Exhibit 99.2

![]()

POET

TECHNOLOGIES INC.

Management’s Discussion

and Analysis

For the Three and Six Months Ended June 30, 2016

POET Technologies Inc. Suite 1107 – 120 Eglinton Avenue East Toronto, Ontario, Canada M4P 1E2 Tel: (416) 368-9411 Fax: (416) 322-5075 |

Management’s Discussion and Analysis

For Six Months Ended June 30, 2016

The following discussion and analysis of the operations, results, and financial position of POET Technologies Inc., (the “Company”) for the six months ended June 30, 2016 (the “Period”) should be read in conjunction with the Company’s condensed unaudited consolidated financial statements for the period ended June 30, 2016 and the Company’s audited consolidated financial statements for the year ended December 31, 2015 and the related notes thereto where applicable both of which were prepared in accordance with International Financial Reporting Standards (“IFRS”). The effective date of this report is August 29, 2016. All financial figures are in United States dollars (“USD”) unless otherwise indicated. The abbreviation “U.S.” used throughout refers to the United States of America.

Forward-Looking Statements

This management discussion and analysis contains forward-looking statements that involve risks and uncertainties. It uses words such as “may”, “would”, “could”, “will”, “likely”, “expect”, “anticipate”, “believe”, “intend”, “plan”, “forecast”, “project”, “estimate”, and other similar expressions to identify forward-looking statements. Forward-looking statements are subject to a variety of risks and uncertainties which could cause actual events or results to differ from those reflected in the forward-looking statements, including, without limitation, risks and uncertainties relating to the early stage of the Company’s development and the possibility that future development of the Company’s technology and business will not be consistent with management’s expectations, difficulties in achieving commercial production or interruptions in such production if achieved, the inherent uncertainty of cost estimates and the potential for unexpected costs and expenses, the uncertainty of profitability and failure to obtain adequate financing on a timely basis. The Company undertakes no obligation to update forward-looking statements if circumstances or Management’s estimates or opinions should change, except to the extent required by law. The reader is cautioned not to place undue reliance on forward-looking statements.

Business Overview

A Second Wave of Growth

Electronics is pervasive in everything we do – at work, at home and on the move. Its ubiquitous presence has been enabled by decades of improvements and enhancements in fundamental semiconductor technologies, which has resulted in smaller, faster and more power efficient devices.

The tangible impact of these enhancements is the ongoing mobility revolution and the explosion in the use of SaaS (Software as a Service) – this manifests itself in the form of “apps” on the cell phone, but drives the need for significant background computations, typically carried out in the “cloud”. Social Networking, Cloud Computing, Internet of Things and the growth of mega-data centers are galvanizing a renewed spurt of growth in photonics.Photonics is the science of light (photon) generation, detection, and manipulation. The word 'photonics' is derived from the Greek word "photos" meaning light; it appeared in the late 1960s to describe a research field whose goal was to use light to perform functions that traditionally fell within the typical domain of electronics (where electrons are primarily used to perform all necessary functions). Investments by Web2.0 companies in mega-data centers and supporting networking infrastructure have created a new and very dynamic segment in the optical components and modules market.

Accordingly, photonics is experiencing a post-telecom second wave of growth – this one, fueled by consumers engaged in always-on social networking, cloud computing, SaAS and the ubiquitous devices that are central to our lives. Thus, progress in the electronics, optics and the semiconductor industry continues to heavily influence and be influenced by day-to-day life – in the way we work, communicate and entertain ourselves. From the most sophisticated extreme-environment satellite applications to the most everyday consumer appliances, the world is increasingly dependent on optical components.

Breaking Through The Bottleneck

Anyone who follows the semiconductor industry is aware of Moore’s Law, which was an observation made by Gordon Moore, the co-founder of Intel and Fairchild Semiconductor, in a 1965 paper that described a doubling every year in the number of components that could be put on an integrated circuit. Approximately a decade later, Moore’s observation of doubling was revised to every two years.

The benefit has been in the form of faster, cheaper and more powerful computers, mobile devices and the other electronics that dominate our daily lives. The integrated circuits that are at the heart of computers and mobile devices are based on silicon as the substrate for wafers and copper to connect all the components together and transfer data. Any processing solution requires two fundamental functions – computation and communication. Computational efficiencies are addressed with Moore’s Law advances in silicon technologies. However, communications, and more specifically high bandwidth data communications, are increasingly challenged with traditional copper interconnects. For decades, evolutionary advancements were able to keep Moore’s Law intact, but the combination of silicon and copper are now pushing the practical limits on diminishing returns.

Enter “More than Moore”. For some time now, alternate technologies based on Silicon and other materials have augmented silicon chips and solutions to continue to provide functionality scaling.Optical technologies are now entering the realm of “More than Moore” technologies with a promise to unlock the interconnect bottlenecks that are increasingly impacting scaled silicon technologies.Copper interconnects, both on chip and off chip, become extremely power hungry at high speeds and threaten to subvert the benefits of Moore’s Law scaling. Today, a revolution is needed in how components on the chip transfer data. New optical solutions are being sought to address these shortcomings.IntegratedPhotonics is one such technology that can augment the capabilities of existing silicon technology and can enable functional integration even in the absence of traditional Moore’s Law scaling.

Cost and power reductions in the world of silicon have been driven by “integration” – or the ability to put multiple functions on a single chip. In order to become a pervasive technology, the world of optics likewise requires an “integration approach” to break the traditional barriers of cost and scalability, as packaging is often one of the most expensive aspects of optoelectronic solutions. Currently, there have been few technologies that have demonstrated the capability to cost effectively integrate multiple optical functions on a single chip.

With the vision of becoming a global leader in Integrated Photonics solutions by deploying innovations in optical and optoelectronic integration, the Company developed a unique, proprietary process that addresses the deficiencies of size, integration, power and cost efficiency associated with current optoelectronic semiconductor manufacturing technologies to enable functional optical integration monolithically at the wafer scale. The novel process can be accommodated in existing semiconductor fabs with minimum re-tooling, thus potentially reducing capital expenditures required to adopt POET’s process technologies. This integrated solution, which has previously been unavailable in optoelectronics enables cheaper, smaller and more energy efficient solutions.

Going to Market

The company is driving current development and growth around three verticals – Data Communications, Sensing and Displays. The company is also accelerating the evaluation of its technology beyond VCSEL based data communications through potential partnerships and joint development programs, while maintaining its operational focus on Data Communications.

For each of its markets, POET continues to develop its unrivaled optoelectronic device and process platform that enables low power, minimized size and component cost for smart optical components. POET’s goal in data communications is to provide data management at the speed of light and the cost of copper.

Data Centers: The Pain Point of POWER

The multi-billion-dollar Data Communications market is a current focus for POET. Data centers are encountering an excruciating pain point in terms of power. Energy management costs are already a significant fraction of the cost of operating a data center today. For data centers, power has become critically important. Historically, the way to solve power problems is integrating multiple components monolithically on a single chip — in short, what has driven silicon technology for years. Now the optics world is primed for a similar transition to integrated solutions. POET offers the only integrated process technology platform with gallium arsenide and optics. Critically, POET’s solution uniquely attacks the cost equation at the component level, the wafer-scale-packaging level and at the wafer-scale-test level – which translates into an overall cost that becomes competitive with copper technology. This is the key to the performance of optics at the price of copper. Other ancillary benefits of optics are lower weight, higher flexibility, smaller size and less electro-magnetic interference – all of which become significant pain points in high-density installations.

Expanded Technology and Product Portfolio

The recent acquisitions of DenseLight Semiconductor Pte. Ltd. (“DenseLight”) and BB Photonics have expanded the Company’s use of III-V based processes from GaAs to now include InP. Through these acquisitions, the Company now designs, manufactures, and delivers leading photonic optical light source products and solutions to the communications, medical, instrumentations and industrial industries. POET Technologies now has the capability to process Indium Phosphide (InP) and Gallium Arsenide (GaAs) based optoelectronic devices and photonic integrated circuits through its in-house wafer fabrication and assembly & test facilities. DenseLight is recognized worldwide for its technological innovations in high performance semiconductor infrared super-luminescent light sources and lasers, with a proven track record in deployed applications. Together with these recent acquisitions, POET Technologies has further advanced its platform approach to the integration of photonic functions. This approach can be applied across a range of material systems to enable both routing and Optical/Electronic (“O/E”) conversion, and the technology is applicable to wavelength multiplexing and de-multiplexing as well as signal routing in both vertical and horizontal directions.

