Graubard Miller The Chrysler Building 405 Lexington Avenue New York, N.Y. 10174-1901 (212) 818-8800 | ||

| facsimile | direct dial number | |

| (212) 818-8881 | (212) 818-8638 | |

| email address | ||

| jgallant@graubard.com |

October 8, 2009

VIA EDGAR AND FEDERAL EXPRESS

Mr. H. Roger Schwall

Assistant Director

Securities and Exchange Commission

100 F Street, N.E.

Washington, DC 20549

| Re: | Cullen Agricultural Holding Corp. |

| Form S-4, Amendment No. 3 |

| Filed October 2, 2009 |

| File No. 333-161773 |

| Triplecrown Acquisition Corp. |

| Preliminary Schedule 14A, Filed September 8, 2009 |

| Definitive Additional Soliciting Material Filed October 1, 2009 |

| File No. 001-33698 |

Dear Mr. Schwall:

On behalf of Cullen Agricultural Holding Corp. (the “Company”) and Triplecrown Acquisition Corp. (“Triplecrown”), set forth below are the responses of the Company’s comments of the staff of the Division of Corporation Finance (the “Staff”) of the Securities and Exchange Commission (the “Commission”), received by letter dated October 6, 2009 (the “October 6 Letter”), with respect to Amendment No. 3 to the Registration Statement (the “Registration Statement”) on Form S-4 (Registration No. 333-161773) filed by the Company on October 2, 2009. The responses to the Staff’s comments are set out in the order in which the comments were set out in the October 6 Letter and are numbered accordingly.

We have enclosed with this letter a marked copy of Amendment No. 4 to the Registration Statement (“Amendment No. 4”), which was filed today by the Company via EDGAR, reflecting all changes to the Registration Statement. Page numbers referred to in the responses reference the applicable pages of Amendment No. 4 unless otherwise noted. We are also delivering three (3) courtesy copies of such marked Registration Statement to Norman Gholson of your office.

Securities and Exchange Commission

October 8, 2009

Page 2

General

| 1. | Where comments on one section or document apply to other disclosure or documents, please make related changes to all affected disclosure. This will eliminate the need for us to issue repetitive comments. References throughout this letter to “you” or “your” refer to Cullen Agricultural Holding Corp., Triplecrown Acquisition Corp., or their respective affiliates, depending on the context. |

Duly noted. We will make related changes to all affected disclosure as requested.

Proposed Timing and Related Issues

| 2. | You will expedite our processing if you are able to deliver the courtesy copies to us on the same business day that you file the next amendment. Also, please remember to provide at the earliest possible time the .pdf files that were the subject of prior comment 8. |

Duly noted. We will deliver courtesy copies of the Company’s filings to the Staff on the same business day as amendments are filed and submit via EDGAR as .pdf files precisely marked electronic versions of the Registration Statement as requested.

| 3. | With regard to the marking that you use to reflect changes to the amended document, as we previously discussed with counsel, we rely on your precise marking to expedite our review. With the next amendment, please ensure that all changes have been precisely marked. For example, at a minimum, changes to page i and pages 35 to 36 of Amendment 3 were not marked precisely. You also failed to provide us with marked copies of the revised opinion you filed as exhibit 5.1, notwithstanding prior comment 7. |

Duly noted. We will insure that all changes have been precisely marked as requested.

| 4. | Update your responses to prior comments 3, 5, and 6, as applicable. |

| · | Under the circumstances, disclose whether you will provide for telephone voting and/or electronic voting via the internet to give stockholders additional time to review the materials that they apparently may be receiving with such limited time that they could be unable to make an informed voting decision. |

| · | We note that Monday, October 12, 2009, is a federal holiday. For the purposes of your response only and not as an indication of when we believe accelerated effectiveness could potentially be achievable, please address by what date and time you would be able to get hard copies of the materials into the hands of all beneficial holders of your securities in the event that the Form S-4 were to be declared effective prior to the close of business on Friday, October 9, 2009. |

Securities and Exchange Commission

October 8, 2009

Page 3

| · | Also advise us what means you will be using to expedite delivery under the circumstances. |

Triplecrown continues to anticipate holding its special meetings of stockholders and warrantholders on October 21, 2009. Additionally, Triplecrown still does not anticipate seeking an extension of its corporate existence for a limited period of time after October 22, 2009 to complete the business combination.

Assuming the Registration Statement was declared effective prior to the close of business on Friday, October 9, 2009, it is anticipated that copies of the definitive proxy statements would be mailed to holders of record on Friday, October 9, 2009 and beneficial holders on Saturday, October 10, 2009. Delivery of such proxy statements would be made by Federal Express to expedite receipt.

