Graubard Miller

The Chrysler Building

405 Lexington Avenue

New York, N.Y. 10174-1901

(212) 818-8800

| facsimile | direct dial number | |

| (212) 818-8881 | (212) 818-8638 | |

| email address | ||

| jgallant@graubard.com |

October 2, 2009

VIA EDGAR AND FEDERAL EXPRESS

Mr. H. Roger Schwall

Assistant Director

Securities and Exchange Commission

100 F Street, N.E.

Washington, DC 20549

| Re: | Cullen Agricultural Holding Corp. |

| Form S-4, Filed September 8, 2009, as amended 9/10/09 and 9/15/09 |

| File No. 333-161773 |

| Triplecrown Acquisition Corp. |

| Preliminary Schedule 14A, Filed September 8, 2009 |

| File No. 001-33698 |

Dear Mr. Schwall:

On behalf of Cullen Agricultural Holding Corp. (the “Company”) and Triplecrown Acquisition Corp. (“Triplecrown”), we respond as follows to the Staff’s comment letter, dated September 29, 2009, relating to the above-captioned Registration Statement. Captions and page references herein correspond to those set forth in the Registration Statement, a copy of which has been marked with the changes from the original filing of the Registration Statement. We are also delivering three (3) courtesy copies of such marked Registration Statement to Norman Gholson of your office.

Please note that for the Staff’s convenience, we have recited each of the Staff’s comments and provided the Company’s response to each comment immediately thereafter.

Form S-4 Filed September 8, 2009, as amended September 10 and September 15, 2009

General

| 1. | Where comments on one section or document apply to other disclosure or documents, please make related changes to all affected disclosure. This will eliminate the need for us to issue repetitive comments. References throughout this letter to “you” or “your” refer to Cullen Agricultural Holding Corp., Triplecrown Acquisition Corp., or their respective affiliates, depending on the context. |

Duly noted. We will make related changes to all affected disclosure as requested.

Securities and Exchange Commission

October 2, 2009

Page 2

Calculation of Registration Fee

| 2. | Identify in the fee table the provision of Rule 457 pursuant to which you determined the maximum offering price. |

We have revised the fee table to indicate the price per security is estimated pursuant to Rule 457(f)(1) as requested.

Proposed Timing and Related Issues

| 3. | You filed the Form S-4 registration statement on September 8, 2009. We note that Triplecrown Acquisition Corp. will be required to dissolve and liquidate if no business combination occurs by October 22, 2009. See page 5. Provide us with a detailed, written explanation of the proposed and contemplated timetable that you believe will be necessary under these circumstances, including the date and time by which you believe the Form S-4 would need to be declared effective. Make clear in your supplemental explanation of timing whether you are allowing time for the adjournments to which you refer throughout the document. |

Triplecrown currently anticipates holding its special meetings of stockholders and warrantholders on October 21, 2009. This would allow Triplecrown one day to adjourn the meetings if necessary. Assuming approval of the proposals presented at the stockholders and warrantholders meetings, the parties would file the necessary charter amendments and certificates of merger with the Delaware Secretary of State following the meeting prior to midnight on October 22, 2009, the date Triplecrown is required to be liquidated if it has not completed a business combination by such time. We have confirmed with the Delaware Secretary of State that they will be able to receive such filings at any time prior to midnight on such date. As long as the filing is received by such time, it will automatically be filed as of such date. Triplecrown does not anticipate seeking an extension of its corporate existence for a limited period of time after October 22, 2009 to complete the business combination.

Securities and Exchange Commission

October 2, 2009

Page 3

Pursuant to Section 253 of the Delaware General Corporation Law, notice of Triplecrown’s meetings must be sent to stockholders and warrantholders at least 20 days prior to the date of the meetings. Accordingly, notice of the meeting was sent to Triplecrown’s stockholders and warrantholders on October 1, 2009. Such notice contained information on a holders’ ability to exercise conversion and appraisal rights. The federal securities laws do not require any greater notice of the transaction. Triplecrown is hopeful to address all of the Staff’s comments and have the Registration Statement declared effective on October 7 or 8 in order to print the definitive proxy statement/prospectus and mail such document to Triplecrown’s stockholders and warrantholders by October 9, 2009, thereby providing holders with 12 days to review the materials distributed. Additionally, once the Registration Statement is declared effective, Triplecrown intends to file a Current Report on Form 8-K and issue a press release so that the public is aware that the documents are available for review online at the SEC’s website. Triplecrown believes such timing would provide stockholders and warrantholders a sufficient amount of time to receive the information and vote on the proposals

| 4. | In your response, set forth the applicable requirements under state and federal law in terms of timing, and make clear how your proposed timetable would comply with those requirements. Include in your discussion the various components, including such items as the filings that would need to be made with the Delaware Secretary of State and the normal processing time for such filings. In that regard, we note also the 14-day and 20-day periods referenced at pages 51 and 55, respectively. |

We refer the Staff to our response to Comment 3 above.

| 5. | Also include your timing analysis in the event that you decide to provide security holders with a separate vote to consider solely the extension of Triplecrown’s corporate existence for a limited period of time after October 22, 2009, if that is an option you are considering. Such a separate vote would of course provide you with more time to respond to staff comments and enable security holders to have adequate time to receive, consider, and vote upon the merger proposal and the other proposals at issue. |

The Company does not anticipate seeking an extension.

| 6. | Explain to us how those voting or converting their shares can do so electronically, including whether there are limitations on the ability of all holders to do so. Make clear what the actual deadlines for such voting or conversion would be in each case. If you will make internet or toll-free telephone voting available to security holders, disclose all necessary details. We note the disclosure regarding voting procedures at page 29. |

We have revised the disclosure on the notice page and pages 8, 9, 11, 12, 39 and 62 of the Registration Statement as requested.

| 7. | In light of the expedited timetable you desire for our processing of your filing, please respond in necessary detail to each portion of each comment that we issue. You will facilitate our review by providing us with clearly and precisely marked versions of (1) the amended disclosure and (2) each exhibit or other document that changes in response to staff comment. Also, in your letter of response, please provide explicit references to the precise page(s) in the marked version of the amendment where the changes appear in response to each comment. |

Duly noted. We have complied with the Staff’s request to the extent possible.

Securities and Exchange Commission

October 2, 2009

Page 4

| 8. | Please submit via EDGAR as .pdf files the precisely marked electronic versions of all changed documents. In that regard, the additional detail that appears in the paper versions you provide will expedite our review if it is also available to us electronically. |

We will submit via EDGAR as .pdf files precisely marked electronic versions of the Registration Statement as requested.

| 9. | You have not yet filed all the required exhibits. With your next amendment, file all remaining exhibits so that you will have an opportunity to respond to any comments that we might issue after having had the chance to see them. In that regard, all contracts, exhibits, and annexes should be provided in the final, signed form, to the extent available. Among items that require filing would be all voting and lockup agreements, including the warrant lockup agreement cited at page 3. All outstanding issues must be resolved prior to your requesting accelerated effectiveness of the Form S-4 registration statement. |

Duly noted. We have filed all remaining exhibits with this filing of the Registration Statement. Please note that the voting and lockup agreements have been removed from the disclosure in the Registration Statement as they will not be sought.

Cover Page

| 10. | Make clear on the cover page what options security holders might have, as well as the timing within which these decisions must be made. Ensure that you cover not only conversion rights but also appraisal rights and potential securities law claims for rescission and damages. Currently, appraisal rights and potential securities law claims for rescission and damages are not mentioned until page 6. Explain in necessary detail the potential impact on these other options from voting or seeking conversion. |

We have revised the disclosure on the cover page of the prospectus as requested.

| 11. | Highlight on the cover page the various options, and expand your related disclosure elsewhere in the document to provide necessary detail about how each of these matters interacts with the others. Summarize on the cover page, and at an appropriate place in the document, provide a comprehensive explanation of the legal impact in each case of abstaining, voting against a proposal, or voting in favor of a proposal. For example, if voting in favor of the merger proposal could adversely impact potential damages claims, disclose this. |

We have revised the disclosure on the cover page of the prospectus and page 39 of the Registration Statement as requested.