Areas of expertise include:

| o | Vertical Cavity and Edge Emitting Lasers in the wavelength range from 850nm to 1610nm |

| o | Super-luminescent Light Emitting Diodes for Sensing Products in the fields of Test and Measurement, Navigation devices such as Fiber Optic Gyroscopes, Structural Health Monitoring such as LIDAR and Medical Applications (Optical Coherence Tomography) |

| o | High speed RF devices and characterization |

| o | High speed data communications component design and manufacturing |

| o | Up to 6-inch III-V wafer processing, process requirements, equipment |

Company Products

The company’s product portfolio and roadmap are now focused on:

| o | Broadband Super-Luminescent LEDs (Light Emitting Diodes) |

| o | Narrow Linewidth Lasers |

| o | DFB (Distributed Feedback) Lasers for Data Communications |

| o | VCSELs (Vertical Cavity Surface Emitting Lasers) and VCSEL based Transceivers |

| o | 100Gbs ROSA (Receiver Optical Sub-Assemblies) and TOSA (Transmitter Optical Sub-Assemblies) for 100G Transceivers |

| o | High Power ELEDs (Edge Emitting Light Emitting Diodes) |

| o | CWDM (Coarse Wavelength Division Multiplexing) Laser Arrays |

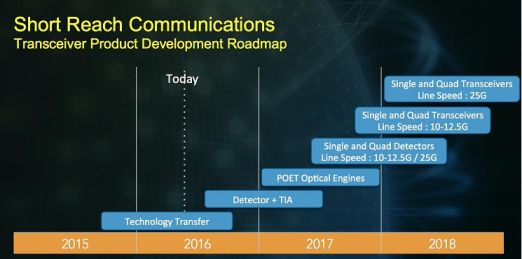

The exhibits below show the Company’s product development and roadmaps:

The company is also enabling an expanded photonic sensing roadmap with target applications shown in the figure below.

Fabrication and Assembly Capabilities

POET Technologies provides one-stop design and manufacturing solutions, from photonics design and simulation, epitaxial growth, wafer fabrication, chip production, in-line optical coating, sub-mounting, photonic measurements, product tests and screening.

POET Technologies is operationally ready for responsive prototyping and quality production. The 50,000 sq. ft. purpose-built facility in Singapore houses its R&D, product design and manufacturing operations under one roof. Its 15,000 sq. ft. clean room is fully equipped for enabling vertically integrated volume manufacturing, from wafer fabrication to test and packaging.

The Company has an experienced team with deep know-how in GaAs and InP semiconductors wafer processing. Together with its operationally ready manufacturing and photonics design center, various ODM and design-in programs can be supported for both discrete and integrated optical components.

Intellectual Property and Know-How

The Company has a number of issued patents and patents pending related to the semiconductor Planar Opto-Electronic Technology (“POET”). Currently, the Company is working on the design of III-V semiconductor devices, processes, and products for data communication applications in the consumer, data center and high performance computing segments. The POET platform could enable applications in adjacent markets, including industrial and consumer mobility.

The Company is incorporated under the laws of the Province of Ontario. The Company’s shares trade under the symbol “PTK” on the TSX Venture Exchange in Canada and under the symbol “POETF” on the OTCQX in the U.S.

The following sections discuss its business in more detail.

The POET Semiconductor Technology Process IP

Prior to the recent acquisitions and since, POET has been focused on a new process for making devices using gallium arsenide as the substrate for wafers instead of silicon. Gallium arsenide has a number of advantages over silicon, including faster speeds and lower energy consumption. But for POET, the real driver is the fact that gallium arsenide is the preeminent substrate for integrating electronics and optics onto a chip, predominantly for short reach applications. Optical connections are much faster and more efficient than copper for transferring data within and to/from a chip.

The disruptive potential of the POET technology was first recognized within the military community, and this recognition has remained strong. Applications in this market include infra-red sensor arrays and high frequency RF Monolithic Microwave Integrated Circuits ("MMIC's"). The Company today is conducting research and development related to expansion of the POET platform by adding processes to the POET IP portfolio. It is also engaged in developmental work related to existing POET processes for data communications applications in potential consumer, data center, high performance computing, and industrial markets. The Company continues to develop gallium arsenide-based processes having several potential applications, including: (i) infrared sensor arrays for defense as well as domestic monitoring and imaging applications, (ii) the unique combination of analog, mixed-signal, digital and optical functions on a single chip for use in high volume short reach and very short reach data communication transceivers and (iii) exploring the use of POET’s unique VCSEL technology as smart pixels for augmented reality display applications. The Company believes that the POET process has the potential to fundamentally alter the landscape of optical data communications for a broad range of applications by offering unique integrated optical and electronic components with dramatically lower solutions cost, as well as increased density, reliability and lower power consumption. With the development of the POET process, the Company:

| · | Has successfully produced numerous distinct devices, including on-chip continuous-wave lasers and switching lasers with the potential for eliminating chip-to-chip metallic interconnects, complementary hetero-structure field effect transistors (HFETs), optical thyristors, and resonant cavity detectors. |

| · | Is utilizing Synopsys’ and Coventor’s tools and services to help develop POET Process Design Kits (PDKs) with an initial focus on the components essential for the design of monolithically integrated VCSEL based optical transceivers. PDKs comprise a library of design rules and parameters for POET’s technology that can eventually enable the Company and its partners to implement the POET fabrication process into their preferred products. |

| · | Is continuing to consider foundry relationships with commercial pure-play 6” foundry suppliers. In 2015, the Company signed a VCSEL Manufacturing Services agreement for early prototyping and initial development and long term manufacturing with Wavetek Microelectronics Corporation (“Wavetek”). Wavetek, which is a wholly owned subsidiary of United Microelectronics Corporation (“UMC”), is a pure-play semiconductor foundry based in Taiwan. In addition, the Company has signed an epitaxial wafer supply agreement with Epiworks Inc. (“Epiworks”), which is a leading provider of MOCVD wafers to the electronics and optical industry. These relationships are helping to accelerate the “Lab-to-Fab” transition of the POET technology to a 6" wafer scale. These engagements will provide the baseline process flow in a manufacturing environment and lead to the demonstration of product prototypes. |

| · | Has successfully validated POET’s process technology transfer to a high volume production foundry facility. |

| · | Has demonstrated resonant cavity detector performance that exceeds the performance of detectors currently in the market. |

| · | Has achieved its first demonstration of functional Hetero-junction Field Effect Transistors (HFETs) down to 250nm effective gate lengths on the same proprietary epitaxy and utilizing the same integrated process sequence that was previously used to demonstrate high performance detectors. This milestone is the latest in POET’s initiative to integrate a detector, HFET and laser together into a single chip, the three key components of an active optical cable, a current market target for POET. |

With an immediate view to commercializing the POET platform, the management team is focused on exploiting existing high growth markets where the disruptive value of POET’s intellectual property provides sustained competitive differentiation.

DenseLight

The Company recently completed the acquisition of DenseLight Semiconductor Pte. Ltd. (“DenseLight”) on May 11, 2016. The DenseLight subsidiary operates an ISO9001 certified fab facility in Singapore, which designs, manufactures, and sells leading photonic optical light source products and solutions to the communications, medical, instrumentations, industrial, defense, and security industries. DenseLight processes Indium Phosphide (InP) and Gallium Arsenide (GaAs) based optoelectronic devices and photonic integrated circuits through its in-house wafer fabrication and assembly & test facilities. Indium Phosphide is the pre-eminent substrate for manufacturing optical components that support long wavelength (long reach) applications. This addition to POET’s existing GaAs capabilities – required for long reach communications – significantly expands POET’s Served Addressable Market (SAM).

