UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of March 2023

Commission File Number: 001-36298

GeoPark Limited

(Exact name of registrant as specified in its charter)

Calle 94 N° 11-30 8° piso

Bogota, Colombia

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F | X |

| Form 40-F |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes |

| No | X |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes |

| No | X |

GEOPARK LIMITED

TABLE OF CONTENTS

ITEM

| 1. | GeoPark Limited Consolidated Financial Statements as of and for the year ended December 31, 2022 |

Item 1

GEOPARK LIMITED

CONSOLIDATED

FINANCIAL STATEMENTS

As of and for the year ended December 31, 2022

| |

| |

2 | Report of Independent Registered Public Accounting Firm |

4 | Consolidated Statement of Income |

5 | Consolidated Statement of Comprehensive Income |

6 | Consolidated Statement of Financial Position |

7 | Consolidated Statement of Changes in Equity |

8 | Consolidated Statement of Cash Flow |

9 | Notes to the Consolidated Financial Statements |

| |

| |

| |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the shareholders and the Board of Directors of

GeoPark Limited

Opinion on the Financial Statements

We have audited the accompanying consolidated statements of financial position of GeoPark Limited (the Company) as of December 31, 2022 and 2021, the related consolidated statements of income, comprehensive income, changes in equity and cash flow for each of the three years in the period ended December 31, 2022 and the related notes (collectively referred to as the “consolidated financial statements”). In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Company at December 31, 2022 and 2021, and the results of its operations and its cash flows for each of the three years in the period ended December 31, 2022, in conformity with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB).

Basis for Opinion

These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

Critical Audit Matter

The critical audit matter communicated below is a matter arising from the current period audit of the financial statements that was communicated or required to be communicated to the audit committee and that: (i) relates to accounts or disclosures that are material to the financial statements and (ii) involved our especially challenging, subjective or complex judgments. The communication of the critical audit matter does not alter in any way our opinion on the consolidated financial statements, taken as a whole, and we are not, by communicating the critical audit matter below, providing a separate opinion on the critical audit matter or on the accounts or disclosures to which it relates.

Effect of estimated proved and probable oil and gas reserves on the depreciation of property, plant and equipment

Description of the Matter

At December 31, 2022, the carrying value of the Company’s property, plant and equipment was US$ 667 million and depreciation expense was US$ 91 million for the year then ended. As discussed in Note 2.11 the proved and probable reserves are used by the Company in the successful efforts method of accounting for its oil and gas properties. Under such method oil and gas properties are depreciated using the unit-of-production method based on commercial proved and probable oil and gas reserves, as estimated by an independent international oil and gas consulting firm. Proved and probable oil and gas reserves estimates are based on geological, geophysical and engineering assessments of expected reservoir characteristics, future production rates based on historical performance and expected future operating and investment activities. Estimating reserves also requires the selection of inputs, including future oil and gas prices and quality differentials, assumed effects of regulation by governmental agencies, tax rates by jurisdiction and future development and operating costs, among others.

2

Auditing the Company’s depreciation calculations is complex because of the use of the work of the independent international oil and gas consulting firm and the evaluation of management’s determination of the inputs described above used by the engineers in estimating commercial proved and probable oil and gas reserves. Also, the assumptions used by management are subject to changes due to future events and conditions and evaluating them requires significant auditor judgement.

How We Addressed the Matter in Our Audit

We obtained an understanding, evaluated the design and tested the operating effectiveness of the Company’s internal controls over its process to calculate depreciation expense, including management’s controls over proved and probable oil and gas reserves’ estimation process.

Our audit procedures included, among others, evaluating the professional qualifications and objectivity of the Company’s internal reservoir engineers primarily responsible for overseeing the preparation of the reserve estimates and the independent international oil and gas consulting firm hired by the Company. In addition, we evaluated the completeness and accuracy of the financial data and inputs used in estimating proved and probable oil and gas reserves and we identified and evaluated corroborative and contrary evidence. For proved undeveloped reserves, we evaluated management’s development plan by assessing consistency of the development projections with the Company’s drill plan and the availability of capital to develop such plan. We also tested the mathematical accuracy of the depreciation computations of property, plant and equipment, including comparing the proved and probable oil and gas reserve amounts used in the calculations to the Reserve Reports prepared by the independent international oil and gas consulting firm.

/s/ PISTRELLI, HENRY MARTIN Y ASOCIADOS S.R.L.

Member of Ernst & Young Global Limited

We have served as the Company’s auditor since 2020.

Buenos Aires, Argentina

March 8, 2023

3

CONSOLIDATED STATEMENT OF INCOME

| | | | | | | | |

Amounts in US$´000 | | Note | | 2022 | | 2021 | | 2020 |

REVENUE | | 7 | | 1,049,579 | | 688,543 | | 393,692 |

Commodity risk management contracts (loss) gain | | 8 | | (70,221) | | (109,191) | | 8,081 |

Production and operating costs | | 9 | | (359,779) | | (212,790) | | (125,072) |

Geological and geophysical expenses | | 12 | | (10,529) | | (7,891) | | (14,951) |

Administrative expenses | | 13 | | (50,024) | | (46,828) | | (50,315) |

Selling expenses | | 14 | | (7,995) | | (8,730) | | (5,844) |

Depreciation | | | | (96,692) | | (88,969) | | (118,073) |

Write-off of unsuccessful exploration efforts | | 20 | | (25,789) | | (12,262) | | (52,652) |

Impairment loss for non-financial assets, net | | 20‑37 | | — | | (4,334) | | (133,864) |

Other income (expenses) | | | | 527 | | (11,739) | | (11,665) |

OPERATING PROFIT (LOSS) | | | | 429,077 | | 185,809 | | (110,663) |

Financial expenses | | 15 | | (57,073) | | (64,112) | | (64,582) |

Financial income | | 15 | | 3,180 | | 1,652 | | 3,166 |

Foreign exchange gain (loss) | | 15 | | 19,725 | | 5,049 | | (13,008) |

PROFIT (LOSS) BEFORE INCOME TAX | | | | 394,909 | | 128,398 | | (185,087) |

Income tax expense | | 17 | | (170,474) | | (67,271) | | (47,863) |

PROFIT (LOSS) FOR THE YEAR | | | | 224,435 | | 61,127 | | (232,950) |

Earnings (Losses) per share (in US$). Basic | | 19 | | 3.78 | | 1.00 | | (3.84) |

Earnings (Losses) per share (in US$). Diluted | | 19 | | 3.75 | | 0.99 | | (3.84) |

The notes on pages 9 to 81 are an integral part of these Consolidated Financial Statements.

4

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

| | | | | | |

Amounts in US$´000 | | 2022 | | 2021 | | 2020 |

Profit (Loss) for the year | | 224,435 | | 61,127 | | (232,950) |

Other comprehensive income: | |

| |

| |

|

Items that may be subsequently reclassified to profit or loss | |

| |

| |

|

Currency translation differences | | 2,121 | | (1,438) | | (8,449) |

Gain (Loss) on cash flow hedges | | 966 | | — | | (6,770) |

Income tax (expense) benefit relating to cash flow hedges | | (483) | | — | | 2,166 |

Other comprehensive profit (loss) for the year | | 2,604 | | (1,438) | | (13,053) |

| | | | | | |

Total comprehensive profit (loss) for the year | | 227,039 | | 59,689 | | (246,003) |

The notes on pages 9 to 81 are an integral part of these Consolidated Financial Statements.

