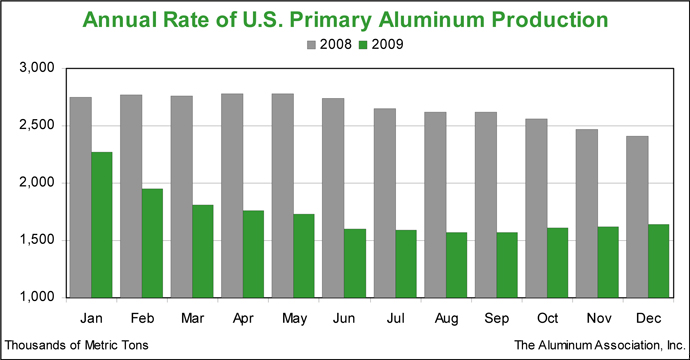

| 4. | We note your revised disclosure indicating that the statement that production capacity at New Madrid “represents more than 15% of total 2009 U.S. primary aluminum production” is now based on statistics from the Aluminum Association. Please provide us with data to substantiate this statement. Please also refer to our prior comment 7 for guidance regarding substantiating statements. We also note that the data from the Aluminum Association submitted with your response letter dated March 1, 2010 relates to downstream business data, whereas New Madrid is a part of your upstream business. |

Response: The Company respectfully advises that the related source material can be found free of charge from the Aluminum Association’s website at the following link:

http://www.aluminum.org/Content/NavigationMenu/NewsStatistics/StatisticsReports/PrimaryProduction/

USPrimaryProduction2009.pdf

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 3

Total U.S. 2009 production as shown per the above link totals 1,727,167 metric tonnes, divided by New Madrid’s annual full production capacity of 263,000 metric tonnes equals 15%. We have also attached the document referred to above as Exhibit 4 to this letter.

Risk Factors, page 22

“We have substantial indebtedness . . . .”, page 22

“Restrictive covenants under the indentures . . . .”, page 22

| 5. | We note your statements regarding potential noncompliance with restrictive covenants and resulting events of default. Disclose whether any of these restrictive covenants provide for events of default with immediate effect and no cure or grace period, and if so, generally describe such events of default. Also include a brief description of any restrictive covenants or events of default that would not be considered usual and customary. |

Response: The Company has revised the Registration Statement in response to the Staff’s comment. Please see page 26.

“Our operations have been and will continue to be exposed . . . .”, page 31

| 6. | We note your disclosure that you recently reached an “understanding” with the Government of Jamaica and that if the Company and the Government of Jamaica “are unable to finalize definitive documentation consistent with that understanding, possible revisions could result in a net increase in [your] costs.” Please update this risk factor and related disclosure to provide the status of the finalization of such definitive documentation. |

Response: The Company has revised the Registration Statement in response to the Staff’s comment. Please see pages 35 and 100.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Critical Accounting Policies and Estimates, page 57

| 7. | We note your response to our prior comment number 35. Please tell us what consideration you have given to providing a separate critical accounting policy related to your post-retirement benefit plans, including your discount rate assumption and your expected rate of return on plan assets. We note that your estimates for these assumptions have changed in each period presented. |

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 4

Response: We respectfully advise the Staff that in preparing its disclosures related to critical accounting estimates, the Company considered the guidance of FR 72, “Commission Guidance Regarding Management’s Discussion and Analysis of Financial Condition and Results of Operations”. Those considerations led the Company to the disclosure of what management believed were the Company’s critical accounting policies and estimates. Specifically related to post-retirement benefit plans, the Company’s evaluation included the following:

| 1. | The Company considered that the discount rate and long-term rate of return assumptions do not involve a high level of subjectivity and judgment, whether considering post-retirement benefit plan accounting on its own, and particularly not in contrast to the assumptions inherent in the other accounting policies and estimates identified as critical. In reaching this conclusion the Company considered that there is clear authoritative accounting guidance about how the discount rate for measuring post-retirement benefit plans should be determined, and that the calculation of that rate is subject to relevant comparison to market data by actuarial and employee benefit consulting firms, and therefore to informed rate setting by management. The same considerations apply to the expected long-term rate of return on plan assets. The Company concluded that these factors indicated a lower level of subjectivity and judgment for post-retirement benefit plans than for other sensitive accounting areas. |

| 2. | Accounting for post-retirement benefit plans does not involve matters that are subject to significant management discretion, whether considering post-retirement benefit plan accounting on its own, or in contrast to the accounting for the accounting policies and estimates identified as critical. |

| 3. | The future impact of reasonably likely changes in estimates and assumptions is not expected to materially affect the Company’s financial condition or operating performance , whether considering post-retirement benefit plan accounting on its own, and particularly not in contrast to the assumptions inherent in the other accounting policies and estimates we identified as critical. The Staff accurately points out that the Company’s discount rate and expected rate-of-return assumptions have changed in each period presented. However, these changes have been within a fairly narrow range. The Noranda Pension Plan discount rate assumption, which is the most sensitive estimate, has moved within a range of plus 10 basis points to minus 17 basis points. At December 31, 2009, a ten basis point change in the discount rate would have changed our benefit obligation by $4 million, on a total obligation of $305.1 million. |

While the Company agrees with the Staff, as noted in its response to comment #8, that its liquidity discussion should provide more disclosure about the impact of regulatory requirements such as the Pension Protection Act of 2006, the Company respectfully advises that it does not believe its post-retirement benefit plans warrant inclusion in an MD&A discussion of critical accounting policies and estimates.