The DenseLight acquisition was a significant step in the POET progression as the transaction provided a fabrication facility, provided a group of products with customers, and could potentially accelerate the introduction of future POET devices. The acquisition also provided POET with established distribution and sales channels, which can be leveraged as POET commercializes a growing product portfolio.

The acquisition provides POET with immediate revenue and a path to growing the business through a more differentiated product roadmap. It provides the Company with an entry into Indium Phosphide (InP) based solutions which in turn enables the Company to address the entire Data Center market and not just the market served with short wavelengths lasers possible with Gallium Arsenide (GaAs). The acquisitions allow the Company to engage prospective customers with an extensive suite of integrated photonics products, thereby enabling multiple differentiated product sales and enhancing potential revenue.

Finally, the acquisition of DenseLight also provided POET with the means to receive an offer of support from the Economic Development Board (“EDB”) of Singapore to grow its R&D operations in Singapore. This significant support from the EDB will bring among other benefits, significant incentives to POET and its subsidiaries, DenseLight and BB Photonics, to reduce overall operating costs and to accelerate the Company’s growth through combined operations in Singapore. POET expects to gain meaningful leverage from Singapore-based research and development efficiencies, infrastructure, learning institutions, human capital, and strong high-technology manufacturing.

BB Photonics

BB Photonics develops photonic integrated components for the data center market utilizing embedded dielectric technology that is intended to enable on-chip athermal wavelength control and lower the total solution cost of data center photonic integrated circuits. This strategic acquisition was designed to provide POET with additional differentiated intellectual property and know-how for further product development targeted at the end-to-end data communications market.

Through the acquisition of BB Photonics, POET now has the potential to develop photonic integrated components for high speed data networks using POET’s platform approach. This technology platform can then be applied across a range of material systems to have the potential to enable both routing and O/E conversion. The technology is applicable to wavelength multiplexing and de-multiplexing as well as signal routing in both vertical and horizontal directions. The initial device application for the platform is photonic integrated circuit for the 100Gbit ethernet market, with photonic integration with the potential to enable lower cost, higher speed and smaller footprint for 100G transceivers.

The acquisition of BB Photonics is expected to accelerate the introduction of POET’s first 100Gbps products. More specifically, the company expects to offer 25Gbps receiver solutions in 2017.

Market Strategy

Social networking, Mobile, Analytics and Cloud Computing (“SMAC”) are driving a continuous need for improvements in bandwidth and data handling capacity. This has driven and continues to drive significant growth in data centers. The cloud data center traffic growth is over 25%[1] compound annual growth rate (“CAGR “) and is expected to continue to grow at this rate for the next few years. Power consumption in Data Centers has now become a significant issue. There is a need to proliferate low power computing and communications technology in the data centers – and enable the conversion of the power hungry copper based communication links to fiber optics.

We believe that our POET platform technology is applicable to a large portion of the optoelectronic semiconductor market as it represents an integrated comprehensive solution to increasing the performance potential of semiconductors in an economical and functional manner. The technology may particularly be capable of addressing the power challenges currently faced in data centers. POET may provide the potential for revolutionary innovation that enables it to manage more data at the performance of light but at competitive cost points of copper. Based on the Company’s interactions with potential customers, POET may provide significant value in applications where it addresses the need for lower power consumption, solution size, and cost efficiency.

Data centers today are enduring an excruciating pain point in terms of power. Energy management costs for US data centers alone had approached US$9 billion in 2013 according to the National Resources Defense Council and are forecast to rise to $13.7 Billion by 2020. Each watt of heat that does not have to be rejected from the rack could be worth savings in outright direct energy but also in indirect energy related to cooling costs. A single copper direct attach cable consumes about 3W of power per end. For example a single mega-data center with between 10,000-100,000 servers has a rough estimate of potentially 100,000 copper links. If you can save 5W of power per copper link used in this one data center, this can easily translate into 500 Kilowatts of saved energy translating into significant savings in operating expenses for a single mega data center. We believe data communications are primed for an integrated optoelectronic device and process platform that can enable low power, minimized size and component cost. This is the first opportunity that POET is targeting to address, with its patented process that integrates digital, high-speed analog and optical devices on the same chip. We believe that the process can enable managing data at the speed of light and the cost of copper.

The POET platform may provide the following advantages to the industry:

| · | Up to 10X power savings improvement over existing copper technologies (especially for high speed data communication links) |

| · | Up to 5X cost improvement over existing optical component solutions |

| · | Performance and Power of optical solutions at the price points competitive to that of copper, thus potentially accelerating a transition to optical communications from cumbersome copper links |

| · | Flexible and integrated solution that can be applied to virtually any technical application that commands an optical IO for high bandwidth, including chip to chip communications, on-board optics and on-chip optical communications |

The Company’s strategy is to complete development of its VCSEL based integrated optical platform and monetize this technology with a mix of product and licensing revenue, while continuing research towards the expansion of the IP portfolio.

With the acquisition of DenseLight and BB photonics, along with 3rd party foundry relationships for the processing of wafers, the Company is increasing its international footprint. There are complexities associated with this scope of operation, including language, time zones, regulations and technology transfer issues. However, there are also benefits as the technological market is also international. Currently, the Company has applied for an export permit from the US Department of Commerce for the transfer of its proprietary epitaxial stack for further processing by an international third party foundry to continue the development of the VCSEL. We anticipate that we will need additional export permits in the future as our global reach increases.

_________________

1 Source: Cisco Global Cloud Index 2014

Key Success Drivers

The POET platform, which is covered by numerous patents and patents pending, may make possible the economic production of fully-integrated optoelectronic semiconductor devices with lower cost, smaller form factors and reduced power consumption compared to conventional photonics technologies. The Company will continue to drive research, as the expansion of the IP portfolio is important to the future of POET. The currently developed integrated VCSEL technology is in its early development stage and has been transferred to a commercial manufacturing source where development is ongoing. The company expects to validate the performance of some of its individual optical and electronic components in 2016.

The acquisition of DenseLight and BB Photonics Inc. (“BB Photonics”) has added experienced technologists, IP and know-how, technologies and products and customers to the POET portfolio. With these strategic acquisitions, the Company is well positioned to offer a unique and differentiated IP that allows it to expand its reach both within the Data Center and to Long Haul applications. These acquisitions expedite the Company’s commercialization roadmap. The Company is now generating revenue while having direct and preferred access to a fab infrastructure for future product development, access to product sales and channel distribution networks and a broader product portfolio of photonic products.

The success of early stage semiconductor companies is highly dependent on their ability to identify milestones that push the limit of existing technology and the achievement of those milestones in a timely fashion. The Company has demonstrated such successes in the past and continues to establish and achieve significant milestones. Significant milestones achieved over the last 3 years include:

1) Achieving radio frequency and microwave operation of both n-channel and p-channel transistors. By reaching this milestone, 3-inch POET wafers fabricated at BAE Systems (Nashua, NH) yielded submicron n-channel and micron-sized p-channel transistors operating at frequencies of 42 GHz and 3 GHz respectively.

2) The integration of the complementary inverter. Specifically, the Company successfully demonstrated complementary heterostructure field effect transistor based inverter operation using the POET process.

3) The fabrication of infrared (IR) detectors, using its proprietary planar optoelectronic technology (POET) platform. Adding to its significance is the fact that the POET wafers used for the IR devices were fabricated within an independent foundry, BAE Systems’ Microelectronics Center in Nashua, New Hampshire. This milestone represents the integration by a third party of the optoelectronic process previously demonstrated in POET laboratories.

4) Demonstration of a two terminal Thyristor VCSEL – which is a key optical engine in the creation of single chip optoelectronic transceivers and changes the current paradigm of analog lasers and detectors.

5) Recent demonstration of a best in class two terminal resonant cavity detector – which is also a critical device component used in its optical transceiver products.

6) Most recentfirst demonstration of functional Hetero-junction Field Effect Transistors (HFETs) down to 250nm effective gate lengths on the same proprietary epitaxy and utilizing the same integrated process sequence that was previously used to demonstrate high performance detectors.

