UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2008 |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT of 1934 |

Commission file number 000-53587

Invitel Holdings A/S

(Exact name of Registrant as specified in its charter)

Denmark

(Jurisdiction of incorporation or organization)

Puskas Tivador u. 8-10, H-2040 Budaors, Hungary

(Address of principal executive offices)

Peter T. Noone

General Counsel, Invitel Holdings A/S

1201 Third Avenue, Suite 3400

Seattle, WA 98101-3034

Telephone: 206-654-0204

Facsimile: 206-652-2911

(Name, Telephone, Facsimile Number and Address of Company Contact Person)

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | | Name of each exchange on which registered |

Ordinary Shares of EUR 0.01 each American Depository Shares, each representing one Ordinary Share, EUR 0.01 per Ordinary Share | | NYSE Amex Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

The number of outstanding shares of each of the issuer’s classes of capital or common stock as of December 31, 2008 was:

16,425,733 shares of common stock (subsequently converted to Ordinary Shares)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ¨ Yes x No

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirement for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ¨ Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer” and “large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

¨ Large accelerated filer x Accelerated filer ¨ Non-accelerated filer

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing.

| | | | |

| x U.S. GAAP | | ¨ International Financial Reporting Standards as issued by the International Accounting Standards Board | | ¨ Other |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow: ¨ Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

Preliminary Note

On February 24, 2009, the stockholders of Hungarian Telephone and Cable Corp., a Delaware company (“HTCC”), approved the adoption of an agreement and plan of merger among HTCC, Invitel Sub LLC, a Delaware limited liability company (“MergeCo”), and Invitel Holdings A/S, a Danish company (“Invitel Holdings”), whereby HTCC would effectively change its place of incorporation from Delaware to Denmark by merging HTCC with and into MergeCo, which would be the surviving company and become a wholly owned direct subsidiary of Invitel Holdings, and pursuant to which each share of HTCC would automatically be converted into the right to receive one American depositary share of Invitel Holdings representing one ordinary share of Invitel Holdings.

On February 26, 2009, the merger and reorganization were completed and the HTCC shareholders became holders of American depositary shares of Invitel Holdings.

Invitel Holdings’ American depositary shares and the underlying ordinary shares are registered with the Securities and Exchange Commission (the “SEC”) pursuant to Section 12 of the Securities Exchange Act of 1934. Invitel Holdings is a “foreign private issuer” as defined in Rule 3b-4 of the General Rules and Regulations Under the Securities Exchange Act of 1934. As a foreign private issuer, Invitel Holdings is required to file with the SEC Annual Reports on Form 20-F. Pursuant to subsection (g) of Rule 12g-3 “Registration of Securities of Successor Issuers Under Section 12(b) or Section 12(g)” of the General Rules and Regulations Under the Securities Exchange Act of 1934, Invitel Holdings is required to file with the SEC, as successor issuer to HTCC, an annual report for 2008 containing such information that would be required if filed by HTCC, Invitel Holdings’ predecessor.

HTCC would have been required to file an annual report containing the disclosure required by SEC Form 10-K with financial statements prepared in accordance with United States Generally Accepted Accounting Principles (U.S. GAAP). Accordingly, this Annual Report of Invitel Holdings on Form 20-F contains such information (including the numbers, captions and text of all items of Form 10-K) that HTCC would have filed but for the completion of the reorganization merger.

For 2009, and as permitted by the SEC, Invitel Holdings currently intends to prepare its financial statements in accordance with International Financial Reporting Standards (“IFRS”) and to change its reporting currency from U.S. dollars to euros.

CERTAIN DEFINITIONS AND PRESENTATION OF GENERAL INFORMATION

In this annual report, unless indicated otherwise in this report or the context requires otherwise, the following definitions shall apply:

American Depositary Shares (ADS). A security that allows shareholders in the United States to hold and trade interests in foreign-based companies more easily. ADSs are often evidenced by certificates known as American depositary receipts, or ADRs. Invitel Holdings A/S is a Danish corporation that issues ordinary shares. Each Invitel Holdings A/S ADS represents one Invitel Holdings A/S ordinary share.

Common Stock. The common stock of Hungarian Telephone and Cable Corp., par value $0.001.

Company. Hungarian Telephone and Cable Corp., together with its consolidated subsidiaries (succeeded by Invitel Holdings A/S, as successor to Hungarian Telephone and Cable Corp., and its consolidated subsidiaries).

DKK. The Danish kroner, which is the lawful currency of Denmark.

E.U. The European Union.

EU-15.A reference to the following member countries of the European Union: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Spain, Sweden and the United Kingdom.

Euro, € or EUR. The euro, which is the lawful currency of the participating member states of the E.U.

Euroweb. Euroweb Hungary and Euroweb Romania, collectively.

Euroweb Hungary. Euroweb Internet Szolgáltató ZRt., a Hungarian company, which was an indirect subsidiary of HTCC until it merged into Invitel effective January 1, 2008.

Euroweb Romania. Euroweb Romania S.A., a Romanian company, which was an indirect subsidiary of HTCC (now an indirect subsidiary of Invitel Holdings).

FASB. The Financial Accounting Standards Board.

forint or HUF. The Hungarian forint, which is the lawful currency of the Republic of Hungary.

historical concession area. Each of the 54 geographically defined concessions areas for local public fixed line voice telephony service in Hungary which, prior to 2002, were served by local telephone operators with exclusive rights and responsibilities for providing local fixed line telecommunications services.

Holdco I. HTCC Holdco I B.V., a company incorporated in the Netherlands, which was an indirect subsidiary of HTCC (now an indirect subsidiary of Invitel Holdings).

Holdco II. HTCC Holdco II B.V., a company incorporated in the Netherlands, which was an indirect subsidiary of HTCC (now an indirect subsidiary of Invitel Holdings).

HTCC. Hungarian Telephone and Cable Corp., a Delaware company and the parent company prior to the Reorganization which was completed on February 26, 2009. HTCC was merged out of existence following the completion of the Reorganization merger and succeeded by Invitel Holdings.

-1-

HTCC Subsidiaries. All of the subsidiary companies that were directly or indirectly owned by HTCC (now directly or indirectly owned by Invitel Holdings).

Hungarotel. Hungarotel Távközlési Zrt., a Hungarian company, which was an indirect subsidiary of HTCC until it merged into Invitel effective January 1, 2008.

Hungarotel historical concession areas. The areas in which Hungarotel operated five telecommunications concessions granted by the Hungarian government on an exclusive basis until 2002.

Invitel. Invitel Távközlési Zrt., a Hungarian company, which was an indirect subsidiary of HTCC (now an indirect subsidiary of Invitel Holdings).

Invitel Acquisition. The acquisition by the Company of Matel Holdings and its direct and indirect subsidiaries, including its principal operating subsidiaries Invitel and Euroweb, which acquisition was completed on April 27, 2007.

Invitel historical concession areas. The areas in which Invitel operated nine telecommunications concessions granted by the Hungarian government on an exclusive basis until 2002.

Invitel Holdings. Invitel Holdings A/S, a Danish company, and the parent company (as successor to Hungarian Telephone and Cable Corp.) following the Reorganization which was completed on February 26, 2009.

Invitel Holdings ADSs. The American Depositary Shares or ADSs that represent Invitel Holdings A/S’s ordinary shares. Each Invitel Holdings A/S ADS represents one Invitel Holdings A/S ordinary share.

Invitel Holdings Hungary. Invitel Holdings Hungary Kft., a Hungarian company, which was a direct subsidiary of HTCC (now a direct subsidiary of Invitel Holdings).

Invitel International. Invitel International AG, an Austrian company which was an indirect subsidiary of HTCC (now an indirect subsidiary of Invitel Holdings). Memorex Telex Communications AG was renamed Invitel International AG effective July 25, 2008.

Invitel International Hungary.Invitel International Hungary Kft., a Hungarian company, which was an indirect subsidiary of HTCC (now an indirect subsidiary of Invitel Holdings).

