UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report of

Registered Management Investment Companies

Investment Company Act File Number: 811-22215

International Growth and Income Fund

(Exact Name of Registrant as Specified in Charter)

One Market, Steuart Tower

Suite 2000

San Francisco, California 94105

(Address of Principal Executive Offices)

Registrant's telephone number, including area code: (415) 421-9360

Date of fiscal year end: June 30

Date of reporting period: June 30, 2014

Patrick F. Quan

International Growth and Income Fund

One Market, Steuart Tower

Suite 2000

San Francisco, California 94105

(Name and Address of Agent for Service)

Copies to:

Michael Glazer

Bingham McCutchen LLP

355 South Grand Avenue, Suite 4400

Los Angeles, California 90071

(Counsel for the Registrant)

ITEM 1 – Reports to Stockholders

![]()

Selectivity has

helped us navigate

a complex world.

Special feature page 6

| |

| International Growth and

Annual report |

International Growth and Income Fund seeks to provide long-term growth of capital with current income by investing primarily in the stocks of larger, well-established companies domiciled outside the U.S.

This fund is one of more than 40 offered by one of the nation’s largest mutual fund families, American Funds, from Capital Group. For more than 80 years, Capital has invested with a long-term focus based on thorough research and attention to risk.

Fund results shown in this report, unless otherwise indicated, are for Class A shares at net asset value. If a sales charge (maximum 5.75%) had been deducted, the results would have been lower. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. For current information and month-end results, visit americanfunds.com.

Here are the average annual total returns on a $1,000 investment with all distributions reinvested for periods ended June 30, 2014:

| Class A shares | 1 year | 5 years | Lifetime (since 10/1/08) | |||

| Reflecting 5.75% maximum sales charge | 15.59% | 11.77% | 10.36% |

For other share class results, visit americanfunds.com and americanfundsretirement.com.

The total annual fund operating expense ratio is 0.91% for Class A shares as of the prospectus dated August 29, 2014 (unaudited).

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, investment results reflect fee waivers and/or expense reimbursements, without which results would have been lower. Visit americanfunds.com for more information.

The fund’s 30-day yield for Class A shares as of July 31, 2014, reflecting the 5.75% maximum sales charge and calculated in accordance with the U.S. Securities and Exchange Commission formula, was 2.12%.

Investing outside the United States may be subject to risks such as currency fluctuations, periods of illiquidity and price volatility. These risks may be heightened in connection with investments in developing countries. Refer to the fund prospectus and the Risk Factors section of this report for more information on these and other risks associated with investing in the fund.

The fund pursues

international growth

with a dividend focus.

Special feature

| 6 | Navigating a complex world with a selective approach and flexible mandate |

Contents

| 1 | Letter to investors |

| 5 | The value of a $10,000 investment |

| 12 | Summary investment portfolio |

| 16 | Financial statements |

| 34 | Board of trustees and other officers |

International stock markets rallied for the second straight year, supported by ongoing global monetary stimulus and improving economic conditions in Europe, the United States and other key markets.

For the 12 months ended June 30, 2014, shares of International Growth and Income Fund advanced 22.66% for those who reinvested distributions totaling $2.55 a share — a figure that includes, on a per share basis, quarterly dividend payments totaling about $1.18 and a $1.37 capital gain paid in December. This amounts to an income return of 3.8%.

The fund’s total return exceeded the 21.75% return of its primary benchmark, the unmanaged MSCI ACWI (All Country World Index) ex USA. The index measures a broad range of developed- and developing-country stock markets excluding the U.S. The fund also slightly outpaced the 22.28% return of the Lipper International Funds Index, a peer group measure.

The market environment

Most of the world’s stock markets

Results at a glance

For periods ended June 30, 2014, with all distributions reinvested

| Cumulative total returns | Average annual total returns | |||||||||||

| 1 year | 5 years | Lifetime (since 10/1/08) | ||||||||||

| International Growth and Income Fund (Class A shares) | 22.66 | % | 13.11 | % | 11.51 | % | ||||||

| MSCI ACWI ( All Country World Index) ex USA* | 21.75 | 11.11 | 7.16 | |||||||||

| Lipper International Funds Index | 22.28 | 12.02 | 7.73 | |||||||||

| * | The market index is unmanaged and, therefore, has no expenses. The index reflects dividends net of withholding taxes. Investors cannot invest directly in an index. |

| International Growth and Income Fund | 1 |

Where the fund’s assets were invested

Percent of net assets by country as of June 30, 2014

| International Growth and Income Fund | MSCI ACWI ex USA* | |||||||

| Europe | ||||||||

| Euro zone† | 32.1 | % | 22.4 | % | ||||

| United Kingdom | 18.6 | 15.3 | ||||||

| Switzerland | 5.4 | 6.4 | ||||||

| Sweden | 1.5 | 2.2 | ||||||

| Other Europe | 1.2 | 3.6 | ||||||

| 58.8 | 49.9 | |||||||

| Asia/Pacific | ||||||||

| Japan | 8.9 | 14.4 | ||||||

| Hong Kong | 5.4 | 2.0 | ||||||

| China | 3.5 | 3.9 | ||||||

| Taiwan | 3.1 | 2.6 | ||||||

| India | 2.6 | 1.4 | ||||||

| Australia | 2.3 | 5.5 | ||||||

| Other Asia/Pacific | .8 | 6.5 | ||||||

| 26.6 | 36.3 | |||||||

| The Americas | ||||||||

| Canada | 5.4 | 7.6 | ||||||

| Mexico | 1.4 | 1.1 | ||||||

| United States | .3 | — | ||||||

| Other Americas | — | 2.9 | ||||||

| 7.1 | 11.6 | |||||||

| Other | ||||||||

| South Africa | .3 | 1.6 | ||||||

| Other countries | — | .6 | ||||||

| .3 | 2.2 | |||||||

| Convertible securities, bonds, notes & other debt instruments, short-term securities & other assets less liabilities | 7.2 | — | ||||||

| Total | 100.0 | % | 100.0 | % | ||||

| * | The MSCI ACWI (All Country World Index) ex USA is weighted by market capitalization. |

| † | Countries using the euro as a common currency: Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia and Spain. |

recorded strong positive results for the fiscal year. European stocks notched outstanding returns amid soaring mergers-and-acquisitions activity, particularly in the health care sector. Stocks were bolstered by new stimulus measures initiated by the European Central Bank as it sought to stave off Japan-style deflation. Among other steps, the central bank cut a key interest rate to less than zero to encourage banks to boost lending. Euro-zone GDP rose by an annualized 0.8% in the first quarter of 2014 and inflation stood at 0.5% in May.

A number of Europe’s most economically troubled countries, including Spain (57.17%), Greece (55.08%) and Ireland (34.97%), delivered particularly noteworthy stock market gains. Germany (29.35%) and France (28.07%), the euro zone’s two largest economies, also outpaced the broader market. Overall, the MSCI Europe Index rose 29.28% in U.S. dollar terms.1

Despite considerable volatility, Japanese shares (+9.85%) ended in positive territory. After soaring more than 50%, in local currency terms, in fiscal-year 2013, Japan’s stock market sold off in the early months of 2014, hurt in part by a slowing Chinese economy and worries over the potential impact of a sales tax that took effect in April. However, stocks closed out the fiscal year with gains after revised data showed that the Japanese economy had grown faster in the first quarter than initially reported.

Developing market results were generally positive despite the slowdown in China’s economy and geopolitical strife in some countries. Indian equities advanced 27.40% as investors were cheered by the election

| 1 | Unless otherwise indicated, country and sector returns are based on MSCI indexes and measured in U.S. dollars with net dividends reinvested. |

| 2 | International Growth and Income Fund |

of reform-minded Narendra Modi as prime minister. China’s stock market gained 15.67% for the fiscal year as investors weighed indications that the government would take measured steps against a slowing economy and property market. Elsewhere, shares in Chile (–12.45%) and Indonesia (–11.88%) declined for U.S. investors as both countries’ currencies slid against the U.S. dollar.

All 10 sectors that comprise the MSCI ACWI ex USA posted double-digit returns during the period. Energy stocks (+27.61%) led markets higher as military clashes in Ukraine and Iraq raised fears of potential oil and gas shortages. The information technology (+27.66%) and health care (+26.51%) sectors also recorded outstanding gains.

Solid support from top holdings

The investment professionals who help manage the fund construct the portfolio one company at a time, basing their decisions on fundamental research. While sector and country returns offer a backdrop, individual investment selection plays a primary role in driving the fund’s results.

