UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22208

Valued Advisers Trust

(Exact name of registrant as specified in charter)

| Ultimus Asset Services, LLC 225 Pictoria Drive, Suite 450 | Cincinnati, OH 45246 | |

| (Address of principal executive offices) | (Zip code) |

Capitol Services, Inc.

615 S. Dupont Hwy.

Dover, DE 19901

(Name and address of agent for service)

With a copy to:

John H. Lively, Esq.

The Law Offices of John H. Lively & Associates, Inc.

A member firm of The 1940 Act Law GroupTM

11300 Tomahawk Creek Parkway,

Suite 310

Leawood, KS 66221

Registrant’s telephone number, including area code: 513-587-3400

Date of fiscal year end: 5/31

Date of reporting period: 11/30/16

Item 1. Reports to Stockholders.

SEMI-ANNUAL

REPORT

November 30, 2016

BFS Equity Fund

BFS Equity Fund

Letter to Shareholders

Dear Fellow Shareholders,

Greetings in the New Year! This report covers the six-month period June 1, 2016 through November 30, 2016.

At the beginning of its fiscal year, the BFS Equity Fund (the “Fund”) had net assets of $23.9 million. During the course of the last six months, the net assets of the Fund increased 3.3% to $24.7 million as of November 30, 2016. This growth was driven by both inflows from investors into the Fund as well as by the modest positive investment returns achieved by the Fund over the last six months. As of November 30, 2016, there were approximately 544 investors in the Fund.

This report includes a commentary from the Lead Portfolio Manager, Tim Foster, and Co-Portfolio Managers, Tom Sargent and Keith LaRose. You will also find a listing of the portfolio holdings as of November 30, 2016, as well as financial statements and detailed information about the performance and positioning of the Fund.

The S&P 500® Index (“S&P 500”) hit what was at the time an all-time high at 2,193.42 on August 23, 2016, but as the presidential race tightened amidst charges and counter-charges between the contenders, the S&P 500 sold off around 3% by the close of trading on November 7, 2016, the night before the election. As the returns came in and it began to look like Trump might win, the Dow Jones Industrial Average futures plunged over 800 points. Yet, when the stock market opened the next morning, the S&P 500 showed little change and then began to rise, confounding the predictions of many investors. Like most, we were surprised, believing that Trump’s unconventional behavior and threats on trade would cause many investors to sell. Instead, investors focused on the pro-business aspects of Trump’s platform including the possibility of tax reform, repatriation of billions of dollars of offshore funds by U.S. multi-nationals, and less regulation. As a result, a large, short-term gulf in performance swiftly opened between more stable businesses and more cyclical businesses, with value stocks outperforming growth stocks post-election. Between Election Day and November 30, 2016, the S&P 500 rose 2.95% bringing its total return for the six-month period to 6.01%. With strong weightings in industrials, financials, and value stocks, the Dow Jones Industrial Average ended the six-month period with an even better total return of 8.89%. The Fund achieved a positive total return of 2.94% for the six-month period ended November 30, 2016.

1

Since the market’s close on Election Day, November 8, 2016, the S&P 500 has continued its upward trend. Investors are enthusiastic about President Trump’s plans to accelerate economic growth and create new jobs. Much of what we know of President Trump’s policies emanate from his ad hoc tweets on Twitter and, thus, it is difficult to state with any certainty his economic priorities but they appear to be the following:

| • | Reform the tax code, including significantly decreasing individual and corporate tax rates |

| • | Enact policies which will encourage U.S. multi-nationals to repatriate hundreds of billions of U.S. dollars now in overseas banks |

| • | Plan and execute significant U.S. infrastructure spending |

| • | Cut regulation, including repealing many aspects of the Dodd-Frank Act |

| • | Repeal the Affordable Care Act, replacing it with a less costly, more efficient health care system |

| • | Renegotiate the North American Free Trade Agreement and halt Chinese infractions of World Trade Organization rules |

| • | Create millions of new manufacturing jobs, especially in the Rust Belt |

This program represents an ambitious effort to increase economic growth. It is likely that President Trump will succeed in his efforts on the tax front, as Republicans hold both houses of Congress. It is also probable that the Trump administration will be able to roll back some regulations, which are perceived to hinder economic growth – especially in the banking and finance sector. However, in the areas of immigration and health care, change will be more difficult, as the nation continues to be evenly divided at the ballot box. The parts of President Trump’s program which deal with trade and bringing manufacturing jobs back to the U.S. are problematic and even potentially quite harmful. Damaging trade wars could result, leading to a serious recession and the loss of millions of jobs.

At the moment, a recession does not appear likely in 2017. During the third quarter of 2016, GDP growth bounced back to 3.5%. In 2016, 2.2 million jobs were created – while down from 2.7 million jobs created in 2015, it is still a positive sign. The consumer sector of the U.S economy, which accounts for more than 70% of GDP, appears to be in good shape. While the market is no longer inexpensive, it is not as overvalued as some might argue. We remain cautiously optimistic that there is a reasonable chance that the bull market can continue another year.

2

In closing, it is important to reiterate our belief that our investment strategy of investing in quality growth stocks purchased with a risk-mitigating approach and positioned to provide a margin of safety in the case of economic or market weakness is effective over the longer term. Of the 36 companies which the Fund owned as of November 30, 2016, 28 pay dividends, and several are so-called “dividend aristocrats” – companies which have increased their dividend payouts annually for the past 25 years. We believe the Fund’s ownership of shares in quality companies with strong brands, good balance sheets, professional management, and robust cash flow should be able to withstand market corrections, even bear markets, and perform well over the longer term.

The Portfolio Managers of the Fund and I are shareholders together with you. We thank you for the trust that you have placed in us to manage your assets.

Sincerely,

Stephen L. Willcox

President

Bradley, Foster & Sargent, Inc.

3

BFS Equity Fund

Portfolio Managers’ Letter

TO OUR SHAREHOLDERS

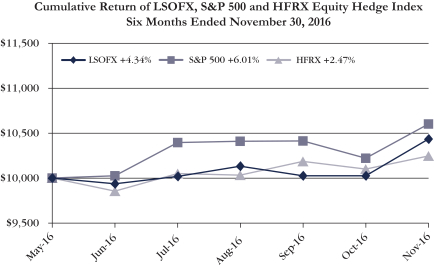

November 30, 2016 marks the third anniversary for the Fund. During this three year period, the Fund’s net asset value has increased from $10.00 to $11.89. For the six month period from June 1, 2016 to November 30, 2016, the Fund produced a total return of 2.94%. The S&P 500 produced a total return of 6.01% during this same period.

The Fund commenced operations in the mid to late stage of the recovery from the 2008 Financial Crisis. Understanding the market rally was well underway for this economic recovery cycle, the management team chose to ease the Fund into the market action by avoiding large sector or single stock bets and to build a portfolio we believe can perform solidly under all economic and market scenarios. Employing this initially conservative approach has resulted in less than benchmark performance during this three year period of rising stock prices. While we cannot forecast how the strategy will play out during market declines, preparing and positioning for those periods by staying disciplined about valuations is certainly part of our thinking.

While lagging the S&P 500 benchmark for the six month period, we continued to narrow down our portfolio of stocks to 36 with a focus on what we believe to be the best candidates for long term growth under both productive and adverse economic conditions. A portfolio of 36 names is more narrowly focused than many mutual funds, yet the diversity of the portfolio extends into all of the market sectors we see as currently attractive. The importance of maintaining a focus on a relatively short list of holdings is to ensure we understand each of the companies we own and how those business models and stock valuations are sustainable under multiple economic and market conditions. The Fund is widely held among the principals and families of Bradley, Foster & Sargent. Our interests are aligned with yours to see the Fund prosper on both an absolute and relative basis. For now, we are pleased to see our NAV rising and we look forward to seeing what we believe to be a portfolio of above average participants in the S&P 500 outperforming the rest of the pack over time.

Subsequent to our third year anniversary, the Morningstar mutual fund rating service initiated coverage of the Fund.

