Exhibit 99.1

FS Investment Corporation

AN INTRODUCTION TO FSIC

FEBRUARY 19, 2014

PRESENTED BY:

Franklin Square Capital Partners is not affiliated with Franklin Resources/Franklin Templeton Investments or the Franklin Funds.

Important Considerations

An investment in the common stock of FS Investment Corporation (FSIC, we or us) involves a high degree of risk and may be considered speculative. The following are some of the risks an investment in our common stock involves; however, you should carefully consider all of the information found in the section of our Forms 10-Q and 10-K filings entitled “Risk Factors” and in our other public filings before deciding

to invest in shares of our common stock.

An investment strategy focused primarily on privately held companies presents certain challenges, including the lack of available information about these companies.

Investing in middle-market companies involves a number of significant risks, any one of which could have a material adverse effect on our operating results.

A lack of liquidity in certain of our investments may adversely affect our business.

We are subject to financial market risks, including changes in interest rates, which may have a substantial negative impact on our investments.

We have borrowed funds to make investments, which increases the volatility of our investments and may increase the risks of investing in our securities.

We have limited operating history and are subject to the business risks and uncertainties associated with any new business.

Our distributions may be funded from unlimited amounts of offering proceeds or borrowings, which may constitute a return of capital and reduce the amount of capital available to us for investment.

This presentation is for informational purposes only and is not an offer to buy or the solicitation of an offer to sell any securities of FSIC. The tender offer will be made only pursuant to an offer to purchase, letter of transmittal and related materials (the Tender Materials) that FSIC intends to distribute to its stockholders and file with the Securities and Exchange Commission (SEC). The full details of the tender offer, including complete instructions on how to tender shares of common stock, will be included in the Tender Materials, which FSIC will distribute to stockholders and file with the SEC upon the commencement of the tender offer. Stockholders are urged to carefully read the Tender Materials when they become available because they will contain important information, including the terms and conditions of the tender offer. Stockholders may obtain free copies of the Tender Materials that FSIC files with the SEC at the SEC’s website at: www.sec.gov or by calling the information agent who will be identified in the

Tender Materials. In addition, stockholders may obtain free copies of FSIC’s filings with the SEC from FSIC’s website at: www.fsinvestmentcorp.com or by contacting FSIC at Cira Centre, 2929 Arch Street, Suite 675, Philadelphia, PA 19104 or by phone

at (877) 628-8575.

2

Forward-Looking Statements

Some of the statements in this presentation constitute forward-looking statements because they relate to future events or the future performance or financial condition of FSIC. The forward-looking statements contained in this presentation may include statements as to: our future operating results; our business prospects and the prospects of our portfolio companies; the impact of the investments that we expect to make; the ability of our portfolio companies to achieve their objectives; our current and expected financings and investments; the adequacy of our cash resources, financing sources and working capital; the timing and amount of cash flows, distributions and dividends, if any, from our portfolio companies; our contractual arrangements and relationships with third parties; actual and potential co nflicts of interest with FB Income Advisor, LLC (FB Advisor), FS Investment Advisor, LLC, FS Energy and Power Fund, FSIC II Advisor, LLC, FS Investment Corporation II, GSO / Blackstone Debt Funds Management LLC or any of their respective affiliates; the dependence of our future success on the general economy and its effect on the industries in which we may invest; our use of financial leverage; the ability of FB Advisor to locate suitable investments for us and to monitor and administer our investments; the ability of FB Advisor or its affiliates to attract and retain highly talented professionals; our ability to maintain our qualification as a regulated investment company (RIC) and as a business development company (BDC); the impact on our business of the Dodd-Frank Wall Street Reform and Consumer Protection Act and the rules and regulations issued thereunder; the effect of changes to tax legislation and our tax position; the tax status of the enterprises in which we invest; our ability to complete the listing of our shares of common stock on the New York Stock Exchange LLC (NYSE); our ability to complete the related tender offer; and the price at which shares of our common stock may trade on the NYSE, which may be higher or lower than the purchase price in the tender offer.

In addition, words such as “anticipate,” “believe,” “expect” and “intend” indicate a forward-looking statement, although not all forward-looking statements include these words. The forward-looking statements contained in this presentation involve risks and uncertainties. Our actual results could differ materially from those implied or expressed in the forward-looking statements for any reason. Factors that could cause actual results to differ materially include: changes in the economy; risks associated with possible disruption in our operations or the economy generally due to terrorism or natural disasters; and future changes in laws or regulations and conditions in our operating areas.

We have based the forward-looking statements included in this presentation on information available to us on the date of this presentation. Except as required by the federal securities laws, we undertake no obligation to revise or update any forward-looking statements, whether as a result of new information, future events or otherwise. You are advised to consult any additional disclosures that we may make directly to stockholders or through reports that we have filed and may file in the future with the Securities and Exchange Commission (SEC), including annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K. In addition, information related to past performance, while helpful as an evaluative tool, is not necessarily indicative of future results, the achievement of which cannot be assured.

Investors should not view the past performance of FSIC, or information about the market, as indicative of FSIC’s future results.

3

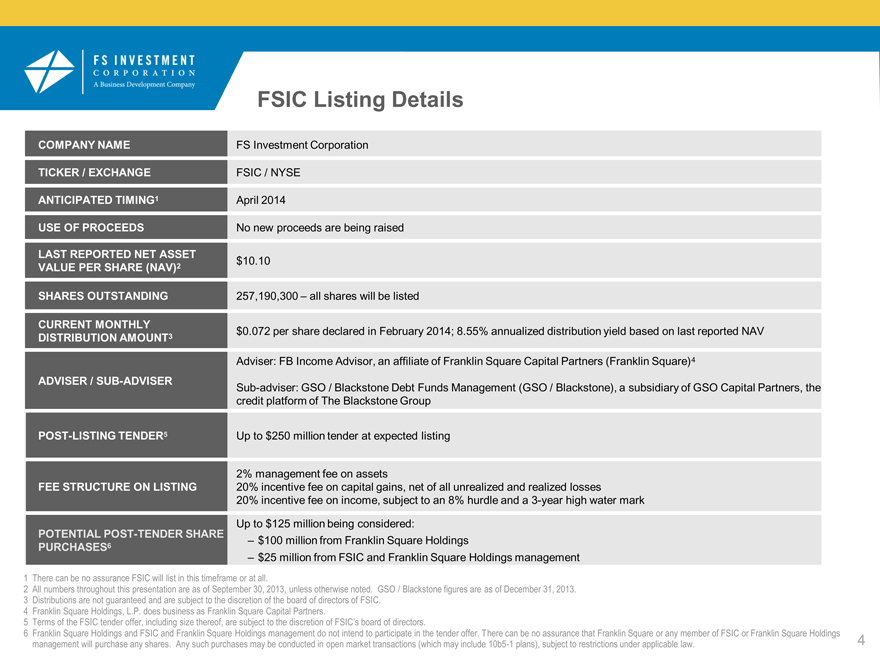

FSIC Listing Details

COMPANY NAME

FS Investment Corporation

TICKER / EXCHANGE

FSIC / NYSE

ANTICIPATED TIMING1

April 2014

USE OF PROCEEDS

No new proceeds are being raised

LAST REPORTED NET ASSET

VALUE PER SHARE (NAV)2

$10.10

SHARES OUTSTANDING

257,190,300 – all shares will be listed

CURRENT MONTHLY

DISTRIBUTION AMOUNT3

$0.072 per share declared in February 2014; 8.55% annualized distribution yield based on last reported NAV

Adviser: FB Income Advisor, an affiliate of Franklin Square Capital Partners (Franklin Square)4

ADVISER / SUB-ADVISER

Sub-adviser: GSO / Blackstone Debt Funds Management (GSO / Blackstone), a subsidiary of GSO Capital Partners, the

credit platform of The Blackstone Group

POST-LISTING TENDER5

Up to $250 million tender at expected listing

2% management fee on assets

FEE STRUCTURE ON LISTING

20% incentive fee on capital gains, net of all unrealized and realized losses

20% incentive fee on income, subject to an 8% hurdle and a 3-year high water mark

Up to $125 million being considered:

POTENTIAL POST-TENDER SHARE

–

$100 million from Franklin Square Holdings

PURCHASES6

–

$25 million from FSIC and Franklin Square Holdings management

1 There can be no assurance FSIC will list in this timeframe or at all.

2 All numbers throughout this presentation are as of September 30, 2013, unless otherwise noted. GSO / Blackstone figures are as of December 31, 2013.