We have revised the disclosure on pages 11 and 41 of the Registration Statement to indicate that stockholders and warrantholders who hold their securities through a broker or bank will have the option to authorize their proxies to vote their securities electronically through the Internet or by telephone. Additionally, once the Registration Statement is declared effective, Triplecrown intends to file a Current Report on Form 8-K and issue a press release so that the public is aware that the documents are available for review online at the SEC’s website.

Triplecrown believes such steps would provide stockholders and warrantholders a sufficient amount of time to receive the information and vote on the proposals.

| 5. | We note your response to prior comment 20. Please further revise to update or include for the first time disclosure missing, for example, from pages 4, 47, 124, 133, and 153. Also, explain whether you are making a Hart-Scott-Rodino filing as discussed at page 2 and, if so, discuss the timing parameters that relate to the HSR approval process. Make clear in the amendment where you have provided the new or changed disclosure. |

We have included the above-referenced disclosure as requested. Please note that the Company has confirmed with the Federal Trade Commission that no Hart-Scott-Rodino filing is required for this transaction and we have therefore removed the reference to such filing.

Other General Comments

| 6. | We note your response to our prior comments 9 and 16. However, references to lockup agreements remain in the following places in the filing: page 36; Annex J (form of Lock-Up Agreement); and Item 10.4 on the Exhibit Index. Please advise or revise. |

Our prior responses to comments 9 and 16 related to the voting and lockup agreements involving the warrants. The lockup agreement referenced on page 36 and filed as Annex J relates to the shares to be received by Cullen Inc. Holdings Ltd. upon consummation of the transaction. Such lockup was executed upon the signing of the merger agreement and remains in effect. We have revised the disclosure on pages 2, 30, 49 and J-1 of the Registration Statement to indicate the date such lockup was executed.

Securities and Exchange Commission

October 8, 2009

Page 4

| 7. | We note your response to our prior comment 41 and reissue the entire comment. Among other things, please disclose when the lockup agreements described on page 36 of your filing were executed. |

We refer to the Staff to our response to comment 6 above.

| 8. | Include clear disclosure on the cover page, in the risk factors, and throughout your document to indicate whether you intend to use such a substantial amount of the available trust funds for purchases such that you could be left with no working capital. We note the disclosure at pages 20 and 65 to that effect. Also, reconcile this statement with the disclosure elsewhere in the filing that $150 million is anticipated to be used “to implement Cullen Agritech’s business model.” In your. response to our prior comment 40 you state that “$150 million is the amount of funds that CAH would need to fully expand and operate its business.” With regard to this and other business plan disclosure, the current presentation does not afford those voting with sufficiently clear and unambiguous information in order to facilitate an informed vote and investment decision. We may have further comments after reviewing your response. |

We have revised the disclosure on the cover page of the prospectus and on pages 3, 9, 33, 46 and 96 of the Registration Statement as requested.

| 9. | We note your responses to our prior comments 29 and 30. Please add a discussion of the fiduciary duties of the Triplecrown Founders and other person who have fiduciary roles with respect to Triplecrown. Also, notwithstanding your response, provide the Risk Factors or other disclosure that prior comment 30 requested. |

We have revised the disclosure on page 63 of the Registration Statement to provide the requested disclosure relating to fiduciary duties. We have further revised the disclosure on page 33 of the Registration Statement to provide the requested risk factor disclosure.

| 10. | We note your response to our prior comment 28. Among other things, we note your statement in your response letter that “purchases would be made in private transactions in specific individual instances with sophisticated investors.” Please add a statement to that effect in your filing. |

The disclosure on page 63 of the Registration Statement currently provides as follows:

“It is anticipated that Triplecrown and/or Cullen Agritech would approach a limited number of large holders of Triplecrown stock that have voted against the merger proposal and demanded conversion of their shares, or that have indicated an intention to do so, and engage in direct negotiations for the purchase of such holders’ positions. All holders approached in this manner would be institutional or sophisticated holders.”

Securities and Exchange Commission

October 8, 2009

Page 5

We have revised the disclosure on page 65 of the Registration Statement to clarify that purchases would be made in private transactions in specific individual instances with sophisticated investors as requested.