MARKET COMMENTARY

This six month period can be uniquely divided into five months of pre-election and one month of post-election profiles. Uncertainty abounded in the pre-election period notwithstanding the rising probability for a continuation of a Democratic presidency,

4

with one set of likely winners and another set of losers among the market sectors. By the evening of the election with the surprising, if not shocking, Trump victory, those market participants still in the game from both sides of the political aisle likely fell off their chairs over in an effort to pull their cards from the table and to reassess what might happen next under an unorthodox populist agenda. As the dark horse candidate nosed ahead towards the finish line, futures plummeted by 800 points on the Dow Jones Industrial Index (“Dow”) and it looked to be a coming rout at the post-election day market opening bell. Remarkably, by the time the opening bell did sound at 9:30 a.m. post-election day, the decline in the futures evaporated and the market opened flat. Within two trading days, the Dow was off to a subsequent 2000 point rally. Within the indices, many of the pre-election winners became losers and many of the laggards raced to new highs. Specifically, Industrials and Financials became the new market darlings, while Healthcare, Consumer Staples and interest rate sensitive Utilities and Real Estate Investment Trusts (“REITs”) lost nearly all of their pre-election gains. The ten year U.S. Treasury leaped from approximately 1.5% to 2.5% and the bond market suffered sharp losses. The 35 year bull market for bonds is now likely history, in our opinion. The Goldman Sachs commodity index surged, with the index up for the 2016 year to date, as of late December, by 25%. Oil prices have doubled since their February 2016 lows. Natural gas is up 50% year to date. Industrial commodities rallied with copper up 22%. Gold, a victim of post-election U.S. dollar strength, rolled over with a 20+% decline. Post-election 2016 held enough surprises to upend almost every investors’ apple cart!

INVESTMENT STRATEGY

Despite the market’s recent confidence that new policy initiatives will drive GDP growth above the lethargic 2% pace of the past couple of years, we believe that the reality is that it may take more time and encounter more bumps in the road than the current consensus views. The Fed has clearly interpreted the dramatic improvement in labor markets as compelling evidence to moderate extremely accommodative monetary policy. The Fed notched up the Federal Funds rate by 25 basis points for the second time this cycle in December 2016. There is no escaping rising rates driving down bond prices, but rising rates present a headwind for equities as well. Higher rates correlate with lower equity multiples, providing a headwind for equities. Fundamentally, it will be earnings growth that drives stock prices higher from here. Lower corporate tax rates may help, but a stronger U.S. dollar may provide a counterpunch to that beneficial effect. Barring any changes to the tax code for now, we believe overall corporate profits may advance mid-single digits in 2017. Sectors with significant changes in underlying pricing like banking, energy and many basic materials may see double digit earnings growth. Many consumer

5

packaged goods companies may only see low single digit growth, especially considering the stronger U.S. dollar.

We like companies that offer unique products and/or services. We have added two new names in the big data arena. The marketing data these companies provide, like Nielsen in the consumer goods and media industries, as well as Quintiles in the pharmaceuticals arena, is essential for producer companies to define, market, monitor and defend their products in global commerce. We continue with our allocations to double digit growth prospects, like Alphabet, Amazon, Facebook and Under Armour. In the cyclical growth category, we like Caterpillar, Deere, Delta and Mosaic. Beneficiaries of recent positive events include Chubb, given the synergy opportunities of the merger of the former Ace and Chubb insurance companies. We also like Mondelez’s opportunities to expand operating margins in the new efficiency frontier pioneered by private equity group 3G’s purchase of Heinz and Kraft. Among our best-of-breed holdings are Exxon, Schlumberger, Disney, Starbucks, J.P. Morgan, Microsoft and Zoetis. Core holdings that we like that operate in the relentless pursuit of lean manufacturing include Danaher, Fortive and United Technologies.

INVESTMENT COMMENTARY

As of the third quarter of 2016, S&P 500 profits showed positive year over year comparisons for the first time in five quarters. The sharp recovery in oil prices certainly aided the profitability of the Energy sector. The pre-election stabilization of the U.S. dollar helped reduce currency headwinds for U.S. exporters. With commodity prices up sharply, coupled with cycle low unemployment (sub 5%) and accelerating average hourly earnings, we believe the bottom in inflation is now probably behind us. Enhanced pricing power enabled by modestly accelerating inflation, as well as the potential for lower corporate taxes promised by the new administration, should drive continued positive earnings comparisons in both 2017 and 2018. The companies that can exploit these factors to accelerate their earnings growth will likely be the stock market winners, and our primary focus, going forward.

Industrials

Industrials were our largest absolute weighting at 20.0% in the Fund, almost double the 10.5% weighting for the S&P 500. Although the Fund’s Industrial sector’s return for the six month period lagged the S&P 500 Industrial sector modestly at +9.6% versus +12.2%, the sector was a very positive contributor to total return. Deere was our best performing industrial at +27.8%, followed closely by Raytheon at +16.6% and Caterpillar at +16.5%. Nielsen, which had been among our best performing industrials, reported a surprisingly

6

soft third quarter and the stock’s return was down -18.2% for the six month period. We believe Nielsen has a virtually impenetrable moat in its marketing data for media and consumer packaged goods companies. The generous 2.9% dividend provides an attractive incentive to remain a loyal shareholder while discretionary spending picks up with the economy.

Technology

Technology was our second heaviest weighted sector at 18.6%, slightly lower than the S&P 500 Technology sector at 20.8%. Our Tech selections returned +4.3% over the past six months versus the S&P 500 Technology sector return of +9.4%. Amphenol, Apple and Microsoft provided solid returns of +16.8%, +11.9% and +15.2%, respectively. Cognizant at -17.8% and MasterCard at -2.4% had the largest negative returns. We maintain our holdings in still rapidly growing Alphabet (the Fund’s largest holding at 3.8% of the portfolio), Adobe and Facebook which provided returns of +3.6%, +3.4%, and -0.3% respectively. While their performances were modest during the six month period, their long term growth prospects remain robust.

Healthcare

We overweighted Healthcare in the Fund at 16.2% versus 13.7% for the S&P 500. Healthcare became a political football during the election process and the market behaved as if the sector would make no money for any investors. The Fund’s Healthcare sector performance of -0.1% was better than the S&P 500 decline of -2.8%. Danaher, IMS, Merck and Zoetis all provided solid mid-single digit returns, while Abbot Laboratories, Quintiles, Novartis and Thermo Fisher balanced the gains with offsetting declines. Given the current discounted valuations and continued growth prospects for both pharmaceutical and biotech stocks, we believe the sector will again return to above average market performance. We also like the non-pharma exposure to healthcare including Thermo Fisher’s dominance of life science equipment distribution, the diagnostic and medical device profiles of Abbott and Johnson & Johnson, and the dominant position in the animal health sector of Zoetis.

Consumer Discretionary

Also overweighted versus the S&P 500 was the Consumer Discretionary sector at 15.6% versus 12.3% for the S&P 500. We ran into a number of headwinds in our Consumer Discretionary holdings and our performance in the sector at -4.2% lagged the S&P 500 Consumer Discretionary sector, which returned +4.0%. Consumer Discretionary names proved vexing this period. The economy was sluggish, but improving in the later months. If some of the tax reduction proposals of the new administration are enacted, we believe

7

consumers will have more disposable income in their pockets and discretionary spending will improve. We eked out small gains with Starbucks at +6.5% and Amazon at +3.8%. We suffered our worst loss with Under Armour at -18.4%. Under Armour is worth noting because the company continues on a 20+% growth course. We continue to accumulate the stock. Uncertainty about trade policies on foreign made goods hurt Under Armour and created negative returns for Nike (-8.8%) as well. We think both companies offer extraordinary global consumer franchises and will continue to thrive in almost any economic scenario. Disney is one of our largest positions in the Fund at 3.2% of the portfolio; however, it provided almost no return this period at +0.6%, but the Disney media franchise is one of the world’s strongest and we believe Disney will continue to garner a healthy share of global consumer spending.