Seven of the fund’s top-10 holdings outpaced the MSCI ACWI ex USA for the fiscal year, and these positions represent a variety of industries. They included the utility EDP - Energias de Portugal (+62.28%), pharmaceutical companies AstraZeneca (+56.79%) and Novartis (+27.47%); oil companies TOTAL (+48.04%) and Royal Dutch Shell (+31.47%); insurer Prudential (+40.36%); and Imperial Tobacco (+29.79%), the fund’s sixth-largest holding. Elsewhere among the top-10 holdings, French insurer AXA (+21.64%) and Taiwan

| Largest equity holdings (as of June 30, 2014) | ||||||

| Company | Country | Percent of net assets | ||||

| AXA | France | 2.4 | % | |||

| EDP - Energias de Portugal | Portugal | 2.3 | ||||

| Novartis | Switzerland | 2.2 | ||||

| AstraZeneca | United Kingdom | 2.0 | ||||

| Taiwan Semiconductor Manufacturing | Taiwan | 2.0 | ||||

| Imperial Tobacco | United Kingdom | 1.9 | ||||

| Royal Dutch Shell | United Kingdom | 1.9 | ||||

| Prudential | United Kingdom | 1.8 | ||||

| TOTAL | France | 1.8 | ||||

| HSBC Holdings | United Kingdom | 1.8 | ||||

| International Growth and Income Fund | 3 |

Semiconductor Manufacturing (+14.40%) trailed the broader market, while U.K. bank HSBC Holdings (–2.38%) was the only of the top 10 investments to decline.

The fund also received strong contributions from a number of investments in the consumer discretionary sector, a broad category that includes media companies, auto manufacturers and makers of luxury goods. Top contributors in this area included OPAP (+112.68%), German auto manufacturer BMW (+45.03%) and casino operator Wynn Macau (+44.87%).

In addition to HSBC Holdings, a number of other holdings lost ground. They included Japanese banks Sumitomo Mitsui Financial Group (–8.68%) and Shinsei Bank (–0.79%) French industrial conglomerate Vallourec (–11.50%) and South African retailer Shoprite Holdings (–22.84%).

Maintaining a long-term view

Overall, the global economy continues to strengthen. Shortly after the close of the fiscal year, a troubled Portuguese financial institution missed a coupon payment, rekindling investor fears about Europe’s debt crisis. While we believe Europe has stabilized and remains on track toward recovery, the incident serves as a reminder that recoveries generally don’t happen in a straight line.

We continue to watch developments in Asia closely, as Japan seeks to restore normal economic growth through the policies of Prime Minister Shinzo Abe and China’s leaders pursue better balance in its domestic economy. However, rather than invest in economies or countries, our focus is on individual companies. Through intensive research, we continue to find opportunities to invest in what we believe are strong, attractively valued companies in markets across Europe and Asia. To learn more about our selective approach to investing, we invite you to read the feature article beginning on page 6.

We continue to focus on the long term and encourage you to do the same. We thank you for your commitment to International Growth and Income Fund.

Cordially,

Steven T. Watson

Vice Chairman of the Board

Carl Kawaja

President

August 12, 2014

For current information about the fund, visit americanfunds.com.

| 4 | International Growth and Income Fund |

The value of a $10,000 investment

How a $10,000 investment has fared (for the period October 1, 2008, to June 30, 2014, with distributions reinvested)

Fund results shown are for Class A shares and reflect deduction of the maximum sales charge of 5.75% on the $10,000 investment.¹ Thus, the net amount invested was $9,425. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. For current information and month-end results, visit americanfunds.com.

| 1 | As outlined in the prospectus, the sales charge is reduced for accounts (and aggregated investments) of $25,000 or more and is eliminated for purchases of $1 million or more. There is no sales charge on dividends or capital gain distributions that are reinvested in additional shares. |

| 2 | All results are calculated with dividends and capital gains reinvested. |

| 3 | The market index is unmanaged and, therefore, has no expenses. The index reflects dividends net of withholding taxes. Investors cannot invest directly in an index. |

| 4 | For the period October 1, 2008 (when the fund began operations), through October 31, 2008. |

Average annual total returns based on a $1,000 investment (for periods ended June 30, 2014)*

| 1 year | 5 years | Lifetime (since 10/1/08) | ||||||||||

| Class A shares | 15.59 | % | 11.77 | % | 10.36 | % | ||||||

| * | Assumes reinvestment of all distributions and payment of the maximum 5.75% sales charge. |

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, investment results reflect fee waivers and/or expense reimbursements, without which results would have been lower. Visit americanfunds.com for more information.

| International Growth and Income Fund | 5 |

Navigating a complex world with a selective approach and flexible mandate

While we launched the fund in the midst of a very significant downturn, shortly afterward we experienced a strong upturn. Thus far the fund has weathered stormy seas and also prospered when the sailing was smoother. If we hit stormy seas again, we believe we can continue to do well.

Carl Kawaja

International Growth and Income Fund pursues a dual objective on behalf of its investors: It seeks to provide both long-term growth of capital and current income. In service of this mission, the fund’s managers focus primarily on well-established companies domiciled outside the U.S. that usually pay dividends.

That focus has served investors well over nearly six years since the fund began operations. From its birth on October 1, 2008, through the close of the most recent fiscal year, the fund has generated an average annual return of 11.51%, outpacing its primary benchmark, the unmanaged MSCI ACWI (All Country World Index) ex USA, by an average of more than 4 percentage points a year. In their pursuit of superior long-term results, the investment professionals who manage the fund don’t focus on particular geographic regions. Rather, they work hard to uncover opportunity at the company level.

In the following pages, we will revisit the premise behind International Growth and Income Fund, look at how the international investing climate has changed since the fund’s founding and explore how highly selective investing — supported by intensive research and a long-term perspective — helps the fund pursue its objectives.

Seeking a sensible approach to international investing

The potential for long-term capital appreciation and diversification long have been recognized as important reasons for investing internationally. Broadly speaking, markets outside the United States represent vast opportunity for long-term investors. As of June 2014, about 51% of world market capitalization came from securities in non-U.S. markets (as represented by the MSCI ACWI Index). Of course, investing beyond U.S. borders does involve some additional risks — currency fluctuations, differing regulations and periods of illiquidity among them.

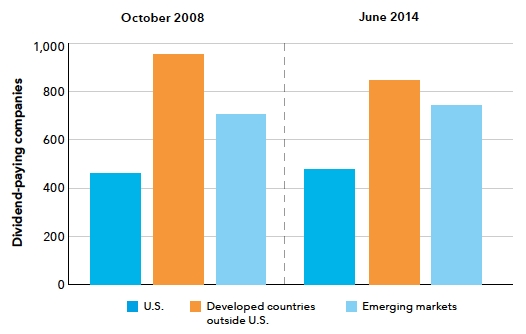

For a number of years leading up to the introduction of the fund, its investment advisor, Capital Research and Management Company, had been tracking a compelling trend in these markets. More and more companies had been demonstrating a commitment to the idea that a portion of earnings should be returned to investors in the form of regular dividend payments. In October 2008, there were more than 950 dividend-paying companies domiciled in developed markets outside the U.S., as measured by the MSCI EAFE (Europe, Australasia, Far East) Index, many of which had been raising their dividends (see chart on page 8). That figure was significantly higher than the number of dividend payers among U.S. companies.

The fund’s investment professionals believe that this trend provided a compelling long-term opportunity. “When we began the fund, we thought the idea of investing with a focus on dividend-paying companies domiciled outside the U.S. could provide

| 6 | International Growth and Income Fund |

The search for dividends not only provides you with current income, but also with some expectation for lower volatility.

Steve Watson

long-term value for investors,” says portfolio manager Andrew Suzman. “If you look back over the last 100 years, dividends and growth of dividends have been responsible for a very substantial portion of most equity market returns. Dividend-focused investing can go in and out of fashion, but it is intuitively and practically a very sound way to build a portfolio.”

Why are dividends so important? Steady dividend payments over a long period of time often indicate a profitable, well-managed company that’s willing to share its good fortune with shareholders. In other words, dividends are often a hallmark of quality. What’s more, dividends can serve as a cushion against market volatility.

“The search for dividends not only provides you with current income, but also with some expectation for lower volatility because income tends to provide a valuation floor,” says Steve Watson, vice chairman of the fund’s board and a portfolio manager. “But we do not set out to invest solely for dividend income. At the same time, we are looking for stocks whose full value is not recognized by the market, so we are offering investors the prospect of long-term capital appreciation as well.”

Unwavering focus amid a sea of change

This relatively conservative approach was tested early. When the fund opened its doors on October 1, 2008, it was greeted by the worst global financial crisis since the 1930s. In the U.S., financial institutions were confronted with mounting loan losses as housing troubles that had been unfolding since 2007 came to a head. Lehman Brothers, then the fourth-largest

As the world turns: global dividend opportunities then and now

While conditions across global markets have changed considerably since International Growth and Income Fund began, opportunities to invest in dividend paying companies outside the U.S. remain vast.