Definitive Additional Soliciting Material filed October 1, 2009 Summary of the Material Terms of the Merger, page 5

| 11. | In the second full bullet point paragraph on page 6, you state in a parenthetical that “(except in certain limited situations such as transfers to family members, upon a holder’s death or pursuant to a domestic relations order).” Revise to clarify that you are not providing a list of three separate items. |

We have revised the disclosure on page 2 of the Registration Statement to clarify that transfers could be made in four separate instances.

Form S-4, Amendment No. 3 Filed October 2, 2009 Cover page

| 12. | We note your responses to our prior comments 10 and 11 and reissue those comments in part. Although the various choices that your security holders have are discussed in various places in the document, please add a centralized discussion outlining the choices your security holders have and the potential impact of each choice on the other choices available to them. You may add this as a Question and Answer, in which case include on the cover page a cross reference to this discussion. |

We have revised the disclosure on the cover page of the prospectus and on page 7 of the Registration Statement as requested.

| 13. | Please further revise to comply, with prior comment 12. Also add the page number to the reference to the Conflicts section which you cite here and at page 9. |

We have revised the disclosure on the cover page of the prospectus and on page 10 of the Registration Statement as requested.

Summary of the Material Terms of the Merger, page 1

| 14. | We note your response to prior comment 19. Please revise to identify by name each of the Triplecrown Founders, or include a cross reference to such disclosure. |

We have revised the disclosure on page 1 of the Registration Statement as requested.

Securities and Exchange Commission

October 8, 2009

Page 6

| 15. | We note your discussion of the potential purchases and inducements at page 3 and elsewhere. Revise to disclose that all such activity will be carried out in full compliance with all applicable state laws and federal securities laws. |

We have revised the disclosure on pages 3 and 65 of the Registration Statement to indicate that all such activity will be carried out in full compliance with applicable state laws and federal securities laws as requested.

Questions and Answers, page 5

| 16. | Revise the charts you provided in response to prior comment 21 to include entries for Mr. Watson; with regard to his post closing ownership, reflect the percentage amount he would own assuming maximum conversion. Add additional text to both charts to make clear that CAH is the registrant. Also, revise the tabular disclosure in the first column at page 7 to identify clearly each entity that Mr. Watson controls, rather than just including that information for Natural Dairy. |

We have revised the disclosure on pages 6 and 7 of the Registration Statement as requested.

| 17. | Clarify the reference to electronic voting at page 8, in light of the related disclosure at page 40. |

We have revised the disclosure on page 41of the Registration Statement as requested.

| 18. | We note your response to prior comment 24. Nonetheless, it appears that rather than suggesting the warrants would be the same “except for,” more precise disclosure at page 9 and elsewhere would indicate that in fact the terms of the warrants will be substantially changed pursuant to the warrant amendment proposal. Please revise accordingly, or further explain your position. |

We have revised the disclosure on pages 9 and 152 of the Registration Statement as requested.

| 19. | You refer to “another business combination” at page 10. We remind you of prior comments 1 and 42. |

We have revised the disclosure on page 11 of the Registration Statement to remove the reference to “another business combination” as requested.

| 20. | If security holders follow your guidance at page 11 and mail their proxies such that they would arrive the day prior to your meeting, disclose the date by which such proxies would require mailing. See also comment 4 of this letter. |

We have revised the disclosure on page 11 of the Registration Statement as requested.

Securities and Exchange Commission

October 8, 2009

Page 7

Comparative Share Information

Unaudited Pro Forma Consolidated Per Share Information, page 20

| 21. | You used footnote (2) with respect to “Basic earnings per share” and “Diluted earnings per share” for the year ended December 31, 2008; however, footnote (2) describes how to calculate book value per share. Please revise to explain why the calculation of book value per share impacts your earnings per share calculations. |

We have revised the disclosure on pages 20 and 21 of the Registration Statement as requested.

Risk Factors, page 22

| 22. | We reissue prior comment 48. For example, the breeding/ hedging strategy appears at page 25; you refer to a “favorable” regulatory environment in the new text at page 27; and you retain other mitigating text throughout the section. |

We have revised the disclosure in the risk factors as requested.

| 23. | Please revisit your characterization of Cullen Agritech’s farming system at page 24 and elsewhere as “proven.” Due to the relatively limited model that you appear to be using, it would appear to be more accurate to refer to others having tested the system on a limited basis. Please revise or advise. |

We have revised the disclosure on pages 24, 50, 106, 121 and 129 of the Registration Statement as requested.

| 24. | Add a new risk factor regarding the significant decrease in winter milk production among cows that eat only greens, and the difficulty farmers have experienced in making a profit as a result. This information appeared in the supplemental materials you provided in response to prior comment 71. |