Securities and Exchange Commission

October 2, 2009

Page 5

| 12. | Provide on the cover page the most salient information, and limit it to one page. Eliminate extraneous information, such as much of the text that appears in lines 2 through 5 of the first paragraph. |

We have revised the disclosure on the cover page of the prospectus as requested.

| 13. | Identify the conflicts of interest on the cover page and, at each place the recommendations of the board appear, disclose the conflicts in equally prominent type. Identify those with conflicts, naming Mr. Watson, and briefly identify the nature of the conflicts. Include an entry in the table of contents for the expanded conflicts of interest section which currently appears at page 49, but which should appear immediately following the Risk Factors section. Add a new question and answer to identify briefly the conflicts. With a view toward disclosure, identify the consultants who will receive stock if the reorganization occurs. |

We have revised the disclosure on the cover page of the prospectus, the table of contents on page “i” and pages 9, 35 and 36 of the Registration Statement as requested.

| 14. | Highlight on the cover page, in the notice, and elsewhere the potential adverse tax consequences regarding the warrants noted in the Graubard tax opinion. |

We have revised the disclosure on the cover page, the notice and elsewhere to discuss the potential adverse tax consequences of the transaction as requested.

| 15. | In the first paragraph of the final prospectus cover page used to sell the shares in your initial public offering, you state that you were formed for the purpose of acquiring an operating business in the financial services industry. You state throughout that prospectus that the combination must be with a target with a fair market value of at least 80% of the trust account balance. Furthermore, you state at page 13 and elsewhere in the 1PO prospectus that “We will not consummate a business combination with any target business affiliated with any of our officers, directors or founders.” Disclose prominently on the Form S-4 cover page that the prospectus you used to offer and sell your shares made clear throughout that your charter prohibits, and that you would not complete, the type of business combination that you now propose. |

We have revised the disclosure on the cover page of the prospectus as requested.

Securities and Exchange Commission

October 2, 2009

Page 6

Other General Comments

| 16. | Make clear throughout the document, including in the forepart, what raw and percentage vote is required for each of the various proposals or to result in more than the 30% conversion threshold. Describe how the existence of the separate founders’ securities and any lockup agreements impacts the percentage or numbers required in each case. For example, if as a result of the warrant lockup agreement the percentage of votes necessary to defeat the warrant amendment proposal is in fact greater than 50% of the warrants held by those not party to the agreement, disclose the particulars. Make corresponding revisions to the “Vote of Triplecrown’s Stockholders Required” and “Vote of Triplecrown’s Warrantholders Required” sections at page 28. |

We have revised the disclosure on page 39 of the Registration Statement as requested. Please note that the voting and lockup agreements have been removed from the disclosure in the Registration Statement as they will not be sought.

| 17. | We note that the proposals to be submitted to stockholders and warrantholders currently are numbered on the relevant proxy cards in a manner that differs from the manner in which they are numbered in the notices of meetings and the preliminary Proxy Statement. Use a consistent numbering system for the proposals throughout the notices of meetings, the Proxy Statement and the proxy cards, or explain why you believe such consistency is unnecessary. |

We have revised the disclosure on the notices to keep the numbering of the proposals consistent with the proxy cards as requested.

| 18. | It appears that there may be items which should be disclosed separately and upon which stockholders should be provided an opportunity to vote separately. Please refer to Rule 14a-4(a)(3) of the Exchange Act of 1934. For example, we note the disclosure in the notice to stockholders that stockholder approval will no longer be required to increase or decrease the authorized amounts of common stock and preferred stock, but the form of proxy does not provide stockholders with a separate vote on this matter. |

We have removed the above-referenced disclosure on increasing or decreasing authorized amounts of stock from the Registration Statement as such information was mistakenly included in this filing. Accordingly, we respectfully do not believe that any additional information need be presented separately.

Securities and Exchange Commission

October 2, 2009

Page 7

| 19. | At the first time each defined term, such as Public Shares or Founders appears, define the term. In the alternative and at a minimum, provide the reader with a reference to the precise page where the definition appears. For example, you first define “Natural Dairy” at page 107 and it appears that one can derive the definition of Founders from text at page 125. Also eliminate or explain the references in your document to Two Harbors. |

The term “Triplecrown Founders” was defined on page 1 of the initial filing of the Registration Statement. We have revised the disclosure on page 2 of the Registration Statement to define the terms “Public Shares” and “Natural Dairy” as requested. We have further revised the disclosure on page 63 of the Registration Statement to replace the reference of “Two Harbors” with “CAH.”

| 20. | Update disclosure to provide current information throughout your document, eliminating blanks where such information is known. Where such information is subject to change, you may so indicate by the use of brackets, as you appear to have done at page 97. Among items requiring updates are the following, which comprise a non-exhaustive list: |

| · | Final results of ongoing negotiations with the underwriters regarding the deferred underwriting compensation; |

| · | Identities of all directors and officers of each entity and affiliates, such as Natural Dairy, both prior to and after consummation of the reorganization; |

| · | The number and percentage of holders referenced at page 51 as holding their securities in street name; and |

| · | Confirmation that the land sale was in fact closed on or prior to September 15, 2009, as scheduled. |

We have revised the disclosure throughout the Registration Statement to update the disclosure to the extent currently possible as requested.

| 21. | In the forepart of the document, provide charts to show all parties, material affiliates, their ownership structure, and percentage of ownership, both prior to and as a result of the reorganization. Also provide detailed tabular disclosure to clarify the ownership structure assuming maximum conversion and assuming minimum conversion. |

We have revised the disclosure on pages 6 and 7 of the Registration Statement as requested.

| 22. | Provide us with the numbers of record holders of each security, as well as the percentage of each security that is held of record. Provide us with an estimate as to the number of beneficial holders. |

We have revised the disclosure on page 153 of the Registration Statement as requested. Please note that all securities are held of record.

Securities and Exchange Commission

October 2, 2009

Page 8

| 23. | With regard to the conversion option, confirm whether electronic delivery will be available to all holders, providing the details in each case. We note the related disclosure in the notice and at page 5, for example. |

We have revised the disclosure on the notice and pages 7 and 62 of the Registration Statement to indicate that delivery may be effected by all stockholders either physically or electronically at the holder’s option.

| 24. | Explain the assertion in the last paragraph on page 5 that the warrants would have terms that are “substantially similar in all material respects,” notwithstanding the “subject to the amendments” text that follows. In that regard, if these warrants in fact would be deemed to constitute a new security, revise the corresponding text to make this clear. In that regard, we also note numbered paragraph 9 in the Graubard tax opinion. |

We have revised the disclosure on page 9 of the Registration Statement to clarify that the warrants to be received will be the same as the Triplecrown warrants except for the amendments contemplated by the warrant amendment proposals. The warrants to be received by holders in exchange for their Triplecrown warrants will constitute a different security solely from a tax perspective pursuant to the rules and regulations of the Internal Revenue Services (as reflected in our opinion).

| 25. | We note your disclosure on page 37 and elsewhere that approximately $539 million is held in deposit in the trust account. We also note your disclosure that the aggregate merger consideration implies a total value of Cullen Agritech of $155 million. This is approximately 29% of the amount in the trust account. In view of the large difference between the value of the target company and the amount in the trust account, please explain and quantify in greater detail how the amounts in the trust account are anticipated to be used if the merger is approved. Also revise all references to the fair market value merely being “less than 80%” and instead making clear that rather than 80% it is 29% or providing other appropriate text to make clear the magnitude of the difference. |

With respect to the first part of the Staff’s comment, the following disclosure was included in the initial filing of the Registration Statement (initially on page 3):

At the closing of the merger, the funds in Triplecrown’s trust account will be released to pay transaction fees and expenses (including the balance of the purchase price for the land to be used by CAH following consummation of the merger), deferred underwriting discounts and commissions, tax liabilities, if any, and reimbursement of expenses of the Triplecrown Founders and to make purchases of Public Shares, if any. The balance of the funds will be released to CAH to pay Triplecrown stockholders who properly exercise their conversion rights and for working capital and general corporate purposes of CAH and Cullen Agritech. Additionally, if CAH has access to more than $150 million after closing of the merger, CAH may use such funds, depending on market conditions, to repurchase shares of common stock.

Securities and Exchange Commission

October 2, 2009

Page 9

We have revised the foregoing disclosure on pages 3, 9, 45 and 95 to provide greater quantification of the known expenses as well as the intended uses following the merger.

