Washington, D.C. 20549

Mark L. Winget

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Life is Complex.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready—no more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports

right to your e-mail!

www.investordelivery.com

If you receive your Nuveen Fund

dividends and statements from your

financial professional or brokerage account.

or

www.nuveen.com/client-access

If you receive your Nuveen Fund

dividends and statements directly from

Nuveen.

NOT FDIC INSURED MAY LOSE

VALUE NO BANK GUARANTEE

3

Chair’s Letterto Shareholders Dear Shareholders,

As 2020 draws to a close, the concerns that dominated much of the year are beginning to show signs of easing. COVID-19 vaccines are being administered around the world, with several of the vaccine candidates announcing high efficacy rates during their phase 3 trials. Markets took a generally positive view of Joe Biden winning the Electoral College, with Congress’s final confirmation of the Electoral College vote anticipated on January 6, 2021. The U.S. economy has made a significant, although incomplete, turnaround from the depths of a historic recession. In December, Congress passed another $900 billion in aid to individuals and businesses, extending some of the programs enacted earlier in the crisis. The bill’s next step is the President’s review and his approval or disapproval. Ongoing fiscal and monetary stimulus along with widening vaccine distribution have bolstered confidence that a semblance of normalcy can return in 2021.

While the markets’ longer-term outlook has brightened, we expect intermittent bouts of volatility to continue into the new year. COVID-19 cases are still alarmingly high in some regions, and the renewed restrictions on social and business activity taken by local and, in some cases, national authorities will undoubtedly hinder the economy’s momentum. The pandemic’s course can still be unpredictable. The timeline of vaccine rollouts depends on many variables, public confidence can shift and real-world efficacy remains to be seen. Additionally, the outcome of the Senate majority – which determines whether the government will be under split control or a Democrat majority – rests with Georgia’s two run-off elections on January 5, 2021. Nevertheless, short-term market fluctuations can provide opportunities to invest in new ideas as well as upgrade existing positioning, within our goal of providing long-term value for our shareholders.

The new year can be an opportune time to assess your portfolio’s resilience and readiness for what may come next. We encourage you to review your time horizon, risk tolerance and investment goals with your financial professional. On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Terence J. Toth

Chair of the Board

December 22, 2020

4

Portfolio Managers’ Comments

Nuveen Municipal Value Fund, Inc. (NUV)

Nuveen AMT-Free Municipal Value Fund (NUW)

Nuveen Municipal Income Fund, Inc. (NMI)

Nuveen Enhanced Municipal Value Fund (NEV)

These Funds feature portfolio management by Nuveen Asset Management, LLC (NAM), an affiliate of Nuveen, LLC, the Funds’ investment adviser. Portfolio managers Daniel J. Close, CFA, Christopher L. Drahn, CFA, and Steven M. Hlavin discuss U.S. economic and municipal market conditions, key investment strategies and the twelve-month performance of these four national Funds. Dan has managed NUV and NUW since 2016. Chris assumed portfolio management responsibility for NMI in 2011. Steve has been involved in the management of NEV since its inception in 2009, taking on full portfolio management responsibility in 2010.

During August 2020, the Nuveen New Jersey Municipal Value Fund (NJV) and Nuveen Pennsylvania Municipal Value Fund (NPN) were approved for merger into NUW by the Funds’ Board of Trustees. The merger is pending shareholder approval.

What factors affected the U.S. economy and financial markets during the twelve-month reporting period ended October 31, 2020?

The U.S. economy rebounded more quickly than expected from the deep downturn caused by the COVID-19 crisis and containment measures. As business and social activities were drastically restricted in March and April 2020 to slow the spread of COVID-19, U.S. gross domestic product (GDP) shrank 31.4% on an annualized basis in the second quarter of 2020 (following a 5% decline in the first quarter), according to the Bureau of Economic Analysis (BEA) “third” estimate. GDP measures the value of goods and services produced by the nation’s economy less the value of the goods and services used up in production, adjusted for price changes. Government relief programs provided significant aid to individuals and businesses as the economy began reopening in May 2020, which helped the economy bounce back strongly over the summer months. GDP rose 33.1% in the third quarter of 2020, according to the BEA’s “second” estimate. While the third quarter gain was historic, the economy remained below pre-pandemic growth levels. GDP growth was 2.4% in the fourth quarter of 2019 and 2.2% for 2019 overall.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch). This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings, while BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Bond insurance guarantees only the payment of principal and interest on the bond when due, and not the value of the bonds themselves, which will fluctuate with the bond market and the financial success of the issuer and the insurer. Insurance relates specifically to the bonds in the portfolio and not to the share prices of a Fund. No representation is made as to the insurers’ ability to meet their commitments.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

5

Portfolio Managers’ Comments (continued)

Consumer spending, the largest driver of the economy, was well supported earlier in this reporting period by low unemployment, wage gains and tax cuts. However, the COVID-19 crisis containment measures drove a significant drop in consumer spending and a sharp rise in unemployment starting in March 2020. The Bureau of Labor Statistics said the unemployment rate rose to 6.9% in October 2020 from 3.6% in October 2019. As of October 2020, slightly more than half of the 22 million jobs lost in March and April 2020 have been recovered. The average hourly earnings rate appeared to soar, growing at an annualized rate of 4.5% in October 2020, despite the spike in unemployment. Earnings data was skewed by the concentration of job losses in lower-wage work, which effectively eliminated most of the low-wage data, resulting in an average of mostly higher numbers. The overall trend of inflation remained muted, as decreases in gasoline, apparel and transportation prices offset an increase in food prices. The Bureau of Labor Statistics said the Consumer Price Index (CPI) increased 1.2% over the twelve-month reporting period ended October 31, 2020 before seasonal adjustment.

Prior to the COVID-19 crisis recession, the U.S. Federal Reserve (the Fed) had reduced its benchmark interest rate to support the economy’s slowing growth. The Fed also stopped shrinking its bond portfolio sooner than scheduled and began buying short-term Treasury bills to help money markets operate smoothly and maintain short-term borrowing rates at low levels.

As the health and economic crisis deepened, the Fed enacted an array of emergency measures in March 2020 to stabilize the financial system and support the markets, including cutting its main interest rate to near zero, offering lending programs to aid small and large companies and allowing unlimited bond purchases, known as quantitative easing. There were no policy changes at the Fed’s April, June and July 2020 meetings, where Chairman Powell reiterated a commitment to keep rates near zero until the economy recovers and maintained a cautious outlook for the U.S. economy. Also at the July 2020 meeting, the Fed extended some of its pandemic funding facilities by another three months to December 2020. At the annual Jackson Hole Economic Symposium, held virtually in August 2020, the Fed announced a change in inflation policy to average inflation targeting. Under this regime, the Fed will tolerate the inflation rate temporarily overshooting the target rate to offset periods of below-target inflation, so that inflation averages a 2% rate over time. The Fed provided further clarification of the new inflation policy and left the benchmark interest rate unchanged at its September 2020 meeting. (As expected, there were no policy changes at the Fed’s November 2020 meeting, which occurred after the close of this reporting period.)

In March and April 2020, the U.S. government approved three aid packages. These included $2 trillion allocated across direct payments to Americans, an expansion of unemployment insurance, loans to large and small businesses, funding to hospitals and health agencies and support to state and local governments, as well as more than $100 billion in funding to health agencies and employers offering paid leave. As some of these programs began to expire, additional relief measures were under discussion in Congress, but a final deal had not been reached as of the end of this reporting period. The election outcome, subsequent to the close of the reporting period, did not change expectations for a stimulus bill, but the timing and size remained uncertain.

The COVID-19 crisis rapidly dwarfed all other market concerns starting in late February 2020. Equity and commodity markets sold-off and safe-haven assets rallied in March 2020 as China, other countries and then the United States initiated quarantines, restricted travel and shuttered factories and businesses. The potential economic shock was particularly difficult to assess, which amplified market volatility. An ill-timed oil price war between the Organization of the Petroleum Exporting Countries (OPEC) and non-OPEC member Russia, which caused oil prices to plunge in March 2020, exacerbated the market sell-off.

6

Geopolitical uncertainty remained elevated with the U.S. presidential election, the Brexit transition period winding down and U.S.-China relations deteriorating. While markets remained concerned about the potential for a disputed outcome, the next round of fiscal stimulus was expected to follow the presidential election. In Europe, the EU and U.K. continued to negotiate, but had not yet reached, a final Brexit agreement after the U.K. formally exited at the end of January 2020 and triggered the one-year transition period (which ends on December 31, 2020). Although China and the U.S. signed a “phase one” trade deal in January 2020, tensions continued to flare over other trade and technology/security issues, Hong Kong’s sovereignty and the management of the COVID-19 crisis.