The Company has successfully raised over CA$17.5 million in equity financing through private placements and an additional CA$30.3 million through the exercise of stock options and warrants since June 2012 of which CA$3.9 million was raised through the exercise of stock options and warrants during the period.

The Company’s future success will also depend on critical human capital. In this regard, the Company appointed a Chief Executive Officer, Chief Operating Officer and other key members of the operations team in 2015. Three new board members were also appointed in 2015 with unique industry insight and experience. The Company has also launched a recruitment drive for other key executives and engineering personnel.

Significant Events and Milestones During 2016

In 2016, the Company continued to execute on its stated strategic plan. The Company has achieved the following significant milestones in 2016:

| 1) | On March 22, 2016, the Company and the Institute of Micro Electronics Engineering, a Singapore Agency for Science, Technology and Research launched a joint 18-month development initiative for smart pixel applications. The project is designed to adapt the POET platform to potential applications in smart pixel technology for the burgeoning augmented reality market. |

| 2) | On April 4, 2016, the Company announced the following: |

| a. | The Company demonstrated a resonant cavity detector fabricated at the Company’s foundry supplier with performance that exceeds best in class. |

| b. | The Company successfully validated its process transfer to a 6-inch high volume production foundry. |

| c. | Due to health reasons, Dr. Geoff Taylor, the founder of the POET process, announced his retirement, effective April 30, 2016. |

| 3) | On May 11, 2016 the Company acquired all the issued and outstanding shares of DenseLight Semiconductor Pte. Ltd. in an all stock acquisition for $10,500,000. If DenseLight’s revenue meets or exceeds a certain target for 2016, the sellers will be entitled to receive an additional $1,000,000 worth of common shares from the Company. |

| 4) | On May 17, 2016, the Company hosted its first investor day conference in Toronto. The conference was well received with 140 participants physically attending and another 600 connected via teleconference or online to watch the live web-cast. |

| 5) | On June 22, 2016, the Company acquired all the issued and outstanding shares of BB Photonics, a New Jersey company and its subsidiary BB Photonics UK Ltd, collectively BB Photonics, a designer of integrated photonic solutions for the data communications market for consideration of $1,550,000. The all stock purchase was accomplished with the issuance of 1,996,090 common share of the Company at a price of $0.777 per share. |

Summary of Quarterly Results

Following are the highlights of financial data of the Company for the most recently completed eight quarters which have been derived from the Company’s consolidated financial statements prepared in accordance with IFRS:

| Jun.30/16 | Mar. 31/16 | Dec. 31/15 | Sep. 30/15 | Jun. 30/15 | Mar. 31/15 | Dec. 31/14 | Sep. 30/14 | |||||||||||||||||||||||||

| Sales | $ | 576,741 | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||||||||

| Cost of sales | 409,965 | - | - | - | - | - | - | - | ||||||||||||||||||||||||

| Research and development | 437,599 | 530,469 | 932,618 | 767,124 | 715,732 | 564,602 | 457,470 | 504,131 | ||||||||||||||||||||||||

| Depreciation and amortization | 239,958 | 87,844 | 83,526 | 82,022 | 79,587 | 74,728 | 70,222 | 66,050 | ||||||||||||||||||||||||

| Professional fees | 272,287 | 140,200 | 225,118 | 110,389 | 353,892 | 122,716 | 134,339 | 325,695 | ||||||||||||||||||||||||

| Wages and benefits | 1,192,887 | 483,169 | 414,857 | 423,214 | 269,015 | 198,965 | 578,071 | 405,012 | ||||||||||||||||||||||||

| Management and consulting fees | 172,401 | 157,805 | 156,154 | 160,303 | 168,700 | 180,614 | 140,040 | 290,327 | ||||||||||||||||||||||||

| Stock-based compensation (1) | 887,990 | 1,259,051 | 1,491,713 | 1,621,751 | 1,110,758 | 593,898 | 1,044,330 | 2,613,335 | ||||||||||||||||||||||||

| General expenses and rent | 417,224 | 260,764 | 353,399 | 285,802 | 241,088 | 364,316 | 204,857 | 192,935 | ||||||||||||||||||||||||

| Impairment and other loss | - | 80,453 | - | - | - | - | - | - | ||||||||||||||||||||||||

| Investment (income), including interest | (14,950 | ) | (20,802 | ) | (20,188 | ) | (18,979 | ) | (22,793 | ) | (14,471 | ) | - | - | ||||||||||||||||||

| Net loss | $ | 3,438,620 | $ | 2,978,953 | $ | 3,637,197 | $ | 3,431,626 | $ | 2,915,979 | $ | 2,085,368 | $ | 2,629,329 | $ | 4,397,485 |

| (1) | Stock based compensation allocated between General and Administrative and Research and Development issuances is combined for MD&A purposes. For financial statement presentation purposes, stock based compensation is split betweenGeneral and Administrative &Research and Development. |

Explanation of Quarterly Results for the three months ended June 30, 2016 ("Q2 2016")

Net loss for Q2 2016, includes the operations of DenseLight and BB Photonics, while the loss for Q2 2015 reflected the operations of the Company without those subsidiaries which were both acquired in Q2. The loss for the period was $3,438,620 as compared to loss of $2,915,979 in Q2 2015. The following discusses the significant variances between Q2 2016 and the three months ended June 30, 2015 ("Q2 2015").

During Q2 2016, the Company reported sales of $576,741 and gross margin of $166,776 or 29%. Due to the accounting rules relating to acquisitions, gross margin is lower than what would have been reported had the acquisition not taken place. Finished goods inventory is carried at fair value on the date of acquisition, finished goods inventory was written up by $178,087, this resulted in increased cost of sales and lower gross margin on inventory sold from the acquisition date to the end of Q2 2016. Gross margin will continue to be affected by the write up until that related finished goods inventory is sold. Adjusted gross margin for the Q2 2016 was 39%. Adjusted gross margin normalizes gross margin for the quarter by reversing the impact of the fair value inventory adjustment.

Research and development (“R&D”) decreased by 39% or $278,133 from $715,732 in Q2 2015 to $437,599 in Q2 2016. During Q2 2016, the Company spent significant time on the due diligence process relating to technology and products of BB Photonics and DenseLight to ensure a seamless integration with POET. The attention on the integration and due diligence resulted in an increase in general expenses and a reduction in R&D. Additionally, the Company adopted an outsourced R&D model which resulted in $100,000 of savings on R&D salaries over the period. R&D expense in Q2 2016 is consistent with the expectations of the Company.

Professional fees in Q2 2016 decreased by $81,605 from $353,892 in Q2 2015 to $272,287. During Q2 2016, the Company incurred $220,000 of professional fees relating to the acquisition of BB Photonics and DenseLight. Although, similar expenses were not incurred in Q2 2015, professional fees in Q2 2015 were high due to the recruitment fees paid in recruiting two new executives. In order to control its professional fees, in April 2015, the Company arranged a billing model with its regular professional advisors that would reduce the period over period fluctuations in their fees.

The 343% increase of $923,872 in wages and benefits from $269,015 in Q2 2015 to $1,192,887 in Q2 2016 was a result of a number of changes from Q2 2015 to Q2 2016. These changes include; addition of the COO and CEO in June 2015, inclusion of wages and benefits of DenseLight since May 12, 2016 with no comparable DenseLight salaries expensed in Q2 2015, and accrued but unpaid retention bonus to the COO and, executive retention bonus to CEO included in the original employment agreement due and payable in mid-June 2016, the one year anniversary. The total bonus payable of $550,000 was voluntarily deferred by both executives to a future date.

General expenses and rent increased in Q2 2016 as compared to Q2 2015 by $176,136. The expense was $241,088 in Q2 2015 and $417,224 in Q2 2016. The expense was unusually high in Q2 2016 due to the increased travel, due diligence and other acquisition costs related to the acquisition of DenseLight and BB Photonics. The expense also includes the activities of DenseLight since May 12, 2016 which contributed $74,000 to the expense in Q2 2016. The Company also incurred substantial shipping costs in transferring most of its equipment from the US to Singapore in Q2 2016 as part of its integration plan.

