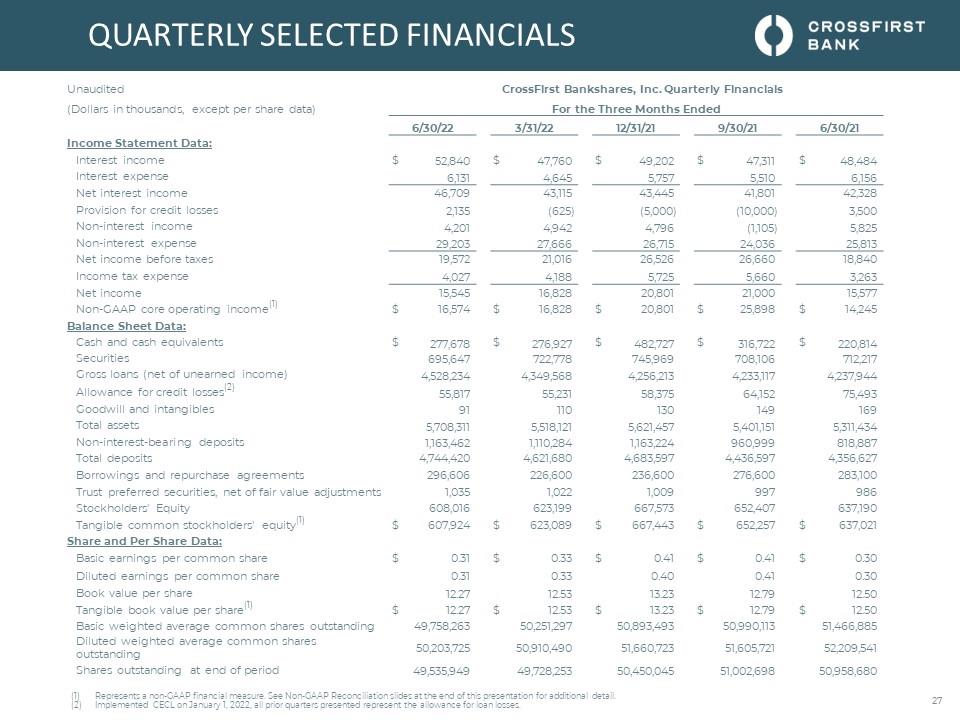

QUARTERLY SELECTED FINANCIALS CROSSFIRST

BANKSAHRES, INC. Unaudited CrossFirst Bankshares, Inc.

Quarterly Financials (Dollars in thousands, except per share data)