Despite the severe sell-off in March 2020, municipal bonds managed positive performance over the twelve-month reporting period. For most of the reporting period, a significant decline in interest rates drove municipal bond prices higher, with positive technical and fundamental conditions also supporting credit spread tightening. Prior to the emergence of the novel coronavirus, interest rates had been pressured lower by signs that the economy’s momentum was slowing, a more dovish central bank policy, geopolitical tensions (especially regarding trade) and bouts of equity market volatility. Then, from late February through March 2020, coronavirus risks permeated the markets, sending U.S. Treasury yields to historic lows. Rate volatility increased sharply in that six-week period. As liquidity became stressed, investors began to liquidate any asset possible, including municipal bonds. Municipal bond prices declined rapidly (and yields spiked higher), amid rampant selling across both the high grade and high yield segments that was exacerbated in some cases by exchange-traded fund and closed-end fund selling. Municipal bond prices became severely dislocated from Treasury prices. Credit spreads widened significantly during the March 2020 sell-off, ending the month above their long-term average. Monetary and fiscal interventions from the Fed and U.S. government helped the market recover in April and May, although spreads remain wider than average as of the end of the reporting period. The municipal yield curve steepened over this reporting period, with a pronounced drop in yields at the short end of the curve spearheading the steepening.

Prior to the market turmoil in March 2020, municipal bond gross issuance nationwide had been robust. The overall low level of interest rates encouraged issuers to continue to actively refund their outstanding debt. In these transactions the issuers are issuing new bonds and taking the bond proceeds and redeeming (calling) old bonds. These refunding transactions have ranged from 30% to 60% of total issuance over the past few years. Thus, the net issuance (all bonds issued less bonds redeemed) is actually much lower than the gross issuance. So, while gross issuance volume has been adequate, the net has not and this was an overall positive technical factor on municipal bond investment performance in recent years. Notably, taxable municipal bond issuance has increased meaningfully since the advent of the Tax Cut and Jobs Act of 2017, which prohibits municipal issuers from issuing new tax-exempt bonds to pre-refund existing tax-exempt bonds. However, municipalities have taken advantage of the low interest rate environment and the strong demand for yield to issue taxable municipal debt, enabling them to save on net interest costs while adding to the scarcity value of tax-exempt issues.

Municipal bond funds saw consistently positive cash flows throughout 2019 and into early 2020, then suffered significant outflows in March 2020, particularly from high yield municipal bond funds. After the market stabilized in April 2020, fund flows subsequently turned positive again, bringing year-to-date flows through October 2020 back into positive territory. Demand has been resilient even though municipal defaults, as expected, have increased somewhat in 2020. Notably, default activity has occurred mainly in sectors with greater COVID-19 risk exposure, such as senior living, corporate-backed and real estate-backed. Additionally, while municipal credit ratings remain under pressure given the uncertain economic outlook, a wave of downgrades

7

Portfolio Managers’ Comments (continued)

has not materialized. With interest rates in the U.S. and globally remaining near all-time lows, the appetite for yield has continued to drive investors toward higher after-tax yielding assets, including U.S. municipal bonds. Additionally, as tax payers have adjusted to the 2017 tax law, which caps the state and local tax (SALT) deduction for individuals, there has been increased demand for tax-exempt municipal bonds, especially in states with high income taxes and/or property taxes.

What key strategies were used to manage the Funds during the twelve-month reporting period ended October 31, 2020, and how did these strategies influence performance?

Each Fund’s primary investment objective is to provide current income exempt from regular federal income tax by investing primarily in a portfolio of municipal obligations issued by state and local government authorities or certain U.S. territories. For NUV, NUW and NMI, each Fund may use inverse floating rate securities (or tender option bond financing) to more efficiently implement its investment strategy to create up to 10% effective leverage. NEV also uses inverse floating rate securities to create effective leverage, but to a greater extent than NUV, NUW and NMI. A further discussion on leverage can be found in the Fund Leverage section of this report.

Despite historic volatility in the municipal market during March and April 2020, municipal bond performance was positive over the twelve-month reporting period overall. Municipal yields fell, in concert with a steep drop in Treasury yields as the U.S. economy fell into a deep recession amid the virus lockdown. The decline was more dramatic at the short end of the municipal yield curve, which steepened the yield curve over the reporting period. Demand for municipal bonds recovered after the March-April 2020 sell-off, with mutual fund inflows resuming a positive trend (although more so for high grade than high yield municipal funds) and the market absorbing significant supply. With demand normalizing, high grade municipal bonds have made a full recovery from the March-April 2020 COVID-19 crisis, while high yield credit spreads have narrowed meaningfully but remained wider than where they began the reporting period.

Prior to the COVID-19 crisis market turmoil in late February 2020, most of the Funds’ trading was driven by reinvesting the proceeds from called and maturing bonds. One of the notable transactions during this reporting period was the state of Ohio refunding its legacy Buckeye Tobacco Settlement bonds and issuing new replacement bonds. All four Funds owned the legacy bonds and bought some of the replacement bonds. After the March 2020 sell-off, the market was favorable for executing tax-loss swaps. This strategy entailed selling depreciated bonds with lower yields and buying similarly structured but higher yielding bonds. This approach was implemented to enhance the Funds’ income earning capability and seek to make the Fund more tax efficient.

For NUV, the Fund reinvested the proceeds from called and maturing bonds across a wide range of sectors. In the second half of the reporting period, looking especially to beaten down sectors, the Fund bought six toll roads, three water and sewer, five dedicated tax, two public utilities, one health care, one tobacco, one New York City local general obligation (GO) and one transportation “other” (New York Metropolitan Transportation Authority (“MTA”)) bonds. We favored structures offering 4% and 5% coupons and longer maturities bonds. The Fund executed several tax loss swaps in May 2020, when prevailing market conditions were favorable to do so, such as state of Illinois debt and some narrow-based sales tax revenue bonds.

8

NUW invested similarly to NUV during this reporting period. Although with fewer bonds rolling off NUW’s portfolio, trading was less active. NUW bought New York MTAs, a New York City local GO, one health care, one dedicated tax, one public utility and a tobacco settlement bond (Michigan tobacco), and executed a tax loss swap. The Fund sold a few positions in the second half of the reporting period to fund new purchases. Conditions were more favorable for selling high grade paper at a loss, including Emory University, Austin Electric and some pre-refunded bonds, to reinvest in bonds with higher embedded yields. Like NUV, new purchases in NUW favored 4% and 5% coupon structures and primarily longer maturities.

NMI engaged in a number of tax loss swaps, most of which occurred in April and May 2020. As the market rebounded through the summer, the opportunities somewhat dissipated. Over the course of this reporting period, NMI’s sector weightings were not significantly changed, although there were slight weighting increases in the health care and tax-backed sectors. Although certain sectors and ratings categories were hit harder than others in the March-April 2020 sell-off, the Fund generally sought to maintain allocations to such sectors, and occasionally added incremental and opportunistic exposure. The Fund’s overall credit profile was also generally unchanged over the reporting period, although the AA rated category increased slightly. Additionally, the Fund continued a trend of utilizing lower coupon bond structures (for example, 4% coupon bonds rather than 5%) for the bonds’ more attractive characteristics and still reasonable defensiveness if interest rates rise.

Much of NEV’s trading was driven by reinvesting proceeds from bond calls and maturities, including the refundings of Buckeye Tobacco and Los Angeles County Tobacco bonds and maturing of U.S. Steel and Barclays Center Arena Brooklyn bonds, as well as a significant amount of tax loss swaps. The Fund added positions across a diverse group of sectors, including health care, transportation, sales tax revenue, tobacco, industrial development revenue (IDR), local GOs and airports. Also during this reporting period, NEV acquired shares in Energy Harbor when its holdings of certain municipal bonds issued by FirstEnergy Solutions were converted into Energy Harbor equity as part of FirstEnergy Solution’s emergence from bankruptcy protection. Over time, we expect to sell these shares and reinvest the proceeds into municipal bonds. Other municipal bonds issued by FirstEnergy Solutions, now known as Energy Harbor, were reinstated, which NEV still held its portfolio.

As of October 31, 2020, NUV, NUW and NEV continued to use inverse floating rate securities. We employ inverse floaters for a variety of reasons, including duration management, income enhancement and total return enhancement. As part of our duration management strategies, during this reporting period NUW entered into duration-shortening interest rate futures contracts. As interest rates declined, these contracts had a negative impact on performance during the reporting period.

How did the Funds perform during the twelve-month reporting period ended October 31, 2020?

