Exhibit 99.2

KAH Hospice Company-Personal Care

(A carve-out business of KAH Hospice Company, Inc.)

Condensed Combined Financial Statements for the Nine Months Ended September 30, 2024 (Unaudited)

KAH Hospice company-PERSONAL CARE

Index

Page

kAh hospice company-Personal CARE

condensed COMBINED STATEMENT OF OPERATIONS (unaudited)

(In thousands)

See Accompanying Notes to Unaudited Combined Financial Statements.

2

kAh hospice company-Personal CARE

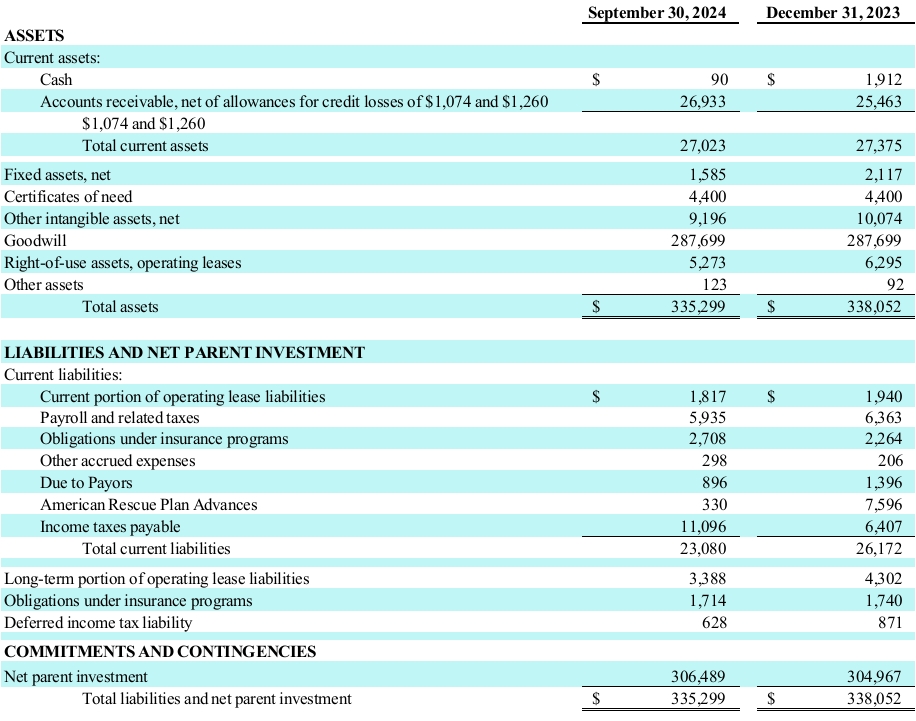

condensed COMBINED balance sheets (unaudited)

(In thousands)

See Accompanying Notes to Unaudited Combined Financial Statements.

3

kah hospice company-Personal CARE

condensed COMBINED statement of NET PARENT INVESTMENT (unaudited)

for the nine months ended September 30, 2024

(In thousands)

See Accompanying Notes to Unaudited Combined Financial Statements.