3 Distributions are not guaranteed and are subject to the discretion of the board of directors of FSIC.

4 Franklin Square Holdings, L.P. does business as Franklin Square Capital Partners.

5 Terms of the FSIC tender offer, including size thereof, are subject to the discretion of FSIC’s board of directors.

6 Franklin Square Holdings and FSIC and Franklin Square Holdings management do not intend to participate in the tender offer. There can be no assurance that Franklin Square or any member of FSIC or Franklin Square Holdings

management will purchase any shares. Any such purchases may be conducted in open market transactions (which may include 10b5-1 plans), subject to restrictions under applicable law. 4

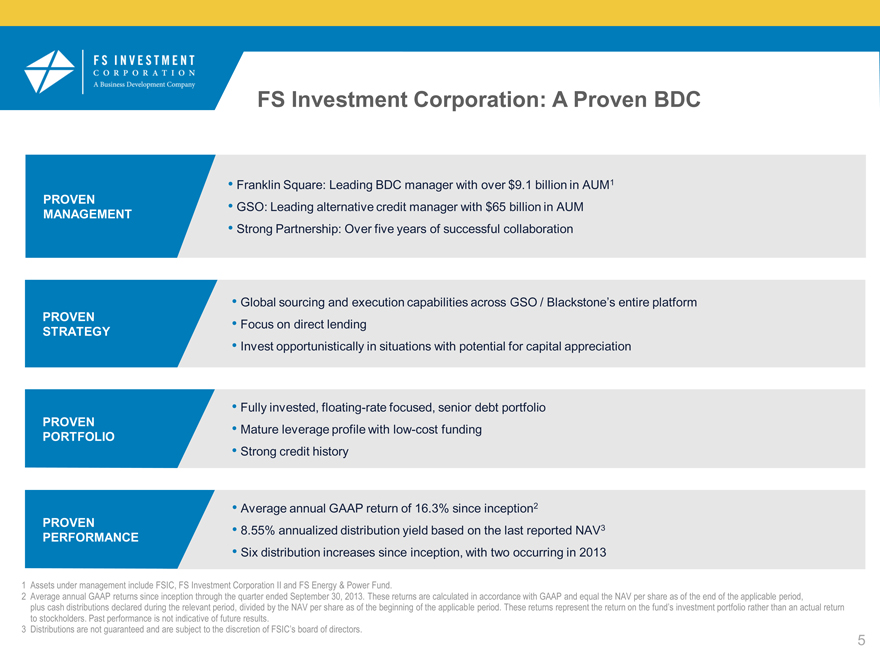

FS Investment Corporation: A Proven BDC

• Franklin Square: Leading BDC manager with over $9.1 billion in AUM1

PROVEN • GSO: Leading alternative credit manager with $65 billion in AUM

MANAGEMENT

• Strong Partnership: Over five years of successful collaboration

• Global sourcing and execution capabilities across GSO / Blackstone’s entire platform

PROVEN • Focus on direct lending

STRATEGY

• Invest opportunistically in situations with potential for capital appreciation

• Fully invested, floating-rate focused, senior debt portfolio

PROVEN • Mature leverage profile with low-cost funding

PORTFOLIO

• Strong credit history

• Average annual GAAP return of 16.3% since inception2

PROVEN • 8.55% annualized distribution yield based on the last reported NAV3

PERFORMANCE

• Six distribution increases since inception, with two occurring in 2013

1Assets under management include FSIC, FS Investment Corporation II and FS Energy & Power Fund.

2Average annual GAAP returns since inception through the quarter ended September 30, 2013. These returns are calculated in accordance with GAAP and equal the NAV per share as of the end of the applicable period, plus cash distributions declared during the relevant period, divided by the NAV per share as of the beginning of the applicable period. These returns represent the return on the fund’s investment portfolio rather than an actual return to stockholders. Past performance is not indicative of future results.

3Distributions are not guaranteed and are subject to the discretion of FSIC’s board of directors.

5

Proven Management

• Franklin Square: Leading BDC manager with over $9.1 billion in AUM

PROVEN • GSO: Leading alternative credit manager with $65 billion in AUM

MANAGEMENT

• Strong Partnership: Over five years of successful collaboration

PROVEN

STRATEGY

PROVEN

PORTFOLIO

PROVEN

PERFORMANCE

6

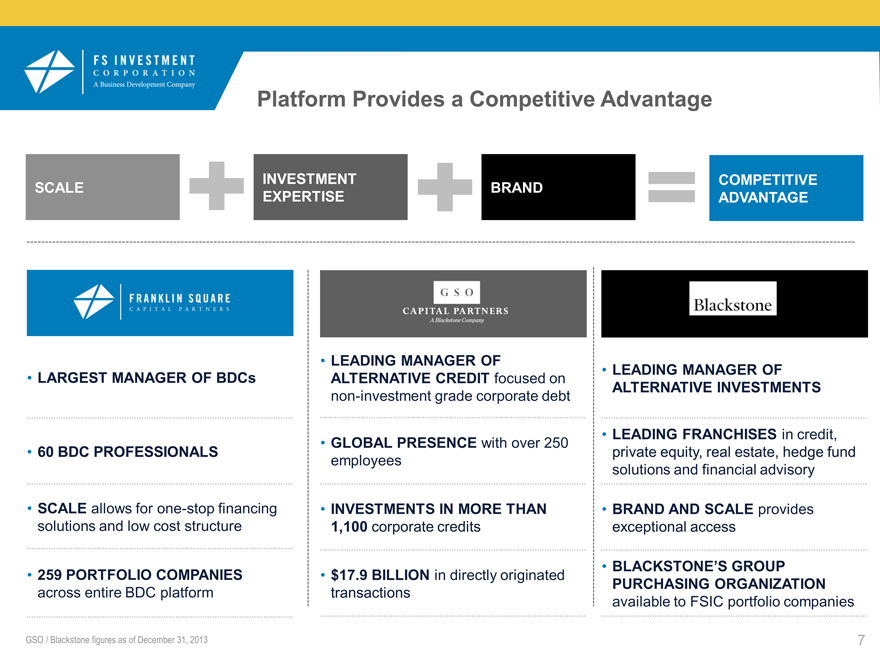

Platform Provides a Competitive Advantage

INVESTMENT COMPETITIVE

SCALE BRAND

EXPERTISE ADVANTAGE

LARGEST MANAGER OF BDCs

60 BDC PROFESSIONALS

SCALE allows for one-stop financing solutions and low cost structure

259 PORTFOLIO COMPANIES across entire BDC platform

GSO / Blackstone figures as of December 31, 2013

LEADING MANAGER OF

ALTERNATIVE CREDIT focused on non-investment grade corporate debt

GLOBAL PRESENCE with over 250 employees

INVESTMENTS IN MORE THAN 1,100 corporate credits

$17.9 BILLION in directly originated transactions

LEADING MANAGER OF ALTERNATIVE INVESTMENTS

LEADING FRANCHISES in credit, private equity, real estate, hedge fund solutions and financial advisory

BRAND AND SCALE provides exceptional access

BLACKSTONE’S GROUP

PURCHASING ORGANIZATION available to FSIC portfolio companies

7

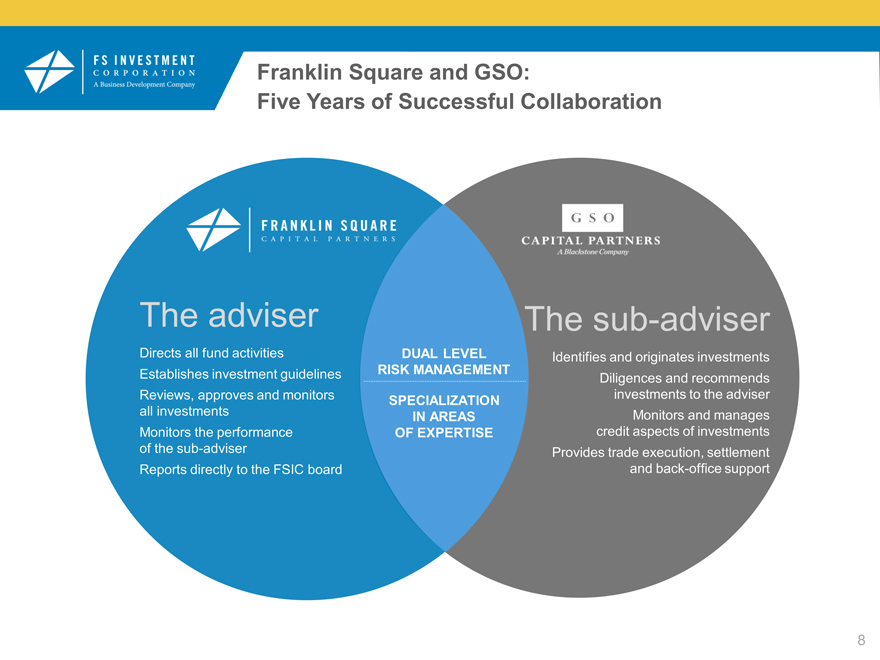

Franklin Square and GSO:

Five Years of Successful Collaboration

The adviser The sub-adviser

Directs all fund activities DUAL LEVEL Identifies and originates investments

Establishes investment guidelines RISK MANAGEMENT Diligences and recommends

Reviews, approves and monitors SPECIALIZATION investments to the adviser

all investments IN AREAS Monitors and manages

Monitors the performance OF EXPERTISE credit aspects of investments

of the sub-adviser Provides trade execution, settlement

Reports directly to the FSIC board and back-office support

8

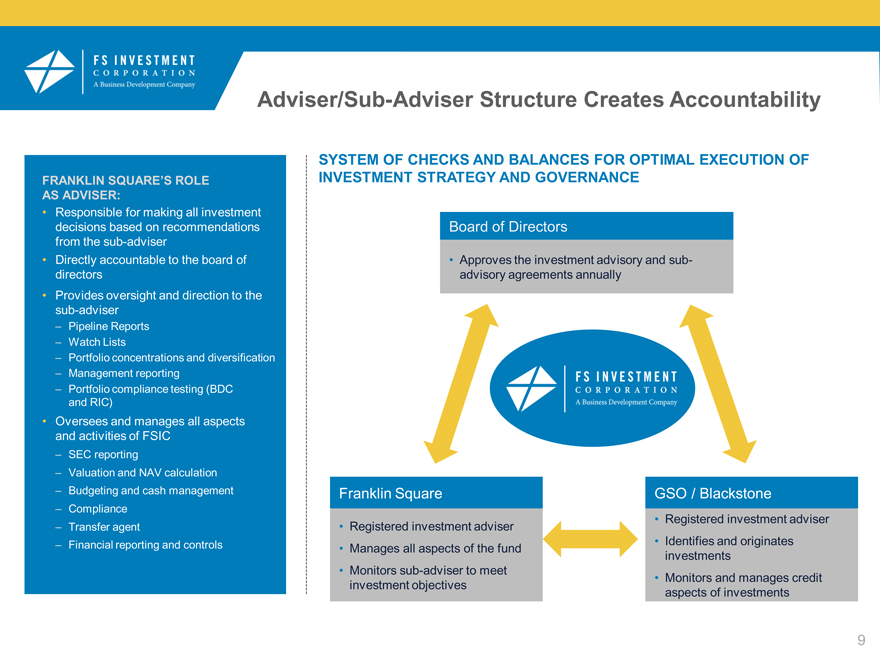

Adviser/Sub-Adviser Structure Creates Accountability

FRANKLIN SQUARE’S ROLE

AS ADVISER:

