united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

| Investment Company Act file number | 811-22208 |

| Valued Advisers Trust |

| (Exact name of registrant as specified in charter) |

| Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 | Cincinnati, OH 45246 |

| (Address of principal executive offices) | (Zip code) |

Ultimus Fund Solutions, LLC

Attn: Gregory Knoth

225 Pictoria Drive, Suite 450

Cincinnati, OH 45246

(Name and address of agent for service)

| Registrant's telephone number, including area code: | 513-587-3400 |

| Date of fiscal year end: | 5/31 | |

| Date of reporting period: | 11/30/2019 |

Item 1. Reports to Stockholders.

BFS Equity Fund

SEMI-ANNUAL REPORT

November 30, 2019

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically by contacting the Fund at (855) 575-2430 or, if you own these shares through a financial intermediary, you may contact your financial intermediary.

You may elect to receive all future reports in paper free of charge. You can inform the Fund that you wish to continue receiving paper copies of your shareholder reports by contacting the Fund at (855) 575-2430. If you own shares through a financial intermediary, you may contact your financial intermediary or follow instructions included with this document to elect to continue to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held with the fund complex or at your financial intermediary.

185 Asylum Street ● City Place II ● Hartford, CT 06103 ● (855) 575-2430

BFS Equity Fund

Letter to Shareholders

Dear Fellow Shareholders,

Greetings in the New Year! This semi-annual report covers the six-month period from June 1, 2019 through November 30, 2019.

On June 1, 2019, the BFS Equity Fund (the “Fund”) had net assets of $36.0 million. During the six-month period, the net assets of the Fund increased 17.9% to $42.4 million as of November 30, 2019. This growth was driven both by inflows from investors into the Fund, as well as by the positive investment returns achieved by the Fund over the six months. As of November 30, 2019, there were over 685 investors in the Fund.

This report includes a commentary from the Lead Portfolio Manager, Tim Foster, and Co-Portfolio Managers, Tom Sargent and Keith LaRose. You will also find a listing of the portfolio holdings as of November 30, 2019, as well as financial statements and detailed information about the performance and positioning of the Fund.

As 2019 draws to a close, the year will be remembered as a continuation of the longest expansion on record in the U.S., central bank balance sheet contraction followed by expansion, negative interest rate debt totaling over $17 trillion at one point, and a U.S.-China trade war. It was also a year that saw an increase in the momentum of innovation encompassing artificial intelligence, automation, sustainability, and solutions to combat the negative impact of climate change.

As we head into 2020, politics – namely the U.S. presidential election – will bring policy uncertainty, while the impact of the impeachment trial should be clarified once the Senate addresses the articles of impeachment. Internationally, it is expected that the implications of Brexit will be better understood by the year-end, if not sooner. And the Phase 1 trade deal with China should eventually be signed, resulting in tariff rollbacks and increased purchases of U.S. agricultural products by China.

There is general agreement among analysts that interest rates and unemployment rates should stay relatively low, although wage inflation could prove to be a headwind. Other possible headwinds include tax-cut driven payouts falling back to normal levels, reduced company share buybacks, and anti-trust investigations of some of the FAANG stocks.

1

Notwithstanding these possible headwinds, a better GDP trajectory and continued earnings growth, as driven by the consumer (housing, jobs), should help support equity valuations.

To mitigate these and other risks, our investment strategy focuses on the long-term investment in quality growth stocks that are positioned to provide a margin of safety in the case of economic or market weakness. Of the 43 companies which the Fund owned as of November 30, 2019, 36 paid dividends, and several are so-called “dividend aristocrats” – companies which have increased their dividend payouts annually for the past 25 years. We continue to believe the Fund’s ownership of shares in quality companies with strong brands, sound business models, good balance sheets, professional management, and robust cash flows should be able to withstand market corrections, even bear markets, and perform well over the longer term.

The Portfolio Managers of the BFS Equity Fund and I are shareholders together with you. We thank you for the trust that you have placed in us to manage your assets.

Sincerely,

Stephen L. Willcox

President

Bradley, Foster & Sargent, Inc.

2

BFS Equity Fund

Portfolio Managers Letter

TO OUR SHAREHOLDERS

November 30, 2019 marks the sixth anniversary for the BFS Equity Fund (the “Fund”). During this six-year period, the Fund has improved its net asset value from $10.00 to $17.46 per share. For the six-month semiannual period from June 1, 2019 to November 30, 2019, the Fund produced a total return of +13.38%. For the trailing twelve-month period, the Fund produced a return of +17.13%. The S&P 500 Index (“S&P 500”) produced a total return of +15.26% for the comparable six-month period and +16.11% for the comparable twelve-month period. Over the six years since inception, the Fund has produced average yearly returns of +10.57% on an annualized basis.

It has been a good six years to be in the market. Stocks have enjoyed a relatively stable period of low inflation, low interest rates and modest, but consistent economic growth. This has led to a period of relatively low volatility in the market, with a brief exception in the fourth quarter of 2018 when the market experienced a near 20% correction, largely driven by an untimely tightening of monetary policy. The Federal Reserve reversed course in 2019, lowering the Fed Funds rate three times through the end of November and the stock market resumed its upward trajectory.

The correction that did occur during the last quarter of 2018 squeezed out entirely the advance the market made during the first three quarters of 2018, to end the year with a loss of -4%. Given that S&P 500 profits were up in the mid +20% range, that was a very unlikely outcome. This year, S&P 500 profits are up mid-single digits and the market is up mid +20% through the end of November. This is yet another unlikely outcome, but one that leads us to believe that this year’s market gains are playing catch up to last year’s corporate profit gains and not borrowing on next year’s earnings.

MARKET COMMENTARY

The current bull market is now pushing toward a record level in both magnitude and duration. In this context it might be fair to assume that we may be late in this cycle and that a recession and/or significant market pullback may be close at hand. The simple sentence that has often derailed investors in the past is: “It’s different this time.” Well, we think it might be.

3

Bull markets don’t die of old age, they die of excess. Market corrections are just that – a revaluation that eliminates the excesses built up in the prior cycle. Market conditions in the fourth quarter of 2019 failed to register many of the excesses seen in prior Market-Tops. From the market peaks in 2001 and 2007, the correction process eliminated nearly 50% of the market’s value. These valuation resets often behave in a pendulum-like manner, whereby emotions of both the greed and fear variety can overshoot the fair value mark on both the downside as well as the upside.

We believe the current valuation of the market seems close-to-fair, skewed somewhat to the upside. Most stock valuations fall within a range of about 9 times earnings on the low side to 25 times earnings on the high side, the exceptions being highly cyclical companies with large swings in earnings and very high growth companies, where investors are willing to pay a high price today for expected high earnings in the future. The P/E of the market today is about 18 times earnings. The 30-year average is closer to 16, so a modest premium exists today reflecting the extremely low levels of both inflation and interest rates. Present values of future earnings are simply worth more today when inflation is not eroding future purchasing power and lower prevailing interest rates raise present discounted values. And importantly, corporate earnings are expected to grow at a mid-single digit pace in 2020 as they have in 2019. Valuation does not appear to be excessive.

Monetary and fiscal policies also have notable impacts on the market. Trillion-dollar budget deficits certainly suggest fiscal policy of a stimulative nature. Real interest rates of close to zero suggest a very accommodative monetary policy as well. Real GDP growth is currently running around 2%. This is well below the “economic speed limit” and hardly excessive. Signals from Washington suggest neither of these policies will be reversing any time soon.

Speculation is another factor of excess. Speculation can be in evidence on both the institutional and individual investor fronts. Merger and Acquisition (M&A), as well as Initial Public Offering (IPO) activity often spikes near Market-Tops. While the absolute value of M&A activity is at record levels relative to the current market capitalization, it is well within bounds. IPO activity appeared somewhat frothier earlier this year, but the bulk of IPOs sold in 2019 are now trading below their original offering prices. From the perspective of the individual investor, the virtual definition of a top is when everyone is already on board. Remarkably, almost half a trillion dollars has been pulled from equity mutual funds and Exchange-Traded Funds (ETFs) since the market bottom in 2009, while

4

nearly two trillion risk-averse dollars have been added to fixed income funds and ETFs at a time when interest rates are near their all-time lows. This time, speculative excess may be the hallmark of the fixed income markets rather than equity markets.