Source: MSCI USA Index, MSCI EAFE Index, MSCI Emerging Markets Index.

| 8 | International Growth and Income Fund |

![]()

investment bank in the U.S., had recently declared bankruptcy. The crisis quickly spread to financial institutions in other markets around the world. Central banks took aggressive action to help keep financial markets functioning.

Unemployment soared — the U.S. alone lost more than 7.5 million jobs as a result of the recession — and export activity around the world declined sharply, helping to push much of the global economy into deep recession. Over the subsequent 24 months, a sovereign debt crisis unfolded in Europe, leaving many investors questioning the viability of the euro currency and economic union. What’s more, China’s economy, which had been a source of strength, began to slow, further unnerving investors.

It is fair to characterize those early days as dark ones. Yet fund managers viewed the market volatility as an opportunity, so they set out to identify companies that could thrive regardless of evolving market and economic conditions. “We really believed the fund had long-term merits, but when we got started I think it is safe to say that we proceeded with great caution,” recalls Andrew. “That being said, it turns out that starting in a difficult moment produced some long-term buying opportunities, which has helped us produce strong returns for investors over the past five years.”

Much has changed, much has not

In recent years, conditions have been decidedly more upbeat. Today, the U.S. stock market is in its fifth year of a bull market. The 18-nation euro zone has pulled out of recession, and the European Central Bank recently instituted a number of stimulus measures, including a negative interest rate for its overnight depositors and special funding arrangements that would benefit banks in peripheral countries, as it seeks to ensure better economic health and growth. Japan is seeking, via the policies of Prime Minister Shinzo Abe, to return to sustainable growth over the long term. China has slowed down, but is seeking a firmer footing for its economy over the long term.

Some things have not changed. As the chart on page 8 shows, international markets continue to represent significant opportunity for dividend-focused investors. And the fund’s managers continue to rely on fundamental research to identify those companies that they believe are well positioned to help the fund meet its growth-and-income objective at any given point in a market cycle.

“Going forward we believe this fund’s mission continues to make sense,” says Carl Kawaja, president of the fund and a portfolio manager. “While we launched the fund in the midst of a very significant downturn, shortly afterward we experienced a strong upturn. Thus far the fund has weathered stormy seas and also prospered when the sailing was smoother. If we hit stormy seas again, we believe we can continue to do well.”

While there have been periods when the fund has trailed the unmanaged MSCI ACWI ex USA, over its lifetime it has generated higher returns than both that benchmark and the Lipper International Funds Index, a measure of its competitors. And it has done so with lower volatility (see chart on page 10).

“With the benefit of hindsight, these five-plus years proved to be a rewarding time for investing in larger companies with a multinational footprint that offered income in the form of dividends,” says Steve. “And it proved to be a good time to seek out companies that, through intensive fundamental analysis, seem undervalued by the market relative to their long-term prospects. Our approach has worked well over the last five years, but I wouldn’t

| International Growth and Income Fund | 9 |

say there is anything special about those years. I believe the fund’s approach is simply a good approach.”

Selectivity driven by deep research

Rather than investing in particular sectors, geographies or categories of stocks, the investment professionals who help manage the fund develop a deep understanding of individual companies and then invest one company at a time, based on whether they believe a particular firm is attractively valued based on its growth potential and business prospects. At the heart of this approach is intensive fundamental research.

Consider that while dividend paying stocks have done well in an international context, investing based on that criterion alone would not have been enough to produce the return that the fund has over its lifetime. During that period, the companies in the MSCI ACWI ex USA that paid the highest dividends — specifically those ranked in the top 40% of the index by weighted dividend yield — generated an average cumulative return of roughly 66%. That compares with an 87% cumulative return for the fund.

“It was also important to invest in the companies that grew their dividends and the companies that were nimble enough to adjust in the midst of a global financial crisis,” says Carl. “Anybody can go find out what the highest yielding stocks are and buy those — a passive, index-based investment could do that. But a passively managed fund can’t figure out which companies are going to grow their dividends over the next five years, or which companies are best able to navigate unexpected developments on the competitive landscape. That only comes from doing the research, understanding the fundamentals and meeting the managements.”

Looking where others don’t

The fund’s managers do not make investment decisions based on short-term market conditions. Rather they decide with the expectation of investing in companies for the long term. This long term investment outlook allows them to invest in what they believe are strong companies when they are overlooked by the market and hold them until the market recognizes their value.

Consider, for example, EDP – Energias de Portugal, a major electricity provider and the fund’s second-largest holding; and Piraeus Bank, a Greek financial institution. The companies are domiciled in countries whose economies have been among the most troubled in Europe in recent years.

“One thing that I have been a little struck by is, who would have guessed that a Portuguese utility company or a Greek bank would end up being among our

Fund results shown are for Class A shares at net asset value. If a sales charge (maximum 5.75%) had been deducted, the results would have been lower. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. For current information and month-end results, visit americanfunds.com.

Return vs volatility (10/31/08–6/30/14)

Superior returns with less volatility

Over its nearly six-year lifetime, International Growth and Income Fund has delivered higher returns than its primary benchmark, the MSCI ACWI ex USA, and other measures.

Source: MSCI, Lipper. Volatility is calculated at net asset value using annualized standard deviation (based on monthly returns). Returns are calculated at net asset value, with all distributions reinvested. Market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index. MSCI ACWI (All Country World Index) ex USA is a free-float-adjusted market-capitalization-weighted index that measures equity market results in the global developed and emerging markets, excluding the United States. MSCI World Index ex USA is a free-float-adjusted market-capitalization-weighted index that is designed to measure equity market results of developed markets, excluding the United States. The MSCI indexes reflect dividends net of withholding taxes.

| 10 | International Growth and Income Fund |

significant holdings today?” observes Carl. “It just shows you how quickly the world can change and how important the fund’s flexibility is.”

In the case of EDP, investors had been wary of investing in Portugal for a number of years, as the country confronted substantial debt burden. Many feared that the company would face excessive taxation as the Portuguese government sought revenue to address budget shortfalls. The investment analyst who covers EDP for the fund, however, believed it was a strong company that was undervalued by the market. It has been a holding since the fund’s launch.

“One of the nice things about our long-term approach is sometimes something doesn’t work right away, but rather than abandon the idea and look elsewhere, we may buy more shares at a lower price if we still believe in the thesis behind an investment,” says Steve.

Consider Taiwan Semiconductor Manufacturing (TSMC), the fund’s fifth-largest investment. The company, which also has been in the portfolio since the fund’s launch, makes chips that have enabled rapid advances in technology for smartphones. In the early days of the fund’s life, the world was preoccupied with smartphones, Steve recalls, and Samsung Electronics — a primary competitor of TSMC — was deemed to be the primary beneficiary of that trend. But Shailesh Jaitly, an analyst based in Hong Kong, believed that TSMC’s advantage in leading-edge mobile technologies would help it take market share and expand pricing power. More recently, TSMC has had strong results whereas Samsung Electronics earnings have been disappointing.

“That is an example of our long-term approach and tremendously deep knowledge of a company based on research,” says Steve. “Shailesh has been watching TSMC for more than 15 years and may know that company better than any other analyst in the world.”

Swiss drug maker Novartis, the fund’s third-largest investment, had been out of favor for a number of years due to expiring patents for two key medications and manufacturing problems at a U.S. plant. But analyst Eric Keisman saw potential in the company’s pipeline of drugs in development. The company, which also has been a holding since the fund’s launch, has generated relatively strong results in recent years. To be sure, some of the fund’s long-time holdings — South African mining company Impala Platinum Holdings and Dutch bank ING Groep, for example — have disappointed thus far. But the fund’s managers have the freedom to hold on to investments during challenging periods if they believe the company represents value over the longer term.

Fund objectives inform all decisions

As they seek to identify companies with the potential to do well over time, the fund’s managers rely on a proven process known as The Capital System.SM Under this system, the fund’s three managers are supported by dozens of experienced investment analysts located in markets all across the globe. These professionals work hard to identify those companies that can help the fund meet its mission.

“We had a theory that growth and income investing would be fruitful, and it has been,” says Carl. “We had a theory that there were some non-U.S. companies that would grow their dividends, and they have. And we also had a theory that international investing could be a prudent part of people’s portfolios, and that has been true.”

Whatever conditions arise over the coming years, the fund’s managers will continue to focus on those objectives.