For the Three Months Ended 6/30/22 3/31/22 12/31/21 9/30/21 6/30/21

Income Statement Data: Interest income $ 52,840 $ 47,760 $ 49,202

$ 47,311 $ 48,484 Interest expense 6,131 4,645 5,757 5,510

6,156 Net interest income 46,709 43,115 43,445 41,801 42,328

Provision for credit losses 2,135 (625) (5,000) (10,000) 3,500 Non-interest

income 4,201 4,942 4,796 (1,105) 5,825 Non-interest expense

29,203 27,666 26,715 24,036 25,813 Net income before taxes 19,572

21,016 26,526 26,660 18,840 Income tax expense 4,027 4,188

5,725 5,660 3,263 Net income 15,545 16,828 20,801 21,000 15,577

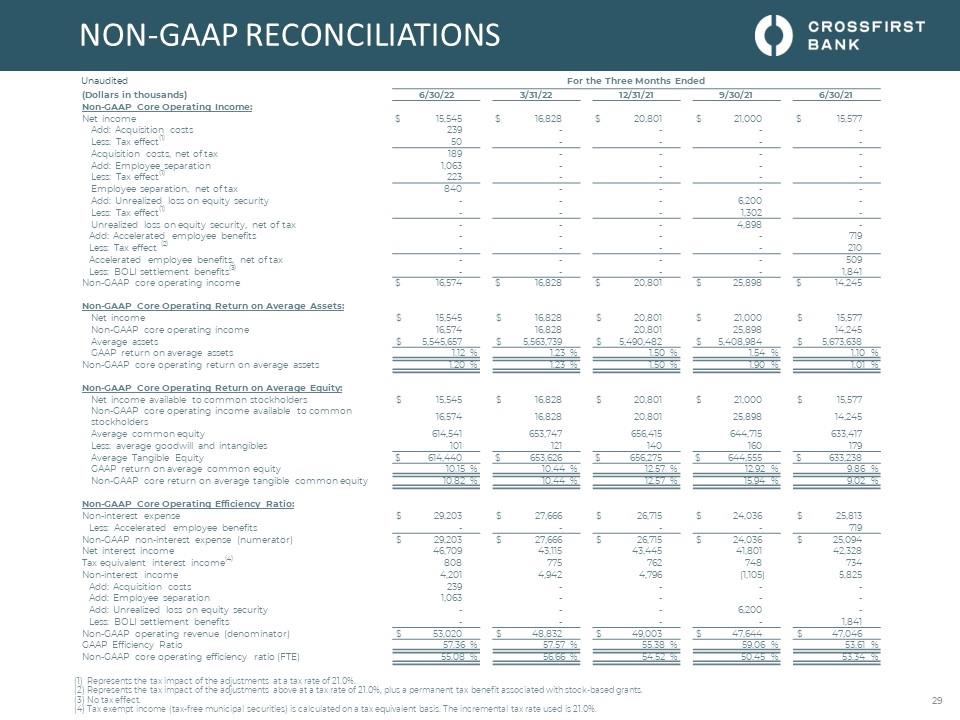

Non-GAAP core operating income(1) $ 16,574 $ 16,828 $ 20,801

$ 25,898 $ 14,245 Balance Sheet Data: Cash and cash equivalents

$ 277,678 $ 276,927 $ 482,727 $ 316,722 $ 220,814 Securities

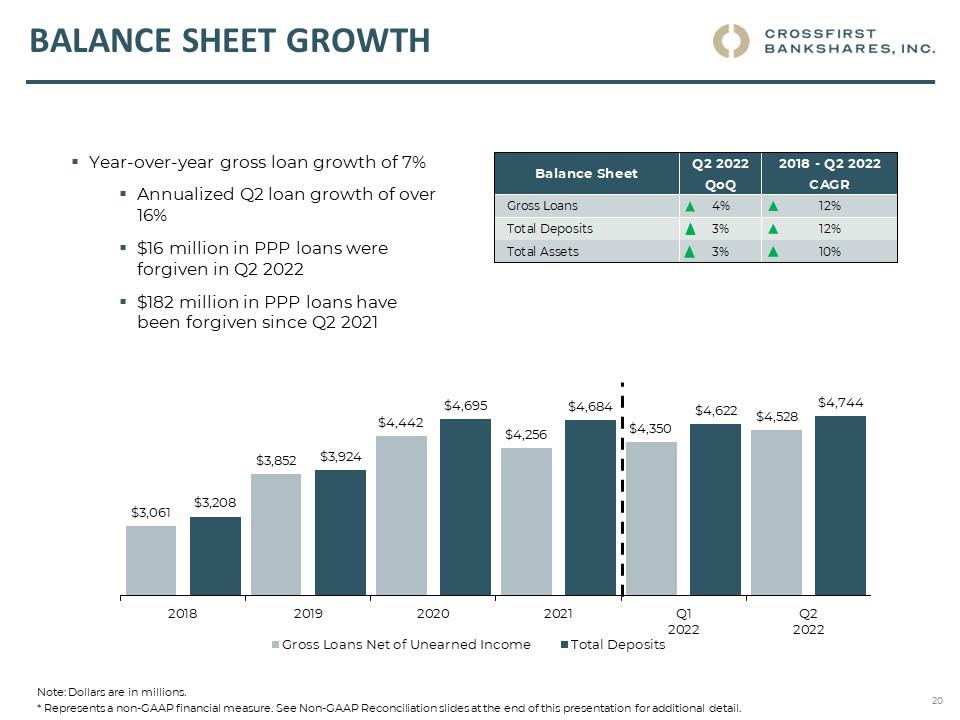

695,647 722,778 745,969 708,106 712,217 Gross loans (net of

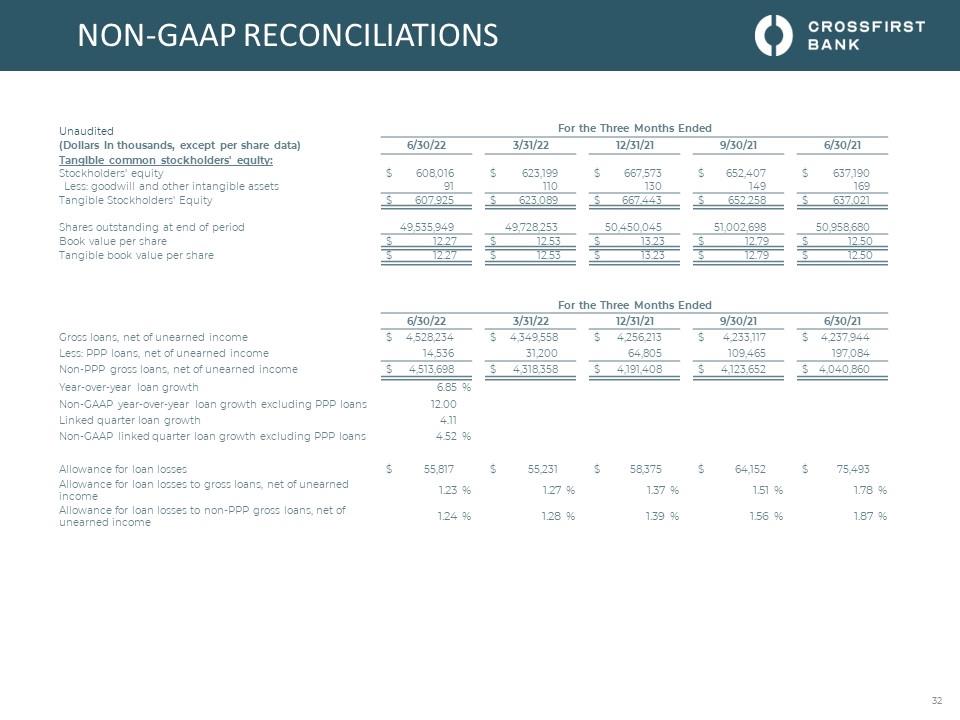

unearned income) 4,528,234 4,349,568 4,256,213 4,233,117

4,237,944 Allowance for credit losses(2) 55,817 55,231 58,375

64,152 75,493 Goodwill and intangibles 91 110 130 149

169 Total assets 5,708,311 5,518,121 5,621,457 5,401,151 5,311,434

Non-interest-bearing deposits 1,163,462 1,110,284 1,163,224

