Exhibit(c)(4)

|

Clearwire

Board of Directors Presentation December 12, 2012

Evercore Partners

These materials have been prepared by Evercore Group L.L.C. (“Evercore”) for the Board of Directors of Clearwire Corporation (the “Company”) to whom such materials are directly addressed and delivered and may not be used or relied upon for any purpose other than as specifically contemplated by a written agreement with Evercore. These materials are based on information provided by or on behalf of the Company and/or other potential transaction participants, from public sources or otherwise reviewed by Evercore. Evercore assumes no responsibility for independent investigation or verification of such information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates and forecasts of future financial performance prepared by or reviewed with the management of the Company and/or other potential transaction participants or obtained from public sources, Evercore has assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such management (or, with respect to estimates and forecasts obtained from public sources, represent reasonable estimates). Evercore has not made nor assumed any responsibility for making any independent valuation or appraisal of the assets or liabilities of the Company, nor has Evercore been furnished with any such appraisals. No representation or warranty, express or implied, is made as to the accuracy or completeness of such information and nothing contained herein is, or shall be relied upon as, a representation, whether as to the past, the present or the future. These materials were designed for use by specific persons familiar with the business and affairs of the Company. These materials are not intended to provide the sole basis for evaluating, and should not be considered a recommendation with respect to, any transaction or other matter. These materials have been developed by and are proprietary to Evercore and were prepared exclusively for the benefit and internal use of the Board of Directors of the Company.

These materials were compiled on a confidential basis for use by the Board of Directors of the Company in evaluating the potential transaction described herein and not with a view to public disclosure or filing thereof under state or federal securities laws, and may not be reproduced, disseminated, quoted or referred to, in whole or in part, without the prior written consent of Evercore.

These materials do not constitute an offer or solicitation to sell or purchase any securities and are not a commitment by Evercore (or any affiliate) to provide or arrange any financing for any transaction or to purchase any security in connection therewith. Evercore assumes no obligation to update or otherwise revise these materials. These materials may not reflect information known to other professionals in other business areas of Evercore and its affiliates.

Evercore and its affiliates do not provide legal, accounting or tax advice. Accordingly, any statements contained herein as to tax matters were neither written nor intended by Evercore or its affiliates to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on such taxpayer. Each person should seek legal, accounting and tax advice based on his, her or its particular circumstances from independent advisors regarding the impact of the transactions or matters described herein.

Evercore Partners

Table of Contents

Preliminary Draft - Confidential

Section

Transaction Overview I

Valuation Analysis II

Appendix

Evercore Partners

I. Transaction Overview

Evercore Partners

Transaction Overview

Preliminary Draft - Confidential

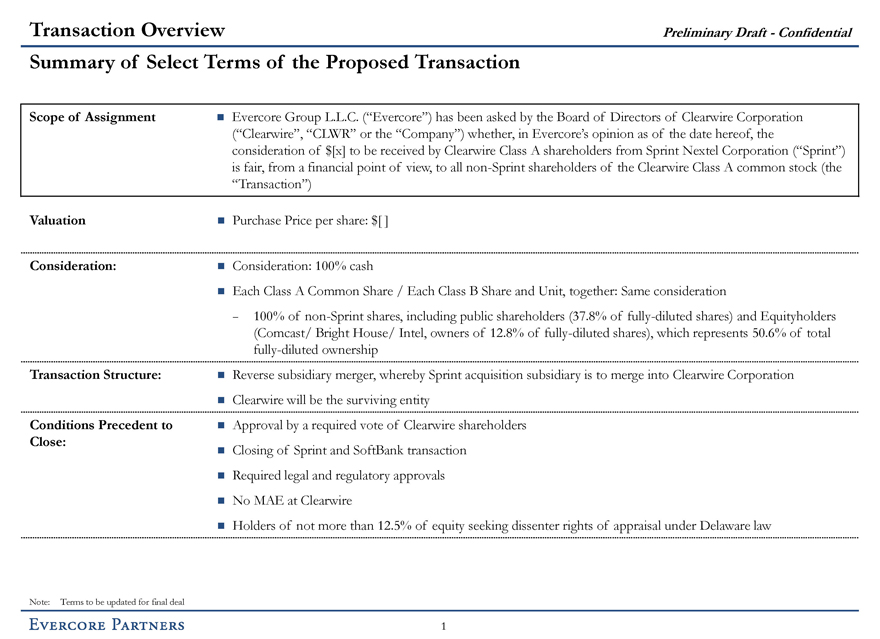

Summary of Select Terms of the Proposed Transaction

Scope of Assignment

Evercore Group L.L.C. (“Evercore”) has been asked by the Board of Directors of Clearwire Corporation (“Clearwire”, “CLWR” or the “Company”) whether, in Evercore’s opinion as of the date hereof, the consideration of $[x] to be received by Clearwire Class A shareholders from Sprint Nextel Corporation (“Sprint”) is fair, from a financial point of view, to all non-Sprint shareholders of the Clearwire Class A common stock (the “Transaction”)

Valuation

Purchase Price per share: $[ ]

Consideration:

Consideration: 100% cash

Each Class A Common Share / Each Class B Share and Unit, together: Same consideration

- 100% of non-Sprint shares, including public shareholders (37.8% of fully-diluted shares) and Equityholders (Comcast/ Bright House/ Intel, owners of 12.8% of fully-diluted shares), which represents 50.6% of total fully-diluted ownership

Transaction Structure:

Reverse subsidiary merger, whereby Sprint acquisition subsidiary is to merge into Clearwire Corporation

Clearwire will be the surviving entity

Conditions Precedent to Close:

Approval by a required vote of Clearwire shareholders

Closing of Sprint and SoftBank transaction

Required legal and regulatory approvals

No MAE at Clearwire

Holders of not more than 12.5% of equity seeking dissenter rights of appraisal under Delaware law

Note: Terms to be updated for final deal

Evercore Partners

1

Transaction Overview

Preliminary Draft - Confidential

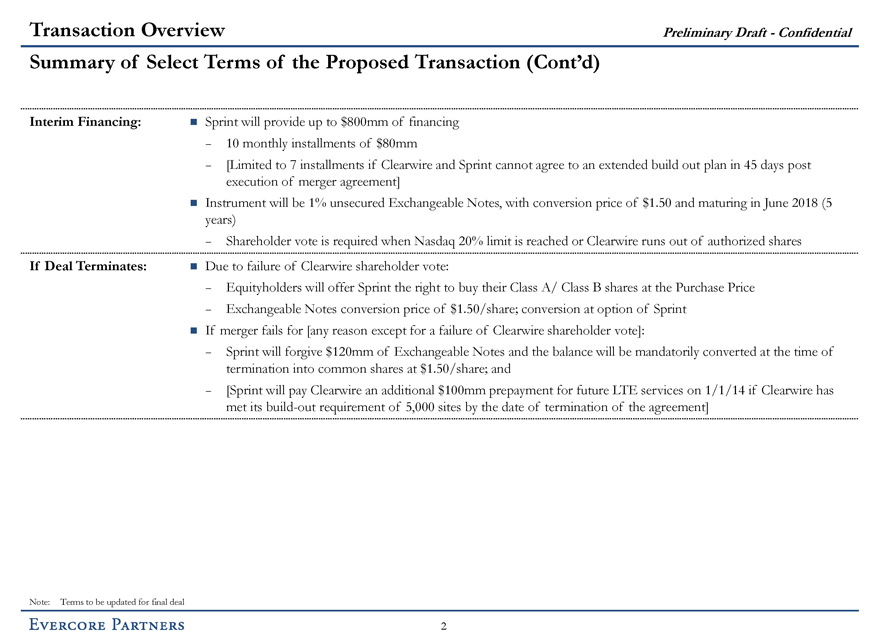

Summary of Select Terms of the Proposed Transaction (Cont’d)

Interim Financing:

Sprint will provide up to $800mm of financing

- 10 monthly installments of $80mm

- [Limited to 7 installments if Clearwire and Sprint cannot agree to an extended build out plan in 45 days post execution of merger agreement]

Instrument will be 1% unsecured Exchangeable Notes, with conversion price of $1.50 and maturing in June 2018 (5 years)

- Shareholder vote is required when Nasdaq 20% limit is reached or Clearwire runs out of authorized shares

If Deal Terminates:

Due to failure of Clearwire shareholder vote:

- Equityholders will offer Sprint the right to buy their Class A/ Class B shares at the Purchase Price

- Exchangeable Notes conversion price of $1.50/share; conversion at option of Sprint

If merger fails for [any reason except for a failure of Clearwire shareholder vote]:

- Sprint will forgive $120mm of Exchangeable Notes and the balance will be mandatorily converted at the time of termination into common shares at $1.50/share; and

- [Sprint will pay Clearwire an additional $100mm prepayment for future LTE services on 1/1/14 if Clearwire has met its build-out requirement of 5,000 sites by the date of termination of the agreement]

Note: Terms to be updated for final deal

Evercore Partners

2

Transaction Overview

Preliminary Draft - Confidential

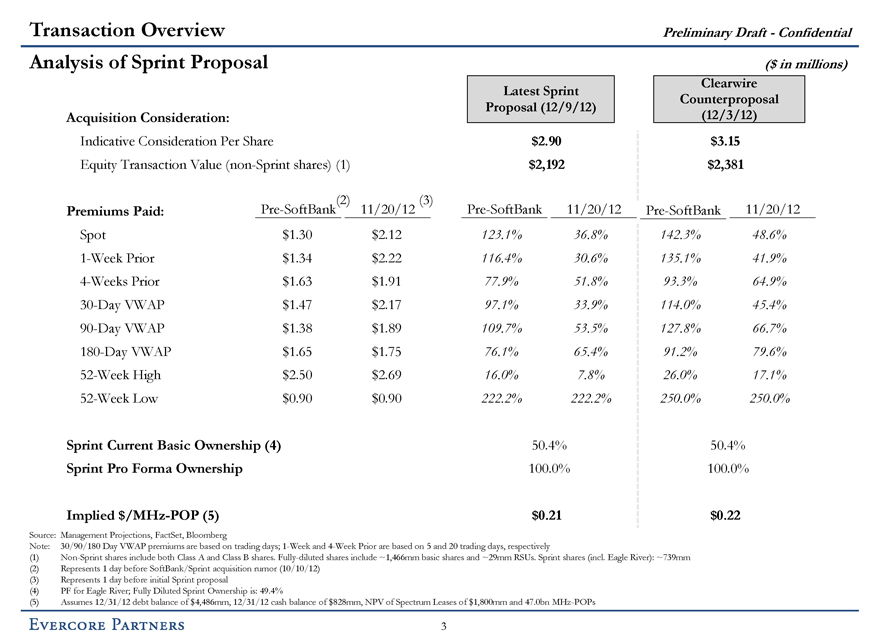

Analysis of Sprint Proposal

($ in millions)