Responsible for making all investment decisions based on recommendations from the sub-adviser

Directly accountable to the board of directors

Provides oversight and direction to the sub-adviser

Pipeline Reports

Watch Lists

Portfolio concentrations and diversification

Management reporting

Portfolio compliance testing (BDC and RIC)

Oversees and manages all aspects and activities of FSIC

SEC reporting

Valuation and NAV calculation

Budgeting and cash management

Compliance

Transfer agent

Financial reporting and controls

SYSTEM OF CHECKS AND BALANCES FOR OPTIMAL EXECUTION OF INVESTMENT STRATEGY AND GOVERNANCE

Board of Directors

Approves the investment advisory and sub-advisory agreements annually

Franklin Square GSO / Blackstone

Registered investment adviser Registered investment adviser

Manages all aspects of the fund Identifies and originates

investments

Monitors sub-adviser to meet Monitors and manages credit

investment objectives aspects of investments

9

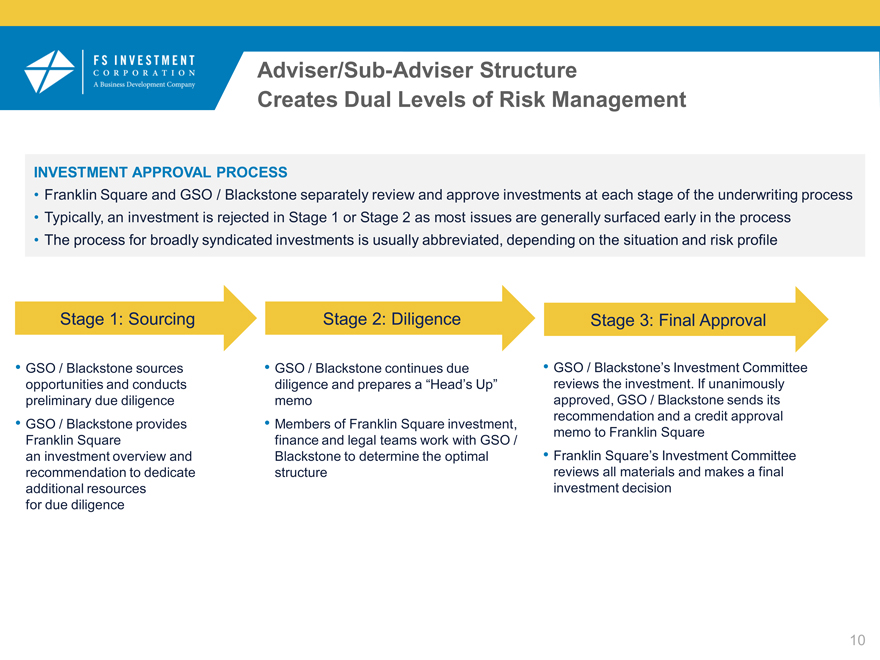

Adviser/Sub-Adviser Structure

Creates Dual Levels of Risk Management

INVESTMENT APPROVAL PROCESS

Franklin Square and GSO / Blackstone separately review and approve investments at each stage of the underwriting process

Typically, an investment is rejected in Stage 1 or Stage 2 as most issues are generally surfaced early in the process

The process for broadly syndicated investments is usually abbreviated, depending on the situation and risk profile

Stage 1: Sourcing

Stage 2: Diligence

GSO / Blackstone sources opportunities and conducts preliminary due diligence

GSO / Blackstone provides Franklin Square an investment overview and recommendation to dedicate additional resources for due diligence

GSO / Blackstone continues due diligence and prepares a “Head’s Up” memo

Members of Franklin Square investment, finance and legal teams work with GSO / Blackstone to determine the optimal structure

Stage 3: Final Approval

GSO / Blackstone’s Investment Committee reviews the investment. If unanimously approved, GSO / Blackstone sends its recommendation and a credit approval memo to Franklin Square

Franklin Square’s Investment Committee reviews all materials and makes a final investment decision

10

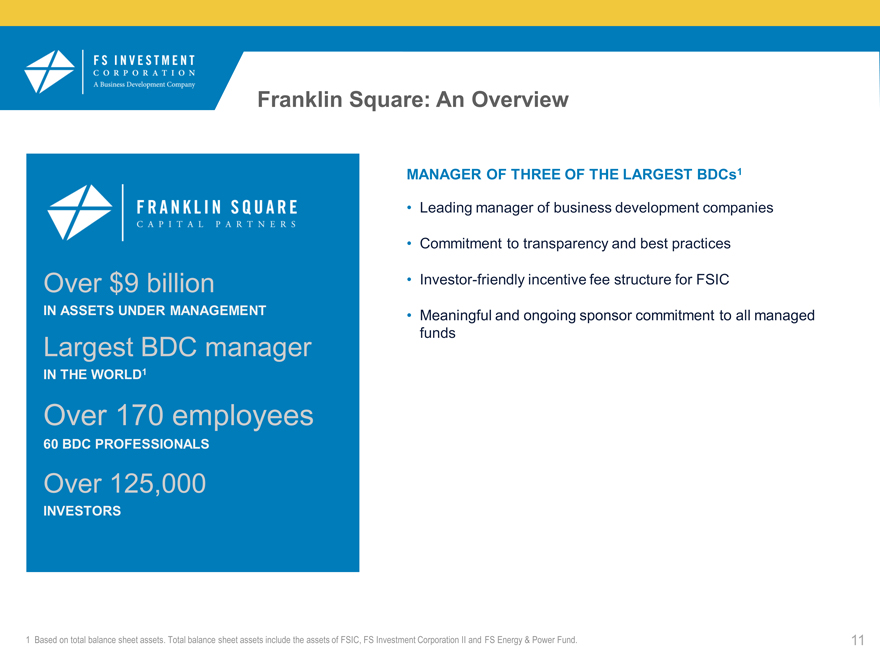

Franklin Square: An Overview

MANAGER OF THREE OF THE LARGEST BDCs1

• Leading manager of business development companies

• Commitment to transparency and best practices

Over $9 billion • Investor-friendly incentive fee structure for FSIC

IN ASSETS UNDER MANAGEMENT • Meaningful and ongoing sponsor commitment to all managed

funds

Largest BDC manager

IN THE WORLD1

Over 170 employees

60 BDC PROFESSIONALS

Over 125,000

INVESTORS

1 Based on total balance sheet assets. Total balance sheet assets include the assets of FSIC, FS Investment Corporation II and FS Energy & Power Fund.

11

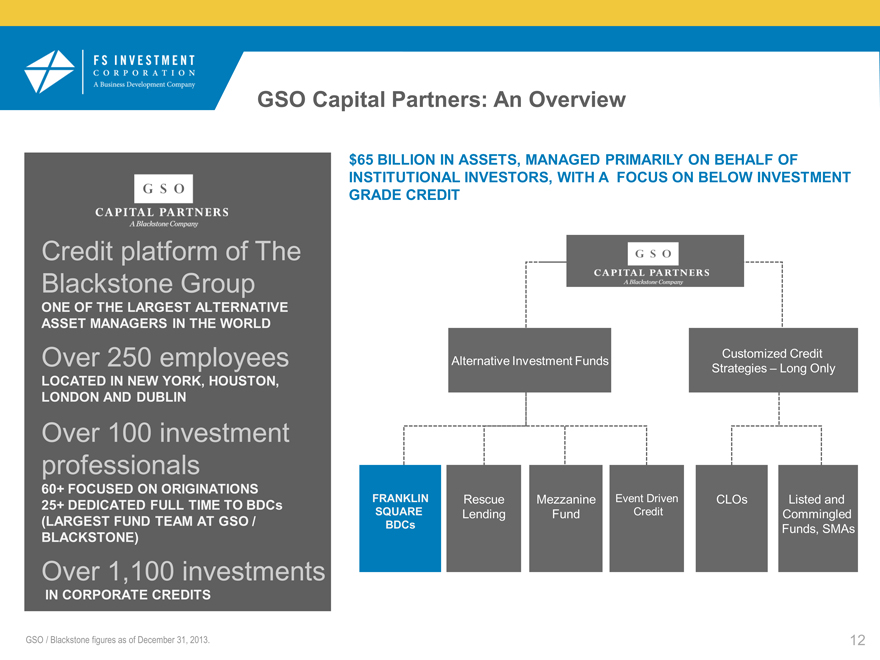

GSO Capital Partners: An Overview

$65 BILLION IN ASSETS, MANAGED PRIMARILY ON BEHALF OF

INSTITUTIONAL INVESTORS, WITH A FOCUS ON BELOW INVESTMENT

GRADE CREDIT

Credit platform of The

Blackstone Group

ONE OF THE LARGEST ALTERNATIVE

ASSET MANAGERS IN THE WORLD

Over 250 employees Alternative Investment Funds Customized Credit

Strategies – Long Only

LOCATED IN NEW YORK, HOUSTON,

LONDON AND DUBLIN

Over 100 investment

professionals

60+ FOCUSED ON ORIGINATIONS

25+ DEDICATED FULL TIME TO BDCs FRANKLIN Rescue Mezzanine Event Driven CLOs Listed and

SQUARE Lending Fund Credit Commingled

(LARGEST FUND TEAM AT GSO / BDCs Funds, SMAs

BLACKSTONE)

Over 1,100 investments

IN CORPORATE CREDITS

GSO / Blackstone figures as of December 31, 2013.