5

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

| | | | | | |

Amounts in US$´000 | | Note | | 2022 | | 2021 |

ASSETS | | | | | | |

NON-CURRENT ASSETS | | | | | | |

Property, plant and equipment | | 20 | | 666,879 | | 614,047 |

Right-of-use assets | | 28 | | 37,011 | | 21,014 |

Prepayments and other receivables | | 22 | | 121 | | 148 |

Other financial assets | | 25 | | 12,877 | | 13,883 |

Deferred income tax asset | | 18 | | 18,943 | | 14,072 |

TOTAL NON-CURRENT ASSETS | |

| | 735,831 | | 663,164 |

CURRENT ASSETS | |

| |

| |

|

Inventories | | 23 | | 14,434 | | 10,915 |

Trade receivables | | 24 | | 71,794 | | 70,531 |

Prepayments and other receivables | | 22 | | 22,106 | | 22,650 |

Derivative financial instrument assets | | 25 | | 967 | | 126 |

Other financial assets | | 25 | | — | | 864 |

Cash and cash equivalents | | 25 | | 128,843 | | 100,604 |

Assets held for sale | | 36 | | — | | 26,887 |

TOTAL CURRENT ASSETS | |

| | 238,144 | | 232,577 |

TOTAL ASSETS | |

| | 973,975 | | 895,741 |

EQUITY | |

| |

| |

|

Equity attributable to owners of the Company | |

| |

| |

|

Share capital | | 26.1 | | 58 | | 60 |

Share premium | | | | 134,798 | | 169,220 |

Reserves | | | | 61,876 | | 83,554 |

Accumulated losses | | | | (81,147) | | (314,779) |

TOTAL EQUITY | |

| | 115,585 | | (61,945) |

LIABILITIES | |

| |

| |

|

NON-CURRENT LIABILITIES | |

| |

| |

|

Borrowings | | 27 | | 485,114 | | 656,176 |

Lease liabilities | | 28 | | 22,051 | | 12,513 |

Provisions and other long-term liabilities | | 29 | | 51,947 | | 62,848 |

Deferred income tax liability | | 18 | | 70,123 | | 20,947 |

Trade and other payables | | 30 | | — | | 1,540 |

TOTAL NON-CURRENT LIABILITIES | |

| | 629,235 | | 754,024 |

CURRENT LIABILITIES | |

| |

| |

|

Borrowings | | 27 | | 12,528 | | 17,916 |

Lease liabilities | | 28 | | 10,000 | | 8,231 |

Derivative financial instrument liabilities | | 25 | | 19 | | 20,757 |

Current income tax liabilities | | | | 65,002 | | 8,801 |

Trade and other payables | | 30 | | 141,606 | | 127,513 |

Liabilities associated with assets held for sale | | 36 | | — | | 20,444 |

TOTAL CURRENT LIABILITIES | |

| | 229,155 | | 203,662 |

TOTAL LIABILITIES | |

| | 858,390 | | 957,686 |

TOTAL EQUITY AND LIABILITIES | |

| | 973,975 | | 895,741 |

The notes on pages 9 to 81 are an integral part of these Consolidated Financial Statements.

6

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

| | | | | | | | | | | | |

| | Attributable to owners of the Company | | | ||||||||

| | Share | | Share | | Other | | Translation | | Accumulated | | |

Amount in US$‘000 | | Capital | | Premium | | Reserve | | Reserve | | Losses | | Total |

Equity as of January 1, 2020 | | 59 | | 173,716 | | 116,291 | | (3,820) | | (153,361) | | 132,885 |

Comprehensive income: | |

| |

| |

| |

| |

| | |

Loss for the year | | — | | — | | — | | — | | (232,950) | | (232,950) |

Other comprehensive loss for the year | | — | | — | | (4,604) | | (8,449) | | — | | (13,053) |

Total Comprehensive loss for the year 2020 | | — | | — | | (4,604) | | (8,449) | | (232,950) | | (246,003) |

Transactions with owners: | |

| |

| |

| |

| |

| | |

Share-based payment (a) (Note 31) | | 2 | | 7,349 | | — | | — | | 5,445 | | 12,796 |

Repurchase of shares (Note 26.1) | | (1) | | (4,008) | | — | | — | | — | | (4,009) |

Cash distribution (Note 26.2) | | — | | — | | (4,859) | | — | | — | | (4,859) |

Stock distribution (Note 26.3) | | 1 | | 2,342 | | (2,343) | | — | | — | | — |

Total 2020 | | 2 | | 5,683 | | (7,202) | | — | | 5,445 | | 3,928 |

Balances as of December 31, 2020 | | 61 | | 179,399 | | 104,485 | | (12,269) | | (380,866) | | (109,190) |

Comprehensive income: | |

| |

| |

| |

| |

| | |

Profit for the year | | — | | — | | — | | — | | 61,127 | | 61,127 |

Other comprehensive loss for the year | | — | | — | | — | | (1,438) | | — | | (1,438) |

Total Comprehensive (loss) profit for the year 2021 | | — | | — | | — | | (1,438) | | 61,127 | | 59,689 |

Transactions with owners: | |

| |

| |

| |

| |

| | |

Share-based payment (Note 31) | | — | | 1,661 | | — | | — | | 4,960 | | 6,621 |

Repurchase of shares (Note 26.1) | | (1) | | (11,840) | | — | | — | | — | | (11,841) |

Cash distribution (Note 26.2) | | — | | — | | (7,224) | | — | | — | | (7,224) |

Total 2021 | | (1) | | (10,179) | | (7,224) | | — | | 4,960 | | (12,444) |

Balances as of December 31, 2021 | | 60 | | 169,220 | | 97,261 | | (13,707) | | (314,779) | | (61,945) |

Comprehensive income: | |

| |

| |

| |

| |

| | |

Profit for the year | | — | | — | | — | | — | | 224,435 | | 224,435 |

Other comprehensive profit for the year | | — | | — | | 483 | | 2,121 | | — | | 2,604 |

Total Comprehensive profit for the year 2022 | | — | | — | | 483 | | 2,121 | | 224,435 | | 227,039 |

Transactions with owners: | |

| |

| |

| |

| |

| | |

Share-based payment (Note 31) | | 1 | | 1,840 | | — | | — | | 9,197 | | 11,038 |

Repurchase of shares (Note 26.1) | | (3) | | (36,262) | | — | | — | | — | | (36,265) |

Cash distribution (Note 26.2) | | — | | — | | (24,282) | | — | | — | | (24,282) |

Total 2022 | | (2) | | (34,422) | | (24,282) | | — | | 9,197 | | (49,509) |

Balances as of December 31, 2022 | | 58 | | 134,798 | | 73,462 | | (11,586) | | (81,147) | | 115,585 |

| (a) | Includes issuance of shares to certain employees as part of their 2019 bonus compensation of US$ 4,352,000. |

The notes on pages 9 to 81 are an integral part of these Consolidated Financial Statements.

7

CONSOLIDATED STATEMENT OF CASH FLOW

| | | | | | | | |

Amounts in US$‘000 | | Note | | 2022 | | 2021 | | 2020 |

Cash flows from operating activities | |

| |

| |

| |

|

Profit (Loss) for the year | | | | 224,435 | | 61,127 | | (232,950) |

Adjustments for: | |

| |

| |

| |

|

Income tax expense | | 17 | | 170,474 | | 67,271 | | 47,863 |

Depreciation | | | | 96,692 | | 88,969 | | 118,073 |

Loss on disposal of property, plant and equipment | | | | 73 | | 787 | | 417 |

Impairment loss for non-financial assets | | 20‑37 | | — | | 4,334 | | 133,864 |

Write-off of unsuccessful exploration efforts | | 20 | | 25,789 | | 12,262 | | 52,652 |

Accrual of borrowing’s interests | | | | 36,360 | | 44,378 | | 48,690 |

Borrowings cancellation costs | | 15 | | 5,141 | | 6,308 | | — |

Amortization of other long-term liabilities | | 29 | | (2,407) | | (223) | | (387) |