We have revised the disclosure on page 27 of the Registration Statement as requested.

| 25. | Add a new risk factor that makes clear that the fairness advisor was not asked to provide an opinion regarding the fairness of the transaction to security holders, but only opined as to “Triplecrown.” Also identify clearly the assumptions underlying its opinion but which might not be accurate, such as the availability of $150,000,000 to use for the proposed business. |

We have revised the disclosure on page 32 of the Registration Statement as requested to include a new risk factor titled “The fairness opinion Triplecrown received did not indicate whether the valuation of Cullen Agritech negotiated between Triplecrown and Cullen Agritech was fair, from a financial point of view, to the unaffiliated stockholders of Triplecrown.” We have also revised the disclosure contained in the risk factor titled “The fairness opinion Triplecrown received assumed that Cullen Agritech had access to the capital it needed to implement its business plan and therefore Cullen Agritech may not be worth as much as such valuation supposes” in further response to this comment.

Securities and Exchange Commission

October 8, 2009

Page 8

Interests of Triplecrown’s Directors, page 35

| 26. | Revise to clarify whose shares in particular will be cancelled, and whose will not be, if the merger is consummated. |

We have revised the disclosure on page 36 of the Registration Statement as requested.

Special Meetings of Triplecrown Stockholders and Warrantholders Recommendation of Triplecrown Board of Directors, page 38

| 27. | We reissue prior comments 13 and 93, and remind you to reference the more complete “conflicts” disclosure that appears elsewhere. Make corresponding changes at page 44 and elsewhere, as required. |

We have revised the disclosure on pages 45, 71, 92, 93, 94 and 95 of the Registration Statement as requested.

Vote of Triplecrown’s Stockholders Required, page 39

| 28. | We note your disclosure that “voting in favor of the merger proposal would not limit your rights to seek rescission or damages as described in this proxy statement/prospectus.” Please expand your disclosure to state, if true, that a stockholder’s right to seek rescission does not end upon consummation of the merger proposal discussed in the document. In that case, also specify the precise length of time during which the right to seek rescission would remain available to stockholders. |

We have revised the disclosure on page 40 of the Registration Statement as requested.

| 29. | The last paragraph includes disclosure that appears to be inconsistent with the disclosure in the second paragraph on page 40 regarding potential waiver. Please revise to provide consistent disclosure. |

We have revised the disclosure on page 40 of the Registration Statement as requested.

Securities and Exchange Commission

October 8, 2009

Page 9

The Merger Proposal, page 45

| 30. | Provide more precise disclosure to set forth the amounts to be used for the various purposes you list in the third paragraph under “Triplecrown.” If there are potential ranges, specify the upper and lower limits in each case. |

We have revised the disclosure on pages 3, 9, 31, 46 and 96 of the Registration Statement as requested.

Cullen Agritech, page 46

| 31. | With a view to disclosure, quantify the number of full-time employees and identify the officers and directors of each entity you list in this section. |

We have revised the disclosure on pages 47 and 124 of the Registration Statement as requested.

| 32. | Disclose in necessary detail how Mr. Watson and Dr. Watson are affiliated with each named entity. Disclose on the cover page and in the Conflicts section that Dr. Watson, Mr. Watson’s brother, is the sole employee of Cullen Agritech. |

We have revised the disclosure on the cover page of the prospectus and on pages 36, 47 and 125 of the Registration Statement as requested.

Background of the Merger, page 48

| 33. | We note your response to prior comment 54. If you pursued other targets which would have failed the 80% trust fund threshold requirement, disclose that explicitly. Also disclose when you first pursued a target which failed to meet one of the requisites set forth in your final IPO prospectus. |

We have revised the disclosure on page 50 of the Registration Statement as requested.

| 34. | We remind you of our prior comment 55. |

Duly noted.

| 35. | Revise the disclosure regarding the May 22 visit to the “research farms” to clarify who owned the properties and operations in question at the time. Also disclose which if any contractual arrangements were in place by that time with regard to the potential acquisition by Cullen Investments or any of its affiliates. |

We have revised the disclosure on page 50 and 124 of the Registration Statement as requested.

Securities and Exchange Commission

October 8, 2009

Page 10

| 36. | Provide us with a copy of the e-mail you reference in the new text on page 49. |

We hereby supplementally provide the Staff with the requested email correspondence as requested.