With respect to the second part of the Staff’s comment, we have revised the disclosure on pages 1, 42 and 48 of the Registration Statement as requested.

| 26. | We note the disclosure throughout this document that Triplecrown may utilize proceeds from the trust to enter into purchase transactions with stockholders to ensure that less than 30% of its stockholders vote against the transaction and seek conversion of their shares. At certain points in the document, for example on pages 52 and 53, you appear to state that there is a limitation on the price you would offer to purchase the shares. Please revise to address this issue each time you discuss these possible purchase transactions. |

We have revised the disclosure on pages 3 and 44 of the Registration Statement as requested.

| 27. | Clarify further how Triplecrown will select which stockholders from whom to purchase shares. Also, if it decides to extend the time period to solicit additional votes, clarify whether Triplecrown will select stockholders who have already submitted votes via proxy or at the meeting, and have made their conversion demands. |

As indicated on page 63 of the Registration Statement, Triplecrown would approach a limited number of large holders of stock that have voted against the merger proposal and demanded conversion of their shares, or that have indicated an intention to do so, and enter into the above-referenced transactions. Accordingly, we respectfully believe the Staff’s comment is already addressed in the disclosure. Therefore, we have not revised the disclosure in the Registration Statement in response to this comment.

| 28. | We note your disclosure on page 52 that Triplecrown, the Triplecrown Founders, Cullen Agritech or their respective affiliates may offer to purchase Triplecrown’s common stock issued in Triplecrown’s initial public offering. Please provide us a detailed analysis of the applicability of the tender offer rules, including Rule 13e-4 and Regulation 14E, to those offers and/or purchases. |

While the Securities and Exchange Commission has not yet defined the term “tender offer,” it has provided a set of seven elements as being characteristic of a tender offer as described in Wellman v. Dickinson and in other cases. As set forth below, we do not believe that a majority of these elements would be present in the purchase of public shares as described in the Registration Statement. Accordingly, we do not believe the tender offer rules are applicable to such purchases.

Securities and Exchange Commission

October 2, 2009

Page 10

(a) Active and widespread solicitation of public shareholders for the shares of an issuer. Triplecrown, the Triplecrown Founders, Cullen Agritech and their respective affiliates do not intend to engage in any type of active or widespread solicitation of public stockholders for Triplecrown’s stock. Instead, purchases would be made in private transactions in specific individual instances with sophisticated investors, if at all.

(b) Solicitation made for a substantial percentage of the issuer’s stock. It is possible that purchases could rise to a percentage that would be substantial enough to be considered the type of purchases contemplated by this element. However, as there is no set amount of purchases that will definitely be made, it is possible that a smaller percentage of shares would be purchased.

(c) Offer to purchase made at a premium over the prevailing market price. It is anticipated that any purchases would be made at the current per-share price that would be offered to stockholders who vote no against the proposed business combination and seek conversion of their shares. Accordingly, stockholders who enter into purchase arrangements with Triplecrown would be treated no better than a stockholder who did not enter into such arrangement but sought conversion of his shares instead.

(d) Terms of the offer are firm rather than negotiable. As indicated above, purchases, if any, will be done in private transactions in specific individual instances. Therefore the terms will be negotiable based on each specific transaction.

(e) Offer contingent on the tender of a fixed number of shares, often subject to a fixed maximum number to be purchased. As indicated above, purchases will be done on an individual basis rather than being tied to a fixed maximum number to be purchased.

(f) Offer open only a limited period of time. Purchases could be made at any time up to the meeting of stockholders at which the business combination is to be approved. Triplecrown has until October 22, 2009 to complete the business combination. Accordingly, purchases could last several weeks.

(g) Offeree subjected to pressure to sell his stock. As indicated above, since the purchases could last for several weeks, there is not the type of pressure on stockholders to rush into “hurried, uninformed” investment decisions that the tender offer rules were designed to protect against. Furthermore, unlike a regular non-blank check company, since a stockholder will always have the right to vote no against the proposed business combination and seek conversion and receive the same price, there is absolutely no pressure for such stockholder to sell his shares.

Securities and Exchange Commission

October 2, 2009

Page 11

When considering the totality of the circumstances in the present instance, we respectfully submit that any tender offer concerns should not apply. In the Hanson Trust case, 774 F.2d 47 (2d Cir. 1985), the Second Circuit declined to elevate Wellman to a ‘litmus test’, and stated that the question — whether a solicitation constitutes a “tender offer” within the meaning of Section 14(d) — turns on whether, viewing the transaction in the light of the totality of the circumstances, there appears to be a likelihood that unless the pre-acquisition filing requirements of Section 14(d) are followed there will be a substantial risk that solicitees will lack information needed to make a carefully considered appraisal of the proposal put before them.1 Triplecrown and the Company currently have a robust and fulsome disclosure document, the proxy statement/prospectus, on file with the Commission and freely available to all stockholders. Accordingly, stockholders have all the information available to them necessary to make a carefully considered appraisal of the proposal put before them. Further, the type of holder that would typically be approached by Triplecrown and Cullen Agritech regarding the above-referenced purchases are sophisticated, institutional holders – investors that do not lack for information. Accordingly, we do not believe that the tender offer rules apply to this transaction.

| 29. | We note your disclosure of possible side transactions by Triplecrown, the Triplecrown Founders, Cullen Agritech and their respective affiliates with potential investors or existing holders of Public Shares in order to induce them to purchase Public Shares and/or vote in favor of the merger proposal with respect to currently owned Public Shares and, in each case, to remain a stockholder of CAH following consummation of the merger. You state on page 52 that “there would be no limit on the consideration that may be paid pursuant to these arrangements.” If Triplecrown, Cullen Agritech and their respective affiliates might offer more than the conversion price in these side transactions, please revise to explain how paying a premium to change the votes, which reflect stockholder intent, would be in the best interests of all stockholders. |

We have clarified the disclosure on page 63 of the Registration Statement to indicate that Triplecrown will not be entering into the above-refferenced side transactions with potential investors or existing holders of public shares in order to induce them to purchase public shares or vote in favor of the merger proposal. The only transactions that Triplecrown will be entering into will result in Triplecrown purchasing public shares with a maximum purchase price of the per-share conversion price. Transactions with potential investors or existing stockholders to induce them to purchase stock or vote "yes" with respect to already-owned stock would be undertaken only by the Triplecrown Founders or Cullen Agritech and their respective affiliates in their individual capacities and not on behalf of Triplecrown. Accordingly, since any premiums would be paid by these persons and not Triplecrown, it is in the best interests of all stockholders since it allows the transaction to be approved without any impact to Triplecrown.

1 Although one court, S-G Securities v. Fuqua Investment Co. 466 F.Supp. 1114 (D.Mass.1978). 587 F.Supp. at 1256-57, has applied a two prong test to determine if a tender offer is occurring — (1) A publicly announced intention by the purchaser to acquire a block of the stock of the target company for purposes of acquiring control thereof, and (2) a subsequent rapid acquisition by the purchaser of large blocks of stock through open market and privately negotiated purchases – that case involved a publicly announced program that already met many of the Wellman factors and there was a noted lack of adequate disclosure available to securityholders. As indicated above, this present situation does not meet many of the Wellman factors and there is significant disclosure available to securityholders. Therefore, we respectfully believe that such analysis should not apply to the present circumstances.

Securities and Exchange Commission

October 2, 2009

Page 12

| 30. | Similarly, explain how the payment of consideration to only certain stockholders so that they purchase Public Shares or vote in favor of the merger proposal, would be fair to and in the best interests of all stockholders, including those who will not be offered or receive any such consideration. In the alternative, make clear that such arrangements clearly would not be fair to and in the best interests of those stockholders not receiving such consideration. Provide corresponding risk factors disclosure, as appropriate. |

As indicated in response to comment 29 above, since Triplecrown will not be entering into these types of arrangements, Triplecrown is not paying consideration to "only certain stockholders." Furthermore, since any premiums would be paid by the persons who are entering into these arrangements (Triplecrown Founders, Cullen Agritech and their respective affiliates) and not Triplecrown, it is in the best interests of all stockholders since it allows the transaction to be approved without any financial impact on Triplecrown. Accordingly, we respectfully believe that this comment is no longer applicable and have not revised the disclosure in the Registration Statement in response thereto.

| 31. | Explain whether Eric J. Watson and Dr. Richard H. Watson are related to one another. If so, make appropriate disclosures. If not, so state. |

We have revised the disclosure on pages 3, 4 and 133 of the Registration Statement as requested.