Financials

Financials were the fifth largest sector weighting in the Fund at 12.8%, somewhat lower than the 14.6% weighting for the S&P 500. As bank stocks rocketed in the aftermath of the election, our underweighting and lagging performance of +9.4 versus the S&P 500 of +18.0% was one of the primary contributing factors to the Fund’s overall performance lagging the S&P 500 benchmark. J.P. Morgan drove our performance in the sector at +24.7%, followed by US Bancorp at +16.8% and American Express at +10.6%. Our biggest regret is not owning more of all three! Wells Fargo hurt our returns at -11.8%. The cross selling and consumer fraud discoveries at the company at least temporarily clocked the stock. While generally trying to avoid reactive selling to negative news, we had purchased Wells Fargo because of our confidence in management. These damaging management discoveries negated our investment thesis. When an investment thesis is negated, we sell the stock regardless of gain or loss. We sold our entire Wells Fargo position in August. A new addition to the Financial sector is Chubb. While the stock only produced a modest +2.2% gain in the period, we have high hopes that the Ace management team will bring new efficiencies and synergies to the Chubb franchise. Chubb is now the second largest holding in the Fund at 3.6% of the portfolio.

Energy

During a year in which oil prices ranged between $27 and $57 per barrel, the Energy sector proved volatile, but contributed positive returns as oil prices generally drifted higher as the year progressed. The Fund was somewhat underweighted at 6.6% versus the S&P 500 at 7.5%. The Fund’s return at +8.2% lagged the S&P 500 return of +11.2%. We are not surprised that our performance trailed the index during the period. For most of the period, we owned only two energy stocks: Exxon, which returned +0.2%, and

8

Schlumberger, which returned +10.9%. We view both as best in class and consider them to be core holdings in the Energy sector, regardless of interim performance variances versus the benchmarks. Spectra Energy was our best performer at +13.4%, but after its takeover by Enbridge Energy, we saw little upside in the stock and sold the position in August.

Consumer Staples

Consumer Staples was a leading sector early in the year, but lost significant ground to the market post-election. Given still high relative values, we underweighted the sector at 4.4% versus the S&P 500 weighting of 9.3%. Returns were negative for the Fund at -5.8% and for the S&P 500, as well, at -2.8%. Pepsi was our best performer with a nominal return of only +1.1%. Mondelez was the worst at -6.5%. Interestingly, there had been shareholder activism to combine the two companies. While we see that as unlikely, we believe Mondelez has lagged the margin improvement evident in names like Kraft Heinz and we see Mondelez either driving itself in the enhanced margin direction or being driven by outside influences, such as activist shareholders, to improve margins.

Materials, Telecommunication Services, Utilities and REITs

The Fund had only a single holding across all of these sectors. Mosaic, a fertilizer manufacturer, drove performance of +7.4% for our Materials sector exposure. The S&P 500 Materials sector returned about the same at +7.5%. The managers of the Fund are of a mind that interest rates hit bottom in 2016 and will likely continue to rise in the coming years. The interest rate sensitivity of REITs, Utilities and Telecom, given their high dividend yields, was reason enough for the Fund to avoid exposure to any of these sectors. That strategy worked well as the S&P 500 REITs, Utilities and Telecoms returned -6.1%, -3.2%, and 0.0%, respectively.

CLOSING COMMENTS

While the market continues to sell at a not unreasonable multiple relative to history and to prevailing interest rates, the post-Trump rally may have gotten a little ahead of itself. Proposals for economic stimulus, from tax cuts to massive fiscal spending projects, may or may not actually happen, may or may not actually work, and, in any event, will likely take more time than the recent rally in stock prices may suggest. There has been little reason to sell and realize potentially taxable gains late in the year. There may be more reason to do so in the new year. We do not attempt to time the market by raising large amounts of cash, but we do like to take a conservative stance in our stock selections. The market flip flopped from a preference for growth pre-election to a strong preference for value post-election. We own what we believe to be high quality companies in both

9

categories. We believe that the longer term focus we employ will enable us to find exceptional current value within both profiles and that the market should eventually come to appreciate the improved earnings we now foresee down the road as they materialize.

We, at Bradley, Foster & Sargent, Inc., look forward to serving you through our management of the BFS Equity Fund. Thank you for placing your capital under our care.

| Timothy Foster | Keith LaRose | Thomas Sargent | ||

| Lead Portfolio Manager | Co-Portfolio Manager | Co-Portfolio Manager |

10

BFS Equity Fund

SEMI-ANNUAL PERFORMANCE REVIEW

(UNAUDITED)

The Fund performed behind the S&P 500 and the Dow Jones Industrial Average for the six month period ended November 30, 2016, returning +2.94% versus +6.01% for the S&P 500 and +8.98% for the Dow Jones Industrial Average.

Key Detractors from Relative Results

| • | Sector weightings were a contributing factor to the Fund’s underperformance vs. the S&P 500 and the Dow Jones Industrial Average. Our over weighting in the underperforming Healthcare sector (16.2% vs. 13.7% for the S&P 500), as well our underweighting in the better performing Financial sector (12.8% vs. 14.6% for the S&P 500) and Energy sector (6.6% vs. 7.5% for the S&P 500) proved to be an anchor for the Fund in measuring up to the benchmark indices. |

| • | Adverse stock selection, particularly in the Financial and Technology sectors, also detracted from performance. Larger positions, such as Alphabet with a return of +3.6%, trailed the Tech sector returns. Another favorite long term growth name, Disney at a return of -0.6%, also provided sub-benchmark returns. Our purchase of Under Armour was ill timed, as this stock suffered a -18.4% pullback since our purchase. We continue to hold all three names and expect improved performance from them in subsequent periods. |

Key Contributors to Relative Results

| • | Two stocks provided well above benchmark returns: Deere at +27.8% and J.P. Morgan +24.7%. |

| • | The Fund’s large overweighting in Industrials (20.0% vs. 10.5% for the S&P 500) helped by providing a +9.6% return. |

| • | Avoiding the REIT, Utility and Telecom sectors proved beneficial to the Fund’s performance as these three sectors provided virtually no net gains to the S&P 500 performance for the period. |

November 30, 2016

FUND INFORMATION

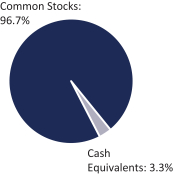

ASSET ALLOCATION

(as a percentage of total investments)

TEN LARGEST HOLDINGS (%) | FUND | |||

Alphabet, Inc. — Class A | 3.8 | |||

Chubb Ltd. | 3.6 | |||

Exxon Mobil Corp. | 3.5 | |||

Facebook, Inc. | 3.4 | |||

Apple, Inc. | 3.4 | |||

Amazon.com, Inc. | 3.4 | |||

JPMorgan Chase & Co. | 3.3 | |||

Walt Disney Co./The | 3.2 | |||

Schlumberger Ltd. | 3.1 | |||

U.S. Bancorp | 3.0 | |||

SECTOR DIVERSIFICATION (%) | FUND | S&P 500 | ||||||

Industrial | 20.0 | 10.5 | ||||||

Information Technology | 18.6 | 20.8 | ||||||

Healthcare | 16.2 | 13.7 | ||||||

Consumer Discretionary | 15.6 | 12.3 | ||||||

Financials | 12.8 | 14.6 | ||||||

Energy | 6.6 | 7.5 | ||||||

Consumer Staples | 4.4 | 9.3 | ||||||

Cash Equivalents | 3.3 | 0.0 | ||||||

Materials | 2.5 | 2.9 | ||||||

Telecommunication Services | 0.0 | 2.5 | ||||||

Utilities | 0.0 | 3.1 | ||||||

REITs | 0.0 | 2.8 | ||||||

11

BFS Equity Fund

Investment Results (Unaudited)