Acquisition Consideration:

Latest Sprint Proposal (12/9/12)

Clearwire Counterproposal (12/3/12)

Indicative Consideration Per Share

$2.90 $3.15

Equity Transaction Value (non-Sprint shares) (1)

$2,192 $2,381

Premiums Paid:

Pre-SoftBank(2)

11/20/12 (3)

Pre-SoftBank

11/20/12

Pre-SoftBank

11/20/12

Spot

$1.30 $2.12 123.1% 36.8% 142.3% 48.6%

1-Week Prior

$1.34 $2.22 116.4% 30.6% 135.1% 41.9%

4-Weeks Prior

$1.63 $1.91 77.9% 51.8% 93.3% 64.9%

30-Day VWAP

$1.47 $2.17 97.1% 33.9% 114.0% 45.4%

90-Day VWAP

$1.38 $1.89 109.7% 53.5% 127.8% 66.7%

180-Day VWAP

$1.65 $1.75 76.1% 65.4% 91.2% 79.6%

52-Week High

$2.50 $2.69 16.0% 7.8% 26.0% 17.1%

52-Week Low

$0.90 $0.90 222.2% 222.2% 250.0% 250.0%

Sprint Current Basic Ownership (4)

50.4% 50.4%

Sprint Pro Forma Ownership

100.0% 100.0%

Implied $/MHz-POP (5)

$0.21

$0.22

Source: Management Projections, FactSet, Bloomberg

Note: 30/90/180 Day VWAP premiums are based on trading days; 1-Week and 4-Week Prior are based on 5 and 20 trading days, respectively

(1) Non-Sprint shares include both Class A and Class B shares. Fully-diluted shares include ~1,466mm basic shares and ~29mm RSUs. Sprint shares (incl. Eagle River): ~739mm

(2) Represents 1 day before SoftBank/Sprint acquisition rumor (10/10/12)

(3) Represents 1 day before initial Sprint proposal

(4) PF for Eagle River; Fully Diluted Sprint Ownership is: 49.4%

(5) Assumes 12/31/12 debt balance of $4,486mm, 12/31/12 cash balance of $828mm, NPV of Spectrum Leases of $1,800mm and 47.0bn MHz-POPs

Evercore Partners

3

Transaction Overview

Preliminary Draft - Confidential

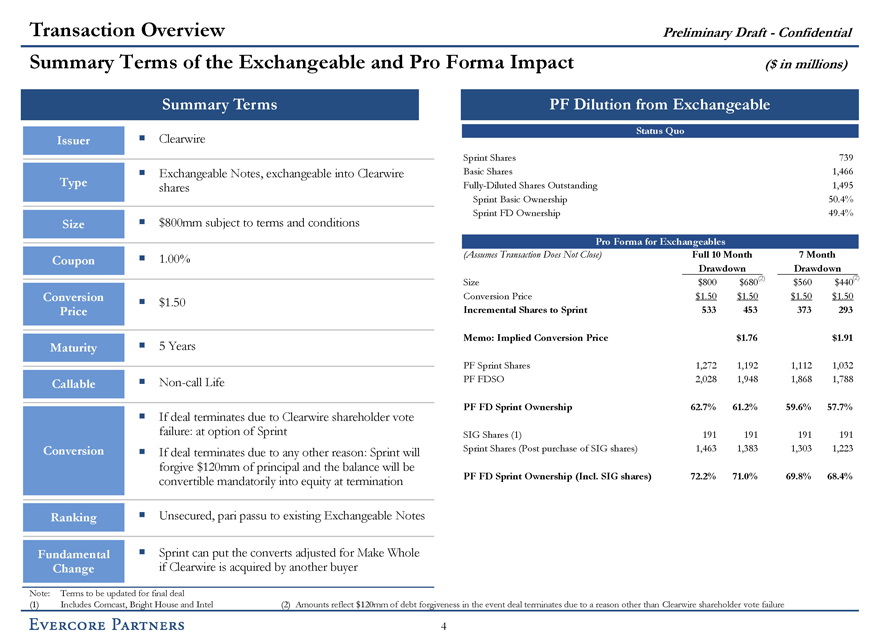

Summary Terms of the Exchangeable and Pro Forma Impact

($ in millions)

Summary Terms

Issuer

Clearwire

Type

Exchangeable Notes, exchangeable into Clearwire shares

Size

$800mm subject to terms and conditions

Coupon

1.00%

Conversion Price

$1.50

Maturity

5 Years

Callable

Non-call Life

If deal terminates due to Clearwire shareholder vote failure: at option of Sprint

Conversion

If deal terminates due to any other reason: Sprint will forgive $120mm of principal and the balance will be convertible mandatorily into equity at termination

Ranking

Unsecured, pari passu to existing Exchangeable Notes

Fundamental Change

Sprint can put the converts adjusted for Make Whole if Clearwire is acquired by another buyer

PF Dilution from Exchangeable

Status Quo

Sprint Shares 739

Basic Shares 1,466

Fully-Diluted Shares Outstanding 1,495

Sprint Basic Ownership 50.4%

Sprint FD Ownership 49.4%

Pro Forma for Exchangeables

(Assumes Transaction Does Not Close)

Full 10 Month Drawdown

7 Month Drawdown

Size

$800 $680(2)

$560

$440(2)

Conversion Price

$1.50 $1.50 $1.50 $1.50

Incremental Shares to Sprint

533 453 373 293

Memo: Implied Conversion Price

$1.76 $1.91

PF Sprint Shares

1,272 1,192 1,112 1,032

PF FDSO

2,028 1,948 1,868 1,788

PF FD Sprint Ownership

62.7% 61.2% 59.6% 57.7%

SIG Shares (1)

191 191 191 191

Sprint Shares (Post purchase of SIG shares)

1,463 1,383 1,303 1,223

PF FD Sprint Ownership (Incl. SIG shares)

72.2% 71.0% 69.8% 68.4%

Note: Terms to be updated for final deal

(1) Includes Comcast, Bright House and Intel

(2) Amounts reflect $120mm of debt forgiveness in the event deal terminates due to a reason other than Clearwire shareholder vote failure

Evercore Partners

4

Transaction Overview

Preliminary Draft - Confidential

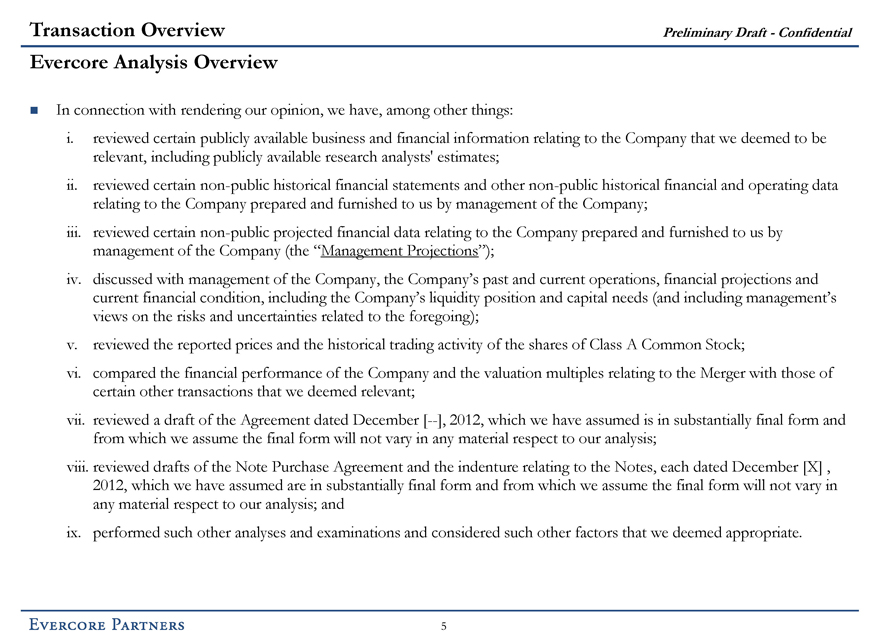

Evercore Analysis Overview

In connection with rendering our opinion, we have, among other things:

i. reviewed certain publicly available business and financial information relating to the Company that we deemed to be relevant, including publicly available research analysts’ estimates;

ii. reviewed certain non-public historical financial statements and other non-public historical financial and operating data relating to the Company prepared and furnished to us by management of the Company;

iii. reviewed certain non-public projected financial data relating to the Company prepared and furnished to us by management of the Company (the “Management Projections”);

iv. discussed with management of the Company, the Company’s past and current operations, financial projections and current financial condition, including the Company’s liquidity position and capital needs (and including management’s views on the risks and uncertainties related to the foregoing);

v. reviewed the reported prices and the historical trading activity of the shares of Class A Common Stock;

vi. compared the financial performance of the Company and the valuation multiples relating to the Merger with those of certain other transactions that we deemed relevant;

vii. reviewed a draft of the Agreement dated December [--], 2012, which we have assumed is in substantially final form and from which we assume the final form will not vary in any material respect to our analysis;

viii. reviewed drafts of the Note Purchase Agreement and the indenture relating to the Notes, each dated December [X] , 2012, which we have assumed are in substantially final form and from which we assume the final form will not vary in any material respect to our analysis; and

ix. performed such other analyses and examinations and considered such other factors that we deemed appropriate.

Evercore Partners

5

Transaction Overview

Preliminary Draft - Confidential

Evercore Analysis Overview (Cont’d)

For purposes of our analysis and opinion, we have assumed and relied upon, without undertaking any independent verification of, the accuracy and completeness of all of the information publicly available, and all of the information supplied or otherwise made available to, discussed with, or reviewed by us, and we assume no liability therefor.

We have assumed that the Management Projections have been reasonably prepared on bases reflecting the best currently available estimates and good faith judgments of management of the Company as to the future financial performance of the Company under the business assumptions reflected therein. We have not made nor assumed any responsibility for making any independent valuation or appraisal of the assets or liabilities of the Company, nor have we been furnished with any such appraisals.

We have also assumed that there have been no material changes in the Company’s assets, financial condition, results of operations, business or prospects since the date of its last financial statement made available to us. We express no view as to any projected financial data relating to the Company or the assumptions on which they are based.

We were not authorized to solicit, and did not solicit, interest from any third party with respect to the acquisition of any or all of the shares of Company Common Stock or any business combination or other extraordinary transaction involving the Company.

The full text of our opinion provided with this presentation sets forth assumptions made, matters considered and limitations on the review undertaken in conjunction with the opinion. You are urged to read the opinion carefully and in its entirety.

