UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FormN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number811-22321

MAINSTAY FUNDS TRUST

(Exact name of Registrant as specified in charter)

51 Madison Avenue, New York, NY 10010

(Address of principal executive offices) (Zip code)

J. Kevin Gao, Esq.

30 Hudson Street

Jersey City, New Jersey 070302

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212)576-7000

Date of fiscal year end: April 30

(MainStay MacKay Short Term Municipal Fund)

Date of reporting period: April 30, 2019

FORMN-CSR

Item 1. Reports to Stockholders.

MainStay MacKay Short Term Municipal Fund

(Formerly known as MainStay MacKay Tax Advantaged Short Term Bond Fund)

Message from the President and Annual Report

April 30, 2019

Beginning on January 1, 2021, paper copies of each MainStay Fund’s annual and semiannual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from MainStay Funds or from your financial intermediary. Instead, the reports will be made available on the MainStay Funds’ website. You will be notified by mail and provided with a website address to access the report each time a new report is posted to the website.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. At any time, you may elect to receive reports and other communications from MainStay Funds electronically by calling toll-free 800-624-6782, by sending an e-mail to MainStayShareholderServices@nylim.com, or by contacting your financial intermediary.

You may elect to receive all future shareholder reports in paper form free of charge. If you hold shares of a MainStay Fund directly, you can inform MainStay Funds that you wish to receive paper copies of reports by calling toll-free 800-624-6782 or by sending an e-mail to MainStayShareholderServices@nylim.com. If you hold shares of a MainStay Fund through a financial intermediary, please contact the financial intermediary to make this election. Your election to receive reports in paper form will apply to all MainStay Funds in which you are invested and may apply to all funds held with your financial intermediary.

| Not FDIC/NCUA Insured | Not a Deposit | May Lose Value | No Bank Guarantee | Not Insured by Any Government Agency | ||||

This page intentionally left blank

Message from the President

Despite volatile market conditions, stocks and bonds in the United States and around the world generally gained ground during the12-month period ended April 30, 2019.

The reporting period began on a positive note with strong U.S. economic expansion and moderate levels of growth in much of the developed world, accompanied by historically low interest rates and restrained inflation. However, high equity valuations, particularly in the information technology sector, drove equity and fixed-income markets lower in October 2018. The prospect of rising interest rates, as the U.S. Federal Reserve Board (Fed) gradually hiked its benchmark, further added to this decline. Markets plunged further in early December 2018 in response to concerns that the Fed was raising rates too aggressively and that trade conflicts between the U.S. and China could prove more difficult to resolve than previously expected.

Market sentiment turned positive in the last week of December 2018 after the Fed indicated that additional rate hikes were put on hold, positioning financial markets to bounce back quickly in 2019. Investors overlooked ongoing concerns regarding mounting trade tensions between the U.S. and China and an increasingly unclear global economic picture, focusing instead on continued U.S. economic growth, low unemployment, restrained inflation and better than expected corporate earnings. By April 30, 2019, most U.S.-based equity and fixed-income sectors climbed back into positive territory, with some areas of the domestic market recording impressive gains. International markets showed signs of recovery as well, though generally less robust than in the United States.

Among U.S. equities,large-cap stocks tended to outperform their smaller-caps counterparts, while growth stocks generally outperformed value-oriented issues. Among industry sectors, information technology led the market’s advance, followed by consumer discretionary, communications services, industrials and materials. Of the market’s 11 sectors, only energy ended the reporting period in mildly negative territory, largely due to declining oil and gas prices. Health care also significantly underperformed the broader market largely due to uncertainties regarding potential regulatory changes.

Not surprisingly, traditionally less volatile U.S. fixed-income instruments traded in a narrower range than equities. For the most part, corporate bonds suffered relatively mild declines in late 2018 and recovered along with their equity counterparts through the end of the reporting period. Most other bond sectors produced comparatively steady positive performance throughout the reporting period, with lower-credit quality, higher-yielding, longer-duration securities generally leading the group’s advance. On average, municipal bonds performed in the middle of the pack while continuing to providetax-advantaged returns for eligible investors.

Amid volatile conditions for most financial markets, we’re pleased that MainStay MacKay Short Term Municipal Fund met its objective of providing shareholders with current income exempt from regular federal income tax. We remain sharply focused on providing you, as a MainStay shareholder, with the experienced and disciplined fund management that we believe underpins an effective, long-term investment strategy. Whatever tomorrow’s investment environment brings, you can rely on our portfolio managers to pursue the objectives of their individual Funds as outlined in the prospectus with the energy and dedication you have come to expect.

While volatility will always remain characteristic of financial markets, your financial professional remains an excellent resource to help you review your investment strategy and make any necessary updates or revisions. We encourage you to discuss with them any questions you may have regarding the report that follows, and to seek their advice in meeting your evolving financial goals. We also invite you to visit our website at nylinvestments.com/funds for more information on investing and the MainStay Funds.

Sincerely,

Kirk C. Lehneis

President

The opinions expressed are as of the date of this report and are subject to change. There is no guarantee that any forecast made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. Past performance is no guarantee of future results.

Not part of the Annual Report

Investors should refer to the Fund’s Summary Prospectus and/or Prospectus and consider the Fund’s investment objectives, strategies, risks, charges and expenses carefully before investing. The Summary Prospectus and/or Prospectus contain this and other information about the Fund. You may obtain copies of the Fund’s Summary Prospectus, Prospectus and Statement of Additional Information free of charge, upon request, by calling toll-free 800-624-6782, by writing to NYLIFE Distributors LLC, Attn: MainStay Marketing Department, 30 Hudson Street, Jersey City, NJ 07302 or by sending ane-mail to MainStayShareholderServices@nylim.com. These documents are also available via the MainStay Funds’ website at nylinvestments.com/funds. Please read the Summary Prospectus and/or Prospectus carefully before investing.

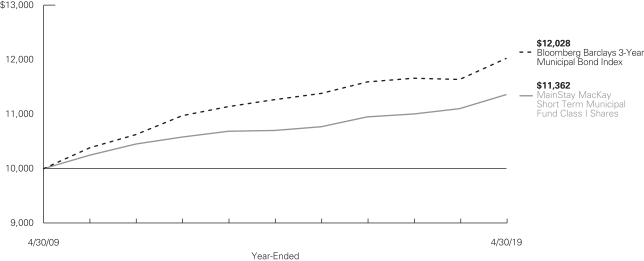

Investment and Performance Comparison1(Unaudited)

Performance data quoted represents past performance. Past performance is no guarantee of future results. Because of market volatility and other factors, current performance may be lower or higher than the figures shown. Investment return and principal value will fluctuate, and as a result, when shares are redeemed, they may be worth more or less than their original cost. The graph below depicts the historical performance of Class I shares of the Fund. Performance will vary from class to class based on differences in class-specific expenses and sales charges. For performance information current to the most recent month-end, please call 800-624-6782 or visit nylinvestments.com/funds.

Average Annual Total Returns for the Year-Ended April 30, 20192

| Class | Sales Charge | Inception Date | One Year | Five Years | Ten Years | Gross Expense Ratio3 | ||||||||||||||||||

| Class A Shares | Maximum 1% Initial Sales Charge4 | With sales charges Excluding sales charges | | 1/2/2004 | | | 0.91 1.93 | %

| | 0.29 0.90 | %

| | 0.71 1.02 | %

| | 0.74 0.74 | %

| |||||||

| Investor Class Shares | Maximum 1% Initial Sales Charge4 | With sales charges Excluding sales charges | | 2/28/2008 | | | 0.54 1.56 |

| | –0.11 0.50 |

| | 0.32 0.62 |

| | 1.26 1.26 |

| |||||||

| Class I Shares | No Sales Charge | 1/2/1991 | 2.34 | 1.20 | 1.28 | 0.49 | ||||||||||||||||||

| 1. | The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on distributions or Fund share redemptions. Total returns reflect maximum applicable sales charges as indicated in the table above, if any, changes in share price, and reinvestment of dividend and capital gain distributions. The graph assumes the initial investment amount shown above and reflects the deduction of all sales charges that would have applied for the period of investment. Performance figures may reflect certain fee waivers and/or expense limitations, without which total returns may have been lower. For more information on share classes and current fee waivers and/or expense limitations (if any), please refer to the Notes to Financial Statements. |

| 2. | Effective June 1, 2015, the Fund changed, among other things, its investment objective and principal investment strategies. Effective May 22, 2018, the Fund made further changes to, among other things, its principal investment strategies. Effective February 28, 2019, the Fund further changed its investment objective. The performance information shown in this report reflects the Fund’s prior investment objectives and principal investment strategies, as applicable. |

| 3. | The gross expense ratios presented reflect the Fund’s “Total Annual Fund Operating Expenses” from the most recent Prospectus, as supplemented, and may differ from other expense ratios disclosed in this report. |

| 4. | The maximum initial sales charge prior to June 1, 2015 was 3.00%. |

The footnotes on the next page are an integral part of the table and graph and should be carefully read in conjunction with them.

| 5 |

| Benchmark Performance | One Year | Five Years | Ten Years | |||||||||

Bloomberg Barclays 3-Year Municipal Bond Index5 | 3.31 | % | 1.30 | % | 1.86 | % | ||||||

Morningstar Muni National Short Category Average6 | 2.71 | 1.08 | 1.66 | |||||||||

| 5. | The Bloomberg Barclays 3-Year Municipal Bond Index is the Fund’s primary broad-based securities-market index for comparison purposes. The Bloomberg Barclays 3-Year Municipal Bond Index is considered representative of the broad-based market for investment grade, tax-exempt bonds with a maturity range of 2-4 years. Results assume reinvestment of all dividends and capital gains. An investment cannot be made directly into an index. |

| 6. | The Morningstar Muni National Short Category Average is representative of funds that invest in bonds issued by state and local governments to fund |

| public projects. The income from these bonds is generally free from federal taxes and/or from state taxes in the issuing state. To lower risk, some of these portfolios spread their assets across many states and sectors. Other portfolios buy bonds from only one state in order to get the state-tax benefit. These portfolios have durations of less than 4.5 years. Results are based on average total returns of similar funds with all dividends and capital gain distributions reinvested. |

The footnotes on the preceding page are an integral part of the table and graph and should be carefully read in conjunction with them.

| 6 | MainStay MacKay Short Term Municipal Fund |

Cost in Dollars of a $1,000 Investment in Mainstay MacKay Short Term Municipal Fund (Unaudited)

The example below is intended to describe the fees and expenses borne by shareholders during the six-month period from November 1, 2018, to April 30, 2019, and the impact of those costs on your investment.