The tables in each Fund’s Performance Overview and Holding Summaries section of this report provide the Funds’ total returns at net asset value (NAV) for the period ended October 31, 2020. Each Fund’s total returns at NAV are compared with the performance of a corresponding market index.

For the twelve months ended October 31, 2020, the total returns at NAV for the NUV, NUW and NMI underperformed the return for the national S&P Municipal Bond Index and NEV performed in line with the national index.

9

Portfolio Managers’ Comments (continued)

The factors affecting performance in this reporting period included yield curve and duration positioning, credit ratings allocation and sector allocation. In addition, the use of leverage was an important factor affecting performance of NEV. Leverage is discussed in more detail later in the Fund Leverage section of this report.

After the turmoil of the March-April 2020 period, yields fell somewhat more uniformly across the high grade (AAA rated) municipal yield curve over the second half of the reporting period, such that the entire curve was lower in yield when viewed over a full twelvemonth timeframe. Generally, longer duration bonds performed better in this reporting period. For NUV and NUW, duration and yield curve positioning was a positive contributor to relative performance, with outperformance from both an overweight allocation to the longest duration segment and an underweight allocation to the shortest duration segment. NUW also held a duration-shortening interest rate future position that was negative for performance. NMI held a modest overweight in longer duration bonds, which generally aided relative performance and offset the negative impact of some older lower duration holdings. For NEV, which uses leverage to a greater extent than the other three Funds, the leveraged duration position had a negligible impact on total return performance during the reporting period.

For the reporting period overall, the high grade (AAA and AA) ratings categories generally performed the best, although credit spreads did generally grind somewhat tighter and helped performance over the second half of the reporting period. Credit ratings allocations had the largest impact on the Funds’ relative performance in this period. NUV and NUW held overweight allocations to A rated and BBB rated bonds, which were detrimental, as spreads widened significantly for lower rated credits in March 2020 and had only partially recovered by the end of the reporting period. The Funds were also hurt by underweight allocations to high grade paper (AAA and AA rated for NUV, and AAA rated for NUW). NMI’s credit quality positioning was also disadvantageous, with overweights to A rated, BBB rated and non-rated bonds and underweights to AAA and AA rated bonds all detracting from performance. In addition, NMI held longer duration positions in Metropolitan Pier Illinois zero coupon bonds that performed poorly due to spread widening. NEV’s overweight allocation to bonds rated BBB and below was the main detractor from relative performance.

On a sector allocation basis, NUV and NUW performed well. NUV’s overweight to the pre-refunded and appropriation debt sectors and underweight positioning in senior living/life care facilities added to relative performance, offsetting the underperformance of an underweight to state and local GOs. NUW was most helped by overweight allocation to pre-refunded bonds and an underweight to senior living/life care facilities, while an underweight to state GOs modestly detracted. NMI’s underweighting and security selection in the strong performing tax-supported sector (particularly GOs) dampened relative performance. In the health care sector, NMI’s overweight in the senior living/life care facilities and security selection in the hospital segment were also unfavorable to performance. NEV’s overweight to the tobacco sector, which was the best performing sector in the market, along with strong security selection within the sector, contributed positively to performance. However, NEV’s overall sector positioning detracted from performance due to underweight allocations to stronger performing sectors such as utilities and state and local GOs, and overweight allocations to lagging sectors such as hospitals and IDRs.

10

Individual security selection was disadvantageous for NUV and NUW in this reporting period. The timing of certain purchases worked against the two Funds, as bonds bought when interest rates were near the lows in June, July and August underperformed. Bonds with BBB and A ratings also tended to lag in this reporting period. However, our selection in long dated zero coupon bonds was beneficial. NEV also held a number of standout performers in zero coupon bonds, particularly Buckeye Tobacco and Puerto Rico Childrens Trust Fund Tobacco Settlement bonds. Additionally, NEV benefited from the reinstatement of Energy Harbor (formerly FirstEnergy Solutions) secured bonds after the company successfully exited bankruptcy (as described in the strategy section of this commentary). The Fund’s strong performing tobacco and Energy Harbor secured bond positions helped offset weakness in the Energy Harbor equity position, which suffered a correction on negative headline news about the predecessor company and its former parent company, and in bonds that have been slower to recover from the March 2020 market stress, such as state of Illinois GOs, Chicago GOs and New Jersey State Transportation debt.

11

IMPACT OF THE FUNDS’ LEVERAGE STRATEGIES ON PERFORMANCE

One important factor impacting the returns of NEV’s common shares relative to its comparative benchmark was the Fund’s use of leverage. The Fund obtains leverage through investments in inverse floating rate securities, which represent a leveraged investment in an underlying bond. This was also a factor, although less significantly, for NUV and NUW because their use of leverage is more modest. NMI did not invest in inverse floating rate securities during the reporting period.

The Funds use leverage because our research has shown that, over time, leveraging provides opportunities for additional income. The opportunity arises when short-term rates that a Fund pays on its leveraging instruments are lower than the interest the Fund earns on its portfolio of long-term bonds that it has bought with the proceeds of that leverage. This has been particularly true in the recent market environment where short-term rates have been low by historical standards.

However, use of leverage can expose Fund common shares to additional price volatility. When a Fund uses leverage, the Fund’s common shares will experience a greater increase in their net asset value if the municipal bonds acquired through the use of leverage increase in value, but will also experience a correspondingly larger decline in their net asset value if the bonds acquired through leverage decline in value. All this will make the shares’ total return performance more variable over time.

In addition, common share income in levered funds will typically decrease in comparison to unlevered funds when short-term interest rates increase and increase when short-term interest rates decrease. In recent quarters, fund leverage expenses have generally tracked the overall movement of short-term tax-exempt interest rates. While fund leverage expenses are somewhat higher than their recent lows, leverage nevertheless continues to provide the opportunity for incremental common share income, particularly over longer-term periods.

| | | | | |

Leverage had a negligible impact on the performance of NUV, NUW and NEV over the reporting period. | | |

As of October 31, 2020, the Funds’ percentages of leverage are as shown in the accompanying table. | | |

| NUV | NUW | NMI | NEV |

Effective Leverage* | 1.35% | 0.76% | 0.00% | 34.80% |

* | Effective Leverage is a Fund’s effective economic leverage, and includes both regulatory leverage and the leverage effects of certain derivative and other investments in a Fund’s portfolio that increase the Fund’s investment exposure. Currently, the leverage effects of Tender Option Bond (TOB) inverse floater holdings are included in effective leverage values. A Fund, however, may from time to time borrow on a typically transient basis in connection with its day-to-day operations, primarily in connection with the need to settle portfolio trades. Such incidental borrowings are excluded from the calculation of a Fund’s effective leverage ratio. |

12

COMMON SHARE DISTRIBUTION INFORMATION

The following information regarding the Funds’ distributions is current as of October 31, 2020. Each Fund’s distribution levels may vary over time based on each Fund’s investment activity and portfolio investment value changes.

During the current reporting period, each Fund’s distributions to common shareholders were as shown in the accompanying table.

| Per Common Share Amounts |

| Monthly Distributions (Ex-Dividend Date) | NUV | NUW | NMI | NEV |

November 2019 | $0.0310 | $0.0470 | $0.0360 | $0.0565 |

December | 0.0310 | 0.0390 | 0.0360 | 0.0565 |

January | 0.0310 | 0.0390 | 0.0360 | 0.0565 |

February | 0.0310 | 0.0390 | 0.0360 | 0.0565 |

March | 0.0310 | 0.0390 | 0.0330 | 0.0565 |

April | 0.0310 | 0.0390 | 0.0330 | 0.0565 |

May | 0.0310 | 0.0390 | 0.0330 | 0.0610 |

June | 0.0310 | 0.0390 | 0.0330 | 0.0610 |

July | 0.0310 | 0.0390 | 0.0330 | 0.0610 |

August | 0.0310 | 0.0390 | 0.0330 | 0.0610 |

September | 0.0310 | 0.0390 | 0.0330 | 0.0610 |

October 2020 | 0.0310 | 0.0390 | 0.0330 | 0.0610 |

| Total Distributions from Net Investment Income | $0.3720 | $0.4760 | $0.4080 | $0.7050 |

| Total Distributions from Long Term Capital Gains* | $ — | $ — | $0.0357 | $ — |

| Total Distributions | 0.3720 | 0.4760 | 0.4437 | 0.7050 |

| |

| Yields | | | | |

Market Yield** | 3.44% | 2.89% | 3.50% | 5.01% |

Taxable-Equivalent Yield** | 5.73% | 4.88% | 5.91% | 8.46% |

* | Distribution paid in December 2019. |

** | Market Yield is based on the Fund’s current annualized monthly dividend divided by the Fund’s current market price as of the end of the reporting period. Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis. It is based on a federal income tax rate of 40.8%. Your actual federal income tax rate may differ from the assumed rate. The Taxable-Equivalent Yield also takes into account the percentage of the Fund’s income generated and paid by the Fund (based on payments made during the previous calendar year) that was not exempt from federal income tax. Separately, if the comparison were instead to investments that generate qualified dividend income, which is taxable at a rate lower than an individual’s ordinary graduated tax rate, the fund’s Taxable-Equivalent Yield would be lower. |

Each Fund seeks to pay regular monthly dividends out of its net investment income at a rate that reflects its past and projected net income performance. To permit each Fund to maintain a more stable monthly dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net income actually earned by the Fund during the period. Distributions to common shareholders are determined on a tax basis, which may differ from amounts recorded in the accounting records. In instances where the monthly dividend exceeds the earned net investment income, the Fund would report a negative undistributed net ordinary income. Refer to Note 6 – Income Tax Information for additional information regarding the amounts of undistributed net ordinary income and undistributed net long-term capital gains and the character of the actual distributions paid by the Fund during the period.