“Thus far we have faced a lot of uncertainty and a lot of volatility,” says Steve. “And yet we’ve managed to generate reasonable returns and reasonable income for our investors, and we believe that by working hard and sticking to our disciplined approach, we can continue to find attractive long-term investment opportunities.” ¢

| International Growth and Income Fund | 11 |

Summary investment portfolio June 30, 2014

| Industry sector diversification | Percent of net assets |

| Country diversification | Percent of net assets | |||

| Euro zone* | 32.1 | % | ||

| United Kingdom | 18.6 | |||

| Japan | 8.9 | |||

| Switzerland | 5.4 | |||

| Hong Kong | 5.4 | |||

| Canada | 5.4 | |||

| China | 3.5 | |||

| Taiwan | 3.1 | |||

| India | 2.6 | |||

| Australia | 2.3 | |||

| Other countries | 5.5 | |||

| Convertible securities, bonds, notes & other debt instruments, short-term securities & other assets less liabilities | 7.2 | |||

| * | Countries using the euro as a common currency; those represented in the fund’s portfolio are Belgium, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Portugal and Spain. |

| Common stocks 92.27% | Shares | Value (000) | Percent of net assets | |||||||||

| Financials 27.14% | ||||||||||||

| AXA SA | 9,083,200 | $ | 217,099 | 2.38 | % | |||||||

| Prudential PLC | 7,274,148 | 166,941 | 1.83 | |||||||||

| HSBC Holdings PLC (United Kingdom) | 9,006,896 | 91,392 | ||||||||||

| HSBC Holdings PLC (Hong Kong) | 5,642,396 | 57,222 | 1.63 | |||||||||

| Eurobank Ergasias SA1 | 252,821,128 | 127,743 | 1.40 | |||||||||

| Banco Santander, SA1 | 11,785,376 | 123,131 | 1.35 | |||||||||

| Sumitomo Mitsui Financial Group, Inc. | 2,830,000 | 118,558 | 1.30 | |||||||||

| Bankia, SA1 | 53,300,000 | 103,345 | 1.14 | |||||||||

| Shinsei Bank, Ltd. | 43,088,000 | 96,975 | 1.07 | |||||||||

| Grupo Financiero Santander México, SAB de CV, Class B (ADR) | 7,300,200 | 96,947 | 1.06 | |||||||||

| Svenska Handelsbanken AB, Class A | 1,569,000 | 76,812 | .84 | |||||||||

| Link Real Estate Investment Trust | 13,415,418 | 72,180 | .79 | |||||||||

| BNP Paribas SA | 1,037,530 | 70,388 | .77 | |||||||||

| Sun Hung Kai Properties Ltd. | 4,759,402 | 65,277 | .72 | |||||||||

| Piraeus Bank SA1 | 26,507,881 | 58,802 | .65 | |||||||||

| Other securities | 930,127 | 10.21 | ||||||||||

| 2,472,939 | 27.14 | |||||||||||

| Consumer discretionary 9.84% | ||||||||||||

| OPAP SA | 5,673,200 | 100,988 | 1.11 | |||||||||

| SES SA, Class A (FDR) | 2,175,000 | 82,497 | .91 | |||||||||

| ProSiebenSat.1 Media AG | 1,768,000 | 78,765 | .86 | |||||||||

| Carphone Warehouse Group PLC | 12,010,000 | 66,307 | .73 | |||||||||

| SJM Holdings Ltd. | 24,000,000 | 60,136 | .66 | |||||||||

| Other securities | 507,933 | 5.57 | ||||||||||

| 896,626 | 9.84 | |||||||||||

| Energy 9.22% | ||||||||||||

| Royal Dutch Shell PLC, Class B | 3,908,000 | 170,046 | 1.87 | |||||||||

| TOTAL SA | 2,285,550 | 165,181 | 1.81 | |||||||||

| Enbridge Inc. | 2,220,520 | 105,361 | 1.16 | |||||||||

| China Petroleum & Chemical Corp., Class H | 106,420,000 | 101,471 | 1.11 | |||||||||

| Keyera Corp. | 800,000 | 58,936 | .65 | |||||||||

| Paramount Resources Ltd.1 | 1,050,000 | 58,599 | .64 | |||||||||

| Crescent Point Energy Corp. | 1,260,000 | 55,841 | .61 | |||||||||

| Other securities | 125,125 | 1.37 | ||||||||||

| 840,560 | 9.22 | |||||||||||

| 12 | International Growth and Income Fund |

| Shares | Value (000) | Percent of net assets | ||||||||||

| Industrials 7.75% | ||||||||||||

| Abertis Infraestructuras, SA, Class A | 4,054,050 | $ | 93,288 | 1.02 | % | |||||||

| Adecco SA | 930,000 | 76,556 | .84 | |||||||||

| Meggitt PLC | 8,446,847 | 73,147 | .80 | |||||||||

| Wolseley PLC | 1,112,684 | 60,993 | .67 | |||||||||

| Geberit AG | 170,700 | 59,922 | .66 | |||||||||

| Other securities | 342,654 | 3.76 | ||||||||||

| 706,560 | 7.75 | |||||||||||

| Information technology 7.18% | ||||||||||||

| Taiwan Semiconductor Manufacturing Co. Ltd. | 43,481,506 | 184,219 | 2.02 | |||||||||

| STMicroelectronics NV | 13,793,000 | 123,746 | 1.36 | |||||||||

| Quanta Computer Inc. | 26,454,835 | 77,084 | .85 | |||||||||

| Other securities | 269,052 | 2.95 | ||||||||||

| 654,101 | 7.18 | |||||||||||

| Consumer staples 6.80% | ||||||||||||

| Imperial Tobacco Group PLC | 3,935,000 | 177,114 | 1.94 | |||||||||

| British American Tobacco PLC | 2,670,300 | 158,943 | 1.74 | |||||||||

| Nestlé SA | 774,700 | 60,016 | .66 | |||||||||

| Other securities | 223,923 | 2.46 | ||||||||||

| 619,996 | 6.80 | |||||||||||

| Utilities 6.23% | ||||||||||||

| EDP - Energias de Portugal, SA | 41,172,000 | 206,565 | 2.27 | |||||||||

| Power Assets Holdings Ltd. | 13,985,500 | 122,254 | 1.34 | |||||||||

| Power Grid Corp. of India Ltd. | 36,840,000 | 85,263 | .93 | |||||||||

| National Grid PLC | 4,487,744 | 64,515 | .71 | |||||||||

| Other securities | 88,959 | .98 | ||||||||||

| 567,556 | 6.23 | |||||||||||

| Health care 6.13% | ||||||||||||

| Novartis AG | 2,172,000 | 196,675 | 2.16 | |||||||||

| AstraZeneca PLC | 2,505,000 | 186,080 | 2.04 | |||||||||

| Other securities | 176,190 | 1.93 | ||||||||||

| 558,945 | 6.13 | |||||||||||

| Telecommunication services 4.93% | ||||||||||||

| Orange | 8,380,000 | 132,246 | 1.45 | |||||||||

| KDDI Corp. | 930,000 | 56,725 | .62 | |||||||||

| HKT Trust, units | 48,085,000 | 56,644 | .62 | |||||||||

| Other securities | 204,101 | 2.24 | ||||||||||

| 449,716 | 4.93 | |||||||||||

| Materials 4.80% | ||||||||||||

| L’Air Liquide SA2 | 273,152 | 36,879 | ||||||||||

| L’Air Liquide SA, non-registered shares | 235,612 | 31,811 | .93 | |||||||||

| L’Air Liquide SA, bonus shares2 | 118,891 | 16,052 | ||||||||||

| Potash Corp. of Saskatchewan Inc. | 1,715,400 | 65,117 | .72 | |||||||||

| Other securities | 287,138 | 3.15 | ||||||||||

| 436,997 | 4.80 | |||||||||||

| Miscellaneous 2.25% | ||||||||||||

| Other common stocks in initial period of acquisition | 204,744 | 2.25 | ||||||||||

| Total common stocks (cost: $6,657,107,000) | 8,408,740 | 92.27 | ||||||||||

| Preferred securities 0.15% | ||||||||||||

| Financials 0.14% | ||||||||||||

| HSBC Holdings PLC, Series 2, 8.00% | 472,795 | 12,825 | .14 | |||||||||

| Miscellaneous 0.01% | ||||||||||||

| Other preferred securities in initial period of acquisition | 1,225 | .01 | ||||||||||

| Total preferred securities (cost: $12,739,000) | 14,050 | .15 | ||||||||||

| International Growth and Income Fund | 13 |

| Rights & warrants 0.35% | Value (000) | Percent of net assets | ||||||||||

| Financials 0.32% | ||||||||||||

| Other securities | $ | 28,746 | .32 | % | ||||||||

| Miscellaneous 0.03% | ||||||||||||

| Other rights & warrants in initial period of acquisition | 2,844 | .03 | ||||||||||