Several other Market-Top signposts are notably absent from the current market as well. Credit spreads are a good indicator of the likelihood of corporate bond defaults. At present, credit spreads are relatively well behaved with little indication of impending doom. Narrowing market leadership is another indicator of a market losing its upward momentum. Remember the “Nifty Fifty” of the 70s, the “Five Horsemen” of the 90s and the “FAANGs” of more recent vintage? These were the handful of stocks that drove the stock market to a peak in prior cycles. Presently, though, most stock sectors are behaving well. In fact, there has been a recent emergence of value stocks performing in line with the growth favorites that have led this cycle since the 2009 bottom. The Market-Top list continues with an inverted yield curve. This red flag appeared several months ago but has since reversed itself. Commodity prices often spike near Market-Tops, but commodities from grains to metals to energy are now generally quiescent and far from prior peaks.

To sum it up, we generally find ourselves in a growing economy with full employment, little inflationary pressure, an accommodative Fed, and a stock market that appears fully, but not overly valued. Excess does not appear to be the Barbarian at the Gate to close the chapter on this cycle. Good news, indeed!

But, (you knew this was coming), every element cited above can, and will, change. We follow an extended checklist and will adjust both portfolio holdings and general aggressiveness guided by changes in these elements and additional signposts. Through several decades of investing, we have rarely let politics be a primary driver of strategy; however, this time, it may be different, as well. The divisiveness of our current two-party system has never been so extreme. Regardless of where your own politics may lie, capitalism is at the heart of the productive resources in this country and hence of the stock market. Pro-capitalist policies are generally good for the market. Pro-socialist policies are generally not. In our view, should the election process over the next eleven months shift in favor of more government control and less free enterprise, the equity market will likely suffer as a result.

5

One further thought – a reminder about volatility. While the largest drawdown during the six-month period was only 6%, the typical drawdown in the equity market in any given year is roughly 14%. So even with the stars aligned for a generally conducive equity backdrop, a 10-15% pullback should not be unexpected.

INVESTMENT COMMENTARY

Information Technology

The information technology sector was the Fund’s heaviest weighted sector at 26.4%, an overweighting to the S&P 500 information technology sector weighting of 22.8%. In general, we see the information technology sector exhibiting the best prospects for growth versus all other S&P 500 sectors. Stock selection within the sector led to a total return of +19.5% during the period versus +23.5% for the benchmark. Apple was the Fund’s top-performing stock (+53.7%) during the period, but it was underweighted relative to the benchmark. Of the Fund’s holdings in this sector, only Cisco had a negative return for the period (-11.7%), but we continue to hold Cisco and have recently added to the position, given the attractive relative valuation, dividend and growth prospects, especially in future 5G build-outs. We added three new tech positions during the period: Ceridian Holdings, Fiserv and SS&C Technologies. All provide essential software and services to the financial services industries, as well as corporate HR departments.

Healthcare

Healthcare continued as the Fund’s second heaviest weighting at 17.7% versus the S&P 500 healthcare weighting of 14.1%. The Fund’s total return of +8.4% during the period trailed the S&P 500 sector return of +15.1%. Healthcare runs a close second to information technology in terms of what we believe are the best prospects for growth. Zoetis was the Fund’s top performer (+19.6%). Two stocks, which formerly contributed positively to relative returns, slipped during the period. Johnson & Johnson lost -1.0% and was sold, given the enormous wave of product liability cases the company faces. Mettler Toledo simply got ahead of itself in valuation. We added to the position, given the current weakness. UnitedHealth Group was the sector’s worst performing stock (-9.3%). The political winds suggesting Medicare-for-all delivered a crushing, but somewhat temporary, blow to many healthcare stocks. Unfortunately, we lost our conviction and sold the stock at a loss. It was an untimely sale, given the subsequent rebound in the stock’s price.

6

Industrial

The industrial sector was the Fund’s third largest weighting at 15.0%, a significant overweight to the S&P 500 at 9.3%. Relative performance was a win, with the Fund’s total return during the period of +19.4% beating the benchmark return of +15.0%. All but one industrial holding provided a positive return with Raytheon leading the pack (+25.9%) and Stanley Black & Decker close behind (+25.8%). Fortive was the odd man out with a return of -5.0%. Trade negotiations were a vital influence on the group with large daily price movements dependent on negotiation chatter. 3M was sold during the period for the same reason we sold J&J. The PFAS liability the company faces could be very significant, and we chose to sidestep the risk. One new purchase is Boeing. The 737 Max issue has provided an attractive entry point. In a global duopoly with Airbus, Boeing will most certainly get their planes back in the air.

Financials

Financials ranked fourth largest among our sector weightings in the Fund, weighing in at 10.0%, but underweighted to the S&P 500 financials weighting of 13.1%. Every financial holding in the Fund contributed to the sector’s +14.8% return for the period, but was shy of the benchmark return of +17.1%. The banks performed especially well, with J.P. Morgan contributing the best return of +26.2%, followed by Citigroup with +22.6%.

Consumer Discretionary

Weighing in at 7.7%, consumer discretionary stocks were somewhat underweighted versus the S&P 500 weighting of the sector at 9.8%. The Fund outperformed the benchmark with a return of +13.1% versus +10.1% for the S&P 500. The Fund’s largest contributor was Nike (+21.8%). Home Depot was second (+17.7%). Amazon had a somewhat disappointing return of +1.5%, but the Fund’s weighting in Amazon was well below the benchmark weighting. We still believe Amazon offers great growth prospects going forward, but we are cautious at the current valuation.

Consumer Staples

The Fund’s consumer staples sector weighting was 5.9% versus 7.2% for the benchmark. The Fund’s performance of +13.0% was in line with the benchmark performance of +12.9%. Costco, “everybody’s” favorite place to shop for value, was our standout performer at +25.7%. Constellation Brands and Mondelez contributed positive mid-single digit returns.

7

Communication Services

We own two stocks in the communication services sector: Alphabet and Disney. Both produced attractive returns of +17.9% and +15.5%, respectively. The Fund was underweight the sector at 5.7% versus 10.5% for the benchmark, but outperformed the benchmark with the Fund returning +16.9% versus the benchmark return of +13.9%. (While we had owned Facebook, we exited our position in the first half of the fiscal year.)

Materials

The Fund had only two holdings in the materials sector. Our longtime holding of Ecolab was relatively flat for the period at a +1.9% return, but our single gold holding, Agnico Eagle Mines, performed well (+16.8%).

Energy

Energy continues to shrink as an S&P 500 sector, down to 4.2% as measured against the prior six-month period of the index. The Fund was underweight the benchmark at 2.2%. Chevron produced a total return of +5.0%, with help from a healthy dividend. EOG Resources, which is more leveraged to falling energy prices, declined -16.7% and was sold.

Real Estate

The Fund’s single exposure to real estate is Weyerhaeuser, which performed well, contributing a return of +18.1% for the period. Low mortgage rates, good household formation and a housing market that, in general, is still in recovery mode provided a constructive backdrop for lumber prices and a positive outlook for Weyerhaeuser.

CLOSING COMMENTS

Our portfolio remains fairly concentrated with 43 holdings, and our turnover remains relatively low (an annual rate of 23.8% over the six-month period). We generally buy names with at least a 3-5 year outlook and will likely own most of these names for many years to come.

The forward P/E of the market has been fairly consistent in the 16-18 range for several years. So has the low level of interest rates. If rates remain at these low levels, which the Fed has implied as likely, then one might expect market returns in keeping with a roughly 18 multiple on earnings 5-7% higher than 2019. While the robust returns thus far in 2019

8

may have been playing catch up from the robust earnings gains of 2018, it might be wise to temper expectations for 2020 returns to something well below the recent trendline. The 2020 election may prove to be the wildcard.