Non-cash stock-based compensation decreased by $222,768 from $1,110,758 in Q2 2015 to $887,990 in Q2 2016. The annual company stock incentive grant was awarded in June 2015 in the prior year subsequent to the AGM, while the current year award was undertaken after the period end on July 7, 2016. The valuation of stock options is driven by a number of factors including the number of options granted, the strike price and the volatility of the Company’s stock. The stock option expense is dependent on the timing of the stock option grant and the amortization of the options as they vest. The stock options vest in accordance with the policies determined by the Board of Directors from time to time consistent with the provisions of the 2015 Plan which grants discretion to the Board of Directors.

Depreciation and amortization increased by $160,371 from Q2 2015 to Q2 2016. The expense in Q2 2015 was $79,587 as compared to $239,958 in Q2 2016. The increase included $149,723 relating to the $8,706,029 increase in property and equipment resulting from the acquisition of DenseLight and BB Photonics.

Explanation of Results for the Six Months Ended June 30, 2016

The loss for the six months increased from $5,001,347 to $6,417,573 or $1,416,226. The current period’s loss includes $347,744 loss from DenseLight. Significant changes period over period were as follows:

Sales

The Company reported sales of $576,741 during the period wholly attributable to the newly acquired DenseLight subsidiary. No sales were reported in Q2 2015. Gross margin during the period was 29%. Due to the accounting rules relating to acquisitions, gross margin is lower than what would have been reported had the acquisition not taken place. Finished goods inventory is carried at fair value on the date of acquisition, finished goods inventory was written up by $178,087, this resulted in increased cost of sales and lower gross margin on inventory sold from the acquisition date to the period end. Gross margin will continue to be affected by the write up until that related finished goods inventory has been sold. Adjusted gross margin for the period was 39%. Adjusted gross margin normalizes gross margin for the period by reversing the impact of the fair value inventory adjustment.

Research and Development

R&D expense decreased by $312,266 from Q2 2015. R&D expense was $1,280,334 in Q2 2015 and $968,068 in Q2 2016. The Company has chosen to outsource a significant portion of its R&D. The outsourcing to Companies like Wavetek and Epiworks has resulted in the Company achieving a milestone with its resonant cavity detector. The Company has demonstrated a detector that exceeds the performance of the best detectors currently in the market. Synergies in technology development and operations resulted in reduced R&D expenses.

Wages and Benefits

Wages and benefits had the most significant increase from Q2 2015 to Q2 2016. The expense increased by 258% from $467,980 in Q2 2015 to $1,676,056 in Q2 2016. The drivers to the increase were addition of the COO and CEO in June 2015, inclusion of wages and benefits of DenseLight from May 12, 2016 to June 30, 2016 with no comparable DenseLight salaries expensed in Q2 2015, and accrued but unpaid retention bonus to the COO and executive retention bonus to CEO included in the original employment agreement due and payable in mid June 2016, the one year anniversary. The total bonus payable of $550,000 was voluntarily deferred by both executives to a future date.

General Expenses and Rent

General expenses and rent increased by $68,307 from $605,404 in Q2 2015 to $673,711 in Q2 2016. During Q2 2016, the Company acquired DenseLight and BB Photonics. The Company incurred acquisition costs related to the acquisition which included extra travel, freight to ship equipment to Singapore and regulatory transaction costs. The Q2 2016 expense also includes $74,000 general expenses of DenseLight from May 12, 2016 to June 30, 2016. These increases in Q2 2016 were offset by higher than normal Q2 2015 expenses related investor relations and promotion.

Stock-based Compensation

Non-cash stock-based compensation increased by $442,395 from $1,704,646 in Q2 2015 to $2,147,041 in Q2 2016. The valuation of stock options is driven by a number of factors including the number of options granted, the strike price and the volatility of the Company’s stock. The stock option expense is dependent on the timing of the stock option grant and the amortization of the options as they vest. The stock options vest in accordance with the policies determined by the Board of Directors from time to time consistent with the provisions of the 2015 Plan which grants discretion to the Board of Directors.

Depreciation and Amortization

The expense in Q2 2015 was $154,315 as compared to $327,802 in Q2 2016. The increase of $173,487 included $149,723 of depreciation relating to the new property and equipment resulting from the acquisition of DenseLight and BB Photonics of 8,706,029.

Explanation of Material Variations by Quarter for the Last Eight Quarters

Q2 2016 compared to Q1 2016

The Company had no sales in Q1 2016. The sales are wholly related to DenseLight which was acquired on May 11, 2016.

Depreciation and amortization in Q2 2016 was $239,958 as compared to $87,844 in Q1 2016. The increase of $152,114 over Q1 2016 included $149,723 of depreciation relating to new property and equipment resulting from the acquisition of DenseLight and BB Photonics of $8,706,029.

Professional fees increased by $132,087 from Q1 2016 to Q2 2016. The acquisition of DenseLight and BB Photonics contributed to the substantial increase from Q1 2016 to Q2 2016. The Company required the services of various professional consultants including solicitors, accountants and appraisers to complete the acquisition of both companies.

Wages and benefits had a substantial increase of $709,718 from Q1 2016 to Q2 2016. The increase was a result of accrued but unpaid executive bonus of $550,000 to the CEO and COO that was payable in mid-June 2016, the amount was voluntarily deferred by them to a future date as well as the inclusion of DenseLight and its wages and benefits of $261,721 for the period from May 12, 2016, acquisition date to the quarter end.

General expenses and rent increased by $156,460 or 60% from Q1 2016 to Q2 2016. DenseLight contributed $74,000 to the increase during the period. The difference resulted from additional costs incurred relating to the acquisition of DenseLight and BB Photonics.

Non-cash stock-based compensation decreased by $371,061 from $1,259,051 in Q1 2016 to $887,990 in Q2 2016. The valuation of stock options is driven by a number of factors including the number of options granted, the strike price and the volatility of the Company’s stock. The stock option expense is dependent on the timing of the stock option grant and the amortization of the options as they vest. The stock options vest in accordance with the policies determined by the Board of Directors from time to time consistent with the provisions of the 2015 Plan which grants discretion to the Board of Directors.

Q1 2016 compared to Q4 2015

R&D decreased by $402,149 from Q4 2015 to Q1 2016. In Q4 2015, the Company committed to transition to an increased outsourcing model as the most effective manner to monetize the POET process. During Q4 2015, the Company incurred additional upfront costs associated with establishing new foundry and technology development relationships with companies like Anadigics Inc., Epiworks, Wavetek and Intelligent Epitaxy Technology to expedite the technology development. In Q1 2016, the Company received positive information on its detectors produced by Wavetek. The Company’s detectors have better performance than any detectors currently on the market.

Professional fees decreased by $84,918 from $225,118 in Q4 2015 to $140,200 in Q1 2016. In Q4 2015, the Company paid additional legal fees associated with the expansion of the Company’s patent portfolio coverage in a number of foreign jurisdictions. The Company also spent additional fees on professional services involved in testing the efficiency of the Company’s internal controls as required by the Sarbanes Oxley Act of 2002.

In Q1 2016, the Company paid a $25,000 performance bonus to the COO. In addition to this payment the differential increase of $43,312 in wages and benefits over Q4 2015 was partially due to marginal increase in salaries and higher director fees paid in Q1 2016 than Q4 2015. Cumulative increase in wages and benefits over Q4 2015 was $68,312.

General expenses decreased by $92,635 from Q4 2015 to Q1 2016 due primarily to the costs of closing the UConn lab facilities in Q4 2015 and the investor relations and travel costs associated with the Company’s road show in November 2015 to generate interest in the Company and its technology.

In Q1 2016, non-cash stock-based compensation decreased by $232,662 from Q4 2015. This is a result of the timing of stock based compensation expense relative to the vesting date of the historical granted stock options. The valuation of stock options is driven by a number of factors including the quantity of options granted, the strike price and the volatility of the Company’s stock. The stock option expense is dependent on the timing of the stock option grant and the amortization of the options as they vest.