Evercore Partners

6

|

Transaction Overview

Preliminary Draft - Confidential

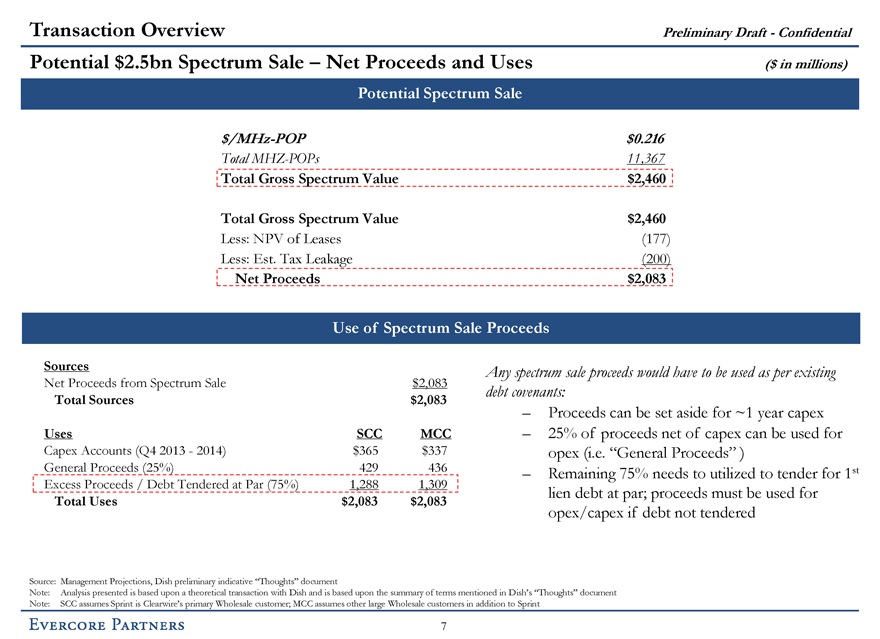

Potential $2.5bn Spectrum Sale - Net Proceeds and Uses

($ in millions)

Potential Spectrum Sale

$/MHz-POP

$0.216

Total MHZ-POPs

11,367

Total Gross Spectrum Value

$2,460

Total Gross Spectrum Value

$2,460

Less: NPV of Leases

(177)

Less: Est. Tax Leakage

(200)

Net Proceeds

$2,083

Use of Spectrum Sale Proceeds

Sources

Net Proceeds from Spectrum Sale

$2,083

Total Sources

$2,083

Uses

SCC

MCC

Capex Accounts (Q4 2013 - 2014)

$365

$337

General Proceeds (25%)

429

436

Excess Proceeds / Debt Tendered at Par (75%)

1,288

1,309

Total Uses

$2,083

$2,083

Any spectrum sale proceeds would have to be used as per existing debt covenants:

– Proceeds can be set aside for ~1 year capex

– 25% of proceeds net of capex can be used for opex (i.e. “General Proceeds” )

– Remaining 75% needs to utilized to tender for 1st lien debt at par; proceeds must be used for opex/capex if debt not tendered

Source: Management Projections, Dish preliminary indicative “Thoughts” document

Note: Analysis presented is based upon a theoretical transaction with Dish and is based upon the summary of terms mentioned in Dish’s “Thoughts” document

Note: SCC assumes Sprint is Clearwire’s primary Wholesale customer; MCC assumes other large Wholesale customers in addition to Sprint

Evercore Partners

7

|

Transaction Overview

Preliminary Draft - Confidential

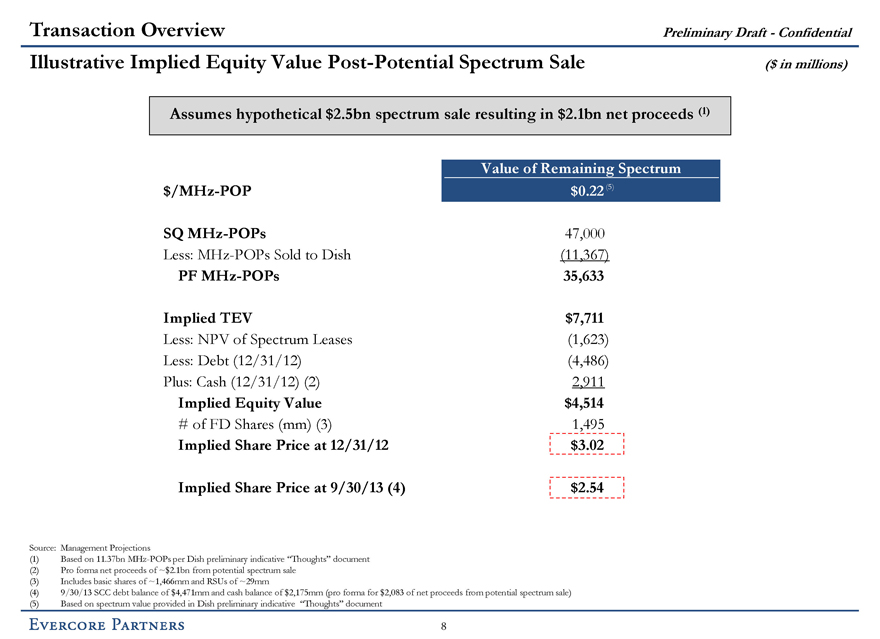

Illustrative Implied Equity Value Post-Potential Spectrum Sale

($ in millions)

Assumes hypothetical $2.5bn spectrum sale resulting in $2.1bn net proceeds (1)

Value of Remaining Spectrum

$/MHz-POP

$0.22 (5)

SQ MHz-POPs

47,000

Less: MHz-POPs Sold to Dish

(11,367)

PF MHz-POPs

35,633

Implied TEV

$7,711

Less: NPV of Spectrum Leases

(1,623)

Less: Debt (12/31/12)

(4,486)

Plus: Cash (12/31/12) (2)

2,911

Implied Equity Value

$4,514

# of FD Shares (mm) (3)

1,495

Implied Share Price at 12/31/12

$3.02

Implied Share Price at 9/30/13 (4)

$2.54

Source: Management Projections

(1) Based on 11.37bn MHz-POPs per Dish preliminary indicative “Thoughts” document

(2) Pro forma net proceeds of ~$2.1bn from potential spectrum sale

(3) Includes basic shares of ~1,466mm and RSUs of ~29mm

(4) 9/30/13 SCC debt balance of $4,471mm and cash balance of $2,175mm (pro forma for $2,083 of net proceeds from potential spectrum sale)

(5) Based on spectrum value provided in Dish preliminary indicative “Thoughts” document

Evercore Partners

8

|

II. Valuation Analysis

Evercore Partners

Valuation Analysis

Preliminary Draft - Confidential

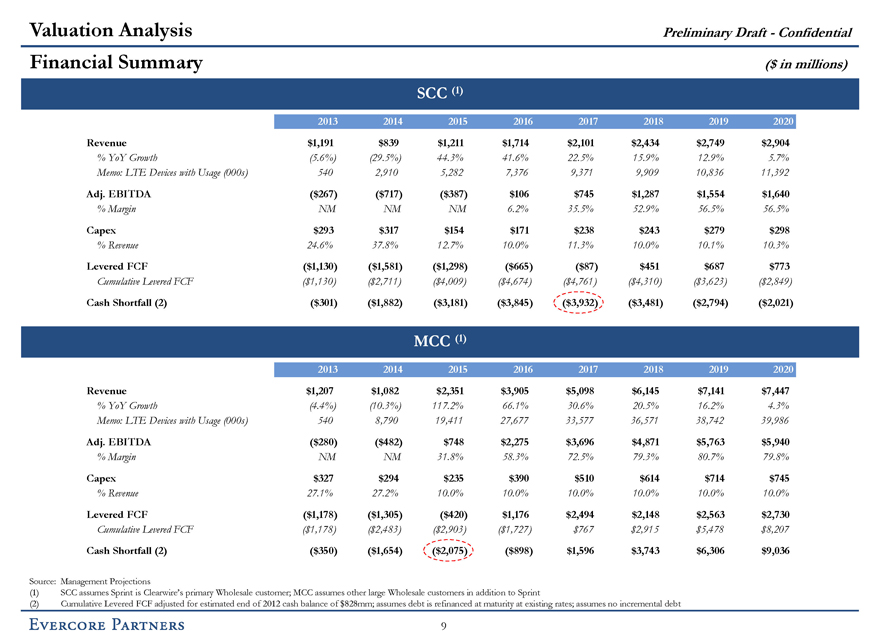

Financial Summary

($ in millions)

SCC (1)

2013 2014 2015 2016 2017 2018 2019 2020

Revenue

$1,191 $839 $1,211 $1,714 $2,101 $2,434 $2,749 $2,904

% YoY Growth

(5.6%) (29.5%) 44.3% 41.6% 22.5% 15.9% 12.9% 5.7%

Memo: LTE Devices with Usage (000s)

540 2,910 5,282 7,376 9,371 9,909 10,836 11,392

Adj. EBITDA

($267) ($717) ($387) $106 $745 $1,287 $1,554 $1,640

% Margin

NM NM NM 6.2% 35.5% 52.9% 56.5% 56.5%

Capex

$293 $317 $154 $171 $238 $243 $279 $298

% Revenue

24.6% 37.8% 12.7% 10.0% 11.3% 10.0% 10.1% 10.3%

Levered FCF

($1,130) ($1,581) ($1,298) ($665) ($87) $451 $687 $773

Cumulative Levered FCF

($1,130) ($2,711) ($4,009) ($4,674) ($4,761) ($4,310) ($3,623) ($2,849)

Cash Shortfall (2)

($301) ($1,882) ($3,181) ($3,845) ($3,932) ($3,481) ($2,794) ($2,021)

MCC (1)

2013 2014 2015 2016 2017 2018 2019 2020

Revenue

$1,207 $1,082 $2,351 $3,905 $5,098 $6,145 $7,141 $7,447

% YoY Growth

(4.4%) (10.3%) 117.2% 66.1% 30.6% 20.5% 16.2% 4.3%

Memo: LTE Devices with Usage (000s)

540 8,790 19,411 27,677 33,577 36,571 38,742 39,986

Adj. EBITDA

($280) ($482) $748 $2,275 $3,696 $4,871 $5,763 $5,940

% Margin

NM NM 31.8% 58.3% 72.5% 79.3% 80.7% 79.8% Capex $327 $294 $235 $390 $510 $614 $714 $745

% Revenue

27.1% 27.2% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0%

Levered FCF

($1,178) ($1,305) ($420) $1,176 $2,494 $2,148 $2,563 $2,730

Cumulative Levered FCF

($1,178) ($2,483) ($2,903) ($1,727) $767 $2,915 $5,478 $8,207

Cash Shortfall (2)

($350) ($1,654) ($2,075) ($898) $1,596 $3,743 $6,306 $9,036

Source: Management Projections

(1) SCC assumes Sprint is Clearwire’s primary Wholesale customer; MCC assumes other large Wholesale customers in addition to Sprint