Unwinding of long-term liabilities | | 15 | | 6,026 | | 5,079 | | 5,894 |

Accrual of share-based payment | | | | 11,038 | | 6,621 | | 8,444 |

Foreign exchange (gain) loss | | 15 | | (19,725) | | (5,049) | | 3,594 |

Unrealized (gain) loss on commodity risk management contracts | | 8 | | (13,023) | | (463) | | 12,978 |

Income tax paid | | | | (33,355) | | (65,273) | | (25,193) |

Changes in working capital | | 5 | | (40,047) | | (9,351) | | (5,240) |

Cash flows from operating activities – net | | | | 467,471 | | 216,777 | | 168,699 |

Cash flows from investing activities | |

| |

| |

| |

|

Purchase of property, plant and equipment | | | | (168,808) | | (129,258) | | (75,298) |

Acquisition of business, net of cash acquired | | 36.1 | | — | | — | | (272,335) |

Proceeds from disposal of long-term assets | | 36.2-36.3 | | 15,135 | | 2,700 | | — |

Cash flows used in investing activities – net | | | | (153,673) | | (126,558) | | (347,633) |

Cash flows from financing activities | |

| |

| |

| |

|

Proceeds from borrowings | | 5 | | — | | 172,174 | | 350,000 |

Debt issuance costs paid | | 5 | | — | | (2,019) | | (7,507) |

Principal paid | | 5 | | (172,522) | | (274,934) | | (3,575) |

Interest paid | | 5 | | (36,514) | | (42,592) | | (37,594) |

Borrowings cancellation and other costs paid | | 5 | | (9,118) | | (12,908) | | — |

Lease payments | | 5 | | (7,851) | | (7,518) | | (9,380) |

Repurchase of shares | | 26.1 | | (36,265) | | (11,841) | | (4,009) |

Cash distribution | | 26.2 | | (24,282) | | (7,224) | | (4,859) |

Payments for transactions with former non-controlling interest | | | | — | | (3,580) | | (11,931) |

Cash flows (used in) from financing activities – net | | | | (286,552) | | (190,442) | | 271,145 |

Net increase (decrease) in cash and cash equivalents | | | | 27,246 | | (100,223) | | 92,211 |

| | | | | | | | |

Cash and cash equivalents at January 1 | | | | 100,604 | | 201,907 | | 111,180 |

Currency translation differences | | | | 993 | | (1,080) | | (1,484) |

Cash and cash equivalents at the end of the year | | | | 128,843 | | 100,604 | | 201,907 |

| | | | | | | | |

Ending Cash and cash equivalents are specified as follows: | |

| |

| |

| |

|

Cash in bank and bank deposits | | | | 128,831 | | 100,587 | | 201,884 |

Cash in hand | | | | 12 | | 17 | | 23 |

Cash and cash equivalents | | | | 128,843 | | 100,604 | | 201,907 |

The notes on pages 9 to 81 are an integral part of these Consolidated Financial Statements.

8

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Note 1 General Information

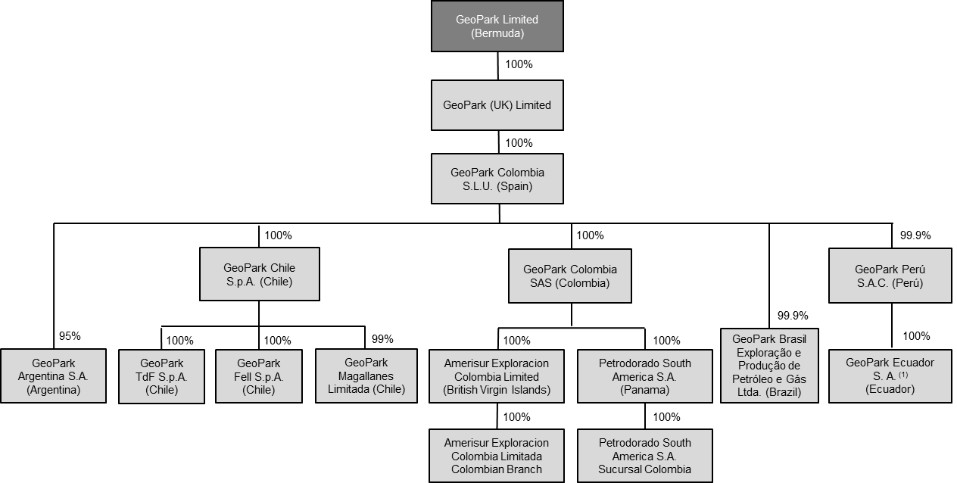

GeoPark Limited (the “Company”) is a company incorporated under the law of Bermuda. The Registered Office address is Clarendon House, 2 Church Street, Hamilton HM11, Bermuda.

The principal activities of the Company and its subsidiaries (the “Group” or “GeoPark”) are exploration, development and production for oil and gas reserves in Colombia, Chile, Brazil and Ecuador.

These Consolidated Financial Statements were authorized for issue by the Board of Directors on March 7, 2023.

Note 2 Summary of significant accounting policies

The principal accounting policies applied in the preparation of these Consolidated Financial Statements are set out below. These policies have been consistently applied to the years presented, unless otherwise stated.

2.1 Basis of preparation

The Consolidated Financial Statements of GeoPark Limited have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”), under the historical cost basis, except for the following: certain financial assets and liabilities (including derivative instruments) measured at fair value, and assets held for sale – measured at fair value less costs to sell.

The Consolidated Financial Statements are presented in thousands of United States Dollars (US$’000) and all values are rounded to the nearest thousand (US$’000), except in the footnotes and where otherwise indicated.

The preparation of financial statements in conformity with IFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the Group’s accounting policies. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the Consolidated Financial Statements are disclosed in this note under the title “Accounting estimates and assumptions”.

All the information included in these Consolidated Financial Statements corresponds to the Group, except where otherwise indicated.

2.1.1 Changes in accounting policy and disclosure

2.1.1.1 New and amended standards and interpretations

The Group applied for the first-time certain standards and amendments, which are effective for annual periods beginning on or after January 1, 2022. The Group has not early adopted any other standard, interpretation or amendment that has been issued but is not yet effective.

Onerous Contracts – Costs of Fulfilling a Contract – Amendments to IAS 37

An onerous contract is a contract under which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits expected to be received under it.

The amendments specify that when assessing whether a contract is onerous or loss-making, an entity needs to include costs that relate directly to a contract to provide goods or services including both incremental costs and an allocation of costs directly related to contract activities. General and administrative costs do not relate directly to a contract and are excluded unless they are explicitly chargeable to the counterparty under the contract.

The Group applied the amendments at the beginning of the reporting period. These amendments had no impact on the Consolidated Financial Statements of the Group as there were no contracts for which it had not fulfilled all of its obligations during the reporting period.

9

Note 2 Summary of significant accounting policies (continued)

2.1 Basis of preparation (continued)

2.1.1 Changes in accounting policy and disclosure (continued)

2.1.1.1 New and amended standards and interpretations (continued)

Reference to the Conceptual Framework – Amendments to IFRS 3

The amendments replace a reference to a previous version of the IASB’s Conceptual Framework with a reference to the current version issued in March 2018 without significantly changing its requirements.

The amendments add an exception to the recognition principle of IFRS 3 Business Combinations to avoid the issue of potential ‘day 2’ gains or losses arising for liabilities and contingent liabilities that would be within the scope of IAS 37 Provisions, Contingent Liabilities and Contingent Assets or IFRIC 21 Levies, if incurred separately. The exception requires entities to apply the criteria in IAS 37 or IFRIC 21, respectively, instead of the Conceptual Framework, to determine whether a present obligation exists at the acquisition date.

The amendments also add a new paragraph to IFRS 3 to clarify that contingent assets do not qualify for recognition at the acquisition date.

In accordance with the transitional provisions, the Group applies the amendments prospectively, i.e., to business combinations occurring after the beginning of the annual reporting period in which it first applies the amendments (the date of initial application).