Average Annual Total Returns(a) (For the periods ended November 30, 2016)

| Six Months | One Year | Since Inception (November 8, 2013) | ||||||||||

BFS Equity Fund | 2.94% | 1.49% | 6.04% | |||||||||

S&P 500® Index(b) | 6.01% | 8.06% | 9.64% | |||||||||

Dow Jones Industrial Average®(c) | 8.98% | 10.91% | 9.25% | |||||||||

Total annual fund operating expenses, as disclosed in the BFS Equity Fund’s (the “Fund”) prospectus dated September 28, 2016, were 1.86% of average daily net assets (1.25% after fee waivers/expense reimbursements by Bradley, Foster & Sargent, Inc. (the “Adviser”)). The Adviser has contractually agreed to waive or limit its fees and assume other expenses of the Fund until September 30, 2017, so that total annual fund operating expenses does not exceed 1.00%. This contractual arrangement may only be terminated by mutual consent of the Adviser and the Board of Trustees of the Trust, and it will automatically terminate upon the termination of the investment advisory agreement between the Fund and the Adviser. This operating expense limitation does not apply to: (i) interest, (ii) taxes, (iii) brokerage commissions, (iv) other expenditures which are capitalized in accordance with generally accepted accounting principles, (v) other extraordinary expenses not incurred in the ordinary course of the Fund’s business, (vi) dividend expense on short sales, (vii) expenses incurred under a plan of distribution under Rule 12b-1, and (viii) expenses that the Fund has incurred but did not actually pay because of an expense offset arrangement, if applicable, in any fiscal year. The operating expense limitation also excludes any “Fees and Expenses of Acquired Funds,” which are the expenses indirectly incurred by the Fund as a result of investing in money market funds or other investment companies, including ETFs, that have their own expenses. Each waiver or reimbursement of an expense by the Advisor is subject to repayment by the Fund within the three fiscal years following the fiscal year in which the expense was incurred, provided that the Fund is able to make the repayment without exceeding the expense limitation in place at the time of the waiver or reimbursement.

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption Fund shares. The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. Current performance of a Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (855) 575-2430.

| (a) | Average annual total returns reflect any change in price per share and assume the reinvestment of all distributions. The Fund’s returns reflect any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would have been lower. Total returns for periods less than one year are not annualized. |

| (b) | The S&P 500® Index (“S&P 500”) is a widely recognized unmanaged index of equity prices and is representative of a broader market and range of securities than is found in the Fund’s portfolio. The index is an unmanaged benchmark that assumes reinvestment of all distributions and excludes the effect of taxes and fees. Individuals cannot invest directly in this index; however, an individual can invest in exchange traded funds or other investment vehicles that attempt to track the performance of a benchmark index. |

| (c) | The Dow Jones Industrial Average® is a widely recognized unmanaged index of equity prices and is representative of a narrower market and range of securities than is found in the Fund’s portfolio. The index is an unmanaged benchmark that assumes reinvestment of all distributions and excludes the effect of taxes and fees. Individuals cannot invest directly in this index; however, an individual can invest in exchange traded funds or other investment vehicles that attempt to track the performance of a benchmark index. |

The Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Fund and may be obtained by calling the same number as above. Please read it carefully before investing.

The Fund is distributed by Unified Financial Securities, LLC, member FINRA/SIPC.

12

Availability of Portfolio Schedule (Unaudited)

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (“SEC”) as of the end of the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q will be available at the SEC’s website at www.sec.gov. The Fund’s Form N-Q may be reviewed and copied at the Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330.

13

BFS Equity Fund

Schedule of Investments (Unaudited)

November 30, 2016

| Shares | Fair Value | |||||||

| COMMON STOCKS — 96.55% | ||||||||

| Aerospace & Defense — 5.26% | ||||||||

| 4,000 | Raytheon Co. | $ | 598,160 | |||||

| 6,500 | United Technologies Corp. | 700,180 | ||||||

|

| |||||||

| 1,298,340 | ||||||||

|

| |||||||

| Airlines — 2.73% | ||||||||

| 14,000 | Delta Air Lines, Inc. | 674,520 | ||||||

|

| |||||||

| Banks — 3.01% | ||||||||

| 15,000 | U.S. Bancorp | 744,300 | ||||||

|

| |||||||

| Beverages — 2.03% | ||||||||

| 5,000 | PepsiCo, Inc. | 500,500 | ||||||

|

| |||||||

| Biotechnology — 1.79% | ||||||||

| 1,500 | Biogen, Inc. * | 441,105 | ||||||

|

| |||||||

| Chemicals — 2.53% | ||||||||

| 22,000 | Mosaic Co./The | 624,800 | ||||||

|

| |||||||

| Computers & Peripherals — 3.36% | ||||||||

| 7,500 | Apple, Inc. | 828,900 | ||||||

|

| |||||||

| Consumer Finance — 2.92% | ||||||||

| 10,000 | American Express Co. | 720,400 | ||||||

|

| |||||||

| Diversified Financial Services — 3.25% | ||||||||

| 10,000 | JPMorgan Chase & Co. | 801,700 | ||||||

|

| |||||||

| Electronic Equipment, Instruments & Components — 2.49% | ||||||||

| 9,000 | Amphenol Corp. — Class A | 614,340 | ||||||

|

| |||||||

| Energy Equipment & Services — 3.06% | ||||||||

| 9,000 | Schlumberger Ltd. | 756,450 | ||||||

|

| |||||||

| Food Products — 2.34% | ||||||||

| 14,000 | Mondelez International, Inc. — Class A | 577,360 | ||||||

|

| |||||||

| Health Care Equipment & Supplies — 2.31% | ||||||||

| 15,000 | Abbott Laboratories | 571,050 | ||||||

|

| |||||||

| Hotels, Restaurants & Leisure — 2.11% | ||||||||

| 9,000 | Starbucks Corp. | 521,730 | ||||||

|

| |||||||

| Industrial Conglomerates — 5.27% | ||||||||

| 8,000 | Danaher Corp. | 625,360 | ||||||

| 22,000 | General Electric Co. | 676,720 | ||||||

|

| |||||||

| 1,302,080 | ||||||||

|

| |||||||

| Insurance — 3.63% | ||||||||

| 7,000 | Chubb Ltd. | 896,000 | ||||||

|

| |||||||

| Internet & Catalog Retail — 3.34% | ||||||||

| 1,100 | Amazon.com, Inc. * | 825,627 | ||||||

|

| |||||||

See accompanying notes which are an integral part of the financial statements.

14

BFS Equity Fund

Schedule of Investments (Unaudited) (continued)

November 30, 2016

| Shares | Fair Value | |||||||

| COMMON STOCKS — (continued) | ||||||||

| Internet Software & Services — 7.13% | ||||||||

| 1,200 | Alphabet, Inc. — Class A * | $ | 931,056 | |||||

| 7,000 | Facebook, Inc. — Class A * | 828,940 | ||||||

|

| |||||||

| 1,759,996 | ||||||||

|

| |||||||

| Life Sciences Tools & Services — 5.23% | ||||||||

| 7,680 | Quintiles IMS Holdings, Inc. * | 590,054 | ||||||

| 5,000 | Thermo Fisher Scientific, Inc. | 700,550 | ||||||

|

| |||||||

| 1,290,604 | ||||||||

|

| |||||||

| Machinery — 6.63% | ||||||||

| 5,000 | Caterpillar, Inc. | 477,800 | ||||||

| 5,000 | Deere & Co. | 501,000 | ||||||

| 12,000 | Fortive Corp. | 659,880 | ||||||

|

| |||||||

| 1,638,680 | ||||||||

|

| |||||||

| Media — 3.21% | ||||||||

| 8,000 | Walt Disney Co./The | 792,960 | ||||||

|

| |||||||

| Oil, Gas & Consumable Fuels — 3.53% | ||||||||

| 10,000 | Exxon Mobil Corp. | 873,000 | ||||||

|

| |||||||

| Pharmaceuticals — 4.25% | ||||||||

| 4,000 | Johnson & Johnson | 445,200 | ||||||

| 12,000 | Zoetis, Inc. | 604,560 | ||||||

|

| |||||||

| 1,049,760 | ||||||||

|

| |||||||

| Professional Services — 2.62% | ||||||||

| 15,000 | Nielsen Holdings PLC | 646,500 | ||||||

|

| |||||||

| Software — 5.63% | ||||||||

| 6,500 | Adobe Systems, Inc. * | 668,265 | ||||||

| 12,000 | Microsoft Corp. | 723,120 | ||||||

|

| |||||||

| 1,391,385 | ||||||||

|

| |||||||

| Specialty Retail — 2.62% | ||||||||

| 5,000 | Home Depot, Inc./The | 647,000 | ||||||

|

| |||||||

| Textiles, Apparel & Luxury Goods — 4.27% | ||||||||

| 10,000 | NIKE, Inc. | 500,700 | ||||||

| 18,000 | Under Armour, Inc. — Class A * | 554,400 | ||||||

|

| |||||||

| 1,055,100 | ||||||||

|

| |||||||

Total Common Stocks (Cost $20,633,157) | 23,844,187 | |||||||

|

| |||||||

See accompanying notes which are an integral part of the financial statements.