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 5

Liquidity and Capital Resources, page 73

| 8. | Your response indicates in December 2009, you contributed an additional $20 million to your post-retirement benefit plans. Please expand your liquidity disclosures to discuss this additional funding and how debt covenant restrictions if any, impact your ability to maintain or improve your funded status. Further, please expand you disclosures to describe your pension funding status as defined in the Pension Protection Act of 2006 and any restrictions to your plans associated with the current funding level. |

Response: The Company respectfully advises the Staff that there are no debt covenant restrictions that directly impact our ability to maintain or improve funded status. As of January 1, 2009, the Adjusted Funding Target Attainment Percentage (AFTAP) under the Pension Protection Act of 2006 for each pension plan was at least 80%. Currently, there are no benefit restrictions. The additional $20 million contributed to the pension plans in December 2009 was based on estimates of funding needed to maintain an AFTAP of 80% as of January 1, 2010. The Company has revised the Registration Statement in response to the Staff’s comment. Please see page 78.

Commodity Price Risks, page 81

Non-Performance Risk, page 83

| 9. | We note your response to our prior comment 23 indicating that the master agreement with Merrill Lynch is a form ISDA Master Agreement. To facilitate a better understanding of the nature of this master agreement, please expand your disclosure to include a general discussion of ISDA master agreements, schedules, and confirmations, similar to the information provided in your response. |

Response: The Company has revised the Registration Statement in response to the Staff’s comment. Please see page 86.

Executive Compensation, page 109

| 10. | We note that you have not included any disclosure in response to Item 402(s) of Regulation S-K. Please advise us of the basis for your conclusion that disclosure is not necessary and describe the process you undertook to reach that conclusion. |

Response: On February 9, 2010 the Compensation Committee of our Board of Directors conducted an evaluation of the relationship between risk and compensation at the Company. Following discussion and recommendation from management, the Compensation Committee found that risks arising from the Company’s compensation

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 6

programs are not reasonably likely to have a material adverse effect on the Company. This finding was based on several qualitative factors, including the belief that the compensation for employees is comprised of the right mix of fixed and “at risk” components, that the performance metrics used for the Company’s Incentive Plan employ multiple criteria and promote sound management, and that employees are not rewarded for, or encouraged to undertake, unreasonable or excessive risk-taking activities. On February 10, 2010, based on the recommendation of the Compensation Committee, the Board of Directors of the Company made the same finding that risks arising out of the Company’s compensation programs are not reasonably likely to have a material adverse effect on the Company. These findings are reflected in the minutes of the Compensation Committee and Board of Directors meetings as of the dates set forth herein.

Elements Used to Achieve Compensation Objectives, page 111

| 11. | Please revise to delete duplicative disclosure. For example, you have repeated on pages 110 and 111 almost verbatim the several sentences that begin “The Company has not in recent years retained Hay Associates...” and end “...we have in place with the executive officer.” |

Response: The Company has revised the Registration Statement to remove duplicative disclosure in response to the Staff’s comment. Please see page 118.

| 12. | We note your disclosure on page 112 that “the performance targets and actual performance achieved . . . will not be disclosed [because such disclosure] would cause significant competitive harm . . . .” Please provide on a supplemental basis a detailed explanation for your conclusion that the information should be excluded. Refer to Instruction 4 to Item 402(b) of Regulation S-K. If you have an appropriate basis for omitting these targets, you must discuss how difficult or likely it will be for the named executive officers to achieve the undisclosed target levels. In discussing how difficult or likely it will be to achieve the target levels or other factors, provide as much detail as necessary. Refer to Question 118.04 of the Regulation S-K Compliance and Disclosure Interpretations available athttp://www.sec.gov/divisions/corpfin/guidance/regs-kinterp.htm. |

The Company respectfully advises that in response to the SEC’s comment, the Company has revised the Registration Statement to (i) disclose certain performance targets (the “Disclosed Targets”) and (ii) provide additional disclosure regarding the difficulty of achieving the Company’s performance targets.

The Company has disclosed the Disclosed Targets on page 120 of the Registration Statement in an effort to be responsive to the Staff’s comment and because it has determined that such disclosure, while not material to an investor’s understanding of the Company’s compensation arrangements and while entailing some risk of competitive harm, does not present the same level of competitive sensitivity as the performance targets that the Company has not disclosed. The disclosure of the Disclosed Targets is not intended to, and does not, constitute an admission that the Disclosed Targets are required to be disclosed.

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 7

The Company has not, however, disclosed performance targets with respect to the following metrics: safety, downstream free cash flow, and alumina cash funding cost (the “Confidential Targets”).

The Company respectfully provides the supplemental analysis below to demonstrate that (i) none of the Confidential Targets is material to an investor’s understanding of the Company’s compensation arrangements, and (ii) Instruction 4 to Regulation S-K Item 402(b) is applicable to each of the Confidential Targets, and therefore the Confidential Targets should not be disclosed because the quantitative operational and financial targets underlying each of the Confidential Targets involve confidential financial information, the disclosure of which would result in significant competitive harm to the Company.

None of the Confidential Targets is material to an investor’s understanding of the compensation programs for the Company’s named executive officers.

As the Company has disclosed in the Registration Statement, determination of bonuses under the Company’s 2009 Incentive Plan (the “Plan”) is based on multiple performance metrics for each of the Company’s named executive officers. For 2009 (which was established at the beginning of 2009, before the Joint Venture Transaction), compensation under the Plan for named executive officers not specifically assigned to either the upstream or downstream segment was based on a composite of the results of the two segments, plus a metric related to Noranda Alumina cash cost. Conversely, compensation under the Plan for executives specifically assigned to one of the two segments was based 50% on the Plan result for the executive’s specific segment and 50% on the results as calculated for other named executive officers as described above. As the Company has previously disclosed, upstream performance is based on six independent metrics (safety, net cash cost, upstream adjusted EBITDA, metal production, enterprise change in cash, and enterprise adjusted EBITDA). Downstream performance is determined based on four metrics (safety, downstream adjusted EBITDA, downstream free cash flow, and enterprise adjusted EBITDA). The Company selected these goals and specific targets because they are critical cornerstones of the Company’s strategic plan and are expected to be the most meaningful metrics to build a sustainable competitive position. Therefore, the Company establishes these performance metrics to align the organization to achieve these extremely challenging goals.