12

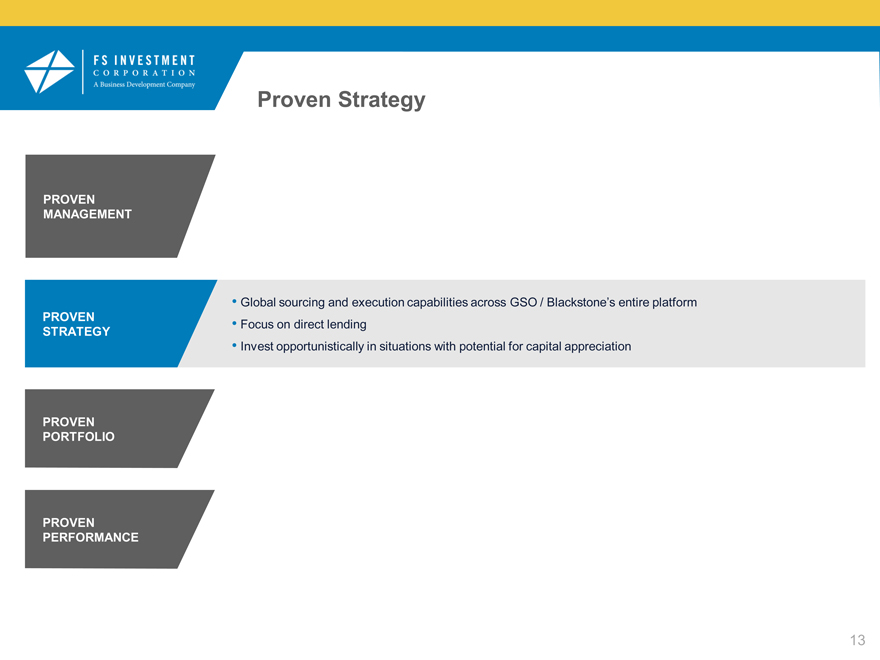

Proven Strategy

PROVEN

MANAGEMENT

• Global sourcing and execution capabilities across GSO / Blackstone’s entire platform

PROVEN • Focus on direct lending

STRATEGY

• Invest opportunistically in situations with potential for capital appreciation

PROVEN

PORTFOLIO

PROVEN

PERFORMANCE

13

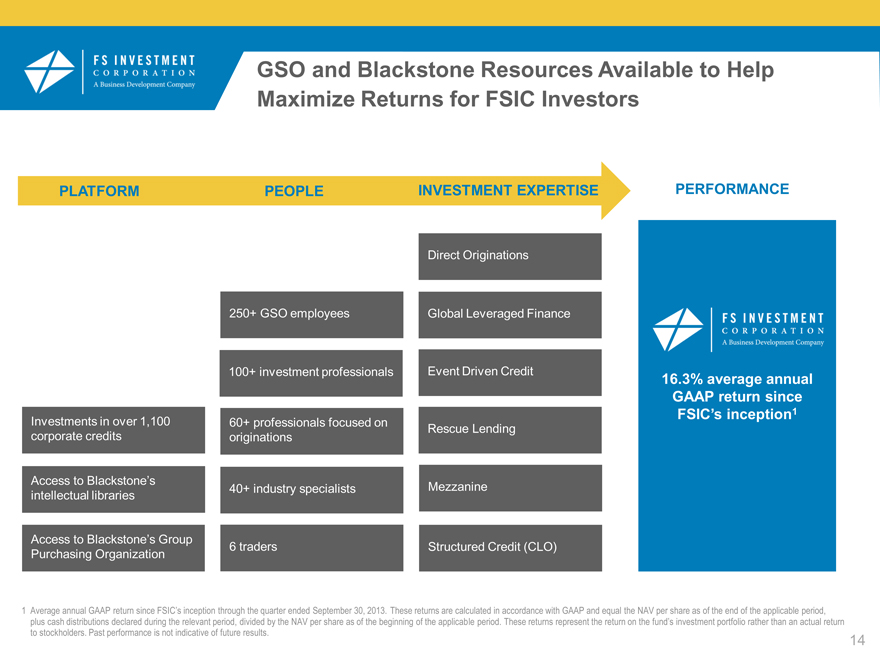

GSO and Blackstone Resources Available to Help

Maximize Returns for FSIC Investors

PLATFORM PEOPLE INVESTMENT EXPERTISE PERFORMANCE

Direct Originations

250+ GSO employees Global Leveraged Finance

100+ investment professionals Event Driven Credit 16.3% average annual

GAAP return since

FSIC’s inception1

Investments in over 1,100 60+ professionals focused on Rescue Lending

corporate credits originations

Access to Blackstone’s 40+ industry specialists Mezzanine

intellectual libraries

Access to Blackstone’s Group 6 traders Structured Credit (CLO)

Purchasing Organization

1Average annual GAAP return since FSIC’s inception through the quarter ended September 30, 2013. These returns are calculated in accordance with GAAP and equal the NAV per share as of the end of the applicable period, plus cash distributions declared during the relevant period, divided by the NAV per share as of the beginning of the applicable period. These returns represent the return on the fund’s investment portfolio rather than an actual return

to stockholders. Past performance is not indicative of future results.

14

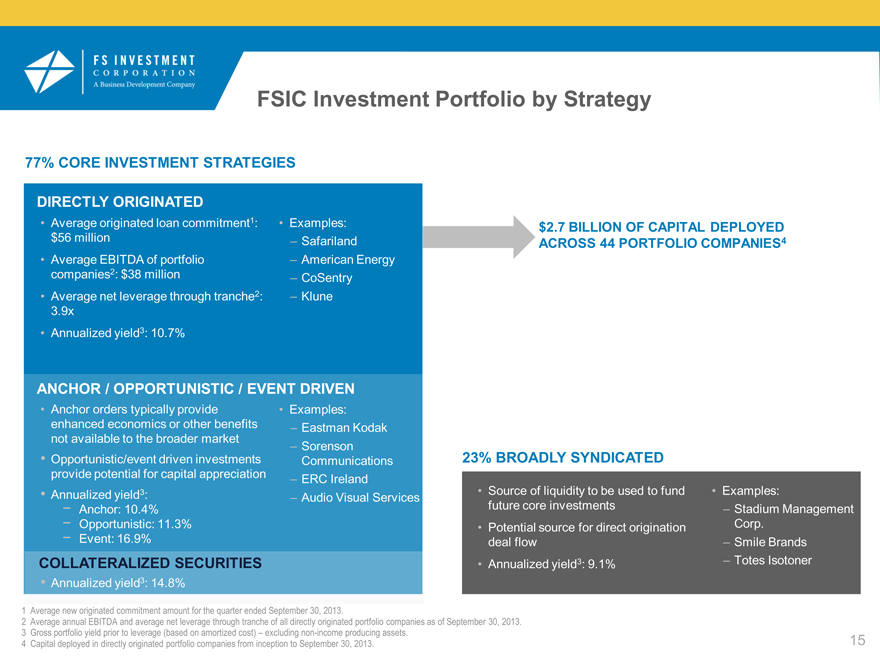

FSIC Investment Portfolio by Strategy

77% CORE INVESTMENT STRATEGIES

DIRECTLY ORIGINATED

Average originated loan commitment1: $56 million

Average EBITDA of portfolio companies2: $38 million

Average net leverage through tranche2: 3.9x

Annualized yield3: 10.7%

Examples: $2.7 BILLION OF CAPITAL DEPLOYED

– Safariland ACROSS 44 PORTFOLIO COMPANIES4

– American Energy

– CoSentry

– Klune

ANCHOR / OPPORTUNISTIC / EVENT DRIVEN

Anchor orders typically provide enhanced economics or other benefits not available to the broader market

Opportunistic/event driven investments

provide potential for capital appreciation

Annualized yield3:

- Anchor: 10.4%

- Opportunistic: 11.3%

- Event: 16.9%

COLLATERALIZED SECURITIES

Annualized yield3: 14.8%

Examples:

Eastman Kodak

Sorenson

Communications

ERC Ireland

Audio Visual Services

23% BROADLY SYNDICATED

Source of liquidity to be used to fund future core investments

Potential source for direct origination deal flow

Annualized yield3: 9.1%

1 Average new originated commitment amount for the quarter ended September 30, 2013.

2 Average annual EBITDA and average net leverage through tranche of all directly originated portfolio companies as of September 30, 2013.

3 Gross portfolio yield prior to leverage (based on amortized cost) – excluding non-income producing assets.

4 Capital deployed in directly originated portfolio companies from inception to September 30, 2013.

Examples:

Stadium Management

Corp.