These amendments had no impact on the Consolidated Financial Statements of the Group as there were no business combinations during the reporting period.

Property, Plant and Equipment: Proceeds before Intended Use – Amendments to IAS 16 Leases

The amendment prohibits entities from deducting from the cost of an item of property, plant and equipment, any proceeds of the sale of items produced while bringing that asset to the location and condition necessary for it to be capable of operating in the manner intended by management. Instead, an entity recognizes the proceeds from selling such items, and the costs of producing those items, in profit or loss.

In accordance with the transitional provisions, the Group applies the amendments retrospectively only to items of PP&E made available for use on or after the beginning of the earliest period presented when the entity first applies the amendment (the date of initial application).

These amendments had no significant impact on the Consolidated Financial Statements of the Group as there were only sales of such items produced by property, plant and equipment made available for use in Ecuador during 2022.

IFRS 1 First-time Adoption of International Financial Reporting Standards – Subsidiary as a first-time adopter

The amendment permits a subsidiary that elects to apply paragraph of IFRS 1 to measure cumulative translation differences using the amounts reported in the parent’s consolidated financial statements, based on the parent’s date of transition to IFRS, if no adjustments were made for consolidation procedures and for the effects of the business combination in which the parent acquired the subsidiary. This amendment is also applied to an associate or joint venture that elects to apply paragraph of IFRS 1.

These amendments had no impact on the Consolidated Financial Statements of the Group as it is not a first-time adopter.

10

Note 2 Summary of significant accounting policies (continued)

2.1 Basis of preparation (continued)

2.1.1 Changes in accounting policy and disclosure (continued)

2.1.1.1 New and amended standards and interpretations (continued)

IFRS 9 Financial Instruments – Fees in the ‘10 per cent’ test for derecognition of financial liabilities

The amendment clarifies the fees that an entity includes when assessing whether the terms of a new or modified financial liability are substantially different from the terms of the original financial liability. These fees include only those paid or received between the borrower and the lender, including fees paid or received by either the borrower or lender on the other’s behalf. There is no similar amendment proposed for IAS 39 Financial Instruments: Recognition and Measurement.

In accordance with the transitional provisions, the Group applies the amendment to financial liabilities that are modified or exchanged on or after the beginning of the annual reporting period in which the entity first applies the amendment (the date of initial application). These amendments had no impact on the Consolidated Financial Statements of the Group as there were no modifications of the Group’s financial instruments during the period.

2.1.1.2 Standards issued but not yet effective

The new and amended standards and interpretations that are issued, but not yet effective, up to the date of issuance of these Consolidated Financial Statements are disclosed below. The Group intends to adopt these new and amended standards and interpretations, if applicable, when they become effective.

Classification of Liabilities as Current or Non-current – Amendments to IAS 1

In January 2020, the IASB issued amendments to paragraphs 69 to 76 of IAS 1 to specify the requirements for classifying liabilities as current or non-current. The amendments clarify:

| ● | what is meant by a right to defer settlement, |

| ● | that a right to defer must exist at the end of the reporting period, |

| ● | that classification is unaffected by the likelihood that an entity will exercise its deferral right, and |

| ● | that only if an embedded derivative in a convertible liability is itself an equity instrument would the terms of a liability not impact its classification. |

The amendments are effective for annual periods beginning on or after January 1, 2023 and must be applied retrospectively. The Group is currently assessing the impact the amendments will have on current practice and whether existing loan agreements may require renegotiation.

Definition of Accounting Estimates - Amendments to IAS 8

In February 2021, the IASB issued amendments to IAS 8, in which it introduces a definition of ‘accounting estimates’. The amendments clarify the distinction between changes in accounting estimates and changes in accounting policies and the correction of errors. Also, they clarify how entities use measurement techniques and inputs to develop accounting estimates.

The amendments are effective for annual periods beginning on or after January 1, 2023 and apply to changes in accounting policies and changes in accounting estimates that occur on or after the start of that period. Earlier application is permitted as long as this fact is disclosed.

The amendments are not expected to have a material impact on the Group’s Consolidated Financial Statements.

11

Note 2 Summary of significant accounting policies (continued)

2.1 Basis of preparation (continued)

2.1.1 Changes in accounting policy and disclosure (continued)

2.1.1.2 Standards issued but not yet effective (continued)

Disclosure of Accounting Policies - Amendments to IAS 1 and IFRS Practice Statement 2

In February 2021, the IASB issued amendments to IAS 1 and IFRS Practice Statement 2 Making Materiality Judgements, in which it provides guidance and examples to help entities apply materiality judgements to accounting policy disclosures. The amendments aim to help entities provide accounting policy disclosures that are more useful by replacing the requirement for entities to disclose their ‘significant’ accounting policies with a requirement to disclose their ‘material’ accounting policies and adding guidance on how entities apply the concept of materiality in making decisions about accounting policy disclosures.

The amendments to IAS 1 are applicable for annual periods beginning on or after January 1, 2023 with earlier application permitted. Since the amendments to the Practice Statement 2 provide non-mandatory guidance on the application of the definition of material to accounting policy information, an effective date for these amendments is not necessary.

The Group is currently revisiting their accounting policy information disclosures to ensure consistency with the amended requirements.

2.2 Going concern

The Directors regularly monitor the Group’s cash position and liquidity risks throughout the year to ensure that it has sufficient funds to meet forecasted operational and investment funding requirements. Sensitivities are run to reflect latest expectations of expenditures, oil and gas prices and other factors to enable the Group to manage the risk of any funding short falls and/or potential debt covenant breaches.

Considering the performance of the operations, the Group’s cash position of US$ 128,843,000, the oil hedge strategy to mitigate the price risk exposure within the next twelve months, the deleveraging process executed in 2021 and 2022 (see Note 27), and the fact that its total indebtedness as of December 31, 2022 matures in 2027, the Directors have formed a judgement, at the time of approving the Consolidated Financial Statements, that there is a reasonable expectation that the Group has adequate resources to meet all its obligations for the foreseeable future. For this reason, the Directors have continued to adopt the going concern basis in preparing the Consolidated Financial Statements.

2.3 Consolidation

Subsidiaries are all entities (including structured entities) over which the Group has control. The Group controls an entity when the Group is exposed to, or has rights to, variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity. Subsidiaries are fully consolidated from the date on which control is transferred to the Group. They are deconsolidated from the date that control ceases.

Intercompany transactions, balances and unrealized gains on transactions between the Group and its subsidiaries are eliminated. Unrealized losses are also eliminated unless the transaction provides evidence of an impairment of the asset transferred. Amounts reported in the financial statements of subsidiaries have been adjusted where necessary to ensure consistency with the accounting policies adopted by the Group.

12

Note 2 Summary of significant accounting policies (continued)

2.4 Segment reporting

Operating segments are reported in a manner consistent with the internal reporting provided to the chief operating decision-maker. The chief operating decision-maker, who is responsible for allocating resources and assessing performance of the operating segments, has been identified as the Executive Committee. This committee is integrated by the Chief Executive Officer, Chief Financial Officer, Chief Technical Officer, Chief Operating Officer, Chief Strategy, Sustainability and Legal Officer and Chief People Officer. This committee reviews the Group’s internal reporting in order to assess performance and allocate resources. Management has determined the operating segments based on these reports.

2.5 Foreign currency translation

2.5.1 Functional and presentation currency

The Consolidated Financial Statements are presented in US Dollars, which is the Group’s presentation currency.

Items included in the Consolidated Financial Statements of each of the Group’s entities are measured using the currency of the primary economic environment in which the entity operates (the “functional currency”). The functional currency of Group companies incorporated in Colombia, Chile, Argentina and Ecuador is the US Dollar, meanwhile for the Group´s Brazilian company the functional currency is the local currency, which is the Brazilian Real.

