Exhibit 99.1

|

March 16, 2017

To the Unitholders of Steel Partners Holdings L.P.:

Steel Partners had a good year from both a financial and operating perspective. During the past year, we continued to simplify our business structure by starting the process to purchase the 36% of Steel Excel Inc. we didn’t own. This transaction closed in early 2017, and we are now much closer to our goal of having one company.

I want to thank all of our outside directors for their objectivity, thoroughness and dedication. I also want to thank everyone at Steel for their persistent efforts and focus on our journey from good to great.

The immediate effect of simplifying our business structure is a meaningful reduction in costs and time. We eliminate duplicative expenses associated with managing public companies, such as insurance, accounting and director fees. Additionally, as one company, we can more efficiently implement our Steel growth and development program to enable and empower our people to reach their potential. At this point in time, Steel Partners has made a strategic decision to make fewer minority investments in public companies and focus on growth and driving value by acquiring and operating entire companies. We will continue to buy and build businesses for the long-term, including bolt-on acquisitions and new platforms.

We remain attracted to companies comprising multiple businesses, where the easy and most visible fix is to divest under-performing assets tax-efficiently, and where other business units can benefit from operational improvements including, but not limited to, footprint optimization, management incentive programs, reduction of corporate overhead, competitive improvement programs, lean manufacturing and elimination of business waste.

We continue to focus on prudent capital allocation to support organic growth, new product development, and research and development, as well as acquisitions. We look for risk-adjusted returns on invested capital in all areas, including profitable growth, cost savings, energy reduction, footprint reduction, and automation.

Additionally, we will also use our capital to purchase our own shares when they are trading at a significant discount to our intrinsic valuation. In 2016, Steel Partners purchased 503,463 common units for $7.3 million at an average price of $14.49, and our Board of Directors approved a new repurchase program in December 2016 for up to 2 million common units.

Also, our Board of Directors approved a special, one-time cash dividend of $.15 per unit, which was paid on January 13, 2017, to unitholders of record as of January 3, 2017.

Subsequent to the close of 2016, as part of our business simplification program, we successfully completed the purchase of the 36% of Steel Excel Inc. shares that we did not own at $17.80 per share of newly issued 6.0% Series A preferred units of Steel Partners Holdings, that are now trading on the New York Stock Exchange under the ticker symbol “SPLPPRA.” The first regular quarterly dividend in connection with the preferred units, amounting to $.15 per unit (and representing the amount of the regular quarterly distribution pro-rated from the February 7, 2017 date of issuance), was paid on March 15, 2017, to unitholders of record as of March 1, 2017.

And, on March 6, 2017, we offered to acquire all of the outstanding shares of common stock of Handy & Harman (NASDAQ: HNH) not owned by Steel Partners or its subsidiaries for a price of $29.00 per share, or approximately $106.7 million. Steel Partners currently owns approximately 70% of Handy & Harman’s outstanding shares. Our proposal contemplates that stockholders of Handy & Harman (other than Steel Partners and its subsidiaries) would receive in total approximately $106.7 million in liquidation preference of Steel Partners 6.0% Series A preferred units. If this transaction is consummated, we will truly be ONE Steel. Stay tuned.

A LOOK at Steel Partners Today

Below you can see the progress we have made with our business simplification plan:

|

*Steel Excel, DGT, and Steel Services Ltd. are included in SPLP

*API and WebBank are included in WebFinancial Holding Corp.

* * * * *

THE STEEL WAY

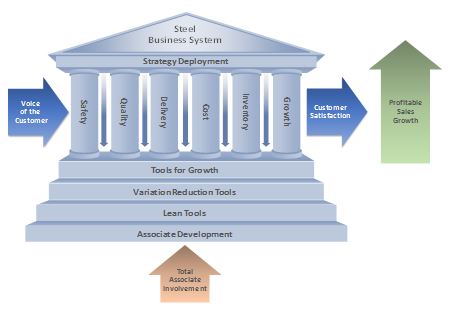

The Steel Way is the methodology we use to invest and manage our businesses. From lean manufacturing to wellness, environmental, health and safety programs, we are committed to empowering our employees, holding them accountable, and rewarding them for success. By focusing on the six pillars of safety, quality, delivery, cost, inventory, and growth, we are constantly driving toward “True North.”

|

Steel Business System represents our culture, includes a collection of Lean Manufacturing and Six Sigma tools, and much more. As we like to say, it may be simple, but it certainly isn’t easy. It is through our commitment to continuous improvement that we continue to develop our competitive advantages and deliver profitable results.