Smile Brands

Totes Isotoner

15

`

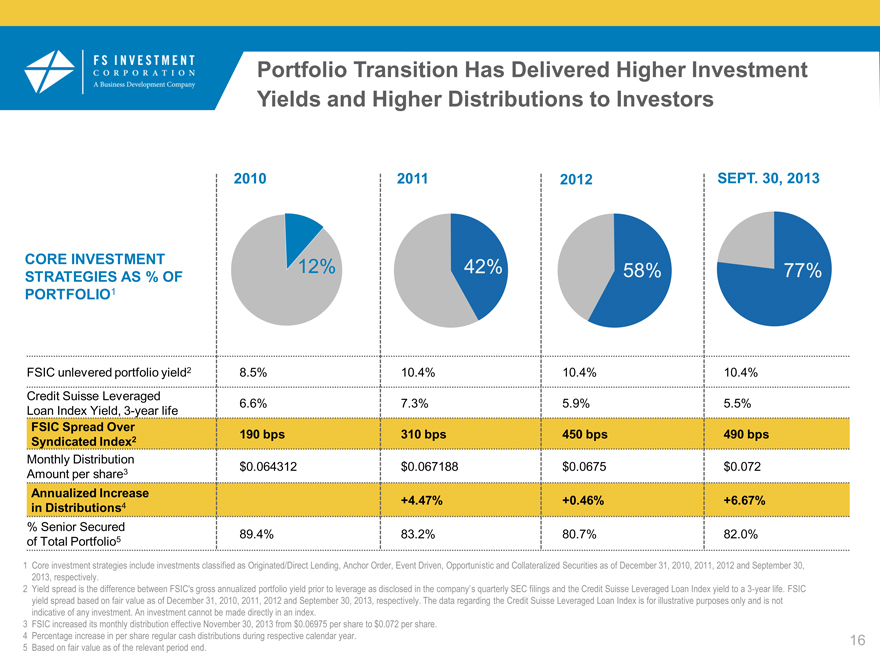

Portfolio Transition Has Delivered Higher Investment

Yields and Higher Distributions to Investors

2010

2011

2012

SEPT. 30, 2013

CORE INVESTMENT 12% 42% 58% 77%

STRATEGIES AS % OF

PORTFOLIO1

FSIC unlevered portfolio yield2 8.5% 10.4% 10.4% 10.4%

Credit Suisse Leveraged 6.6% 7.3% 5.9% 5.5%

Loan Index Yield, 3-year life

FSIC Spread Over 190 bps 310 bps 450 bps 490 bps

Syndicated Index2

Monthly Distribution $0.064312 $0.067188 $0.0675 $0.072

Amount per share3

Annualized Increase +4.47% +0.46% +6.67%

in Distributions4

% Senior Secured 89.4% 83.2% 80.7% 82.0%

of Total Portfolio5

1 Core investment strategies include investments classified as Originated/Direct Lending, Anchor Order, Event Driven, Opportunistic and Collateralized Securities as of December 31, 2010, 2011, 2012 and September 30, 2013, respectively.

2 Yield spread is the difference between FSIC’s gross annualized portfolio yield prior to leverage as disclosed in the company’s quarterly SEC filings and the Credit Suisse Leveraged Loan Index yield to a 3-year life. FSIC yield spread based on fair value as of December 31, 2010, 2011, 2012 and September 30, 2013, respectively. The data regarding the Credit Suisse Leveraged Loan Index is for illustrative purposes only and is not indicative of any investment. An investment cannot be made directly in an index.

3 FSIC increased its monthly distribution effective November 30, 2013 from $0.06975 per share to $0.072 per share.

4 Percentage increase in per share regular cash distributions during respective calendar year. 16

5 Based on fair value as of the relevant period end.

GSO / Blackstone Has Long-Standing Relationships with Private Equity Sponsors and Corporate Clients

GSO / BLACKSTONE’S SELECT NETWORK OF CLIENTS PROVIDES SIGNIFICANT SOURCING OPPORTUNITIES

AEA Investors

Access Capital Advisors

AIG Highstar

Altamont

Amaya Gaming Group

American Capital

Apex

Ares

Areva

Audax Group

Avista

Axa Private Equity

Bain Capital

Beecken Petty O’Keefe

Behrman Capital

Blackstone

Bruckman, Rosser, Sherrill

Carlyle

CD&R

Cerberus

Charlesbank Capital Partners

Chesapeake

CHS Capital

CIVC and Management

Clarion

Clayton Dubilier & Rice

Clearlake Capital

Crestview Partners

CVC Capital Partners

Cypress Group

Diamond Castle

DLJ Merchant Banking

Dunes Point

EIG

First Atlantic

Genstar

Golden Gate Capital

Goldman Sachs

Goldner Hawn Johnson Morrison

Gordon Brothers

Gores Capital

Graham Partners

Harvest Partners

Hellman & Friedman

Insight Equity

Investcorp

Jeff Gural

JLL Partners

Jupiter Partners

Kanders

Kolhberg Kravis Roberts

Leonard Green & Partners

Lincolnshire

Lion Capital

LS Power

Mid Europa Partners

Monitor Clipper Partners

Morgan Stanley

NANA Regional Corp.

Natural Gas Partners

Nautic Partners

NBC

Nova Capital Management

Oak Hill

Odyssey Investment Partners

Parthenon Capital

Permira

Plain Exploration

Platinum Equity

Quicksilver Resources

Ripplewood

Riverstone

Rockland Capital

Sequel Holdings

Siris Capital

Snow, Phipps Group

Sony / ATV

Southfield Capital

SPC Partners

Starwood Capital

Stephens Capital Partners

Summit Partners

TA Associates

Tailwind Capital

Tenaska Power Fund

Thomas Lee

TPG

Triangle Management

Vance Street

Vector

Vestar Capital

Victor Homes

Warburg Pincus

Wellspring

17

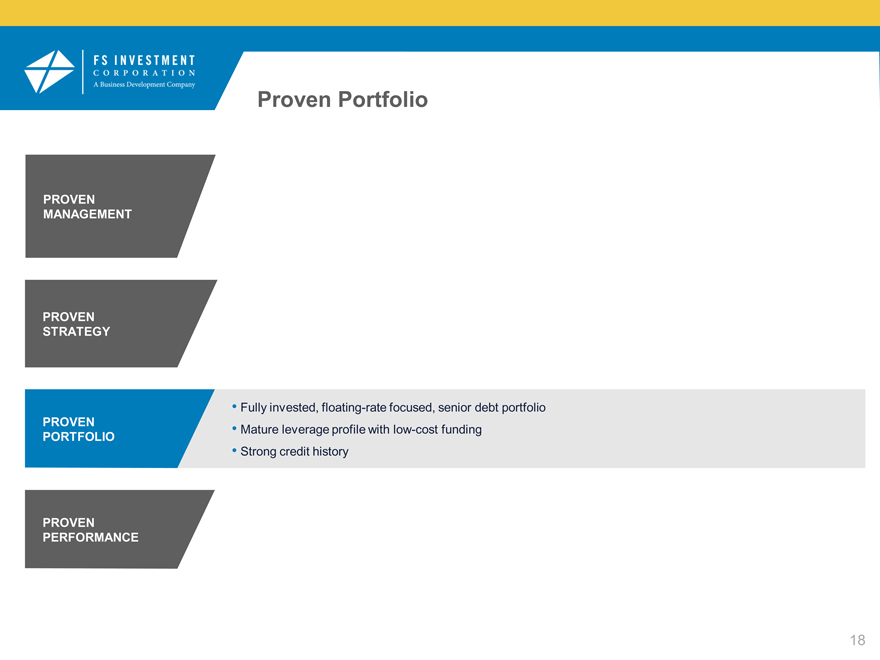

Proven Portfolio

PROVEN

MANAGEMENT

PROVEN

STRATEGY

• Fully invested, floating-rate focused, senior debt portfolio

PROVEN • Mature leverage profile with low-cost funding

PORTFOLIO

• Strong credit history

PROVEN

PERFORMANCE

18

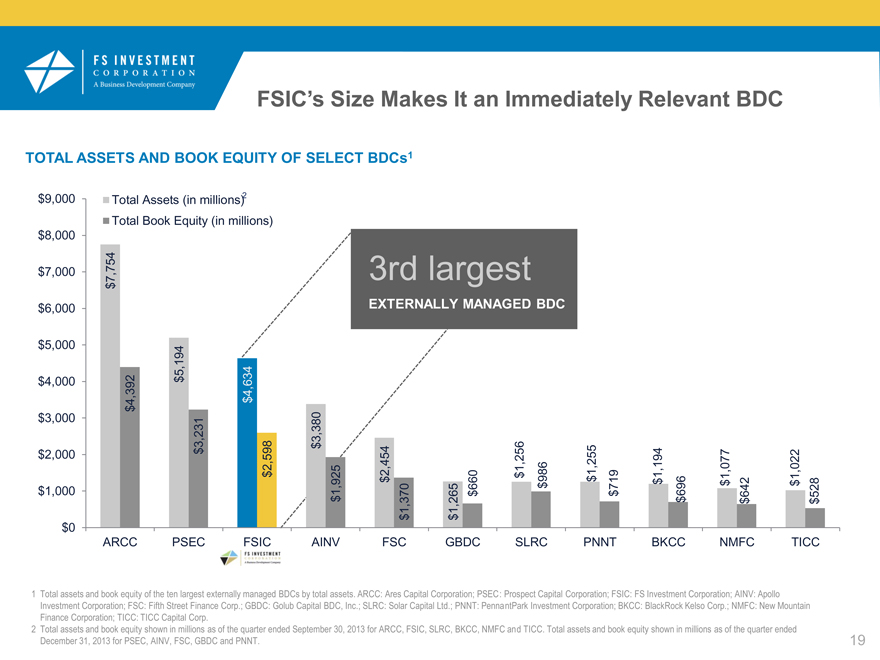

FSIC’s Size Makes It an Immediately Relevant BDC

TOTAL ASSETS AND BOOK EQUITY OF SELECT BDCs1

$9,000 Total Assets (in millions)2

Total Book Equity (in millions)