| Total rights & warrants (cost: $0) | 31,590 | .35 | ||||||||||

| Convertible securities 0.72% | ||||||||||||

| Other 0.72% | ||||||||||||

| Other securities | 65,400 | .72 | ||||||||||

| Total convertible securities (cost: $77,844,000) | 65,400 | .72 | ||||||||||

| Bonds, notes & other debt instruments 1.80% | Principal amount (000) | |||||||||||

| Corporate bonds & notes 0.97% | ||||||||||||

| Financials 0.38% | ||||||||||||

| SMFG Preferred Capital USD 3 Ltd., junior subordinated 9.50% (undated)3,4 | $ | 5,410 | 6,808 | .08 | ||||||||

| Other securities | 27,720 | .30 | ||||||||||

| 34,528 | .38 | |||||||||||

| Consumer staples 0.03% | ||||||||||||

| British American Tobacco International Finance PLC 9.50% 20183 | 2,000 | 2,601 | .03 | |||||||||

| Other 0.56% | ||||||||||||

| Other securities | 50,749 | .56 | ||||||||||

| Total corporate bonds & notes | 87,878 | .97 | ||||||||||

| U.S. Treasury bonds & notes 0.64% | ||||||||||||

| Other securities | 58,532 | .64 | ||||||||||

| Bonds & notes of governments outside the U.S. 0.19% | ||||||||||||

| Other securities | 17,195 | .19 | ||||||||||

| Total bonds, notes & other debt instruments (cost: $162,400,000) | 163,605 | 1.80 | ||||||||||

| Short-term securities 3.99% | ||||||||||||

| Federal Home Loan Bank 0.075%–0.083% due 8/20–12/5/2014 | 118,800 | 118,784 | 1.30 | |||||||||

| Freddie Mac 0.08%–0.14% due 9/17–12/8/2014 | 56,600 | 56,586 | .62 | |||||||||

| Other securities | 188,173 | 2.07 | ||||||||||

| Total short-term securities (cost: $363,527,000) | 363,543 | 3.99 | ||||||||||

| Total investment securities (cost: $7,273,617,000) | 9,046,928 | 99.28 | ||||||||||

| Other assets less liabilities | 66,140 | .72 | ||||||||||

| Net assets | $ | 9,113,068 | 100.00 | % | ||||||||

This summary investment portfolio is designed to streamline the report and help investors better focus on the fund’s principal holdings. See the inside back cover for details on how to obtain a complete schedule of portfolio holdings.

As permitted by U.S. Securities and Exchange Commission regulations, “Miscellaneous” securities include holdings in their first year of acquisition that have not previously been publicly disclosed.

“Other securities” includes all issues that are not disclosed separately in the summary investment portfolio, including some securities which were pledged as collateral for net losses. The total value of pledged collateral was $724,000, which represented .01% of the net assets of the fund.

| 14 | International Growth and Income Fund |

Forward currency contracts

The fund has entered into forward currency contracts to sell currencies as shown in the following table. The average notional amount of open forward currency contracts was $220,591,000 over the prior 12-month period.

| Unrealized | ||||||||||||

| Contract amount | depreciation | |||||||||||

| Receive | Deliver | at 6/30/2014 | ||||||||||

| Settlement date | Counterparty | (000) | (000) | (000) | ||||||||

| Sales: | ||||||||||||

| Australian dollars | 7/18/2014 | Bank of New York Mellon | $ 30,744 | A$ 33,325 | $(635 | ) | ||||||

| Australian dollars | 9/11/2014 | Bank of America, N.A. | $ 29,475 | A$ 31,800 | (352 | ) | ||||||

| Japanese yen | 7/10/2014 | HSBC Bank | $ 5,399 | ¥ 550,000 | (31 | ) | ||||||

| Japanese yen | 7/14/2014 | HSBC Bank | $ 111,764 | ¥ 11,372,592 | (510 | ) | ||||||

| Japanese yen | 7/18/2014 | UBS AG | $ 14,542 | ¥ 1,490,000 | (168 | ) | ||||||

| Japanese yen | 7/31/2014 | Bank of America, N.A. | $ 8,364 | ¥ 850,000 | (28 | ) | ||||||

| Japanese yen | 8/14/2014 | UBS AG | $ 1,469 | ¥ 150,000 | (12 | ) | ||||||

| Japanese yen | 8/14/2014 | Citibank | $ 16,657 | ¥ 1,700,000 | (130 | ) | ||||||

| Japanese yen | 8/14/2014 | Bank of New York Mellon | $ 23,515 | ¥ 2,400,000 | (184 | ) | ||||||

| Japanese yen | 9/4/2014 | Bank of America, N.A. | $ 5,865 | ¥ 600,000 | (60 | ) | ||||||

| $(2,110 | ) | |||||||||||

The following footnotes apply to either the individual securities noted or one or more of the securities aggregated and listed as a single line item.

| 1 | Security did not produce income during the last 12 months. |

| 2 | Valued under fair value procedures adopted by authority of the board of trustees. The total value of all such securities, including those in “Miscellaneous” and “Other securities,” was $55,488,000, which represented .61% of the net assets of the fund. |

| 3 | Acquired in a transaction exempt from registration under Rule 144A or section 4(2) of the Securities Act of 1933. May be resold in the U.S. in transactions exempt from registration, normally to qualified institutional buyers. The total value of all such securities, including those in “Other securities,” was $173,878,000, which represented 1.91% of the net assets of the fund. |

| 4 | Coupon rate may change periodically. |

Key to abbreviations and symbol

ADR = American Depositary Receipts

FDR = Fiduciary Depositary Receipts

A$ = Australian dollars

¥ = Japanese yen

See Notes to Financial Statements

| International Growth and Income Fund | 15 |

| Statement of assets and liabilities | |

| at June 30, 2014 | (dollars in thousands) |

| Assets: | ||||||||

| Investment securities, at value (cost: $7,273,617) | $ | 9,046,928 | ||||||

| Cash denominated in currencies other than U.S. dollars (cost: $2,511) | 2,513 | |||||||

| Cash | 739 | |||||||

| Receivables for: | ||||||||

| Sales of investments | $ | 54,605 | ||||||

| Sales of fund’s shares | 28,558 | |||||||

| Dividends and interest | 30,619 | 113,782 | ||||||

| 9,163,962 | ||||||||

| Liabilities: | ||||||||

| Unrealized depreciation on open forward currency contracts | 2,110 | |||||||

| Payables for: | ||||||||

| Purchases of investments | 27,062 | |||||||

| Repurchases of fund’s shares | 8,896 | |||||||

| Investment advisory services | 3,676 | |||||||

| Services provided by related parties | 2,377 | |||||||

| Trustees’ deferred compensation | 1,585 | |||||||

| Other | 5,188 | 48,784 | ||||||

| Net assets at June 30, 2014 | $ | 9,113,068 | ||||||

| Net assets consist of: | ||||||||

| Capital paid in on shares of beneficial interest | $ | 7,178,751 | ||||||

| Undistributed net investment income | 10,527 | |||||||

| Undistributed net realized gain | 157,258 | |||||||

| Net unrealized appreciation | 1,766,532 | |||||||

| Net assets at June 30, 2014 | $ | 9,113,068 |

(dollars and shares in thousands, except per-share amounts)