Steel Services continues to enhance the value of all our companies by providing a variety of shared services, including legal, tax, accounting, human resources, analysis, treasury, lean oversight, compliance, administration, environmental, health and safety, business development, audit, merger and acquisition services, and by providing Presidents and CFOs for many of Steel Partners’ operating businesses.

Through the consolidation of corporate overhead and back office functions, we continue to realize cost savings for our affiliated companies, and are able to deliver more efficient and effective services.

Steel Procurement Council is comprised of more than 30 members who are appointed by their CEOs to continuously collaborate and add value by leveraging our combined purchasing power.

In 2016, the Steel Partners Purchasing Council focused on deepening our relationship with current suppliers and identifying secondary suppliers where prudent. We also focused on ensuring the compliance of the supply chain with all regulations and developing best practices across the affiliates.

Steel Environmental Health & Safety Councilis comprised of the health and safety teams at the Steel affiliate companies and representatives from the legal and human resources departments. In 2016, the council was able to tour an API facility to see best practices in use and learn from each other. This year, the council is tasked with continuing to standardize a safety program across the entire business to ensure that safety is truly our number one priority.

Steel Growis our way of developing and managing our team of people. At Steel, we see ourselves as a true team. Everyone on the team has a job to do, and we all have responsibilities to ourselves and each other. I see leaders whose jobs are similar to coaches, encouraging their employees, and ensuring that their “tanks are filled” and that they are empowered to do their jobs. I see employees who show up every day with positive attitudes of growth, ready to take on new challenges where they are needed and deliver results day in and day out.

Our talent management program is working well. We continue to develop and retain our proven management team to ensure continued success for many years to come.

Last year, William Fejes took the reins at Handy & Harman Group as CEO and President, following the acquisition of SL Industries, where he previously served as CEO and President. Jeff Svoboda, previously CEO and President of Handy & Harman Group, is now Vice Chairman of Steel Partners Holdings and also continues to serve Handy & Harman and API on their Board of Directors. Doug Woodworth also was elevated to CFO of Steel Partners and Handy & Harman, after serving as Vice President and Controller of Handy & Harman since 2012.

Steel Partners CEO Summitis our annual gathering of all CEOs and Presidents. This year, capital allocation, best practices, development opportunities, and market trends will all be presented to ensure that our entire management team is marching to the same drum.

Bruce Greenwald from Columbia University will be joining us at the CEO Summit to discuss capital allocation. Professor Greenwald holds the Robert Heilbrunn Professorship of Finance and Asset Management at Columbia Business School and is the academic Director of the Heilbrunn Center for Graham & Dodd Investing. Described by theNew York Times as "a guru to Wall Street's gurus," Greenwald is an authority on value investing, with additional expertise in productivity and the economics of information. I am honored and very excited to have Bruce join us.

In our relentless drive to increase value,Tim Grover, author and celebrity trainer, will be at the CEO Summit to talk about going from “Good to Great to Unstoppable.” Since 1989, when Tim Grover began working with Michael Jordan, he has set the standard for elite training and excellence in sports performance worldwide. Internationally-renowned for his work with Hall-of-Famers and champions such as Michael Jordan, Kobe Bryant, Dwyane Wade, and hundreds of other superstars from all sports, he is the unparalleled preeminent authority on the science and art of achieving physical and mental dominance. We look forward to having Tim with us.

* * * * *

A LOOK AT OUR FINANCIALS

Currently, Steel Partners consists of 100%-owned businesses, controlled subsidiaries and some non-controlled businesses. Today, we have approximately 18 companies, with a total of more than 4,857 employees and 72 plants operating in 8 countries.