Example

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including exchange fees and sales charges (loads) on purchases (as applicable), and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses (as applicable). This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 made at the beginning of the six-month period and held for the entire period from November 1, 2018, to April 30, 2019.

This example illustrates your Fund’s ongoing costs in two ways:

Actual Expenses

The second and third data columns in the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid during the six months ended April 30, 2019. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then

multiply the result by the number under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The fourth and fifth data columns in the table below provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for thesix-month period shown. You may use this information to compare the ongoing costs of investing in the Fund with the ongoing costs of investing in other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as exchange fees or sales charges (loads). Therefore, the fourth and fifth data columns of the table are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Share Class | Beginning Account Value 11/1/18 | Ending Account Value (Based on Actual Returns and Expenses) 4/30/19 | Expenses Paid During Period1 | Ending Account Value (Based on Hypothetical 5% Annualized Return and Actual Expenses) 4/30/19 | Expenses Paid During Period1 | Net Expense Ratio During Period2 | ||||||||||||||||

| Class A Shares | $ | 1,000.00 | $ | 1,012.30 | $ | 3.49 | $ | 1,021.32 | $ | 3.51 | 0.70% | |||||||||||

| Investor Class Shares | $ | 1,000.00 | $ | 1,009.90 | $ | 5.83 | $ | 1,018.99 | $ | 5.86 | 1.17% | |||||||||||

| Class I Shares | $ | 1,000.00 | $ | 1,013.80 | $ | 2.00 | $ | 1,022.81 | $ | 2.01 | 0.40% | |||||||||||

| 1. | Expenses are equal to the Fund’s annualized expense ratio of each class multiplied by the average account value over the period, divided by 365 and multiplied by 181 (to reflect the six-month period). The table above represents the actual expenses incurred during the six-month period. |

| 2. | Expenses are equal to the Fund’s annualized expense ratio to reflect the six-month period. |

| 7 |

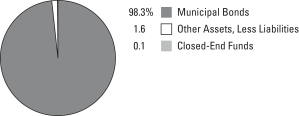

Portfolio Composition as of April 30, 2019(Unaudited)

See Portfolio of Investments beginning on page 10 for specific holdings within these categories. The Fund’s holdings are subject to change.

Top Ten Issuers Held as of April 30, 2019(Unaudited)

| 1. | Territory of Guam, Revenue Bonds, 5.00%, due 11/15/19–12/1/21 |

| 2. | State of Illinois, Unlimited General Obligation, 5.00%, due 11/1/19–6/1/21 |

| 3. | State of Ohio, Capital Facilities Lease-Appropriation, Revenue Bonds, 2.20%, due 10/1/36 |

| 4. | Main Street Natural Gas, Inc., Revenue Bonds, 2.426%–5.00%, due 5/15/20–4/1/48 |

| 5. | New Jersey Economic Development Authority, School Facilities Construction, Revenue Bonds, 5.25%–5.50%, due 12/15/19–9/1/23 |

| 6. | New Jersey Transportation Trust Fund Authority, Transportation System, Revenue Bonds, 5.25%–5.50%, due 12/15/20–12/15/23 |

| 7. | State of North Carolina, Capital Improvement, Revenue Bonds, 5.00%, due 5/1/19 |

| 8. | Indiana Health & Educational Facilities Financing Authority, Ascension Senior Health Credit Group, Revenue Bonds, 1.375%–1.75%, due 10/1/27–11/15/31 |

| 9. | County of Anne Arundel MD, Unlimited General Obligation, 5.00%, due 10/1/19 |

| 10. | New Jersey Economic Development Authority, Revenue Bonds, 5.00%, due 11/1/19–6/15/21 |

| 8 | MainStay MacKay Short Term Municipal Fund |

Portfolio Management Discussion and Analysis(Unaudited)

Questions answered by portfolio managers John Loffredo, CFA, Robert DiMella, CFA, Michael Petty, David Dowden, Scott Sprauer, Frances Lewis and John Lawlor of MacKay Shields LLC, the Fund’s Subadvisor.

How did MainStay MacKay Short Term Municipal Fund perform relative to its benchmark and peer group during the 12 months ended April 30, 2019?

For the 12 months ended April 30, 2019, Class I shares of MainStay MacKay Short Term Municipal Fund returned 2.34%, underperforming the 3.31% return of the Fund’s primary benchmark, the Bloomberg Barclays3-Year Municipal Bond Index. Over the same period, Class I shares also underperformed the 2.71% return of the Morningstar Muni National Short Category Average.1

What factors affected the Fund’s relative performance during the reporting period?

During the reporting period, the Fund’s underweight exposure to bonds from New York detracted from relative performance, as did the Fund’s Treasury hedge. However, overweight exposure to securities from Guam and underweight exposure to securities from Virginia contributed positively to performance relative to the Bloomberg Barclays3-Year Municipal Bond Index. (Contributions take weightings and total returns into account.)

Were there any changes to the Fund during the reporting period?

Effective February 28, 2019, the Fund’s investment objective was modified to seek current income exempt from regular federal income tax. Also on February 28, 2019, John Lawlor was added as a portfolio manager of the Fund. John Loffredo, Robert DiMella, Michael Petty, David Dowden, Scott Sprauer and Francis Lewis continue to manage the Fund. For more information about these changes refer to the supplements dated December 14, 2018, and February 28, 2019.

What was the Fund’s duration2 strategy during the reporting period?

The Fund targeted a shorter duration posture than its benchmark, the Bloomberg Barclays3-Year Municipal Bond Index. At the end of the reporting period, the Fund’s modified duration to

worst3 was 1.23 years while the benchmark’s modified duration to worst was 2.46 years.

During the reporting period, which sectors were the strongest positive contributors to the Fund’s relative performance and which sectors were particularly weak?

The strongest contributors to the Fund’s performance relative to the Bloomberg Barclays3-Year Municipal Bond Index were beneficial security selection in the hospital, industrial development revenue/pollution control revenue (IDR/PCR) and resource recovery sectors. The Fund’s overweight exposure to the prerefunded/escrowed to maturity (ETM), state general obligation, and transportation sectors detracted from relative performance.

What were some of the Fund’s largest purchases and sales during the reporting period?

The Fund remained focused on diversification and liquidity, so no individual transaction was considered significant.

How did the Fund’s sector weightings change during the reporting period?

During the reporting period, the Fund decreased its exposure to the hospital, education and water/sewer sectors while increasing its exposure to the leasing, special tax and electric sectors. The Fund decreased its exposure to bonds from New York and Minnesota while increasing its exposure to bonds from North Carolina, Illinois and Georgia during the same period.

How was the Fund positioned at the end of the reporting period?

At the end of the reporting period, the Fund held overweight positions relative to the Bloomberg Barclays3-Year Municipal Bond Index in the hospital and leasing sectors and to bonds from New Jersey and Illinois. At the same point in time, the Fund held underweight exposure to the prerefunded/ETM and state general obligation sectors and to bonds from New York and California.

| 1. | See page 5 for other share class returns, which may be higher or lower than Class I share returns. See page 6 for more information on benchmark and peer group returns. |

| 2. | Duration is a measure of the price sensitivity of a fixed-income investment to changes in interest rates. Duration is expressed as a number of years and is considered a more accurate sensitivity gauge than average maturity. |

| 3. | Modified duration is inversely related to the approximate percentage change in price for a given change in yield. Duration to worst is the duration of a bond computed using the bond’s nearest call date or maturity, whichever comes first. This measure ignores future cash flow fluctuations due to embedded optionality. |

The opinions expressed are those of the portfolio managers as of the date of this report and are subject to change. There is no guarantee that any forecasts will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

| 9 |

Portfolio of InvestmentsApril 30, 2019

| Principal Amount | Value | |||||||

Long-Term Bonds 98.4%† Municipal Bonds 98.3% |

| |||||||

Arizona 0.2% | ||||||||

Industrial Development Authority of the City of Phoenix, Downtown Phoenix Student LLC, Revenue Bonds | $ | 50,000 | $ | 55,002 | ||||

City of Tucson AZ, Certificates of Participation Insured: AGM | 350,000 | 359,111 | ||||||

Glendale Union School District No. 205, School Improvement Project, Unlimited General Obligation | 540,000 | 560,822 | ||||||

|

| |||||||

| 974,935 | ||||||||

|

| |||||||

California 11.0% |

| |||||||

Alta Loma School District, Capital Appreciation, Unlimited General Obligation | 1,750,000 | 1,682,975 | ||||||