Thus, each named executive officer’s 2009 Annual Incentive Plan bonus was determined based on at least nine separate performance goals. Given that the Plan represents only a portion of total compensation and the relative percentage of Plan compensation represented by each of the Confidential Targets is fairly small, the Company does not believe that the disclosure of any of the underlying targets would be material to an

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 8

investor’s understanding of the Company’s annual incentive compensation awards under the Plan or the Company’s total executive compensation program. The Company believes that disclosing the Confidential Targets would not further the Staff’s objective of making executive compensation disclosure accessible to the average investor.

Instruction 1 to the rules governing the Compensation Discussion and Analysis states that the purpose of the Compensation Discussion and Analysis is to provide investors with “material information that is necessary to an understanding” of a company’s compensation arrangements. Thus, the rules governing the Compensation Discussion and Analysis merely require disclosure of the formula for determining awards to the extent material. Neither the rules nor the preamble to the rules expressly require performance target disclosure, if not considered to be material. The disclosures we provide regarding the structure of the incentive program and the amount of the annual incentive award that was achieved provide the investors with information sufficient to assess the degree of difficulty inherent in achieving the objectives. Given the complexity and number of sub-goals, disclosure and analysis of each of the individual Confidential Targets and their achievement levels is not material to the understanding of the Plan.

The Confidential Targets include confidential business and operational information that is not otherwise disclosed to the public.

The Company submits that certain of the Confidential Targets constitute confidential commercial or financial information, as those terms are defined by the standards set forth in Exemption 4 of the Freedom of Information Act and Rule 406 of the Securities Act of 1933, as amended (the “Securities Act”), and therefore the Company may properly withhold the Confidential Targets from public disclosure. The Confidential Targets should be afforded confidential treatment for the reasons set forth below:

| 1. | The Company has not publicly disclosed the Confidential Targets. |

The Company has consistently treated its targets and actual results for safety, segment cash flow, and alumina cash funding cost as highly confidential information that has not been publicly disclosed, but rather has been regarded as confidential inside the Company and has not been disclosed outside the Company. The Company has not, for example, disclosed any of this information to analysts. In particular, the Company has never publicly disclosed its safety statistics, cash flows or operational funding results on a segment or operating location basis, and believes, for the reasons discussed below, that such disclosure would result in significant competitive harm. As a result, the Company believes that the Confidential Targets may be withheld from disclosure because their disclosure would cause competitive harm to the Company.

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 9

| 2. | Disclosure of the Confidential Targets would cause competitive harm to the Company by providing its competitors with highly sensitive information regarding its business strategy. |

The Company believes the performance targets and actual performance for the just completed fiscal year for the Confidential Targets are sensitive, confidential financial information because they represent unique economic data with respect to the business. The Company believes that disclosure of this sensitive information would provide other aluminum manufacturers in the highly competitive metals industry, as well as the Company’s business partners, with insight into its operational and financial structure, and could jeopardize the Company’s ability to compete, as well as its future negotiating position in a variety of business transactions.

As most recently described in Amendment No. 4 to the Company’s Registration Statement, the Company operates in the highly fragmented and competitive metals industry. The Company competes with a number of large, well-established companies in each of the markets in which the Company operates. Competition in the metals industry is based primarily on costs, quality, service, price and technological innovation. Success in this field requires significant outlays of capital and human effort, reduction in, and maintenance of, costs, as well as innovation in production processes and product applications. Disclosure of the Confidential Targets creates a significant impediment because it provides non-public or foreign competitors, who are not required to disclose their targets, key knowledge of the Company’s business goals and future plans and, accordingly, would severely limit the Company’s ability to compete in the metals industry.

Safety. Disclosure of the safety metric and achievement could be harmful because it would allow a competitor to gain critical insight into the Company’s operational strengths and weaknesses in this area of particular focus. Because of the speed of competitive response in this industry, disclosure of these metrics and achievement levels with respect to the Confidential Targets would provide sufficient benchmark information to permit competitors to adjust their resources and strategy to the competitive detriment of the Company.

Downstream Free Cash Flow. The Company’s downstream business competes in the production and sale of rolled aluminum products with a number of other aluminum rolling mills, including large, single-purpose sheet mills, continuous casters and other multi-purpose mills. In addition, the Company’s downstream business competes with other rolled aluminum products suppliers, on the basis of quality, price, timeliness of delivery, technological innovation, and customer service. Disclosure of free cash flow metrics for the downstream segment would give

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 10

competitors key metrics on the Company’s capacity to re-invest in its assets and human capital. By having these clear and direct benchmarks, competitors could reset their own targets and productivity programs, impairing the Company’s ability to create a sustainable competitive position.

Alumina Cash Funding Cost. The Company’s upstream segment competes with a large number of other value-added metals producers on an international, national, regional and local basis. The Company’s primary product, aluminum, also competes with other materials, such as steel, copper, plastics, composite materials and glass, among others, for various applications. Alumina is the largest raw material cost component in producing aluminum, and therefore cost and funding information is particularly sensitive. The Company also competes, to a lesser extent, with primary metals producers, who typically sell to very large customers.

The Company has also provided historical data on achievement levels that demonstrate the difficulty of achieving such targets.

The Company also respectfully advises the Staff that it has revised the Registration Statement to provide historical data on annual bonus achievement levels in prior fiscal years to provide further information on the historical difficulty of achievement of performance objectives. Please see page 119. The Company believes disclosing the difficulty of achieving the performance targets, including the historical success rates in reaching the targets as shown below, provides investors with valuable information on which to assess the difficulty of achievement of performance goals.