15

BFS Equity Fund

Schedule of Investments (Unaudited) (continued)

November 30, 2016

| Shares | Fair Value | |||||||

| MONEY MARKET FUNDS — 3.34% | ||||||||

| 824,650 | Fidelity Investments Government Money Market Portfolio — Institutional Class, 0.32% (a) | $ | 824,650 | |||||

|

| |||||||

Total Money Market Funds (Cost $824,650) | 824,650 | |||||||

|

| |||||||

Total Investments – 99.89% (Cost $21,457,807) | 24,668,837 | |||||||

|

| |||||||

Other Assets in Excess of Liabilities – 0.11% | 26,930 | |||||||

|

| |||||||

NET ASSETS – 100.00% | $ | 24,695,767 | ||||||

|

| |||||||

| (a) | Rate disclosed is the seven day effective yield as of November 30, 2016. |

| * | Non-income producing security. |

The industries shown on the schedule of investments are based on the Global Industry Classification Standard, or GICS® (“GICS”). The GICS was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by Ultimus Asset Services, LLC.

See accompanying notes which are an integral part of the financial statements.

16

BFS Equity Fund

Statement of Assets and Liabilities (Unaudited)

November 30, 2016

Assets | ||||

Investments in securities at fair value (cost $21,457,807) | $ | 24,668,837 | ||

Dividends receivable | 44,801 | |||

Prepaid expenses | 18,449 | |||

Total Assets | 24,732,087 | |||

Liabilities | ||||

Payable to Adviser | 4,775 | |||

Payable to administrator, fund accountant, and transfer agent | 6,863 | |||

Distribution fees accrued | 10,115 | |||

Other accrued expenses | 14,567 | |||

Total Liabilities | 36,320 | |||

Net Assets | $ | 24,695,767 | ||

Net Assets consist of: | ||||

Paid-in capital | $ | 22,085,736 | ||

Accumulated undistributed net investment income | 101,377 | |||

Accumulated undistributed net realized loss from investment transactions | (702,376 | ) | ||

Net unrealized appreciation on investments | 3,211,030 | |||

Net Assets | $ | 24,695,767 | ||

Shares outstanding (unlimited number of shares authorized, no par value) | 2,077,748 | |||

Net asset value, offering and redemption price per share | $ | 11.89 |

17

See accompanying notes which are an integral part of the financial statements.

BFS Equity Fund

Statement of Operations (Unaudited)

For the six months ended November 30, 2016

Investment Income |

| |||

Dividend income | $ | 200,358 | ||

Total investment income | 200,358 | |||

Expenses |

| |||

Investment Adviser | 90,932 | |||

Distribution (12b-1) | 30,311 | |||

Administration | 19,052 | |||

Fund accounting | 12,534 | |||

Registration | 12,361 | |||

Legal | 9,197 | |||

Transfer agent | 9,077 | |||

Audit | 8,022 | |||

Printing | 6,564 | |||

Trustee | 2,568 | |||

Custodian | 2,126 | |||

Miscellaneous | 15,883 | |||

Total expenses | 218,627 | |||

Fees waived by Adviser | (66,626 | ) | ||

Net operating expenses | 152,001 | |||

Net investment income | 48,357 | |||

Net Realized and Change in Unrealized Gain on Investments |

| |||

Net realized gain on investment securities transactions | 110,451 | |||

Net change in unrealized appreciation of investment securities | 538,879 | |||

Net realized and change in unrealized gain on investments | 649,330 | |||

Net increase in net assets resulting from operations | $ | 697,687 | ||

18

See accompanying notes which are an integral part of the financial statements.

BFS Equity Fund

Statements of Changes in Net Assets

| Increase (Decrease) in Net Assets due to: | For the Six Months Ended November 30, 2016 (Unaudited) | For the Year Ended May 31, 2016 | ||||||

Operations | ||||||||

Net investment income | $ | 48,357 | $ | 94,935 | ||||

Net realized gain/(loss) on investment securities transactions | 110,451 | (458,394 | ) | |||||

Net change in unrealized appreciation of investment securities | 538,879 | 217,958 | ||||||

Net increase (decrease) in net assets resulting from operations | 697,687 | (145,501 | ) | |||||

Distributions | ||||||||

From net investment income | — | (69,881 | ) | |||||

Total distributions | — | (69,881 | ) | |||||

Capital Transactions | ||||||||

Proceeds from shares sold | 807,019 | 5,178,205 | ||||||

Reinvestment of distributions | — | 62,385 | ||||||

Amount paid for shares redeemed | (693,086 | ) | (1,308,552 | ) | ||||

Net increase in net assets resulting from capital transactions | 113,933 | 3,932,038 | ||||||

Total Increase in Net Assets | 811,620 | 3,716,656 | ||||||

Net Assets |

| |||||||

Beginning of period | 23,884,147 | 20,167,491 | ||||||

End of period | $ | 24,695,767 | $ | 23,884,147 | ||||

Accumulated undistributed net investment income included in net assets at end of period | $ | 101,377 | $ | 53,020 | ||||

Share Transactions | ||||||||

Shares sold | 69,123 | 455,719 | ||||||

Shares issued in reinvestment of distributions | — | 5,364 | ||||||

Shares redeemed | (59,468 | ) | (118,087 | ) | ||||

Net increase in shares outstanding | 9,655 | 342,996 | ||||||

19

See accompanying notes which are an integral part of the financial statements.

BFS Equity Fund

Financial Highlights

(For a share outstanding during each period)

| For the Six Months Ended November 30, 2016 (Unaudited) | For the Year Ended May 31, 2016 | For the Year Ended May 31, 2015 | For the Period Ended May 31, 2014(a) | |||||||||||||

Selected Per Share Data: | ||||||||||||||||

Net asset value, beginning of period | $11.55 | $11.69 | $10.73 | $10.00 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Income from investment operations: | ||||||||||||||||

Net investment income | 0.02 | 0.04 | 0.02 | 0.04 | ||||||||||||

Net realized and unrealized gain/(loss) on investments | 0.32 | (0.15 | ) | 0.97 | 0.70 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Total from investment operations | 0.34 | (0.11 | ) | 0.99 | 0.74 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Less distributions to shareholders from: | ||||||||||||||||

Net investment income | — | (0.03 | ) | (0.03 | ) | (0.01 | ) | |||||||||

|

|

|

|

|

|

|

| |||||||||

Total distributions | — | (0.03 | ) | (0.03 | ) | (0.01 | ) | |||||||||

|

|

|

|

|

|

|

| |||||||||

Net asset value, end of period | $ 11.89 | $ 11.55 | $ 11.69 | $ 10.73 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total Return(b) | 2.94 | %(c) | (0.91 | )% | 9.27 | % | 7.36 | %(c) | ||||||||

Ratios and Supplemental Data: | ||||||||||||||||

Net assets, end of period (000) | $24,696 | $23,884 | $20,167 | $12,745 | ||||||||||||

Ratio of net expenses to average net assets | 1.25 | %(d) | 1.25 | % | 1.25 | % | 1.25 | %(d) | ||||||||

Ratio of expenses to average net assets before waiver and reimbursement | 1.80 | %(d) | 1.86 | % | 2.26 | % | 3.93 | %(d) | ||||||||

Ratio of net investment income to average net assets | 0.40 | %(d) | 0.43 | % | 0.30 | % | 0.68 | %(d) | ||||||||

Ratio of net investment income/(loss) to average net assets before waiver and reimbursement | (0.15 | )%(d) | (0.18 | )% | (0.71 | )% | (2.00 | )%(d) | ||||||||

Portfolio turnover rate | 27.12 | %(c) | 49.38 | % | 51.17 | % | 46.50 | %(c) | ||||||||

| (a) | For the period November 8, 2013 (commencement of operations) to May 31, 2014. |

| (b) | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of dividends, if any. |

| (c) | Not annualized |

| (d) | Annualized |

20

See accompanying notes which are an integral part of the financial statements.