(2) Cumulative Levered FCF adjusted for estimated end of 2012 cash balance of $828mm; assumes debt is refinanced at maturity at existing rates; assumes no incremental debt

Evercore Partners

9

Valuation Analysis

Preliminary Draft - Confidential

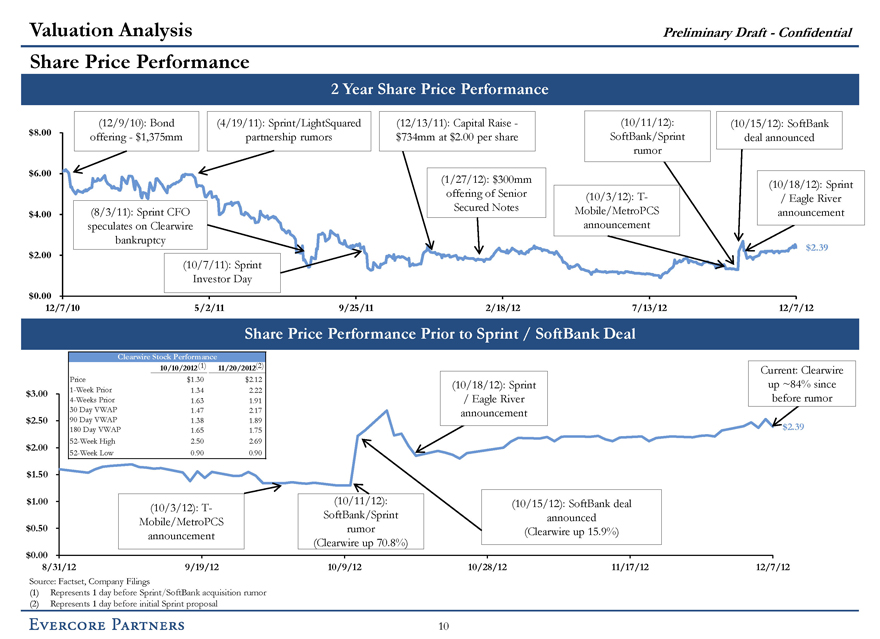

Share Price Performance

2 Year Share Price Performance

$8.00

$6.00

$4.00

$2.00

$0.00

(12/9/10): Bond offering - $1,375mm

(4/19/11): Sprint/LightSquared partnership rumors

(12/13/11): Capital Raise - $734mm at $2.00 per share

(10/11/12): SoftBank/Sprint rumor

(10/15/12): SoftBank deal announced

(1/27/12): $300mm offering of Senior Secured Notes

(10/3/12): T-Mobile/MetroPCS announcement

(10/18/12): Sprint / Eagle River announcement

(8/3/11): Sprint CFO speculates on Clearwire bankruptcy

$2.39

(10/7/11): Sprint Investor Day

12/7/10

5/2/11

9/25/11

2/18/12

7/13/12

12/7/12

Share Price Performance Prior to Sprint / SoftBank Deal

Clearwire Stock Performance

10/10/2012 (1)

11/20/2012 (2)

Price

$1.30 $2.12

1-Week Prior

1.34 2.22

4-Weeks Prior

1.63 1.91

30 Day VWAP

1.47 2.17

90 Day VWAP

1.38 1.89

180 Day VWAP

1.65 1.75

52-Week High

2.50 2.69

52-Week Low

0.90 0.90

$3.00

$2.50

$2.00

$1.50

$1.00

$0.50

$0.00

(10/18/12): Sprint / Eagle River announcement

Current: Clearwire up ~84% since before rumor

$2.39

(10/3/12): T-Mobile/MetroPCS announcement

(10/11/12): SoftBank/Sprint rumor (Clearwire up 70.8%)

(10/15/12): SoftBank deal announced (Clearwire up 15.9%)

8/31/12

9/19/12

10/9/12

10/28/12

11/17/12

12/7/12

Source: Factset, Company Filings

(1) Represents 1 day before Sprint/SoftBank acquisition rumor

(2) Represents 1 day before initial Sprint proposal

Evercore Partners

10

Valuation Analysis

Preliminary Draft - Confidential

($ in millions)

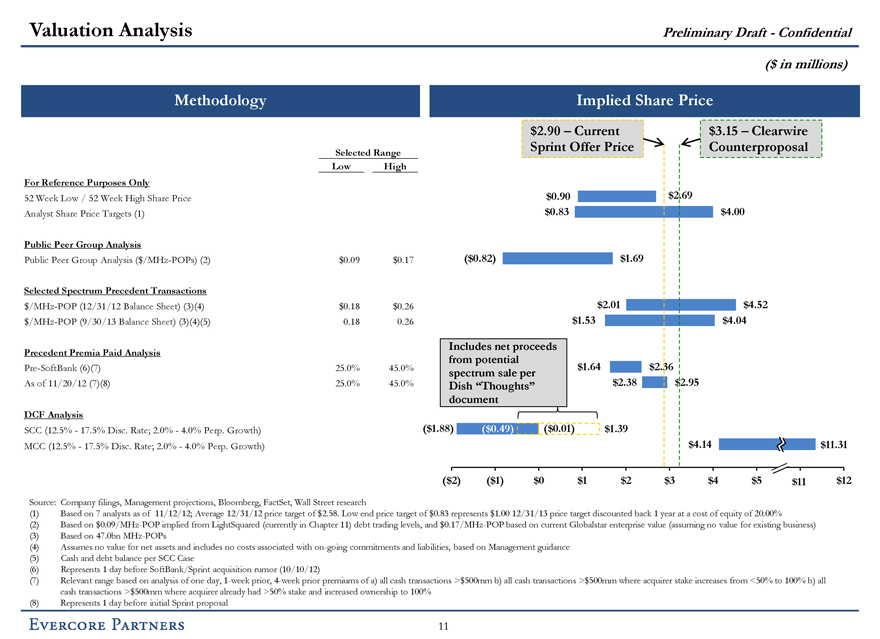

Methodology

Implied Share Price

Selected Range

Low High

For Reference Purposes Only

52 Week Low / 52 Week High Share Price

Analyst Share Price Targets (1)

Public Peer Group Analysis

Public Peer Group Analysis ($/MHz-POPs) (2)

$0.09 $0.17

Selected Spectrum Precedent Transactions

$/MHz-POP (12/31/12 Balance Sheet) (3)(4)

$0.18 $0.26

$/MHz-POP (9/30/13 Balance Sheet) (3)(4)(5)

0.18 0.26

Precedent Premia Paid Analysis

Pre-SoftBank (6)(7)

25.0% 45.0%

As of 11/20/12 (7)(8)

25.0% 45.0%

DCF Analysis

SCC (12.5% - 17.5% Disc. Rate; 2.0% - 4.0% Perp. Growth)

MCC (12.5% - 17.5% Disc. Rate; 2.0% - 4.0% Perp. Growth)

$2.90 - Current Sprint Offer Price

$3.15 - Clearwire Counterproposal

$0.90 $2.69

$0.83 $4.00

($0.82) $1.69

$2.01

$4.52

$1.53

$4.04

Includes net proceeds from potential spectrum sale per Dish “Thoughts” document

$ 1.64

$2.36

$2.38

$2.95

$1.88)

($0.49)

($0.01)

$1.39

$4.14

$11.31

($2)

($1)

$0

$1

$2

$3

$4

$5

$11

$12

Source: Company filings, Management projections, Bloomberg, FactSet, Wall Street research

(1) Based on 7 analysts as of 11/12/12; Average 12/31/12 price target of $2.58. Low end price target of $0.83 represents $1.00 12/31/13 price target discounted back 1 year at a cost of equity of 20.00%

(2) Based on $0.09/MHz-POP implied from LightSquared (currently in Chapter 11) debt trading levels, and $0.17/MHz-POP based on current Globalstar enterprise value (assuming no value for existing business)

(3) Based on 47.0bn MHz-POPs

(4) Assumes no value for net assets and includes no costs associated with on-going commitments and liabilities, based on Management guidance

(5) Cash and debt balance per SCC Case

(6) Represents 1 day before SoftBank/Sprint acquisition rumor (10/10/12)

(7) Relevant range based on analysis of one day, 1-week prior, 4-week prior premiums of a) all cash transactions >$500mm b) all cash transactions >$500mm where acquirer stake increases from <50% to 100% b) all cash transactions >$500mm where acquirer already had >50% stake and increased ownership to 100%

(8) Represents 1 day before initial Sprint proposal

Evercore Partners

11

Valuation Analysis

Preliminary Draft - Confidential

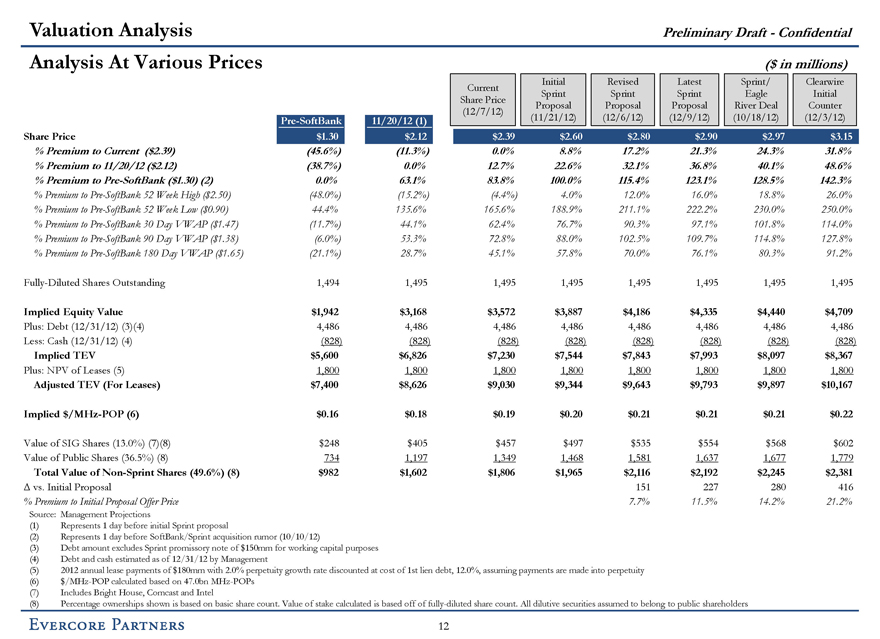

Analysis At Various Prices

($ in millions)

Pre-SoftBank

11/20/12 (1)

Current Share Price (12/7/12)

Initial Sprint Proposal (11/21/12)

Revised Sprint Proposal (12/6/12)

Latest Sprint Proposal (12/9/12)

Sprint/ Eagle River Deal (10/18/12)

Clearwire Initial Counter (12/3/12)

Share Price

$1.30 $2.12 $2.39 $2.60 $2.80 $2.90 $2.97 $3.15

% Premium to Current ($2.39)