In conclusion, the Company believes the disclosure in the Registration Statement of actual bonus amounts, the detailed description of the 2009 Incentive Plan, the aggregate percentage achievement, the Disclosed Targets, and information provided on the difficulty of achieving both the Disclosed Targets and the Confidential Targets provides more than adequate information for an investor. The Company believes that the Confidential Targets identified above are confidential information which, if disclosed, would result in significant competitive harm.

Financial Statements

Noranda Aluminum Holding Corporation

Note 2. Joint Venture Transaction

| 13. | Your disclosure explains that based on the fair values assigned to the assets acquired and liabilities assumed, you recorded a bargain purchase gain of $101.8 million. Please tell us if you have reassessed whether you have correctly identified |

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 11

all assets acquired and liabilities assumed as contemplated in ASC 805-30-25-4 and, if so, describe to us in sufficient detail the process you used to perform the reassessment. As part of your response, please tell us the substantive business reasons for the structure of the transaction. |

Response: The Company consummated the Joint Venture Transaction on August 31, 2009. Prior to recognizing the bargain purchase gain in December 2009, as required by ASC 805-30-25-4, the Company reassessed whether it had correctly identified all of the assets acquired and all of the liabilities assumed. As part of that reassessment, we reviewed the procedures used to measure and recognize the (a) the identifiable assets acquired and liabilities assumed, (b) the noncontrolling interest in the acquiree, if any, (c) our previously held equity interest in the acquired entities, and (d) the consideration transferred. In making this reassessment, we considered the business reasons for the structure of the transaction to ensure we had appropriately valued all important elements underlying the transaction.

Reassessment

The following timeline summarizes the key dates and activities in our accounting for the bargain purchase gain:

| 1. | On August 31, 2009, the Company closed the Joint Venture Transaction. |

| 2. | On November 16, 2009, the Company filed its third quarter 2009 Form 10-Q. In the financial statements included in the third quarter 2009 Form 10-Q, the Company recorded a $127.3 million credit in the balance sheet, labeled “unallocated purchase price”. The Company disclosed that this credit was being recorded in the balance sheet pending the final identification and evaluation of the fair value of the tangible and intangible assets acquired and liabilities assumed as of the closing date of the Joint Venture Transaction. That credit represented the excess of the preliminary fair values of the Company’s 50% joint venture interest over the carrying values of such joint venture interests as of August 31, 2009 of $12.5 million and the excess of the preliminary fair values of the remaining assets acquired and liabilities assumed in the Joint Venture Transaction over the estimated consideration of $114.8 million. |

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 12

In preparing the financial statements as of and for the three and nine months ended September 30, 2009, the Company completed the following processes related to determining the fair values of assets acquired and liabilities assumed:

| a. | The Company obtained the following preliminary valuations from a single third party valuation specialist as of August 31, 2009: |

| i. | Enterprise fair values of Gramercy and St. Ann. These enterprise fair value calculations were used to calculate the preliminary fair values of the Company’s existing 50% interest in Gramercy and St. Ann, and were updates of similar enterprise valuations prepared for the June 30, 2009 impairment testing of the Company’s equity method investments in those entities. |

| ii. | Valuations of inventory, real estate, machinery and equipment, and intangibles. The property and intangibles valuations considered an economic obsolescence factor to ensure that the values assigned to these assets were supported by the enterprise discounted cash flow valuations. |

| iii. | Valuation of the Government of Jamaica’s 51% non-controlling interest in St. Ann Jamaican Bauxite Partnership. |

| b. | The Company considered recorded accruals and existing documentation related to environmental liabilities and asset retirement obligations as of August 31, 2009. |

| i. | Re-valued pre-acquisition balances based on assumed applicable market participant discount rates |

| ii. | Compared projected cash flows to previously issued environmental reports |

| iii. | Reviewed previously issued environmental reports and correspondence with legal counsel for indications of unrecorded environmental liabilities. |

| c. | The Company obtained from third party actuarial specialists preliminary valuations of pension and OPEB obligations and plan assets as of August 31, 2009. |

| d. | The Company reviewed the trial balances of both Gramercy and St. Ann to identify any balance sheet accounts which no longer represented an asset or liability at the acquisition date. The Company also performed procedures to evaluate whether any additional assets and liabilities should be recorded. In doing so, the Company evaluated its contracts and relationships for intangible assets that meet the criteria for recognition apart from goodwill and provides guidance in applying the recognition criteria. At both Gramercy and St. Ann the Company evaluated the need to recognize an intangible asset for trademarks and tradenames, but concluded along with our third party valuation specialists that the value a market participant would assign to such an asset was immaterial given the nature of the business. At Gramercy, the Company recognized an asset for customer relationships; however, at St. Ann, the valuation for such an asset was considered to be immaterial. |

| e. | The Company performed a preliminary review of significant Gramercy and St. Ann accounting policies to identify any significant differences in accounting policies. |

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 13

| f. | The Company reviewed the accounting applied by Gramercy and St. Ann to individually significant transactions during the pre-acquisition period of 2009 to determine that appropriate recognition was applied to those transactions. |

| g. | The Company considered transactions between the acquisition date and the date the September 2009 financial statements were issued to determine whether any of the values assigned should be adjusted, or if any new assets or liabilities should be recognized. |

| h. | The Company considered the overall reasonableness of recording a bargain purchase gain based on the procedures performed as discussed above. While the Company believed the economics of the transaction clearly supported a bargain purchase gain, it deferred recognition of the bargain purchase gain until such time as it could perform the re-assessment required by ASC 805-30-25-4. |

| 3. | On March 2, 2010, the Company filed its 2009 Form 10-K. In its 2009 financial statements, the Company recorded an $18.5 million gain on its previously held equity interests and a $101.8 million bargain purchase gain after (i) completing the re-assessment of whether it had correctly identified all of the assets acquired and all of the liabilities assumed, and (ii) recognizing the additional assets and liabilities identified in the review. The Company utilized the guidance in ASC 805-30-3-4 through ASC 805-30-3-6 in connection with the re-assessment. |

| a. | The Company obtained the following final valuations from a single third party valuation specialist as of August 31, 2009: |

| i. | Enterprise fair values of Gramercy and St. Ann. |

| ii. | Valuations of inventory, real estate, machinery and equipment, and intangibles. We updated our economic obsolescence factor considerations to include the final enterprise fair values of Gramercy and St. Ann. |

| iii. | Valuation of the Government of Jamaica’s 51% non-controlling interest in St. Ann Jamaican Bauxite Partnership. |