$8,000

$7,000 7,754 3rd largest

$

$6,000 EXTERNALLY MANAGED BDC

$5,000

5,194 34

$4,000 2 $ 4,6

4,39 $

$

$3,000 3,231 3,380

$

$2,000 $

2,598 5 ,454 1,256 6 ,255 ,194 ,077 ,022

$ 2 0 $ 98 1 1 1 1

$1,000 1,92 $

$ $ 66 $ $ 719 $ 696 $ 642 $ 528

$ 1,370 1,265 $ $ $

$ $

$0

ARCC PSEC FSIC AINV FSC GBDC SLRC PNNT BKCC NMFC TICC

1 Total assets and book equity of the ten largest externally managed BDCs by total assets. ARCC: Ares Capital Corporation; PSEC: Prospect Capital Corporation; FSIC: FS Investment Corporation; AINV: Apollo

Investment Corporation; FSC: Fifth Street Finance Corp.; GBDC: Golub Capital BDC, Inc.; SLRC: Solar Capital Ltd.; PNNT: PennantPark Investment Corporation; BKCC: BlackRock Kelso Corp.; NMFC: New Mountain

Finance Corporation; TICC: TICC Capital Corp.

2 Total assets and book equity shown in millions as of the quarter ended September 30, 2013 for ARCC, FSIC, SLRC, BKCC, NMFC and TICC. Total assets and book equity shown in millions as of the quarter ended

December 31, 2013 for PSEC, AINV, FSC, GBDC and PNNT. 19

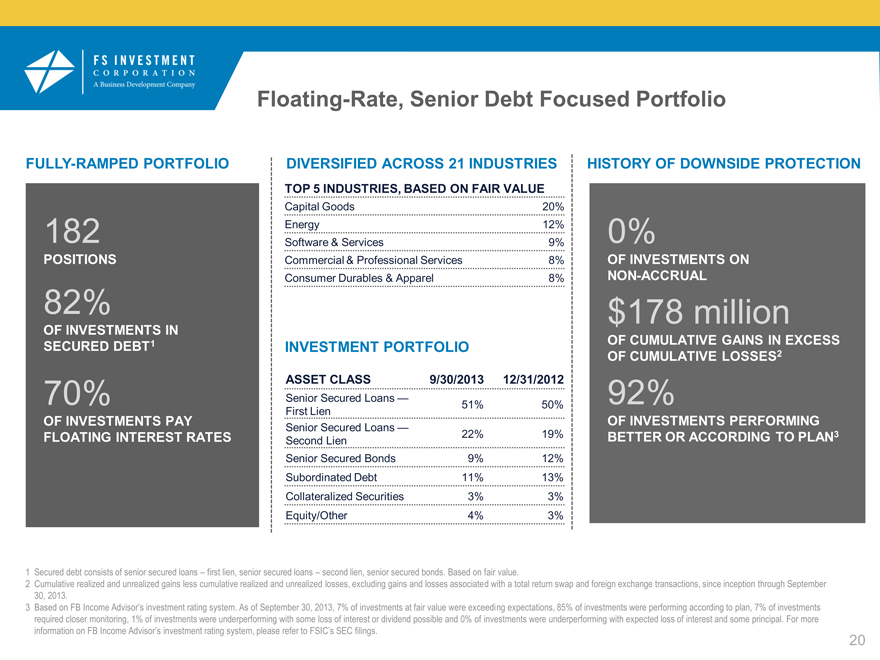

Floating-Rate, Senior Debt Focused Portfolio

FULLY-RAMPED PORTFOLIO DIVERSIFIED ACROSS 21 INDUSTRIES HISTORY OF DOWNSIDE PROTECTION

TOP 5 INDUSTRIES, BASED ON FAIR VALUE

Capital Goods 20%

182 Energy 12% 0%

Software & Services 9%

POSITIONS Commercial & Professional Services 8% OF INVESTMENTS ON

Consumer Durables & Apparel 8% NON-ACCRUAL

82% $178 million

OF INVESTMENTS IN

SECURED DEBT1 INVESTMENT PORTFOLIO OF CUMULATIVE GAINS IN EXCESS

OF CUMULATIVE LOSSES2

ASSET CLASS 9/30/2013 12/31/2012

70% Senior Secured Loans — 92%

First Lien 51% 50%

OF INVESTMENTS PAY OF INVESTMENTS PERFORMING

Senior Secured Loans —

FLOATING INTEREST RATES Second Lien 22% 19% BETTER OR ACCORDING TO PLAN3

Senior Secured Bonds 9% 12%

Subordinated Debt 11% 13%

Collateralized Securities 3% 3%

Equity/Other 4% 3%

1 Secured debt consists of senior secured loans – first lien, senior secured loans – second lien, senior secured bonds. Based on fair value.

2 Cumulative realized and unrealized gains less cumulative realized and unrealized losses, excluding gains and losses associated with a total return swap and foreign exchange transactions, since inception through September 30, 2013.

3 Based on FB Income Advisor’s investment rating system. As of September 30, 2013, 7% of investments at fair value were exceeding expectations, 85% of investments were performing according to plan, 7% of investments required closer monitoring, 1% of investments were underperforming with some loss of interest or dividend possible and 0% of investments were underperforming with expected loss of interest and some principal. For more information on FB Income Advisor’s investment rating system, please refer to FSIC’s SEC filings.

20

Low Cost of Leverage Allows for Focus on Senior Debt

TYPE OF FACILITY MATURITY

FACILITIES AS OF SEPTEMBER 30, 2013 RATE

FACILITY AMOUNT DATE

(in thousands)

Citibank Credit Facility Revolving L + 1.75% $550,000 August 29, 2015

Deutsche Bank Credit Facility1 Revolving L + 1.50% $125,000 December 20, 2014

J.P. Morgan Facility Repurchase 3.25% $950,000 April 15, 2017

Wells Fargo Credit Facility Revolving L + 1.50% to 2.75% $250,000 May 17, 2017

Total debt outstanding under debt facilities $1,892,504

Debt/equity ratio 72.9%

% of debt outstanding at fixed interest rates 47.9%

% of debt outstanding at variable interest rates 52.1%

Gross annualized portfolio yield prior to leverage 10.4%

Weighted average cost of debt 2.7%

Net interest margin 770 bps

1 On December 20, 2013, the maturity of the Deutsche Bank Credit Facility was extended to December 20, 2014 and the maximum commitment amount was reduced from $240 million to $125 million.

21

PROVEN

MANAGEMENT

PROVEN

STRATEGY

PROVEN

PORTFOLIO

FS Investment Corporation: A Proven BDC

Average annual GAAP return of 16.3% since inception1

PROVEN

8.55% annualized distribution yield based on the last reported NAV2

PERFORMANCE

Six distribution increases since inception, with two occurring in 2013

1Average annual GAAP returns since inception through the quarter ended September 30, 2013. These returns are calculated in accordance with GAAP and equal the NAV per share as of the end of the applicable period, plus cash distributions declared during the relevant period, divided by the NAV per share as of the beginning of the applicable period. These returns represent the return on the fund’s investment portfolio rather than an actual return to stockholders.

2Distributions are not guaranteed and are subject to the discretion of FSIC’s board of directors.

22

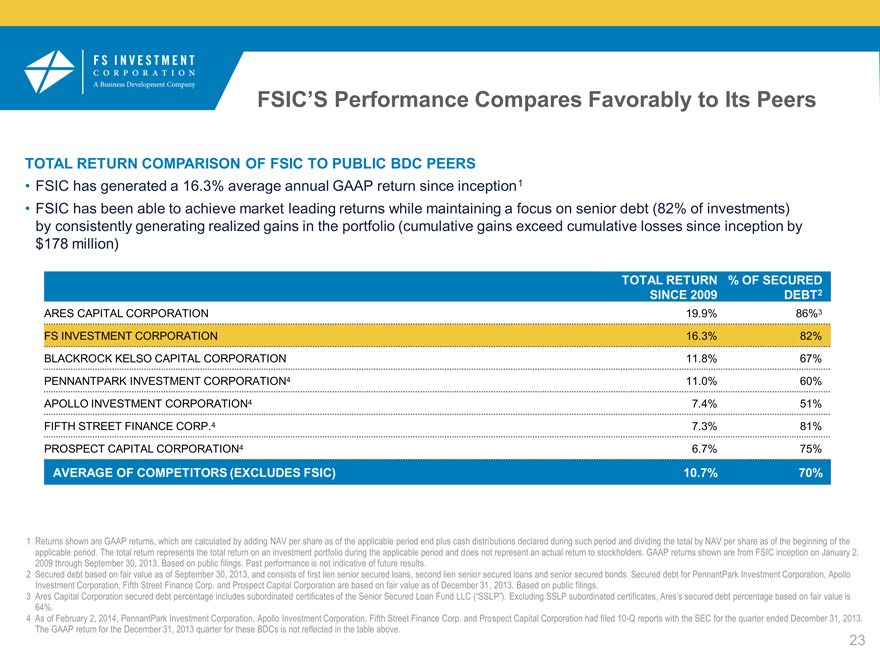

FSIC’S Performance Compares Favorably to Its Peers

TOTAL RETURN COMPARISON OF FSIC TO PUBLIC BDC PEERS

FSIC has generated a 16.3% average annual GAAP return since inception 1

FSIC has been able to achieve market leading returns while maintaining a focus on senior debt (82% of investments) by consistently generating realized gains in the portfolio (cumulative gains exceed cumulative losses since inception by $178 million)