We at Bradley, Foster & Sargent, Inc. look forward to serving you through our management of the BFS Equity Fund. Thank you for placing your capital under our care.

Timothy Foster | Keith LaRose | Thomas Sargent |

Performance: The Bottom Line

Average annual total return reflects the change in the value of an investment, assuming reinvestment of distributions from net investment income and net realized capital gains (the net profits earned upon the sale of securities that have grown in value), less the losses for the sale of securities that decreased in value and assuming a constant rate of performance each year. The hypothetical investment and the average annual total returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During periods of reimbursement the Fund’s total return will be greater than it would be had the reimbursement not occurred. How the Fund did in the past is no guarantee of how it will do in the future.

9

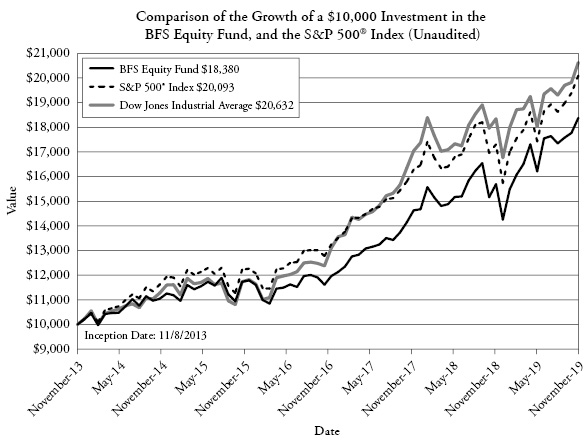

$10,000 Over 10 Years

Let’s say hypothetically that $10,000 was invested in the Fund, on November 8, 2013. The following chart shows how the value of your investment would have changed, and also shows how the S&P 500® Index performed over the same period.

The chart above assumes an initial investment of $10,000 made on November 8, 2013 (commencement of operations) held through November 30, 2019. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Fund, and to obtain performance data current to the most recent month end or to request a prospectus, please call (855) 575-2430. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Fund before investing. The Fund’s prospectus contains this and other information about the Fund, and should be read carefully before investing.

10

BFS Equity Fund

SEMI-ANNUAL

PERFORMANCE REVIEW

(UNAUDITED)

The Fund performed modestly behind the S&P 500 for the six-month period ended November 30, 2019, returning +13.38% versus +15.26% for the S&P 500. For the trailing twelve-month period, the Fund outpaced the S&P 500 with a return of +17.13% versus +16.11% for the S&P 500.

Key Detractors from Relative Results

1. | The timing of the Fund’s purchase and sale of UnitedHealth Group led to the unfortunate outcome of buying high and selling low. UNH is the leading managed healthcare company, but we simply lost confidence given the debate over universal healthcare. |

2. | Soft oil prices led to a leveraged reaction in EOG Resources, which was also sold at a loss. |

3. | Higher weightings in information technology (particularly in Apple which returned +53.7%) and financials would have helped to enhance performance. |

Key Contributors to Relative Results

1. | The Fund’s top ten positions all contributed positively to absolute performance. |

2. | The large overweight (15.0% vs. 9.3%) and outperformance of the S&P 500 industrial sector (+19.4 vs. +15.0%) was also a significant contributor to the Fund’s performance versus the S&P 500. |

3. | Although a small weighting, Weyerhaeuser led to the best sector performance relative to the benchmark in the real estate sector. |

FUND INFORMATION

November 30, 2019

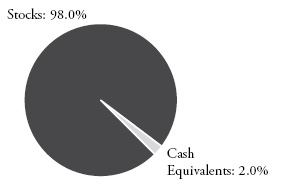

ASSET ALLOCATION

(as a percentage of total investments)

TEN LARGEST HOLDINGS (%) | FUND |

Alphabet Inc. Class A | 3.1 |

Agnico Eagle Mines Limited | 2.8 |

JPMorgan Chase | 2.8 |

Danaher | 2.8 |

Fiserv | 2.7 |

Walt Disney | 2.7 |

Chubb Limited | 2.7 |

Citigroup | 2.7 |

Oracle | 2.7 |

SS&C Technologies | 2.6 |

SECTOR | FUND | S&P 500 |

Information Technology | 26.4 | 22.8 |

Healthcare | 17.7 | 14.1 |

Industrial | 15.0 | 9.3 |

Financials | 10.0 | 13.1 |

Consumer Discretionary | 7.7 | 9.8 |

Consumer Staples | 5.9 | 7.2 |

Communication Services | 5.7 | 10.5 |

Materials | 5.0 | 2.7 |

Real Estate | 2.4 | 3.0 |

Energy | 2.2 | 4.2 |

Cash Equivalents | 2.0 | 0.0 |

Utilities | 0.0 | 3.3 |

Availability of Portfolio Schedule (Unaudited)

The Fund files its complete schedule of investments with the Securities and Exchange Commission (“SEC”) as of the end of the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available at the SEC’s website at www.sec.gov.

11

BFS Equity Fund

Investment Results (Unaudited)

Average Annual Total Returns(a) (For the periods ended November 30, 2019)

Six | One | Three | Five | Since Inception | |

BFS Equity Fund | 13.38% | 17.13% | 15.38% | 10.30% | 10.57% |

S&P 500® Index (b) | 15.26% | 16.11% | 14.88% | 10.98% | 12.20% |

Dow Jones Industrial Average® (c) | 14.42% | 12.48% | 16.32% | 12.20% | 12.69% |

Total annual fund operating expenses, as disclosed in the BFS Equity Fund’s (the “Fund”) prospectus dated September 28, 2019, were 1.57% of average daily net assets (1.25% after fee waivers/expense reimbursements by Bradley, Foster & Sargent, Inc. (the “Adviser”)). The Adviser has contractually agreed to waive or limit its fees and to assume other expenses of the Fund until September 30, 2020, so that Total Annual Fund Operating Expenses does not exceed 1.00%. This contractual arrangement may only be terminated by mutual consent of the Adviser and the Board of Trustees of the Valued Advisers Trust (the “Trust”), and it will automatically terminate upon the termination of the investment advisory agreement between the Trust and the Adviser. This operating expense limitation does not apply to: (i) interest, (ii) taxes, (iii) brokerage commissions, (iv) other expenditures which are capitalized in accordance with generally accepted accounting principles, (v) other extraordinary expenses not incurred in the ordinary course of the Fund’s business, (vi) dividend expense on short sales, (vii) expenses incurred under a plan of distribution under Rule 12b-1, and (viii) expenses that the Fund has incurred but did not actually pay because of an expense offset arrangement, if applicable, in any fiscal year. The operating expense limitation also excludes any “Acquired Fund Fees and Expenses,” which are the expenses indirectly incurred by the Fund as a result of investing in money market funds or other investment companies, including exchange-traded funds, that have their own expenses. Each waiver or reimbursement of an expense by the Adviser is subject to repayment by the Fund within the three years following such waiver or reimbursement, provided that the Fund is able to make the repayment without exceeding the expense limitation in place at the time of the waiver or reimbursement and the expense limitation in place at the time of the repayment.

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (855) 575-2430.

(a) | Average annual total returns reflect any change in price per share and assume the reinvestment of all distributions. The Fund’s returns reflect any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would have been lower. Total returns for periods less than one year are not annualized. |

(b) | The S&P 500® Index is a widely recognized unmanaged index of equity prices and is representative of a broader market and range of securities than is found in the Fund’s portfolio. The index is an unmanaged benchmark that assumes reinvestment of all distributions and excludes the effect of taxes and fees. Individuals cannot invest directly in this index; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index. |

(c) | The Dow Jones Industrial Average® is a widely recognized unmanaged index of equity prices and is representative of a narrower market and range of securities than is found in the Fund’s portfolio. The index is an unmanaged benchmark that assumes reinvestment of all distributions and excludes the effect of taxes and fees. Individuals cannot invest directly in this index; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index. |

The Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Fund and may be obtained by calling the same number as above. Please read it carefully before investing.