All monthly dividends paid by each Fund during the current reporting period were paid from net investment income. If a portion of the Fund’s monthly distributions is sourced or comprised of elements other than net investment income, including capital gains and/or a return of capital, common shareholders will be notified of those sources. For financial reporting purposes, the per share amounts of each Fund’s distributions for the reporting period are presented in this report’s Financial Highlights. For income tax purposes, distribution information for each Fund as of its most recent tax year end is presented in Note 6 – Income Tax Information within the Notes to Financial Statements of this report.

13

Common Share Information (continued)

NUVEEN CLOSED-END FUND DISTRIBUTION AMOUNTS

The Nuveen Closed-End Funds’ monthly and quarterly periodic distributions to shareholders are posted on www.nuveen.com and can be found on Nuveen’s enhanced closed-end fund resource page, which is at https://www.nuveen.com/resource-center-closedendfunds, along with other Nuveen closed-end fund product updates. To ensure timely access to the latest information, shareholders may use a subscribe function, which can be activated at this web page (https://www.nuveen.com/subscriptions).

COMMON SHARE EQUITY SHELF PROGRAM

During the current reporting period, NUW and NMI were authorized by the Securities and Exchange Commission to issue additional common shares through an equity shelf program (Shelf Offering). Under these programs, NUW and NMI, subject to market conditions, may raise additional capital from time to time in varying amounts and offering methods at a net price at or above each Fund’s NAV per common share. The total amount of common shares authorized under these Shelf Offerings are shown in the accompanying table.

| NUW | NMI |

Additional authorized common shares | 1,500,000 | 2,200,000* |

* | Represents additional authorized common shares for the period September 23, 2020 through October 31, 2020. An additional 800,000 common shares were authorized for the period November 1, 2019 through March 8, 2020. |

During the current reporting period, NMI sold common shares through its Shelf Offering at a weighted average premium to the NAV per common share as shown in the accompanying table.

| NMI |

Common shares sold through shelf offering | 371,496 |

Weighted average premium to NAV per common share sold | 1.73% |

Refer to the Notes to Financial Statements, Note 5 – Fund Shares for further details on Shelf Offerings and each Fund’s transactions.

COMMON SHARE REPURCHASES

During August 2020, the Funds’ Board of Directors/Trustees reauthorized an open-market common share repurchase program, allowing each Fund to repurchase an aggregate of up to approximately 10% of its outstanding common shares.

As of October 31, 2020, and since the inception of the Funds’ repurchase programs, the Funds have cumulatively repurchased and retired their outstanding common shares as shown in the accompanying table.

| NUV | NUW | NMI | NEV |

Common shares cumulatively repurchased and retired | — | — | — | — |

Common shares authorized for repurchase | 20,690,000 | 1,550,000 | 915,000 | 2,495,000 |

During the current reporting period, the Funds did not repurchase any of their outstanding common shares.

OTHER COMMON SHARE INFORMATION

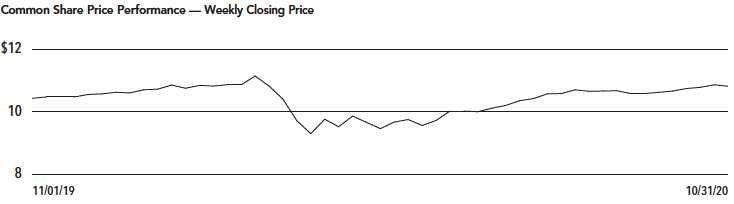

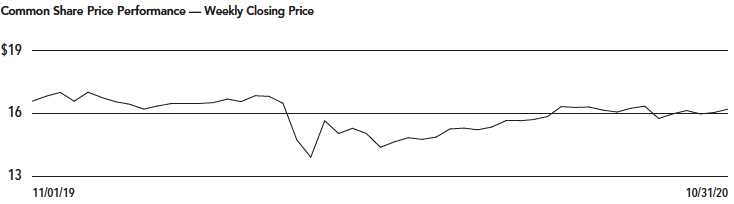

As of October 31, 2020, and during the current reporting period, the Funds’ common share prices were trading at a premium/(discount) to their common share NAVs as shown in the accompanying table.

| NUV | NUW | NMI | NEV |

Common share NAV | $10.48 | $16.81 | $11.08 | $15.05 |

Common share price | $10.81 | $16.21 | $11.31 | $14.61 |

Premium/(Discount) to NAV | 3.15% | (3.57)% | 2.08% | (2.92)% |

12-month average premium/(discount) to NAV | (1.09)% | (5.23)% | 0.33% | (4.01)% |

14

| | |

| NUV | Nuveen Municipal Value Fund, Inc. |

| Performance Overview and Holding Summaries as of October 31, 2020 |

| | | | |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section. | | |

| Average Annual Total Returns as of October 31, 2020 | | | |

| | Average Annual | |

| 1-Year | 5-Year | 10-Year |

NUV at Common Share NAV | 2.72% | 4.35% | 4.96% |

NUV at Common Share Price | 7.41% | 5.36% | 5.17% |

S&P Municipal Bond Index | 3.55% | 3.68% | 4.05% |

Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

15

| | |

| NUV | Performance Overview and Holding Summaries as of October 31, 2020 (continued) |

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

| Fund Allocation | |

| (% of net assets) | |

Long-Term Municipal Bonds | 100.6% |

Other Assets Less Liabilities | 0.8% |

| Net Assets Plus Floating Rate | |

| Obligations | 101.4% |

Floating Rate Obligations | (1.4)% |

| Net Assets | 100% |

| Portfolio Credit Quality | |

| (% of total investment exposure) | |

U.S. Guaranteed | 11.2% |

AAA | 6.0% |

AA | 29.2% |

A | 27.3% |

BBB | 17.8% |

BB or Lower | 3.1% |

N/R (not rated) | 5.4% |

| Total | 100% |

| Portfolio Composition | |

| (% of total investments) | |

Tax Obligation/Limited | 24.3% |

Transportation | 20.5% |

Tax Obligation/General | 12.8% |

U.S. Guaranteed | 11.7% |

Utilities | 9.4% |

Health Care | 9.2% |

Other | 12.1% |

| Total | 100% |

| States and Territories | |

| (% of total municipal bonds) | |

Texas | 15.6% |

Illinois | 11.8% |

California | 8.8% |

New York | 6.4% |

Colorado | 6.2% |

Florida | 4.3% |

New Jersey | 4.1% |

Ohio | 3.7% |

Washington | 3.5% |

Nevada | 2.8% |

Michigan | 2.7% |

Virginia | 2.4% |

Indiana | 2.3% |

Georgia | 2.3% |

South Carolina | 1.8% |

Kentucky | 1.7% |

Other1 | 19.6% |

| Total | 100% |

1 See Portfolio of Investments for details on “other” States and Territories.

16

| | |

| NUW | Nuveen AMT-Free Municipal Value Fund |

| Performance Overview and Holding Summaries as of October 31, 2020 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section. | | |

| Average Annual Total Returns as of October 31, 2020 | | | |

| | Average Annual | |

| 1-Year | 5-Year | 10-Year |

NUW at Common Share NAV | 2.33% | 3.98% | 4.78% |

NUW at Common Share Price | (0.77)% | 3.25% | 4.05% |

S&P Municipal Bond Index | 3.55% | 3.68% | 4.05% |

Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

17

| | |

| NUW | Performance Overview and Holding Summaries as of October 31, 2020 (continued) |