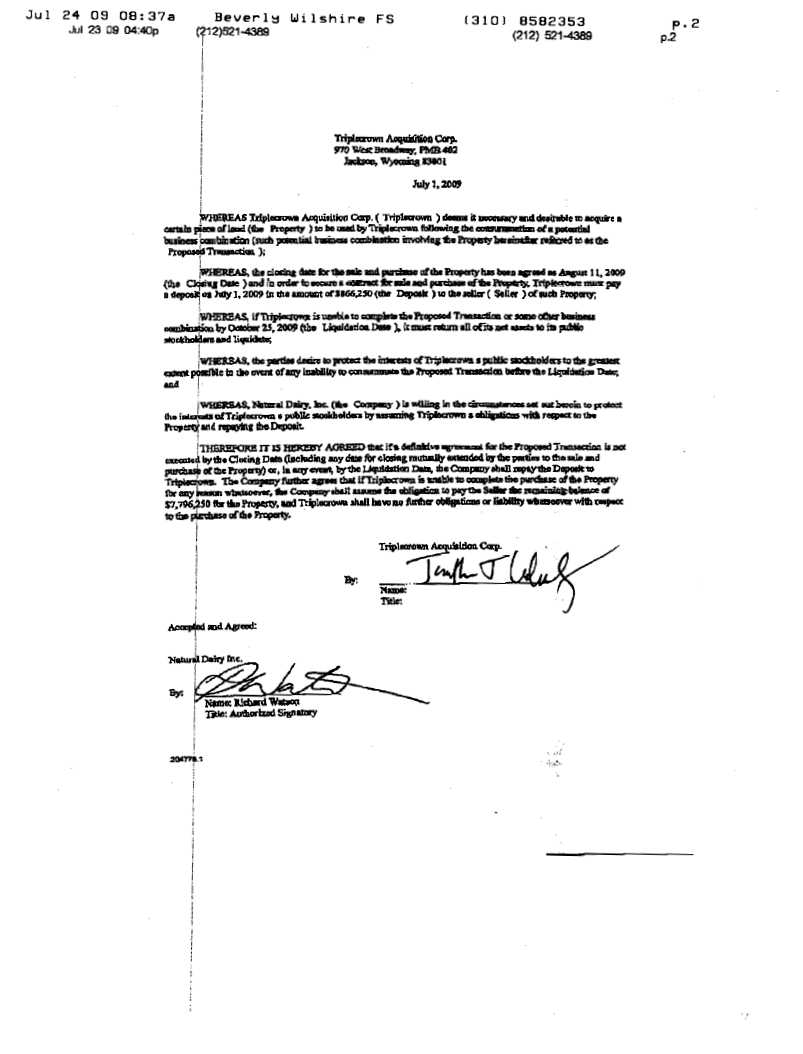

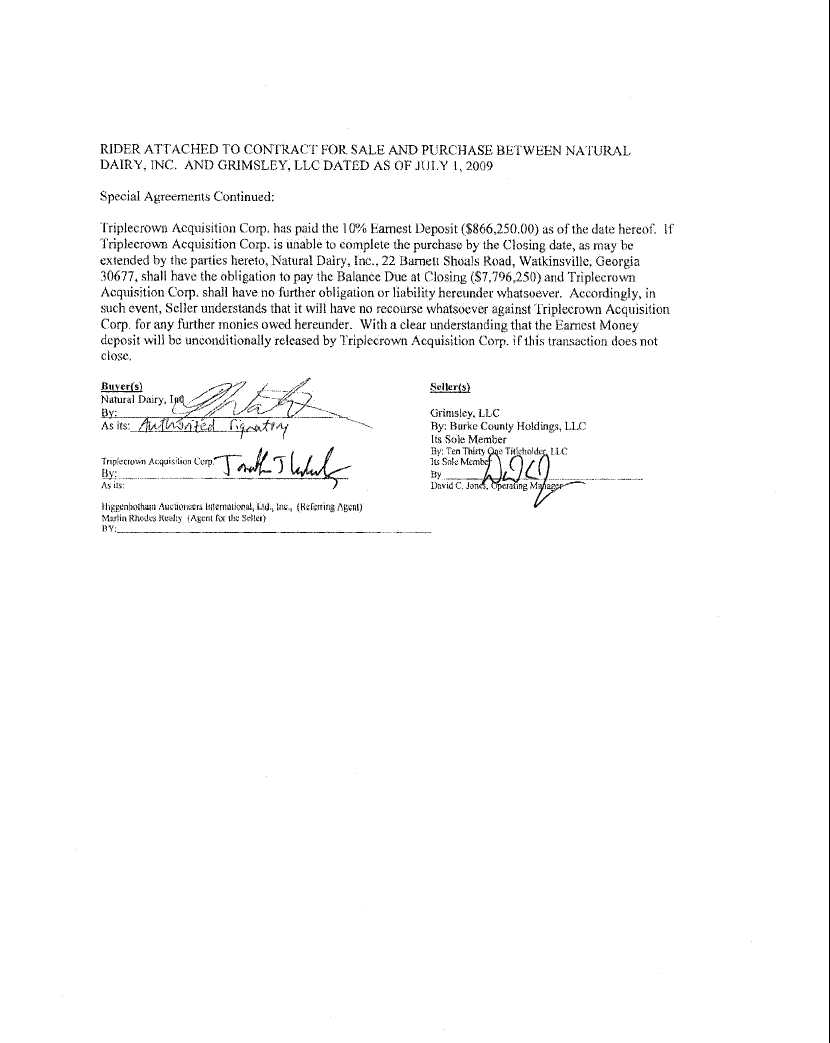

| 37. | Clarify when Triplecrown paid the referenced deposit. |

We have revised the disclosure on page 50 of the Registration Statement as requested.

| 38. | We note your responses to our prior comments 56 and 57. Disclose whether the Board members and Audit Committee members who approved the proposed business combination and the contract for the purchase of land were disinterested as to these particular transactions. |

We have revised the disclosure on page 50 of the Registration Statement as requested.

| 39. | We note your response to our prior comment 58. Please provide us with a copy of Cullen Agritech’s first proposed written business plan, created on May 6, 2008, as described on page 46 of your filing. |

We hereby supplementally provide the Staff with the requested business plan.

| 40. | We note your response to our prior comment 60. Please enhance your disclosure to address the following issues: |

| · | What entity or entities have been running the research farms since their inception in late 2007? |

| · | What personnel are staffing these farms? |

| · | How many and what types of personnel are there? |

| · | Are any of the personnel working on the farms anticipated to become staff of Cullen Agritech after the business combination? |

| · | If so, how many, and in what roles? |

We have revised the disclosure on pages 47 and 124 of the Registration Statement as requested.

Securities and Exchange Commission

October 8, 2009

Page 11

| 41. | We note the statement on page 49 that “Mr. Watson then formed Cullen Agritech on June 3, 2009 and began the process of transferring the intellectual property and personnel to Cullen Agritech.” Clarify what intellectual property and personnel have been transferred, and from which entity in each case. Address whether additional intellectual property and personnel will be transferred after the business combination. If so, clarify what intellectual property and personnel will be transferred at that point. Disclose any payments that have been or are anticipated to be made in this regard, and to whom they have been or will be made. |

We have revised the disclosure on pages 50 and 124 of the Registration Statement as requested.

| 42. | We note your response to our prior comment 63 and reissue the comment in part. Disclose who negotiated the land purchase terms on behalf of Triplecrown. |