The Fund is distributed by Ultimus Fund Distributors, LLC, member FINRA/SIPC.

12

BFS Equity Fund

Schedule of Investments (Unaudited)

November 30, 2019

| Shares | Fair Value | ||||||

COMMON STOCKS — 97.99% | ||||||||

Aerospace & Defense — 6.48% | ||||||||

Boeing Company (The) | 2,500 | $ | 915,450 | |||||

Raytheon Company | 4,000 | 869,680 | ||||||

United Technologies Corporation | 6,500 | 964,210 | ||||||

| 2,749,340 | ||||||||

Banks — 5.45% | ||||||||

Citigroup, Inc. | 15,000 | 1,126,800 | ||||||

JPMorgan Chase & Company | 9,000 | 1,185,840 | ||||||

| 2,312,640 | ||||||||

Beverages — 2.19% | ||||||||

Constellation Brands, Inc., Class A | 5,000 | 930,300 | ||||||

Chemicals — 2.20% | ||||||||

Ecolab, Inc. | 5,000 | 933,350 | ||||||

Communications Equipment — 2.46% | ||||||||

Cisco Systems, Inc. | 23,000 | 1,042,130 | ||||||

Consumer Finance — 1.84% | ||||||||

American Express Company | 6,500 | 780,780 | ||||||

Electronic Equipment, Instruments & Components — 4.64% | ||||||||

Amphenol Corporation, Class A | 10,000 | 1,040,000 | ||||||

TE Connectivity Ltd. | 10,000 | 927,100 | ||||||

| 1,967,100 | ||||||||

Entertainment — 2.68% | ||||||||

Walt Disney Company (The) | 7,500 | 1,136,850 | ||||||

Equity Real Estate Investment Trusts (REITs) — 2.44% | ||||||||

Weyerhaeuser Company | 35,000 | 1,032,850 | ||||||

Food & Staples Retailing — 2.47% | ||||||||

Costco Wholesale Corporation | 3,500 | 1,049,335 | ||||||

Food Products — 1.24% | ||||||||

Mondelez International, Inc., Class A | 10,000 | 525,400 | ||||||

See accompanying notes which are an integral part of these financial statements. | 13 |

BFS Equity Fund

Schedule of Investments (Unaudited) (continued)

November 30, 2019

| Shares | Fair Value | ||||||

COMMON STOCKS — 97.99% - continued | ||||||||

Health Care Equipment & Supplies — 6.78% | ||||||||

Abbott Laboratories | 8,000 | $ | 683,600 | |||||

Danaher Corporation | 8,000 | 1,167,840 | ||||||

Stryker Corporation | 5,000 | 1,024,300 | ||||||

| 2,875,740 | ||||||||

Hotels, Restaurants & Leisure — 1.71% | ||||||||

Starbucks Corporation | 8,500 | 726,155 | ||||||

Insurance — 2.68% | ||||||||

Chubb Ltd. | 7,500 | 1,136,100 | ||||||

Interactive Media & Services — 3.08% | ||||||||

Alphabet, Inc., Class A(a) | 1,000 | 1,304,090 | ||||||

Internet & Direct Marketing Retail — 2.13% | ||||||||

Amazon.com, Inc.(a) | 500 | 900,400 | ||||||

IT Services — 4.75% | ||||||||

Automatic Data Processing, Inc. | 5,000 | 853,900 | ||||||

Fiserv, Inc.(a) | 10,000 | 1,162,400 | ||||||

| 2,016,300 | ||||||||

Life Sciences Tools & Services — 6.68% | ||||||||

Illumina, Inc.(a) | 3,200 | 1,026,432 | ||||||

Mettler-Toledo International, Inc.(a) | 1,200 | 863,292 | ||||||

Thermo Fisher Scientific, Inc. | 3,000 | 941,850 | ||||||

| 2,831,574 | ||||||||

Machinery — 8.49% | ||||||||

Caterpillar, Inc. | 6,500 | 940,745 | ||||||

Deere & Company | 5,000 | 840,250 | ||||||

Fortive Corporation | 11,000 | 793,870 | ||||||

Stanley Black & Decker, Inc. | 6,500 | 1,025,310 | ||||||

| 3,600,175 | ||||||||

Metals & Mining — 2.81% | ||||||||

Agnico Eagle Mines Ltd. | 20,000 | 1,192,000 | ||||||

Oil, Gas & Consumable Fuels — 2.21% | ||||||||

Chevron Corporation | 8,000 | 937,040 | ||||||

14 | See accompanying notes which are an integral part of these financial statements. |

BFS Equity Fund

Schedule of Investments (Unaudited) (continued)

November 30, 2019

| Shares | Fair Value | ||||||

COMMON STOCKS — 97.99% - continued | ||||||||

Pharmaceuticals — 4.20% | ||||||||

Novartis AG - ADR | 9,500 | $ | 876,850 | |||||

Zoetis, Inc. | 7,500 | 903,900 | ||||||

| 1,780,750 | ||||||||

Software — 12.02% | ||||||||

Adobe, Inc.(a) | 3,000 | 928,590 | ||||||

Ceridian HCM Holding, Inc.(a) | 15,000 | 905,400 | ||||||

Microsoft Corporation | 7,000 | 1,059,660 | ||||||

Oracle Corporation | 20,000 | 1,122,800 | ||||||

SS&C Technologies Holdings, Inc. | 18,000 | 1,080,900 | ||||||

| 5,097,350 | ||||||||

Specialty Retail — 2.08% | ||||||||

Home Depot, Inc. (The) | 4,000 | 882,040 | ||||||

Technology Hardware, Storage & Peripherals — 2.52% | ||||||||

Apple, Inc. | 4,000 | 1,069,000 | ||||||

Textiles, Apparel & Luxury Goods — 1.76% | ||||||||

NIKE, Inc., Class B | 8,000 | 747,920 | ||||||

Total Common Stocks (Cost $27,358,297) | 41,556,709 | |||||||

MONEY MARKET FUNDS — 2.00% | ||||||||

Fidelity Investments Money Market Government Portfolio, Institutional Class, 1.57%(b) | 848,228 | 848,228 | ||||||

Total Money Market Funds (Cost $848,228) | 848,228 | |||||||

Total Investments — 99.99% (Cost $28,206,525) | 42,404,937 | |||||||

Other Assets in Excess of Liabilities — 0.01% | 3,717 | |||||||

NET ASSETS — 100.00% | $ | 42,408,654 | ||||||

(a) | Non-income producing security. |

(b) | Rate disclosed is the seven day effective yield as of November 30, 2019. |

ADR - American Depositary Receipt

The industries shown on the schedule of investments are based on the Global Industry Classification Standard, or GICS® (“GICS”). The GICS was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by Ultimus Fund Solutions, LLC.