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

| Fund Allocation | |

| (% of net assets) | |

Long-Term Municipal Bonds | 99.6% |

Other Assets Less Liabilities | 1.2% |

| Net Assets Plus Floating Rate | |

| Obligations | 100.8% |

Floating Rate Obligations | (0.8)% |

| Net Assets | 100% |

| Portfolio Credit Quality | |

| (% of total investment exposure) | |

U.S. Guaranteed | 1.1% |

AAA | 6.3% |

AA | 35.4% |

A | 28.1% |

BBB | 19.7% |

BB or Lower | 2.7% |

N/R (not rated) | 6.7% |

| Total | 100% |

| Portfolio Composition | |

| (% of total investments) | |

Tax Obligation/Limited | 24.0% |

Tax Obligation/General | 16.7% |

Utilities | 15.1% |

Transportation | 13.0% |

Health Care | 11.0% |

Water and Sewer | 8.5% |

Other | 11.7% |

| Total | 100% |

| States and Territories | |

| (% of total municipal bonds) | |

California | 14.5% |

Texas | 12.3% |

Illinois | 9.1% |

Colorado | 7.1% |

Nevada | 6.3% |

New York | 5.6% |

Florida | 4.7% |

Georgia | 3.8% |

Kentucky | 3.6% |

Maryland | 3.4% |

Washington | 3.1% |

Puerto Rico | 3.1% |

Ohio | 2.9% |

New Jersey | 2.4% |

Other1 | 18.1% |

| Total | 100% |

1 See Portfolio of Investments for details on “other” States and Territories.

18

| | |

| NMI | Nuveen Municipal Income Fund, Inc. |

| Performance Overview and Holding Summaries as of October 31, 2020 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section. | | |

| Average Annual Total Returns as of October 31, 2020 | | | |

| | Average Annual | |

| 1-Year | 5-Year | 10-Year |

NMI at Common Share NAV | 1.86% | 3.62% | 4.95% |

NMI at Common Share Price | 3.87% | 4.84% | 4.83% |

S&P Municipal Bond Index | 3.55% | 3.68% | 4.05% |

Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

19

| | |

| NMI | Performance Overview and Holding Summaries as of October 31, 2020 (continued) |

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

| Fund Allocation | |

| (% of net assets) | |

Long-Term Municipal Bonds | 99.3% |

Other Assets Less Liabilities | 0.7% |

| Net Assets | 100% |

| Portfolio Credit Quality | |

| (% of total investment exposure) | |

U.S. Guaranteed | 13.3% |

AAA | 0.6% |

AA | 18.6% |

A | 34.5% |

BBB | 20.0% |

BB or Lower | 5.1% |

N/R (not rated) | 7.9% |

| Total | 100% |

| Portfolio Composition | |

| (% of total investments) | |

Health Care | 22.9% |

Tax Obligation/General | 14.4% |

U.S. Guaranteed | 13.1% |

Transportation | 12.7% |

Tax Obligation/Limited | 12.0% |

Education and Civic Organizations | 8.9% |

Utilities | 6.4% |

Other | 9.6% |

| Total | 100% |

| States and Territories | |

| (% of total municipal bonds) | |

California | 15.7% |

Illinois | 10.2% |

Colorado | 10.1% |

Texas | 6.6% |

Florida | 6.3% |

Wisconsin | 5.8% |

Missouri | 4.1% |

New Jersey | 2.9% |

Georgia | 2.8% |

Pennsylvania | 2.8% |

New York | 2.7% |

Michigan | 2.5% |

Ohio | 2.5% |

Indiana | 2.5% |

Arizona | 2.5% |

Other1 | 20.0% |

| Total | 100% |

1 See Portfolio of Investments for details on “other” States and Territories.

20

| | |

| NEV | Nuveen Enhanced Municipal Value Fund |

| Performance Overview and Holding Summaries as of October 31, 2020 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section. | | |

| Average Annual Total Returns as of October 31, 2020 | | | |

| | Average Annual | |

| 1-Year | 5-Year | 10-Year |

NEV at Common Share NAV | 3.55% | 4.59% | 6.18% |

NEV at Common Share Price | 5.03% | 4.47% | 6.22% |

S&P Municipal Bond Index | 3.55% | 3.68% | 4.05% |

Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

21

| | |

| NEV | Performance Overview and Holding Summaries as of October 31, 2020 (continued) |

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

| Fund Allocation | |

| (% of net assets) | |

Long-Term Municipal Bonds | 132.7% |

Common Stocks | 1.4% |

Other Assets Less Liabilities | 2.6% |

| Net Assets Plus Floating Rate | |

| Obligations | 136.7% |

Floating Rate Obligations | (36.7)% |

| Net Assets | 100% |

| Portfolio Credit Quality | |

| (% of total investment exposure) | |

U.S. Guaranteed | 7.5% |

AAA | 3.9% |

AA | 28.5% |

A | 13.6% |

BBB | 27.3% |

BB or Lower | 10.3% |

N/R (not rated) | 8.0% |

N/A (not applicable) | 0.9% |

| Total | 100% |

| Portfolio Composition | |

| (% of total investments) | |

Tax Obligation/Limited | 23.9% |

Transportation | 17.3% |

Health Care | 16.8% |

Tax Obligation/General | 11.8% |

Education and Civic Organizations | 6.9% |

U.S. Guaranteed | 6.5% |

Utilities | 6.0% |

Other | 10.8% |

| Total | 100% |

| States and Territories | |

| (% of total municipal bonds) | |

Illinois | 14.1% |

New Jersey | 10.1% |

California | 8.4% |

New York | 7.5% |

Wisconsin | 6.4% |

Pennsylvania | 5.6% |

Ohio | 5.3% |

Florida | 4.7% |

Louisiana | 4.4% |

Guam | 4.4% |

Georgia | 2.8% |

Texas | 2.7% |

Virginia | 2.6% |

Indiana | 2.5% |

Other1 | 18.5% |

| Total | 100% |

1 See Portfolio of Investments for details on “other” States and Territories.

22

Shareholder Meeting Report

The annual meeting of shareholders was held on August 5, 2020 for NUV, NUW, NMI and NEV. The meeting was held virtually due to public health concerns regarding the ongoing COVID-19 pandemic; at this meeting the shareholders were asked to elect Board members.

| NUV | NUW | NMI | NEV |

| Common | Common | Common | Common |

| shares | shares | shares | shares |

| Approval of the Board Members was reached as follows: | | | | |

John K. Nelson | | | | |

| For | 173,381,228 | 13,863,799 | 7,592,947 | 22,104,293 |

| Withhold | 3,440,838 | 503,000 | 542,642 | 649,816 |

| Total | 176,822,066 | 14,366,799 | 8,135,589 | 22,754,109 |

Terence J. Toth | | | | |

| For | 173,162,921 | 13,859,828 | 7,682,228 | 22,148,279 |

| Withhold | 3,659,145 | 506,971 | 453,361 | 605,830 |

| Total | 176,822,066 | 14,366,799 | 8,135,589 | 22,754,109 |

Robert L. Young | | | | |

| For | 173,424,902 | 13,884,483 | 7,693,347 | 22,167,553 |

| Withhold | 3,397,164 | 482,316 | 442,242 | 586,556 |

| Total | 176,822,066 | 14,366,799 | 8,135,589 | 22,754,109 |

23

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Directors/Trustees

Nuveen Municipal Value Fund, Inc.

Nuveen AMT-Free Municipal Value Fund

Nuveen Municipal Income Fund, Inc.

Nuveen Enhanced Municipal Value Fund:

Opinion on the Financial Statements

We have audited the accompanying statements of assets and liabilities of Nuveen Municipal Value Fund, Inc., Nuveen AMT-Free Municipal Value Fund, Nuveen Municipal Income Fund, Inc., and Nuveen Enhanced Municipal Value Fund (the Funds), including the portfolios of investments, as of October 31, 2020, the related statements of operations and cash flows (Nuveen Enhanced Municipal Value Fund) for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the related notes (collectively, the financial statements) and the financial highlights for each of the years in the five-year period then ended. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Funds as of October 31, 2020, the results of their operations and cash flows (Nuveen Enhanced Municipal Value Fund) for the year then ended, the changes in their net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Funds in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Such procedures also included confirmation of securities owned as of October 31, 2020, by correspondence with custodians and brokers or other appropriate auditing procedures. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements and financial highlights. We believe that our audits provide a reasonable basis for our opinion.

/s/ KPMG LLP

We have served as the auditor of one or more Nuveen investment companies since 2014.