Conflicts of Interest

| 32. | In the revised section you provide in response to comment 13 of this letter, describe all financial and other material conflicts of interest in necessary detail. For example, provide quantification and details regarding the aggregate potential financial impact on the value of each individual’s securities if the transaction were not to occur and the company were forced to liquidate. Also disclose clearly the aggregate amount when all directors’ interests are combined. In addition to providing the information based on current market values, you also may discuss the amount at issue based upon the purchase price of the various securities at issue. Clearly present the potential losses and gains in each case. |

We have revised the disclosure on pages 35 and 36 of the Registration Statement.

Securities and Exchange Commission

October 2, 2009

Page 13

Conditions to Completion of the Merger

| 33. | Notwithstanding the disclosure that appears at page 63, provide in the forepart a summary of the material conditions to completion of the merger. Disclose explicitly which if any conditions have been satisfied, and state if true that any and all conditions are waivable. Also disclose for each listed condition whether the waiver of a given condition would be deemed material and would warrant resolicitation of the vote. If no condition rises to the level of resolicitation if waived, state this clearly. |

With respect to the first part of the Staff’s comment, we have revised the disclosure on pages 2 and 76 of the Registration Statement as requested.

With respect to the second part of the Staff’s comment, we have revised the disclosure on page 76 of the Registration Statement to indicate that, except for the waiver of the condition to approve the warrant amendments, the parties will not grant any waiver of a material condition. Accordingly, resolicitation in those instances would not be required. With respect to the warrant amendments, the disclosure already advises holders to assume that the amendments will not be approved, so a waiver of that condition will not require resolicitation either.

| 34. | If a material condition were to be waived, disclose the minimum number of full business days in advance of the meeting you would notify those voting of the waiver, and explain how they would be notified. Disclose the date after which you would not waive any material conditions. Discuss whether in each such case, holders would be able to change their votes by electronic means up to the date and time of the meeting. We note the related disclosure under “Waiver’ at page 64. In that connection, explain why at page 65 you indicate that you would send out a supplement with regard to an amendment to the merger agreement only if such amendment is material. |

As indicated in response to comment 33 above, we have revised the disclosure on page 76 of the Registration Statement to indicate that, except for the waiver of the condition to approve the warrant amendments, the parties will not grant any waiver of a material condition.

Summary of the Material Terms of the Merger, page 1

| 35. | We note your disclosure that “Cullen Agritech will provide advisory services associated with the implementation of efficient farming techniques and promote a methodology that incorporates components of New Zealand’s pasture-based fanning system. Cullen Agritech’s principle [sic] focus will be to improve agricultural yields through forage and animal sciences.” It is not clear from this disclosure, or from other disclosures in the document, if Cullen Agritech’s principal focus is to improve other entities’ agricultural yields via advisory services, or the yields of the dairy farming operation carried out by Natural Dairy Inc., or both. Please expand your disclosures here, and elsewhere in the document where necessary, to clearly explain the expected business activities of Cullen Agritech. |

We have revised the disclosure on the cover page of the prospectus as well as pages 1, 46, 105, 118, 127, F-1 and F-7 as requested.

Securities and Exchange Commission

October 2, 2009

Page 14

| 36. | You indicate at page 1 and elsewhere that none of the other opportunities “were believed to be as attractive to public stockholders as the proposed merger.” Provide more context to this conclusion, including a discussion of those attributes which may be viewed objectively as less favorable or attractive. For example, it would appear unlikely that any of the other opportunities involved affiliates or possible targets which essentially had no assets, employees, or operations. |

We currently provide investors with the material positive and adverse factors that Triplecrown’s board of directors considered in approving the transaction in the sections entitled “The Merger Proposal – Triplecrown’s Board of Directors’ Reasons for the Approval of the Merger” and “ – Adverse Factors Considered by Triplecrown” appearing on pages 50 through 53 of the Registration Statement. We have revised page 1 of the Registration Statement to direct readers to such sections. We have also revised such sections to further explain the factors considered by Triplecrown’s board of directors. We have also revised the disclosure on page 1 regarding the phrase “were believed to be as attractive to public stockholders as the proposed merger.”

| 37. | Expand the disclosure in the first bullet point on page 2 to identify the “certain limited situations,” or explain to us why this information is not necessary. |

We have revised the disclosure on page 2 of the Registration Statement as requested.

| 38. | With regard to disclosure in the second bullet point on page 2, explain how entering into a contract for the purchase of land is consistent with Triplecrown’s “Code of Ethics” cited at page 125 and the disclosure Triplecrown provided in its IPO prospectus. Also eliminate the inconsistencies that appear at page 37 and elsewhere with regard to whether it will receive again those funds in the event that the reorganization does not occur. Provide appropriate disclosure in the conflicts section, and file a signed version of the contract as an exhibit to the Form S-4. |

With respect to the first part of the Staff’s comment, Triplecrown’s Code of Ethics states that Triplecrown should avoid conflicts of interest, wherever possible, except under guidelines or resolutions approved by the Board of Directors (or the appropriate committee of the Board). Triplecrown’s Board of Directors and Audit Committee approved and ratified the contract for the purchase of the land. Accordingly, such actions are consistent with the Code of Ethics. Furthermore, Triplecrown’s IPO prospectus specifically indicated that Triplecrown could pay deposits or down payments in connection with a proposed business combination. See for instance the risk factor titled “If the net proceeds of this offering not being held in the trust account are insufficient to allow us to operate for at least the next 24 months, we may be unable to complete a business combination” contained on page 21 of the prospectus as well as the line item titled “Working capital to cover miscellaneous expenses (potentially including deposits or down payments for a proposed business combination), director and officer liability insurance premiums, transfer agent, warrant agent and trustee fees and reserves” contained in the Use of Proceeds section on page 41 of the prospectus.

Securities and Exchange Commission

October 2, 2009

Page 15

With respect to the second part of the Staff’s comment, we have revised the disclosure on pages 2, 36 and 148 of the Registration Statement to eliminate any inconsistencies as requested.

With respect to the third part of the Staff’s comment, we have included a signed version of the contract as an exhibit to the Registration Statement as requested. However, information is already included in the conflicts of interest section (now included on page 36 of the Registration Statement in the 2nd bullet point).

| 39. | As for the disclosure in the fifth bullet point on page 2, revise the referenced text to describe all methods under consideration in necessary detail, rather than suggesting that only “some possible methods” are described. |

We have revised the disclosure on page 3 of the Registration Statement as requested.

| 40. | Revise the sixth bullet point on page 2 to clarify, if true, that any repurchases would only be undertaken using funds in excess of the $150 million. State whether there are limitations on the price that you would offer to repurchase shares or on the amount of shares you would purchase, and provide additional details at an appropriate place elsewhere in the document. Also expand the bullet point to identify briefly the possible impact of such purchases, as you have done in the risk factor captioned “If the merger is completed, a large portion of the funds” at page 24. |

With respect to the first two parts of the Staff’s comment, we have revised the disclosure on page 3 and elsewhere in the Registration Statement as appropriate. With respect to the last part of the Staff’s comment, we respectfully believe that no additional disclosure is necessary. The only time that funds will be used to purchase shares after the consummation of the merger is if more than $150 million is available to CAH after the closing. $150 million is the amount of funds that CAH would need to fully expand and operate its business. The disclosure on prior page 24 discusses the situation if CAH does not have sufficient funds to fully expand and operate its business. Accordingly, we have not revised the disclosure in the Registration Statement in response to this part of the Staff’s comment.

| 41. | Where you describe any agreements, including the lockup or voting agreements you mention at page 3, revise to disclose the date(s) that such agreements were executed. |

Triplecrown has not entered into any of the above-referenced lockup or voting agreements and has no intention of doing so. We have revised the disclosure throughout the Registration Statement to remove the references to such agreements.

| 42. | If true, disclose prominently that the proposed business combination is the only business combination that will be presented to security holders prior to the imminent termination of Triplecrown’s corporate existence on October 22, 2009. |

We have revised the disclosure on the cover page of the prospectus as requested.

Securities and Exchange Commission

October 2, 2009

Page 16

Questions and Answers, page 4

| 43. | Prior to and as background for “Since Triplecrown’s amended and restated certificate,” please insert a new question and answer to address briefly how this deal is different from what was proposed and promised in the IPO prospectus. |

We have revised the disclosure on page 10 of the Registration Statement as requested.