Invitel Technocom. Invitel Technocom Kft, a Hungarian company, which was an indirect subsidiary of HTCC (now an indirect subsidiary of Invitel Holdings). PanTel Technocom Kft. was renamed Invitel Technocom Kft. effective January 1, 2008.

Invitel Telecom. Invitel Telecom Kft., a Hungarian company, which was an indirect subsidiary of HTCC (now an indirect subsidiary of Invitel Holdings). Tele2 Magyarország Kft. was renamed Invitel Telecom Kft. effective January 1, 2008.

Matel. Magyar Telecom B.V., a company incorporated in The Netherlands, which was an indirect subsidiary of HTCC (now an indirect subsidiary of Invitel Holdings).

Matel Holdings. Matel Holdings N.V., a company incorporated in The Netherlands Antilles, which was an indirect subsidiary of HTCC (now an indirect subsidiary of Invitel Holdings).

-2-

Memorex. Memorex Telex Communications AG, an Austrian company, together with its consolidated subsidiaries. Memorex Telex Communications AG was renamed Invitel International AG effective July 25, 2008.

Memorex Acquisition. The acquisition by the Company of 95.7% of the outstanding equity of Memorex, which acquisition was completed on March 5, 2008. We acquired the remaining minority interest on August 28, 2008.

Memorex Subsidiaries. The consolidated subsidiaries of Memorex (now Invitel International AG’s subsidiaries).

NHH. The Hungarian National Communications Authority.

our historical concession areas or the Company’s historical concession areas. The Hungarotel historical concession areas and the Invitel historical concession areas combined.

Ordinary Shares. The shares issued by Invitel Holdings A/S with a nominal value of EUR 0.01 each.

PanTel. PanTel Távközlési Kft., a Hungarian company, which was an indirect subsidiary of HTCC until it merged into Invitel effective January 1, 2008.

PanTel Technocom. PanTel Technocom Kft, a Hungarian company, which was an indirectsubsidiary of HTCC (now an indirect subsidiary of Invitel Holdings A/S). PanTel Technocom Kft. was renamed Invitel Technocom Kft. effective January 1, 2008.

Registrant. Refers to Invitel Holdings A/S as successor to Hungarian Telephone and Cable Corp., which is the parent company and registered with the United States Securities and Exchange Commission.

Reorganization. The Reorganization completed on February 26, 2009 pursuant to which HTCC effectively changed its place of incorporation from Delaware to Denmark by merging HTCC with and into a wholly owned subsidiary of Invitel Holdings A/S, a newly formed company in Denmark that we created for the purpose of the Reorganization. Each share of HTCC was converted into the right to receive one American Depositary Share of Invitel Holdings A/S. After completion of the Reorganization, Invitel Holdings A/S and its subsidiaries continue to conduct the business formerly conducted by HTCC and its subsidiaries.

Report. This annual report on Form 20-F for the fiscal year ended December 31, 2008.

RIO. Reference Interconnect Offer.

RUO. Reference Unbundling Offer.

SEC. The United States Securities and Exchange Commission.

SMP. Significant Market Power. A telecommunications services provider, which has been designated with significant market power following a market analysis by the Hungarian regulatory authorities.

T-Com. The brand name under which Magyar Telekom Plc. operates its fixed line telecommunications business in Hungary.

-3-

TDC. TDC A/S, a Danish company (formerly known as Tele Danmark A/S), together with its affiliates. TDC is our majority stockholder and owns approximately 64.6% of our outstanding equity.

Tele2 Hungary. Tele2 Magyarország Kft., a Hungarian company, which was an indirect subsidiary of HTCC (now an indirect subsidiary of Invitel Holdings A/S). Tele2 Magyarország Kft. was renamed Invitel Telecom Kft. effective January 1, 2008.

Tele2 Hungary Acquisition. The acquisition by the Company of Tele2 Hungary, which acquisition was completed on October 18, 2007.

U.S. dollar, USD or $. The U.S. dollar, which is the lawful currency of the United States of America.

V-holding. V-holding Tanácsadó Zrt., a Hungarian company, which was an indirect subsidiary of HTCC until it merged into Invitel effective January 1, 2008.

we, us and our. Refers to the Company.

In addition, we have included a glossary of certain technical terms used in this Report under the heading “Glossary of Terms”.

-4-

GLOSSARY OF TERMS

Our industry uses many terms and acronyms that may not be familiar to you. To assist you in reading this Report, we have provided below definitions of some of these terms.

Access or Telephone Lines. Telephone lines reaching from the customer’s premises to a connection with the telephone service provider’s network. When we refer to our access lines or telephone lines, we include our customers with either a wired or fixed wireless connection to our network.

Access Network. The part of the telecommunications network which connects the end users to the backbone.

Average Revenue Per User (ARPU). The average revenue per user.

Asynchronous Transfer Mode (ATM). An international high-speed, high-volume, packet-switching protocol which supplies bandwidth on demand and divides any signal (voice, data or video) into efficient, manageable packets for ultra-fast switching.

Backbone. A centralized high-speed network that interconnects smaller, independent networks.

Bitstream Access. The provision of broadband access on local loops using DSL technology.

Bandwidth. The number of bits of information which can move through a communications medium in a given amount of time (normally measured in bits per second).

Broadband. High speed access to the Internet. Telecommunication in which a wide band of frequencies is available to transmit information. Because a wide band of frequencies is available, information can be multiplexed and sent on many different frequencies or channels within the band concurrently, allowing more information to be transmitted in a given amount of time. Various definers have assigned a minimum data rate to qualify as broadband.

Cable Modem. A device that enables a PC to connect to the cable TV network and receive data at a high speed.

Carrier Selection (CS).The ability to select the telecommunications service provider for certain calls on a call-by-call basis, whereby a telecommunications service provider different from the default telecommunications service provider may be selected by the customer by dialing a prefix when making certain calls.

Carrier Pre-Selection (CPS).The ability to select the telecommunications service provider for certain calls on a pre-set basis so that the selected telecommunications service provider is the default telecommunications service provider on such calls without having to dial a prefix.

Central Office (CO). The site with the local telecommunications services provider’s equipment that routes calls to and from customers. It also connects customers to Internet Service Providers and long distance carriers.

Churn. A measure of customers who stop purchasing our services as manifested by the loss of either voice traffic (as measured in minutes) or lines, leading to reduced revenue.

Co-location. A type of service where the customer’s telecommunications equipment and/or other hardware and equipment is housed within the provider’s facilities usually for the purpose of connecting the customer’s network with other networks. The co-location provider is typically responsible for power and connectivity.

-5-

Dark Fiber.Unused fiber optic cable. Fiber optic cables convey information in the form of light pulses so that “dark” fiber means that no light pulses are being sent over the fiber optic cable.

Dense Wavelength Division Multiplexing (DWDM).A way of increasing the capacity of fiber optic networks. DWDM carries multiple colors of light, or multiple wavelengths on a single strand of fiber.

Digital.A method of storing, processing and transmitting information through the use of distinct electronic or optical pulses that represent the binary digits 0 and 1. Digital transmission and switching technologies employ a sequence of these pulses to represent information as opposed to the continuously variable analog signal. The precise digital numbers minimize distortion (such as graininess or snow in the case of video transmission, or static or other background distortion in the case of audio transmission).

Digital Subscriber Line (DSL). An access technology that allows voice and high-speed data to be sent simultaneously over local exchange service copper facilities.

Ethernet.A local area network architecture. It is the most common type of connection computers use in a local area network. An Ethernet port looks much like a regular phone jack, but is slightly wider. This port can be used to connect a computer to another computer, a local network, or an external DSL or cable modem.

Fiber Optic Cable.A type of cable made from hair-thin glass (rather than copper) through which information travels as light. Fiber optic cables have a much greater bandwidth capacity than metal cables. Fiber optic cables form the basis for telecommunication providers’ backbone networks in transmitting information long distances.