See accompanying notes which are an integral part of these financial statements. | 15 |

BFS Equity Fund

Statement of Assets and Liabilities (Unaudited)

November 30, 2019

Assets | ||||

Investments in securities at fair value (cost $28,206,525) (Note 3) | $ | 42,404,937 | ||

Receivable for fund shares sold | 1,267 | |||

Dividends receivable | 39,848 | |||

Tax reclaims receivable | 920 | |||

Prepaid expenses | 20,885 | |||

Total Assets | 42,467,857 | |||

Liabilities | ||||

Payable to Adviser (Note 4) | 17,179 | |||

Payable to Administrator (Note 4) | 6,751 | |||

Distribution (12b-1) fees accrued (Note 4) | 17,106 | |||

Payable to trustees | 482 | |||

Other accrued expenses | 17,685 | |||

Total Liabilities | 59,203 | |||

Net Assets | $ | 42,408,654 | ||

Net Assets consist of: | ||||

Paid-in capital | $ | 27,476,502 | ||

Accumulated earnings | 14,932,152 | |||

Net Assets | $ | 42,408,654 | ||

Shares outstanding (unlimited number of shares authorized, no par value) | 2,428,600 | |||

Net asset value, offering and redemption price per share (Note 2) | $ | 17.46 | ||

16 | See accompanying notes which are an integral part of these financial statements. |

BFS Equity Fund

Statement of Operations (Unaudited)

For the six months ended November 30, 2019

Investment Income | ||||

Dividend income | $ | 292,825 | ||

Total investment income | 292,825 | |||

Expenses | ||||

Investment Adviser fees (Note 4) | 149,541 | |||

Distribution (12b-1) fees (Note 4) | 49,847 | |||

Administration fees (Note 4) | 19,000 | |||

Registration expenses | 14,809 | |||

Fund accounting fees (Note 4) | 12,500 | |||

Legal fees | 11,401 | |||

Transfer agent fees (Note 4) | 9,000 | |||

Audit and tax preparation fees | 8,750 | |||

Printing and postage expenses | 4,355 | |||

Trustee fees | 3,370 | |||

Insurance expenses | 2,295 | |||

Custodian fees | 2,108 | |||

Miscellaneous | 14,380 | |||

Total expenses | 301,356 | |||

Fees contractually waived by Adviser (Note 4) | (52,581 | ) | ||

Net operating expenses | 248,775 | |||

Net investment income | 44,050 | |||

Net Realized and Change in Unrealized Gain (Loss) on Investments | ||||

Net realized gain on investment securities transactions | 281,918 | |||

Net change in unrealized appreciation on investments | 4,576,223 | |||

Net realized and change in unrealized gain on investments | 4,858,141 | |||

Net increase in net assets resulting from operations | $ | 4,902,191 | ||

See accompanying notes which are an integral part of these financial statements. | 17 |

BFS Equity Fund

Statements of Changes in Net Assets

Increase (Decrease) in Net Assets due to: | For the | For the | ||||||

Operations | ||||||||

Net investment income | $ | 44,050 | $ | 97,347 | ||||

Net realized gain on investment securities transactions | 281,918 | 715,995 | ||||||

Net change in unrealized appreciation on investments | 4,576,223 | 1,346,387 | ||||||

Net increase in net assets resulting from operations | 4,902,191 | 2,159,729 | ||||||

Distributions to Shareholders from Earnings (Note 2) | — | (1,113,363 | ) | |||||

Capital Transactions | ||||||||

Proceeds from shares sold | 2,528,275 | 5,524,451 | ||||||

Reinvestment of distributions | — | 950,796 | ||||||

Amount paid for shares redeemed | (982,093 | ) | (3,311,176 | ) | ||||

Net increase in net assets resulting from capital transactions | 1,546,182 | 3,164,071 | ||||||

Total Increase in Net Assets | 6,448,373 | 4,210,437 | ||||||

Net Assets | ||||||||

Beginning of period | 35,960,281 | 31,749,844 | ||||||

End of period | $ | 42,408,654 | $ | 35,960,281 | ||||

Share Transactions | ||||||||

Shares sold | 152,647 | 360,348 | ||||||

Shares issued in reinvestment of distributions | — | 73,138 | ||||||

Shares redeemed | (59,256 | ) | (220,822 | ) | ||||

Net increase in shares outstanding | 93,391 | 212,664 | ||||||

18 | See accompanying notes which are an integral part of these financial statements. |

BFS Equity Fund

Financial Highlights

(For a share outstanding during each period)

For the Six | For the | For the | For the | For the | For the | |||||||||||||||||||

Selected Per Share Data: | ||||||||||||||||||||||||

Net asset value, beginning of period | $ | 15.40 | $ | 14.96 | $ | 13.01 | $ | 11.55 | $ | 11.69 | $ | 10.73 | ||||||||||||

Income from investment operations: | ||||||||||||||||||||||||

Net investment income | 0.02 | 0.04 | 0.04 | 0.04 | 0.04 | 0.02 | ||||||||||||||||||

Net realized and unrealized gain/(loss) on investments | 2.04 | 0.90 | 1.96 | 1.47 | (0.15 | ) | 0.97 | |||||||||||||||||

Total from investment operations | 2.06 | 0.94 | 2.00 | 1.51 | (0.11 | ) | 0.99 | |||||||||||||||||

Less distributions to shareholders from: | ||||||||||||||||||||||||

Net investment income | — | (0.04 | ) | (0.04 | ) | (0.05 | ) | (0.03 | ) | (0.03 | ) | |||||||||||||

Net realized gains | — | (0.46 | ) | (0.01 | ) | — | — | — | ||||||||||||||||

Total distributions | — | (0.50 | ) | (0.05 | ) | (0.05 | ) | (0.03 | ) | (0.03 | ) | |||||||||||||

Net asset value, end of period | $ | 17.46 | $ | 15.40 | $ | 14.96 | $ | 13.01 | $ | 11.55 | $ | 11.69 | ||||||||||||

Total Return(a) | 13.38 | %(b) | 6.84 | % | 15.36 | % | 13.15 | % | (0.91 | )% | 9.27 | % | ||||||||||||

Ratios and Supplemental Data: | ||||||||||||||||||||||||

Net assets, end of period (000 omitted) | $ | 42,409 | $ | 35,960 | $ | 31,750 | $ | 27,185 | $ | 23,884 | $ | 20,167 | ||||||||||||

Ratio of net expenses to average net assets | 1.25 | %(c) | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | % | ||||||||||||

Ratio of expenses to average net assets before waiver and reimbursement | 1.51 | %(c) | 1.57 | % | 1.65 | % | 1.75 | % | 1.86 | % | 2.26 | % | ||||||||||||

Ratio of net investment income to average net assets | 0.22 | %(c) | 0.28 | % | 0.26 | % | 0.35 | % | 0.43 | % | 0.30 | % | ||||||||||||

Portfolio turnover rate | 12.19 | %(b) | 38.71 | % | 38.17 | % | 47.82 | % | 49.38 | % | 51.17 | % | ||||||||||||

(a) | Total return represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

(b) | Not annualized. |

(c) | Annualized. |

See accompanying notes which are an integral part of these financial statements. | 19 |

BFS Equity Fund

Notes to the Financial Statements (Unaudited)

November 30, 2019

NOTE 1. ORGANIZATION

The BFS Equity Fund (the “Fund”) was organized as an open-end diversified series of Valued Advisers Trust (the “Trust”) on July 23, 2013 and commenced operations on November 8, 2013. The Trust is a management investment company established under the laws of Delaware by an Agreement and Declaration of Trust dated June 13, 2008 (the “Trust Agreement”). The Trust Agreement permits the Board of Trustees (the “Board”) to issue an unlimited number of shares of beneficial interest of separate series without par value. The Fund is one of a series of funds authorized by the Board. The Fund’s investment adviser is Bradley, Foster & Sargent, Inc. (the “Adviser”). The investment objective of the Fund is long-term appreciation through growth of principal and income.

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES

The Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies.” The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. These policies are in conformity with generally accepted accounting principles in the United States of America (“GAAP”).

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

Federal Income Taxes – The Fund makes no provision for federal income or excise tax. The Fund has qualified and intends to qualify each year as a regulated investment company (“RIC”) under subchapter M of the Internal Revenue Code of 1986, as amended, by complying with the requirements applicable to RICs and by distributing substantially all of its taxable income. The Fund also intends to distribute sufficient net investment income and net realized capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains. If the required amount of net investment income or gains is not distributed, the Fund could incur a tax expense.

As of and during the six months ended November 30, 2019, the Fund did not have any liabilities for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense on the statement of operations when incurred. During the six months ended November 30, 2019, the Fund did not incur any interest or penalties. Management of the Fund has reviewed tax positions taken in tax years that remain subject to examination by all major tax jurisdictions, including federal (i.e., the last three tax year ends and the interim tax period since then, as applicable). Management believes that there is no tax liability resulting from unrecognized tax benefits related to uncertain tax positions taken.