(45.6%) (11.3%) 0.0% 8.8% 17.2% 21.3% 24.3% 31.8%

% Premium to 11/20/12 ($2.12)

(38.7%) 0.0% 12.7% 22.6% 32.1% 36.8% 40.1% 48.6%

% Premium to Pre-SoftBank ($1.30) (2)

0.0% 63.1% 83.8% 100.0% 115.4% 123.1% 128.5% 142.3%

% Premium to Pre-SoftBank 52 Week High ($2.50)

(48.0%) (15.2%) (4.4%) 4.0% 12.0% 16.0% 18.8% 26.0%

% Premium to Pre-SoftBank 52 Week Low ($0.90)

44.4% 135.6% 165.6% 188.9% 211.1% 222.2% 230.0% 250.0%

% Premium to Pre-SoftBank 30 Day VWAP ($1.47)

(11.7%) 44.1% 62.4% 76.7% 90.3% 97.1% 101.8% 114.0%

% Premium to Pre-SoftBank 90 Day VWAP ($1.38)

(6.0%) 53.3% 72.8% 88.0% 102.5% 109.7% 114.8% 127.8%

% Premium to Pre-SoftBank 180 Day VWAP ($1.65)

(21.1%) 28.7% 45.1% 57.8% 70.0% 76.1% 80.3% 91.2%

Fully-Diluted Shares Outstanding

1,494 1,495 1,495 1,495 1,495 1,495 1,495 1,495

Implied Equity Value

$1,942 $3,168 $3,572 $3,887 $4,186 $4,335 $4,440 $4,709

Plus: Debt (12/31/12) (3)(4)

4,486 4,486 4,486 4,486 4,486 4,486 4,486 4,486

Less: Cash (12/31/12) (4)

(828) (828) (828) (828) (828) (828) (828) (828)

Implied TEV

$5,600 $6,826 $7,230 $7,544 $7,843 $7,993 $8,097 $8,367

Plus: NPV of Leases (5)

1,800 1,800 1,800 1,800 1,800 1,800 1,800 1,800

Adjusted TEV (For Leases)

$7,400 $8,626 $9,030 $9,344 $9,643 $9,793 $9,897 $10,167

Implied $/MHz-POP (6)

$0.16 $0.18 $0.19 $0.20 $0.21 $0.21 $0.21 $0.22

Value of SIG Shares (13.0%) (7)(8)

$248 $405 $457 $497 $535 $554 $568 $602

Value of Public Shares (36.5%) (8)

734 1,197 1,349 1,468 1,581 1,637 1,677 1,779

Total Value of Non-Sprint Shares (49.6%) (8)

$982 $1,602 $1,806 $1,965 $2,116 $2,192 $2,245 $2,381

vs. Initial Proposal

151 227 280 416

% Premium to Initial Proposal Offer Price

7.7% 11.5% 14.2% 21.2%

Source: Management Projections

(1) Represents 1 day before initial Sprint proposal

(2) Represents 1 day before SoftBank/Sprint acquisition rumor (10/10/12)

(3) Debt amount excludes Sprint promissory note of $150mm for working capital purposes

(4) Debt and cash estimated as of 12/31/12 by Management

(5) 2012 annual lease payments of $180mm with 2.0% perpetuity growth rate discounted at cost of 1st lien debt, 12.0%, assuming payments are made into perpetuity

(6) $/MHz-POP calculated based on 47.0bn MHz-POPs

(7) Includes Bright House, Comcast and Intel

(8) Percentage ownerships shown is based on basic share count. Value of stake calculated is based off of fully-diluted share count. All dilutive securities assumed to belong to public shareholders

Evercore Partners

12

Valuation Analysis

Preliminary Draft - Confidential

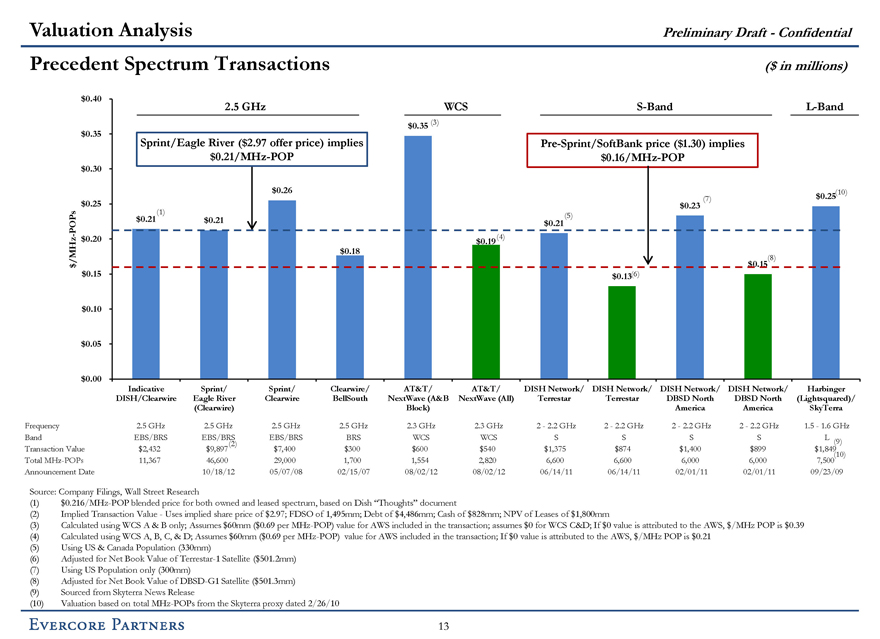

Precedent Spectrum Transactions

($ in millions)

$0.40

$0.35

$0.30

$0.25

$0.20

$0.15

$0.10

$0.05

$0.00

2.5 GHz

WCS

S-Band

L-Band

$0.35 (3)

Sprint/Eagle River ($2.97 offer price) implies $0.21/MHz-POP

Pre-Sprint/SoftBank price ($1.30) implies $0.16/MHz-POP

$0.26

$0.23 (7)

$0.25 (10)

$ 0.21 (1)

$0.21

$0.21 (5)

$0.19 (4)

$0.18

$/MHz-POPs

$0.15 (8)

$0.13 (6)

Indicative DISH/Clearwire

Sprint/ Eagle River (Clearwire)

Sprint/ Clearwire

Clearwire/ BellSouth

AT&T/ NextWave (A&B Block)

AT&T/ NextWave (All)

DISH Network/ Terrestar

DISH Network/ Terrestar

DISH Network/ DBSD North America

DISH Network/ DBSD North America

Harbinger (Lightsquared)/ SkyTerra

Frequency

2.5 GHz 2.5 GHz 2.5 GHz 2.5 GHz 2.3 GHz 2.3 GHz 2 - 2.2 GHz 2 - 2.2 GHz 2 - 2.2 GHz 2 - 2.2 GHz 1.5 - 1.6 GHz

Band

EBS/BRS EBS/BRS EBS/BRS BRS WCS WCS S S S S L

Transaction Value

$2,432 $9,897(2) $7,400 $300 $600 $540 $1,375 $874 $1,400 $899 $1,849(9)

Total MHz-POPs

11,367 46,600 29,000 1,700 1,554 2,820 6,600 6,600 6,000 6,000 7,500(10)

Announcement Date

10/18/12 05/07/08 02/15/07 08/02/12 08/02/12 06/14/11 06/14/11 02/01/11 02/01/11 09/23/09

Source: Company Filings, Wall Street Research

(1) $0.216/MHz-POP blended price for both owned and leased spectrum, based on Dish “Thoughts” document

(2) Implied Transaction Value - Uses implied share price of $2.97; FDSO of 1,495mm; Debt of $4,486mm; Cash of $828mm; NPV of Leases of $1,800mm

(3) Calculated using WCS A & B only; Assumes $60mm ($0.69 per MHz-POP) value for AWS included in the transaction; assumes $0 for WCS C&D; If $0 value is attributed to the AWS, $/MHz POP is $0.39

(4) Calculated using WCS A, B, C, & D; Assumes $60mm ($0.69 per MHz-POP) value for AWS included in the transaction; If $0 value is attributed to the AWS, $/MHz POP is $0.21

(5) Using US & Canada Population (330mm)

(6) Adjusted for Net Book Value of Terrestar-1 Satellite ($501.2mm)

(7) Using US Population only (300mm)

(8) Adjusted for Net Book Value of DBSD-G1 Satellite ($501.3mm)

(9) Sourced from Skyterra News Release

(10) Valuation based on total MHz-POPs from the Skyterra proxy dated 2/26/10

Evercore Partners

13

Valuation Analysis

Preliminary Draft - Confidential

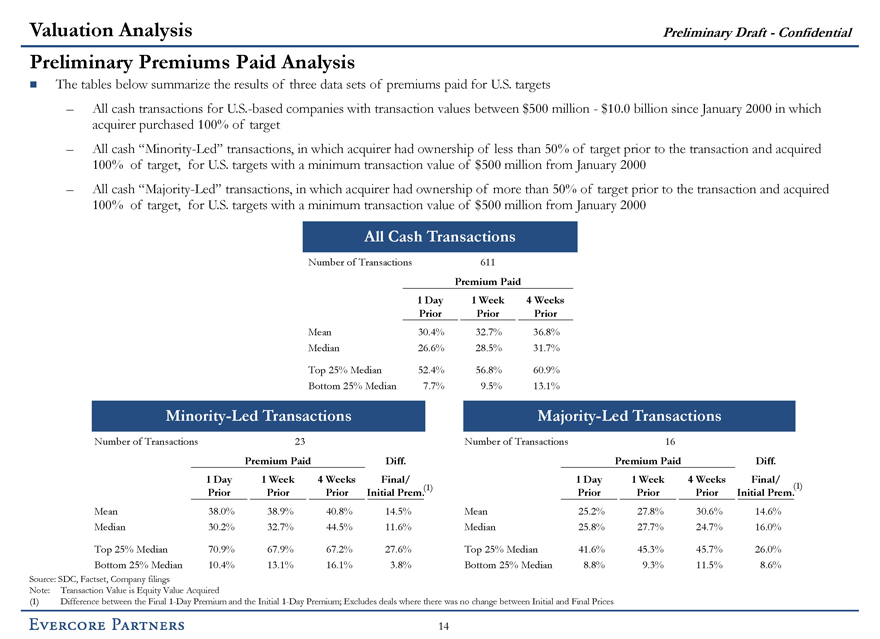

Preliminary Premiums Paid Analysis

The tables below summarize the results of three data sets of premiums paid for U.S. targets

- All cash transactions for U.S.-based companies with transaction values between $500 million - $10.0 billion since January 2000 in which acquirer purchased 100% of target

- All cash “Minority-Led” transactions, in which acquirer had ownership of less than 50% of target prior to the transaction and acquired 100% of target, for U.S. targets with a minimum transaction value of $500 million from January 2000