We have revised the disclosure on page 50 of the Registration Statement as requested.

| 43. | We note your response to our prior comment 71 and the supplemental materials you have provided. Ensure that you provide legible copies of all materials in future responses. You do not provide adequate support for your statement that there is a “significant shortage” of milk in the Southeastern U.S. We also did not find support for your statement that “The Eastern Seaboard represents the largest fresh liquid milk market in the world, and this market is currently starved of supply.” Please make appropriate revisions to your filing by deleting unsupported statements and adding references to third party materials that support statements for which there is objective third party support. |

Duly noted. We have revised the disclosure on pages 51, 52, 111, 113, 122 and 125 in response to this comment.

| 44. | We note your response to our prior comments 73 and 74 and reissue the comments. Explain the work that has occurred on the research farms, who owns and operates the research farms, what staff conducts the work, what intellectual property has been created and who owns the intellectual property. |

We have revised the disclosure on pages 50 and 124 of the Registration Statement as requested.

Triplecrown’s Board of Directors’ Reasons, page 50

| 45. | Wherever you refer to your advisory board, geneticists, or others “associated” with the various affiliated entities, clarify in each case whether there are corresponding employment or consulting arrangements. If not, disclose any consideration these referenced individuals have received, will receive, or were promised in exchange for being so identified. |

We have revised the disclosure on pages 47 and 124 of the Registration Statement as requested.

Securities and Exchange Commission

October 8, 2009

Page 12

| 46. | Provide independent third party support for your “world’s leading” and other like assertions, such as those that appear in the second paragraph on page 123. Also provide us with copies of all studies you cite in the new text on page 51, marked and highlighted to show those portions that support your disclosure. |

We have revised the disclosure on pages 51, 121 and 124 of the Registration Statement as requested. We have also provided the support as requested.

