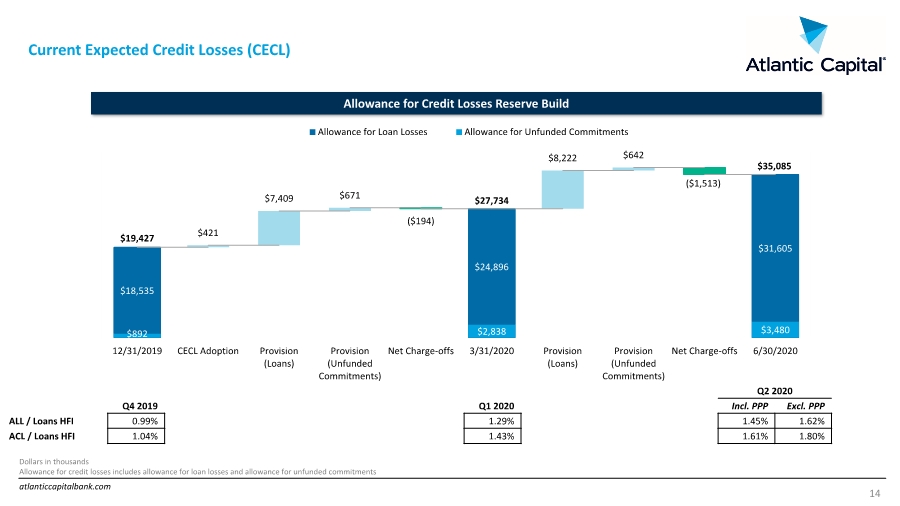

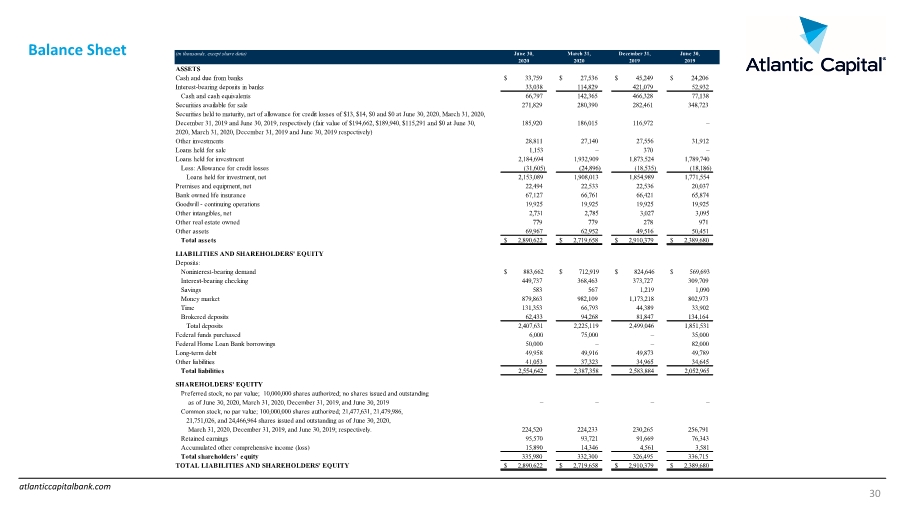

| atlanticcapitalbank.com Balance Sheet 30 (in thousands, except share data) June 30, March 31, December 31, June 30, 2020 2020 2019 2019 ASSETS Cash and due from banks $ 33,759 $ 27,536 $ 45,249 $ 24,206 Interest-bearing deposits in banks 33,038 114,829 421,079 52,932 Cash and cash equivalents 66,797 142,365 466,328 77,138 Securities available for sale 271,829 280,390 282,461 348,723 Securities held to maturity, net of allowance for credit losses of $13, $14, $0 and $0 at June 30, 2020, March 31, 2020, December 31, 2019 and June 30, 2019, respectively (fair value of $194,662, $189,940, $115,291 and $0 at June 30, 2020, March 31, 2020, December 31, 2019 and June 30, 2019 respectively) 185,920 186,015 116,972 – Other investments 28,811 27,140 27,556 31,912 Loans held for sale 1,153 – 370 – Loans held for investment 2,184,694 1,932,909 1,873,524 1,789,740 Less: Allowance for credit losses (31,605) (24,896) (18,535) (18,186) Loans held for investment, net 2,153,089 1,908,013 1,854,989 1,771,554 Premises and equipment, net 22,494 22,533 22,536 20,037 Bank owned life insurance 67,127 66,761 66,421 65,874 Goodwill - continuing operations 19,925 19,925 19,925 19,925 Other intangibles, net 2,731 2,785 3,027 3,095 Other real estate owned 779 779 278 971 Other assets 69,967 62,952 49,516 50,451 Total assets $ 2,890,622 $ 2,719,658 $ 2,910,379 $ 2,389,680 LIABILITIES AND SHAREHOLDERS' EQUITY Deposits: Noninterest-bearing demand $ 883,662 $ 712,919 $ 824,646 $ 569,693 Interest-bearing checking 449,737 368,463 373,727 309,709 Savings 583 567 1,219 1,090 Money market 879,863 982,109 1,173,218 802,973 Time 131,353 66,793 44,389 33,902 Brokered deposits 62,433 94,268 81,847 134,164 Total deposits 2,407,631 2,225,119 2,499,046 1,851,531 Federal funds purchased 6,000 75,000 – 35,000 Federal Home Loan Bank borrowings 50,000 – – 82,000 Long-term debt 49,958 49,916 49,873 49,789 Other liabilities 41,053 37,323 34,965 34,645 Total liabilities 2,554,642 2,387,358 2,583,884 2,052,965 SHAREHOLDERS' EQUITY Preferred stock, no par value; 10,000,000 shares authorized; no shares issued and outstanding as of June 30, 2020, March 31, 2020, December 31, 2019, and June 30, 2019 – – – – Common stock, no par value; 100,000,000 shares authorized; 21,477,631, 21,479,986, 21,751,026, and 24,466,964 shares issued and outstanding as of June 30, 2020, March 31, 2020, December 31, 2019, and June 30, 2019; respectively. 224,520 224,233 230,265 256,791 Retained earnings 95,570 93,721 91,669 76,343 Accumulated other comprehensive income (loss) 15,890 14,346 4,561 3,581 Total shareholders’ equity 335,980 332,300 326,495 336,715 TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY $ 2,890,622 $ 2,719,658 $ 2,910,379 $ 2,389,680 |