- All cash “Majority-Led” transactions, in which acquirer had ownership of more than 50% of target prior to the transaction and acquired 100% of target, for U.S. targets with a minimum transaction value of $500 million from January 2000

All Cash Transactions

Number of Transactions

611

Premium Paid

1 Day Prior 1 Week Prior 4 Weeks Prior

Mean

30.4% 32.7% 36.8%

Median

26.6% 28.5% 31.7%

Top 25% Median

52.4% 56.8% 60.9%

Bottom 25% Median

7.7% 9.5% 13.1%

Minority-Led Transactions

Number of Transactions

23

Premium Paid

1 Day Prior 1 Week Prior 4 Weeks Prior

Diff. Final/ Initial Prem.(1)

Mean

38.0% 38.9% 40.8% 14.5%

Median

30.2% 32.7% 44.5% 11.6%

Top 25% Median

70.9% 67.9% 67.2% 27.6%

Bottom 25% Median

10.4% 13.1% 16.1% 3.8%

Majority-Led Transactions

Number of Transactions

16

Premium Paid

1 Day Prior 1 Week Prior 4 Weeks Prior

Diff. Final/ Initial Prem.(1)

Mean

25.2% 27.8% 30.6% 14.6%

Median

25.8% 27.7% 24.7% 16.0%

Top 25% Median

41.6% 45.3% 45.7% 26.0%

Bottom 25% Median

8.8% 9.3% 11.5% 8.6%

Source: SDC, Factset, Company filings

Note: Transaction Value is Equity Value Acquired

(1) Difference between the Final 1-Day Premium and the Initial 1-Day Premium; Excludes deals where there was no change between Initial and Final Prices

Evercore Partners

14

Valuation Analysis

Preliminary Draft - Confidential

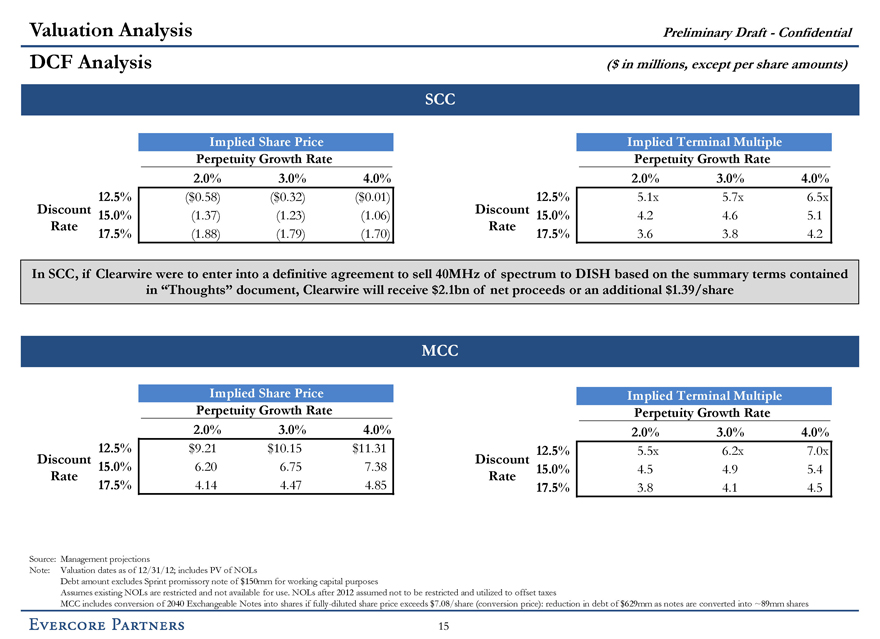

DCF Analysis

($ in millions, except per share amounts)

SCC

Implied Share Price

Perpetuity Growth Rate

2.0% 3.0% 4.0%

12.5% ($0.58) ($0.32) ($0.01)

Discount Rate

15.0%

(1.37) (1.23) (1.06)

17.5%

(1.88) (1.79) (1.70)

Implied Terminal Multiple

Perpetuity Growth Rate

2.0% 3.0% 4.0%

12.5% 5.1x 5.7x 6.5x

Discount Rate

15.0% 4.2 4.6 5.1

17.5% 3.6 3.8 4.2

In SCC, if Clearwire were to enter into a definitive agreement to sell 40MHz of spectrum to DISH based on the summary terms contained in “Thoughts” document, Clearwire will receive $2.1bn of net proceeds or an additional $1.39/share

MCC

Implied Share Price

Perpetuity Growth Rate

2.0% 3.0% 4.0%

12.5% $9.21 $10.15 $11.31

Discount Rate

15.0% 6.20 6.75 7.38

17.5% 4.14 4.47 4.85

Implied Terminal Multiple

Perpetuity Growth Rate

2.0%

3.0%

4.0%

Discount Rate

12.5% 5.5x 6.2x 7.0x

15.0% 4.5 4.9 5.4

17.5% 3.8 4.1 4.5

Source: Management projections

Note: Valuation dates as of 12/31/12; includes PV of NOLs

Debt amount excludes Sprint promissory note of $150mm for working capital purposes

Assumes existing NOLs are restricted and not available for use. NOLs after 2012 assumed not to be restricted and utilized to offset taxes

MCC includes conversion of 2040 Exchangeable Notes into shares if fully-diluted share price exceeds $7.08/share (conversion price): reduction in debt of $629mm as notes are converted into ~89mm shares

Evercore Partners

15

Appendix

Evercore Partners

Appendix

Preliminary Draft - Confidential

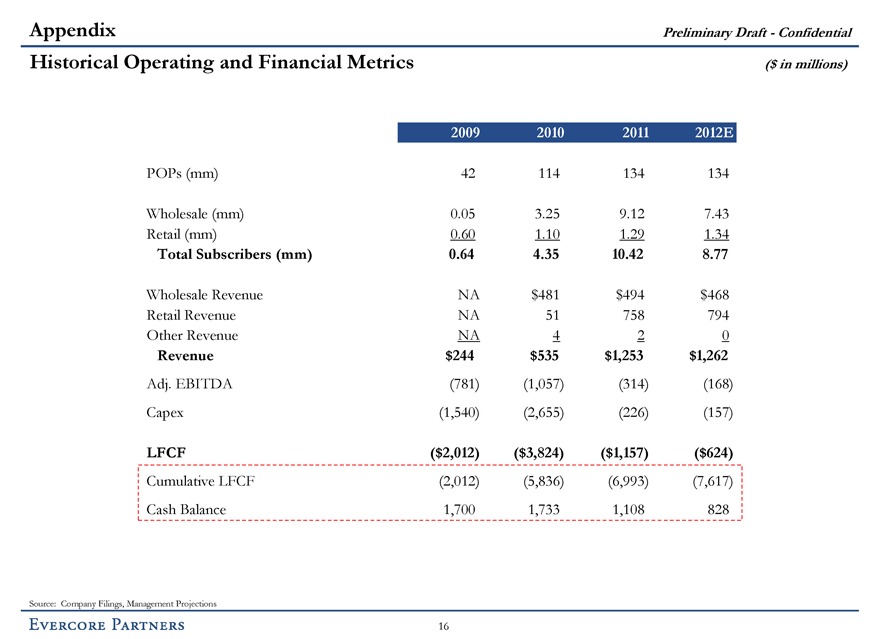

Historical Operating and Financial Metrics

($ in millions)

2009 2010 2011 2012E

POPs (mm)

42 114 134 134

Wholesale (mm)

0.05 3.25 9.12 7.43

Retail (mm)

0.60 1.10 1.29 1.34

Total Subscribers (mm)

0.64 4.35 10.42 8.77

Wholesale Revenue

NA $481 $494 $468

Retail Revenue

NA 51 758 794

Other Revenue

NA 4 2 0

Revenue

$244 $535 $1,253 $1,262

Adj. EBITDA

(781) (1,057) (314) (168)

Capex

(1,540) (2,655) (226) (157)

LFCF

($2,012) ($3,824) ($1,157) ($624)

Cumulative LFCF

(2,012) (5,836) (6,993) (7,617)

Cash Balance

1,700 1,733 1,108 828

Source: Company Filings, Management Projections

Evercore Partners

16

Appendix

Preliminary Draft - Confidential

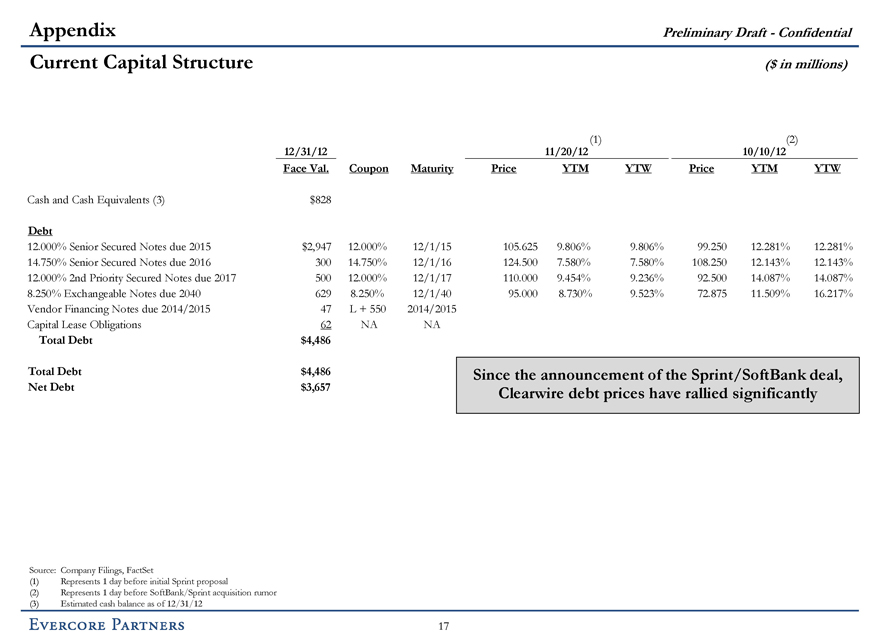

Current Capital Structure

($ in millions)

12/31/12

11/20/12(1) 10/10/12(2)

Face Val. Coupon Maturity Price YTM YTW Price YTM YTW

Cash and Cash Equivalents (3)

$828

Debt

12.000% Senior Secured Notes due 2015

$2,947 12.000% 12/1/15 105.625 9.806% 9.806% 99.250 12.281% 12.281%

14.750% Senior Secured Notes due 2016

300 14.750% 12/1/16 124.500 7.580% 7.580% 108.250 12.143% 12.143%

12.000% 2nd Priority Secured Notes due 2017

500 12.000% 12/1/17 110.000 9.454% 9.236% 92.500 14.087% 14.087%

8.250% Exchangeable Notes due 2040

629 8.250% 12/1/40 95.000 8.730% 9.523% 72.875 11.509% 16.217%

Vendor Financing Notes due 2014/2015

47 L+550 2014/2015

Capital Lease Obligations

62 NA NA

Total Debt

$4,486

Total Debt

$4,486

Net Debt

$3,657

Since the announcement of the Sprint/SoftBank deal, Clearwire debt prices have rallied significantly