For the year ended December 31, 2016, revenue grew to $1.164 billion, from $965 million in 2015. Income before taxes, equity method investments and other investments held at fair value for 2016 was $22.4 million, compared with $23.4 million in 2015. Net income attributable to the Company's common unitholders for the year was $6.6 million, or $0.25 per diluted common unit, compared with $136.7 million, or $4.98 per diluted common unit, in 2015. Net income from continuing operations attributable to common unitholders was $6.6 million, or $0.25 per diluted common unit, compared with $81.2 million, or $2.96 per diluted common unit, in 2015. Net income from discontinued operations attributable to common unitholders for the year was $0, compared with $55.5 million, or $2.02 per diluted common unit, in 2015.

As of December 31, 2016, there were 26,152,976 Steel Partners common units outstanding. Steel Partners’ total assets were $1.97 billion, and unitholders’ equity was $549 million. Per unit book value was $20.98. Steel Partners unit closing price on the NYSE at December 30, 2016 was $15.50 per unit, and management’s beneficial ownership was approximately 50%.

Due to the complexity of our financial statements, we believe one should value Steel Partners using a sum-of-the-parts methodology, which indicates a significantly higher unit value than book value. Today, our emphasis has shifted in a major way to owning and operating businesses. Many of these are worth far more than their cost-based carrying value and combined, significantly more than the current unit price valuation. Below is the sum-of-the-parts analysis:

Symbol | Description | Current Market Value (in millions) | Per SPLP Unit | |||||||

HNH | HANDY & HARMAN | $ | 218.7 | $ | 8.36 | |||||

| N/A | API (1) | 84.4 | 3.23 | |||||||

| N/A | WEBBANK (2) | 319.4 | 12.21 | |||||||

AJRD | AEROJET ROCKETDYNE | 75.1 | 2.87 | |||||||

| N/A | STEEL EXCEL (3) | 108.4 | 4.14 | |||||||

MLNK | MODUSLINK GLOBAL SOLUTIONS | 14.2 | 0.54 | |||||||

OTHER INVESTMENTS | 39.9 | 1.53 | ||||||||

NET DEBT | (54.7 | ) | (2.08 | ) | ||||||

Total Value | $ | 805.4 | $ | 30.80 | ||||||

1. | Valued at API acquisition cost plus Hazen and AMP acquisition costs. |

2. | WebBank 12 months after tax NI for the year ended Dec. 31, 2016 at a multiple of 12. |

3. | Valued at Steel Excel tender offer price of $17.80 per share, less the value of SPLP units owned by Steel Excel. |

ACQUISITION CRITERIA

Acquisitions will continue to play a major role in our growth, as we continue to add value for all of our stakeholders. We are interested in acquiring companies with a minimum of $25 million of EBITDA, gross margins above 20%, high returns on invested capital, sustainable competitive advantages and strong brands. We like businesses participating in structural changes, where the company is positioned to gain market share.

We have significant experience working through all layers of the capital structure, as well as pre-bankruptcy and bankruptcy matters. We prefer healthy companies, where the business has the characteristics stated above, but we are open minded if the balance sheet is challenged as we can utilize our balance sheet and operating system to improve the business outlook.

Our focus on capital allocation and return on invested capital allows us to grow our businesses and make acquisitions while mitigating our risk. We have rigid parameters for capital allocation, but we have a very long investment horizon.

Going into 2017, we will focus on the business simplification plan. We will also continue to adhere to our rigid capital allocations and modest use of leverage by making acquisitions where it makes sense. We will drive the “Steel Way” to deliver our highly efficient operating performance using the Steel Business System, and we will continue to develop our bench of talent to enable every individual to reach their potential.

We always take an active approach to our investments and the management of our businesses. We eat our own cooking as we are the largest owner of Steel Partners.

Thank you for your continued support and input.

Respectfully,

Warren G. Lichtenstein

“Nothing in the world can take the place of Persistence. Talent will not; nothing is more common than unsuccessful men with talent. Genius will not; unrewarded genius is almost a proverb. Education will not; the world is full of educated derelicts. Persistence and Determination alone are omnipotent.”