Anaheim Public Financing Authority, Public Improvements Project, Revenue Bonds | 300,000 | 287,157 | ||||||

Auburn Urban Development Authority Successor Agency, Auburn Redevelopment Project, Tax Allocation | 140,000 | 140,267 | ||||||

Cabrillo Unified School District, Capital Appreciation, Unlimited General Obligation | 400,000 | 391,372 | ||||||

California Educational Facilities Authority, Loyola Marymount University, Revenue Bonds | 3,000,000 | 2,820,450 | ||||||

California Health Facilities Financing Authority, Los Angeles Biomedical Research Institute, Revenue Bonds | ||||||||

3.00%, due 9/1/20 | 215,000 | 218,294 | ||||||

4.00%, due 9/1/21 | 275,000 | 288,057 | ||||||

4.00%, due 9/1/22 | 300,000 | 319,581 | ||||||

4.00%, due 9/1/23 | 310,000 | 335,432 | ||||||

California Municipal Finance Authority, California Lutheran University, Revenue Bonds | ||||||||

5.00%, due 10/1/20 | 325,000 | 339,729 | ||||||

5.00%, due 10/1/21 | 250,000 | 268,583 | ||||||

| Principal Amount | Value | |||||||

California (continued) | ||||||||

California Municipal Finance Authority, Community Medical Centers, Revenue Bonds | $ | 1,100,000 | $ | 1,158,344 | ||||

California Municipal Finance Authority, LAX Integrated Express Solutions Project, Revenue Bonds | 1,300,000 | 1,461,603 | ||||||

California Municipal Finance Authority, Paradise Valley Estates Project, Revenue Bonds | 500,000 | 500,925 | ||||||

California Municipal Finance Authority, West Village Student Housing Project, Revenue Bonds | 1,000,000 | 1,111,940 | ||||||

California School Finance Authority, Aspire Public Schools, Revenue Bonds | 130,000 | 130,958 | ||||||

California School Finance Authority, Classical Academies Project, Revenue Bonds | 5,050,000 | 5,944,506 | ||||||

California State Educational Facilities Authority, Art Center College of Design, Revenue Bonds | ||||||||

Series A | 125,000 | 127,408 | ||||||

Series A | 290,000 | 312,771 | ||||||

Series A | 200,000 | 220,938 | ||||||

Series A | 215,000 | 242,903 | ||||||

California State Health Facilities Financing Authority, Dignity Health, Revenue Bonds | 2,700,000 | 2,700,000 | ||||||

California Statewide Communities Development Authority, Methodist Hospital of Southern California Project, Revenue Bonds | ||||||||

5.00%, due 1/1/20 | 365,000 | 372,468 | ||||||

5.00%, due 1/1/21 | 300,000 | 315,024 | ||||||

5.00%, due 1/1/22 | 500,000 | 539,130 | ||||||

| 10 | MainStay MacKay Short Term Municipal Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

| Principal Amount | Value | |||||||

| Municipal Bonds (continued) |

| |||||||

California (continued) | ||||||||

City of Oakland CA, Revenue Bonds | $ | 1,000,000 | $ | 979,700 | ||||

Inglewood Unified School District, Unlimited General Obligation | ||||||||

Series B, Insured: BAM | 500,000 | 502,800 | ||||||

Series B, Insured: BAM | 1,000,000 | 1,027,370 | ||||||

Los Angeles Department of Airports, Revenue Bonds (a) | ||||||||

Series C | 1,000,000 | 1,001,220 | ||||||

Series A | 1,065,000 | 1,135,695 | ||||||

Los Angeles Unified School District, Unlimited General Obligation | 3,000,000 | 3,017,640 | ||||||

Monrovia Redevelopment Agency Successor Agency, Central Redevelopment Project, Tax Allocation | 600,000 | 600,000 | ||||||

Oxnard County Water Revenue, Revenue Bonds | ||||||||

Insured: BAM | 500,000 | 501,345 | ||||||

Insured: BAM | 925,000 | 957,981 | ||||||

Insured: BAM | 280,000 | 299,079 | ||||||

Sacramento City Financing Authority, Capital Appreciation, Tax Allocation | 4,170,000 | 3,969,548 | ||||||

Sacramento County Sanitation District Financing Authority, Revenue Bonds | 2,000,000 | 1,995,020 | ||||||

San Diego Redevelopment Agency Successor Agency, Tax Allocation | 250,000 | 249,745 | ||||||

San Francisco City & County International Airports Communities, Revenue Bonds | 2,965,000 | 3,060,740 | ||||||

| Principal Amount | Value | |||||||

California (continued) | ||||||||

San Ysidro School District, Unlimited General Obligation | $ | 1,320,000 | $ | 1,446,284 | ||||

Santa Fe Springs Community Development Commission, Consolidated Redevelopment Project, Tax Allocation | 500,000 | 487,525 | ||||||

Southern California Public Power Authority, Apex Power Project No. 1, Revenue Bonds | 1,300,000 | 1,394,601 | ||||||

Stockton Public Financing Authority, Water Revenue, Revenue Bonds | ||||||||

Series A, Insured: BAM | 750,000 | 760,177 | ||||||

Series A, Insured: BAM | 400,000 | 419,624 | ||||||

Series A, Insured: BAM | 500,000 | 538,770 | ||||||

Ukiah Unified School District, Capital Appreciation, Unlimited General Obligation Insured: NATL-RE | 875,000 | 839,615 | ||||||

Vallejo City Unified School District, Unlimited General Obligation | 2,500,000 | 2,573,375 | ||||||

|

| |||||||

| 49,988,669 | ||||||||

|

| |||||||

Colorado 0.7% |

| |||||||

Colorado Health Facilities Authority, Catholic Health Initiatives, Revenue Bonds | 1,360,000 | 1,429,442 | ||||||

Denver City & County Airport Revenue | 550,000 | 576,944 | ||||||

E-470 Public Highway Authority, Revenue Bonds | 1,000,000 | 1,009,860 | ||||||

|

| |||||||

| 3,016,246 | ||||||||

|

| |||||||

Connecticut 1.6% |

| |||||||

City of Bridgeport CT, Unlimited General Obligation | 1,000,000 | 1,038,910 | ||||||

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | 11 |

Portfolio of InvestmentsApril 30, 2019 (continued)

| Principal Amount | Value | |||||||

| Municipal Bonds (continued) |

| |||||||

Connecticut (continued) |

| |||||||

City of Hartford CT, Unlimited General Obligation | ||||||||

Series C, Insured: AGM | $ | 200,000 | $ | 213,688 | ||||

Series A, Insured: AGM | 1,000,000 | 1,088,310 | ||||||

Connecticut State Health & Educational Facility Authority, Quinnipiac University, Revenue Bonds | 800,000 | 803,016 | ||||||

State of Connecticut, Unlimited General Obligation | ||||||||

Series C | 2,210,000 | 2,348,280 | ||||||

Series C | 1,500,000 | 1,678,605 | ||||||

|

| |||||||

| 7,170,809 | ||||||||

|

| |||||||

Florida 3.0% |

| |||||||

City of Lakeland FL, Lakeland Regional Health Systems, Revenue Bonds | 265,000 | 269,616 | ||||||

County of Broward Port Facilities, Revenue Bonds | 2,420,000 | 2,517,720 | ||||||

County of Miami-Dade Seaport Department, Revenue Bonds | 2,140,000 | 2,166,536 | ||||||

Escambia County, Gulf Power Co. Project, Revenue Bonds | 500,000 | 500,000 | ||||||

Florida Department of Environmental Protection, Revenue Bonds | 1,000,000 | 1,038,680 | ||||||

Mid-Bay Bridge Authority, Revenue Bonds | 1,000,000 | 1,071,630 | ||||||

Orange County, Tourist Development Tax, Revenue Bonds | 5,000,000 | 5,070,800 | ||||||

State of Florida Lottery, Revenue Bonds | 1,100,000 | 1,106,061 | ||||||

|

| |||||||

| 13,741,043 | ||||||||

|

| |||||||

| Principal Amount | Value | |||||||

Georgia 5.1% |

| |||||||

Burke County Development Authority, Georgia Power Co., Vogtle Project, Revenue Bonds | $ | 4,500,000 | $ | 4,500,000 | ||||

Heard County Development Authority, Georgia Power Co., Plant Wansley, Revenue Bonds | 4,500,000 | 4,500,000 | ||||||

Main Street Natural Gas, Inc., Revenue Bonds | ||||||||

Series B | 5,000,000 | 4,960,450 | ||||||

Series A | 1,000,000 | 1,028,920 | ||||||

Series A | 500,000 | 526,560 | ||||||

Series A | 550,000 | 591,921 | ||||||

Series A | 1,000,000 | 1,098,500 | ||||||

Municipal Electric Authority of Georgia, Revenue Bonds | ||||||||

Series 18A | 230,000 | 234,552 | ||||||

Series HH | 1,460,000 | 1,488,893 | ||||||

Series B | 2,250,000 | 2,293,785 | ||||||

State of Georgia, Unlimited General Obligation | 1,925,000 | 1,935,780 | ||||||

|

| |||||||

| 23,159,361 | ||||||||

|

| |||||||

Guam 3.4% |

| |||||||

Guam Government Waterworks Authority, Water & Wastewater Systems Revenue, Revenue Bonds | 400,000 | 411,976 | ||||||

Port Authority of Guam, Revenue Bonds | ||||||||

Series C | 500,000 | 501,590 | ||||||

Series C | 500,000 | 504,650 | ||||||

Series B | 250,000 | 251,058 | ||||||

Series B | 400,000 | 429,676 | ||||||

Territory of Guam, Business Privilege Tax, Revenue Bonds | 660,000 | 671,827 | ||||||