Shares of beneficial interest issued and outstanding (no stated par value) —

unlimited shares authorized (249,312 total shares outstanding)

| Shares | Net asset value | |||||||||||

| Net assets | outstanding | per share | ||||||||||

| Class A | $ | 5,027,032 | 137,509 | $ | 36.56 | |||||||

| Class B | 16,066 | 440 | 36.54 | |||||||||

| Class C | 309,399 | 8,484 | 36.47 | |||||||||

| Class F-1 | 1,225,962 | 33,543 | 36.55 | |||||||||

| Class F-2 | 1,228,459 | 33,593 | 36.57 | |||||||||

| Class 529-A | 129,253 | 3,539 | 36.52 | |||||||||

| Class 529-B | 693 | 19 | 36.51 | |||||||||

| Class 529-C | 32,310 | 889 | 36.36 | |||||||||

| Class 529-E | 4,661 | 128 | 36.52 | |||||||||

| Class 529-F-1 | 10,878 | 297 | 36.57 | |||||||||

| Class R-1 | 9,107 | 249 | 36.49 | |||||||||

| Class R-2 | 53,278 | 1,464 | 36.40 | |||||||||

| Class R-3 | 45,865 | 1,256 | 36.50 | |||||||||

| Class R-4 | 50,782 | 1,390 | 36.54 | |||||||||

| Class R-5 | 20,643 | 562 | 36.72 | |||||||||

| Class R-6 | 948,680 | 25,950 | 36.56 | |||||||||

See Notes to Financial Statements

| 16 | International Growth and Income Fund |

| Statement of operations | |

| for the year ended June 30, 2014 | (dollars in thousands) |

| Investment income: | ||||||||

| Income: | ||||||||

| Dividends (net of non-U.S. taxes of $25,479) | $ | 326,888 | ||||||

| Interest | 16,043 | $ | 342,931 | |||||

| Fees and expenses*: | ||||||||

| Investment advisory services | 38,479 | |||||||

| Distribution services | 17,300 | |||||||

| Transfer agent services | 8,155 | |||||||

| Administrative services | 2,088 | |||||||

| Reports to shareholders | 418 | |||||||

| Registration statement and prospectus | 383 | |||||||

| Trustees’ compensation | 578 | |||||||

| Auditing and legal | 129 | |||||||

| Custodian | 1,277 | |||||||

| Other | 227 | 69,034 | ||||||

| Net investment income | 273,897 | |||||||

| Net realized gain and unrealized appreciation on investments, forward currency contracts and currency: | ||||||||

| Net realized gain (loss) on: | ||||||||

| Investments | 236,798 | |||||||

| Forward currency contracts | 7,221 | |||||||

| Currency transactions | (818 | ) | 243,201 | |||||

| Net unrealized appreciation (depreciation) on: | ||||||||

| Investments (net of non-U.S. taxes of $5,042) | 1,020,842 | |||||||

| Forward currency contracts | (4,654 | ) | ||||||

| Currency translations | 664 | 1,016,852 | ||||||

| Net realized gain and unrealized appreciation on investments, forward currency contracts and currency | 1,260,053 | |||||||

| Net increase in net assets resulting from operations | $ | 1,533,950 |

*Additional information related to class-specific fees and expenses is included in the Notes to Financial Statements.

See Notes to Financial Statements

| International Growth and Income Fund | 17 |

| Statements of changes in net assets | |

| (dollars in thousands) |

| Year ended June 30 | ||||||||

| 2014 | 2013 | |||||||

| Operations: | ||||||||

| Net investment income | $ | 273,897 | $ | 156,009 | ||||

| Net realized gain on investments, forward currency contracts and currency transactions | 243,201 | 268,628 | ||||||

| Net unrealized appreciation on investments, forward currency contracts and currency translations | 1,016,852 | 465,269 | ||||||

| Net increase in net assets resulting from operations | 1,533,950 | 889,906 | ||||||

| Dividends and distributions paid to shareholders: | ||||||||

| Dividends from net investment income | (269,581 | ) | (159,324 | ) | ||||

| Distributions from net realized gain on investments | (291,114 | ) | — | |||||

| Total dividends and distributions paid to shareholders | (560,695 | ) | (159,324 | ) | ||||

| Net capital share transactions | 1,789,408 | 728,944 | ||||||

| Total increase in net assets | 2,762,663 | 1,459,526 | ||||||

| Net assets: | ||||||||

| Beginning of year | 6,350,405 | 4,890,879 | ||||||

| End of year (including undistributed and distributions in excess of net investment income: $10,527 and $(6,399), respectively) | $ | 9,113,068 | $ | 6,350,405 | ||||

See Notes to Financial Statements

| 18 | International Growth and Income Fund |

Notes to financial statements

1. Organization

International Growth and Income Fund (the “fund”) is registered under the Investment Company Act of 1940 as an open-end, diversified management investment company. The fund seeks to provide long-term growth of capital with current income by investing primarily in the stocks of larger, well-established companies domiciled outside the U.S.

The fund has 16 share classes consisting of five retail share classes (Classes A, B and C, as well as two F share classes, F-1 and F-2), five 529 college savings plan share classes (Classes 529-A, 529-B, 529-C, 529-E and 529-F-1) and six retirement plan share classes (Classes R-1, R-2, R-3, R-4, R-5 and R-6). The 529 college savings plan share classes can be used to save for college education. The retirement plan share classes are generally offered only through eligible employer-sponsored retirement plans. The fund’s share classes are described further in the following table:

| Share class | Initial sales charge | Contingent deferred sales charge upon redemption | Conversion feature | |||

| Classes A and 529-A | Up to 5.75% | None (except 1% for certain redemptions within one year of purchase without an initial sales charge) | None | |||

| Classes B and 529-B* | None | Declines from 5% to 0% for redemptions within six years of purchase | Classes B and 529-B convert to Classes A and 529-A, respectively, after eight years | |||

| Class C | None | 1% for redemptions within one year of purchase | Class C converts to Class F-1 after 10 years | |||

| Class 529-C | None | 1% for redemptions within one year of purchase | None | |||

| Class 529-E | None | None | None | |||

| Classes F-1, F-2 and 529-F-1 | None | None | None | |||

| Classes R-1, R-2, R-3, R-4, R-5 and R-6 | None | None | None |

*Class B and 529-B shares of the fund are not available for purchase.

Holders of all share classes have equal pro rata rights to assets, dividends and liquidation proceeds. Each share class has identical voting rights, except for the exclusive right to vote on matters affecting only its class. Share classes have different fees and expenses (“class-specific fees and expenses”), primarily due to different arrangements for distribution, administrative and shareholder services. Differences in class-specific fees and expenses will result in differences in net investment income and, therefore, the payment of different per-share dividends by each share class.

2. Significant accounting policies

The fund is an investment company that applies the accounting and reporting guidance issued in Topic 946 by the U.S. Financial Accounting Standards Board. The fund’s financial statements have been prepared to comply with U.S. generally accepted accounting principles (“U.S. GAAP”). These principles require the fund’s investment adviser to make estimates and assumptions that affect reported amounts and disclosures. Actual results could differ from those estimates. The fund follows the significant accounting policies described in this section, as well as the valuation policies described in the next section on valuation.

Security transactions and related investment income — Security transactions are recorded by the fund as of the date the trades are executed with brokers. Realized gains and losses from security transactions are determined based on the specific identified cost of the securities. In the event a security is purchased with a delayed payment date, the fund will segregate liquid assets sufficient to meet its payment obligations. Dividend income is recognized on the ex-dividend date and interest income is recognized on an accrual basis. Market discounts, premiums and original issue discounts on fixed-income securities are amortized daily over the expected life of the security.

Class allocations — Income, fees and expenses (other than class-specific fees and expenses) and realized and unrealized gains and losses are allocated daily among the various share classes based on their relative net assets. Class-specific fees and expenses, such as distribution, administrative and shareholder services, are charged directly to the respective share class.

| International Growth and Income Fund | 19 |

Dividends and distributions to shareholders — Dividends and distributions to shareholders are recorded on the ex-dividend date.

Currency translation — Assets and liabilities, including investment securities, denominated in currencies other than U.S. dollars are translated into U.S. dollars at the exchange rates supplied by one or more pricing vendors on the valuation date. Purchases and sales of investment securities and income and expenses are translated into U.S. dollars at the exchange rates on the dates of such transactions. The effects of changes in exchange rates on investment securities are included with the net realized gain or loss and net unrealized appreciation or depreciation on investments in the fund’s statement of operations. The realized gain or loss and unrealized appreciation or depreciation resulting from all other transactions denominated in currencies other than U.S. dollars are disclosed separately.

3. Valuation

Capital Research and Management Company (“CRMC”), the fund’s investment adviser, values the fund’s investments at fair value as defined by U.S. GAAP. The net asset value of each share class of the fund is generally determined as of approximately 4:00 p.m. New York time each day the New York Stock Exchange is open.

Methods and inputs — The fund’s investment adviser uses the following methods and inputs to establish the fair value of the fund’s assets and liabilities. Use of particular methods and inputs may vary over time based on availability and relevance as market and economic conditions evolve.

Equity securities are generally valued at the official closing price of, or the last reported sale price on, the exchange or market on which such securities are traded, as of the close of business on the day the securities are being valued or, lacking any sales, at the last available bid price. Prices for each security are taken from the principal exchange or market on which the security trades.