4

Kah hospice company-Personal care

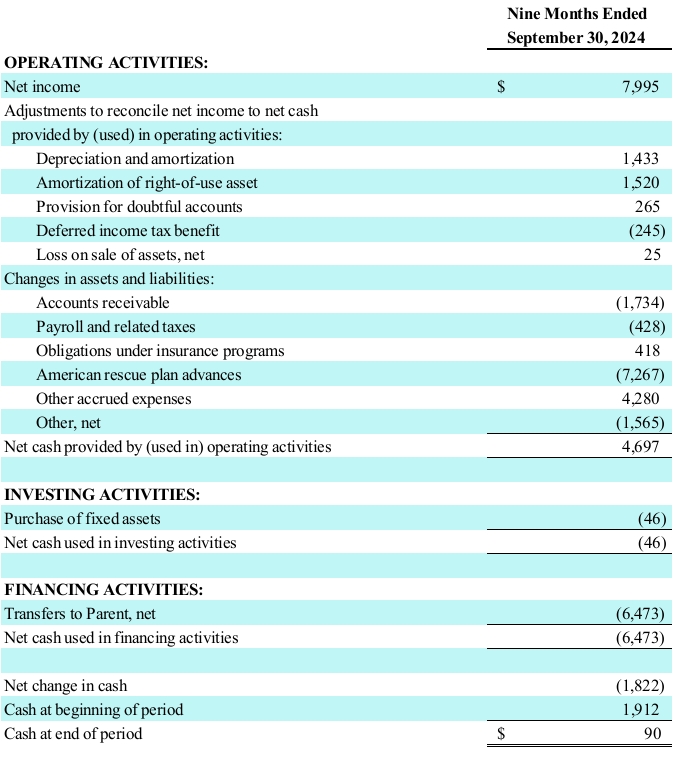

condensed COMBINED Statement of CASH FLOWS (unaudited)

(In thousands)

See Accompanying Notes to Unaudited Combined Financial Statements.

5

kah hospice company-Personal care

Notes to condensed COMBINED financial statements

Note 1. Basis of Presentation

Reporting Entity

KAH Hospice Company-Personal Care (“the Company”) is an operating division of KAH Hospice Company, Inc. (“KAH”) The division provides personal care services for patients in a variety of settings, including their homes, nursing centers, and other residential settings. The Company provides services in 48 locations in 7 states as of September 30, 2024.

On August 11, 2022, Clayton, Dubilier & Rice (“CD&R”) purchased 60% of the Equity interests of KAH from Humana, Inc. Previously, Humana owned 100% of the equity interests of KAH.

On June 8, 2024, Curo Health Services, LLC (“Curo”), a subsidiary of KAH, entered into a Stock and Asset Purchase Agreement with Addus Healthcare, Inc. Under the terms of the agreement, Curo sold the Company as defined as all of the outstanding equity interests in wholly owned subsidiaries of IntegraCare of Abilene, LLC, NP Plus, LLC, Girling Health Care Services of Knoxville, Inc. and Girling Health Care, Inc. as well as, certain assets relating to the personal care business from its wholly owned subsidiaries Central Arizona Home Health Care, Inc., Community Home Care & Hospice, LLC, TNMO Healthcare, LLC and Odyssey HealthCare Operating A, LP. Together, the outstanding equity interests and assets of the Company were purchased for $350 million. The transaction is expected to close in late 2024.

Principles of combination

The accompanying unaudited condensed combined financial statements of the Company and its subsidiaries and the notes thereto presented in this report have been prepared in accordance with the rules applicable to interim financial statements, and do not include all disclosures required by accounting principles generally accepted in the United States of America (“GAAP”) for annual financial statements. In the opinion of the Company, the accompanying unaudited condensed financial statements contain all adjustments, consisting of only normal recurring adjustments, necessary for a fair statement of its financial position as of September 30, 2024, and its results of operations and cash flows for the nine months ended September 30, 2024. The condensed balance sheet at December 31, 2023 was derived from audited annual financial statements but does not contain all of the footnote disclosures from the annual financial statements. Results for the periods ended September 30, 2024 are not necessarily indicative of the results to be experienced for the year ending December 31, 2024. These financial statements are prepared on the same basis as and should be read in conjunction with the Company’s audited combined financial statements and related notes for the year ended December 31, 2023.

The accompanying condensed combined financial statements of the Company and its subsidiaries have been derived from the combined financial statements and accounting records of KAH as if the Company had operated on a stand-alone basis during the periods presented and were prepared utilizing the management approach, in accordance with generally accepted accounting principles in the United States of America (“GAAP”).

The income tax amounts in these combined financial statements have been calculated based on a separate return

methodology and are presented as if the Company’s income gave rise to separate federal and state consolidated income tax return filing obligations in the respective jurisdictions in which it operates. In addition to various separate state and local income tax filings, the Company joins with KAH in various U.S. federal, state and local consolidated income tax filings.