In obtaining these final valuations, the Company re-assessed its cash flow projections in light of actual post-acquisition results to ensure such projections utilized at August 31, 2009 were appropriate. The Company also took into account knowledge gained from its post-acquisition integration activities in re-assessing its assumptions. This is not to say that the Company adjusted the August 31, 2009 valuations to reflect actual

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 14

results subsequent to August 31, 2009, which, because of an improvement in overall economic conditions, were generally more favorable than our assumptions. Rather, the Company identified where significant differences occurred, and assessed whether those results gave rise to alternative assumptions based on what was known or knowable at August 31, 2009. These subsequent developments did not call into question the Company’s valuations, but rather validated the significant assumptions.

| b. | The Company obtained the results of a comprehensive environmental review by a third party environmental specialist. The Company compared projected cash flows related to environmental liabilities and asset retirement obligations to previously issued environmental reports. It also considered whether the third party specialist’s reports contained indications of unrecorded environmental liabilities and asset retirement obligations. |

The Company made the determination to engage the third party environmental specialist because, as part of its evaluation of the business purposes behind the transaction, it recognized that concern over potential environmental remediation liabilities and asset retirement obligations would have been an important factor in a market participant’s determination of the enterprise values of Gramercy and St. Ann, as well as in the determination of the fair values of assumed liabilities.

| c. | The Company obtained from third party actuarial specialists final valuations of pension and OPEB obligations and plan assets as of August 31, 2009. |

| d. | The Company updated its review of the trial balances of both Gramercy and St. Ann to identify any balance sheet accounts which no longer represented an asset or liability at the acquisition date. In performing this updated review, the Company took into account knowledge gained from our post-acquisition integration activities and our year-end closing procedures. These post-acquisition integration activities included accounting mapping activities to incorporate the general ledger balances of Gramercy and St. Ann into the Company’s consolidated financial statements, and were therefore sufficiently detailed to identify necessary adjustments in the August 31, 2009 fair values of assets acquired and liabilities assumed. The Company also updated its previously performed procedures to evaluate whether any additional assets and liabilities should be recorded. Based on knowledge gained from our post-acquisition integration activities and our year-end closing procedures. The Company’s conclusion was that no other assets and liabilities should be recognized. |

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 15

| e. | The Company updated its consideration of the significant Gramercy and St. Ann accounting policies as part of the preparation of our year-end financial reporting process, to identify any significant differences in accounting policies. |

| f. | The Company considered transactions after the acquisition date up to the date the 2009 financial statements were issued to determine whether any of the values assigned should be adjusted, or if any new assets or liabilities should be recognized. |

| g. | The Company re-assessed the overall reasonableness of recording a bargain purchase gain. |

Substantive Business Reasons for the Structure

As consideration in the Joint Venture Transaction, we agreed to release Century from a guarantee for the funding of certain obligations, including environmental remediation and asset retirement obligations, approximately $23 million of trade payables to Gramercy for previously purchased alumina, and the obligation to purchase 50% of Gramercy’s smelter grade alumina output at cost in 2010. In connection with the Joint Venture Transaction, the Company entered into an agreement under which Century agreed to purchase 125kmt of alumina from Gramercy in 2009 at a price equal to the budgeted cash cost for the remainder of 2009, and other quantities in 2010 at market prices.

While not in a position to speak to Century’s business reasons for entering into the Joint Venture Transactions, the Company believes that Century’s decision to exit the partnership for a small cash payment was consistent with their other activities in 2009, as they curtailed a substantial portion of their US operations and sought to reduce their cost structure. For the Company’s part, it had no other alumina purchase contracts in place, and our make-versus-buy evaluation led us to believe that, given a view of pending improvements in aluminum prices, Gramercy’s alumina was the most cost advantageous source for the New Madrid smelter. Given that the Company had no expectation of needing to curtail the operations at Gramercy and St. Ann, it did not view releasing Century from their guarantees as harmful to its position. The ability to enter into a short-term supply agreement with Century allowed the Company to continue a reliable alumina source with a favorable cost structure, while allowing sufficient time to enter into third party contracts to absorb the portion of Gramercy’s alumina production volume that exceeded Noranda’s needs.

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 16

Note 22. Fair Value Measurements

| 14. | We note your disclosure of the fair value of your pension and OPEB plan assets is aggregated within one line of your tabular disclosure. Please tell us how you considered the disclosure requirements of paragraph d.5.ii. of ASC 715-20-50-1. |

Response: The Company respectfully advises that in the process of preparing financial statements for the year ended December 31, 2009, its interpretation of the disclosure requirements of ASC 715-20-50-1 produced two separate disclosures as of each date for which a consolidated balance sheet was presented:

| 1. | The fair value of each major category of plan assets can be derived from the Company’s financial statements in Note 14 “Pensions and other Post-Retirement Benefits”. The Company disclosed separately for Noranda Plans and St. Ann Plans, as those terms were defined in the notes, the pension plans’ weighted-average asset allocations at December 31, 2008 and 2009 by asset category. OPEB plan assets were not material. |

| 2. | In Note 22 “Fair Value Measurements” the Company disclosed the level within the fair value hierarchy in which the fair value measurements in their entirety fell, segregating fair value measurements between Level 1 and Level 2. |