BFS Equity Fund

Notes to Financial Statements (Unaudited)

November 30, 2016

NOTE 1 – ORGANIZATION

The BFS Equity Fund (the “Fund”) was organized as an open-end diversified series of Valued Advisers Trust (the “Trust”) on July 23, 2013 and commenced operations on November 8, 2013. The Trust is a management investment company established under the laws of Delaware by an Agreement and Declaration of Trust dated June 13, 2008 (the “Trust Agreement”). The Trust Agreement permits the Trustees to issue an unlimited number of shares of beneficial interest of separate series without par value. The Fund is one of a series of funds authorized by the Board of Trustees (the “Board”). The Fund’s investment adviser is Bradley, Foster & Sargent, Inc. (the “Adviser”). The investment objective of the Fund is long-term appreciation through growth of principal and income.

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES

The Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”. The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. These policies are in conformity with generally accepted accounting principles in the United States of America (“GAAP”).

Securities Valuation – All investments in securities are recorded at their estimated fair value as described in Note 3.

Federal Income Taxes – The Fund makes no provision for federal income or excise tax. The Fund has qualified and intends to qualify each year as a regulated investment company (“RIC”) under subchapter M of the Internal Revenue Code of 1986, as amended, by complying with the requirements applicable to RICs and by distributing substantially all of its taxable income. The Fund also intends to distribute sufficient net investment income and net capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains. If the required amount of net investment income or gains is not distributed, the Fund could incur a tax expense.

As of, and during the six months ended November 30, 2016, the Fund did not have a liability for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the statement of operations. During the six months ended November 30, 2016, the Fund did not incur any interest or penalties.

Expenses – Expenses incurred by the Trust that do not relate to a specific fund of the Trust are allocated to the individual funds based on each fund’s relative net assets or another appropriate basis.

Security Transactions and Related Income – The Fund follows industry practice and records security transactions on the trade date for financial reporting purposes. The Fund has chosen specific identification as its tax lot identification method for all securities transactions. Interest income is recorded on an accrual basis and dividend income is recorded on the ex-dividend date except in the case of foreign securities, in which case dividends are generally recorded as soon as such information becomes available. Discounts and premiums on securities purchased are accreted or amortized using the effective interest method. The ability of issuers of debt securities held by the Fund to meet their obligations may be affected by economic and political developments in a

21

BFS Equity Fund

Notes to Financial Statements (Unaudited) (continued)

November 30, 2016

specific country or region. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

Dividends and Distributions – The Fund intends to distribute its net investment income and net realized long-term and short-term capital gains, if any, at least annually. Dividends and distributions to shareholders, which are determined in accordance with income tax regulations, are recorded on the ex-dividend date. The treatment for financial reporting purposes of distributions made to shareholders during the period from net investment income or net realized capital gains may differ from their ultimate treatment for federal income tax purposes. These differences are caused primarily by differences in the timing of the recognition of certain components of income, expense or realized capital gain for federal income tax purposes. Where such differences are permanent in nature, they are reclassified in the components of the net assets based on their ultimate characterization for federal income tax purposes. Any such reclassifications will have no effect on net assets, results of operations or net asset values per share of the Fund.

NOTE 3 – SECURITIES VALUATION AND FAIR VALUE MEASUREMENTS

Fair value is defined as the price that the Fund would receive upon selling an investment in an orderly transaction to an independent buyer in the principal or most advantageous market of the investment. GAAP establishes a three-tier hierarchy to maximize the use of observable market data and minimize the use of unobservable inputs and establish classification of fair value measurements for disclosure purposes.

Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, for example, the risk inherent in a particular valuation technique used to measure fair value including a pricing model and/or the risk inherent in the inputs to the valuation technique. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

| • | Level 1 – unadjusted quoted prices in active markets for identical investments and/or registered investment companies where the value per share is determined and published and is the basis for current transactions for identical assets or liabilities at the valuation date. |

| • | Level 2 – other significant observable inputs (including, but not limited to, quoted prices for an identical security in an inactive market, quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| • | Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining fair value of investments based on the best information available) |

22

BFS Equity Fund

Notes to Financial Statements (Unaudited) (continued)

November 30, 2016

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy which is reported, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

Equity securities that are traded on any stock exchange are generally valued at the last quoted sale price on the security’s primary exchange. Lacking a last sale price, an exchange traded security is generally valued at its last bid price. Securities traded in the NASDAQ over-the-counter market are generally valued at the NASDAQ Official Closing Price. When using the market quotations and when the market is considered active, the security is classified as a Level 1 security. In the event that market quotations are not readily available or are considered unreliable due to market or other events, the Fund values its securities and other assets at fair value in accordance with policies established by and under the general supervision of the Board. Under these policies, the securities will be classified as Level 2 or 3 within the fair value hierarchy, depending on the inputs used.

Investments in mutual funds, including money market mutual funds, are generally priced at the ending net asset value (“NAV”) provided by the pricing agent of the funds. These securities will be categorized as Level 1 securities.

In accordance with the Trust’s valuation policies, the Adviser is required to consider all appropriate factors relevant to the value of securities for which it has determined other pricing sources are not available or reliable as described above. No single standard exists for determining fair value, because fair value depends upon the circumstances of each individual case. As a general principle, the current fair value of an issue of securities being valued by the Adviser would appear to be the amount that the owner might reasonably expect to receive for them upon their current sale. Methods that are in accordance with this principle may, for example, be based on (i) a multiple of earnings; (ii) a discount from market of a similar freely traded security (including a derivative security or a basket of securities traded on other markets, exchanges or among dealers); or (iii) yield to maturity with respect to debt issues, or a combination of these and other methods. Fair-value pricing is permitted if, in the Adviser’s opinion, the validity of market quotations appears to be questionable based on factors such as evidence of a thin market in the security based on a small number of quotations, a significant event occurs after the close of a market but before the Fund’s NAV calculation that may affect a security’s value, or the Adviser is aware of any other data that calls into question the reliability of market quotations.

The following is a summary of the inputs used to value the Fund’s investments as of November 30, 2016:

| Valuation Inputs | ||||||||||||||||

| Assets | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Common Stocks(a) | $ | 23,844,187 | $ | – | $ | – | $ | 23,844,187 | ||||||||

Money Market Funds | 824,650 | – | – | 824,650 | ||||||||||||

Total | $ | 24,668,837 | $ | – | $ | – | $ | 24,668,837 | ||||||||

| (a) | Refer to Schedule of Investments for industry classifications. |

23

BFS Equity Fund

Notes to Financial Statements (Unaudited) (continued)

November 30, 2016

The Fund did not hold any investments during the reporting period for which other significant observable inputs (Level 2) were used in determining fair value. The Fund did not hold any assets during the reporting period for which significant unobservable inputs (Level 3) were used in determining fair value; therefore, no reconciliation of Level 3 securities is included for this reporting period. The Fund did not hold any derivative instruments during the reporting period.

The Trust recognizes transfers between fair value hierarchy levels at the end of the reporting period. There were no transfers between any levels as of November 30, 2016 based on input levels assigned at May 31, 2016.