Territory of Guam, Revenue Bonds | ||||||||

Series D | 1,000,000 | 1,015,320 | ||||||

| 12 | MainStay MacKay Short Term Municipal Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

| Principal Amount | Value | |||||||

| Municipal Bonds (continued) |

| |||||||

Guam (continued) |

| |||||||

Territory of Guam, Revenue Bonds (continued) |

| |||||||

Series D | $ | 2,740,000 | $ | 2,852,148 | ||||

Series A | 3,230,000 | 3,365,886 | ||||||

Series A | 5,295,000 | 5,632,133 | ||||||

|

| |||||||

| 15,636,264 | ||||||||

|

| |||||||

Hawaii 0.2% |

| |||||||

State of Hawaii, Unlimited General Obligation | 1,000,000 | 1,014,080 | ||||||

|

| |||||||

Illinois 10.7% |

| |||||||

Chicago Board of Education, Chicago School Board, Unlimited General Obligation | 400,000 | 405,804 | ||||||

Chicago Board of Education, Unlimited General Obligation | ||||||||

Series A, Insured: NATL-RE | 1,775,000 | 1,798,217 | ||||||

Series A, Insured: AGM | 1,600,000 | 1,769,216 | ||||||

Chicago Midway International Airport, Revenue Bonds | 1,425,000 | 1,454,825 | ||||||

Chicago Park District, Limited General Obligation | ||||||||

Series C | 955,000 | 964,197 | ||||||

Series C | 450,000 | 458,010 | ||||||

Series E | 750,000 | 782,250 | ||||||

Series E | 800,000 | 853,256 | ||||||

Chicago Transit Authority, Revenue Bonds | 5,000,000 | 5,378,200 | ||||||

City of Chicago IL, Waterworks Second Lien, Revenue Bonds | 245,000 | 248,729 | ||||||

Cook County Community High School District No. 212 Leyden, Revenue Bonds | 1,140,000 | 1,134,243 | ||||||

| Principal Amount | Value | |||||||

Illinois (continued) | ||||||||

Cook County Community Unit School District No. 401 Elmwood Park, Limited General Obligation | $ | 1,340,000 | $ | 1,406,290 | ||||

Cook County School District, No. 81 Schiller Park, Limited General Obligation | 570,000 | 577,535 | ||||||

County of Cook IL, Unlimited General Obligation | 1,665,000 | 1,733,165 | ||||||

Illinois Educational Facilities Authority, University of Chicago, Revenue Bonds | 2,250,000 | 2,251,462 | ||||||

Illinois Finance Authority, Edward Elmhurst Obligated Group, Revenue Bonds | 300,000 | 313,290 | ||||||

Illinois Finance Authority, Rosalind Franklin University of Medicine & Science, Revenue Bonds | 250,000 | 249,873 | ||||||

Illinois Sports Facilities Authority, Revenue Bonds | 925,000 | 921,541 | ||||||

Illinois State University, Auxiliary Facilities System, Revenue Bonds | ||||||||

Series A, Insured: AGM | 505,000 | 529,503 | ||||||

Series B, Insured: AGM | 250,000 | 262,130 | ||||||

Series A, Insured: AGM | 425,000 | 455,400 | ||||||

Series B, Insured: AGM | 645,000 | 691,137 | ||||||

La Salle County School District No. 141, Unlimited General Obligation | ||||||||

Insured: MAC | 560,000 | 578,133 | ||||||

Insured: MAC | 585,000 | 610,091 | ||||||

Insured: MAC | 370,000 | 390,742 | ||||||

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | 13 |

Portfolio of InvestmentsApril 30, 2019 (continued)

| Principal Amount | Value | |||||||

| Municipal Bonds (continued) |

| |||||||

Illinois (continued) | ||||||||

Madison Macoupin Etc Counties Illinois Community College District No. 536, Lewis & Clark Community College, Unlimited General Obligation | ||||||||

4.50%, due 5/1/20 | $ | 305,000 | $ | 312,857 | ||||

5.00%, due 11/1/22 | 420,000 | 450,912 | ||||||

Madison Macoupin Etc Counties Illinois Community College District No. 536, Unlimited General Obligation | ||||||||

Series A | 150,000 | 155,276 | ||||||

Series A | 70,000 | 74,024 | ||||||

Peoria County School District No. 68 Oak Grove, Unlimited General Obligation | 180,000 | 180,279 | ||||||

Public Building Commission of Chicago, Chicago Transit Authority, Revenue Bonds Insured: AMBAC | 1,000,000 | 1,120,190 | ||||||

Railsplitter Tobacco Settlement Authority, Revenue Bonds | 3,765,000 | 3,897,076 | ||||||

Randolph County Community Unit School District No. 140 Sparta, Unlimited General Obligation | 210,000 | 212,715 | ||||||

Regional Transportation Authority, Revenue Bonds | 1,560,000 | 1,563,884 | ||||||

Round Lake IL, Lakewood Grove Special Service Area No. 3 & 4, Special Tax Insured: BAM | 499,000 | 499,699 | ||||||

Sales Tax Securitization Corp., Revenue Bonds | 1,250,000 | 1,337,687 | ||||||

State of Illinois, Junior Obligation, Revenue Bonds | 610,000 | 612,111 | ||||||

State of Illinois, Sales Tax, Revenue Bonds | ||||||||

5.00%, due 6/15/22 | 655,000 | 706,175 | ||||||

Series C | 95,000 | 102,422 | ||||||

| Principal Amount | Value | |||||||

Illinois (continued) | ||||||||

State of Illinois, Unlimited General Obligation | ||||||||

Series B | $ | 5,000,000 | $ | 5,073,350 | ||||

5.00%, due 6/1/21 | 4,000,000 | 4,199,400 | ||||||

Upper Illinois River Valley Development Authority, Morris Hospital, Revenue Bonds | 575,000 | 599,282 | ||||||

Village of Cary IL, Special Service Area No. 2, Special Tax | 149,000 | 148,347 | ||||||

Village of Crestwood IL, Alternate Revenue Source, Unlimited General Obligation | 500,000 | 500,150 | ||||||

Western Illinois University, Revenue Bonds Insured: BAM | 460,000 | 471,118 | ||||||

|

| |||||||

| 48,434,193 | ||||||||

|

| |||||||

Indiana 4.4% |

| |||||||

City of Indianapolis IN, Economic Development, Revenue Bonds | 5,900,000 | 5,900,000 | ||||||

City of Whiting IN, Environmental Facilities, BP Products North America, Revenue Bonds | 5,000,000 | 5,002,250 | ||||||

Hammond Multi-School Building Corp., Revenue Bonds | ||||||||

4.00%, due 1/15/20 | 470,000 | 477,111 | ||||||

4.00%, due 7/15/21 | 330,000 | 345,055 | ||||||

5.00%, due 1/15/22 | 555,000 | 599,045 | ||||||

5.00%, due 7/15/22 | 1,040,000 | 1,137,177 | ||||||

Indiana Health & Educational Facilities Financing Authority, Ascension Senior Health Credit Group, Revenue Bonds (c) | ||||||||

Series A-9 | 4,985,000 | 4,960,723 | ||||||

Series 2006 B-3 | 1,400,000 | 1,401,778 | ||||||

|

| |||||||

| 19,823,139 | ||||||||

|

| |||||||

Iowa 0.3% |

| |||||||

City of Coralville IA, Certificates of Participation | ||||||||

Series E | 465,000 | 464,861 | ||||||

Series E | 500,000 | 498,410 | ||||||

| 14 | MainStay MacKay Short Term Municipal Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

| Principal Amount | Value | |||||||

| Municipal Bonds (continued) |

| |||||||

Iowa (continued) | ||||||||

City of Coralville IA, Corporate Purpose Bonds, Unlimited General Obligation | $ | 270,000 | $ | 270,000 | ||||

Xenia Rural Water District, Capital Loan Notes, Revenue Bonds | 375,000 | 376,391 | ||||||

|

| |||||||

| 1,609,662 | ||||||||

|

| |||||||

Kansas 0.3% |

| |||||||

Johnson County Unified School District No. 233 Olathe, Unlimited General Obligation | 1,250,000 | 1,305,363 | ||||||

|

| |||||||

Kentucky 1.1% |

| |||||||

Kentucky Bond Development Corp., Lexington Center Corp. Project, Revenue Bonds | 550,000 | 604,852 | ||||||

Kentucky Bond Development Corp., Revenue Bonds | ||||||||

5.00%, due 9/1/19 | 390,000 | 394,161 | ||||||

5.00%, due 9/1/21 | 325,000 | 347,958 | ||||||

Louisville & Jefferson County Metropolitan Government, Louisville Gas & Electric Co., Revenue Bonds | 3,000,000 | 3,001,110 | ||||||

Louisville / Jefferson County Metropolitan Government, Norton Healthcare, Revenue Bonds | 790,000 | 823,654 | ||||||

|

| |||||||

| 5,171,735 | ||||||||

|

| |||||||

Louisiana 1.9% |

| |||||||

E Baton Rouge Parish, Road & Street Improvement, Revenue Bonds Insured: AGC | 2,000,000 | 2,017,720 | ||||||

Evangeline Parish Road & Drain Sales Tax District No. 1, Revenue Bonds Insured: AGM | 500,000 | 524,895 | ||||||