Q4 2015 compared to Q3 2015

In Q4 2015, professional fees increased by $114,729 over Q3 2015 due to the legal fees incurred relating to the expanded coverage of the Company’s patent portfolio and additional fees related to testing the effectiveness of the Company’s internal controls as required by the Sarbanes Oxley Act.

General and administrative increased by $67,597 in Q4 2015 as compared to Q3 2015 due to the increase in investor relations and travel during the quarter. The Company engaged in a European road show in November 2015 to generate interest in the Company and its technology. Additionally, the Company incurred moving and travel costs associated with the closure of the Uconn facilities.

In Q4 2015, the costs associated with new established foundry and technology development relationships with companies like Anadigics Inc., Epiworks and Intelligent Epitaxy Technology to expedite the technology development were incurred. The Company incurred costs of $449,200 relating to these new parties on the expedited technology work being done as compared to $290,215 in Q3 2015, which accounts for the majority of the $165,494 increase.

In Q4 2015, non-cash stock-based compensation decreased by $130,038 from Q3 2015. This is a result of the timing of stock based compensation expense relative to the vesting date of the historical granted stock options. The valuation of stock options is driven by a number of factors including the quantity of options granted, the strike price and the volatility of the Company’s stock. The stock option expense is dependent on the timing of the stock option grant and the amortization of the options as they vest.

Q3 2015 compared to Q2 2015

In Q3 2015, professional fees decreased by $243,503 from Q2 2015. The Company successfully recruited two high profile executive officers (CEO and COO). The Company paid $200,000 in recruitment fees related to Drs. Deshmukh’s and Venkatesan’s employment in Q2 2015. Both executives were appointed in June 2015. No recruitment fees were paid in Q3 2015.

Wages and benefits increased by $154,199 due to the addition of the new CEO and COO. Wages and benefits will be higher over the short term as the transition of responsibilities continues from the former interim CEO to the new CEO as both salaries are incurred by the company in the transition period.

Non-cash stock-based compensation in Q3 2015 was $510,993 higher than the expense in Q2 2015. The increase was impacted by timing of the expense related to the 10,430,000 stock options granted throughout calendar 2015. The Company granted 7,857,000 stock options to new executives (CEO and COO). The valuation of stock options is driven by a number of factors including the quantity of options granted, the strike price and the volatility of the Company’s stock. The stock option expense is dependent on the timing of the stock option grant and the amortization of the options as they vest.

Q2 2015 compared to Q1 2015

In Q2 2015, professional fees increased by $231,176 over Q1 2015. The Company successfully recruited two high profile executive officers (CEO and COO). The Company paid $200,000 in recruitment fees in Q2 related to Drs. Deshmukh’s and Venkatesan’s employment. Both executives were appointed in June 2015.

In Q2 2015, the Company increased its R&D efforts. Additional consultants were engaged by the Company. The $151,130 increase in R&D, is partially comprised of an additional $60,000 in consulting fees during Q2 in excess of Q1. The remaining increase was a result of the expanded scope of BAE’s foundry services to the Company.

General and administrative in Q2 2015 was $241,088 as compared to $364,316 in Q1 2015, a decrease of $123,228. In Q1 2015, the Company increased its investor relations, travel and promotion. The Company implemented a promotion program for POET which included advertisements on Bloomberg TV and the Fox News Network, which was expensed solely in Q1. Additionally, there were increases in maintenance and repair costs, resulting from the improper installation of new equipment by a third party and the purchasing of $15,000 of specialized software required to optimize the optical elements of the POET process.

Non-cash stock-based compensation in Q2 2015 was $516,860 in excess of the expense in Q1 2015. The increase was impacted by 9,930,000 stock options granted in Q2 as compared to 500,000 granted in Q1 2015. The Company granted 7,857,000 stock options to new executives (CEO and COO) in Q2 2015. The valuation of stock options is driven by a number of factors including the quantity of options granted, the strike price and the volatility of the Company’s stock. The stock option expense is dependent on the timing of the stock option grant and the amortization of the options as they vest.

Q1 2015 compared to Q4 2014

In Q1 2015, research and development expenses increased by $107,132 over Q4 2014 due to the addition of a Program Manager in Q1 2015 along with substantial overtime incurred during the quarter in connection with the rectification of improper installation of new equipment as previously discussed. The issues relating to the improper installation were rectified in Q1 2015.

Wages and benefits in Q1 2015 were $198,965 compared to $578,071 in Q4 2014. Q4 2014 included $230,000 paid in bonuses and $165,000 paid in directors’ fees. No bonuses were paid in Q1 2015 and director fees consisted of $39,981 in Q1 2015. The director fees in Q4 2014 included an expense for two quarters (Q3 2014 payment and Q4 2014 accrual).

In Q1 2015, non-cash stock-based compensation decreased by $450,432 from Q4 2014. This is a result of the timing of stock based compensation expense relative to the vesting date of the historical granted stock options. The valuation of stock options is driven by a number of factors including the quantity of options granted, the strike price and the volatility of the Company’s stock. The stock option expense is dependent on the timing of the stock option grant and the amortization of the options as they vest.

In Q1 2015, general and administrative increased by $159,459 over Q4 2014 due to increased investor relations, travel and promotion in this period. The Company implemented a promotion program for POET which included advertisements on Bloomberg TV and the Fox News Network which was expensed solely in Q1. Additionally, increases were incurred in maintenance and repair costs, resulting from the improper installation of new equipment by a third party and the leasing of specialized software required to optimize the optical elements of the POET process.

Q4 2014 compared to Q3 2014

Stock-based compensation and professional fees both decreased significantly from Q3 2014 to Q4 2014. Stock based compensation was $2,613,335 in Q3 2014 compared to $1,044,330 in Q4 2014. The valuation of stock options is driven by a number of factors including the quantity of options granted, the strike price and the volatility of the Company’s stock. The stock option expense is dependent on the timing of the stock option grant and the amortization of the options as they vest.

Professional fees were $325,695 in Q3 2014 compared to $134,339 in Q4 2014. In Q3 2014, the Company incurred expenses for the updated Pellegrino valuation report. Additionally, professional fees were incurred in recruiting the new Executive Co-Chairman in Q3 2014.

Wages and benefits increased by $173,059 from Q3 2014 to Q4 2014, due primarily to a performance bonus of $230,000 paid to the former interim CEO and former COO of the Company.

Segment Disclosure

The Company and its subsidiaries operate in a single segment; the design, manufacture and sale of semi-conductor products and services for military and commercial applications. The Company’s operating and reporting segment reflects the management reporting structure of the organization and the manner in which the chief operating decision maker regularly assesses information for decision making purposes, including the allocation of resources. A summary of the Company's operations is below:

ODIS Inc. (“ODIS”)

Odis is the developer of the POET platform semiconductor process IP for monolithic fabrication of integrated circuit devices containing both electronic and optical elements on a single die.

BB Photonics

BB Photonics develops photonic integrated components for the datacenter market utilizing embedded dielectric technology that is intended to enable on-chip athermal wavelength control and lower the total solution cost of datacenter photonic integrated circuits.

DenseLight

DenseLight designs, manufactures, and delivers photonic optical light source products and solutions to the communications, medical, instrumentations, industrial, defense, and security industries. DenseLight processes III-V based optoelectronic devices and photonic integrated circuits through its in-house wafer fabrication and assembly & test facilities.