NOTE 4 – FEES AND OTHER TRANSACTIONS WITH AFFILIATES AND OTHER SERVICE PROVIDERS

Under the terms of the investment advisory agreement on behalf of the Fund (the “Agreement”), the Adviser manages the Fund’s investments subject to oversight of the Board. As compensation for its services, the Fund is obligated to pay the Adviser a fee computed and accrued daily and paid monthly at an annual rate of 0.75% of the average daily net assets of the Fund. For the six months ended November 30, 2016, the Adviser earned a fee of $90,932 from the Fund before the waivers described below. At November 30, 2016, the Fund owed the Adviser $4,775.

The Adviser has contractually agreed to waive or limit its fee and reimburse other expenses of the Fund, until September 30, 2017, so that the ratio of total annual operating expenses does not exceed 1.00%. This operating expense limitation does not apply to interest, taxes, brokerage commissions, other expenditures which are capitalized in accordance with GAAP, other extraordinary expenses not incurred in the ordinary course of the Fund’s business, dividend expense on short sales, expenses incurred under a plan of distribution under Rule 12b-1, and expenses that the Fund has incurred but did not actually pay because of an expense offset arrangement, if applicable, incurred by the Fund in any fiscal year. The operating expense limitation also excludes any “Fees and Expenses of Acquired Funds,” which are the expenses indirectly incurred by the Fund as a result of investing in money market funds or other investment companies, including ETFs, that have their own expenses. The Adviser may be entitled to recoup the sum of all fees previously waived or expenses reimbursed during any of the previous three years, less any recoupment previously paid, provided total expenses do not exceed the limitation set forth above. For the six months ended November 30, 2016, fees and expenses totaling $66,626 were waived or reimbursed by the Adviser. The amounts subject to repayment by the Fund, pursuant to the aforementioned conditions are as follows:

| Recoverable through May 31, | Amount | |||

| 2017 | $146,030 | |||

| 2018 | 163,520 | |||

| 2019 | 135,629 | |||

| 2020 | 66,626 | |||

The Trust retains Ultimus Asset Services, LLC (“Ultimus”) to provide the Fund with administration and compliance, fund accounting, and transfer agent services, including all regulatory reporting.

24

BFS Equity Fund

Notes to Financial Statements (Unaudited) (continued)

November 30, 2016

For the six months ended November 30, 2016, Ultimus earned fees of $19,052 for administration services, $12,534 for fund accounting services and $9,077 for transfer agent services. At October 31, 2016, the Fund owed Ultimus $6,863 for such services.

The officers and one trustee of the Trust are members of management and/or employees of Ultimus. Unified Financial Securities, LLC (the “Distributor”) acts as the principal distributor of the Fund’s shares. Certain officers of the Trust are officers of the Distributor and each such person may be deemed to be an affiliate of the Distributor.

The Fund has adopted a Distribution Plan (the “Plan”) pursuant to Rule 12b-1 under the Investment Company Act of 1940 (the “1940 Act”). The Plan provides that the Fund will pay the Distributor and/or any registered securities dealer, financial institution or any other person (the “Recipient”) a shareholder servicing fee of 0.25% of the average daily net assets of the Fund in connection with the promotion and distribution of the Fund’s shares or the provision of personal services to shareholders, including, but not necessarily limited to, advertising, compensation to underwriters, dealers and selling personnel, the printing and mailing of prospectuses to other than current Fund shareholders, the printing and mailing of sales literature and servicing shareholder accounts (“12b-1 Expenses”). The Fund or Distributor may pay all or a portion of these fees to any recipient who renders assistance in distributing or promoting the sale of shares, or who provides certain shareholder services, pursuant to a written agreement. For the six months ended November 30, 2016, 12b-1 expense incurred by the Fund was $30,311. The Fund owed $10,115 for 12b-1 fees as of November 30, 2016.

NOTE 5 – PURCHASES AND SALES OF SECURITIES

For the six months ended November 30, 2016, purchases and sales of investment securities, other than short-term investments and short-term U.S. government obligations, were as follows:

Purchases | Sales | |||

| $6,492,883 | $ | 6,426,616 | ||

There were no purchases or sales of long-term U.S. government obligations during the six months ended November 30, 2016.

NOTE 6 – ESTIMATES

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

NOTE 7 – BENEFICIAL OWNERSHIP

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of a fund creates a presumption of control of a fund, under Section 2(a) (9) of the 1940 Act. At November 30, 2016, Charles Schwab & Co., Inc. (“Schwab”) owned, as record shareholder, 56% of

25

BFS Equity Fund

Notes to Financial Statements (Unaudited) (continued)

November 30, 2016

the outstanding shares of the Fund. It is not known whether Schwab or any of the underlying beneficial owners owned or controlled more than 25% of the voting securities of the Fund.

NOTE 8 – FEDERAL TAX INFORMATION

At November 30, 2016, the net unrealized appreciation (depreciation) of investments for tax purposes was as follows:

Gross Unrealized Appreciation | $ | 3,430,422 | ||

Gross Unrealized Depreciation | (237,923 | ) | ||

Net Unrealized Appreciation on Investments | $ | 3,192,499 |

At November 30, 2016, the aggregate cost of securities for federal income tax purposes was $21,476,338.

At May 31, 2016, the Fund’s most recent fiscal year end, the components of distributable earnings (accumulated losses) on a tax basis were as follows:

Undistributed ordinary income | $ | 53,020 | ||

Accumulated capital and other losses | (794,296 | ) | ||

Unrealized appreciation | 2,653,620 | |||

Total | $ | 1,912,344 |

The difference between book and tax basis appreciation was attributable primarily to the tax deferral of losses on wash sales.

The tax character of distributions paid for the fiscal year ended May 31, 2016 was as follows:

| 2016 | ||||

Distributions paid from: | ||||

Ordinary Income | $ | 69,881 | ||

As of May 31, 2016, the Fund has available for federal tax purposes an unused capital loss carryforward of $31,655 and $400,253 of long-term and short-term capital losses, respectively, with no expiration, which is available to offset against future taxable net capital gains. To the extent that these carryforwards are used to offset future gains, it is probable that the amount offset will not be distributed to shareholders.

Certain capital losses incurred after October 31, and within the current taxable year, are deemed to arise on the first business day of the Fund’s following taxable year. For the tax year ended May 31, 2016, the Fund deferred post October capital losses in the amount of $362,388.

NOTE 9 – COMMITMENTS AND CONTINGENCIES

The Fund indemnifies its officers and trustees for certain liabilities that may arise from performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred.

26

BFS Equity Fund

Notes to Financial Statements (Unaudited) (continued)

November 30, 2016

NOTE 10 – SUBSEQUENT EVENTS

Management of the Fund has evaluated the need for disclosure and/or adjustments resulting from subsequent events through the date these financials were issued. Management has determined there were no items requiring adjustment of the financial statements or additional disclosure.

27

BFS Equity Fund

Summary of Fund Expenses (Unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs; and (2) ongoing costs, including management fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example in the table below is based on an investment of $1,000 invested at the beginning of the period, and held for the six month period from June 1, 2016 to November 30, 2016.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60), then multiply the result by the number in the first line under the heading “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| Beginning Account Value June 1, 2016 | Ending Account Value November 30, 2016 | Expenses Paid During the Period(a) | ||||||||||

Actual | $ | 1,000.00 | $ | 1,029.40 | $ | 6.36 | ||||||

Hypothetical(b) | $ | 1,000.00 | $ | 1,018.80 | $ | 6.33 | ||||||

| (a) | Expenses are equal to the Fund’s annualized expense ratio of 1.25%, multiplied by the average account value over the period, multiplied by 183/365. |

| (b) | Assumes a 5% return before expenses. |

28

BFS Equity Fund

Investment Advisory Agreement Approval (Unaudited)

At a meeting held on June 7-8, 2016, the Board of Trustees (the “Board”) considered the renewal of the Investment Advisory Agreement (the “Agreement”) between Valued Advisers Trust (the “Trust”) and Bradley, Foster & Sargent, Inc. (“BFS”) with respect to the BFS Equity Fund (the “Fund”). BFS provided written information to the Board to assist the Board in its considerations.