– Calvin Coolidge

“The price of success comes from the avenue of hard work.”

– Tommy Lasorda

BUSINESS UPDATES

Aerojet Rocketdyne Holdings, Inc. (NYSE:AJRD),www.rocket.com, is a manufacturer of aerospace and defense systems, and also has a real estate business.

Our initial investment in Aerojet Rocketdyne was made on August 4, 2000.

As of December 31, 2016, Steel Partners owns approximately 6% of Aerojet Rocketdyne, with a market value of $75.1 million.

For the year ended December 31, 2016, Aerojet Rocketdyne Holdings, Inc. had sales of $1.76 billion, compared with $1.71 billion in the prior year. The balance sheet had net debt of $315.3 million, and the Aerojet Rocketdyne total contract backlog was $4.5 billion as of December 31, 2016.

2016 was a busy year for the team at Aerojet Rocketdyne. The business continued to focus on its Competitive Improvement Plan (CIP) that was launched in 2015. This program, intended to reduce cost and increase operating efficiency, is approximately halfway through its four-year implementation period. The team also rolled out a codified business operating system in early 2016 called ARBOS (Aerojet Rocketdyne Business Operating System). The operating system’s over-arching goal is reducing risk, process variability and product defects, thereby creating a high degree of customer satisfaction.

There were several structure and staffing changes announced in 2016 as well. I was named Executive Chairman in June of 2016. In this expanded role, Aerojet Rocketdyne’s Board determined that my background, knowledge of the business, and industry contacts are valuable to the company and would drive more value with me serving as an executive of Aerojet Rocketdyne with a greater time commitment. To enhance communication, create focus and reduce cost, Aerojet Rocketdyne also restructured the organization, consolidating the previous six business units into two – Space and Defense. Lastly, the business appointed three new executives at the senior staff level. Arjun Kampani was named VP, General Counsel in April of 2016. Paul Lundstrom was named VP, Chief Financial Officer in November of 2016. And in February of 2017, the business appointed Jerry Tarnacki as Senior VP of the Space business unit. All have significant experience in aerospace and defense businesses. Mr. Kampani was a top M&A lawyer at General Dynamics. Mr. Lundstrom served in various CFO roles prior to running the investor relations function for United Technologies. Prior to joining Aerojet Rocketdyne as Vice President of Quality, Continuous Improvement and Mission Assurance, Jerry Tarnacki held various roles of increasing responsibility at Pratt & Whitney.

Aerojet Rocketdyne overhauled its capital structure in 2016. Aerojet Rocketdyne raised more than $1 billion of debt and debt facilities, including a $300 million convertible bond offering in December, lowering the company’s interest rate, removing restrictive covenants inherent in the prior facility, and providing optionality for multiple capital deployment strategies.

This is an exciting time in the space and defense industry, and we plan to aggressively increase the value of Aerojet Rocketdyne.

Handy & Harman Ltd. (NASDAQ (CM): HNH),www.handyharman.com, is a diversified manufacturer of engineered industrial products, with leading market positions.

Our initial investment in Handy & Harman was on February 4, 1998.

On March 6, 2017, we announced a proposal to acquire all outstanding shares of common stock of Handy & Harman not owned by Steel Partners or its subsidiaries for a price of $29.00 per share, or approximately $106.7 million. Steel Partners currently owns approximately 70% of Handy & Harman’s outstanding shares. Our proposal contemplates that stockholders of Handy & Harman (other than Steel Partners and its subsidiaries) would receive in total approximately $106.7 million in liquidation preference of Steel Partners 6.0% Series A preferred units.

Handy & Harman manages its group of businesses on a decentralized basis, with operations principally in North America.

As of December 31, 2016, Steel Partners owned approximately 70% of Handy & Harman, with a market value of $218.7 million.

In June 2016, Handy & Harman acquired all the outstanding shares of SL Industries Inc. (SLI) for approximately $162.0 million, resulting in the creation of its new Electrical Products business unit. In September 2016, it acquired certain assets of the Electromagnetic Enterprise Division of Hamilton Sunstrand Corporation for approximately $62.6 million, expanding the new business unit’s capabilities in certain product sectors.