Louisiana Local Government Environmental Facilities & Community Development Authority, University Student Housing, Revenue Bonds | 555,000 | 555,699 | ||||||

| Principal Amount | Value | |||||||

Louisiana (continued) |

| |||||||

Louisiana Public Facilities Authority, Willis-Knighton Medical Center, Revenue Bonds | $ | 5,400,000 | $ | 5,400,000 | ||||

|

| |||||||

| 8,498,314 | ||||||||

|

| |||||||

Maine 0.2% |

| |||||||

State of Maine, Unlimited General Obligation | 810,000 | 812,236 | ||||||

|

| |||||||

Maryland 2.4% |

| |||||||

County of Anne Arundel MD, Unlimited General Obligation | 6,165,000 | 6,254,393 | ||||||

Maryland Health & Higher Educational Facilities Authority, Broadmead Issue, Revenue Bonds | 1,750,000 | 1,791,335 | ||||||

Prince George’s County, Regional Medical Center, Certificates of Participation | 1,040,000 | 1,089,525 | ||||||

Washington Suburban Sanitary Commission, General Unlimited Obligation | 1,955,000 | 1,960,376 | ||||||

|

| |||||||

| 11,095,629 | ||||||||

|

| |||||||

Massachusetts 0.8% |

| |||||||

Massachusetts Development Finance Agency, UMass Boston Student Housing Project, Revenue Bonds | 985,000 | 997,342 | ||||||

Massachusetts Housing Finance Agency, Revenue Bonds | 2,535,000 | 2,535,887 | ||||||

|

| |||||||

| 3,533,229 | ||||||||

|

| |||||||

Michigan 2.4% |

| |||||||

City of Detroit MI Sewage Disposal System, Second Lien, Revenue Bonds | 1,500,000 | 1,661,910 | ||||||

City of Detroit MI Sewage Disposal System, Senior Lien, Revenue Bonds | 1,000,000 | 1,005,620 | ||||||

Harper Woods School District, Unlimited General Obligation | 500,000 | 500,000 | ||||||

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | 15 |

Portfolio of InvestmentsApril 30, 2019 (continued)

| Principal Amount | Value | |||||||

| Municipal Bonds (continued) |

| |||||||

Michigan (continued) | ||||||||

Lincoln Consolidated School District, Unlimited General Obligation | $ | 1,180,000 | $ | 1,180,000 | ||||

Michigan Finance Authority, Trinity Health Credit Group, Revenue Bonds | ||||||||

Series MI-1 | 200,000 | 210,344 | ||||||

Series MI-1 | 200,000 | 216,494 | ||||||

Series MI-1 | 200,000 | 222,478 | ||||||

Michigan Finance Authority, Wayne County Criminal Justice Center Project, Revenue Bonds | 500,000 | 555,130 | ||||||

Michigan Strategic Fund, Detroit Edison Project, Revenue Bonds | 2,000,000 | 1,949,340 | ||||||

Royal Oak Hospital Finance Authority, Beaumont Health Credit Group, Revenue Bonds | 1,500,000 | 1,516,350 | ||||||

State of Michigan, School Loan, Revenue Bonds | 715,000 | 732,839 | ||||||

Warren Consolidated Schools, Unlimited General Obligation | 1,080,000 | 1,080,000 | ||||||

|

| |||||||

| 10,830,505 | ||||||||

|

| |||||||

Minnesota 1.7% |

| |||||||

Kanabec County MN, FirstLight Health System, Revenue Bonds | 2,750,000 | 2,750,357 | ||||||

State of Minnesota, Unlimited General Obligation | 4,940,000 | 4,981,249 | ||||||

|

| |||||||

| 7,731,606 | ||||||||

|

| |||||||

Mississippi 1.2% |

| |||||||

City of Jackson MS Water & Sewer System, Revenue Bonds | 625,000 | 639,162 | ||||||

| Principal Amount | Value | |||||||

Mississippi (continued) |

| |||||||

Mississippi Development Bank, Jackson Public School District, Revenue Bonds Insured: BAM | $ | 450,000 | $ | 483,008 | ||||

Mississippi Development Bank, Jackson Water & Sewer System Project, Revenue Bonds | 1,000,000 | 1,045,950 | ||||||

Mississippi Gaming Tax, Revenue Bonds | ||||||||

Series A | 500,000 | 507,495 | ||||||

Series A | 750,000 | 785,362 | ||||||

Series A | 700,000 | 754,600 | ||||||

Series A | 1,000,000 | 1,106,070 | ||||||

|

| |||||||

| 5,321,647 | ||||||||

|

| |||||||

Missouri 1.0% |

| |||||||

Kansas City Industrial Development Authority, Downtown Redevelopment District, Revenue Bonds | 4,420,000 | 4,739,566 | ||||||

|

| |||||||

Montana 0.2% |

| |||||||

Montana Facilities Finance Authority, Kalispell Regional Medical Center, Revenue Bonds | 915,000 | 935,011 | ||||||

|

| |||||||

Nebraska 1.2% |

| |||||||

Central Plains Energy, Project No. 4, Revenue Bonds | 5,000,000 | 5,554,100 | ||||||

|

| |||||||

Nevada 0.7% |

| |||||||

County of Washoe N.V., Sierra Pacific Power Co. Project, Revenue Bonds | 3,000,000 | 2,998,140 | ||||||

|

| |||||||

New Hampshire 0.7% |

| |||||||

New Hampshire Business Finance Authority, United Illuminating Co., Revenue Bonds | 3,000,000 | 3,077,190 | ||||||

|

| |||||||

| 16 | MainStay MacKay Short Term Municipal Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

| Principal Amount | Value | |||||||

| Municipal Bonds (continued) |

| |||||||

New Jersey 11.2% |

| |||||||

Atlantic County Improvement Authority, Stockton University Atlantic City, Revenue Bonds | $ | 3,745,000 | $ | 3,918,468 | ||||

Borough of North Plainfield NJ, Unlimited General Obligation | 330,000 | 335,000 | ||||||

City of Atlantic City NJ, Tax Appeal, Unlimited General Obligation | ||||||||

Series B, Insured: AGM | 200,000 | 204,846 | ||||||

Series A, Insured: BAM | 600,000 | 630,624 | ||||||

City of Bayonne NJ, Unlimited General Obligation | 1,000,000 | 1,004,690 | ||||||

Essex County Improvement Authority, Revenue Bonds Insured: County Guaranteed | 500,000 | 507,290 | ||||||

Garden State Preservation Trust, Revenue Bonds | ||||||||

Series C, Insured: AGM | 3,175,000 | 3,228,149 | ||||||

Series C, Insured: AGM | 1,535,000 | 1,612,886 | ||||||

Greater Egg Harbor Regional High School District, Unlimited General Obligation Insured: AGM | 1,000,000 | 1,017,290 | ||||||

New Jersey Economic Development Authority, North Star Academy Charter School of Newark, Inc., Revenue Bonds | 200,000 | 210,468 | ||||||

New Jersey Economic Development Authority, Revenue Bonds | ||||||||

Series B | 5,000,000 | 5,077,850 | ||||||

Series DDD | 960,000 | 1,016,890 | ||||||

New Jersey Economic Development Authority, School Facilities Construction, Revenue Bonds | ||||||||

Series K; Insured: AMBAC | 300,000 | 315,306 | ||||||

Series K; Insured: AMBAC | 5,000,000 | 5,112,100 | ||||||

| Principal Amount | Value | |||||||

New Jersey (continued) | ||||||||

New Jersey Economic Development Authority, School Facilities Construction, Revenue Bonds (continued) | ||||||||

Series N-1, Insured: NATL-RE | $ | 1,500,000 | $ | 1,696,605 | ||||

New Jersey State Economic Development Authority, Revenue Bonds | 2,525,000 | 2,962,961 | ||||||

New Jersey Transportation Trust Fund Authority, Federal Highway Reimbursement, Revenue Bonds | 1,000,000 | 1,129,430 | ||||||

New Jersey Transportation Trust Fund Authority, Transportation System, Revenue Bonds | ||||||||

Series B, Insured: AMBAC | 275,000 | 312,029 | ||||||

Series B, Insured: NATL-RE | 5,000,000 | 5,274,900 | ||||||

Series B, Insured: AGC | 1,000,000 | 1,057,620 | ||||||

New Jersey Turnpike Authority, Revenue Bonds | 6,000,000 | 6,010,740 | ||||||

Passaic Valley Sewerage Commissioners, Sewer System, Revenue Bonds | 2,190,000 | 2,478,313 | ||||||

State of New Jersey, Unlimited General Obligation | 225,000 | 226,780 | ||||||

Tobacco Settlement Financing Corp., Revenue Bonds | ||||||||

Series A | 500,000 | 501,340 | ||||||

Series A | 2,500,000 | 2,579,475 | ||||||

Series A | 500,000 | 529,465 | ||||||

Series A | 1,250,000 | 1,356,400 | ||||||

Series A | 250,000 | 277,233 | ||||||

Trenton Parking Authority, Revenue Bonds | 170,000 | 169,342 | ||||||

|

| |||||||

| 50,754,490 | ||||||||

|

| |||||||

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | 17 |

Portfolio of InvestmentsApril 30, 2019 (continued)

| Principal Amount | Value | |||||||

| Municipal Bonds (continued) |

| |||||||

New Mexico 0.2% |

| |||||||

Rio Rancho Water & Wastewater Systems, Revenue Bonds | $ | 800,000 | $ | 827,832 | ||||

|

| |||||||

New York 5.9% |

| |||||||

City of Long Beach, Limited General Obligation | ||||||||

Insured: BAM | 600,000 | 632,142 | ||||||

Insured: BAM | 615,000 | 667,023 | ||||||

Dutchess County Resource Recovery Agency, Revenue Bonds | 1,055,000 | 1,075,034 | ||||||