960,999 818,887 Total deposits 4,744,420 4,621,680 4,683,597

4,436,597 4,356,627 Borrowings and repurchase agreements

296,606 226,600 236,600 276,600 283,100 Trust preferred

securities, net of fair value adjustments 1,035 1,022 1,009 997 986 Stockholders'

Equity 608,016 623,199 667,573 652,407 637,190 Tangible

common stockholders' equity(1) $ 607,924 $ 623,089 $ 667,443

$ 652,257 $ 637,021 Share and Per Share Data: Basic earnings

per common share $ 0.31 $ 0.33 $ 0.41 $ 0.41 $ 0.30 Diluted earnings

per common share 0.31 0.33 0.40 0.41

0.30 Book value per share 12.27 12.53 13.23 12.79 12.50 Tangible

book value per share(1) $ 12.27 $ 12.53 $ 13.23 $ 12.79 $ 12.50

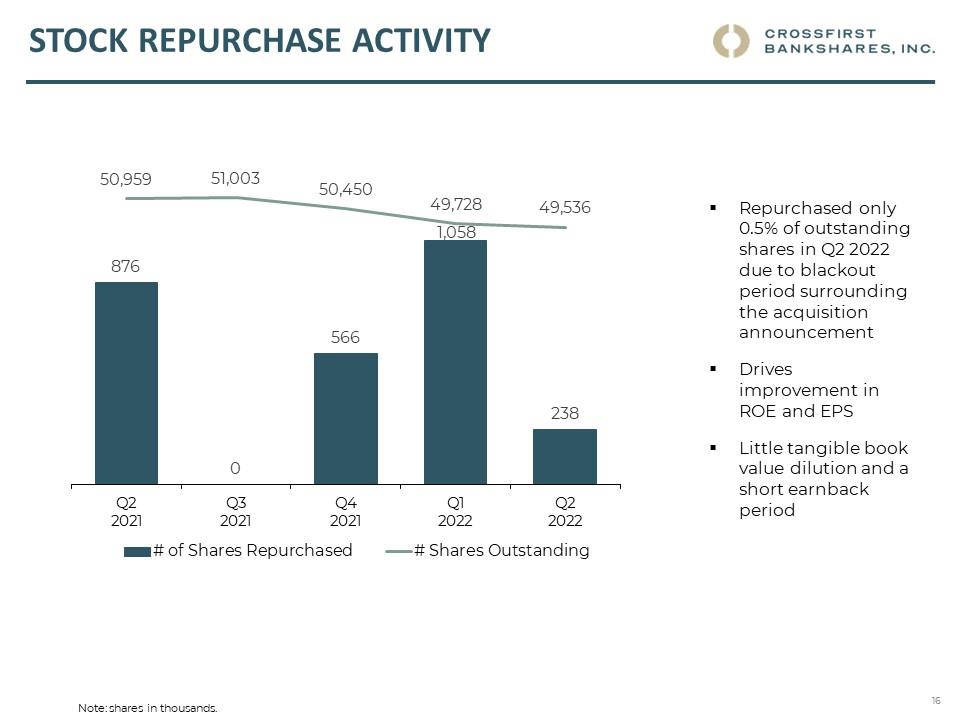

Basic weighted average common shares outstanding 49,758,263

50,251,297 50,893,493 50,990,113 51,466,885 Diluted weighted

average

common shares outstanding 50,203,725 50,910,490 51,660,723 51,605,721

52,209,541 Shares outstanding at end of period 49,535,949 49,728,253

50,450,045 51,002,698 50,958,680 Represents a non-GAAP financial

measure. See Non-GAAP Reconciliation slides at the end of this

presentation for additional detail. Implemented CECL on January

1, 2022, all prior quarters presented represent the allowance for loan

losses. 27