TOTAL RETURN% OF SECURED

SINCE 2009 DEBT2

ARES CAPITAL CORPORATION 19.9% 86%3

FS INVESTMENT CORPORATION 16.3% 82%

BLACKROCK KELSO CAPITAL CORPORATION 11.8% 67%

PENNANTPARK INVESTMENT CORPORATION4 11.0% 60%

APOLLO INVESTMENT CORPORATION4 7.4% 51%

FIFTH STREET FINANCE CORP.4 7.3% 81%

PROSPECT CAPITAL CORPORATION4 6.7% 75%

AVERAGE OF COMPETITORS (EXCLUDES FSIC) 10.7% 70%

1 Returns shown are GAAP returns, which are calculated by adding NAV per share as of the applicable period end plus cash distributions declared during such period and dividing the total by NAV per share as of the beginning of the applicable period. The total return represents the total return on an investment portfolio during the applicable period and does not represent an actual return to stockholders. GAAP returns shown are from FSIC inception on January 2, 2009 through September 30, 2013. Based on public filings. Past performance is not indicative of future results.

2 Secured debt based on fair value as of September 30, 2013, and consists of first lien senior secured loans, second lien senior secured loans and senior secured bonds. Secured debt for PennantPark Investment Corporation, Apollo Investment Corporation, Fifth Street Finance Corp. and Prospect Capital Corporation are based on fair value as of December 31, 2013. Based on public filings.

3 Ares Capital Corporation secured debt percentage includes subordinated certificates of the Senior Secured Loan Fund LLC (“SSLP”). Excluding SSLP subordinated certificates, Ares’s secured debt percentage based on fair value is

64%.

4 As of February 2, 2014, PennantPark Investment Corporation, Apollo Investment Corporation, Fifth Street Finance Corp. and Prospect Capital Corporation had filed 10-Q reports with the SEC for the quarter ended December 31, 2013. The GAAP return for the December 31, 2013 quarter for these BDCs is not reflected in the table above. 23

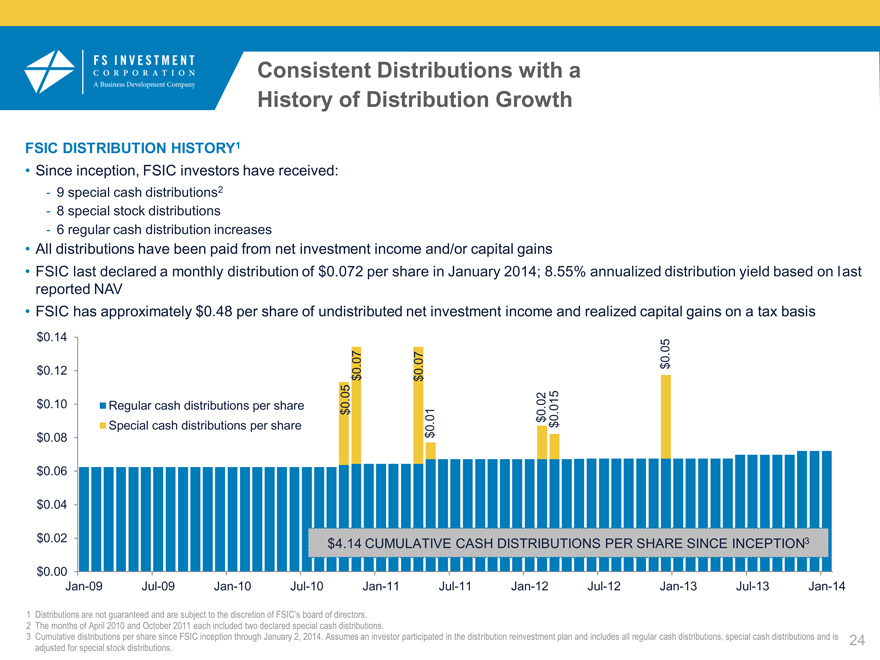

Consistent Distributions with a

History of Distribution Growth

FSIC DISTRIBUTION HISTORY1

Since inception, FSIC investors have received:

9 special cash distributions2

8 special stock distributions

6 regular cash distribution increases

All distributions have been paid from net investment income and/or capital gains

FSIC last declared a monthly distribution of $0.072 per share in January 2014; 8.55% annualized distribution yield based on last reported NAV

FSIC has approximately $0.48 per share of undistributed net investment income and realized capital gains on a tax basis

$0.14

05

.

07 07 0

$0.12 0 . 0 . $

$ $

05

$0.10 Regular cash distributions per share 0 . . 02 015

$ 0 .

01 $ 0

Special cash distributions per share . $

0

$0.08 $

$0.06

$0.04

$0.02 $4.14 CUMULATIVE CASH DISTRIBUTIONS PER SHARE SINCE INCEPTION3

$0.00

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14

1 Distributions are not guaranteed and are subject to the discretion of FSIC’s board of directors.

2 The months of April 2010 and October 2011 each included two declared special cash distributions.

3 Cumulative distributions per share since FSIC inception through January 2, 2014. Assumes an investor participated in the distribution reinvestment plan and includes all regular cash distributions, special cash distributions and is 24

adjusted for special stock distributions.

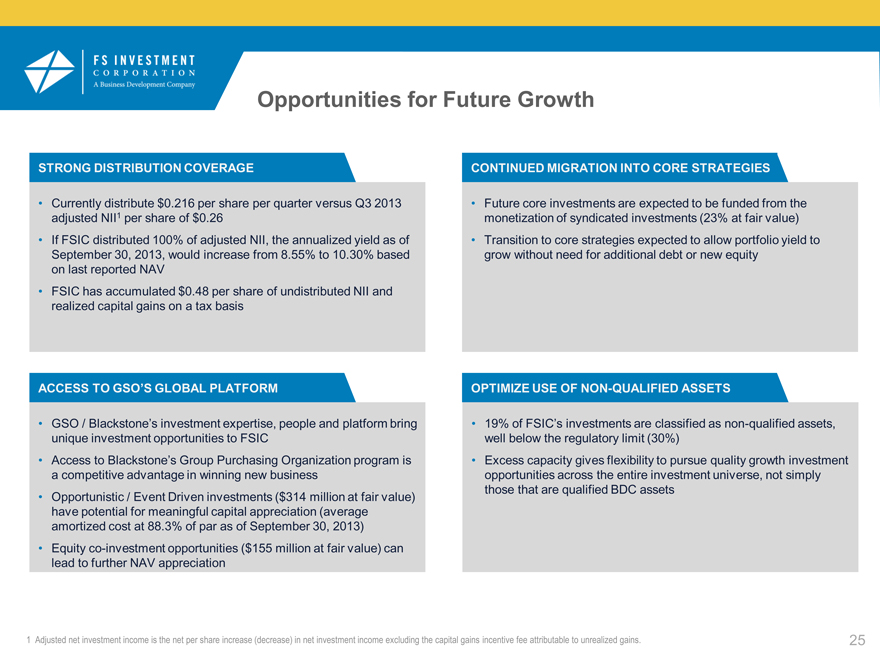

Opportunities for Future Growth

STRONG DISTRIBUTION COVERAGE

Currently distribute $0.216 per share per quarter versus Q3 2013 adjusted NII1 per share of $0.26

If FSIC distributed 100% of adjusted NII, the annualized yield as of

September 30, 2013, would increase from 8.55% to 10.30% based on last reported NAV

FSIC has accumulated $0.48 per share of undistributed NII and realized capital gains on a tax basis

ACCESS TO GSO’S GLOBAL PLATFORM

GSO / Blackstone’s investment expertise, people and platform bring unique investment opportunities to FSIC

Access to Blackstone’s Group Purchasing Organization program is a competitive advantage in winning new business

Opportunistic / Event Driven investments ($314 million at fair value) have potential for meaningful capital appreciation (average amortized cost at 88.3% of par as of September 30, 2013)

Equity co-investment opportunities ($155 million at fair value) can lead to further NAV appreciation

CONTINUED MIGRATION INTO CORE STRATEGIES

Future core investments are expected to be funded from the monetization of syndicated investments (23% at fair value)

Transition to core strategies expected to allow portfolio yield to grow without need for additional debt or new equity

OPTIMIZE USE OF NON-QUALIFIED ASSETS

19% of FSIC’s investments are classified as non-qualified assets, well below the regulatory limit (30%)

Excess capacity gives flexibility to pursue quality growth investment opportunities across the entire investment universe, not simply those that are qualified BDC assets

1 Adjusted net investment income is the net per share increase (decrease) in net investment income excluding the capital gains incentive fee attributable to unrealized gains. 25