Hempstead Town Local Development Corp., Molloy College Project, Revenue Bonds | ||||||||

5.00%, due 7/1/20 | 1,235,000 | 1,279,213 | ||||||

5.00%, due 7/1/21 | 435,000 | 462,827 | ||||||

Metropolitan Transportation Authority, Revenue Bonds | 3,500,000 | 3,615,465 | ||||||

New York State Dormitory Authority, Interagency Council Pooled Loan Program, Revenue Bonds | ||||||||

SubseriesA-1 | 275,000 | 282,189 | ||||||

SubseriesA-1 | 255,000 | 266,988 | ||||||

SubseriesA-1 | 400,000 | 424,860 | ||||||

SubseriesA-1 | 430,000 | 463,527 | ||||||

New York State Housing Finance Agency, 350 West 34th Street, Revenue Bonds | 2,100,000 | 2,100,000 | ||||||

New York Transportation Development Corp., LaGuardia Airport Terminals C&D Redevelopment Project, Revenue Bonds | 5,000,000 | 5,369,700 | ||||||

Niagara Frontier Transportation Authority, Buffalo Niagara International Airport, Revenue Bonds (a) | ||||||||

Series A | 1,600,000 | 1,645,296 | ||||||

Series A | 1,850,000 | 1,955,468 | ||||||

| Principal Amount | Value | |||||||

New York (continued) |

| |||||||

Port Authority of New York & New Jersey, Revenue Bonds (a) | ||||||||

5.00%, due 9/15/19 | $ | 4,750,000 | $ | 4,807,902 | ||||

5.00%, due 10/15/21 | 375,000 | 404,156 | ||||||

Westchester County Local Development Corp., Westchester Medical Center, Revenue Bonds | 1,145,000 | 1,161,912 | ||||||

|

| |||||||

| 26,613,702 | ||||||||

|

| |||||||

North Carolina 3.0% |

| |||||||

Charlotte Airport Revenue, Charlotte Douglas International Airport, Revenue Bonds | 550,000 | 575,256 | ||||||

Guilford County, Unlimited General Obligation | 1,830,000 | 1,881,862 | ||||||

State of North Carolina, Capital Improvement, Revenue Bonds | 6,500,000 | 6,500,000 | ||||||

State of North Carolina, Unlimited General Obligation | 2,500,000 | 2,506,950 | ||||||

Wake County, Hammond Road Detention Center, Revenue Bonds | 2,275,000 | 2,281,347 | ||||||

|

| |||||||

| 13,745,415 | ||||||||

|

| |||||||

Ohio 3.9% |

| |||||||

Akron Bath Copley Joint Township Hospital District, Township Hospital District , Revenue Bonds | 1,000,000 | 1,096,270 | ||||||

City of Cleveland OH, Airport System, Revenue Bonds | 500,000 | 524,330 | ||||||

City of Dayton OH Airport, Revenue Bonds | 995,000 | 1,038,661 | ||||||

City of Toledo OH, Limited General Obligation Insured: AGM | 1,540,000 | 1,560,082 | ||||||

Cleveland Department of Public Utilities Division of Public Power, Revenue Bonds | 3,000,000 | 3,144,330 | ||||||

| 18 | MainStay MacKay Short Term Municipal Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

| Principal Amount | Value | |||||||

| Municipal Bonds (continued) |

| |||||||

Ohio (continued) |

| |||||||

Lucas County Ohio Hospital Revenue, ProMedica Healthcare Obligated Group, Revenue Bonds | $ | 500,000 | $ | 507,550 | ||||

Ohio Higher Educational Facility Commission, Otterbein University Project, Revenue Bonds | 915,000 | 925,339 | ||||||

State of Ohio, Capital Facilities Lease-Appropriation, Revenue Bonds | 8,800,000 | 8,800,000 | ||||||

|

| |||||||

| 17,596,562 | ||||||||

|

| |||||||

Oklahoma 0.2% |

| |||||||

Weatherford Industrial Trust Educational Facilities, Weatherford Public Schools Project, Revenue Bonds | 1,000,000 | 1,056,970 | ||||||

|

| |||||||

Pennsylvania 3.2% |

| |||||||

Capital Region Water, Revenue Bonds | 1,300,000 | 1,308,736 | ||||||

Centre County Hospital Authority, Mount Nittany Medical Center, Revenue Bonds | 240,000 | 242,841 | ||||||

City of Reading PA, Unlimited General Obligation | 620,000 | 625,952 | ||||||

Commonwealth of Pennsylvania, Certificates of Participation | ||||||||

Series A | 300,000 | 310,188 | ||||||

Series A | 350,000 | 371,546 | ||||||

Series A | 300,000 | 326,166 | ||||||

Dauphin County General Authority, Pinnacle Health System Project, Revenue Bonds | 500,000 | 516,545 | ||||||

Hazleton Area School District, Limited General Obligation | ||||||||

Series B, Insured: BAM | 375,000 | 375,334 | ||||||

| Principal Amount | Value | |||||||

Pennsylvania (continued) | ||||||||

Hazleton Area School District, Limited General Obligation (continued) | ||||||||

Series A, Insured: BAM | $ | 600,000 | $ | 610,374 | ||||

Lancaster Higher Education Authority, Harrisburg Area Community, Revenue Bonds | 685,000 | 694,042 | ||||||

Lycoming County Authority, Pennsylvania College of Technology, Revenue Bonds | 755,000 | 761,644 | ||||||

Pennsylvania Turnpike Commission, Oil Franchise Tax, Revenue Bonds | 1,000,000 | 1,019,610 | ||||||

Philadelphia Gas Works Co., 1998 General Ordinance, Revenue Bonds | 2,030,000 | 2,057,466 | ||||||

Philadelphia Gas Works Co., Revenue Bonds | 800,000 | 806,456 | ||||||

Philadelphia School District, Unlimited General Obligation | 700,000 | 751,394 | ||||||

Philadelphia Water & Wastewater Revenue, Revenue Bonds | ||||||||

Series A | 1,500,000 | 1,520,670 | ||||||

Series A | 2,000,000 | 2,093,220 | ||||||

|

| |||||||

| �� | 14,392,184 | |||||||

|

| |||||||

Puerto Rico 2.6% |

| |||||||

Commonwealth of Puerto Rico, CPI- Linked Bonds-Public Improvement, Unlimited General Obligation | 655,000 | 654,384 | ||||||

Commonwealth of Puerto Rico, Public Improvement, Unlimited General Obligation | ||||||||

Insured: AGM | 900,000 | 921,915 | ||||||

Series A, Insured: NATL-RE | 3,545,000 | 3,558,187 | ||||||

Insured: AGM | 525,000 | 527,121 | ||||||

Series A, Insured: NATL-RE | 420,000 | 430,395 | ||||||

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | 19 |

Portfolio of InvestmentsApril 30, 2019 (continued)

| Principal Amount | Value | |||||||

| Municipal Bonds (continued) |

| |||||||

Puerto Rico (continued) | ||||||||

Puerto Rico Electric Power Authority, Revenue Bonds | ||||||||

Series MM, Insured: NATL-RE | $ | 230,000 | $ | 230,669 | ||||

Series UU, Insured: NATL-RE | 290,000 | 290,844 | ||||||

Series MM, Insured: NATL-RE | 275,000 | 280,253 | ||||||

Series N, Insured: NATL-RE | 620,000 | 622,058 | ||||||

Series L, Insured: NATL-RE | 60,000 | 60,223 | ||||||

Puerto Rico Highway & Transportation Authority, Revenue Bonds | ||||||||

Series AA, Insured: NATL-RE | 1,100,000 | 1,104,092 | ||||||

Series AA, Insured: NATL-RE | 1,020,000 | 1,045,245 | ||||||

Puerto Rico Municipal Finance Agency, Revenue Bonds | ||||||||

Series A, Insured: AGM | 240,000 | 240,816 | ||||||

Series A, Insured: AGM | 250,000 | 250,950 | ||||||

Series C, Insured: AGM | 965,000 | 970,308 | ||||||

Puerto Rico Public Buildings Authority, Government Facilities, Revenue Bonds | 800,000 | 802,656 | ||||||

|

| |||||||

| 11,990,116 | ||||||||

|

| |||||||

Rhode Island 0.6% |

| |||||||

Rhode Island Commerce Corp., Grant Anticipation Rhode Island Department, Revenue Bonds | 1,000,000 | 1,036,990 | ||||||

Rhode Island Health & Educational Building Corp., Hospital Financing-Lifespan Obligated Group, Revenue Bonds | 1,500,000 | 1,544,790 | ||||||

|

| |||||||

| 2,581,780 | ||||||||

|

| |||||||

South Carolina 0.6% |

| |||||||

South Carolina Ports Authority, Revenue Bonds | 1,490,000 | 1,497,763 | ||||||

| Principal Amount | Value | |||||||

South Carolina (continued) |

| |||||||

Sumter Two School Facilities, Inc., Sumter School District Project, Revenue Bonds Insured: BAM | $ | 1,065,000 | $ | 1,083,147 | ||||

|

| |||||||

| 2,580,910 | ||||||||

|

| |||||||

Tennessee 0.3% |

| |||||||

Memphis-Shelby County Airport Authority, Revenue Bonds | 1,290,000 | 1,370,535 | ||||||