The condensed combined financial statements include an allocation of expenses related to certain KAH corporate functions as discussed in Note 4. The condensed combined financial statements also include revenues and expenses directly attributable to the Company and assets and liabilities specifically attributable to the Company. KAH’s third-party debt and related interest expense have not been attributed to the Company, because the Company is not the primary legal obligor of the debt and the borrowings are not specifically identifiable to the Company. The entities combined in these financial statements were part of KAH’s Collateral and Guarantee Requirement agreement pursuant to which the Company agreed, jointly and severally, fully and unconditionally to guarantee all of KAH’s obligations under the credit agreement. Additionally, the Company is part of KAH’s security agreement, pursuant to which a first-priority security interest was granted in substantially all present and future real, personal and intangible assets, including the

6

kah hospice company-Personal care

Notes to condensed COMBINED financial statements (Continued)

pledge of 100 percent of all outstanding capital stock of the Company’s subsidiaries to secure full payment of the obligations for the ratable benefit of the lenders. Net parent investment represents the Company’s cumulative earnings as adjusted for cash distributions and cash contributions from its parent.

The Company eliminates all intercompany transactions within the Company from its financial results. Transactions between the Company and KAH have been included in these condensed combined financial statements. The transfers with KAH that are not expected to be settled are reflected in net parent investment on the condensed combined balance sheets and condensed combined statement of net parent investment. Within the condensed combined statement of cash flow, these transfers are treated as an operating, financing or noncash activity determined by the nature of the transactions. Transactions between the Company and KAH or between the Company and Humana are considered related party transactions. Refer to Note 4 for more information regarding related party transactions.

Recently issued accounting requirements

In December 2023, the FASB issued ASU 2023-09, Improvement to Income Tax Disclosures, which requires disclosure of disaggregated income taxes paid, prescribes standard categories for the components of the effective tax rate reconciliation, and modifies other income tax-related disclosures. ASU 2023-09 is effective for fiscal years beginning after December 15, 2024, may be applied prospectively or retrospectively, and allows for early adoption. These requirements are not expected to have an impact on the Company’s financial statements and will expand income tax disclosures.

In November 2024, the FASB issued ASU No. 2024-03 ("ASU 2024-03"), Income Statement - Reporting Comprehensive Income - Expense Disaggregation Disclosures (Subtopic 220-40): Disaggregation of Income Statement Expenses, which is intended to improve disclosures about a public business entity's expenses, primarily through additional disaggregation of income statement expenses. ASU 2024-03 is effective for annual periods beginning after December 15, 2026, and interim periods beginning after December 15, 2027, with early adoption permitted. The amendments in ASU 2024-03 should be applied either prospectively to financial statements issued for reporting periods after the effective date or retrospectively to any or all prior periods presented in the financial statements. The Company is currently evaluating the ASU to determine the impact on the Company's disclosures.

Summary of significant accounting policies

Use of estimates

The preparation of the financial statements in conformity with GAAP requires the use of estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting periods. Significant estimates and assumptions are used for, but not limited to: (1) revenue reserves for contractual adjustments and uncollectible amounts; (2) fair value of acquired assets and assumed liabilities in business combinations; (3) asset impairments, including goodwill; (4) corporate allocations. Future events and their effects cannot be predicted with certainty; accordingly, the Company’s accounting estimates require the exercise of judgment. The accounting estimates used in the preparation of the financial statements will change as new events occur, as more experience is acquired, as additional information is obtained, and as the operating environment changes. The Company evaluates and updates its assumptions and estimates on an ongoing basis and may employ outside experts to assist in its evaluation, as considered necessary. Actual results could differ from those estimates.