The Company respectfully advises that it believes these disclosures were sufficient to enable financial statement users to assess the inputs and valuation techniques used to develop fair value measurements of plan assets in our December 31, 2009 financial statements. In light of the Staff’s comment the Company proposes making disclosures in the following format beginning with its condensed consolidated financial statements as of and for the three month period ended March 31, 2010 in its first quarter Form 10-Q:

The table below sets forth by level within the fair value hierarchy of our assets and liabilities that were measured at fair value on a recurring basis as of December 31, 2009 (in thousands):

| Level 1 | Level 2 | Level 3 | Total Fair Value | |||||||

| $ | $ | $ | $ | |||||||

Cash equivalents | 154,902 | — | — | 154,902 | ||||||

Derivative assets | — | 202,697 | — | 202,697 | ||||||

Derivative liabilities | — | (39,153 | ) | — | (39,153 | ) | ||||

Pension plan assets: | ||||||||||

Equity securities | 141,826 | 788 | — | 142,614 | ||||||

Fixed income | 79,458 | 2,787 | — | 82,245 | ||||||

Foreign currency | 3,758 | 1,346 | — | 5,104 | ||||||

Money market funds | 2,456 | 100 | — | 2,556 | ||||||

Cash and cash equivalents and other | 2,241 | — | — | 2,240 | ||||||

Total | 384,641 | 168,565 | — | 553,206 | ||||||

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 17

Note 25. Business Segment Information, page F-64

| 15. | We note your response to our prior comment number 34 and have reviewed the supplemental information provided. Based on your response, it appears the components of your “Upstream segment” (New Madrid Smelter, Gramercy & St. Ann) represent operating segments as defined by ASC 280-10-50-1. Further, the operating results you provide in your materials reviewed by the CODM appear to meet the quantitative thresholds for disclosure prescribed in ASC 280-10-50-12. In addition, the information you have provided thus far, does not appear to indicate that the operating segments comprising your “Upstream segment” meet the quantitative and qualitative aggregation criteria described in ASC 280-10-50-11. In particular, we note significantly different gross margin percentages for these operating segments indicating dissimilar economic characteristics as well as several qualitative differences. As such, please provide segment disclosures for these operating segments or otherwise explain why such disclosure is not necessary. |

Response: The Company respectfully advises that it has identified the Upstream segment consistent with a “management approach” (that is, based on its management reporting structure). With respect to ASC 280-10-50-1, the Company respectfully advises the Staff that Gramercy and St. Ann are not operating segments because all three of the requirements set forth in that guidance are not met. Specifically, with respect to item (b) of ASC 280-10-50-1, the operating results of Gramercy and St. Ann are not regularly reviewed by the CODM to make decisions about either the allocation of resources to those plant sites individually or about the assessment of their specific performance. Such resource allocation decisions and performance assessments are made by our CODM to the Upstream segment based on the aggregate operating results of the New Madrid smelter, Gramercy, and St. Ann.

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 18

We refer the Staff to the guidance in ASC 280-10-50-6, which provides that “[…] other factors may identify a single set of components as constituting a public entity’s operating segments, including the nature of the business activities of each component, the existence of managers responsible for them, and information presented to the board of directors.” We also refer the Staff to the guidance in ASC 280-10-50-7, which provides that “Generally, an operating segment has a segment manager who is directly accountable to and maintains regular contact with the chief operating decision maker to discuss operating activities, financial results, forecasts, or plans for the segment.” The following discussion describes in detail our consideration of these two paragraphs of ASC 280-10-50. We have considered these two paragraphs together, since they overlap to some degree related to the existence of managers responsible for the components, and the discussion of a segment manager.

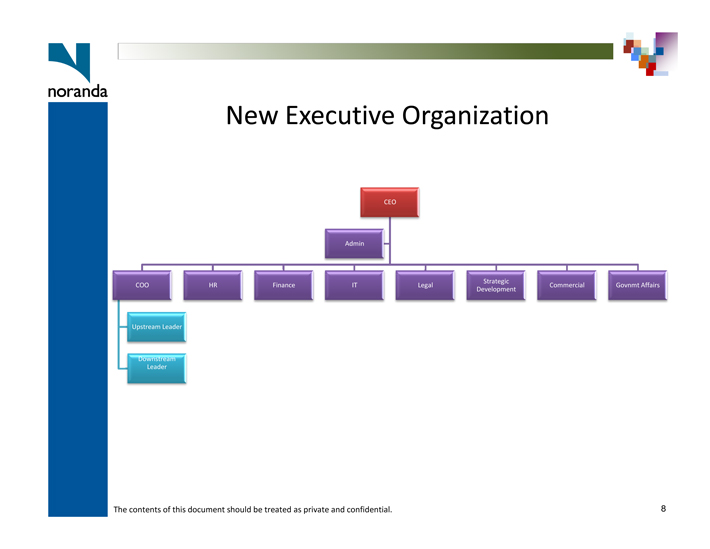

| 1. | The Company’s organizational structure provides a segment leader who is directly accountable and maintains regular contact with the CODM to discuss operating activities, financial results, forecasts or plans for the segment. Post-acquisition integration has resulted in a change away from the legal entity management structure in place when Gramercy and St. Ann were 50%-owned joint ventures. The post-acquisition Upstream structure consists of a Segment Leader who is a part of the Noranda Executive Team (“NET”). The NET is the group of senior executives over each of our key functional and strategic areas. The Upstream Segment Leader is a direct report to the Chief Operating Officer (the “COO”) who reports to the CODM, and who is also a member of the NET. Currently, the COO is the Upstream Segment Leader. In the upstream segment, the plant managers of New Madrid, Gramercy, and St. Ann report to the Upstream Segment Leader. (See Exhibit 15A to this letter.) |

The Company believes the role of Upstream Segment Leader is consistent with the description of a segment manager as provided in ASC 280-10-50-7. The Company therefore believes its organization supports the view that New Madrid, Gramercy, and St. Ann are a single segment. Through membership in the NET, the Upstream Segment Leader is directly accountable and maintains regular contact with the CODM to discuss operating activities, financial results, forecasts or plans for the upstream segment. Based on low authorization limits and limited interaction with the CODM, the Company does not believe the plant managers meet the definition of a segment manager, and that therefore, the plants are not operating segments.