Chicago, Illinois

December 28, 2020

24

| | |

| NUV | Nuveen Municipal Value Fund, Inc. Portfolio of Investments October 31, 2020 |

| | | | | | |

| Principal | | | Optional Call | | |

| Amount (000) | | Description (1) | Provisions (2) | Ratings (3) | Value |

| | LONG-TERM INVESTMENTS – 100.6% | | | |

| | MUNICIPAL BONDS – 100.6% | | | |

| | Alabama – 0.2% | | | |

| | Birmingham Airport Authority, Alabama, Airport Revenue Bonds, Series 2020: | | | |

| $ 255 | | 4.000%, 7/01/39 – BAM Insured | 7/30 at 100.00 | AA | $ 289,366 |

| 225 | | 4.000%, 7/01/40 – BAM Insured | 7/30 at 100.00 | AA | 254,486 |

| 3,805 | | Homewood, Alabama, General Obligation Warrants, Series 2016, 5.000%, 9/01/36 | 9/26 at 100.00 | AA+ | 4,577,682 |

| 4,285 | | Total Alabama | | | 5,121,534 |

| | Alaska – 0.1% | | | |

| 2,710 | | Northern Tobacco Securitization Corporation, Alaska, Tobacco Settlement Asset-Backed | 11/20 at 100.00 | B3 | 2,710,678 |

| | Bonds, Series 2006A, 5.000%, 6/01/32 | | | |

| | Arizona – 1.4% | | | |

| 3,370 | | Arizona Industrial Development Authority, Hospital Revenue Bonds, Phoenix Children’s | 2/30 at 100.00 | A1 | 3,741,610 |

| | Hospital, Series 2020A, 4.000%, 2/01/50 | | | |

| 7,525 | | Chandler Industrial Development Authority, Arizona, Industrial Development Revenue | No Opt. Call | A+ | 8,645,397 |

| | Bonds, Intel Corporation Project, Series 2019, 5.000%, 6/01/49 (AMT) (Mandatory Put 6/03/24) | | | |

| 2,935 | | Phoenix Civic Improvement Corporation, Arizona, Airport Revenue Bonds, Senior Lien | 7/27 at 100.00 | Aa3 | 3,479,883 |

| | Series 2017A, 5.000%, 7/01/35 | | | |

| 780 | | Phoenix Civic Improvement Corporation, Arizona, Excise Tax Revenue Bonds, Subordinate | 7/30 at 100.00 | AAA | 912,779 |

| | Lien Series 2020A, 4.000%, 7/01/45 | | | |

| 5,600 | | Salt Verde Financial Corporation, Arizona, Senior Gas Revenue Bonds, Citigroup Energy | No Opt. Call | A3 | 7,489,832 |

| | Inc Prepay Contract Obligations, Series 2007, 5.000%, 12/01/37 | | | |

| 4,240 | | Scottsdale Industrial Development Authority, Arizona, Hospital Revenue Bonds, Scottsdale | 11/20 at 100.00 | AA | 4,253,950 |

| | Healthcare, Series 2006C Re-offering, 5.000%, 9/01/35 – AGM Insured | | | |

| | Tucson, Arizona, Water System Revenue Bonds, Refunding Series 2017: | | | |

| 1,000 | | 5.000%, 7/01/34 | 7/27 at 100.00 | AA | 1,236,780 |

| 750 | | 5.000%, 7/01/35 | 7/27 at 100.00 | AA | 924,997 |

| 26,200 | | Total Arizona | | | 30,685,228 |

| | California – 8.8% | | | |

| 4,615 | | Anaheim Public Financing Authority, California, Lease Revenue Bonds, Public Improvement | No Opt. Call | AA | 4,510,240 |

| | Project, Series 1997C, 0.000%, 9/01/23 – AGM Insured | | | |

| 5,000 | | Bay Area Toll Authority, California, Revenue Bonds, San Francisco Bay Area Toll Bridge, | 4/23 at 100.00 | AA– (4) | 5,574,400 |

| | Series 2013S-4, 5.000%, 4/01/38 (Pre-refunded 4/01/23) | | | |

| 3,645 | | California County Tobacco Securitization Agency, Tobacco Settlement Asset-Backed Bonds, | 11/20 at 48.64 | CCC– | 1,770,559 |

| | Gold Country Settlement Funding Corporation, Refunding Series 2006, 0.000%, 6/01/33 | | | |

| 405 | | California County Tobacco Securitization Agency, Tobacco Settlement Asset-Backed Bonds, | 6/30 at 100.00 | BBB+ | 450,611 |

| | Los Angeles County Securitization Corporation, Series 2020A, 4.000%, 6/01/49 | | | |

| 1,250 | | California County Tobacco Securitization Agency, Tobacco Settlement Asset-Backed Bonds, | 12/30 at 100.00 | BBB+ | 1,385,525 |

| | Sonoma County Tobacco Securitization Corporation, Series 2020A, 4.000%, 6/01/49 | | | |

| 1,175 | | California Department of Water Resources, Central Valley Project Water System Revenue | 12/26 at 100.00 | AAA | 1,465,143 |

| | Bonds, Refunding Series 2016AW, 5.000%, 12/01/33 | | | |

| 10,000 | | California Health Facilities Financing Authority, California, Revenue Bonds, Sutter | 11/26 at 100.00 | A+ | 11,653,200 |

| | Health, Refunding Series 2016B, 5.000%, 11/15/46 | | | |

| 1,200 | | California Health Facilities Financing Authority, Revenue Bonds, Children’s Hospital Los | 8/27 at 100.00 | BBB+ | 1,399,332 |

| | Angeles, Series 2017A, 5.000%, 8/15/37 | | | |

| 3,850 | | California Health Facilities Financing Authority, Revenue Bonds, Saint Joseph Health | 7/23 at 100.00 | AA– | 4,253,711 |

| | System, Series 2013A, 5.000%, 7/01/33 | | | |

25

| | |

| NUV | Nuveen Municipal Value Fund, Inc. Portfolio of Investments (continued) October 31, 2020 |

| | | | | | |

| Principal | | | Optional Call | | |

| Amount (000) | | Description (1) | Provisions (2) | Ratings (3) | Value |

| | California (continued) | | | |

| $ 6,130 | | California Municipal Finance Authority, Revenue Bonds, Linxs APM Project, Senior Lien | 6/28 at 100.00 | BBB– | $ 6,987,832 |

| | Series 2018A, 5.000%, 12/31/43 (AMT) | | | |

| 2,725 | | California Pollution Control Financing Authority, Water Furnishing Revenue Bonds, San | 1/29 at 100.00 | BBB | 3,104,129 |

| | Diego County Water Authority Desalination Project Pipeline, Refunding Series 2019, 5.000%, | | | |

| | 11/21/45, 144A | | | |

| 1,625 | | California State Public Works Board, Lease Revenue Bonds, Various Capital Projects, | 11/23 at 100.00 | Aa3 | 1,826,793 |

| | Series 2013I, 5.000%, 11/01/38 | | | |

| 5,000 | | California State, General Obligation Bonds, Various Purpose Series 2011, 5.000%, 10/01/41 | 10/21 at 100.00 | Aa2 | 5,199,550 |

| 3,500 | | California Statewide Communities Development Authority, California, Revenue Bonds, Loma | 6/26 at 100.00 | BB | 3,787,525 |

| | Linda University Medical Center, Series 2016A, 5.000%, 12/01/46, 144A | | | |

| 4,505 | | Covina-Valley Unified School District, Los Angeles County, California, General | No Opt. Call | A+ | 4,049,770 |

| | Obligation Bonds, Series 2003B, 0.000%, 6/01/28 – FGIC Insured | | | |

| 5,700 | | East Bay Municipal Utility District, Alameda and Contra Costa Counties, California, | 6/27 at 100.00 | AAA | 6,954,684 |

| | Water System Revenue Bonds, Green Series 2017A, 5.000%, 6/01/45 | | | |

| 2,180 | | Foothill/Eastern Transportation Corridor Agency, California, Toll Road Revenue Bonds, | 1/31 at 100.00 | A– | 2,460,893 |

| | Refunding Series 2013A, 0.000%, 1/15/42 (5) | | | |

| 30,000 | | Foothill/Eastern Transportation Corridor Agency, California, Toll Road Revenue Bonds, | No Opt. Call | AA+ (4) | 29,874,900 |

| | Series 1995A, 0.000%, 1/01/22 (ETM) | | | |

| 13,920 | | Golden State Tobacco Securitization Corporation, California, Tobacco Settlement | 6/22 at 100.00 | N/R | 14,318,390 |

| | Asset-Backed Bonds, Series 2018A-1, 5.000%, 6/01/47 | | | |

| 4,000 | | Los Angeles County Metropolitan Transportation Authority, California, Measure R Sales | 6/30 at 100.00 | AA | 4,791,160 |