2.5.2 Transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at period-end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognized in the Consolidated Statement of Income.

The results and financial position of foreign operations that have a functional currency different from the presentation currency are translated into the presentation currency as follows: assets and liabilities are translated at the closing rate, and income and expenses are translated at average exchange rates. All resulting exchange differences are recognized in Other comprehensive income.

2.6 Joint arrangements

Under IFRS 11, investments in joint arrangements are classified as either joint operations or joint ventures depending on the contractual rights and obligations of each investor. The Group has assessed the nature of its joint arrangements and determined them to be joint operations. The Group combines its share in the joint operations individual assets, liabilities, results and cash flows on a line-by-line basis with similar items in its Consolidated Financial Statements.

2.7 Business combinations

Business combinations are accounted for using the acquisition method. The cost of an acquisition is measured as the aggregate of the consideration transferred, which is measured at the acquisition date fair value, and the amount of any non-controlling interests in the acquiree. For each business combination, the Group elects whether to measure the non-controlling interests in the acquiree at fair value or at the proportionate share of the acquiree’s identifiable net assets. Acquisition-related costs are expensed as incurred and included in administrative expenses.

The Group determines that it has acquired a business when the acquired set of activities and assets include an input and a substantive process that together significantly contribute to the ability to create outputs. The acquired process is considered substantive if it is critical to the ability to continue producing outputs, and the inputs acquired include an organized workforce with the necessary skills, knowledge, or experience to perform that process or it significantly contributes to the ability to continue producing outputs and is considered unique or scarce or cannot be replaced without significant cost, effort, or delay in the ability to continue producing outputs.

13

Note 2 Summary of significant accounting policies (continued)

2.7 Business combinations (continued)

When the Group acquires a business, it assesses the financial assets and liabilities assumed for appropriate classification and designation in accordance with the contractual terms, economic circumstances and pertinent conditions as at the acquisition date. This includes the separation of embedded derivatives in host contracts by the acquiree.

Any contingent consideration to be transferred by the acquirer will be recognized at fair value at the acquisition date. Contingent consideration classified as equity is not remeasured and its subsequent settlement is accounted for within equity. Contingent consideration classified as an asset or liability that is a financial instrument and within the scope of IFRS 9 Financial Instruments, is measured at fair value with the changes in fair value recognized in the statement of profit or loss in accordance with IFRS 9. Other contingent consideration that is not within the scope of IFRS 9 is measured at fair value at each reporting date with changes in fair value recognized in profit or loss.

Goodwill is initially measured at cost (being the excess of the aggregate of the consideration transferred and the amount recognized for non-controlling interests and any previous interest held over the net identifiable assets acquired and liabilities assumed). If the fair value of the net assets acquired is in excess of the aggregate consideration transferred, the Group re-assesses whether it has correctly identified all of the assets acquired and all of the liabilities assumed and reviews the procedures used to measure the amounts to be recognized at the acquisition date. If the reassessment still results in an excess of the fair value of net assets acquired over the aggregate consideration transferred, then the gain is recognized in profit or loss.

Revenue from the sale of crude oil and gas is recognized at the point in time when control of the product is transferred to the customer, which is generally when the product is physically transferred into a pipe or other delivery mechanism and the customer accepts the product. Consequently, the Group’s performance obligations are considered to relate only to the sale of crude oil and gas, with each barrel of crude oil equivalent considered to be a separate performance obligation under the contractual arrangements in place.

The Group’s sales of crude oil are priced based on market prices. The sales price is linked to US dollar denominated crude oil international benchmarks, such as Brent, adjusted for certain marketing and quality discounts based on, among other things, American Petroleum Institute (“API”) gravity, viscosity, sulphur content, delivery point and transport costs. The Group’s sales of natural gas are priced based on long-term Gas Supply contracts with customers.

Revenue is shown net of VAT, discounts related to the sale and overriding royalties due to the ex-owners of oil and gas properties where the royalty arrangements represent a retained working interest in the property. See Note 33.1.

2.9 Production and operating costs

Production and operating costs are recognized in the Consolidated Statement of Income on the accrual basis of accounting. These costs include wages and salaries incurred to achieve the revenue for the year. Direct and indirect costs of raw materials and consumables, rentals, and royalties are also included within this account.

2.10 Financial results

Financial results include interest expenses, interest income, bank charges, the amortization of financial assets and liabilities, and foreign exchange gains and losses. The Group has capitalized the borrowing cost directly attributable to wells and facilities identified as qualifying assets, if applicable. Qualifying assets are assets that necessarily take a substantial period of time to get ready for their intended use or sale. The capitalization rate used to determine the amount of borrowing costs to be capitalized, if any, is the weighted average interest rate applicable to the Group’s general borrowings.

14

Note 2 Summary of significant accounting policies (continued)

2.11 Property, plant and equipment

Property, plant and equipment are stated at historical cost less depreciation and impairment charges, if applicable. Historical cost includes expenditure that is directly attributable to the acquisition of the items; including provisions for asset retirement obligation.

Oil and gas exploration and production activities are accounted for in accordance with the successful efforts method on a field by field basis. The Group accounts for exploration and evaluation activities in accordance with IFRS 6, Exploration for and Evaluation of Mineral Resources, capitalizing exploration and evaluation costs until such time as the economic viability of producing the underlying resources is determined. Costs incurred prior to obtaining legal rights to explore are expensed immediately to the Consolidated Statement of Income.

Exploration and evaluation costs may include: license acquisition, geological and geophysical studies (i.e.: seismic), direct labor costs and drilling costs of exploratory wells. No depreciation and/or amortization are charged during the exploration and evaluation phase. Upon completion of the evaluation phase, the prospects are either transferred to oil and gas properties or charged to expense (exploration costs) in the period in which the determination is made, depending whether they have discovered reserves or not. If not developed, exploration and evaluation assets are written off after three years, unless it can be clearly demonstrated that the carrying value of the investment is recoverable.

A charge of US$ 25,789,000 has been recognized in the Consolidated Statement of Income within Write-off of unsuccessful exploration efforts (US$ 12,262,000 in 2021 and US$ 52,652,000 in 2020). See Note 20.

All field development costs are considered construction in progress until they are finished and capitalized within oil and gas properties, and are subject to depreciation once completed. Such costs may include the acquisition and installation of production facilities, development drilling costs (including dry holes, service wells and seismic surveys for development purposes), project-related engineering and the acquisition costs of rights and concessions related to proved properties.

Workovers of wells made to develop reserves and/or increase production are capitalized as development costs. Maintenance costs are charged to the Consolidated Statement of Income when incurred.

Capitalized costs of proved oil and gas properties and production facilities and machinery are depreciated on a licensed area by the licensed area basis, using the unit of production method, based on commercial proved and probable oil and gas reserves. The calculation of the “unit of production” depreciation considers estimated future finding and development costs and is based on current year-end unescalated price levels. Changes in reserves and cost estimates are recognized prospectively. Reserves are converted to equivalent units on the basis of approximate relative energy content.

Depreciation of the remaining property, plant and equipment assets (i.e. furniture and vehicles) not directly associated with oil and gas activities has been calculated by means of the straight-line method by applying such annual rates as required to write-off their value at the end of their estimated useful lives. The useful lives range between 3 years and 10 years.

Depreciation is allocated in the Consolidated Statement of Income as a separate line to better follow the performance of the business.

An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount (see Impairment of non-financial assets in Note 2.13).

2.12 Provisions and other long-term liabilities

Provisions for asset retirement obligations and other environmental liabilities, deferred income, restructuring obligations and legal claims are recognized when the Group has a present legal or constructive obligation as a result of past events, it is probable that an outflow of resources will be required to settle the obligation, and the amount has been reliably estimated. Restructuring provisions, if any, comprise lease termination penalties and employee services termination payments.