Fixed Lines/Fixed Telephone Lines. Refers to both wireline and fixed wireless telephone access lines.

Fixed Wireless. The operation of wireless devices (such as a telephone) in fixed locations such as homes and offices. The geographic range of the mobility is limited to a small area.

Frame Relay.A high speed switching technology, primarily used to interconnect multiple local area networks.

GSM. Global system for mobile communications.

Incumbent. The dominant operator which was licensed to enter the market and establish a proprietary network under the protection of a regulatory monopoly.

Incumbent Local Telephone Operator (ILTO). A traditional fixed line telecommunications services provider that, until 2002, had the exclusive right and responsibility for providing local telecommunications services in certain local service areas within Hungary.

Integrated Services Digital Network (ISDN).A telecommunications standard that uses digital transmission technology to support voice, video and data communication applications over regular telephone lines.

Internet. A public network based on a common communication protocol which supports communication through the world wide web.

Internet Protocol (IP).A protocol for transferring information across the Internet in packets of data.

Internet Service Provider (ISP). A business that provides Internet access to customers.

-6-

ISDN2. ISDN access with two channels designed primarily for residential use.

ISDN30. ISDN access with 30 channels designed primarily for business use.

Last Mile.The telecommunications technology that connects the customer’s premises directly to the network of the telecommunications provider, traditionally a wired connection through a twisted pair copper wire telephone cable (in the case of the telecommunications provider) or a coaxial cable (in the case of a cable television operator) but it can also be a fixed wireless connection.

Leased Lines.A telephone line (a direct circuit or channel) specifically dedicated to an end-user organization for the purpose of directly connecting two or more of that organization’s sites. They are used to transmit voice, data or video between the sites.

Local Area Network (LAN). A network located in a single location such as a floor, department or building.

Local Loop.The telephone line that runs from the local telephone company’s equipment to the end user’s premise. The local loop can be made up of fiber, copper or wireless media. It usually refers to the wired connection from a telephone company’s central office in a local area to its customer’s premises.

Local Loop Unbundling (LLU).The process of making the local loop available to the local loop owner’s competitors.

LRIC. A cost accounting methodology focusing on long-run incremental costs.

Managed Leased Line. A leased line monitored, managed and controlled by a network management system offering an increased level of flexibility, reliability and security.

Metropolitan Area Network (MAN).A network that covers a metropolitan area such as a portion of a city. The area is larger than that covered by a local area network but smaller than the area covered by a wide area network.

Mobile. Generally refers to wireless or cellular telecommunications with limited geographical constraints.

Multiplexing.The combination of multiple analog or digital signals for transmission over a single line.

Multiprotocol Label Switching (MPLS). A widely supported method of speeding up data communications over combined IP/ATM networks.

Network. An arrangement of data devices that can communicate with each other such as the telephone network over which telephones and modems communicate with each other.

number portability. The ability of a customer to transfer from one telecom operator to another and retain the original telephone number.

Point of Presence (POP).The physical location where the line from a long distance carrier or the server of an Internet Service Provider connects to the line of the local telecommunications service provider (usually at the local telephone company’s central office).

Point to Multipoint (PMP).Refers to the use of microwave technology to link the telecommunications service provider’s point-of-presence with a number of remote customer locations.

-7-

Point to Point (PP).Refers to the use of microwave technology to link the telecommunications service provider’s point-of-presence directly with one single customer location.

Public Switched Telephone Network (PSTN). A traditional landline network for voice telephony.

SME. Refers to small and medium-sized enterprises.

SoHo. Refers to small office/home office.

Synchronous Digital Hierarchy (SDH).The international standard for synchronous data transmission over fiber optic cables. The North American equivalent of SDH is SONET.

Transit Services.An interconnection service whereby a carrier provides transportation services for information (voice, data and video) by linking two networks that are not directly interconnected.

Tier 1 Provider. A Tier 1 provider is a network operator of an IP network which connects to the entire Internet solely via Settlement Free Interconnection, commonly known as “peering”. Tier 1 providers have service level agreements which include 99.9% uptime guarantees, impressive security, continuous and clean power and protection from fire, earthquakes and other disasters.

Unbundling.The granting of unbundled access to the local loop so that the third party operators requesting access to the local loop are not required to purchase interconnection services from the incumbent operator; also referred to as “local loop unbundling”.

Universal Mobile Telecommunications System (UMTS).A third generation (3G) wireless system designed to provide a wide range of voice, high speed data and multimedia services.

Virtual Local Area Network (VLAN). A network architecture which allows geographically distributed users to communicate as if they were on a single physical local area network.

Virtual Private Network (VPN).A private network that operates securely within a public network (such as the Internet) by means of encrypting transmissions. It provides the functions and features of a private network without the need for dedicated private lines between different end-user organization’s sites. Each end-user organization’s site connects to the network provider’s network rather than directly to the end-user’s other sites.

Voice over Internet Protocol (VoIP). The transmission of voice using Internet-based technology over a broadband connection rather than a traditional wire and switch-based telephone network.

Wholesale naked DSL. The provision of DSL services on a stand-alone basis without fixed line voice services.

Wide Area Network (WAN). A geographically dispersed network that is housed in more than one location. Its area is larger than that covered by a metropolitan area network.

Wireless Local Loop.A wireless connection between the customer’s premises and the telephone company’s central office.

Worldwide Interoperability for Microwave Access (WiMAX).A telecommunications technology that provides for the wireless transmission of data using a variety of transmission modes.

In addition, we have included a list of certain other defined terms used in this Report under the heading“Certain Definitions and Presentation of General Information”.

-8-

EXCHANGE RATE INFORMATION

In this Report certain amounts stated in euros or forint have also been stated in U.S. dollars solely for the informational purposes of the reader, and should not be construed as a representation that such euro or forint amounts actually represent such U.S. dollar amounts or could be, or could have been, converted into U.S. dollars at the rate indicated or at any other rate. Unless otherwise stated or the context otherwise requires, such amounts have been stated at December 31, 2008 exchange rates.

Forint per Euro

The following table sets out, for the periods and dates indicated, the period-end, average, high and low official rates set by the National Bank of Hungary for forint per EUR 1.00. We make no representation that the forint amounts referred to in this Report could have been or could be converted into any currency at any particular rate or at all. As of May 8, 2009, the rate was 278.71.

| | | | | | | | |

| | | Forint/Euro Exchange Rates |

| | | Period-End | | Average | | High | | Low |

| | | (amounts in HUF/EUR 1.00) |

Year | | | | | | | | |

2004 | | 245.93 | | 251.68 | | 270.00 | | 243.42 |

2005 | | 252.73 | | 248.05 | | 255.93 | | 241.42 |

2006 | | 252.30 | | 264.27 | | 282.69 | | 249.55 |

2007 | | 253.35 | | 251.31 | | 261.17 | | 244.96 |

2008 | | 264.78 | | 251.25 | | 275.79 | | 229.11 |

Forint per U.S. Dollar

The following table sets out, for the periods and dates indicated, the period-end, average, high and low official rates set by the National Bank of Hungary for forint per $1.00. We make no representation that the forint amounts referred to in this Report could have been or could be converted into any currency at any particular rate or at all. As of May 8, 2009, the rate was 207.73.

| | | | | | | | |

| | | Forint/$ Exchange Rates |

| | | Period-End | | Average | | High | | Low |

| | | (amounts in HUF/$1.00) |

Year | | | | | | | | |

2004 | | 180.29 | | 202.63 | | 217.24 | | 180.19 |

2005 | | 213.58 | | 199.66 | | 217.54 | | 180.58 |

2006 | | 191.62 | | 210.51 | | 225.01 | | 191.02 |

2007 | | 172.61 | | 183.83 | | 199.52 | | 171.13 |

2008 | | 187.91 | | 171.80 | | 218.76 | | 144.11 |

-9-

U.S. Dollar per Euro

The following table sets out, for the periods and dates indicated, the period-end, average, high and low official rates set by the National Bank of Hungary for U.S. dollar per EUR 1.00. We make no representation that the euro amounts referred to in this Report could have been or could be converted into any currency at any particular rate or at all. As of May 8, 2009, the rate was 1.34.