The Company completed the acquisition of Gramercy and St. Ann at the end of August 2009, and the operational integration process for those locations is still in progress. In February 2010 with the announced workforce reduction in its U.S. operations, duplicate positions in New Madrid, Gramercy and St. Ann were eliminated and consolidated into single positions to support all three locations. The stated purpose of the workforce reduction was to de-layer decision making processes related to allocating resources and assessing performance. Although the role of Upstream Segment Leader is currently held by the COO to ensure effective execution of the transition, the Company’s organizational chart and authorization matrices clearly identify the COO and Upstream Segment Leader as separate roles.

The Company advises that the Management Packageprovided to the CODM is the standard reporting package utilized by the COO/Upstream Segment Leader and is not prepared specifically for use by the CODM. As such, the Management Package contains information that is useful for a variety of levels of analysis by the COO/Upstream Segment Leader, but the CODM’s focus is on the aggregate results of New Madrid, Gramercy, and St. Ann when making decisions regarding the allocation of resources of the assessment of results.

| 2. | Information presented to the Board of Directors focuses on performance of the integrated upstream business level, not the plant level. To illustrate, Noranda has provided under separate cover a copy of two board deliverables. Exhibit 15B is an excerpt of the portion of the February 2010 board of director materials which summarized 2009 results. See slides 57, 59, 60 related to 2009, and slides 70 and 72 which are summaries of 2010 budget information. Exhibit 15C is the December 2009 version of a monthly highlight “flash” report that is delivered to the board1. |

As is the case in the Management Package the Company previously provided to the Staff, the board materials contain key component metrics, provided for informational purposes to the Board, particularly given the recentness of the acquisition. However, such metrics are within the context of the integrated upstream operation, which is the level at which resource allocation decisions and performance assessment are determined. Given that the Company completed the acquisition of Gramercy and St. Ann at the end of August 2009 and continues along the process of post-acquisition integration, the Company does not believe the presentation of these component metrics over-rides the fact that the operations of the three components are organized and managed as an integrated upstream operation.

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 19

| 3. | The relationship of the New Madrid, Gramercy, and St. Ann operations essentially require that decisions be made at the integrated upstream business level and not at the facility level. First, market dynamics of price and volume for bauxite, alumina and aluminum move together. Second, the business activities of New Madrid, Gramercy and St. Ann are closely aligned through integration and raw material specifications, so that decisions must be made with total supply chain view in mind. |

As the aluminum prices and demand change, decisions are made at the Upstream level including capital allocation, sales volume allocation, customer allocation, product development resources and cost management. Our capital allocation decisions illustrate our focus on Gramercy as a low-cost alumina source for New Madrid.

In addition to being vertically integrated with New Madrid, Gramercy’s and St. Ann’s operations are closely aligned in terms of production processes, scheduling, quality control and related functions. The nature of the bauxite excavated – porosity, density, chemistry – are such that Gramercy’s plant facilities and production processes have been tailored to Jamaican bauxite, and cannot be easily substituted by bauxite from other sources.

The Company advises that it has maintained consistency within its 10-Q and 10-K filings, including MD&A, of discussing its business as an integrated producer of value-added primary aluminum products (upstream) and high quality rolled aluminum coils (downstream) segment. The Company has maintained similar consistency in its conference calls, press releases, and web site.

| 4. | Our incentive compensation structure is consistent with our view that assessment of performance is based on the contribution to the cash flows of the Upstream segment as a whole. Although not yet finalized, under the Company’s 2010 incentive compensation structure, we expect the CODM’s and COO’s metrics to be based principally on the financial results of the enterprise, the downstream segment and the integrated upstream segment, without specific dependency on New Madrid, Gramercy, or St. Ann as individual units. Gramercy and St. Ann plant management payouts will be 50% weighted to their contribution to New Madrid’s alumina cost. There are no incentive metrics for New Madrid, Gramercy or St. Ann profitability on a standalone basis. |

| 1 | Legal counsel for the Company will provide Exhibit 15B and Exhibit 15C under separate cover, on a confidential and supplemental basis pursuant to Rule 12b-4 under the Exchange Act and Rule 418 under the Securities Act. In accordance with Rule 12b-4 and Rule 418, legal counsel for the Company will request that these materials be returned promptly following completion of the Staff’s review thereof. Legal counsel for the Company also will request confidential treatment of these materials pursuant to the provisions of 17 C.F.R. §200.83. |

Ms. Parker & Ms. McNeil

Securities and Exchange Commission

March 29, 2010

Page 20

| 5. | Post-acquisition integration activities support our view that the Upstream Segment Leader has meaningful autonomy. Beginning in 2010, the operations of Gramercy and New Madrid have been restructured so that New Madrid purchases all of Gramercy’s smelter grade alumina output, and coordinates the negotiation and fulfillment of third party sales of excess material. Upstream’s leadership has worked directly with Noranda’s centralized commercial team, not Gramercy personnel to negotiate contracts between New Madrid and third parties related to the quantity of smelter grade alumina in excess of New Madrid’s needs. Upstream leadership and Noranda’s centralized commercial team, not St. Ann personnel, are responsible for renegotiating the renewal of the contract with Sherwin related to St. Ann bauxite in excess of Gramercy’s requirements. |

In summary, the Company respectfully advises the Staff that the Company’s facts and circumstances support its identification of a single operating segment for the upstream business in accordance with ASC 280. Decisions are made at the integrated upstream business level other than the operating location or component level. The information presented to the Board of Directors, the performance objectives and criteria underlying compensation plans, the level of autonomy given to segment managers and recent actions taken by segment managers based solely on their authority all provide sufficient evidence to support the Company’s view.