Selected Historical Consolidated Financial Information, page 11

| 44. | It appears that there may be an inconsistency between the positive $1,000 presented here as a figure for CAH stockholder’s equity and the negative $1,000 presented as a figure for CAH stockholder’s deficit on page F-13 of the financial statements. Please revise, or otherwise advise. |

We have revised the disclosure on page 15 of the Registration Statement to remove the above-referenced inconsistency as requested.

| 45. | With regard to the information presented for Cullen Agricultural Technologies Inc., please revise to refer to such statements as combined, rather than consolidated. |

We have revised the disclosure on page 15 of the Registration Statement as requested.

Selected Unaudited Pro Forma Condensed Combined Financial Information, page 13

| 46. | Please revise to include a brief introduction to the pro forma information, including a reference to where the reader can find additional information. |

We have revised the disclosure on pages 17 and 18 of the Registration Statement as requested.

| 47. | Please tell us how you considered disclosing the information required by Item 3(f) of Form S-4. |

We have included information required by Item 3(f) of Form S-4 on page 18 of the Registration Statement as requested.

Securities and Exchange Commission

October 2, 2009

Page 17

Risk Factors, page 14

| 48. | Eliminate text which mitigates the risks you present, including for example references to your hedging / breeding plans at page 17 and clauses which begin “although,” “however,” or “despite.” Similarly, disclose each risk plainly and directly, eliminating suggestions that you “cannot assure” a particular outcome. |

We have revised the risk factors to remove mitigating language as requested.

| 49. | Disclose in a new risk factor any risks and potential limitations on the importation of farm products and technology from New Zealand, including anything related to the production of hybrid cattle. We note the “state line” disclosure at the top of page 16 and the export disclosure at page 105. |

We have revised the disclosure on page 27 of the Registration Statement as requested.

| 50. | With a view toward expanded disclosure, advise, us whether you are aware of any federal or state limitations or restrictions relating to the import of cattle, other livestock, or related reproductive items. We note the disclosure at page 101, including the suggestion that you will have exclusive “access to these grazing lines” and to related “embryo, semen and genetic screening technologies.” |

We have revised the disclosure on page 27 of the Registration Statement to include a new risk factor titled “Inability to obtain required import permits could reduce the ability of Cullen Agritech to achieve certain long term operating efficiences” and included additional disclosure regarding such restrictions on page 125 of the Registration Statement. Additionally, we have removed the above-referenced phrases from the disclosure.

Forward-Looking Statements, page 25

| 51. | Because the Form S-4 registers an initial public offering, statements related to the proposed merger in other filings and statements in the proxy statement/prospectus do not constitute forward-looking statements within the definition of the PSLRA of 1995. Please revise accordingly. |

We have revised the disclosure on page 34 of the Registration Statement as requested.

| 52. | If you retain this section, revise to explain why potential conflicts of interest with regard to approving the merger would constitute forward-looking statements. |

We have revised the disclosure on page 34 of the Registration Statement to remove the above-referenced disclosure, as we have determined that such information does not constitute forward-looking statements.

Proxy Solicitation Costs, page 29

| 53. | Confirm that you will file all personal solicitation materials to be used, as Rule 14a-6(c) requires. |

We hereby confirm that all proxy solicitation material will be filed with the Commission.

Securities and Exchange Commission

October 2, 2009

Page 18

The Merger Proposal

Background of the Merger, page 37

| 54. | We note your statement that: |

“Triplecrown delivered and negotiated over two dozen letters of intent to those prospective target companies in which it believed a suitable transaction could be structured. However, none of these letters of intent were ever executed by the targets. The majority of these target companies ultimately rejected these letters of intent due to the perceived inherent shortcomings of Triplecrown’s operating structure, dilution and warrant overhang.”

Please add additional detail as to the kinds of prospective target companies mentioned here, the negotiations conducted, and the reasons the targets provided for their rejection. You may group like transactions together for purposes of your discussion.

We have revised the disclosure on pages 48 and 49 of the Registration Statement as requested.

| 55. | You explain that Triplecrown entered into negotiations with the underwriters in its IPO regarding the reduction of their deferred underwriting commissions payable at the consummation of the merger, and that such negotiations continue to be ongoing. We also note that Triplecrown entered into discussions with the underwriters to obtain their consent to any necessary amendments to the agreements entered into in connection with the IPO. Please update this information as necessary. |

We wish to advise the Staff that negotiations are still ongoing and no update is available at this time. As the negotiations progress, we will revise the disclosure accordingly.

| 56. | We note that the Triplecrown IPO prospectus states on page 75 that “Any affiliated transactions must be approved by a majority of our independent and disinterested directors.” Also, the Triplecrown certificate of incorporation indicates at Article SEVENTH, paragraph (G) that “The Audit Committee of the Corporation’s Board of Directors will review and approve all payments made by the Corporation to its initial stockholders, sponsors, officers, directors and their or the Corporation’s affiliates. Any payment made to a member of the Audit Committee will be reviewed and approved by the Board of Directors, with any member of the Board of Directors that has a financial interest in such payment abstaining from such review and approval.” Please revise to address expressly whether the approval of the proposed business combination followed these procedures. |

We have revised the disclosure on pages 49 and 50 of the Registration Statement as requested.

Securities and Exchange Commission

October 2, 2009

Page 19

| 57. | Also discuss in detail the contract for the purchase of the land to be used by CAH. Explain what, if any, special procedures were followed, insofar as Mr. Watson serves both as CEO of CAH and as chairman and treasurer of Triplecrown Acquisition. |

We have revised the disclosure on page 49 of the Registration Statement to indicate that the payments for the land contract were approved by Triplecrown’s board of directors and audit committee, with Mr. Watson abstaining from the vote due to his relationship with Cullen Agritech.

| 58. | Provide enhanced detail regarding the precise dates and reasons for the formation of Cullen Agritech (in June 2009) and CAH (in August 2009). To the extent either or both was formed in anticipation of a possible business combination with Triplecrown, explain the role played by Mr. Watson and any other interested parties in their formation. |

As indicated on page 46 of the Registration Statement, the Company was formed on August 27, 2009, solely for the purpose of effecting the merger with Triplecrown and becoming the publicly traded company thereafter. We have revised the disclosure on page 46 of the Registration Statement to clarify the role that Mr. Watson played in the formation of the Company as well as to clarify that Cullen Agritech was formed on June 3, 2009 and to provide greater information regarding its formation.

| 59. | If both entities were formed entirely apart from and without consideration of Triplecrown, explain how and when Mr. Watson became affiliated with each. |

We refer the Staff to our response to comment 58 above.

| 60. | Provide a detailed timeline to show when each material event in each entity’s development took place, including for example the dates the entity: |

| · | reduced to writing its business plan; |

| · | hired its (first) employee, naming each such employee; |

| · | became affiliated with Mr. Watson; |

| · | became affiliated with Dr. Watson; |

| · | entered into any material contracts, including the “strategic cooperation agreement with New Zealand Agritech” mentioned at page 103, the land purchase cited at page 111, and any employment contracts; |

| · | retained any consultants; |

| · | assembled “an experienced group of pastoral scientists and dairy science industry participants to further enhance its position as an innovation and technology company” as suggested at page 98 {and also separately support the assertion regarding its position in that regard}; |

Securities and Exchange Commission

October 2, 2009

Page 20

| · | retained the “in-house scientific experts” cited at page 38; |

| · | retained members of an advisory board; and |

| · | acquired rights with respect to the “proprietary, pasture-based, farming system for the production of raw milk” mentioned at page 107. |

We have revised the disclosure on page 46 of the Registration Statement as requested.

| 61. | Provide a more detailed discussion of the status of each entity at the times contact and meetings first took place with Mr. Ledecky and with the board. Disclose the precise date that Mr. Watson indicated to Mr. Ledecky that Cullen Agritech might be “an attractive opportunity for Triplecrown.” |

We have revised the disclosure on page 49 of the Registration Statement as requested.

| 62. | Explain when the contract for land purchase was entered into, when deposits were paid, and if true why these events took place prior to Triplecrown board consideration or approval. |

We have revised the disclosure on page 49 of the Registration Statement as requested.

| 63. | Disclose who negotiated the land purchase terms on behalf of Triplecrown and who authorized the contract terms, including the payment of a deposit. |

We have revised the disclosure on page 49 of the Registration Statement as requested.

| 64. | Disclose how and when information concerning the proposed transaction with Cullen Agritech “was delivered to the directors.” |

We have revised the disclosure on page 49 of the Registration Statement as requested.

| 65. | Clarify precisely which members of management discussed Triplecrown’s “efforts to find a suitable candidate for a business combination” and the “benefits of selecting Cullen Agritech.” If Mr. Watson was involved in discussing these matters, make that clear. |

We have revised the disclosure on page 49 of the Registration Statement as requested.

| 66. | Clarify who participated in the “considerable discussion” by the board on August 7, 2009, and discuss the overall role Mr. Watson played at the meeting. |

We have revised the disclosure on page 49 of the Registration Statement as requested.