Revenues

Net revenue from contracts with customers is recognized in the period in which the performance obligations are satisfied under the Company’s contracts by transferring the requested services to patients in amounts that reflect the consideration which is expected to be received in exchange for providing patient care, which is the transaction price allocated to the services provided in accordance with Accounting Standards Codification (“ASC”) 606, Revenue from Contracts with Customers, and all of the related amendments. Net revenue is recognized as performance obligations are satisfied, which can vary depending on the type of services provided. The performance obligation is the delivery of patient care in accordance with the requested services outlined in physicians’ orders or state program referrals, which are based on the specific needs of each patient.

7

kah hospice company-Personal care

Notes to condensed COMBINED financial statements (Continued)

The performance obligations are associated with contracts in duration of less than one year; therefore, the optional exemption provided by ASC 606 was elected resulting in the Company not being required to disclose the aggregate amount of the transaction price allocated to the performance obligations that are unsatisfied or partially unsatisfied as of the end of the reporting period.

The Company determines the transaction price based on gross charges for services provided, reduced by estimates for explicit and implicit price concessions. The Company’s estimates of contractual adjustments and uncollectible amounts require the exercise of judgment. Explicit price concessions include contractual adjustments provided to various payers. They are recorded for the difference between the Company’s standard rates and the contracted rates to be realized from patients and third-party payers. Implicit price concessions include discounts provided to self-pay, uninsured patients or other payers, adjustments resulting from regulatory reviews, audits, billing reviews and other matters and are estimated by the Company based on historical collection experience and success rates in the claim appeals and adjudication process. The Company assesses the ability to collect for the services provided at the time of patient admission based on the verification of the patient’s insurance coverage under Medicaid, commercial insurance and other payers. Subsequent changes to the estimate of the transaction price are recorded as adjustments to net revenue in the period of change. Subsequent changes that are determined to be the result of an adverse change in the patient’s ability to pay (i.e. change in credit risk) are recorded as a provision for doubtful accounts within selling, general and administrative expenses.

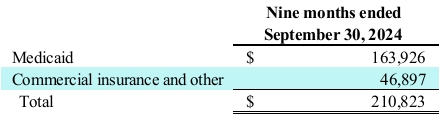

A summary of revenue by payer type follows (in thousands):

Sources of net revenue fall into Medicaid, commercial insurance, and other payers. Reimbursement is based on each payer’s predetermined fee schedule applied to each service provided. Revenue is therefore recognized as services are provided based on these various fee schedules.

Deferred Revenue

The American Rescue Plan Act of 2021 (“ARPA”) is a relief package with numerous provisions that affect healthcare providers and was signed into law in March 2021. ARPA provides for relief funding for eligible state, local, territorial, and Tribal governments to mitigate the fiscal effects of the COVID-19 public health emergency. Additionally, the law provides for a 10-percentage point increase in federal matching funds for Medicaid home and community-based services (“HCBS”) from April 1, 2021, through March 31, 2022, provided the state satisfied certain conditions. States are permitted to use the state funds equivalent to the additional federal funds through March 31, 2025. States must use the monies attributable to this matching fund increase to supplement, not supplant, their level of state spending for the implementation of activities enhanced under the Medicaid HCBS in effect as of April 1, 2021.

HCBS spending plans for the additional matching funds vary by state, but common initiatives in which the Company is participating include those aimed at strengthening the provider workforce (e.g. efforts to recruit and retain direct service providers). The Company is required to properly and fully document the use of such funds in reports to the state in which the funds originated. Funds may be subject to recoupment if not expended or if they are expended on non-approved uses. In total, the Company received state funding provided by ARPA in aggregate amount of $25.1 million. During the nine months ended September 30, 2024, the Company recorded revenue of $7.3 million and related costs of services sold of approximately $6.7 million. As of September 30, 2024 and December 31, 2023, the deferred portion of ARPA funding was $0.3 million and $7.6 million, respectively, and is reflected on the condensed combined balance sheet.