20

BFS Equity Fund

Notes to the Financial Statements (Unaudited) (continued)

November 30, 2019

Expenses – Expenses incurred by the Trust that do not relate to a specific fund of the Trust are allocated to the individual funds based on each fund’s relative net assets or another appropriate basis (as determined by the Board).

Security Transactions and Related Income – The Fund follows industry practice and records security transactions on the trade date for financial reporting purposes. The specific identification method is used for determining gains or losses for financial statement and income tax purposes. Dividend income is recorded on the ex-dividend date and interest income is recorded on an accrual basis. Discounts and premiums on securities purchased are accreted or amortized using the effective interest method, if applicable. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

Dividends and Distributions – The Fund intends to distribute its net investment income and net realized long-term and short-term capital gains, if any, at least annually. Dividends and distributions to shareholders, which are determined in accordance with income tax regulations, are recorded on the ex-dividend date. The treatment for financial reporting purposes of distributions made to shareholders during the period from net investment income or net realized capital gains may differ from their ultimate treatment for federal income tax purposes. These differences are caused primarily by differences in the timing of the recognition of certain components of income, expense or realized capital gain for federal income tax purposes. Where such differences are permanent in nature, they are reclassified among the components of net assets based on their ultimate characterization for federal income tax purposes. Any such reclassifications will have no effect on net assets, results of operations or net asset value (“NAV”) per share of the Fund.

Share Valuation – The NAV is calculated each day the New York Stock Exchange is open by dividing the total value of the Fund’s assets, less liabilities, by the number of shares outstanding for the Fund.

NOTE 3. SECURITIES VALUATION AND FAIR VALUE MEASUREMENTS

Fair value is defined as the price that the Fund would receive upon selling an investment in a timely transaction to an independent buyer in the principal or most advantageous market of the investment. GAAP establishes a three-tier hierarchy to maximize the use of observable market data and minimize the use of unobservable inputs and to establish classification of fair value measurements for disclosure purposes.

Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk (the risk inherent in a particular valuation technique used to measure fair value including a pricing model and/or the risk inherent in the inputs to the valuation technique). Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed based on market data obtained and available from sources independent of the reporting entity. Unobservable inputs are inputs that reflect

21

BFS Equity Fund

Notes to the Financial Statements (Unaudited) (continued)

November 30, 2019

the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

● | Level 1 – unadjusted quoted prices in active markets for identical investments and/or registered investment companies where the value per share is determined and published and is the basis for current transactions for identical assets or liabilities at the valuation date |

● | Level 2 – other significant observable inputs (including, but not limited to, quoted prices for an identical security in an inactive market, quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

● | Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining fair value of investments based on the best information available) |

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy which is reported, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

Equity securities that are traded on any stock exchange are generally valued at the last quoted sale price on the security’s primary exchange. Lacking a last sale price, an exchange-traded security is generally valued at its last bid price. Securities traded in the NASDAQ over-the-counter market are generally valued at the NASDAQ Official Closing Price. When using the market quotations and when the market is considered active, the security is classified as a Level 1 security. In the event that market quotations are not readily available or are considered unreliable due to market or other events, the Fund values its securities and other assets at fair value in accordance with policies established by and under the general supervision of the Board. Under these policies, the securities will be classified as Level 2 or 3 within the fair value hierarchy, depending on the inputs used.

Investments in mutual funds, including money market mutual funds, are generally priced at the ending NAV. These securities are categorized as Level 1 securities.

In accordance with the Trust’s valuation policies, the Adviser is required to consider all appropriate factors relevant to the value of securities for which it has determined other pricing sources are not available or reliable as described above. No single method exists for determining fair value, because fair value depends upon the circumstances of each individual case. As a general principle, the current fair value of a security being valued by the Adviser would be the amount that the Fund might reasonably expect to receive upon the current sale. Methods that are in accordance with this principle may, for example, be based on (i) a multiple of earnings; (ii) a discount from market prices of a similar freely traded security (including a derivative security or a basket of securities traded on other markets, exchanges or among dealers); or (iii) yield to maturity with respect to debt

22

BFS Equity Fund

Notes to the Financial Statements (Unaudited) (continued)

November 30, 2019

issues, or a combination of these and other methods. Fair-value pricing is permitted if, in the Adviser’s opinion, the validity of market quotations appears to be questionable based on factors such as evidence of a thin market in the security based on a small number of quotations, a significant event occurs after the close of a market but before the Fund’s NAV calculation that may affect a security’s value, or the Adviser is aware of any other data that calls into question the reliability of market quotations.

The following is a summary of the inputs used to value the Fund’s investments as of November 30, 2019:

Valuation Inputs | ||||||||||||||||

Assets | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Common Stocks(a) | $ | 41,556,709 | $ | — | $ | — | $ | 41,556,709 | ||||||||

Money Market Funds | 848,228 | — | — | 848,228 | ||||||||||||

Total | $ | 42,404,937 | $ | — | $ | — | $ | 42,404,937 | ||||||||

(a) | Refer to Schedule of Investments for industry classifications. |

The Fund did not hold any investments at the end of the reporting period for which significant unobservable inputs (Level 3) were used in determining fair value; therefore, no reconciliation of Level 3 securities is included for this reporting period.

NOTE 4. TRANSACTIONS WITH AFFILIATES AND OTHER SERVICE PROVIDERS

Under the terms of the investment advisory agreement on behalf of the Fund, the Adviser manages the Fund’s investments subject to oversight of the Board. As compensation for its services, the Fund pays the Adviser a fee, computed and accrued daily and paid monthly, at an annual rate of 0.75% of the average daily net assets of the Fund. For the six months ended November 30, 2019, the Adviser earned a fee of $149,541 from the Fund before the waivers described below. At November 30, 2019, the Fund owed the Adviser $17,179.

The Adviser has contractually agreed to waive its management fee and/or reimburse certain operating expenses until September 30, 2020, but only to the extent necessary so that the Fund’s net expenses, excluding brokerage fees and commissions, borrowing costs (such as interest and dividend expenses on securities sold short), taxes, extraordinary expenses, fees and expenses paid under a distribution plan adopted pursuant to Rule 12b-1, fees and expenses paid under a shareholder services plan, and indirect expenses (such as “acquired funds fees and expenses”) do not exceed 1.00%.

Each waiver or reimbursement of an expense by the Adviser is subject to repayment by the Fund within the three years following such waiver or reimbursement, provided that the Fund is able to make the repayment without exceeding the expense limitation in place at the time of the waiver or reimbursement and the expense limitation in place at the time of the repayment. The contractual agreement is in effect through September 30, 2020.

23

BFS Equity Fund

Notes to the Financial Statements (Unaudited) (continued)

November 30, 2019

The expense cap may not be terminated prior to this date except by mutual consent of the Adviser and the Board. For the six months ended November 30, 2019, the Adviser waived fees of $52,581.

The amounts subject to repayment by the Funds, pursuant to the aforementioned conditions, are as follows:

Recoverable through | ||||

May 31, 2020 | $ | 57,961 | ||

May 31, 2021 | 117,155 | |||

May 31, 2022 | 110,755 | |||

November 30, 2022 | 52,581 |

The Trust retains Ultimus Fund Solutions, LLC (“Ultimus” or “Administrator”) to provide the Fund with administration and compliance (including a chief compliance officer), fund accounting, and transfer agent services, including all regulatory reporting. For the six months ended November 30, 2019, the Administrator earned fees of $19,000 for administration and compliance services, $12,500 for fund accounting services and $9,000 for transfer agent services. At November 30, 2019, the Fund owed the Administrator $6,751 for such services.

The officers and one trustee of the Trust are members of management and/or employees of the Administrator. Ultimus Fund Distributors, LLC (the “Distributor”), a wholly-owned subsidiary of Ultimus, acts as the distributor of the Fund’s shares.