Securities and Exchange Commission

October 2, 2009

Page 21

| 67. | Disclose the dates and participants involved in all substantive negotiations, and revise to clarify whether negotiations were limited to the period from August 24 through August 28, 2009. |

We have revised the disclosure on page 49 of the Registration Statement as requested.

| 68. | Describe how the structure and consideration to be paid in the transaction was determined, and explain any changes that occurred as a result of negotiations. If the draft merger agreement provided August 28 did not materially differ from the final executed merger agreement, disclose this explicitly. |

With respect to the first part of the Staff’s comment, we have revised the disclosure on page 48 of the Registration Statement as requested.

With respect to the second part of the Staff’s comment, we have revised the disclosure on page 50 of the Registration Statement to clarify that the signed agreement did not materially differ from the draft circulated on August 28, 2009, as requested.

| 69. | Summarize the content and conclusions of the discussions held at each meeting. |

We respectfully believe that the content and conclusions of each meeting was previously disclosed in the Registration Statement. For instance, the content of the August 7, 2009 board and committee meeting was to discuss the transaction and the need to pay an additional deposit on the land contract and the conclusion was to authorize management to continue to negotiate the transaction with Cullen Agritech and to authorize and ratify all deposits paid on the land (contained on page 49 of the Registration Statement). Accordingly, we have not revised the disclosure in the Registration Statement in response to this comment.

| 70. | Disclose when the fairness advisor was retained. |

We have revised the disclosure on page 53 of the Registration Statement as requested.

Triplecrown’s Board of Directors’ Reasons for Approval of the Merger, page 38

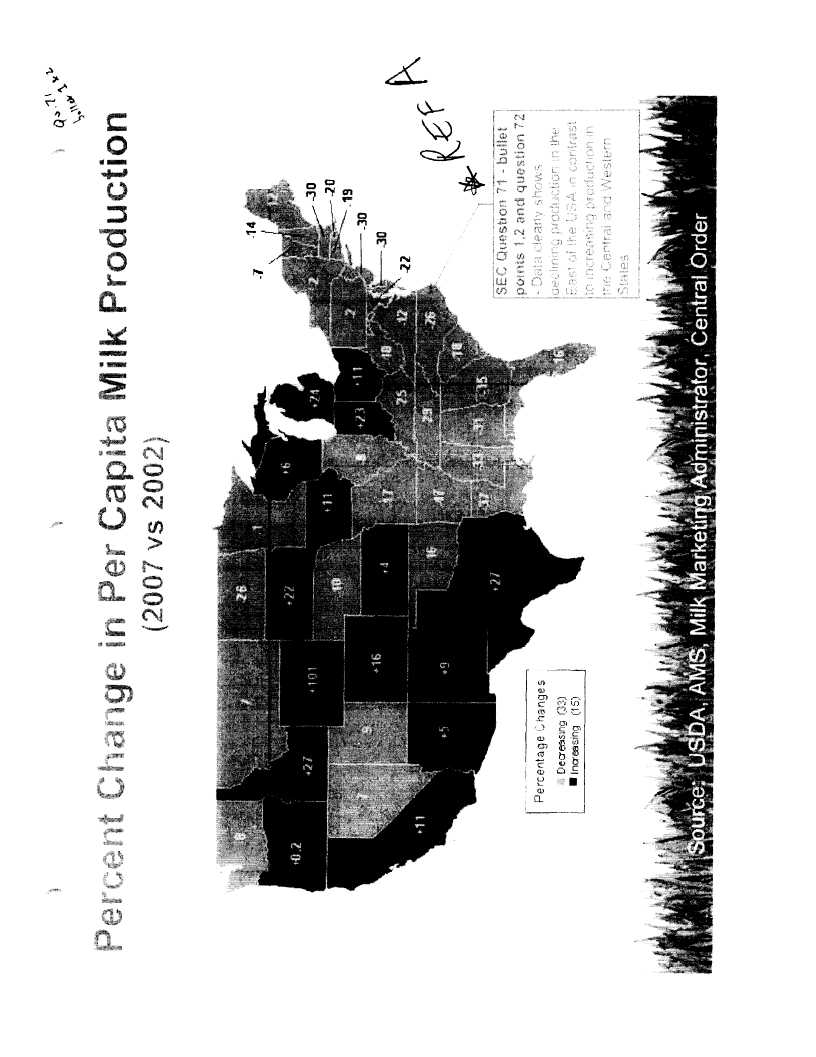

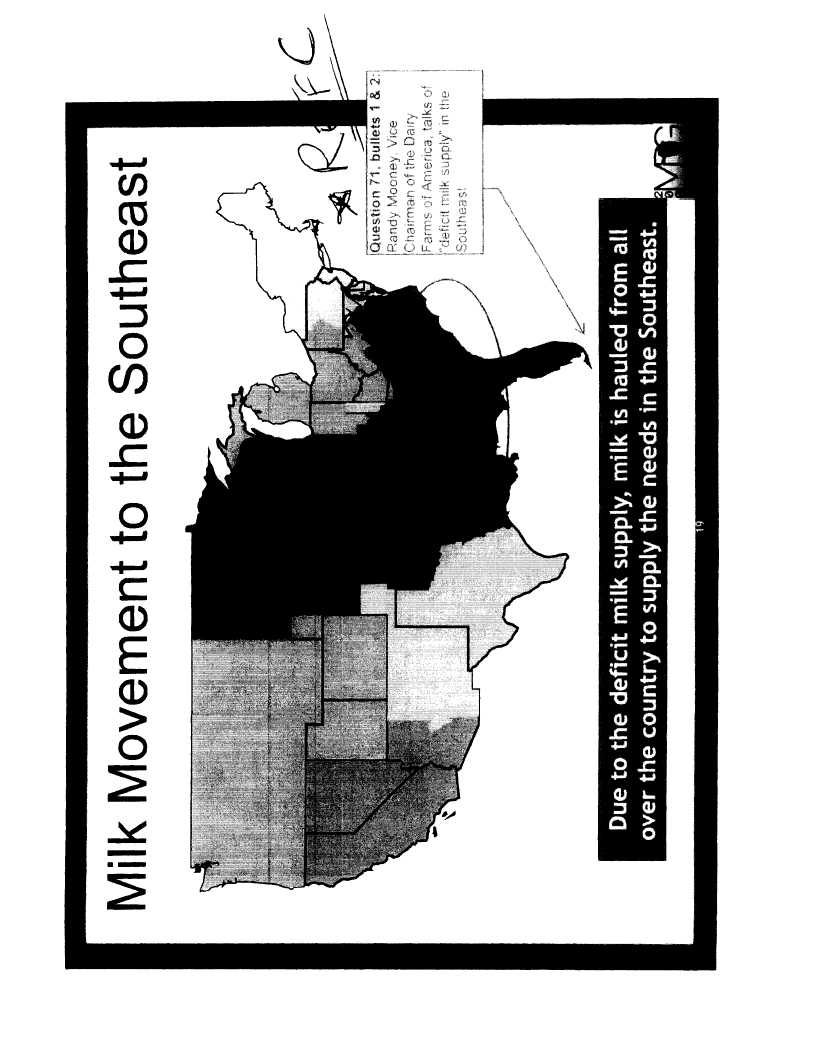

| 71. | Please provide us with copies of objective, third party materials that support the following assertions: |

| · | There is currently a significant shortage in the supply of fresh liquid milk in the Southeastern United States. |

| · | The Eastern Seaboard represents the largest fresh liquid milk market in the world, and this market is currently “starved of supply.” |

| · | Currently, there is a small but rapidly growing market for grass-fed or pasture- fed beef products. |

Securities and Exchange Commission

October 2, 2009

Page 22

| · | The grass-fed milk market is virtually non-existent due to the dominance of the confinement model and the lack of producers who have the technical knowledge to product milk on pasture year round. |

Also provide us with independently sourced material to show what percentage of milk production in the United States results from dairy farms which are at least partially forage based.