| | Tax Revenue Bonds, Refunding Junior Subordinate Green Series 2020A, 4.000%, 6/01/37 | | | |

| | Merced Union High School District, Merced County, California, General Obligation Bonds, | | | |

| | Series 1999A: | | | |

| 2,500 | | 0.000%, 8/01/23 – FGIC Insured | No Opt. Call | AA– | 2,457,675 |

| 2,555 | | 0.000%, 8/01/24 – FGIC Insured | No Opt. Call | AA– | 2,489,745 |

| 2,365 | | Montebello Unified School District, Los Angeles County, California, General Obligation | No Opt. Call | A– | 2,165,441 |

| | Bonds, Election 1998 Series 2004, 0.000%, 8/01/27 – FGIC Insured | | | |

| | Mount San Antonio Community College District, Los Angeles County, California, General | | | |

| | Obligation Bonds, Election of 2008, Series 2013A: | | | |

| 3,060 | | 0.000%, 8/01/28 (5) | 2/28 at 100.00 | Aa1 | 3,540,726 |

| 2,315 | | 0.000%, 8/01/43 (5) | 8/35 at 100.00 | Aa1 | 2,386,024 |

| 3,550 | | M-S-R Energy Authority, California, Gas Revenue Bonds, Citigroup Prepay Contracts, | No Opt. Call | A | 5,530,225 |

| | Series 2009C, 6.500%, 11/01/39 | | | |

| 10,150 | | Placer Union High School District, Placer County, California, General Obligation Bonds, | No Opt. Call | AA | 7,794,997 |

| | Series 2004C, 0.000%, 8/01/33 – AGM Insured | | | |

| | San Bruno Park School District, San Mateo County, California, General Obligation Bonds, | | | |

| | Series 2000B: | | | |

| 2,575 | | 0.000%, 8/01/24 – FGIC Insured | No Opt. Call | Aa2 | 2,500,840 |

| 2,660 | | 0.000%, 8/01/25 – FGIC Insured | No Opt. Call | Aa2 | 2,550,142 |

| 415 | | San Diego Tobacco Settlement Revenue Funding Corporation, California, Tobacco Settlement | 6/28 at 100.00 | BBB | 436,319 |

| | Bonds, Subordinate Series 2018C, 4.000%, 6/01/32 | | | |

| 10,000 | | San Francisco Airports Commission, California, Revenue Bonds, San Francisco | 5/29 at 100.00 | A1 | 12,263,200 |

| | International Airport, Refunding Second Series 2019D, 5.000%, 5/01/39 | | | |

| 250 | | San Francisco Redevelopment Financing Authority, California, Tax Allocation Revenue | 2/21 at 100.00 | BBB+ (4) | 254,058 |

| | Bonds, Mission Bay South Redevelopment Project, Series 2011D, 7.000%, 8/01/41 | | | |

| | (Pre-refunded 2/01/21) | | | |

| 12,095 | | San Joaquin Hills Transportation Corridor Agency, Orange County, California, Toll Road | No Opt. Call | Baa2 | 11,148,445 |

| | Revenue Bonds, Refunding Series 1997A, 0.000%, 1/15/25 – NPFG Insured | | | |

| 13,220 | | San Mateo County Community College District, California, General Obligation Bonds, | No Opt. Call | AAA | 12,027,688 |

| | Series 2006A, 0.000%, 9/01/28 – NPFG Insured | | | |

26

| | | | | | |

| Principal | | | Optional Call | | |

| Amount (000) | | Description (1) | Provisions (2) | Ratings (3) | Value |

| | California (continued) | | | |

| $ 5,000 | | San Mateo Union High School District, San Mateo County, California, General Obligation | No Opt. Call | Aaa | $ 4,900,850 |

| | Bonds, Election of 2000, Series 2002B, 0.000%, 9/01/24 – FGIC Insured | | | |

| 5,815 | | San Ysidro School District, San Diego County, California, General Obligation Bonds, | 8/25 at 29.16 | AA | 1,530,741 |

| | Refunding Series 2015, 0.000%, 8/01/48 | | | |

| 2,000 | | Tobacco Securitization Authority of Northern California, Tobacco Settlement Asset-Backed | 11/20 at 100.00 | B | 2,007,980 |

| | Bonds, Refunding Series 2005A-2, 5.400%, 6/01/27 | | | |

| 190,950 | | Total California | | | 191,803,443 |

| | Colorado – 6.2% | | | |

| 7,500 | | Arapahoe County School District 6, Littleton, Colorado, General Obligation Bonds, Series | 12/28 at 100.00 | AA | 9,582,825 |

| | 2019A, 5.500%, 12/01/43 | | | |

| 7,105 | | Colorado Health Facilities Authority, Colorado, Revenue Bonds, Catholic Health | 1/23 at 100.00 | BBB+ (4) | 7,844,062 |

| | Initiatives, Series 2013A, 5.250%, 1/01/45 (Pre-refunded 1/01/23) | | | |

| 4,155 | | Colorado Health Facilities Authority, Colorado, Revenue Bonds, CommonSpirit Health, | 8/29 at 100.00 | BBB+ | 4,506,222 |

| | Series 2019A-1, 4.000%, 8/01/44 | | | |

| 1,255 | | Colorado High Performance Transportation Enterprise, C-470 Express Lanes Revenue Bonds, | 12/24 at 100.00 | BBB | 1,354,948 |

| | Senior Lien Series 2017, 5.000%, 12/31/51 | | | |

| 2,000 | | Colorado State Board of Governors, Colorado State University Auxiliary Enterprise System | 3/22 at 100.00 | AA (4) | 2,126,400 |

| | Revenue Bonds, Series 2012A, 5.000%, 3/01/41 (Pre-refunded 3/01/22) | | | |

| 4,500 | | Colorado State, Building Excellent Schools Today, Certificates of Participation, Series | 3/28 at 100.00 | Aa2 | 5,517,495 |

| | 2018N, 5.000%, 3/15/37 | | | |

| | Colorado State, Certificates of Participation, Lease Purchase Financing Program, | | | |

| | National Western Center, Series 2018A: | | | |

| 1,250 | | 5.000%, 9/01/30 | 3/28 at 100.00 | Aa2 | 1,581,375 |

| 2,000 | | 5.000%, 9/01/31 | 3/28 at 100.00 | Aa2 | 2,517,260 |

| 1,260 | | 5.000%, 9/01/32 | 3/28 at 100.00 | Aa2 | 1,577,016 |

| 620 | | 5.000%, 9/01/33 | 3/28 at 100.00 | Aa2 | 770,158 |

| 3,790 | | Colorado State, Certificates of Participation, Rural Series 2018A, 5.000%, 12/15/37 | 12/28 at 100.00 | Aa2 | 4,750,159 |

| | Denver City and County, Colorado, Airport System Revenue Bonds, Series 2012B: | | | |

| 2,750 | | 5.000%, 11/15/25 | 11/22 at 100.00 | AA– | 2,986,692 |

| 2,200 | | 5.000%, 11/15/29 (Pre-refunded 11/15/22) | 11/22 at 100.00 | AA– (4) | 2,409,440 |

| 5,160 | | Denver City and County, Colorado, Airport System Revenue Bonds, Subordinate Lien Series | 11/23 at 100.00 | A+ | 5,623,523 |

| | 2013B, 5.000%, 11/15/43 | | | |

| 2,000 | | Denver Convention Center Hotel Authority, Colorado, Revenue Bonds, Convention Center | 12/26 at 100.00 | Baa2 | 2,134,540 |

| | Hotel, Refunding Senior Lien Series 2016, 5.000%, 12/01/35 | | | |

| | E-470 Public Highway Authority, Colorado, Senior Revenue Bonds, Series 2000B: | | | |

| 9,660 | | 0.000%, 9/01/29 – NPFG Insured | No Opt. Call | A | 8,390,193 |

| 24,200 | | 0.000%, 9/01/31 – NPFG Insured | No Opt. Call | A | 19,847,630 |

| 17,000 | | 0.000%, 9/01/32 – NPFG Insured | No Opt. Call | A | 13,500,720 |

| 1,705 | | E-470 Public Highway Authority, Colorado, Senior Revenue Bonds, Series 2020A, | | | |

| | 5.000%, 9/01/40 | 9/24 at 100.00 | A | 1,932,038 |

| 7,600 | | E-470 Public Highway Authority, Colorado, Toll Revenue Bonds, Refunding Series 2006B, | 9/26 at 52.09 | A | 3,585,452 |

| | 0.000%, 9/01/39 – NPFG Insured | | | |

| 8,000 | | Public Authority for Colorado Energy, Natural Gas Purchase Revenue Bonds, Colorado | No Opt. Call | A+ | 12,346,400 |