| | | | | | | | |

| | | $/Euro Exchange Rates |

| | | Period-End | | Average | | High | | Low |

| | | (amounts in HUF/$1.00) |

Year | | | | | | | | |

2004 | | 1.36 | | 1.24 | | 1.36 | | 1.18 |

2005 | | 1.18 | | 1.24 | | 1.35 | | 1.17 |

2006 | | 1.32 | | 1.26 | | 1.33 | | 1.18 |

2007 | | 1.47 | | 1.37 | | 1.49 | | 1.29 |

2008 | | 1.41 | | 1.46 | | 1.60 | | 1.24 |

-10-

CAUTIONARY STATEMENTS CONCERNING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 20-F contains forward-looking statements. Statements that are not historical facts are forward-looking statements made pursuant to the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995. These statements are based on our estimates and assumptions and are subject to risks and uncertainties, which could cause actual results to differ materially from those expressed or implied in the statements. Words such as “believes”, “anticipates”, “estimates”, “expects”, “intends” and similar expressions are intended to identify forward-looking statements. Forward-looking statements (including oral representations) are only predictions or statements of current plans, which we review continuously. For all forward-looking statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

The following important factors, along with those factors discussed elsewhere in this Annual Report on Form 20-F and in our other reports filed with the Securities and Exchange Commission, could affect future results and could cause those results to differ materially from those expressed in the forward-looking statements:

| | • | | Our inability to execute our business strategy; |

| | • | | Costs or difficulties related to the Reorganization and related transactions, which could be greater than expected; |

| | • | | The continuing effects of the global economic crisis and in particular the effects of the recent macroeconomic issues affecting the Hungarian economy; |

| | • | | Changes in the growth rate of the overall Hungarian, E.U. and Central and South Eastern European economies such that inflation, interest rates, currency exchange rates, business investment and consumer spending are impacted; |

| | • | | Our ability to effectively manage and otherwise monitor our operations, costs, regulatory compliance and service quality; |

| | • | | Changes in consumer preferences for different telecommunication technologies, including trends toward mobile and cable substitution; |

| | • | | Our ability to generate growth or profitable growth; |

| | • | | Material changes in available technology and the effects of such changes including product substitutions and deployment costs; |

| | • | | Our ability to retain key employees; |

| | • | | Political changes in Hungary; |

| | • | | Changes in our accounting assumptions that regulatory agencies, including the SEC, may require or that result from changes in the accounting rules or their application, which could result in an impact on our financial results; |

| | • | | Our ability to successfully complete the integration of any businesses or companies that we may acquire into our operations; and |

| | • | | The factors referred to in the “Risk Factors” section of this Report. |

-11-

You should consider these important factors in evaluating any forward-looking statements in this Annual Report on Form 20-F or otherwise made by us or on our behalf. We urge you to read the entire Report for a more complete discussion of the factors that could affect our future performance, the Hungarian and Central and South Eastern European telecommunications industry and Hungary in general. In light of these risks, uncertainties and assumptions, the events described or suggested by the forward-looking statements in this Report may not occur.

Except as required by law or applicable stock exchange rules or regulations, we undertake no obligation to update or revise publicly any forward-looking statement, whether as a result of new information, future events or otherwise. All subsequent written and oral forward-looking statements attributable to us or to persons acting on our behalf are expressly qualified in their entirety by the cautionary statements referred to above and contained elsewhere in this Report.

-12-

PART I

Item 1. Business.

Company Overview

Hungarian Telephone and Cable Corp. was incorporated in Delaware in 1992 as a holding company to acquire concessions from the government of the Republic of Hungary to own and operate local fixed line telecommunications networks in Hungary as Hungary privatized its telecommunications industry.

We are the second largest fixed line telecommunications services provider in Hungary and the incumbent provider of fixed line telecommunications services to residential and business customers in our 14 historical concession areas, where we have a dominant market share. We are also the number one alternative fixed line operator outside our historical concession areas in Hungary, and we are the number one independent wholesale provider of data and capacity services in Central and South Eastern Europe.

We provide telecommunications services in Hungary and in the region through our Hungarian and other operating subsidiaries under our common brand: Invitel. We also provide Internet and data services to business customers in Romania through our Romanian subsidiary, Euroweb Romania.

Our historical concession areas are geographically clustered and cover an estimated 2.1 million people, representing approximately 21% of Hungary’s population. Outside our historical concession areas, we believe that we are well positioned to continue to grow our revenue and market share using our fully owned state-of-the-art backbone network, our experienced sales force and our comprehensive portfolio of services. Our extensive fiber optic backbone network (comprising approximately 8,500 route kilometers in Hungary) provides us with nationwide and international reach. It allows business and wholesale customers in particular, to be connected directly to our network to access voice, data and Internet services.

Outside Hungary, we are the leading independent provider of wholesale data and capacity services throughout Central and South Eastern Europe. Our regional fiber optic backbone network comprises 23,000 route kilometers of fiber with 40 major points of presence in 19 countries. Our clients include the incumbent telecommunications services providers in these countries as well as alternative fixed line telecommunications services providers, mobile operators, cable television operators and Internet Service Providers. We also provide services to telecommunication services providers from Western Europe and the United States, enabling them to meet the regional demands of their corporate clients.

We operate in the following four market segments:

| | • | | Mass Market Voice.We provide a full range of basic and value-added voice-related services to our residential and small office and home office (“SoHo”) customers both inside and outside our historical concession areas. These services include local, national and international calling, voicemail, fax, Integrated Services Digital Network (“ISDN”) and directory assistance services. |

| | • | | Mass Market Internet.We provide Digital Subscriber Line (“DSL”) broadband and dial-up Internet services to our Mass Market customers nationwide. Since June 2008, we have also provided IPTV (TV delivered over DSL broadband connections) services to customers in most of our historical concession areas, and introduced these services in our remaining historical concession areas in February. |

-13-

| | • | | Business.We provide fixed line voice, data, Internet and server hosting services to business (comprised of small and medium-sized enterprises (“SMEs”) and larger corporations), government and other institutional customers nationwide. |

| | • | | Wholesale.We provide voice, data and network capacity services on a wholesale basis to a number of other telecommunications and Internet Service Providers both within Hungary and across the Central and South Eastern Europe region. |

We have a diversified revenue and cash flow base, reducing our susceptibility to market pressures in any particular market segment. For the year ended December 31, 2008, we derived approximately 28% of our revenue from Mass Market Voice, 10% from Mass Market Internet, 27% from Business and 35% from Wholesale. See Note 17 “Segments” in the Notes to Consolidated Financial Statements for information on revenue by segment, gross margin by segment and net book value of assets by country. The assets outside of Hungary are mainly attributable to the Wholesale segment.

As of December 31, 2008, we had approximately 382,000 telephone lines connected to our network within our historical concession areas to service Mass Market Voice customers and we had approximately 440,000 active Mass Market Voice customers outside our historical concession areas connected primarily through Carrier Pre-Selection (“CPS”) and Carrier Selection (“CS”) (with a small amount connected through Local Loop Unbundling, “LLU”). This is compared to December 31, 2007 when we had approximately 405,000 telephone lines in service within our historical concession areas to service Mass Market Voice customers and approximately 664,000 active Mass Market Voice customers connected through indirect access outside our historical concession areas. The decrease in the number of active Mass Market Voice customers outside our historical concession areas from 664,000 as of December 31, 2007 to 440,000 as of December 31, 2008 is due to churn of low value CS and CPS customers.