8

kah hospice company-Personal care

Notes to condensed COMBINED financial statements (Continued)

Accounts receivable

Accounts receivable consist primarily of amounts due from the Medicaid program, other government programs, managed care health plans, commercial insurance companies and individual patients. Accounts receivable from services rendered are reported at their estimated transaction price which takes into account price concessions from the various payers. The concentration of accounts receivable by payer class as a percentage of total net accounts receivable is as follows:

While revenues and accounts receivable from the Medicaid program are significant to its operations, the Company does not believe there are significant credit risks associated with this government agency. The Company does not believe there are any other significant concentrations of revenues from any particular payer that would subject us to any significant credit risks in the collection of accounts receivable.

Accounts requiring collection efforts are reviewed by patient account representatives, who employ various collection efforts, including contacting the applicable parties, providing financial or clinical information to allow for payment or to overturn payer decisions to deny payment, and arranging payment plans, among other techniques. When in-house efforts are exhausted or it is a more prudent use of resources, commercial insurance and other accounts may be turned over to a collection agency.

The collection of outstanding receivables from Medicaid is the Company’s primary source of cash and is critical to its operating performance. While it is the Company’s policy to verify eligibility for these programs prior to a patient being admitted, there are some circumstances in which that verification by the payer may take some period of time.

If actual results are not consistent with the Company’s assumptions and judgments, the Company may be exposed to gains or losses that could be material. Changes in general economic conditions, federal or state governmental programs, payer mix or business office operations could affect the Company’s collection of accounts receivable, financial position, results of operation and cash flows.

Allocated expense

Amounts were allocated from KAH for costs attributable to the operations of the Company. The expenses incurred by KAH include costs from certain support center and shared service functions provided by KAH to the Company.

All support center costs that were specifically identifiable to the Company have been allocated to the Company and are included in the accompanying condensed combined statement of operations. The results of operations for the Company include allocations for certain support functions that were previously provided on a centralized basis by KAH to all or part of the Company, including cash management, information technology services, accounts receivable oversight, property and equipment record keeping, accounts payable processing, payroll and general bookkeeping. Additionally, KAH manages general business functions on behalf of the Company, including human resources, financial reporting and legal services. KAH refers to these expenses as support center allocations and, where specific identification of charges attributable to the Company was not practicable, such costs have been allocated based on a percentage of net revenues.

In the opinion of management, the cost allocations have been determined on a reasonable basis and include all the costs of doing business. The amounts that would have been or will be incurred on a stand-alone basis could differ from the amounts allocated due to economies of scale, management judgment, or other factors. See Note 4 for additional information regarding related party transactions.

9

kah hospice company-Personal care

Notes to condensed COMBINED financial statements (Continued)

Note 2. Income Taxes

The Company’s effective tax rate for the nine months ended September 30, 2024 was 19.9%. For the nine months ended September 30, 2024, the effective tax rate was lower than the U.S. federal statutory rate of 21.0% primarily due to the Company’s qualifying for available Work Opportunity Tax Credits.

Federal and state tax expense included in the condensed consolidated statement of operations was $2.0 million for the nine months ended September 30, 2024.

Note 3. Commitments and Contingencies

Management continually evaluates contingencies based upon the best available information. In addition, allowances for losses are provided currently for disputed items that have continuing significance, such as certain third-party reimbursements and tax returns.

Management believes that allowances for losses have been provided to the extent necessary and that its assessment of contingencies is reasonable. Principal contingencies are described below:

Revenues

Certain third-party payments are subject to examination by agencies administering the various reimbursement programs. The Company is contesting the denial of certain payments by third parties to the Company’s customers.

Legal and regulatory proceedings

From time to time, the Company is subject to legal and/or administrative proceedings incidental to its business. It is the opinion of management that the outcome of pending legal and/or administrative proceedings will not have a material effect on the Company’s combined balance sheets and combined statement of operations.

Obligations Under Insurance Programs

The Company is obligated for certain costs under various insurance programs maintained by KAH, including workers’ compensation, professional liability, property and general liability, and employee health and welfare.