For the year ended December 31, 2016, net sales grew to $828.3 million, from $649.5 million in 2015. Income from continuing operations before tax and equity investment for 2016 was $8.4 million, compared with $41.5 million in 2015. Loss from continuing operations, net of tax, for 2016 was $10.9 million, or $0.89 per basic and diluted common share, compared with income of $17.0 million, or $1.49 per basic and diluted common share, in 2015. Results for 2016 include certain significant acquisition and integration-related charges, and substantially higher depreciation and amortization, associated with Handy & Harman’s recently completed acquisitions, as well as other non-cash goodwill and asset impairment charges. Absent those charges, results were significantly better in 2016 than 2015. Handy & Harman will continue to measure the success of our businesses based on their operating cash flows, which increased by $24.5 million, compared with 2015.

Handy & Harman continues to carefully manage its portfolio of companies and is actively seeking strategic acquisition candidates.

ModusLink Global Solutions Inc. (NASDAQ: MLNK),www.moduslink.com,through its wholly-owned subsidiaries, ModusLink Corporation and ModusLink PTS, Inc. (together ModusLink), is a global provider of comprehensive supply chain, logistics and eBusiness solutions. ModusLink today, partners with many of the world’s largest and most trusted brands, including Cisco, eBay, EMC, Ericsson, Fitbit, Fujitsu, GoPro, HP, Lenovo, Microsoft, Sony, Toshiba and others.

Solutions provided range from value-added warehousing and distribution, repair and recovery, returns management, reverse logistics, financial management, and aftersales, in addition to end-to-end eBusiness solutions, which support the emergence of the Internet of Things (IoT). ModusLink’s operations are supported by more than 20 global sites across North America, Europe and the Asia/Pacific region, which in total, manage over $4.5 billion of client materials on an annual basis.

Our initial investment in ModusLink was made on June 13, 2012.

ModusLink has a July 31year end. As of December 31, 2016, Steel Partners and Handy & Harman had a combined ownership interest of approximately 18.2 million shares, or 32.9% in ModusLink, with a market value of approximately $26.5 million. ModusLink currently has a market capitalization of approximately $91.8 million and had federal NOLs of approximately $2.1 billion as of July 31, 2016.

For the year ended July 31, 2016, ModusLink reported net sales of $459.0 million, compared with $561.7 million for the year ended July 31, 2015. Net loss for the year ended July 31, 2016 was $61.3 million, or $1.18 per share, compared with a net loss of $18.4 million, or $0.35 per share, for the year ended July 31, 2015.

Jim Henderson is now the CEO of ModusLink, assuming this position in March 2016. Under his leadership, ModusLink embarked on a series of process enhancements and lean initiatives, some of which leverage Steel Partners’ operational excellence platform. These efforts have enabled ModusLink to better service its clients, improve its offering and lower its cost basis to improve financial performance.

From a corporate perspective, ModusLink remains interested in acquiring businesses at a favorable multiple, businesses which can further strengthen its comprehensive supply chain and logistics offering, global footprint, eBusiness capabilities, or a new platform company with significant operations in the United States, good gross margins and returns on invested capital. Please let us know if any come to mind.

Steel Excel Inc., www.steelexcel.com, has two operating subsidiaries: Steel Energy Services Ltd. (Steel Energy) and Steel Sports Inc. (Steel Sports).

Our initial investment in Steel Excel was in 2007.

For the year ended December 31, 2016, our Energy segment, which consists of our Steel Excel subsidiary, reported net revenue of $94.0 million, as compared with $132.6 million in 2015. The segment incurred a loss of $11.5 million in 2016, as compared with a loss of $95.1 million in 2015. The loss for 2016 included impairment charges of $7.2 million related to marketable securities and other investments; the loss for 2015 included impairment charges of $19.6 million related to goodwill and impairment charges of $59.8 million related to marketable securities. At December 31, 2016, the segment had cash and marketable securities totaling $141.0 million, and Federal NOLs totaling of $158.0 million. During the year, Steel Excel repurchased 1,130,391 shares for $11.3 million at an average price of $9.99.