With respect to the first three above-referenced statements, we have supplementally provided the Staff with objective third party materials as requested.

With respect to the fourth above-referenced statement, we have supplementally provided the Staff with objective third party materials as requested. However, the statement: “lack of producers who have technical knowledge to produce milk on pasture year round” is implied by the lack of producers executing this model, combined with Cullen Agritech’s understanding of the complexity and scientific research it believes is required in order to successfully execute a model which produces milk on pasture year round through a cost effective system.

With respect to the final part of the Staff’s comment, Cullen Agritech’s management does not believe that accurate data to this effect is available. Due to the unconsolidated nature of the United States dairy industry and the large number of farms with less than 100 cows, accurate data on all farm management strategies is not available. Cullen Agritech’s management also points out that Cullen Agritech’s farming system is based on cows grazing 365 days of the year, which is a very different model to those that partially graze.

| 72. | Address recent media reports suggesting that there is an oversupply of milk in the United States. For example, one such report on the front page of a national newspaper suggests that, as a result of such oversupply, 230,000 cows have been culled since January 2009. Discuss the potential impact on your business plan and results of operations due to this oversupply, or explain why it would have no impact on your business. |

We have revised the disclosure on page 112 of the Registration Statement as requested.

| 73. | Clarify in necessary detail how Cullen Agritech, formed in June 2009, has been able to implement and provide its system, as the disclosure in the first paragraph on page 39 suggests. |

We have revised the disclosure on pages 50 and 51 of the Registration Statement to clarify the disclosure as requested.

Securities and Exchange Commission

October 2, 2009

Page 23

| 74. | Where you refer to Cullen Agritech’s “system” as resulting in healthier livestock and increased longevity, disclose over what period of time this longevity has been noted by Cullen Agritech, or revise to more accurately reflect its actual business history and experience. |

We have revised the disclosure on page 51 of the Registration Statement as requested.

| 75. | Explain how you can project reduced labor costs using “custom made” milking systems which you have neither tested nor used to date. We note the disclosure under “Reduced labor costs” on page 39 in that regard. |

We have revised the disclosure on page 52 of the Registration Statement to indicate that reduced labor costs is in comparison to traditional confinement system in the United States.

| 76. | We note the reference to “financial projections” at page 40. Ensure that all material projections exchanged or provided to the fairness advisor, as well as any other non-public information material to an investment decision, are properly disclosed in the amended Form S-4. |

The above-referenced financial projections were previously included on page 101 of the Registration Statement and are currently included on page 115 of the Registration Statement. Furthermore, we have been advised by the Company that all material financial information presented to the fairness advisor has been properly disclosed in the Registration Statement. Accordingly, we have not revised the disclosure in the Registration Statement in response to this comment.

Fairness Opinion, page 40

| 77. | Expand the first paragraph on page 40 to clarify whether the fairness advisor opined regarding fairness to stockholders and to warrantholders. |

In accordance with its engagement letter dated August 17, 2009, the fairness advisor did not opine regarding fairness to stockholder or warrant holders. We have revised the disclosure on page 53 of the Registration Statement to reflect the foregoing.

| 78. | Eliminate any suggestion that the reader must refer to the full text of the opinion for a discussion of the assumptions, procedures followed, matters considered, and limits, instead discussing these items in necessary detail. |

We have revised the disclosure on page 53 of the Registration Statement as requested.

| 79. | To eliminate any ambiguity regarding the target audience, revise the third paragraph so that you do not indicate that the opinion is directed to the board. |

Given that the Duff & Phelps opinion is addressed to Triplecrown’s board, which an investor can read, as it is included as Annex K of the proxy statement/prospectus, we believe that not indicating that the opinion is directed to the board could confuse investors. We therefore have not revised the disclosure in the Registration Statement response to this comment.

Securities and Exchange Commission

October 2, 2009

Page 24

| 80. | Identify by name the management of Triplecrown and of Cullen Agritech responsible for preparing the “certain financial forecasts” cited in the sixth bullet point on page 42. |

We have revised the disclosure on page 54 of the Registration Statement as requested.

| 81. | Specify the “other analyses” and “other factors” the advisor cites at the bottom of page 42, or revise to disclose that none was material. |

We have removed the above-referenced disclosure as such information was not material.

| 82. | Disclose in necessary detail the “U.S. Dairy Business Plan” cited in the fifth bullet point on page 43. |

We have revised the disclosure on page 54 of the Registration Statement to clarify what “U.S. Dairy Business Plan” as requested.

| 83. | Insofar as the advisor indicates at page 43 that its opinion “cannot and should not be relied upon” if “any of the foregoing assumptions or any of the facts” are materially untrue, disclose all such items in necessary detail. |

The assumptions and facts referred to above were previously set forth in detail in the bullet points on pages 57 and 59 of the Registration Statement. Accordingly, we have not revised the disclosure in the Registration Statement in response to this comment.

| 84. | Explain in necessary detail the reference in footnotes 1 at pages 44 and 46 to “an adjusted version of projections provided by Triplecrown’s management.” Discuss what adjustments were made, as well as Triplecrown’s basis and particular expertise enabling it to prepare for Cullen Agritech U.S. dairy business estimates for the next nine years. |

We have revised the disclosure on page 57 of the Registration Statement as requested.

| 85. | Identify those members of management that prepared the forecasts and estimates referenced at pages 44 and 45, and explain when and on what basis they were prepared. |

We have revised the disclosure on page 57 of the Registration Statement as requested.

Securities and Exchange Commission

October 2, 2009

Page 25

| 86. | Explain why you suggest that none of the projections should be relied upon “as to the past.” |

We have revised the disclosure on page 57 of the Registration Statement to remove the above-referenced disclosure

| 87. | Explain the reference at page 46 to “(stabilized)” EBITDA for 2012. Also define “normalized earnings” for that same year, as referenced at page 48. |

We have revised the disclosure on pages 59 and 60 of the Registration Statement as requested.

| 88. | Explain why any data points or companies were excluded from the analyses. Where data was unavailable for a particular company or transaction, disclose this. In that connection, it is unclear how the Ma Anshan transaction was used for purpose of the analysis at page 47. |

Although publicly available multiples data was not available for the Ma Anshan, Duff & Phelps believes that including the transaction demonstrates investment activity in the sector. China Mengniu Dairy Co. Ltd. was analyzed in Duff & Phelps’ Selected Public Company Analysis; however its valuation multiples were well above the range of the other selected companies and were therefore excluded. We have revised the disclosure on page 60 of the Registration Statement to include the foregoing.

| 89. | Explain the reference to footnote 4 in the table on page 47. |

We have revised the disclosure on page 60 of the Registration Statement to remove the above-referenced footnote.

| 90. | Revise to explain the significance, if any, of the $155 million valuation falling “near the top of each of the ranges of value indications.” |

We have revised the disclosure on page 61 of the Registration Statement as requested.

Actions that may be taken, page 52

| 91. | Clarify whether the consideration you cite in the last sentence of the second paragraph potentially includes securities that were to be canceled or placed in escrow. |

We have revised the disclosure on page 63 of the Registration Statement as requested.

Securities and Exchange Commission

October 2, 2009

Page 26

Anticipated Accounting Treatment, page 58

| 92. | You disclose that because Cullen Agritech’s CEO is the Chairman of the Board of Triplecrown, Cullen Agritech is a related party, which results in consolidating Cullen Agritech’s assets and liabilities at carrying value with those of Triplecrown. You also note that the cost of the purchase will be based on the par value of the Triplecrown common stock issued to the Cullen Agritech stockholder. Please provide us with your analysis that references authoritative accounting literature supporting this accounting treatment. As part of your response, please tell us how you considered EITF 02-5. |

In analyzing the accounting treatment of the transaction, we primarily looked to the accounting guidance in SAB 48 (Topic 5.g.), “Transfers of Nonmonetary Assets By Promoters or Shareholders”. We considered EITF 02-5, however we do not believe that the transaction is a common control merger as defined in that standard for two reasons: (i) Cullen Agritech is not a “business”, as that term is defined in SFAS 141(r), therefore it is not a business combination, and (ii) common control (between Triplecrown and Cullen Agritech), which is generally defined in EITF 02-5 as an individual or group that holds more than 50% of the voting interest in each entity, does not exist.