Fixed-income securities, including short-term securities, are generally valued at prices obtained from one or more pricing vendors. Vendors value such securities based on one or more of the inputs described in the following table. The table provides examples of inputs that are commonly relevant for valuing particular classes of fixed-income securities in which the fund is authorized to invest. However, these classifications are not exclusive, and any of the inputs may be used to value any other class of fixed-income security.

| Fixed-income class | Examples of standard inputs | |

| All | Benchmark yields, transactions, bids, offers, quotations from dealers and trading systems, new issues, spreads and other relationships observed in the markets among comparable securities; and proprietary pricing models such as yield measures calculated using factors such as cash flows, financial or collateral performance and other reference data (collectively referred to as “standard inputs”) | |

| Corporate bonds & notes; convertible securities | Standard inputs and underlying equity of the issuer | |

| Bonds & notes of governments & government agencies | Standard inputs and interest rate volatilities | |

| Mortgage-backed; asset-backed obligations | Standard inputs and cash flows, prepayment information, default rates, delinquency and loss assumptions, collateral characteristics, credit enhancements and specific deal information |

When the fund’s investment adviser deems it appropriate to do so (such as when vendor prices are unavailable or not deemed to be representative), fixed-income securities will be valued in good faith at the mean quoted bid and ask prices that are reasonably and timely available (or bid prices, if ask prices are not available) or at prices for securities of comparable maturity, quality and type.

Securities with both fixed-income and equity characteristics, or equity securities traded principally among fixed-income dealers, are generally valued in the manner described for either equity or fixed-income securities, depending on which method is deemed most appropriate by the fund’s investment adviser. Forward currency contracts are valued at the mean of representative quoted bid and ask prices, generally based on prices supplied by one or more pricing vendors.

Securities and other assets for which representative market quotations are not readily available or are considered unreliable by the fund’s investment adviser are fair valued as determined in good faith under fair valuation guidelines adopted by authority of the fund’s board of trustees as further described. The investment adviser follows fair valuation guidelines, consistent with U.S. Securities and Exchange Commission rules and guidance, to consider relevant principles and factors when making fair value determinations. The investment adviser considers relevant indications of value that are reasonably and timely available to it in determining the fair value to

| 20 | International Growth and Income Fund |

be assigned to a particular security, such as the type and cost of the security; contractual or legal restrictions on resale of the security; relevant financial or business developments of the issuer; actively traded similar or related securities; conversion or exchange rights on the security; related corporate actions; significant events occurring after the close of trading in the security; and changes in overall market conditions. In addition, the closing prices of equity securities that trade in markets outside U.S. time zones may be adjusted to reflect significant events that occur after the close of local trading but before the net asset value of each share class of the fund is determined. Fair valuations and valuations of investments that are not actively trading involve judgment and may differ materially from valuations that would have been used had greater market activity occurred.

Processes and structure — The fund’s board of trustees has delegated authority to the fund’s investment adviser to make fair value determinations, subject to board oversight. The investment adviser has established a Joint Fair Valuation Committee (the “Fair Valuation Committee”) to administer, implement and oversee the fair valuation process, and to make fair value decisions. The Fair Valuation Committee regularly reviews its own fair value decisions, as well as decisions made under its standing instructions to the investment adviser’s valuation teams. The Fair Valuation Committee reviews changes in fair value measurements from period to period and may, as deemed appropriate, update the fair valuation guidelines to better reflect the results of back testing and address new or evolving issues. The Fair Valuation Committee reports any changes to the fair valuation guidelines to the board of trustees with supplemental information to support the changes. The fund’s board and audit committee also regularly review reports that describe fair value determinations and methods.

The fund’s investment adviser has also established a Fixed-Income Pricing Review Group to administer and oversee the fixed-income valuation process, including the use of fixed-income pricing vendors. This group regularly reviews pricing vendor information and market data. Pricing decisions, processes and controls over security valuation are also subject to additional internal reviews, including an annual control self-evaluation program facilitated by the investment adviser’s compliance group.

Classifications — The fund’s investment adviser classifies the fund’s assets and liabilities into three levels based on the inputs used to value the assets or liabilities. Level 1 values are based on quoted prices in active markets for identical securities. Level 2 values are based on significant observable market inputs, such as quoted prices for similar securities and quoted prices in inactive markets. Certain securities trading outside the U.S. may transfer between Level 1 and Level 2 due to valuation adjustments resulting from significant market movements following the close of local trading. Level 3 values are based on significant unobservable inputs that reflect the investment adviser’s determination of assumptions that market participants might reasonably use in valuing the securities. The valuation levels are not necessarily an indication of the risk or liquidity associated with the underlying investment. For example, U.S. government securities are reflected as Level 2 because the inputs used to determine fair value may not always be quoted prices in an active market. The following tables present the fund’s valuation levels as of June 30, 2014 (dollars in thousands):

| Investment securities | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Assets: | ||||||||||||||||

| Common stocks: | ||||||||||||||||

| Financials | $ | 2,472,939 | $ | — | $ | — | $ | 2,472,939 | ||||||||

| Consumer discretionary | 896,626 | — | — | 896,626 | ||||||||||||

| Energy | 840,560 | — | — | 840,560 | ||||||||||||

| Industrials | 706,560 | — | — | 706,560 | ||||||||||||

| Information technology | 654,101 | — | — | 654,101 | ||||||||||||

| Consumer staples | 619,996 | — | — | 619,996 | ||||||||||||

| Utilities | 567,556 | — | — | 567,556 | ||||||||||||

| Health care | 558,945 | — | — | 558,945 | ||||||||||||

| Telecommunication services | 449,716 | — | — | 449,716 | ||||||||||||

| Materials | 384,066 | 52,931 | — | 436,997 | ||||||||||||

| Miscellaneous | 204,744 | — | — | 204,744 | ||||||||||||

| Preferred securities | 1,225 | 12,825 | — | 14,050 | ||||||||||||

| Rights & warrants | 29,033 | 2,557 | — | 31,590 | ||||||||||||

| Convertible securities | — | 65,400 | — | 65,400 | ||||||||||||

| Bonds, notes & other debt instruments | — | 163,605 | — | 163,605 | ||||||||||||

| Short-term securities | — | 363,543 | — | 363,543 | ||||||||||||

| Total | $ | 8,386,067 | $ | 660,861 | $ | — | $ | 9,046,928 | ||||||||

| International Growth and Income Fund | 21 |

| Other investments* | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Liabilities: | ||||||||||||||||

| Unrealized depreciation on open forward currency contracts | $ | — | $ | (2,110 | ) | $ | — | $ | (2,110 | ) | ||||||

*Forward currency contracts are not included in the investment portfolio.

4. Risk factors

Investing in the fund may involve certain risks including, but not limited to, those described below.

Market conditions — The prices of, and the income generated by, the common stocks and other securities held by the fund may decline — sometimes rapidly or unpredictably — due to various factors, including events or conditions affecting the general economy or particular industries; overall market changes; local, regional or global political, social or economic instability; governmental or governmental agency responses to economic conditions; and currency, interest rate and commodity price fluctuations.

Issuer risks — The values of, and the income generated by, securities held by the fund may also decline in response to various factors directly related to the issuers of such securities, including reduced demand for an issuer’s goods or services, poor management performance and strategic initiatives such as mergers, acquisitions or dispositions and the market response to any such initiative.

Investing outside the U.S. — Securities of issuers domiciled outside the U.S., or with significant operations outside the U.S., may lose value because of adverse political, social, economic or market developments in the countries or regions in which the issuers operate. These securities may also lose value due to changes in foreign currency exchange rates against the U.S. dollar and/or currencies of other countries. Securities markets in certain countries may be more volatile and/or less liquid than those in the U.S. Investments outside the U.S. may also be subject to different accounting practices and different regulatory, legal and reporting standards, and may be more difficult to value, than those in the U.S. In addition, the value of investments outside the U.S. may be reduced by foreign taxes, including foreign withholding taxes on interest and dividends. Further, there may be increased risks of delayed settlement of securities purchased or sold by the fund. The risks of investing outside the U.S. may be heightened in connection with investments in emerging markets.

Investing in emerging markets — Investing in emerging markets may involve risks in addition to and greater than those generally associated with investing in the securities markets of developed countries. For instance, developing countries may have less developed legal and accounting systems than those in developed countries. The governments of these countries may be less stable and more likely to impose capital controls, nationalize a company or industry, place restrictions on foreign ownership and on withdrawing sale proceeds of securities from the country, and/or impose punitive taxes that could adversely affect the prices of securities. In addition, the economies of these countries may be dependent on relatively few industries that are more susceptible to local and global changes. Securities markets in these countries can also be relatively small and have substantially lower trading volumes. As a result, securities issued in these countries may be more volatile and less liquid, and may be more difficult to value, than securities issued in countries with more developed economies and/or markets. Additionally, there may be increased settlement risks for transactions in local securities.

Investing in growth-oriented stocks — Growth-oriented common stocks and other equity-type securities (such as preferred stocks, convertible preferred stocks and convertible bonds) may involve larger price swings and greater potential for loss than other types of investments.

Investing in income-oriented stocks — Income provided by the fund may be reduced by changes in the dividend policies of, and the capital resources available for dividend payments at, the companies in which the fund invests.