The Company operates geographically in the United States, Canada and Singapore. Geographical information is as follows:

| 2016 | ||||||||||||||||

| As of June 30, | Singapore | US | Canada | Consolidated | ||||||||||||

| Current assets | $ | 2,174,203 | $ | 5,176,808 | $ | 7,088,669 | $ | 14,439,680 | ||||||||

| Non-current assets held for sale | - | 35,000 | - | 35,000 | ||||||||||||

| Property and equipment | 8,486,817 | 957,395 | 3,188 | 9,447,400 | ||||||||||||

| Patents and licenses | - | 433,642 | - | 433,642 | ||||||||||||

| Unallocated intangibles and goodwill | 7,775,304 | - | - | 7,775,304 | ||||||||||||

| Total Assets | $ | 18,436,324 | $ | 6,602,845 | $ | 7,091,857 | $ | 32,131,026 | ||||||||

| For the six months ended June 30, | Singapore | US | Canada | Consolidated | ||||||||||||

| Sales | $ | 576,741 | $ | - | $ | - | $ | 576,741 | ||||||||

| Cost of sales | 409,965 | - | - | 409,965 | ||||||||||||

| Selling, marketing and administration | 496,141 | 4,140,642 | 717,381 | 5,354,164 | ||||||||||||

| Research and development | 18,379 | 1,167,105 | - | 1,185,484 | ||||||||||||

| Impairment loss | - | 63,522 | - | 63,522 | ||||||||||||

| Loss on disposal of property and equipment | - | - | 16,931 | 16,931 | ||||||||||||

| Investment income | - | - | (35,752 | ) | (35,752 | ) | ||||||||||

| Net Loss | $ | 347,744 | $ | 5,371,269 | $ | 698,560 | $ | 6,417,573 | ||||||||

| 2015 | ||||||||||||||||

| As of December 31, | Singapore | US | Canada | Consolidated | ||||||||||||

| Current assets | $ | - | $ | 3,055,947 | $ | 11,504,972 | $ | 14,560,919 | ||||||||

| Property and equipment | - | 924,443 | 22,664 | 947,107 | ||||||||||||

| Patents and licenses | - | 426,813 | - | 426,813 | ||||||||||||

| Total Assets | $ | - | $ | 4,407,203 | $ | 11,527,636 | $ | 15,934,839 | ||||||||

| For the six months ended June 30, | Singapore | US | Canada | Consolidated | ||||||||||||

| General and administration | $ | - | $ | 2,844,107 | $ | 613,191 | $ | 3,457,298 | ||||||||

| Research and development | - | 1,581,313 | - | 1,581,313 | ||||||||||||

| Other income | - | - | (37,264 | ) | (37,264 | ) | ||||||||||

| Net Loss | $ | - | $ | 4,425,420 | $ | 575,927 | $ | 5,001,347 | ||||||||

Note: Certain prior period amounts have been reclassified to conform with the current year's presentation.

Liquidity and Capital Resources

The Company had working capital of $12,522,987 on June 30, 2016 as compared to $14,045,498 on December 31, 2015. The Company is reporting adjusted working capital which removes contingent consideration payable from the calculation as the Company’s obligation for this liability is non-cash. Adjusted working capital is $12,889,959 at June 30, 2016 and $14,045,498 at December 31, 2015.

During the six month period ended June 30, 2016, the Company raised $2,941,975 from the exercise of stock options and warrants to assist with its liquidity. The Company, however, used $4,668,379 on operations. The cash flow spent on operations included funding the loss of DenseLight from acquisition date of May 11, 2016 along with one-time cash out flows relating to the acquisitions during the period.

The Company’s balance sheet as at June 30, 2016 reflects assets with a book value of $32,131,026 (2015 - $15,934,839) of which 45% (2015 - 91%) or $14,474,680 (2015 - $14,560,919) is current and consists primarily of cash totaling $12,759,617 (2015 - $14,409,996). The Company’s liquidity and unencumbered balance sheet will allow for investments in capital equipment and valuable human capital which are necessary to enable the Company to achieve its technical and operational milestones while driving DenseLight to be EBITDA positive.

Based on current plans and cash utilization, we believe we have sufficient liquidity to support our operations and technological programs beyond August 2017, which include further development of the POET semiconductor process and increasing the POET intellectual property portfolio to enable us to exploit POET, through licenses and collaborative arrangements and funding DenseLight’s operations.

The Company is embarking on an aggressive plan of attempting to monetize POET while simultaneously improving shareholder value. The focus, therefore, is to remain sufficiently capitalized to facilitate this.

Acquisitions

DenseLight

On May 11, 2016, the Company acquired all the issued and outstanding shares of DenseLight, a designer, manufacturer and provider of photonic sensing and optical light source products for consideration of $10,500,000. The all stock purchase was accomplished with the issuance of 13,611,150 common share of the Company at a price of $0.771 per share. The Company also committed to issuing shares representing $1,000,000 to the sellers in the event that DenseLight meets or exceeds a pre-determined revenue target during calendar 2016.

This acquisition provides the Company with direct access to its own fab infrastructure, acquired in the transaction, for future product development, access to product sales and channel distribution networks and a broader product portfolio of photonic products, technology and know-how.

Upon closing the acquisition, the Company negotiated a settlement agreement relating to obligations that were due to past or current employees of DenseLight. As part of the settlement agreement, the Company issued 1,738,236 common shares at a price of $0.771 per share for a total of $1,343,629. The Company also paid $240,266 to current and past employees as part of the debt settlement. Accounts payable and accrued liabilities include $289,179 still due to past and current employees that will be paid over the next 11 months.

The Company also settled a loan of $500,000 owing to EDB Investments Pte. Ltd., an investor in DenseLight, with the issuance of 648,150 shares at a price of 0.771 per share.

Former management shareholders of DenseLight agreed not to sell, transfer, pledge or otherwise dispose of the shares of the Company for a period of six months, at which time they may each sell up to 25% of their shares. They may sell an additional 25% of the shares after twelve months. Thereafter, all management shareholders shall be able to sell the remaining shares after 24 months from closing. Former non-management shareholders of DenseLight agreed not to sell, transfer, pledge or otherwise dispose of the shares they received for six months, at which time such they may sell up to 25% of the shares received. Thereafter, they may sell the remaining shares after 12 months from closing.

On acquisition, DenseLight held accounts receivable and unbilled revenue in the amount of $366,630 which reflected fair value. The Company does not expect that there will be any contractual cash flows that may not be realized.

The acquisition has been accounted for using the acquisition method of accounting. Acquisition related costs of $197,284 were expensed in the period and included in selling, marketing and administrative expenses.

A final assessment of the fair value of identifiable assets and liabilities acquired has not yet been completed. A preliminary assessment of the acquisition has been determined as follows:

| Fair value of consideration paid | ||||

| Fair value of 13,611,150 shares issued | $ | 10,500,000 | ||

| Contingent consideration payable | 366,972 | |||

| Total consideration | $ | 10,866,972 | ||

| Recognised amounts of identifiable net assets: | ||||

| Cash | $ | 2,971 | ||

| Accounts receivables and prepaid expenses | 662,296 | |||

| Inventory | 412,690 | |||

| Property and equipment | 8,635,650 | |||

| Unallocated intangibles and goodwill | 6,303,585 | |||

| Trade payables | (2,658,437 | ) | ||

| Loans and advances | (1,000,000 | ) | ||

| Deferred tax liability | (1,491,783 | ) | ||

| Net assets acquired | $ | 10,866,972 | ||

Loans and advances include $500,000 that was advanced to DenseLight by the Company prior to its acquisition as part of a services agreement.

From the date of acquisition, DenseLight contributed $576,741 to consolidated revenues and $347,744 to consolidated net loss. Had the acquisition occurred on January 1, 2016, the Company estimates that DenseLight's contribution to consolidated revenue would have been $1,037,882 and would have contributed net income of $329,240 after the impact of recoveries and accounting fair value adjustments arising from the acquisition. In determining these amounts, the Company assumed that the preliminary fair value adjustments that arose on the acquisition date would have been the same had the acquisition occurred on January 1, 2016. Had the acquisition not occurred the company would have reported a loss.

BB Photonics

On June 22, 2016, the Company acquired all the issued and outstanding shares of BB Photonics, a designer of integrated photonic solutions for the data communications market for consideration of $1,550,000. The all stock purchase was accomplished with the issuance of 1,996,090 common share of the Company at a price of $0.777 per share.

The acquisition of BB Photonics provides the Company with additional differentiated intellectual property and know-how for product development which will enable the Company to better service its first identified commercialization market, the end-to-end data communications market, and augment its sensing roadmap.

The acquisition has been accounted for using the acquisition method of accounting. Acquisition related costs of $59,930 were expensed in the period and included in selling, marketing and administrative expenses.