The Trustees discussed the fact that BFS no longer waives its entire management fee for the Fund. Counsel reminded the Trustees of their fiduciary duties and responsibilities as summarized in a memorandum from his firm, including the factors to be considered, and the application of those factors to BFS. In assessing the factors and reaching its decision, the Board took into consideration information furnished by BFS and the Trust’s other service providers for the Board’s review and consideration throughout the year, as well as information specifically prepared or presented in connection with the annual renewal process, including: (i) reports regarding the services and support provided to the Fund and its shareholders by BFS; (ii) quarterly assessments of the investment performance of the Fund by personnel of BFS; (iii) commentary on the reasons for the performance; (iv) presentations by BFS addressing its investment philosophy, investment strategy, personnel, and operations; (v) compliance and audit reports concerning the Fund and BFS; (vi) disclosure information contained in the registration statement of the Trust and the Form ADV of BFS; and (vii) a memorandum from trust counsel, that summarized the fiduciary duties and responsibilities of the Board in reviewing and approving the Agreement. The Board also requested and received materials including, without limitation: (i) documents containing information about BFS, including its financial information, its personnel, and the services provided to the Fund; (ii) investment advice, performance, compliance, legal matters related to the Fund; (iii) comparative expense and performance information for other mutual funds with strategies similar to the Fund; and (iv) benefits to be realized by BFS from its relationship with the Fund. The Board did not identify any particular information that was most relevant to its consideration to approve the Agreement and each Trustee may have afforded different weight to the various factors.

| 1. | The nature, extent, and quality of the services to be provided by BFS. In this regard, the Board considered BFS’s responsibilities under the Agreement. The Trustees considered the services being provided by BFS to the Fund including, without limitation: the quality of its investment advisory services (including research and recommendations with respect to portfolio securities), its process for formulating investment recommendations and assuring compliance with the Fund’s investment objectives and limitations, its coordination of services for the Fund among the Fund’s service providers, and its efforts to promote the Fund and grow its assets. The Trustees considered BFS’s continuity of, and commitment to: retain qualified personnel, maintain and enhance its resources and systems, and overseeing the management of the Fund’s portfolio and investment objective. The Trustees considered BFS’s personnel, including their education and experience. After considering the foregoing information and further information in the meeting materials provided by BFS, the Board concluded that, in light of all the facts and circumstances, the nature, extent, and quality of the services provided by BFS were satisfactory and adequate for the Fund. |

| 2. | Investment Performance of the Fund and BFS. In this regard, the Trustees compared the performance of the Fund with the performance of funds with similar objectives managed by other investment advisers, with aggregated peer group data, as well as with the performance of the Fund’s benchmark. The Trustees also considered the consistency of BFS’s management of the Fund with its investment objectives, strategies, and limitations. The Trustees noted |

29

that the Fund had outperformed its benchmark for the calendar year 2015, but had underperformed compared to the benchmark for the year-to-date period as of March 31, 2016. They also noted that the Fund had outperformed its peer group average for the three-month and one-year periods. The Board reviewed the performance of BFS in managing a composite with investment strategies similar to that of the Fund and observed that the Fund’s performance was above the composite for the one-year period but it trailed the composite for the year-to-date period as of March 31, 2016. After further reviewing and discussing these and other relevant factors, the Board concluded, in light of all the facts and circumstances, that the investment performance of the Fund and BFS was satisfactory. |

| 3. | The costs of the services to be provided and profits to be realized by BFS from the relationship with the Fund. In this regard, the Trustees considered: (1) BFS’s financial condition; (2) the asset level of the Fund; (3) the overall expenses of the Fund; and (4) the nature and frequency of management fee payments. The Trustees reviewed information provided by BFS regarding its profits associated with managing the Fund, noting that BFS is currently waiving most of its management fee and reimbursing a portion of the Fund’s expenses. The Trustees also considered potential benefits for BFS in managing the Fund. The Trustees then compared the fees and expenses of the Fund (including the management fee) to other comparable mutual funds. The Trustees noted that the Fund’s management fee was below the average and median management fees of peers in its category. The Trustees also noted that the Fund’s net expense ratio was relatively comparable to that of the average and median of peers in its category, because of BFS’s contractual commitment to limit the expenses of the Fund. Based on the foregoing, the Board concluded that the fees to be paid to BFS by the Fund and the profits to be realized by BFS, in light of all the facts and circumstances, were fair and reasonable in relation to the nature and quality of the services provided by BFS. |

| 4. | The extent to which economies of scale would be realized as the Fund grows and whether advisory fee levels reflect these economies of scale for the benefit of the Fund’s investors. In this regard, the Board considered the Fund’s fee arrangements with BFS. The Board considered that while the management fee remained the same at all asset levels, the Fund’s shareholders experienced benefits from the Fund’s expense limitation arrangement. The Trustees noted that once the Fund’s expenses fell below the cap set by the arrangement, the shareholders would continue to benefit from economies of scale under the Fund’s arrangements with other service providers to the Fund, and the Trustees attributed this benefit, in part, to the direct and indirect efforts of BFS at the inception of the Fund to ensure that a cost structure was in place that was beneficial for the Fund as it grew. In light of its ongoing consideration of the Fund’s asset and fees levels and expectations for growth, the Board determined that the Fund’s fee arrangements, in light of all the facts and circumstances, were fair and reasonable in relation to the nature and quality of the services provided by BFS. |

| 5. | Possible conflicts of interest and benefits to BFS. In considering BFS’s practices regarding conflicts of interest, the Trustees evaluated the potential for conflicts of interest and considered such matters as the experience and ability of the advisory personnel assigned to the Fund; the basis of decisions to buy or sell securities for the Fund and/or BFS’s other accounts; and the substance and administration of BFS’s code of ethics. The Trustees also considered disclosure in the registration statement of the Trust relating to BFS’s potential conflicts of interest. The Trustees noted that BFS may utilize soft dollars and the Trustees |

30

noted BFS’s policies and processes for managing the conflicts of interest that could arise from soft dollar arrangements. The Trustees noted other potential benefits to BFS, including the fact that the Fund provides an attractive vehicle for smaller accounts, which may increase the total assets under management by BFS. Based on the foregoing, the Board determined that the standards and practices of BFS relating to the identification and mitigation of potential conflicts of interest and the benefits to be realized by BFS in managing the Fund were satisfactory. |

After additional consideration of the factors delineated in the memorandum provided by counsel and further discussion among the Board members, the Board determined to approve the continuation of the Agreement between the Trust and BFS.

31

VALUED ADVISERS TRUST

PRIVACY POLICY

The following is a description of the policies of the Valued Advisers Trust (the “Trust”) regarding disclosure of nonpublic personal information that shareholders provide to a series of the Trust (each, a “Fund”) or that the Fund collects from other sources. In the event that a shareholder holds shares of a Fund through a broker-dealer or other financial intermediary, the privacy policy of the financial intermediary would govern how shareholder nonpublic personal information would be shared with nonaffiliated third parties.

Categories of Information a Fund May Collect. A Fund may collect the following nonpublic personal information about its shareholders:

| • | Information the Fund receives from a shareholder on applications or other forms, correspondence, or conversations (such as the shareholder’s name, address, phone number, social security number, and date of birth); and |

| • | Information about the shareholder’s transactions with the Fund, its affiliates, or others (such as the shareholder’s account number and balance, payment history, cost basis information, and other financial information). |

Categories of Information a Fund May Disclose. A Fund may not disclose any nonpublic personal information about its current or former shareholders to unaffiliated third parties, except as required or permitted by law. A Fund is permitted by law to disclose all of the information it collects, as described above, to its service providers (such as the Fund’s custodian, administrator, transfer agent, accountant and legal counsel) to process shareholder transactions and otherwise provide services to the shareholder.