As of December 31, 2008, we had approximately 139,000 Mass Market broadband DSL customers, of which approximately 112,000 were connected directly to our networks within our historical concession areas and 27,000 were outside our historical concession areas and serviced principally by our purchasing wholesale DSL services from the incumbent local telephone operator, primarily T-Com. T-Com is the brand name under which Magyar Telekom Plc. operates its fixed line telecommunications business in Hungary. This compares to December 31, 2007 when we had 122,000 broadband DSL customers. The number of IPTV customers increased to 4,005 as of December 31, 2008 since June 2008, when we introduced this service.

As of December 31, 2008, we had approximately 48,000 voice telephone lines connecting business customers within our historical concession areas, compared to approximately 47,000 lines at 2007 year end. Outside our historical concession areas, we had approximately 58,000 direct access voice telephone lines and approximately 12,000 indirect access voice telephone lines as of December 31, 2008, compared to approximately 58,000 direct access voice telephone lines and approximately 13,000 indirect access voice telephone lines as of December 31, 2007. As of December 31, 2008, we had approximately 17,000 DSL lines and approximately 15,000 leased lines compared to approximately 16,000 DSL lines and approximately 13,000 leased lines as of December 31, 2007.

In the Wholesale market, we had approximately 600 customers as of December 31, 2008, which customers include telecommunication services providers from Western Europe and the United States, incumbent telecommunications services providers, alternative fixed line telecommunications services providers, mobile operators, cable television operators and Internet Service Providers. As of December 31, 2007, we had approximately 300 customers.

Our current business is a result of the recent combination of Invitel, Memorex and the Hungarian business of Tele2 with our existing business. On April 27, 2007, we acquired Invitel for a total

-14-

consideration, including the assumption of net indebtedness on closing, of EUR 470 million (approximately $639 million at closing). Invitel was the second largest fixed line telecommunications services provider in Hungary and the incumbent provider of fixed line telecommunications services in nine historical concession areas while we were the third largest fixed line telecommunications services provider in Hungary and the incumbent provider of fixed line telecommunications services in five historical concession areas. We are now better able to compete against T-Com, the former national monopoly, which is the largest fixed line telecommunications services provider in Hungary. We have realized approximately EUR 17 million (approximately $22.6 million at current exchange rates) in annualized operating expense synergies as a result of the Invitel Acquisition at the end of 2008. This exceeds our original estimate of EUR 14 million (approximately $18.6 million at current exchange rates) that we estimated when we announced that we had agreed to purchase Invitel in January 2007.

We were providing and marketing services in Hungary through our Hungarian subsidiaries Hungarotel, PanTel and PanTel Technocom and internationally through PanTel, while Invitel was providing and marketing services in Hungary through Invitel and Euroweb Hungary and internationally through Invitel. Invitel was also providing and marketing Internet and data services to business customers in Romania through its Romanian subsidiary, Euroweb Romania. Following the Invitel Acquisition, we decided to market all of our products and services under a single unified brand name – Invitel (except in Romania, where we maintain the Euroweb brand).

On October 18, 2007, we purchased the Hungarian business of Tele2, the Swedish-based alternative telecom operator, by purchasing the entire equity interest in Tele2’s Hungarian subsidiary (“Tele2 Hungary”) for EUR 4 million in cash (approximately $5.6 million at closing). Tele2 Hungary (renamed Invitel Telecom Kft.) provided Carrier Selection and Carrier Pre-Selection fixed line telecommunications services to the Mass Market as a reseller using the network facilities of other operators pursuant to regulated resale agreements.

On March 5, 2008, we acquired 95.7% of the outstanding equity in Austrian-based Memorex Telex Communications AG (the “Memorex Acquisition”). The total purchase consideration for Memorex (subsequently re-named Invitel International AG) was EUR 103.6 million (approximately $157.3 million at closing) including the assumption of debt and transaction costs and other directly related expenses. On August 28, 2008 we also acquired the remaining 4.3% of Memorex from the minority shareholders in Memorex, which gave us 100% ownership of the equity in Memorex. The final purchase price for the Memorex minority interest was EUR 1.9 million (approximately $2.9 million at closing). Memorex was one of the leading alternative telecommunications providers in the Central and South Eastern European region. Memorex provided wholesale data and capacity services to leading global telecommunications providers and Internet companies between a number of countries in the region including Austria, Bulgaria, the Czech Republic, Italy, Romania, Slovakia, Turkey, and Ukraine. Memorex operated over 12,500 route kilometers of fiber optic cable in the region which enabled it to provide high quality wholesale services to large international carriers. Memorex invested approximately EUR 54 million (approximately $71.8 million at current exchange rates) in its network over the two years prior to the acquisition. Following the completion of the Memorex Acquisition, we are the leading independent provider of wholesale capacity and data services in Central and South Eastern Europe.

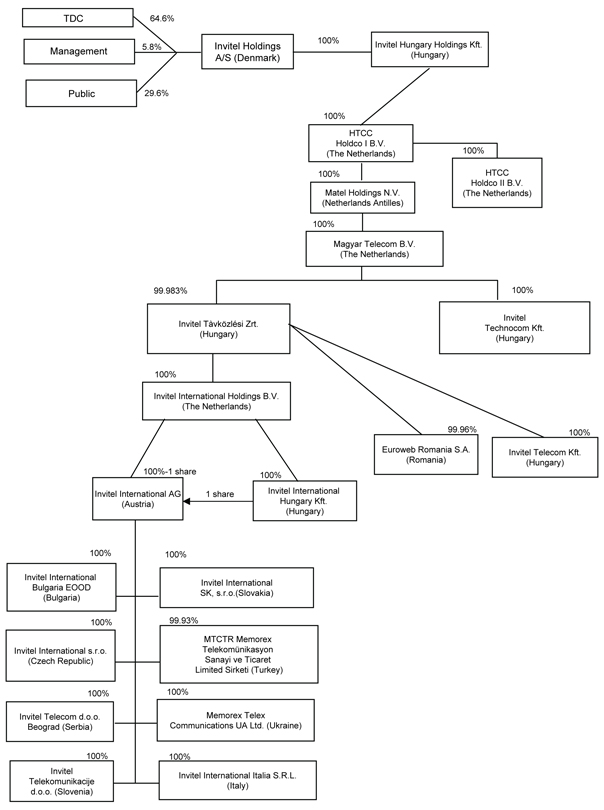

We have substantially completed an internal reorganization of our operating subsidiaries to better reflect our business segments and to realize some operational efficiencies. As our result, we have consolidated and renamed some subsidiaries. An updated organizational chart of our subsidiaries is included within this Report.

We had $555 million in total revenue in 2008, up from $385 million in 2007.

Our goal is to provide customers with good value telecommunications services coupled with exceptional service and to be a cost efficient telecommunications service provider. Our primary risk is

-15-

our ability to retain existing customers and attract new customers in a competitive market. Our success depends upon our operating and marketing strategies, as well as market acceptance of our telecommunications services within Hungary and the region.

We will continue to explore other strategic merger, acquisition or alliance opportunities. In addition, we will also continuously review our service portfolio to identify service opportunities that can enhance our competitive position.

Our principal office in Hungary is located at Puskas Tivadar u. 8-10, H-2040 Budaörs; telephone +36 (1) 801-1500. Our United States telephone number is +1 (206) 654-0204. Our web site address is http://www.invitel.hu and it contains a link to our filings with the SEC.

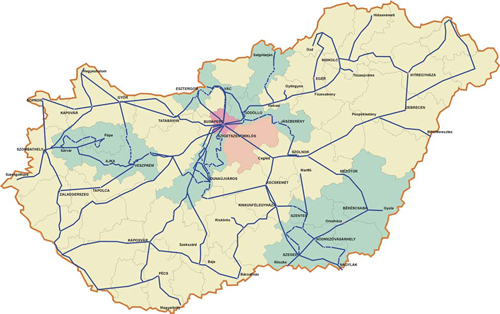

On the following pages, you will find: (i) a map showing Hungary’s location within Europe; (ii) a diagram showing our historical concessions areas in Hungary, along with our Hungarian telecommunications backbone network; (iii) a diagram showing our international wholesale network; and (iv) a diagram showing our current corporate structure.