Fairness Opinion, page 53

| 47. | Explain in greater detail how the projections came about, including what information was exchanged and provided among the parties. Make clear where the raw data derived from originally. We note in particular the disclosure at pages 57 and 115, for example. |

We have revised the disclosure on page 58 of the Registration Statement as requested.

| 48. | We reissue prior comment 83. For example, make clear that the forecasts assume availability of more than $400,000,000 in capital. |

We have revised the disclosure on page 56 of the Registration Statement as requested.

Anticipated Accounting Treatment, page 69

| 49. | Your response to prior comment number 92 indicates you concluded Cullen Agritech is not a business as defined in SFAS 141(R). Please provide us with a detailed analysis of how you considered paragraphs A4 through A9 of SFAS 141(R) in arriving at this conclusion. |

SFAS 141(R) defines a business as an integrated set of activities and assets that is capable of being conducted and managed for the purpose of providing a return in the form of dividends, lower costs, or other economic benefits directly to investors or other owners, members, or participants. A business consists of inputs and processes applied to those inputs that have the ability to create outputs.

An input is defined as any economic resource that creates, or has the ability to create, outputs when one or more processes are applied to it. Currently, Cullen Agritech (“CAT”) has not performed any activities other than its corporate formation. The only input CAT has is the intellectual property and knowledge it will obtain upon closing. CAT does not have certain essential inputs (i.e. operating farm, livestock and certain equipment) necessary to be considered a business. Additionally, CAT does not have economic resources necessary to obtain additional inputs from third parties.

A process is defined as any system, standard, protocol, convention, or rule that, when applied to an input or inputs, creates or has the ability to create outputs. CAT has no processes and no organized workforce having the necessary skills and experience that are capable of being applied to inputs to create outputs.

Although outputs are not required to qualify as a business, CAT does not currently have any outputs.

In arriving at our conclusion, we have also considered other factors to determine whether a set of activities and assets in the development stage constitute a business. CAT has not commenced planned activities and has not obtained processes that would be required to be applied to inputs and does not have the ability to obtain access to customers that will purchase the outputs.

Based upon the above, we conclude that CAT does not qualify as a business under the guidance of SFAS 141(R), paragraphs A4 through A9.

U.S. Federal Income Tax Considerations, page 79

| 50. | We reissue prior comment 94. Please revise the caption accordingly. Offering Proceeds Held in Trust, page 95. |

We have revised the disclosure on the cover page of the prospectus and pages i, 3 and 80 of the Registration Statement as requested.

| 51. | We reissue prior comment 101. |

We have revised the disclosure on page 96 of the Registration Statement as requested.

Securities and Exchange Commission

October 8, 2009

Page 13

Business of Cullen Agritech, page 105

| 52. | We note your response to our prior comment 104 and reissue the entire comment. |

We have revised the disclosure on pages 106, 113, 114, 115 and 121 of the Registration Statement as requested.

| 53. | Revise the new disclosure at page 112 to clarify whether the culling did not occur to any meaningful extent in the Southeast. |

We have revised the disclosure on page 113 of the Registration Statement.

Cullen Agricultural Technologies, Inc., Forecasted Statement of Operations, page 116

| 54. | In your response to prior comment number 105, you explain that you revised the disclosure to include disclosure of significant changes in financial position. However, we are unable to locate such information within the disclosures. Please revise to include information regarding significant changes in your financial position, or tell us why you believe such information is not needed. |

We have revised the disclosure on page 118 of the Registration Statement as requested.

| 55. | Please revise to provide a measure of gross profit, or cost of sales, as discussed in paragraph 8.06 of Chapter 8 of the AJCPA Audit and Accounting Guide for Prospective Financial Information. Please also include applicable discussion regarding the assumptions used with regard to your measure of gross profit, or cost of sales. |

We have revised the disclosure on pages 117 and 120 of the Registration Statement as requested.

| 56. | We note you present EBITDA and EBIT as part of your forecasted statement of operations. Please tell us how your presentation and related disclosures comply with Item 10(e) of Regulation S-K. |

We have revised the disclosure on page 117 of the Registration Statement as requested.

Summary of Significant Assumptions Revenue, page 117

| 57. | Please revise your disclosure to address whether the number of cows per year are expected to be mature or immature (i.e. producing or not producing). In addition, as it relates to the single farm parameters presented on page 115, please clarify if the $4 million expected to be spent on livestock is for mature or immature cows. |

We have revised the disclosure on pages 116 and 118 of the Registration Statement as requested.