15

Note 2 Summary of significant accounting policies (continued)

2.12 Provisions and other long-term liabilities (continued)

Provisions are measured at the present value of the expenditures expected to be required to settle the obligation using a pre-tax rate that reflects current market assessments of the time value of money and the risks specific to the obligation. The increase in the provision due to the passage of time is recognized as financial expense.

2.12.1 Asset Retirement Obligation

The Group records the fair value of the liability for asset retirement obligations in the period in which the wells are drilled. When the liability is initially recorded, the Group capitalizes the cost by increasing the carrying amount of the related long-lived asset. Over time, the liability is accreted to its present value at each reporting period, and the capitalized cost is depreciated over the estimated useful life of the related asset. According to interpretations and the application of current legislation, and on the basis of the changes in technology and the variations in the costs of restoration necessary to protect the environment, the Group has considered it appropriate to periodically re-evaluate future costs of well-capping. The effects of this recalculation are included in the Consolidated Financial Statements in the period in which this recalculation is determined and reflected as an adjustment to the provision and the corresponding property, plant and equipment asset.

2.12.2 Deferred Income

Government grants and other contributions relating to the purchase of property, plant and equipment are included in non-current liabilities as deferred income and they are credited to the Consolidated Statement of Income over the expected lives of the related assets. Grants from the government are recognized at their fair value where there is a reasonable assurance that the grant will be received and the Group will comply with all attached conditions.

2.13 Impairment of non-financial assets

Assets that are not subject to depreciation and/or amortization are tested annually for impairment. Assets that are subject to depreciation and/or amortization are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable.

An impairment loss is recognized for the excess of the asset’s carrying amount over its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs to sell and value in use. For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash flows (cash-generating units), generally a licensed area. Non-financial assets other than goodwill that suffered impairment are reviewed for possible reversal of the impairment at each reporting date.

No asset should be kept as an exploration and evaluation asset for a period of more than three years, except if it can be clearly demonstrated that the carrying value of the investment will be recoverable.

During 2022, no impairment losses were recognized or reversed. Net impairment losses were recognized for US$ 4,334,000 and US$ 133,864,000 in 2021 and 2020, respectively. See Note 37. The write-offs are detailed in Note 20.

2.14 Lease contracts

The Group assesses at contract inception whether a contract is, or contains, a lease. That is, if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration.

2.14.1 Right-of-use assets

The Group recognizes right-of-use assets at the commencement date of the lease. Right of use assets are measured at cost, less any accumulated depreciation and impairment losses, an adjusted for any measurement of lease liabilities.

16

Note 2 Summary of significant accounting policies (continued)

2.14 Lease contracts (continued)

2.14.1 Right-of-use assets (continued)

The cost of right-of-use assets comprise the following:

| ● | the amount of the initial measurement of lease liability, |

| ● | any lease payments made at or before the commencement date less any lease incentives received, |

| ● | any initial direct costs, and |

| ● | restoration costs. |

The Group leases various offices, facilities, machinery and equipment. Lease contracts are typically made for fixed periods of 1 to 15 years but may have extension options. Lease terms are negotiated on an individual basis and contain a wide range of different terms and conditions. Right-of-use assets are depreciated on a straight-line basis over the shorter of the lease term and the estimated useful lives of the assets.

If ownership of the leased asset transfers to the Group at the end of the lease term or the cost reflects the exercise of a purchase option, depreciation is calculated using the estimated useful life of the asset. The right-of-use assets are also subject to impairment.

2.14.2 Lease liabilities

At the commencement date of the lease, the Group recognizes lease liabilities measured at the present value of lease payments to be made over the lease term. Lease liabilities include the net present value of the following lease payments:

| ● | fixed payments, less any lease incentives receivable, |

| ● | variable lease payments that are based on an index or a rate, |

| ● | amounts expected to be payable by the lessee under residual value guarantees, |

| ● | the exercise price of a purchase option if the lessee is reasonably certain to exercise that option, and |

| ● | payments of penalties for terminating the lease, if the lease term reflects the lessee exercising that option. |

In calculating the present value, the lease payments are discounted using the interest rate implicit in the lease. If that rate cannot be determined, the Group’s incremental borrowing rate is used, being the rate that the lessee would have to pay to borrow the funds necessary to obtain an asset of similar value in a similar economic environment with similar terms and conditions. After the commencement date, the amount of lease liabilities is increased to reflect the accretion of interest and reduced for the lease payments made. In addition, the carrying amount of lease liabilities is remeasured if there is a modification, a change in the lease term, a change in the lease payments (e.g., changes to future payments resulting from a change in an index or rate used to determine such lease payments) or a change in the assessment of an option to purchase the underlying asset.

2.14.3 Short-term leases and leases of low-value assets

The Group applies the short-term lease recognition exemption to its short-term leases of machinery and equipment (i.e., those leases that have a lease term of 12 months or less from the commencement date and do not contain a purchase option). It also applies the lease of low-value assets recognition exemption to leases of IT equipment and small items of office furniture that are considered to be low value. Lease payments on short-term leases and leases of low-value assets are recognized as expense on a straight-line basis over the lease term.

2.15 Inventories

Inventories comprise crude oil and materials.

Crude oil is measured at the lower of cost and net realizable value. Materials are measured at the lower of cost and recoverable amount. The cost of materials and consumables is calculated at acquisition price with the addition of transportation and similar costs. Cost is determined using the first-in, first-out (FIFO) method.

17

Note 2 Summary of significant accounting policies (continued)

2.16 Current and deferred income tax

The tax expense for the year comprises current and deferred income tax. Income tax is recognized in the Consolidated Statement of Income.

The current income tax charge is calculated on the basis of the tax laws enacted or substantially enacted at the financial statements date in the countries where the Company’s subsidiaries operate and generate taxable income. The computation of the income tax expense involves the interpretation of applicable tax laws and regulations in many jurisdictions. The resolution of tax positions taken by the Group, through negotiations with relevant tax authorities or through litigation, can take several years to complete and, in some cases, it is difficult to predict the ultimate outcome.

Deferred income tax is recognized, using the liability method, on temporary differences arising between the tax bases of assets and liabilities and their carrying amounts in the Consolidated Financial Statements. Deferred income tax is determined using tax rates (and laws) that have been enacted or substantially enacted as of the financial statements date and are expected to apply when the related deferred income tax asset is realized, or the deferred income tax liability is settled.

In addition, the Group has tax-loss carry-forwards in certain tax jurisdictions that are available to be offset against future taxable profit. However, deferred income tax assets are recognized only to the extent that it is probable that taxable profit will be available against which the unused tax losses can be utilized. Management judgment is exercised in assessing whether this is the case. To the extent that actual outcomes differ from management’s estimates, taxation charges or credits may arise in future periods.

Deferred income tax liabilities are provided on taxable temporary differences arising from investments in subsidiaries and joint arrangements, except for deferred income tax liability where the timing of the reversal of the temporary difference is controlled by the Group and it is probable that the temporary difference will not reverse in the foreseeable future. The Group is able to control the timing of dividends from its subsidiaries and hence does not expect taxable profit. Hence deferred income tax is recognized in respect of the retained earnings of overseas subsidiaries only if at the date of the Consolidated Financial Statements, dividends have been accrued as receivable or a binding agreement to distribute past earnings in future has been entered into by the subsidiary. As mentioned above the Group does not expect that the temporary differences will revert in the foreseeable future.

Deferred income tax balances are provided in full, with no discounting.

2.17 Non-current assets or disposal groups held for sale

Non-current assets or disposal groups are classified as held for sale if their carrying amount will be recovered principally through a sale transaction rather than through continuing use and a sale is considered highly probable. They are measured at the lower of their carrying amount and fair value less costs to sell, except for assets such as deferred tax assets, assets arising from employee benefits, financial assets and investment property that are carried at fair value and contractual rights under insurance contracts, which are specifically exempt from this requirement.