Source: Company Filings, FactSet

(1) Represents 1 day before initial Sprint proposal

(2) Represents 1 day before SoftBank/Sprint acquisition rumor

(3) Estimated cash balance as of 12/31/12

Evercore Partners

17

Appendix

Preliminary Draft - Confidential

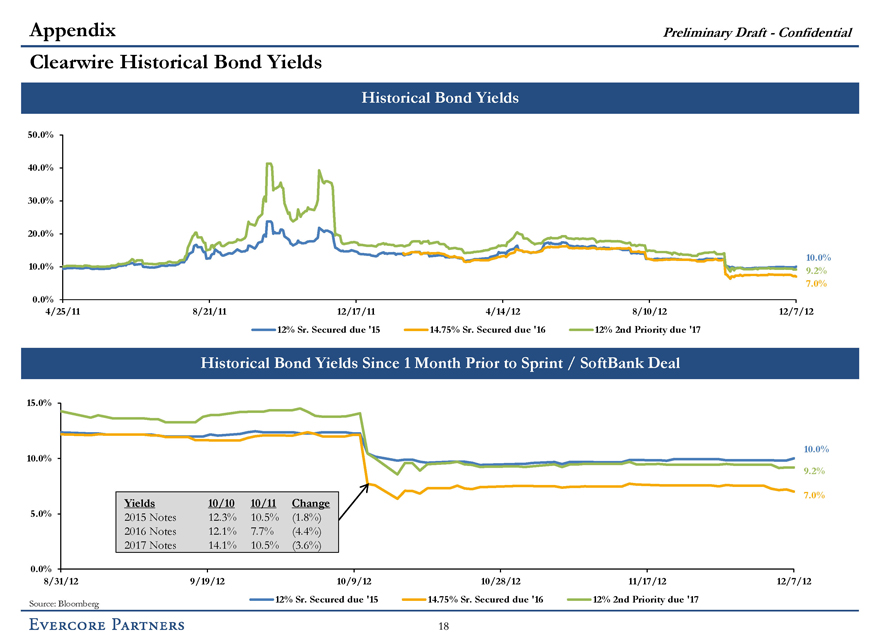

Clearwire Historical Bond Yields

Historical Bond Yields

50.0%

40.0%

30.0%

20.0%

10.0%

10.0%

9.2%

7.0%

0.0%

4/25/11

8/21/11

12/17/11

4/14/12

8/10/12

12/7/12

12% Sr. Secured due ‘15

14.75% Sr. Secured due ‘16

12% 2nd Priority due ‘17

Historical Bond Yields Since 1 Month Prior to Sprint / SoftBank Deal

15.0%

10.0%

10.0%

9.2%

7.0%

5.0%

0.0%

Yields

10/10

10/11

Change

2015 Notes

12.3%

10.5%

(1.8%)

2016 Notes

12.1%

7.7%

(4.4%)

2017 Notes

14.1%

10.5%

(3.6%)

8/31/12

9/19/12

10/9/12

10/28/12

11/17/12

12/7/12

Source: Bloomberg

12% Sr. Secured due ‘15

14.75% Sr. Secured due ‘16

12% 2nd Priority due ‘17

Evercore Partners

18

. |

Appendix

Preliminary Draft - Confidential

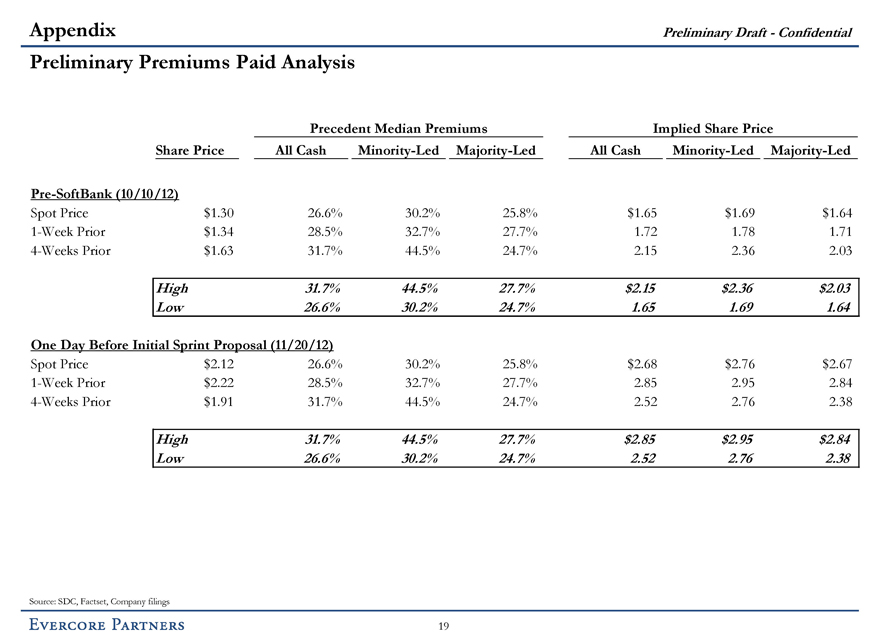

Preliminary Premiums Paid Analysis

Precedent Median Premiums

Implied Share Price

Share Price All Cash Minority-Led Majority-Led All Cash Minority-Led Majority-Led

Pre-SoftBank (10/10/12)

Spot Price

$1.30 26.6% 30.2% 25.8% $1.65 $1.69 $1.64

1-Week Prior

$1.34 28.5% 32.7% 27.7% 1.72 1.78 1.71

4-Weeks Prior

$1.63 31.7% 44.5% 24.7% 2.15 2.36 2.03

High

Low

31.7% 44.5% 27.7% $2.15 $2.36 $2.03

26.6% 30.2% 24.7% 1.65 1.69 1.64

One Day Before Initial Sprint Proposal (11/20/12)

Spot Price

$2.12 26.6% 30.2% 25.8% $2.68 $2.76 $2.67

1-Week Prior

$2.22 28.5% 32.7%27.7% 2.85 2.95 2.84

4-Weeks Prior

$1.91 31.7% 44.5% 24.7% 2.52 2.76 2.38

High

Low

31.7% 44.5% 27.7% $2.85 $2.95 $2.84

26.6% 30.2% 24.7% 2.52 2.76 2.38

Source: SDC, Factset, Company filings

Evercore Partners

19

Appendix

Preliminary Draft - Confidential

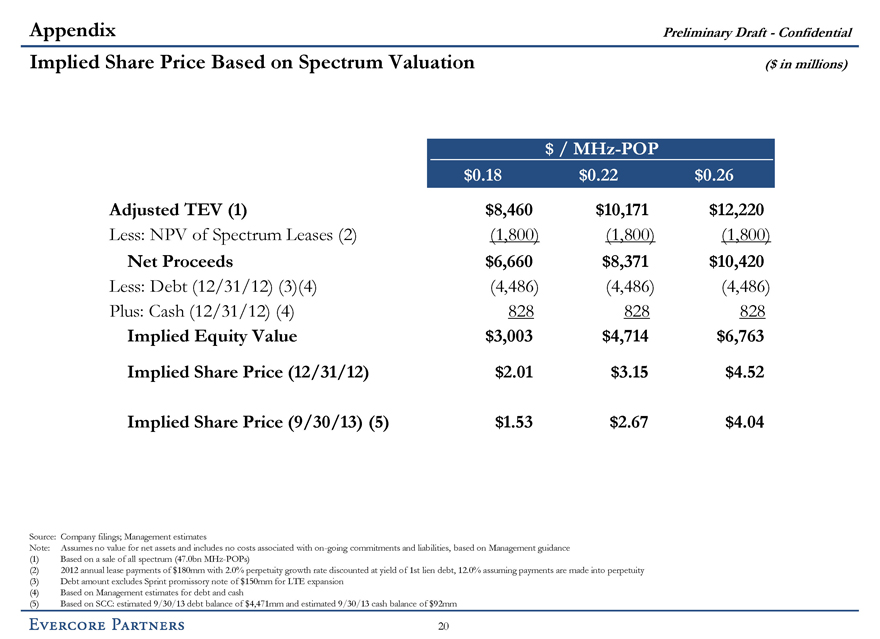

Implied Share Price Based on Spectrum Valuation

($ in millions)

$ / MHz-POP

$0.18 $0.22 $0.26

Adjusted TEV (1)

$8,460 $10,171 $12,220

Less: NPV of Spectrum Leases (2)

(1,800) (1,800) (1,800)

Net Proceeds

$6,660 $8,371 $10,420

Less: Debt (12/31/12) (3)(4)

(4,486) (4,486) (4,486)

Plus: Cash (12/31/12) (4)

828 828 828

Implied Equity Value

$3,003 $4,714 $6,763

Implied Share Price (12/31/12)

$2.01 $3.15 $4.52

Implied Share Price (9/30/13) (5)

$1.53 $2.67 $4.04

Source: Company filings; Management estimates

Note: Assumes no value for net assets and includes no costs associated with on-going commitments and liabilities, based on Management guidance

(1) Based on a sale of all spectrum (47.0bn MHz-POPs)

(2) 2012 annual lease payments of $180mm with 2.0% perpetuity growth rate discounted at yield of 1st lien debt, 12.0% assuming payments are made into perpetuity

(3) Debt amount excludes Sprint promissory note of $150mm for LTE expansion

(4) Based on Management estimates for debt and cash

(5) Based on SCC: estimated 9/30/13 debt balance of $4,471mm and estimated 9/30/13 cash balance of $92mm

Evercore Partners

20

Appendix

Preliminary Draft - Confidential

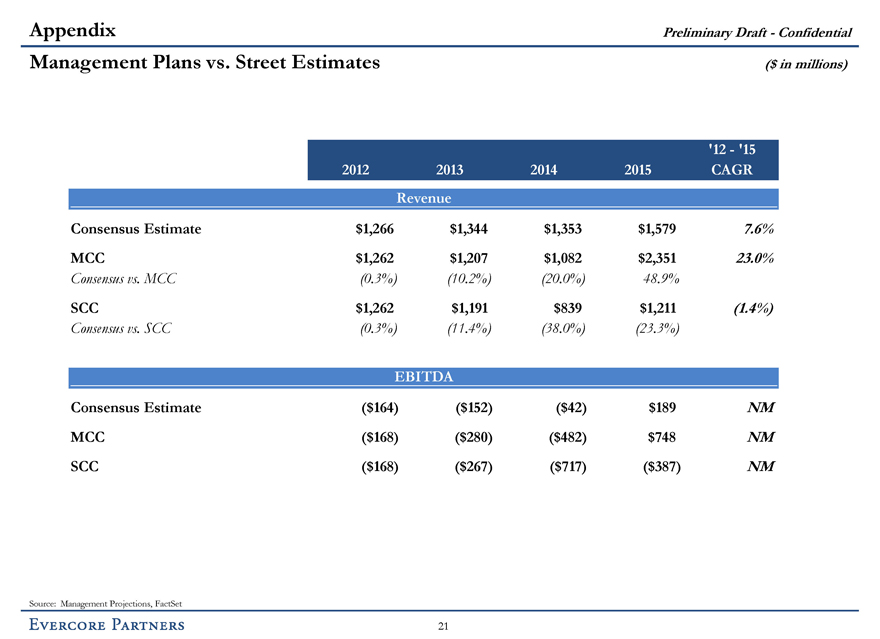

Management Plans vs. Street Estimates

($ in millions)