Appendix

MANAGEMENT TEAM BIOGRAPHIES

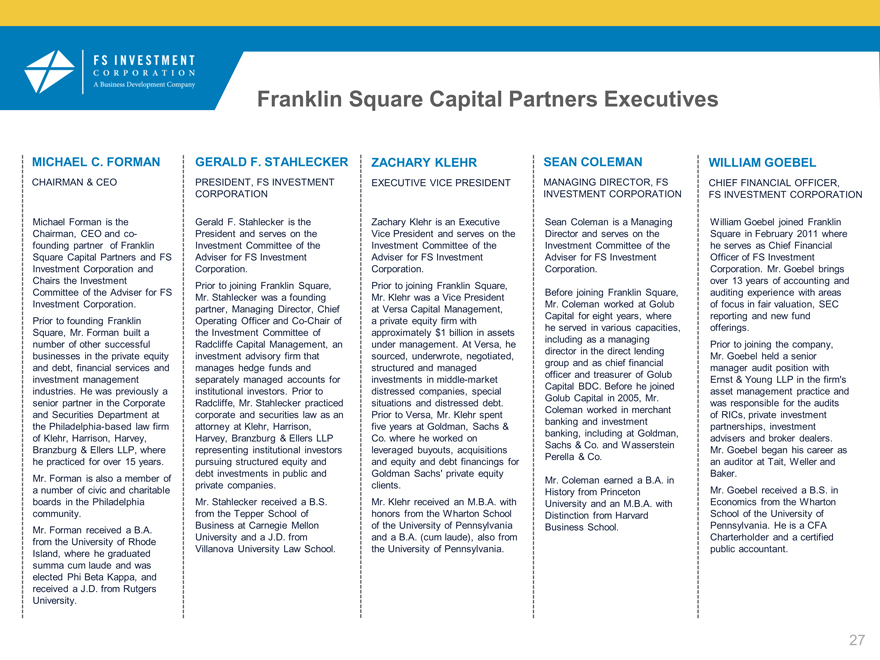

Franklin Square Capital Partners Executives

MICHAEL C. FORMAN

CHAIRMAN & CEO

Michael Forman is the Chairman, CEO and co-founding partner of Franklin Square Capital Partners and FS Investment Corporation and Chairs the Investment Committee of the Adviser for FS Investment Corporation.

Prior to founding Franklin Square, Mr. Forman built a number of other successful businesses in the private equity and debt, financial services and investment management industries. He was previously a senior partner in the Corporate and Securities Department at the Philadelphia-based law firm of Klehr, Harrison, Harvey, Branzburg & Ellers LLP, where he practiced for over 15 years. Mr. Forman is also a member of a number of civic and charitable boards in the Philadelphia community.

Mr. Forman received a B.A. from the University of Rhode Island, where he graduated summa cum laude and was elected Phi Beta Kappa, and received a J.D. from Rutgers University.

GERALD F. STAHLECKER

PRESIDENT, FS INVESTMENT CORPORATION

Gerald F. Stahlecker is the President and serves on the Investment Committee of the Adviser for FS Investment Corporation.

Prior to joining Franklin Square, Mr. Stahlecker was a founding partner, Managing Director, Chief Operating Officer and Co-Chair of the Investment Committee of Radcliffe Capital Management, an investment advisory firm that manages hedge funds and separately managed accounts for institutional investors. Prior to Radcliffe, Mr. Stahlecker practiced corporate and securities law as an attorney at Klehr, Harrison, Harvey, Branzburg & Ellers LLP representing institutional investors pursuing structured equity and debt investments in public and private companies.

Mr. Stahlecker received a B.S. from the Tepper School of Business at Carnegie Mellon University and a J.D. from Villanova University Law School.

ZACHARY KLEHR

EXECUTIVE VICE PRESIDENT

Zachary Klehr is an Executive Vice President and serves on the Investment Committee of the Adviser for FS Investment Corporation.

Prior to joining Franklin Square, Mr. Klehr was a Vice President at Versa Capital Management, a private equity firm with approximately $1 billion in assets under management. At Versa, he sourced, underwrote, negotiated, structured and managed investments in middle-market distressed companies, special situations and distressed debt. Prior to Versa, Mr. Klehr spent five years at Goldman, Sachs & Co. where he worked on leveraged buyouts, acquisitions and equity and debt financings for Goldman Sachs’ private equity clients.

Mr. Klehr received an M.B.A. with honors from the Wharton School of the University of Pennsylvania and a B.A. (cum laude), also from the University of Pennsylvania.

SEAN COLEMAN

MANAGING DIRECTOR, FS INVESTMENT CORPORATION

Sean Coleman is a Managing Director and serves on the Investment Committee of the Adviser for FS Investment Corporation.

Before joining Franklin Square, Mr. Coleman worked at Golub Capital for eight years, where he served in various capacities, including as a managing director in the direct lending group and as chief financial officer and treasurer of Golub Capital BDC. Before he joined Golub Capital in 2005, Mr. Coleman worked in merchant banking and investment banking, including at Goldman, Sachs & Co. and Wasserstein Perella & Co.

Mr. Coleman earned a B.A. in History from Princeton University and an M.B.A. with Distinction from Harvard Business School.

WILLIAM GOEBEL

CHIEF FINANCIAL OFFICER, FS INVESTMENT CORPORATION

William Goebel joined Franklin Square in February 2011 where he serves as Chief Financial Officer of FS Investment Corporation. Mr. Goebel brings over 13 years of accounting and auditing experience with areas of focus in fair valuation, SEC reporting and new fund offerings.

Prior to joining the company, Mr. Goebel held a senior manager audit position with Ernst & Young LLP in the firm’s asset management practice and was responsible for the audits of RICs, private investment partnerships, investment advisers and broker dealers. Mr. Goebel began his career as an auditor at Tait, Weller and Baker.

Mr. Goebel received a B.S. in Economics from the Wharton School of the University of Pennsylvania. He is a CFA Charterholder and a certified public accountant.

27

BENNETT J. GOODMAN

SENIOR MANAGING DIRECTOR AND CO-FOUNDER, GSO / BLACKSTONE

Bennett Goodman is a Senior Managing Director of The Blackstone Group, and current member of the Blackstone Management Committee.

Before co-founding GSO Capital Partners in 2005, Mr. Goodman was a Founder and Managing Partner of the Alternative Capital Division of Credit Suisse (CSFB) where he was responsible for overseeing $33 billion of assets under management in private equity and credit oriented strategies. He joined CSFB in November 2000 when CSFB acquired DLJ, where he joined in 1988 as the founder of the High Yield Capital Markets Group and Served as Global Head of Leveraged Finance.

Mr. Goodman graduated from Lafayette College and the Harvard

Business School.

GSO Capital Partners Executives Focused on FSIC

DOUGLAS I. OSTROVER

SENIOR MANAGING DIRECTOR AND CO-FOUNDER, GSO / BLACKSTONE

Before co-founding GSO Capital Partners in 2005, Mr. Ostrover was a Managing Director and Chairman of the Leveraged Finance Group of CSFB where he was responsible for all of CSFB’s origination, distribution and trading activities relating to high yield securities, leveraged loans, high yield credit derivatives and distressed securities. Mr. Ostrover joined CSFB in November 2000 when CSFB acquired DLJ, where he was a Managing Director in charge of High Yield and Distressed Sales, Trading and Research.

Mr. Ostrover received a B.A. in Economics from the University of Pennsylvania and an M.B.A. from the Stern School of Business of New York University.

TRIPP SMITH

SENIOR MANAGING DIRECTOR AND CO-FOUNDER, GSO / BLACKSTONE

Before co-founding GSO Capital Partners in 2005, Mr. Smith was Global Head of the Capital Markets Group within the Alternative Capital Division of CSFB. Mr. Smith joined CSFB in November 2000 when it acquired DLJ, where he was Global Head of High Yield Capital Markets. Mr. Smith had been a member of DLJ’s high yield team since he joined the firm in 1993. Prior to that, Mr. Smith worked for Smith Barney and Drexel Burnham Lambert.

Mr. Smith received a B.B.A. in Accounting from the University of Notre Dame.

DANIEL H. SMITH

SENIOR MANAGING DIRECTOR, GSO / BLACKSTONE

Mr. Smith is the Group Head of GSO / Blackstone Debt Funds Management and is a member of its Investment Committee.

Before joining GSO Capital in 2005, Mr. Smith was Managing Partner and

Co-head of RBC Capital Market’s

Alternative Investments Unit at Royal Bank of Canada in New York. Mr. Smith joined RBC in 2001 from Indosuez Capital, a division of Crédit Agricole Indosuez, where he was a Co-Head and Managing Director overseeing the firm’s debt investments business and merchant banking activities. He began his career in investment management in 1987 at Van Kampen American Capital where he focused on below investment grade corporate debt.

Mr. Smith received a B.S. in Petroleum Engineering from the University of Southern California and a Masters in Management from the J.L. Kellogg Graduate School of Management at Northwestern University.

BRAD MARSHALL

MANAGING DIRECTOR AND PORTFOLIO MANAGER FOR FS INVESTMENT CORPORATION

Mr. Marshall serves as a Senior Portfolio Manager for FS Investment Corporation and is a member of GSO / Blackstone Debt

Funds Management’s Investment

Committee.

Before joining GSO Capital Partners in 2005, Mr. Marshall worked in various roles at RBC

Capital Market’s Alternative

Investments Unit at Royal Bank of Canada, including fixed income high yield research and business development within RBC’s private equity funds effort. Prior to RBC, Mr. Marshall helped develop a private equity funds business for TAL Global, a Canadian asset management division of CIBC, and prior to that, he co-founded a microchip verification software company where he served as chief financial officer.

Mr. Marshall received an M.B.A. from McGill University in Montreal and a B.A. with honors in Economics from Queen’s University in Kingston, Canada.

28