An impairment loss is recognized for any initial or subsequent write-down of the asset or disposal group to fair value less costs to sell. A gain is recognized for any subsequent increases in fair value less costs to sell of an asset or disposal group, but not in excess of any cumulative impairment loss previously recognized. A gain or loss not previously recognized by the date of the sale of the non-current asset or disposal group is recognized at the date of derecognition.

Non-current assets (including those that are part of a disposal group) are not depreciated or amortized while they are classified as held for sale. Interest and other expenses attributable to the liabilities of a disposal group classified as held for sale continue to be recognized.

Non-current assets classified as held for sale and the assets of a disposal group classified as held for sale are presented separately from the other assets in the Consolidated Statement of Financial Position. The liabilities of a disposal group classified as held for sale are presented separately from other liabilities in the Consolidated Statement of Financial Position.

18

Note 2 Summary of significant accounting policies (continued)

2.18 Financial assets

Financial assets are divided into the following categories: amortized cost; financial assets at fair value through profit or loss and fair value through other comprehensive income. The classification depends on the Group’s business model for managing the financial assets and the contractual terms of the cash flows. The Group reclassifies debt investments when and only when its business model for managing those assets changes.

All financial assets not at fair value through profit or loss are initially recognized at fair value, plus transaction costs. Transaction costs of financial assets carried at fair value through profit or loss, if any, are expensed to profit or loss.

Derecognition of financial assets occurs when the rights to receive cash flows from the investments expire or are transferred and substantially all of the risks and rewards of ownership have been transferred. An assessment for impairment is undertaken at each balance sheet date.

Interest and other cash flows resulting from holding financial assets are recognized in the Consolidated Statement of Income when receivable, regardless of how the related carrying amount of financial assets is measured.

Amortized cost are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They are included in current assets, except for maturities greater than twelve months after the balance sheet date. These are classified as non-current assets. These financial assets comprise trade and other receivables and cash and cash equivalents in the Consolidated Statement of Financial Position. They arise when the Group provides money, goods or services directly to a debtor with no intention of trading the receivables. These financial assets are subsequently measured at amortized cost using the effective interest method, less provision for impairment, if applicable.

Any change in their value through impairment or reversal of impairment is recognized in the Consolidated Statement of Income. All of the Group’s financial assets are classified as amortized cost.

2.19 Other financial assets

Non-current other financial assets include contributions made for environmental obligations according to a Colombian and Brazilian government request and are restricted for those purposes.

Current other financial assets include short-term investments with original maturities up to twelve months and over three months.

2.20 Impairment of financial assets

The Group assesses on a forward-looking basis the expected credit losses associated with its debt instruments. The impairment methodology applied depends on whether there has been a significant increase in credit risk. For trade receivables, the Group applies the simplified approach permitted by IFRS 9, which requires expected lifetime losses to be recognized from initial recognition of the receivables.

2.21 Cash and cash equivalents

Cash and cash equivalents includes cash in hand, deposits held at call with banks, other short-term highly liquid investments with original maturities of three months or less that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value, and bank overdrafts. Bank overdrafts, if any, are shown within borrowings in the current liabilities section of the Consolidated Statement of Financial Position.

19

Note 2 Summary of significant accounting policies (continued)

2.22 Trade and other payables

Trade payables are obligations to pay for goods or services that have been acquired in the ordinary course of the business from suppliers. Accounts payable are classified as current liabilities if payment is due within one year or less (or in the normal operating cycle of the business if longer). If not, they are presented as non-current liabilities.

Trade payables are recognized initially at fair value and subsequently measured at amortized cost using the effective interest method.

2.23 Derivatives and hedging activities

Derivative financial instruments are recognized in the Consolidated Statement of Financial Position as assets or liabilities and initially and subsequently measured at fair value. They are presented as current assets or liabilities if they are expected to be settled within 12 months after the end of the reporting period.

The mark-to-market fair value of the Group's outstanding derivative instruments is based on independently provided market rates and determined using standard valuation techniques, including the impact of counterparty credit risk and are within level 2 of the fair value hierarchy.

2.23.1 Cash flow hedges that qualify for hedge accounting

The effective portion of changes in the fair value of derivatives that are designated and qualify as cash flow hedges is recognized in Other Reserve within Equity. The gain or loss relating to the ineffective portion is recognized immediately in the Consolidated Statement of Income.

When forward contracts are used to hedge forecast transactions, the Group designates the change in fair value of the forward contract as the hedging instrument. Gains or losses relating to the effective portion of the change in the fair value of the forward contracts are recognized in Other Reserve within Equity.

Where the hedged item subsequently results in the recognition of a non-financial asset, both the deferred hedging gains and losses and the deferred time value of the option contracts or deferred forward points, if any, are included within the initial cost of the asset.

When a hedging instrument expires, or is sold or terminated, or when a hedge no longer meets the criteria for hedge accounting, any cumulative deferred gain or loss and deferred costs of hedging in Equity at that time remains in Equity until the forecast transaction occurs, resulting in the recognition of a non-financial asset. When the forecast transaction is no longer expected to occur, the cumulative gain or loss and deferred costs of hedging that were reported in Equity are immediately reclassified to the Consolidated Statement of Income.

For more information about derivatives designated as cash flow hedges please refer to Note 36.1 and Note 8.

2.23.2 Other Derivatives

Certain derivative instruments do not qualify for hedge accounting. Changes in the fair value of any derivative instrument that does not qualify for hedge accounting are recognized immediately in the Consolidated Statement of Income.

For more information about derivatives related to commodity risk management please refer to Note 8 and for more information about derivatives related to currency risk management please refer to Note 3 Currency risk.

2.24 Borrowings

Borrowings are obligations to pay cash and are recognized when the Group becomes a party to the contractual provisions of the instrument.

20

Note 2 Summary of significant accounting policies (continued)

2.24 Borrowings (continued)

Borrowings are recognized initially at fair value, net of transaction costs incurred. Borrowings are subsequently stated at amortized cost; any difference between the proceeds (net of transaction costs) and the redemption value is recognized in the Consolidated Statement of Income over the period of the borrowings using the effective interest method.

Direct issue costs are charged to the Consolidated Statement of Income on an accrual basis using the effective interest method.

2.25 Share capital

Equity comprises the following:

| ● | "Share capital" representing the nominal value of equity shares. |

| ● | "Share premium" representing the excess over nominal value of the fair value of consideration received for equity shares, net of expenses of the share issuance. |

| ● | "Other reserve" representing: |

| - | the difference between the proceeds from the transaction with non-controlling interests received against the book value of the shares acquired in the Chilean and Colombian subsidiaries, and |

| - | the changes in the fair value of the effective portion of derivatives designated as cash flow hedges. |

| ● | "Translation reserve" representing the differences arising from translation of investments in overseas subsidiaries. |

| ● | "(Accumulated losses) Retained earnings" representing: |

| - | accumulated earnings and losses, and |

| - | the equity element attributable to shares granted according to IFRS 2 but not issued at year end. |

The Group operates a number of equity-settled share-based compensation plans comprising share awards payments to employees and other third-party contractors. Share-based payment transactions are measured in accordance with IFRS 2.

The fair value of the share awards payments is determined at the grant date by reference to the market value of the shares, calculated using the Geometric Brownian Motion method or the Monte Carlo simulation, and recognized as an expense over the vesting period.

Service and non-market performance conditions are not taken into account when determining the grant date fair value of awards, but the likelihood of the conditions being met is assessed as part of the Group’s best estimate of the number of equity instruments that will ultimately vest. Market performance conditions are reflected within the grant date fair value. Any other conditions attached to an award, but without an associated service requirement, are considered to be non-vesting conditions. Non-vesting conditions are reflected in the fair value of an award and lead to an immediate expensing of an award unless there are also service and/or performance conditions.