Metropolitan Government Nashville & Davidson County Health & Educational Facilities Board, Lipscomb University Project, Revenue Bonds | 200,000 | 201,712 | ||||||

|

| |||||||

| 1,572,247 | ||||||||

|

| |||||||

Texas 5.9% |

| |||||||

City of Dallas TX, Waterworks & Sewer Systems, Revenue Bonds | 3,500,000 | 3,501,785 | ||||||

City of Houston TX, Airport System, Revenue Bonds | 500,000 | 532,640 | ||||||

City of Houston TX, Utility System, Revenue Bonds | 450,000 | 452,970 | ||||||

Dallas-Fort Worth International Airport, Revenue Bonds | 1,000,000 | 1,048,100 | ||||||

Fort Bend Municipal Utility District, No. 169 Contract, Revenue Bonds | ||||||||

Series A, Insured: AGM | 925,000 | 974,201 | ||||||

Series A, Insured: AGM | 465,000 | 483,730 | ||||||

Harris County Municipal Utility District No. 419, Unlimited General Obligation Insured: AGM | 735,000 | 738,116 | ||||||

Harris County-Houston Sports Authority, Revenue Bonds | 1,500,000 | 1,525,410 | ||||||

| 20 | MainStay MacKay Short Term Municipal Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

| Principal Amount | Value | |||||||

| Municipal Bonds (continued) |

| |||||||

Texas (continued) |

| |||||||

Houston Hotel Occupancy Tax Hotel Occupancy & Special, Revenue Bonds | $ | 2,900,000 | $ | 2,882,658 | ||||

Little Elm Independent School District, Capital Appreciation, Unlimited General Obligation Insured: PSF | 500,000 | 471,880 | ||||||

Montgomery County Municipal Utility District No. 46, Unlimited General Obligation | 1,455,000 | 1,455,757 | ||||||

North Central Texas Community College District, Revenue Bonds | 380,000 | 389,382 | ||||||

State of Texas, Revenue Notes | 6,000,000 | 6,043,560 | ||||||

Texas Municipal Gas Acquisition & Supply Corp. III, Revenue Bonds | 650,000 | 661,563 | ||||||

Texas State Public Finance Authority, Financing System Texas Southern University, Revenue Bonds | ||||||||

Insured: BAM | 1,000,000 | 1,000,000 | ||||||

Insured: BAM | 1,500,000 | 1,528,275 | ||||||

Viridian Municipal Management District, Road Improvement, Unlimited General Obligation | ||||||||

Insured: AGM | 505,000 | 522,549 | ||||||

Insured: AGM | 300,000 | 315,492 | ||||||

Insured: AGM | 550,000 | 587,862 | ||||||

Insured: AGM | 300,000 | 324,642 | ||||||

Viridian Municipal Management District, Utility Improvement, Unlimited General Obligation | ||||||||

Insured: AGM | 260,000 | 269,035 | ||||||

Insured: AGM | 225,000 | 236,619 | ||||||

Insured: AGM | 395,000 | 422,192 | ||||||

Insured: AGM | 305,000 | 330,053 | ||||||

|

| |||||||

| 26,698,471 | ||||||||

|

| |||||||

| Principal Amount | Value | |||||||

U.S. Virgin Islands 0.4% |

| |||||||

Virgin Islands Public Finance Authority, Revenue Bonds | $ | 1,810,000 | $ | 1,782,850 | ||||

|

| |||||||

Utah 0.2% |

| |||||||

Salt Lake City Airport Revenue | 725,000 | 772,966 | ||||||

|

| |||||||

Vermont 0.0%‡ |

| |||||||

Vermont Educational & Health Building Financing Agency, Saint Michael’s College-Green Bond, Revenue Bonds | 130,000 | 131,031 | ||||||

|

| |||||||

Virginia 2.0% |

| |||||||

Virginia Commonwealth Transportation Board, Revenue Bonds | 6,075,000 | 6,082,411 | ||||||

Virginia Public School Authority, Special Obligation, Revenue Bonds | 2,990,000 | 3,113,846 | ||||||

|

| |||||||

| 9,196,257 | ||||||||

|

| |||||||

Washington 0.3% |

| |||||||

Douglas County Public Utility Distrist No. 1, Wells Hydroelectric, Revenue Bonds | 1,170,000 | 1,219,608 | ||||||

|

| |||||||

Wisconsin 1.4% |

| |||||||

Burlington Area School District, Unlimited General Obligation | 1,000,000 | 1,000,150 | ||||||

Public Finance Authority, Affinity Living Group, Revenue Bonds | 2,000,000 | 2,003,340 | ||||||

Wisconsin State Health & Educational Facilities Authority, Advocate Aurora Health Credit Group, Revenue Bonds | 3,500,000 | 3,486,805 | ||||||

|

| |||||||

| 6,490,295 | ||||||||

|

| |||||||

Total Municipal Bonds | 446,176,358 | |||||||

|

| |||||||

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | 21 |

Portfolio of InvestmentsApril 30, 2019 (continued)

| Shares | Value | |||||||

| Closed-End Funds 0.1% |

| |||||||

Florida 0.1% |

| |||||||

BlackRock Florida Municipal 2020 Term Trust, 1.95% (e) | 34,857 | $ | 497,061 | |||||

|

| |||||||

Total Closed-End Funds | 497,061 | |||||||

|

| |||||||

TotalLong-Term Bonds | 446,673,419 | |||||||

|

| |||||||

Total Investments | 98.4 | % | 446,673,419 | |||||

Other Assets, Less Liabilities | 1.6 | 7,299,800 | ||||||

Net Assets | 100.0 | % | $ | 453,973,219 | ||||

| † | Percentages indicated are based on Fund net assets. |

| ‡ | Less than one-tenth of a percent. |

| (a) | Interest on these securities was subject to alternative minimum tax. |

| (b) | May be sold to institutional investors only under Rule 144A or securities offered pursuant to Section 4(a)(2) of the Securities Act of 1933, as amended. |

| (c) | Coupon rate may change based on changes of the underlying collateral or prepayments of principal. The coupon rate shown represents the rate at period end. |

| (d) | Variable-rate demand notes (VRDNs)—Provide the right to sell the security at face value on either that day or within the rate-reset period. VRDNs will normally trade as if the maturity is the earlier put date, even though stated maturity is longer. The interest rate is reset on the put date at a stipulated daily, weekly, monthly, quarterly, or other specified time interval to reflect current market conditions. These securities do not indicate a reference rate and spread in their description. The maturity date shown is the final maturity. |

| (e) | Current yield as of April 30, 2019. |

The following abbreviations are used in the preceding pages:

AGC—Assured Guaranty Corp.

AGM—Assured Guaranty Municipal Corp.

AMBAC—Ambac Assurance Corp.

BAM—Build America Mutual Assurance Co.

MAC—Municipal Assurance Corp.

NATL-RE—National Public Finance Guarantee Corp.

PSF—Permanent School Fund

Q-SBLF—Qualified School Bond Loan Fund

The following is a summary of the fair valuations according to the inputs used as of April 30, 2019, for valuing the Fund’s assets:

Description | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | ||||||||||||

Asset Valuation Inputs | ||||||||||||||||

| Investments in Securities (a) | ||||||||||||||||

| Long-Term Bonds | ||||||||||||||||

Municipal Bonds | $ | — | $ | 446,176,358 | $ | — | $ | 446,176,358 | ||||||||

Closed-End Funds | 497,061 | — | — | 497,061 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| Total Investments in Securities | $ | 497,061 | $ | 446,176,358 | $ | — | $ | 446,673,419 | ||||||||

|

|

|

|

|

|

|

| |||||||||

| (a) | For a complete listing of investments and their industries, see the Portfolio of Investments. |

| 22 | MainStay MacKay Short Term Municipal Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Statement of Assets and Liabilitiesas of April 30, 2019

| Assets | ||||

Investment in securities, at value | $ | 446,673,419 | ||

Cash | 1,351,102 | |||

Receivables: | ||||

Dividends and interest | 5,487,294 | |||

Fund shares sold | 1,706,807 | |||

Other assets | 56,491 | |||

|

| |||

Total assets | 455,275,113 | |||

|

| |||

| Liabilities | ||||

Payables: | ||||

Fund shares redeemed | 956,753 | |||

Manager (See Note 3) | 110,067 | |||

Transfer agent (See Note 3) | 27,072 | |||

NYLIFE Distributors (See Note 3) | 23,731 | |||

Shareholder communication | 19,540 | |||

Custodian | 10,108 | |||

Professional fees | 6,248 | |||

Trustees | 200 | |||

Accrued expenses | 3,274 | |||

Dividend payable | 144,901 | |||

|

| |||

Total liabilities | 1,301,894 | |||

|

| |||

Net assets | $ | 453,973,219 | ||

|

| |||

| Composition of Net Assets | ||||

Shares of beneficial interest outstanding (par value of $.001 per share) unlimited number of shares authorized | $ | 47,379 | ||