The Company may be subject to workers’ compensation claims and lawsuits alleging negligence or other similar legal claims. KAH and Humana maintain various insurance programs to cover this risk with insurance policies subject to substantial deductibles and retention amounts. The Company recognizes its obligations associated with these programs in the period the claim is incurred. The cost of both reported claims and claims incurred but not reported, up to specified deductible limits, have generally been estimated based on historical data, industry statistics, the Company’s specific historical claims experience, current enrollment statistics and other information. The Company’s estimates of its obligations and the resulting reserves are reviewed and updated from time to time, but at least quarterly. The elements which impact this critical estimate include the number, type and severity of claims and the policy deductible limits; therefore, the estimate is sensitive and changes in the estimate could have a material impact on the Company’s condensed combined financial statements.

The Company’s workers’ compensation and professional and general liability costs under these programs were $1.4 million in the nine months ended September 30, 2024. Workers’ compensation and professional liability claims, including any changes in estimate relating thereto, are recorded primarily in cost of services sold in the Company’s condensed combined statement of operations.

KAH maintains insurance coverage on individual claims under these programs and are responsible for the cost of individual workers’ compensation claims and individual professional liability claims up to policy deductibles occurrence. KAH also maintain excess liability coverage relating to professional liability and casualty claims. Payments under KAH’s workers’ compensation program are guaranteed by letters of credit. The Company records its share of costs under these programs. The Company believes that its present insurance coverage and reserves are sufficient to cover

10

kah hospice company-Personal care

Notes to condensed COMBINED financial statements (Continued)

currently estimated exposures, but there can be no assurance that the Company will not incur liabilities in excess of recorded reserves or in excess of its insurance limits.

The Company provides employee health and welfare benefits under a self-insured program maintained by KAH. Employee health and welfare benefit costs were $2.4 million for the nine months ended September 30, 2024. Changes in estimates of the Company’s employee health and welfare claims are recorded in cost of services sold for clinical associates and in selling, general and administrative costs for administrative associates in the Company’s statement of operations.

Note 4. Related Party Transactions

Support center allocations

The results of operations for the Company include allocations for certain support functions that were provided all or in part on a centralized basis by KAH, including cash management, information services support, accounts receivable processing, property and equipment record keeping, accounts payable processing, payroll and general bookkeeping. Additionally, KAH manages general business functions on behalf of the Company, including human resources, financial reporting and legal services. KAH refers to these expenses as support center allocations and they have been allocated based on a percentage of net revenues. The total allocated selling, general and administrative charges for the nine months ended September 30, 2024 was $13.0 million.

Debt and intercompany interest

The carve-out condensed combined balance sheets do not include any third-party debt held by KAH and the condensed combined statement of operations do not include any interest expense associated with the third-party debt held by KAH.

Employee benefits

The Company participates in defined contribution retirement plans sponsored by KAH covering employees who meet certain minimum eligibility requirements. Benefits are determined as a percentage of a participant’s contributions and generally are vested based upon length of service. Retirement plan expense for the Company was $0.4 million for the nine months ended September 30, 2024. Amounts equal to retirement plan expense are funded annually.

Other intercompany balances

Transactions between the Company and KAH or between the Company and Humana have been included in these condensed combined financial statements. The transfers with KAH that are not expected to be settled, are reflected in net parent investment in the condensed combined balance sheets and condensed combined statement of net parent investment. The net parent investment at September 30, 2024 and December 31, 2023 was $306.5 million and $305.0 million, respectively. Within the condensed combined statement of cash flows, these transfers are treated as financing activities. Transactions between the Company and KAH or between the Company and Humana are considered related party transactions.

Note 5. Subsequent Events

The Company has evaluated subsequent events from September 30, 2024 through February 14, 2025, the date at which the condensed combined financial statements were available for issuance. On December 2, 2024 Addus Homecare Corporation completed the acquisition of the Company for $350 million which was funded through a combination of cash on hand and its existing revolving credit facility.

11