No expense is recognized for awards that do not ultimately vest because non-market performance and/or service conditions have not been met. Where awards include a market or non-vesting condition, the transactions are treated as vested irrespective of whether the market or non-vesting condition is satisfied, provided that all other performance and/or service conditions are satisfied.

At each reporting date, the entity revises its estimates of the number of options that are expected to vest. It recognizes the impact of the revision to original estimates, if any, in the Consolidated Statement of Income, with a corresponding adjustment to equity.

When the awards are exercised, the Company issues new shares. The proceeds received net of any directly attributable transaction costs are credited to share capital (nominal value) and share premium.

21

Note 3 Financial Instruments-risk management

The Group is exposed through its operations to the following financial risks:

| ● | Currency risk |

| ● | Price risk |

| ● | Credit risk– concentration |

| ● | Funding and liquidity risk |

| ● | Interest rate risk |

| ● | Capital risk |

The policy for managing these risks is set by the Board of Directors. Certain risks are managed centrally, while others are managed locally following guidelines communicated from the corporate department. The policy for each of the above risks is described in more detail below.

Currency risk

In Colombia, Chile, Argentina and Ecuador the functional currency is the US Dollar. The fluctuation of the local currencies of these countries against the US Dollar, except for Ecuador where the local currency is the US Dollar, does not impact the loans, costs and revenue held in US Dollars; but it does impact receivables or payables originated in local currency mainly corresponding to VAT and income tax.

The Group minimises the local currency positions in Colombia, Chile and Argentina by seeking to balance local and foreign currency assets and liabilities. However, tax receivables (VAT) seldom match with local currency liabilities. Therefore, the Group maintains a net exposure to them, except for what it is described below.

Since December 2018, GeoPark decided to manage its future exposure to local currency fluctuation with respect to income tax balances in Colombia. Consequently, from time to time the Group entered into derivative financial instruments in order to anticipate any currency fluctuation with respect to income taxes to be paid during the first half of the following year. As of December 31, 2022 and 2021, there were no currency risk management contracts in place. In 2023, GeoPark entered into derivative financial instruments (zero-premium collars) with local banks in Colombia, for an amount equivalent to US$ 38,000,000, in order to anticipate any currency fluctuation with respect to a portion of the estimated income taxes to be paid in April and June 2023.

Most of the Group's assets held in those countries are associated with oil and gas productive assets. Those assets, even in the local markets, are generally settled in US Dollar equivalents.

During 2022, the Colombian Peso devalued by 21% (16% and 5% in 2021 and 2020, respectively) and the Chilean Peso devalued by 1% (devalued by 19% in 2021 and revalued by 5% in 2020), both against the US Dollar.

If the Colombian Peso and the Chilean Peso had each devalued an additional 10% against the US dollar, with all other variables held constant, post-tax profit for the year would have been higher by US$ 14,695,000 (post-tax profit would have been higher by US$ 9,070,000 in 2021 and post-tax loss would have been lower by US$ 9,057,000 in 2020).

In Brazil, the functional currency is the local currency, which is the Brazilian Real. The fluctuation of the US Dollars against the Brazilian Real does not impact the loans, costs and revenues held in Brazilian Real; but it does impact the balances denominated in US Dollars. Such is the case of the provision for asset retirement obligation and the lease liabilities.

22

Note 3 Financial Instruments-risk management (continued)

Currency risk (continued)

During 2022, the Brazilian Real revalued by 7% against the US Dollar (devalued by 7% and 29% in 2021 and 2020, respectively). If the Brazilian Real had devalued an additional 10% against the US dollar, with all other variables held constant, post-tax profit for the year would have been lower by US$ 726,000 (post-tax profit would have been lower by US$ 780,000 in 2021 and post-tax loss would have been higher by US$ 909,000 in 2020).

As currency rate changes between the US Dollar and the local currencies, the Group recognizes gains and losses in the Consolidated Statement of Income.

Price risk

The realized oil price for the Group is linked to US dollar denominated crude oil international benchmarks. The market price of this commodity is subject to significant volatility and has historically fluctuated widely in response to relatively minor changes in the global supply and demand for oil, the geopolitical landscape, armed conflicts, the economic conditions and a variety of additional factors. The main factors affecting realized prices for gas sales vary across countries with some closely linked to international references while others are more domestically driven.

In Colombia, the realized oil price is linked to either the Vasconia crude reference price, a marker broadly used in the Llanos Basin, or the Oriente crude reference price, a marker broadly used for crude sales in Esmeraldas, Ecuador, for the crude oil of the Putumayo Basin that is transported through Ecuador. In both basins, the reference price is then adjusted for certain marketing and quality discounts based on, among other things, API, viscosity, sulphur content, delivery point and transport costs.

In Chile, the oil price is linked to Dated Brent minus certain marketing and quality discounts such as, API, sulphur content and others.

GeoPark has signed a long-term Gas Supply Contract with Methanex in Chile. The price of the gas sold under this contract is determined by a formula that considers a basket of international methanol prices, including US and European price indices.

In Brazil, prices for gas produced in the Manati Field are based on a long-term off-take contract with Petrobras. The price of gas sold under this contract is denominated in Brazilian Real and is adjusted annually for inflation pursuant to the Brazilian General Market Price Index (Indice Geral de Preços do Mercado), or IGPM.

In Ecuador, the oil price is linked to Brent and adjusted by a differential that varies month to month and resembles Oriente crude reference.

23

Note 3 Financial Instruments-risk management (continued)

Price risk (continued)

If oil and methanol prices had fallen by 10% compared to actual prices during the year, with all other variables held constant, considering the impact of the derivative contracts in place, post-tax profit for the year would have been lower by US$ 47,330,000 (post-tax profit would have been lower by US$ 17,899,000 in 2021 and post-tax loss would have been higher by US$ 21,014,000 in 2020).

GeoPark manages part of the exposure to crude oil price volatility using derivatives. The Group considers these derivative contracts to be an effective manner of properly managing commodity price risk. The price risk management activities mainly employ combinations of options and key parameters are based on forecasted production and budget price levels. GeoPark has also obtained credit lines from industry leading counterparties to minimize the potential cash exposure of the derivative contracts (see Note 8).

Credit risk– concentration

The Group’s credit risk relates mainly to accounts receivable where the credit risks correspond to the recognized values of commodities sold or hedged. GeoPark considers that there is no significant risk associated to the Group’s major customers and hedging counterparties.

In Colombia, GeoPark allocates its sales on a competitive basis to industry leading participants including traders and other producers. During 2022, the oil and gas production was sold to three clients which concentrate 97% of the Colombian subsidiaries’ revenue, accounting for 90% of the consolidated revenue (99% and 98% of the Colombian subsidiaries’ revenue, accounting for 89% and 83% of the consolidated revenue in 2021 and 2020). Delivery points include wellhead and other locations on the Colombian pipeline system for the Llanos Basin production. The Putumayo Basin production is delivered to clients FOB in Esmeraldas, Ecuador, and to the Colombian pipeline system in case of contingencies in Ecuador that affect the transport through the Ecuadorian pipeline system. The outstanding contracts for Colombian production extend through the first half of 2023. GeoPark manages its counterparty credit risk associated to sales contracts by periodic evaluation of the counterparties’ credit profile and, in certain contracts, including early payment conditions to minimize the exposure.

In Chile, the oil production is sold to ENAP, the State-owned oil and gas company (1% of the consolidated revenue in 2022, 2021 and 2020), and the gas production is sold to the local subsidiary of Methanex, a Canadian public company (1% of the consolidated revenue in 2022, 2% in 2021 and 4% in 2020).

In Brazil, all the hydrocarbons from Manati Field are sold to Petrobras, the State-owned company, which is the operator of the Manati Field (2% of the consolidated revenue in 2022, 3% in 2021 and 2020).