-16-

Hungary and Surrounding Countries

-17-

Hungarian Telecommunications Backbone Network

and Historical Concession Areas

historical concessions areas

-18-

International Wholesale Network

-19-

Organizational Structure

(as of May 2009)

-20-

Company History

We acquired the right to operate fixed line telecommunications networks in five historical concession areas from the Hungarian government and purchased the existing telecommunications infrastructure, including 61,400 telephone lines, from T-Com in 1995 and 1996. The acquired telecommunications infrastructure was somewhat antiquated (manual exchanges and analog lines). We overhauled the existing infrastructure with a major capital expenditures program. The results of this investment are expanded and modern telecommunications networks in these five historical concession areas deploying Siemens and Ericsson technology. We were able to provide connections to our customers who had waited years (in some cases, for over 20 years) for telephone service and offer modern telecommunications services beyond traditional voice services to all of our customers. We now own and operate all public telephone exchanges and local loop telecommunications network facilities in these five historical concession areas and were, until the expiration of our exclusivity rights in 2002, the sole provider of non-cellular local voice telephone services in such areas. Until recently, we operated and marketed this business through our Hungarian subsidiary Hungarotel, which was merged into Invitel as of January 1, 2008. The five Hungarotel historical concession areas cover a population of approximately 668,000 with approximately 280,000 residences.

The PanTel Acquisition

We purchased an initial 25% interest in PanTel in November 2004 and acquired the remaining 75% from Royal KPN NV, the Dutch telecommunications provider (“KPN”), on February 28, 2005. PanTel was Hungary’s leading alternative telecommunications provider with a nationwide fiber optic backbone telecommunications network linking every county in Hungary. PanTel provided voice, data and Internet services to businesses throughout Hungary in competition with other telecommunications services providers including T-Com. PanTel’s subsidiary, PanTel Technocom, provided telecommunications services to MOL (the Hungarian oil company) and operated and maintained various parts of MOL’s telecommunications network.

PanTel also used its network capacity to transport voice, data and Internet traffic on a wholesale basis for other telecommunications services providers and Internet Service Providers in Hungary. PanTel’s network also crossed Hungary’s borders and, using a combination of owned and leased capacity, extended PanTel’s wholesale services into other countries of the Central and South Eastern European region. As of January 1, 2008, we merged PanTel into Invitel and changed PanTel Technocom’s name to Invitel Technocom.

PanTel was founded in 1998 by KPN, MÀV Rt. (“MAV,” the Hungarian state railroad company) and KFKI Investment Ltd. (a Hungarian entity) to compete with T-Com, the former State-controlled telecommunications company which had a government-protected monopoly in the Hungarian domestic and international long distance fixed line voice telecommunications market. Following a tender process, the Hungarian government awarded PanTel licenses to provide data transmission and other services that were not subject to T-Com’s government-protected monopoly rights for long distance voice services. In 1999, PanTel began building, along MAV’s railroad rights-of-way, what became a 3,700 kilometer long state-of-the-art fiber optic backbone telecommunications network. PanTel also built metropolitan area networks, including a metropolitan area network covering Budapest, which connected to PanTel’s backbone network. PanTel also acquired a license for the 3.5 GHz wireless frequency block.

Until 2002, PanTel was only allowed to offer data and Voice over IP (“VoIP”) services in Hungary. When the Hungarian government ended T-Com’s monopoly rights for long distance voice services, PanTel was able to compete with T-Com and offer all modern telecommunications services including traditional voice services.

-21-

The Invitel Acquisition

In 2007 we combined our operations with Invitel following the acquisition of Invitel Távközlesi Zrt. (“Invitel”), a Hungarian company, on April 27, 2007, by way of the acquisition of the shares of Invitel’s parent company, Matel Holdings N.V.

Invitel began its operations in Hungary in 1994. Invitel initially owned and operated two Hungarian telecommunication companies which had the right to operate in four historical concession areas in Csongrad and Pest counties. In 1996 and 1997, Invitel developed its network infrastructure within those areas and in 1998 established a joint venture for the provision of data services in and out of its historical concession areas, especially in Budapest. In 1999, Invitel acquired Jásztel ZRt., a regional telephone operating company operating in the Jászberény historical concession area (east of Budapest). In the same year, Invitel also acquired Corvin Telecom Távközlesi Zrt., a Hungarian company, which was an optical network operator specializing in data transmission which allowed Invitel to further the development of its Budapest joint venture. In 2000, Invitel acquired four additional historical concession areas (Dunaújváros, Esztergom, Veszprém and Szigetszentmiklós) through the acquisition of United Telecom International B.V. from Alcatel of France.

In 2000 and 2001, Invitel developed its national telecommunications backbone network to connect major centers outside the Invitel historical concession areas. Invitel also developed metropolitan area networks, particularly in Budapest. In 2001, Invitel was granted one of five national 3.5 GHz licenses over which it deployed a point-to-multipoint microwave network. In the same year, Invitel also began its Internet access activity nationwide.

Utilizing its Hungarian national backbone and its metropolitan networks, Invitel provided wholesale domestic and international voice and data transit services to Hungarian and international telecommunications services providers. Invitel was among the first telecom operators to provide services in and out of Serbia, both in terms of data capacity and voice traffic. Invitel also generated significant revenue leasing its fiber backbone towards Romania.

On May 23, 2006, Invitel acquired Euroweb International Corporation’s two Internet and telecom related operating subsidiaries, Euroweb Hungary and Euroweb Romania. Euroweb provided Internet access and additional value-added services including international/national leased line and voice services primarily to Business customers.

The Tele2 Hungary Acquisition

On October 18, 2007 we purchased the Hungarian business of Tele2, the Swedish-based alternative telecom operator, by purchasing the entire equity interests in Tele2’s Hungarian subsidiary for EUR 4 million in cash (approximately $5.6 million at closing). Tele2 Hungary provided Carrier Selection and Carrier Pre-Selection fixed line telecommunications services to the Mass Market as a reseller using the network facilities of other operators pursuant to regulated resale agreements. At closing Tele2 Hungary (since renamed Invitel Telecom Kft.) had approximately 460,000 active Mass Market customers.

The Memorex Acquisition

On March 5, 2008 we acquired 95.7% of the outstanding equity in Austrian-based Memorex Telex Communications AG (“Memorex”). On August 28, 2008 we also acquired the remaining 4.3% stake of Memorex from the minority shareholders in Memorex, which gave us 100% ownership of the equity in Memorex. The final purchase price for the Memorex minority interest was EUR 1.9 million (approximately $2.9 million at closing). Memorex (now re-named Invitel International AG) was one of the leading alternative telecommunications providers in the Central and South Eastern European region. Memorex provided wholesale data and capacity services to leading global telecommunications providers

-22-

and Internet companies between 14 countries in the region including Austria, Bulgaria, the Czech Republic, Italy, Romania, Slovakia, Turkey, and Ukraine. Memorex operated over 12,500 route kilometers of fiber optic cable in the region which enabled it to provide high quality wholesale services to large international carriers.

Strategy

Invitel Holdings intends to continue the strategy pursued by HTCC, which is based on the following objectives:

Maximizing voice revenue and cash flow in our historical concession areas.