Securities and Exchange Commission

October 8, 2009

Page 14

| 58. | Please revise your disclosure to explain how the amount of milk production and milk price corresponds to the revenue amounts presented on page 116. |

We have revised the disclosure on page 118 of the Registration Statement as requested.

| 59. | Please revise to discuss how your forecasted average milk production per cow compares with other industry participants and your historical experience. |

We have revised the disclosure on page 118 of the Registration Statement as requested.

Earning (Loss) Per Share, page 117

| 60. | Your disclosure explains that the calculation of earnings per share is based upon total shares outstanding of 34,757,295. Please tell us how this number of shares corresponds to the number of weighted average shares outstanding used in the pro forma presentation of 74,076,148. |

The forecasted 36,730,214 shares are comprised of the pro forma total of 74,076,148 shares less 37,345,934 shares that are expected to be repurchased should all of the shareholders approve the transaction (maximum conversion would result in the same forecasted share amount). This is based on the forecast assumption that there will be $150,000,000 of available capital, net of $19,300,000 of deferred underwriting fees and $5,000,000 in transaction expenses, with all excess funds being used to repurchase shares at the current price of $9.76 per share, as discussed on page 45 of the Registration Statement.

The calculation is as follows:

| · | $538,796,312 - Amount in Trust as of September 30, 2009 |

| · | Less: $174,300,000: $150,000,000 to fund operations, $19,300,000 deferred underwriting fees and $5,000,000 in transaction fees |

| · | Equals: $364,496,312 amount used to repurchase 37,345,934 shares |

| · | Forecasted 36,730,214 shares (74,076,148 pro forma shares 37,345,934 shares repurchased) |

Securities and Exchange Commission

October 8, 2009

Page 15

Properties, page 124

| 61. | We note your response to our prior comment 106 and reissue the entire comment. Identify the owner. Explain the location and size of the research farms. Explain the arrangements pursuant to which the research and development activity is occurring on the third party’s land. Explain whether the third party has any rights to the intellectual property being developed on its land. |

We have revised the disclosure on pages 124 and 125 of the Registration Statement as requested.

Environmental Regulations, page 125

| 62. | Explain why management is not concerned by the environmental regulations discussed at page 125, when it plans 2,300 cows per site, rather than the referenced 700 cow exemptive limit. |

We have revised the disclosure on page 126 of the Registration Statement as requested.

Employees, page 126

| 63. | We note your response to our prior comment 107 and reissue the entire comment. We note your statement on page 50 stating that “Key personnel associated with Cullen Agritech developed Cullen Agritech’s farming system and has been proven on research farms in Girard, Georgia, the first of which was established in late 2007 [emphasis added].” Explain who the “key personnel” are, the exact nature of their “association” with Cullen Agritech, who owns and operates the research farms, who has been conducting the research and development work, how the work has been staffed, who owns the intellectual property rights relating to the fanning system, and how the fanning system has been “proven” and by whom. Also clarify the time periods during which all of this occurred. We also refer you to your response to prior comment 50, in which you suggest that you have removed the indicated assertions. |

We have revised the disclosure on pages 52 and 124 of the Registration Statement as requested.

Management of CAH Following the Merger, page 133

| 64. | Revise the new text at page 133 to provide Mr. Watson’s business experience since June 2008, clarifying when he began each new position in that period. Also explain the reference to “in conjunction with Cullen Investments.” |

We have revised the disclosure on pages 125 and 135 of the Registration Statement as requested.

Securities and Exchange Commission

October 8, 2009

Page 16

Exhibit Index

| 65. | We note your response to our prior comment 115 and the addition of Exhibit 214. Please revise so that Exhibit 23.4 refers to Exhibit 8.1 as well as Exhibit 5.1, since Graubard Miller’s consent is needed for its tax opinion as well as its legality opinion. |

We have revised the disclosure on pages II-4 and II-10 of the Registration Statement as requested.

| 66. | We note your response to our prior comment 114 and reissue the comment in part. When incorporating by reference to an exhibit to a previous filing, please specify exactly which exhibit to that previous filing is being incorporated by reference. |

We have revised the disclosure on pages II-4, II-9 and II-10 of the Registration Statement as requested.

If you have any questions, please do not hesitate to contact me at the above telephone and facsimile numbers.

Sincerely, /s/ Jeffrey M. Gallant Jeffrey M. Gallant |

JMG:kab

Enclosures

| cc: | Douglas S. Ellenoff, Esq. |

| Eric J. Watson |