| | Springs Utilities, Series 2008, 6.500%, 11/15/38 | | | |

| 5,000 | | Rangely Hospital District, Rio Blanco County, Colorado, General Obligation Bonds, | 11/21 at 100.00 | Baa3 | 5,158,500 |

| | Refunding Series 2011, 6.000%, 11/01/26 | | | |

| 3,750 | | Regional Transportation District, Colorado, Denver Transit Partners Eagle P3 Project | 11/20 at 100.00 | Baa3 | 3,756,750 |

| | Private Activity Bonds, Series 2010, 6.000%, 1/15/41 | | | |

| 4,945 | | Regional Transportation District, Colorado, Sales Tax Revenue Bonds, Fastracks Project, | 11/26 at 100.00 | AA+ | 5,863,089 |

| | Series 2017A, 5.000%, 11/01/40 | | | |

| 4,250 | | University of Colorado, Enterprise System Revenue Bonds, Series 2018B, 5.000%, 6/01/43 | 6/28 at 100.00 | Aa1 | 5,224,142 |

| 133,655 | | Total Colorado | | | 134,887,029 |

27

| | |

| NUV | Nuveen Municipal Value Fund, Inc. Portfolio of Investments (continued) October 31, 2020 |

| | | | | | |

| Principal | | | Optional Call | | |

| Amount (000) | | Description (1) | Provisions (2) | Ratings (3) | Value |

| | Connecticut – 0.8% | | | |

| $ 1,500 | | Connecticut Health and Educational Facilities Authority, Revenue Bonds, Hartford | 7/21 at 100.00 | A+ (4) | $ 1,546,215 |

| | HealthCare, Series 2011A, 5.000%, 7/01/41 (Pre-refunded 7/01/21) | | | |

| 8,440 | | Connecticut State, General Obligation Bonds, Series 2015E, 5.000%, 8/01/29 | 8/25 at 100.00 | A1 | 9,973,464 |

| 5,000 | | Connecticut State, General Obligation Bonds, Series 2015F, 5.000%, 11/15/33 | 11/25 at 100.00 | A1 | 5,879,900 |

| 10,153 | | Mashantucket Western Pequot Tribe, Connecticut, Special Revenue Bonds, Subordinate | No Opt. Call | N/R | 659,964 |

| | Series 2013A, 0.070%, 7/01/31 (cash 4.000%, PIK 2.050%) (6) | | | |

| 25,093 | | Total Connecticut | | | 18,059,543 |

| | District of Columbia – 0.6% | | | |

| 15,000 | | District of Columbia Tobacco Settlement Corporation, Tobacco Settlement Asset-Backed | 11/20 at 20.76 | N/R | 3,106,500 |

| | Bonds, Series 2006A, 0.000%, 6/15/46 | | | |

| 5,390 | | District of Columbia Water and Sewer Authority, Public Utility Revenue Bonds, Senior | 4/28 at 100.00 | AAA | 6,671,850 |

| | Lien Series 2018B, 5.000%, 10/01/43 | | | |

| 2,390 | | Washington Metropolitan Area Transit Authority, District of Columbia, Dedicated Revenue | 7/30 at 100.00 | AA | 2,752,635 |

| | Bonds, Series 2020A, 4.000%, 7/15/45 | | | |

| 22,780 | | Total District of Columbia | | | 12,530,985 |

| | Florida – 4.4% | | | |

| 1,240 | | Broward County, Florida, Half-Cent Sales Tax Revenue Bonds, Refunding Series 2020, | 10/30 at 100.00 | AA+ | 1,478,303 |

| | 4.000%, 10/01/40 | | | |

| 3,000 | | Cape Coral, Florida, Water and Sewer Revenue Bonds, Refunding Series 2011, 5.000%, | 10/21 at 100.00 | AA (4) | 3,129,330 |

| | 10/01/41 (Pre-refunded 10/01/21) – AGM Insured | | | |

| 565 | | Florida Development Finance Corporation, Educational Facilities Revenue Bonds, | 6/25 at 100.00 | N/R | 630,574 |

| | Renaissance Charter School Income Projects, Series 2015A, 6.000%, 6/15/35, 144A | | | |

| | Florida Development Finance Corporation, Florida, Surface Transportation Facility | | | |

| | Revenue Bonds, Virgin Trains USA Passenger Rail Project , Series 2019A: | | | |

| 3,400 | | 6.250%, 1/01/49 (AMT) (Mandatory Put 1/01/24), 144A | 11/20 at 104.00 | N/R | 2,956,538 |

| 3,400 | | 6.375%, 1/01/49 (AMT) (Mandatory Put 1/01/26), 144A | 11/20 at 105.00 | N/R | 2,919,104 |

| 3,400 | | 6.500%, 1/01/49 (AMT) (Mandatory Put 1/01/29), 144A | 11/20 at 105.00 | N/R | 2,913,154 |

| | Fort Myers, Florida, Utility System Revenue Bonds, Refunding Subordinate Series 2020B: | | | |

| 1,400 | | 5.000%, 10/01/27 – AGM Insured | No Opt. Call | AA | 1,779,428 |

| 1,750 | | 5.000%, 10/01/28 – AGM Insured | No Opt. Call | AA | 2,268,613 |

| 4,000 | | Gainesville, Florida, Utilities System Revenue Bonds, Series 2017A, 5.000%, 10/01/37 | 10/27 at 100.00 | AA– | 4,926,760 |

| 3,500 | | Gainesville, Florida, Utilities System Revenue Bonds, Series 2019A, 5.000%, 10/01/44 | 10/29 at 100.00 | AA– | 4,436,425 |

| 2,290 | | Hillsborough County Aviation Authority, Florida, Revenue Bonds, Tampa International | 10/24 at 100.00 | A1 | 2,578,838 |

| | Airport, Subordinate Lien Series 2015B, 5.000%, 10/01/40 | | | |

| 5,090 | | Miami-Dade County Expressway Authority, Florida, Toll System Revenue Bonds, Series | 11/20 at 100.00 | A | 5,103,132 |

| | 2010A, 5.000%, 7/01/40 | | | |

| 9,500 | | Miami-Dade County Health Facility Authority, Florida, Hospital Revenue Bonds, Miami | 8/21 at 100.00 | A (4) | 9,901,565 |

| | Children’s Hospital, Series 2010A, 6.000%, 8/01/46 (Pre-refunded 8/01/21) | | | |

| 2,000 | | Miami-Dade County, Florida, Aviation Revenue Bonds, Miami International Airport, | 10/24 at 100.00 | A2 | 2,253,060 |

| | Refunding Series 2014B, 5.000%, 10/01/37 | | | |

| 4,000 | | Miami-Dade County, Florida, Transit System Sales Surtax Revenue Bonds, Refunding Series | 7/22 at 100.00 | AA (4) | 4,315,440 |

| | 2012, 5.000%, 7/01/42 (Pre-refunded 7/01/22) | | | |

| | Orlando Utilities Commission, Florida, Utility System Revenue Bonds, Series 2018A: | | | |

| 3,500 | | 5.000%, 10/01/36 | 10/27 at 100.00 | AA | 4,335,625 |

| 3,780 | | 5.000%, 10/01/37 | 10/27 at 100.00 | AA | 4,661,383 |

| 1,120 | | 5.000%, 10/01/38 | 10/27 at 100.00 | AA | 1,374,318 |

| 10,725 | | Orlando, Florida, Contract Tourist Development Tax Payments Revenue Bonds, Series 2014A, | 5/24 at 100.00 | AA+ (4) | 12,443,359 |

| | 5.000%, 11/01/44 (Pre-refunded 5/01/24) | | | |

| 3,250 | | Palm Beach County Health Facilities Authority, Florida, Revenue Bonds, Jupiter Medical | 11/22 at 100.00 | BBB+ | 3,377,595 |

| | Center, Series 2013A, 5.000%, 11/01/43 | | | |

28

| | | | | | |

| Principal | | | Optional Call | | |

| Amount (000) | | Description (1) | Provisions (2) | Ratings (3) | Value |

| | Florida (continued) | | | |

| $ 4,000 | | Pembroke Pines, Florida, Capital Improvement Revenue Bonds, Series 2019A, | 7/29 at 100.00 | AA | $ 4,659,200 |

| | 4.000%, 7/01/38 | | | |

| 1,020 | | Putnam County Development Authority, Florida, Pollution Control Revenue Bonds, Seminole | 5/28 at 100.00 | A– | 1,221,450 |

| | Electric Cooperative, Inc Project, Refunding Series 2018B, 5.000%, 3/15/42 | | | |