We believe that the substance of the transaction is analogous to SAB 48, which describes a set of facts where “nonmonetary assets are exchanged by … shareholders for … part of a company’s common stock just prior to or contemporaneously with a first-time public offering.” SAB 48 indicates that the “staff believes that transfers of nonmonetary assets to a company by its promoters or shareholders in exchange for stock prior to or at the time of the company’s initial public offering normally should be recorded at the transferors’ historical cost basis determined under GAAP.”

Cullen Agritech would not meet the definition of a business as there are no inputs or outputs. Accordingly, since the only substantive asset in Cullen Agricultural will be the [Intellectual Property], it is more akin to the issuance of common stock in exchange for the “nonmonetary asset”, than a business. Eric Watson, is the Chairman of the Board of Triplecrown, and owns approximately 9.6% of its common stock and is the sole indirect owner of Cullen Agritech. Additionally, since the transaction is with a shell company (Triplecrown) and the shareholders are voting whether the transaction should move forward or the trust fund should be liquidated, the transaction is also analogous to an initial public offering of Triplecrown.

As a result of the foregoing, we believe that the assets and liabilities of Cullen Agritech should be recorded at their historical cost basis determined under GAAP. The reference to “par value” in the “Anticipated Accounting Treatment” section has been eliminated.

Required Vote, page 58

| 93. | Revise to make clear that in recommending approval, the board has conflicts of interest. Also, as to each finding of fairness and recommendation, clarify whether the board is unanimous. |

We have revised the disclosure on pages 70, 91, 92, 93 and 94 of the Registration Statement as requested.

Securities and Exchange Commission

October 2, 2009

Page 27

U.S. Federal Income Tax Considerations to Triplecrown Stockholders, page 66

| 94. | Revise the caption and the first sentence to clarify that you are disclosing the material federal income tax consequences. |

We have revised the disclosure on page 79 of the Registration Statement as requested.

| 95. | Please expand the discussion here to include all of the salient points from the tax opinion. |

We have revised the disclosure on page 79 of the Registration Statement as requested.

Unaudited Pro Forma Condensed Combined Financial Information

Unaudited Pro Forma Condensed Combined Statement of Operations, page 68

| 96. | We are unable to locate the explanation for Note 7 in your Pro Forma Income Statement Adjustments on page 69. Additionally, your Pro Forma Income Statement Adjustments provide an explanation for Note 6, which we are unable to locate on this page. Please revise to resolve these discrepancies. |

We have revised the disclosure on page 84 of the Registration Statement as requested.

Notes to Unaudited Pro Forma Condensed Combined Financial Information Pro Forma Income Statement Adjustments, page 69

| 97. | Note 1 explains that you included a pro forma adjustment of $19,320,000 related to the deferred underwriting fees in conjunction with your 1P0, and $5,000,000 for estimated legal and other advisory expenses related to the merger. Please explain to us why you believe it is appropriate to include these items as pro forma adjustments for the statement of operations. Specifically, tell us how these charges are expected to have a continuing impact on the registrant, and are factually supportable. If they are not, please revise your presentation to remove the amounts as a pro forma adjustment from the statement of operations. Please see Article 11-02(b)(6) of Regulation S-X for additional information. |

| This comment is also applicable to the pro forma adjustment explanation for Note 12 for the June 30, 2009 condensed statement of operations on page 73. |

The only adjustments that were included related to deferred underwriting fees and transaction expenses in respect to their effect on interest income. Accordingly, we have not revised the disclosure in the Registration Statement in response to this comment.

Securities and Exchange Commission

October 2, 2009

Page 28

| 98. | We note your reconciliation of the number of weighted average shares outstanding used in calculating earnings per shares in Note 4. Please explain to us, and revise your disclosure to further describe the adjustments identified as ‘Decrease cash held in trust account,’ `Increase cash and cash equivalents’, and ‘Shares repurchased’. This comment is also applicable to the pro forma adjustment explanation for Note 15 for the June 30, 2009 condensed statement of operations on page 73. |

We have revised the disclosure on pages 84 and 88 of the Registration Statement as requested.

Notes to Unaudited Pro Forma Condensed Combined Financial Statements, June 30, 2009, Dane 72

| 99. | The explanation of Note 1 and 2 at the top of the page explains that such amounts are derived from the audited financial statements of Triplecrown Acquisition Corp for the year ended December 31, 2008, and from the audited consolidated financial statements of CAT Corporation as of August 18, 2009. As you present pro forma information as of June 30, 2009, this explanation does not appear to be applicable to all places the reference is used. Please also revise to clarify who you are referring when using the term CAT Corporation. If you are referring to Cullen Agricultural Technologies Inc., please revise to use consistently defined terms. Finally, as you have previously provided and used Note 1 to explain a pro forma adjustment related to your December 31, 2008 statement of operations on page 69, please revise your reference so there is only one Note 1 so as to not be confusing to a reader. |

We have revised the disclosure on pages 84 through 89 of the Registration Statement as requested.

Proposals to be Considered by the Triplecrown Warrantholders The Warrant Amendment Proposals, page 78

| 100. | Please tell us how you plan to account for the proposed amendments to the warrant agreement governing Triplecrown’s outstanding warrants to (i) increase the warrant exercise price from $7.50 to $12.00; (ii) extend the expiration date from October 21, 2012 to October 21, 2013; and (iii) increase the price at which the stock must trade for the warrants to be called for redemption from $13.75 per share to $17.00 per share. |

The Company is aware that a modification in an equity instrument that results in material incremental fair value needs to be accounted for in the financial statements. Based upon the guidance prescribed in ASC 718 and the Black-Scholes option pricing model for the warrants, the modification of the warrants in connection with the merger will not result in any incremental fair value of the warrants, because the significant increase in the strike price from $7.50 to $12.00 more than offsets the one year extension of the expiration date. Therefore, we have assumed that no warrants will be exercised immediately following the consummation of the merger because the expected fair value per share of Cullen Agritech’s common stock will be below the amended strike price of the warrants and the warrants would also be anti dilutive. We have revised the disclosure on page 81 of the Registration Statement to clarify the foregoing.

Securities and Exchange Commission

October 2, 2009

Page 29

Offering Proceeds Held in Trust, page 80

| 101. | Explain how a greater amount was placed in trust than constituted the net proceeds. Also quantify the “remaining balance” for that purpose. |

The net proceeds were less than the amount placed in trust because the amount placed in trust included an accrual that was estimated related to the expenses of the initial public offering. When the accrual was settled, the amount actually paid was greater than the accrual. Accordingly, we have not revised the disclosure in the Registration Statement in response to this comment.

Code of Ethics, page 89

| 102. | Provide us with a copy of the code of ethics referenced. |

The Code of Ethics of Triplecrown was filed as Exhibit 14 with Triplecrown’s IPO prospectus (SEC File No. 333-144523). We have filed the Code of Ethics for the Company as Exhibit 14 with this amendment to the Registration Statement.

Business of Cullen Agritech, page 90.

| 103. | Explain why you rely on fifteen year old information, particularly in light of the more recent media reports alluded to elsewhere in this comment letter. |

We have revised the disclosure on page 106 of the Registration Statement as requested.

| 104. | Explain in greater detail the basis for the claims you make under “Key Components to Cullen Agritech’s Pasture Based Grazing System” at page 99. It appears that Cullen Agritech “will own” this system, but has not yet operated it. Make similar revisions throughout this section to clarify which claims relate to others’ business operations and results, and which refer to yours. |

We have revised the disclosure throughout the section titled “Business of Cullen Agritech” as requested.

Securities and Exchange Commission

October 2, 2009

Page 30

Implementation of Cullen Agritech’s Farming Systems in the Southeastern US, page 99

| 105. | On pages 100 to 101 you present information that appears to be a forecast of Cullen Agritech’s performance over the next several years. As such, please revise your presentation and disclosure to comply with the guidance provided in the AICPA Audit and Accounting Guide for Prospective Financial Information. |