2012 2013 2014 2015 ‘12 - ‘15 CAGR

Revenue

Consensus Estimate

$1,266 $1,344 $1,353 $1,579 7.6%

MCC

$1,262 $1,207 $1,082 $2,351 23.0%

Consensus vs. MCC

(0.3%) (10.2%) (20.0%) 48.9%

SCC

$1,262 $1,191 $839 $1,211 (1.4%)

Consensus vs. SCC

(0.3%) (11.4%) (38.0%) (23.3%)

EBITDA

Consensus Estimate

($164) ($152) ($42) $189 NM

MCC

($168) ($ 280) ($482) $ 748 NM

SCC

($168) ($ 267) ($717) ($ 387) NM

Source: Management Projections, FactSet

Evercore Partners

21

Appendix

Preliminary Draft - Confidential

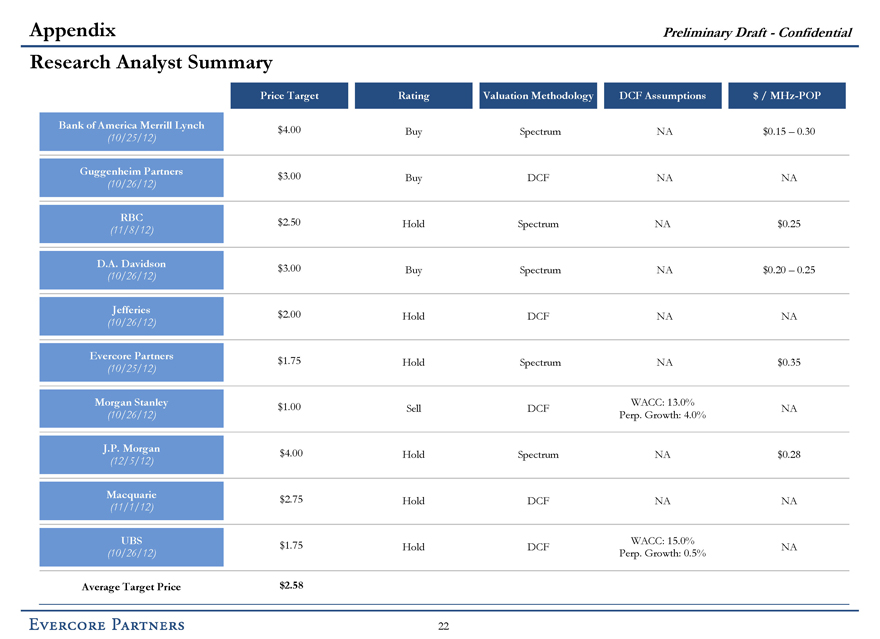

Research Analyst Summary

Price Target Rating Valuation Methodology DCF Assumptions $ / MHz-POP

Bank of America Merrill Lynch (10/25/12)

$4.00 Buy Spectrum NA $0.15 - 0.30

Guggenheim Partners (10/26/12)

$3.00 Buy DCF NA NA

RBC (11/8/12)

$2.50 Hold Spectrum NA $0.25

D.A. Davidson (10/26/12)

$3.00 Buy Spectrum NA $0.20 - 0.25

Jefferies (10/26/12)

$2.00 Hold DCF NA NA

Evercore Partners (10/25/12)

$1.75 Hold Spectrum NA $0.35

Morgan Stanley (10/26/12)

$1.00 Sell DCF WACC: 13.0% Perp. Growth: 4.0% NA

J.P. Morgan (12/5/12)

$4.00 Hold Spectrum NA $0.28

Macquarie (11/1/12)

$2.75 Hold DCF NA NA

UBS (10/26/12)

$1.75 Hold DCF WACC: 15.0% Perp. Growth: 0.5% NA

Average Target Price

$2.58

Evercore Partners

22

Appendix

Preliminary Draft - Confidential

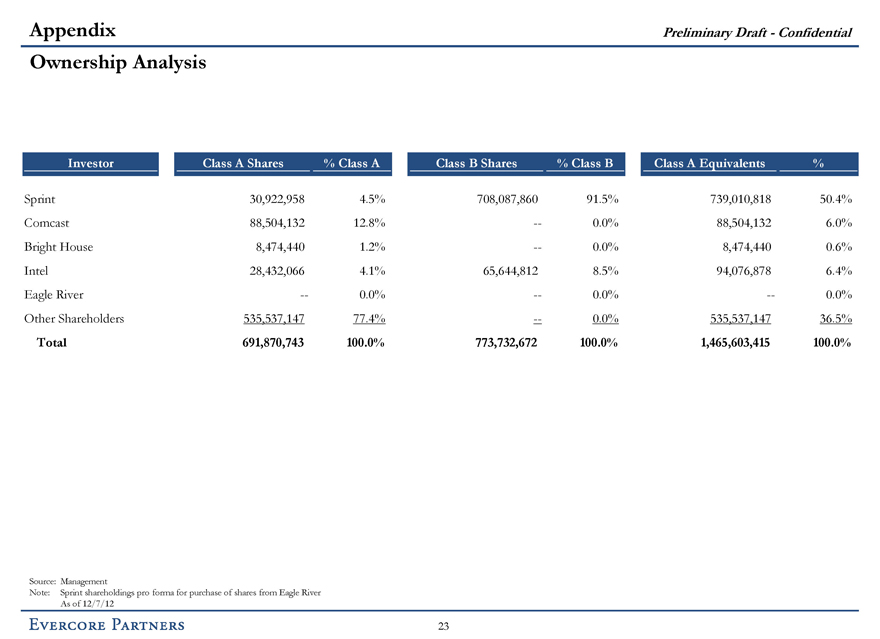

Ownership Analysis

Investor

Class A Shares % Class A Class B Shares % Class B Class A Equivalents %

Sprint

30,922,958 4.5% 708,087,860 91.5% 739,010,818 50.4%

Comcast

88,504,132 12.8% -- 0.0% 88,504,132 6.0%

Bright House

8,474,440 1.2% -- 0.0% 8,474,440 0.6%

Intel

28,432,066 4.1% 65,644,812 8.5% 94,076,878

6.4%

Eagle River

-- 0.0% -- 0.0% -- 0.0%

Other Shareholders

535,537,147 77.4% -- 0.0% 535,537,147 36.5%

Total

691,870,743 100.0% 773,732,672 100.0% 1,465,603,415 100.0%

Source: Management

Note: Sprint shareholdings pro forma for purchase of shares from Eagle River As of 12/7/12

Evercore Partners

23

Appendix

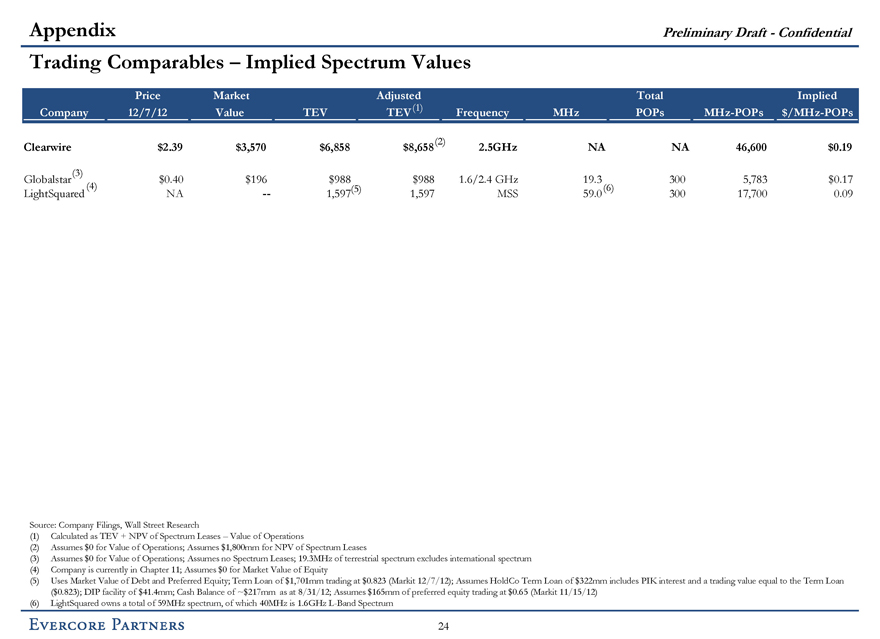

Preliminary Draft - Confidential

Trading Comparables - Implied Spectrum Values

Company Price 12/7/12 Market Value TEV Adjusted TEV (1) Frequency MHz Total POPs MHz-POPs Implied $/MHz-POPs

Clearwire

$2.39 $3,570 $6,858 $8,658 (2) 2.5GHz NA NA 46,600 $0.19

Globalstar(3)

$0.40 $196 $988 $988 1.6/2.4 GHz 19.3 300 5,783 $0.17

LightSquared (4)

NA -- 1,597(5) 1,597 MSS 59.0 (6) 300 17,700 0.09

Source: Company Filings, Wall Street Research

(1) Calculated as TEV + NPV of Spectrum Leases - Value of Operations

(2) Assumes $0 for Value of Operations; Assumes $1,800mm for NPV of Spectrum Leases

(3) Assumes $0 for Value of Operations; Assumes no Spectrum Leases; 19.3MHz of terrestrial spectrum excludes international spectrum

(4) Company is currently in Chapter 11; Assumes $0 for Market Value of Equity

(5) Uses Market Value of Debt and Preferred Equity; Term Loan of $1,701mm trading at $0.823 (Markit 12/7/12); Assumes HoldCo Term Loan of $322mm includes PIK interest and a trading value equal to the Term Loan

($0.823); DIP facility of $41.4mm; Cash Balance of ~$217mm as at 8/31/12; Assumes $165mm of preferred equity trading at $0.65 (Markit 11/15/12)

(6) LightSquared owns a total of 59MHz spectrum, of which 40MHz is 1.6GHz L-Band Spectrum

Evercore Partners

24