A final assessment of the fair value of identifiable assets and liabilities acquired has not yet been completed. A preliminary assessment of the acquisition has been determined as follows:

| Fair value of consideration paid | ||||

| Fair value of 1,996,090 shares issued | $ | 1,550,000 | ||

| Recognised amounts of identifiable net assets: | ||||

| Cash | $ | 15,820 | ||

| Property and equipment | 70,379 | |||

| Unallocated intangibles and goodwill | 1,471,719 | |||

| Trade payables | (7,918 | ) | ||

| Net assets acquired | $ | 1,550,000 | ||

From the date of acquisition, BB Photonics contributed nil to consolidated revenues and $6,688 to consolidated net loss. Had the acquisition occurred on January 1, 2016, the Company estimates that BB Photonics' contribution to consolidated revenue would have been nil and it would have contributed net loss of $97,699. In determining these amounts, the Company assumed that the preliminary fair value adjustments that arose on the acquisition date would have been the same had the acquisition occurred on January 1, 2016.

Related Party Transactions

Compensation to key management personnel were as follows:

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2016 | 2015 | 2016 | 2015 | |||||||||||||

| Salaries | $ | 1,171,333 | $ | 428,849 | $ | 1,725,623 | $ | 801,023 | ||||||||

| Share-based payments(1) | 775,842 | 327,993 | 1,684,305 | 830,364 | ||||||||||||

| Total | $ | 1,947,175 | $ | 756,842 | $ | 3,409,928 | $ | 1,631,387 | ||||||||

(1) Share-based payments are the fair value of options granted to key management personnel and expensed during the year as calculated using the Black-Scholes model.

The Company paid or accrued $28,996 and $56,333 respectively in fees and disbursements for the three and six months ended June 30, 2016 (2015 - $32,243 and $85,227) to a law firm, of which a director is counsel, for legal services rendered to the Company.

All transactions with related parties have occurred in the normal course of operations and are measured at the exchange amounts, which are the amounts of consideration established and agreed to by the related parties.

Critical Accounting Estimates

Accounts receivable

Accounts receivable are amounts due from customers from the sale of products or services in the ordinary course of business. Accounts receivables are classified as current (on the consolidated statements of financial position) if payment is due within one year of the reporting period date, and are initially recognized at fair value and subsequently measured at amortized cost.

The provision policy for doubtful accounts of the Company is based on the ageing analysis and management's ongoing evaluation of the recoverability of the outstanding receivables. A considerable amount of judgement is required in assessing the ultimate realization of these receivables, including the assessment of the creditworthiness and the past collection history of each customer. If the financial conditions of these customers were to deteriorate,resulting in an impairment of their ability to make payments, additional allowances may be required. As at the balance sheet date, no provision was required for accounts receivable.

Inventories

Inventories consist of raw material inventories, work in process, and finished goods and are recorded at the lower of cost and net realizable value. Cost is determined on a first in first out basis and includes all costs of purchase, costs of conversion and other costs incurred in bringing the inventory to its present condition.

An assessment is made of the net realizable value of inventory at each reporting period. Net realizable value is the estimated selling price less the estimated cost of completion and the estimated costs necessary to make the sale. When circumstances that previously caused inventories to be written down no longer exist or when there is clear evidence of an increase in net realizable value because of changed economic circumstances, the amount of any write down previously recorded is reversed so that the new carrying amount is the lower of the cost and the revised net realizable value. Raw materials are not written down unless the goods in which they are incorporated are expected to be sold for less than cost, in which case, they are written down by reference to replacement cost of the raw materials, as this is the best indicator of net realizable value.

Property and equipment

Property and equipment are recorded at cost. Depreciation is calculated based on the estimated useful life of the asset using the following method and useful lives:

| Machinery and equipment | Straight Line, 5 years | |

| Leasehold improvements | Straight Line, 5 years or life of the lease, whichever is less | |

| Office equipment | Straight Line, 5 years |

Contingent consideration

The Company may pay future consideration related to acquisitions based upon performance measures contractually agreed at the time of purchase. Management estimates the future consideration payable based on underlying contract terms, and best estimates of the future performance of the acquiree. Depending on the future performance of the acquiree, management estimates of the amounts payable for future consideration related to acquisitions may materially differ from the consideration ultimately paid.

Stock-based Compensation

Stock options and warrants awarded to non-employees are accounted for using the fair value of the instrument awarded or service provided, whichever is considered more reliable. Stock options and warrants awarded to employees are accounted for using the fair value method. The fair value of such stock options and warrants granted is recognized as an expense on a proportionate basis consistent with the vesting features of each tranche of the grant. The fair value is calculated using the Black-Scholes option pricing model with assumptions applicable at the date of grant.

Other stock-based payments

The Company accounts for other stock-based payments based on the fair value of the equity instruments issued or service provided, whichever is more reliable.

Cumulative Translation Adjustment

IFRS requires certain gains and losses such as certain exchange gains and losses arising from the translation of the financial statements of a self-sustaining foreign operation to be included in comprehensive income.

Recent Accounting Pronouncements

The Company has considered all recently issued accounting pronouncements and does not believe the adopting of such pronouncements will have a material impact on its consolidated financial statements. Please see note 3 of the financial statements for additional information.

Financial Instruments and Risk Management

The Company's financial instruments consist of cash and cash equivalents, accounts receivable, non current assets held for sale, accounts payable and accrued liabilities and contingent consideration payable. Unless otherwise noted, it is management's opinion that the Company is not exposed to significant interest risk arising from these financial instruments. The Company estimates that the fair value of these instruments approximates fair value due to their short term nature.

The contingent consideration payable related to acquisitions is a financial instrument carried at fair value and is measured at fair value through profit or loss. The contingent consideration payable arose on the acquisition of DenseLight. The purchase and sale agreement provides for an additional $1,000,000 worth of shares to be issued to the sellers should gross revenue from DenseLight exceed certain targets for 2016.

The fair value of the contingent consideration payable is determined by estimating the probability of the Company making that future payment and then discounting it to present value using a discount rate of 9% being the estimated cost of debt for the Company. A final assessment of the purchase price may yield a different valuation.

Exchange Rate Risk

The Company is exposed to foreign currency risk with the Canadian dollar and Singapore dollar. The Company maintains bank accounts and cash reserves in three currencies with the majority of reserves currently in Canadian dollars which has exposure to currency fluctuations. Most of the Company’s operations are transacted in US dollars and Singapore Dollars. A 10% change in the Canadian dollar and Singapore dollar would increase or decrease other comprehensive loss by $961,346.

Interest Rate Risk

Cash equivalents bear interest at fixed rates, and as such, are subject to interest rate risk resulting from changes in fair value from market fluctuations in interest rates. The Company does not depend on interest from its investments to fund its operations.

Credit Risk

The Company is exposed to credit risk associated with its accounts receivable. The Company has accounts receivable from both governmental and non-governmental agencies. Credit risk is minimized substantially by ensuring the credit worthiness of the entities with which it carries on business. Credit terms are provided on a case by case basis. The Company has not experienced any significant instances of non-payment from its customers.

The Company's accounts receivable aging was as follows:

| June 30, 2016 | December 31, 2015 | |||||||

| Current | $ | 405,560 | $ | - | ||||

| 31 - 60 days | 50,885 | - | ||||||

| 61 - 90 days | 69,033 | - | ||||||

| > 90 days | 7,341 | - | ||||||

| Unbilled receivables | 296,052 | - | ||||||

The Company has accounts receivable from one governmental agency representing 59% of total accounts receivable, 60% of which is unbilled at June 30, 2016. The billed portion is current.

World Economic Risk

Like many other companies, the world economic climate could have an impact on the Company's business and the business of many of its current and prospective customers. A slump in demand for electronic-based devices, due to a world economic crisis, may impact any anticipated licensing revenue.

Obsolescence Risk

The Company designs, manufactures and sells various highly technological electronic products that could become obsolete should lower priced competitors or new technology enter the market. This would expose the company to obsolescence risk in inventory balances, but also a risk of obsolescence in the product offering. The redesign of the product offering could take significant time or could never occur.

Liquidity Risk

The Company predominately relies on equity funding for liquidity to meet current and foreseeable financial requirements.

Strategy and Outlook