Additional paid-in capital | 453,291,308 | |||

|

| |||

| 453,338,687 | ||||

Total distributable earnings (loss)(1) | 634,532 | |||

|

| |||

Net assets | $ | 453,973,219 | ||

|

| |||

Class A | ||||

Net assets applicable to outstanding shares | $ | 113,023,188 | ||

|

| |||

Shares of beneficial interest outstanding | 11,794,192 | |||

|

| |||

Net asset value per share outstanding | $ | 9.58 | ||

Maximum sales charge (1.00% of offering price) | 0.10 | |||

|

| |||

Maximum offering price per share outstanding | $ | 9.68 | ||

|

| |||

Investor Class | ||||

Net assets applicable to outstanding shares | $ | 3,833,657 | ||

|

| |||

Shares of beneficial interest outstanding | 398,957 | |||

|

| |||

Net asset value per share outstanding | $ | 9.61 | ||

Maximum sales charge (1.00% of offering price) | 0.10 | |||

|

| |||

Maximum offering price per share outstanding | $ | 9.71 | ||

|

| |||

Class I | ||||

Net assets applicable to outstanding shares | $ | 337,116,374 | ||

|

| |||

Shares of beneficial interest outstanding | 35,186,042 | |||

|

| |||

Net asset value and offering price per share outstanding | $ | 9.58 | ||

|

|

| (1) | See Note 10. |

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | 23 |

Statement of Operationsfor the year ended April 30, 2019

| Investment Income (Loss) | ||||

Income | ||||

Interest | $ | 7,461,410 | ||

Dividends | 3,207 | |||

|

| |||

Total income | 7,464,617 | |||

|

| |||

Expenses | ||||

Manager (See Note 3) | 1,319,543 | |||

Distribution/Service—Class A (See Note 3) | 254,152 | |||

Distribution/Service—Investor Class (See Note 3) | 8,528 | |||

Transfer agent (See Note 3) | 143,503 | |||

Registration | 91,284 | |||

Professional fees | 79,128 | |||

Shareholder communication | 28,955 | |||

Custodian | 23,452 | |||

Trustees | 9,023 | |||

Miscellaneous | 18,992 | |||

|

| |||

Total expenses before waiver/reimbursement | 1,976,560 | |||

Expense waiver/reimbursement from Manager (See Note 3) | (139,397 | ) | ||

|

| |||

Net expenses | 1,837,163 | |||

|

| |||

Net investment income (loss) | 5,627,454 | |||

|

| |||

| Realized and Unrealized Gain (Loss) on Investments and Futures Contracts |

| |||

Net realized gain (loss) on: | ||||

Investment transactions | (231,522 | ) | ||

Futures transactions | (22,623 | ) | ||

|

| |||

Net realized gain (loss) on investments and futures transactions | (254,145 | ) | ||

|

| |||

Net change in unrealized appreciation (depreciation) on investments | 2,888,874 | |||

|

| |||

Net realized and unrealized gain (loss) on investments and futures transactions | 2,634,729 | |||

|

| |||

Net increase (decrease) in net assets resulting from operations | $ | 8,262,183 | ||

|

| |||

| 24 | MainStay MacKay Short Term Municipal Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Statements of Changes in Net Assets

for the years ended April 30, 2019 and April 30, 2018

| 2019 | 2018 | |||||||

| Increase (Decrease) in Net Assets |

| |||||||

Operations: | ||||||||

Net investment income (loss) | $ | 5,627,454 | $ | 3,518,928 | ||||

Net realized gain (loss) on investments and futures contracts | (254,145 | ) | (261,068 | ) | ||||

Net change in unrealized appreciation (depreciation) on investments and futures contracts | 2,888,874 | (1,241,965 | ) | |||||

|

| |||||||

Net increase (decrease) in net assets resulting from operations | 8,262,183 | 2,015,895 | ||||||

|

| |||||||

Distributions to shareholders(1): | ||||||||

Class A | (1,304,594 | ) | ||||||

Investor Class | (27,705 | ) | ||||||

Class I | (4,296,551 | ) | ||||||

|

| |||||||

| (5,628,850 | ) | |||||||

|

| |||||||

Dividends to shareholders from net investment income: | ||||||||

Class A | (1,323,485 | ) | ||||||

Investor Class | (18,646 | ) | ||||||

Class I | (2,176,761 | ) | ||||||

|

| |||||||

Total dividends and distributions to shareholders | (5,628,850 | ) | (3,518,892 | ) | ||||

|

| |||||||

Capital share transactions: | ||||||||

Net proceeds from sale of shares | 438,680,545 | 199,137,746 | ||||||

Net asset value of shares issued to shareholders in reinvestment of dividends | 4,248,851 | 2,701,265 | ||||||

Cost of shares redeemed | (251,882,183 | ) | (255,509,908 | ) | ||||

|

| |||||||

Increase (decrease) in net assets derived from capital share transactions | 191,047,213 | (53,670,897 | ) | |||||

|

| |||||||

Net increase (decrease) in net assets | 193,680,546 | (55,173,894 | ) | |||||

| Net Assets | ||||||||

Beginning of year | 260,292,673 | 315,466,567 | ||||||

|

| |||||||

End of year(2) | $ | 453,973,219 | $ | 260,292,673 | ||||

|

| |||||||

| (1) | For the year ended April 30, 2019, the requirement to disclose dividends and distributions paid to shareholders from net investments income and/or net realized gain on investments was modified and are now presented together as distributions to shareholders. (See Note 10) |

| (2) | End of year net assets includes undistributed (overdistributed) net investment income of $(8,709) in 2018. The requirement to disclose the corresponding amount as of April 30, 2019 was eliminated. See Note 4 for tax basis of distributable earnings. (See Note 10) |

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | 25 |

Financial Highlightsselected per share data and ratios

| Year ended April 30, | November 1, 2014 through April 30, | Year ended October 31, | ||||||||||||||||||||||

| Class A | 2019 | 2018 | 2017 | 2016 | 2015* | 2014 | ||||||||||||||||||

Net asset value at beginning of period | $ | 9.51 | $ | 9.56 | $ | 9.61 | $ | 9.54 | $ | 9.54 | $ | 9.59 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net investment income (loss) (a) | 0.12 | 0.10 | 0.08 | 0.07 | 0.01 | 0.04 | ||||||||||||||||||

Net realized and unrealized gain (loss) on investments | 0.07 | (0.05 | ) | (0.05 | ) | 0.06 | 0.01 | (0.03 | ) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total from investment operations | 0.19 | 0.05 | 0.03 | 0.13 | 0.02 | 0.01 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| Less dividends and distributions: | ||||||||||||||||||||||||

From net investment income | (0.12 | ) | (0.10 | ) | (0.08 | ) | (0.06 | ) | (0.01 | ) | (0.04 | ) | ||||||||||||

From net realized gain on investments | — | — | (0.00 | )‡ | — | (0.01 | ) | (0.02 | ) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total dividends and distributions | (0.12 | ) | (0.10 | ) | (0.08 | ) | (0.06 | ) | (0.02 | ) | (0.06 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net asset value at end of period | $ | 9.58 | $ | 9.51 | $ | 9.56 | $ | 9.61 | $ | 9.54 | $ | 9.54 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total investment return (b) | 2.04 | %(c) | 0.54 | % | 0.27 | % | 1.41 | % | 0.27 | % | 0.09 | % | ||||||||||||

| Ratios (to average net assets)/Supplemental Data: | ||||||||||||||||||||||||

Net investment income (loss) | 1.28 | % | 1.06 | % | 0.79 | % | 0.69 | % | 0.33 | %†† | 0.41 | % | ||||||||||||

Net expenses | 0.71 | % | 0.80 | % | 0.80 | % | 0.80 | % | 0.86 | %†† | 0.86 | % | ||||||||||||

Expenses (before waiver/reimbursement) | 0.71 | % | 0.84 | % | 0.84 | % | 0.94 | % | 1.24 | %†† | 1.07 | % | ||||||||||||

Portfolio turnover rate | 96 | % | 69 | % | 85 | % | 66 | % | 7 | % | 30 | % | ||||||||||||

Net assets at end of period (in 000’s) | $ | 113,023 | $ | 98,982 | $ | 147,029 | $ | 111,768 | $ | 18,908 | $ | 20,086 | ||||||||||||

| †† | Annualized. |

| ‡ | Less than one cent per share. |

| * | The Fund changed its fiscal year end from October 31 to April 30. |

| (a) | Per share data based on average shares outstanding during the period. |

| (b) | Total investment return is calculated exclusive of sales charges and assumes the reinvestment of dividends and distributions. For periods of less than one year, total return is not annualized. |

| (c) | Total investment return may reflect adjustments to conform to generally accepted accounting principles. |

| Year ended April 30, | November 1, 2014 through April 30, | Year ended October 31, | ||||||||||||||||||||||

| Investor Class | 2019 | 2018 | 2017 | 2016 | 2015* | 2014 | ||||||||||||||||||

Net asset value at beginning of period | $ | 9.54 | $ | 9.59 | $ | 9.64 | $ | 9.56 | $ | 9.57 | $ | 9.61 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net investment income (loss) (a) | 0.08 | 0.06 | 0.04 | 0.03 | (0.00 | )‡ | 0.01 | |||||||||||||||||

Net realized and unrealized gain (loss) on investments | 0.07 | (0.05 | ) | (0.05 | ) | 0.07 | 0.00 | ‡ | (0.02 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total from investment operations | 0.15 | 0.01 | (0.01 | ) | 0.10 | 0.00 | ‡ | (0.01 | ) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| Less dividends and distributions: | ||||||||||||||||||||||||

From net investment income | (0.08 | ) | (0.06 | ) | (0.04 | ) | (0.02 | ) | (0.00 | )‡ | (0.01 | ) | ||||||||||||

From net realized gain on investments | — | — | (0.00 | )‡ | — | (0.01 | ) | (0.02 | ) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total dividends and distributions | (0.08 | ) | (0.06 | ) | (0.04 | ) | (0.02 | ) | (0.01 | ) | (0.03 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net asset value at end of period | $ | 9.61 | $ | 9.54 | $ | 9.59 | $ | 9.64 | $ | 9.56 | $ | 9.57 | ||||||||||||

|

|

|

|