Management — The investment adviser to the fund actively manages the fund’s investments. Consequently, the fund is subject to the risk that the methods and analyses employed by the investment adviser in this process may not produce the desired results. This could cause the fund to lose value or its investment results to lag relevant benchmarks or other funds with similar objectives.

| 22 | International Growth and Income Fund |

5. Certain investment techniques

Forward currency contracts — The fund has entered into forward currency contracts, which represent agreements to exchange currencies on specific future dates at predetermined rates. The fund’s investment adviser uses forward currency contracts to manage the fund’s exposure to changes in exchange rates. Upon entering into these contracts, risks may arise from the potential inability of counterparties to meet the terms of their contracts and from possible movements in exchange rates.

On a daily basis, the fund’s investment adviser values forward currency contracts and records unrealized appreciation or depreciation for open forward currency contracts in the fund’s statement of assets and liabilities. Realized gains or losses are recorded at the time the forward currency contract is closed or offset by another contract with the same broker for the same settlement date and currency.

Closed forward currency contracts that have not reached their settlement date are included in the respective receivables or payables for closed forward currency contracts in the fund’s statement of assets and liabilities. Net realized gains or losses from closed forward currency contracts and net unrealized appreciation or depreciation from open forward currency contracts are recorded in the fund’s statement of operations.

The following tables present the financial statement impacts resulting from the fund’s use of forward currency contracts as of June 30, 2014 (dollars in thousands):

| Asset | Liability | ||||||||||||

| Contract | Location on statement of assets and liabilities | Value | Location on statement of assets and liabilities | Value | |||||||||

| Forward currency | Unrealized appreciation on open forward currency contracts | $ | — | Unrealized depreciation on open forward currency contracts | $ | 2,110 | |||||||

| Net realized gain | Net unrealized depreciation | ||||||||||||

| Contract | Location on statement of operations | Value | Location on statement of operations | Value | |||||||||

| Forward currency | Net realized gain on forward currency contracts | $ | 7,221 | Net unrealized depreciation on forward currency contracts | $ | (4,654) | |||||||

Collateral — The fund participates in a collateral program due to its use of forward currency contracts. The program calls for the fund to either receive or pledge collateral based on the net gain or loss on unsettled forward currency contracts by counterparty. The purpose of the collateral is to cover potential losses that could occur in the event that either party cannot meet its contractual obligations.

Rights of offset — The fund has entered into enforceable master netting agreements with certain counterparties for forward currency contracts, where amounts payable by each party to the other in the same currency, with the same settlement date and with the same counterparty are settled net of each party’s payment obligation. For financial reporting purposes, the fund does not offset financial assets and financial liabilities that are subject to netting arrangements in the statement of assets and liabilities.

The following table presents the fund’s forward currency contracts by counterparty, including those that are subject to potential offset on the statement of assets and liabilities as of June 30, 2014 (dollars in thousands):

| Gross amounts recognized in the | Gross amounts not offset in the statement of assets and liabilities and subject to a master netting agreement | |||||||||||||||||||||

| Counterparty | statement of assets and liabilities | Available to offset | Non-cash collateral* | Cash collateral | Net amount | |||||||||||||||||

| Liabilities: | Bank of America, N.A. | $ | 440 | $ | — | $ | (97 | ) | $ | — | $ | 343 | ||||||||||

| Bank of New York Mellon | 819 | — | (629 | ) | — | 190 | ||||||||||||||||

| Citibank | 130 | — | — | — | 130 | |||||||||||||||||

| HSBC Bank | 541 | — | — | — | 541 | |||||||||||||||||

| UBS AG | 180 | — | — | — | 180 | |||||||||||||||||

| $ | 2,110 | $ | — | $ | (726 | ) | $ | — | $ | 1,384 | ||||||||||||

*Non-cash collateral is shown on a settlement basis.

| International Growth and Income Fund | 23 |

6. Taxation and distributions

Federal income taxation — The fund complies with the requirements under Subchapter M of the Internal Revenue Code applicable to mutual funds and intends to distribute substantially all of its net taxable income and net capital gains each year. The fund is not subject to income taxes to the extent such distributions are made. Therefore, no federal income tax provision is required.

As of and during the period ended June 30, 2014, the fund did not have a liability for any unrecognized tax benefits. The fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the statement of operations. During the period, the fund did not incur any interest or penalties.

The fund is not subject to examination by U.S. federal tax authorities for tax years before 2010, by state tax authorities for tax years before 2009 and by tax authorities outside the U.S. for tax years before 2011.

Non-U.S. taxation — Dividend and interest income are recorded net of non-U.S. taxes paid. Gains realized by the fund on the sale of securities in certain countries are subject to non-U.S. taxes. The fund records a liability based on unrealized gains to provide for potential non-U.S. taxes payable upon the sale of these securities.

Distributions — Distributions paid to shareholders are based on net investment income and net realized gains determined on a tax basis, which may differ from net investment income and net realized gains for financial reporting purposes. These differences are due primarily to different treatment for items such as currency gains and losses; short-term capital gains and losses; capital losses related to sales of certain securities within 30 days of purchase; unrealized appreciation of certain investments in securities outside the U.S.; and cost of investments sold. The fiscal year in which amounts are distributed may differ from the year in which the net investment income and net realized gains are recorded by the fund for financial reporting purposes. The fund may also designate a portion of the amount paid to redeeming shareholders as a distribution for tax purposes.

During the year ended June 30, 2014, the fund reclassified $5,000 from undistributed net investment income and $6,046,000 from undistributed net realized gain to capital paid in on shares of beneficial interest and $12,615,000 from undistributed net realized gain to undistributed net investment income to align financial reporting with tax reporting.

As of June 30, 2014, the tax-basis components of distributable earnings, unrealized appreciation (depreciation) and cost of investment securities were as follows (dollars in thousands):

| Undistributed ordinary income | $ | 21,491 | ||

| Undistributed long-term capital gains | 159,852 | |||

| Gross unrealized appreciation on investment securities | 1,890,315 | |||

| Gross unrealized depreciation on investment securities | (132,173 | ) | ||

| Net unrealized appreciation on investment securities | 1,758,142 | |||

| Cost of investment securities | 7,288,786 |

| 24 | International Growth and Income Fund |

The tax character of distributions paid to shareholders was as follows (dollars in thousands):

| Year ended June 30, 2014 | Year ended June 30, 2013 | |||||||||||||||||||||||

| Ordinary | Long-term | Total distributions | Ordinary | Long-term | Total distributions | |||||||||||||||||||

| Share class | income | capital gains | paid | income | capital gains | paid | ||||||||||||||||||

| Class A | $ | 151,235 | $ | 166,941 | $ | 318,176 | $ | 95,896 | $ | — | $ | 95,896 | ||||||||||||

| Class B | 420 | 657 | 1,077 | 348 | — | 348 | ||||||||||||||||||

| Class C | 7,109 | 10,102 | 17,211 | 4,138 | — | 4,138 | ||||||||||||||||||

| Class F-1 | 36,770 | 38,807 | 75,577 | 18,507 | — | 18,507 | ||||||||||||||||||

| Class F-2 | 34,585 | 33,681 | 68,266 | 18,570 | — | 18,570 | ||||||||||||||||||

| Class 529-A | 3,799 | 4,247 | 8,046 | 2,280 | — | 2,280 | ||||||||||||||||||

| Class 529-B | 17 | 28 | 45 | 15 | — | 15 | ||||||||||||||||||

| Class 529-C | 731 | 1,066 | 1,797 | 400 | — | 400 | ||||||||||||||||||

| Class 529-E | 126 | 156 | 282 | 71 | — | 71 | ||||||||||||||||||

| Class 529-F-1 | 318 | 336 | 654 | 160 | — | 160 | ||||||||||||||||||

| Class R-1 | 225 | 242 | 467 | 123 | — | 123 | ||||||||||||||||||

| Class R-2 | 1,226 | 1,746 | 2,972 | 717 | — | 717 | ||||||||||||||||||

| Class R-3 | 1,210 | 1,499 | 2,709 | 708 | — | 708 | ||||||||||||||||||

| Class R-4 | 1,267 | 1,286 | 2,553 | 607 | — | 607 | ||||||||||||||||||

| Class R-5 | 1,447 | 1,877 | 3,324 | 1,132 | — | 1,132 | ||||||||||||||||||

| Class R-6 | 29,096 | 28,443 | 57,539 | 15,652 | — | 15,652 | ||||||||||||||||||

| Total | $ | 269,581 | $ | 291,114 | $ | 560,695 | $ | 159,324 | $ | — | $ | 159,324 | ||||||||||||