The Fund has adopted a Distribution Plan (the “Plan”) pursuant to Rule 12b-1 under the Investment Company Act of 1940 (the “1940 Act”). The Plan provides that the Fund will pay the Distributor and/or any registered securities dealer, financial institution or any other person (the “Recipient”) a shareholder servicing fee of 0.25% of the average daily net assets of the Fund in connection with the promotion and distribution of the Fund’s shares or the provision of shareholder support services to shareholders, including, but not necessarily limited to, advertising, compensation to underwriters, dealers and selling personnel, the printing and mailing of prospectuses to other than current Fund shareholders, the printing and mailing of sales literature and servicing shareholder accounts (“12b-1 fees”). The Fund or Distributor may pay all or a portion of these fees to any Recipient who renders assistance in distributing or promoting the sale of shares, or who provides certain shareholder services, pursuant to a written agreement. For the six months ended November 30, 2019, 12b-1 fees incurred by the Fund were $49,847. The Fund owed $17,106 for 12b-1 fees as of November 30, 2019.

NOTE 5. PURCHASES AND SALES OF SECURITIES

For the six months ended November 30, 2019, purchases and sales of investment securities, other than short-term investments, were $7,107,035 and $4,714,978, respectively.

There were no purchases or sales of long-term U.S. government obligations during the six months ended November 30, 2019.

24

BFS Equity Fund

Notes to the Financial Statements (Unaudited) (continued)

November 30, 2019

NOTE 6. FEDERAL TAX INFORMATION

At November 30, 2019, the net unrealized appreciation (depreciation) of investments for tax purposes was as follows:

Gross unrealized appreciation | $ | 14,167,365 | ||

Gross unrealized depreciation | (21,241 | ) | ||

Net unrealized appreciation on investments | $ | 14,146,124 | ||

Tax cost of investments | $ | 28,258,813 |

At November 30, 2019, the difference between book basis and tax basis unrealized appreciation (depreciation) is attributable to the tax deferral of losses on wash sales.

The tax character of distributions paid for the fiscal year ended May 31, 2019, the Fund’s most recent fiscal year end, was as follows:

Distributions paid from: | ||||

Ordinary income(a) | $ | 83,219 | ||

Long-term capital gains | 1,030,144 | |||

Total distributions paid | $ | 1,113,363 |

(a) | For federal income tax purposes, distributions of short-term capital gains are treated as ordinary income distributions. |

At May 31, 2019, the components of accumulated earnings (accumulated losses) on a tax basis were as follows:

Undistributed ordinary income | $ | 39,481 | ||

Undistributed long-term capital gains | 420,579 | |||

Unrealized appreciation on investments | 9,569,901 | |||

Total | $ | 10,029,961 |

NOTE 7. COMMITMENTS AND CONTINGENCIES

The Trust indemnifies its officers and Trustees for certain liabilities that may arise from their performance of their duties to the Trust or the Fund. Additionally, in the normal course of business, the Trust enters into contracts that contain a variety of representations and warranties which provide general indemnifications. The Trust’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Trust that have not yet occurred.

25

BFS Equity Fund

Notes to the Financial Statements (Unaudited) (continued)

November 30, 2019

NOTE 8. SUBSEQUENT EVENTS

Effective December 31, 2019, the Fund’s principal underwriter and distributor, Unified Financial Securities, LLC, (“Unified”) merged with and into Ultimus Fund Distributors, LLC (“UFD”). On that date, the distribution agreement pursuant to which Unified served as the principal underwriter of the Fund automatically terminated and was, with the Board’s approval, replaced with a new distribution agreement on substantially the same terms, except that UFD is the new principal underwriter.

Management of the Fund has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date at which these financial statements were issued. Based upon this evaluation, management has determined there were no additional items requiring adjustment of the financial statements or additional disclosure.

26

BFS Equity Fund

Summary of Fund Expenses (Unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction and (2) ongoing costs, including management fees and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from June 1, 2019 through November 30, 2019.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the second line of the table below is useful in comparing ongoing costs only and will not help you determine the relative costs of owning different funds. In addition, if transaction costs were included, your costs would have been higher.

Beginning | Ending | Expenses Paid | Annualized | |

Actual | $1,000.00 | $1,133.80 | $ 6.67 | 1.25% |

Hypothetical(b) | $1,000.00 | $1,018.82 | $ 6.31 | 1.25% |

(a) | Expenses are equal to the Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

(b) | Hypothetical assumes 5% annual return before expenses. |

27

BFS Equity Fund

Investment Advisory Agreement Approval

(Unaudited)

At a meeting held on June 5-6, 2019, the Board of Trustees (the “Board”) considered the renewal of the Investment Advisory Agreement (the “BFS Agreement”) between Valued Advisers Trust (the “Trust”) and Bradley, Foster & Sargent, Inc. (“BFS”) with respect to the BFS Equity Fund (the “Fund”). BFS provided written information to the Board to assist the Board in its considerations.

Counsel reminded the Trustees of their fiduciary duties and responsibilities as summarized in a memorandum from his firm, including the factors to be considered, and the application of those factors to BFS. In assessing the factors and reaching its decision, the Board took into consideration information furnished by BFS and the Trust’s other service providers for the Board’s review and consideration throughout the year, as well as information specifically prepared or presented in connection with the annual renewal process, including: (i) reports regarding the services and support provided to the Fund and its shareholders by BFS; (ii) quarterly assessments of the investment performance of the Fund by personnel of BFS; (iii) commentary on the reasons for the performance; (iv) presentations by BFS addressing its investment philosophy, investment strategy, personnel, and operations; (v) compliance and audit reports concerning the Fund and BFS; (vi) disclosure information contained in the registration statement of the Trust and the Form ADV of BFS; and (vii) a memorandum from trust counsel, that summarized the fiduciary duties and responsibilities of the Board in reviewing and approving the BFS Agreement. The Board also requested and received materials including, without limitation: (a) documents containing information about BFS, including its financial information; a description of its personnel and the services it provides to the Fund; information on BFS’ investment advice and performance; summaries of the Fund’s expenses, compliance program, current legal matters, and other general information; (b) comparative expense and performance information for other mutual funds with strategies similar to the Fund; and (c) the benefits to be realized by BFS from its relationship with the Fund. The Board did not identify any particular information that was most relevant to its consideration of the BFS Agreement, and each Trustee may have afforded different weight to the various factors.

1. | The nature, extent, and quality of the services to be provided by BFS. The Board considered BFS’s responsibilities under the BFS Agreement. The Trustees considered the services being provided by BFS to the Fund including, without limitation: the quality of its investment advisory services (including research and recommendations with respect to portfolio securities), its process for formulating investment recommendations and assuring compliance with the Fund’s investment objectives and limitations, its coordination of services for the Fund among the Fund’s service providers, and its efforts to promote the Fund and grow its assets. The Trustees considered BFS’s continuity of, and commitment to retain qualified personnel, commitment to maintain and enhance its resources and systems, and options that allow the Fund to maintain its goals, and BFS’s continued cooperation with the Board and counsel for the Fund. The Trustees considered BFS’s personnel, including their education and experience. After considering the foregoing information and |

28

BFS Equity Fund

Investment Advisory Agreement Approval (Unaudited)(continued)

further information in the Meeting materials provided by BFS, the Board concluded that, in light of all the facts and circumstances, the nature, extent, and quality of the services provided by BFS were satisfactory and adequate for the Fund.