We intend to maximize the revenue and cash flow derived from the provision of voice services within our historical concession areas through the continued migration of customers from traffic-based to subscription-based packages with higher monthly fees and lower usage charges, the ongoing introduction of targeted, innovative and flexible service offerings and by continuously improving our customer service. In addition, we have focused on, and will continue focusing on, formulating effective strategies to retain customers and defend against churn in our historical concession areas resulting from competition from operators using Carrier Selection and Carrier Pre-Selection, as well as from cable television operators. Examples of these strategies include:

| | • | | Pricing our service offerings to limit the incentive to switch to a competitor; |

| | • | | Offering new commercial packages with a higher monthly fee but with local and off-peak calls included in the base subscription or with low call charges in all directions or various combinations of bundled minutes; |

| | • | | Launching win-back activities aimed at Carrier Pre-Selection, Carrier Selection and cable users with new promotional offers; |

| | • | | Establishing and developing loyalty programs, which will offer exclusive benefits to our customers; |

| | • | | Offering attractive bundled packages (voice and Internet and IPTV) to counter bundled service offerings by cable television operators; and |

| | • | | Conducting programs to proactively migrate existing customers to more attractive packages via our telesales channels in combination with targeted promotional campaigns. |

Capitalizing on growth opportunities for Mass Market DSL services, both in and outside our historical concession areas.

We believe that there is potential for continued growth of DSL services in Hungary due to market growth and the expected eventual convergence of personal computer and Internet penetration with Western European levels. Furthermore, DSL continues to maintain a higher market share than cable for broadband Internet access in Hungary. Broadband Internet usage has grown significantly in Hungary with penetration estimated to have increased from 0.7% of the households in Hungary as of December 31, 2002 to an estimated 42% as of December 31, 2008. In comparison, broadband Internet penetration in EU-15 countries was estimated at approximately 50% of households as of December 31, 2008.

We intend to continue to capitalize on the above trend by continuing to grow our DSL customer base both inside and outside our historical concession areas. We grew our DSL business faster than the total DSL market in 2007 and 2008. The growth in our DSL customer base is a key business priority as we believe it will increase line retention and stimulate fixed line revenue growth. For example, we have acquired the majority of our new fixed line contracts through bundled voice/DSL offerings. We intend to continue to grow our DSL business principally through the following initiatives:

| | • | | The recent introduction of IPTV to enable us to offer triple play (telephone, broadband Internet and TV) and dual play packages (broadband Internet and TV or telephone and TV) initially in our historical concession areas; |

-23-

| | • | | The use of unbundled local loops in T-Com’s area to offer increasingly attractive and profitable higher speed Internet and bundled voice/Internet services; |

| | • | | The use of WiMAX technology (and our existing 3.5Ghz licences) to provide broadband access in those “in historical concession” areas where there is no copper network today; |

| | • | | Maintaining a broad mix of distribution channels such as our own and outsourced telesales, owned shops, third party channels and points of sale, and agent networks; |

| | • | | Quarterly promotions supported by targeted television, radio and billboard advertising campaigns; and |

| | • | | Developing innovative bundled packages with progressively increased broadband access speeds. |

Expanding our Business revenue and market share nationwide.

We will continue to focus on expanding our business customer base and growing our share of the national business to business (“B2B”) market. We intend to capitalize on our extensive national backbone network, which means that in many cases business customers can be connected directly to our network, resulting in higher margins and more competitive pricing through lower access costs. Up until now, business customers have been connected directly to our backbone network mainly through the use of metropolitan fiber, line-of-site microwave, or leased circuits. Increasingly, in the future, we plan to add new customers through local loop unbundling, or the use of WiMAX technology. Lower value/volume business customers outside our historical concession areas are served through indirect methods such as Carrier Pre-Selection voice, and by buying DSL wholesale capacity from the incumbent. We plan to grow our revenue and increase our share in the business market through the following actions:

| | • | | Focusing principally on new customer acquisitions in the small and medium enterprises market through attractively priced, easily understood, voice, data, Internet and value added services, sold through an efficient direct sales organization and complemented by high quality customer care; |

| | • | | Capitalizing on our traditional strength in the high-end corporate market and utilizing our extensive infrastructure, to selectively pursue a number of larger new corporate business customers; |

| | • | | Retaining existing customers through effective account management, attractive renewal packages and continued customer care enhancement, such as the recent introduction of our Top 100 program; |

| | • | | Taking advantage of more extensive local loop unbundling and WiMAX opportunities to enhance service offerings and reduce access costs outside our historical concession areas; |

| | • | | Cross selling new services to existing customers; and |

| | • | | The continued development of our service portfolio and the introduction of a broader range of value added services such as server hosting and server virtualization services. |

-24-

Continuing to leverage our modern national and regional backbone networks and our position as the number one independent data and capacity services carrier in the Central and South Eastern European region to continue to grow our revenue in the Wholesale market.

We intend to continue to leverage our modern backbone telecommunications network in the wholesale market in Hungary, selling capacity on our network to other service providers for the national and international transmission of their voice, data and Internet traffic. We believe that our ability to offer bandwidth capacity at competitive prices provides us with a competitive edge in the Wholesale market.

After the successful acquisition of Memorex, we have become the leading independent, infrastructure-based wholesale provider of data and capacity services in Central and South-Eastern Europe. We have an extensive regional network with 40 major points of presence in 19 countries in Central and South Eastern Europe via a fiber network of 23,000 route kilometers. The regional market is expected to continue to grow, being driven by growth in Internet traffic, general economic development and increasing mobile penetration. We believe that we are ideally positioned to take advantage of this growth, based on our leadership position and being strategically located between Central and South Eastern Europe and Western Europe.

Continuing to identify and evaluate further opportunities for consolidation.

We believe that we are well positioned to participate in any further consolidation of the Hungarian telecommunications sector as a result of our market position as the number one alternative fixed line operator in Hungary, our significant understanding of the competitive environment in Hungary, both as an incumbent and as an alternative operator, and our solid track record of improving efficiency, achieving operating cost savings and realizing synergies from bolt-on acquisitions.

Hungary

Hungary is located in Central Europe bordering on Austria, Slovenia, Croatia, Serbia, Romania, Ukraine and Slovakia. It has approximately 10 million inhabitants, approximately 1.8 million of whom reside in Hungary’s capital, Budapest.

For nearly 40 years, Hungary had a one-party government and a centrally planned economy. Democracy was restored and the foundations of a market economy were built between 1988 and 1990. Free elections were held in 1990. Today, Hungary has a parliamentary democracy with a single-chamber National Assembly. As a result of a large scale privatization effort, private enterprise has become the basis of the Hungarian economy.

Since 1990, foreign direct investment into Hungary has been approximately EUR 69 billion. Hungary, Poland and the Czech Republic are the recipients of more than 50% of the total foreign direct investment into the former communist countries in the region. Since 1995, the Hungarian government has embarked on an economic stabilization effort aimed at putting the economy on a sustainable path of low-inflation growth. The unemployment rate has decreased from 10.3% in 1995 to 8.0% at December 31, 2008.

On May 1, 2004, Hungary joined the E.U., together with nine other countries. Hungary plans to adopt the euro as its currency between 2011 and 2014, although no official deadline has been declared by the government. Hungary joined the North Atlantic Treaty Organization in 1999. Hungary is also a member of the Organization for Economic Co-operation and Development and the World Trade Organization.

In addition to a significant budget deficit, in recent years the Hungarian economy has been marked by a large current account deficit, rapid credit growth and a reliance by Hungarian businesses and consumers on foreign currency loans. These factors have left Hungary especially vulnerable to a financial crisis.

-25-

On October 22, 2008, the National Bank of Hungary raised its base interest rate from 8.5% to 11.5% in an effort to support the forint foreign exchange rate. At the end of that month, the Hungarian government adopted a set of policies agreed upon with the E.U., the European Central Bank and the International Monetary Fund to bolster the Hungarian economy’s near-term stability and improve its long-term growth potential by ensuring fiscal sustainability and strengthening the financial sector. In addition, the International Monetary Fund extended Hungary significant financial assistance. The National Bank of Hungary has gradually lowered its base rate to the current 9.5%. See Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations-Macroeconomic Factors.”