* * * * *

Should you request further clarification of any of the issues raised in this letter or the Registration Statement, please contact the undersigned at (212) 403-1000.

Sincerely,

/s/ Andrew J. Nussbaum

Andrew J. Nussbaum

Exhibit 4

| Nicholas A. Adams, Jr. | Henry F. Sattlethight | |

| V.P., Statistics & Business Information | Manager, Statistical Programs | |

| Tel: 1-703-358-2984 | Tel: 1-703-358-2985 | |

| Fax: 1-703-358-2961 | Fax: 1-703-358-2961 | |

E-mail: nadams@aluminum.org

| E-mail: hsattlethight@aluminum.org

|

U.S. PRIMARY ALUMINUM PRODUCTION

| Report for December 2009 | Issued: January 11, 2010 |

Based on Aluminum Association surveys, U.S. primary aluminum production totaled 1,727,167 metric tons (tonnes) in 2009, a decrease of 35.0 percent from the 2008 total of 2,659,053 tonnes. For the month of December 2009, the annual rate of production totaled 1,644,549 tonnes, off 31.7 percent from the December 2008 annual rate of 2,407,701 tonnes. Compared to the previous month, the annual rate of production rose 1.5 percent over the November 2009 total of 1,621,038 tonnes. Actual production for the month of December 2009 totaled 139,674 tonnes.

Participating companies account for 100 percent of U.S. primary aluminum production.

Primary Aluminum Production (Thousands of Metric Tons) | Dec. | % Chng Dec/Dec | Nov. 2009 | % Chng Dec/Nov | Year-to-Date | % Chng 09/08 | ||||||||||

| 2009 | 2008 | 2009 | 2008 | |||||||||||||

Annual Rate | 1,644.5 | 2,407.7 | -31.7 | 1,621.0 | 1.5 | 1,727.2 | 2,659.1 | -35.0 | ||||||||

This report is available on The Aluminum Association web site: www.aluminum.org.

| The Association estimates total industry shipments based on reports by its members of their shipments for the latest month. The Association expands these data to total industry utilizing expansion ratio that attempts to reflect the relationship of reporters to the total industry. While the Association believes that its statistical procedures and methods are reliable, it does not warrant the accuracy or completeness of the data. All data contained herein are subject to revision. © The Aluminum Association, Inc. |

4-1

REPORTING COMPANIES

Report Received (Date) | Participating Companies | |

January 8, 2010 | Alcoa Inc. | |

January 11, 2010 | Century Aluminum Co. | |

January 7, 2010 | Noranda Aluminum, Inc. | |

January 8, 2010 | Ormet Corporation | |

January 7, 2010 | Rio Tinto Alcan | |

| Due Association: | January 11,2010 | |

| Last Report Received: | January 11,2010 | |

4-2

U.S. PRIMARY ALUMINUM PRODUCTION

(metric tons)

| PR-1 Report: December | Issued: January 11, 2010 | |||||||||||

| Production | Average Daily Rate of Production | Annual Rate of Production | ||||||||||

| 2009 | 2008 | 2009 | 2008 | 2009 | 2008 | |||||||

January | 192,639 | 233,254 | 6,214 | 7,524 | 2,268,169 | 2,753,902 | ||||||

February | 149,371 | 219,268 | 5,151 | 7,561 | 1,880,014 | 2,767,314 | ||||||

March | 153,708 | 233,913 | 4,958 | 7,546 | 1,809,788 | 2,761,683 | ||||||

QTR Total | 495,718 | 686,435 | 5,447 | 7,543 | 1,988,320 | 2,760,827 | ||||||

April | 145,039 | 227,800 | 4,835 | 7,593 | 1,764,641 | 2,779,160 | ||||||

May | 147,027 | 235,613 | 4,743 | 7,600 | 1,731,124 | 2,781,753 | ||||||

June | 131,766 | 224,488 | 4,392 | 7,483 | 1,603,153 | 2,738,753 | ||||||

QTR Total | 423,832 | 687,901 | 4,657 | 7,559 | 1,699,986 | 2,766,723 | ||||||

July | 135,389 | 224,851 | 4,367 | 7,253 | 1,594,096 | 2,654,692 | ||||||

August | 133,409 | 222,153 | 4,304 | 7,166 | 1,570,783 | 2,622,839 | ||||||

September | 129,349 | 214,451 | 4,312 | 7,148 | 1,573,746 | 2,616,302 | ||||||

QTR Total | 398,147 | 661,455 | 4,328 | 7,190 | 1,579,605 | 2,631,440 | ||||||

October | 136,560 | 216,929 | 4,405 | 6,998 | 1,607,884 | 2,561,162 | ||||||

November | 133,236 | 202,402 | 4,441 | 6,747 | 1,621,038 | 2,469,304 | ||||||

December | 139,674 | 203,931 | 4,506 | 6,578 | 1,644,549 | 2,407,701 | ||||||

QTR Total | 409,470 | 623,262 | 4,451 | 6,775 | 1,624,528 | 2,479,499 | ||||||

Total Year | 1,727,167 | 2,659,053 | 4,732 | 7,265 | 1,727,167 | 2,659,053 | ||||||

This report is based on information reported to the Association by participants, which is aggregated by the Association. While the Association believes that its statistical procedures and methods are reliable, it does not warrant the accuracy or completeness of the data. All data contained herein are subject to revision.

4-3

Exhibit 15A