2. | Investment Performance of the Fund and BFS. The Trustees compared the performance of the Fund with the performance of funds with similar objectives managed by other investment advisers, with aggregated peer group data, as well as with the performance of the Fund’s benchmark. The Trustees also considered the consistency of BFS’s management of the Fund with its investment objectives, strategies, and limitations. The Trustees noted that the Fund had outperformed as compared to its benchmark for the year-to-date and one-year periods ended March 31, 2019, but underperformed the benchmark for the three-year, five-year, and since inception periods ended on that date. They also noted that the Fund had outperformed as compared to its Morningstar category for the one-month and one-year periods ended March 31, 2019, but had underperformed for the three-month, three-year and five year periods. With regard to the custom peer group, the Trustees noted that the Fund had outperformed as compared to the average and median for the one-month, three-month, and one-year periods ended March 31, 2019, and had underperformed for the three-year period. With regard to the five-year period, the Trustees noted that the Fund had outperformed as compared to the average, but underperformed as compared to the median. The Board reviewed the performance of BFS in managing a composite with investment strategies similar to that of the Fund and observed that the Fund’s performance was above the composite for the year-to-date period ended March 31, 2019, and below the composite for the calendar year 2018. The Trustees took into consideration discussions with representatives of BFS regarding the reasons for the performance of the Fund. After further reviewing and discussing these and other relevant factors, the Board concluded, in light of all the facts and circumstances, that the investment performance of the Fund and BFS was satisfactory. |

3. | The costs of the services to be provided and profits to be realized by BFS from the relationship with the Fund. The Trustees considered: (1) BFS’s financial condition; (2) the asset level of the Fund; (3) the overall expenses of the Fund; and (4) the nature and frequency of management fee payments. The Trustees reviewed information provided by BFS regarding its profits associated with managing the Fund, noting that BFS is currently waiving a large portion of its management fee. The Trustees also considered potential benefits for BFS in managing the Fund. The Trustees then compared the fees and expenses of the Fund (including the management fee) to other comparable mutual funds. The Trustees noted that the Fund’s management fee was above the average and median management fees of its Morningstar category. The Trustees also noted that the Fund’s net expense ratio was also above that of the average and median of its category, taking into consideration BFS’s contractual commitment to limit the expenses of the Fund. When comparing the Fund’s fees to those of its custom peer group, the Trustees noted that the Fund’s management |

29

BFS Equity Fund

Investment Advisory Agreement Approval (Unaudited)(continued)

fee was below the average and equal to the median. They also noted that the Fund’s net expense ratio was slightly above both the average and median of the peer group. Based on the foregoing, the Board concluded that the fees to be paid to BFS by the Fund and the profits to be realized by BFS, in light of all the facts and circumstances, were fair and reasonable in relation to the nature and quality of the services provided by BFS.

4. | The extent to which economies of scale would be realized as the Fund grows and whether advisory fee levels reflect these economies of scale for the benefit of the Fund’s investors. The Board considered the Fund’s fee arrangements with BFS. The Board considered that while the management fee remained the same at all asset levels, the Fund’s shareholders experienced benefits from the Fund’s expense limitation arrangement. The Trustees noted that once the Fund’s expenses fell below the cap set by the arrangement, the shareholders would continue to benefit from economies of scale under the Fund’s arrangements with other service providers to the Fund, and the Trustees attributed this benefit, in part, to the direct and indirect efforts of BFS at the inception of the Fund to ensure that a cost structure was in place that was beneficial for the Fund as it grew. In light of its ongoing consideration of the Fund’s asset and fees levels and expectations for growth, the Board determined that the Fund’s fee arrangements, in light of all the facts and circumstances, were fair and reasonable in relation to the nature and quality of the services provided by BFS. |

5. | Possible conflicts of interest and benefits to BFS. In considering BFS’s practices regarding conflicts of interest, the Trustees evaluated the potential for conflicts of interest and considered such matters as the experience and ability of the advisory personnel assigned to the Fund; the basis of decisions to buy or sell securities for the Fund and/or BFS’s other accounts; and the substance and administration of BFS’s code of ethics. The Trustees also considered disclosure in the registration statement of the Trust relating to BFS’s potential conflicts of interest. The Trustees noted that BFS may utilize soft dollars and the Trustees noted BFS’s policies and processes for managing the conflicts of interest that could arise from soft dollar arrangements. The Trustees noted other potential benefits to BFS, including the fact that the Fund provides an attractive vehicle for smaller accounts, which may increase the total assets under management by BFS. Based on the foregoing, the Board determined that the standards and practices of BFS relating to the identification and mitigation of potential conflicts of interest and the benefits to be realized by BFS in managing the Fund were satisfactory. |

After additional consideration of the factors delineated in the memorandum provided by counsel and further discussion among the Board members, the Board determined to approve the continuation of the BFS Agreement.

30

FACTS | WHAT DOES BFS EQUITY FUND (THE “FUND”) DO WITH YOUR PERSONAL INFORMATION? | |

Why? | Financial companies choose how they share your personal information. Federal law gives consumers the right to limit some but not all sharing. Federal law also requires us to tell you how we collect, share, and protect your personal information. Please read this notice carefully to understand what we do. | |

What? | The types of personal information we collect and share depend on the product or service you have with us. This information can include:

■ Social Security number ■ account balances and account transactions ■ transaction or loss history and purchase history ■ checking account information and wire transfer instructions When you are no longer our customer, we continue to share your information as described in this notice. | |

How? | All financial companies need to share customers’ personal information to run their everyday business. In the section below, we list the reasons financial companies can share their customers’ personal information; the reasons the Fund chooses to share; and whether you can limit this sharing. | |

Reasons we can share your personal information | Does the Fund share? | |

For our everyday business purposes — | Yes | |

For our marketing purposes — | No | |

For joint marketing with other financial companies | No | |

For our affiliates’ everyday business purposes – | No | |

For our affiliates’ everyday business purposes – | No | |

For nonaffiliates to market to you | No | |

Questions? | Call (855) 575-2430 | |

31

Who we are | |

Who is providing this notice? | BFS Equity Fund |

What we do | |

How does the Fund protect my personal information? | To protect your personal information from unauthorized access and use, we use security measures that comply with federal law. These measures include computer safeguards and secured files and buildings. Our service providers are held accountable for adhering to strict policies and procedures to prevent any misuse of your nonpublic personal information. |

How does the Fund collect my personal information? | We collect your personal information, for example, when you

■ open an account or deposit money ■ buy securities from us or sell securities to us ■ make deposits or withdrawals from your account ■ give us your account information ■ make a wire transfer ■ tell us who receives the money ■ tell us where to send the money ■ show your government-issued ID ■ show your driver’s license |

Why can’t I limit all sharing? | Federal law gives you the right to limit only

■ sharing for affiliates’ everyday business purposes — information about your creditworthiness ■ affiliates from using your information to market to you ■ sharing for nonaffiliates to market to you State laws and individual companies may give you additional rights to limit sharing. |

Definitions | |

Affiliates | Companies related by common ownership or control. They can be financial and nonfinancial companies.

■ Bradley, Foster & Sargent, Inc, the investment adviser to the Fund, could be deemed to be an affiliate. |

Nonaffiliates | Companies not related by common ownership or control. They can be financial and nonfinancial companies.

■ The Fund does not share your personal information with nonaffiliates so they can market to you. |

Joint marketing | A formal agreement between nonaffiliated financial companies that together market financial products or services to you.

■ The Fund doesn’t jointly market. |

32

This page is intentionally left blank.

Proxy Voting

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities and information regarding how the Fund voted those proxies during the most recent twelve month period ended June 30, are available (1) without charge upon request by calling the Fund at (855) 575-2430 and (2) in Fund documents filed with the Securities and Exchange Commission (“SEC”) on the SEC’s website at www.sec.gov.

TRUSTEES

Andrea N. Mullins, Chairperson

Ira P. Cohen

Mark J. Seger

OFFICERS

Adam T. Kornegay, Principal Executive Officer and President

Gregory T. Knoth, Principal Financial Officer and Treasurer

Martin R. Dean, Interim Chief Compliance Officer

Carol J. Highsmith, Vice President and Secretary

INVESTMENT ADVISER

Bradley, Foster & Sargent, Inc.

185 Asylum Street, City Place II

Hartford, CT 06103

DISTRIBUTOR

Ultimus Fund Distributors, LLC

225 Pictoria Drive, Suite 450