The following table sets out Hungary’s annual GDP growth and inflation rates since 2003.

| | | | |

| | | Annual GDP Growth Rate | | Annual Inflation Rate |

| | | (%) | | (%) |

2003 | | 3.4 | | 4.7 |

2004 | | 5.2 | | 6.8 |

2005 | | 4.1 | | 3.6 |

2006 | | 3.9 | | 3.9 |

2007 | | 1.0 | | 8.5 |

2008 | | 0.5 | | 6.1 |

Hungarian Telecommunications Industry

In 1989, the Hungarian state owned Post, Telegraph and Telephone was divided into three separate companies: the Hungarian Broadcasting Company, the Hungarian Post Office and Magyar Távközlési Vállalat (the former Hungarian Telecommunications Operator which was privatized in 1992 and is now Magyar Telekom Plc. and operates its fixed line telecommunications business in Hungary under the T-Com brand name, “T-Com”).

As a result of Act LXXII of 1992 on Telecommunications (the “1992 Telecommunications Act”), the Hungarian government divided Hungary in 1993 into 54 geographically defined concession areas for local public fixed line voice telephony services (each, a “historical concession area”). Although the geographic concession areas set forth by the 1992 Telecommunications Act were repealed by the 2001 Communications Act, the currently operating telecommunications services providers are still the primary operators in those geographic areas of Hungary, which previously constituted their historical concession areas as defined by the 1992 Telecommunications Act.

In August 1993, the Ministry of Transport, Telecommunications and Water Management (the “Ministry”) announced an international tender for the right to provide international and domestic long distance telephony services throughout Hungary and to provide local public fixed line voice telephony services in 29 out of the 54 historical concession areas, including Budapest. The Ministry selected T-Com as the winner of this tender.

In September 1993, the Ministry announced a second competitive bid for the exclusive right to provide local public fixed line voice telephony services in the remaining 25 of the 54 historical concession areas. The Ministry awarded 23 out of the 25 concession areas offered in the second tender. The rights to operate 15 of those historical concession areas were distributed among 12 local telephone operators (each a Local Telephone Operator or “LTO”). T-Com, either directly or through predecessor companies, was awarded eight historical concession areas and was additionally chosen as the default provider in the two concession areas where there was no successful bidder. Each of the LTOs (including

-26-

the company and its predecessors) received 25-year licenses to provide local basic telephony services with exclusive rights in their respective historical concession areas until 2002. Each of the LTOs, other than T-Com, negotiated a separate asset purchase agreement with T-Com to acquire each historical concession area’s existing telephony plant and equipment.

The liberalization of the fixed line telecommunications market in Hungary could only be launched following the expiration of T-Com’s exclusive right to provide international and domestic long distance telephony services in December 2001 and the expiration of each LTO’s exclusive concession rights in their respective historical concession areas in 2002. In connection with Hungary’s accession into the E.U., in order to transpose the E.U. regulatory framework into the Hungarian legal system, the 2004 Communications Act was adopted and restructured the regulatory authorities responsible for the supervision of the liberalized telecommunications market, with the primary supervisory authority being the National Communications Authority. See “-Hungarian Regulatory Environment.”

Hungarian Fixed Line Telecommunications Industry Today

We are the second largest incumbent fixed line telecommunications operator with 14 of the above mentioned historical concession areas. In addition to us, the two other incumbent fixed line telecommunications services providers operating in Hungary today are T-Com and UPC Hungary:

| | • | | T-Com: T-Com is the largest provider of fixed line telecommunications services in Hungary. T-Com is the successor company of the former monopoly provider of long distance and international telephony services in Hungary, and the provider of local telephony services in 39 historical concession areas. T-Com has an estimated 56% national residential fixed voice and Internet market share and an estimated 61% national business market share. T-Com is listed on both the Budapest Stock Exchange and the New York Stock Exchange (its parent company is Deutsche Telekom AG, which owns 59.2% of T-Com). |

| | • | | UPC Hungary: UPC Hungary is a wholly-owned subsidiary of Liberty Group, Inc., a global cable operator that operates within 15 countries, principally in Europe. UPC Hungary provides local telephony services in one historical concession area and through its cable network covers approximately 1.2 million homes where it provides Internet and fixed voice services in addition to cable television. UPC Hungary has an estimated 14% national residential fixed voice and Internet market share. |

The Hungarian Telecommunications Markets

Fixed Line Voice

The fixed line telecommunications market in Hungary has been characterized by a slow decline in the number of subscriber lines in recent years. The penetration of fixed lines has fallen from a peak of approximately 38% in 2000 to approximately 31% as of December 31, 2008 (expressed as a proportion of the overall population), primarily as a result of the rapid increase in mobile penetration from approximately 10% of the population in 1998 to over 100% by the end of 2007 (and the resulting migration of both residential and Business traffic from fixed to mobile networks) as well as increased competition from cable television operators (offering “triple play” packages comprised of television, Internet and voice services). The fixed line penetration per household as of December 31, 2008 was approximately 61%. However, in terms of subscribers, the contraction of the fixed line market has slowed as the mobile penetration growth has also slowed and broadband penetration has increased. The number of fixed lines decreased by 4% from the end of 2007 to the end of 2008 while the increase in the mobile penetration rate was 11% from the end of 2007 to the end of 2008.

-27-

Internet

The most significant fixed line Internet Service Providers in Hungary in addition to us are T-Online (part of T-Com), GTS-Datanet (“GTS”), and Enternet, each providing both residential (dial-up and DSL) and Business (DSL and leased line) Internet services. Incumbent fixed line operators also benefit from the telecommunications traffic generated by dial-up customers and from providing the DSL wholesale services to reseller Internet Service Providers. As an alternative to DSL based broadband services, cable television operators (subject to the technical conditions of their networks) make available broadband Internet access services through cable modems connected to the cable television network. Cable television based broadband access offers substantially the same speed and quality as the DSL technology, for a price comparable to DSL prices. Both T-Com (through its cable television operator, T-Kábel) and UPC Hungary, the two largest cable television operators, offer broadband Internet access services in certain parts of our historical concession areas. As of the end of December 2008, the percentage of the Mass Market broadband Internet access market attributable to DSL was approximately 51% with the remaining 49% attributable to cable broadband.

Data

The provision of data services has been liberalized in Hungary since 1992, with no regulatory barriers to entering into the market. This factor, together with Hungary’s expected economic growth and central location, attracted significant investment into the data communications sector. Not only did incumbent fixed line operators expand their existing networks but alternative service providers emerged and established backbone and access networks (the part of the telecommunications network that connects the end users to the backbone), providing both wholesale broadband data transmission and data services (including voice over IP) primarily targeting the Business market in Budapest and in large business centers in other parts of Hungary. Alternative service providers typically benefit from the combined use of existing third party incumbent networks and state of the art new networks (typically fiber optical based) and agreements with international telecommunications operators. Currently, the most important providers of data transmission services in Hungary other than us are T-Com and GTS.

Mobile

Hungary was the first country in Central and Eastern Europe to introduce public mobile telecommunications services. Currently there are three mobile operators providing mobile voice telephone services in Hungary: T-Mobile (part of T-Com); Pannon GSM (a Telenor affiliate operating since 1993); and Vodafone (operating since 1999). These mobile operators provide GSM services in both the 900 and 1800 MHz band and, pursuant to licenses awarded by the government in 2004, 3G Universal Mobile Telecommunications System (“UMTS”) services.

The mobile communications market in Hungary is highly competitive and characterized by successive promotional campaigns and price competition. Historically, mobile telephony, due in part to limited fixed line penetration in the 1980s and early 1990s, increased rapidly in penetration in Hungary which has led to a mobile penetration rate which is significantly higher than that of fixed lines. As of December 31, 2008, mobile penetration was over 121% as compared with a fixed line penetration rate of 31% (in each case expressed as a proportion of the population) and as compared with a fixed line household penetration of 61%. Mobile operators have also successfully introduced new tariff structures for voice (such as pre-payment). The financial success of mobile operators has been further supported by the relatively high prices which they have been able to charge to fixed line operators for terminating voice calls to their mobile customers that originated on fixed line networks.