Steel Energy has three subsidiaries – Sun Well Service, (www.sunwellservice.com), Rogue Pressure Services, (www.roguepressureservices.com), and Black Hawk Energy Services, (www.blackhawkenergyservices.com) – that provide premium oil well services to exploration and production companies working in North Dakota, as well as New Mexico, Colorado, and Texas.

Steel Sports Inc. strives to provide a first-class youth sports experience emphasizing positive experiences and instilling the core values of discipline, teamwork, safety, respect, and integrity. For more information, please visit the company’s website (www.steel-sports.com). Steel Sports currently has two operating subsidiaries, Baseball Heaven, Inc. (www.baseballheavenli.com), a premier venue for amateur and youth baseball, and UK Elite Soccer, Inc., a provider of youth soccer programs and camps. Steel Sports also operates a CrossFit™ facility.

In February 2017, Steel Partners Holdings L.P. completed a transaction through which it acquired the remaining shares of Steel Excel not previously owned.

WebFinancial Holding Corp.

WebBank (Private),www.webbank.com, an FDIC-insured, Utah-chartered bank located in Salt Lake City, is 91.2% owned by Steel Partners. The Bank is engaged in a full range of banking activities, including making loans, issuing credit cards and taking federally insured deposits. It is also a leading provider of national revolving and closed-end consumer and small business financing programs.

Our initial investment in WebBank was in 1996.

WebBank offers revolving and closed-end credit to consumers and small businesses nationwide, partnering with nonbank finance companies, financial technology platforms, retailers and manufacturers to offer access to WebBank's products. Revenue is largely derived from these loans, which provide fee and interest income. Despite significant declines in a number of WebBank’s key programs, caused by capital market disruptions, WebBank successfully added new partners, new products and began holding more assets to maturity in 2016. Pretax income was $48.9 million in 2016, as compared to $52.4 million in 2015.

The Bank reported net income of $29.2 million for 2016 and a return on average equity of 37.6%. The Bank made $5.0 million in dividend payments to its parent in 2016. The Bank’s December 31, 2016 total assets and equity capital were $464.5 million and $88.7 million, respectively.

API Group, www.apigroup.com, is a leading manufacturer and distributor of foils, laminates and holographic materials which provide exceptional brand enhancement for consumer goods and printed media worldwide.

Our initial investment in API was on January 24, 1997.

Steel gained control of API’s operations on April 17, 2015. Net sales for 2016 totalled approximately $170.0 million, with operating income of $5.0 million. The company also generated cash flow from operations of $7.4 million. During 2016, API made two acquisitions: the Osgood, Indiana lamination facility of Hazen Paper and Amsterdam Metallized Products in Amsterdam, Netherlands. During 2016, API also divested its security holographics business in Salford, United Kingdom.

Steel Partners Results Since Inception |

|

1. | Net of all fees and expenses before 20% incentive fee. |

2. | NAV calculated from October 1, 1993, the founding date of Steel Partners II L.P. |

3. | January 1, 2011 – April 30, 2011: NAV prepared for the full month of April 2011 though units began to trade on the OTC market on April 19, 2011. |

4. | April 19, 2011 – December 31, 2011: The units traded on the OTC market during this period. Nearly all shares were held in book entry at American Stock Transfer, so there was little trading volume. |

5. | January 1, 2012 – April 4, 2012: The units traded on the OTC market during this period. Nearly all shares were held in book entry at American Stock Transfer, so there was little trading volume. |

6. | April 5, 2012 – December 31, 2014: The units were listed and began trading on the NYSE on April 5, 2012, and remain trading on the NYSE to present day. |

7. | Unit price at 12-31-12: $11.79 |

8. | Unit price at 12-31-13: $17.35 |

9. | Unit price at 12-31-14: $17.65 |

10. | Unit price at 12-31-15: $16.38 |

11. | Unit price at 12-31-16: $15.50 |

Page 13